QuickLinks -- Click here to rapidly navigate through this documentAs filed with the Securities and Exchange Commission on January 3, 2007

No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form F-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Masonite International Inc.

(Exact name of registrant as specified in its charter)

Canada

(State or other jurisdiction of

incorporation or organization) | | 2431

(Primary Standard Industrial

Classification Code Number) | | Not Applicable

(I.R.S. Employer

Identification No.) |

1600 Britannia Road East

Mississauga, Ontario L4W 1J2 Canada

(905) 670-6500

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices) |

Masonite Corporation

(Exact name of registrant as specified in its charter) | | Masonite International Corporation

(Exact name of registrant as specified in its charter) |

Delaware

(State or other jurisdiction

of incorporation

or organization) |

|

2431

(Primary Standard

Industrial Classification

Code Number) |

|

64-0198020

(I.R.S. Employer

Identification No.) |

|

Ontario, Canada

(State or other jurisdiction

of incorporation

or organization) |

|

2431

(Primary Standard

Industrial Classification

Code Number) |

|

98-0377314

(I.R.S. Employer

Identification No.) |

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609

(813) 877-2726

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices) |

|

1600 Britannia Road East

Mississauga, Ontario L4W 1J2 Canada

(905) 670-6500

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices) |

Frederick Arnold

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609

(813) 739-3000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies:

Joseph H. Kaufman, Esq.

Simpson Thacher & Bartlett LLP

425 Lexington Avenue

New York, New York 10017-3954

Tel: (212) 455-2000

Fax: (212) 455-2502

Approximate date of commencement of proposed sale of the securities to the public: The exchange will occur as soon as practicable after the effective date of this Registration Statement.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

|

Title of Each Class Of

Securities to be Registered

|

|

Amount to Be

Registered

|

|

Proposed

Maximum

Offering Price

Per Unit

|

|

Proposed

Maximum

Aggregate

Offering Price

|

|

Amount Of

Registration

Fee

|

|---|

|

| Senior Subordinated Notes due 2015 issued by Masonite Corporation | | $412,000,000 | | 100%(1) | | $412,000,000(1) | | $44,084(2) |

|

| Guarantees of Senior Subordinated Notes due 2015 issued by Masonite Corporation(3) | | (4) | | (4) | | (4) | | (4) |

|

Senior Subordinated Notes due 2015 issued by

Masonite International Corporation | | $358,000,000 | | 100%(1) | | $358,000,000(1) | | $38,306(2) |

|

| Guarantees of Senior Subordinated Notes due 2015 issued by Masonite International Corporation(3) | | (4) | | (4) | | (4) | | (4) |

|

- (1)

- Estimated solely for the purpose of calculating the registration fee under Rule 457 of the Securities Act of 1933, as amended.

- (2)

- The registration fee for the securities offered hereby was calculated under Rule 457(f)(2) of the Securities Act of 1933, as amended.

- (3)

- See inside facing page for table of additional registrant guarantors.

- (4)

- Pursuant to Rule 457(n) under the Securities Act of 1933, as amended, no separate fee for the guarantees is payable.

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANT GUARANTORS

Exact Name of Registrant

As Specified In Its Charter

| | State or other

Jurisdiction of

Incorporation

or Organization

| | IRS

Employer

Identification

Number

| | Address, Including

Zip Code, of

Registrant's Principal

Executive Offices

| | Phone Number

|

|---|

| 3061275 Nova Scotia Company | | Nova Scotia | | Not Applicable | | 1600 Britannia Road East

Mississauga, Ontario

L4W 1J2

Canada | | (905) 670-6500 |

Bonlea Limited |

|

United Kingdom |

|

Not Applicable |

|

Birthwaite Business Park

Huddersfield Road

Darton, Barnsley S75 5JS

United Kingdom |

|

+44-1226-383434 |

Castlegate Entry Systems, Inc. |

|

Canada |

|

Not Applicable |

|

1600 Britannia Road East

Mississauga, Ontario

L4W 1J2

Canada |

|

(905) 670-6500 |

Crown Door Corporation |

|

Canada |

|

Not Applicable |

|

1600 Britannia Road East

Mississauga, Ontario

L4W 1J2

Canada |

|

(905) 670-6500 |

Cutting Edge Tooling, Inc. |

|

Florida |

|

83-0338818 |

|

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609 |

|

(813) 877-2726 |

Door Installation Specialists Corporation |

|

Florida |

|

20-1562354 |

|

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609 |

|

(813) 877-2726 |

Eger Properties |

|

California |

|

68-0316847 |

|

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609 |

|

(813) 877-2726 |

Florida Made Door Co. |

|

Florida |

|

59-0737960 |

|

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609 |

|

(813) 877-2726 |

Masonite Chile Holdings S.A. |

|

Chile |

|

Not Applicable |

|

Ruta Q-50, Km. 1,5

Cabrero, Chile

447000 |

|

+56-43-404402 |

Masonite Components |

|

Ireland |

|

Not Applicable |

|

Derryoughter

Drumsna

Carrick on Shannon

Co. Leitrim

Republic of Ireland |

|

+353-71-9659500 |

Masonite Europe |

|

Ireland |

|

Not Applicable |

|

Derryoughter

Drumsna

Carrick on Shannon

Co. Leitrim

Republic of Ireland |

|

+353-71-9659500 |

Masonite Europe Limited |

|

United Kingdom |

|

Not Applicable |

|

Birthwaite Business Park

Huddersfield Road,

Darton, Barnsley, S75 5JS

United Kingdom |

|

+44-1226-383434 |

Masonite Ireland |

|

Ireland |

|

Not Applicable |

|

Derryoughter

Drumsna

Carrick on Shannon

Co. Leitrim

Republic of Ireland |

|

+353-71-9659500 |

Masonite Mexico, S.A. de C.V. |

|

Mexico |

|

Not Applicable |

|

Carretera Laredo Km. 23

Cienega de Flores, Estado

Nuevo Leon 65550

Mexico |

|

+5281-8220-8900 |

Masonite PrimeBoard Inc. |

|

North Dakota |

|

20-2765752 |

|

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609 |

|

(813) 877-2726 |

Pintu Acquisition Company, Inc. |

|

Delaware |

|

62-1647932 |

|

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609 |

|

(813) 877-2726 |

Premdor Crosby Limited |

|

United Kingdom |

|

Not Applicable |

|

Birthwaite Business Park

Huddersfield Road,

Darton, Barnsley, S75 5JS

United Kingdom |

|

+44-1226-383434 |

Premdor Finance LLC |

|

Delaware |

|

51-0404966 |

|

Nemours Building, Suite 1414

1007 Orange Street

Wilmington, Delaware 19801 |

|

(302) 652-5200 |

| | | | | | | | | |

Premdor U.K. Holdings Limited |

|

United Kingdom |

|

Not Applicable |

|

Birthwaite Business Park

Huddersfield Road,

Darton, Barnsley S75 5JS

United Kingdom |

|

+44-1226-383434 |

WMW, Inc. |

|

Delaware |

|

76-0533326 |

|

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609 |

|

(813) 877-2726 |

Woodlands Millwork I, Ltd. |

|

Texas |

|

76-0285989 |

|

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609 |

|

(813) 877-2726 |

Information contained herein is subject to completion or amendment. A registration statement relating to those securities has been filed with the Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This prospectus shall not constitute an offer to sell or the solicitation of an offer to buy.

Subject to Completion, dated January 3, 2007

PRELIMINARY PROSPECTUS

Masonite International Inc.

Masonite Corporation Masonite International Corporation

OFFER TO EXCHANGE

Up to $412,000,000 aggregate principal amount of Senior Subordinated Notes due 2015 issued by Masonite Corporation, which have been registered under the Securities Act of 1933, for any and all outstanding Senior Subordinated Notes due 2015 issued by Masonite Corporation.

Up to $358,000,000 aggregate principal amount of Senior Subordinated Notes due 2015 issued by Masonite International Corporation, which have been registered under the Securities Act of 1933, for any and all outstanding Senior Subordinated Notes due 2015 issued by Masonite International Corporation.

The exchange notes will be fully and unconditionally guaranteed on an unsecured basis by our parent company, Masonite International Inc., and certain of our domestic and foreign subsidiaries.

We are conducting the exchange offer in order to provide you with an opportunity to exchange your unregistered outstanding notes for freely tradeable exchange notes that have been registered under the Securities Act of 1933.

The Exchange Offer

- •

- We will exchange all outstanding notes that are validly tendered and not validly withdrawn for an equal principal amount of exchange notes representing the same underlying indebtedness that are freely tradeable.

- •

- You may withdraw tenders of outstanding notes at any time prior to the expiration date of the exchange offer.

- •

- The exchange offer expires at 5:00 p.m., New York City time, on , 2007 which is the 21st business day after the date of this prospectus.

- •

- The exchange of outstanding notes for exchange notes in the exchange offer will not be a taxable event for U.S. or Canadian federal income tax purposes.

- •

- The terms of the exchange notes to be issued in the exchange offer are substantially identical to the outstanding notes, except that the exchange notes will be freely tradeable.

All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the indentures. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the outstanding notes under the Securities Act.

You should carefully consider the "Risk Factors" beginning on page 19 of this prospectus before participating in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the exchange notes to be distributed in the exchange offer or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2007.

TABLE OF CONTENTS

| | Page

|

|---|

| Presentation of Financial and Other Information | | i |

| Enforceability of Civil Liabilities | | ii |

| Exchange Rate Information | | ii |

| Industry Data | | ii |

| Prospectus Summary | | 1 |

| Risk Factors | | 19 |

| Forward-looking Statements | | 37 |

| Use of Proceeds | | 38 |

| Capitalization | | 39 |

| The Transaction | | 40 |

| Unaudited Pro Forma Consolidated Financial Information | | 42 |

| Selected Historical Consolidated Financial Data | | 47 |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | | 51 |

| Industry Overview | | 90 |

Business |

|

92 |

| Directors and Senior Management | | 104 |

| Major Shareholders and Related Party Transactions | | 107 |

| Description of Certain Indebtedness | | 110 |

| The Exchange Offer | | 113 |

| Description of Notes | | 123 |

| Certain U.S. Federal Income Tax Consequences | | 182 |

| Certain Canadian Federal Income Tax Considerations | | 183 |

| Certain ERISA Considerations | | 184 |

| Book-Entry, Settlement and Clearance | | 185 |

| Plan of Distribution | | 188 |

| Legal Matters | | 189 |

| Experts | | 189 |

| Available Information | | 189 |

| Index to Consolidated Financial Statements | | F-1 |

We have not authorized any dealer, salesperson or other person to give any information or represent anything to you other than the information contained in this prospectus. You must not rely on unauthorized information or representations.

This prospectus does not offer to sell nor ask for offers to buy any of the securities in any jurisdiction where it is unlawful, where the person making the offer is not qualified to do so, or to any person who cannot legally be offered the securities. The information in this prospectus is current only as of the date on its cover, and may change after that date.

Following the date of this prospectus we will be subject to reporting obligations and any filings we make will be available via the website of the United States Securities and Exchange Commission, or SEC, atwww.sec.gov. You can also obtain any filed documents regarding us without charge by written or oral request to:

Masonite International Inc.

One North Dale Mabry Highway, Suite 950

Tampa, Florida 33609

Attn. Frederick Arnold

Telephone: (813) 739-3000

Please note that copies of documents provided to you will not include exhibits.

In order to receive timely delivery of requested documents in advance of the expiration date of the exchange offer, you should make your request no later than , 2007, which is five business days before you must make a decision regarding the exchange offer.

See "Available Information".

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Unless we indicate otherwise, financial information in this preliminary prospectus has been prepared in accordance with Canadian GAAP. Canadian GAAP differs in some respects from U.S. GAAP, and thus our financial statements may not be comparable to the financial statements of U.S. companies. Certain differences as they apply to us are summarized in note 26 to the annual

i

consolidated financial statements and note 20 of the unaudited interim consolidated financial statements included elsewhere in this prospectus.

ENFORCEABILITY OF CIVIL LIABILITIES

Masonite International Inc. is incorporated under the Canada Business Corporations Act and Masonite International Corporation, a subsidiary of Masonite International Inc., is incorporated under the Ontario Business Corporations Act. Certain of our guarantors are also incorporated in jurisdictions outside of the United States. Each of Masonite International Inc. and Masonite International Corporation has its principal executive office in Ontario, Canada. Certain of the directors, officers and experts named in this prospectus are not residents of the United States, and all or a substantial portion of their assets and a substantial portion of the assets of Masonite International Inc., Masonite International Corporation and our non-U.S. guarantors are located outside of the United States. It may be difficult for you to effect service of process within the United States upon us or our directors, officers and experts who are not residents of the United States or to realize in the United States upon judgments of U.S. courts based upon the civil liability under the federal securities laws of the United States. We have been advised by Davies Ward Phillips & Vineberg LLP, our Canadian counsel, that there is doubt as to the enforceability in Canada against us or against our directors, officers or experts who are not residents of the United States, in original actions or in actions for enforcement of judgments of U.S. courts, of liabilities based solely upon the federal securities laws of the United States.

EXCHANGE RATE INFORMATION

The following table sets forth, for the periods indicated, translations of Canadian dollars into U.S. dollars at specified rates. These translations have been made at the indicated noon-buying rate in New York City for cable transfers in Canadian dollars as certified for customs purposes by the Federal Reserve Bank of New York. These rates are provided solely for your convenience. They are not necessarily the rates used by us in the preparation of our financial statements.

Year Ended December 31

| | Average

|

|---|

| 2001 | | 0.6444 |

| 2002 | | 0.6368 |

| 2003 | | 0.7186 |

| 2004 | | 0.7702 |

| 2005 | | 0.8269 |

Recent Monthly Data

| | Average

| | Low

| | High

|

|---|

| April 2006 | | 0.8742 | | 0.8534 | | 0.8926 |

| May 2006 | | 0.9009 | | 0.8903 | | 0.9100 |

| June 2006 | | 0.8979 | | 0.8902 | | 0.9090 |

| July 2006 | | 0.8855 | | 0.8990 | | 0.8760 |

| August 2006 | | 0.8943 | | 0.8840 | | 0.9037 |

| September 2006 | | 0.8760 | | 0.8872 | | 0.9048 |

INDUSTRY DATA

We obtained the industry, market and competitive position data referenced throughout this prospectus from our own internal estimates and research as well as from industry and general publications and research, and surveys and studies conducted by third parties. Industry publications, studies and surveys generally state that they have been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe that each of these publications, studies and surveys is reliable, we have not independently verified market and industry data from third party sources. While we believe our internal company research is reliable, such research has not been verified by any independent source.

ii

PROSPECTUS SUMMARY

This summary highlights information appearing elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before participating in the exchange offer. You should read the entire prospectus carefully.

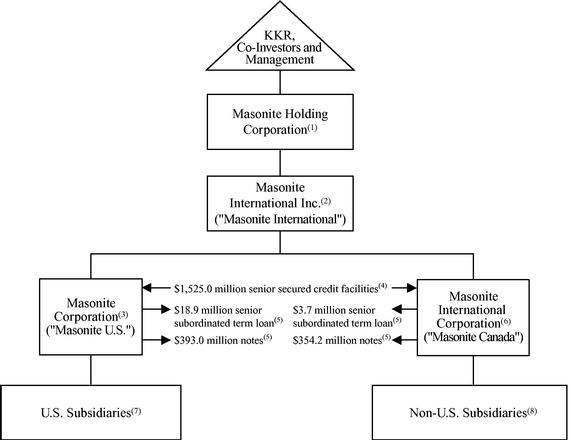

Unless the context otherwise requires, in this prospectus "Masonite", the "Company", "we", "us" and "our" refer to Masonite International Inc. ("Masonite International") and its subsidiaries; and references to the "Issuers" mean Masonite Corporation ("Masonite U.S.") and Masonite International Corporation ("Masonite Canada"), the issuers of the notes. Masonite U.S., a direct wholly owned subsidiary of Masonite International, operates Masonite International's U.S. subsidiaries. Masonite Canada, also a direct wholly owned subsidiary of Masonite International, operates Masonite International's Canadian subsidiaries as well as certain other non-U.S. subsidiaries. All amounts are in U.S. dollars unless specified otherwise. Unless otherwise indicated, financial information identified in this prospectus as "pro forma" gives effect to the closing of the acquisition pursuant to which we were acquired by affiliates of Kohlberg Kravis Roberts & Co. L.P. ("KKR") (the "Transaction") and certain other events as described under "Unaudited Pro Forma Consolidated Financial Information."

Our Company

We are one of the largest manufacturers of doors in the world, with a significant market share in both interior and exterior door products. We sell approximately 50 million doors per year in over 70 countries, including the United States, Canada, the United Kingdom, France, and throughout Central and Eastern Europe. For the year ended December 31, 2005 our sales were $2.4 billion.

Our products are marketed under well-recognized brand names throughout the world. In North America, we market our doors primarily under the Masonite brand, which is a leading brand in the door industry. Our sales are derived from two primary sources of door demand: residential repair, renovation and remodeling of existing homes, and the construction of new homes. We believe that sales to the residential repair, renovation and remodeling sector represents the larger component of our business in North America. Approximately 79% of our 2005 sales were generated in North America, where we believe we have a leading market share in both interior and exterior doors, 18% in Europe, and the remainder in South America, Asia, Africa and the Middle East.

We have a global manufacturing and distribution footprint, with over 80 facilities in 18 countries, primarily in North America and Europe. We are a vertically integrated producer, manufacturing key components of doors, including composite molded and veneer door facings, glass door lites and cut stock. In order to realize cost advantages and efficiencies provided by vertical integration, we have integrated the various operations in our North American segment as well as our Europe and Other segment to the point where we share common systems, financing and infrastructure. We believe that our high level of vertical integration provides us with competitive and cost advantages over competitors not as vertically integrated, and enhances our ability to develop new and proprietary products.

As part of our "all products" cross-merchandising strategy, we provide our customers with a broad product offering of interior and exterior doors and entry systems at various price points. We manufacture a broad line of interior doors, including residential molded, flush, stile and rail, louvre and specially-ordered commercial and architectural doors. We also manufacture exterior residential steel and fiberglass doors and entry systems. In 2005, sales of interior and exterior products accounted for approximately 64% and 36% of our revenue, respectively. In addition, we also sell certain door components to other door manufacturers.

We sell doors through multiple distribution channels, including: (i) directly to retail home center customers; (ii) one-step distributors that sell directly to homebuilders and contractors; and (iii) two-step wholesale distributors that resell to other distributors. For North American retail home center

1

customers, our numerous door fabrication facilities provide value-added fabrication and logistical services, including store delivery of pre-hung interior and exterior doors. We believe our ability to provide: (i) a broad product range; (ii) frequent, rapid, on-time and complete delivery; (iii) consistency in products and merchandising; (iv) national service; and (v) special order programs differentiate us from our competitors.

Post-Transaction Initiatives

We were acquired on April 6, 2005 by an affiliate of KKR. Since the acquisition we have implemented a strategic focus designed to enhance the operating performance of our business and deliver increased value to our customers.

Our "Blueprint for Profitable Growth" focuses employees at all levels on achieving key customer and manufacturing metrics, including targets for customer service, product profitability and manufacturing efficiencies. To accomplish these goals we have deployed an intensive program based upon "Lean Sigma" methodologies, along with a comprehensive review of product pricing. In addition, we have introduced a detailed set of operational metrics which are used to assess facility performance and to benchmark best practices across the company. We believe that these initiatives will provide us with a strong platform for future profitability and growth.

Business Strengths

We believe that we are distinguished by the following business strengths:

Leading Global Manufacturer. With operations in 18 countries and customers in over 70 countries, we are a leading manufacturer of doors in the United States, Canada, the United Kingdom and France.

Diversified Business. Our business is diversified by geography and distribution channel, with a broad product offering of doors. We sell products through multiple distribution channels, including one- and two-step distributors, retail home centers and wholesale building supply dealers, thereby reducing our reliance on any one channel.

Focus on Stable End Market. We generate the majority of our revenue from residential repair, renovation and remodeling spending, which has historically been less cyclical than new construction spending.

Strong Brand Recognition. Our brands are well recognized for their design, innovation, reliability and quality. We market our doors globally, primarily under the Masonite® and Premdor® brands, as well as other well-recognized names.

Strong Customer Relationships with Well-Established Multi-Channel Distribution. We have well-established relationships within all door distribution channels. Our top ten customers have been purchasing doors from us for more than 10 years on average and we believe that we are typically their leading door supplier.

Low Cost Producer with Leading Technology and Infrastructure. We have numerous design, process and product patents developed primarily at our 141,000 square foot research facility in West Chicago.

Vertically Integrated Operations. We are one of the few vertically integrated manufacturers of doors in the world, enabling us to control the many facets of production, decrease lead times and enhance customer service.

2

Business Strategy

We intend to build upon our leading position in the door market worldwide through the following key elements of our business strategy:

Implement the Blueprint for Profitable Growth. Our Blueprint for Profitable Growth was introduced during the fourth quarter of 2005 and distributed to employees around the world and to many of our customers, suppliers and investors. The Blueprint provides direction for all employees with clear, distinct and common goals and actions that we believe will enable us to improve operations across our business.

We identified three priorities which we believe will improve our performance:

- •

- Creating a common culture across the Company with a focus on operational excellence while preserving our traditional entrepreneurial spirit.

- •

- Driving cost reductions through all parts of our business, including at the plant level through improving core operational metrics; in the supply chain as we build capabilities to better manage and reduce materials, services and distribution costs; and in administrative costs by challenging all spending in selling and administrative cost centers.

- •

- Improving pricing discipline based on a comprehensive understanding of customer and product line profitability, and the value that we provide to our customers.

Enhance Value Proposition for Our Customers. Through the implementation of Lean Sigma, we intend to further enhance the value we provide to our customers by decreasing our lead times and focusing on other key customer service metrics.

Continue Leadership in New Product Design and Technology. We consider our strong focus on research and development to be one of our major strengths and intend to capitalize on our leadership in this area through the development of new and innovative products and improved manufacturing processes.

Issuer Information

Masonite International Inc., the parent company of Masonite Corporation and Masonite International Corporation, was incorporated under the Canada Business Corporations Act on February 2, 2005. Masonite Corporation is a Delaware corporation incorporated on September 1, 1925. Masonite International Corporation and Specialty Buildings Products Ltd. amalgamated on May 30, 2005 to form Masonite International Corporation under the Ontario Business Corporations Act.

Our principal executive offices are located at 1600 Britannia Road East, Mississauga, Ontario, Canada L4W 1J2 and One North Dale Mabry Highway, Suite 950, Tampa, Florida 33609. Our telephone number is (905) 670-6500 and (813) 877-2726, respectively. Our web site is located at www.masonite.com. Information on our web site does not constitute part of this prospectus and is not incorporated by reference herein.

3

Summary of the Terms of the Exchange Offer

On April 6, 2005, in connection with the closing of the Transaction, we entered into a $770.0 million senior subordinated loan agreement. The proceeds of the loan were used to partially fund the Transaction. See "The Transaction". The senior subordinated loan initially carried an interest rate of LIBOR plus 6.00%, which increased over time to a maximum interest rate of 11% per annum. On October 6, 2006, the senior subordinated loan was repaid in full with the automatic issuance of a new debt obligation comprised of a senior subordinated term loan bearing an interest rate of 11% and maturing on April 6, 2015. Certain lenders exercised their option on and after October 6, 2006 to receive Senior Subordinated Notes due 2015 for all or a part of the principal amount of the senior subordinated term loan of such lender then outstanding (the "private placement").

In this prospectus, the terms "outstanding notes" refers to the Senior Subordinated Notes due 2015 issued by Masonite Corporation (the "outstanding U.S. notes") and the Senior Subordinated Notes due 2015 issued by Masonite International Corporation (the "outstanding Canada notes") issued in the private placement; the term "exchange notes" refers to Senior Subordinated Notes due 2015 issued by Masonite Corporation and the Senior Subordinated Notes due 2015 issued by Masonite International Corporation, as registered under the Securities Act of 1933, as amended (the "Securities Act"); and the term "notes" refers to both the outstanding notes and the exchange notes.

| General | | In connection with the private placement, we entered into a registration rights agreement with The Bank of New York, as Trustee, for the holders of the outstanding notes (the "Trustee"), in which we and the guarantors agreed, among other things, to use our commercially reasonable efforts to file a registration statement within 90 days (January 4, 2007) after the date on which the outstanding notes were first issued and to cause the registration statement to become effective by the date that is 180 days (April 4, 2007) from the date outstanding notes were first issued. |

| | | You are entitled to exchange in the exchange offer your outstanding notes for exchange notes representing the same underlying indebtedness, which are identical in all material respects to the outstanding notes except: |

| | | • | | the exchange notes have been registered under the Securities Act; |

| | | • | | the exchange notes are not entitled to certain registration rights which are applicable to the outstanding notes under the registration rights agreement; and |

| | | • | | certain additional interest rate provisions of the registration rights agreement are no longer applicable. |

| The Exchange Offer | | We are offering to exchange up to: |

| | | • | | $412,000,000 aggregate principal amount of Senior Subordinated Notes due 2015 issued by Masonite Corporation, which have been registered under the Securities Act, for any and all outstanding Senior Subordinated Notes due 2015 issued by Masonite Corporation; and |

| | | • | | $358,000,000 aggregate principal amount of Senior Subordinated Notes due 2015 issued by Masonite International Corporation, which have been registered under the Securities Act, for any and all outstanding Senior Subordinated Notes due 2015 issued by Masonite International Corporation. |

| | | | | |

4

| | | Subject to the satisfaction or waiver of specified conditions, we will exchange, as evidence of the same underlying indebtedness, the exchange notes for all outstanding notes that are validly tendered and not validly withdrawn prior to the expiration of the applicable exchange offer. We will cause the exchange to be effected promptly after the expiration of the exchange offer. |

| | | Upon completion of the exchange offer, there may be no market for the outstanding notes and you may have difficulty selling them. |

| Resales | | Based on interpretations by the staff of the Securities and Exchange Commission, or the "SEC", set forth in no-action letters issued to third parties referred to below, we believe that you may resell or otherwise transfer exchange notes issued in the exchange offer without complying with the registration and prospectus delivery requirements of the Securities Act, if: |

| | | 1. | | you are acquiring the exchange notes in the ordinary course of your business; |

| | | 2. | | you do not have an arrangement or understanding with any person to participate in a distribution of the exchange notes; |

| | | 3. | | you are not an "affiliate" of either of the Issuers within the meaning of Rule 405 under the Securities Act; and |

| | | 4. | | you are not engaged in, and do not intend to engage in, a distribution of the exchange notes. |

| | | If you are not acquiring the exchange notes in the ordinary course of your business, or if you are engaging in, intend to engage in, or have any arrangement or understanding with any person to participate in, a distribution of the exchange notes, or if you are an affiliate of the Issuers, then: |

| | | 1. | | you cannot rely on the position of the staff of the SEC enunciated inMorgan Stanley & Co., Inc. (available June 5, 1991),Exxon Capital Holdings Corporation (available May 13, 1988), as interpreted in the SEC's letter to Shearman & Sterling dated July 2, 1993, or similar no- action letters; and |

| | | 2. | | in the absence of an exception from the position of the SEC stated in (1) above, you must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale or other transfer of the exchange notes. |

| | | If you are a broker-dealer and receive exchange notes for your own account in exchange for outstanding notes that you acquired as a result of market-making or other trading activities, you must acknowledge that you will deliver a prospectus, as required by law, in connection with any resale or other transfer of the exchange notes that you receive in the exchange offer. See "Plan of Distribution." |

| | | | | |

5

| Expiration Date | | The exchange offer will expire at 5:00 p.m., New York City time, on , 2007, which is the 21st business day after the date of this prospectus, unless extended by us. We do not currently intend to extend the expiration date of the exchange offer. |

| Withdrawal | | You may withdraw the tender of your outstanding notes at any time prior to the expiration date of the exchange offer. We will return to you any of your outstanding notes that are not accepted for any reason for exchange, without expense to you, promptly after the expiration or termination of the exchange offer. |

| Interest on the Exchange Notes and the Outstanding Notes | | Each exchange note will bear interest at the rate per annum set forth on the cover page of this prospectus from the most recent date to which interest has been paid on the outstanding notes or, if no interest has been paid on the outstanding notes, from October 6, 2006. The interest on the notes will be payable on each April 15 and October 15, beginning April 15, 2007. No interest will be paid on outstanding notes following their acceptance for exchange. |

| Conditions to the Exchange Offer | | The exchange offer is subject to customary conditions, which we may assert or waive. See "The Exchange Offer—Conditions to the exchange offer." |

| Procedures for Tendering Outstanding Notes | | If you wish to participate in the exchange offer, you must complete, sign and date the accompanying letter of transmittal, or a facsimile of the letter of transmittal, according to the instructions contained in this prospectus and the letter of transmittal. You must then mail or otherwise deliver the letter of transmittal, or a facsimile of the letter of transmittal, together with the outstanding notes and any other required documents, to the exchange agent at the address set forth on the cover page of the letter of transmittal. If you hold outstanding notes through The Depository Trust Company, or "DTC", and wish to participate in the exchange offer for the outstanding notes, you must comply with the Automated Tender Offer Program procedures of DTC. By signing, or agreeing to be bound by, the letter of transmittal, you will represent to us that, among other things: |

| | | 1. | | you are acquiring the exchange notes in the ordinary course of your business; |

| | | 2. | | you do not have an arrangement or understanding with any person to participate in a distribution of the exchange notes; |

| | | 3. | | you are not an "affiliate" of any of the Issuers within the meaning of Rule 405 under the Securities Act; and |

| | | 4. | | you are not engaged in, and do not intend to engage in, a distribution of the exchange notes. |

| | | If you are a broker-dealer and receive exchange notes for your own account in exchange for outstanding notes that you acquired as a result of market-making or other trading activities, you must represent to us that you will deliver a prospectus, as required by law, in connection with any resale or other transfer of such exchange notes. |

| | | | | |

6

| | | If you are not acquiring the exchange notes in the ordinary course of your business, or if you are engaged in, or intend to engage in, or have an arrangement or understanding with any person to participate in, a distribution of the exchange notes, or if you are an affiliate of any of the Issuers, then you cannot rely on the positions and interpretations of the staff of the SEC and you must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale or other transfer of the exchange notes. |

| Special Procedures for Beneficial Owners | | If you are a beneficial owner of outstanding notes that are held in the name of a broker, dealer, commercial bank, trust company or other nominee, and you wish to tender those outstanding notes in the exchange offer, you should contact such person promptly and instruct such person to tender those outstanding notes on your behalf. |

| Guaranteed Delivery Procedures | | If you wish to tender your outstanding notes and your outstanding notes are not immediately available or you cannot deliver your outstanding notes, the letter of transmittal and any other documents required by the letter of transmittal or you cannot comply with the DTC procedures for book-entry transfer prior to the expiration date, then you must tender your outstanding notes according to the guaranteed delivery procedures set forth in this prospectus under "The Exchange Offer—Guaranteed delivery procedures." |

| Effect on Holders of Outstanding Notes | | In connection with the issuance of the outstanding notes, we entered into a registration rights agreement with the Trustee for the holders of the outstanding notes that grants the holders of outstanding notes registration rights. By making the exchange offer, we will have fulfilled most of our obligations under the registration rights agreement. Accordingly, we will not be obligated to pay additional interest as described in the registration rights agreement. If you do not tender your outstanding notes in the exchange offer, you will continue to be entitled to all the rights and limitations applicable to the outstanding notes as set forth in the applicable indenture, except we will not have any further obligation to you to provide for the registration of the outstanding notes under the registration rights agreement and we will not be obligated to pay additional interest as described in the registration rights agreement, except in certain limited circumstances. |

| | | To the extent that outstanding notes are tendered and accepted in the exchange offer, the trading market for outstanding notes could be adversely affected. |

| Consequences of Failure to Exchange | | All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the indenture. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the outstanding notes under the Securities Act. |

| | | | | |

7

| Certain Federal Income Tax Consequences | | The exchange of outstanding notes for exchange notes in the exchange offer will not be a taxable event for United States or Canadian federal income tax purposes. See "Certain U.S. Federal Income Tax Consequences" and "Certain Canadian Federal Income Tax Consequences." |

| Use of Proceeds | | We will not receive any cash proceeds from the issuance of exchange notes in the exchange offer. |

| Exchange Agent | | The Bank of New York, whose address and telephone number are set forth in the section captioned "The exchange offer—exchange agent" of this prospectus, is the exchange agent for the exchange offer. |

8

Summary of the Terms of the Exchange Notes

The terms of the exchange notes are identical in all material respects to the terms of the outstanding notes, except that the exchange notes will not contain terms with respect to transfer restrictions or additional interest upon a failure to fulfill certain of our obligations under the registration rights agreement. The exchange notes will evidence the same debt as the outstanding notes. The exchange notes will be governed by the same indentures under which the outstanding notes were issued, and each series of the exchange notes and the outstanding notes will constitute a single class and series of notes for all purposes under the respective indenture. The following summary is not intended to be a complete description of the terms of the notes. For a more detailed description of the notes, see "Description of Notes." The outstanding notes and the exchange notes are collectively referred to herein as the "notes" unless the context otherwise requires.

Issuers |

|

Masonite U.S. and Masonite Canada. |

Securities |

|

Up to $412,000,000 aggregate principal amount of 11% Senior Subordinated Notes due 2015 issued by Masonite U.S.; and |

|

|

Up to $358,000,000 aggregate principal amount of 11% Senior Subordinated Notes due 2015 issued by Masonite Canada. |

Maturity Date |

|

The notes will mature on April 6, 2015. |

Interest Payment Dates |

|

We will pay interest on the notes on April 15 and October 15, commencing on April 15, 2007. Interest accrued on the indebtedness evidenced by the exchange notes from October 6, 2006. |

Additional Amounts |

|

If Masonite Canada is required to withhold or deduct any Canadian taxes from any payment under or with respect to its notes, it will pay such additional amounts as may be necessary so that the net amount received by each holder after such withholding or deduction will not be less than the amount such holder would have received if such taxes had not been withheld or deducted, subject to the exceptions described under the heading "Description of Notes—Additional Amounts." |

Guarantees |

|

All payments with respect to the notes, including principal and interest, are fully and unconditionally guaranteed on an unsecured senior basis by Masonite International, the Issuers' direct parent company, by the other Issuer, and by each of the Issuers' existing and future U.S. restricted subsidiaries and by certain of the Issuers' non-U.S. restricted subsidiaries. |

Ranking |

|

The outstanding notes are, and the exchange notes will be, our unsecured senior subordinated obligations and: |

|

|

• |

|

are subordinated in right of payment to our existing and future senior debt, including our senior secured credit facilities; |

|

|

• |

|

rank equally in right of payment to all of our future senior subordinated debt; |

|

|

• |

|

are effectively subordinated in right of payment to all of our existing and future secured debt (including our senior secured credit facilities), to the extent of the value of the assets securing such debt, and are structurally subordinated to all obligations of any of our subsidiaries that is not a guarantor of the notes; and |

| | | | | |

9

|

|

• |

|

rank senior in right of payment to all of our future debt and other obligations that are, by their terms, expressly subordinated in right of payment to the notes. |

|

|

Similarly, the note guarantees with respect to the outstanding notes are, and the note guarantees with respect to the exchange notes will be, unsecured senior subordinated obligations of the guarantors and: |

|

|

• |

|

are subordinated in right of payment to all of the applicable guarantor's existing and future senior debt, including such guarantor's guarantee under our senior secured credit facilities; |

|

|

• |

|

rank equally in right of payment to all of the applicable guarantor's future senior subordinated debt; |

|

|

• |

|

are effectively subordinated in right of payment to all of the applicable guarantor's existing and future secured debt (including such guarantor's guarantee under our senior secured credit facilities), to the extent of the value of the assets securing such debt, and be structurally subordinated to all obligations of any subsidiary of a guarantor if that subsidiary is not also a guarantor of the notes; and |

|

|

• |

|

rank senior in right of payment to all of the applicable guarantor's future subordinated debt and other obligations that are, by their terms, expressly subordinated in right of payment to the notes. |

|

|

As of September 30, 2006, (1) the notes and related guarantees ranked junior to approximately $1,225.4 million of senior indebtedness under our senior secured credit facilities, and (2) we had an additional $282.0 million of unutilized capacity under our senior secured revolving credit facility (excluding $8.2 million of outstanding undrawn letters of credit). In addition, the notes were structurally subordinated to $34.8 million of senior indebtedness incurred by our non-guarantor subsidiaries. |

Optional Redemption |

|

Prior to April 6, 2010, the Issuers may redeem all or a part of the notes at a redemption price equal to 100% of the principal amount of notes redeemed plus an applicable make-whole premium (as described in "Description of Notes—Optional Redemption") plus accrued and unpaid interest to the redemption date. |

|

|

After April 6, 2010, the Issuers may redeem some or all of the notes at par plus accrued interest plus a premium equal to one half of the coupon on such notes, which premium shall decline ratably on each subsequent anniversary of April 6 to zero on April 6, 2014. |

| | | | | |

10

Optional Redemption After Certain Equity Offerings |

|

In addition, before April 6, 2008, the Issuers may, at their option, redeem up to 35% of the aggregate principal amount of the notes at a redemption price equal to 111% of the face amount thereof with the proceeds of equity offerings;provided that at least 65% of the notes originally issued under the applicable Indenture remain outstanding. |

Change of Control Offer |

|

Upon the occurrence of a change of control, the Issuers will be required, subject to certain conditions, to offer to repurchase the notes at a price equal to 101% of their principal amount plus accrued and unpaid interest and additional interest, if any, to the date of repurchase. See "Description of Notes—Offer to Purchase—Change of Control." |

Asset Sale Proceeds |

|

If we or our subsidiaries engage in asset sales, we generally must either invest the net cash proceeds from such sales in our business within a period of time, prepay senior indebtedness or make an offer to purchase a principal amount of the notes equal to the excess net cash proceeds. The purchase price of the notes will be 100% of their principal amount, plus accrued interest. |

Certain Indenture Provisions |

|

The Issuers issued the notes under indentures among the Issuers, Masonite International, the other guarantors and the trustee. The indentures limit the ability of the Issuers, Masonite International and their restricted subsidiaries to, among other things: |

|

|

• |

|

incur additional indebtedness and issue preferred stock; |

|

|

• |

|

make restricted payments; |

|

|

• |

|

place restrictions on the Issuers, Masonite International and their restricted subsidiaries to pay dividends or make other distributions; |

|

|

• |

|

make investments; |

|

|

• |

|

sell assets; |

|

|

• |

|

enter into transactions with affiliates; |

|

|

• |

|

merge or consolidate with other entities; and |

|

|

• |

|

create or incur liens. |

|

|

Each of the covenants is subject to a number of important exceptions and qualifications. See "Description of Notes—Certain Covenants." |

No Prior Market; Listing |

|

The exchange notes will generally be freely transferable but will be a new issue of securities for which there will not initially be a market. Accordingly, there can be no assurance as to the development or liquidity of any market for the exchange notes. |

| | | | | |

11

ERISA Considerations |

|

The notes may, subject to certain restrictions described in "Certain ERISA Considerations" herein, be sold and transferred to ERISA Plans and Plans. |

Use of Proceeds |

|

We will not receive any cash proceeds from the exchange offer. |

Risk Factors

See "Risk Factors" for a description of some of the risks you should consider before deciding to participate in the exchange offer.

12

Summary Consolidated Financial Data

Set forth below is summary historical consolidated financial data of Masonite International Corporation, the entity acquired pursuant to the Transaction (the "Predecessor"), and summary historical consolidated financial data of Masonite International (the "Successor") at the dates and for the periods indicated. The historical data for the periods presented has been prepared in accordance with Canadian GAAP. The historical data of the Predecessor for the fiscal years ended December 31, 2003 and 2004 and the period from January 1, 2005 to April 6, 2005 have been derived from the Predecessor's historical consolidated financial statements included elsewhere in this prospectus, which have been audited by KPMG LLP. The historical data of the Successor presented as at December 31, 2005 and for the period from February 2, 2005 to December 31, 2005 has been derived from the Successor's historical consolidated financial statements included elsewhere in this prospectus which have been audited by KPMG LLP.

Subsequent to December 31, 2005, Deloitte & Touche LLP was appointed as auditors of the Company. As at the current date, Deloitte & Touche LLP have not audited the financial statements of the Company for an period.

The historical data for the periods from February 2, 2005 to September 30, 2005 and from January 1, 2006 to September 30, 2006 and as at September 30, 2006 have been derived from the unaudited consolidated financial statements of the Successor included elsewhere in this prospectus. This historical data includes, in the opinion of management, all adjustments necessary for a fair presentation of the operating results and financial condition of the Predecessor and Successor, respectively, for such periods and as of such dates.

The summary unaudited pro forma consolidated financial data have been prepared to give effect to the Transaction (defined herein) as if it had occurred on January 1, 2005. The pro forma adjustments are based upon available information and certain assumptions that we believe are reasonable. The summary unaudited pro forma consolidated financial data are for information purposes only and do not purport to represent what our results of operations or financial position actually would have been if the Transaction had occurred at any date, and such data do not purport to project the results of operations for any future period.

The summary historical consolidated financial data should be read in conjunction with and is qualified by reference to, "Unaudited Pro Forma Consolidated Financial Information," "Selected Historical Consolidated Financial Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the consolidated financial statements and accompanying notes thereto included elsewhere in this prospectus.

| | Predecessor

| | Successor(1)

| | Combined(2)

| | Pro Forma

| | Successor(1)

| | Combined(2)

| | Successor(1)

|

|---|

| | Fiscal Years

Ended

December 31,

| | Period From

January 1,

to April 6,

| | Period From

February 2,

to

December 31,

| | Fiscal

Year Ended

December 31,

| | Fiscal Year

Ended

December 31,

| | Period From

February 2,

to

September 30,

| | Nine Months Ended

September 30,

| | Nine Months

Ended

September 30,

|

|---|

| | 2003

| | 2004

| | 2005

| | 2005

| | 2005

| | 2005

| | 2005

| | 2005

| | 2006

|

|---|

| |

| |

| |

| |

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

|

|---|

| | (in millions of U.S. dollars)

|

|---|

| Statement of Operations Data: | | | | | | | | | | | | | | | | | | |

| Sales | | $ | 1,777.2 | | $ | 2,199.9 | | $ | 600.1 | | $ | 1,828.4 | | $ | 2,428.5 | | $ | 2,428.5 | | $ | 1,233.2 | | $ | 1,833.3 | | $ | 1,879.5 |

| Cost of sales | | | 1,380.2 | | | 1,722.7 | | | 486.7 | | | 1,497.9 | | | 1,984.7 | | | 1,964.2 | | | 1,007.9 | | | 1,494.6 | | | 1,486.9 |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

|

| Gross profit | | | 397.1 | | | 477.2 | | | 113.4 | | | 330.4 | | | 443.8 | | | 464.3 | | | 225.3 | | | 338.7 | | | 392.6 |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

|

| Selling, general and administration expenses | | | 162.2 | | | 189.9 | | | 54.4 | | | 161.3 | | | 215.7 | | | 217.7 | | | 105.8 | | | 160.2 | | | 159.2 |

| Depreciation | | | 47.5 | | | 58.5 | | | 17.9 | | | 60.3 | | | 78.2 | | | 79.3 | | | 39.0 | | | 57.0 | | | 65.3 |

| Amortization | | | 0.2 | | | 4.1 | | | 1.1 | | | 29.9 | | | 31.0 | | | 40.0 | | | 20.5 | | | 21.6 | | | 26.7 |

| Interest | | | 36.4 | | | 39.5 | | | 11.2 | | | 137.1 | | | 148.3 | | | 177.8 | | | 90.4 | | | 101.6 | | | 137.2 |

| Other expense (income), net | | | 3.1 | | | 7.7 | | | 66.4 | | | 22.6 | | | 89.0 | | | 12.0 | | | 20.5 | | | 86.8 | | | 16.6 |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

|

13

| | Predecessor

| | Successor(1)

| | Combined(2)

| | Pro Forma

| | Successor(1)

| | Combined(2)

| | Successor(1)

| |

|---|

| | Fiscal Years

Ended

December 31,

| | Period From

January 1,

to April 6,

| | Period From

February 2,

to

December 31,

| | Fiscal Year

Ended

December 31,

| | Fiscal Year

Ended

December 31,

| | Period From

February 2,

to

September 30,

| | Nine Months Ended

September 30,

| | Nine Months

Ended

September 30,

| |

|---|

| | 2003

| | 2004

| | 2005

| | 2005

| | 2005

| | 2005

| | 2005

| | 2005

| | 2006

| |

|---|

| |

| |

| |

| |

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

| |

|---|

| | (in millions of U.S. dollars)

| |

|---|

| Income (loss) before income taxes and non-controlling interest | | | 147.7 | | | 177.4 | | | (37.7 | ) | | (80.8 | ) | | (118.5 | ) | | (62.5 | ) | | (50.9 | ) | | (88.6 | ) | | (12.5 | ) |

| Income taxes | | | 34.5 | | | 42.7 | | | (8.3 | ) | | (16.3 | ) | | (24.6 | ) | | (6.3 | ) | | (19.3 | ) | | (27.6 | ) | | (4.8 | ) |

| Non-controlling interest | | | 5.5 | | | 6.8 | | | 1.3 | | | 5.3 | | | 6.6 | | | 6.6 | | | 4.0 | | | 5.3 | | | 5.6 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Net income (loss)(3) | | $ | 107.7 | | $ | 128.0 | | $ | (30.7 | ) | $ | (69.8 | ) | $ | (100.5 | ) | $ | (62.8 | ) | $ | (35.6 | ) | $ | (66.2 | ) | $ | (13.2 | ) |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Other Financial Data: | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | $ | 49.5 | | $ | 70.2 | | $ | 12.4 | | $ | 69.8 | | $ | 82.2 | | $ | 82.2 | | $ | 41.2 | | $ | 53.6 | | | 35.3 | |

| EBITDA(4) | | | 234.9 | | | 287.3 | | | 58.9 | | | 169.1 | | | 228.1 | | | 246.6 | | | 119.5 | | | 178.5 | | | 233.4 | |

| Adjusted EBITDA(4) | | | 298.4 | | | | | | 228.9 | | | 256.8 | |

| | Successor

|

|---|

| | As at

December 31,

| | As at

September 30,

|

|---|

| | 2005

| | 2006

|

|---|

| |

| | (unaudited)

|

|---|

| | (in millions of U.S. dollars)

|

|---|

| Balance Sheet Data: | | | | | | |

| Cash and cash equivalents | | $ | 47.5 | | $ | 61.3 |

| Working capital | | | 211.2 | | | 249.5 |

| Total assets | | | 3,297.3 | | | 3,262.8 |

| Total debt | | | 2,105.2 | | | 2,030.2 |

| Total shareholder's equity | | | 492.3 | | | 503.2 |

- (1)

- The only activity of the Successor in the February 2, 2005 to April 6, 2005 period is a realized exchange loss of $5.3 million to hedge the Canadian dollars required to close the Transaction. See note 1 of our consolidated financial statements contained elsewhere in this prospectus.

- (2)

- The combined financial data for the period ended September 30, 2005 and the year ended December 31, 2005 represents the combined historical results of the Predecessor and Successor for the periods reported. These combined results are for informational purposes only in order to facilitate discussion and analysis of our results of operations and do not purport to be a presentation in accordance with GAAP.

14

- (3)

- Reconciliation of certain financial data from Canadian GAAP to U.S. GAAP:

| | Predecessor

| | Successor

| | Combined

| | Pro Forma

| | Successor

| | Combined

| | Successor

| |

|---|

| | Fiscal Years

Ended

December 31,

| | Period From

January 1,

2005

to April 6,

| | Period From

February 2,

2005 to

December 31,

| | Fiscal Year

Ended

December 31,

| | Fiscal Year Ended December 31,

| | Period From

February 2,

2005 to

September 30,

| | Nine Months

Ended

September 30,

| | Nine Months

Ended

September 30,

| |

|---|

| | 2003

| | 2004

| | 2005

| | 2005

| | 2005

| | 2005

| | 2005

| | 2005

| | 2006

| |

|---|

| |

| |

| |

| |

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

| |

|---|

| Reconciliation of net income (loss)—Canadian GAAP to U.S. GAAP | |

| Net income (loss)—Canadian GAAP | | $ | 107.7 | | $ | 128.0 | | $ | (30.7 | ) | $ | (69.8 | ) | $ | (100.5 | ) | $ | (62.8 | ) | $ | (35.6 | ) | $ | (66.2 | ) | $ | (13.2 | ) |

| Effect of SFAS 133(a) | | | 3.3 | | | 6.6 | | | 1.4 | | | — | | | 1.4 | | | — | | | — | | | 1.4 | | | — | |

| Effect of EITF 88-16(b) | | | — | | | — | | | — | | | 0.3 | | | 0.3 | | | 0.3 | | | 0.4 | | | 0.3 | | | — | |

| Tax effect of U.S. GAAP adjustments | | | (1.0 | ) | | (1.9 | ) | | (0.5 | ) | | (0.2 | ) | | (0.6 | ) | | (0.1 | ) | | (0.1 | ) | | (0.6 | ) | | — | |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Net income (loss)—U.S. GAAP | | $ | 110.0 | | $ | 132.7 | | $ | (29.7 | ) | $ | (69.6 | ) | $ | (99.4 | ) | $ | (62.6 | ) | $ | (35.3 | ) | $ | (65.0 | ) | $ | (13.2 | ) |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| | Successor

| |

|---|

| | As at December 31,

| | As at September 30,

| |

|---|

| | 2005

| | 2006

| |

|---|

| |

| | (unaudited)

| |

|---|

| Reconciliation of shareholder's equity—Canadian GAAP to U.S. GAAP | | | | |

| Shareholder's equity—Canadian GAAP | | $ | 492.3 | | $ | 503.2 | |

| Effect of SFAS 133(a) | | | 9.9 | | | 12.5 | |

| Effect of EITF 88-16(b) | | | (5.8 | ) | | (1.9 | ) |

| | |

| |

| |

| Shareholder's equity—U.S. GAAP | | $ | 496.4 | | $ | 513.9 | |

| | |

| |

| |

(a) SFAS No. 133: Accounting for derivative instruments and hedging activities ("SFAS 133"):

SFAS 133 and SFAS No. 138, "Accounting for Certain Derivative Instruments and Certain Hedging Activities—an Amendment of SFAS 133", ("SFAS 138") requires that all derivative instruments be reported on the balance sheet at fair value and establishes criteria for designation and effectiveness of hedging relationships.

Forward exchange contracts:

The Company enters into forward exchange contracts to hedge certain forecasted cash flows. The contracts are for periods consistent with the forecasted transactions. All relationships between hedging instruments and hedged items, as well as risk management objectives and strategies are documented. Changes in the spot value of the foreign currency contracts that are designated, effective and qualified as cash flow hedges of forecasted transactions are reported in accumulated other comprehensive income and are reclassified into the same component of earnings and in the same period as the hedged transaction is recognized. Under Canadian GAAP, the derivative instruments are not marked to market and the related off balance sheet gains and losses are recognized in earnings in the same period as the hedged transactions.

15

Interest rate swap agreements:

The Company has entered into interest rate swap agreements to convert a portion of its floating rate debt into fixed rate debt in accordance with the Company's risk management objective of mitigating the variability and uncertainty in its cash flows due to variable interest rates. At the inception of these hedges, Masonite had met the criteria for designation and assessing the effectiveness of hedging relationships, thus these interest rate swaps were designated as cash flow hedges.

For the Predecessor, the criteria under SFAS 133 were not met prior to the establishment of its interest rate swap agreements. Accordingly, any change in the fair value of the interest rate swaps was reported in income from inception to December 31, 2003. As of January 1, 2004, the Company had met the criteria for designation and assessing the effectiveness of hedging relationships, thus the interest rate swaps were designated as cash flow hedges. Under U.S. GAAP, changes in fair value of these financial instruments that are designated as effective and qualify as cash flow hedges are reported in accumulated other comprehensive income and are reclassified into income in the same period as the hedged transaction is reported.

(b) EITF 88-16: Basis in leveraged buyout transactions:

Under Canadian GAAP, the Transaction was accounted for using the purchase method with a 100% change in basis. Under U.S. GAAP, a portion of the purchase cost (representing approximately 1% of the purchase price) of the Transaction is accounted for at the carrying value of management's continuing equity interests. The termination of a former senior executive resulted in a step acquisition, as the percentage of the Company owned by management decreased. The results of this step acquisition are reflected in the operations of the Company in the Successor Period. As at December 31, 2005, approximately 0.4% of the purchase cost of the Transaction is accounted for at the carrying value of management's continuing equity interests. As a result, the purchase cost and the reduction of purchase cost is allocated pro rata to the assets acquired and liabilities assumed and shareholder's equity is reduced by a similar amount.

- (4)

- EBITDA, a measure used historically by management to measure operating performance, is defined as net income plus interest, income taxes, depreciation and amortization, other expense (income), net, (gain) loss on refinancing, net and non-controlling interest. Adjusted EBITDA is defined as EBITDA further adjusted to give effect to adjustments required in calculating covenant ratios and compliance under the indentures governing the notes and our senior secured credit facilities. EBITDA and Adjusted EBITDA are not presentations made in accordance with GAAP, are not measures of financial condition or profitability, and should not be considered as an alternative to (1) net income (loss) determined in accordance with GAAP or (2) operating cash flows determined in accordance with GAAP. Additionally, EBITDA and Adjusted EBITDA are not intended to be measures of free cash flow for management's discretionary use, as they do not include certain cash requirements such as interest payments, tax payments and debt service requirements. We believe that the inclusion of EBITDA and Adjusted EBITDA in this prospectus is appropriate to provide additional information to investors about the calculation of certain financial covenants in the indentures governing the notes and our senior secured credit facilities. Adjusted EBITDA is a material component of these covenants. For instance, both the indentures governing the notes and the senior secured credit facilities contain financial ratios that are calculated by reference to Adjusted EBITDA. Non-compliance with the financial ratio maintenance covenants contained in our senior secured credit facilities could result in the requirement to immediately repay all amounts outstanding under such facilities, while non-compliance with the debt incurrence ratio contained in the indentures governing the notes would prohibit us from being able to incur additional indebtedness other than pursuant to specified exceptions. Because not all companies use identical calculations, these presentations of EBITDA and Adjusted EBITDA may

16

not be comparable to other similarly titled measures of other companies. The following table sets forth a reconciliation of net income to EBITDA and EBITDA to Adjusted EBITDA for the periods indicated:

| | Predecessor

| | Successor

| | Combined

| | Pro Forma

| | Successor

| | Combined

| | Successor

| |

|---|

| | Fiscal Years

Ended

December 31,

| | Period From

January 1,

2005

to April 6,

| | Period From

February 2,

2005 to

December 31,

| | Fiscal Year

Ended

December 31,

| | Fiscal Year Ended December 31,

| | Period From

February 2,

2005 to

September 30,

| | Nine Months

Ended

September 30,

| | Nine Months

Ended

September 30,

| |

|---|

| | 2003

| | 2004

| | 2005

| | 2005

| | 2005

| | 2005

| | 2005

| | 2005

| | 2006

| |

|---|

| |

| |

| |

| |

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

| |

|---|

| | (in millions of U.S. dollars)

| |

|---|

| Reconciliation of net income (loss) to EBITDA: | | | | | | | | | | | | | | | | | | | |

| Net income (loss) | | $ | 107.7 | | $ | 128.0 | | $ | (30.7 | ) | $ | (69.8 | ) | $ | (100.5 | ) | $ | (62.8 | ) | $ | (35.6 | ) | $ | (66.2 | ) | $ | (13.2 | ) |

| Interest | | | 36.4 | | | 39.5 | | | 11.2 | | | 137.1 | | | 148.3 | | | 177.8 | | | 90.4 | | | 101.6 | | | 137.2 | |

| Income taxes | | | 34.5 | | | 42.7 | | | (8.3 | ) | | (16.3 | ) | | (24.6 | ) | | (6.3 | ) | | (19.3 | ) | | (27.6 | ) | | (4.8 | ) |

| Depreciation and amortization | | | 47.7 | | | 62.6 | | | 19.0 | | | 90.3 | | | 109.3 | | | 119.3 | | | 59.5 | | | 78.5 | | | 92.0 | |

| Other expense (income) | | | 3.1 | | | 7.7 | | | 66.4 | | | 22.6 | | | 89.0 | | | 12.0 | | | 20.5 | | | 86.8 | | | 16.6 | |

| Non-controlling interest | | | 5.5 | | | 6.8 | | | 1.3 | | | 5.3 | | | 6.6 | | | 6.6 | | | 4.0 | | | 5.3 | | | 5.6 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| EBITDA | | $ | 234.9 | | $ | 287.3 | | $ | 58.9 | | $ | 169.1 | | $ | 228.1 | | $ | 246.6 | | $ | 119.5 | | $ | 178.5 | | $ | 233.4 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| | Pro Forma

| | Combined

| | Successor

| |

|---|

| | Fiscal Year

Ended

December 31,

| | Nine Months

Ended

September 30,

| | Nine Months

Ended

September 30,

| |

|---|

Reconciliation of EBITDA to Adjusted EBITDA:

| |

|---|

| | 2005

| | 2005

| | 2006

| |

|---|

| EBITDA | | $ | 246.6 | | $ | 178.5 | | $ | 233.4 | |

| | Receivables transaction charges(a) | | | 6.5 | | | 4.2 | | | 5.9 | |

| | Inventory purchase accounting adjustment(b) | | | 1.2 | | | 20.5 | | | — | |

| | U.S. fire(c) | | | 5.0 | | | 5.0 | | | — | |

| | Facility closures/realignments(d) | | | 1.8 | | | 1.8 | | | 1.9 | |

| | Hurricanes impact(e) | | | 7.9 | | | 7.9 | | | (0.7 | ) |

| | U.K. fire(f) | | | 1.6 | | | — | | | — | |

| | Inventory losses(g) | | | 8.4 | | | — | | | 9.0 | |

| | Acquisitions impact (including synergies)(h) | | | 9.5 | | | 7.8 | | | — | |

| | Stock-based compensation(i) | | | 4.5 | | | 1.8 | | | 1.2 | |

| | Franchise and capital tax | | | 3.0 | | | 1.4 | | | 1.9 | |

| | Foreign exchange gains | | | (4.2 | ) | | (1.3 | ) | | (0.6 | ) |

| | Craftmaster contract termination(j) | | | 1.3 | | | 1.3 | | | — | |

| | Other(k) | | | 5.3 | | | — | | | 4.7 | |

| | |

| |

| |

| |

| Adjusted EBITDA | | $ | 298.4 | | $ | 228.9 | | $ | 256.8 | |

| | |

| |

| |

| |

- (a)

- Represents transaction charges related to the sale of receivables.

- (b)

- Margins were impacted by fair value adjustments to increase the value of inventory acquired as part of business combinations. Acquisitions completed following the Transaction resulted in an adjustment that increased cost of sales by approximately $1.2 million during the fourth quarter of 2005.

17

- (c)

- During the first quarter of 2005, we experienced an equipment electrical fire at a door facings plant located in the southeastern United States reducing profitability by an estimated $5.0 million.

- (d)

- We incurred $1.8 million of costs related to a significant realignment of its exterior door manufacturing facilities in the first quarter of 2005. During the first quarter of 2006, we rationalized and relocated certain facilities to better align capacity with demand. Total costs associated with these activities were $1.9 million.

- (e)

- During the third quarter of 2005, our operations were adversely impacted by hurricanes in parts of the southeastern United States, resulting in a $7.9 million reduction in profits. During the third quarter of 2006, we received $0.7 million of insurance proceeds.

- (f)

- In the fourth quarter of 2005, we lost $1.6 million of inventory due to a fire caused by arsonists at a leased warehouse near a factory located in the United Kingdom.

- (g)

- In the fourth quarter of 2005, we undertook a review of a product line of exterior doors that are distributed in the United States. Due to a reduction in anticipated future market demand for the product and the age of the inventory, a write down of $7.0 million was recorded on this inventory. Other write-offs of $1.4 million were also recorded. During the second quarter of 2006, we wrote down $9.0 million of obsolete inventory at various facilities within the organization.

- (h)

- We estimated that the six acquisitions completed during 2005 would have resulted in additional EBITDA that was not included in Masonite's 2005 consolidated results. Included in that calculation of Adjusted EBITDA for the last twelve months ended December 31, 2005 is $9.5 million of pro forma EBITDA and related synergies.

- (i)

- Represents non-cash equity compensation expense.

- (j)

- Represents $1.3 million of estimated cost savings that would have been achieved (in the first quarter of 2005) had the molded door facing supply contract between Masonite and Craftmaster been terminated as of January 1, 2004.

- (k)

- Adjusted EBITDA also excludes certain other costs, including employee future benefits, severance, litigation, and sponsor fees.

18

RISK FACTORS

You should consider carefully the following information about these risks, together with the other information contained in this prospectus, before participating in the exchange offer.

Risks Related to Our Indebtedness and the Notes

We have a substantial amount of indebtedness, which may adversely affect our cash flow and our ability to operate our business, remain in compliance with debt covenants and make payments on our indebtedness, including the notes.

As of September 30, 2006, we had outstanding indebtedness of approximately $2,030.2 million, and availability of $273.8 million under our revolving credit facility after giving effect to outstanding letters of credit. Our outstanding indebtedness represented approximately 78% of our total capitalization (based on total capitalization of $2,594.7 million).

Our substantial indebtedness could have important consequences to you. For example, it could:

- •

- make it more difficult for us to satisfy our obligations with respect to our indebtedness, including the notes, and any failure to comply with the obligations of any of our debt instruments, including financial and other restrictive covenants, could result in an event of default under the indentures governing the notes and the agreements governing such other indebtedness;

- •