QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on July 28, 2008

Registration Statement No. 333-142635

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 7 to

Form S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

CONSONUS TECHNOLOGIES, INC.

(Exact name of Registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 3572 (Primary Standard Industrial Classification Code Number) | 45-0547710 (I.R.S. Employer Identification No.) | ||

301 Gregson Drive Cary, North Carolina 27511 (919) 379-8000 (Address, including zip code, and telephone number, including area code, of Registrant's principal executive office) | ||||

Michael G. Shook Chief Executive Officer Consonus Technologies, Inc. 301 Gregson Drive Cary, North Carolina 27511 (919) 379-8000 (Name, address, including zip code, and telephone number, including area code, of agent for service) | ||||

Copies to: | ||||||

| Steven H. Lang Greenberg Traurig LLP The Forum 3290 Northside Parkway Suite 400 Atlanta, GA 30327 (678) 553-2100 | John Randall Lewis Wilson Sonsini Goodrich & Rosati, Professional Corporation One Market Street Spear Tower, Suite 3300 San Francisco, California 94105-1126 (415) 947-2000 | Brian Pukier Ian Putnam Stikeman Elliott LLP Commerce Court West Suite 5300 199 Bay Street Toronto, Ontario Canada M5L 1B9 (416) 869-5500 | Joris Hogan Kevin Morris Torys LLP 237 Park Avenue New York, New York 10017 (212) 880-6000 | |||

Approximate date of commencement of proposed sale to the public:As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. o

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

PART I

INFORMATION REQUIRED IN PROSPECTUS

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state or other jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 28, 2008

3,000,000 Shares

CONSONUS TECHNOLOGIES, INC.

Common Stock

This is an initial public offering of shares of common stock of Consonus Technologies, Inc. We are offering for sale 3,000,000 shares of our common stock. It is currently estimated that the initial public offering price per share will be between $8.00 and $10.00.

No public market currently exists for our common stock. Our common stock has been approved for quotation on the Nasdaq Capital Market under the symbol "DCTI."

Investing in our common stock involves risks.

See "Risk Factors" beginning on page 12.

Neither the Securities and Exchange Commission nor any other state or foreign securities commission or regulatory authority has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| | Per Share | Total | ||||

|---|---|---|---|---|---|---|

| Initial public offering price | $ | $ | ||||

Underwriting discounts and commissions | $ | $ | ||||

Proceeds, before expenses, to Consonus Technologies, Inc. | $ | $ | ||||

The selling stockholders have granted the underwriters an over-allotment option, exercisable for a period of 30 days from the date of the closing of this offering, to purchase up to 450,000 additional shares of common stock (being 15% of the number of shares offered hereby) to cover over-allotments, if any.

The underwriters expect to deliver the shares on or about , 2008.

| Merriman Curhan Ford & Co. | ||||

Jesup & Lamont Securities Corp. | ||||

The date of this Prospectus is , 2008

No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus. You must not rely on any unauthorized information or representations. This prospectus is an offer to sell only the shares of common stock offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date, unless otherwise indicated.

Through and including , 2008 (the 25th day after the date of this prospectus), all dealers effecting transactions in shares of common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

For investors outside the United States and Canada, neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States and Canada. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

| | Page | |

|---|---|---|

| Prospectus Summary | 1 | |

| Risk Factors | 12 | |

| Special Note Regarding Forward-Looking Statements | 26 | |

| Use of Proceeds | 28 | |

| Dividend Policy | 28 | |

| Capitalization | 29 | |

| Dilution | 30 | |

| Selected Financial Information | 32 | |

| Unaudited Pro Forma Condensed Consolidated Financial Data | 34 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 42 | |

| Our Business | 70 | |

| Management | 86 | |

| Certain Relationships and Related Transactions | 140 | |

| Principal and Selling Stockholders | 148 | |

| Description of Capital Stock | 153 | |

| Shares Eligible for Future Sale | 157 | |

| Material United States Federal Income Tax Considerations | 159 | |

| Underwriting | 163 | |

| Legal Matters | 167 | |

| Experts | 167 | |

| Where You Can Find More Information | 168 | |

| Index to Financial Statements | F-1 |

i

This summary highlights information contained in this prospectus. Because it is a summary, it does not contain all of the information you should consider before investing in our common stock. You should carefully read the entire prospectus. In particular, you should read the section entitled "Risk Factors" and our financial statements and the notes thereto included elsewhere in this prospectus.

INFORMATION ABOUT THIS PROSPECTUS

Unless the context otherwise requires, any references in this prospectus to "Consonus," "CTI," "we," "our," "us" and the "Company" refer to Consonus Technologies, Inc. and its subsidiaries, being Strategic Technologies, Inc., or "STI," and Consonus Acquisition Corp., or "CAC". Unless the context otherwise requires, financial information that relates to periods prior to the STI Merger is presented on a pro forma consolidated basis.

In connection with the STI Merger, CAC's shares in its subsidiary, CTI, were canceled, and the shareholders of STI and CAC exchanged their respective shares for new shares of CTI. As CAC and CTI were under common control by Knox Lawrence International, LLC, or "KLI," at the time of the STI Merger, the financial statements of CAC and CTI have been combined at historical values as of the date of inception (March 31, 2005) of CAC. All references to CAC within the document refer to the combined historical financial statements of CAC and CTI prior to the STI Merger with CTI being the surviving entity.

On January 8, 2008 we completed a reverse stock split whereby each 1.5 shares of our common stock were exchanged for 1 share of common stock. All CAC and CTI share amounts in this prospectus have been retroactively adjusted to give effect to this stock split.

We are a provider of IT infrastructure services and solutions, data center services and related managed services to the growing small and medium size business market in the East, Southeast and select markets in the Western part of the United States. Our highly secure and reliable data centers combined with our ability to offer a comprehensive suite of related IT infrastructure services gives us an ability to offer our clients customized solutions to address their critical needs of data center availability, data manageability, disaster recovery and data center consolidation as well as a variety of other related managed services.

Our data center related services and solutions primarily enable business continuity, back-up and recovery, capacity-on-demand, regulatory compliance (such as email archiving), virtualization, and offer data center best practice methodologies and software as a service. Additionally, we provide managed hosting, maintenance and support for all of our solutions, as well as related professional and consulting services. We have a large and diverse customer base comprised of over 650 active customers in 38 states in the United States.

We have chosen to focus on small and medium size business clients in under-served geographic markets. We define small and medium size businesses as (i) companies having between $50 million and $1 billion in annual revenue, (ii) companies with 300 to 2,000 employees, and (iii) regional and department-level offices of large enterprises.

Our Company is the result of a merger with Strategic Technologies, Inc. which occurred on January 22, 2007, at which time, CAC and STI became our direct wholly-owned subsidiaries. Set forth

1

below is a timeline summarizing the historical background of our Company and our subsidiaries. For a further description of the STI Merger and our history, see "Our Business – Our History."

| Timeline of Key Dates | Description of Event | |

|---|---|---|

| August 31, 1988 | Incorporation of STI | |

| February 22, 2000 | STI acquires Path Tech Software Solutions, Inc. | |

| October 17, 2001 | STI acquires Allied Group, Inc. | |

| March 31, 2005 | Incorporation of CAC | |

| May 2, 2005 | CAC merges with Gazelle Technologies, Inc. | |

| May 31, 2005 | CAC acquires all of the assets of Consonus, Inc. from Questar InfoComm, Inc. | |

| October 13, 2006 | Incorporation of CTI | |

| October 18, 2006 | Execution of the agreement and plan of merger and reorganization by and among CAC and STI and certain other entities, as further described in "Our Business – Our History." | |

| January 22, 2007 | Consummation of the STI Merger; CAC and STI became CTI's direct wholly owned subsidiaries |

In connection with the STI Merger, CAC's shares in its subsidiary, CTI, were canceled, and the shareholders of STI and CAC exchanged their respective shares for new shares of CTI. As CAC and CTI were under common control by KLI at the time of the STI Merger, the financial statements of CAC and CTI have been combined at historical values as of the date of inception (March 31, 2005) of CAC. All references to CAC within the document refer to the combined historical financial statements of CAC and CTI prior to the STI Merger with CTI being the surviving entity.

As part of the STI Merger and as a requirement by our lenders to segregate assets until such time as the Avnet, Inc. indebtedness is fully repaid, we entered into an operating agreement with CAC, STI, KLI, Michael G. Shook, William M. Shook and Irvin J. Miglietta, our principal stockholders, on the closing of the STI Merger, which relates to the operation and management of the Company following the closing of the STI Merger and provides for the joint operation of CAC and STI. The operating agreement, among other things, allocates management responsibilities, provides for the segregation of assets of CAC and STI and sets forth the structure for addressing customer relationships on a going forward basis. Under this agreement, CAC and STI will pool certain management functions in the Company, however, any management, monitoring or other similar fees payable to KLI or its affiliates will not be pooled or otherwise allocated to STI. Pursuant to this agreement, KLI, as CAC's stockholder and the STI stockholders agreed on the composition of the Company's management and the board of directors of CAC and STI following the closing of the STI Merger. The operating agreement will terminate on the repayment of the Avnet indebtedness. For further details on the operating agreement, see "Certain Relationships and Related Transactions – Agreements with our Principal Stockholders."

We believe that our merger with STI has created, or will create, benefits and synergies, including:

- •

- Margin expansion: owning our data centers allows us to operate independently from third party data center providers, if desired, and we expect this to increase our data center utilization by integrating both customer bases.

- •

- Broader service and solution offerings: our IT expertise enables us to provide end-to-end solutions to new and existing customers. The STI Merger has expanded our breadth of service offerings focused on the small and medium size business market. Our hardware and software implementation, configuration expertise and related consulting engagements allow us to offer a broad range of services to our customers.

2

- •

- New services and solutions: our broad operational platform enables the development of new services and solutions designed specifically for small and medium size businesses. For example, we now offer an Internet accessible, remote data back-up service and a real-time remote data replication service which are expected to enable rapid disaster recovery allowing customers to recover from system failures in hours rather than days. This solution was developed utilizing the data center facilities of CAC and the storage expertise of STI. This service was launched on June 1, 2007.

By combining our data centers with STI provided solutions, which include data center best practices, infrastructure design, consulting services and product provisioning, we have created a comprehensive platform to serve the small and medium size business market as well as address an increasing demand for a single-source provider of data center services and solutions. In addition, the STI Merger provides us with cross-selling opportunities over a larger suite of products.

We provide data center and IT infrastructure services and solutions to the growing small and medium size business market. Through CAC's and STI's combined 19 year history, we have developed a comprehensive set of data center-centric skills and capabilities. As a result of the STI Merger, we are now able to utilize this significant combined expertise through our two complementary business lines to deliver customized solutions to our clients on their premises or on a managed basis in our facilities.

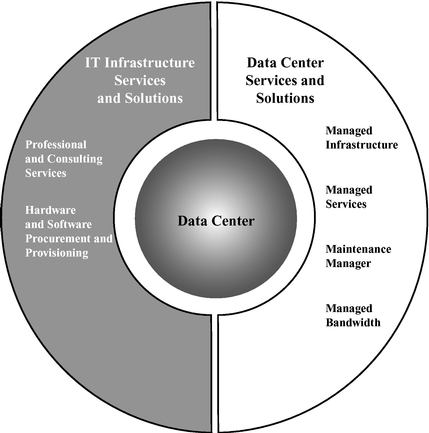

We provide our services and solutions through our two business lines:

- •

- Data center services and solutions: Our data center services and solutions include managed infrastructure, managed services, maintenance manager and managed bandwidth.

- •

- IT Infrastructure services and solutions: Our IT infrastructure services and solutions include professional and consulting services and hardware and software procurement and provisioning.

We believe our strengths can be attributed to several distinguishing factors, including:

- •

- Broad Service Offering: Our comprehensive offering of data center and IT infrastructure services and solutions, which are packaged into "solution" sets, and our single-source service approach, distinguish us in the small and medium-sized business market.

- •

- Diverse and Loyal Customer Base: Our large and diverse customer base consists of over 650 active customers in 38 states in the United States across several industries. No customer exceeded 5% of our consolidated pro forma revenue for the year ended December 31, 2007. We offer managed and hosting services to over 450 of our customers and historically experience very high renewal rates. Specifically, our renewal rate for the twelve months ended March 31, 2008 was approximately 93%.

- •

- Strategic Geographic Presence: We focus on small to medium size businesses in underserved geographic markets where a local presence, broad resources and thought leadership are in demand.

- •

- Focus on High Growth IT Markets: We look to capitalize on the growth trends in IT infrastructure and data center services, such as increased outsourcing of IT. The small and medium size business market is expected to experience higher growth than the overall market with respect to IT related services.

3

- •

- Attractive Business Model Utilization: We believe there are significant opportunities to expand our margins with respect to many of our existing and new customers. All of our data center fixed costs, excluding depreciation, are sufficiently covered based on a current capacity utilization of approximately 74% as of June 30, 2008 for our three data centers. This includes our new data center in the Salt Lake City, Utah area (Presidents Data Center), but excludes our Metro Data Center, as its lease expired on May 31, 2008.

- •

- Recurring Revenues from Data Center Services and Solutions: Revenue derived from our data center services and solutions provides a solid basis for long-term relationships with our customers resulting in strong recurring revenue for this component of our business, which represented approximately 35% of our consolidated pro forma revenues for the year ended December 31, 2007.

- •

- Experienced Management Team: Our experienced and dedicated management team includes a core group of executives and senior managers who have, on average, approximately 22 years of industry experience. The current management team has successfully integrated our prior acquisitions and has achieved organic growth through both geographic expansion and new product offerings.

- •

- Established Relationships with Industry Leading Vendors: Our relationships with leading technology vendors facilitate our ability to meet the IT needs of our customers. Our director and Chief Executive Officer is a member of the Sun Microsystems, Inc. Advisory Council and the Symantec Corporation National Council, and our director and Executive Vice-President of Channels and Alliances is a member of the BMC Software Inc. National Advisory Board. These advisory positions provide us with opportunities to expand our relationships with senior vendor management and align our business strategy with these important vendors.

In addition to increasing penetration with existing customers and adding new clients, our strategy is to provide a comprehensive suite of IT infrastructure and data center services and solutions across our customer base. We will also seek to enhance through the continued development of new services, further geographic expansion and through strategic acquisitions and partnerships, thus participating in industry consolidation on a regional basis. The key components of our growth strategy are:

- •

- Penetration of Existing Customer Base: We currently have over 650 active customers. We believe that our enhanced service and solution offerings represent a significant opportunity to increase our revenue per customer. By cross selling our broad suite of services and solutions, our goal is to expand our share of our customers' IT expenditures. For example, recent cross-sell activities have resulted in new managed services contracts from our existing customers.

- •

- Development of New Solutions: We are continuously developing new services and creating customized solution sets to meet our customers' evolving requirements. We collaborate with our customers, vendors, and industry analysts to create a highly targeted solution roadmap.

- •

- Organic Geographic Expansion: We have grown our business in markets where small and medium size business concentration is high and competition is fragmented. We have developed a disciplined process of identifying, targeting and assessing new expansion opportunities.

- •

- Strategic Acquisitions: We believe that we can accelerate our growth through strategic acquisitions of businesses that expand our solution set and geographic reach. Our senior management and board have considerable acquisition experience and have completed four acquisitions for our business.

4

Our ability to execute our growth strategy is subject to various risks, including those that are generally associated with operating in our industry. For example, we may experience disruptions or complications as we continue to integrate our CAC and STI businesses, our larger customers may choose to in-source IT capabilities as a substitute for our services and solutions, and intense and growing competition from our competitors may subject us to negative pricing pressures. These factors and other factors may limit our ability to successfully execute our business strategy. Investing in our common stock involves substantial risk. You should carefully consider all of the information set forth in this prospectus and, in particular, should evaluate the specific factors set forth under "Risk Factors" in deciding whether to invest in our common stock.

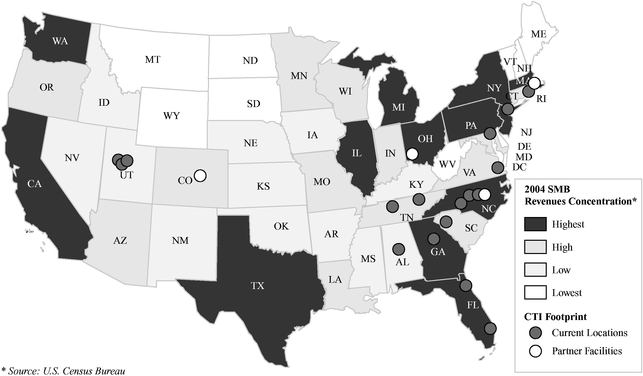

We are headquartered in Cary, North Carolina, with 11 regional sales offices in Atlanta, Georgia; Birmingham, Alabama; Charlotte, North Carolina; Ft. Lauderdale, Florida; Jacksonville, Florida; Glastonbury, Connecticut; Greenville, South Carolina; Knoxville, Tennessee; Nashville, Tennessee; Salt Lake City, Utah, and Rockville, Maryland. We operate three data center facilities in the Salt Lake City, Utah area (excluding our Metro Data Center which lease expired on May 31, 2008) and have contractual arrangements with data center facilities in Denver, Colorado; Cincinnati, Ohio; Boston, Massachusetts and Raleigh, North Carolina. See "Management's Discussion And Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources – Long-Term Debt."

5

CTI is a Delaware corporation incorporated on October 13, 2006. Our principal executive offices are located at 301 Gregson Drive, Cary, North Carolina 27511. Our telephone number is (919) 379-8000. Our website address is www.consonus.com. Information on our website is not, and should not be deemed to be part of this prospectus, and is not being incorporated by reference herein.

On January 22, 2007, we consummated a merger transaction, referred to as the STI Merger, with STI, CAC, and certain other entities. See "Our Business – Our History." CAC was incorporated on March 31, 2005 under the laws of the State of Delaware by its majority stockholder KLI, a private equity firm based in New York City. STI was incorporated on August 31, 1988 under the laws of the State of North Carolina.

As part of the STI Merger and as a requirement by our lenders to segregate assets until such time as the Avnet, Inc. indebtedness is fully repaid, we entered into an operating agreement with CAC, STI, KLI, Michael G. Shook, William M. Shook and Irvin J. Miglietta, our principal stockholders, on the closing of the STI Merger, which relates to the operation and management of the Company following the closing of the STI Merger and provides for the joint operation of CAC and STI. The operating agreement, among other things, allocates management responsibilities, provides for the segregation of assets of CAC and STI and sets forth the structure for addressing customer relationships on a going forward basis. Under this agreement, CAC and STI will pool certain management functions in the Company, however, any management, monitoring or other similar fees payable to KLI or its affiliates will not be pooled or otherwise allocated to STI. Pursuant to this agreement, KLI, as CAC's principal stockholder and the STI stockholders agreed on the composition of the Company's management and the board of directors of CAC and STI following the closing of the STI Merger. The operating agreement will terminate on the repayment of the Avnet indebtedness. For further details on the operating agreement, see "Certain Relationships and Related Transactions – Agreements with our Principal Stockholders."

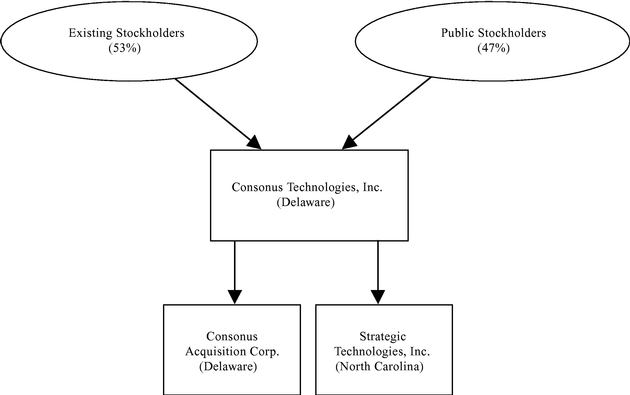

The following diagram illustrates the Company's organizational structure following this offering, excluding any exercise of the over-allotment option:

6

THIRD PARTY AND MANAGEMENT INFORMATION

This prospectus includes market share information, industry data and forecasts obtained from independent industry publications, market research, surveys and other sources. Although we believe these sources to be reliable, we have not independently verified any of the data nor ascertained the underlying economic assumptions relied upon therein. Some data is also based on our management's knowledge of the industry and our estimates and assumptions relating to the industry, some of which are derived from our management's review of data from independent sources. Management's knowledge of the industry has been developed through its experience and participation in the industry. Our management believes that its knowledge of the industry is accurate and its estimates and assumptions are reasonable. However, certain of the information contained herein relating to the industry cannot be independently verified.

7

Offering | 3,000,000 shares of common stock. | |

Shares outstanding after this offering | 6,341,345 shares of common stock. | |

Use of proceeds | We intend to use the net proceeds for the repayment of certain indebtedness, certain advisory services relating to the STI Merger and for sales and marketing, research and development, working capital and other general corporate purposes, including acquisitions or investments. | |

You should read the discussion in the "Use of Proceeds" section of this prospectus for more information. | ||

Offer price | Estimated to be between $8.00 and $10.00 per share. | |

Over-allotment option | The selling stockholders have granted the underwriters an over-allotment option, exercisable for a period of 30 days from the date of the closing of this offering, to purchase up to a total of 450,000 additional shares of common stock (being 15% of the number of shares offered hereby) solely to cover over-allotments, if any, and for market stabilization purposes. We will not receive any proceeds from the sale of the shares of our common stock by the selling stockholders as part of the over-allotment. | |

Dividend policy | We have never declared or paid any dividends on our common stock; however, the declaration and payment of future dividends is discretionary, and the amount, if any, will be dependent upon our results of operations, financial condition, contractual restrictions and other factors deemed relevant by our board of directors. | |

Risk factors | You should read the "Risk Factors" section beginning on page 11 and the other information in this prospectus for a discussion of the factors that you should carefully consider before deciding to invest in our shares of common stock. | |

Proposed Nasdaq Capital Market symbol | DCTI |

The number of shares of common stock to be outstanding after this offering is based on the number of shares of common stock outstanding as of June 30, 2008. The shares of common stock reflect a reverse stock split that was approved by the board of directors and stockholders of CTI in January 2008, whereby each 1.5 shares of common stock were exchanged for 1 share of common stock. These shares include: (i) 84,915 shares of common stock that we have reserved upon the vesting of the outstanding equity awards, as further described under "Management – Assumption of Outstanding Equity Awards in CAC and STI Options in connection with the STI Merger;" and (ii) the number of shares of common stock being issued in connection with this offering. This number does not include:

- •

- 87,023 deferred shares of common stock issued on January 22, 2007 under the 2007 Equity Plan, as further described under "Management – Deferred Stock Agreements;"

- •

- 28,628 shares of common stock reserved for future grant or issuance under the 2007 Equity Plan, as further described under "Management – New Equity Plan of the Company;"

- •

- outstanding options to purchase 164,127 shares of our common stock, at a weighted average exercise price of $24.33 per share, as further described under "Management – Assumption of Outstanding Equity Awards in CAC and STI Options in connection with the STI Merger and Options to Purchase Securities;" and

8

- •

- an outstanding warrant to purchase 231,514 shares of our common stock, at an exercise price of $0.00039 per share, as further described under "Description of Capital Stock – Warrant" and "Certain Relationships and Related Transactions – Warrant."

Except as otherwise indicated in this prospectus, all of the information in this prospectus regarding shares of our common stock reflects no exercise or forfeiture of outstanding options and the warrant to purchase shares of our common stock as further described under "Management – Assumption of Outstanding Equity Awards in CAC and STI Options in connection with the STI Merger and Options to Purchase Securities," "Description of Capital Stock – Warrant" and "Certain Relationships and Related Transactions – Warrant."

We completed a reverse stock split whereby each 1.5 shares of our common stock were exchanged for 1 share of common stock on January 8, 2008. All CAC and CTI share amounts in this prospectus have been retroactively adjusted to give effect to this reverse stock split.

The following table sets forth a summary of certain historical and unaudited pro forma consolidated financial information for CTI, CAC, and its predecessor, Consonus, Inc. for the periods indicated. The following summary historical and unaudited pro forma consolidated financial information should be read in conjunction with our financial statements and related notes and "Selected Financial Information," "Unaudited Pro Forma Condensed Consolidated Financial Data" and "Management's Discussion and Analysis of Financial Condition and Results of Operations," each of which are included elsewhere in this prospectus. Historical results are not necessarily indicative of the results that may be expected for any future period.

The statement of operations information for the year ended December 31, 2005 includes the audited statements of operations of a predecessor company, Consonus, Inc., for the period January 1, 2005 to May 30, 2005 and a successor company for the period May 31, 2005 to December 31, 2005 (CAC was incorporated on March 31, 2005, but did not buy the assets of Consonus, Inc. until May 31, 2005, and therefore this period only includes operations for the period May 31, 2005 to December 31, 2005). The balance sheet information as of December 31, 2005 has been derived from the audited financial statements of CTI.

The statement of operations information for the years ended December 31, 2006 and 2007 and the balance sheet information as of such dates have been derived from the audited financial statements of CTI.

The unaudited statement of operations information for the three months ended March 31, 2008 and the unaudited balance sheet information as of such date has been derived from the unaudited financial statements of CTI.

The unaudited pro forma consolidated statement of operations information of CTI for the year ended December 31, 2007 is derived from such financial statement included elsewhere in this prospectus. See "Unaudited Pro Forma Condensed Consolidated Financial Data."

Our unaudited pro forma condensed consolidated financial data has been prepared by applying pro forma adjustments to the historical financial statements of CTI, the historical financial statements of CAC and the historical financial statements of STI, which are included elsewhere in this prospectus.

In connection with the STI Merger, CAC's shares in its subsidiary, CTI, were canceled, and the shareholders of STI and CAC exchanged their respective shares for new shares of CTI. As CAC and CTI were under common control by KLI at the time of the STI Merger, the financial statements of CAC and CTI have been combined at historical values as of the date of inception (March 31, 2005) of CAC. All

9

references to CAC within this prospectus refer to the combined historical financial statements of CAC and CTI prior to the STI Merger with CTI being the surviving entity.

On January 22, 2007, the STI Merger was effective. The acquisition was accounted for under the purchase method of accounting in accordance with SFAS No. 141, "Business Combinations (SFAS 141)" and the acquired assets and liabilities were recorded at their estimated fair values. The purchase price was approximately $41.7 million consisting of 761,118 shares of our common stock, 231,514 warrants to purchase common stock, and 172,361 of stock options, assumption of $29.5 million in long-term debt, and acquisition related expenses of approximately $1.4 million. The estimated fair value of the equity instruments was approximately $10.8 million.

The unaudited pro forma condensed consolidated statement of operations for the year ended December 31, 2007 gives effect to the following transactions as if each had occurred on January 1, 2007:

- •

- the STI Merger, as discussed above and throughout this prospectus;

- •

- the issuance of 3,000,000 shares of our common stock in this offering at an assumed price of $9.00 per share, the mid-point of the range shown on the cover of this prospectus; and

- •

- the use of the proceeds we will receive as set forth in the "Use of Proceeds" section of this prospectus.

10

The following table presents a summary of certain historical financial information and unaudited pro forma financial information of CTI, CAC and its predecessor (in thousands, including footnotes):

| | Predecessor January 1 to May 30, 2005 (1) | Successor May 31 to December 31, 2005 | Year Ended December 31, 2006 | Year Ended December 31, 2007 | Pro forma Year Ended December 31, 2007 (1) | Three Months Ended March 31, 2008 | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | | | (unaudited) | (unaudited) | |||||||||||||||

| Statement of operations information: | |||||||||||||||||||||

| Revenues | $ | 3,254 | $ | 5,010 | $ | 7,112 | $ | 101,039 | $ | 104,169 | $ | 25,127 | |||||||||

| Cost of revenues | 1,122 | 1,655 | 2,698 | 73,209 | 75,596 | 17,501 | |||||||||||||||

| Gross profit | 2,132 | 3,355 | 4,414 | 27,830 | 28,573 | 7,626 | |||||||||||||||

| Selling, general and administrative expenses (2) | 1,012 | 1,375 | 2,383 | 24,876 | 26,034 | 6,669 | |||||||||||||||

| Depreciation and amortization expense (3) | 288 | 690 | 1,163 | 3,565 | 3,702 | 1,042 | |||||||||||||||

| Acquisition related expenses and write-off of previously capitalized offering costs | – | – | 198 | – | – | 5,924 | |||||||||||||||

| Research and development expense | – | 176 | – | – | – | – | |||||||||||||||

| Total other operating expenses | 1,300 | 2,241 | 3,744 | 28,441 | 29,736 | 13,635 | |||||||||||||||

| Income (loss) from operations | 832 | 1,114 | 670 | (611 | ) | (1,163 | ) | (6,009 | ) | ||||||||||||

Interest income (expense), net (4) | 51 | (600 | ) | (1,133 | ) | (4,035 | ) | (3,153 | ) | (1,070 | ) | ||||||||||

| Other expense | (10 | ) | – | – | – | – | |||||||||||||||

| Income (loss) before taxes | 873 | 514 | (463 | ) | (4,646 | ) | (4,316 | ) | (7,079 | ) | |||||||||||

| Income tax expense (benefit) (5) | 363 | 173 | (176 | ) | 303 | 740 | – | ||||||||||||||

| Net income (loss) | $ | 510 | $ | 341 | $ | (287 | ) | $ | (4,949 | ) | $ | (5,056 | ) | $ | (7,079 | ) | |||||

Balance sheet information: | |||||||||||||||||||||

| Cash and cash equivalents | $ | – | $ | – | $ | 982 | $ | 1,557 | |||||||||||||

| Total assets | 19,498 | 21,673 | 100,971 | 91,624 | |||||||||||||||||

| Long-term debt (including current portion) | 14,356 | 13,717 | 43,121 | 44,506 | |||||||||||||||||

| Total liabilities | 16,515 | 18,018 | 89,662 | 87,788 | |||||||||||||||||

| Stockholders' equity | 2,983 | 3,655 | 11,309 | 3,836 | |||||||||||||||||

- (1)

- No balance sheet data is presented.

- (2)

- For the unaudited pro forma consolidated statement of operations for the year ended December 31, 2007, a total of $(2,762) of pro forma adjustments were made to selling, general and administrative expenses including $67 adjustment for stock compensation expense incurred, $(1,791) adjustment to exclude compensation expense prior to the STI Merger in connection with the forgiveness of notes receivable from shareholders of STI, $(865) adjustment to remove acquisition related expenses incurred by STI prior to the STI Merger and $(173) adjustment to exclude compensation expense related to acceleration of vesting of stock options and the modification of the exercise price of certain options of STI immediately prior to the STI Merger.

See "Unaudited Pro Forma Condensed Consolidated Financial Data", Notes to the Unaudited Pro Forma Condensed Consolidated Financial Statements, Note 4.

- (3)

- For the unaudited pro forma consolidated statement of operations for the year ended December 31, 2007, pro forma adjustments of $85 were made to depreciation and amortization expense related to the amortization of intangibles recorded in connection with the STI Merger.

See "Unaudited Pro Forma Condensed Consolidated Financial Data", Notes to the Unaudited Pro Forma Condensed Consolidated Financial Statements, Note 4.

- (4)

- For the unaudited pro forma consolidated statement of operations for the year ended December 31, 2007, $1,120 adjustment to remove the interest expense associated with the notes payable of STI expected to be paid off with the proceeds of this offering.

See "Unaudited Pro Forma Condensed Consolidated Financial Data", Notes to the Unaudited Pro Forma Condensed Consolidated Financial Statements, Note 4.

- (5)

- For the unaudited pro forma consolidated statement of operations for the year ended December 31, 2007, pro forma adjustments made to tax expense are $437 to reflect the incremental provision for state and federal taxes.

See "Unaudited Pro Forma Condensed Consolidated Financial Data", Notes to the Unaudited Pro Forma Condensed Consolidated Financial Statements, Note 4.

11

Investing in our shares of common stock involves a high degree of risk. You should consider carefully the following factors and the other information in this prospectus before deciding to purchase any of our common stock. If any of the following risks actually occur, our business, financial condition, results of operations and cash flow could suffer materially and adversely. In that case, the trading price of our common stock could decline, and you might lose all or part of your investment.

Our business is the result of our merger with STI and the integration plan for the business has not yet been completed. If we are unsuccessful at implementing our integration plan, it could materially adversely affect our business operations and financial position.

Due to the limited operating history of our business combined with that of STI, on a forward going basis, there are risks associated with the STI Merger including the following:

- •

- integrating STI's business operations, systems, employees, compensation philosophies, services, technologies and sales channels into our existing business will be complex, time-consuming and expensive and, in addition, could lead to morale issues, increased employee turnover and lower productivity than anticipated; and

- •

- the STI Merger may disrupt our ongoing business, divert resources, increase our expenses and distract our management.

The integration process following a merger is inherently unpredictable and subject to delay and unexpected costs. We cannot assure you that we will successfully overcome these risks or any other problems we encounter as a result of the STI Merger. Our inability to deal effectively with these risks and successfully integrate the business and operations of STI into our business could materially adversely affect our business, operations and financial position.

Our operations are governed by an operating agreement which affects our ability to fully integrate our business following the STI merger and precludes Consonus and its shareholders from altering the board of directors and management of CAC and STI without the consent of the parties to the operating agreement and the full repayment of the indebtedness with Avnet,Inc.

Covenants under our operating agreement impose certain restrictions and obligations upon how we operate our business. These restrictions, among other things, require us to:

- •

- segregate the business and assets of CAC and STI;

- •

- set forth a structure for segregating the control of all communications and decisions relating to customers of CAC and STI;

- •

- prevent us from consolidating the assets of CAC and STI or the commingling of funds of CTI, STI and CAC;

- •

- require CTI, STI and CAC to maintain an arm's-length relationship among each other and each of their affiliates; and

- •

- prevent each of CTI, STI and CAC from merging or selling all or substantially all of their assets or shares.

Additionally, pursuant to the operating agreement, neither CTI nor its shareholders have any ability to alter either the board of directors or management of STI or CAC or amend the charter documents of CTI, STI or CAC without the consent of the parties to the operating agreement, including Avnet, Inc. The operating agreement will remain in effect following the public offering unless the Avnet, Inc. indebtedness is fully paid or unless the operating agreement is amended which also would require the consent of each of the parties to the operating agreement. As long as the operating agreement remains outstanding, we will not be able to fully integrate the CAC and STI businesses and our

12

operations will be subject to restrictions beyond our control which could result in a material adverse affect our business, operations and financial position.

We have a limited operating history as a merged company, which may make it difficult for you to evaluate our business and prospects.

We have a limited operating history upon which to evaluate our business and prospects. Further, the STI Merger provides additional uncertainty as we have only recently begun to integrate these two businesses. We cannot provide any assurance that we will be profitable in any given period, if at all. In view of the rapidly evolving nature of our business, our limited operating history and the risks discussed elsewhere in these risk factors and throughout this prospectus, we believe that period to period comparisons of operating results are not meaningful and should not be relied upon as an indication of future performance.

We are subject to restrictive debt covenants that impose operating and financial restrictions on our operations and could limit our ability to grow our business. In the past, CAC and STI have been unable to comply with certain financial covenants contained in their respective credit agreements and have obtained waivers of, and amendments to, such covenants and may be required to seek additional waivers and amendments in the future.

Covenants in our indebtedness impose significant operating and financial restrictions on us. These restrictions prohibit or limit, among other things, our incurrence of additional indebtedness, acquisitions and mergers, asset sales and the creation of certain types of liens. These restrictions could limit our ability to obtain future financing, withstand downturns in our business or take advantage of business opportunities.

Furthermore, our indebtedness requires us to maintain specified financial ratios and to satisfy specified financial condition tests. For example, financial covenants in CAC's credit agreement with U.S. Bank National Association ("U.S. Bank") include a minimum fixed charge coverage ratio covenant, a total funded debt covenant and a minimum net worth covenant as defined in the credit agreement. Financial covenants in STI's credit agreement with Avnet, Inc. include a fixed charge coverage ratio, a limitation on capital expenditures, a minimum quarterly revenue attainment, a quarterly gross margin attainment and a maximum amount of past due trade debt as defined in the credit agreement. Our ability to comply with these ratios or tests may be affected by events beyond our control, including prevailing economic, financial and industry conditions.

Due to the loss of a significant customer in December 2005, our earnings before interest, taxes, depreciation and amortization, or EBITDA, decreased on a trailing twelve month basis which resulted in our failure to maintain the total funded debt covenant as required by our credit agreement with U.S. Bank. As a result, on November 22, 2006, CAC obtained a waiver from U.S. Bank of the total funded debt covenant and on December 12, 2006, the credit agreement was amended to reduce this ratio as of December 31, 2006 and March 31, 2007. The covenants contained in the U.S. Bank credit agreement are measured on a quarterly basis. As of March 31, 2008, CAC was in compliance with all of the covenants, as amended.

STI has been unable to satisfy the fixed charge ratio and past due trade debt covenants in its credit agreement with Avnet on numerous occasions, and, as a result, has sought and received numerous waivers and amendments to the credit agreement such as:

- •

- On June 22, 2006, STI and Avnet amended certain financial covenants in the amended and restated refinancing agreement. The amendment also included a waiver for past debt covenant violations.

- •

- As of September 30, 2006, STI was not in compliance with certain financial covenants of the amended and restated refinancing agreement and in October 2006 STI received a waiver in respect of those covenants.

13

- •

- As of December 31, 2006, STI was not in compliance with certain covenants of the amended and restated refinancing agreement and in January 2007 received a waiver in respect of those covenants.

- •

- As of March 31, 2007, STI was not in compliance with certain covenants of the amended and restated refinancing agreement and on May 1, 2007 entered into a second amendment to the amended and restated refinancing agreement to, among other things, amend certain financial covenants. The second amendment also waived any existing covenant violations.

- •

- As of June 30, 2007, STI was not in compliance with certain covenants of the amended and restated refinancing agreement and in August 2007 STI received a waiver in respect of those covenants. In September 2007, STI entered into a third amendment which, among other things, further amended certain restrictive financial covenants.

- •

- As of September 30, 2007, STI was not in compliance with certain financial covenants under the third amendment to the amended and restated refinancing agreement with Avnet. In October 2007, STI entered into a fourth amendment to the amended and restated refinancing agreement with Avnet which, among other things, cured any existing financial covenant violations and restructured STI's indebtedness. STI's previous indebtedness evidenced by certain promissory notes and outstanding past due trade debt was restructured and consolidated into a new loan in the aggregate principal amount of approximately $20.1 million and the indebtedness consisting of past due trade debt was restructured with a remaining sum of $2.9 million.

- •

- As of December 31, 2007, STI was not in compliance with certain financial covenants under the fourth amendment to the amended and restated refinancing agreement with Avnet. In April 2008, STI received a waiver in respect of those covenants. In July 2008, STI entered into a fifth amendment with Avnet to amend certain restrictive financial covenants for covenant periods beginning March 31, 2008, which allowed the company to be in compliance at March 31, 2008.

The covenants under the Avnet credit facility are tested quarterly except for the past due trade debt 3 month average covenant which is tested monthly. Since the fourth amendment to the amended and restated refinancing agreement dated October 8, 2007, STI has been in compliance with this monthly covenant (past due trade debt 3 month average). See "Management's Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources."

If we are unable to comply with the covenants and ratios in our credit facilities, we may be unable to obtain waivers of non-compliance from the lenders, which would put us in default under the credit facilities, or may require us to pay substantial fees or penalties to the lenders. Either development could have a material adverse effect on our business.

We may experience fluctuations in our financial results which will make it difficult to predict our future performance and may result in volatility in the market price of our common stock.

We have experienced fluctuations in our operating results on a quarterly and annual basis. The fluctuations in our operating results may cause the market price of our common stock to be volatile. We expect to experience significant fluctuations in our operating results in the foreseeable future. This could be as a result of several factors, including but not limited to, the size of our operations, the relative significance, particularly on a quarterly basis, of the timing and scope of a relatively small number of large transactions and the long sales cycles related to many of the services and solutions (including our focus on the re-selling of products) we provide to our customers.

These factors and others all tend to make the timing and amount of our revenue unpredictable and may lead to continued or greater period-to-period fluctuations in revenue than we have experienced historically. As a result of these factors, we believe that our quarterly revenue and results of operations are likely to vary in the future and that period-to-period comparisons of our operating results may not be meaningful. You should not rely on the results of one quarter as an indication of future performance.

14

If our quarterly revenue or results of operations fall below the expectations of investors or securities analysts, the price of our common stock could decline substantially.

Our services and solutions have a long sales cycle that may materially adversely affect our business, financial condition and results of operations.

A customer's decision to co-locate in one of our data centers or to purchase other services and solutions from us typically involves a significant commitment of resources, including time. For example, some customers will be reluctant to commit to locating in our data centers until they are confident that the data center has adequate carrier connections and security features. As a result, we have a long sales cycle. These long sales cycles for new business not currently under contract tend to make the timing and amount of our revenue unpredictable. Furthermore, we may expend significant time and resources in pursuing a particular sale or customer that do not result in revenue. As a result of these factors, we believe that our quarterly revenue and results of operations are likely to vary significantly in the future and that period-to-period comparisons of our operating results may not be meaningful. Delays due to length of our sales cycle may also materially adversely affect our business, financial condition and results of operations.

Our customers may choose to in-source IT capabilities as a substitute for our services and solutions, consolidate their relationships with other providers or choose to manage their IT infrastructure in different ways, any of which could adversely affect our success.

As our customers grow in size and complexity and develop more comprehensive back office capabilities, there is an increasing likelihood that they will choose to in-source key IT activities which were previously provided by us in an attempt to reduce expenses. Although we are focused on building our customer base of small to medium-sized businesses, currently, many of our top 10 customers consist of relatively large enterprises, which may further develop their own internal IT or data storage capabilities, thereby decreasing or eliminating the need for our services and solutions. Additionally, our customers may establish relationships or strengthen existing, or form new relationships with systems integrators, third party consulting firms or other parties, which could lead them to terminate their relationships with us, or pursue alternative means to manage their IT infrastructure or data center related activities. If customers representing a material portion of our revenue base decide to terminate the services and solutions we provide for them, our revenue could materially decline and this may adversely affect our business, operating results and financial position.

The loss of our major customers could have a material adverse effect on our business, financial condition and results of operations.

For the year ended December 31, 2007, our top 10 customers generated approximately 27% of our revenue on an unaudited pro forma basis. We expect that our top 10 customers will continue to account for a significant portion of our revenue for the foreseeable future. In 2005, we lost two significant customers, Wachovia Corporation, which represented approximately 14.6% of the revenues of STI for 2005 and MyFamily.com which represented approximately 27% of the revenues of CAC for the period March 31, 2005 (date of inception) to December 31, 2005. It is possible that other large customers could decide to terminate their relationships with us. The loss of one or more of our top 10 customers, or a substantial decrease in demand by any of those customers for our services and solutions, could have a material adverse effect on our business, results of operations and financial condition.

If our security systems are breached we could incur liability, our services may be perceived as not being secure, and our business and reputation could suffer.

Our business involves the storage, management, and transmission of the proprietary information of customers. Although we employ control procedures to protect the security of data we store, manage and transmit for our customers, we cannot guarantee that these measures will be sufficient for this purpose. Breaches of our security could result in misappropriation of personal information, suspension of hosting operations or interruptions in our services. If our security measures are breached as a result of a

15

third-party action, employee error or otherwise, and as a result customers' information becomes available to unauthorized parties, we could incur liability and our reputation would be damaged. This could lead to the loss of current and potential customers. If we experience any breaches of our network security due to unauthorized access, sabotage, or human error, we may be required to expend significant capital and other resources to remedy, protect against or alleviate these and related problems. We also may not be able to remedy these problems in a timely manner, or at all. Because techniques used to obtain unauthorized network access or to sabotage systems change frequently and generally are not recognized until launched against a target, we may be unable to anticipate these techniques or implement adequate preventive measures. Our systems are also exposed to computer viruses, denial of service attacks and bulk unsolicited commercial email, or spam. Being subject to these events and items could cause a loss of service and data to customers, even if the resulting disruption is temporary.

The property and business interruption insurance we carry may not provide coverage adequate to compensate us fully for losses that may occur or litigation that may be instituted against us in these circumstances. We could be required to make significant expenditures to repair our systems in the event that they are damaged or destroyed, or if the delivery of our services to our customers is delayed and our business could be harmed.

In addition, the U.S. Federal Trade Commission and certain state agencies have investigated various companies' use of their customers' personal information. Various governments have also enacted laws protecting the privacy of consumers' non-public personal information. Our failure to comply with existing laws (including those of foreign countries), the adoption of new laws or regulations regarding the use of personal information that require us to change the way we conduct our business, or an investigation of our privacy practices could increase the costs of operating our business.

We face intense and growing competition. If we are unable to compete successfully, our business will be seriously harmed through loss of customers or increased negative pricing pressure.

The market for our services and solutions is extremely competitive. Our competitors vary in size and in the variety of services and solutions they offer, and include:

- •

- national and international hosting, co-location and managed service providers;

- •

- regional hosting providers; and

- •

- national and international full service IT infrastructure outsourcing providers.

Some of our current and potential direct competitors have longer operating histories, significantly greater financial, technical, marketing and other resources than we do, greater brand recognition and, we believe, a larger base of customers. In addition, competitors may operate more successfully or form alliances to acquire significant market share. These direct competitors may be able to adapt more quickly to new or emerging technologies and changes in customer requirements. They may also be able to devote more resources to the promotion, sale and development of their services and solutions than us and there can be no assurance that our current and future competitors will not be able to develop services and solutions comparable or superior to those offered by us at more competitive prices. As a result, in the future, we may suffer from an inability to offer competitive services and solutions or be subject to negative pricing pressure that would adversely affect our ability to generate revenue and adversely affect our operating results.

Our President and Chief Executive Officer and our Executive Vice President of Channels and Alliances have previously had certain disputes with our controlling stockholder, KLI. To the extent further disputes arise and are not resolved to the satisfaction of the parties, there may be a materially adverse effect on our business.

Our President and Chief Executive Officer and our Executive Vice President of Channels and Alliances have previously had disputes with our controlling stockholder, KLI relating to the obligation of KLI to make incentive payments to the Shooks' in a maximum aggregate amount of approximately $795,000, the terms of the Shooks' employment agreements and the repayment of a $100,000 promissory note due from Michael G. Shook to KLI. The promissory note is now in default and KLI has requested

16

Mr. Michael Shook to repay. However, upon the consummation of this offering and if Michael G. Shook is still employed by STI or the Company in his current capacity, KLI will fund a cash bonus in the minimum amount of $589,593 and a maximum amount of $624,688 to Michael G. Shook. A portion of the cash bonus will be paid in the form of forgiveness of the $100,000 promissory note. To the extent that other disputes may arise and are not satisfactorily resolved, there may be consequences on the Company, including utilization of Mr. Michael Shook and Mr. William Shook's time as well as their morale.

Our business will be adversely affected if we cannot successfully retain key members of our management team or retain, hire, train and manage other key employees, particularly in the sales and customer service areas.

Our continued success is largely dependant on the personal efforts and abilities of our executive officers and senior management, including Michael G. Shook, Chief Executive Officer, John Roger, Executive Vice-President and Chief Operating Officer, William M. Shook, Executive Vice-President of Channels and Alliances and Daniel S. Milburn, Senior Vice-President and Chief Operating Officer of Hosting and Infrastructure Services. Our success also depends on our continued ability to attract, retain, and motivate key employees throughout our business. In particular, we are substantially dependent on our skilled technical employees and our sales and customer service employees. Competition for skilled technical, sales and customer service professionals is intense and our competitors often attempt to solicit our key employees and may be able to offer them employment benefits and opportunities that we cannot. There can be no assurance that we will be able to continue to attract, integrate or retain additional highly qualified personnel in the future. In addition, our ability to achieve significant growth in revenue will depend, in large part, on our success in effectively training sufficient numbers of technical, sales and customer service personnel. New employees require significant training before they achieve full productivity. Our recent and planned hires may not be as productive as anticipated, and we may be unable to hire sufficient numbers of qualified individuals. If we are not successful in retaining our existing employees, or hiring, training and integrating new employees, or if our current or future employees perform poorly, growth in the sales of our services may not materialize and our business will suffer.

We are highly dependent on third-party service and technology providers and any loss, impairment or breakdown in those relationships could damage our operations significantly if we are unable to find alternative providers.

We are dependent on other companies to supply various key components of our infrastructure, including network equipment, telecommunications backbone connectivity, the connections from our customers' networks to our network, and connections to other Internet network providers. We are also dependent on the same companies for the hardware, software and services that we sell and deliver to our customers. For example, approximately 61% of the products we sell and deliver to our customers are provided by Sun Microsystems, Inc. and approximately another 18% of the products and services we sell to our customers are provided by Symantec Corporation, based on billing data for the 12 month period ending April 2008. There can be no assurance that any of these providers will be able to continue to provide these services or products without interruption and in an efficient, cost-effective manner, or that they will be able to adequately meet our needs as our business develops. There is also no assurance that any agreements that we have in place with these third-party providers will not be terminated or will be renewed, or if renewed, renewed on commercially acceptable terms. If we are unable to obtain required products or services from third-party suppliers on a timely basis and at an acceptable cost, we may be unable to provide our data center and IT infrastructure services and solutions on a competitive and timely basis, if at all. If our suppliers fail to provide products or services on a timely basis and at an acceptable cost, we may be unable to meet our customer service commitments and, as a result, we may experience increased costs or loss of revenue, which could have a material adverse effect on our business, financial condition and operating results.

17

We resell products and services of third parties that may require us to pay for such products and services even if our customers fail to pay us for the products and services, which may have a negative impact on our cash flow and operating results.

In order to provide resale services such as bandwidth, managed services, other network management services and infrastructure equipment, we contract with third party service providers, such as Sun Microsystems, Inc., NetApp, Inc., XO Holdings, Inc., VeriSign, Inc. and BMC Software Inc. These services require us to enter into fixed term contracts for services with third party suppliers of products and services. If we experience the loss of a customer who has purchased a resale product or service, we will remain obligated to continue to pay our suppliers for the term of the underlying contracts. The payment of these obligations without a corresponding payment from customers will reduce our financial resources and may have a material adverse affect on our financial performance, cash flow and operating results.

We may fail to adequately protect our proprietary technology, which would allow competitors or others to take advantage of our research and development efforts.

We rely upon trade secrets, proprietary know-how, and continuing technological innovation to develop new data center and IT infrastructure services and solutions and to remain competitive. If our competitors learn of our proprietary technology or processes, they may use this information to produce data center and IT infrastructure services and solutions that are equivalent or superior to our services and solutions, which could materially adversely affect our business, operations and financial position. Our employees and consultants may breach their obligations not to reveal our confidential information, and any remedies available to us may be insufficient to compensate our damages. Even in the absence of such breaches, our trade secrets and proprietary know-how may otherwise become known to our competitors, or be independently discovered by our competitors, which could adversely affect our competitive position.

We are dependent on the reliability and performance of our data centers as well as internally developed systems and operations. Any difficulties in maintaining these systems, whether due to human error or otherwise, may result in service interruptions, decreased service quality for our customers, a loss of customers or increased expenditures.

Our revenue and profit depend on the reliability and performance of our services and solutions. We have contractual obligations to provide service level credits to almost all of our customers against future invoices in the event that certain service disruptions occur. Furthermore, customers may terminate their agreements with us as a result of significant service interruptions, or our inability, whether actual or perceived, to provide our services and solutions at desired quality levels or at any time. If our services are unavailable, or customers are dissatisfied with our performance, we could lose customers, our revenue and profits would decrease and our business operations or financial position could be harmed. In addition, the software and workflow processes that underlie our ability to deliver our services and solutions have been developed primarily by our own employees and consultants. Malfunctions in the software we use or human error could result in our inability to provide services or cause unforeseen technical problems. If we incur significant financial commitments to our customers in connection with our failure to meet service level commitment obligations, we may incur significant liability and our liability insurance and revenue reserves may not be adequate. In addition, any loss of services, equipment damage or inability to meet our service level commitment obligations could reduce the confidence of our customers and could consequently impair our ability to obtain and retain customers, which would adversely affect both our ability to generate revenue and our operating results.

The increased use of high power density equipment may limit our ability to fully utilize our data centers.

Customers are increasing their use of high density electrical equipment, such as blade servers, in our data centers which has significantly increased the demand for power. Because most of our data centers were built several years ago, the current demand for electrical power may exceed our designed capacity in these facilities. As electrical power, not space, is typically the limiting factor in our data

18

centers, our ability to fully utilize our data centers may be limited in these facilities which could have a material adverse effect on our business, results of operations and financial condition.

Our business could be harmed by prolonged electrical power outages or shortages, increased costs of energy or general availability of electrical resources.

Our data centers are susceptible to regional variations in the cost of power, electrical power outages, planned or unplanned power outages such as those that occurred in California during 2001 and the U.S. Northeast in 2003, natural disasters such as the tornados on the U.S. East Coast in 2004 and limitations on availability of adequate power resources. Power outages could harm our customers and our business including the loss of our customers' data and extended service interruptions. While we attempt to limit exposure to system downtime by using backup generators and power supplies, we may not be able to limit our exposure entirely even with these protections in place, as was the case with the power outage we experienced in our Salt Lake City West Data Center in 2005. More recently, we experienced a cooling outage in our Salt Lake City South Data Center in May, 2008 and a power outage in June 2008. In the former case, we were not required to issue any credits due to this incident and it had no adverse effect on our customer base but this may not be the case with respect to future power outages. As a result of our May 2008 cooling outage and our June 2008 power outage, we have had to issue approximately $0.2 million of credits to our customers as a result of these events. Customers typically have 90 days to request such a credit. With respect to any increase in energy costs, we may not be able to pass these increased costs on to our customers which could have a material adverse effect on our business, results of operations and financial condition.

Our systems and data centers are vulnerable to natural disasters and other unexpected problems that could lead to interruptions, delays, loss of data, or the inability to accept and fulfill customer subscriptions.

Hurricanes, fire, floods, power loss, telecommunications failures, earthquakes, break-ins, acts of war or terrorism, computer sabotage and similar events could damage or destroy our data centers as well as the systems and information housed in those facilities or the systems we build and manage for our customers. These disasters or problems could temporarily or permanently prevent us from fulfilling existing service obligations and from securing new customers. These events could also cause loss of service and data to customers. Our business could be seriously harmed even if these disruptions are temporary, and our revenue could decline or customers' confidence in our systems could decrease. We could also be required to make significant expenditures if our systems were damaged or destroyed, or if the delivery of our services to our customers were delayed or stopped by any of these occurrences. Disruptions in our business caused by these events could materially adversely affect our business, operating results and financial position.

We may expand through acquisitions of, or investments in, other companies or technologies which may result in additional dilution to our stockholders and consume resources that may be necessary to sustain our business.

One of our business strategies is to acquire complementary services, technologies or businesses. In connection with one or more of these transactions, we may:

- •

- issue additional shares of common stock or other equity securities that would dilute our stockholders' ownership position and could adversely affect the market price of our common stock;

- •

- use cash that we may need in the future to operate our business; and

- •

- incur debt that could have terms unfavorable to us or that we might be unable to repay.

Any acquisition could involve risks, including, but not limited to, the following:

- •

- integrating acquired business operations, systems, employees, services, technologies and sales channels into our existing business, workforce and services could be complex, time-consuming and expensive;

19

- •

- an acquisition may disrupt our ongoing business, divert resources, increase our expenses and distract our management;

- •

- we may assume debt or other liabilities, known and unknown, including litigation risk, associated with the acquired services, technology or a company;

- •

- to the extent an acquired company has a different corporate culture from ours, we may have difficulty assimilating this organization, which could lead to morale issues, increased turnover of employees and lower productivity than anticipated, and could also have a negative impact on the culture of our existing organization;

- •

- we may be required to record substantial accounting charges; and

- •

- an acquisition may involve entry into geographic or business markets in which we have little or no prior experience.

There is also no assurance that we will be able to complete these transactions at all. For example, in 2006 we attempted to negotiate a merger transaction with another party but we were unable to complete it on commercially reasonable terms. In connection with this transaction, we incurred costs of approximately $198,000. In addition, we may not realize the anticipated benefits of any acquisition, including securing the services of key employees. Incurring unknown liabilities or the failure to realize the anticipated benefits of an acquisition could seriously harm our business. Our inability to deal effectively with these risks could materially adversely affect our business, operations and financial position.

Any of the foregoing or other factors could harm our ability to achieve anticipated levels of profit from acquired services, technologies or businesses, or to realize other anticipated benefits of acquisitions. We may not be able to identify or consummate any future acquisitions on favorable terms, or at all. If we do effect an acquisition, it is possible that the financial markets or investors will view the acquisition negatively. Even if we successfully complete an acquisition, it could adversely affect our business.

We operate in a price sensitive market and we are subject to pressures from customers to decrease our fees for the services and solutions we provide. Any reduction in price would likely reduce our margins and could adversely affect our operating results.

The competitive market in which we conduct our business could require us to reduce our prices. If our competitors offer discounts on certain products or services in an effort to recapture or gain market share or to sell other products, we may be required to lower our prices or offer other favorable terms to compete successfully. Any of these changes would likely reduce our margins and could adversely affect our operating results. Some of our competitors may bundle products and services that compete with us for promotional purposes or as a long-term pricing strategy or provide guarantees of prices and product implementations. In addition, many of the services and solutions that we provide and market are not unique to us and our customers and target customers may not distinguish our services and solutions from those of our competitors. All of these factors could, over time, limit or reduce the prices that we can charge for our services and solutions. If we cannot offset price reductions with a corresponding increase in the number of sales or with lower spending, then the reduced revenue resulting from lower prices would adversely affect our margins and operating results.

If we are unable to retain and grow our customer base, as well as their end-user base, our revenue and profit will be adversely affected.