UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-33236

POWERSHARES DB BASE METALS FUND

(A Series of PowerShares DB Multi-Sector Commodity Trust)

(Exact name of Registrant as specified in its charter)

| | |

| Delaware | | 87-0778075 |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

| | |

c/o DB Commodity Services LLC 60 Wall Street

New York, New York | | 10005 |

| (Address of Principal Executive Offices) | | (Zip Code) |

DB BASE METALS MASTER FUND

(A Series of DB Multi-Sector Commodity Master Trust)

(Exact name of Rule 140 Co-Registrant as specified in its charter)

| | |

| Delaware | | 87-0778076 |

(State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

| | |

c/o DB Commodity Services LLC 60 Wall Street

New York, New York | | 10005 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (212) 250-5883

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, an Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “accelerated filer,” “large accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large Accelerated Filer | | ¨ | | Accelerated Filer | | x |

| | | |

| Non-Accelerated Filer | | ¨ (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of outstanding Shares as of March 31, 2010: 22,600,000 Shares.

POWERSHARES DB BASE METALS FUND

(A SERIES OF POWERSHARES DB MULTI-SECTOR COMMODITY TRUST)

QUARTER ENDED MARCH 31, 2010

TABLE OF CONTENTS

| | | | | | |

| | | |

| | Exhibit 31.1 | | Certification required under Exchange Act Rules 13a–14 and 15d–14 | | E-2 |

| | Exhibit 31.2 | | Certification required under Exchange Act Rules 13a–14 and 15d–14 | | E-3 |

| | Exhibit 32.1 | | Certification of Chief Executive Officer pursuant to 18 U.S.C. Section 1350 as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 | | E-4 |

| | Exhibit 32.2 | | Certification of Principal Financial Officer pursuant to 18 U.S.C. Section 1350 as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 | | E-5 |

i

PART I. FINANCIAL INFORMATION

| ITEM 1. | FINANCIAL STATEMENTS. |

PowerShares DB Base Metals Fund and Subsidiary

Consolidated Statements of Financial Condition

March 31, 2010 (unaudited) and December 31, 2009

| | | | | | | | |

| | | March 31, 2010 | | | December 31, 2009 | |

Assets | | | | | | | | |

Equity in broker trading accounts: | | | | | | | | |

United States Treasury Obligations, at fair value (cost $464,930,033 and $531,954,120, respectively) | | $ | 464,918,085 | | | $ | 531,965,141 | |

Cash held by broker (restricted $40,483,427 and $30,664,456, respectively) | | | 40,483,427 | | | | 30,664,456 | |

Net unrealized appreciation on futures contracts | | | 70,563,444 | | | | 149,256,969 | |

| | | | | | | | |

Deposits with broker | | | 575,964,956 | | | | 711,886,566 | |

| | | | | | | | |

Total assets | | $ | 575,964,956 | | | $ | 711,886,566 | |

| | | | | | | | |

| | |

Liabilities | | | | | | | | |

Payable to broker | | $ | 11,309,206 | | | $ | 71,824,777 | |

Payable for securities purchased | | | 56,979,828 | | | | — | |

Management fee payable | | | 307,045 | | | | 371,745 | |

Brokerage fee payable | | | 1,938 | | | | 6,983 | |

| | | | | | | | |

Total liabilities | | | 68,598,017 | | | | 72,203,505 | |

| | | | | | | | |

| | |

Commitments and Contingencies (Note 9) | | | | | | | | |

| | |

Equity | | | | | | | | |

Shareholders’ equity | | | | | | | | |

General shares: | | | | | | | | |

Paid in capital - 40 shares issued and outstanding as of March 31, 2010 and December 31, 2009, respectively | | | 1,000 | | | | 1,000 | |

Accumulated defecit | | | (102 | ) | | | (99 | ) |

| | | | | | | | |

Total General shares | | | 898 | | | | 901 | |

| | | | | | | | |

| | |

Shares: | | | | | | | | |

Paid in capital - 22,600,000 and 28,400,000 redeemable Shares issued and outstanding as of March 31, 2010 and December 31, 2009, respectively | | | 398,149,516 | | | | 507,550,326 | |

Accumulated earnings | | | 109,215,627 | | | | 132,130,933 | |

| | | | | | | | |

Total Shares | | | 507,365,143 | | | | 639,681,259 | |

| | | | | | | | |

| | |

Total shareholders’equity | | | 507,366,041 | | | | 639,682,160 | |

| | | | | | | | |

| | |

Non-controlling interest in consolidated subsidiary - related party | | | 898 | | | | 901 | |

| | | | | | | | |

Total equity | | | 507,366,939 | | | | 639,683,061 | |

| | | | | | | | |

| | |

Total liabilities and equity | | $ | 575,964,956 | | | $ | 711,886,566 | |

| | | | | | | | |

| | |

Net asset value per share | | | | | | | | |

General shares | | $ | 22.45 | | | $ | 22.53 | |

Shares | | $ | 22.45 | | | $ | 22.52 | |

See accompanying notes to unaudited consolidated financial statements.

1

PowerShares DB Base Metals Fund and Subsidiary

Unaudited Consolidated Schedule of Investments

March 31, 2010

| | | | | | | | | |

Description | | Percentage of

Net Assets | | | Fair Value | | Face Value |

United States Treasury Obligations | | | | | | | | | |

U.S. Treasury Bills, 0.08% due April 1, 2010 | | 11.24 | % | | $ | 57,000,000 | | $ | 57,000,000 |

U.S. Treasury Bills, 0.11% due April 8, 2010 | | 7.29 | | | | 36,999,297 | | | 37,000,000 |

U.S. Treasury Bills, 0.135% due April 15, 2010 | | 4.73 | | | | 23,998,536 | | | 24,000,000 |

U.S. Treasury Bills, 0.105% due April 22, 2010 | | 8.47 | | | | 42,996,216 | | | 43,000,000 |

U.S. Treasury Bills, 0.15% due April 29, 2010 | | 6.80 | | | | 34,495,963 | | | 34,500,000 |

U.S. Treasury Bills, 0.145% due May 6, 2010 | | 13.20 | | | | 66,990,888 | | | 67,000,000 |

U.S. Treasury Bills, 0.145% due May 13, 2010 | | 4.24 | | | | 21,496,367 | | | 21,500,000 |

U.S. Treasury Bills, 0.13% due May 20, 2010 | | 1.18 | | | | 5,998,818 | | | 6,000,000 |

U.S. Treasury Bills, 0.16% due May 27, 2010 | | 0.59 | | | | 2,999,268 | | | 3,000,000 |

U.S. Treasury Bills, 0.125% due June 3, 2010 | | 0.30 | | | | 1,499,614 | | | 1,500,000 |

U.S. Treasury Bills, 0.15% due June 10, 2010 | | 5.12 | | | | 25,992,824 | | | 26,000,000 |

U.S. Treasury Bills, 0.165% due June 17, 2010 | | 7.88 | | | | 39,987,600 | | | 40,000,000 |

U.S. Treasury Bills, 0.155% due June 24, 2010 | | 9.36 | | | | 47,485,038 | | | 47,500,000 |

U.S. Treasury Bills, 0.145% due July 1, 2010 | | 11.23 | | | | 56,977,656 | | | 57,000,000 |

| | | | | | | | | |

Total United States Treasury Obligations (cost $464,930,033) | | 91.63 | % | | $ | 464,918,085 | | | |

| | | | | | | | | |

A portion of the above United States Treasury Obligations are held as initial margin against open futures contracts, as described in Note 4(e).

| | | | | | |

| | | Percentage of

Net Assets | | | Fair

Value |

Description | | |

Unrealized Appreciation on Futures Contracts | | | | | | |

Aluminum (2,938 contracts, settlement date November 15, 2010) | | 3.87 | % | | $ | 19,651,600 |

Copper (909 contracts, settlement date March 14, 2011) | | 5.69 | | | | 28,839,625 |

Zinc (2,749 contracts, settlement date May 17, 2010) | | 4.35 | | | | 22,072,219 |

| | | | | | |

Net Unrealized Appreciation on Futures Contracts | | 13.91 | % | | $ | 70,563,444 |

| | | | | | |

Net unrealized appreciation is comprised of unrealized gains of $72,721,700 and unrealized losses of $2,158,256.

See accompanying notes to unaudited consolidated financial statements.

2

PowerShares DB Base Metals Fund and Subsidiary

Consolidated Schedule of Investments

December 31, 2009

| | | | | | | | | |

| | | Percentage of

Net Assets | | | Fair

Value | | Face

Value |

Description | | | |

United States Treasury Obligations | | | | | | | | | |

U.S. Treasury Bills, 0.07% due January 7, 2010 | | 1.56 | % | | $ | 9,999,990 | | $ | 10,000,000 |

U.S. Treasury Bills, 0.07% due January 14, 2010 | | 3.13 | | | | 19,999,880 | | | 20,000,000 |

U.S. Treasury Bills, 0.005% due January 21, 2010 | | 6.72 | | | | 42,999,441 | | | 43,000,000 |

U.S. Treasury Bills, 0.01% due January 28, 2010 | | 2.89 | | | | 18,499,611 | | | 18,500,000 |

U.S. Treasury Bills, 0.025% due February 4, 2010 | | 9.22 | | | | 58,998,230 | | | 59,000,000 |

U.S. Treasury Bills, 0.065% due February 11, 2010 | | 6.64 | | | | 42,498,428 | | | 42,500,000 |

U.S. Treasury Bills, 0.065% due February 18, 2010 | | 0.94 | | | | 5,999,814 | | | 6,000,000 |

U.S. Treasury Bills, 0.04% due February 25, 2010 | | 12.04 | | | | 76,995,303 | | | 77,000,000 |

U.S. Treasury Bills, 0.06% due March 4, 2010 | | 14.77 | | | | 94,493,007 | | | 94,500,000 |

U.S. Treasury Bills, 0.05% due March 11, 2010 | | 3.28 | | | | 20,998,278 | | | 21,000,000 |

U.S. Treasury Bills, 0.04% due March 18, 2010 | | 5.63 | | | | 35,996,364 | | | 36,000,000 |

U.S. Treasury Bills, 0.07% due March 25, 2010 | | 7.43 | | | | 47,495,060 | | | 47,500,000 |

U.S. Treasury Bills, 0.11% due April 1, 2010 | | 8.91 | | | | 56,991,735 | | | 57,000,000 |

| | | | | | | | | |

Total United States Treasury Obligations (cost $531,954,120) | | 83.16 | % | | $ | 531,965,141 | | | |

| | | | | | | | | |

A portion of the above United States Treasury Obligations are held as initial margin against open futures contracts, as described in Note 4(e).

| | | | | | |

| | | Percentage of

Net Assets | | | Fair

Value |

Description | | |

Unrealized Appreciation on Futures Contracts | | | | | | |

Aluminum (3,693 contracts, settlement date November 15, 2010) | | 4.11 | % | | $ | 26,288,656 |

Copper (1,150 contracts, settlement date March 15, 2010) | | 9.15 | | | | 58,540,481 |

Zinc (3,455 contracts, settlement date May 17, 2010) | | 10.07 | | | | 64,427,832 |

| | | | | | |

Net Unrealized Appreciation on Futures Contracts | | 23.33 | % | | $ | 149,256,969 |

| | | | | | |

Net unrealized appreciation is comprised of unrealized gains of $149,416,350 and unrealized losses of $159,381.

See accompanying notes to unaudited consolidated financial statements.

3

PowerShares DB Base Metals Fund and Subsidiary

Unaudited Consolidated Statements of Income and Expenses

For the Three Months Ended March 31, 2010 and 2009

| | | | | | | | |

| | | Three Months Ended | |

| | | March 31, 2010 | | | March 31, 2009 | |

Income | | | | | | | | |

Interest Income, net | | $ | 72,350 | | | $ | 12,595 | |

| | | | | | | | |

| | |

Expenses | | | | | | | | |

Management Fee | | | 1,002,652 | | | | 101,497 | |

Brokerage Commissions and Fees | | | 11,106 | | | | 4,360 | |

| | | | | | | | |

Total Expenses | | | 1,013,758 | | | | 105,857 | |

| | | | | | | | |

Net investment loss | | | (941,408 | ) | | | (93,262 | ) |

| | | | | | | | |

| | |

Net Realized and Net Change in Unrealized Gain (Loss) on United States Treasury Obligations and Futures | | | | | | | | |

Net Realized Gain (Loss) on | | | | | | | | |

United States Treasury Obligations | | | 1,400 | | | | (600 | ) |

Futures | | | 56,741,190 | | | | (17,229,188 | ) |

| | | | | | | | |

Net realized gain (loss) | | | 56,742,590 | | | | (17,229,788 | ) |

| | | | | | | | |

Net Change in Unrealized Gain (Loss) on | | | | | | | | |

United States Treasury Obligations | | | (22,969 | ) | | | 6,063 | |

Futures | | | (78,693,525 | ) | | | 23,844,288 | |

| | | | | | | | |

Net change in unrealized gain (loss) | | | (78,716,494 | ) | | | 23,850,351 | |

| | | | | | | | |

Net realized and net change in unrealized gain (loss) on United States Treasury Obligations and Futures | | | (21,973,904 | ) | | | 6,620,563 | |

| | | | | | | | |

| | |

Net Income (Loss) | | $ | (22,915,312 | ) | | $ | 6,527,301 | |

| | | | | | | | |

| | |

Less: net (income) loss attributed to the non-controlling interest in consolidated subsidiary - related party | | | 3 | | | | (41 | ) |

| | | | | | | | |

| | |

Net Income (Loss) Attributable to PowerShares DB Base Metals Fund and Subsidiary | | $ | (22,915,309 | ) | | $ | 6,527,260 | |

| | | | | | | | |

See accompanying notes to unaudited consolidated financial statements.

4

PowerShares DB Base Metals Fund and Subsidiary

Unaudited Consolidated Statement of Changes in Shareholders’ Equity

For the Three Months Ended March 31, 2010

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | General Shares | | | Shares | | | | | | | | | | |

| | | Shares | | Paid in

Capital | | Accumulated

Earnings

(Deficit) | | | Total

Equity | | | Shares | | | Paid in

Capital | | | Accumulated

Earnings | | | Total

Equity | | | Total

Shareholders’

Equity | | | Non-controlling

Interest | | | Total

Equity | |

Balance at January 1, 2010 | | 40 | | $ | 1,000 | | $ | (99 | ) | | $ | 901 | | | 28,400,000 | | | $ | 507,550,326 | | | $ | 132,130,933 | | | $ | 639,681,259 | | | $ | 639,682,160 | | | $ | 901 | | | $ | 639,683,061 | |

Sale of Shares | | | | | | | | | | | | | | | 4,200,000 | | | | 89,693,932 | | | | | | | | 89,693,932 | | | | 89,693,932 | | | | | | | | 89,693,932 | |

Redemption of Shares | | | | | | | | | | | | | | | (10,000,000 | ) | | | (199,094,742 | ) | | | | | | | (199,094,742 | ) | | | (199,094,742 | ) | | | | | | | (199,094,742 | ) |

Net Loss | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment loss | | | | | | | | (2 | ) | | | (2 | ) | | | | | | | | | | (941,404 | ) | | | (941,404 | ) | | | (941,406 | ) | | | (2 | ) | | | (941,408 | ) |

Net realized gain on United States Treasury Obligations and Futures | | | | | | | | 84 | | | | 84 | | | | | | | | | | | 56,742,422 | | | | 56,742,422 | | | | 56,742,506 | | | | 84 | | | | 56,742,590 | |

Net change in unrealized loss on United States Treasury Obligations and Futures | | | | | | | | (85 | ) | | | (85 | ) | | | | | | | | | | (78,716,324 | ) | | | (78,716,324 | ) | | | (78,716,409 | ) | | | (85 | ) | | | (78,716,494 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net Loss | | | | | | | | (3 | ) | | | (3 | ) | | | | | | | | | | (22,915,306 | ) | | | (22,915,306 | ) | | | (22,915,309 | ) | | | (3 | ) | | | (22,915,312 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Balance at March 31, 2010 | | 40 | | $ | 1,000 | | $ | (102 | ) | | $ | 898 | | | 22,600,000 | | | $ | 398,149,516 | | | $ | 109,215,627 | | | $ | 507,365,143 | | | $ | 507,366,041 | | | $ | 898 | | | $ | 507,366,939 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

See accompanying notes to unaudited consolidated financial statements.

5

PowerShares DB Base Metals Fund and Subsidiary

Unaudited Consolidated Statement of Changes in Shareholders’ Equity

For the Three Months Ended March 31, 2009

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | General Shares | | | Shares | | | | | | | | | | |

| | | Shares | | Paid in

Capital | | Accumulated

Earnings

(Deficit) | | | Total

Equity | | | Shares | | | Paid in

Capital | | | Accumulated

Earnings

(Deficit) | | | Total

Equity | | | Total

Shareholders’

Equity | | | Non-controlling

Interest | | | Total

Equity | |

Balance at January 1, 2009 | | 40 | | $ | 1,000 | | $ | (523 | ) | | $ | 477 | | | 2,800,000 | | | $ | 95,254,196 | | | $ | (61,833,728 | ) | | $ | 33,420,468 | | | $ | 33,420,945 | | | $ | 477 | | | $ | 33,421,422 | |

Sale of Shares | | | | | | | | | | | | | | | 6,600,000 | | | | 81,293,674 | | | | | | | | 81,293,674 | | | | 81,293,674 | | | | | | | | 81,293,674 | |

Redemption of Shares | | | | | | | | | | | | | | | (400,000 | ) | | | (4,639,152 | ) | | | | | | | (4,639,152 | ) | | | (4,639,152 | ) | | | | | | | (4,639,152 | ) |

Net Income | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment loss | | | | | | | | (1 | ) | | | (1 | ) | | | | | | | | | | (93,260 | ) | | | (93,260 | ) | | | (93,261 | ) | | | (1 | ) | | | (93,262 | ) |

Net realized loss on United States Treasury Obligations and Futures | | | | | | | | (157 | ) | | | (157 | ) | | | | | | | | | | (17,229,474 | ) | | | (17,229,474 | ) | | | (17,229,631 | ) | | | (157 | ) | | | (17,229,788 | ) |

Net change in unrealized gain on United States Treasury Obligations and Futures | | | | | | | | 199 | | | | 199 | | | | | | | | | | | 23,849,953 | | | | 23,849,953 | | | | 23,850,152 | | | | 199 | | | | 23,850,351 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net Income | | | | | | | | 41 | | | | 41 | | | | | | | | | | | 6,527,219 | | | | 6,527,219 | | | | 6,527,260 | | | | 41 | | | | 6,527,301 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Balance at March 31, 2009 | | 40 | | $ | 1,000 | | $ | (482 | ) | | $ | 518 | | | 9,000,000 | | | $ | 171,908,718 | | | $ | (55,306,509 | ) | | $ | 116,602,209 | | | $ | 116,602,727 | | | $ | 518 | | | $ | 116,603,245 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

See accompanying notes to unaudited consolidated financial statements.

6

PowerShares DB Base Metals Fund and Subsidiary

Unaudited Consolidated Statements of Cash Flows

For the Three Months Ended March 31, 2010 and 2009

| | | | | | | | |

| | | Three Months Ended | |

| | | March 31, 2010 | | | March 31, 2009 | |

Cash flows from operating activities: | | | | | | | | |

Net Income (Loss) | | $ | (22,915,312 | ) | | $ | 6,527,301 | |

Adjustments to reconcile net income (loss) to net cash provided by (used for) operating activities: | | | | | | | | |

Cost of securities purchased | | | (407,897,870 | ) | | | (102,955,608 | ) |

Proceeds from securities sold and matured | | | 474,996,572 | | | | 33,999,138 | |

Net accretion of discount on United States Treasury Obligations | | | (73,215 | ) | | | (13,527 | ) |

Net realized (gain) loss on United States Treasury Obligations | | | (1,400 | ) | | | 600 | |

Net change in unrealized (gain) loss on United States Treasury Obligations and futures | | | 78,716,494 | | | | (23,850,351 | ) |

Increase in restricted cash | | | (9,818,971 | ) | | | — | |

Change in operating receivables and liabilities: | | | | | | | | |

Payable for securities purchased | | | 56,979,828 | | | | — | |

Payable to broker | | | (60,515,571 | ) | | | — | |

Management fee payable | | | (64,700 | ) | | | 26,569 | |

Brokerage fee payable | | | (5,045 | ) | | | (458 | ) |

| | | | | | | | |

Net cash provided by (used for) operating activities | | | 109,400,810 | | | | (86,266,336 | ) |

| | | | | | | | |

Cash flows from financing activities: | | | | | | | | |

Proceeds from sale of Shares | | | 89,693,932 | | | | 81,293,674 | |

Redemption of Shares | | | (199,094,742 | ) | | | (4,639,152 | ) |

| | | | | | | | |

Net cash provided by (used for) financing activities | | | (109,400,810 | ) | | | 76,654,522 | |

| | | | | | | | |

Net change in cash held by broker | | | — | | | | (9,611,814 | ) |

Unrestricted cash held by broker at beginning of period | | | — | | | | 30,952,245 | |

| | | | | | | | |

Unrestricted cash held by broker at end of period | | $ | — | | | $ | 21,340,431 | |

| | | | | | | | |

See accompanying notes to unaudited consolidated financial statements.

7

PowerShares DB Base Metals Fund and Subsidiary

Notes to Unaudited Consolidated Financial Statements

March 31, 2010

(1) Organization

PowerShares DB Base Metals Fund (the “Fund”; “Fund” may also refer to the Fund and the Master Fund, collectively, as the context requires), a separate series of PowerShares DB Multi-Sector Commodity Trust (the “Trust”), a Delaware statutory trust organized in seven separate series, and its subsidiary, DB Base Metals Master Fund (the “Master Fund”), a separate series of DB Multi-Sector Commodity Master Trust (the “Master Trust”), a Delaware statutory trust organized in seven separate series were formed on August 3, 2006. DB Commodity Services LLC, a Delaware limited liability company (“DBCS” or the “Managing Owner”), funded both the Fund and the Master Fund with a capital contribution of $1,000 in exchange for 40 General Shares of each of the Fund and the Master Fund. The fiscal year end of the Fund is December 31st. The term of the Fund is perpetual (unless terminated earlier in certain circumstances) as provided in the Amended and Restated Declaration of Trust and Trust Agreement of the Trust and the Master Trust (each a “Trust Agreement,” and collectively, the “Trust Agreements”).

The Fund offers common units of beneficial interest (the “Shares”) only to certain eligible financial institutions (the “Authorized Participants”) in one or more blocks of 200,000 Shares, called a Basket. The proceeds from the offering of Shares are invested in the Master Fund. The Fund and the Master Fund commenced investment operations on January 3, 2007. The Fund commenced trading on the American Stock Exchange (now known as the NYSE Alternext US LLC (the “NYSE Alternext”)) on January 5, 2007 and, as of November 25, 2008, is listed on the NYSE Arca, Inc. (the “NYSE Arca”).

This report covers the three months ended March 31, 2010 and 2009 (hereinafter referred to as the “Three Months Ended March 31, 2010” and the “Three Months Ended March 31, 2009”, respectively).

(2) Fund Investment Overview

The Master Fund invests with a view to tracking the changes, whether positive or negative, in the level of the Deutsche Bank Liquid Commodity Index–Optimum Yield Industrial Metals Excess Return™ (“DBLCI-OY Industrial Metals ER™”, or the “Index”) plus the excess, if any, of the Master Fund’s income from its holdings of United States Treasury Obligations and other high credit quality short-term fixed income securities over the expenses of the Fund and the Master Fund.

The Master Fund also holds United States Treasury Obligations and other high credit quality short-term fixed income securities for deposit with the Master Fund’s commodity broker as margin.

The Index is intended to reflect the change in market value of the base metals sector. The commodities comprising the Index are aluminum, zinc and copper (the “Index Commodities”). The Commodity Futures Trading Commission (the “CFTC”) and commodity exchanges impose position limits on market participants trading in certain commodities included in the Index. The Index is comprised of futures contracts on the Index Commodities that expire in a specific month and trade on a specific exchange (the “Index Contracts”). As disclosed in the Fund’s Prospectus, if the Managing Owner determines in its commercially reasonable judgment that it has become impracticable or inefficient for any reason for the Master Fund to gain full or partial exposure to any Index Commodity by investing in a specific Index Contract, the Master Fund may invest in a futures contract referencing the particular Index Commodity other than the Index Contract or, in the alternative, invest in other futures contracts not based on the particular Index Commodity if, in the commercially reasonable judgment of the Managing Owner, such futures contracts tend to exhibit trading prices that correlate with such Index Commodity.

The Fund does not employ leverage. As of March 31, 2010 and December 31, 2009, the Fund had $575,964,956 (or 100%) and $711,886,566 (or 100%), respectively, of its holdings of cash, United States Treasury Obligations and unrealized appreciation/depreciation on futures contracts on deposit with its Commodity Broker. Of this, $37,850,827 (or 6.57%) and $48,620,958 (or 6.83%), respectively, of the Fund’s holdings of cash and United States Treasury Obligations are required to be deposited as margin in support of the Fund’s long futures positions. For additional information, please see the unaudited Consolidated Schedule of Investments as of March 31, 2010 and the audited Consolidated Schedule of Investments as of December 31, 2009 for a breakdown of the Fund’s portfolio holdings.

8

PowerShares DB Base Metals Fund and Subsidiary

Notes to Unaudited Consolidated Financial Statements—(Continued)

March 31, 2010

DBLCI™ and Deutsche Bank Liquid Commodity Index™ are trademarks of Deutsche Bank AG London (the “Index Sponsor”). The Index Sponsor is an affiliate of the Trust, the Fund, the Master Trust, the Master Fund and the Managing Owner.

(3) Service Providers and Related Party Agreements

The Trustee

Under the Trust Agreements, Wilmington Trust Company, the trustee of the Fund and the Master Fund (the “Trustee”), has delegated to the Managing Owner the exclusive management and control of all aspects of the business of the Trust, the Fund, the Master Trust and the Master Fund. The Trustee will have no duty or liability to supervise or monitor the performance of the Managing Owner, nor will the Trustee have any liability for the acts or omissions of the Managing Owner.

The Managing Owner

The Managing Owner serves the Fund and Master Fund as commodity pool operator, commodity trading advisor and managing owner, and is an indirect wholly-owned subsidiary of Deutsche Bank AG. During the Three Months Ended March 31, 2010 and 2009, the Fund and the Master Fund incurred Management Fees of $1,002,652 and $101,497, respectively. As of March 31, 2010 and December 31, 2009, Management Fees payable to the Managing Owner were $307,045 and $371,745, respectively.

The Commodity Broker

Deutsche Bank Securities Inc., a Delaware corporation, serves as the Master Fund’s clearing broker (the “Commodity Broker”). The Commodity Broker is an indirect wholly-owned subsidiary of Deutsche Bank AG and is an affiliate of the Managing Owner. In its capacity as clearing broker, the Commodity Broker executes and clears each of the Master Fund’s futures transactions and performs certain administrative and custodial services for the Master Fund. As custodian of the Master Fund’s assets, the Commodity Broker is responsible, among other things, for providing periodic accountings of all dealings and actions taken by the Master Trust on behalf of the Master Fund during the reporting period, together with an accounting of all securities, cash or other indebtedness or obligations held by it or its nominees for or on behalf of the Master Fund. During the Three Months Ended March 31, 2010 and 2009, the Fund and the Master Fund incurred brokerage fees of $11,106 and $4,360, respectively. As of March 31, 2010 and December 31, 2009, brokerage fees payable were $1,938 and $6,983, respectively.

The Administrator

The Bank of New York Mellon (the “Administrator”) has been appointed by the Managing Owner as the administrator, custodian and transfer agent of the Master Fund and the Fund, and has entered into separate administrative, custodian, transfer agency and service agreements (collectively referred to as the “Administration Agreement”).

Pursuant to the Administration Agreement, the Administrator performs or supervises the performance of services necessary for the operation and administration of the Fund and the Master Fund (other than making investment decisions), including receiving and processing orders from Authorized Participants to create and redeem Baskets, net asset value calculations, accounting and other fund administrative services. The Administrator retains certain financial books and records, including: Basket creation and redemption books and records, fund accounting records, ledgers with respect to assets, liabilities, capital, income and expenses, the registrar, transfer journals and related details, and trading and related documents received from futures commission merchants.

The Distributor

ALPS Distributors, Inc. (the “Distributor”) provides certain distribution services to the Fund. Pursuant to the Distribution Services Agreement between the Managing Owner in its capacity as managing owner of the Fund, the Fund and the Distributor, the Distributor assists the Managing Owner and the Administrator with certain functions and duties relating to distribution and marketing services to the Fund including reviewing and approving marketing materials.

9

PowerShares DB Base Metals Fund and Subsidiary

Notes to Unaudited Consolidated Financial Statements—(Continued)

March 31, 2010

Invesco Powershares Capital Management LLC

Under the License Agreement among Invesco Powershares Capital Management LLC (the “Licensor”) and the Managing Owner in its own capacity and in its capacity as managing owner of the Fund (the Fund and the Managing Owner, collectively, the “Licensees”), the Licensor granted to each Licensee a non-exclusive license to use the “PowerShares®” trademark (the “Trademark”) anywhere in the world, solely in connection with the marketing and promotion of the Fund and to use or refer to the Trademark in connection with the issuance and trading of the Fund as necessary.

Invesco Aim Distributors, Inc.

Through a marketing agreement between the Managing Owner and Invesco Aim Distributors, Inc. (“Invesco Aim Distributors”), an affiliate of Invesco PowerShares Capital Management LLC (“Invesco PowerShares”), the Managing Owner, on behalf of the Fund and the Master Fund, has appointed Invesco Aim Distributors as a marketing agent. Invesco Aim Distributors assists the Managing Owner and the Administrator with certain functions and duties such as providing various educational and marketing activities regarding the Fund, primarily in the secondary trading market, which activities include, but are not limited to, communicating the Fund’s name, characteristics, uses, benefits, and risks, consistent with the prospectus. Invesco Aim Distributors will not open or maintain customer accounts or handle orders for the Fund. Invesco Aim Distributors engages in public seminars, road shows, conferences, media interviews, and distributes sales literature and other communications (including electronic media) regarding the Fund.

(4) Summary of Significant Accounting Policies

(a) Basis of Presentation and Consolidation

The consolidated financial statements of the Fund have been prepared using U.S. generally accepted accounting principles, and they include the consolidated financial statement balances of the Fund and the Master Fund. Upon the initial offering of the Shares on January 3, 2007, the capital raised by the Fund was used to purchase 100% of the common units of beneficial interest of the Master Fund (the “Master Fund Limited Units”) (excluding common units of beneficial interest of the Master Fund held by the Managing Owner (the “Master Fund General Units”)). The Master Fund Limited Units owned by the Fund provide the Fund and its investors certain controlling rights and abilities over the Master Fund. Consequently, the financial statement balances of the Master Fund have been consolidated with the Fund’s financial statement balances, and all significant inter-company balances and transactions have been eliminated.

(b) Use of Estimates

The preparation of the consolidated financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, revenues and expenses and related disclosure of contingent assets and liabilities during the reporting period of the consolidated financial statements and accompanying notes. Actual results could differ from those estimates.

(c) Financial Instruments and Fair Value

United States Treasury Obligations and commodity futures contracts are recorded in the consolidated statements of financial condition on a trade date basis at fair value with changes in fair value recognized in earnings in each period. The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (the exit price).

Financial Accounting Standards Board (FASB) fair value measurement and disclosure guidance requires a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets and liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy are described below:

10

PowerShares DB Base Metals Fund and Subsidiary

Notes to Unaudited Consolidated Financial Statements—(Continued)

March 31, 2010

Basis of Fair Value Measurement

| | |

Level 1: | | Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities; |

| |

Level 2: | | Quoted prices in markets that are not active or financial instruments for which all significant inputs are observable, either directly or indirectly; |

| |

Level 3: | | Prices or valuations that require inputs that are both significant to the fair value measurement and unobservable. |

A financial instrument’s level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement.

In determining fair value of United States Treasury Obligations and commodity futures contracts, the Fund uses unadjusted quoted market prices in active markets. United States Treasury Obligations and commodity futures contracts are classified within Level 1 of the fair value hierarchy. The Fund does not adjust the quoted prices for United States Treasury Obligations and commodity futures contracts.

(d) Deposits with Broker

The Fund deposits cash and United States Treasury Obligations with its Commodity Broker subject to CFTC regulations and various exchange and broker requirements. The combination of the Fund’s deposits with its Commodity Broker of cash and United States Treasury Obligations and the unrealized profit or loss on open futures contracts (variation margin) represents the Fund’s overall equity in its broker trading account. To meet the Fund’s initial margin requirements, the Fund holds United States Treasury Obligations. The Fund uses its cash held by the Commodity Broker to satisfy variation margin requirements. The Fund earns interest on its cash deposited with the Commodity Broker.

(e) United States Treasury Obligations

The Fund records purchases and sales of United States Treasury Obligations on a trade date basis. These holdings are marked to market based on quoted market closing prices. The Fund holds United States Treasury Obligations for deposit with the Master Fund’s Commodity Broker to meet margin requirements and for trading purposes. Interest income is recognized on an accrual basis when earned. Premiums and discounts are amortized or accreted over the life of the United States Treasury Obligations. Included in the United States Treasury Obligations as of March 31, 2010 and December 31, 2009 was $37,850,827 and $48,620,958, respectively, which is restricted and held against initial margin of the open futures contracts. The Fund purchased $57,000,000 notional amount of United States Treasury Obligations which was unpaid as of March 31, 2010. As a result a payable for securities purchased is recorded for $56,979,828. There was no payable for securities purchased as of December 31, 2009.

(f) Cash Held by Broker

The Fund’s arrangement with the Commodity Broker requires the Fund to meet its variation margin requirement related to the price movements, both positive and negative, on futures contracts held by the Fund by keeping cash on deposit with the Commodity Broker. The Fund defines cash and cash equivalents to be highly liquid investments, with original maturities of three months or less when purchased. As of March 31, 2010, the Fund had $40,483,427 of cash held by the Commodity Broker all of which was restricted. As of December 31, 2009, the Fund had $30,664,456 of cash held by the Commodity Broker, all of which were restricted. Restrictions on cash held by broker pertain to the settlement of closed futures contracts traded on the London Metals Exchange in which cash is not accessible until the settled futures contracts expire. There were no cash equivalents held by the Fund as of March 31, 2010 and December 31, 2009.

(g) Payable to Broker

Balances in the Fund’s variation margin account that are in excess of minimums required by the CFTC regulations and various exchanges and the Commodity Broker requirements, are available to the Fund. As of March 31, 2010, the futures contracts held by the Fund were in an unrealized appreciation position of $70,563,444 of which the Fund utilized $11,309,206 to purchase United States Treasury Obligations. No net interest expense was incurred as unrealized appreciation on open positions of futures contracts exceeded the payable to broker by $59,254,238. As of December 31,

11

PowerShares DB Base Metals Fund and Subsidiary

Notes to Unaudited Consolidated Financial Statements—(Continued)

March 31, 2010

2009, the futures contracts held by the Fund were in an unrealized appreciation position of $149,256,969 of which the Fund utilized $71,824,777 to purchase United States Treasury Obligations. No net interest expense was incurred as unrealized appreciation on open positions of futures contracts exceeded the payable to broker by $77,432,192.

(h) Income Taxes

The Fund and the Master Fund are classified as partnerships for U.S. federal income tax purposes. Accordingly, neither the Fund nor the Master Fund will incur U.S. federal income taxes. No provision for federal, state, and local income taxes has been made in the accompanying consolidated financial statements, as investors are individually liable for income taxes, if any, on their allocable share of the Fund’s share of the Master Fund’s income, gain, loss, deductions and other items.

The major tax jurisdiction and the earliest tax year subject to examination for the Fund: United States 2007.

(i) Futures Contracts

All commodity futures contracts are held and used for trading purposes. The commodity futures are recorded on a trade date basis and open contracts are recorded in the consolidated statement of financial condition at fair value on the last business day of the period, which represents market value for those commodity futures for which market quotes are readily available. However, when market closing prices are not available, the Managing Owner may value an asset of the Master Fund pursuant to policies the Managing Owner has adopted, which are consistent with normal industry standards. Realized gains (losses) and changes in unrealized appreciation (depreciation) on open positions are determined on a specific identification basis and recognized in the consolidated statement of income and expenses in the period in which the contract is closed or the changes occur, respectively. As of March 31, 2010 and December 31, 2009, the futures contracts held by the Fund were in a net unrealized appreciation position of $70,563,444 and $149,256,969, respectively.

(j) Management Fee

The Master Fund pays the Managing Owner a management fee (the “Management Fee”), monthly in arrears, in an amount equal to 0.75% per annum of the daily net asset value of the Master Fund. No separate Management Fee is paid by the Fund. The Management Fee is paid in consideration of the Managing Owner’s commodity futures trading advisory services.

(k) Brokerage Commissions and Fees

The Master Fund incurs all brokerage commissions, including applicable exchange fees, NFA fees, give-up fees, pit brokerage fees and other transaction related fees and expenses charged in connection with trading activities by the Commodity Broker. These costs are recorded as brokerage commissions and fees in the consolidated statement of income and expenses as incurred. The Commodity Broker’s brokerage commissions and trading fees are determined on a contract-by-contract basis. On average, total charges paid to the Commodity Broker were less than $10.00 per round-turn trade for the Three Months Ended March 31, 2010 and 2009 .

(l) Routine Operational, Administrative and Other Ordinary Expenses

The Managing Owner assumes all routine operational, administrative and other ordinary expenses of the Fund and the Master Fund, including, but not limited to, computer services, the fees and expenses of the Trustee, legal and accounting fees and expenses, tax preparation expenses, filing fees and printing, mailing and duplication costs. Accordingly, all such expenses are not reflected in the consolidated statement of income and expenses of the Fund.

(m) Organizational and Offering Costs

All organizational and offering expenses of the Fund and its Master Fund are incurred and assumed by the Managing Owner. Neither the Fund nor its Master Fund are, or will be, responsible to the Managing Owner for the reimbursement of organizational and offering costs. Expenses incurred in connection with the continuous offering of Shares also will be paid by the Managing Owner.

12

PowerShares DB Base Metals Fund and Subsidiary

Notes to Unaudited Consolidated Financial Statements—(Continued)

March 31, 2010

(n) Non-Recurring and Unusual Fees and Expenses

The Master Fund pays all fees and expenses, if any, of the Fund and the Master Fund, which are non-recurring and unusual in nature. Such expenses include legal claims and liabilities, litigation costs or indemnification or other unanticipated expenses. Such fees and expenses, by their nature, are unpredictable in terms of timing and amount. For the Three Months Ended March 31, 2010 and 2009, the Fund and the Master Fund did not incur such expenses.

(5) Fair Value Measurements

The Fund’s assets and liabilities recorded at fair value have been categorized based upon the fair value hierarchy discussed in Note 4(c).

Assets and Liabilities Measured at Fair Value were as follows:

| | | | | | |

| | | March 31, 2010 | | December 31, 2009 |

United States Treasury Obligations (Level 1) | | $ | 464,918,085 | | $ | 531,965,141 |

Commodity Futures Contracts (Level 1) | | $ | 70,563,444 | | $ | 149,256,969 |

There were no Level 2 or Level 3 holdings as of March 31, 2010 and December 31, 2009.

(6) Financial Instrument Risk

In the normal course of its business, the Master Fund is party to financial instruments with off-balance sheet risk. The term “off-balance sheet risk” refers to an unrecorded potential liability that, even though it does not appear on the balance sheet, may result in a future obligation or loss. The financial instruments used by the Master Fund are commodity futures, whose values are based upon an underlying asset and generally represent future commitments that have a reasonable possibility of being settled in cash or through physical delivery. The financial instruments are traded on an exchange and are standardized contracts.

Market risk is the potential for changes in the value of the financial instruments traded by the Master Fund due to market changes, including fluctuations in commodity prices. In entering into these futures contracts, there exists a market risk that such futures contracts may be significantly influenced by adverse market conditions, resulting in such futures contracts being less valuable. If the markets should move against all of the futures contracts at the same time, the Master Fund could experience substantial losses.

Credit risk is the possibility that a loss may occur due to the failure of an exchange clearinghouse to perform according to the terms of a futures contract. Credit risk with respect to exchange-traded instruments is reduced to the extent that an exchange or clearing organization acts as a counterparty to the transactions. The Master Fund’s risk of loss in the event of counterparty default is typically limited to the amounts recognized in the consolidated statement of financial condition and not represented by the futures contract or notional amounts of the instruments.

The Fund and the Master Fund have not utilized, nor do they expect to utilize in the future, special purpose entities to facilitate off-balance sheet financing arrangements and have no loan guarantee arrangements or off-balance sheet arrangements of any kind, other than agreements entered into in the normal course of business noted above.

(7) Share Purchases and Redemptions

(a) Purchases

Shares may be purchased from the Fund only by Authorized Participants in one or more blocks of 200,000 Shares, called a Basket. The Fund issues Shares in Baskets only to Authorized Participants continuously as of noon, New York time, on the business day immediately following the date on which a valid order to create a Basket is accepted by the Fund, at the net asset value of 200,000 Shares as of the closing time of the NYSE Arca or the last to close of the exchanges on which the Master Fund’s assets are traded, whichever is later, on the date that a valid order to create a Basket is accepted by the Fund.

13

PowerShares DB Base Metals Fund and Subsidiary

Notes to Unaudited Consolidated Financial Statements—(Continued)

March 31, 2010

(b) Redemptions

On any business day, an Authorized Participant may place an order with the Managing Owner to redeem one or more Baskets. Redemption orders must be placed by 10:00 a.m., New York time. The day on which the Managing Owner receives a valid redemption order is the redemption order date. Redemption orders are irrevocable. The redemption procedures allow Authorized Participants to redeem Baskets. Individual shareholders may not redeem directly from the Fund.

By placing a redemption order, an Authorized Participant agrees to deliver the Baskets to be redeemed through The Depository Trust Company’s (the “DTC”) book-entry system to the Fund not later than noon, New York time, on the business day immediately following the redemption order date. By placing a redemption order, and prior to receipt of the redemption proceeds, an Authorized Participant’s DTC account is charged the non-refundable transaction fee due for the redemption order.

The redemption proceeds from the Fund consist of the cash redemption amount. The cash redemption amount is equal to the net asset value of the number of Basket(s) requested in the Authorized Participant’s redemption order as of the closing time of the NYSE Arca or the last to close of the exchanges on which the Master Fund’s assets are traded, whichever is later, on the redemption order date. The Fund will distribute the cash redemption amount at noon, New York time, on the business day immediately following the redemption order date through DTC to the account of the Authorized Participant as recorded on DTC’s book-entry system.

The redemption proceeds due from the Fund are delivered to the Authorized Participant at noon, New York time, on the business day immediately following the redemption order date if, by such time on such business day immediately following the redemption order date, the Fund’s DTC account has been credited with the Baskets to be redeemed. If the Fund’s DTC account has not been credited with all of the Baskets to be redeemed by such time, the redemption proceeds are delivered to the extent of whole Baskets received. Any remainder of the redemption proceeds are delivered on the next business day to the extent of remaining whole Baskets received if the Managing Owner receives the fee applicable to the extension of the redemption distribution date which the Managing Owner may, from time-to-time, determine and the remaining Baskets to be redeemed are credited to the Fund’s DTC account by noon, New York time, on such next business day. Any further outstanding amount of the redemption order will be canceled. The Managing Owner is also authorized to deliver the redemption proceeds notwithstanding that the Baskets to be redeemed are not credited to the Fund’s DTC account by noon, New York time, on the business day immediately following the redemption order date if the Authorized Participant has collateralized its obligation to deliver the Baskets through DTC’s book-entry system on such terms as the Managing Owner may from time-to-time agree upon.

(c) Share Transactions

Summary of Share Transactions for the Three Months Ended March 31, 2010 and 2009

| | | | | | | | | | | | | | |

| | | Shares

Three Months Ended | | | Paid in Capital

Three Months Ended | |

| | | March 31, 2010 | | | March 31, 2009 | | | March 31, 2010 | | | March 31, 2009 | |

Shares Sold | | 4,200,000 | | | 6,600,000 | | | $ | 89,693,932 | | | $ | 81,293,674 | |

Shares Redeemed | | (10,000,000 | ) | | (400,000 | ) | | | (199,094,742 | ) | | | (4,639,152 | ) |

| | | | | | | | | | | | | | |

Net Increase/ (Decrease) | | (5,800,000 | ) | | 6,200,000 | | | $ | (109,400,810 | ) | | $ | 76,654,522 | |

| | | | | | | | | | | | | | |

(8) Profit and Loss Allocations and Distributions

Pursuant to the Amended and Restated Declaration of Trust and Trust Agreement of the Master Trust, income and expenses are allocatedpro rata to the Managing Owner as holder of the General Shares and to the Shareholders monthly based on their respective percentage interests as of the close of the last trading day of the preceding month. Any losses allocated to the Managing Owner (as the owner of the General Shares) which are in excess of the Managing Owner’s capital balance are allocated to the Shareholders in accordance with their respective interest in the Master Fund as a percentage of total shareholders’ equity. Distributions (other than redemption of units) may be made at the sole discretion of the Managing Owner on apro rata basis in accordance with the respective capital balances of the shareholders.

14

PowerShares DB Base Metals Fund and Subsidiary

Notes to Unaudited Consolidated Financial Statements—(Continued)

March 31, 2010

(9) Commitments and Contingencies

The Managing Owner, either in its own capacity or in its capacity as the Managing Owner and on behalf of the Fund and the Master Fund, has entered into various service agreements that contain a variety of representations, or provide indemnification provisions related to certain risks service providers undertake in performing services which are in the best interests of the Funds. As of March 31, 2010 no claims had been received by the Fund or the Master Fund and it was therefore not possible to estimate the Fund’s and the Master Fund’s potential future exposure under such indemnification provisions.

(10) Net Asset Value and Financial Highlights

The Fund is presenting the following net asset value and financial highlights related to investment performance for a Share outstanding for the Three Months Ended March 31, 2010 and 2009. The net investment income and total expense ratios are calculated using average net asset value. The net asset value presentation is calculated using daily Shares outstanding. The net investment income and total expense ratios have been annualized. The total return is based on the change in net asset value of the Shares during the period. An individual investor’s return and ratios may vary based on the timing of capital transactions.

The Fund invests substantially all of its assets in the Master Fund in a master-feeder structure. The Fund holds no investment assets other than Master Fund Limited Units. The Fund is the majority Master Fund Limited Unit owner and the Managing Owner holds a non-controlling interest in the Master Fund. Each Share issued by the Fund correlates with the Master Fund Limited Unit issued by the Master Fund and held by the Fund.

Net asset value per Master Fund Limited Unit and Master Fund General Unit (collectively, “Master Fund Units”) is the net asset value of the Master Fund divided by the number of outstanding Master Fund Units. Because there is a one-to-one correlation between Shares and the Master Fund Limited Units, the net asset value per Share and the net asset value per Master Fund Limited Unit are equal.

| | | | | | | | |

| | | Three Months Ended | |

| | | March 31, 2010 | | | March 31, 2009 | |

Net Asset Value | | | | | | | | |

Net asset value per Share, beginning of period | | $ | 22.52 | | | $ | 11.94 | |

Net realized and change in unrealized gain (loss) on United States Treasury Obligations and Futures | | | (0.03 | ) | | | 1.04 | |

Net investment income (loss) | | | (0.04 | ) | | | (0.02 | ) |

| | | | | | | | |

Net income (loss) | | | (0.07 | ) | | | 1.02 | |

Net asset value per Share, end of period | | $ | 22.45 | | | $ | 12.96 | |

| | | | | | | | |

| | |

Market value per Share, beginning of period | | $ | 22.50 | | | $ | 11.91 | |

| | | | | | | | |

Market value per Share, end of period | | $ | 22.51 | | | $ | 13.19 | |

| | | | | | | | |

| | |

Ratio to average Net Assets* | | | | | | | | |

Net investment income (loss) | | | (0.71 | )% | | | (0.67 | )% |

Total expenses | | | 0.76 | % | | | 0.76 | % |

| | |

Total Return, at net asset value ** | | | (0.31 | )% | | | 8.54 | % |

| | | | | | | | |

Total Return, at market value ** | | | 0.04 | % | | | 10.75 | % |

| | | | | | | | |

| * | Percentages are annualized. |

| ** | Percentages are not annualized. |

15

PowerShares DB Base Metals Fund and Subsidiary

Notes to Unaudited Consolidated Financial Statements—(Continued)

March 31, 2010

(11) Subsequent Events

The Fund evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date the financial statements were available to be issued. This evaluation did not result in any subsequent events that necessitated disclosures and/or adjustments.

16

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

This information should be read in conjunction with the consolidated financial statements and notes included in Item 1 of Part I of this Quarterly Report (the “Report”). The discussion and analysis which follows may contain trend analysis and other forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934 which reflect our current views with respect to future events and financial results. Words such as “anticipate,” “expect,” “intend,” “plan,” “believe,” “seek,” “outlook” and “estimate”, as well as similar words and phrases, signify forward-looking statements. PowerShares DB Base Metals Fund’s forward-looking statements are not guarantees of future results and conditions and important factors, risks and uncertainties may cause our actual results to differ materially from those expressed in our forward-looking statements.

You should not place undue reliance on any forward-looking statements. Except as expressly required by the Federal securities laws, DB Commodity Services LLC (the “Managing Owner”), undertakes no obligation to publicly update or revise any forward-looking statements or the risks, uncertainties or other factors described in this Report, as a result of new information, future events or changed circumstances or for any other reason after the date of this Report.

Overview/Introduction

The Fund and the Master Fund seek to track changes, whether positive or negative, in the level of the Deutsche Bank Liquid Commodity Index–Optimum Yield Industrial Metals Excess Return™ (“DBLCI-OY Industrial Metals ER™”, or the “Index”), over time, plus the excess, if any, of the Master Fund’s interest income from its holdings of United States Treasury Obligations and other high credit quality short-term fixed income securities over the expenses of the Fund and the Master Fund. The Shares are designed for investors who want a cost-effective and convenient way to invest in a group of commodity futures on U.S. and non-U.S. markets.

The Fund pursues its investment objective by investing substantially all of its assets in the Master Fund. The Master Fund pursues its investment objective by investing in a portfolio of exchange-traded futures contracts that expire in a specific month and trade on a specific exchange (the “Index Contracts”), in the commodities comprising the Index (the “Index Commodities”). The Index Commodities are aluminum, zinc and copper. The Index is composed of notional amounts of each of the Index Commodities. The Master Fund’s portfolio also includes United States Treasury Obligations and other high credit quality short-term fixed income securities for deposit with the Master Fund’s Commodity Broker as margin.

The notional amount of each Index Commodity included in the Index is intended to reflect the changes in market value of each such Index Commodity within the Index. The closing level of the Index is calculated on each business day by the Index Sponsor based on the closing price of the futures contracts for each of the underlying Index Commodities and the notional amounts of such Index Commodities.

The Index is rebalanced annually in November to ensure that each of the Index Commodities is weighted in the same proportion that such Index Commodities were weighted on September 3, 1997 (the “Base Date”). The following table reflects the index base weights (the “Index Base Weights”) of each Index Commodity on the Base Date:

| | |

Index Commodity | | Index Base Weight (%) |

Aluminum | | 33.33 |

Zinc | | 33.33 |

Copper-Grade A | | 33.33 |

| | |

Closing Level on Base Date: | | 100.00 |

The composition of the Index may be adjusted in the event that the Index Sponsor is not able to calculate the closing prices of the Index Commodities.

17

The following table reflects the Fund weights of each Index Commodity as of March 31, 2010:

| | |

Index Commodity | | Fund Weight (%) |

Aluminum | | 33.84 |

Zinc | | 31.60 |

Copper-Grade A | | 34.56 |

| | |

Closing Level as of March 31, 2010: | | 100.00 |

The Index includes provisions for the replacement of futures contracts as they approach maturity. This replacement takes place over a period of time in order to lessen the impact on the market for the futures contracts being replaced. With respect to each Index Commodity, the Master Fund employs a rule-based approach when it “rolls” from one futures contract to another. Rather than select a new futures contract based on a predetermined schedule (e.g., monthly), each Index Commodity rolls to the futures contract which generates the best possible “implied roll yield.” The futures contract with a delivery month within the next thirteen months which generates the best possible implied roll yield will be included in each Index. As a result, each Index Commodity is able to potentially maximize the roll benefits in backwardated markets and minimize the losses from rolling in contangoed markets.

In general, as a futures contract approaches its expiration date, its price will move towards the spot price in a contangoed market. Assuming the spot price does not change, this would result in the futures contract price decreasing and a negative implied roll yield. The opposite is true in a backwardated market. Rolling in a contangoed market will tend to cause a drag on an Index Commodity’s contribution to the Fund’s return while rolling in a backwardated market will tend to cause a push on an Index Commodity’s contribution to the Fund’s return.

The Deutsche Bank Liquid Commodity Index–Optimum Yield Industrial Metals is calculated in USD on both an excess return (unfunded) and total return (funded) basis.

The futures contract price for each Index Commodity will be the exchange closing price for such Index Commodity on each weekday when banks in New York, New York, are open (the “Index Business Days”). If a weekday is not an Exchange Business Day (as defined in the following sentence) but is an Index Business Day, the exchange closing price from the previous Index Business Day will be used for each Index Commodity. “Exchange Business Day” means, in respect of an Index Commodity, a day that is a trading day for such Index Commodity on the relevant exchange (unless either an Index disruption event or force majeure event has occurred).

On the first New York business day (the “Verification Date”) of each month, each Index Commodity futures contract will be tested in order to determine whether to continue including it in the Index. If the Index Commodity futures contract requires delivery of the underlying commodity in the next month, known as the Delivery Month, a new Index Commodity futures contract will be selected for inclusion in the Index. For example, if the first New York business day is May 1, 2010, and the Delivery Month of the Index Commodity futures contract currently in such Index is June 2010, a new Index Commodity futures contract with a later Delivery Month will be selected.

For each underlying Index Commodity of the Index, the new Index Commodity futures contract selected will be the Index Commodity futures contract with the best possible “implied roll yield” based on the closing price for each eligible Index Commodity futures contract. Eligible Index Commodity futures contracts are any Index Commodity futures contracts having a Delivery Month (i) no sooner than the month after the Delivery Month of the Index Commodity futures contract currently in such Index, and (ii) no later than the 13th month after the Verification Date. For example, if the first New York business day is May 1, 2010 and the Delivery Month of an Index Commodity futures contract currently in the Index is June 2010, the Delivery Month of an eligible new Index Commodity futures contract must be between July 2010 and May 2011. The implied roll yield is then calculated and the futures contract on the Index Commodity with the best possible implied roll yield is then selected. If two futures contracts have the same implied roll yield, the futures contract with the minimum number of months prior to the Delivery Month is selected.

After the futures contract selection, the monthly roll for each Index Commodity subject to a roll in that particular month unwinds the old futures contract and enters a position in the new futures contract. This takes place between the 2nd and 6th Index Business Day of the month.

18

On each day during the roll period, new notional holdings are calculated. The calculations for the futures contracts on the old Index Commodities that are leaving the Index and the futures contracts on the new Index Commodities are then calculated.

On all days that are not monthly index roll days, the notional holdings of each Index Commodity future remains constant.

The Index is re-weighted on an annual basis on the 6th Index Business Day of each November.

The calculation of the Index is expressed as the weighted average return of the Index Commodities.

The Commodity Futures Trading Commission (the “CFTC”) and commodity exchanges impose position limits on market participants trading in certain commodities included in the Index. As disclosed in the Fund’s Prospectus, if the Managing Owner determines in its commercially reasonable judgment that it has become impracticable or inefficient for any reason for the Master Fund to gain full or partial exposure to any Index Commodity by investing in a specific Index Contract, the Master Fund may invest in a futures contract referencing the particular Index Commodity other than the Index Contract or, in the alternative, invest in other futures contracts not based on the particular Index Commodity if, in the commercially reasonable judgment of the Managing Owner, such futures contracts tend to exhibit trading prices that correlate with such Index Commodity. Please seehttp://dbfunds.db.com/dbb/weights.aspx with respect to the most recently available weighted composition of the Fund andhttp://dbfunds.db.com/dbb/index.aspx with respect to the composition of the Index on the Base Date.

The sponsor of the Index (the “Index Sponsor”) is Deutsche Bank AG London. DBLCI™ and Deutsche Bank Liquid Commodity Index™ are trademarks of Deutsche Bank AG. Trademark applications in the United States are pending with respect to both the Fund and the Index. Deutsche Bank AG London is an affiliate of the Trust, the Fund, the Master Trust, the Master Fund and the Managing Owner.

Under the Trust Agreements of the Trust and the Master Trust, Wilmington Trust Company, the Trustee of the Trust and the Master Trust, has delegated to the Managing Owner the exclusive management and control of all aspects of the business of the Trust, the Fund, the Master Trust and the Master Fund. The Trustee will have no duty or liability to supervise or monitor the performance of the Managing Owner, nor will the Trustee have any liability for the acts or omissions of the Managing Owner.

The Index Sponsor obtains information for inclusion in, or for use in the calculation of, the Index from sources the Index Sponsor considers reliable. None of the Index Sponsor, the Managing Owner, the Trust, the Fund, the Master Trust and the Master Fund or any of their respective affiliates accepts responsibility for or guarantees the accuracy and/or completeness of the Index or any data included in the Index.

The Shares are intended to provide investment results that generally correspond to the changes, positive or negative, in the levels of the Index over time. The value of the Shares is expected to fluctuate in relation to changes in the value of the Master Fund’s portfolio. The market price of the Shares may not be identical to the net asset value per Share, but these two valuations are expected to be very close.

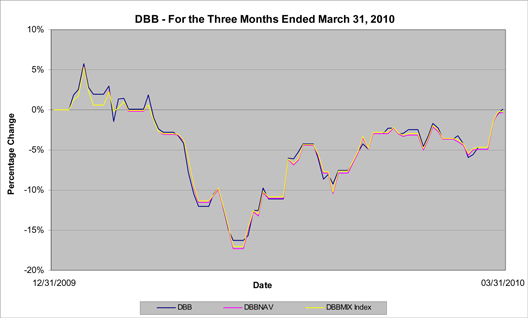

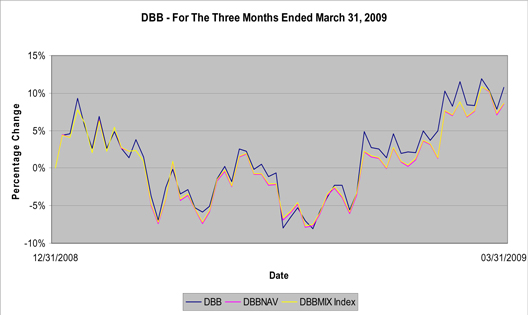

Performance Summary

This report covers the three months ended March 31, 2010 and 2009 (hereinafter referred to as the “Three Months Ended March 31, 2010” and the “Three Months Ended March 31, 2009”, respectively). The Fund commenced trading on the American Stock Exchange (now known as the NYSE Alternext US LLC (the “NYSE Alternext”)) on January 5, 2007, and, as of November 25, 2008, is listed on the NYSE Arca, Inc. (the “NYSE Arca”).

Performance of the Fund and the exchange traded Shares are detailed below in “Results of Operations”. Past performance of the Fund is not necessarily indicative of future performance.

The Index is intended to reflect the change in market value of the Index Commodities. In turn, the Index is intended to reflect the base metals sector. The Deutsche Bank Liquid Commodity Index-Optimum Yield Industrial Metals Total Return™ (the “DBLCI-OY Industrial Metals TR™”), consists of the Index plus 3-month United States Treasury Obligations returns. Past Index results are not necessarily indicative of future changes, positive or negative, in the Index closing levels.

19

The section “Summary of DBLCI-OY Industrial Metals TR™ and Underlying Index Commodity Returns for the Three Months Ended March 31, 2010 and 2009” below provides an overview of the changes in the closing levels of DBLCI-OY Industrial Metals TR™ by disclosing the change in market value of each underlying component Index Commodity through a “surrogate” (and analogous) index plus 3-month United States Treasury Obligations returns. Please note also that the Fund’s objective is to track the Index (not DBLCI-OY Industrial Metals TR™) and the Fund does not attempt to outperform or underperform the Index. The Index employs the optimum yield roll method with the objective of mitigating the negative effects of contango, the condition in which distant delivery prices for futures exceed spot prices, and maximizing the positive effects of backwardation, a condition opposite of contango.

Summary of DBLCI-OY Industrial Metals TR™ and Underlying Index Commodity

Returns for the Three Months Ended March 31, 2010 and 2009

| | | | | | |

Underlying Index | | Aggregate returns for indexes in the

DBLCI-OY Industrial Metals TR™ | |

| | Three Months

Ended

March 31, 2010 | | | Three Months

Ended

March 31, 2009 | |

DB Aluminum Indices | | 2.90 | % | | (11.33 | )% |

DB Zinc Indices | | (8.22 | )% | | 7.11 | % |

DB Copper—Grade A Indices | | 5.32 | % | | 30.23 | % |

AGGREGATE RETURN | | (0.13 | )% | | 8.65 | % |

If the Fund’s interest income from its holdings of fixed income securities were to exceed the Fund’s fees and expenses, the aggregate return on an investment in the Fund is expected to outperform the Index and underperform the DBLCI-OY Industrial Metals TR™. The only difference between the Index and the DBLCI-OY Industrial Metals TR™ is that the Index does not include interest income from a hypothetical basket of fixed income securities while the DBLCI-OY Industrial Metals TR™ does include such a component. The difference between the Index and the DBLCI-OY Industrial Metals TR™ is attributable entirely to the hypothetical interest income from this hypothetical basket of fixed income securities. If the Fund’s interest income from its holdings of fixed income securities exceeds the Fund’s fees and expenses, then the amount of such excess is expected to be distributed periodically. The market price of the Shares is expected to closely track the Index. The aggregate return on an investment in the Fund over any period is the sum of the capital appreciation or depreciation of the Shares over the period, plus the amount of any distributions during the period. Consequently, the Fund’s aggregate return is expected to outperform the Index by the amount of the excess, if any, of its interest income over its fees and expenses but, as a result of the Fund’s fees and expenses, the aggregate return on the Fund is expected to underperform the DBLCI-OY Industrial Metals TR™. If the Fund’s fees and expenses were to exceed the Fund’s interest income from its holdings of fixed income securities, the aggregate return on an investment in the Fund is expected to underperform the Index.

Net Asset Value

Net asset value means the total assets of the Master Fund, including, but not limited to, all futures, cash and investments less total liabilities of the Master Fund, each determined on the basis of U.S. generally accepted accounting principles, consistently applied under the accrual method of accounting. In particular, net asset value includes any unrealized appreciation or depreciation on open commodity futures contracts, and any other credit or debit accruing to the Master Fund but unpaid or not received by the Master Fund. All open commodity futures contracts will be calculated at their then current market value, which will be based upon the settlement price for that particular commodity futures contract traded on the applicable exchange on the date with respect to which net asset value is being determined; provided, that if a commodity futures contract could not be liquidated on such day, due to the operation of daily limits or other rules of the exchange upon which that position is traded or otherwise, the settlement price on the most recent day on which the position could have been liquidated will be the basis for determining the market value of such position for such day. The Managing Owner may in its discretion (and only under extraordinary circumstances, including, but not limited to, periods during which a settlement price of a futures contract is not available due to exchange limit orders or force majeure type events such as systems failure, natural or man-made disaster, act of God, armed conflict, act of terrorism, riot or labor disruption or any similar intervening circumstance) value any asset of the Master Fund pursuant to such other principles as the Managing Owner deems fair and

20

equitable so long as such principles are consistent with normal industry standards. Interest earned on the Master Fund’s brokerage account is accrued monthly. The amount of any distribution is a liability of the Master Fund from the day when the distribution is declared until it is paid.

The Fund invests substantially all of its assets in the Master Fund in a master-feeder structure. The Fund holds no investment assets other than Master Fund Limited Units. The Fund is the majority Master Fund Limited Unit owner and the Managing Owner holds a non-controlling interest in the Master Fund. Each Share issued by the Fund correlates with the Master Fund Limited Unit issued by the Master Fund and held by the Fund.

Net asset value per Master Fund Limited Unit and Master Fund General Unit (collectively, “Master Fund Units”) is the net asset value of the Master Fund divided by the number of outstanding Master Fund Units. Because there is a one-to-one correlation between Shares and Master Fund Limited Units, the net asset value per Share and the net asset value per Master Fund Limited Unit are equal.

Critical Accounting Policies

The Fund’s and Master Fund’s critical accounting policies are as follows:

Preparation of the financial statements and related disclosures in conformity with U.S. generally accepted accounting principles requires the application of appropriate accounting rules and guidance, as well as the use of estimates, and requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, revenue and expense and related disclosure of contingent assets and liabilities during the reporting period of the consolidated financial statements and accompanying notes. Both the Fund’s and the Master Fund’s application of these policies involve judgments and actual results may differ from the estimates used.

The Master Fund holds a significant portion of its assets in futures contracts and United States Treasury Obligations, both of which are recorded on a trade date basis and at fair value in the consolidated financial statements, with changes in fair value reported in the consolidated statement of income and expenses.

The use of fair value to measure financial instruments, with related unrealized gains or losses recognized in earnings in each period is fundamental to the Fund’s financial statements. The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (the exit price).

In determining fair value of United States Treasury Obligations and commodity futures contracts, the Fund uses unadjusted quoted market prices in active markets. FASB fair value measurement and disclosure guidance requires a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The objective of a fair value measurement is to determine the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (an exit price). The hierarchy gives the highest priority to unadjusted quoted prices for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). Assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurement. See Note 4(c) within the financial statements in Item 1 for further information.

When market closing prices are not available, the Managing Owner may value an asset of the Master Fund pursuant to policies the Managing Owner has adopted, which are consistent with normal industry standards.

Realized gains (losses) and changes in unrealized gain (loss) on open positions are determined on a specific identification basis and recognized in the consolidated statement of income and expenses in the period in which the contract is closed or the changes occur, respectively.

Interest income on United States Treasury Obligations is recognized on an accrual basis when earned. Premiums and discounts are amortized or accreted over the life of the United States Treasury Obligations.

21

Market Risk