Filed Pursuant to Rule 424(b)(3)

Registration Nos. 333-163453

333-163453-01

333-163453-02

333-163453-03

333-163453-04

333-163453-05

333-163453-06

333-163453-07

333-163453-08

333-163453-09

333-163453-10

333-163453-11

333-163453-12

333-163453-13

333-163453-14

333-163453-15

POWERSHARES DB MULTI-SECTOR COMMODITY TRUST

POWERSHARES DB ENERGY FUND

POWERSHARES DB OIL FUND

POWERSHARES DB PRECIOUS METALS FUND

POWERSHARES DB GOLD FUND

POWERSHARES DB SILVER FUND

POWERSHARES DB BASE METALS FUND

POWERSHARES DB AGRICULTURE FUND

DB MULTI-SECTOR COMMODITY MASTER TRUST

DB ENERGY MASTER FUND

DB OIL MASTER FUND

DB PRECIOUS METALS MASTER FUND

DB GOLD MASTER FUND

DB SILVER MASTER FUND

DB BASE METALS MASTER FUND

DB AGRICULTURE MASTER FUND

SUPPLEMENT DATED OCTOBER 1, 2010 TO

PROSPECTUS DATED JANUARY 4, 2010

This Supplement updates certain information contained in the Prospectus dated January 4, 2010, as supplemented from time-to-time (the “Prospectus”) of PowerShares DB Multi-Sector Commodity Trust (the “Trust”), PowerShares DB Energy Fund, PowerShares DB Oil Fund, PowerShares DB Precious Metals Fund, PowerShares DB Gold Fund, PowerShares DB Silver Fund, PowerShares DB Base Metals Fund, PowerShares DB Agriculture Fund (collectively, the “Funds”), DB Multi-Sector Commodity Master Trust, DB Energy Master Fund, DB Oil Master Fund, DB Precious Metals Master Fund, DB Gold Master Fund, DB Silver Master Fund, DB Base Metals Master Fund and DB Agriculture Master Fund. All capitalized terms used in this Supplement have the same meaning as in the Prospectus.

Prospective investors in the Funds should review carefully the contents of both this Supplement and the Prospectus.

* * * * * * * * * * * * * * * * * * *

All information in the Prospectus is restated pursuant to this Supplement, except as updated hereby.

Neither the Securities and Exchange Commission nor any state securities commission

has approved or disapproved of these securities or determined if this Supplement is

truthful or complete. Any representation to the contrary is a criminal offense.

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOL NOR HAS THE COMMISSION PASSED UPON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

DB COMMODITY SERVICES LLC

Managing Owner

| I. | Pages 38 through 117 of the Prospectus are hereby deleted and replaced, in their entirety, with the following: |

“PERFORMANCE OF POWERSHARES DB ENERGY FUND (TICKER: DBE), A SERIES OF POWERSHARES DB MULTI-SECTOR COMMODITY TRUST

Name of Pool: PowerShares DB Energy Fund

Type of Pool: Public, Exchange-Listed Commodity Pool

Inception of Trading: January 2007

Aggregate Gross Capital Subscriptions as of June 30, 2010:$587,832,576

Net Asset Value as of June 30, 2010:$334,686,784

Net Asset Value per Share as of June 30, 2010:$23.24

Worst Monthly Drawdown: (28.36)% October 2008

Worst Peak-to-Valley Drawdown: (66.18)% June 2008 – February 2009*

| Monthly Rate of Return | 2010(%) | 2009(%) | 2008(%) | 2007(%) | ||||

January | (8.46) | (6.19) | (1.17) | 0.08 | ||||

February | 5.54 | (5.93) | 10.62 | 5.80 | ||||

March | 2.88 | 5.71 | 1.35 | 5.33 | ||||

April | 5.48 | (1.34) | 10.21 | 0.86 | ||||

May | (14.15) | 22.99 | 14.95 | (0.92) | ||||

June | (0.73) | 3.14 | 10.15 | 3.41 | ||||

July | 2.26 | (12.21) | 2.26 | |||||

August | (3.50) | (6.72) | (4.07) | |||||

September | (0.96) | (11.32) | 7.78 | |||||

October | 7.99 | (28.36) | 12.90 | |||||

November | 1.68 | (14.60) | (2.56) | |||||

December | (0.39) | (13.74)** | 4.95*** | |||||

Compound Rate of Return | (10.65)% (6 months) | 24.81% | (40.74)% | 40.68% |

| * | The Worst Peak-to-Valley Drawdown from June 2008 – February 2009 includes the effect of the $0.44 per Share distribution made to Shareholders of record as of December 17, 2008. Please see Footnote **. |

| ** | The December 2008 return of (13.74)% includes the $0.44 per Share distribution made to Shareholders of record as of December 17, 2008. Prior to the December 30, 2008 distribution, the pool’s return for December 2008 was (11.92)%. |

| *** | The December 2007 return of 4.95% includes the $0.90 per Share distribution made to Shareholders of record as of December 19, 2007. Prior to the December 28, 2007 distribution, the pool’s return for December 2007 was 7.64%. |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

PERFORMANCE OF POWERSHARES DB OIL FUND (TICKER: DBO), A SERIES OF POWERSHARES

DB MULTI-SECTOR COMMODITY TRUST

Name of Pool:PowerShares DB Oil Fund

Type of Pool:Public, Exchange-Listed Commodity Pool

Inception of Trading:January 2007

Aggregate Gross Capital Subscriptions as of June 30, 2010:$803,275,734

Net Asset Value as of June 30, 2010:$497,024,530

Net Asset Value per Share as of June 30, 2010:$23.90

Worst Monthly Drawdown:(29.20)% October 2008

Worst Peak-to-Valley Drawdown:(65.43)% June 2008 – February 2009*

| Monthly Rate of Return | 2010(%) | 2009(%) | 2008(%) | 2007(%) | ||||

January | (8.65) | (5.87) | (3.00) | (2.08) | ||||

February | 7.48 | (4.30) | 10.99 | 6.13 | ||||

March | 4.76 | 7.88 | 0.30 | 4.77 | ||||

April | 4.46 | (1.12) | 12.33 | (2.20) | ||||

May | (16.47) | 26.94 | 12.65 | (2.48) | ||||

June | (3.20) | 1.94 | 11.73 | 4.58 | ||||

July | 3.09 | (11.24) | 2.65 | |||||

August | (3.12) | (5.82) | (4.20) | |||||

September | (1.07) | (12.79) | 9.59 | |||||

October | 8.27 | (29.20) | 15.62 | |||||

November | 2.94 | (15.73) | (2.39) | |||||

December | (0.95) | (11.79)** | 4.85*** | |||||

Compound Rate of Return | (13.12)% (6 months) | 35.65% | (41.42)% | 38.48% |

| * | The Worst Peak-to-Valley Drawdown from June 2008 – February 2009 includes the effect of the $0.12 per Share distribution made to Shareholders of record as of December 17, 2008. Please see Footnote **. |

| ** | The December 2008 return of (11.79)% includes the $0.12 per Share distribution made to Shareholders of record as of December 17, 2008. Prior to the December 30, 2008 distribution, the pool’s return for December 2008 was (11.27)%. |

| *** | The December 2007 return of 4.85% includes the $1.28 per Share distribution made to Shareholders of record as of December 19, 2007. Prior to the December 28, 2007 distribution, the pool’s return for December 2007 was 7.93%. |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

See accompanying Footnotes to Performance Information on page 41.

2

PERFORMANCE OF POWERSHARES DB PRECIOUS METALS FUND (TICKER: DBP), A SERIES OF POWERSHARES DB MULTI-SECTOR COMMODITY TRUST

Name of Pool:PowerShares DB Precious Metals Fund

Type of Pool:Public, Exchange-Listed Commodity Pool

Inception of Trading:January 2007

Aggregate Gross Capital Subscriptions as of June 30, 2010:$424,452,498

Net Asset Value as of June 30, 2010:$279,196,361

Net Asset Value per Share as of June 30, 2010:$42.30

Worst Monthly Drawdown:(18.43)% October 2008

Worst Peak-to-Valley Drawdown:(31.88)% February 2008 – October 2008

| Monthly Rate of Return | 2010(%) | 2009(%) | 2008(%) | 2007(%) | ||||

January | (1.83) | 6.02 | 10.18 | 4.04 | ||||

February | 2.92 | 1.97 | 7.34 | 2.77 | ||||

March | 0.68 | (1.84) | (7.24) | (1.87) | ||||

April | 5.93 | (3.99) | (5.36) | 2.10 | ||||

May | 2.01 | 12.91 | 2.30 | (2.43) | ||||

June | 2.27 | (7.08) | 3.99 | (3.14) | ||||

July | 2.61 | (0.88) | 2.96 | |||||

August | 1.17 | (12.05) | (0.77) | |||||

September | 7.00 | 2.59 | 16.86 | |||||

October | 1.73 | (18.43) | (5.36) | |||||

November | 13.44 | 11.56 | 3.95 | |||||

December | (7.62) | 6.94* | 4.04** | |||||

Compound Rate of Return | 12.41% (6 months) | 26.57% | (3.88)% | 23.72% |

| * | The December 2008 return of 6.94% includes the $0.27 per Share distribution made to Shareholders of record as of December 17, 2008. Prior to the December 30, 2008 distribution, the pool’s return for December 2008 was 7.91%. |

| ** | The December 2007 return of 4.04% includes the $0.60 per Share distribution made to Shareholders of record as of December 19, 2007. Prior to the December 28, 2007 distribution, the pool’s return for December 2007 was 5.58%. |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

PERFORMANCE OF POWERSHARES DB GOLD FUND (TICKER: DGL), A SERIES OF

POWERSHARES DB MULTI-SECTOR COMMODITY TRUST

Name of Pool:PowerShares DB Gold Fund

Type of Pool:Public, Exchange-Listed Commodity Pool

Inception of Trading:January 2007

Aggregate Gross Capital Subscriptions as of June 30, 2010:$343,444,552

Net Asset Value as of June 30, 2010:$239,404,174

Net Asset Value per Share as of June 30, 2010:$44.33

Worst Monthly Drawdown:(18.06)% October 2008

Worst Peak-to-Valley Drawdown:(26.80)% February 2008 – October 2008

| Monthly Rate of Return | 2010(%) | 2009(%) | 2008(%) | 2007(%) | ||||

January | (1.30) | 4.85 | 9.67 | 3.44 | ||||

February | 3.15 | 1.48 | 5.14 | 2.44 | ||||

March | (0.56) | (2.07) | (5.77) | (1.02) | ||||

April | 5.89 | (3.64) | (5.92) | 2.86 | ||||

May | 2.79 | 9.53 | 2.54 | (2.93) | ||||

June | 2.45 | (5.40) | 4.17 | (1.99) | ||||

July | 2.69 | (1.48) | 2.61 | |||||

August | (0.26) | (9.22) | 0.68 | |||||

September | 5.75 | 5.49 | 9.81 | |||||

October | 3.01 | (18.06) | 6.01 | |||||

November | 13.39 | 13.29 | (1.26) | |||||

December | (7.27) | 6.66* | 3.54** | |||||

Compound Rate of Return | 12.89% (6 months) | 22.03% | 2.00% | 26.20% |

| * | The December 2008 return of 6.66% includes the $0.26 per Share distribution made to Shareholders of record as of December 17, 2008. Prior to the December 30, 2008 distribution, the pool’s return for December 2008 was 7.52%. |

| ** | The December 2007 return of 3.54% includes the $0.81 per Share distribution made to Shareholders of record as of December 19, 2007. Prior to the December 28, 2007 distribution, the pool’s return for December 2007 was 5.84%. |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

See accompanying Footnotes to Performance Information on page 41.

3

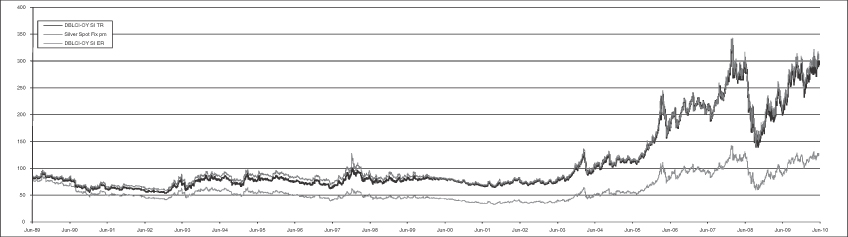

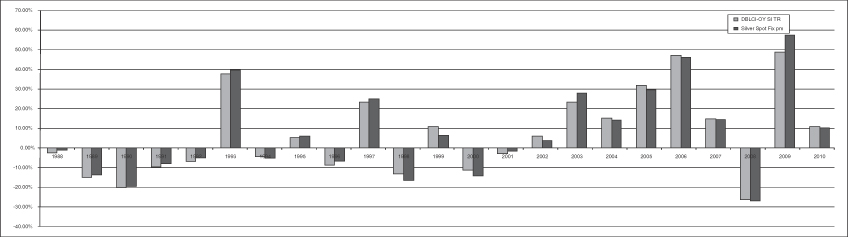

PERFORMANCE OF POWERSHARES DB SILVER FUND (TICKER: DBS), A SERIES OF

POWERSHARES DB MULTI-SECTOR COMMODITY TRUST

Name of Pool:PowerShares DB Silver Fund

Type of Pool:Public, Exchange-Listed Commodity Pool

Inception of Trading:January 2007

Aggregate Gross Capital Subscriptions as of June 30, 2010:$190,497,818

Net Asset Value as of June 30, 2010:$66,336,184

Net Asset Value per Share as of June 30, 2010:$33.17

Worst Monthly Drawdown:(23.42)% August 2008

Worst Peak-to-Valley Drawdown:(51.35)% February 2008 – October 2008

| Monthly Rate of Return | 2010(%) | 2009(%) | 2008(%) | 2007(%) | ||||

January | (4.06) | 11.40 | 12.83 | 6.48 | ||||

February | 1.91 | 4.16 | 16.53 | 4.13 | ||||

March | 6.15 | (0.89) | (12.95) | (4.91) | ||||

April | 6.20 | (5.23) | (4.05) | 0.49 | ||||

May | (1.11) | 26.80 | 1.67 | (0.26) | ||||

June | 1.38 | (13.00) | 3.41 | (7.80) | ||||

July | 2.46 | 1.68 | 4.60 | |||||

August | 6.73 | (23.42) | (6.71) | |||||

September | 11.63 | (10.23) | 13.76 | |||||

October | (2.45) | (20.75) | 3.92 | |||||

November | 13.71 | 4.72 | (2.92) | |||||

December | (9.03) | 8.74* | 2.02** | |||||

Compound Rate of Return | 10.49% (6 months) | 48.10% | (27.16)% | 11.32% |

| * | The December 2008 return of 8.74% includes the $0.22 per Share distribution made to Shareholders of record as of December 17, 2008. Prior to the December 30, 2008 distribution, the pool’s return for December 2008 was 9.92%. |

| ** | The December 2007 return of 2.02% includes the $0.87 per Share distribution made to Shareholders of record as of December 19, 2007. Prior to the December 28, 2007 distribution, the pool’s return for December 2007 was 5.24%. |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

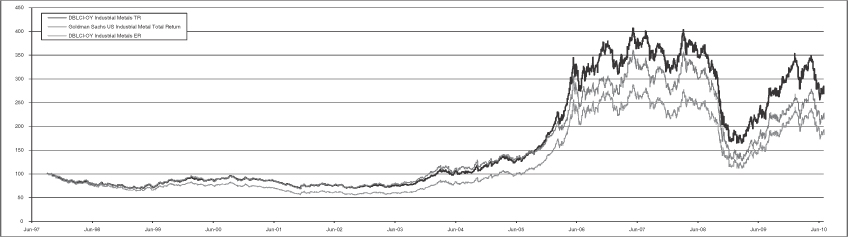

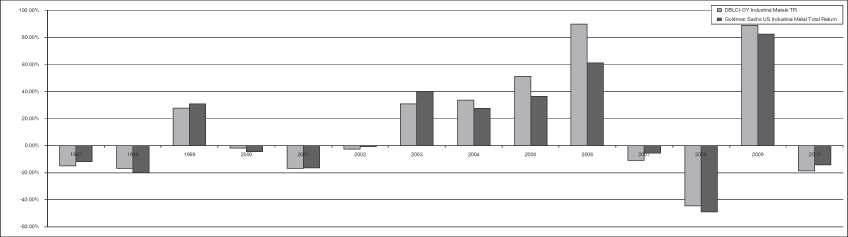

PERFORMANCE OF POWERSHARES DB BASE METALS FUND (TICKER: DBB), A SERIES OF POWERSHARES DB MULTI-SECTOR COMMODITY TRUST

Name of Pool:PowerShares DB Base Metals Fund

Type of Pool:Public, Exchange-Listed Commodity Pool

Inception of Trading:January 2007

Aggregate Gross Capital Subscriptions as of June 30, 2010:$776,478,594

Net Asset Value as of June 30, 2010:$319,884,150

Net Asset Value per Share as of June 30, 2010:$18.18

Worst Monthly Drawdown:(27.29)% October 2008

Worst Peak-to-Valley Drawdown:(60.29)% July 2007 – January 2009*

| Monthly Rate of Return | 2010(%) | 2009(%) | 2008(%) | 2007(%) | ||||

January | (11.50) | (7.37) | 8.82 | (5.84) | ||||

February | 4.12 | 3.71 | 12.16 | 3.70 | ||||

March | 8.17 | 12.99 | (5.59) | 1.88 | ||||

April | (4.12) | 6.48 | (0.87) | 10.74 | ||||

May | (10.43) | 6.30 | (4.54) | (2.40) | ||||

June | (5.71) | 3.07 | 3.92 | (1.19) | ||||

July | 13.82 | (4.21) | 4.86 | |||||

August | 7.55 | (6.74) | (7.61) | |||||

September | (0.43) | (11.14) | 2.37 | |||||

October | 5.97 | (27.29) | (2.43) | |||||

November | 6.81 | (6.46) | (5.95) | |||||

December | 7.98 | (11.29)** | (8.98)*** | |||||

Compound Rate of Return | (19.29)% (6 months) | 88.64% | (45.73)% | (12.00)% |

| * | The Worst Peak-to-Valley Drawdown from July 2007 – January 2009 includes the effect of the $0.96 per Share distribution made to Shareholders of record as of December 19, 2007, and the effect of the $0.28 per Share distribution made to Shareholders of record as of December 17, 2008. Please see Footnotes ** and ***. |

| ** | The December 2008 return of (11.29)% includes the $0.28 per Share distribution made to Shareholders of record as of December 17, 2008. Prior to the December 30, 2008 distribution, the pool’s return for December 2008 was (9.21)%. |

| *** | The December 2007 return of (8.98)% includes the $0.96 per Share distribution made to Shareholders of record as of December 19, 2007. Prior to the December 28, 2007 distribution, the pool’s return for December 2007 was (5.01)%. |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

See accompanying Footnotes to Performance Information on page 41.

4

PERFORMANCE OF POWERSHARES DB AGRICULTURE FUND(TICKER: DBA), A SERIES OF POWERSHARES DB MULTI-SECTOR COMMODITY TRUST

Name of Pool:PowerShares DB Agriculture Fund

Type of Pool:Public, Exchange-Listed Commodity Pool

Inception of Trading:January 2007

Aggregate Gross Capital Subscriptions as of June 30, 2010:$5,528,262,022

Net Asset Value as of June 30, 2010:$1,846,890,647

Net Asset Value per Share as of June 30, 2010:$23.99

Worst Monthly Drawdown:(14.74)% September 2008

Worst Peak-to-Valley Drawdown:(43.49)% February 2008 – February 2009*

| Monthly Rate of Return | 2010(%) | 2009(%) | 2008(%) | 2007(%) | ||||

January | (3.81) | (3.62) | 12.47 | 3.44 | ||||

February | (0.13) | (5.88) | 12.90 | 3.91 | ||||

March | (4.56) | 3.74 | (12.43) | (5.81) | ||||

April | 2.62 | 2.58 | 0.27 | (1.94) | ||||

May | (5.34) | 11.50 | (1.56) | 5.84 | ||||

June | 1.94 | (9.17) | 13.41 | (0.04) | ||||

July | (0.55) | (10.36) | (0.50) | |||||

August | 3.69 | (3.28) | 2.07 | |||||

September | (2.03) | (14.74) | 10.20 | |||||

October | 0.43 | (14.44) | (0.17) | |||||

November | 3.07 | (4.41) | 4.94 | |||||

December | (0.38) | 5.10** | 6.56*** | |||||

Compound Rate of Return | (9.23)% (6 months) | 1.85% | (20.91)% | 31.24% |

| * | The Worst Peak-to-Valley Drawdown from February 2008 – February 2009 includes the effect of the $0.45 per Share distribution made to Shareholders of record as of December 17, 2008. Please see Footnote **. |

| ** | The December 2008 return of 5.10% includes the $0.45 per Share distribution made to Shareholders of record as of December 17, 2008. Prior to the December 30, 2008 distribution, the pool’s return for December 2008 was 6.93%. |

| *** | The December 2007 return of 6.56% includes the $0.45 per Share distribution made to Shareholders of record as of December 19, 2007. Prior to the December 28, 2007 distribution, the pool’s return for December 2007 was 7.89%. |

| **** | As of October 19, 2009, the Fund commenced tracking the Deutsche Bank Liquid Commodity Index Diversified Agriculture Excess Return™. Prior to October 19, 2009, the Fund tracked the Deutsche Bank Liquid Commodity Index–Optimum Yield Agriculture Excess Return™. |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

See accompanying Footnotes to Performance Information.

Footnotes to Performance Information

1. “Aggregate Gross Capital Subscriptions” is the aggregate of all amounts ever contributed to the relevant pool, including investors who subsequently redeemed their investments.

2. “Net Asset Value” is the net asset value of each pool as of June 30, 2010.

3. “Net Asset Value per Share” is the Net Asset Value of the relevant pool divided by the total number of Shares outstanding with respect to such pool as of June 30, 2010.

4. “Worst Monthly Drawdown” is the largest single month loss sustained since inception of trading. “Drawdown” as used in this section of the Prospectus means losses experienced by the relevant pool over the specified period and is calculated on a rate of return basis, i.e., dividing net performance by beginning equity. “Drawdown” is measured on the basis of monthly returns only, and does not reflect intra-month figures. “Month” is the month of the Worst Monthly Drawdown.

5. “Worst Peak-to-Valley Drawdown” is the largest percentage decline in the Net Asset Value per Share over the history of the relevant pool. This need not be a continuous decline, but can be a series of positive and negative returns where the negative returns are larger than the positive returns. “Worst Peak-to-Valley Drawdown” represents the greatest percentage decline from any month-end Net Asset Value per Share that occurs without such month-end Net Asset Value per Share being equaled or exceeded as of a subsequent month-end. For example, if the Net Asset Value per Share of a particular pool declined by $1 in each of January and February, increased by $1 in March and declined again by $2 in April, a “peak-to-valley drawdown” analysis conducted as of the end of April would consider that “drawdown” to be still continuing and to be $3 in amount, whereas if the Net Asset Value per Share had increased by $2 in March, the January-February drawdown would have ended as of the end of February at the $2 level.

6. “Compound Rate of Return” is calculated by multiplying on a compound basis each of the monthly rates of return set forth in the respective charts above and not by adding or averaging such monthly rates of return. For periods of less than one year, the results are year-to-date.

5

DESCRIPTION OF THE DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD EXCESS RETURN™ SECTOR INDEXES AND THE DEUTSCHE BANK LIQUID COMMODITY INDEX EXCESS RETURN™ SECTOR INDEX

DBLCI™ and Deutsche Bank Liquid Commodity Index™ are trade marks of the Index Sponsor and are the subject of Community Trade Mark Nos. 3055043 and 3054996. Trade Mark applications in the United States are pending with respect to both the Trust and aspects of each Index. Any use of these marks must be with the consent of or under license from the Index Sponsor. The Fund, Master Fund and the Managing Owner have been licensed to use DBLCI™ and Deutsche Bank Liquid Commodity Index™. The Index Sponsor does not approve, endorse or recommend the Fund, the Master Fund or the Managing Owner.

General

Each of the Deutsche Bank Liquid Commodity Index–Optimum Yield Excess Return™, or DBLCI-OYER™, and the Deutsche Bank Liquid Commodity Index Excess Return™, or DBLCI ER™ (“DBLCI-OYER™” and “DBLCI ER™,” collectively, “DBLCI™” or “DBLCI ER™”), is intended to reflect the changes in market value, over time, positive or negative, in certain sectors of commodities, or an Index. Each Index is calculated on an excess return, or unfunded basis. All Indexes, excluding portions of the Deutsche Bank Liquid Commodity Index Diversified Agriculture Excess Return™, are rolled in a manner which is aimed at potentially maximizing the roll benefits in backwardated markets and minimizing the losses from rolling in contangoed markets, or Optimum Yield, with respect to each Index. Only Deutsche Bank Liquid Commodity Index Diversified Agriculture Excess Return™ is rolled both on an Optimum Yield basis and non-Optimum Yield basis. Each Index is comprised of one or more underlying commodities, or Index Commodities. The composition of Index Commodities with respect to each Index varies according to each specific sector that such Index intends to reflect. Each Index Commodity is assigned a weight, or Index Base Weight, which is intended to reflect the proportion of such Index Commodity relative to each Index.

Indexes and Covered Sectors

The Indexes track the following sectors:

| • | Deutsche Bank Liquid Commodity Index–Optimum Yield Energy Excess Return™, or DBLCI-OY Energy ER™, is intended to reflect the energy sector. |

| • | Deutsche Bank Liquid Commodity Index–Optimum Yield Crude Oil Excess Return™, or DBLCI-OY CL ER™, is intended to reflect the changes in market value of the crude oil sector. |

| • | Deutsche Bank Liquid Commodity Index–Optimum Yield Precious Metals Excess Return™, or DBLCI-OY Precious Metals ER™, is intended to reflect the precious metals sector. |

| • | Deutsche Bank Liquid Commodity Index–Optimum Yield Gold Excess Return™, or DBLCI-OY GC ER™, is intended to reflect the changes in market value of the gold sector. |

| • | Deutsche Bank Liquid Commodity Index–Optimum Yield Silver Excess Return™, or DBLCI-OY SI ER™, is intended to reflect the changes in market value of the silver sector. |

| • | Deutsche Bank Liquid Commodity Index–Optimum Yield Industrial Metals Excess Return™, or DBLCI-OY Industrial Metals ER™, is intended to reflect the base metals sector. |

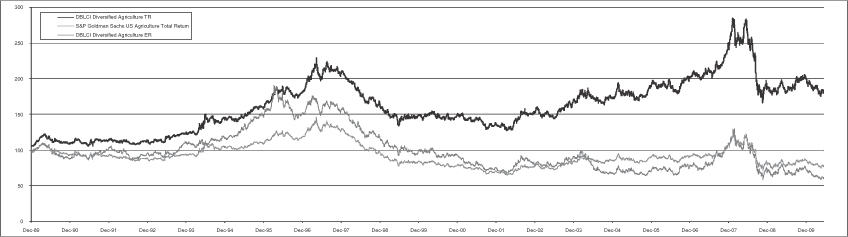

| • | Deutsche Bank Liquid Commodity Index Diversified Agriculture Excess Return™, or DBLCI Diversified Agriculture ER™, is intended to reflect the agricultural sector. |

DBLCI-OY CL ER™, DBLCI-OY GC ER™ and DBLCI-OY SI ER™ are Indexes with a single Index Commodity, or Single Commodity Sector Indexes.

Each Index has been calculated back to a base date, or Base Date. On the Base Date the closing level of each Index, or Closing Level, was 100.

The sponsor of each Index is Deutsche Bank AG London, or Index Sponsor.

6

SECTOR INDEXES OVERVIEW

| Index | Index Commodity | Exchange (Contract Symbol)1 | Base Date | Index Base Weight | |||||

DBLCI-OY Energy ER™ | Light, Sweet Crude Oil (WTI) | NYMEX (CL) | June 4, 1990 | 22.50 | % | ||||

| Heating Oil | NYMEX (HO) | 22.50 | % | ||||||

| Brent Crude Oil | ICE-UK (LCO) | 22.50 | % | ||||||

| RBOB Gasoline | NYMEX (XB) | 22.50 | % | ||||||

| Natural Gas | NYMEX (NG) | 10.00 | % | ||||||

DBLCI-OY CL ER™2 | Light, Sweet Crude Oil (WTI) | NYMEX (CL) | December 2, 1988 | 100.00 | % | ||||

DBLCI-OY Precious Metals ER™ | Gold | COMEX (GC) | December 2, 1988 | 80.00 | % | ||||

| Silver | COMEX (SI) | 20.00 | % | ||||||

DBLCI-OY GC ER™2 | Gold | COMEX (GC) | December 2, 1988 | 100.00 | % | ||||

DBLCI-OY SI ER™2 | Silver | COMEX (SI) | December 2, 1988 | 100.00 | % | ||||

DBLCI-OY Industrial Metals ER™ | Aluminum | LME (MAL) | September 3, 1997 | 33.33 | % | ||||

| Zinc | LME (MZN) | 33.33 | % | ||||||

| Copper - Grade A | LME (MCU) | 33.33 | % | ||||||

DBLCI Diversified Agriculture ER™ | Corn3 | CBOT (C) | January 18, 1989 | 12.50 | % | ||||

| Soybeans3 | CBOT (S) | 12.50 | % | ||||||

| Wheat3 | CBOT (W) | 6.25 | % | ||||||

| Kansas City Wheat3 | KCB (KW) | 6.25 | % | ||||||

| Sugar3 | ICE-US (SB) | 12.50 | % | ||||||

| Cocoa4 | ICE-US (CC) | 11.11 | % | ||||||

| Coffee4 | ICE-US (KC) | 11.11 | % | ||||||

| Cotton4 | ICE-US (CT) | 2.78 | % | ||||||

| Live Cattle4 | CME (LC) | 12.50 | % | ||||||

| Feeder Cattle4 | CME (FC) | 4.17 | % | ||||||

| Lean Hogs4 | CME (LH) | 8.33 | % | ||||||

1Connotes the exchanges on which the underlying futures contracts are traded with respect to each Single Commodity Index.

2DBLCI-OY CL ER™, DBLCI-OY GC ER™, or DBLCI-OY SI ER™ are Sector Indexes with a single Index Commodity, or Single Commodity Sector Indexes.

3Connotes Single Commodity Index rolled on Optimum Yield basis.

4Connotes non-OY Single Commodity Index.

Legend:

“CBOT” means the Board of Trade of the City of Chicago Inc., or its successor.

“CME” means the Chicago Mercantile Exchange, Inc., or its successor.

“COMEX” means the Commodity Exchange Inc., New York, or its successor.

“ICE-UK” means ICE Futures Europe, or its successor.

“ICE-US” means ICE Futures U.S., Inc., or its successor.

“KCB” mean the Board of Trade of Kansas City, Missouri, Inc., or its successor.

“LME” means The London Metal Exchange Limited, or its successor.

“NYMEX” means the New York Mercantile Exchange, or its successor.

7

Composition of Indexes

Each Index, except each Single Commodity Sector Index, is composed of notional amounts of each of the underlying Index Commodities. Each Single Commodity Sector Index is composed of one underlying Index Commodity. The notional amount of each Index Commodity included in each multi-sector Index is intended to reflect the changes in market value of each such Index Commodity within the specific Index. The Closing Level of each Index is calculated on each business day by the Index Sponsor based on the closing price of the futures contracts for each of the underlying Index Commodities and the notional amounts of such Index Commodities.

Each Index, excluding each Single Commodity Sector Index, is rebalanced annually in November to ensure that each of the Index Commodities is weighted in the same proportion that such Index Commodities were weighted on the Base Date.

The composition of each Index may be adjusted in the event that the Index Sponsor is not able to calculate the closing prices of the Index Commodities.

Each Index includes provisions for the replacement of futures contracts as they approach maturity. This replacement takes place over a period of time in order to lessen the impact on the market for the futures contracts being replaced. With respect to each Index Commodity, the Master Fund employs a rule-based approach when it ‘rolls’ from one futures contract to another. Rather than select a new futures contract based on a predetermined schedule (e.g., monthly), each Index Commodity (excluding the following underlying Index Commodities of the DBLCI Diversified Agriculture ER™: Cocoa, Coffee, Cotton, Live Cattle, Feeder Cattle and Lean Hogs, or the non-OY Single Commodity Indexes) rolls to the futures contract which generates the best possible ‘implied roll yield,’ or the OY Single Commodity Indexes. The futures contract with a delivery month within the next thirteen months which generates the best possible implied roll yield will be included in each OY Single Commodity Index. As a result, each OY Single Commodity Index is able to potentially maximize the roll benefits in backwardated markets and minimize the losses from rolling in contangoed markets.

Each of the non-OY Single Commodity Indexes rolls only to the next to expire futures contract as provided below under “Contract Selection (Non-OY Single Commodity Indexes only)”.

In general, as a futures contract approaches its expiration date, its price will move towards the spot price in a contangoed market. Assuming the spot price does not change, this would result in the futures contract price decreasing and a negative implied roll yield. The opposite is true in a backwardated market. Rolling in a contangoed market will tend to cause a drag on an Index Commodity’s contribution to the Fund’s return while rolling in a backwardated market will tend to cause a push on an Index Commodity’s contribution to the Fund’s return.

Each Index is calculated in USD on both an excess return (unfunded) and total return (funded) basis.

The futures contract price for each Index Commodity will be the exchange closing price for such Index Commodity on each weekday when banks in New York, New York are open, or Index Business Days. If a weekday is not an Exchange Business Day (as defined in the following sentence) but is an Index Business Day, the exchange closing price from the previous Index Business Day will be used for each Index Commodity. “Exchange Business Day” means, in respect of an Index Commodity, a day that is a trading day for such Index Commodity on the relevant exchange (unless either an Index disruption event or force majeure event has occurred).

Contract Selection (OY Single Commodity Indexes only)

On the first New York business day, or Verification Date, of each month, each Index Commodity futures contract will be tested in order to determine whether to continue including it in the applicable OY Single Commodity Index. If the Index Commodity futures contract requires delivery of the underlying commodity in the next month, known as the Delivery Month, a new Index Commodity futures contract will be selected for inclusion in such OY Single Commodity Index. For example, if the first New York business day is May 1, 2011, and the Delivery Month of the Index Commodity futures contract currently in such OY Single Commodity Index is June 2011, a new Index Commodity futures contract with a later Delivery Month will be selected.

For each underlying Index Commodity of an OY Single Commodity Index, the new Index Commodity futures contract selected will be the Index Commodity futures contract with the best possible “implied roll yield” based on the closing price for each eligible Index Commodity futures contract. Eligible Index Commodity futures contracts are any

8

Index Commodity futures contracts having a Delivery Month (i) no sooner than the month after the Delivery Month of the Index Commodity futures contract currently in such OY Single Commodity Index, and (ii) no later than the 13th month after the Verification Date. For example, if the first New York business day is May 1, 2011 and the Delivery Month of an Index Commodity futures contract currently in an OY Single Commodity Index is therefore June 2011, the Delivery Month of an eligible new Index Commodity futures contract must be between July 2011 and July 2012. The implied roll yield is then calculated and the futures contract on the Index Commodity with the best possible implied roll yield is then selected. If two futures contracts have the same implied roll yield, the futures contract with the minimum number of months prior to the Delivery Month is selected.

After selection of the replacement futures contract, each OY Single Commodity Index will roll such replacement futures contract as provided in the sub-paragraph “Monthly Index Roll Period with respect to both OY Single Commodity Indexes and Non-OY Single Commodity Indexes.”

[Remainder of page left blank intentionally.]

9

Contract Selection (the Non-OY Commodities only)

On the first Index Business Day of each month, a new Non-OY Commodity futures contract will be selected to replace the old Non-OY Commodity futures contract. The new Non-OY Commodity futures contract selected is as provided in the following schedule:

Contract | Exchange | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | |||||||||||||

Cocoa | ICE-US (CC) | H | K | K | N | N | U | U | Z | Z | Z | H | H | |||||||||||||

Coffee | ICE-US (KC) | H | K | K | N | N | U | U | Z | Z | Z | H | H | |||||||||||||

Cotton | ICE-US (CT) | H | K | K | N | N | Z | Z | Z | Z | Z | H | H | |||||||||||||

Live Cattle | CME (LC) | J | J | M | M | Q | Q | V | V | Z | Z | G | G | |||||||||||||

Feeder Cattle | CME (FC) | H | J | K | Q | Q | Q | U | V | X | F | F | H | |||||||||||||

Lean Hogs | CME (LH) | J | J | M | M | N | Q | V | V | Z | Z | G | G | |||||||||||||

| Month Letter Codes | ||||

| Month | Letter Code | |||

January | F | |||

February | G | |||

March | H | |||

April | J | |||

May | K | |||

June | M | |||

July | N | |||

August | Q | |||

September | U | |||

October | V | |||

November | X | |||

December | Z | |||

After selection of the replacement futures contract, each Non-OY Index Commodity futures contract will be rolled as provided in the sub-paragraph “Monthly Index Roll Period with respect to both OY Index Commodities and Non-OY Index Commodities.”

[Remainder of page left blank intentionally.]

10

Monthly Index Roll Period with respect to both OY Single Commodity Indexes and Non-OY Single Commodity Indexes

After the futures contract selection with respect to both OY Single Commodity Indexes and non-OY Single Commodity Indexes, the monthly roll for each Index Commodity subject to a roll in that particular month unwinds the old futures contract and enters a position in the new futures contract. This takes place between the 2nd and 6th Index Business Day of the month.

On each day during the roll period, new notional holdings are calculated. The calculations for the old Index Commodities that are leaving an Index and the new Index Commodities are then calculated.

On all days that are not monthly index roll days, the notional holdings of each Index Commodity future remains constant.

Each Index is re-weighted on an annual basis on the 6th Index Business Day of each November.

The calculation of each Index is expressed as the weighted average return of the Index Commodities.

Change in the Methodology of an Index

The Index Sponsor employs the methodology described above and its application of such methodology shall be conclusive and binding. While the Index Sponsor currently employs the above described methodology to calculate each Index, no assurance can be given that fiscal, market, regulatory, juridical or financial circumstances (including, but not limited to, any changes to or any suspension or termination of or any other events affecting any Index Commodity or a futures contract) will not arise that would, in the view of the Index Sponsor, necessitate a modification of or change to such methodology and in such circumstances the Index Sponsor may make any such modification or change as it determines appropriate. The Index Sponsor may also make modifications to the terms of an Index in any manner that it may deem necessary or desirable, including (without limitation) to correct any manifest or proven error or to cure, correct or supplement any defective provision of an Index. The Index Sponsor will publish notice of any such modification or change and the effective date thereof as set forth below.

Publication of Closing Levels and Adjustments

In order to calculate each indicative Index level, the Index Sponsor polls Reuters every 15 seconds to determine the real time price of each underlying futures contract with respect to each Index Commodity of the applicable Index. The Index Sponsor then applies a set of rules to these values to create the indicative level of each Index. These rules are consistent with the rules which the Index Sponsor applies at the end of each trading day to calculate the closing level of each Index. A similar polling process is applied to the U.S. Treasury bills to determine the indicative value of the U.S. Treasury bills held by the Fund every 15 seconds throughout the trading day.

The intra-day indicative value per Share of each Fund is calculated by adding the intra-day U.S. Treasury bills level plus the intra-day level of the applicable Index which will then be applied to the last published net asset value of such Fund, less accrued fees.

The Index Sponsor publishes the closing level of each Index daily. The Managing Owner publishes the net asset value of each Fund and the net asset value per Share of each Fund daily. Additionally, the Index Sponsor publishes the intra-day Index level, and the Managing Owner publishes the indicative value per Share of each Fund (quoted in U.S. dollars) once every fifteen seconds throughout each trading day. All of the foregoing information is published as follows:

The current trading price per Share of each Fund (quoted in U.S. dollars) will be published continuously under its ticker symbol as trades occur throughout each trading day on the consolidated tape, Reuters and/or Bloomberg and on the Managing Owner’s website at http://www.dbfunds.db.com, or any successor thereto.

The most recent end-of-day closing level of each Index is published under its own symbol as of the close of business for the NYSE Arca each trading day on the consolidated tape, Reuters and/or Bloomberg and on the Managing Owner’s website at http://www.dbfunds.db.com, or any successor thereto. The most recent end-of-day net asset value of each Fund is published under its own symbol as of the close of business on Reuters and/or Bloomberg and on the Managing Owner’s website at http://www.dbfunds.db.com, or any successor thereto. In addition, the most recent end-of-day net asset value of each Fund is published the following morning on the consolidated tape.

End-of-Day Index Closing Level Symbols; End-of-Day Net Asset Value Symbols

PowerShares DB Energy Fund. The end-of-day closing level of the DBLCI-OY Energy ER is

11

published under the symbol DBENIX. The end-of-day net asset value of PowerShares DB Energy Fund is published under the symbol DBE.NV.

PowerShares DB Oil Fund. The end-of-day closing level of the DBLCI-OY CL ER is published under the symbol DBOLIX. The end-of-day net asset value of PowerShares DB Oil Fund is published under the symbol DBO.NV.

PowerShares DB Precious Metals Fund. The end-of-day closing level of the DBLCI-OY Precious Metals ER is published under the symbol DBPMIX. The end-of-day net asset value of PowerShares DB Precious Metals Fund is published under the symbol DBP.NV.

PowerShares DB Gold Fund. The end-of-day closing level of the DBLCI-OY GC ER is published under the symbol DGLDIX. The end-of-day net asset value of PowerShares DB Gold Fund is published under the symbol DGL.NV.

PowerShares DB Silver Fund. The end-of-day closing level of the DBLCI-OY SI ER is published under the symbol DBSLIX. The end-of-day net asset value of PowerShares DB Silver Fund is published under the symbol DBS.NV.

PowerShares DB Base Metals Fund. The end-of-day closing level of the DBLCI-OY Industrial Metals ER is published under the symbol DBBMIX. The end-of-day net asset value of PowerShares DB Base Metals Fund is published under the symbol DBB.NV.

PowerShares DB Agriculture Fund. The end-of-day closing level of the DBLCI Diversified Agriculture ER is published under the symbol DBAGIX. The end-of-day net asset value of PowerShares DB Agriculture Fund is published under the symbol DBA.NV.

The Managing Owner publishes the net asset value of each Fund and the net asset value per Share of each Fund daily. Additionally, the Index Sponsor publishes the intra-day level of each Index, and the Managing Owner publishes the indicative value per Share of each Fund (quoted in U.S. dollars) once every fifteen seconds throughout each trading day on the consolidated tape, Reuters and/or Bloomberg and on the Managing Owner’s website at http://www.dbfunds.db.com, or any successor thereto. All of the foregoing information is published under the following symbols:

Intra-Day Index Level Symbols and Intra-Day Indicative Values Per Share Symbols

PowerShares DB Energy Fund. The intra-day index level of the DBLCI-OY Energy ER is published under the symbol DBENIX. The intra-day indicative value per Share of PowerShares DB Energy Fund is published under the symbol DBE.IV.

PowerShares DB Oil Fund. The intra-day index level of the DBLCI-OY CL ER is published under the symbol DBOLIX. The intra-day indicative value per Share of PowerShares DB Oil Fund is published under the symbol DBO.IV.

PowerShares DB Precious Metals Fund. The intra-day index level of the DBLCI-OY Precious Metals ER is published under the symbol DBPMIX. The intra-day indicative value per Share of PowerShares DB Precious Metals Fund is published under the symbol DBP.IV.

PowerShares DB Gold Fund. The intra-day index level of the DBLCI-OY GC ER is published under the symbol DGLDIX. The intra-day indicative value per Share of PowerShares DB Gold Fund is published under the symbol DGL.IV.

PowerShares DB Silver Fund. The intra-day index level of the DBLCI-OY SI ER is published under the symbol DBSLIX. The intra-day indicative value per Share of PowerShares DB Silver Fund is published under the symbol DBS.IV.

PowerShares DB Base Metals Fund. The intra-day index level of the DBLCI-OY Industrial Metals ER is published under the symbol DBBMIX. The intra-day indicative value per Share of PowerShares DB Base Metals Fund is published under the symbol DBB.IV.

PowerShares DB Agriculture Fund. The intra-day index level of the DBLCI Diversified Agriculture ER is published under the symbol DBAGIX. The intra-day indicative value per Share of PowerShares DB Agriculture Fund is published under the symbol DBA.IV.

Each Index’s history is also available at https://index.db.com.

The Index Sponsor obtains information for inclusion in, or for use in the calculation of, the Indexes from sources the Index Sponsor considers reliable. None of the Index Sponsor, the Managing Owner, the Funds, the Master Funds or any of their respective affiliates accepts responsibility for or guarantees the accuracy and/or completeness of any of the Indexes or any data included in any of the Indexes.

All of the foregoing information with respect to each Index is also published at https://index.db.com.

The Index Sponsor publishes any adjustments made to each Index on the Managing Owner’s

12

website http://www.dbfunds.db.com and https://index.db.com, or any successor thereto.

Interruption of Index Calculation

Calculation of each Index may not be possible or feasible under certain events or circumstances, including, without limitation, a systems failure, natural or man-made disaster, act of God, armed conflict, act of terrorism, riot or labor disruption or any similar intervening circumstance, that is beyond the reasonable control of the Index Sponsor and that the Index Sponsor determines affects an Index or any Index Commodity. Upon the occurrence of such force majeure events, the Index Sponsor may, in its discretion, elect one (or more) of the following options:

| • | make such determinations and/or adjustments to the terms of such Index as it considers appropriate to determine any closing level on any such appropriate Index business day; and/or |

| • | defer publication of the information relating to such Index until the next Index business day on which it determines that no force majeure event exists; and/or |

| • | permanently cancel publication of the information relating to such Index. |

Additionally, calculation of an Index may also be disrupted by an event that would require the Index Sponsor to calculate the closing price in respect of the relevant Index Commodity on an alternative basis were such event to occur or exist on a day that is a trading day for such Index Commodity on the relevant exchange. If such an Index disruption event in relation to an Index Commodity as described in the prior sentence occurs and continues for a period of five successive trading days for such Index Commodity on the relevant exchange, the Index Sponsor will, in its discretion, either

| • | to continue to calculate the relevant closing price for a further period of five successive trading days for such Index Commodity on the relevant exchange or |

| • | if such period extends beyond the five successive trading days, the Index Sponsor may elect to replace the exchange traded instrument with respect to a specific Index Commodity and shall make all necessary adjustments to the methodology and calculation of an Index as it deems appropriate. |

Historical Closing Levels

Set out below are the Closing Levels and related data with respect to each Index as of June 30, 2010.

With respect to each of the Closing Levels Tables, historic daily Index Closing Levels have been calculated with respect to each Index since the Base Date of each Index.

The Base Date for each Index is as follows:

| Index | Base Date | |

DBLCI-OY Energy ER™ | June 4, 1990 | |

DBLCI-OY CL ER™ | December 2, 1988 | |

DBLCI-OY Precious Metals ER™ | December 2, 1988 | |

DBLCI-OY GC ER™ | December 2, 1988 | |

DBLCI-OY SI ER™ | December 2, 1988 | |

DBLCI-OY Industrial Metals ER™ | September 3, 1997 | |

DBLCI Diversified Agriculture ER™ | January 18, 1989 | |

Each Base Date was selected by the Index Sponsor based on the availability of price data with respect to the relevant underlying futures contracts on the Index Commodities of each Index.

The following three paragraphs apply to each applicable Index, except with respect to DBLCI Diversified Agriculture ER™:

Since March 2003, the historic data with respect to the closing prices of futures contracts on Light, Sweet Crude Oil (CL), Heating Oil (HO), Wheat (W), Corn (C), Gold (GC) and Aluminum (MAL) originated from Reuters. Prior to March 2003, the closing prices of futures contracts on CL, HO, W, C, GC and MAL were obtained from publicly available information from Logical Information Machines (http://www.lim.com), Bloomberg and Reuters. The Index Sponsor has not independently verified the information extracted from these sources. The Index calculation methodology and commodity future selection are the same prior to and following March 2003.

Since June 2006, the historic data with respect to the closing prices of futures contracts on Brent Crude Oil (LCO), RBOB Gasoline (XB), Natural Gas (NG), Silver (SI), Zinc (MZN), Copper—Grade A (MCU), Soybeans (S) and Sugar (SB) originated from Reuters. Prior to June 2006, the closing prices of futures contracts on LCO, XB, NG, SI, MZN, MCU, S and SB were obtained from publicly available information from Logical Information Machines (http://www.lim.com), Bloomberg and Reuters. The Index Sponsor has not independently verified the information extracted from these sources.

13

The Index calculation methodology and commodity future selection are the same prior to and following June 2006.

The Index Sponsor used the return of Unleaded Gasoline (traded on the NYMEX under the symbol “HU”) as a proxy with respect to XB prior to November 2005. On and after November 2005, the Index Sponsor obtained historic data from Reuters with respect to XB. The Index Sponsor considers the use of HU as a proxy for XB prior to November 2005 to be appropriate because XB and HU are sufficiently similar in nature.

The following paragraph applies only to DBLCI Diversified Agriculture ER™:

Since June 2006, the historic data with respect to the closing prices of futures contracts on Feeder Cattle (FC), Cotton #2 (CT), Coffee (KC), Cocoa (CC), Live Cattle (LC), Lean Hogs (LH), Corn (C), Wheat (W), Soybeans (S), Sugar #11 (SB) and Kansas City Wheat (KW) originated from Reuters. Prior to June 2006, the closing prices of futures contracts on Feeder Cattle (FC), Cotton #2 (CT), Coffee (KC), Cocoa (CC), Live Cattle (LC), Lean Hogs (LH), Corn (C), Wheat (W), Soybeans (S), Sugar #11 (SB) and Kansas City Wheat (KW) were obtained from publicly available information from Logical Information Machines (http://www.lim.com), Bloomberg, and Reuters. The Index Sponsor has not independently verified the information extracted from these sources. The Index calculation methodology and commodity future selection are the same prior to and following June 2006.

Complete price histories regarding certain futures contracts on the Index Commodities were not available (e.g., due to lack of trading on specific days). In the event that prices on such futures contracts on the Index Commodities were unavailable during a contract selection day, such futures contracts were excluded from the futures contract selection process. The Index Sponsor believes that the incomplete price histories should not have a material impact on the calculation of any of the Indexes.

Each Index Closing Level is equal to the weighted sum of the market value of the commodity futures contracts of all the respective Index Commodities that comprise each specific Index. The market value of the commodity futures contracts of an Index Commodity is equal to the number of commodity futures contracts of an Index Commodity held multiplied by the commodity futures contracts closing price of an Index Commodity.

The weight of each Index Commodity of a specific Index is linked to the number of commodity futures contracts held of such Index Commodity and the price of commodity futures contracts of the Index Commodity. The weight of an Index Commodity is defined as the market value of the commodity futures contracts of the Index Commodity divided by the sum of all market values of all commodity futures contracts of the Index Commodities that comprise an Index multiplied by 100%.

The Index Commodities Weights Tables reflect the range of the weightings with respect to each of the Index Commodities used to calculate each Index.

The Index rules stipulate the holding in each Index Commodity futures contract. Holdings in each Index Commodity change during the Index rebalancing periods as determined by the optimum yield roll rules.

Cautionary Statement–Statistical Information

Various statistical information is presented on the following pages, relating to the Closing Levels of each Index, on an annual and cumulative basis, including certain comparisons of each Index to other commodities indices. In reviewing such information, prospective investors should consider that:

| • | Changes in Closing Levels of each Index during any particular period or market cycle may be volatile. |

| Index | Worst Peak-to- Valley | Worst Monthly Drawdown and Year | ||

| DBLCI-OY Energy ER™ | (65.81)%, 5/08 — 2/09 | (28.71)%, 10/08 | ||

| DBLCI-OY CL ER™ | (65.23)%, 5/08 — 2/09 | (29.35)%, 10/08 | ||

| DBLCI-OY Precious Metals ER™ | (65.97)%, 12/88 — 3/01 | (18.85)%, 10/08 | ||

| DBLCI-OY GC ER™ | (66.87)%, 12/88 — 3/01 | (18.46)%, 10/08 | ||

| DBLCI-OY SI ER™ | (66.49)%, 12/88 — 11/01 | (23.59)%, 8/08 | ||

| DBLCI-OY Industrial Metals ER™ | (59.03)%, 7/07 — 1/09 | (27.50)%, 10/08 | ||

| DBLCI Diversified Agriculture ER™ | (53.40)%, 4/97 — 4/02 | (14.37)%, 10/08 |

For example, the “Worst Peak-to-Valley Drawdown” of each Index, represents the greatest percentage decline from any month-end Closing Level, without such Closing Level being equaled or exceeded as of a subsequent month-end, which occurred during the above-listed time period.

14

The “Worst Monthly Drawdown” of each Index occurred during the above-listed month and year.

See “Volatility of the Various Indexes” on page 53.

| • | Neither the fees charged by any Fund nor the execution costs associated with establishing futures positions in the Index Commodities are incorporated into the Closing Levels of each Index. Accordingly, such Index Levels have not been reduced by the costs associated with an actual investment, such as a Fund, with an investment objective of tracking the corresponding Index. |

| • | The Indexes were established between May-July 2006 and September 2009, and are independently calculated by Deutsche Bank AG London, the Index Sponsor. The Index calculation methodology and commodity futures contracts selection is the same before and after May-July 2006 and September 2009, as described above. Accordingly, the Closing Levels of each Index, terms of each Index methodology and Index Commodities, reflect an element of hindsight at the time each Index was established. See “The Risks You Face—(10) You May Not Rely on Past Performance or Index Results in Deciding Whether to Buy Shares” and “—(11) Fewer Representative Commodities May Result In Greater Index Volatility.” |

WHILE EACH FUND’S OBJECTIVE IS NOT TO GENERATE PROFIT THROUGH ACTIVE PORTFOLIO MANAGEMENT, BUT IS TO TRACK THE CORRESPONDING INDEX, BECAUSE EACH INDEX WAS ESTABLISHED BETWEEN MAY-JULY 2006 AND SEPTEMBER 2009, CERTAIN INFORMATION RELATING TO INDEX CLOSING LEVELS MAY BE CONSIDERED TO BE “HYPOTHETICAL.” HYPOTHETICAL INFORMATION MAY HAVE CERTAIN INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW.

NO REPRESENTATION IS BEING MADE THAT EACH INDEX WILL OR IS LIKELY TO ACHIEVE ANNUAL OR CUMULATIVE CLOSING LEVELS CONSISTENT WITH OR SIMILAR TO THOSE SET FORTH HEREIN. SIMILARLY, NO REPRESENTATION IS BEING MADE THAT EACH FUND WILL GENERATE PROFITS OR LOSSES SIMILAR TO THE FUND’S PAST PERFORMANCE, WHEN AVAILABLE, OR THE HISTORICAL ANNUAL OR CUMULATIVE CHANGES IN THE CORRESPONDING INDEX CLOSING LEVELS. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY INVESTMENT METHODOLOGIES, WHETHER ACTIVE OR PASSIVE.

ONE OF THE LIMITATIONS OF HYPOTHETICAL INFORMATION IS THAT IT IS GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. TO THE EXTENT THAT INFORMATION PRESENTED HEREIN RELATES TO THE PERIOD SINCE INCEPTION WITH RESPECT TO EACH INDEX THROUGH MAY-JULY 2006 AND SEPTEMBER 2009, AS APPLICABLE, EACH INDEX’S CLOSING LEVELS REFLECT THE APPLICATION OF THE INDEX’S METHODOLOGY, AND SELECTION OF INDEX COMMODITIES, IN HINDSIGHT.

NO HYPOTHETICAL RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THERE ARE NUMEROUS FACTORS, INCLUDING THOSE DESCRIBED UNDER “THE RISKS YOU FACE” HEREIN, RELATED TO THE COMMODITIES MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF EACH FUND’S EFFORTS TO TRACK ITS CORRESPONDING INDEX OVER TIME WHICH CANNOT BE, AND HAVE NOT BEEN, ACCOUNTED FOR IN THE PREPARATION OF SUCH INDEX INFORMATION SET FORTH ON THE FOLLOWING PAGES, ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL PERFORMANCE RESULTS FOR EACH FUND. FURTHERMORE, THE INDEX INFORMATION DOES NOT INVOLVE FINANCIAL RISK OR ACCOUNT FOR THE IMPACT OF FEES AND COSTS ASSOCIATED WITH EACH FUND.

THE MANAGING OWNER COMMENCED OPERATIONS IN JANUARY 2006. AS MANAGING OWNER, THE MANAGING OWNER AND ITS TRADING PRINCIPALS HAVE BEEN MANAGING THE DAY-TO-DAY OPERATIONS FOR THE FUNDS AND RELATED PRODUCTS AND MANAGING FUTURES TRADING ACCOUNTS. BECAUSE THERE ARE LIMITED ACTUAL TRADING RESULTS TO COMPARE TO THE INDEX CLOSING LEVELS SET FORTH HEREIN, PROSPECTIVE INVESTORS SHOULD BE PARTICULARLY WARY OF PLACING UNDUE RELIANCE ON THE ANNUAL OR CUMULATIVE INDEX RESULTS.

[Remainder of page left blank intentionally.]

15

Volatility of the Various Indexes

The following table1 reflects various measures of volatility2 of the history of each Index as calculated on an excess return basis:

| Volatility Type | DBLCI-OY Energy ER™3 | DBLCI-OY CL ER™4 | DBLCI-OY Precious Metals ER™4 | DBLCI-OY GC ER™4 | DBLCI-OY SI ER™4 | DBLCI-OY Industrial Metals ER™5 | DBLCI Diversified Agriculture ER™6 | ||||||||||||||

Daily volatility over full history | 25.59 | % | 27.92 | % | 16.40 | % | 15.27 | % | 25.99 | % | 21.24 | % | 10.38 | % | |||||||

Average rolling 3 month daily volatility | 23.86 | % | 26.13 | % | 15.26 | % | 14.09 | % | 24.17 | % | 19.60 | % | 9.66 | % | |||||||

Monthly return volatility | 25.80 | % | 26.97 | % | 15.95 | % | 14.97 | % | 25.30 | % | 21.54 | % | 12.04 | % | |||||||

Average annual volatility | 24.79 | % | 26.81 | % | 15.21 | % | 14.16 | % | 23.84 | % | 13.02 | % | 9.96 | % | |||||||

The following table reflects the daily volatility on an annual basis of each Index: |

| ||||||||||||||||||||

| Year | DBLCI-OY Energy ER™3 | DBLCI-OY CL ER™4 | DBLCI-OY Precious Metals ER™4 | DBLCI-OY GC ER™4 | DBLCI-OY SI ER™4 | DBLCI-OY Industrial Metals ER™5 | DBLCI Diversified Agriculture ER™6 | ||||||||||||||

1988 | — | 26.56% | 11.17% | 11.41% | 10.73% | — | — | ||||||||||||||

1989 | — | 28.11% | 13.57% | 13.14% | 18.53% | — | 8.35% | ||||||||||||||

1990 | 44.82% | 40.56% | 16.71% | 17.67% | 19.41% | — | 7.92% | ||||||||||||||

1991 | 31.03% | 29.57% | 13.63% | 12.63% | 23.40% | — | 7.85% | ||||||||||||||

1992 | 14.60% | 16.66% | 8.90% | 8.32% | 15.67% | — | 6.93% | ||||||||||||||

1993 | 15.25% | 17.70% | 16.81% | 14.44% | 28.37% | — | 8.24% | ||||||||||||||

1994 | 18.05% | 20.13% | 12.08% | 9.60% | 23.28% | — | 12.80% | ||||||||||||||

1995 | 13.45% | 17.07% | 9.89% | 6.62% | 26.37% | — | 6.78% | ||||||||||||||

1996 | 23.86% | 31.02% | 7.74% | 6.17% | 17.62% | — | 7.80% | ||||||||||||||

1997 | 18.29% | 21.51% | 13.51% | 12.60% | 24.68% | 11.99% | 11.19% | ||||||||||||||

1998 | 23.80% | 27.97% | 14.60% | 12.84% | 29.22% | 14.38% | 8.06% | ||||||||||||||

1999 | 24.43% | 27.10% | 16.54% | 17.35% | 21.74% | 14.07% | 10.74% | ||||||||||||||

2000 | 28.21% | 32.19% | 14.01% | 15.02% | 14.41% | 11.78% | 8.87% | ||||||||||||||

2001 | 27.56% | 29.77% | 13.79% | 14.44% | 17.22% | 12.57% | 8.38% | ||||||||||||||

2002 | 24.63% | 25.52% | 13.51% | 13.44% | 17.43% | 13.12% | 9.51% | ||||||||||||||

2003 | 26.34% | 26.59% | 16.17% | 16.66% | 20.32% | 13.86% | 8.37% | ||||||||||||||

2004 | 28.71% | 30.80% | 19.48% | 16.25% | 35.48% | 20.85% | 11.01% | ||||||||||||||

2005 | 27.49% | 26.55% | 13.23% | 12.38% | 21.32% | 18.18% | 9.40% | ||||||||||||||

2006 | 22.01% | 22.01% | 25.97% | 22.81% | 41.21% | 32.26% | 9.57% | ||||||||||||||

2007 | 19.54% | 21.17% | 14.96% | 13.91% | 21.28% | 20.35% | 9.36% | ||||||||||||||

2008 | 36.57% | 41.43% | 27.33% | 25.53% | 43.01% | 28.81% | 21.09% | ||||||||||||||

2009 | 31.28% | 35.56% | 20.44% | 18.40% | 31.13% | 29.14% | 15.60% | ||||||||||||||

20101 | 20.64% | 23.10% | 15.69% | 14.01% | 26.41% | 26.57% | 11.24% | ||||||||||||||

| 1As | of June 30, 2010. Past Index levels are not necessarily indicative of future Index levels. |

| 2Volatility, | for these purposes, means the following: |

Daily Volatility: The relative rate at which the price of the Index moves up and down, found by calculating the annualized standard deviation of the daily change in price.

Monthly Return Volatility: The relative rate at which the price of the Index moves up and down, found by calculating the annualized standard deviation of the monthly change in price.

Average Annual Volatility: The average of yearly volatilities for a given sample period. The yearly volatility is the relative rate at which the price of the Index moves up and down, found by calculating the annualized standard deviation of the daily change in price for each business day in the given year.

| 3As | of June 4, 1990. Past Index levels are not necessarily indicative of future Index levels. |

| 4As | of December 2, 1988. Past Index levels are not necessarily indicative of future Index levels. |

| 5As | of September 3, 1997. Past Index levels are not necessarily indicative of future Index levels. |

| 6As | of January 18, 1989. Past Index levels are not necessarily indicative of future Index levels. |

16

ENERGY SECTOR DATA

RELATING TO

DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD ENERGY EXCESS RETURN™

(DBLCI-OY ENERGY ER™)

17

CLOSING LEVELS TABLES

DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD ENERGY EXCESS RETURN™

| CLOSING LEVEL | CHANGES | |||||||

| High1 | Low2 | Annual Index Changes3 | Index Changes Since Inception4 | |||||

19905 | 179.19 | 96.66 | 45.52% | 45.52% | ||||

1991 | 147.42 | 107.20 | -20.99% | 14.98% | ||||

1992 | 137.39 | 110.88 | 9.57% | 25.99% | ||||

1993 | 138.78 | 100.51 | -20.19% | 0.56% | ||||

1994 | 122.19 | 95.20 | 6.96% | 7.56% | ||||

1995 | 119.82 | 102.02 | 11.00% | 19.39% | ||||

1996 | 197.83 | 111.99 | 63.92% | 95.71% | ||||

1997 | 204.30 | 159.71 | -18.40% | 59.71% | ||||

1998 | 160.51 | 97.65 | -36.95% | 0.70% | ||||

1999 | 178.20 | 92.77 | 72.80% | 74.00% | ||||

2000 | 298.97 | 167.50 | 41.06% | 145.44% | ||||

2001 | 278.42 | 192.42 | -16.74% | 104.36% | ||||

2002 | 298.19 | 194.55 | 41.97% | 190.12% | ||||

2003 | 391.72 | 284.31 | 32.29% | 283.81% | ||||

2004 | 715.99 | 383.42 | 54.72% | 493.84% | ||||

2005 | 1037.13 | 582.46 | 55.14% | 821.29% | ||||

2006 | 1074.96 | 812.65 | -10.74% | 722.36% | ||||

2007 | 1112.80 | 709.23 | 34.88% | 1009.21% | ||||

2008 | 1772.65 | 559.38 | -40.45% | 560.50% | ||||

2009 | 862.18 | 518.29 | 25.76% | 730.64% | ||||

20106 | 884.28 | 705.31 | -10.22% | 645.72% | ||||

THE FUND WILL TRADE WITH A VIEW TO TRACKING THE DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD ENERGY EXCESS RETURN™ OVER TIME.

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD ENERGY TOTAL RETURN™

| CLOSING LEVEL | CHANGES | |||||||

| High1 | Low2 | Annual Index Changes3 | Index Changes Since Inception4 | |||||

19905 | 183.60 | 97.33 | 51.88% | 51.88% | ||||

1991 | 154.30 | 112.85 | -16.53% | 26.77% | ||||

1992 | 155.82 | 122.35 | 13.48% | 43.86% | ||||

1993 | 160.01 | 118.31 | -17.71% | 18.38% | ||||

1994 | 147.06 | 112.95 | 11.67% | 32.19% | ||||

1995 | 155.68 | 127.46 | 17.38% | 55.17% | ||||

1996 | 270.11 | 146.19 | 72.56% | 167.77% | ||||

1997 | 279.83 | 227.35 | -14.08% | 130.07% | ||||

1998 | 232.17 | 147.51 | -33.81% | 52.29% | ||||

1999 | 282.30 | 141.11 | 81.15% | 175.87% | ||||

2000 | 496.29 | 265.84 | 49.64% | 312.83% | ||||

2001 | 476.58 | 334.41 | -13.77% | 255.97% | ||||

2002 | 527.96 | 339.16 | 44.32% | 413.72% | ||||

2003 | 700.53 | 505.36 | 33.65% | 586.61% | ||||

2004 | 1293.70 | 686.54 | 56.88% | 977.16% | ||||

2005 | 1917.92 | 1056.70 | 60.14% | 1625.00% | ||||

2006 | 2070.40 | 1595.93 | -6.33% | 1515.87% | ||||

2007 | 2285.06 | 1397.07 | 41.00% | 2178.45% | ||||

2008 | 3676.21 | 1165.04 | -39.62% | 1275.66% | ||||

2009 | 1798.15 | 1079.73 | 25.94% | 1632.53% | ||||

20106 | 1845.15 | 1471.84 | -10.17% | 1456.35% | ||||

THE FUND WILL NOT TRADE WITH A VIEW TO TRACKING THE DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD ENERGY TOTAL RETURN™ OVER TIME.

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

See accompanying Notes and Legends.

18

INDEX COMMODITIES WEIGHTS TABLES

DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD ENERGY EXCESS RETURN™

| CL7 | HO7 | LCO7 | XB7 | NG7 | ||||||||||||||||

| High1 | Low2 | High | Low | High | Low | High | Low | High | Low | |||||||||||

19905 | 21.8% | 21.9% | 21.4% | 22.6% | 27.2% | 22.2% | 23.4% | 22.4% | 6.2% | 10.9% | ||||||||||

1991 | 21.8% | 22.5% | 22.8% | 22.7% | 23.8% | 20.0% | 21.5% | 21.8% | 10.1% | 13.1% | ||||||||||

1992 | 21.3% | 22.3% | 23.1% | 23.1% | 21.6% | 21.5% | 21.7% | 22.2% | 12.3% | 10.8% | ||||||||||

1993 | 21.6% | 22.1% | 21.5% | 22.8% | 21.1% | 22.7% | 21.4% | 22.0% | 14.4% | 10.4% | ||||||||||

1994 | 20.6% | 21.7% | 22.4% | 22.5% | 24.7% | 21.9% | 23.0% | 21.8% | 9.3% | 12.1% | ||||||||||

1995 | 22.9% | 24.3% | 21.2% | 22.1% | 23.1% | 23.0% | 23.1% | 21.9% | 9.7% | 8.8% | ||||||||||

1996 | 22.6% | 22.6% | 21.6% | 21.1% | 22.0% | 22.5% | 21.8% | 22.9% | 12.0% | 10.9% | ||||||||||

1997 | 23.2% | 22.5% | 21.6% | 22.6% | 22.2% | 21.6% | 21.4% | 23.1% | 11.4% | 10.1% | ||||||||||

1998 | 22.4% | 22.7% | 22.9% | 23.4% | 21.3% | 21.1% | 23.5% | 22.5% | 9.9% | 10.4% | ||||||||||

1999 | 22.7% | 23.1% | 21.9% | 22.0% | 23.0% | 22.2% | 23.3% | 22.3% | 9.1% | 10.4% | ||||||||||

2000 | 21.8% | 22.9% | 22.5% | 22.2% | 21.2% | 22.8% | 23.2% | 23.2% | 11.4% | 8.9% | ||||||||||

2001 | 23.5% | 22.9% | 22.0% | 22.2% | 21.4% | 21.8% | 22.5% | 22.7% | 10.5% | 10.4% | ||||||||||

2002 | 21.4% | 23.2% | 22.4% | 22.5% | 24.2% | 22.6% | 21.8% | 23.2% | 10.3% | 8.5% | ||||||||||

2003 | 22.7% | 21.2% | 22.6% | 21.5% | 22.3% | 23.2% | 22.3% | 21.8% | 10.2% | 12.3% | ||||||||||

2004 | 23.9% | 22.6% | 23.0% | 22.2% | 23.2% | 21.8% | 21.0% | 22.9% | 8.8% | 10.5% | ||||||||||

2005 | 20.6% | 22.3% | 23.5% | 22.7% | 21.8% | 22.3% | 24.9% | 23.0% | 9.1% | 9.7% | ||||||||||

2006 | 23.3% | 22.8% | 22.7% | 22.7% | 23.2% | 22.9% | 25.3% | 22.8% | 5.5% | 8.7% | ||||||||||

2007 | 22.6% | 22.1% | 22.8% | 23.0% | 22.5% | 22.1% | 23.0% | 22.6% | 9.1% | 10.2% | ||||||||||

2008 | 22.2% | 21.8% | 24.2% | 21.3% | 22.3% | 22.8% | 21.3% | 21.7% | 10.1% | 12.4% | ||||||||||

2009 | 24.5% | 22.7% | 19.4% | 20.7% | 23.9% | 22.8% | 27.5% | 24.3% | 4.7% | 9.6% | ||||||||||

20106 | 22.8% | 22.1% | 23.0% | 23.0% | 23.4% | 22.8% | 23.5% | 23.1% | 7.3% | 9.1% | ||||||||||

THE FUND WILL TRADE WITH A VIEW TO TRACKING THE

DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD ENERGY EXCESS RETURN™ OVER TIME.

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE,

SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD ENERGY TOTAL RETURN™

| CL7 | HO7 | LCO7 | XB7 | NG7 | ||||||||||||||||

| High1 | Low2 | High | Low | High | Low | High | Low | High | Low | |||||||||||

19905 | 21.8% | 21.9% | 21.4% | 22.6% | 27.2% | 22.2% | 23.4% | 22.4% | 6.2% | 10.9% | ||||||||||

1991 | 21.8% | 22.5% | 22.8% | 22.7% | 23.8% | 20.0% | 21.5% | 21.8% | 10.1% | 13.1% | ||||||||||

1992 | 21.3% | 22.3% | 23.2% | 23.1% | 21.6% | 21.5% | 21.5% | 22.2% | 12.5% | 10.8% | ||||||||||

1993 | 21.6% | 22.1% | 21.5% | 22.8% | 21.1% | 22.7% | 21.4% | 22.0% | 14.4% | 10.4% | ||||||||||

1994 | 20.6% | 21.7% | 22.4% | 22.5% | 24.7% | 21.9% | 23.0% | 21.8% | 9.3% | 12.1% | ||||||||||

1995 | 22.9% | 22.9% | 21.2% | 22.4% | 23.1% | 23.1% | 23.1% | 23.3% | 9.7% | 8.4% | ||||||||||

1996 | 22.6% | 22.6% | 21.6% | 21.1% | 22.0% | 22.5% | 21.8% | 22.9% | 12.0% | 10.9% | ||||||||||

1997 | 23.2% | 22.0% | 21.6% | 22.8% | 22.2% | 21.1% | 21.4% | 23.7% | 11.4% | 10.3% | ||||||||||

1998 | 22.4% | 22.7% | 22.9% | 23.4% | 21.3% | 21.1% | 23.5% | 22.5% | 9.9% | 10.4% | ||||||||||

1999 | 22.9% | 23.1% | 22.3% | 22.0% | 22.8% | 22.2% | 23.3% | 22.3% | 8.6% | 10.4% | ||||||||||

2000 | 21.8% | 22.9% | 22.5% | 22.2% | 21.2% | 22.8% | 23.2% | 23.2% | 11.4% | 8.9% | ||||||||||

2001 | 23.5% | 22.9% | 22.0% | 22.2% | 21.4% | 21.8% | 22.5% | 22.7% | 10.5% | 10.4% | ||||||||||

2002 | 21.4% | 23.2% | 22.4% | 22.5% | 24.2% | 22.6% | 21.8% | 23.2% | 10.3% | 8.5% | ||||||||||

2003 | 22.7% | 21.2% | 22.6% | 21.5% | 22.3% | 23.2% | 22.3% | 21.8% | 10.2% | 12.3% | ||||||||||

2004 | 23.9% | 22.6% | 23.0% | 22.2% | 23.2% | 21.8% | 21.0% | 22.9% | 8.8% | 10.5% | ||||||||||

2005 | 20.6% | 22.3% | 23.5% | 22.7% | 21.8% | 22.3% | 24.9% | 23.0% | 9.1% | 9.7% | ||||||||||

2006 | 23.3% | 22.8% | 22.7% | 22.7% | 23.2% | 22.9% | 25.3% | 22.8% | 5.5% | 8.7% | ||||||||||

2007 | 22.6% | 22.1% | 22.8% | 23.0% | 22.5% | 22.1% | 23.0% | 22.6% | 9.1% | 10.2% | ||||||||||

2008 | 22.2% | 21.8% | 24.2% | 21.3% | 22.4% | 22.8% | 21.3% | 21.7% | 10.0% | 12.4% | ||||||||||

2009 | 24.5% | 22.7% | 19.4% | 20.7% | 23.9% | 22.8% | 27.5% | 24.3% | 4.7% | 9.6% | ||||||||||

20106 | 22.8% | 22.1% | 23.0% | 23.0% | 23.4% | 22.8% | 23.5% | 23.1% | 7.3% | 9.1% | ||||||||||

THE FUND WILL NOT TRADE WITH A VIEW TO TRACKING THE DEUTSCHE BANK LIQUID COMMODITY INDEX–OPTIMUM YIELD ENERGY TOTAL RETURN™ OVER TIME.

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND

NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

See accompanying Notes and Legends.

19

All statistics based on data from June 4, 1990 to June 30, 2010.

VARIOUS STATISTICAL MEASURES | DBLCI-OY Energy ER8 | DBLCI-OY Energy TR9 | Goldman Sachs US Energy Total Return10 | |||

Annualized Changes to Index Level11 | 10.5% | 14.6% | 5.8% | |||

Average rolling 3 month daily volatility12 | 23.9% | 23.9% | 29.3% | |||

Sharpe Ratio13 | 0.30 | 0.47 | 0.08 | |||

% of months with positive change14 | 56% | 56% | 53% | |||

Average monthly positive change15 | 6.1% | 6.3% | 7.6% | |||

Average monthly negative change16 | -5.1% | -4.9% | -6.7% | |||

ANNUALIZED INDEX LEVELS17 | DBLCI-OY Energy ER8 | DBLCI-OY Energy TR9 | Goldman Sachs US Energy Total Return10 | |||

1 year | 8.4% | 8.6% | -1.0% | |||

3 year | -5.9% | -4.8% | -14.9% | |||

5 year | -2.0% | 0.5% | -12.3% | |||

7 year | 12.3% | 14.8% | -1.6% | |||

10 year | 11.8% | 14.6% | 0.6% | |||

15 year | 14.0% | 17.9% | 7.4% | |||

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

WHILE THE FUND’S OBJECTIVE IS NOT TO GENERATE PROFIT THROUGH ACTIVE PORTFOLIO MANAGEMENT, BUT IS TO TRACK THE INDEX, BECAUSE THE INDEX WAS ESTABLISHED IN JULY 2006, CERTAIN INFORMATION RELATING TO INDEX CLOSING LEVELS MAY BE CONSIDERED TO BE “HYPOTHETICAL.” HYPOTHETICAL INFORMATION MAY HAVE CERTAIN INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW.

NO REPRESENTATION IS BEING MADE THAT THE INDEX WILL OR IS LIKELY TO ACHIEVE ANNUAL OR CUMULATIVE CLOSING LEVELS CONSISTENT WITH OR SIMILAR TO THOSE SET FORTH HEREIN. SIMILARLY, NO REPRESENTATION IS BEING MADE THAT THE FUND WILL GENERATE PROFITS OR LOSSES SIMILAR TO THE FUND’S PAST PERFORMANCE, WHEN AVAILABLE, OR THE HISTORICAL ANNUAL OR CUMULATIVE CHANGES IN THE INDEX CLOSING LEVELS. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY INVESTMENT METHODOLOGIES, WHETHER ACTIVE OR PASSIVE.

ONE OF THE LIMITATIONS OF HYPOTHETICAL INFORMATION IS THAT IT IS GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. TO THE EXTENT THAT INFORMATION PRESENTED HEREIN RELATES TO THE PERIOD JUNE 1990 THROUGH JUNE 2006, THE INDEX CLOSING LEVELS REFLECT THE APPLICATION OF THE INDEX’S METHODOLOGY, AND SELECTION OF INDEX COMMODITIES, IN HINDSIGHT.

NO HYPOTHETICAL RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THERE ARE NUMEROUS FACTORS, INCLUDING THOSE DESCRIBED UNDER “THE RISKS YOU FACE” HEREIN, RELATED TO THE COMMODITIES MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF THE FUND’S EFFORTS TO TRACK ITS INDEX OVER TIME WHICH CANNOT BE, AND HAVE NOT BEEN, ACCOUNTED FOR IN THE PREPARATION OF SUCH INDEX INFORMATION SET FORTH ON THE FOLLOWING PAGES, ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL PERFORMANCE RESULTS FOR THE FUND. FURTHERMORE, THE INDEX INFORMATION DOES NOT INVOLVE FINANCIAL RISK OR ACCOUNT FOR THE IMPACT OF FEES AND COSTS ASSOCIATED WITH THE FUND.

THE MANAGING OWNER COMMENCED OPERATIONS IN JANUARY 2006. AS MANAGING OWNER, THE MANAGING OWNER AND ITS TRADING PRINCIPALS HAVE BEEN MANAGING THE DAY-TO-DAY OPERATIONS FOR THE FUNDS AND RELATED PRODUCTS AND MANAGING FUTURES TRADING ACCOUNTS. BECAUSE THERE ARE LIMITED ACTUAL TRADING RESULTS TO COMPARE TO THE INDEX CLOSING LEVELS SET FORTH HEREIN, PROSPECTIVE INVESTORS SHOULD BE PARTICULARLY WARY OF PLACING UNDUE RELIANCE ON THE ANNUAL OR CUMULATIVE INDEX RESULTS.

See accompanying Notes and Legends.

20

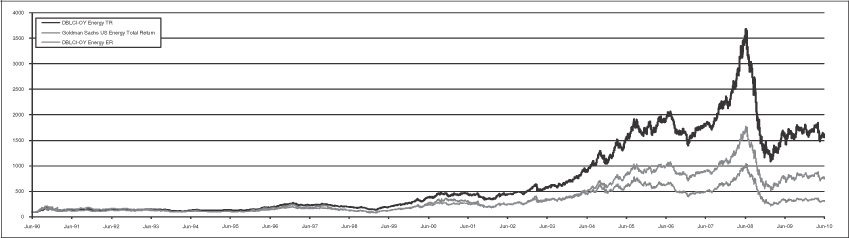

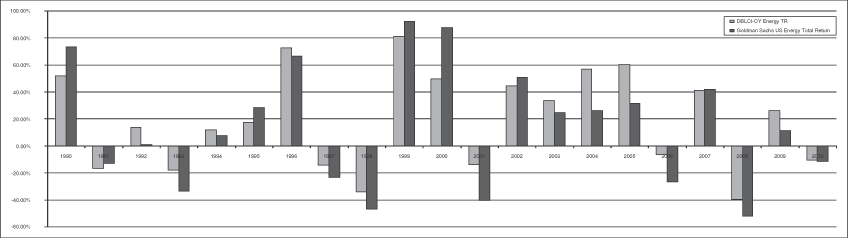

COMPARISON OF DBLCI-OY ENERGY ER, DBLCI-OY ENERGY TR AND GOLDMAN SACHS US ENERGY TOTAL RETURN

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

Each of DBLCI-OY Energy ER, DBLCI-OY Energy TR and Goldman Sachs US Energy Total Return are indices and do not reflect actual trading.

DBLCI-OY Energy TR and Goldman Sachs US Energy Total Return are calculated on a total return basis and do not reflect any fees or expenses.

WHILE THE FUND’S OBJECTIVE IS NOT TO GENERATE PROFIT THROUGH ACTIVE PORTFOLIO MANAGEMENT, BUT IS TO TRACK THE INDEX, BECAUSE THE INDEX WAS ESTABLISHED IN JULY 2006, CERTAIN INFORMATION RELATING TO INDEX CLOSING LEVELS MAY BE CONSIDERED TO BE “HYPOTHETICAL.” HYPOTHETICAL INFORMATION MAY HAVE CERTAIN INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW.

NO REPRESENTATION IS BEING MADE THAT THE INDEX WILL OR IS LIKELY TO ACHIEVE ANNUAL OR CUMULATIVE CLOSING LEVELS CONSISTENT WITH OR SIMILAR TO THOSE SET FORTH HEREIN. SIMILARLY, NO REPRESENTATION IS BEING MADE THAT THE FUND WILL GENERATE PROFITS OR LOSSES SIMILAR TO THE FUND’S PAST PERFORMANCE, WHEN AVAILABLE, OR THE HISTORICAL ANNUAL OR CUMULATIVE CHANGES IN THE INDEX CLOSING LEVELS. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY INVESTMENT METHODOLOGIES, WHETHER ACTIVE OR PASSIVE.

ONE OF THE LIMITATIONS OF HYPOTHETICAL INFORMATION IS THAT IT IS GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. TO THE EXTENT THAT INFORMATION PRESENTED HEREIN RELATES TO THE PERIOD JUNE 1990 THROUGH JUNE 2006, THE INDEX CLOSING LEVELS REFLECT THE APPLICATION OF THE INDEX’S METHODOLOGY, AND SELECTION OF INDEX COMMODITIES, IN HINDSIGHT.

NO HYPOTHETICAL RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THERE ARE NUMEROUS FACTORS, INCLUDING THOSE DESCRIBED UNDER “THE RISKS YOU FACE” HEREIN, RELATED TO THE COMMODITIES MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF THE FUND’S EFFORTS TO TRACK ITS INDEX OVER TIME WHICH CANNOT BE, AND HAVE NOT BEEN, ACCOUNTED FOR IN THE PREPARATION OF SUCH INDEX INFORMATION SET FORTH ON THE FOLLOWING PAGES, ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL PERFORMANCE RESULTS FOR THE FUND. FURTHERMORE, THE INDEX INFORMATION DOES NOT INVOLVE FINANCIAL RISK OR ACCOUNT FOR THE IMPACT OF FEES AND COSTS ASSOCIATED WITH THE FUND.

THE MANAGING OWNER COMMENCED OPERATIONS IN JANUARY 2006. AS MANAGING OWNER, THE MANAGING OWNER AND ITS TRADING PRINCIPALS HAVE BEEN MANAGING THE DAY-TO-DAY OPERATIONS FOR THE FUNDS AND RELATED PRODUCTS AND MANAGING FUTURES TRADING ACCOUNTS. BECAUSE THERE ARE LIMITED ACTUAL TRADING RESULTS TO COMPARE TO THE INDEX CLOSING LEVELS SET FORTH HEREIN, PROSPECTIVE INVESTORS SHOULD BE PARTICULARLY WARY OF PLACING UNDUE RELIANCE ON THE ANNUAL OR CUMULATIVE INDEX RESULTS.

See accompanying Notes and Legends.

21

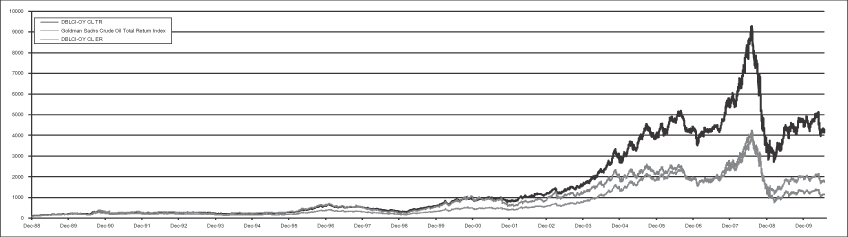

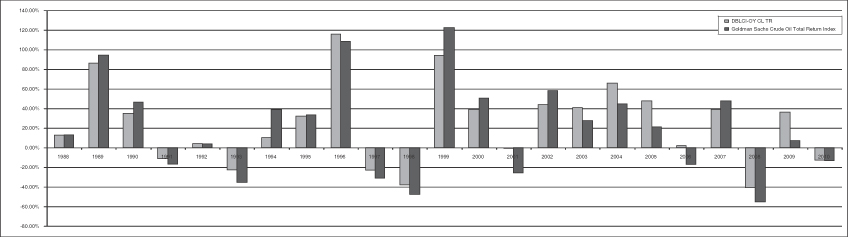

COMPARISON OF DBLCI-OY ENERGY TR AND GOLDMAN SACHS US ENERGY TOTAL RETURN

NEITHER THE PAST PERFORMANCE OF THE FUND NOR THE PRIOR INDEX LEVELS AND CHANGES, POSITIVE AND NEGATIVE, SHOULD BE TAKEN AS AN INDICATION OF THE FUND’S FUTURE PERFORMANCE.

Each of DBLCI-OY Energy TR and Goldman Sachs US Energy Total Return are indices and do not reflect actual trading.

DBLCI-OY Energy TR and Goldman Sachs US Energy Total Return are calculated on a total return basis and do not reflect any fees or expenses.

WHILE THE FUND’S OBJECTIVE IS NOT TO GENERATE PROFIT THROUGH ACTIVE PORTFOLIO MANAGEMENT, BUT IS TO TRACK THE INDEX, BECAUSE THE INDEX WAS ESTABLISHED IN JULY 2006, CERTAIN INFORMATION RELATING TO INDEX CLOSING LEVELS MAY BE CONSIDERED TO BE “HYPOTHETICAL.” HYPOTHETICAL INFORMATION MAY HAVE CERTAIN INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW.

NO REPRESENTATION IS BEING MADE THAT THE INDEX WILL OR IS LIKELY TO ACHIEVE ANNUAL OR CUMULATIVE CLOSING LEVELS CONSISTENT WITH OR SIMILAR TO THOSE SET FORTH HEREIN. SIMILARLY, NO REPRESENTATION IS BEING MADE THAT THE FUND WILL GENERATE PROFITS OR LOSSES SIMILAR TO THE FUND’S PAST PERFORMANCE, WHEN AVAILABLE, OR THE HISTORICAL ANNUAL OR CUMULATIVE CHANGES IN THE INDEX CLOSING LEVELS. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY INVESTMENT METHODOLOGIES, WHETHER ACTIVE OR PASSIVE.

ONE OF THE LIMITATIONS OF HYPOTHETICAL INFORMATION IS THAT IT IS GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. TO THE EXTENT THAT INFORMATION PRESENTED HEREIN RELATES TO THE PERIOD JUNE 1990 THROUGH JUNE 2006, THE INDEX CLOSING LEVELS REFLECT THE APPLICATION OF THE INDEX’S METHODOLOGY, AND SELECTION OF INDEX COMMODITIES, IN HINDSIGHT.

NO HYPOTHETICAL RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THERE ARE NUMEROUS FACTORS, INCLUDING THOSE DESCRIBED UNDER “THE RISKS YOU FACE” HEREIN, RELATED TO THE COMMODITIES MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF THE FUND’S EFFORTS TO TRACK ITS INDEX OVER TIME WHICH CANNOT BE, AND HAVE NOT BEEN, ACCOUNTED FOR IN THE PREPARATION OF SUCH INDEX INFORMATION SET FORTH ON THE FOLLOWING PAGES, ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL PERFORMANCE RESULTS FOR THE FUND. FURTHERMORE, THE INDEX INFORMATION DOES NOT INVOLVE FINANCIAL RISK OR ACCOUNT FOR THE IMPACT OF FEES AND COSTS ASSOCIATED WITH THE FUND.

THE MANAGING OWNER COMMENCED OPERATIONS IN JANUARY 2006. AS MANAGING OWNER, THE MANAGING OWNER AND ITS TRADING PRINCIPALS HAVE BEEN MANAGING THE DAY-TO-DAY OPERATIONS FOR THE FUNDS AND RELATED PRODUCTS AND MANAGING FUTURES TRADING ACCOUNTS. BECAUSE THERE ARE LIMITED ACTUAL TRADING RESULTS TO COMPARE TO THE INDEX CLOSING LEVELS SET FORTH HEREIN, PROSPECTIVE INVESTORS SHOULD BE PARTICULARLY WARY OF PLACING UNDUE RELIANCE ON THE ANNUAL OR CUMULATIVE INDEX RESULTS.

See accompanying Notes and Legends.

22

NOTES AND LEGENDS:

| 1. | “High” reflects the highest closing level of the Index during the applicable year. |

| 2. | “Low” reflects the lowest closing level of the Index during the applicable year. |