| COPSYNC, INC. |

| (A Development Stage Company) |

| Balance Sheets (Continued) |

| | | | | | | |

| LIABILITIES AND STOCKHOLDERS' EQUITY | |

| | | | | | | |

| | | September 30, | | | December 31, | |

| | | 2008 | | | 2007 | |

| | | (Unaudited) | | | | |

| CURRENT LIABILITIES | | | | | | |

| | | | | | | |

| Accounts payable and accrued expenses | | $ | 51,890 | | | $ | 58,015 | |

| Notes payable - related parties | | | - | | | | 33,000 | |

| Convertible notes payable | | | 420,000 | | | | - | |

| Stock deposits | | | 607,345 | | | | - | |

| Notes payable, current portion | | | 7,269 | | | | 6,864 | |

| | | | | | | | | |

| Total Current Liabilities | | | 1,086,504 | | | | 97,879 | |

| | | | | | | | | |

| LONG-TERM LIABILITIES | | | | | | | | |

| | | | | | | | | |

| Notes payable | | | 26,610 | | | | 32,824 | |

| | | | | | | | | |

| Total Long-Term Liabilities | | | 26,610 | | | | 32,824 | |

| | | | | | | | | |

| Total Liabilities | | | 1,113,114 | | | | 130,703 | |

| | | | | | | | | |

| COMMITMENTS AND CONTINGENCIES | | | | | | | | |

| | | | | | | | | |

| STOCKHOLDERS' EQUITY | | | | | | | | |

| | | | | | | | | |

| Series A Preferred stock, par value $0.0001 per share, | | | | | | | | |

| 1,000,000 shares authorized; 100,000 shares issued | | | | | | | | |

| and outstanding | | | 10 | | | | 10 | |

| Common stock, par value $0.0001 per share, | | | | | | | | |

| 500,000,000 shares authorized; 44,132,935 shares | | | | | | | | |

| and 25,000,005 issued and outstanding, respectively | | | 4,413 | | | | 2,500 | |

| Additional paid-in-capital | | | 2,872,818 | | | | 2,604,643 | |

| Deficit accumulated during the development stage | | | (1,793,270 | ) | | | (1,012,473 | ) |

| | | | | | | | | |

| Total Stockholders' Equity | | | 1,083,971 | | | | 1,594,680 | |

| | | | | | | | | |

| TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY | | $ | 2,197,085 | | | $ | 1,725,383 | |

| | | | | | | | | |

| | | | | | |

The accompanying notes are an integral part of these financial statements.

| COPSYNC, INC. |

| (A Development Stage Company) |

|

| (Unaudited) |

| | | | | | | | | | | | | | | | |

| | | For the | | | For the | | | | |

| | | Three Months Ended | | | Nine Months Ended | | | Cumulative | |

| | | September 30, | | | September 30, | | | From | |

| | | 2008 | | | 2007 | | | 2008 | | | 2007 | | | Inception | |

| | | | | | | | | | | | | | | | |

| REVENUES | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| License fee revenue | | $ | 6,450 | | | $ | - | | | $ | 6,450 | | | $ | - | | | $ | 6,450 | |

| Cost of license fee revenue | | | (5,578 | ) | | | - | | | | (5,578 | ) | | | - | | | | (5,578 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Net Revenues | | | 872 | | | | - | | | | 872 | | | | - | | | | 872 | |

| | | | | | | | | | | | | | | | | | | | | |

| OPERATING EXPENSES | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Depreciation and amortization | | | 52,183 | | | | 2,858 | | | | 63,615 | | | | 8,574 | | | | 112,606 | |

| Professional fees | | | 32,124 | | | | - | | | | 66,122 | | | | 2,560 | | | | 112,584 | |

| Salaries and wages | | | 190,310 | | | | 166,035 | | | | 512,199 | | | | 396,626 | | | | 1,197,012 | |

| Patent costs | | | - | | | | - | | | | 15,560 | | | | - | | | | 15,560 | |

| Other general and administrative | | | 7,874 | | | | 28,044 | | | | 122,783 | | | | 109,832 | | | | 378,712 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Operating Expenses | | | 282,491 | | | | 196,937 | | | | 780,279 | | | | 517,592 | | | | 1,816,474 | |

| | | | | | | | | | | | | | | | | | | | | |

| LOSS BEFORE OTHER INCOME (EXPENSE) | | | (281,619 | ) | | | (196,937 | ) | | | (779,407 | ) | | | (517,592 | ) | | | (1,815,602 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| OTHER INCOME (EXPENSE) | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Interest income | | | - | | | | 121 | | | | - | | | | 371 | | | | 16,427 | |

| Other income | | | - | | | | - | | | | - | | | | - | | | | 7,801 | |

| Interest expense | | | - | | | | - | | | | (1,390 | ) | | | - | | | | (1,896 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Total Other Income (Expense) | | | - | | | | 121 | | | | (1,390 | ) | | | 371 | | | | 22,332 | |

| | | | | | | | | | | | | | | | | | | | | |

| NET LOSS | | $ | (281,619 | ) | | $ | (196,816 | ) | | $ | (780,797 | ) | | $ | (517,221 | ) | | $ | (1,793,270 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| LOSS PER COMMON SHARE - BASIC & DILUTED | | $ | (0.01 | ) | | $ | (0.01 | ) | | $ | (0.02 | ) | | $ | (0.02 | ) | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| WEIGHTED AVERAGE NUMBER OF | | | | | | | | | | | | | | | | | | | | |

| COMMON SHARES OUTSTANDING | | | 44,124,547 | | | | 25,000,005 | | | | 35,844,167 | | | | 25,000,005 | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

| COPSYNC, INC. |

| (A Development Stage Company) |

|

| | | | | | | | | | |

| | | For the | | | | |

| | | Nine Months Ended | | | Cumulative | |

| | | September 30, | | | From | |

| | | 2008 | | | 2007 | | | Inception | |

| | | | | | | | | | |

| CASH FLOWS FROM OPERATING ACTIVITIES | | | | | | | | | |

| | | | | | | | | | |

| Net loss | | $ | (780,797 | ) | | $ | (517,221 | ) | | $ | (1,793,270 | ) |

| Adjustments to reconcile net loss to net cash used | | | | | | | | | | | | |

| in operating activities: | | | | | | | | | | | | |

| Depreciation and amortization | | | 63,615 | | | | 8,574 | | | | 112,606 | |

| Write-off of patent costs | | | 15,560 | | | | - | �� | | | 15,560 | |

| Transfer agent fees paid by issued shares | | | - | | | | - | | | | 2,000 | |

| Change in operating assets and liabilities: | | | | | | | | | | | | |

| Lease security deposit | | | - | | | | - | | | | 4,285 | |

| License fees receivable | | | (6,450 | ) | | | - | | | | (6,450 | ) |

| Accounts payable and accrued expenses | | | (6,125 | ) | | | 14,711 | | | | 46,855 | |

| | | | | | | | | | | | | |

| Net Cash Used in Operating Activities | | | (714,197 | ) | | | (493,936 | ) | | | (1,618,414 | ) |

| | | | | | | | | | | | | |

| CASH FLOWS FROM INVESTING ACTIVITIES | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Software development costs | | | - | | | | - | | | | (660,679 | ) |

| Acquisition and cost of patent pending | | | - | | | | - | | | | (15,560 | ) |

| Employee advances | | | (500 | ) | | | - | | | | (500 | ) |

| Purchases of property and equipment | | | (817 | ) | | | (7,214 | ) | | | (88,774 | ) |

| | | | | | | | | | | | | |

| Net Cash Used in Investing Activities | | | (1,317 | ) | | | (7,214 | ) | | | (765,513 | ) |

| | | | | | | | | | | | | |

| CASH FLOWS FROM FINANCING ACTIVITIES | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Issuance of common stock for cash | | | - | | | | 448,819 | | | | 99,888 | |

| Payments on notes payable | | | (5,809 | ) | | | - | | | | 1,565,738 | |

| Partner contribution | | | - | | | | - | | | | 33,000 | |

| Deferred offering costs | | | - | | | | - | | | | (33,250 | ) |

| Payments on loans from related parties - directors and | | | | | | | | | | | | |

| stockholders | | | (15,000 | ) | | | - | | | | (15,000 | ) |

| Proceeds received on convertible notes | | | 672,088 | | | | - | | | | 672,088 | |

| Stock deposits received | | | 607,345 | | | | - | | | | 607,345 | |

| Loans from related parties - Former directors and | | | | | | | | | | | | |

| stockholders | | | - | | | | - | | | | 39,800 | |

| Payment of loans from related parties - former directors | | | | | | | | | | | | |

| and stockholders | | | - | | | | - | | | | (39,800 | ) |

| Loan from third-party entity related to consultant | | | - | | | | - | | | | 15,000 | |

| Repayment of loan from third-party entity related to consultant | | | - | | | | - | | | | (15,000 | ) |

| | | | | | | | | | | | | |

| Net Cash Provided by Financing Activities | | | 1,258,624 | | | | 448,819 | | | | 2,929,809 | |

| | | | | | | | | | | | | |

| NET INCREASE (DECREASE) IN CASH AND CASH | | | | | | | | | | | | |

| EQUIVALENTS | | | 543,110 | | | | (52,331 | ) | | | 545,882 | |

| | | | | | | | | | | | | |

| CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD | | | 2,772 | | | | 96,866 | | | | - | |

| | | | | | | | | | | | | |

| CASH AND CASH EQUIVALENTS, END OF PERIOD | | $ | 545,882 | | | $ | 44,535 | | | $ | 545,882 | |

| | | | | | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

| COPSYNC, INC. |

| (A Development Stage Company) |

| Statements of Cash Flows (Continued) |

| | | | | | | | | | |

| | | For the | | | | |

| | | Nine Months Ended | | | Cumulative | |

| | | September 30, | | | From | |

| | | 2008 | | | 2007 | | | Inception | |

| SUPPLEMENTAL DISCLOSURES: | | | | | | | | | |

| | | | | | | | | | |

| Cash paid for interest | | $ | - | | | $ | - | | | $ | - | |

| Cash paid for taxes | | $ | - | | | $ | - | | | $ | - | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| NON-CASH INVESTING AND FINANCING ACTIVITIES: | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Purchase of fleet vehicles financed by notes payable | | $ | - | | | $ | - | | | $ | 40,000 | |

| Contribution of services - capitalized to software | | | | | | | | | | | | |

| development costs | | $ | - | | | $ | - | | | $ | 966,656 | |

| Common stock issued in lieu of convertible notes payable | | $ | 270,088 | | | $ | - | | | $ | 270,088 | |

| | | | | | | | | | | | | |

| | | | | | | | | | |

The accompanying notes are an integral part of these financial statements.

COPSYNC, INC.

(A Development Stage Company)

September 30, 2008 and December 31, 2007

NOTE 1 - - BASIS OF FINANCIAL STATEMENT PRESENTATION

The accompanying unaudited condensed financial statements have been prepared by the Company pursuant to the rules and regulations of the Securities and Exchange Commission. Certain information and footnote disclosures normally included in financial statements prepared in accordance with generally accepted accounting principles have been condensed or omitted in accordance with such rules and regulations. The information furnished in the interim condensed financial statements includes normal recurring adjustments and reflects all adjustments, which, in the opinion of management, are necessary for a fair presentation of such financial statements. Operating results for the nine months ended September 30, 2008 are not necessarily indicative of the results that may be expected for the year ending December 31, 2008.

COPsync, Inc. (formerly, Global Advance Corporation) (the “Company”), is currently in the development stage. On March 20, 2008, the stockholders of the Company approved an amendment of the Articles of Incorporation to change its name from Global Advance Corporation to COPsync, Inc. This amendment was filed on April 24, 2008.

As more fully described in Note 4, the Company entered into a share exchange agreement with PostInk Technology, LP, by and among PostInk Technology, LP and RSIV, LLC (collectively “PostInk”) for 100% interest in PostInk. The shares issued in the acquisition resulted in the owners of PostInk having operating control of the Company immediately following the acquisition. Therefore, this acquisition has been accounted for in the accompanying financial statements as a reverse acquisition. Therefore, these financial statements represent the continuation of PostInk, not COPsync, Inc. (formerly, Global Advance Corp.), the legal survivor. PostInk is treated as the survivor for accounting purposes and COPsync, Inc. is the survivor for legal purposes. The historical financial statements presented are those of PostInk rather than COPsync, Inc.

NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES | |

Revenue Recognition

The Company is in the development stage and just recently begun to realize licensing revenues from operations. Licensing revenues are recorded monthly, over the life of the licensing agreement.

Loss Per Share

The computation of loss per common share is based on the weighted average number of shares outstanding during the period plus the common stock equivalents which would arise from the exercise of stock options and warrants outstanding using the treasury stock method and the average market price per share during the period. Common stock equivalents, consisting of 75,000,000 warrants as of September 30, 2008, are not included in the below calculations since they are anti-dilutive for the periods presented.

COPSYNC, INC.

(A Development Stage Company)

Notes to the Financial Statements

September 30, 2008 and December 31, 2007

| NOTE 2 - SIGNIFICANT ACCOUNTING POLICIES (Continued) | |

Loss Per Share (Continued)

Following is a reconciliation of the loss per share for the three months and nine months ended September 30, 2008 and 2007:

| | | For the | |

| | | Three Months ended | |

| | | September 30, | |

| | | 2008 | | | 2007 | |

| Net (loss) available to common shareholders | | $ | (281,619 | ) | | $ | (196,816 | ) |

| Weighted average shares | | | 44,124,547 | | | | 25,000,005 | |

| Basic and fully diluted loss per share (based on weighted average shares) | | $ | (0.01 | ) | | $ | (0.01 | ) |

| | | For the | |

| | | Nine Months Ended | |

| | | September 30, | |

| | | 2008 | | | 2007 | |

| Net (loss) available to common shareholders | | $ | (780,797 | ) | | $ | (517,221 | ) |

| Weighted average shares | | | 35,844,167 | | | | 25,000,005 | |

| Basic and fully diluted loss per share (based on weighted average shares) | | $ | (0.02 | ) | | $ | (0.02 | ) |

| | | | | | | | | |

Income Taxes

The Company accounts for income taxes pursuant to SFAS No. 109, “Accounting for Income Taxes” (“SFAS No. 109”). Under SFAS No. 109, deferred tax assets and liabilities are determined based on temporary differences between the bases of certain assets and liabilities for income tax and financial reporting purposes. The deferred tax assets and liabilities are classified according to the financial statement classification of the assets and liabilities generating the differences. The Company maintains a valuation allowance with respect to deferred tax assets.

The Company establishes a valuation allowance based upon the potential likelihood of realizing the deferred tax asset and taking into consideration the Company’s financial position and results of operations for the current period. Future realization of the deferred tax benefit depends on the existence of sufficient taxable income within the carryforward period under the Federal tax laws.

Changes in circumstances, such as the Company generating taxable income, could cause a change in judgment about the realizability of the related deferred tax asset. Any change in the valuation allowance will be included in income in the year of the change in estimate.

COPSYNC, INC.

(A Development Stage Company)

Notes to the Financial Statements

September 30, 2008 and December 31, 2007

NOTE 2 - - SIGNIFICANT ACCOUNTING POLICIES (Continued)

Software Development Costs

The Company capitalizes software development costs in accordance with Statement of Financial Accounting Standards No. 86, “Accounting for Costs of Computer Software to be Sold, Leased or Otherwise Marketed,” under which certain software development costs incurred subsequent to the establishment of technological feasibility may be capitalized and amortized over the estimated lives of the related products.

The Company determines technological feasibility to be established upon completion of (1) product design, (2) detail program design, (3) consistency between product and program design, and (4) review of detail program design to ensure that high risk development issues have been resolved. Upon the general release of the product to customers, development costs for that product are amortized over periods not exceeding three years, based on the estimated economic life of the product. Capitalized software development costs amounted to $1,627,335 as of September 30, 2008 and December 31, 2007. These costs are being amortized, effective September 1, 2008, the date that revenue generating activities commenced. During the year ended December 31, 2006, and during the period from inception on October 23, 2005, through December 31, 2005, various partners contributed services of $483,328, which were capitalized to software development costs.

The Company is currently in the development stage, and has had minimal operations. Originally, the business plan of the Company was to develop a commercial application of a prototype utilizing the design in a patent pending of a “two-foot operated mouse” which is a device intended to provide alternate access to all computer-related mouse functionality through the use of one’s feet, rather than one’s hands. However, during the current year, the Company discontinued this business plan to focus on developing software that will not only enhance productivity and quality of work, but creates a safer work environment for the public safety community by developing the first real-time, nationwide public safety information sharing network.

The accompanying financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which contemplate continuation of the Company as a going concern. The Company has not currently established revenues significant enough to cover its operating costs, and as such, has incurred an operating loss since inception. Further, as of September 30, 2008, the cash resources of the Company were insufficient to meet its current business plan, and the Company had negative working capital. These and other factors raise substantial doubt about the Company’s ability to continue as a going concern. The accompanying financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result from the possible inability of the Company to continue as a going concern.

COPSYNC, INC.

(A Development Stage Company)

Notes to the Financial Statements

September 30, 2008 and December 31, 2007

NOTE 4 - - SIGNIFICANT EVENTS

Stock Issuances

During the three months ended September 30, 2008, the Company issued a total of 771,680 shares of its common stock in lieu of outstanding convertible debt totaling $270,088, or $0.35 per share.

Share Exchange Agreement with PostInk Technology, LP

Effective April 25, 2008, the Company entered into a share exchange agreement (Agreement) with PostInk Technology, LP, by and among PostInk Technology, LP and RSIV, LLC (collectively “PostInk”) for 100% interest in PostInk. Upon the closing date, the Company issued 25,000,005 shares (post forward stock split) of its common stock and 100,000 shares of its Series A Preferred Shares in exchange for 100% of PostInk. The Company also cancelled 29,388,750 shares (post forward stock split) of its common stock. The Company and PostInk also agreed to issue cashless warrants exercisable at $0.01 per share to PostInk shareholders for 75,000,000 shares (post forward stock split) of the Company’s common stock.

On April 17, 2008, the Company amended its Articles of Incorporation to increase its authorized shares from 50,000,000 to 500,000,000, implement a 15-for-1 forward stock split, and authorize 1,000,000 Series A Preferred Stock, par value $0.0001. The accompanying financial statements and related notes thereto have been adjusted accordingly to reflect this forward stock split.

The shares issued in the acquisition resulted in the owners of PostInk having operating control of the Company immediately following the acquisition. Therefore, this acquisition has been accounted for in the accompanying financial statements as a reverse acquisition.

As a result of this transaction, the former shareholders of PostInk acquired or exercised control over a majority of the Company’s shares. Accordingly, the transaction has been treated for accounting purposes as a recapitalization of PostInk; therefore, these financial statements represent a continuation of PostInk, not COPsync, Inc. (formerly, Global Advance Corp.), the legal survivor. PostInk is treated as the survivor for accounting purposes and COPsync, Inc. is the survivor for legal purposes. The historical financial statements presented are those of PostInk rather than COPsync, Inc.

NOTE 5 - - SUBSEQUENT EVENTS

Subsequent to September 30, 2008, the Company issued the following shares of its outstanding common stock:

| - | During October 2008, the Company issued a total of 1,767,000 shares of common stock pursuant to various private placements at $0.40 per share. The cash proceeds of $706,800 had been received by the Company prior to September 30, 2008 (recorded as a stock deposit), less stock offering costs of $99,455, for total proceeds to the Company of $607,345. |

COPSYNC, INC.

(A Development Stage Company)

Notes to the Financial Statements

September 30, 2008 and December 31, 2007

NOTE 5 - - SUBSEQUENT EVENTS (Continued)

| - | During November 2008, the Company issued a total of 74,423,069 shares of common stock in exercise of cashless warrants, issued pursuant to the share exchange agreement with PostInk Technology, LP, as previously discussed. |

(1) Summary of Significant Accounting Policies

Basis of Presentation and Organization

COPsync, Inc. (formerly Global Advance Corporation) (“COPsync” or the “Company”) is a Delaware corporation in the development stage and has not commenced operations. COPsync was incorporated under the laws of the State of Delaware on October 23, 2006. On March 20, 2008, the stockholders of COPsync approved an amendment of the Articles of Incorporation to change its name from Global Advance Corporation to COPsync, Inc. This amendment was filed on April 24, 2008. On March 24, 2008, COPsync entered into a Letter of Intent with PostInk Technology, LP (“PostInk”), a Texas partnership, pursuant to which COPsync agreed to acquire 100 percent of PostInk in exchange for 100,000,000 shares (post forward stock split) of common stock of COPsync. Originally, the business plan of COPsync was to develop a commercial application of a prototype utilizing the design in a patent pending of a “two-foot operated mouse” which is a device intended to provide alternate access to all computer-related mouse functionality through the use of one’s feet, rather than one’s hands. However, as of September 30, 2008, the COPsync discontinued this business plan to focus on developing software that will not only enhance productivity and quality of work, but creates a safer work environment for the public safety community by developing the first real-time, nationwide public safety information sharing network. The accompanying financial statements of COPsync were prepared from the accounts of COPsync under the accrual basis of accounting.

COPsync commenced a capital formation activity to submit a Registration Statement on Form SB-2 to the Securities and Exchange Commissions to register and sell in a self-directed offering 15.0 million shares (post forward stock split) of newly issued common stock at an offering price of $0.01 for proceeds of up to $100,000. On January 30, 2007, COPsync completed the preparation of its registration document, and filed it with the SEC. The Registration Statement was declared effective on April 13, 2007. As of December 31, 2007, COPsync completed the offering, received stock subscriptions for 15.0 million shares (post forward stock split) of common stock, par value $0.0001 per share, at an offering price of $0.01 per share, and deposited proceeds of $100,000.

On November 21, 2007, COPsync entered into a stock purchase agreement (the “Stock Purchase Agreement”) with Rocky Global Enterprises Ltd. and Beaux Beaux Partnership (the “Buyers”), and Oren Rozenberg and Judah Steinberger (the “Sellers”). Pursuant to the terms and conditions of the Stock Purchase Agreement, the Buyers acquired from the Sellers 29,013,750 shares (post forward stock split) of common stock of COPsync. This event triggered a change in control of COPsync, with the Buyers owning approximately 64% of the issued and outstanding shares of common stock of COPsync. Immediately prior to the closing of this transaction, Oren Rozenberg and Judah Steinberger served as the members of the Board of Directors. Pursuant to the terms and conditions set forth in the Stock Purchase Agreement, immediately following the closing of the transaction, Judah Steinberger resigned as Chief Financial Officer, Secretary, and from the Board of Directors; Oren Rozenberg tendered a resignation from the Board of Directors and as Chief Executive Officer; and the parties agreed to appoint the Buyer’s nominee, Krystal Rocha, to the Board of Directors and as Chief Executive Officer, Chief Financial Officer, and Secretary.

Unaudited Interim Financial Statements

COPsync’s interim financial statements as of September 30, 2008, and for the six months ended September 30, 2008, and 2007, and cumulative from inception are unaudited. However, in the opinion of management, the interim financial statements include all adjustments, consisting only of normal recurring adjustments, necessary to present fairly COPsync’s financial position as of September 30, 2008, and the results of its operations and its cash flows for the six months ended September 30, 2008, and 2007, and cumulative from inception. These results are not necessarily indicative of the results expected for the calendar year ending December 31, 2008. The accompanying financial statements and notes thereto do not reflect all disclosures required under accounting principles generally accepted in the United States. Refer to COPsync’s audited financial statements contained in its 10-KSB as of December 31, 2007, for additional information, including significant accounting policies.

Cash and Cash Equivalents

For purposes of reporting within the statement of cash flows, COPsync considers all cash on hand, cash accounts not subject to withdrawal restrictions or penalties, and all highly liquid debt instruments purchased with a maturity of three months or less to be cash and cash equivalents.

Revenue Recognition

COPsync is in the development stage and has yet to realize revenues from operations. Once COPsync has commenced operations, it will recognize revenues when delivery of goods or completion of services has occurred provided there is persuasive evidence of an agreement, acceptance has been approved by its customers, the fee is fixed or determinable based on the completion of stated terms and conditions, and collection of any related receivable is probable.

Loss per Common Share

Basic loss per share is computed by dividing the net loss attributable to the common stockholders by the weighted average number of shares of common stock outstanding during the period. Diluted loss per share is computed similar to basic loss per share except that the denominator is increased to include the number of additional common shares that would have been outstanding if the potential common shares had been issued and if the additional common shares were dilutive. There were no dilutive financial instruments issued or outstanding for the six months ended September 30, 2008, and 2007.

Income Taxes

COPsync accounts for income taxes pursuant to SFAS No. 109, “Accounting for Income Taxes” (“SFAS No. 109”). Under SFAS No. 109, deferred tax assets and liabilities are determined based on temporary differences between the bases of certain assets and liabilities for income tax and financial reporting purposes. The deferred tax assets and liabilities are classified according to the financial statement classification of the assets and liabilities generating the differences.

COPsync maintains a valuation allowance with respect to deferred tax assets. COPsync establishes a valuation allowance based upon the potential likelihood of realizing the deferred tax asset and taking into consideration COPsync’s financial position and results of operations for the current period. Future realization of the deferred tax benefit depends on the existence of sufficient taxable income within the carryforward period under the Federal tax laws.

Changes in circumstances, such as COPsync generating taxable income, could cause a change in judgment about the realizability of the related deferred tax asset. Any change in the valuation allowance will be included in income in the year of the change in estimate.

Fair Value of Financial Instruments

COPsync estimates the fair value of financial instruments using the available market information and valuation methods. Considerable judgment is required in estimating fair value. Accordingly, the estimates of fair value may not be indicative of the amounts COPsync could realize in a current market exchange. As of September 30, 2008, and 2007, the carrying value of accrued liabilities and accounts payable approximated fair value due to the short-term nature and maturity of these instruments.

Property and Equipment

Property and equipment is stated at cost. Expenditures that materially increase useful lives are capitalized, while ordinary maintenance and repairs are expensed as incurred. Depreciation is computed using the straight-line method over the estimated useful lives of the respective assets, ranging as follows:

Computer hardware 3 years

Computer software 3 years

Fleet vehicles 5 years

Furniture and fixtures 5-7 years

Depreciation expense on property and equipment was $11,432 and $5,716 for the six months ended September 30, 2008, and 2007, respectively.

Software Development Costs

The Company capitalizes software development costs in accordance with Statement of Financial Accounting Standards No. 86, “Accounting for Costs of Computer Software to be Sold, Leased or Otherwise Marketed,” under which certain software development costs incurred subsequent to the establishment of technological feasibility may be capitalized and amortized over the estimated lives of the related products. The Company determines technological feasibility to be established upon completion of (1) product design, (2) detail program design, (3) consistency between product and program design, and (4) review of detail program design to ensure that high risk development issues have been resolved. Upon the general release of the product to customers, development costs for that product are amortized over periods not exceeding three years, based on the estimated economic life of the product. Capitalized software development costs amounted to $1,627,335 as of September 30, 2008, and December 31, 2007. These costs have not yet been amortized because revenue generating activities have not yet commenced. During the year ended December 31, 2006, and during the period from inception on October 23, 2006, through December 31, 2005, various partners contributed services of $483,328, which were capitalized to software development costs.

Patent and Intellectual Property

COPsync capitalizes the costs associated with obtaining a Patent or other intellectual property pertaining to its intended business plan. Such costs are amortized over the estimated useful lives of the related assets.

Deferred Offering Costs

COPsync defers as other assets the direct incremental costs of raising capital until such time as the offering is completed. At the time of the completion of the offering, the costs are charged against the capital raised. Should the offering be terminated, deferred offering costs are charged to operations during the period in which the offering is terminated. For the year ended December 31, 2007, $33,250 in deferred offering costs were charged against the capital raised from the completion of an offering of common stock.

Impairment of Long-Lived Assets

COPsync evaluates the recoverability of long-lived assets and the related estimated remaining lives when events or circumstances lead management to believe that the carrying value of an asset may not be recoverable. For the six months ended September 30, 2008, and 2007, no events or circumstances occurred for which an evaluation of the recoverability of long-lived assets was required.

Common Stock Registration Expenses

COPsync considers incremental costs and expenses related to the registration of equity securities with the SEC, whether by contractual arrangement as of a certain date or by demand, to be unrelated to original issuance transactions. As such, subsequent registration costs and expenses are expensed as incurred.

Estimates

The financial statements are prepared on the basis of accounting principles generally accepted in the United States. The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities as of September 30, 2008, and expenses for the three months ended September 30, 2008, and 2007, and cumulative from inception. Actual results could differ from those estimates made by management.

(2) Development Stage Activities and Going Concern

COPsync is currently in the development stage, and has no operations. Originally, the business plan of COPsync was to develop a commercial application of a prototype utilizing the design in a patent pending of a “two-foot operated mouse” which is a device intended to provide alternate access to all computer-related mouse functionality through the use of one’s feet, rather than one’s hands. However, as of September 30, 2008, the COPsync discontinued this business plan to focus on developing software that will not only enhance productivity and quality of work, but creates a safer work environment for the public safety community by developing the first real-time, nationwide public safety information sharing network.

On November 28, 2006, COPsync entered into an Invention Assignment Agreement (“Invention Agreement”) with IdeaPlus Ltd. (“IdeaPlus”), an Israeli company located in Ramat Gan, Israel, whereby COPsync acquired from IdeaPlus all of the right, title and interest in the invention known as the “Two-foot Operated Mouse” (the “Invention”) for consideration of $10,000. Subsequently, the invention became the subject of United States Patent Application 11/614,150 which was filed with the United States Patent and Trademark Office on December 21, 2006. As of September 30, 2008, the Company discontinued the patent and expensed it in the current period.

COPsync commenced a capital formation activity to submit a Registration Statement on Form SB-2 to the SEC to register and sell in a self-directed offering 15.0 million shares (post forward stock split) of newly issued common stock at an offering price of $0.01 for proceeds of up to $100,000. On January 30, 2007, COPsync completed the preparation of its registration document, and filed it with the SEC. The Registration Statement was declared effective on April 13, 2007. As of December 31, 2007, COPsync completed the offering, received stock subscriptions for 15.0 million shares (post forward stock split) of common stock, par value $0.0001 per share, at an offering price of $0.01 per share, and deposited proceeds of $100,000.

The accompanying financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which contemplate continuation of COPsync as a going concern. COPsync has not established any source of revenue to cover its operating costs, and as such, has incurred an operating loss since inception. Further, as of September 30, 2008, the cash resources of COPsync were insufficient to meet its current business plan, and COPsync had negative working capital. These and other factors raise substantial doubt about COPsync’s ability to continue as a going concern. The accompanying financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result from the possible inability of COPsync to continue as a going concern.

(3) Patent Pending

On November 28, 2006, COPsync entered into an Invention Agreement with IdeaPlus, an Israeli company located in Ramat Gan, Israel, whereby COPsync acquired from IdeaPlus all of the right, title and interest in the invention known as the Invention for consideration of $10,000. Under the terms of the Invention Agreement, COPsync was assigned rights to the Invention free of any liens, claims, royalties, licenses, security interests, or other encumbrances. IdeaPlus initially obtained the Invention directly from the inventor. Neither IdeaPlus nor the inventor of the Invention is an officer or director of COPsync, or an investor or promoter of such. Subsequently, the Invention became the subject of United States Patent Application 11/614,150 which was filed with the United States Patent and Trademark Office on December 21, 2006. The historical cost of obtaining the Invention and filing for the patent has been capitalized by COPsync, and amounted to $15,560. As of September 30, 2008, the Company discontinued the patent and expensed it in the current period.

(4) Loans from Related Parties

During the year ended December 31, 2007, loans from related parties – former Directors and stockholders, representing working capital advances from two former Directors who are also stockholders of COPsync, amounting to $39,800, were paid in full.

As of September 30, 2008, the Chief Executive Officer loaned the company $18,000 and paid expenses on the Company’s behalf of $6,409. As of September 30, 2008, the Company owed this officer $24,409.

(5) Common Stock

On December 22, 2006, COPsync issued 30,000,000 shares (post forward stock split) of its common stock to two individuals who are former directors and officers for proceeds of $200.

Pursuant to the Consulting Agreement entered into on April 18, 2007, with Island Capital Management, LLC dba Island Stock Transfer (“Island Stock Transfer”), on April 19, 2007, COPsync issued 375,000 shares (post forward stock split) of its common stock to Island Stock Transfer as payment for services valued at $2,000.

COPsync commenced a capital formation activity to submit a Registration Statement on Form SB-2 to the SEC to register and sell in a self-directed offering 15.0 million shares (post forward stock split) of newly issued common stock at an offering price of $0.01 for proceeds of up to $100,000. On January 30, 2007, COPsync completed the preparation of its registration document, and filed it with the SEC. The Registration Statement was declared effective on April 13, 2007. As of December 31, 2007, COPsync completed the offering, received stock subscriptions for 15.0 million shares (post forward stock split) of common stock, par value $0.0001 per share, at an offering price of $0.01 per share, and deposited proceeds of $100,000. In addition, during the year ended December 31, 2007, COPsync recognized as an offset to the proceeds from the offering of common stock $33,500 of deferred offering costs.

On April 25, 2008, COPsync entered into a share exchange agreement and a plan of Share Exchange with PostInk Technology LP (“PostInk”) (the “Share Exchange Agreement”) by and among PostInk Technology, LP and RSIV, LLC (collectively “POST”) for 100% interest of POST. Upon closing date, COPsync issued 25,000,005 shares (post forward stock split) of its common stock and 100,000 shares of its Series A Preferred Shares in exchange for 100% of POST. COPsync also cancelled 27,388,750 shares (post forward stock split) of its common stock. COPsync and POST also agree to issue cashless warrants exercisable at $0.01 per share to POST shareholders for 75,000,000 shares (post forward stock split) of COPsync’s common stock.

On April 17, 2008, COPsync amended its Articles of Incorporation to increase its authorized shares from 50,000,000 to 500,000,000, implement a 15-for-1 forward stock split, and authorize 1,000,000 Series A Preferred Stock, par value $0.001. The accompanying financial statements and related notes thereto have been adjusted accordingly to reflect this forward stock split.

(6) Change in Officers and Directors

As discussed in Notes 1 and 5, and pursuant to the terms and conditions set forth in the Stock Purchase Agreement, Judah Steinberger resigned as Chief Financial Officer, Secretary, and from the Board of Directors; Oren Rozenberg tendered a resignation from the Board of Directors and as Chief Executive Officer; and Krystal Rocha was appointed as Chairman of the Board of Directors, Chief Executive Officer, Chief Financial Officer, and Secretary.

On April 18, 2008, COPsync resolved to appoint Russell Chaney as Chief Executive Officer, Chief Financial Officer, Director, and Chairman of the Board of Directors. It was also resolved to appoint Shane Rapp as President, Secretary, and Director. On said date, Krystal Rocha tendered her resignation as Chairman of the Board of Directors, Chief Executive Officer, Chief Financial Officer, and Secretary. On April 25, 2008, Krystal Rocha officially resigned as Chief Executive Officer, Chief Financial Officer, and Secretary. On May 1, 2008, Russell Chaney accepted the appointment as COPsync’s Chief Executive Officer, Chief Financial Officer, Director, and Chairman of the Board of Directors. On said date, Shane Rapp accepted the appointment as COPsync’s President, Secretary, and Director. On May 5, 2008, Krystal Rocha officially resigned as Chairman of the Board of Directors.

(7) Related Party Transactions

As described in Note 4, during the year ended December 31, 2007, COPsync paid $39,800 to two individuals who were former Directors, officers, and principal stockholders of COPsync for working capital loans.

As of September 30, 2008, the Chief Executive Officer loaned the company $18,000 and paid expenses on the Company’s behalf of $6,409. As of September 30, 2008, the Company owed this officer $24,409.

(8) Transfer Agent Agreement

On April 18, 2007, COPsync entered into a Consulting Agreement with Island Stock Transfer for consulting and advisory services. Under the Agreement, COPsync agreed to pay to Island Stock Transfer initial fees amounting to $4,000 plus transaction fees payable as follows: (1) $1,000 due at the time of execution of the Agreement; and, $1,000 within 60 days; (2) the issuance of 375,000 shares (post forward stock split) of COPsync’s common stock with a value of $2,000; and (3) transaction fees in accordance with the fee schedule for services of Island Stock Transfer. COPsync also has the right under the Agreement to repurchase the 375,000 shares (post forward stock split) of common stock from Island Stock Transfer for a period of 12 months for $10,000. As of December 31, 2007, COPsync had paid the initial fee of $1,000 for consulting and advisory services, an additional $1,000 within 60 days of the execution of the Agreement, and issued 25,000 shares of common stock for such services with a value of $2,000.

(9) Income Taxes

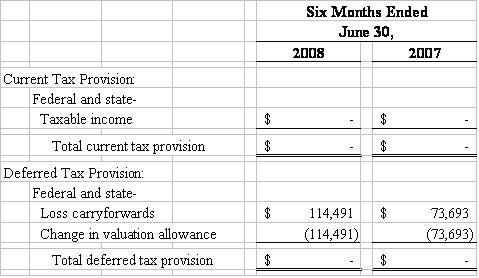

The provision (benefit) for income taxes for the three months ended September 30, 2008, and 2007 was as follows (assuming a 23% effective tax rate):

COPsync had deferred income tax assets as of September 30, 2008, as follows:

COPsync provided a valuation allowance equal to the deferred income tax assets for the six months ended September 30, 2008, and 2007, because it is not presently known whether future taxable income will be sufficient to utilize the loss carryforwards.

As of September 30, 2008, COPsync had approximately $1,511,651 in tax loss carryforwards that can be utilized in future periods to reduce taxable income, and expire in various years through the year 2027.

(10) Commitments

COPsync has a verbal commitment with a third-party consultant to provide financial and capital formation services for which the management of COPsync has agreed to pay approximately $5,000 per calendar quarter, plus out-of-pocket expenses, commencing in the year 2007. During the year ended December 31, 2006, COPsync borrowed $15,000 from an entity affiliated with this consultant for working capital to commence its organizational, patent application, and capital formation activities. The amount borrowed was repaid before December 31, 2006. For the year ended December 31, 2007, fees amounting to $23,000 were paid to the third-party consultant.

(11) Recent Accounting Pronouncements

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities – Including an amendment of FASB Statement No. 115” (“SFAS No. 159”), which permits entities to measure many financial instruments and certain other items at fair value that are not currently required to be measured at fair value. An entity would report unrealized gains and losses on items for which the fair value option has been elected in earnings at each subsequent reporting date. The objective is to improve financial reporting by providing entities with the opportunity to mitigate volatility in reported earnings caused by measuring related assets and liabilities differently without having to apply complex hedge accounting provisions. The decision about whether to elect the fair value option is applied instrument by instrument, with a few exceptions; the decision is irrevocable; and it is applied only to entire instruments and not to portions of instruments. SFAS No. 159 requires disclosures that facilitate comparisons (a) between entities that choose different measurement attributes for similar assets and liabilities and (b) between assets and liabilities in the financial statements of an entity that selects different measurement attributes for similar assets and liabilities. SFAS No. 159 is effective for financial statements issued for fiscal years beginning after November 15, 2007. Early adoption is permitted as of the beginning of a fiscal year, provided the entity also elects to apply the provisions of SFAS No. 157. Upon implementation, an entity shall report the effect of the first re-measurement to fair value as a cumulative-effect adjustment to the opening balance of retained earnings. Since the provisions of SFAS No. 159 are applied prospectively, any potential impact will depend on the instruments selected for fair value measurement at the time of implementation. The management of COPsync does not believe that this new pronouncement will have a material impact on its financial statements.

In December 2007, the FASB issued SFAS No. 141R, “Business Combinations – Revised 2007” (“SFAS No. 141R”), which replaces FASB Statement No. 141, “Business Combinations.” SFAS No. 141R establishes principles and requirements intending to improve the relevance, representational faithfulness, and comparability of information that a reporting entity provides in its financial reports about a business combination and its effects. This is accomplished through requiring the acquirer to recognize assets acquired and liabilities assumed arising from contractual contingencies as of the acquisition date, measured at their acquisition-date fair values. This includes contractual contingencies only if it is more likely than not that they meet the definition of an asset of a liability in FASB Concepts Statement No. 6, “Elements of Financial Statements – a replacement of FASB Concepts Statement No. 3.” This statement also requires the acquirer to recognize goodwill as of the acquisition date, measured as a residual. However, this statement improves the way in which an acquirer’s obligations to make payments conditioned on the outcome of future events are recognized and measured, which in turn improves the measure of goodwill. This statement also defines a bargain purchase as a business combination in which the total acquisition-date fair value of the consideration transferred plus any noncontrolling interest in the acquiree, and it requires the acquirer to recognize that excess in earnings as a gain attributable to the acquirer. This, therefore, improves the representational faithfulness and completeness of the information provided about both the acquirer’s earnings during the period in which it makes a bargain purchase and the measures of the assets acquired in the bargain purchase. COPsync does not expect the adoption of this pronouncement to have a material impact on its financial statements.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements – an amendment of ARB No. 51” (“SFAS No. 160”), which establishes accounting and reporting standards to improve the relevance, comparability, and transparency of financial information in its consolidated financial statements. This is accomplished by requiring all entities, except not-for-profit organizations, that prepare consolidated financial statements to (a) clearly identify, label, and present ownership interests in subsidiaries held by parties other than the parent in the consolidated statement of financial position within equity, but separate from the parent’s equity; (b) clearly identify and present both the parent’s and the noncontrolling interest’s attributable consolidated net income on the face of the consolidated statement of income; (c) consistently account for changes in parent’s ownership interest while the parent retains it controlling financial interest in subsidiary and for all transactions that are economically similar to be accounted for similarly; (d) measure of any gain, loss, or retained noncontrolling equity at fair value after a subsidiary is deconsolidated; and (e) provide sufficient disclosures that clearly identify and distinguish between the interests of the parent and the interests of the noncontrolling owners. This Statement also clarifies that a noncontrolling interest in a subsidiary is an ownership interest in the consolidated entity that should be reported as equity in the consolidated financial statements. SFAS No. 160 is effective for fiscal years and interim periods on or after December 15, 2008. The management of COPsync does not expect the adoption of this pronouncement to have a material impact on its financial statements.

In March 2008, the FASB issued FASB Statement No. 161, “Disclosures about Derivative Instruments and Hedging Activities – an Amendment of FASB Statement 133” (“SFAS No. 161”). SFAS No. 161 enhances required disclosures regarding derivatives and hedging activities, including enhanced disclosures regarding how: (a) an entity uses derivative instruments; (b) derivative instruments and related hedged items are accounted for under FASB No. 133, “Accounting for Derivative Instruments and Hedging Activities”; and (c) derivative instruments and related hedged items affect an entity’s financial position, financial performance, and cash flows. Specifically, FASB No. 161 requires:

| | ● | Disclosure of the objectives for using derivative instruments be disclosed in terms of underlying risk and accounting designation; |

| | ● | Disclosure of the fair values of derivative instruments and their gains and losses in a tabular format; |

| | ● | Disclosure of information about credit-risk-related contingent features; and |

| | ● | Cross-reference from the derivative footnote to other footnotes in which derivative-related information is disclosed. |

FASB No. 161 is effective for fiscal years and interim periods beginning after November 15, 2008. Earlier application is encouraged. The management of COPsync does not expect the adoption of this pronouncement to have a material impact on its financial statements.

In May 2008, the FASB issued FASB Statement No. 162, “The Hierarchy of Generally Accepted Accounting Principles” (“SFAS No. 162”). SFAS No. 162 identifies the sources of accounting principles and the framework for selecting the principles used in the preparation of financial statements of nongovernmental entities that are presented in conformity with generally accepted accounting principles in the United States of America. The sources of accounting principles that are generally accepted are categorized in descending order as follows:

| a) | FASB Statements of Financial Accounting Standards and Interpretations, FASB Statement 133 Implementation Issues, FASB Staff Positions, and American Institute of Certified Public Accountants (AICPA) Accounting Research Bulletins and Accounting Principles Board Opinions that are not superseded by actions of the FASB. |

| b) | FASB Technical Bulletins and, if cleared by the FASB, AICPA Industry Audit and Accounting Guides and Statements of Position. |

| c) | AICPA Accounting Standards Executive Committee Practice Bulletins that have been cleared by the FASB, consensus positions of the FASB Emerging Issues Task Force (EITF), and the Topics discussed in Appendix D of EITF Abstracts (EITF D-Topics). |

| d) | Implementation guides (Q&As) published by the FASB staff, AICPA Accounting Interpretations, AICPA Industry Audit and Accounting Guides and Statements of Position not cleared by the FASB, and practices that are widely recognized and prevalent either generally or in the industry. |

On May 26, 2008, the FASB issued FASB Statement No. 163, “Accounting for Financial Guarantee Insurance Contracts” (“SFAS No. 163”). SFAS No. 163 clarifies how FASB Statement No. 60, “Accounting and Reporting by Insurance Enterprises” (“SFAS No. 60”), applies to financial guarantee insurance contracts issued by insurance enterprises, including the recognition and measurement of premium revenue and claim liabilities. It also requires expanded disclosures about financial guarantee insurance contracts.

The accounting and disclosure requirements of SFAS No. 163 are intended to improve the comparability and quality of information provided to users of financial statements by creating consistency. Diversity exists in practice in accounting for financial guarantee insurance contracts by insurance enterprises under SFAS No. 60, “Accounting and Reporting by Insurance Enterprises.” That diversity results in inconsistencies in the recognition and measurement of claim liabilities because of differing views about when a loss has been incurred under FASB Statement No. 5, “Accounting for Contingencies” (“SFAS No. 5”). SFAS No. 163 requires that an insurance enterprise recognize a claim liability prior to an event of default when there is evidence that credit deterioration has occurred in an insured financial obligation. It also requires disclosure about (a) the risk-management activities used by an insurance enterprise to evaluate credit deterioration in its insured financial obligations and (b) the insurance enterprise’s surveillance or watch list.

SFAS No. 163 is effective for financial statements issued for fiscal years beginning after December 15, 2008, and all interim periods within those fiscal years, except for disclosures about the insurance enterprise’s risk-management activities. Disclosures about the insurance enterprise’s risk-management activities are effective the first period beginning after issuance of SFAS No. 163. Except for those disclosures, earlier application is not permitted. Management of PCMT does not expect the adoption of this pronouncement to have material impact on its financial statements.

(12) Subsequent Events

On June 6, 2008, the Company authorized the issuance of shares to be disbursed from convertible notes issued to certain Limited Partners of the original Limited Partnership – PostInk Technology, LP. Issuance of common stock began on July 15, 2008, and will be issued over a six month period.

Item 2 - MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FORWARD-LOOKING STATEMENTS

This quarterly report contains forward-looking statements as that term is defined in Section 27A of the United States Securities Act of 1933 and section 21E of the United States Securities Exchange Act of 1934. These statements relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors”, that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

Our financial statements are stated in United States dollars and are prepared in conformity with generally accepted accounting principles in the United States of America for interim financial statements. The following discussion should be read in conjunction with our financial statements and the related notes that appear elsewhere in this quarterly report.

The following discussion should be read in conjunction with the Company’s interim consolidated financial statements and the notes related thereto included in item 1 above which have been prepared in accordance with the accounting principles generally accepted in the United States of America. The discussion of results, causes and trends should not be construed to imply any conclusion that such results, causes or trend will necessarily continue in the future.

COMPANY DESCRIPTION

PostInk has developed the first integrated software product COPsync, which provides a real-time, nationwide information sharing network for all law enforcement officers. COPsync, Inc. is the only Law Enforcement software provider to have full information sharing networking available to all subscribing agencies at the point of incident via Laptop Computer or Handheld devices. It is the Company’s mission that the all Law Enforcement officers of the future will be armed, in REAL TIME, with the critical information necessary to protect the public and themselves. COPsync, Inc. currently has over 3600+ Police Officers committed to utilize COPsync™. Beta testing is complete and COPsync™ is available for general release, as a result the number of committed officers will rapidly grow.

As of September 30th, COPsync™ had successfully submitted, processed and relayed over 19,800 officer initiated information requests. On average, COPsync™ is returning results to mobile users in less than 5 seconds, well within the 32 second average set forth by the NCIC 2000 standards for mobile clients. COPsync, Inc. continues to garner support from Law Enforcement agencies; during the past quarter 32 additional agencies expressed interest and gave their commitment to utilize COPsync™ in their respective agencies. COPsync, Inc. must obtain funding to establish a favorable balance sheet to implement the existing contracts with 116 Law Enforcement agencies currently subscribed to COPsync™.

Law Enforcement agencies and Associations at the Federal, State and Local levels are pushing information sharing initiatives. Global Justice XML standards were developed and have been published by the US Federal Government since 1997. To date, interoperability between Law Enforcement agencies in the United States fails to exist. This failure is directly related to software vendors that have remained focused on their existing methods of doing business including proprietary development, which does not focus on global information sharing. COPsync, Inc. will fulfill the interoperability role through the deployment of COPsync™. COPsync™ is an overlay product to existing technologies that can be deployed without jeopardizing the existing vendor relationships. COPsync, Inc.'s method of data integration will bring existing vendors into compliance with federal mandates established after 9/11.

COPSYNC™ SOFTWARE

COPsync™ provides an innovative and open architecture software platform. Most software vendors in this space continue to maintain and support closed architecture systems with archaic methodologies related to providing information to the officer on the street and interagency information sharing

During this quarter, the 2.3 and 2.4 versions of COPsync were released, Windows Vista Compatibility Testing was completed, and an enhanced Location Search module to search Civil Process records was released. Reports can now be opened directly from this module. COPsync™ now provides a visual and audible alert whenever a warning message comes back in a return from a TLETS query. Officers now get alerted for stolen vehicle, registered sex offenders, officer safety alerts, wanted persons, and much more.

Additionally, the Company reworked and vastly improved the interface for handling additional occupants during a Traffic Stop and added the capability to import an officer's signature into the system and print the signature on appropriate forms. We updated the Crash Report to support the new version put out by the Texas Department of Transportation and added the ability to open, directly from COPsync, the Texas Department of Transportation’s instructions for Crash Reporting.

Further improvements during the quarter included, adding a Field Interview module which allows officers to track interactions with the public even when a violation may not have occurred. The Company added the ability to print a Lab Submission Form from the Offense Report as well as adding the ability to archive reports that may not be escalated through the approval process. COPsync enhanced Civil Process to allow “Writ Of Possessions” to import Information from the Corresponding Served Eviction Citation, enhanced User Profile search to display information and allow for more filtering options, and added Export & Print functionality to Field Interview. Additionally we added ability to specify multiple “Consent to Searches” in the Offense Report, and added the ability to archive reports that may not be escalated through the approval process.

GRANTS AND FUNDING

COPsync, Inc. has successfully been approved to utilize government provided funding and Homeland Security funds for the integration and implementation of its technology in Law Enforcement Agencies. This is a true milestone, being that NO other software vendors in this space have qualified for Information Sharing Grants. These grants currently maintain billions of dollars to be utilized for informational sharing purposes. COPsync, Inc. has successfully assisted more than 20 Law Enforcement agencies in drafting and submitting applications for various funding options during the past quarter, and will continue to assist agencies in the future with their capital needs.

During this time frame, Copsync, inc. also rolled out and modified the Copsync Technology Assistance Program. The CTAP assists agencies in by providing various forms of financing assistance in order to expedite the agency “going live” with the Copsync software suite. In addition to CTAP, we have continued our pursuit of federal and state funding through grants, including, but not limited to the Border Security Equipment and Technology (BSET) grant and the Criminal Justice Planning Fund sponsored by the East Texas Council of Governments.

During the third quarter, we continued processing grant applications for the Border Security Equipment and Technology (BSET) Grant. This grant is only for those agencies participating in border security operations such as Operation Border Star. A large percentage of our client agencies are located in counties eligible to apply for these funds. In February of this year the company met with the head of Texas Homeland Security and a representative from Texas Border Security Operations. Both representatives recommended COPsync to agencies along the Texas/Mexico border. The BSET Grant is one of the methods of acquiring funds to support border security operations under Texas Homeland Security and Texas Border Security Operations.

As a result of our efforts, the Live Oak County Sheriff’s Office was awarded $117,196 under the BSET Grant. Work on the BSET Grant is ongoing and will continue into the fourth quarter. Our office also began processing applications for the 2008 Homeland Security Grant Program (HSGP) for all of our eligible clients in the East Texas Council of Governments. The 2008 HSGP provides federal funding to be used for projects that support the 12 homeland security investments approved by the US Department of Homeland Security (DHS). The work on these applications is ongoing and will continue into the fourth quarter.

SALES & MARKETING

Copsync, inc. has been very active in sales and marketing during the third quarter of 2008. Beginning with the Sheriff’s Association of Texas Training Seminar that took place in San Antonio, Texas in July, which generated over Fifty different Sheriffs requesting additional information, in the form of Demonstrations of our software. COPsync, Inc. is poised to rapidly expand in the trillion Dollar Law Enforcement, Emergency Service and Fire District profession. This growth can be quickly realized leveraging Homeland Security grant initiatives. COPsync, Inc. will see this growth through the culmination of technology and strategic partnerships with marquee corporations.

(a) Plan of Operation

Cash Requirements and of Need for additional funds: twelve months. We continue to face certain minimal cash requirements for corporate maintenance, legal and professional and auditing expenses. Our cash requirements for these purposes are not in issue.

Cautionary Statement: There can be no assurance that we will be successful in raising capital through private placements or otherwise. Even if we are successful in raising capital through the sources specified, there can be no assurances that any such financing would be available in a timely manner or on terms acceptable to us and our current shareholders. Additional equity financing could be dilutive to our then existing shareholders, and any debt financing could involve restrictive covenants with respect to future capital raising activities and other financial and operational matters.

Critical Accounting Policies and Recent Accounting Pronouncements

Management believes the estimates, assumptions and judgments involved in the accounting policies described below have the greatest potential impact on the Company’s financial statements. Because of the uncertainty inherent in these matters, actual results could differ from the estimates used in applying the critical accounting policies. Within the context of these critical accounting policies, management is not currently aware of any reasonably likely event that would result in materially different amounts being reported.

Recent accounting pronouncements

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities“. This Statement permits entities to choose to measure many financial assets and financial liabilities at fair value. Unrealized gains and losses on items for which the fair value option has been elected are reported in earnings. SFAS No. 159 is effective for fiscal years beginning after November 15, 2007. The Company is currently assessing the impact of SFAS No. 159 on its financial position and results of operations.

In June 2007, the FASB issued FASB Staff Position No. EITF 07-3, “Accounting for Nonrefundable Advance Payments for Goods or Services Received for use in Future Research and Development Activities” (“FSP EITF 07-3”), which addresses whether nonrefundable advance payments for goods or services that used or rendered for research and development activities should be expensed when the advance payment is made or when the research and development activity has been performed. Management is currently evaluating the effect of this pronouncement on financial statements.

In December 2007, the FASB issued SFAS No. 141 (Revised 2007), “Business Combinations.” SFAS No. 141 (Revised 2007) changes how a reporting enterprise accounts for the acquisition of a business. SFAS No. 141 (Revised 2007) requires an acquiring entity to recognize all the assets acquired and liabilities assumed in a transaction at the acquisition-date fair value, with limited exceptions, and applies to a wider range of transactions or events. SFAS No. 141 (Revised 2007) is effective for fiscal years beginning on or after December 15, 2008 and early adoption and retrospective application is prohibited.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statements”, which is an amendment of Accounting Research Bulletin (“ARB”) No. 51. This statement clarifies that a noncontrolling interest in a subsidiary is an ownership interest in the consolidated entity that should be reported as equity in the consolidated financial statements. This statement changes the way the consolidated income statement is presented, thus requiring consolidated net income to be reported at amounts that include the amounts attributable to both parent and the noncontrolling interest. This statement is effective for the fiscal years, and interim periods within those fiscal years, beginning on or after December 15, 2008. Based on current conditions, the Company does not expect the adoption of SFAS 160 to have a significant impact on its results of operations or financial position.

In March 2008, the FASB issued SFAS No. 161, “Disclosures about Derivative Instruments and Hedging Activities an amendment of FASB Statement No. 133.” This Statement changes the disclosure requirements for derivative instruments and hedging activities. Entities are required to provide enhanced disclosures about (a) how and why an entity uses derivative instruments, (b) how derivative instruments and related hedged items are accounted for under Statement 133 and its related interpretations, and (c) how derivative instruments and related hedged items affect an entity’s financial position, financial performance, and cash flows. Based on current conditions, the Company does not expect the adoption of SFAS 161 to have a significant impact on its results of operations or financial position.

In April 2008, the FASB issued 142-3 “Determination of the useful life of Intangible Assets”, which amends the factors a company should consider when developing renewal assumptions used to determine the useful life of an intangible asset under SFAS142. This Issue is effective for financial statements issued for fiscal years beginning after December 15, 2008, and interim periods within those fiscal years. SFAS 142 requires companies to consider whether renewal can be completed without substantial cost or material modification of the existing terms and conditions associated with the asset. FSP 142-3 replaces the previous useful life criteria with a new requirement—that an entity consider its own historical experience in renewing similar arrangements. If historical experience does not exist then the Company would consider market participant assumptions regarding renewal including 1) highest and best use of the asset by a market participant, and 2) adjustments for other entity-specific factors included in SFAS 142. The Company is currently evaluating the impact that adopting SFAS No.142-3 will have on its financial statements.

In May 2008, the FASB issued SFAS No. 162, “The Hierarchy of Generally Accepted Accounting Principles.” This Statement identifies the sources of accounting principles and the framework for selecting the principles to be used in the preparation of financial statements of nongovernmental entities that are presented in conformity with generally accepted accounting principles (GAAP) in the United States (the GAAP hierarchy). This Statement will not have an impact on the Company’s financial statements.

In May 2008, the FASB issued SFAS No. 163, “Accounting for Financial Guarantee Insurance Contracts, an interpretation of FASB Statement No. 60.” The scope of this Statement is limited to financial guarantee insurance (and reinsurance) contracts, as described in this Statement, issued by enterprises included within the scope of Statement 60. Accordingly, this Statement does not apply to financial guarantee contracts issued by enterprises excluded from the scope of Statement 60 or to some insurance contracts that seem similar to financial guarantee insurance contracts issued by insurance enterprises (such as mortgage guaranty insurance or credit insurance on trade receivables). This Statement also does not apply to financial guarantee insurance contracts that are derivative instruments included within the scope of FASB Statement No. 133, “Accounting for Derivative Instruments and Hedging Activities.” This Statement will not have an impact on the Company’s financial statements.

(b) Management's Discussion and Analysis of Financial Condition and Results of Operations. This discussion and analysis of our financial condition and results of operations includes "forward-looking" statements that reflect our current views with respect to future events and financial performance. We use words such as "expect," "anticipate," "believe," and "intend" and similar expressions to identify forward-looking statements. You should be aware that actual results may differ materially from our expressed expectations because of risks and uncertainties inherent in future events and you should not rely unduly on these forward looking statements. We will not necessarily update the information in this discussion if any forward-looking statement later turns out to be inaccurate. Reference in the following discussion to "our", "us" and "we" refer to our operations and the operations of our subsidiaries, except where the context otherwise indicates or requires.

This discussion and analysis of financial condition and results of operations should be read in conjunction with our audited Financial Statements included in this filing. Our consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States, and reflect our historical financial position, results of operations, and cash flows. The financial information included in this filing, is not necessarily indicative of our future performance.

Revenue in the three months ended September 30, 2008 was $6,450 compared to $nil for the nine months ended September 30, 2007, no change.

General and administrative expenses for the three months ended September 30, 2008 $7,874 compared to $28,044 for the nine months ended September 30, 2007, an decrease of $20,170 due to a decrease in private placement offering related expense from 2007.

The Company recorded a provision for federal and state income taxes of $nil for the three months ended September 30, 2008 compared to $nil for the nine months ended September 30, 2007.

Liquidity and Capital Resources.

As of September 30, 2008 the current assets exceeded the current liabilities by $1,083,971. During the period ended September 30, 2008 and through April 25, 2008, the Company issued a total of 25,000,005 restricted shares of common stock for the acquisition of PostInk Technology LP.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Investors should consider each of the following risk factors and the other information in this Quarterly Report, including COPsync’s financial statements and the related notes, in evaluating the Company’s business and prospects. The risks and uncertainties described below are not the only ones that impact on COPsync’s business. Additional risks and uncertainties not presently known to the Company or the Company currently considers immaterial may also impair its business operations. If any of the following risks actually occur, the Company’s business and financial results could be harmed. In that case, the trading price of COPsync’s Common Stock could decline.

1. COPsync’s stock price is volatile with wide fluctuations in the past that are likely to continue in the future. The Company’s common stock trades domestically on the OTC-BB, a relatively illiquid and extremely volatile market. In order to maintain its listing status on the OTC-BB, the Company must file periodic reports with the SEC in a timely manner. If the Company does not maintain its reporting status it may have its securities delisted from the OTC-BB.

2. A small number of COPsync’s stockholders own a substantial amount of the Company's Common Stock, and if such stockholders were to sell those shares in the public market within a short period of time, the price of COPsync’s Common Stock could drop significantly.

3. Power-Save may not be able to attract and retain qualified personnel necessary for the implementation of its business strategy. If the Company is not able to attract or retain qualified personnel, it is likely that the Company would be unable to remain competitive in its business resulting in a material adverse effect on COPsync’s operations.