Exhibit 99.1

| Tyco Electronics Merrill Lynch Technology Conference 2008 Terrence Curtin Executive Vice President & Chief Financial Officer May 6, 2008 |

| Page 2 This presentation contains certain “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. These statements are based on management’s current expectations and are subject to risks, uncertainty and changes in circumstances, which may cause actual results, performance or achievements to differ materially from anticipated results, performance or achievements. All statements contained herein that are not clearly historical in nature are forward-looking and the words “anticipate,” “believe,” “expect,” “estimate,” “plan,” and similar expressions are generally intended to identify forward-looking statements. Forward-looking statements involve risks, uncertainties, and assumptions. The forward-looking statements in this presentation may include statements addressing the following subjects: future financial condition and operating results. Economic, business, competitive and/or regulatory factors affecting Tyco Electronics’ business are examples of factors, among others, that could cause actual results to differ materially from those described in the forward-looking statements. In addition, Tyco Electronics’ historical combined financial information is not necessarily representative of the results it would have achieved as an independent, publicly-traded company and may not be a reliable indicator of its future results. Tyco Electronics has no intention and is under no obligation to (and expressly disclaims any such intention or obligation to) update or alter its forward-looking statements whether as a result of new information, future events or otherwise, except to the extent required by law. More detailed information about these and other factors is set forth in Tyco Electronics’ Annual Report on Form 10-K for the fiscal year ended September 28, 2007 and Quarterly Reports on Form 10-Q for the quarterly periods ended December 28, 2007 and March 28, 2008, as well as in current reports on Form 8-K filed by Tyco Electronics. Where we have used non-GAAP financial measures, reconciliations to the most comparable GAAP measure is provided, along with a disclosure on the usefulness of the non-GAAP measure, in the Appendix section of this presentation. Forward-Looking Statement / Non-GAAP Measures |

| Page 3 Tyco Electronics Overview • A leading global provider of engineered electronic components, network infrastructure solutions, undersea telecommunication systems and wireless systems • Global leader in attractive, growing industries • Diverse customer base and industry base • Global reach and scale • Established track record of innovation leadership • Strong cash flow generation and financial flexibility • Growth and margin improvement opportunities |

| Page 4 Market dynamics should continue to drive above-GDP growth Market Drivers • Electronic feature growth in all industries • Miniaturization and higher data-speed requirements • Broadband and wireless proliferation • Upgrade of global energy networks “Dot Com” Bubble & Bust 27 Year historical CAGR = 6.1% Source: 2007 Connector Market Handbook, Bishop and Associates, Inc. World Connector Market Sales Growth: 1980-2007 100 150 200 250 300 350 400 450 500 550 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 Growth Index (1980=100) 100 150 200 250 300 350 400 450 500 550 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 Growth Index (1980=100) |

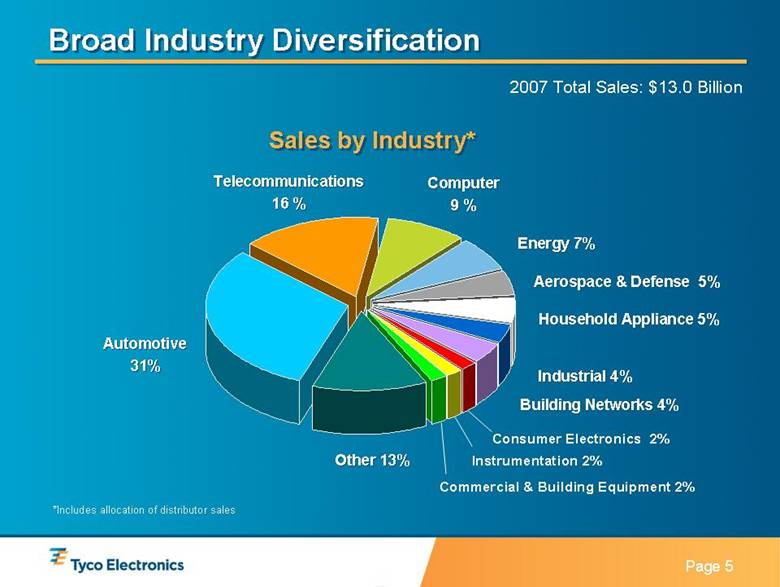

| Page 5 Computer 9 % Automotive 31% Telecommunications 16 % Aerospace & Defense 5% Household Appliance 5% Energy 7% Consumer Electronics 2% Other 13% Instrumentation 2% Commercial & Building Equipment 2% Industrial 4% Building Networks 4% Sales by Industry* Broad Industry Diversification 2007 Total Sales: $13.0 Billion *Includes allocation of distributor sales |

| Page 6 Consumer Markets Approx. 60% Infrastructure / Industrial Markets – Approx. 40% Approximately 40% of Sales Come From Long-Cycle Markets 2007 Total Sales: $13.0 Billion • Automotive • Computer • Mobile Phone • Appliance • Consumer Electronics • A & D • Comm. Equip. • Industrial • Energy • Comm. Service Providers • Building Networks • Wireless Networks • Undersea Telecom |

| Page 7 Asia ex- China 16% China 12% Europe 37% Americas 35% Asia ex- China 16% China 12% Europe 37% Americas 35% Sales by Geography Asia Total 28% Global Reach and Scale • Balanced geographic presence • Located near our customers – 7,000+ engineers – 17 global design centers – 5,000+ salespeople serving customers in 150+ countries – Manufacturing in 25+ countries • Significant presence in China – $1.6 billion of sales – 32,200 employees – 15 manufacturing facilities 2007 Total Sales: $13.0 Billion |

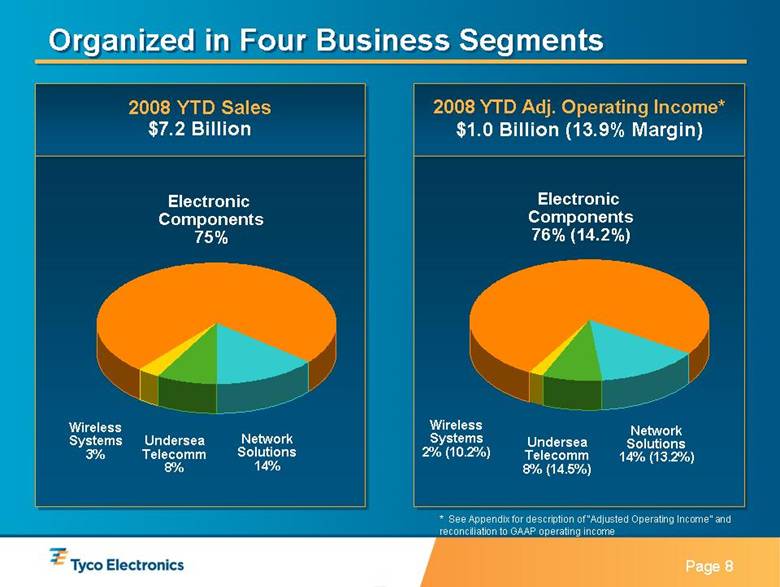

| Page 8 2008 YTD Sales $7.2 Billion Electronic Components 75% Network Solutions 14% Undersea Telecomm 8% Wireless Systems 3% Organized in Four Business Segments * See Appendix for description of “Adjusted Operating Income” and reconciliation to GAAP operating income 2008 YTD Adj. Operating Income* $1.0 Billion (13.9% Margin) Electronic Components 76% (14.2%) Network Solutions 14% (13.2%) Wireless Systems 2% (10.2%) Undersea Telecomm 8% (14.5%) |

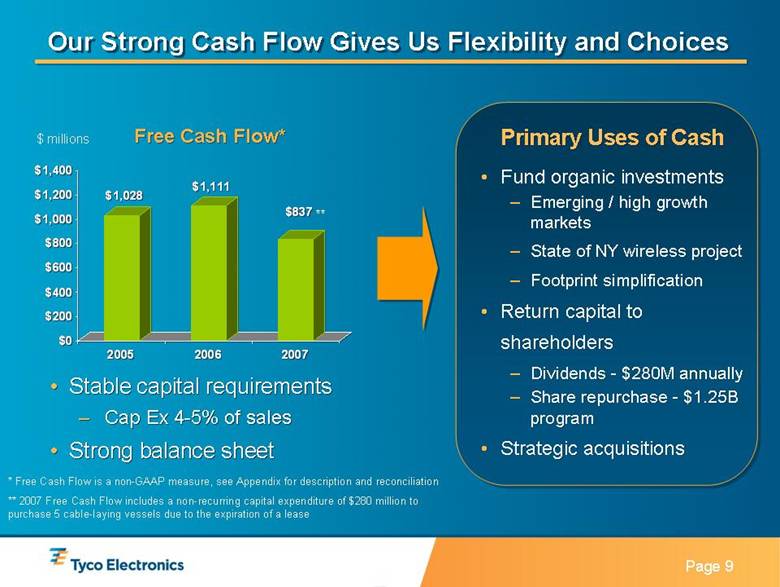

| Page 9 $1,028 $1,111 $837 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 2005 2006 2007 $1,028 $1,111 $837 $0 $200 $400 $600 $800 $1,000 $1,200 $1,400 2005 2006 2007 • Fund organic investments – Emerging / high growth markets – State of NY wireless project – Footprint simplification • Return capital to shareholders – Dividends - $280M annually – Share repurchase - $1.25B program • Strategic acquisitions Primary Uses of Cash Free Cash Flow* $ millions * Free Cash Flow is a non-GAAP measure, see Appendix for description and reconciliation ** 2007 Free Cash Flow includes a non-recurring capital expenditure of $280 million to purchase 5 cable-laying vessels due to the expiration of a lease Our Strong Cash Flow Gives Us Flexibility and Choices • Stable capital requirements – Cap Ex 4-5% of sales • Strong balance sheet ** |

| Page 10 Strategic Priorities • Organic sales growth* of 5-7% • Operating margins above 15% • Free cash flow approximately equal to net income** 3-Year Objectives Year Objectives * See Appendix for description of “Organic Sales Growth,” a non-GAAP measure ** Before dividends and cash outflows to build the State of New York wireless network • Focus the portfolio • Achieve organic growth of 5 to 7% – Accelerate growth in under – penetrated markets – Enhance leadership position in emerging markets • Improve margins by streamlining operations and improving productivity • Target acquisitions to accelerate sales and income growth |

| Page 11 First Half Performance * See Appendix for description and reconciliation of “Adjusted Operating Income”, “Adjusted Earnings Per Share”, “Free Cash Flow” and “Organic Sales Growth” • Sales growth in Industrial and Infrastructure markets including Undersea Telecommunications, Wireless Systems, Network Solutions and industrial markets in Electronic Components segment • Operating Income growth primarily due to higher sales levels and favorable sales mix in Undersea Telecommunications and Wireless Systems Drivers 6 Months 6 Months FY2008 FY2007 Actual Organic* Sales $7,220 $6,179 16.8% 9.8% Adjusted OI* $1,007 $840 19.9% Adjusted OI % 13.9% 13.6% Adjusted EPS* $1.29 $1.08 19.4% Free Cash Flow* $614 $10 Growth |

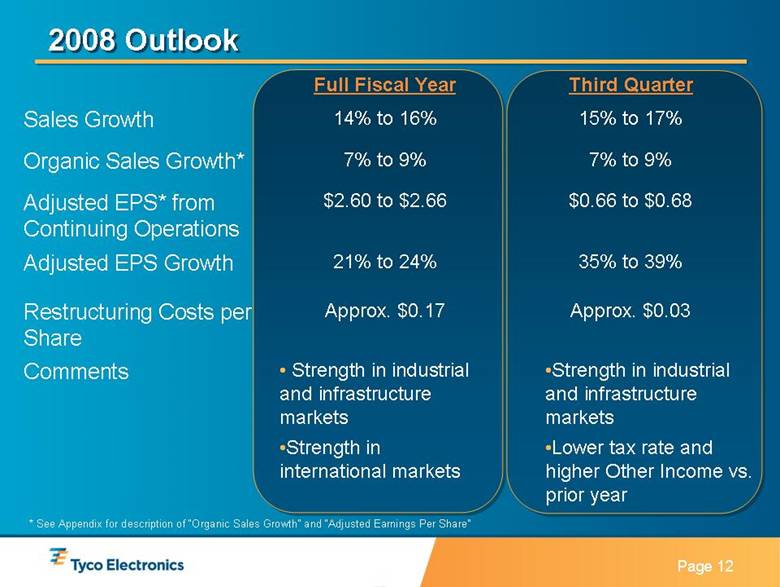

| Page 12 2008 Outlook 15% to 17% 14% to 16% Sales Growth Approx. $0.03 Approx. $0.17 Restructuring Costs per Share •Strength in industrial and infrastructure markets •Lower tax rate and higher Other Income vs. prior year • Strength in industrial and infrastructure markets •Strength in international markets Comments 35% to 39% 21% to 24% Adjusted EPS Growth $0.66 to $0.68 $2.60 to $2.66 Adjusted EPS* from Continuing Operations 7% to 9% 7% to 9% Organic Sales Growth* Third Quarter Full Fiscal Year * See Appendix for description of “Organic Sales Growth” and “Adjusted Earnings Per Share” |

| Page 13 A solid foundation with significant opportunity Tyco Electronics Summary • A leading global provider of engineered electronic components, network infrastructure solutions, undersea telecommunication systems and wireless systems • Global leader in attractive, growing industries • Diverse customer base and industry base • Global reach and scale • Established track record of innovation leadership • Strong cash flow generation and financial flexibility • Growth and margin improvement opportunities |

| Appendix |

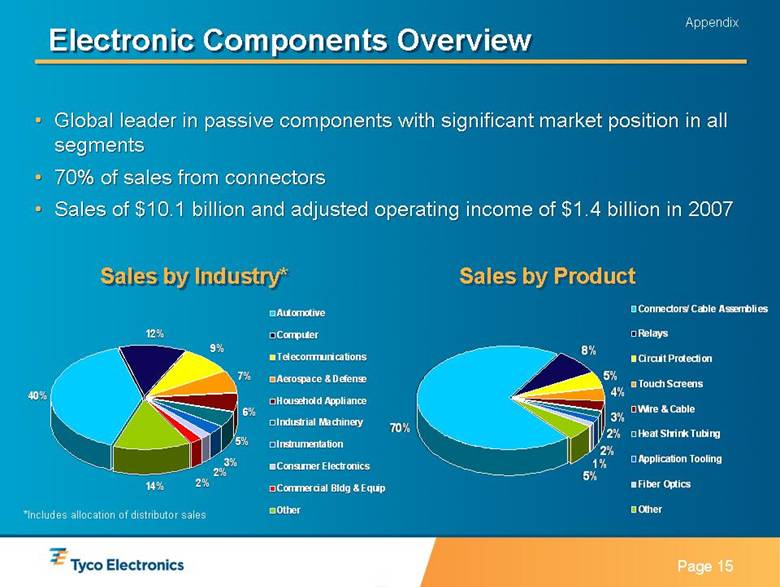

| Page 15 Sales by Industry* Sales by Product 40% 12% 9% 14% 2% 6% 5% 3% 2% 7% Automotive Computer Telecommunications Aerospace & Defense Household Appliance Industrial Machinery Instrumentation Consumer Electronics Commercial Bldg & Equip Other 40% 12% 9% 14% 2% 6% 5% 3% 2% 7% Automotive Computer Telecommunications Aerospace & Defense Household Appliance Industrial Machinery Instrumentation Consumer Electronics Commercial Bldg & Equip Other Electronic Components Overview • Global leader in passive components with significant market position in all segments • 70% of sales from connectors • Sales of $10.1 billion and adjusted operating income of $1.4 billion in 2007 70% 8% 5% 5% 3% 2% 2% 1% 4% Connectors/ Cable Assemblies Relays Circuit Protection Touch Screens Wire & Cable Heat Shrink Tubing Application Tooling Fiber Optics Other 70% 8% 5% 5% 3% 2% 2% 1% 4% Connectors/ Cable Assemblies Relays Circuit Protection Touch Screens Wire & Cable Heat Shrink Tubing Application Tooling Fiber Optics Other *Includes allocation of distributor sales Appendix |

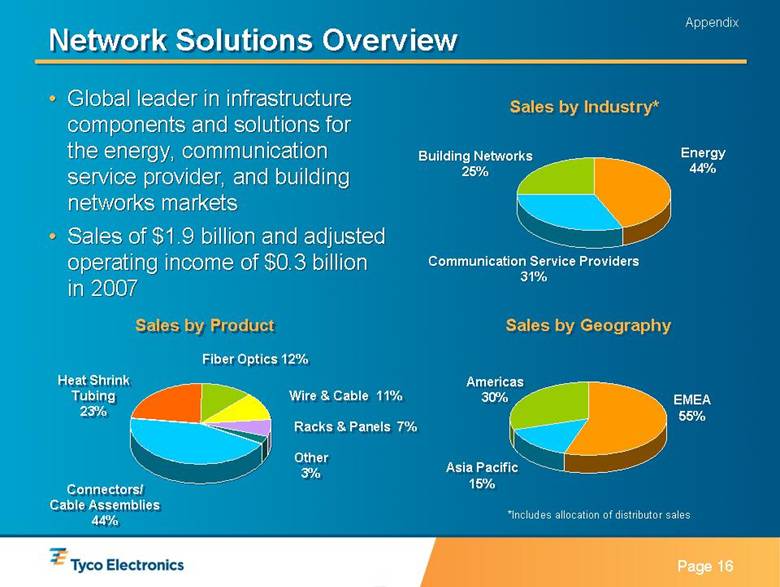

| Page 16 Sales by Industry* Sales by Product Communication Service Providers 31% Building Networks 25% Heat Shrink Tubing 23% Wire & Cable 11% Racks & Panels 7% Fiber Optics 12% Other 3% Connectors/ Cable Assemblies 44% Sales by Geography EMEA 55% Americas 30% Asia Pacific 15% Energy 44% Network Solutions Overview • Global leader in infrastructure components and solutions for the energy, communication service provider, and building networks markets • Sales of $1.9 billion and adjusted operating income of $0.3 billion in 2007 *Includes allocation of distributor sales Appendix |

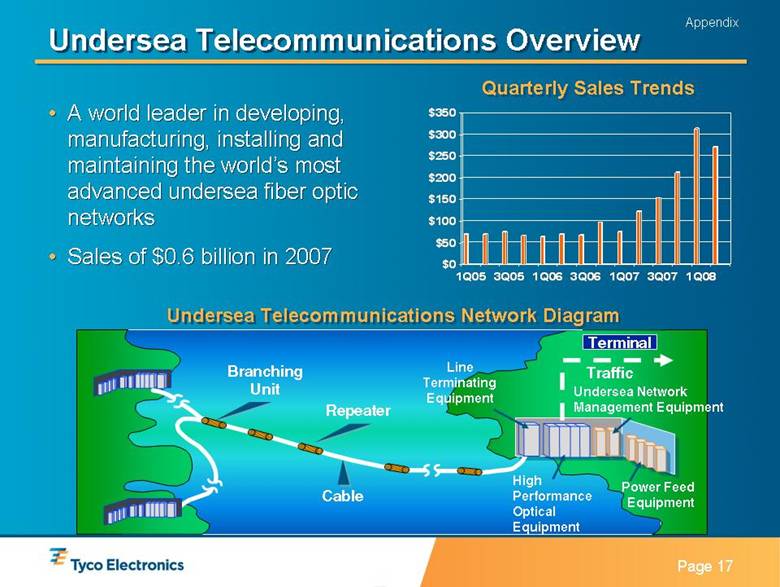

| Page 17 Quarterly Sales Trends Undersea Telecommunications Overview • A world leader in developing, manufacturing, installing and maintaining the world’s most advanced undersea fiber optic networks • Sales of $0.6 billion in 2007 $0 $50 $100 $150 $200 $250 $300 $350 1Q05 3Q05 1Q06 3Q06 1Q07 3Q07 1Q08 Branching Unit Repeater Cable Terminal Traffic Line Terminating Equipment Power Feed Equipment High Performance Optical Equipment Undersea Telecommunications Network Diagram Undersea Network Management Equipment Appendix |

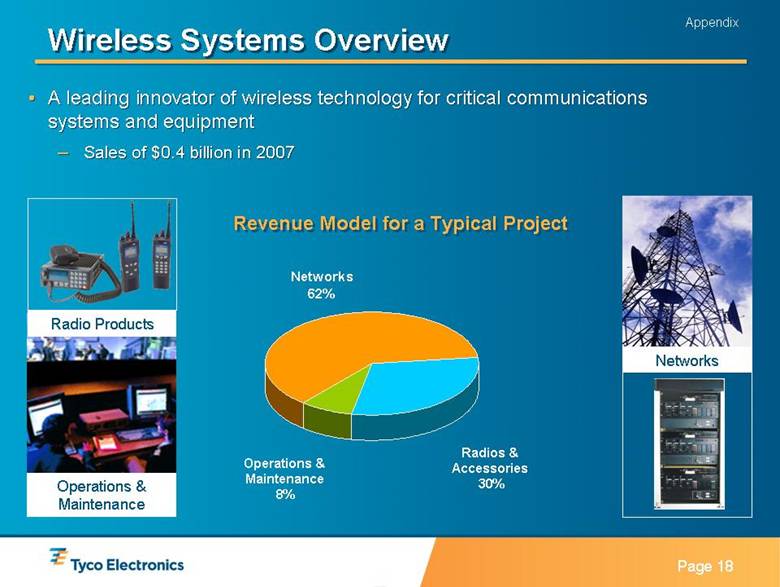

| Page 18 Wireless Systems Overview • A leading innovator of wireless technology for critical communications systems and equipment – Sales of $0.4 billion in 2007 Appendix Operations & Maintenance Radio Products Revenue Model for a Typical Project Networks 62% Radios & Accessories 30% Operations & Maintenance 8% Networks |

| Page 19 NON-GAAP Measures Appendix “Organic Sales Growth,” “Adjusted Operating Income,” “Adjusted Earnings Per Share,” “Adjusted Operating Margin,” and “Free Cash Flow” (FCF) are non- GAAP measures and should not be considered replacements for GAAP results. “Organic Sales Growth” is a useful measure used by the company to measure the underlying results and trends in the business. The difference between reported net sales growth (the most comparable GAAP measure) and Organic Sales Growth (the non-GAAP measure) consists of the impact from foreign currency, acquisitions and divestitures. Organic Sales Growth is a useful measure of the company’s performance because it excludes items that: i) are not completely under management’s control, such as the impact of foreign currency exchange; or ii) do not reflect the underlying growth of the company, such as acquisition and divestiture activity. It is also a component of the company’s compensation programs. The limitation of this measure is that it excludes items that have an impact on the company’s sales. This limitation is best addressed by using organic sales growth in combination with the GAAP numbers. The company has presented its operating income before unusual items including costs related to the separation, legal settlements, restructuring costs and other income or charges (“Adjusted Operating Income”). The company utilizes Adjusted Operating Income to assess segment level core operating performance and to provide insight to management in evaluating segment operating plan execution and underlying market conditions. It is also a significant component in the company’s incentive compensation plans. Adjusted Operating Income is a useful measure for investors because it better reflects the company’s underlying operating results, trends and the comparability of these results between periods. The difference between Adjusted Operating Income and operating income (the most comparable GAAP measure) consists of the impact of charges related to litigation settlement costs, separation-related costs and restructuring costs and other income or charges that may mask the underlying operating results and/or business trends. The limitation of this measure is that it excludes the financial impact of items that would otherwise either increase or decrease the company’s reported operating income. This limitation is best addressed by using Adjusted Operating Income in combination with operating income (the most comparable GAAP measure) in order to better understand the amounts, character and impact of any increase or decrease on reported results. The company has presented its operating margin before unusual items including costs related to the separation, legal settlements, restructuring costs and other income or charges (“Adjusted Operating Margin”). The company presents and forecasts its Adjusted Operating Margin before unusual items to give investors a perspective on the underlying business results. Because the company cannot predict the amount and timing of such items and the associated charges or gains that will be recorded in the company’s financial statements, it is difficult to include the impact of those items in the forecast. The company has presented adjusted diluted earnings per share, which is earnings per share from continuing operations before unusual items, including costs related to the separation, legal settlements, restructuring costs, loss on retirement of debt and other income or charges (“Adjusted Earnings Per Share”). The company presents Adjusted Earnings Per Share because we believe that it is appropriate for investors to consider results excluding these items in addition to our results in accordance with GAAP. We believe such a measure provides a picture of our results that is more comparable among periods since it excludes the impact of unusual items, which may recur occasionally, but tend to be irregular as to timing, thereby making comparisons between periods more difficult. This limitation is best addressed by using Adjusted Earnings Per Share in combination with earnings per share (the most comparable GAAP measure) in order to better understand the amounts, character and impact of any increase or decrease on reported results. |

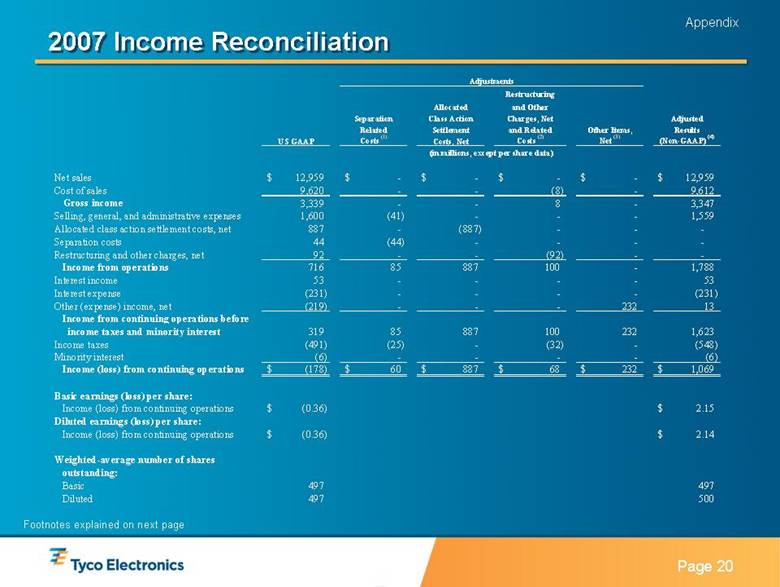

| Page 20 2007 Income Reconciliation Appendix Footnotes explained on next page Restructuring Allocated and Other Separation Class Action Charges, Net Adjusted Related Settlement and Related Other Items, Results US GAAP Costs (1) Costs, Net Costs (2) Net (3) (Non-GAAP) (4) Net sales 12,959 $ - $ - $ - $ - $ 12,959 $ Cost of sales 9,620 - - (8) - 9,612 Gross income 3,339 - - 8 - 3,347 Selling, general, and administrative expenses 1,600 (41) - - - 1,559 Allocated class action settlement costs, net 887 - (887) - - - Separation costs 44 (44) - - - - Restructuring and other charges, net 92 - - (92) - - Income from operations 716 85 887 100 - 1,788 Interest income 53 - - - - 53 Interest expense (231) - - - - (231) Other (expense) income, net (219) - - - 232 13 Income from continuing operations before income taxes and minority interest 319 85 887 100 232 1,623 Income taxes (491) (25) - (32) - (548) Minority interest (6) - - - - (6) Income (loss) from continuing operations (178) $ 60 $ 887 $ 68 $ 232 $ 1,069 $ Basic earnings (loss) per share: Income (loss) from continuing operations (0.36) $ 2.15 $ Diluted earnings (loss) per share: Income (loss) from continuing operations (0.36) $ 2.14 $ Weighted-average number of shares outstanding: Basic 497 497 Diluted 497 500 (in millions, except per share data) Adjustments |

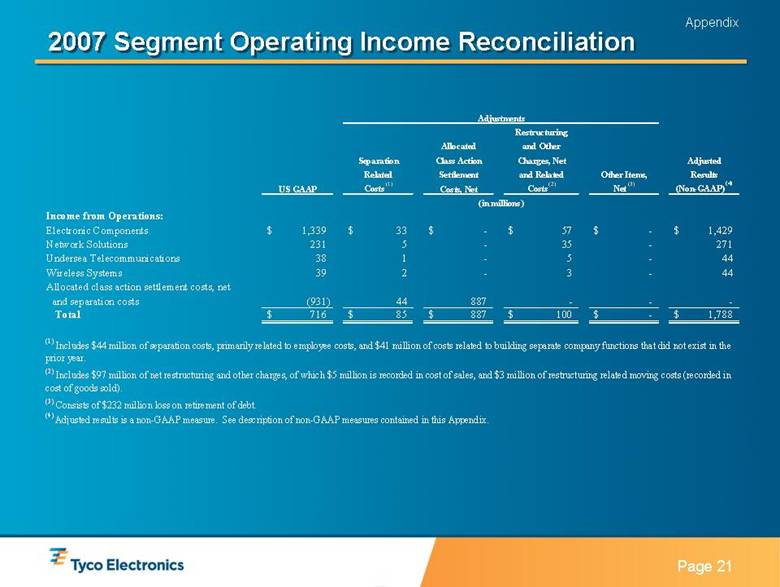

| Page 21 2007 Segment Operating Income Reconciliation Appendix Restructuring Allocated and Other Separation Class Action Charges, Net Adjusted Related Settlement and Related Other Items, Results US GAAP Costs (1) Costs, Net Costs (2) Net (3) (Non-GAAP) (4) Income from Operations: Electronic Components 1,339 $ 33 $ - $ 57 $ - $ 1,429 $ Network Solutions 231 5 - 35 - 271 Undersea Telecommunications 38 1 - 5 - 44 Wireless Systems 39 2 - 3 - 44 Allocated class action settlement costs, net and separation costs (931) 44 887 - - - Total 716 $ 85 $ 887 $ 100 $ - $ 1,788 $ (2) Includes $97 million of net restructuring and other charges, of which $5 million is recorded in cost of sales, and $3 million of restructuring related moving costs (recorded in cost of goods sold). (3) Consists of $232 million loss on retirement of debt. (4) Adjusted results is a non-GAAP measure. See description of non-GAAP measures contained in this Appendix. Adjustments (in millions) (1) Includes $44 million of separation costs, primarily related to employee costs, and $41 million of costs related to building separate company functions that did not exist in the prior year. |

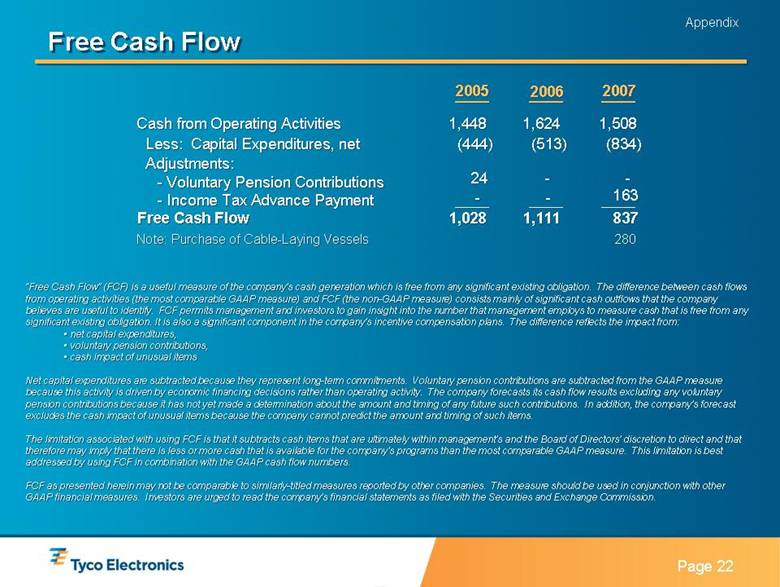

| Page 22 Free Cash Flow Appendix “Free Cash Flow” (FCF) is a useful measure of the company’s cash generation which is free from any significant existing obligation. The difference between cash flows from operating activities (the most comparable GAAP measure) and FCF (the non-GAAP measure) consists mainly of significant cash outflows that the company believes are useful to identify. FCF permits management and investors to gain insight into the number that management employs to measure cash that is free from any significant existing obligation. It is also a significant component in the company’s incentive compensation plans. The difference reflects the impact from: • net capital expenditures, • voluntary pension contributions, • cash impact of unusual items Net capital expenditures are subtracted because they represent long-term commitments. Voluntary pension contributions are subtracted from the GAAP measure because this activity is driven by economic financing decisions rather than operating activity. The company forecasts its cash flow results excluding any voluntary pension contributions because it has not yet made a determination about the amount and timing of any future such contributions. In addition, the company’s forecast excludes the cash impact of unusual items because the company cannot predict the amount and timing of such items. The limitation associated with using FCF is that it subtracts cash items that are ultimately within management’s and the Board of Directors’ discretion to direct and that therefore may imply that there is less or more cash that is available for the company's programs than the most comparable GAAP measure. This limitation is best addressed by using FCF in combination with the GAAP cash flow numbers. FCF as presented herein may not be comparable to similarly-titled measures reported by other companies. The measure should be used in conjunction with other GAAP financial measures. Investors are urged to read the company’s financial statements as filed with the Securities and Exchange Commission. 2005 2006 Cash from Operating Activities 1,448 1,624 Less: Capital Expenditures, net (444) (513) Adjustments: - Voluntary Pension Contributions - Income Tax Advance Payment 24 - Free Cash Flow 1,028 1,111 2007 1,508 (834) 837 163 - - - Note: Purchase of Cable-Laying Vessels 280 |

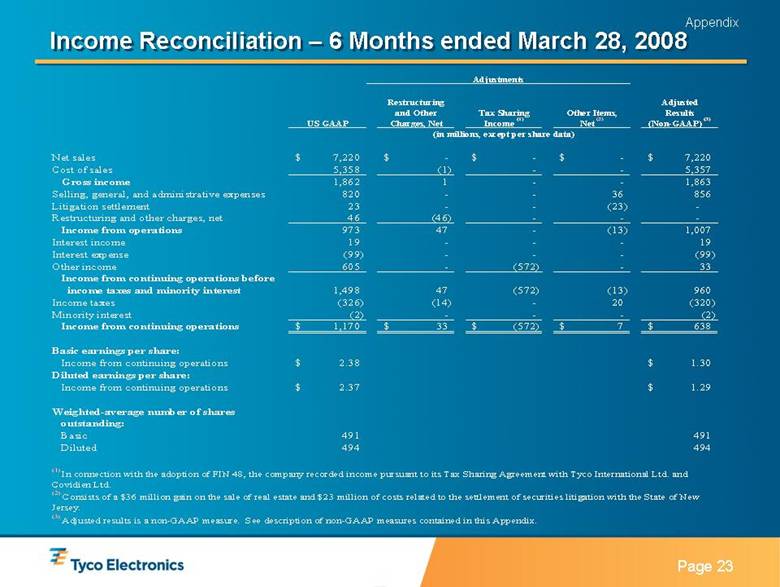

| Page 23 Appendix Income Reconciliation – 6 Months ended March 28, 2008 Restructuring Adjusted and Other Tax Sharing Other Items, Results US GAAP Charges, Net Income (1) Net (2) (Non-GAAP) (3) Net sales 7,220 $ - $ - $ - $ 7,220 $ Cost of sales 5,358 (1) - - 5,357 Gross income 1,862 1 - - 1,863 Selling, general, and administrative expenses 820 - - 36 856 Litigation settlement 23 - - (23) - Restructuring and other charges, net 46 (46) - - - Income from operations 973 47 - (13) 1,007 Interest income 19 - - - 19 Interest expense (99) - - - (99) Other income 605 - (572) - 33 Income from continuing operations before income taxes and minority interest 1,498 47 (572) (13) 960 Income taxes (326) (14) - 20 (320) Minority interest (2) - - - (2) Income from continuing operations 1,170 $ 33 $ (572) $ 7 $ 638 $ Basic earnings per share: Income from continuing operations 2.38 $ 1.30 $ Diluted earnings per share: Income from continuing operations 2.37 $ 1.29 $ Weighted-average number of shares outstanding: Basic 491 491 Diluted 494 494 Adjustments (3) Adjusted results is a non-GAAP measure. See description of non-GAAP measures contained in this Appendix. (in millions, except per share data) (2) Consists of a $36 million gain on the sale of real estate and $23 million of costs related to the settlement of securities litigation with the State of New Jersey. (1) In connection with the adoption of FIN 48, the company recorded income pursuant to its Tax Sharing Agreement with Tyco International Ltd. and Covidien Ltd. |

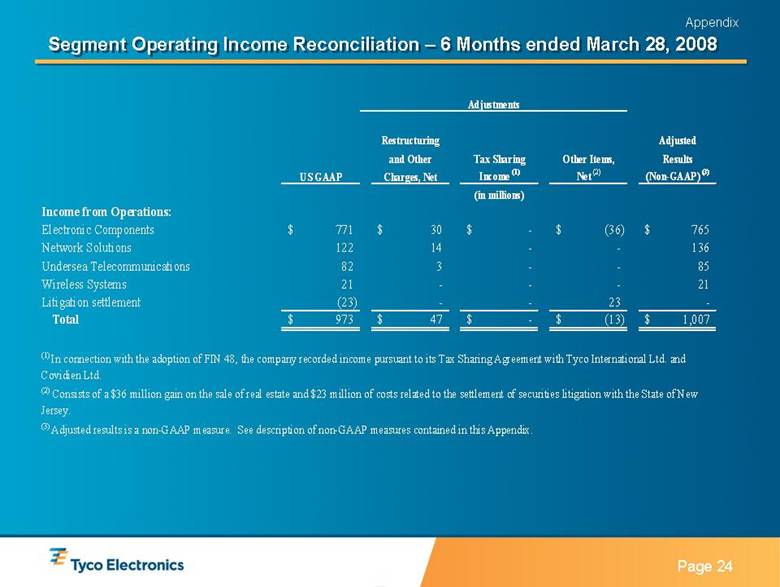

| Page 24 Segment Operating Income Reconciliation – 6 Months ended March 28, 2008 Appendix Restructuring Adjusted and Other Tax Sharing Other Items, Results US GAAP Charges, Net Income (1) Net (2) (Non-GAAP) (3) Income from Operations: Electronic Components 771 $ 30 $ - $ (36) $ 765 $ Network Solutions 122 14 - - 136 Undersea Telecommunications 82 3 - - 85 Wireless Systems 21 - - - 21 Litigation settlement (23) - - 23 - Total 973 $ 47 $ - $ (13) $ 1,007 $ (3) Adjusted results is a non-GAAP measure. See description of non-GAAP measures contained in this Appendix. Adjustments (in millions) (2) Consists of a $36 million gain on the sale of real estate and $23 million of costs related to the settlement of securities litigation with the State of New Jersey. (1) In connection with the adoption of FIN 48, the company recorded income pursuant to its Tax Sharing Agreement with Tyco International Ltd. and Covidien Ltd. |

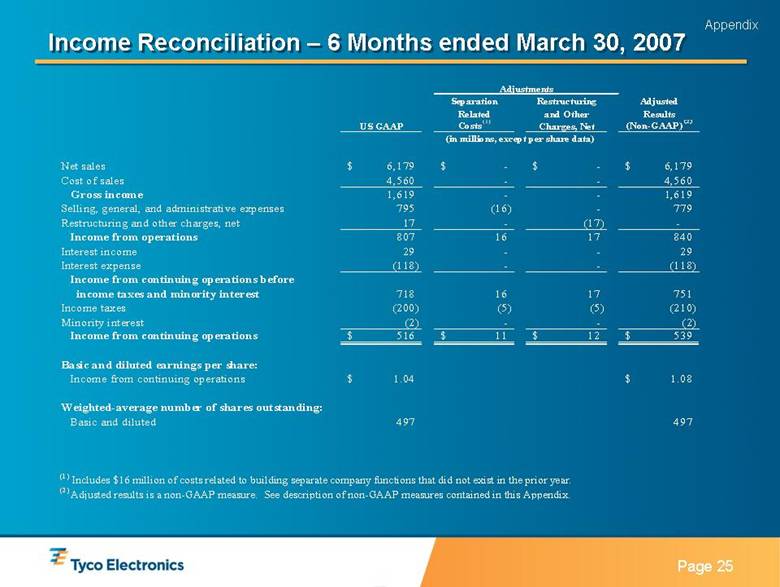

| Page 25 Income Reconciliation – 6 Months ended March 30, 2007 Appendix Separation Restructuring Adjusted Related and Other Results US GAAP Costs (1) Charges, Net (Non-GAAP) (2) Net sales 6,179 $ - $ - $ 6,179 $ Cost of sales 4,560 - - 4,560 Gross income 1,619 - - 1,619 Selling, general, and administrative expenses 795 (16) - 779 Restructuring and other charges, net 17 - (17) - Income from operations 807 16 17 840 Interest income 29 - - 29 Interest expense (118) - - (118) Income from continuing operations before income taxes and minority interest 718 16 17 751 Income taxes (200) (5) (5) (210) Minority interest (2) - - (2) Income from continuing operations 516 $ 11 $ 12 $ 539 $ Basic and diluted earnings per share: Income from continuing operations 1.04 $ 1.08 $ Weighted-average number of shares outstanding: Basic and diluted 497 497 (2) Adjusted results is a non-GAAP measure. See description of non-GAAP measures contained in this Appendix. (in millions, except per share data) (1) Includes $16 million of costs related to building separate company functions that did not exist in the prior year. Adjustments |

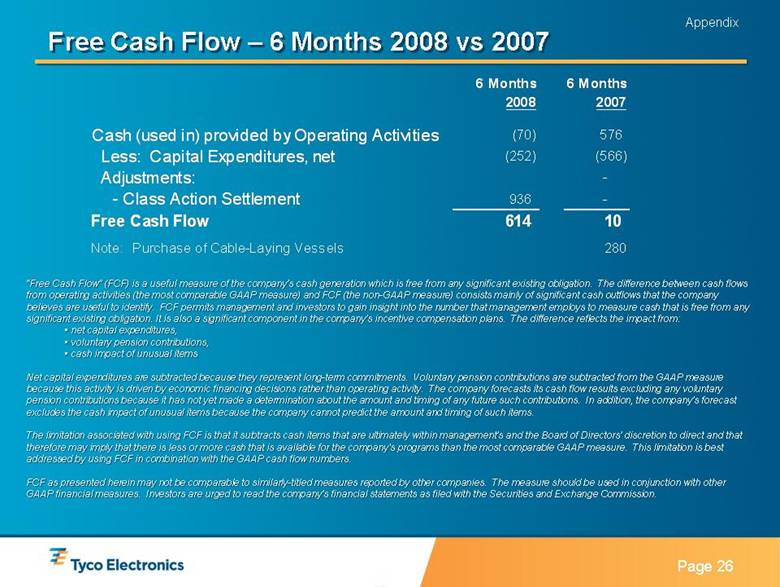

| Page 26 Free Cash Flow – 6 Months 2008 vs 2007 Appendix “Free Cash Flow” (FCF) is a useful measure of the company’s cash generation which is free from any significant existing obligation. The difference between cash flows from operating activities (the most comparable GAAP measure) and FCF (the non-GAAP measure) consists mainly of significant cash outflows that the company believes are useful to identify. FCF permits management and investors to gain insight into the number that management employs to measure cash that is free from any significant existing obligation. It is also a significant component in the company’s incentive compensation plans. The difference reflects the impact from: • net capital expenditures, • voluntary pension contributions, • cash impact of unusual items Net capital expenditures are subtracted because they represent long-term commitments. Voluntary pension contributions are subtracted from the GAAP measure because this activity is driven by economic financing decisions rather than operating activity. The company forecasts its cash flow results excluding any voluntary pension contributions because it has not yet made a determination about the amount and timing of any future such contributions. In addition, the company’s forecast excludes the cash impact of unusual items because the company cannot predict the amount and timing of such items. The limitation associated with using FCF is that it subtracts cash items that are ultimately within management’s and the Board of Directors’ discretion to direct and that therefore may imply that there is less or more cash that is available for the company's programs than the most comparable GAAP measure. This limitation is best addressed by using FCF in combination with the GAAP cash flow numbers. FCF as presented herein may not be comparable to similarly-titled measures reported by other companies. The measure should be used in conjunction with other GAAP financial measures. Investors are urged to read the company’s financial statements as filed with the Securities and Exchange Commission. 6 Months 6 Months 2008 2007 Cash (used in) provided by Operating Activities (70) 576 Less: Capital Expenditures, net (252) (566) Adjustments: - - Class Action Settlement 936 - Free Cash Flow 614 10 Note: Purchase of Cable-Laying Vessels 280 |

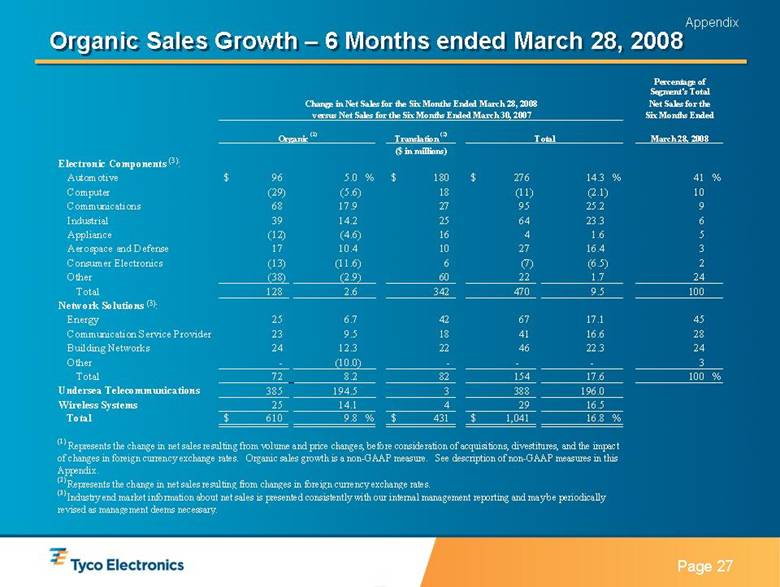

| Page 27 Appendix Organic Sales Growth – 6 Months ended March 28, 2008 Translation (2) Electronic Components (3): Automotive 96 $ 5.0 % 180 $ 276 $ 14.3 % 41 % Computer (29) (5.6) 18 (11) (2.1) 10 Communications 68 17.9 27 95 25.2 9 Industrial 39 14.2 25 64 23.3 6 Appliance (12) (4.6) 16 4 1.6 5 Aerospace and Defense 17 10.4 10 27 16.4 3 Consumer Electronics (13) (11.6) 6 (7) (6.5) 2 Other (38) (2.9) 60 22 1.7 24 Total 128 2.6 342 470 9.5 100 Network Solutions (3): Energy 25 6.7 42 67 17.1 45 Communication Service Provider 23 9.5 18 41 16.6 28 Building Networks 24 12.3 22 46 22.3 24 Other - (10.0) - - - 3 Total 72 8.2 82 154 17.6 100 % Undersea Telecommunications 385 194.5 3 388 196.0 Wireless Systems 25 14.1 4 29 16.5 Total 610 $ 9.8 % 431 $ 1,041 $ 16.8 % (3) Industry end market information about net sales is presented consistently with our internal management reporting and may be periodically revised as management deems necessary. (1) Represents the change in net sales resulting from volume and price changes, before consideration of acquisitions, divestitures, and the impact of changes in foreign currency exchange rates. Organic sales growth is a non-GAAP measure. See description of non-GAAP measures in this Appendix. (2) Represents the change in net sales resulting from changes in foreign currency exchange rates. versus Net Sales for the Six Months Ended March 30, 2007 ($ in millions) Percentage of Segment's Total Change in Net Sales for the Six Months Ended March 28, 2008 Net Sales for the Six Months Ended Organic (1) Total March 28, 2008 |