Exhibit 99.1

A Differentiated Model with

Sustainable Advantage

Investor Presentation

June 3, 2008

Nasdaq: GLRE

This presentation includes statements about future economic performance, finances, expectations, plans and prospects of Greenlight Capital Re, Ltd. (“the Company”) that constitute forward-looking statements for purposes of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those suggested by such statements.

For further information regarding cautionary statements and factors affecting future results, please refer to the Company’s most recent Annual Report on Form 10-K, the Quarterly Report on Form 10-Q filed subsequent to the Annual Report and other documents filed by the Company with the SEC. The Company undertakes no obligation to update or revise publicly any forward-looking statement whether as a result of new information, future developments or otherwise. All information as of March 31, 2008 unless otherwise noted.

2

Short formal presentations, followed by Q&A and a reception

Today’s Agenda

John Andre, Group V.P. A.M. Best – Industry Overview and Rating Process

Len Goldberg, CEO – Background and Vision

Bart Hedges, President and CUO – Underwriting Philosophy and Examples

David Einhorn, Chairman – Investment Review/Preview

Tim Courtis, CFO – Capital and Risk Management

Q&A and Reception

Best’s Perspectives on Reinsurance and

Bermuda Segment

Capacity readily available in nearly all markets

High cedant retentions, capital market solutions and

government actions reduce demand

New entrants and incumbent diversification change

competitive landscape

Bermudan reinsurers expand scope through U.S. E&S

markets and Lloyd’s Syndicates

3

Review of Reinsurance and Bermuda

Segment - continued

Enterprise Risk Management fully embraced

Improved modeling tools enable reinsurers to garner

appropriate rates relative to exposures

Capital management-extensive share repurchase and

increased dividend pay-outs

Subprime impact modest with some exceptions

4

Review of Reinsurance and Bermuda

Segment - continued

Harder to generate adequate risk-adjusted returns

relative to capital at risk

Moderate M&A Activity-no blockbusters

Capital market solutions broadly accepted

5

Preview of Reinsurance and Bermuda

Segment - continued

Anticipating another profitable 2008

Pressure on margins intensifies

Wild-card is catastrophes

Double-digit rate decreases at Jan 1 renewals

Capital & risk management even more critical

Acquisitions likely as growth is hard to come by

6

Financial Trends-Bermuda Insurance

and Reinsurance

2005

(1)

2006

2007

2008P

Net Premiums Written Growth %

5.4

3.2

0.8

3.0

Loss & LAE Ratio

92.8

55.7

54.9

65.0

Underwriting Expense Ratio

26.5

28.3

28.0

28.0

Combined Ratio

119.3

84.1

82.9

93.0

Less: Loss Reserve Development

(1.0)

(2.2)

(5.2)

(2.5)

AY Combined Ratio (Normalized)

120.3

86.3

88.2

95.5

Change in Equity %

5.6

40.7

14.4

3.8

Return on Equity %

(7.0)

17.2

15.9

12.4

7

(1) Excludes Class of 2005 Source: A.M. Best

Best’s Rating Perspective – Bringing it

all Together

Capital strength is the foundation

Sustained, stable operating profitability ensures

future strength

Well-diversified, strong business profile ensures

stability

Depth, experience and stability of management

influences profile

8

9

Why Greenlight Re?

Differentiated, symmetric approach

Low leverage model with significant upside potential

A- rating from A.M. Best with ability to invest 100%

in equities

Proven underwriting and investment capabilities

Uniquely positioned for current market conditions

= Sustainable Advantage

Managing Our Business

10

11

We are a Cayman Islands specialty property and casualty reinsurer

with a differentiated reinsurance and investment strategy

Greenlight Re Vision

Capitalize on inefficiencies in the traditional approach to

reinsurance

Generate superior underwriting economics

Derive superior returns from both sides of the balance sheet

Maintain a highly skilled and focused team

Align long-term management and shareholder interests

Focus on long-term growth in book value per share

12

Greenlight Re Model

Focus on downside on a deal-

by-deal basis

Fewer, bigger deals that are

important to our clients and us

Focus on deal economics

Bottom-up approach to

underwriting portfolio

Portfolio is sum total of good

opportunities

Small team of highly skilled

generalists

Capital preservation on

investment-by-investment basis

Concentrate on best

investment ideas

Focus on business economics

Bottom-up approach to

investment selection

Portfolio is sum total of good

opportunities

Small team of highly skilled

generalists

Liability

Asset

DELIVER SUPERIOR LONG-TERM GROWTH IN BOOK VALUE

A fundamentally different, symmetric approach to the reinsurance business

13

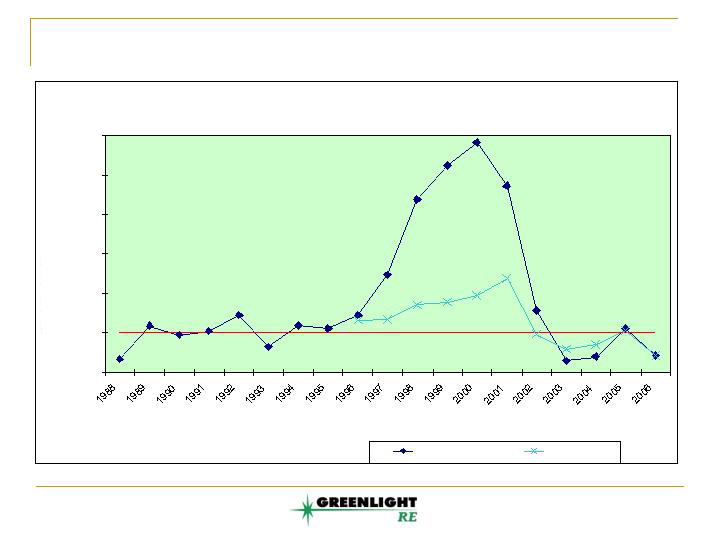

Cyclical Opportunities

Source: National Association of Insurance Commissioners (NAIC) Annual Statement Database.

Casualty Excess Reinsurance

80.0%

100.0%

120.0%

Combined

Ratio

140.0%

160.0%

180.0%

200.0%

Current Estimate

Initial Estimate

14

Underwriting Philosophy

Lead underwriter for majority of transactions

Generalists with flexibility to look at a wide range of

opportunities

Rigorous modeling combined with practical underwriting

experience

Each contract stands on its own

Incorporate risk-aversion into pricing

Focus on transaction economics rather than on earnings or

premium growth

Cradle-to-grave underwriting and administration process

15

Select contracts which offer superior economic returns

Concentrate on underserved/dislocated markets with unique

needs

Focus on strategic relationships rather than price driven or

commodity buyers

Frequency business orientation; severity business more

opportunistic

Generalist team approach with client access to decision

makers

Service both global and Cayman markets

Underwriting Opportunities

Our Underwriters

16

17

Specialist underwriter requires rated reinsurer for program

$20 million in annual premium, maximum loss of $1 million on any

one event (frequency business)

Client wants to share risk with us

Client values underwriting results and is willing to give up float

Solution:

We reinsure 100% of the business and then share underwriting

results with a Cayman captive owned by the specialist

underwriter

We keep the float (we share economic risk, not cash flows)

which also acts as collateral

Underwriting Strategy: An Attractive Deal

18

Company requires $100 million protection against severity losses

The level of protection required has never been breached, and

models show it is a 1-in-100 year event

Client shares little/no risk once our cover is breached

Company offers $5 million of premium

Result:

The market accepts this deal and 10 different reinsurers

participate, but not Greenlight Re

Significant model uncertainty, enormous downside risk, non-

lead position, commoditized

Underwriting Strategy: Taking a Pass

19

Investment Approach

Portfolio managed exclusively by DME Advisors, an affiliate of

Greenlight Capital

Value-oriented strategy

Primarily long/short publicly-traded equity and corporate debt

securities

Lower volatility than equity indices

Limited leverage

Investment program matched to Greenlight Re’s goals

Maximize total risk-adjusted return with focus on capital

preservation

Direct claim on assets

14.6% annualized return (net of fees) from August 2004 through

May 2008

20

Investment Portfolio Summary

Data since IPO (13 months May 2007 - May 2008):

Performance

Average

GLRE

S&P 500

(gross)

Exposure

Annualized Return

12.9%

-3.4%

Long

-0.9%

90%

Annualized Std. Dev

8.5%

11.5%

Short

18.0%

-53%

Current Top 5 Long Positions

Current Position Concentration

Ameriprise Financial, Inc

Long

Short

Arkema

Top 5

36%

22%

Criteria Caixa Corp

Top 10

55%

31%

Microsoft Corporation

Target Corp

Exposure

97%

-52%

Current Investment Environment

21

22

Current Investment Environment

Credit crisis still playing out

Defensively positioned

Long unlevered companies at low absolute valuations

with strong market positions and/or internal restructuring

opportunities

Short credit sensitive financials and companies at high

multiples of earnings estimates that assume a second-

half recovery

Don’t be a hero

23

Compensation Framework

Align management and shareholders

Compensate for true increase in economic value, not for

premium growth, GAAP accounting, irrational

exuberance or “fully deploying capital”

Cash Bonus Program:

Track economics of every contract individually

No bonus when underwriting ROE less than Risk Free return

Target Bonus when ROE = target ROE

Uncapped upside when ROE in excess of target

First bonus payment after three years with continuous roll-forward

So far, so good

24

Risk and Capital Management

2007 premium to capital ratio of 0.2, anticipated to

increase as portfolio develops

Low leverage play:

No corporate debt

Low premium-to-capital and reserve-to-capital ratios

Frequency business orientation

CEO and CFO review reserves by account every quarter

Proposal to amend Company’s Articles of Association to

allow flexibility for share repurchases

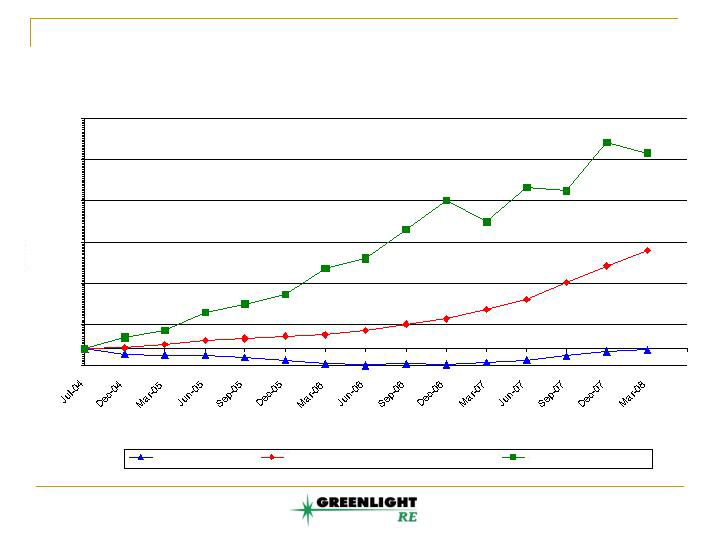

($10)

$15

$40

Millions

$65

$90

$115

$140

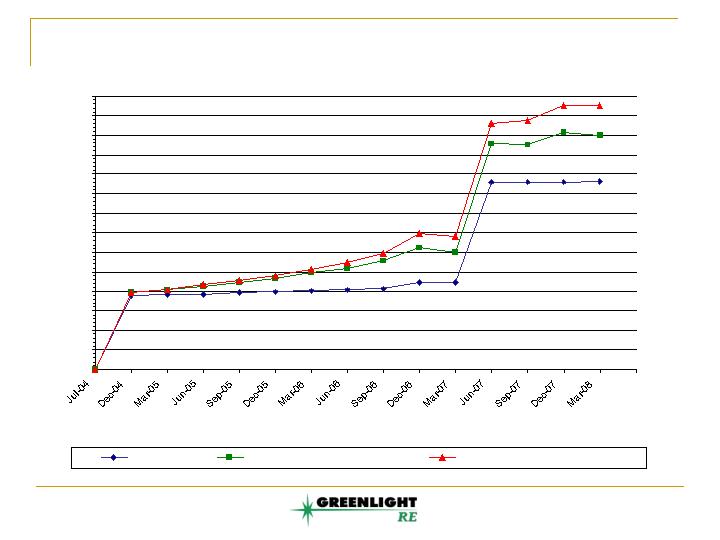

Quarter ended

Cumulative net UW profit

Cumulative net UW profit plus risk free inv. income

Cumulative Actual net income

25

Contributions to Retained Earnings

26

NA

NA

221.0

99.0%

Book Value Growth

$ in millions

Notes:

1. The Composite Ratio is the ratio of underwriting losses incurred and acquisition costs, excluding internal expenses, to premiums earned.

2. The Combined Ratio is the sum of the loss ratio, acquisition cost ratio and the internal expense ratio.

3. 2004 and 2005 have been adjusted for principal outstanding on a promissory note which was fully repaid in 2006.

$ per share

NA

NA

248.0

98.6%

75.5

109.6

312.2

105.9%

Composite Ratio1

Combined Ratio2

Capital and Surplus3

Invested Assets/Capital

80.0

92.2

605.6

110.0%

14.6% CAGR in fully diluted book value per share since inception

80.2

96.4

600.1

111.7%

$(4.8)

$35.3

$57.0

$26.3

$6.8

$10.40

$11.63

$14.27

$16.57

$16.40

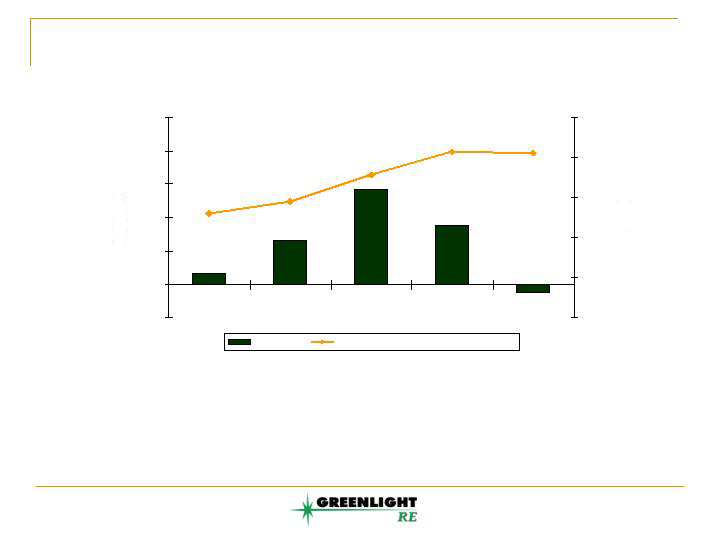

(20.0)

0.0

20.0

Net Income

40.0

60.0

80.0

100.0

2004

2005

2006

2007

1Q 2008

$0.00

$4.00

$8.00

BVPS

$12.00

$16.00

$20.00

Net Income

Basic Adjusted Book Value per Share

Net Invested Assets

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$550

$600

$650

$700

Millions

Quarter ended

Capital

Capital + Retained Earnings

Capital + Retained Earnings + Float

27

Current ROE Sensitivity

Assumptions:

Earned Premium = 20% of capital

Invested Assets = 120% of capital

Combined Ratio (%)

80.0

90.0

100.0

110.0

120.0

5.0

10

8

6

4

2

10.0

16

14

12

10

8

15.0

22

20

18

16

14

20.0

28

26

24

22

20

Investment

Return

(%)

25.0

34

32

30

28

26

28

Combined Ratio (%)

80.0

90.0

100.0

110.0

120.0

5.0

24

16

9

1

(6)

10.0

33

25

18

10

3

15.0

41

34

26

19

11

20.0

50

43

35

28

20

Investment

Return

(%)

25.0

59

51

44

36

29

29

Hypothetical ROE Sensitivity

Assumptions:

Earned Premium = 75% of capital

Invested Assets = 175% of capital

30

Why Greenlight Re?

Differentiated, symmetric approach

Low leverage model with significant upside potential

A- rating from A.M. Best with ability to invest 100% in

equities

Proven underwriting and investment capabilities

Uniquely positioned for current market conditions

= Sustainable Advantage

31

Q&A

###

Forward-Looking Statements

This news release contains forward-looking statements within the meaning of the U.S. federal securities laws. We intend these forward-looking statements to be covered by the safe harbor provisions for forward-looking statements in the U.S. Federal securities laws. These statements involve risks and uncertainties that could cause actual results to differ materially from those contained in forward-looking statements made on behalf of the Company. These risks and uncertainties include the impact of general economic conditions and conditions affecting the insurance and reinsurance industry, the adequacy of our reserves, our ability to assess underwriting risk, trends in rates for property and casualty insurance and reinsurance, competition, investment market fluctuations, trends in insured and paid losses, catastrophes, regulatory and legal uncertainties and other factors described in our annual report on Form 10-K filed with the Securities Exchange Commission. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

About Greenlight Capital Re, Ltd.

Greenlight Re (www.greenlightre.ky) is a specialty property and casualty reinsurance company based in the Cayman Islands. The Company provides a variety of custom-tailored reinsurance solutions to the insurance, risk retention group, captive and financial marketplaces. Established in 2004, Greenlight Re selectively offers customized reinsurance solutions in markets where capacity and alternatives are limited. With a focus on deriving superior returns from both sides of the balance sheet, Greenlight Re’s assets are managed according to a value-oriented equity-focused strategy that complements the Company’s business goal of long-term growth in book value per share.

Contact:

Alex Stanton

Stanton Crenshaw Communications

(212) 780-1900

alex@stantoncrenshaw.com