China Skyrise Digital Service (CSKD) Inactive

Filed: 13 Aug 10, 12:00am

August 13, 2010

Kathleen Collins

Accounting Branch Chief

Division of Corporation Finance

U.S. Securities and Exchange Commission

100 F Street, N.E., Mail Stop 4561

Washington, D.C. 20549

Re: China Skyrise Digital Service, Inc.

Form 10-K for the Year Ended December 31, 2009

File No. 333-139940

Dear Ms. Collins:

On behalf of China Skyrise Digital Service, Inc. (the “Company,” “we,” or “our”), we hereby submit the following responses to the comments of the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) received on July 1, 2010, with respect to our Form 10-K for the Year Ended December 31, 2009 (the “10-K”). We intend to file an Amendment No. 1 to the 10-K (the “10-K/A”) with the Commission, as necessary, as soon as we determine which of the Staff’s comments will need to be addressed in such amendments.

We understand and agree that:

a. the Company is responsible for the adequacy and accuracy of the disclosure in the filing;

b. the Company’s comments or changes to disclosure in response to Staff comments do not foreclose the Commission from taking any action with respect to the filing; and

c. the Company may not assert Staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

For the convenience of the Staff, each of the Staff’s comments is included and is followed by the corresponding response of the Company. Unless the context indicates otherwise, references in this letter to “we,” “us” and “our” refer to the Company on a consolidated basis.

Kathleen Collins

Accounting Branch Chief

August 13, 2010

Page 2

Response: We will revise the description of our product and service offerings in future filings, to correctly reflect that we are engaged in the development, sale and maintenance of residential safety and video surveillance packaged solutions, and that because the majority of our revenues are project based, they are generally non-recurring. We will also clarify that we offer installation services to those of our customers who request it but that our installation services have historically been an insignificant portion of our total revenues.

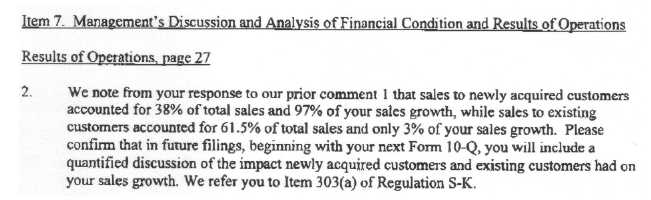

Response: We note your comment and we hereby confirm that in future filings, beginning with our Form 10-Q for the period ended June 30, 2010, we will include a qualified discussion of the impact newly acquired customers and existing customers had on our sales growth.

Kathleen Collins

Accounting Branch Chief

August 13, 2010

Page 3

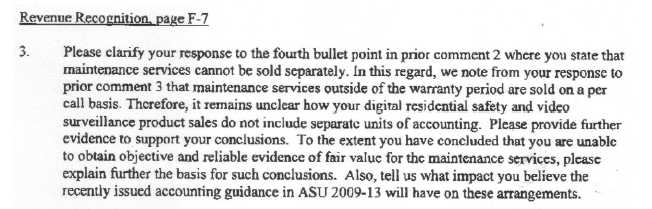

Response: We do not sell installation and maintenance services separately from sales of our surveillance products. The maintenance services sold outside of warranty period are only an extension of existing maintenance services provided at the time of sale. So far we have only extended maintenance services for a few projects and the income from these services are insignificant.

It is difficult for us to obtain reliable evidence of the fair value of the maintenance services provided with our products as they are closely related to our products and there is no open market for such services. We believe that the recently issued accounting guidance in ASU 2009-13 will have little impact on our current arrangements. We understand that if we should sell standalone maintenance services in the future or we are later able to establish an objective selling price for our current maintenance services, we will separately account for the revenue from such services.

Response: The language on page 2 of the Form 10-K was an error. That disclosure should read “Maintenance services in our packaged solutions are included for the first two years following installation, however, our customers may extend such maintenance services after the expiration of this two-year period.”

Kathleen Collins

Accounting Branch Chief

August 13, 2010

Page 4

Response: Our contractual arrangements include customer acceptance provisions for our products but do not include a right of return. Customer acceptance of a product is established upon successful testing of the product by the customer.

Response: Customized software relate to any ad hoc customer software requirements related to our projects. So far our revenue from the sale of customized software is insignificant and we have not yet signed any contracts to provide customer support for customized software systems. As we receive more revenue from the sale of customized software we will separately account for revenue.

* * *

Kathleen Collins

Accounting Branch Chief

August 13, 2010

Page 5

If you would like to discuss our response or any other matters regarding the Company, please contact Louis A. Bevilacqua, Esq. of Pillsbury Winthrop Shaw Pittman LLP, our outside special securities counsel at (202) 663-8158.

Very truly yours,

CHINA SKYRISE DIGITAL SERVICE INC.

By:/s/ Mingchun Zhou

Mingchun Zhou

Chief Executive Officer

cc: Louis A. Bevilacqua, Esq.

Dawn Bernd-Schulz, Esq.