2015 & 2014 ANNUAL REP

Exhibit 99.8

KKR Nautilus Aggregator Limited

KKR NAUTILUS AGGREGATOR LIMITED Financial Statements as of and for the Years Ended December 31, 2015 and 2014 (Unaudited) | |

These financial statements have not been audited by our independent accountants, and they assume no responsibility for such financial statements.

KKR NAUTILUS AGGREGATOR LIMITED

TABLE OF CONTENTS

Page

FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED DECEMBER 31, 2015 AND 2014 (UNAUDITED):

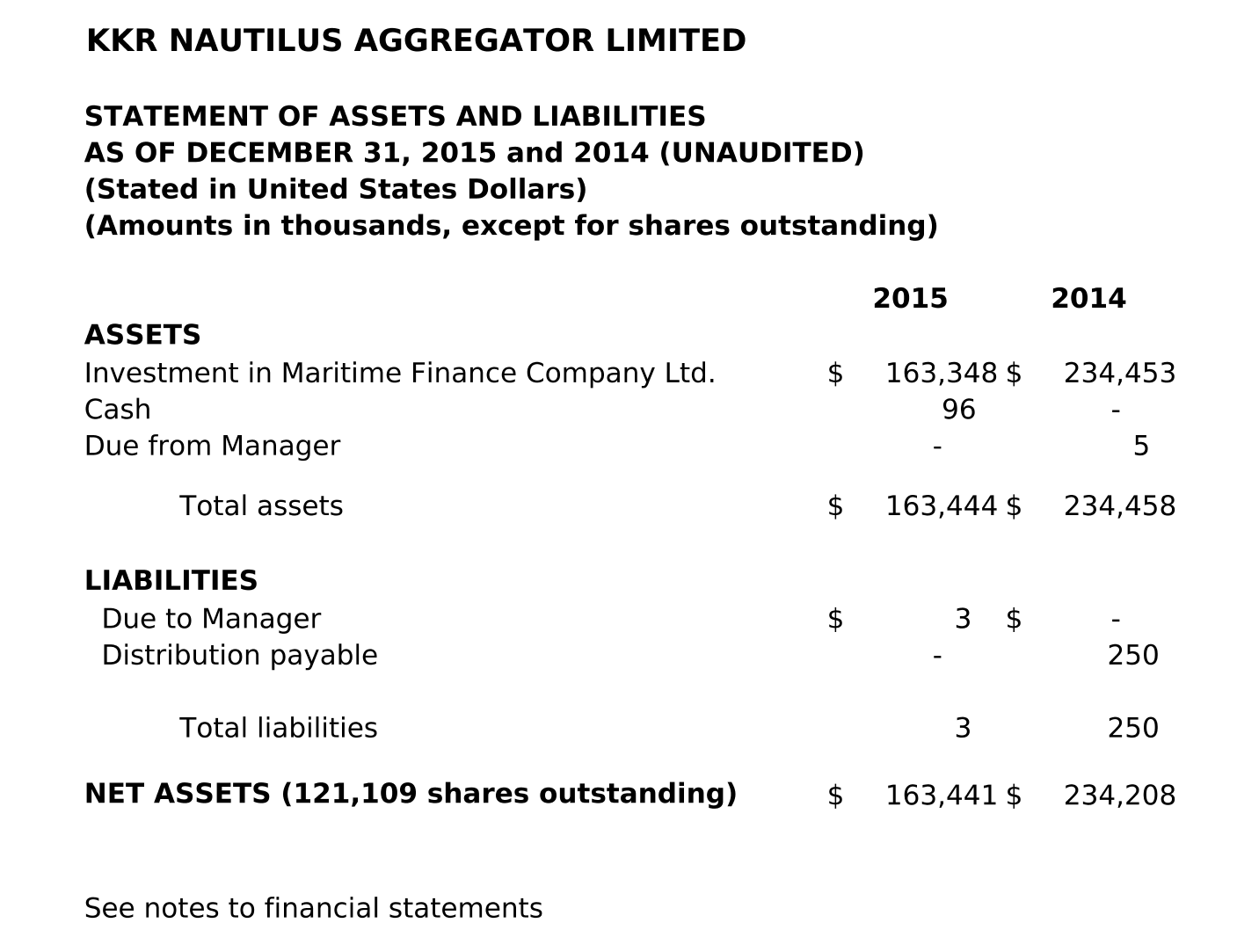

Statement of Assets and Liabilities 1

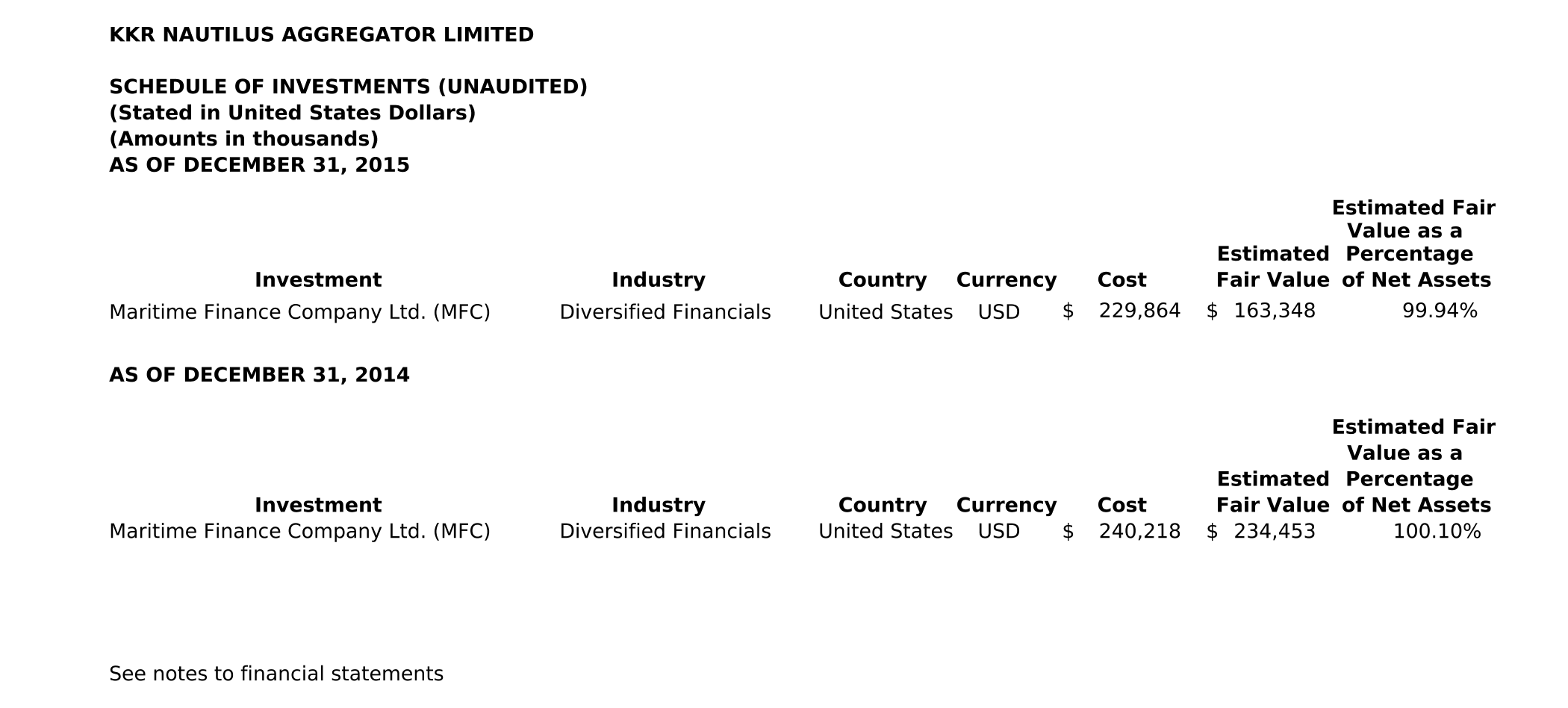

Schedule of Investments 2

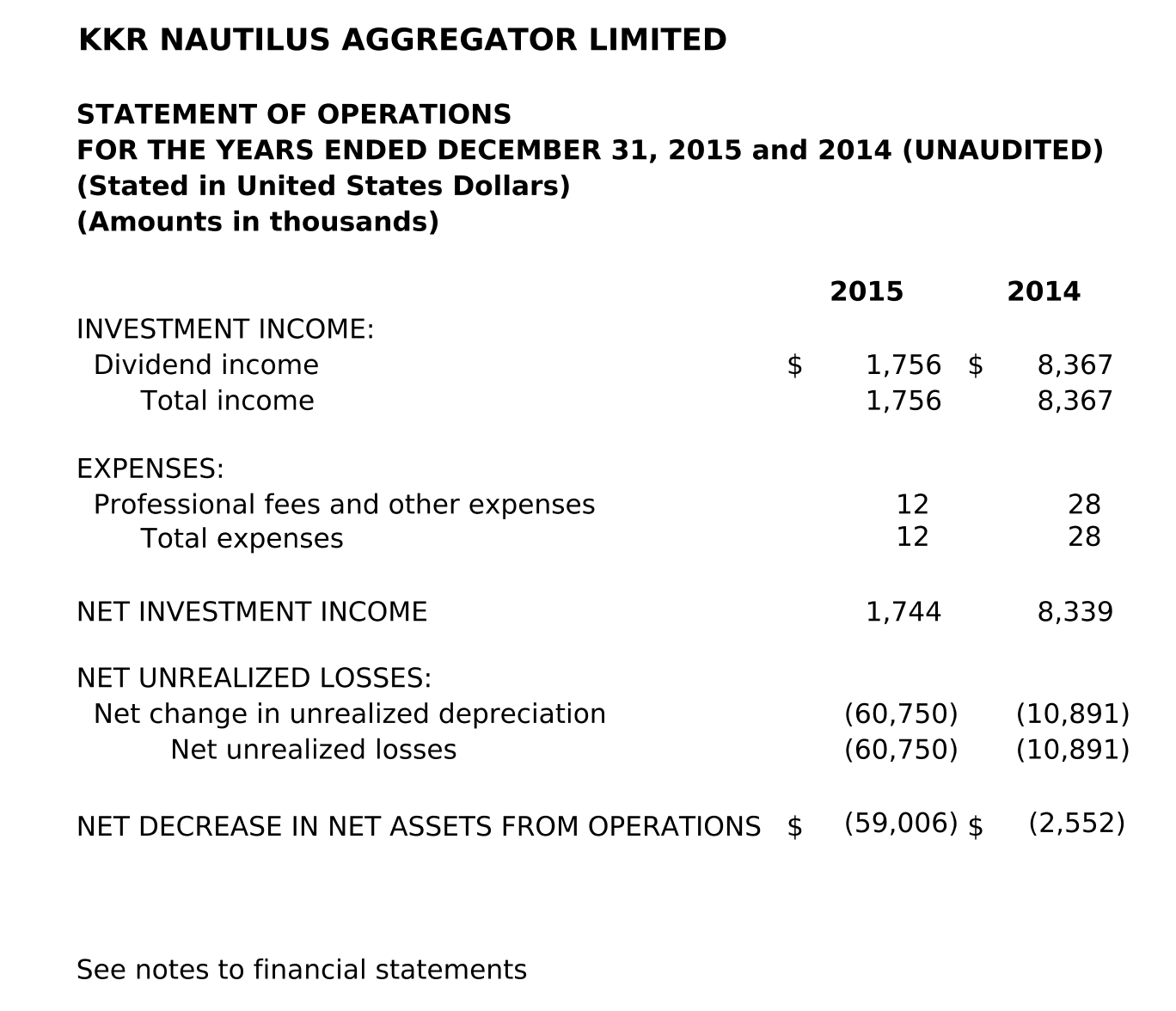

Statement of Operations 3

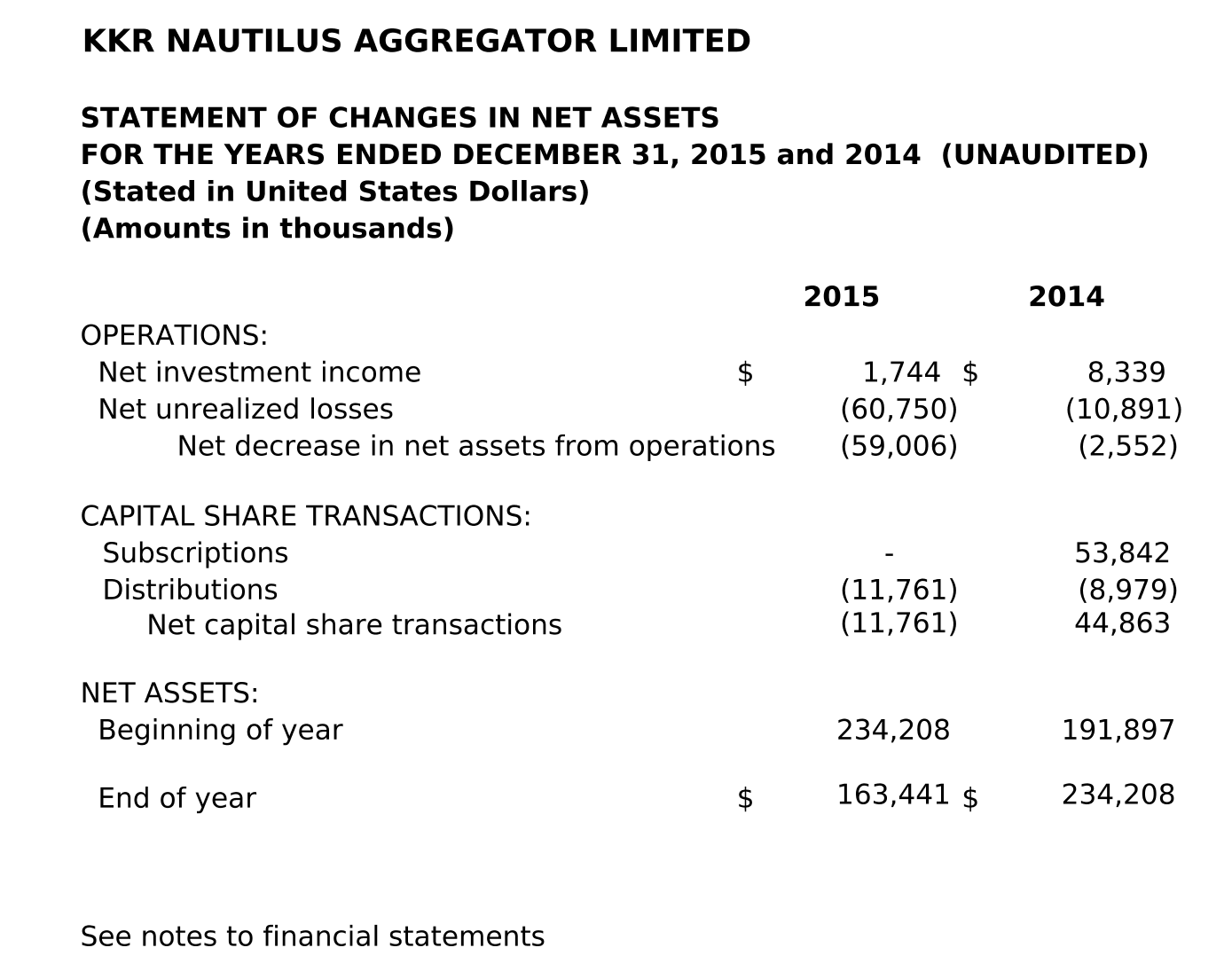

Statement of Changes in Net Assets 4

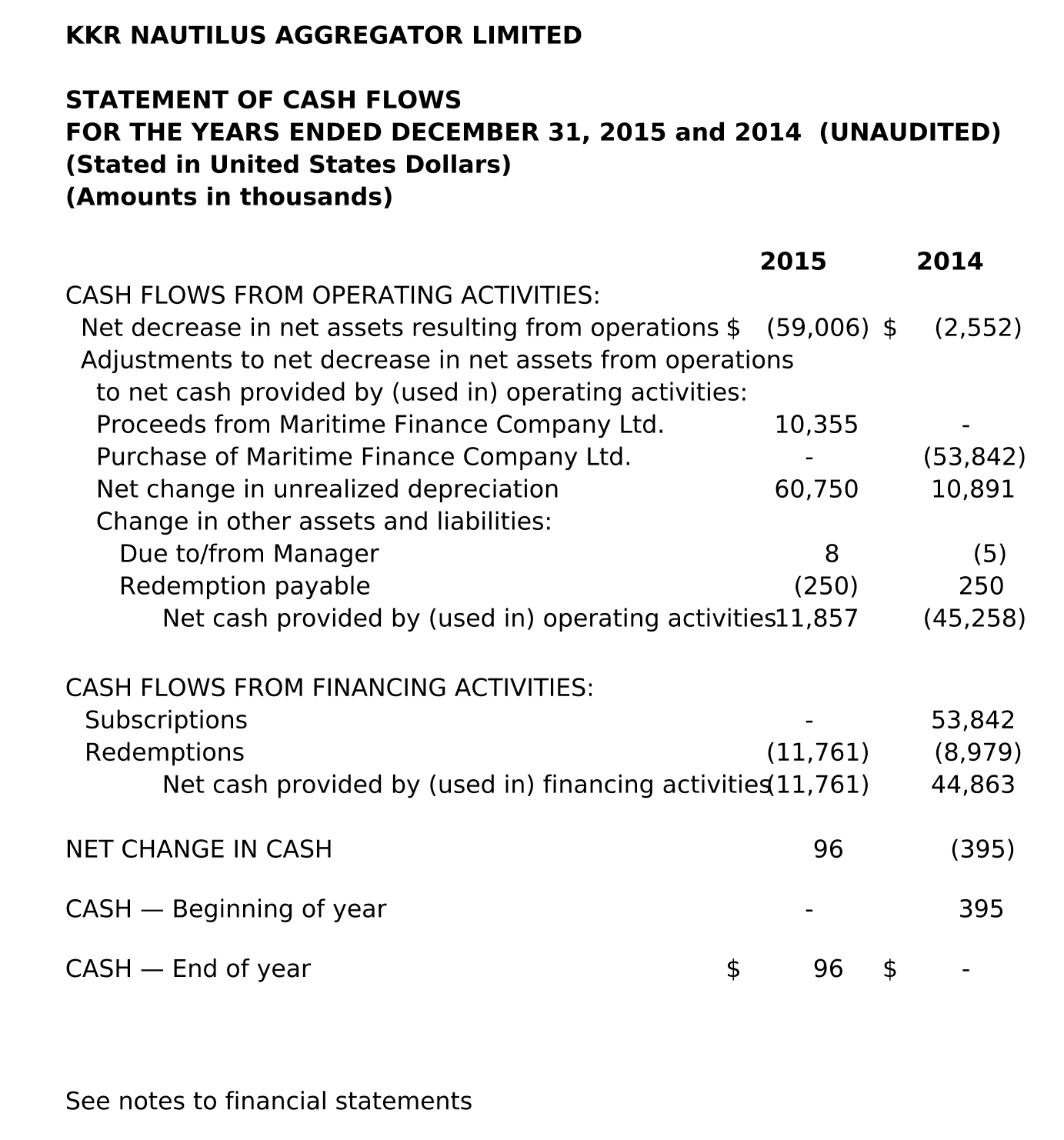

Statement of Cash Flows 5

Notes to Financial Statements 6-13

Statement of Assets and Liabilities 1

Schedule of Investments 2

Statement of Operations 3

Statement of Changes in Net Assets 4

Statement of Cash Flows 5

Notes to Financial Statements 6-13

KKR NAUTILUS AGGREGATOR LIMITED

NOTES TO FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2015 AND 2014 (UNAUDITED)

(STATED IN UNITED STATES DOLLARS)

| 1. | ORGANIZATION |

KKR Nautilus Aggregator Limited (the “Fund”), an exempted company organized under the provisions of the Companies Law of the Cayman Islands, was formed and registered under the Mutual Funds Law of the Cayman Islands on July 25, 2013. The Fund received its initial investor subscriptions and commenced operations on September 18, 2013 The Directors of the Fund are employees of KKR Credit Advisors (US) LLC (“KKR Credit” and “the Manager”) and KKR Credit manages the day-to-day operations of the Fund. KKR Credit is a wholly owned subsidiary of Kohlberg Kravis Roberts & Co. L.P. (“KKR”).

The Fund’s primary investment objective is to make an indirect investment in the Maritime Finance Company Ltd.

The Fund charges no management fee or performance-based compensation to its investors.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING PRINCIPLES |

Basis of Presentation — The Fund is considered an investment company as defined in Accounting Standards Codification (“ASC”) Topic 946 Financial Services – Investment Companies (“ASC 946”). The accompanying financial statements are presented in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”), using the specialized guidance in ASC 946. The functional currency of the Fund is Canadian dollar and the financial statements presented herein are presented in Canadian dollars.

Use of Estimates — The preparation of financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that could affect the amounts reported in the Fund’s financial statements and accompanying notes. Actual results could differ from management’s estimates.

Investments — Investments are carried at estimated fair value and are accounted for on a trade-date basis. Distribution income is recorded when declared.

Cash and Cash Equivalents — Cash and cash equivalents include cash on hand and cash held in banks. There were no cash equivalents as of December 31, 2015 and December 31, 2014.

Income Taxes —The Fund is a Cayman Islands exempted company. The Cayman Islands do not impose income tax and as such, the Fund has not incurred any Cayman Islands income tax expense. The Fund is treated as a partnership for U.S. federal income tax purposes and is generally not subject to U.S. federal income tax at the entity level, but the Fund may own investments that from time to time generate income that is subject to certain foreign tax withholding. Federal and state income tax statutes require that the income or loss of a Fund be included in the tax returns of the individual partners.

In accordance with the authoritative guidance the Fund determines whether a tax position of the Fund is more likely than not to be sustained upon examination by the applicable taxing authority, including the resolution of any related appeals or litigation processes, based on the technical merits of the position. The tax benefit to be recognized is measured as the largest amount of benefit that is greater than 50% likely of being realized upon ultimate settlement, which could result in the Fund recording a tax liability that would reduce net assets. The Fund reviews and evaluates tax positions in its major jurisdictions and determines whether or not there are uncertain tax positions that require financial statement recognition. Based on this review, the Fund has determined the major tax jurisdictions are where the Fund is organized and where the Fund makes investments; however no reserves for uncertain tax positions were required to have been recorded as a result of the adoption of such guidance for any of the Fund’s open tax years. If the Fund determines it does not have a U.S federal tax return filing requirement for a certain year, such year remains open indefinitely. The Fund is additionally not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months. As a result, no other income tax liability or expense has been recorded in the accompanying financial statements.

Fair Value Measurements — Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Where available, fair value is based on observable market prices or parameters, or derived from such prices or parameters. Where observable prices or inputs are not available, valuation models are applied. These valuation techniques involve some level of management estimation and judgment, the degree of which is dependent on the price transparency for the instruments or market and the instruments’ complexity for disclosure purposes.

Assets and liabilities recorded at fair value in the statement of assets and liabilities are categorized based upon the level of judgment associated with the inputs used to measure their value. Hierarchical levels, as defined under U.S. GAAP, are directly related to the amount of subjectivity associated with the inputs to fair valuations of these assets and liabilities, and are as follows:

Level 1 — Inputs are unadjusted, quoted prices in active markets for identical assets or liabilities at the measurement date.

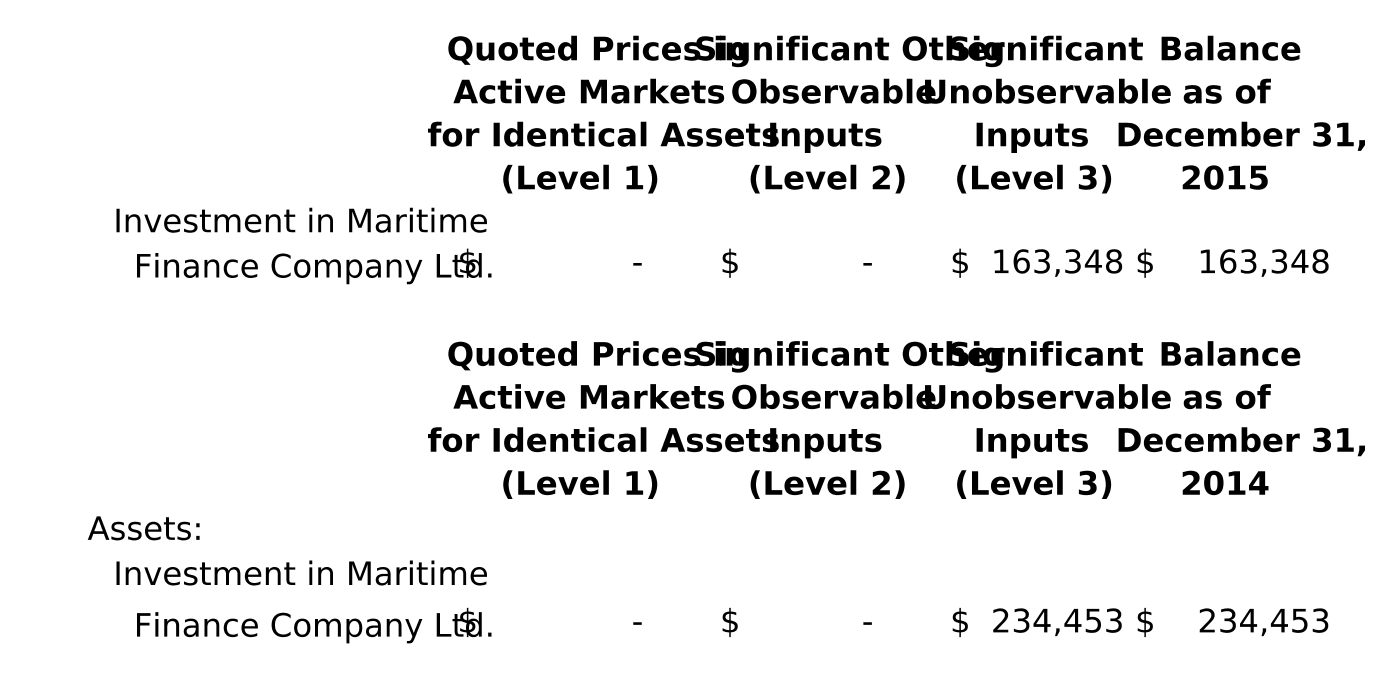

There were no assets or liabilities in this category as of December 31, 2015 and December 31, 2014.

Level 2 — Inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. Level 2 inputs include quoted prices for similar instruments in active markets, and inputs other than quoted prices that are observable for the asset or liability.

There were no assets or liabilities in this category as of December 31, 2015 and December 31, 2014.

Level 3 — Inputs are unobservable inputs for the asset or liability, and include situations where there is little, if any, market activity for the asset or liability.

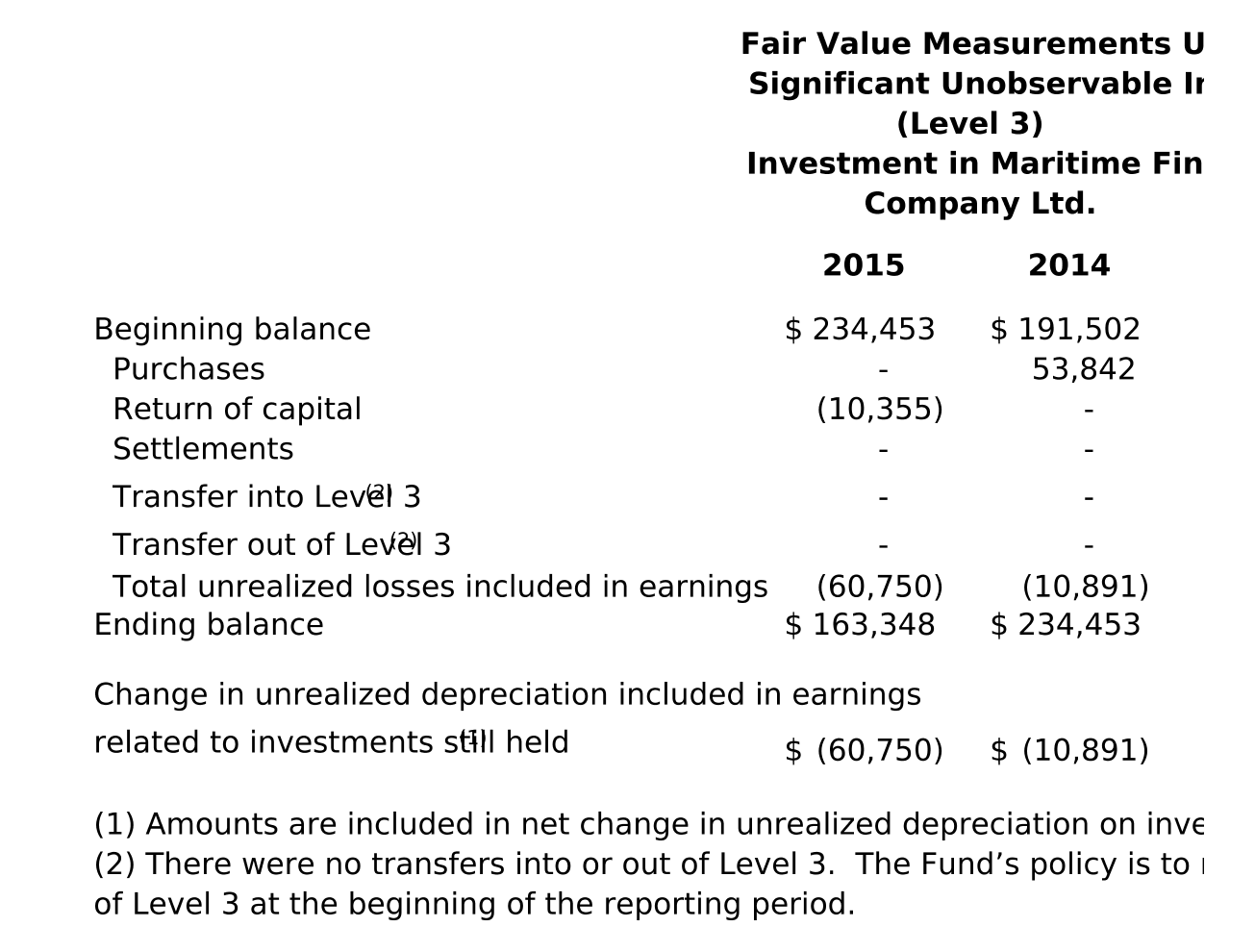

The Fund’s investment in Maritime Finance Company Ltd. was valued using Level 3 inputs as of December 31, 2015 and December 31, 2014.

A significant decrease in the volume and level of activity for the asset or liability is an indication that transactions or quoted prices may not be representative of fair value because in such market conditions there may be increased instances of transactions that are not orderly. In those circumstances, further analysis of transactions or quoted prices is needed, and a significant adjustment to the transactions or quoted prices may be necessary to estimate fair value.

The availability of observable inputs can vary depending on the financial asset or liability and is affected by a wide variety of factors, including, for example, the type of product, whether the product is new, whether the product is traded on an active exchange or in the secondary market, and the current market condition. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised by the Fund in determining fair value is greatest for instruments categorized in Level 3. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement in its entirety falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The Fund’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and consideration of factors specific to the asset. The variability of the observable inputs affected by the factors described above may cause transfers between Levels 1, 2, and/or 3, which the Fund recognizes at the beginning of each reporting period.

Many financial assets and liabilities have bid and ask prices that can be observed in the marketplace. Bid prices reflect the highest price that the Fund and others are willing to pay for an asset. Ask prices represent the lowest price that the Fund and others are willing to accept for an asset. For financial assets and liabilities whose inputs are based on bid-ask prices, the Fund does not require that fair value always be a predetermined point in the bid-ask range. The Fund’s policy is to allow for mid-market pricing and adjusting to the point within the bid-ask range that meets the Fund’s best estimate of fair value.

Depending on the relative liquidity in the markets for certain assets, the Fund may transfer assets to Level 3 if the Fund determines that observable quoted prices, obtained directly or indirectly, are not available. The valuation techniques used for the assets and liabilities that are valued using Level 3 inputs of the fair value hierarchy are described below.

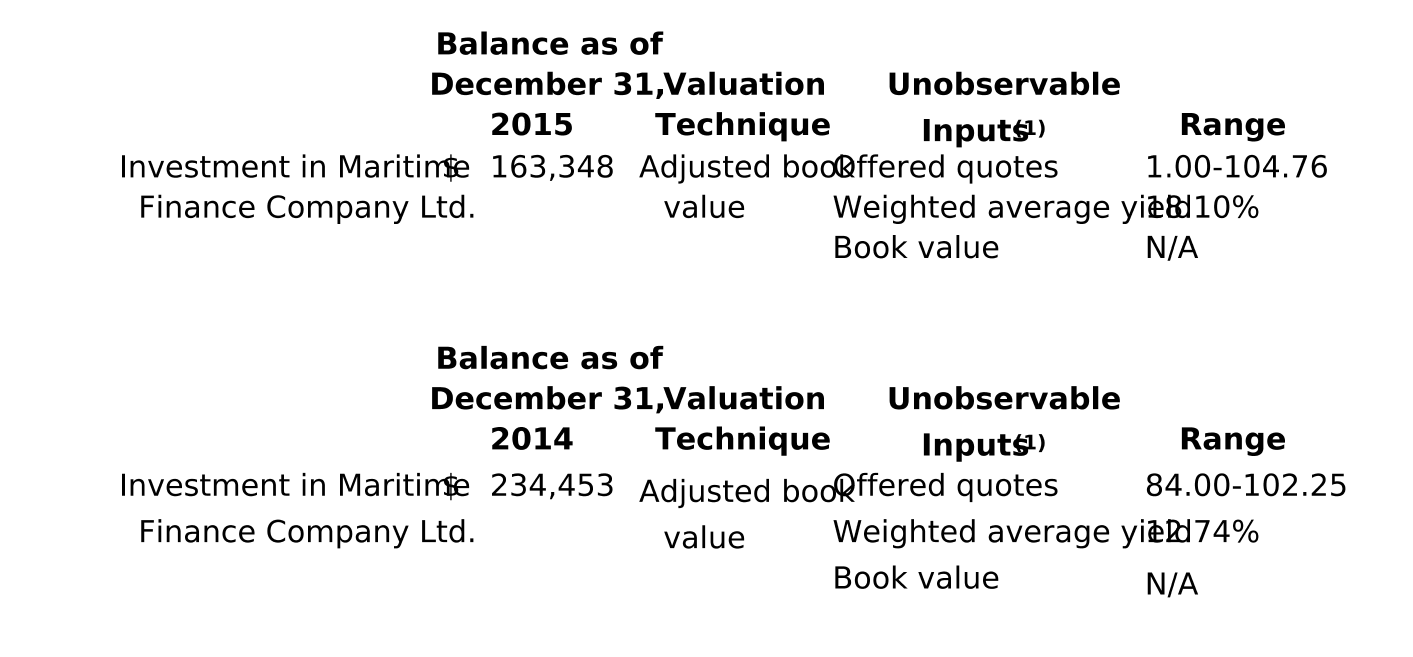

Investment in Maritime Finance Company Ltd. — The investment in Maritime Finance Company Ltd. was initially valued at the transaction price and subsequently valued using an internally developed model in the absence of readily observable market prices. Valuation models are generally based on market and income (discounted cash flow) approaches, in which various internal and external factors are considered. Factors include key financial inputs and recent public and private transactions for comparable investments. Key inputs used for the adjusted book value approach include offered quotes, weighted average yield and book value.

Key unobservable inputs that have a significant impact on the Fund’s Level 3 valuations as described above are included in Note 5. The Fund utilizes several unobservable pricing inputs and assumptions in determining the fair value of its Level 3 investments. These unobservable pricing inputs and assumptions may differ by asset and in the application of the Fund’s valuation methodologies. The reported fair value estimates could vary materially if the Fund had chosen to incorporate different unobservable pricing inputs and other assumptions or, for applicable investments, if the Fund only used either the discounted cash flow methodology or the market comparables methodology instead of assigning a weighting to both methodologies.

Valuation Process — The valuation process involved in Level 3 measurements for assets and liabilities is completed on a quarterly basis and is designed to subject the valuation of Level 3 investments to an appropriate level of consistency, oversight and review. KKR Credit utilizes a valuation committee, whose members consist of the KKR Credit’s Chief Financial Officer, General Counsel and certain other employees of the KKR Credit. The valuation committee is responsible for coordinating and implementing the Fund’s quarterly valuation process.

Investments are generally valued based on quotations from third party pricing services, unless such a quotation is unavailable or is determined to be unreliable or inadequately representing the fair value of the particular assets. In that case, valuations are based on either valuation data obtained from one or more other third party pricing sources, including broker dealers, or will reflect the valuation committee’s good faith determination of estimated fair value based on other factors considered relevant. For assets classified as Level 3, the investment professionals are responsible for documenting preliminary valuations based on various factors including their evaluation of financial and operating data, company specific developments, market valuations of comparable companies and model projections discussed above. All valuations are approved by the valuation committee.

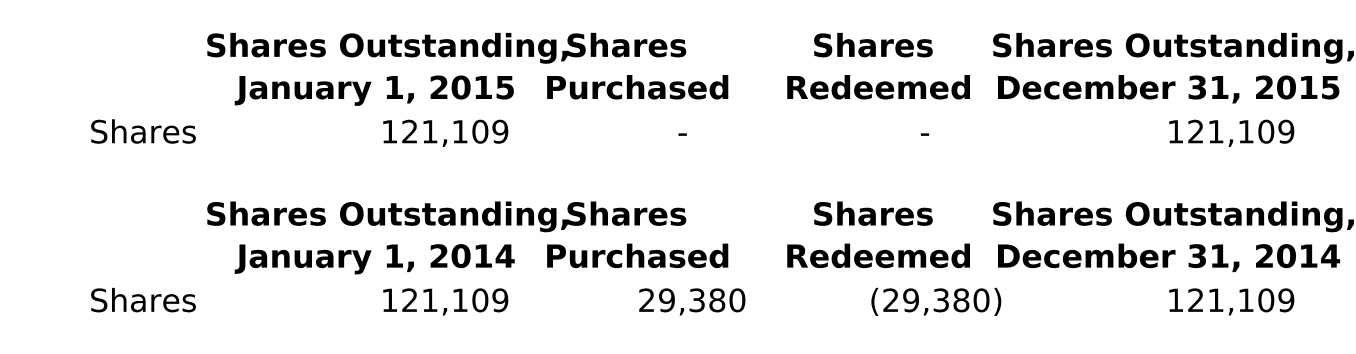

| 3. | SHARE CAPITAL |

The authorized share capital of the Fund is $50,000 divided into 1,000 Management Shares of par value $1.00 each and 4,900,000 Participating shares of par value $0.01 each.

Share capital transactions for the years ended December 31, 2015 and 2014 are as follows:

No owner of the Fund’s shares is entitled to distributions except at the discretion of KKR Credit. KKR Credit, in its sole discretion, may establish reserves and holdbacks for estimated accrued expenses, liabilities, and contingencies, which could reduce the amount of any distribution. Distributions made by KKR Credit during the year were the result of cash flows received from the Fund’s investment in Maritime Finance Company Ltd.

At the end of each accounting period of the Fund, any net capital appreciation or depreciation is allocated to the shareholders in proportion to their opening share balance for such accounting period.

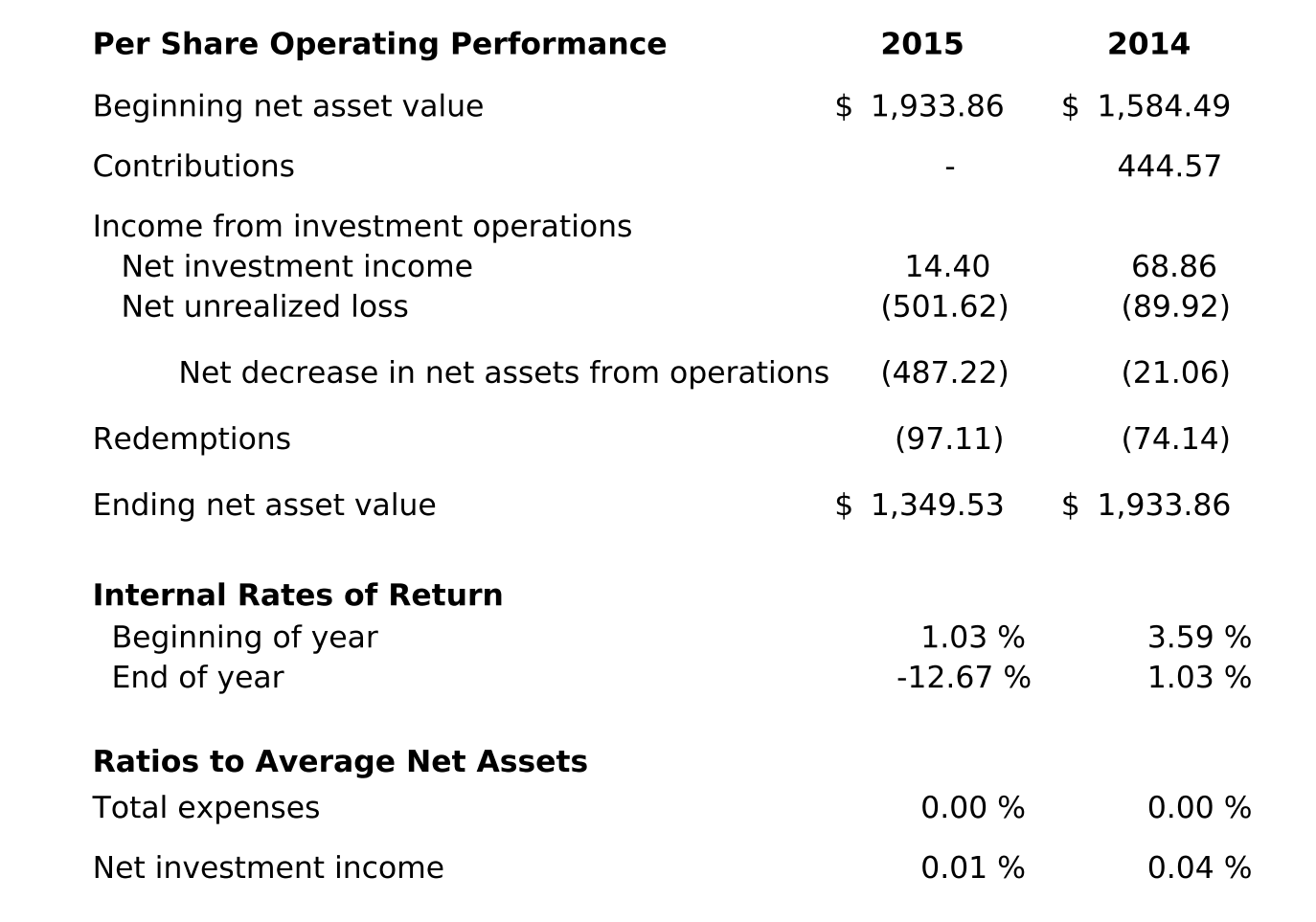

| 4. | FINANCIAL HIGHLIGHTS |

Financial highlights for the years ended December 31, 2015 and 2014 are as follows:

The financial highlights presented above are calculated for the shareholders as a whole. An individual shareholder’s results may vary based on the timing of capital transactions. The internal rate of return from the commencement of operations was computed based on actual dates of capital contributions and distributions, and the shareholders’ capital at the end of the reporting period.

| 5. | FAIR VALUE DISCLOSURE |

The following table presents information about the Fund’s investments measured at fair value on a recurring basis as of December 31, 2015 and 2014, and indicates the fair value hierarchy of the inputs utilized by the Fund to determine such fair value (amounts in thousands):

For the years ended December 31, 2015 and 2014, there were no transfers between Levels.

The following table presents additional information about investments that are measured at fair value on a recurring basis for which the Fund has utilized Level 3 inputs to determine fair value as of December 31, 2015 and December 31, 2014 (amounts in thousands):

The following table presents additional information about valuation techniques and inputs used for assets that are measured at fair value and categorized within Level 3 as of December 31, 2015 and December 31, 2014 (fair value amounts in thousands):

(1) In determining certain of the significant unobservable inputs used in the fair value measurement of the Fund’s assets , management evaluates a variety of factors including economic, industry and market trends and developments; market valuations of comparable companies; and company specific developments including potential exit strategies and realization opportunities. Significant increases or decreases in any of these inputs in isolation could result in significantly lower or higher fair value measurement.

| 6. | CONCENTRATION OF RISK |

In the ordinary course of business, the Fund manages a variety of risks, including market risk and credit risk. Market conditions such as interest rates, availability of credit, inflation rates, foreign exchange rates, economic uncertainty, changes in law, and trade barriers may affect the level and volatility of the prices of financial instruments and the liquidity of the Fund’s investments. Market risk is a risk of potential adverse changes to the value of financial instruments because of changes in market conditions such as interest and currency rate movements and volatility in commodity or security prices. The Fund is also subject to credit and counterparty risks when entering into transactions.

KKR Credit believes that the Fund’s liquidity level is in excess of that necessary to sufficiently enable the Fund to meet its anticipated liquidity requirements, including, but not limited to, payment of fees and administrative expenses.

| 7. | SUBSEQUENT EVENTS |

The Fund evaluated subsequent events through March 31, 2016 and determined that no additional disclosures were necessary.

******