Bioheart, Inc.

13794 NW 4th Street, Suite 212,

Sunrise, Florida 33325

December 14, 2012

VIA EDGAR

United States Securities and Exchange Commission

100 F Street, NE

Division of Corporate Finance

Washington, D.C. 20549

Re:

Re: Bioheart, Inc.

Form 10-K for the Fiscal Year Ended December 31, 2011 (the “Annual Report”)

Post-Effective Registration Statement (SEC File #333-179096) on Form S-1 to be filed

Request for Waiver

Ladies and Gentlemen:

Bioheart, Inc., a Florida corporation (the "Registrant”), submits this Application to Dispense with Consent,pursuant to Rule 437 of Regulation C of the Securities Act of 1933, as amended (the “Securities Act”), requesting that the staff waive the requirement that the Registrant obtain a consent to use the report from the Registrant’s prior auditor, Jewett, Schwartz, Wolfe & Associates (“JSW”), because the Registrant is unable to obtain the consent of the registrant’s prior auditor, JSW, required to be filed with the Annual Report and the Post-Effective Registration Statement(SEC File #333-179096) on Form S-1 to be filed.

JSW audited the Registrant’s financial statements for the year ended December 31, 2009, the consent for their use required to be filed by the Registrant with the annual report on Form 10-K for the fiscal year ended December 31, 2011 and also required to be filed on a Post-Effective Registration Statement (SEC File #333-179096) on Form S-1 to be filed. In February, 2011, JSW advised Registrant that the audit related work of several public clients (defined as issuers under PPCAOB standards) of its audit practice was acquired by RBSM LLP (“RBSM”), an independent registered public accounting firm. As a result, JSW resigned as the Registrant’s independent registered public accounting firm and the Company engaged RBSM as its independent registered public accounting firm. On January 24, 2012, The Registrant advised RBSM LLP of its decision to replace RBSM as the Registrant’s independent registered public accounting firm and engaged Fiondella, Milone & LaSaracina LLP (“FML”) as its independent registered public accounting firm for the Registrant’s fiscal year ended December 31, 2011.

The audit report of FML and RBSM on the Registrant’s financial statements for the year ended December 31, 2011 were included in the annual report on Form 10-K for the fiscal

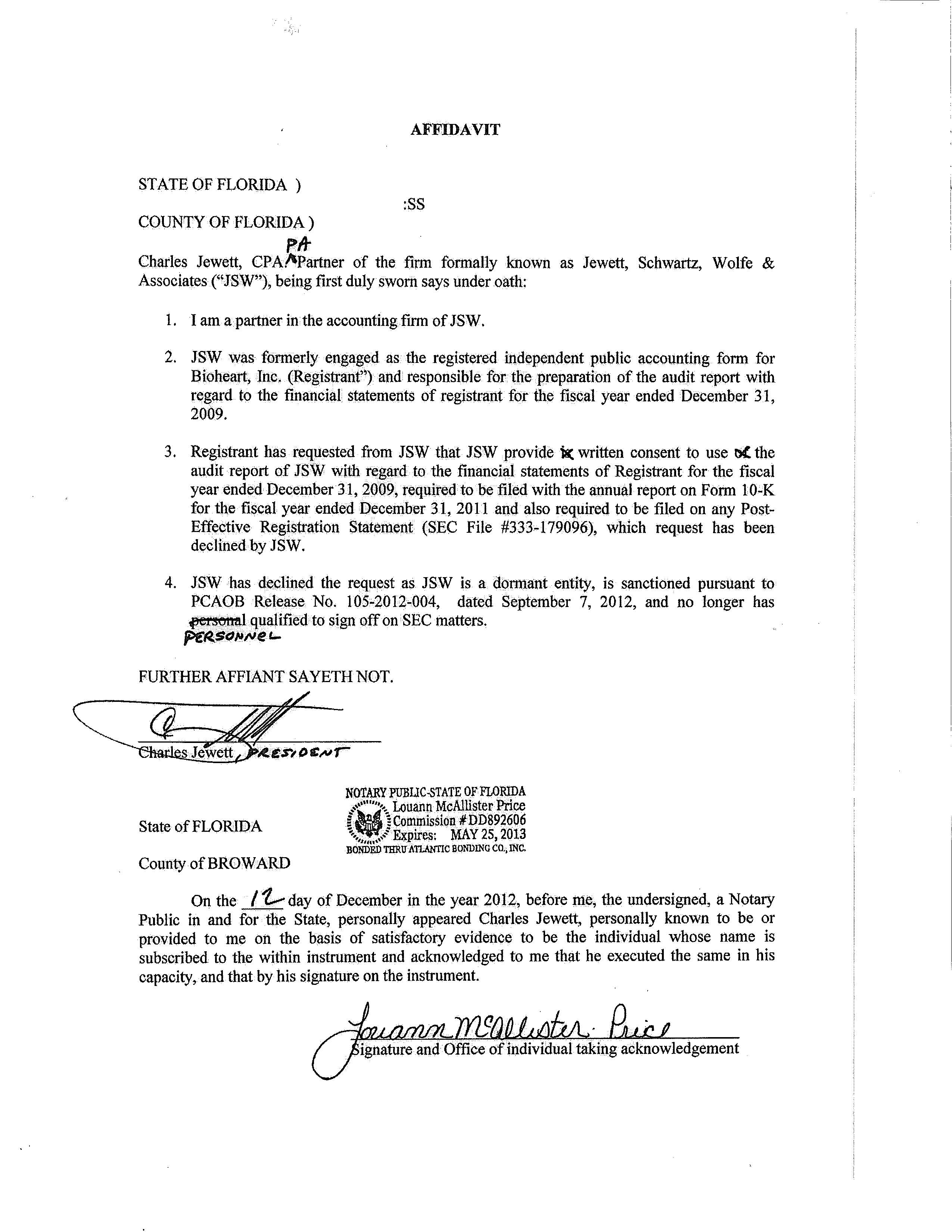

year ended December 31, 2011with the consent of RBSM and the audit report of FML and RBSM on the Registrant’s financial statements for the year ended December 31, 2011 will be included in the Post-Effective Registration Statement (SEC File #333-179096) on Form S-1, to be filed, with the consent of RBSM and FML. Registrant asked JSM to provide a written consent to the use of its audit report for the 2009 financial statements in the annual report on Form 10-K for the fiscal year ended December 31, 2011 and in Post-Effective Registration Statement (SEC File #333-179096) on Form S-1 to be filed, which request was declined by JSW, citing as reasons thatJSW is a dormant entity, is sanctioned pursuant to PCAOB Release No. 105-2012-004, dated September 7, 2012, and no longer has personal qualified to sign off on SEC matters.

Accordingly, the obtaining of a consent of JSW to the use of its audit report in the annual report on Form 10-K for the fiscal year ended December 31, 2011and in Post-Effective Registration Statement (SEC File #333-179096) on Form S-1 to be filed, is impracticable or involves undue hardship within the scope of Rule 437.

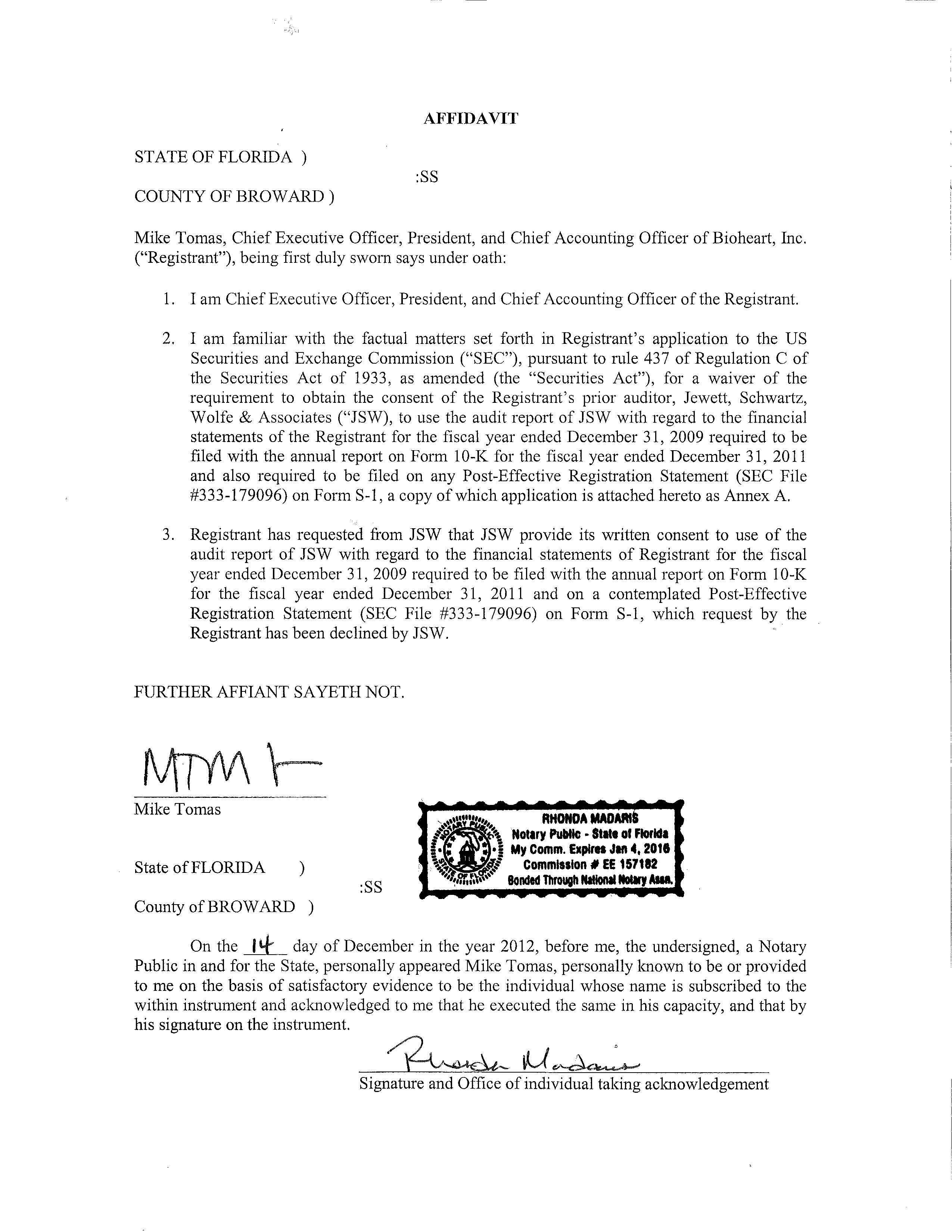

The factual matters in this application are supported by the affidavit of Mike Tomes, the Registrant’s Chief Executive Officer, President and Principal Accounting Officer, and Charles Jewett, CPA, a partner of JSW, both of which are attached hereto.

If the staff agrees to the waiver requested hereby,

·

The Registrant will state under Experts section of the Post-Effective Registration Statement (SEC File #333-179096) on Form S-1 to be filed that, although an audit report was issued by the Registrant’s former auditor on Registrant’s 2009 financial statements and is referenced and used by the subsequent auditor in the Post-Effective Registration Statement, and its public filings, such former auditor has not permitted the use of its report in the Post-Effective Registration Statement.

·

The Registrant included the following language in the Form 10-K/A for the year ended December 31, 2011: PROVIDED BELOW IS A COPY OF THE ACCOUNTANT’S REPORT ISSUED BY JEWETT, SCHWARTZ, WOLFE & ASSOCIATES (“JSW”), OUR FORMER INDEPENDENT PUBLIC ACCOUNTANTS, IN CONNECTION WITH THE FILING OF OUR ANNUAL REPORT ON FORM 10-K FOR THE YEAR ENDED DECEMBER 31, 2009. THIS AUDIT REPORT IS A COPY OF THE PREVIOUSLY ISSUED REPORT AND HAS NOT BEEN REISSUED BY JSW IN CONNECTION WITH THE FILING OF THIS ANNUAL REPORT FILED ON FORM 10-K/A. INVESTORS MAY NOT BE ABLE TO BRING AN ACTION AGAINST JSW PURSUANT TO THE SECURITIES ACT OF 1933 OR THE SECURITIES EXCHANGE ACT OF 1934 WITH RESPECT TO SUCH REPORT OR WITH RESPECT TO THIS ANNUAL REPORT AND, THEREFORE, ANY RECOVERY FROM JSW MAY BE LIMITED. THE FOREGOING LIMITATIONS RESPECTING JSW IN NO WAY LIMITS INVESTORS’ RIGHT OF ACTION AGAINST OR RECOVERY FROM THE COMPANY;. and included the following risk Factor:Recourse against and recovery from our

prior auditor may be limited.The Company’s auditor Jewett, Schwartz, Wolfe and Associates (“JSW”) who audited our consolidated financial statements at December 31, 2009 and 2008, and the cumulative period from August 12, 1999 (date of inception) to December 31, 2009, has ceased operations and has not reissued its report in this annual report. Accordingly, investors are cautioned that any recourse or recovery they may have against or from such auditor arising out of our consolidated financial statements at December 31, 2009 and 2008 may be limited (though any such limitation shall not have any affect upon our liability for such financial statements).

·

Registrant will follow the guidance in paragraph 65 of AU 9508.15 regarding the 2009 financial statements included in the Post-Effective Registration Statement (SEC File #333-179096) on Form S-1 to be filed. Consistent with this guidance, as it has with the Form 10-K/A for the year ended December 31, 2011, Registrant will include a prominent disclosure on the face of the JSW audit report included in the Post-Effective Registration Statement that (a) the report is a copy of the previously issued JSW report, and (b) the report has not been reissued by JSW.

·

Registrant will clearly disclose, in the Post-Effective Registration Statement (SEC File #333-179096) on Form S-1 to be filed, as it has with the Form 10-K/A for the year ended December 31, 2011, the limitations on recovery by investors due to the lack of a reissued audit opinion in the Risk Factors section of the Management’s Discussion and Analysis in the Post-Effective Registration Statement.

We hereby acknowledge that Registrant is responsible for the adequacy and accuracy of the disclosures in public filings, and the approval of the application to dispense with auditor consent or staff comments or changes to disclosure in response to staff comments di not foreclose the commission from taking any action with respect to any public filings, and the Registrant may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

Thank you very much for your consideration. Should you require any further information, please contact me at 954-835-1500,mtomas6@bellsouth.net, or by facsimile at 954-845-9976. Otherwise, I look forward to a favorable response to our application that we may proceed with the filing of the Post-Effective registration Statement and satisfy the staff comment received by letter on December 11, 2012, without the requirement of having to obtain the consent of JSW to the inclusion of their audit report.

Very truly yours,

/s/ Mike Tomas

Mike Tomas

Chief Executive Officer