UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ Annual Report Under Section 13 Or 15(d) Of The Securities Exchange Act Of 1934

For the fiscal year ended December 31, 2017

or

☐ Transition Report Under Section 13 Or 15(d) Of The Securities Exchange Act Of 1934

For the transition period from _____to _____

COMMISSION FILE NUMBER: 000-52446

ACTINIUM PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 74-2963609 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

275 Madison Avenue, 7th Fl.

New York, NY 10016

(Address of principal executive offices) (Zip Code)

(646) 677-3870

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of exchange on which registered | |

| Common stock, par value $0.001 | NYSE American |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Date File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of the chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☒ |

| Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ |

| Emerging growth company | ☒ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 126-2 of the act): Yes ☐ No ☒

The aggregate market value of voting stock held by nonaffiliates of the registrant as of June 30, 2017, the last business day of the registrant’s most recently completed second fiscal quarter, based on the closing price of the common stock on the NYSE AMERICAN on June 30, 2017 was $71,393,269.

As of March 16, 2018, 110,198,660 shares of common stock, $0.001 par value per share, were outstanding.

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Report”) contains forward looking statements that involve risks and uncertainties, principally in the sections entitled “Description of Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” All statements other than statements of historical fact contained in this prospectus, including statements regarding future events, our future financial performance, business strategy and plans and objectives of management for future operations, are forward-looking statements. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “should,” or “will” or the negative of these terms or other comparable terminology. Although we do not make forward looking statements unless we believe we have a reasonable basis for doing so, we cannot guarantee their accuracy. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks outlined under “Risk Factors” or elsewhere in this prospectus, which may cause our or our industry’s actual results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time and it is not possible for us to predict all risk factors, nor can we address the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause our actual results to differ materially from those contained in any forward-looking statements. All forward-looking statements included in this document are based on information available to us on the date hereof, and we assume no obligation to update any such forward-looking statements.

You should not place undue reliance on any forward-looking statement, each of which applies only as of the date of this prospectus. Before you invest in our securities, you should be aware that the occurrence of the events described in the section entitled “Risk Factors” and elsewhere in this prospectus could negatively affect our business, operating results, financial condition and stock price. Except as required by law, we undertake no obligation to update or revise publicly any of the forward-looking statements after the date of this prospectus to conform our statements to actual results or changed expectations.

Business Overview

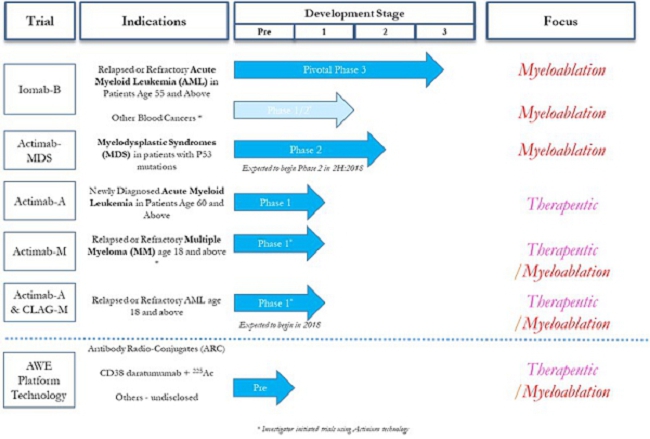

Actinium Pharmaceuticals Inc. is a clinical-stage biopharmaceutical company focused on developing and potentially commercializing targeted therapies for improved myeloablation and conditioning of the bone marrow prior to a bone marrow transplant and for the targeting and killing of cancer cells. Our targeted therapies are Antibody Radio-Conjugates, or ARC, that combine the targeting ability of monoclonal antibodies (“mAb”) with the cell-killing ability of radioisotopes. Our ARC’s have demonstrated the ability to improve access to bone marrow transplants with the potential for better outcomes, namely increased marrow engraftment and survival. Our product pipeline consists of two ARC product candidates that are currently being studied in three clinical trials. Two additional clinical trials are expected to begin patient enrollment in 2018. In each of the indications, we believe our product candidates are either first-in-class or have best–in-class potential. Our lead myeloablation product candidate, Iomab-B, is currently being studied in a pivotal Phase 3 trial as a conditioning agent in older patients with relapsed or refractory (“r/r”) Acute Myeloid Leukemia AML (“AML”) who are ineligible for a bone marrow transplant as they cannot withstand chemotherapy-based conditioning. Iomab-B is an ARC that is comprised of the anti-CD45 mAb apamistamab and the radioisotope iodine-131 (“131I”). Our CD33 program trials include; the ongoing Phase 2 Actimab-A trial for patients newly diagnosed with AML over the age of 60, the Phase 1 Actimab-M trial for patients with refractory multiple myeloma, the planned Phase 2 Actimab-MDS trial for patients with high-risk myelodysplastic syndrome (“MDS”) with a p53 genetic mutation and the Phase 1 Actimab-A & CLAG-M trial for patients with r/r AML. These trials are studying our ARC drug candidate comprised of the anti-CD33 mAb lintuzumab and the radioisotope actinium-225 (“225Ac”). In addition, we are developing our Actinium Warhead Enabling, or AWE, Technology Platform. We plan to leverage our intellectual property and know-how to create additional ARC drug candidates by labeling225Ac to targeting moieties that we will either progress in clinical trials or out-license.

Bone marrow is semi-solid tissue found within the spongy section of bones that produces new blood cells in a process called hematopoiesis. Bone marrow contains hematopoietic stem cells that give rise to the three classes of blood cells that are found in circulation: red blood cells and platelets that are responsible for blood function and white blood cells that are responsible for immune system function. A bone marrow transplant may be the only potentially curative treatment option, or the best treatment option, for patients with blood cancers such as leukemias, lymphomas and multiple myeloma, or benign blood, or marrow disorders such as inherited immune system disorders, sickle cell disease and severe aplastic anemia.

In order to receive a bone marrow transplant, (“BMT”), patients are administered treatment to ablate or destroy their bone marrow in a process referred to as myeloablation. Myeloablative treatments typically consist of chemotherapy and external radiation, which is also called total body radiation. As an alternative to myeloablation, the bone marrow may also be conditioned or prepared for a transplant via lower intensity treatment know as reduced intensity conditioning, which uses lower doses of external radiation and less toxic types of chemotherapy. Patients with blood cancers must ideally be disease–free, or at least in remission, before receiving myeloablative or conditioning therapy. Myeloablative treatments are associated with greater and more severe toxicities, including higher treatment-related mortality rates that may be too intense for patients, particularly those of advanced age, to tolerate as compared to reduced intensity conditioning. Reduced intensity conditioning is generally better tolerated by patients but is associated with higher rates of relapse, which can reduce overall survival. Our ARC based approach is designed to target blood cancer and bone marrow cells via a mAb and deliver potent radioisotope payloads directly to those cells to achieve myeloablation without systemic toxicities. In doing so, we hope to improve access to BMT for a greater number of patients while improving outcomes through improved myeloablation via our ARC technologies.

We have licensed our product candidates and ARC technologies from the Fred Hutchinson Cancer Research Center and the Memorial Sloan Kettering Cancer Center. These licenses include rights to certain patents and we own outright patents pertaining to our product candidates and AWE technology platform. Our intellectual property portfolio consists of 68 issued and pending patent applications that we have licensed or fully own. We have compiled scientific and medical advisory boards of thought-leading physicians in their respective fields to advise and guide us though the development process of our pipeline product candidates.

We have also developed proprietary know-how related to the development, manufacturing and supply chain required for our product candidates. We supply our product candidates to clinical trial sites on a just-in-time basis through the manufacturing of our drug product components, final drug product and the distribution of our final drug product to medical centers where our trials are conducted. In the case of Iomab-B, we calculate, produce and supply personalized doses for our clinical trial. We have secured access to131I produced by two premier commercial global suppliers. We project that these two suppliers have sufficient131I production capacity to meet our commercial needs for the Iomab-B program. We have secured access to225Ac through a renewable contractual arrangement with the United States Department of Energy, or DOE. We project that these quantities are sufficient to support early stages of commercialization of actinium isotope-based products and that the DOE’s accelerator route of production of225Ac has the potential to provide commercial quantities of225Ac. We have also developed our own proprietary process for industrial-scale225Ac production in a cyclotron in quantities adequate to support full product commercialization.

| 1 |

Pipeline

Myeloablation Product Candidates

We are developing two first-in-class product candidates focused on improving access to and outcomes from bone marrow transplant through improved myeloablation. Our ARC product candidates target antigens that are expressed on certain cancer cell types with mAbs that are labeled with radioisotopes that are able to destroy cellular DNA and kill these cells with the energy that they emit. We utilize certain mAbs and radioisotopes to develop product candidates that are ideally suited for particular disease indications and patient populations. Our lead myeloablation product candidate is Iomab-B, an ARC consisting of an anti-CD45 mAb and the radioisotope iodine-131, or131I. We are also developing an ARC consisting of the anti-CD33 mAb lintuzumab and the radioisotope actinium-225, or225Ac, in a study that we call Actimab-MDS.

CD33 Program Trials

CD33 is an antigen that has been found to be expressed in patients with certain hematologic malignancies including AML, MDS and multiple myeloma. CD33 is expressed in up to 90% of patients with AML, approximately 75% of patients with MDS and 25-35% of patients with multiple myeloma. We are developing our lintuzumab-225Ac ARC for these indications in the following clinical trials:

| ● | Actimab-A phase 2 clinical trial for patients with AML | |

| ● | Actimab-M phase 1 clinical trial for patients with multiple myeloma which is first in class and | |

| ● | Actimab-A phase 1 clinical trial in combination with CLAG-M, a salvage chemotherapy regimen, in patients with r/r AML. |

We intend to develop our best-in-class CD33 program to address a broad population of patients with CD33 expressing hematologic indications and deliver the best outcomes using our ARC technological approach.

| 2 |

Actinium Warhead Enabling (AWE) Technology Platform and Program

Our proprietary AWE Technology Platform is supported by intellectual property and know-how that enables the creation of225Ac radio-conjugates, wherein a biomolecular targeting agent is labeled with the225Ac payload to enhance targeted cell killing. As of March 2018, we have four issued and one pending patent related to our AWE Technology Platform in the U.S. having expirations in 2021, 2030 and 2023 and 21 issued or pending patents outside of the U.S. Our intellectual property covers the use of the “gold standard” chelator DOTA, (tetracarboxylic acid), an organic compound used to attach, or conjugate, radioisotopes to monoclonal antibodies and any conceivable derivative thereof. Additionally, we hold intellectual property protection around methods of chelation or labeling of the targeting agent with225Ac as well as newer next generation methods of chelation or labeling. We are studying our AWE Technology Platform in preclinical studies to demonstrate proof of concept to enable research collaborations and partnerships.

Business Strategy

We intend to potentially develop Iomab-B and other potential myeloablation products through registration studies and approval. If our efforts are successful, we may elect to commercialize our myeloablation products on our own, or with a partner in the United States and out-license the rights to develop and commercialize the product to a strategic partner outside of the United States. If we commercialize our products independently, we intend to build a commercial distribution network that can supply our myeloablation product candidates to the top 50-100 bone marrow transplant centers in the U.S., where a majority of patients are myeloablated and receive their transplants. In the case of our CD33 program product candidates, we will potentially develop these up to and including a Phase 2 proof-of-concept human clinical trial (a trial designed to provide data on the drug’s efficacy). We will most likely seek to enter into strategic partnerships whereby the strategic partner(s) co-fund(s) further human clinical trials of the drug that are needed to obtain regulatory approvals for commercial sale within and outside of the United States. In parallel, we intend to identify and begin initial proof-of-concept trials with our AWE Technology Platform in other cancer indications. We intend to retain marketing rights for our products in the United States whenever possible and out-license marketing rights to our partners for the rest of the world. We may also seek to in license other applicable opportunities should such technology become available.

Market Opportunity

We believe that improved myeloablation prior to a BMT could result in improved access and outcomes for patients, as well as provide a pharmacoeconomic benefit. The Center for International Blood and Marrow Transplant Research (CIBMTR) estimates that there approximately 22,000 patients received an autologous or allogeneic BMT’s in the United States in 2015. The American Cancer Society estimates that approximately 172,000 patients will be diagnosed with leukemia, lymphoma or multiple myeloma and that approximately 1.2 million patients are living with, or are in remission from these diseases. A BMT is a potentially curative or potentially best treatment option for certain patients with these blood cancers and we intend to develop our ARC product candidates with the goal of improving BMT access and outcomes for these patients. According to a study published in the Journal of Medical Economics, real-world economic burden of hematopoietic cell transplantation among a large US commercially insured population with hematologic malignancies, the healthcare cost for patients receiving an autologous BMT were $390,000 while the healthcare costs for patients receiving an allogeneic BMT were $745,000. We believe that reduction in toxicities and resulting hospital stays associated with current chemotherapy-based myeloablation regimens could reduce these costs. We intend to collect pharmacoeconomic data in our current and future clinical trials for Iomab-B and other myeloablation product candidates to determine if our therapies lead to a cost benefit. Iomab-B has demonstrated efficacy in myeloablation prior to a BMT for blood cancer indications, including AML, MDS, ALL, Hodgkin’s Lymphoma, NHL and multiple myeloma. These are indications for which Iomab-B can be developed and it is our intention to explore these opportunities. We believe the aggregate worldwide market potential for the treatment of AML, MDS, ALL, Hodgkin’s Lymphoma, NHL and multiple myeloma is approximately $6.6 billion.

For our CD33 program drug candidates, we are competing in the marketplace for cancer treatments estimated to have reached over $83 billion in 2016 sales, according to “The Global Use of Medicines: Outlook Through 2016 Report by the IMS Institute for Healthcare Informatics, July 2012”. While surgery, radiation and chemotherapy remain staple treatments for cancer, their use is limited by the fact that they often cause substantial damage to normal cells. On the other hand, targeted monoclonal antibody therapies exert most or all of their effect directly on cancer cells, but often lack sufficient killing power to eradicate all cancer cells with just the antibody. A new approach for treating cancer is to combine the precision of antibody-based targeting agents with the killing power of radiation, or chemotherapy, by attaching powerful killing agents to precise molecular carriers called monoclonal antibodies. We use mAbs labeled with radioisotopes to deliver potent doses of radiation directly to cancer cells while sparing healthy tissues. The radioisotopes we use are the alpha emitter225Ac and the beta emitter 131-I. 131-I is among the best known and well characterized radioisotopes. It is used very successfully in treatment of papillary and follicular thyroid cancer as well as other thyroid conditions. It is also attached to a monoclonal antibody in treatment of NHL. It is also used experimentally with different carriers in other cancers.225Ac has many unique properties and we believe we are a leader in developing this alpha emitter for clinical applications using our proprietary AWE technology platform.

| 3 |

Our executive office is located at 275 Madison Ave, 7th Floor, New York, NY 10016 and telephone number is (646) 677-3870. Our website address is http://www.actiniumpharma.com. Except as set forth below, the information on our website is not part of this Annual Report on Form 10-K.

Clinical Trials

Myeloablation Product Candidates

We are focused on developing ARC product candidates that improve bone marrow transplant access and outcomes through improved myeloablation. Myeloablation is an integral step prior to a bone cell transplant whereby a patient’s bone marrow is ablated to make room for stem cells from a donor. A stem cell transplant may be the only potentially curative treatment option or the best treatment option for patients with blood cancers such as leukemias, lymphomas and multiple myeloma or benign blood or marrow disorders such as inherited immune system disorders, sickle cell disease and severe aplastic anemia. We are currently conducting two clinical trials for product candidates focused on myeloablation, a pivotal phase 3 trial for Iomab-B and the phase 2 Actimab-MDS trial both of which are first in their class

Iomab-B Pivotal Phase 3 Trial

Iomab-B is our lead product candidate currently in a pivotal phase 3 multicenter clinical trial. We licensed Iomab-B from the Fred Hutchinson Cancer Research Center, or FHCRC, where it was developed and studied extensively in numerous clinical trials in a range of hematologic indications and patient populations. Iomab-B consists of the monoclonal antibody apamistamab and the beta emitting radioisotope131I. Apamistamab has been studied in 10 Phase 1 or Phase 2 clinical trials in patients with AML, MDS, ALL, multiple myeloma and lymphomas at various stages of the disease such as newly diagnosed, relapsed or refractory and first remission. There are additional investigator-initiated trials ongoing at FHCRC. The indication selected for our pivotal phase 3 trial is myeloablation and bone marrow conditioning for HSCT in patients with relapsed and refractory AML over the age of 55.

Previous Iomab-B clinical trials leading to our current pivotal Phase 3 trial included:

| Indications | N | Key Findings | ||

| AML, MDS, ALL (adult) | 34 | –7/34 patients with median disease-free state (“DFS”) of 17 years. | ||

| –18/34 patients in remission at day 80 | ||||

| AML >1st remission (adult) | 23 | –15/23 in remission at day 28 | ||

| AML 1st remission (age 16-50) | 43 | –23/43 DFS from 5-16 years | ||

| –30/43 in remission at day 28 | ||||

| –33/43 in remission at day 80 | ||||

| High-risk MDS, advanced AML | 68 in dose escalation study | –CR (complete remission) in virtually all patients | ||

| (age 50+) | 31 treated at MTD | –1-year survival ~40% for all patients | ||

| –1-year survival ~45% for patients treated at MTD (“maximum tolerated dose”) | ||||

| High-risk MDS, AML (age 18–50) | 14 in dose escalation | All patients achieved full donor chimerism by day 28 post-transplant | ||

| High-risk MDS, AML –haploidentical donors (adult) | 8 in dose escalation | –6/8 treated patients achieved CR by day.28 –8/8 patients 100% donor chimerism by day28 |

| 4 |

Ongoing clinical trials using the apamistamab antibody include:

| Indications | Phase | |

| AML, ALL and high-risk MDS | Phase 1/2 |

Actimab-MDS Phase 2 Trial

In December 2017, we announced Actimab-MDS, a planned phase 2 trial for our second ARC product candidate focused on improved myeloablation. Actimab-MDS consists of the anti-CD33 mAb lintuzumab labeled with the radioisotope225Ac. The planned Actimab-MDS phase 2 will be conducted with the MDS Clinical Research Consortium that is comprised of the Cleveland Clinical Taussig Cancer Institute, Dana-Farber Cancer Institute, MD Anderson Cancer Center, H. Lee Moffitt Cancer Center and Research Institute, Weill Medical College of Cornell University and the Sidney Kimmel Comprehensive Cancer Center at Johns Hopkins. Dr. Gail Roboz, Director, Leukemia Program and Professor of Medicine at Weill Medical College of Cornell University will serve as principal investigator for the trial.

The Actimab-MDS trial will enroll patients with high-risk MDS that have a p53 genetic mutation, which is estimated to occur in approximately 20% of MDS patients. Patients with a p53 mutation have been found to have poorer survival outcomes following a bone marrow transplant. We expect to meet with the U.S. Food & Drug Administration, or FDA, in the first half of 2018 to discuss the regulatory pathway for this product candidate. Currently, we expect to conduct a 50-80 patient, single arm, phase 2 trial. Patients enrolled in the trial will receive a single infusion of lintuzumab labeled with225Ac at a dose of 4.0 µCi/kg prior to receiving a bone marrow transplant. We expect that overall survival will be the primary endpoint of the study measured at either one or two years.

CD33 Program Trials

We are developing our ARC product candidate that consists of the anti-CD33 mAb lintuzumab and the radioisotope225Ac for multiple hematologic malignancies. CD33 is an antigen shown to be expressed in up to 90% of patients with AML, 75% of patients with MDS and 35% of patients with multiple myeloma. Our lintzumab-225Ac ARC is a second-generation construct that was developed at the Memorial Sloan Kettering Cancer Center, or MSKCC. The first-generation product consisted of the same monoclonal antibody lintuzumab but utilized the radioisotope bismuth-213 (“213Bi”), a daughter of225Ac.

In preclinical animal models, doses in the nanocurie range prolonged survival. In humans, Actimab-A was previously studied in a Phase 1 monotherapy trial of relapsed or refractory AML patients at MSKCC. Dose levels in that study re-confirmed the substantially higher potency of225Ac -lintuzumab, as compared to equivalent dosing of the first-generation 213Bi-lintuzumab construct, which had nevertheless established safety and efficacy in a Phase 1/2 trial in high-risk AML with cytoreduction.

High potency means that a relatively low amount of drug is needed to produce a given effect. In preclinical and Phase 1 clinical studies,225Ac -lintuzumab has demonstrated at least 500-1000 times higher potency than the first-generation predecessor 213Bi-lintuzumab upon which it is based. This difference is due to intrinsic physicochemical properties of225Ac -lintuzumab that were first established in vitro, in which225Ac -lintuzumab killed multiple cell lines at doses at least 1000 times lower (based on LD50 values) than 213Bi-lintuzumab analogs. Key factors in225Ac -lintuzumab’s higher potency are the yield of 4 alpha-emitting isotopes per225Ac (compared to 1 alpha decay for bismuth 213) and much longer half-life (10 day for225Ac vs 46 minutes for 213Bi).

| 5 |

Collectively, these two constructs have been studied in over 100 patients including the following trials:

| — | Phase 1 clinical trial with Bismab-A, the first-generation product consisting of the same monoclonal antibody Lintuzumab and213Bi alpha emitter, a daughter of225Ac; | |

| — | Phase 1/2 clinical trial with Bismab-A, the first-generation product consisting of the same monoclonal antibody Lintuzumab and213Bi alpha emitter, a daughter of225Ac; and | |

| — | Dose escalating pilot Phase 1 clinical trial with Actimab-A, the current product consisting of the Lintuzumab monoclonal antibody and225Ac -alpha emitter. |

Completed Actimab-A related clinical trials outcomes:

| — | The Phase 2 arm of the Bismab-A drug study has shown signs of the drug’s efficacy and safety, including reduction in peripheral blast counts and complete responses in some patients.213Bi is a daughter, i.e., product of the degradation of225Ac, with cancer cell killing properties similar to225Ac but is less potent. The Phase 1 Actimab-A trial at MSKCC with a single-dose administration of Actimab-A showed elimination of leukemia cells from blood in 67% of all evaluable patients who received a full dose and in 83% of those treated at dose levels above 0.5 microcuries per kilogram (µCi/kg), and eradication of leukemia cells in both blood and bone marrow in 20% of all evaluable patients and 25% of those treated at dose levels above 0.5 µCi/kg. Maximum tolerated single dose in this trial was established at 3 µCi/kg. | |

| — | The Phase 1 portion of the trial with lintuzumab225Ac at fractionated doses was a dose-finding study. The results of the study showed that 28% (5 of 18) of patients had objective responses (2CR, 1CRp and 2 Cri (complete remission with incomplete blood count recovery) with median response duration of 9.1 months. Mean bone marrow blast reduction amongst evaluable patients (14 of 18) was 67% with 57% of patients having bone marrow blast reduction of 50% or greater and 79% (11 of 14) of patients having bone marrow blast reductions after one cycle of therapy. Maximum tolerated dose was not reached in this trial. We elected to progress to the Phase 2 portion of the trial at 2.0 μCi/kg/fraction, the highest dose level from the Phase 1 portion of the trial. |

Sources: Jurcic JG. Targeted Alpha-Particle Immunotherapy with Bismuth-213 and Actinium-225 for Acute Myeloid Leukemia. J. Postgrad Med Edu Res 2013, 47(1):14-17; ; JG Jurcic et al, Phase 1 Trial of the Targeted Alpha- Particle Nano-Generator Actinium-225 (225Ac)-Lintuzumab in Acute Myeloid Leukemia (AML) J Clin Oncol 29:2011 (suppl, abstr 6516); McDevitt MR et al, “Tumor Therapy with Targeted Atomic Nanogenerators” Science 2001, 294:1537—1540; Rosenblat TL et al, “Sequential cytarabine and alpha-particle immunotherapy with bismuth- 213-lintuzumab (HuM195) for acute myeloid leukemia” Clin Cancer Res. 2010, 16(21):5303-5311; Jurcic JG et al. “Phase I Trial of the Targeted Alpha-Particle Nano-Generator Actinium-225 (225Ac)-Lintuzumab in Acute Myeloid Leukemia (AML)” Blood (ASH Meeting Abstracts) 2012.

Ongoing Actimab-A Phase 2 trial:

Our most advanced CD33 program trial is a Phase 2 clinical trial in patients newly diagnosed with AML who are over the age of 60 and unfit for intensive chemotherapy. The Phase 2 portion of the trial will enroll 53 patients and studies Actimab-A as a monotherapy. We received agreement from the FDA for multiple revisions to the trial protocol for the Phase 2 portion of the trial that include:

| — | Removing the use of low dose cytarabine from the Phase 2 protocol, | |

| — | Stipulating peripheral blast burden as an inclusion criteria with 200 ML being the threshold | |

| — | Mandating the use of hydroxyurea in patients with peripheral blast count above 200 ML to lower their peripheral blasts below 200ML/ prior to Actimab-A administration | |

| — | Mandating the use of granulocyte colony-stimulating factor (GCSF) support |

At the American Society of Hematology, or ASH, annual meeting in December 2017, we presented via poster, preliminary results from the ongoing phase 2 clinical trial. This trial is enrolling patients newly diagnosed with AML who are over the age of 60 that are unfit for intense chemotherapy. This trial allows patients with prior hematologic disease to enroll and 69% of patients (9 of 13) had antecedent hematologic disease (5 MDS, 2 CMML, 1 Atypical CML, 1 tAML) and 7 of these patients were previously treated with hypomethylating agents. We reported a 69% objective response in evaluable patients (9 of 13) (3 CRp and 6 CRi), and our target response rate for this trial was 35%. We also reported a 98% median reduction in bone marrow blasts (10 of 13). Minimal extramedullary toxicities were observed in this patient population. Myelosuppression was observed in all patients and determined to be longer in duration than desirable in unfit patients who by definition are medically infirm. As a result, the dose level was reduced from 2.0 µCi/kg to 1.5 µCi/kg on Days 1 and 8.

| 6 |

Actimab-M Phase 1 Trial

Actimab-M is comprised of the anti-CD33 monoclonal antibody lintuzumab coupled to225Ac and is the same construct, which is currently being studied in a Phase 2 Actimab-A clinical trial in patients newly diagnosed with AML who are over the age of 60. The Phase 1 Actimab-M trial is an open label, dose-escalation study. Patients will be administered a starting dose level of 0.5 μCi/Kg via infusion on day 1 of each cycle for up to 8 cycles with each cycle lasting 42 days. If this dose level is deemed safe, a second dose level of 1.0 μCi/kg will be explored for up to 4 cycles, also of 42 days per cycle. Total dose received per patient is not to exceed 4.0 μCi/kg. In the event of dose limiting toxicities (DLTs) at the 0.5 μCi/Kg dose level, a dose level of 0.25 μCi/Kg will be explored. The Phase 1 trial will estimate maximum tolerated dose (MTD), assess adverse events, measure response rates (objective response rate, complete response rate, stringent complete response rate, very good partial response rate and partial response rate) as well as progression free survival (PFS) and overall survival (OS). To our knowledge, we are the only company developing a multi-disease CD33 targeting program and the first company to develop a CD33 targeting product candidate for patients with multiple myeloma.

Actimab-A and CLAG-M Phase 1 Trial

In February 2018, we announced that the Medical College of Wisconsin would be starting an investigator-initiated Phase 1 trial studying our lintuzumab-225Ac ARC in combination with CLAG-M, a salvage chemotherapy regimen. CLAG-M consists of Cladribine, Cytarabine, G-CSF and Mitoxantrone that is administered to patients over five consecutive days. This Phase 1 trial will add a single infusion of Actimab-A to CLAG-M that will be administered on day 7. This is a dose-finding study that will explore Actimab-A at dose levels of 0.25 uCi/kg, 0.50 uCi/kg and 0.75 uCi/kg that will assess safety by monitoring DLT’s. In addition, efficacy will be assessed by remission rates (CR, CRp, and CRi), rate of patients receiving a bone marrow transplant, overall survival at 1 year and progression free survival (“PFS”).

Actinium Warhead Enabling (AWE) Technology Platform and Program

Our proprietary AWE Technology Platform is supported by intellectual property and know-how that enables the creation of225Ac radio conjugates wherein a biomolecular targeting agent is labeled with the225Ac payload to enhance targeted cell killing. As of March 2018, we have four issued and one pending patent related to our AWE Technology Platform in the U.S. having expirations in 2021, 2030 and 2023 and 21 issued or pending patents outside of the U.S The intellectual property covers the use of the “gold standard” chelator DOTA, (tetracarboxylic acid), an organic compound used to attach, or conjugate, radioisotopes to monoclonal antibodies and any conceivable derivative thereof. Additionally, we hold intellectual property protection around methods of chelation or labeling of the targeting agent with225Ac as well as newer next-generation methods of chelation or labeling.

In November 2017 we announced the availability of our proprietary AWE Technology Platform via the AWE Program for partnerships and collaborations. In tandem, we demonstrated the AWE Technology Platform at the ASH 2017 Annual Meeting with the targeting agent daratumumab - an asset that is distinct from the Company’s AWE-generated, clinical-stage lintuzumab-225Ac. Daratumumab is an anti-CD38 antibody which is marketed by Johnson & Johnson (JNJ) under the trade name Darzalex® for the treatment of multiple myeloma. We first demonstrated the adaptability of the AWE Technology Platform by successfully labeling daratumumab with225Ac. Importantly, the ability of the225Ac enabled daratumumab to engage with its target was unhindered compared to the naked daratumumab. The stability of the constructs was tested to assure reliable labeling. The impact of225Ac-daratumumab was then compared to that of the naked antibody in three cells lines with varying expression levels of the CD38 target. Treatment of these cell lines with225Ac-daratumumab demonstrated both a time and concentration-dependence and, in every instance the225Ac-enabled daratumumab demonstrated superior cell killing over its unlabeled counterpart. As an additional control and to demonstrate the specificity of the cell killing, a cell line that did not express the intended CD38 target was treated with both225Ac-daratumumab and daratumumab. In this scenario no cell killing was observed for both the treatment groups, supporting that cell killing observed with the225Ac-daratumumab is specific and that there are no off-target effects from the radioisotope. Following this initial promising validation, further pre-clinical development of the225Ac-daratumumab asset has been pursued, wherein the value of the225Ac-daratumumab was assessedin vivo in xenograft mouse models.

We have led and successfully demonstrated the adaptability and robust labeling that can be achieved with the AWE Platform Technology. Moreover, the AWE Program provides a potential partner with access to the know-how, capabilities and facilities to execute on a validation study for an225Ac enabled radio conjugate in addition to access to the AWE Platform Technology. The studies with225Ac-daratumumab provides an example of the enhanced therapeutic effect that can be achieved from the utilization of our core platform technology to enable an asset with225Ac positioning the generation of actinium radio conjugates as a viable therapeutic approach.

Operations

Our current operations are primarily focused on furthering the development of our clinical drug candidates for myeloablation, our CD33 program drug candidates, supporting investigator-initiated clinical trials that use our drug candidates and leveraging our AWE platform to create new clinical programs and contribute to collaborations.

Operations related to Iomab-B include progressing the ongoing multi-center Phase 3 pivotal trial (a trial that leads to registration trial marketing approved by the FDA), which includes investigator engagement, site activation and supporting patient enrollment. In addition, we are focused on commercial-scale manufacturing of apamistamab suitable for an approval trial and preparation of appropriate regulatory submissions. We are also focused on producing final Iomab-B drug product material that consists of apamistamab labelled with the isotope131I. We have secured access to131I produced by two premier commercial global suppliers. We project that these two suppliers have sufficient131I production capacity to meet our commercial needs for the Iomab-B program. We are aware of other global suppliers of131I with whom we believe we can secure commercial supply agreement if necessary. Operations related to our planned Phase 2 Actimab-MDS trial include preparation for appropriate regulatory submissions, protocol development and investigator engagement.

| 7 |

In the case of our CD33 program, key ongoing activities include progressing the multi-center Phase 2 Actimab-A trial, the Phase 1 Actimab-M trial and planned Phase 1 Actimab-A and CLAG-M combination trial, managing isotope and other materials supply chain and managing the manufacturing of the finished drug candidate product. We have secured access to225Ac through a renewable contractual arrangement with the United States Department of Energy, or DOE. We project that these quantities are sufficient to support early stages of commercialization of actinium isotope-based products and that the DOE’s accelerator route of production of225Ac has the potential to provide commercial quantities of225Ac. We have also developed our own proprietary process for industrial-scale225Ac production in a cyclotron in quantities adequate to support full product commercialization. In addition, we are aware of numerous sources from which we may secure additional quantities of the225Ac isotope.

Intellectual Property Portfolio and Regulatory Protections

Intellectual Property

We have developed or in-licensed numerous patents and patent applications and possess substantial know-how and trade secrets related to the development and manufacture of our products. As of March 2018, our patent portfolio includes: 68 issued and pending patent applications, of which 11 are issued in the United States, 4 are pending in the United States, and 53 are issued internationally and pending internationally. Additionally, several non-provisional patent applications are expected to be filed in 2018 based on provisional patent applications filed in 2017. This is part of an ongoing strategy to strengthen our intellectual property position. About one quarter of our patents are in-licensed from third parties and the remainder are Actinium-owned. These patents cover key areas of our business, including use of the actinium-225 and other alpha emitting isotopes attached to cancer specific carriers like monoclonal antibodies, methods for manufacturing key components of our product candidates including actinium-225, the alpha emitting radioisotope and carrier antibodies, and methods for manufacturing finished product candidates for use in cancer treatment.

We have licensed the rights to two issued patents in the area of drug preparation for methods of making humanized antibodies for our product Actimab-A that will expire in 2018 and 2019, respectively. We own five issued patents including one divisional patent in the United States and 32 patents outside of the United States, including one divisional patent related to the manufacturing of actinium in a cyclotron that will expire in 2027. We own or have licensed the rights to three issued patents in the United States and 14 patents outside of the United States related to the generation of radioimmunoconjugates that will expire in 2021, 2030 and 2032 respectively. We own or have licensed the rights to use one issued patent, one pending patent and two provisional patents for methods of treatment with our product Actimab-A that will expire in 2019. For Iomab-B we own one pending patent for anti-CD45 immunoglobulin composition and one pending patent the administration of a conjugated antibody.

A patent whose claims address methods of treating hematopoietic malignancies with Iomab-B is pending; still, we have developed a proprietary strategy based on trade secret protection and the potential for orphan drug and data exclusivities. The BC8 antibody, cell line and related know-how has been exclusively licensed by us from FHCRC in exchange for milestone payments, royalties and research support.

Patents related to the lintuzumab antibody component of our CD33 product candidates have been exclusively licensed by us from AbbVie Biotherapeutics Corp. for use with alpha-emitting radioisotopes in exchange for future development and commercialization milestones, a royalty on net sales for a period of 12.5 years from first commercial sale, a negotiation right to be our clinical and/or commercial antibody supplier, a negotiation right to co-promote Actimab-A in the United States on terms to be negotiated, and the grant-back of intellectual property (IP) rights covering improvements to the antibody for use other than with an alpha-emitting isotope. Patents covering actinium-225 conjugated to antibodies have been exclusively licensed by us from MSKCC in exchange for license fees, research support payments, development milestone payments, and royalties on net sales for the term of the licensed patents or, if later, 10 years from first commercial sale, or of any sublicense income we may receive. We source225Ac under an agreement with the Oak Ridge National Laboratory that expires at the end of 2018. We believe that we will be able to renew this contract for additional annual periods, as we have since 2009.

Regulatory Protections

The indications for which we are developing our product candidates for are orphan drug designations, which are disease indications that affect fewer than 200,000 patients in the United States and less than 5 in 10,000 patients in the European Union (“EU”). We have received orphan drug designation for Iomab-B and our lintuzumab-CD33 ARC for patients with AML in both the United States and the EU. As a result, if our products are to be approved they may receive 7 years and 10 years of market exclusivity in the US and EU, respectively. In addition, our product candidates are biologics combined with radioisotopes. The Hatch-Waxman Act requires that a manufacturer of generic drugs, for which a biologic drug is called a biosimilar, requires that the manufacturer demonstrate bioequivalence. We believe that due to the nature of radioisotopes having half-lives combined with the complexities of biologic drugs would make it difficult for a manufacturer to demonstrate bioequivalence of our product candidates.

Competition Overview

In the field of bone marrow transplantation, pharmaceuticals currently used for bone marrow ablation/conditioning are generic drugs and to our knowledge there are no significant industry efforts to advance clinical programs in the area of myeloablation that are directly competitive, especially in older patients. To our knowledge, we are the only company with a multi-disease, multi-target product pipeline that is focused on myeloablation.

| 8 |

For our CD33 Program, there are several companies developing drugs for AML based on numerous approaches/modalities including antibody drug conjugate (ADC), naked monoclonal antibodies and bispecific antibodies. Mylotarg™, an ADC developed and marketed by Pfizer is the only FDA approved CD33 targeted therapy for adult patients and children two years and older with relapsed or refractory CD33-positive AML. Seattle Genetics was developing SGN-CD33A, a CD33 targeting ADC, but discontinued the development of its clinical trials associated with this product candidate in June 2017. Immunogen is also developing a CD33 targeting ADC, IMGN779, that is currently in a Phase 1 clinical trial for r/r AML patients age 18 and above. Amgen is developing a CD3/CD33 bispecific BiTE (AMG330) as is Amphivena (AMV-564), both of which are in Phase 1 clinical trial for r/r AML patients age 18 and above. Boehringer Ingelheim is developing a CD33 targeting naked antibody (BI836858) for patients with r/r AML or MDS age 18 and above. These drugs have different safety profiles and mechanisms of action compared to our drug candidates. AML in older patients remains an area of high medical need that could accommodate many new products with favorable safety and efficiency profiles. We will begin studying our225Ac – lintuzumab ARC in combination with chemotherapy regimens for patients with AML. We have announced that our first combination trial will be with CLAG-M for patients with relapsed or refractory disease. Combination therapies are commonly used in hematologic indications, but we believe we are the only225Ac based ARC product candidate that is being explored in combination studies in hematologic indications. To our knowledge, we are the only company with a CD33 targeting drug and the only225Ac based ARC product candidate for patients with multiple myeloma.

Government Regulation

Governmental authorities in the United States and other countries extensively regulate, among other things, the research, development, testing, manufacture, labeling, promotion, advertising, distribution and marketing of radioimmunotherapy pharmaceutical products such as those being developed by us. In the United States, the FDA regulates such products under the Federal Food, Drug and Cosmetic Act (FDCA) and implements regulations. Failure to comply with applicable FDA requirements, both before and after approval, may subject us to administrative and judicial sanctions, such as a delay in approving or refusal by the FDA to approve pending applications, warning letters, product recalls, product seizures, total or partial suspension of production or distribution, injunctions and/or criminal prosecution.

U.S. Food and Drug Administration Regulation

Our research, development and clinical programs, as well as our manufacturing and marketing operations, are subject to extensive regulation in the United States and other countries. Most notably, all of our products that may in the future be sold in the United States are subject to regulation by the FDA. Certain of our product candidates in the United States require FDA pre-marketing approval of a BLA pursuant to 21 C.F.R. § 314. Foreign countries may require similar or more onerous approvals to manufacture or market these products.

Failure by us or by our suppliers to comply with applicable regulatory requirements can result in enforcement action by the FDA, the Nuclear Regulatory Commission or other regulatory authorities, which may result in sanctions, including but not limited to, untitled letters, warning letters, fines, injunctions, consent decrees and civil penalties; customer notifications or repair, replacement, refunds, recall, detention or seizure of our products; operating restrictions or partial suspension or total shutdown of production; refusing or delaying our requests for BLA premarket approval of new products or modified products; withdrawing BLA approvals that have already been granted; and refusal to grant export.

Employees

As of March 16, 2018, we have 25 full-time employees. None of these employees are covered by a collective bargaining agreement, and we believe our relationship with our employees is good. We also engage consultants on an as-needed basis to supplement existing staff.

| 9 |

In analyzing our company, you should consider carefully the following risk factors, together with all of the other information included in this Annual Report on Form 10-K. Factors that could cause or contribute to differences in our actual results include those discussed in the following subsection, as well as those discussed above in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere throughout this Annual Report on Form 10-K. Each of the following risk factors, either alone or taken together, could adversely affect our business, operating results and financial condition, as well as adversely affect the value of an investment in our company. The risks and uncertainties described below are not the only ones we face. Additional risks not currently known to us or other factors not perceived by us to present significant risks to our business at this time also may impair our business operations.

Risks Related to Our Business

We are a clinical-stage company and have generated no revenue from commercial sales to date.

We are a clinical-stage biopharmaceutical company with a limited operating history. We have no products approved for commercial sale and have not generated any revenue from product sales to date. We will encounter risks and difficulties frequently experienced by early-stage companies in rapidly evolving fields. If we do not address these risks successfully, our business will suffer.

We have incurred net losses in every year since our inception and anticipate that we will continue to incur net losses in the future.

We are not profitable and have incurred losses in each period since our inception. As of December 31, 2017, we had an accumulated deficit of $163.2 million. For the years ended December 31, 2017 and 2016, we reported a net loss of $26.6 million and $24.3 million, respectively. We expect to continue to operate at a net loss as we continue our research and development efforts, continue to conduct clinical trials and develop manufacturing, sales, marketing and distribution capabilities. There can be no assurance that the products under development by us will be approved for sale in the United States or elsewhere. Furthermore, there can be no assurance that if such products are approved they will be successfully commercialized, which would have an adverse effect on our business prospects, financial condition and results of operation.

If we fail to obtain additional financing, we will be unable to continue or complete our product development and you will likely lose your entire investment.

We do not currently have sufficient funding for the completion of development nor commercialization of our product candidates and we will need to continue to seek capital from time to time to continue development of our product candidates and to acquire and develop other product candidates. Our first product candidate is not expected to be commercialized, if approved, until at least 2019 and any partnering revenues that it may generate may not be sufficient to fund our ongoing operations. Our cash balance as of December 31, 2017 was $17.4 million. During the year ended December 31, 2017, we raised total net proceeds of approximately $3.8 million from the sale of our common stock through our ATM. On August 2, 2017, we completed an underwritten public offering of 21,500,000 shares of our common stock and warrants to purchase 18,275,000 shares of common stock at an offering price to the public of $0.75 per share. The gross proceeds from this offering were $16.1 million, before deducting underwriting discounts and commissions and other estimated offering expenses.

Our business or operations may change in a manner that would consume available funds more rapidly than anticipated and substantial additional funding may be required to maintain operations, fund expansion, develop new or enhanced products, acquire complementary products, business or technologies or otherwise respond to competitive pressures and opportunities, such as a change in the regulatory environment or a change in preferred cancer treatment modalities. However, we may not be able to secure funding when we need it or on favorable terms.

| 10 |

To raise additional capital, we may in the future offer additional shares of our common stock or other securities convertible into or exchangeable for our common stock. We cannot assure you that we will be able to sell shares or other securities in any other offering at a price per share that is equal to or greater than the price per share paid by investors, and investors purchasing shares or other securities in the future could have rights superior to existing stockholders.

If we cannot raise adequate funds to satisfy our capital requirements, we will have to delay, scale back or eliminate our research and development activities, clinical studies or future operations. We may also be required to obtain funds through arrangements with collaborators, which arrangements may require us to relinquish rights to certain technologies or products that we otherwise would not consider relinquishing, including rights to future product candidates or certain major geographic markets. We may further have to license our technology to others. This could result in sharing revenues which we might otherwise have retained for ourselves. Any of these actions may harm our business, financial condition and results of operations.

The amount of funding we will need depends on many factors, including the progress, timing and scope of our product development programs; the progress, timing and scope of our preclinical studies and clinical trials; the time and cost necessary to obtain regulatory approvals; the time and cost necessary to further develop manufacturing processes and arrange for contract manufacturing; our ability to enter into and maintain collaborative, licensing and other commercial relationships; and our partners’ commitment of time and resources to the development and commercialization of our products.

We have limited access to the capital markets and even if we can raise additional funding, we may be required to do so on terms that are dilutive to you.

We have limited access to the capital markets to raise funds. The capital markets have been unpredictable in the recent past for radioisotope and other oncology companies and unprofitable companies such as ours. In addition, it is generally difficult for development-stage companies to raise capital under current market conditions. The amount of capital that a company such as ours is able to raise often depends on variables that are beyond our control. As a result, we may not be able to secure financing on terms attractive to us, or at all. If we are able to consummate a financing arrangement, the amount raised may not be sufficient to meet our future needs. If adequate funds are not available on acceptable terms, or at all, our business, including our technology licenses, results of operations, financial condition and our continued viability will be materially adversely affected.

Risks Related to Regulation

The FDA or comparable foreign regulatory authorities may disagree with our regulatory plans and we may fail to obtain regulatory approval of our product candidates.

Our products are subject to rigorous regulation by the FDA and numerous other federal, state and foreign governmental authorities. The process of seeking regulatory approval to market a radio-immunotherapy product is expensive and time-consuming, and, notwithstanding the effort and expense incurred, approval is never guaranteed. If we are not successful in obtaining timely approval of our products from the FDA, we may never be able to generate significant revenue and may be forced to cease operations. In particular, the FDA permits commercial distribution of a new radio-immunotherapy product only after a Biologics License Application (BLA) for the product has received FDA approval. The BLA process is costly, lengthy and inherently uncertain. Any BLA filed by us will have to be supported by extensive data, including, but not limited to, technical, preclinical, clinical trial, manufacturing and labeling data, to demonstrate to the FDA’s satisfaction the safety and efficacy of the product for its intended use. The lengthy approval process as well as the unpredictability of future clinical trial results may result in our failing to obtain regulatory approval to market our product candidates, which would significantly harm our business, results of operations and prospects. In addition, even if we were to obtain approval, regulatory authorities may approve any of our product candidates for fewer or more limited indications than we request, may not approve the price we intend to charge for our products, may grant approval contingent on the performance of costly post-marketing clinical trials, or may approve a product candidate with a label that does not include the labeling claims necessary or desirable for the successful commercialization of that product candidate. Any of the foregoing scenarios could materially harm the commercial prospects for our product candidates.

| 11 |

The approval process in the United States and in other countries could result in unexpected and significant costs for us and consume management’s time and other resources. The FDA and other foreign regulatory agencies could ask us to supplement our submissions, collect non-clinical data, conduct additional clinical trials or engage in other time-consuming actions, or it could simply deny our applications. In addition, even if we obtain approval to market our products in the United States or in other countries, the approval could be revoked, or other restrictions imposed if post-market data demonstrates safety issues or lack of effectiveness. We cannot predict with certainty how, or when, the FDA or other regulatory authorities will act. If we are unable to obtain the necessary regulatory approvals, our financial condition and cash flow may be materially adversely affected, and our ability to grow domestically and internationally may be limited. Additionally, even if we obtain approval, regulatory authorities may approve any of our product candidates for fewer or more limited indications that we request. The Company’s products may not be approved for the specific indications that are most necessary or desirable for successful commercialization or profitability.

We have not demonstrated that any of our products are safe and effective for any indication.

We currently have three products in clinical development. In December 2015, the FDA cleared our IND filing for Iomab-B, and we are currently enrolling patients in the randomized, controlled, pivotal, Phase 3 clinical trial. Assuming the trial meets its endpoints, it will form the basis for a BLA. Additionally, there are physician IND trials at the FHCRC that have been conducted or are currently ongoing at FHCRC with Iomab-B and the BC8 antibody we licensed. We have completed the Phase 1 portion of the Phase 1/2 multi- center trial for patient with AML with fractionated doses of Actimab-A under its own federal IND and are enrolling patients in the Phase 2 portion of the trial. In February 2017, we initiated a Phase 1 clinical trial of Actimab-M in patients with refractory multiple myeloma and we are currently enrolling patients on this trial.

We may encounter substantial delays in our clinical trials or may not be able to conduct our trials on the timelines we expect.

We cannot predict whether we will encounter problems with any of our ongoing or planned clinical trials that will cause us or regulatory authorities to delay, suspend, or discontinue clinical trials or to delay the analysis of data from ongoing clinical trials. Any of the following could delay or disrupt the clinical development of our product candidates and potentially cause our product candidates to fail to receive regulatory approval:

| ● | conditions imposed on us by the FDA or comparable foreign authorities regarding the scope or design of our clinical trials; |

| ● | delays in receiving, or the inability to obtain, required approvals from institutional review boards (IRBs) or other reviewing entities at clinical sites selected for participation in our clinical trials; |

| ● | delays in enrolling patients into clinical trials; |

| ● | a lower than anticipated retention rate of patients in clinical trials; |

| ● | the need to repeat or discontinue clinical trials as a result of inconclusive or negative results or unforeseen complications in testing or because the results of later trials may not confirm positive results from earlier preclinical studies or clinical trials; | |

| ● | inadequate supply, delays in distribution, deficient quality of, or inability to purchase or manufacture drug product, comparator drugs or other materials necessary to conduct our clinical trials; |

| ● | unfavorable FDA or other foreign regulatory inspection and review of a clinical trial site or records of any clinical or preclinical investigation; |

| ● | serious and unexpected drug-related side effects experienced by participants in our clinical trials, which may occur even if they were not observed in earlier trials or only observed in a limited number of participants; |

| 12 |

| ● | a finding that the trial participants are being exposed to unacceptable health risks; |

| ● | the placement by the FDA or a foreign regulatory authority of a clinical hold on a trial; or |

| ● | delays in obtaining regulatory agency authorization for the conduct of our clinical trials. |

We may suspend, or the FDA or other applicable regulatory authorities may require us to suspend, clinical trials of a product candidate at any time if we or they believe the patients participating in such clinical trials, or in independent third party clinical trials for drugs based on similar technologies, are being exposed to unacceptable health risks or for other reasons.

Further, individuals involved with our clinical trials may serve as consultants to us from time to time and receive stock options or cash compensation in connection with such services. If these relationships and any related compensation to the clinical investigator carrying out the study result in perceived or actual conflicts of interest, or the FDA concludes that the financial relationship may have affected interpretation of the study, the integrity of the data generated at the applicable clinical trial site may be questioned and the utility of the clinical trial itself may be jeopardized. The delay, suspension or discontinuation of any of our clinical trials, or a delay in the analysis of clinical data for our product candidates, for any of the foregoing reasons, could adversely affect our efforts to obtain regulatory approval for and to commercialize our product candidates, increase our operating expenses and have a material adverse effect on our financial results.

Clinical trials may also be delayed or terminated as a result of ambiguous or negative interim results. In addition, a clinical trial may be suspended or terminated by us, the FDA, the IRBs at the sites where the IRBs are overseeing a trial, or a data safety monitoring board, or DSMB (Data Safety Monitoring Board)/DMC (Data Monitoring Committee), overseeing the clinical trial at issue, or other regulatory authorities due to a number of factors, including:

| ● | failure to conduct the clinical trial in accordance with regulatory requirements or our clinical protocols; |

| ● | inspection of the clinical trial operations or trial sites by the FDA or other regulatory authorities resulting in the imposition of a clinical hold; |

| ● | varying interpretation of data by the FDA or similar foreign regulatory authorities; |

| ● | failure to achieve primary or secondary endpoints or other failure to demonstrate efficacy; |

| ● | unforeseen safety issues; or |

| ● | lack of adequate funding to continue the clinical trial. |

Modifications to our product candidates may require federal approvals.

The BLA application is the vehicle through which the company may formally propose that the FDA approve a new pharmaceutical for sale and marketing in the United States. Once a particular product candidate receives FDA approval, expanded uses or uses in new indications of our products may require additional human clinical trials and new regulatory approvals, including additional IND and BLA submissions and premarket approvals before we can begin clinical development, and/or prior to marketing and sales. If the FDA requires new approvals for a particular use or indication, we may be required to conduct additional clinical studies, which would require additional expenditures and harm our operating results. If the products are already being used for these new indications, we may also be subject to significant enforcement actions.

Conducting clinical trials and obtaining approvals is a time-consuming process, and delays in obtaining required future approvals could adversely affect our ability to introduce new or enhanced products in a timely manner, which in turn would have an adverse effect on our business prospects, financial condition and results of operation.

| 13 |

The FDA or comparable foreign regulatory authorities may disagree with our regulatory plans, and we may fail to obtain regulatory approval of our product candidates.

In June 2012, we acquired rights to BC8 (Iomab), a clinical stage monoclonal antibody with safety and efficacy data in more than 500 patients in need of HSCT. Iomab-B is our product candidate that links131I to the BC8 antibody that is being studied in an ongoing Phase 3 pivotal trial. Product candidates utilizing this antibody would require BLA approval before they can be marketed in the United States. We have ongoing a Phase 2 portion of our multi-center Phase 1/2 Actimab-A clinical trial for our product candidate consisting of the anti-CD33 antibody lintuzumab linked with the isotope225Ac in AML. We are also studying our lintuzumab-225AC product candidate in our Phase 1 Actimab-M trial for patient with multiple myeloma and are planning to conduct a Phase 2 Actimab-MDS trial for patients with high-risk MDS with a p53 genetic mutation prior to a bone marrow transplant and are planning a Phase 1 clinical trial in combination with CLAG-M for patients with relapsed or refractory AML. Product candidates utilizing this antibody would require BLA approval before they can be marketed in the United States. We are in the early stages of evaluating other product candidates consisting of conjugates of225Ac with human or humanized antibodies for pre-clinical and clinical development in other types of cancer. The FDA may not approve these products for the indications that are necessary or desirable for successful commercialization. The FDA may fail to approve any BLA we submit for new product candidates or for new intended uses or indications for approved products or future product candidates. Failure to obtain FDA approval for our products in the proposed indications would have a material adverse effect on our business prospects, financial condition and results of operations.

Clinical trials necessary to support approval of our product candidates are time-consuming and expensive.

Initiating and completing clinical trials necessary to support FDA approval of a BLA for Iomab-B, CD33 program candidates, and other product candidates, is a time-consuming and expensive process, and the outcome is inherently uncertain. Moreover, the results of early clinical trials are not necessarily predictive of future results, and any product candidate we advance into clinical trials may not have favorable results in later clinical trials. We have worked with the FDA to develop a clinical trial designed to test the safety and efficacy of Iomab-B in patients with relapsed or refractory AML who are age 55 and above prior to a BMT. This trial is designed to support a BLA filing for marketing approval by the FDA, pending results from the trial. We have also worked with the FDA to develop a clinical trial designed to test the initial safety and efficacy of Actimab-A in newly diagnosed AML patients over the age of 60. Subsequent to the completion of the Phase 1 portion of the Phase 1/2 clinical trial we submitted protocol amendments to the FDA in August of 2016, which were agreed upon in September of 2016. The Phase 2 portion of the trial is now underway with the purpose of examining the use of Actimab-A in AML patients who are not eligible for approved forms of treatment with curative intent. The trial is not designed to support marketing approval for the product candidate, and one or more additional trials will have to be conducted in the future before we file a BLA. In addition, there can be no assurance that the data generated during the trial will meet our chosen safety and effectiveness endpoints or otherwise produce results that will eventually support the filing or approval of a BLA. Even if the data from this trial are favorable, these data may not be predictive of the results of any future clinical trials.

Our clinical trials may fail to demonstrate adequately the efficacy and safety of our product candidates, which would prevent or delay regulatory approval and commercialization.

Even if our clinical trials are completed as planned, we cannot be certain that their results will support our product candidate claims or that the FDA or foreign authorities will agree with our conclusions regarding them. Success in pre-clinical studies and early clinical trials does not ensure that later clinical trials will be successful, and we cannot be sure that the later trials will replicate the results of prior trials and pre-clinical studies. The clinical trial process may fail to demonstrate that our product candidates are safe and effective for the proposed indicated uses. If FDA concludes that the clinical trials for Iomab-B, Actimab-A, Actimab-M, or any other product candidate for which we might seek approval, have failed to demonstrate safety and effectiveness, we would not receive FDA approval to market that product candidate in the United States for the indications sought. In addition, such an outcome could cause us to abandon the product candidate and might delay development of others. Any delay or termination of our clinical trials will delay or preclude the filing of any submissions with the FDA and, ultimately, our ability to commercialize our product candidates and generate revenues. It is also possible that patients enrolled in clinical trials will experience adverse side effects that are not currently part of a product candidate’s profile.

| 14 |

The intellectual property related to antibodies we have licensed has expired or likely expired

The humanized antibody, lintuzumab, which we use in our CD33 program product candidates is covered by the claims of issued patents that we license from Facet Biotech Corporation, a wholly-owned subsidiary of AbbVie Laboratories. We believe the key patents related to this antibody have likely expired and are undertaking a review of the intellectual property and conducting a business analysis related to this agreement. Post patent expiration, it is generally possible that others may be eventually able to use an antibody with the same sequence, and we will then need to rely on additional patent protection covering alpha particle drug products comprising225Ac. Any competing product based on the lintuzumab antibody is likely to require several years of development before achieving our product candidate’s current status and may be subject to significant regulatory hurdles but is nevertheless a possibility that could negatively impact our business in the future. Neither the antibody portion nor the composition of matter as a whole for the conjugated Iomab-B product candidate is covered by the claims of any issued or pending patents. Accordingly, there are no patents that would prevent others from using an antibody with the same antibody sequence in any drug product (e.g., those comprising131I or alpha particle emitters). Any competing product based on the antibody used in Iomab-B is likely to require several years of development before achieving our product candidate’s current status and may be subject to significant regulatory hurdles but is nevertheless a possibility that could negatively impact our business in the future.

The indications for which we are developing our product candidates for are orphan drug designations, which are disease indications that affect fewer than 200,000 patients in the United States and less than 5 in 10,000 patients in the European Union (“EU”). We have received orphan drug designation for Iomab-B and our lintuzumab-CD33 ARC for patients with AML in both the United States and the EU. As a result, if our products are to be approved they may receive 7 years and 10 years of market exclusivity in the US and EU, respectively. In addition, our product candidates are biologics combined with radioisotopes. The Hatch-Waxman Act requires that a manufacturer of generic drugs, which for a biologic drug is called a biosimilar, requires that the manufacturer demonstrate bioequivalence. We believe that due to the nature of radioisotopes having half-lives combined with the complexities of biologic drugs would make it difficult for a manufacturer to demonstrate bioequivalence of our product candidates.

Our CD33 program clinical trials are testing the same drug construct

Our CD33 program clinical trials including our Phase 2 Actimab-A trial in AML, Phase 1 trial in multiple myeloma, planned Phase 2 trial in high-risk MDS and planned Phase 1 trial in combination with CLAG-M in AML are studying the same drug construct consisting of225Ac labeled lintuzumab. Negative results from any of these trials could negatively impact our ability to enroll or complete our other trials studying225Ac labeled lintuzumab.

We may be unable to obtain a sufficient supply of225Acmedical grade isotope.

225Ac medical grade isotope is a key component of Actimab-A, Actimab-M and other225Ac based drug candidates that we might consider. There are limited quantities of225Ac available today. The existing supplier of225Ac to us is Oak Ridge National Laboratory, or ORNL, a science and energy national laboratory in the Department of Energy system. ORNL manufactures225Ac by eluting it from its supply of Thorium-229. Although this has proven to be a very reliable source of production for a number of years, it is limited by the quantity of Thorium-229 at ORNL. We believe that the current approximate maximum of225Ac production from this source is sufficient for approximately 1,000–2,000 patient treatments per year. Since our needs are significantly below that amount at this time and will continue to be below that prior to commercializing a product with a potential of selling more than 2,000 patient doses per year, we believe that this supply will be sufficient for completion of clinical trials and early commercialization. Our contract for supply of this isotope from ORNL must be renewed yearly, and the current contract extends through the end of 2018. While we expect this contract will be renewed at the end of its term as it has since 2009, there can be no assurance that ORNL will renew the contract or that the United States Department of Energy will not change its policies that allow for the sale of isotope to us. Failure to acquire sufficient quantities of medical grade225Ac would make it impossible to effectively complete clinical trials and to commercialize Actimab-A, Actimab-M and any other225Ac based drug candidates that we may develop and would materially harm our business.

| 15 |

If we encounter difficulties enrolling patients in our clinical trials, our clinical development activities could be delayed or otherwise adversely affected.

The timely completion of clinical trials in accordance with their protocols depends on our ability to enroll a sufficient number of patients who remain in the trial until its conclusion. We may experience difficulties in patient enrollment in our clinical trials for a variety of reasons, including:

| ● | the size and nature of the patient population; |

| ● | the patient eligibility criteria defined in the protocol; |

| ● | the size of the study population required for analysis of the trial’s primary endpoints; |

| ● | the proximity of patients to trial sites; |