KBL Healthcare Acquisition Corp III (KHA) Inactive

Filed: 3 Jun 09, 12:00am

To Engage in Business Combination with

To Engage in Business Combination with

KBL Healthcare Acquisition Corp. III (NYSE Amex: KHA) Investor Presentation PRWT Services, Inc. June 2, 2009

www.kblhealthcare.com www.prwt.com

2 Interests of the Parties in the Merger KBL HEALTHCARE ACQUISTION CORP. III (“KBL”) AND PRWT SERVICES, INC. (“PRWT”) ARE HOLDING PRESENTATIONS FOR CERTAIN OF KBL’S STOCKHOLDERS, AS WELL AS

2 Interests of the Parties in the Merger KBL HEALTHCARE ACQUISTION CORP. III (“KBL”) AND PRWT SERVICES, INC. (“PRWT”) ARE HOLDING PRESENTATIONS FOR CERTAIN OF KBL’S STOCKHOLDERS, AS WELL AS

OTHER PERSONS WHO MIGHT BE INTERESTED IN PURCHASING KBL SECURITIES, REGARDING THE BUSINESS COMBINATION BETWEEN KBL AND PRWT, AS DESCRIBED IN

THE PRELIMINARY PROXY STATEMENT/PROSPECTUS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON APRIL 22, 2009, AS SAME IS AMENDED FROM TIME TO

TIME. SUCH PRELIMINARY PROXY STATEMENT/PROSPECTUS, INCLUDING SOME OR ALL OF THE EXHIBITS ATTACHED THERETO, AND THIS PRESENTATION WILL BE

DISTRIBUTED TO PARTICIPANTS AT SUCH PRESENTATIONS. CITIGROUP GLOBAL MARKETS, INC. (“CITIGROUP”), JEFFERIES & COMPANY, INC. (“JEFFERIES”) AND EARLYBIRDCAPITAL, INC. (“EBC”), EACH AN UNDERWRITER OF KBL’S

INITIAL PUBLIC OFFERING (“IPO”) CONSUMMATED IN JULY 2007, ARE ASSISTING KBL IN THESE EFFORTS WITHOUT CHARGE, OTHER THAN THE REIMBURSEMENT OF THEIR

OUT-OF-POCKET EXPENSES. ADDITIONALLY, THE UNDERWRITERS DEFERRED $4,140,000 OF THE COMMISSIONS OWED TO THEM IN CONNECTION WITH THE IPO UNTIL THE

CLOSING OF KBL’S BUSINESS COMBINATION. FURTHER, KBL HEALTHCARE MANAGEMENT, INC. (“KHMI”), AN AFFILIATE OF CERTAIN OF THE EXECUTIVE OFFICERS AND

DIRECTORS OF KBL, HAS ENTERED INTO A GENERAL ADVISORY AGREEMENT WITH PRWT, WHICH WILL BECOME EFFECTIVE UPON CONSUMMATION OF THE BUSINESS

COMBINATION BETWEEN KBL AND PRWT, UNDER WHICH KHMI WOULD BE PAID A FEE OF $250,000 PER YEAR IN CONNECTION WITH SERVICES TO BE RENDERED TO PRWT,

AND CERTAIN OF PRWT’S OFFICERS WILL ENTER INTO NEW EMPLOYMENT AGREEMENTS TO BE EFFECTIVE UPON CONSUMMATION OF THE BUSINESS COMBINATION. KBL AND ITS DIRECTORS AND EXECUTIVE OFFICERS, PRWT AND ITS STOCKHOLDERS, DIRECTORS AND EXECUTIVE OFFICERS, AND THEIR RESPECTIVE AFFILIATES, MAY

ENTER INTO ARRANGEMENTS TO PURCHASE SHARES OF COMMON STOCK AND/OR WARRANTS OF KBL IN OPEN MARKET OR PRIVATELY NEGOTIATED TRANSACTIONS PRIOR

TO THE CONSUMMATION OF THE BUSINESS COMBINATION. KBL AND ITS DIRECTORS AND EXECUTIVE OFFICERS, PRWT AND ITS STOCKHOLDERS, DIRECTORS AND EXECUTIVE OFFICERS, AND EACH OF CITIGROUP, JEFFERIES AND

EBC MAY BE DEEMED TO BE PARTICIPANTS IN THE SOLICITATION OF PROXIES FOR THE SPECIAL MEETING OF KBL STOCKHOLDERS TO BE HELD TO APPROVE THE MERGER. STOCKHOLDERS OF KBL AND OTHER INTERESTED PERSONS ARE ADVISED TO READ KBL’S AND PRWT’S PRELIMINARY PROXY STATEMENT/PROSPECTUS AND, WHEN

AVAILABLE, KBL’S AND PRWT’S DEFINITIVE PROXY STATEMENT/PROSPECTUS IN CONNECTION WITH KBL’S SOLICITATION OF PROXIES FOR THE SPECIAL MEETING BECAUSE

THESE PROXY STATEMENT/PROSPECTUSES WILL CONTAIN IMPORTANT INFORMATION. SUCH PERSONS CAN ALSO READ KBL’S FINAL PROSPECTUS, DATED JULY 19, 2007,

FOR A DESCRIPTION OF THE SECURITY HOLDINGS OF THE KBL OFFICERS AND DIRECTORS AND OF THE UNDERWRITERS AND THEIR RESPECTIVE INTERESTS IN THE

SUCCESSFUL CONSUMMATION OF THIS BUSINESS COMBINATION. THE DEFINITIVE PROXY STATEMENT/PROSPECTUS WILL BE MAILED TO KBL STOCKHOLDERS AS OF THE

RECORD DATE TO VOTE ON THE ACQUISITION. STOCKHOLDERS WILL ALSO BE ABLE TO OBTAIN A COPY OF THE DEFINITIVE PROXY STATEMENT/PROSPECTUS, WITHOUT

CHARGE, BY DIRECTING A REQUEST TO: KBL HEALTHCARE ACQUISTION CORP. IIII, 380 LEXINGTON AVENUE, 31ST FLOOR, NEW YORK, NEW YORK 10168. THE DEFINITIVE

PROXY STATEMENT/PROSPECTUS CAN ALSO BE OBTAINED, WITHOUT CHARGE, AT THE SECURITIES AND EXCHANGE COMMISSION’S INTERNET SITE (HTTP://WWW.SEC.GOV).

3 Forward-Looking Statements THIS PRESENTATION CONTAINS FORWARD-LOOKING STATEMENTS. FORWARD-LOOKING STATEMENTS INCLUDE, BUT ARE NOT LIMITED TO, STATEMENTS REGARDING KBL’S

3 Forward-Looking Statements THIS PRESENTATION CONTAINS FORWARD-LOOKING STATEMENTS. FORWARD-LOOKING STATEMENTS INCLUDE, BUT ARE NOT LIMITED TO, STATEMENTS REGARDING KBL’S

AND/OR PRWT’S OR THEIR RESPECTIVE MANAGEMENT’S EXPECTATIONS, HOPES, BELIEFS, INTENTIONS OR STRATEGIES REGARDING THE FUTURE. IN ADDITION, ANY

STATEMENTS THAT REFER TO PROJECTIONS, FORECASTS OR OTHER CHARACTERIZATIONS OF FUTURE EVENTS OR CIRCUMSTANCES, INCLUDING ANY UNDERLYING

ASSUMPTIONS, ARE FORWARD-LOOKING STATEMENTS. THE WORDS “ANTICIPATE,” “BELIEVE,” “CONTINUE,” “COULD,” “ESTIMATE,” “EXPECT,” “INTEND,” “MAY,” “MIGHT,” “PLAN,”

“POSSIBLE,” “POTENTIAL,” “PREDICT,” “SHOULD,” “WOULD” AND SIMILAR EXPRESSIONS MAY IDENTIFY FORWARD-LOOKING STATEMENTS, BUT THE ABSENCE OF THESE

WORDS DOES NOT MEAN THAT A STATEMENT IS NOT FORWARD-LOOKING. FORWARD-LOOKING STATEMENTS MAY INCLUDE, FOR EXAMPLE, STATEMENTS ABOUT OUR:

ABILITY TO COMPLETE A COMBINATION WITH ONE OR MORE TARGET BUSINESSES; SUCCESS IN RETAINING OR RECRUITING, OR CHANGES REQUIRED IN, OUR OFFICERS,

KEY EMPLOYEES OR DIRECTORS FOLLOWING A BUSINESS COMBINATION; OUR MANAGEMENT TEAM’S ALLOCATION OF THEIR TIME TO OTHER BUSINESSES AND

POTENTIALLY HAVING CONFLICTS OF INTEREST WITH OUR BUSINESS OR IN APPROVING A BUSINESS COMBINATION; POTENTIAL INABILITY TO OBTAIN ADDITIONAL

FINANCING TO COMPLETE A BUSINESS COMBINATION; AN INABILITY TO SATISFY THE CONDITIONS TO THE BUSINESS COMBINATION; LIMITED POOL OF PROSPECTIVE

TARGET BUSINESSES; POTENTIAL CHANGE IN CONTROL IF WE ACQUIRE ONE OR MORE TARGET BUSINESSES FOR STOCK; PUBLIC SECURITIES’ LIMITED LIQUIDITY AND

TRADING; FAILURE TO LIST OR DELISTING OF OUR SECURITIES FROM THE NYSE AMEX STOCK EXCHANGE OR AN INABILITY TO HAVE OUR SECURITIES LISTED ON THE

NASDAQ STOCK EXCHANGE FOLLOWING A BUSINESS COMBINATION; USE OF PROCEEDS NOT IN TRUST OR AVAILABLE TO US FROM INTEREST INCOME ON THE TRUST

ACCOUNT BALANCE; OUR FINANCIAL PERFORMANCE FOLLOWING THE BUSINESS COMBINATION; PRWT’S INABILITY TO ACHIEVE ITS BUSINESS OBJECTIVES OR IMPLEMENT

ITS STRATEGIES OR MAINTAIN ITS MINORITY COMPANY CERTIFCATIONS; OR AN INABILITY TO SECURE CONTRACTS CURRENTLY BEING NEGOTIATED OR TO BE NEGOTIATED

IN THE FUTURE. THE FORWARD-LOOKING STATEMENTS CONTAINED IN THIS PRESENTATION ARE BASED ON OUR CURRENT EXPECTATIONS AND BELIEFS CONCERNING FUTURE

DEVELOPMENTS AND THEIR POTENTIAL EFFECTS ON US. THERE CAN BE NO ASSURANCE THAT FUTURE DEVELOPMENTS AFFECTING US WILL BE THOSE THAT WE HAVE

ANTICIPATED. THESE FORWARD-LOOKING STATEMENTS INVOLVE A NUMBER OF RISKS, UNCERTAINTIES (SOME OF WHICH ARE BEYOND OUR CONTROL) OR OTHER

ASSUMPTIONS THAT MAY CAUSE ACTUAL RESULTS OR PERFORMANCE TO BE MATERIALLY DIFFERENT FROM THOSE EXPRESSED OR IMPLIED BY THESE FORWARD-

LOOKING STATEMENTS. THESE RISKS AND UNCERTAINTIES INCLUDE, BUT ARE NOT LIMITED TO, THOSE FACTORS DESCRIBED UNDER THE HEADING “RISK FACTORS.”

SHOULD ONE OR MORE OF THESE RISKS OR UNCERTAINTIES MATERIALIZE, OR SHOULD ANY OF OUR ASSUMPTIONS PROVE INCORRECT, ACTUAL RESULTS MAY VARY IN

MATERIAL RESPECTS FROM THOSE PROJECTED IN THESE FORWARD-LOOKING STATEMENTS. WE UNDERTAKE NO OBLIGATION TO UPDATE OR REVISE ANY FORWARD-

LOOKING STATEMENTS, WHETHER AS A RESULT OF NEW INFORMATION, FUTURE EVENTS OR OTHERWISE, EXCEPT AS MAY BE REQUIRED UNDER APPLICABLE SECURITIES

LAWS AND/OR IF AND WHEN MANAGEMENT KNOWS OR HAS A REASONABLE BASIS ON WHICH TO CONCLUDE THAT PREVIOUSLY DISCLOSED PROJECTIONS ARE NO LONGER

REASONABLY ATTAINABLE. THIS CURRENT REPORT AND THE EXHIBITS HERETO INCLUDE CERTAIN FINANCIAL INFORMATION NOT DERIVED IN ACCORDANCE WITH GENERALLY ACCEPTED ACCOUNTING

PRINCIPLES ("GAAP"). KBL AND PRWT BELIEVE THAT THE PRESENTATION OF THESE NON-GAAP MEASURES PROVIDE INFORMATION THAT IS USEFUL TO INVESTORS. WE

HAVE INCLUDED A RECONCILIATION OF THIS INFORMATION TO THE MOST COMPARABLE GAAP MEASURES WHERE APPLICABLE.

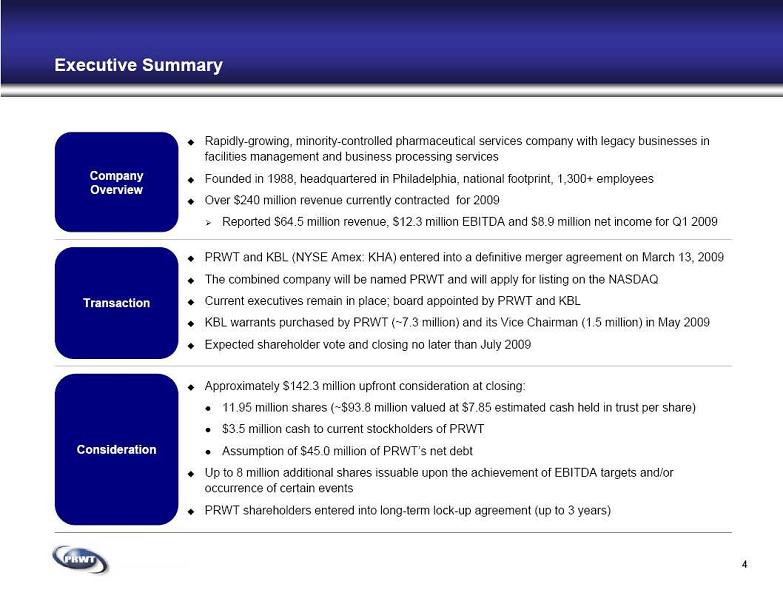

Executive Summary Transaction Consideration PRWT and KBL (NYSE Amex: KHA) entered into a definitive merger agreement on March 13, 2009 The combined company will be named PRWT and will apply for listing on the NASDAQ Current executives remain in place; board appointed by PRWT and KBL KBL warrants purchased by PRWT (~7.3 million) and its Vice Chairman (1.5 million) in May 2009 Expected shareholder vote and closing no later than July 2009 Approximately $142.3 million upfront consideration at closing: 11.95 million shares (~$93.8 million valued at $7.85 estimated cash held in trust per share) $3.5 million cash to current stockholders of PRWT Assumption of $45.0 million of PRWT’s net debt Up to 8 million additional shares issuable upon the achievement of EBITDA targets and/or

Executive Summary Transaction Consideration PRWT and KBL (NYSE Amex: KHA) entered into a definitive merger agreement on March 13, 2009 The combined company will be named PRWT and will apply for listing on the NASDAQ Current executives remain in place; board appointed by PRWT and KBL KBL warrants purchased by PRWT (~7.3 million) and its Vice Chairman (1.5 million) in May 2009 Expected shareholder vote and closing no later than July 2009 Approximately $142.3 million upfront consideration at closing: 11.95 million shares (~$93.8 million valued at $7.85 estimated cash held in trust per share) $3.5 million cash to current stockholders of PRWT Assumption of $45.0 million of PRWT’s net debt Up to 8 million additional shares issuable upon the achievement of EBITDA targets and/or

occurrence of certain events PRWT shareholders entered into long-term lock-up agreement (up to 3 years) Company

Overview Rapidly-growing, minority-controlled pharmaceutical services company with legacy businesses in

facilities management and business processing services Founded in 1988, headquartered in Philadelphia, national footprint, 1,300+ employees Over $240 million revenue currently contracted for 2009 Reported $64.5 million revenue, $12.3 million EBITDA and $8.9 million net income for Q1 2009 4

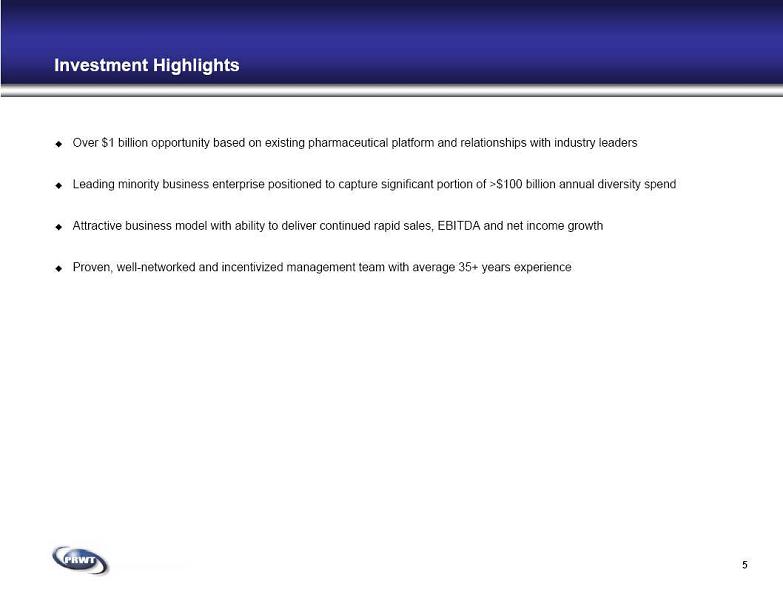

Investment Highlights 5 Over $1 billion opportunity based on existing pharmaceutical platform and relationships with industry leaders Leading minority business enterprise positioned to capture significant portion of >$100 billion annual diversity spend Attractive business model with ability to deliver continued rapid sales, EBITDA and net income growth Proven, well-networked and incentivized management team with average 35+ years experience

Investment Highlights 5 Over $1 billion opportunity based on existing pharmaceutical platform and relationships with industry leaders Leading minority business enterprise positioned to capture significant portion of >$100 billion annual diversity spend Attractive business model with ability to deliver continued rapid sales, EBITDA and net income growth Proven, well-networked and incentivized management team with average 35+ years experience

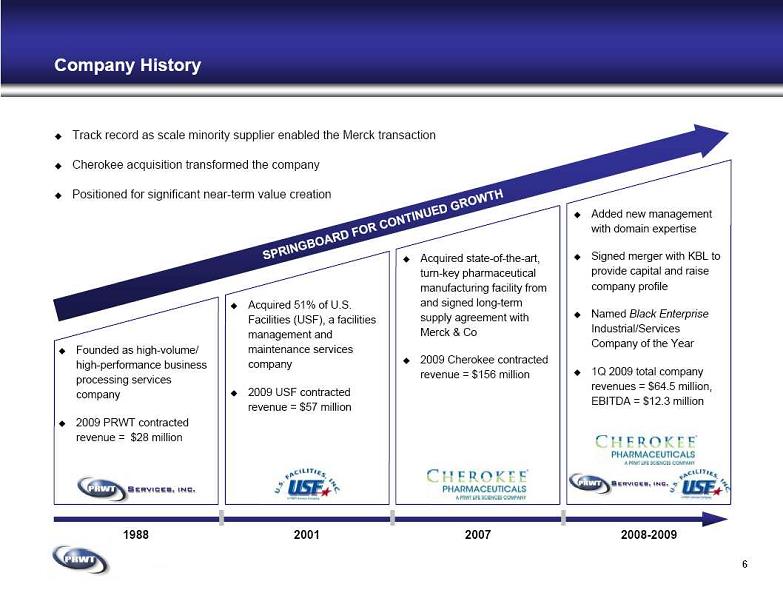

Company History Acquired 51% of U.S.

Company History Acquired 51% of U.S.

Facilities (USF), a facilities

management and

maintenance services

company 2009 USF contracted

revenue = $57 million Acquired state-of-the-art,

turn-key pharmaceutical

manufacturing facility from

and signed long-term

supply agreement with

Merck & Co 2009 Cherokee contracted

revenue = $156 million 2001 2008-2009 Founded as high-volume/

high-performance business

processing services

company 2009 PRWT contracted

revenue = $28 million 6 Added new management

with domain expertise Signed merger with KBL to

provide capital and raise

company profile Named Black Enterprise

Industrial/Services

Company of the Year 1Q 2009 total company

revenues = $64.5 million,

EBITDA = $12.3 million 2007 1988 Track record as scale minority supplier enabled the Merck transaction Cherokee acquisition transformed the company Positioned for significant near-term value creation

7 Cherokee Pharmaceuticals Cherokee Pharmaceuticals facility in Riverside, PA. 340 Acres 105 Buildings 400 Employees Pittsburgh Erie Scranton Allentown Philadelphia Harrisburg Rt. 80 Riverside

7 Cherokee Pharmaceuticals Cherokee Pharmaceuticals facility in Riverside, PA. 340 Acres 105 Buildings 400 Employees Pittsburgh Erie Scranton Allentown Philadelphia Harrisburg Rt. 80 Riverside

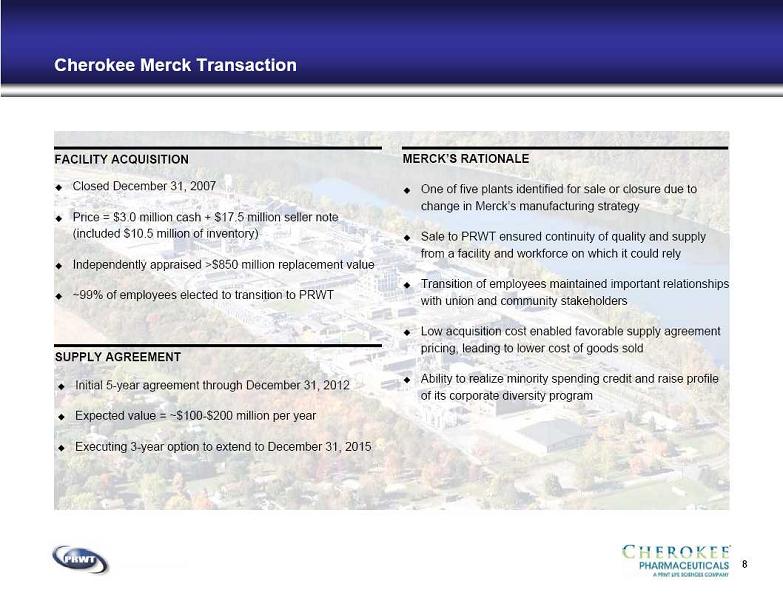

8 Cherokee Merck Transaction FACILITY ACQUISITION SUPPLY AGREEMENT Closed December 31, 2007 Price = $3.0 million cash + $17.5 million seller note

8 Cherokee Merck Transaction FACILITY ACQUISITION SUPPLY AGREEMENT Closed December 31, 2007 Price = $3.0 million cash + $17.5 million seller note

(included $10.5 million of inventory) Independently appraised >$850 million replacement value ~99% of employees elected to transition to PRWT MERCK’S RATIONALE One of five plants identified for sale or closure due to

change in Merck’s manufacturing strategy Sale to PRWT ensured continuity of quality and supply

from a facility and workforce on which it could rely Transition of employees maintained important relationships

with union and community stakeholders Low acquisition cost enabled favorable supply agreement

pricing, leading to lower cost of goods sold Ability to realize minority spending credit and raise profile

of its corporate diversity program Initial 5-year agreement through December 31, 2012 Expected value = ~$100-$200 million per year Executing 3-year option to extend to December 31, 2015

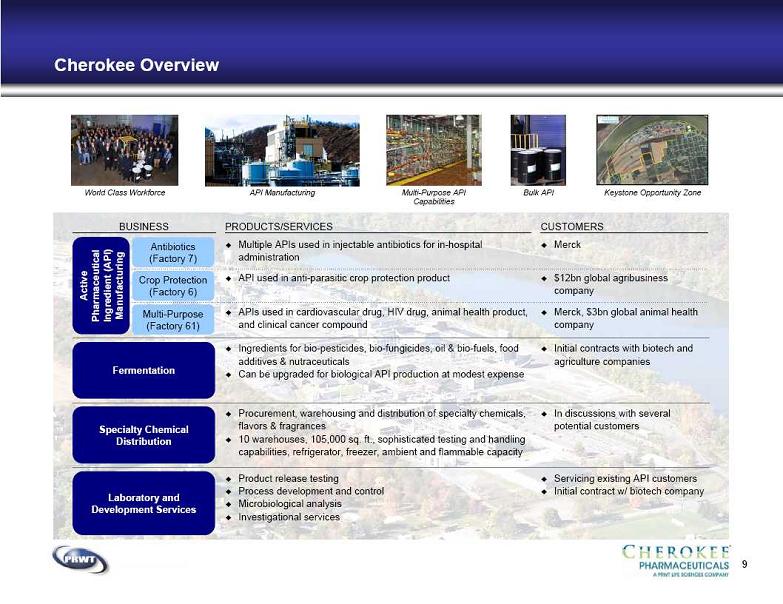

9 Cherokee Overview API Manufacturing Multi-Purpose API

9 Cherokee Overview API Manufacturing Multi-Purpose API

Capabilities CUSTOMERS Merck Initial contracts with biotech and

agriculture companies In discussions with several

potential customers Servicing existing API customers Initial contract w/ biotech company $12bn global agribusiness

company Merck, $3bn global animal health

company BUSINESS Fermentation Specialty Chemical

Distribution Laboratory and

Development Services Antibiotics

(Factory 7) Crop Protection

(Factory 6) Multi-Purpose

(Factory 61) PRODUCTS/SERVICES Multiple APIs used in injectable antibiotics for in-hospital

administration Ingredients for bio-pesticides, bio-fungicides, oil & bio-fuels, food

additives & nutraceuticals Can be upgraded for biological API production at modest expense Procurement, warehousing and distribution of specialty chemicals,

flavors & fragrances 10 warehouses, 105,000 sq. ft., sophisticated testing and handling

capabilities, refrigerator, freezer, ambient and flammable capacity Product release testing Process development and control Microbiological analysis Investigational services API used in anti-parasitic crop protection product APIs used in cardiovascular drug, HIV drug, animal health product,

and clinical cancer compound Bulk API Keystone Opportunity Zone World Class Workforce

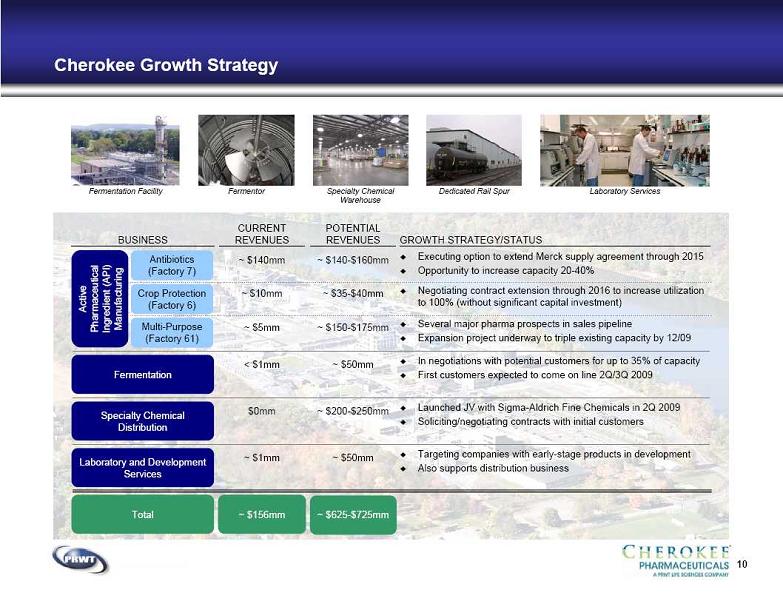

10 Cherokee Growth Strategy Laboratory Services Specialty Chemical

10 Cherokee Growth Strategy Laboratory Services Specialty Chemical

Warehouse Fermentor GROWTH STRATEGY/STATUS Executing option to extend Merck supply agreement through 2015 Opportunity to increase capacity 20-40% Negotiating contract extension through 2016 to increase utilization

to 100% (without significant capital investment) Several major pharma prospects in sales pipeline Expansion project underway to triple existing capacity by 12/09 In negotiations with potential customers for up to 35% of capacity First customers expected to come on line 2Q/3Q 2009 Launched JV with Sigma-Aldrich Fine Chemicals in 2Q 2009 Soliciting/negotiating contracts with initial customers Targeting companies with early-stage products in development Also supports distribution business BUSINESS Fermentation Specialty Chemical

Distribution Laboratory and Development

Services Antibiotics

(Factory 7) Crop Protection

(Factory 6) Multi-Purpose

(Factory 61) Total CURRENT

REVENUES ~ $140mm ~ $10mm ~ $5mm < $1mm $0mm ~ $1mm ~ $156mm POTENTIAL

REVENUES ~ $625-$725mm ~ $140-$160mm ~ $35-$40mm ~ $150-$175mm ~ $50mm ~ $200-$250mm ~ $50mm Fermentation Facility Dedicated Rail Spur

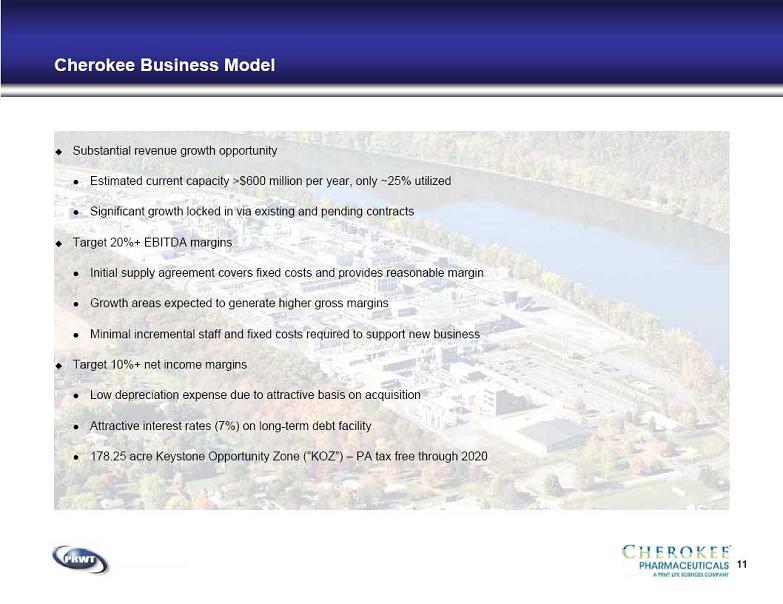

11 Cherokee Business Model Substantial revenue growth opportunity Estimated current capacity >$600 million per year, only ~25% utilized Significant growth locked in via existing and pending contracts Target 20%+ EBITDA margins Initial supply agreement covers fixed costs and provides reasonable margin Growth areas expected to generate higher gross margins Minimal incremental staff and fixed costs required to support new business Target 10%+ net income margins Low depreciation expense due to attractive basis on acquisition Attractive interest rates (7%) on long-term debt facility 178.25 acre Keystone Opportunity Zone (“KOZ”) – PA tax free through 2020

11 Cherokee Business Model Substantial revenue growth opportunity Estimated current capacity >$600 million per year, only ~25% utilized Significant growth locked in via existing and pending contracts Target 20%+ EBITDA margins Initial supply agreement covers fixed costs and provides reasonable margin Growth areas expected to generate higher gross margins Minimal incremental staff and fixed costs required to support new business Target 10%+ net income margins Low depreciation expense due to attractive basis on acquisition Attractive interest rates (7%) on long-term debt facility 178.25 acre Keystone Opportunity Zone (“KOZ”) – PA tax free through 2020

12 Cherokee Competitive Positioning Customers under long-term contract and have long-

12 Cherokee Competitive Positioning Customers under long-term contract and have long-

standing relationships with Cherokee Many products require dedicated facilities and/or complex

manufacturing techniques that would be hard to replicate Pharmaceutical products (including manufacturing

processes) are highly regulated by FDA Offshore (e.g. China/India) manufacturing considered risky

for high-value and/or hard-to-manufacture products High quality and service levels State-of-the-art facility/workforce with big pharma

capabilities and infrastructure Reliable U.S.-based outsourcing solution with 50+ year

track record and Merck heritage Cost competitive solution relative to internal production or

alternative suppliers Plus, minority supplier spending credit HIGH SWITCHING COSTS FOR CURRENT CUSTOMERS ATTRACTIVE OFFERING TO NEW CUSTOMERS

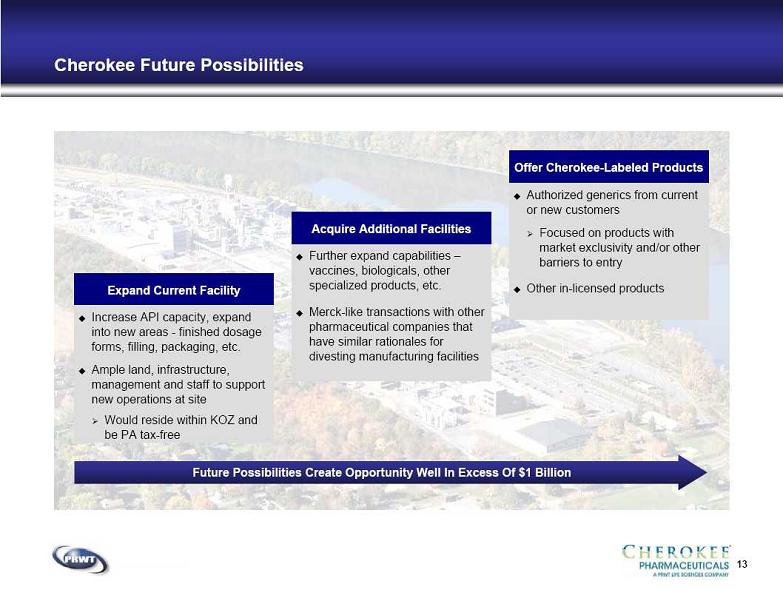

13 Cherokee Future Possibilities Acquire Additional Facilities Further expand capabilities –

13 Cherokee Future Possibilities Acquire Additional Facilities Further expand capabilities –

vaccines, biologicals, other

specialized products, etc. Merck-like transactions with other

pharmaceutical companies that

have similar rationales for

divesting manufacturing facilities Expand Current Facility Increase API capacity, expand

into new areas - finished dosage

forms, filling, packaging, etc. Ample land, infrastructure,

management and staff to support

new operations at site Would reside within KOZ and

be PA tax-free Offer Cherokee-Labeled Products Authorized generics from current

or new customers Focused on products with

market exclusivity and/or other

barriers to entry Other in-licensed products Future Possibilities Create Opportunity Well In Excess Of $1 Billion

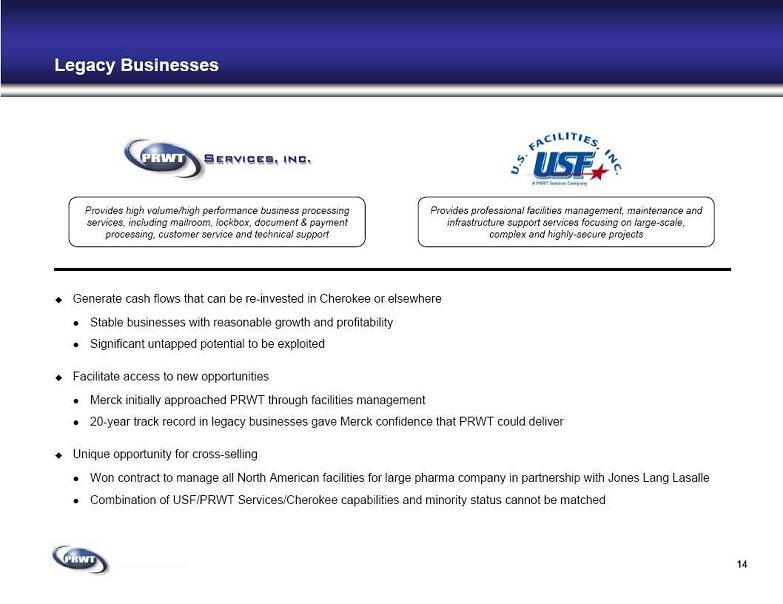

14 Legacy Businesses Generate cash flows that can be re-invested in Cherokee or elsewhere Stable businesses with reasonable growth and profitability Significant untapped potential to be exploited Facilitate access to new opportunities Merck initially approached PRWT through facilities management 20-year track record in legacy businesses gave Merck confidence that PRWT could deliver Unique opportunity for cross-selling Won contract to manage all North American facilities for large pharma company in partnership with Jones Lang Lasalle Combination of USF/PRWT Services/Cherokee capabilities and minority status cannot be matched Provides high volume/high performance business processing

14 Legacy Businesses Generate cash flows that can be re-invested in Cherokee or elsewhere Stable businesses with reasonable growth and profitability Significant untapped potential to be exploited Facilitate access to new opportunities Merck initially approached PRWT through facilities management 20-year track record in legacy businesses gave Merck confidence that PRWT could deliver Unique opportunity for cross-selling Won contract to manage all North American facilities for large pharma company in partnership with Jones Lang Lasalle Combination of USF/PRWT Services/Cherokee capabilities and minority status cannot be matched Provides high volume/high performance business processing

services, including mailroom, lockbox, document & payment

processing, customer service and technical support Provides professional facilities management, maintenance and

infrastructure support services focusing on large-scale,

complex and highly-secure projects

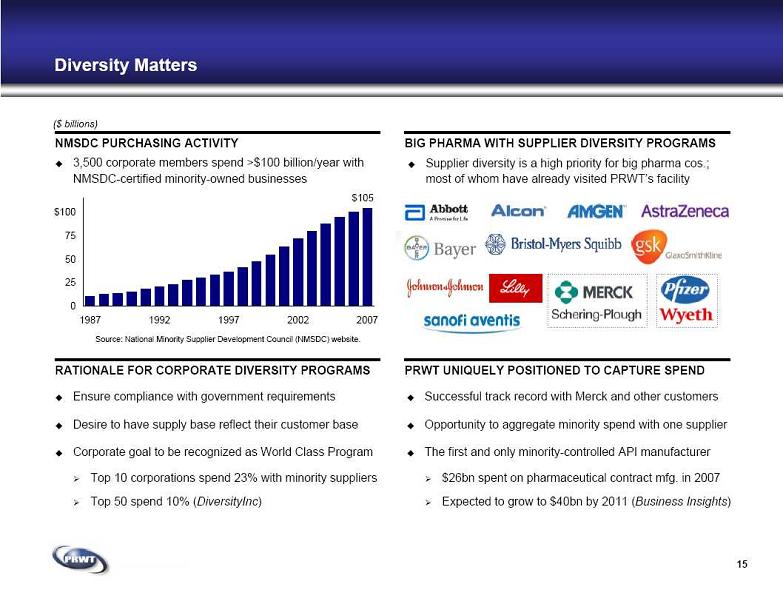

15 Diversity Matters BIG PHARMA WITH SUPPLIER DIVERSITY PROGRAMS Source: National Minority Supplier Development Council (NMSDC) website. ($ billions) PRWT UNIQUELY POSITIONED TO CAPTURE SPEND RATIONALE FOR CORPORATE DIVERSITY PROGRAMS NMSDC PURCHASING ACTIVITY Ensure compliance with government requirements Desire to have supply base reflect their customer base Corporate goal to be recognized as World Class Program Top 10 corporations spend 23% with minority suppliers Top 50 spend 10% (DiversityInc) 3,500 corporate members spend >$100 billion/year with

15 Diversity Matters BIG PHARMA WITH SUPPLIER DIVERSITY PROGRAMS Source: National Minority Supplier Development Council (NMSDC) website. ($ billions) PRWT UNIQUELY POSITIONED TO CAPTURE SPEND RATIONALE FOR CORPORATE DIVERSITY PROGRAMS NMSDC PURCHASING ACTIVITY Ensure compliance with government requirements Desire to have supply base reflect their customer base Corporate goal to be recognized as World Class Program Top 10 corporations spend 23% with minority suppliers Top 50 spend 10% (DiversityInc) 3,500 corporate members spend >$100 billion/year with

NMSDC-certified minority-owned businesses Supplier diversity is a high priority for big pharma cos.;

most of whom have already visited PRWT’s facility Successful track record with Merck and other customers Opportunity to aggregate minority spend with one supplier The first and only minority-controlled API manufacturer $26bn spent on pharmaceutical contract mfg. in 2007 Expected to grow to $40bn by 2011 (Business Insights) $105 0 25 50 75 $100 125 1987 1992 1997 2002 2007

16 Management Willie Johnson, Founder & Chairman 18 years Commissioner - PA Office of Social

16 Management Willie Johnson, Founder & Chairman 18 years Commissioner - PA Office of Social

Services Former Owner & CEO, Fidelity Systems Jerry Johnson, Vice Chairman Chairman, Radnor Trust Holdings Former EVP, Safeguard Scientifics (NYSE:

SFE) Harold Epps, President & CEO President since Nov 2007, CEO since Oct 2008 Former VP, Quadrant-EPP Murvin Lackey, President Cherokee Distribution Former VP, GlaxoSmithKline Formerly held senior positions at AMOCO,

Digital Equipment Corp. Mark Schweiker, President PRWT Services President & CEO, Greater Philadelphia

Chamber of Commerce Former PA Governor & Lt. Governor George Burrell, EVP & General Counsel Former CEO, Innovation Philadelphia Former Secretary of External Affairs for the

City of Philadelphia John McCarey, EVP & CFO Former CFO, Lockheed Martin IMS Former corporate SVP of finance and EVP,

ACS Government Solutions John Elliot, President Cherokee Pharmaceuticals President of Cherokee since 2008 Prior 25-year career at GlaxoSmithKline, most

recently as Senior Vice President James Dobrowolski, President U.S. Facilities Former President, Halifax Technical

Services Skip Lee, EVP Business Development Former SVP, TSS; Former SVP (M&A),

ACS; Former Senior positions at Lockheed

Martin IMS Note: Willie Johnson and Jerry Johnson are not related. Mark Schweiker expected to begin in July 2009.

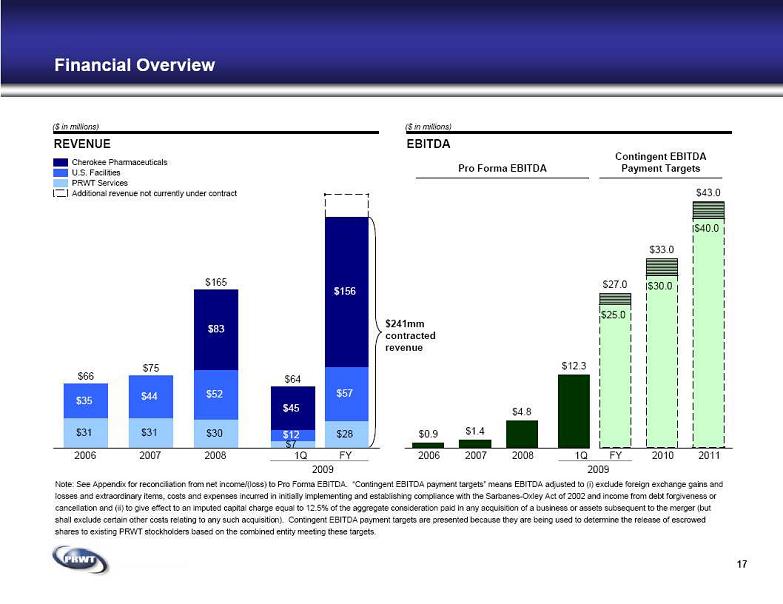

FY Financial Overview REVENUE Cherokee Pharmaceuticals U.S. Facilities PRWT Services EBITDA ($ in millions) ($ in millions) Contingent EBITDA

FY Financial Overview REVENUE Cherokee Pharmaceuticals U.S. Facilities PRWT Services EBITDA ($ in millions) ($ in millions) Contingent EBITDA

Payment Targets Pro Forma EBITDA Note: See Appendix for reconciliation from net income/(loss) to Pro Forma EBITDA. “Contingent EBITDA payment targets” means EBITDA adjusted to (i) exclude foreign exchange gains and

losses and extraordinary items, costs and expenses incurred in initially implementing and establishing compliance with the Sarbanes-Oxley Act of 2002 and income from debt forgiveness or

cancellation and (ii) to give effect to an imputed capital charge equal to 12.5% of the aggregate consideration paid in any acquisition of a business or assets subsequent to the merger (but

shall exclude certain other costs relating to any such acquisition). Contingent EBITDA payment targets are presented because they are being used to determine the release of escrowed

shares to existing PRWT stockholders based on the combined entity meeting these targets. 17 $241mm

contracted

revenue Additional revenue not currently under contract 2009 2006 2007 2008 1Q FY 2006 2007 2008 2010 2011 2009 1Q $31 $31 $30 $28 $35 $44 $52 $57 $156 $83 $66 $75 $165 $25.0 $30.0 $40.0 $43.0 $33.0 $27.0 $4.8 $1.4 $0.9

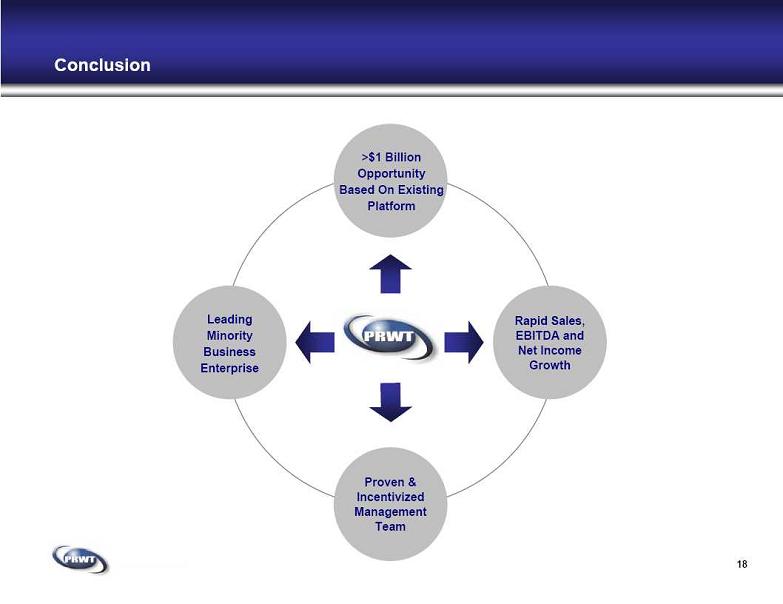

Conclusion 18 >$1 Billion

Conclusion 18 >$1 Billion

Opportunity

Based On Existing

Platform Rapid Sales,

EBITDA and

Net Income

Growth Leading

Minority

Business

Enterprise Proven &

Incentivized

Management

Team

19 Appendix PRWT Services, Inc.

19 Appendix PRWT Services, Inc.

20 PRWT Services: A Leading Provider since 1988 SERVICES OFFERED GROWTH STRATEGY CUSTOMERS Call Center Claims Processing Collection & Processing Customer Service Data entry Document Imaging & Capturing EMS Services Lockbox Mailroom Payment Processing Access additional potential customers Expand into commercial markets with focus on life

20 PRWT Services: A Leading Provider since 1988 SERVICES OFFERED GROWTH STRATEGY CUSTOMERS Call Center Claims Processing Collection & Processing Customer Service Data entry Document Imaging & Capturing EMS Services Lockbox Mailroom Payment Processing Access additional potential customers Expand into commercial markets with focus on life

sciences – participating in first contract with U.S.

Facilities and Jones Lang Lasalle Geographic expansion beyond Philadelphia and other

key cities Broaden product/service offering Acquiring marketing rights to scalable software platform

to move into higher-value applications Increase focus under new leadership Incoming President has commercial market expertise

and significant relationships with key potential

customers Additional sales and business development resources

added Maximize cross-selling opportunities with Cherokee and

U.S. Facilities

21 U.S. Facilities: A Facilities Management Services Provider since 1967 SERVICES OFFERED GROWTH STRATEGY CUSTOMERS Access additional potential customers Expand into commercial markets with focus on life

21 U.S. Facilities: A Facilities Management Services Provider since 1967 SERVICES OFFERED GROWTH STRATEGY CUSTOMERS Access additional potential customers Expand into commercial markets with focus on life

sciences – recently won first contract in partnership with

Jones Lang Lasalle Target additional federal government customers – recently

placed on GSA schedules for facilities management

services Continue geographic expansion beyond core Philadelphia

and Virginia markets Maximize cross-selling opportunities with Cherokee and

PRWT Services Boiler & Chiller Plants Bridges & Navigation

Systems Building Alteration &

Construction Custodial & Related Services Equipment Systems Integrated Pest Management Mailroom & Messenger

Services Physical & Electronic

Security Project Management Trash Removal &

Recycling Warehouse & Logistics

Facilities City of Philadelphia

TRIPLEX Curran-Fromhold/

Riverside

Correctional

Facilities U.S. Army Corps of

Engineers Atlantic

Intracoastal

Waterway Virginia Department

of Transportation Social Security

Administration

Mid-Atlantic Service

Center Thurgood Marshall

Federal Judiciary

Building D.C. Unified

Communication

Center

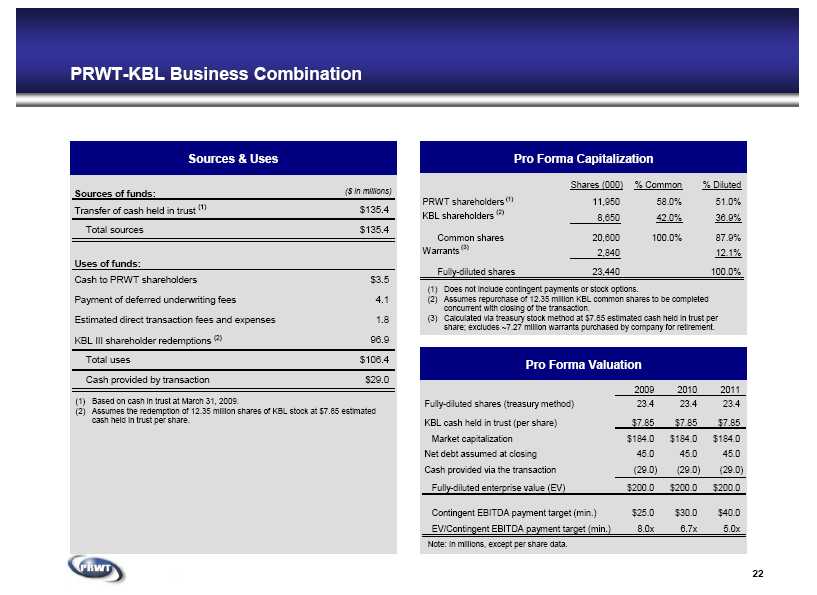

Sources & Uses 22 PRWT-KBL Business Combination Pro Forma Capitalization (1) Based on cash in trust at March 31, 2009. (2) Assumes the redemption of 12.35 million shares of KBL stock at $7.85 estimated

Sources & Uses 22 PRWT-KBL Business Combination Pro Forma Capitalization (1) Based on cash in trust at March 31, 2009. (2) Assumes the redemption of 12.35 million shares of KBL stock at $7.85 estimated

cash held in trust per share. (1) Does not include contingent payments or stock options. (2) Assumes repurchase of 12.35 million KBL common shares to be completed

concurrent with closing of the transaction. (3) Calculated via treasury stock method at $7.85 estimated cash held in trust per

share; excludes ~7.27 million warrants purchased by company for retirement. ($ in millions) Pro Forma Valuation Note: In millions, except per share data. Sources of funds: Transfer of cash held in trust (1) $135.4 Total sources $135.4 Uses of funds: Cash to PRWT shareholders $3.5 Payment of deferred underwriting fees 4.1 Estimated direct transaction fees and expenses 1.8 KBL III shareholder redemptions (2) 96.9 Total uses $106.4 Cash provided by transaction $29.0 Shares (000) % Common % Diluted PRWT shareholders (1) 11,950 58.0% 51.0% KBL shareholders (2) 8,650 42.0% 36.9% Common shares 20,600 100.0% 87.9% Warrants (3) 2,840 12.1% Fully-diluted shares 23,440 100.0% 2009 2010 2011 Fully-diluted shares (treasury method) 23.4 23.4 23.4 KBL cash held in trust (per share) $7.85 $7.85 $7.85 Market capitalization $184.0 $184.0 $184.0 Net debt assumed at closing 45.0 45.0 45.0 Cash provided via the transaction (29.0) (29.0) (29.0) Fully-diluted enterprise value (EV) $200.0 $200.0 $200.0 Contingent EBITDA payment target (min.) $25.0 $30.0 $40.0 EV/Contingent EBITDA payment target (min.) 8.0x 6.7x 5.0x

23 Summary Condensed Consolidated Income Statement (1) (1) Income statements for three months ended March 31, 2009 and March 31, 2008 unaudited. Annual income statements for 2008, 2007 and 2006 audited. (2) We believe that EBITDA is useful to stockholders as a measure of comparative operating performance, as it is less susceptible to variances in actual performance resulting from

23 Summary Condensed Consolidated Income Statement (1) (1) Income statements for three months ended March 31, 2009 and March 31, 2008 unaudited. Annual income statements for 2008, 2007 and 2006 audited. (2) We believe that EBITDA is useful to stockholders as a measure of comparative operating performance, as it is less susceptible to variances in actual performance resulting from

depreciation, amortization and other non-cash charges and more reflective of changes in pricing decisions, cost controls and other factors that affect operating performance. We also

believe EBITDA is useful to stockholders as a way to evaluate our ability to incur and service debt, make capital expenditures and meet working capital requirements. EBITDA is not

intended as a measure of our operating performance, as an alternative to net income (loss) or as an alternative to any other performance measure in conformity with U.S. generally

accepted accounting principles or as an alternative to cash flow provided by operating activities as a measure of liquidity. (3) Pro Forma EBITDA represents EBITDA plus non-recurring items. We have provided Pro Forma EBITDA because PRWT's management believes it provides meaningful information to

investors. Among other things, it may assist investors in evaluating the Company's operating results. We believe this non-GAAP disclosure provides important supplemental information

to management and investors regarding financial and business trends relating to PRWT's financial condition and results of operations. ($ in 000s) Three Month Ended March 31, Year Ended December 31, 2009 2008 2008 2007 2006 Product revenue $45,513 $8,196 $81,568 $75,322 $66,461 Service revenue 18,947 21,031 83,777 - - Total revenue $64,460 $29,227 $165,345 $75,322 $66,461 Cost of product revenue 29,911 9,948 69,312 - - Cost of service revenue 16,973 18,367 71,676 66,108 58,113 Gross profit $17,576 $912 $24,357 $9,214 $8,348 Selling, general and administrative expense 6,455 4,078 34,686 8,339 7,680 Income/(loss) from operations $11,121 ($3,166) ($10,329) $875 $668 Interest expense 1,395 643 4,289 151 299 Other (income)/expense (306) (315) (32) 43 (251) Income/(loss) before taxes and non-controlling interest $10,032 ($3,494) ($14,586) $681 $620 Income tax expense 1,125 162 530 2,031 277 Net income attributable to non-controlling interest 1 124 467 511 225 Net income/(loss) attributable to PRWT Services, Inc. $8,906 ($3,780) ($15,583) ($1,861) $118 Reconciliation of net income (loss) to EBITDA (2) and Pro Forma EBITDA (3) Net income/(loss) attributable to PRWT Services, Inc. $8,906 ($3,780) ($15,583) ($1,861) $118 Depreciation and amortization 833 548 3,094 234 241 Interest expense 1,395 643 4,289 151 299 Income tax expense 1,125 162 530 2,031 277 EBITDA $12,259 ($2,427) ($7,670) $555 $935 Non-recurring items: One time cash bonus - - $4,587 - - One time stock grant and related charges - - 4,176 - - Other one time costs - $0 2,537 $817 - Loss on trading securities ($0) - 1,147 - - Total non-recurring items ($0) $0 $12,447 $817 - Pro Forma EBITDA $12,259 ($2,427) $4,777 $1,372 $935

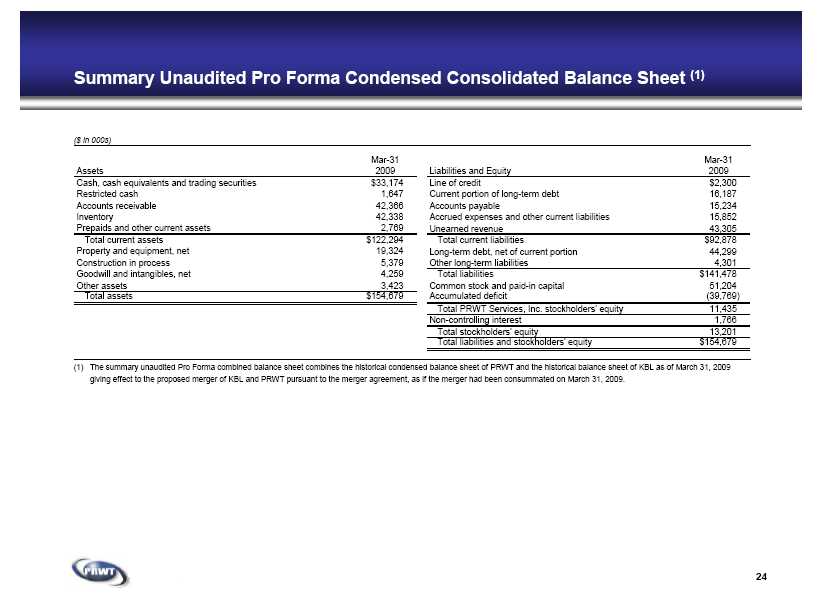

24 Summary Unaudited Pro Forma Condensed Consolidated Balance Sheet (1) ($ in 000s) (1) The summary unaudited Pro Forma combined balance sheet combines the historical condensed balance sheet of PRWT and the historical balance sheet of KBL as of March 31, 2009

24 Summary Unaudited Pro Forma Condensed Consolidated Balance Sheet (1) ($ in 000s) (1) The summary unaudited Pro Forma combined balance sheet combines the historical condensed balance sheet of PRWT and the historical balance sheet of KBL as of March 31, 2009

giving effect to the proposed merger of KBL and PRWT pursuant to the merger agreement, as if the merger had been consummated on March 31, 2009. Assets Mar-31 2009 Cash, cash equivalents and trading securities $33,174 Restricted cash 1,647 Accounts receivable 42,366 Inventory 42,338 Prepaids and other current assets 2,769 Total current assets $122,294 Property and equipment, net 19,324 Construction in process 5,379 Goodwill and intangibles, net 4,259 Other assets 3,423 Total assets $154,679 Liabilities and Equity Mar-31 2009 Line of credit $2,300 Current portion of long-term debt 16,187 Accounts payable 15,234 Accrued expenses and other current liabilities 15,852 Unearned revenue 43,305 Total current liabilities $92,878 Long-term debt, net of current portion 44,299 Other long-term liabilities 4,301 Total liabilities $141,478 Common stock and paid-in capital 51,204 Accumulated deficit (39,769) Total PRWT Services, Inc. stockholders' equity 11,435 Non-controlling interest 1,766 Total stockholders' equity 13,201 Total liabilities and stockholders' equity $154,679