UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR/A

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22027

FundVantage Trust

(Exact name of registrant as specified in charter)

301 Bellevue Parkway

Wilmington, DE 19809

(Address of principal executive offices) (Zip code)

Joel L. Weiss

JW Fund Management LLC

100 Springdale Rd., Suite A3-416

Cherry Hill, NJ 08003

(Name and address of agent for service)

Registrant’s telephone number, including area code: 856-528-3500

Date of fiscal year end: April 30

Date of reporting period: April 30, 2017

EXPLANATORY NOTE: Registrant is filing this amendment to its Form N-CSR for the fiscal quarter ended April 30, 2017 originally filed with the Securities and Exchange Commission on July 7, 2017 (Accession Number 0001193125-17-224297). The purpose of this amendment is to revise the Aggregate Audit Fees under Item 4(a) which was previously incorrect. Except as set forth above, this amendment does not amend, update or change any other items or disclosures found in the original Form N-CSR filing.

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Reports to Shareholders are attached herewith.

BRADESCO LATIN AMERICAN EQUITY FUND

Annual Investment Adviser’s Report

April 30, 2017

(Unaudited)

Dear Shareholder,

Across the globe, the last twelve months will be remembered for the political backlash against globalization.

In the US, Donald Trump’s shock victory in the Presidential election demonstrated the power of an economic platform based on protectionism (in terms of trade and immigration flows) and fiscal expansion (through tax cuts and the expansion of infrastructure investments).

In Europe, the UK voted to leave the European Union, creating uncertainty across the continent about not only the economic implications but also the political consequences of the split. Also within the framework of increasing conservatism, the Italian population rejected a referendum that would have seen some modernization of the Italian political system, the failed vote climaxing in the resignation of Prime Minister, Matteo Renzi.

In the face of increasing global uncertainty and the absence of inflationary pressure, monetary authorities in the Eurozone, UK and Japan decided to broaden accommodative policies. Going against this movement, the US Federal Reserve raised interest rates, due to a tightening labor market and an expected increase of inflation.

In China, the government was active in trying to revive the economy, adding fiscal and monetary stimulus, removing fears of a sharp slowdown in economic activity.

China’s economic activity was strong in the first months of 2017. Nonetheless, we expect economic growth in China to weaken, particularly after mid-2017, as the government tightens policy. Three recent developments support this expectation. First, after monetary and fiscal easing that started at the end of the second half of 2015 and continued for most of 2016, the government initiated a policy shift in late September 2016 by implementing macroprudential measures to cool off the Property sector. Second, the central bank hiked several policy rates in early 2017.

Finally, the government has lowered its GDP growth target, setting a 2017 goal of around 6.5% in 2017, compared with its 6.5%-7.0% target for 2016.

Overall, in 2016, the divergence of monetary policy between the US and other developed countries continued. In summary, even though short-term impacts of politically disruptive dialogues on the real economy were lower than expected, in the medium term they could be detrimental to the world economy.

In Brazil, continuing recession and progress with fiscal reforms creates space for the start of a rate cutting cycle. For 2016, Brazil’s GDP declined by 3.6%, following a contraction of 3.8% in 2015. Political instability, lack of investor and consumer confidence, high-interest rates and deterioration of the labor market form the backdrop of this negative environment. As a direct consequence of weak domestic demand,

1

BRADESCO LATIN AMERICAN EQUITY FUND

Annual Investment Adviser’s Report (Continued)

April 30, 2017

(Unaudited)

inflation fell from 10.7% in 2015 to 6.3% in 2016. Another result of extended economic contraction is fiscal deterioration and its knock-on effect on public debt, requiring a review of public sector spending. In this sense, the approval of the Proposed Amendment to the Constitution (PEC 241), which stipulates a ceiling for the growth of public spending, was a sign that Congress was ready to restore fiscal balance. In addition, the government also sent Congress a proposal for Pension Reform. Falling inflation (current and expected) and improvement of the fiscal perspective in the medium term was fundamental for COPOM to reduce the SELIC rate by 300 basis points as of April 2017 (to 11.25%). In summary, despite the negative repercussions of the economic contraction, the main positive of 2016 was that the government began trying to find solutions to structural problems, such as in the case of public spending.

In Mexico, economic activity has been resilient, in spite of the recent shocks. The deterioration in bilateral relations with its top trading partner (the U.S.) and the sharp rise of inflation (caused by the liberalization of gasoline prices and the MXN sell-off) have weakened Mexico’s growth prospects. Yet Mexico’s GDP growth only slowed down moderately in 2016, to 2.3% (from 2.6% in 2015), and activity began 2017 on solid footing (the monthly GDP proxy rose by 3% year over year in January).

Overall, higher inflation (eating through real wages), tighter monetary and fiscal policies, and the uncertainties surrounding trade relations with the U.S. will likely weigh down internal demand, while exports will likely be a buffer. Importantly, the central bank just announced a whopping dividend of MXN 321.7 billion (1.5% of GDP) stemming from exchange-rate gains on international reserves. This dividend, recorded as government revenues, marks a crucial step toward meeting the government’s fiscal targets in 2017 and hence averting a rating downgrade. Of course, the reduced likelihood of a downgrade is positive for the MXN valuation, which had been appreciating recently as a result of central bank intervention and the more constructive dialogue between the Mexican and U.S. governments.

Peru’s growth prospects have weakened substantially after two unexpected shocks. First, a corruption scandal involving previous administrations and construction firms has paralyzed some of the largest infrastructure projects in the country. Second, a weather shock that began as heavy rainfall in January has mutated into a full-fledged “coastal El Niño”, triggering destructive flooding and landslides. The impact on activity, though likely to be temporary and concentrated in agriculture and fishing in the northern coast, extends to the manufacturing (Lima’s eastern industrial area was severely affected), construction and mining industries. Against this backdrop, the government is expected to implement expansive macro policies. The Ministry of Finance has already announced a fiscal stimulus package (0.8 pp of GDP). The central bank is likely to cut rates, but it will probably wait a bit (at least until it is confident that inflation expectations will remain anchored). Also, the strong increase of the terms of trade (driven by metal prices) will serve as a cushion against these economic headwinds.

2

BRADESCO LATIN AMERICAN EQUITY FUND

Annual Investment Adviser’s Report (Continued)

April 30, 2017

(Unaudited)

Portfolio Review and Outlook

Latam equities had a good run in the last twelve months, posting a strong 17% in USD led by Brazilian (29.7%) and Chilean (15.4%) markets. Sector-wise the main highlights were Materials and Financials.

The performance, however, was uneven. Mexico posted a negative 1.7% performance while Colombia delivered a positive 1.9%.

The inflection point in Brazilian politics together with the turnaround in commodities favored the notable outperformance of the Brazilian equity market. The rally in commodity prices that began in 4Q16 extended into 1Q17.

Fund-wise, we saw a positive gain of 13.63% in the period, but the fund underperformed the benchmark by 2.73%.

The largest detractor to performance relative to the index was the index’s weighting in Banco Bradesco, in which the fund is not permitted to invest because of regulatory constraints. During the period Banco Bradesco was up 29%.

Brazilian banks were particularly benefited by the strong flows into EM and Brazilian markets.

Investors were positive in Brazil mainly due to (1) gradual advances of reforms to allow a more benign trajectory for the country’s debt-to-GDP dynamics and overall competiveness; (2) declining domestic interest rates to boost economic activity in the second half of 2017 onwards, lower discount rates for equities and increase attractiveness of equities versus domestic fixed income; and (3) a benign outlook for a hefty earnings growth range in 2017-2018 given low base, high commodity prices, strong USD-BRL, lower interest rates and operating leverage as Brazil finds its way out of recession.

We prefer Itau over Bradesco.

The second largest detractor was our underweight in America Movil. The stock was up 11.04% in USD. We are underweight on AMX, given increasing competition in Mexico and Colombia, coupled with a tough regulatory environment, which is taking a toll on profitability.

The company’s first quarter of 2017 results surprised on the upside, with revenues up 19% y/y, EBITDA up 6% y/y and Earnings up 13x. Most of the beat came from a 4% weaker MXN, while also counting with improvements in Brazil, Colombia and smaller operations. Mexico came slightly below expectations in revenues and margins.

3

BRADESCO LATIN AMERICAN EQUITY FUND

Annual Investment Adviser’s Report (Continued)

April 30, 2017

(Unaudited)

The performance data quoted represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher. For performance current to the most recent month-end, please call (866) 640-5705.

Brazil posted relevant improvements in mobile growth and margins. Mobile service revenues accelerated sequentially, signaling a more rational pricing behavior and possibly indicating a positive read-across for Vivo/Tim. Margins improved on cost reductions associated with certain technical areas.

Still on the negative side, our overweight in Concentradora Fibra Danhos, an experienced real estate developer, contributed negatively to performance as the stock dropped 18% in the period.

Adverse performance could be in part explained by the interest rate cycle but also by the impact that Trump initiatives could have on Mexico and especially on industrial real estate assets.

On the positive side, our overweight in Itau worked well and was the most important contributor to performance.

We are positive in Itau as we believe Itau has been the most proactive Brazilian bank in adjusting its business model to the more challenging business environment in recent years (high indebtedness levels, deterioration in growth conditions, competition from government-controlled banks) by reducing costs, making opportunistic acquisitions, growing fee businesses, improving the digital channel and de-risking its loan portfolio.

Another important contributor to performance was our overweight on Cia Energetica de Sao Paulo (“CESP”). The stock outperformed on the back of government talks resuming studies for the potential privatization of CESP. According to the management team, political developments, the end of the power crisis and the normalization of micro conditions removed uncertainties that dented the possibilities of privatization in the past few years.

Latam equity fundamentals have begun to see some improvement in the second half of the year. Recovery in commodity prices, improving default trends, and stronger foreign currency in the second half of 2016 have started to materialize in better rating trends, while continued capex reductions, liability management exercises, and conservative corporate behavior (with some exceptions) have helped alleviate the pressure of declining earnings growth.

However, while many of these trends should carry on, the uncertainty about the new US administration’s policies has increased the risks for the trajectory of the region.

In particular, the outlook for Latin America has turned less clear as countries such as Mexico are in the direct firing line of US trade protectionism and the risks around the magnitude of the expected economic recovery of the region are pointing to the downside. Additionally, corruption-related headlines involving Temer’s government in Brazil are reminders of the country’s still fragile recovery prospects.

4

BRADESCO LATIN AMERICAN EQUITY FUND

Annual Investment Adviser’s Report (Concluded)

April 30, 2017

(Unaudited)

As a result, while growth in Latin America is expected to pick up in 2017, Bradesco Asset Management forecasts are now more tepid than a few months back.

Also, despite offering compelling investment opportunities within EM peers, Latin America is still vulnerable to global factors.

Natalia Kerkis – Portfolio Manager

May 22, 2017

This letter is intended to assist shareholders in understanding how the Fund performed during the fiscal year ended April 30, 2017 and reflects the views of the investment adviser at the time of this writing. Of course, these views may change and do not guarantee the future performance of the Fund or the markets.

Portfolio composition is subject to change. The current and future portfolio holdings of the Fund are subject to investment risks. The investment return and principle value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

5

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Annual Investment Adviser’s Report

April 30, 2017

(Unaudited)

Dear Fund Shareholder,

Across the globe, the last twelve months will be remembered for the political backlash against globalization.

In the US, Donald Trump’s shock victory in the Presidential election demonstrated the power of an economic platform based on protectionism (in terms of trade and immigration flows) and fiscal expansion (through tax cuts and the expansion of infrastructure investments).

In Europe, the UK voted to leave the European Union, creating uncertainty across the continent about not only the economic implications but also the political consequences of the split. Also within the framework of increasing conservatism, the Italian population rejected a referendum that would have seen some modernization of the Italian political system, the failed vote climaxing in the resignation of Prime Minister, Matteo Renzi.

In the face of increasing global uncertainty and the absence of inflationary pressure, monetary authorities in the Eurozone, UK and Japan decided to broaden accommodative policies. Going against this movement, the US Federal Reserve raised interest rates, due to a tightening labor market and an expected increase of inflation.

In China, the government was active in trying to revive the economy, adding fiscal and monetary stimulus, removing fears of a sharp slowdown in economic activity.

China’s economic activity was strong in the first months of 2017. Nonetheless, we expect economic growth in China to weaken, particularly after mid-2017, as the government tightens policy. Three recent developments support this expectation. First, after monetary and fiscal easing that started at the end of the second half of 2015 and continued for most of 2016, the government initiated a policy shift in late September 2016 by implementing macroprudential measures to cool off the Property sector. Second, the central bank hiked several policy rates in early 2017.

Finally, the government has lowered its GDP growth target, setting a 2017 goal of around 6.5% in 2017, compared with its 6.5%-7.0% target for 2016.

Overall, in 2016, the divergence of monetary policy between the US and other developed countries continued. In summary, even though short-term impacts of politically disruptive dialogues on the real economy were lower than expected, in the medium term they could be detrimental to the world economy.

In Brazil, continuing recession and progress with fiscal reforms creates space for the start of a rate cutting cycle. For 2016, Brazil’s GDP declined by 3.6%, following a contraction of 3.8% in 2015. Political instability, lack of investor and consumer confidence, high-interest rates and deterioration of the labor market form the backdrop of this negative environment. As a direct consequence of weak domestic demand,

6

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Annual Investment Adviser’s Report (Continued)

April 30, 2017

(Unaudited)

inflation fell from 10.7% in 2015 to 6.3% in 2016. Another result of extended economic contraction is fiscal deterioration and its knock-on effect on public debt, requiring a review of public sector spending. In this sense, the approval of the Proposed Amendment to the Constitution (PEC 241), which stipulates a ceiling for the growth of public spending, was a sign that Congress was ready to restore fiscal balance. In addition, the government also sent Congress a proposal for Pension Reform. Falling inflation (current and expected) and improvement of the fiscal perspective in the medium term was fundamental for The Monetary Policy Committee of the Brazilian Central Bank (“COPOM”) to reduce the SELIC rate (the Brazilian Central Bank’s overnight rate) by 300 basis points as of April 2017 (to 11.25%). In summary, despite the negative repercussions of the economic contraction, the main positive of 2016 was that the government began trying to find solutions to structural problems, such as in the case of public spending.

In Mexico, economic activity has been resilient, in spite of the recent shocks. The deterioration in bilateral relations with its top trading partner (the U.S.) and the sharp rise of inflation (caused by the liberalization of gasoline prices and the Mexican peso (“MEX”) sell-off) have weakened Mexico’s growth prospects. Yet Mexico’s GDP growth only slowed down moderately in 2016, to 2.3% (from 2.6% in 2015), and activity began 2017 on solid footing (the monthly GDP proxy rose by 3% year over year in January).

Overall, higher inflation (eating through real wages), tighter monetary and fiscal policies, and the uncertainties surrounding trade relations with the U.S. will likely weigh down internal demand, while exports will likely be a buffer. Importantly, the central bank just announced a whopping dividend of MXN 321.7 billion (1.5% of GDP) stemming from exchange-rate gains on international reserves. This dividend, recorded as government revenues, marks a crucial step toward meeting the government’s fiscal targets in 2017 and hence averting a rating downgrade. Of course, the reduced likelihood of a downgrade is positive for the MXN valuation, which had been appreciating recently as a result of central bank intervention and the more constructive dialogue between the Mexican and U.S. governments.

Peru’s growth prospects have weakened substantially after two unexpected shocks. First, a corruption scandal involving previous administrations and construction firms has paralyzed some of the largest infrastructure projects in the country. Second, a weather shock that began as heavy rainfall in January has mutated into a full-fledged “coastal El Niño”, triggering destructive flooding and landslides. The impact on activity, though likely to be temporary and concentrated in agriculture and fishing in the northern coast, extends to the manufacturing (Lima’s eastern industrial area was severely affected), construction and mining industries. Against this backdrop, the government is expected to implement expansive macro policies. The Ministry of Finance has already announced a fiscal stimulus package (0.8 pp of GDP). The central bank is likely to cut rates, but it will probably wait a bit (at least until it is confident that inflation expectations will remain anchored). Also, the strong increase of the terms of trade (driven by metal prices) will serve as a cushion against these economic headwinds.

7

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Annual Investment Adviser’s Report (Continued)

April 30, 2017

(Unaudited)

Portfolio Review and Outlook

From May 1, 2016 to April 30, 2017 the Bradesco Latin American Hard Currency Bond Fund (the “Fund”) Institutional Class shares returned 9.82%. The CS (Credit Suisse) Latin America Corporate Index 0-6Y A/B Buckets, the Fund’s benchmark, performed 10.64% during the same period.

Brazil has been the best performing country in the period. The resilience recently shown by the Brazilian corporate bonds has been surprising investors. Following the strong performance delivered until the broad market correction in November (US elections), spreads across the class kept narrowing over the following months amid a tough sequence of domestic and international events.

Brazil benefited from positive political events. In particular, Brazil’s outperformance was triggered notably by the impeachment of Dilma Rousseff and the change in government that followed. Just to have an idea of the change in the mood regarding Brazilian assets, 5Y Brazilian CDS was at the 340 level in April 2017 and moved down to 218 in April 2017. Strong spread compression in Brazilian curve also contributed positively to performance as the country represents around 75% of the fund.

Our strategy to be invested in government related companies after the impeachment in Brazil proved to be right as we were able to capture the compression of the spreads and outperformance of those companies.

All sectors delivered solid performances, but Oil & Gas (with Petrobras being the main highlight due to the change in management), Metals & Mining (mainly due to higher commodity prices and CSN, Vale, Gerdau) and Financials (BANBRA perps, Caixa’s curve) were the best performing sectors in the period (based on returns and attribution).

Looking at individual performance, it is not surprising that most of the outperformers were Brazilian credits. In particular, the long-end of Petrobras, Vale, Gerdau and Banco do Brazil curves are among the best performing credits.

Latam corporate fundamentals have begun to see some improvement in the second half of the year. Recovery in commodity prices, improving default trends, and stronger FX in 2H16 have started to materialize in better credit rating trends, while continued capex reductions, liability management exercises, and conservative corporate behavior (with some exceptions) have helped alleviate the pressure of declining earnings growth.

However, while many of these trends should carry on, the uncertainty about the new US administration’s policies has increased the risks for the trajectory of the region.

8

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Annual Investment Adviser’s Report (Concluded)

April 30, 2017

(Unaudited)

In particular, the outlook for Latin America has turned less clear as countries such as Mexico are in direct firing line of US trade protectionism and the risks around the magnitude of the expected economic recovery of the region are pointing to the downside. Additionally, corruption-related headlines involving Temer’s government in Brazil are reminders of the country’s still fragile recovery prospects.

As a result, while growth in Latin America is expected to pick up in 2017, Bradesco Asset Management forecasts are now more tepid than a few months back.

Also, despite offering the highest yields among Emerging Market peers, Latin America is more vulnerable to global factors.

However, the region is more sensitive to interest rate fluctuations given its longer average duration and the main base of bondholders is dominated by foreign investors rather than locals, which makes it more vulnerable to fund outflows.

Clayton Rodrigues – Portfolio Manager

May 22, 2017

This letter is intended to assist shareholders in understanding how the Fund performed during the fiscal year ended April 30, 2017 and reflects the views of the investment adviser at the time of this writing. Of course, these views may change and do not guarantee the future performance of the Fund or the markets.

Portfolio composition is subject to change. The current and future portfolio holdings of the Fund are subject to investment risks. The investment return and principle value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

9

BRADESCO LATIN AMERICAN EQUITY FUND

Annual Report

Performance Data

April 30, 2017

(Unaudited)

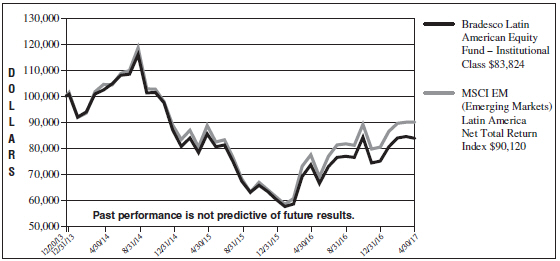

Comparison of Change in Value of $100,000 (investment minimum) Investment in Bradesco Latin American Equity Fund’s Institutional Class vs. MSCI EM (Emerging Markets) Latin America Net Total Return Index.

Average Annual Total Returns for the Periods Ended April 30, 2017 | ||||||||||||

| 1 Year | 3 Year | Since Inception | ||||||||||

Institutional Class | 13.63 | % | -6.49 | % | -5.15%* | |||||||

MSCI EM (Emerging Markets) Latin America Net | ||||||||||||

Total Return Index | 16.36 | % | -4.83 | % | -3.06%** | |||||||

| * | Institutional Class shares of the Bradesco Latin American Equity Fund (the “Fund”) commenced operations on December 20, 2013. |

| ** | Benchmark performance is from the commencement date of Institutional Class shares of the Fund (December 20, 2013) and is not the commencement date of the benchmark itself. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained by calling (866) 640-5705.

The Fund’s total gross and net operating expense ratio, as stated in the current prospectus dated September 1, 2016, is 2.99% and 1.76%, respectively, of the Fund’s average daily net assets for Institutional Class shares, which may differ from the actual expenses incurred by the Fund for the period covered by this report. A 2.00% redemption fee applies to shares redeemed within 30 days of purchase. The redemption fee is not reflected in the returns shown above. BRAM US LLC (“BRAM US” or the “Adviser”) has contractually agreed to waive or otherwise reduce its annual compensation received from the Fund to the extent necessary to ensure that the Fund’s “Total Annual Fund Operating Expenses”, excluding taxes, any class specific fees and expenses (such as Rule 12b-1 distribution fees, shareholder service fees or transfer agency fees) “Acquired Fund” fees and expenses, interest, extraordinary items and brokerage

10

BRADESCO LATIN AMERICAN EQUITY FUND

Annual Report

Performance Data

April 30, 2017

(Unaudited)

commissions, do not exceed 1.75% of average daily net assets of the Fund (the “Expense Limitation”). The Expense Limitation will remain in place until August 31, 2017, unless the Board of Trustees of the FundVantage Trust (the “Trust”) approves its earlier termination. The Adviser may recoup any expenses or fees it has reimbursed within a three-year period from the year in which the Adviser reduced its compensation and/or assumed expenses of the Fund. The Adviser is permitted to seek reimbursement from the Fund, subject to certain limitations, for fees it waived and Fund expenses it paid to the extent the total annual fund operating expenses do not exceed the limits described above or any lesser limits in effect as the time of reimbursement. No recoupment will occur unless the Fund’s expenses are below the Expense Limitation.

The Fund intends to evaluate performance as compared to that of the MSCI EM (Emerging Markets) Latin America Net Total Return Index (net of foreign withholding taxes) (the “Index”). The Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of emerging markets in Latin America. The MSCI EM (Emerging Markets) Latin America Net Total Return Index consists of the following 5 emerging market country indexes: Brazil, Chile, Colombia, Mexico, and Peru. An index is unmanaged and it is not possible to invest in an index.

The Fund is non-diversified which means it may be invested in a limited number of issuers geographically particularly Latin America and more susceptible to any economic, political and regulatory events. The Fund invests primarily in markets of emerging countries which are riskier and may be considered speculative. In addition, many emerging securities markets have far lower trading volumes, currency devaluation risk and less liquidity than developed markets. The Fund may invest in derivatives (futures, options, and swaps), depositary receipts and small to mid-capitalization companies all of which may cause greater volatility and less liquidity. Funds that invest in derivatives are subject to the risks of the underlying securities which may be more sensitive to changes in market conditions and may amplify risks. The use of certain derivatives may also have a leveraging effect which may increase the volatility of the Fund and reduce its returns.

Foreign securities are subject to political, social, or economic risks including instability in the country of the issuer of a security, variation in international trade patterns, the possibility of the imposition of exchange controls, expropriation, confiscatory taxation, limits on movement to currency or other assets and nationalization of assets.

11

BRADESCO LATIN AMERICAN EQUITY FUND

Annual Report

Performance Data

April 30, 2017

(Unaudited)

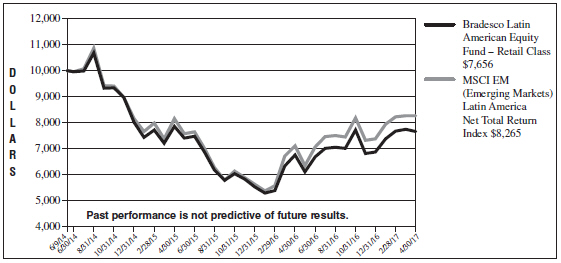

Comparison of Change in Value of $10,000 Investment in Bradesco Latin American Equity Fund’s Retail Class vs. MSCI EM (Emerging Markets) Latin America Net Total Return Index.

Average Annual Total Returns for the Periods Ended April 30, 2017 | ||||||||

| 1 Year | Since Inception | |||||||

Retail Class | 13.43 | % | -8.83%* | |||||

MSCI EM (Emerging Markets) Latin America Net | ||||||||

Total Return Index | 16.36 | % | -6.46%** | |||||

| * | Retail Class shares of the Bradesco Latin American Equity Fund (the “Fund”) commenced operations on June 9, 2014. |

| ** | Benchmark performance is from the commencement date of Retail Class shares of the Fund (June 9, 2014) only and is not the commencement date of the benchmark itself. |

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained by calling (866) 640-5705.

The Fund’s total gross and net operating expense ratio, as stated in the current prospectus dated September 1, 2016, is 3.24% and 2.01%, respectively, of the Fund’s average daily net assets for Retail Class shares, which may differ from the actual expenses incurred by the Fund for the period covered by this report. A 2.00% redemption fee applies to shares redeemed within 30 days of purchase. The redemption fee is not reflected in the returns shown above. BRAM US LLC (“BRAM US” or the “Adviser”) has contractually agreed to waive or otherwise reduce its annual compensation received from the Fund to the extent necessary to ensure that the Fund’s “Total Annual Fund Operating Expenses”, excluding taxes, any class specific fees and expenses (such as Rule 12b-1 distribution fees, shareholder service fees or transfer agency fees) “Acquired Fund” fees and expenses, interest, extraordinary items and brokerage

12

BRADESCO LATIN AMERICAN EQUITY FUND

Annual Report

Performance Data (Concluded)

April 30, 2017

(Unaudited)

commissions, do not exceed 1.75% of average daily net assets of the Fund (the “Expense Limitation”). The Expense Limitation will remain in place until August 31, 2017, unless the Board of Trustees of the FundVantage Trust (the “Trust”) approves its earlier termination. The Adviser may recoup any expenses or fees it has reimbursed within a three-year period from the year in which the Adviser reduced its compensation and/or assumed expenses of the Fund. The Adviser is permitted to seek reimbursement from the Fund, subject to certain limitations, for fees it waived and Fund expenses it paid to the extent the total annual fund operating expenses do not exceed the limits described above or any lesser limits in effect as the time of reimbursement. No recoupment will occur unless the Fund’s expenses are below the Expense Limitation.

The Fund intends to evaluate performance as compared to that of the MSCI EM (Emerging Markets) Latin America Net Total Return Index (net of foreign withholding taxes) (the “Index”). The Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of emerging markets in Latin America. The MSCI EM (Emerging Markets) Latin America Net Total Return Index consists of the following 5 emerging market country indexes: Brazil, Chile, Colombia, Mexico, and Peru. An index is unmanaged and it is not possible to invest in an index.

The Fund is non-diversified which means it may be invested in a limited number of issuers geographically particularly Latin America and more susceptible to any economic, political and regulatory events. The Fund invests primarily in markets of emerging countries which are riskier and may be considered speculative. In addition, many emerging securities markets have far lower trading volumes, currency devaluation risk and less liquidity than developed markets. The Fund may invest in derivatives (futures, options, and swaps), depositary receipts and small to mid-capitalization companies all of which may cause greater volatility and less liquidity. Funds that invest in derivatives are subject to the risks of the underlying securities which may be more sensitive to changes in market conditions and may amplify risks. The use of certain derivatives may also have a leveraging effect which may increase the volatility of the Fund and reduce its returns.

Foreign securities are subject to political, social, or economic risks including instability in the country of the issuer of a security, variation in international trade patterns, the possibility of the imposition of exchange controls, expropriation, confiscatory taxation, limits on movement to currency or other assets and nationalization of assets.

13

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Annual Report

Performance Data

April 30, 2017

(Unaudited)

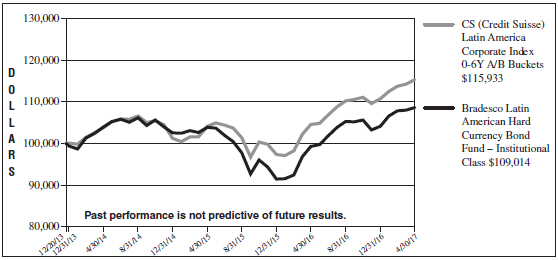

Comparison of Change in Value of $100,000 (investment minimum) Investment in Bradesco Latin American Hard Currency Bond Fund’s Institutional Class vs. CS (Credit Suisse) Latin America Corporate Index 0-6Y A/B Buckets.

Average Annual Total Returns for the Periods Ended April 30, 2017 | ||||||||||||

| 1 Year | 3 Year | Since Inception | ||||||||||

Institutional Class | 9.82 | % | 1.55 | % | 2.60%* | |||||||

CS (Credit Suisse) Latin America Corporate Index 0-6Y A/B Buckets | 10.64 | % | 3.71 | % | 4.50%** | |||||||

| * | Institutional Class shares of the Bradesco Latin American Hard Currency Bond Fund (the “Fund”) commenced operations on December 20, 2013. |

| ** | Benchmark performance is from the commencement date of Institutional Class shares of the Fund (December 20, 2013 and is not the commencement date of the benchmark itself. |

The performance data includes adjustments in accordance with accounting principles generally accepted in the United States of America and, consequently, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions.

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained by calling (866) 640-5705.

The Fund’s total gross and net operating expense ratio, as stated in the current prospectus dated September 1, 2016, is 2.42% and 1.51%, respectively, of the Fund’s average daily net assets for Institutional Class shares, which may differ from the actual expenses incurred by the Fund for the period covered by this report. A 2.00% redemption fee applies to shares redeemed within 30 days of purchase. The redemption fee is not reflected in the returns shown above. BRAM US LLC (“BRAM US” or the “Adviser”) has contractually agreed to waive or otherwise reduce its annual

14

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Annual Report

Performance Data

April 30, 2017

(Unaudited)

compensation received from the Fund to the extent necessary to ensure that the Fund’s “Total Annual Fund Operating Expenses”, excluding taxes, any class-specific fees and expenses (such as Rule 12b-1 distribution fees, shareholder service fees or transfer agency fees), “Acquired Fund” fees and expenses, interest, extraordinary items and brokerage commissions, do not exceed 1.50% of average daily net assets of the Fund (the “Expense Limitation”). The Expense Limitation will remain in place until August 31, 2017, unless the Board of Trustees of the FundVantage Trust (the “Trust”) approves its earlier termination. The Adviser may recoup any expenses or fees it has reimbursed within a three-year period from the year in which the Adviser reduced its compensation and/or assumed expenses of the Fund. The Adviser is permitted to seek reimbursement from the Fund, subject to certain limitations, for fees it waived and Fund expenses it paid to the extent the total annual fund operating expenses do not exceed the limits described above or any lesser limits in effect as the time of reimbursement. No recoupment will occur unless the Fund’s expenses are below the Expense Limitation amount. Total returns would be lower had such fees and/or expenses not been waived and/or reimbursed.

The Fund intends to evaluate performance as compared to that of the CS (Credit Suisse) Latin America Corporate Index 0-6Y A/B Buckets (the “Index”). The Index is a subset index of the Credit Suisse-Latin America Corporate Index (“CS-LACI”). It contains bonds with less than 6 years to maturity and rated “B-” or higher (composite of Moody’s, S&P, and Fitch ratings as determined by Credit Suisse’s methodology). CS-LACI is a diversified basket of liquid, tradable Latin American corporate bond issues that are denominated in US dollars. This index provides a region-specific benchmark that represents characteristics, pricing, and total return performance of different asset classes within the Latin American corporate bond universe. This index is divided into three different categories, including supranational, quasi-sovereign, and corporate bonds and can be broken down by country of issuance. An index is unmanaged and it is not possible to invest in an index.

The Fund is non-diversified which means it may be invested in a limited number of issuers particularly in Latin America and more susceptible to any economic, political and regulatory events. The Fund invests primarily in markets of emerging countries which are riskier and may be considered speculative as well as derivatives which may amplify volatility. In addition, many emerging securities markets have far lower trading volumes, currency devaluation risk and less liquidity than developed markets. The Fund invests in below investment grade bonds (known as “junk bonds”) and may be less liquid and subject to greater volatility. The Fund is subject to the same risks as the underlying bonds in the portfolio such as credit, prepayment, sovereign debt, call and interest rate risk. As interest rates rise the value of bond prices will decline.

Foreign securities are subject to political, social, or economic risks including instability in the country of the issuer of a security, variation in international trade patterns, the possibility of the imposition of exchange controls, expropriation, confiscatory taxation, limits on movement to currency or other assets and nationalization of assets.

15

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Annual Report

Performance Data

April 30, 2017

(Unaudited)

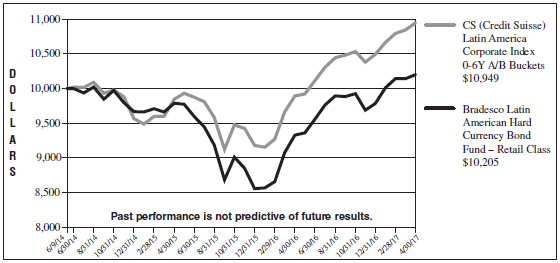

Comparison of Change in Value of $10,000 Investment in Bradesco Latin American Hard Currency Bond Fund’s Retail Class vs. CS (Credit Suisse) Latin America Corporate Index 0-6Y A/B Buckets.

Average Annual Total Returns for the Period Ended April 30, 2017 |

| |||||||||

| 1 Year | Since Inception | |||||||||

Retail Class | 9.38 | % | 0.71%* | |||||||

CS (Credit Suisse) Latin America Corporate Index 0-6Y A/B Buckets | 10.64 | % | 3.18%** | |||||||

| * | Retail Class shares of the Bradesco Latin American Hard Currency Bond Fund (the “Fund”) commenced operations on June 9, 2014. |

| ** | Benchmark performance is from the commencement date of Retail Class shares of the Fund (June 9, 2014) only and is not the commencement date of the benchmark itself. |

The performance data includes adjustments in accordance with accounting principles generally accepted in the United States of America and, consequently, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions.

The performance data quoted represents past performance and does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Current performance may be lower or higher. Performance data current to the most recent month-end may be obtained by calling (866) 640-5705.

The Fund’s total gross and net operating expense ratio, as stated in the current prospectus dated September 1, 2016, is 2.67% and 1.76%, respectively, of the Fund’s average daily net assets for Retail Class shares, which may differ from the actual expenses incurred by the Fund for the period covered by this report. A 2.00% redemption fee applies to shares redeemed within 30 days of purchase. The redemption fee is not reflected in the returns shown above. BRAM US LLC (“BRAM US” or the “Adviser”) has contractually agreed to waive or otherwise reduce its annual

16

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Annual Report

Performance Data (Concluded)

April 30, 2017

(Unaudited)

compensation received from the Fund to the extent necessary to ensure that the Fund’s “Total Annual Fund Operating Expenses”, excluding taxes, any class-specific fees and expenses (such as Rule 12b-1 distribution fees, shareholder service fees or transfer agency fees), “Acquired Fund” fees and expenses, interest, extraordinary items and brokerage commissions, do not exceed 1.50% of average daily net assets of the Fund (the “Expense Limitation”). The Expense Limitation will remain in place until August 31, 2017, unless the Board of Trustees of the FundVantage Trust (the “Trust”) approves its earlier termination. The Adviser may recoup any expenses or fees it has reimbursed within a three-year period from the year in which the Adviser reduced its compensation and/or assumed expenses of the Fund. The Adviser is permitted to seek reimbursement from the Fund, subject to certain limitations, for fees it waived and Fund expenses it paid to the extent the total annual fund operating expenses do not exceed the limits described above or any lesser limits in effect as the time of reimbursement. No recoupment will occur unless the Fund’s expenses are below the Expense Limitation amount. Total returns would be lower had such fees and/or expenses not been waived and/or reimbursed.

The Fund intends to evaluate performance as compared to that of the CS (Credit Suisse) Latin America Corporate Index 0-6Y A/B Buckets (the “Index”). The Index is a subset index of the Credit Suisse Latin America Corporate Index (“CS-LACI”). It contains bonds with less than 6 years to maturity and rated “B-” or higher (composite of Moody’s, S&P, and Fitch ratings as determined by Credit Suisse’s methodology). CS-LACI is a diversified basket of liquid, tradable Latin American corporate bond issues that are denominated in US dollars. This index provides a region-specific benchmark that represents characteristics, pricing, and total return performance of different asset classes within the Latin American corporate bond universe. This index is divided into three different categories, including supranational, quasi-sovereign, and corporate bonds and can be broken down by country of issuance. An index is unmanaged and it is not possible to invest in an index.

The Fund is non-diversified which means it may be invested in a limited number of issuers particularly in Latin America and more susceptible to any economic, political and regulatory events. The Fund invests primarily in markets of emerging countries which are riskier and may be considered speculative as well as derivatives which may amplify volatility. In addition, many emerging securities markets have far lower trading volumes, currency devaluation risk and less liquidity than developed markets. The Fund invests in below investment grade bonds (known as “junk bonds”) and may be less liquid and subject to greater volatility. The Fund is subject to the same risks as the underlying bonds in the portfolio such as credit, prepayment, sovereign debt, call and interest rate risk. As interest rates rise the value of bond prices will decline.

Foreign securities are subject to political, social, or economic risks including instability in the country of the issuer of a security, variation in international trade patterns, the possibility of the imposition of exchange controls, expropriation, confiscatory taxation, limits on movement to currency or other assets and nationalization of assets.

17

BRADESCO FUNDS

Fund Expense Disclosure

April 30, 2017

(Unaudited)

As a shareholder of the Bradesco Funds (each a “Fund” and together, the “Funds”), you incur two types of costs: (1) transaction costs, including redemption fees; and (2) ongoing costs, including management fees and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

This example is based on an investment of $1,000 invested from November 1, 2016, through April 30, 2017 and held for the entire period.

Actual Expenses

The first line for each Fund in the accompanying tables provide information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each Fund in the accompanying tables provide information about hypothetical account values and hypothetical expenses based on such Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund(s) and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the accompanying tables are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the second line of the accompanying tables are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

18

BRADESCO FUNDS

Fund Expense Disclosure (Concluded)

April 30, 2017

(Unaudited)

| Bradesco Latin American Equity Fund | |||||||||||||||

Beginning Account Value |

Ending Account Value |

Expenses Paid | |||||||||||||

Institutional Class | |||||||||||||||

Actual | $ | 1,000.00 | $ | 993.30 | $ | 8.65 | |||||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,016.12 | 8.75 | ||||||||||||

Retail Class | |||||||||||||||

Actual | $ | 1,000.00 | $ | 992.20 | $ | 9.88 | |||||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,014.88 | 9.99 | ||||||||||||

| Bradesco Latin American Hard Currency Bond Fund | |||||||||||||||

Beginning Account Value |

Ending Account Value |

Expenses Paid | |||||||||||||

Institutional Class | |||||||||||||||

Actual | $ | 1,000.00 | $ | 1,029.30 | $ | 7.55 | |||||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,017.36 | 7.50 | ||||||||||||

Retail Class | |||||||||||||||

Actual | $ | 1,000.00 | $ | 1,027.90 | $ | 8.80 | |||||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,016.12 | 8.75 | ||||||||||||

| * | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2017 of 1.75% and 2.00% for the Institutional Class and the Retail Class shares, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Fund’s ending account values on the first line in the table are based on the actual six-month total returns for the Fund of (0.67)% and (0.78)% for the Institutional Class and the Retail Class shares, respectively. |

| ** | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2017 of 1.50% and 1.75% for the Institutional Class and the Retail Class shares, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Fund’s ending account values on the first line in the table are based on the actual six-month total returns for the Fund of 2.93% and 2.79% for the Institutional Class and the Retail Class shares, respectively. |

19

BRADESCO LATIN AMERICAN EQUITY FUND

Portfolio Holdings Summary Table

April 30, 2017

(Unaudited)

The following table presents a summary by sector of the portfolio holdings of the Fund:

| % of Net Assets | Value | |||||||||

COMMON STOCK: | ||||||||||

Banks | 17.0 | % | $ | 2,648,238 | ||||||

Food | 8.5 | 1,335,546 | ||||||||

REITS | 7.0 | 1,090,767 | ||||||||

Retailing | 6.5 | 1,021,704 | ||||||||

Oil & Gas | 6.3 | 981,306 | ||||||||

Building Materials | 6.1 | 951,893 | ||||||||

Telecommunications | 6.1 | 948,297 | ||||||||

Diversified Financial Services | 5.0 | 781,831 | ||||||||

Pharmaceuticals | 3.6 | 557,833 | ||||||||

Commercial Services | 2.9 | 454,749 | ||||||||

Airlines | 2.8 | 443,600 | ||||||||

Electric | 2.7 | 428,195 | ||||||||

Insurance | 1.9 | 291,987 | ||||||||

Software | 1.4 | 220,798 | ||||||||

Water Utilities | 1.1 | 170,978 | ||||||||

Transportation Infrastructure | 0.9 | 144,716 | ||||||||

Auto Parts & Equipment | 0.9 | 138,475 | ||||||||

Preferred Stocks | 15.9 | 2,478,150 | ||||||||

Registered Investment Company | 4.6 | 713,647 | ||||||||

Liabilities in Excess of Other Assets | (1.2 | ) | (186,304 | ) | ||||||

|

|

|

| |||||||

NET ASSETS | 100.0 | % | $ | 15,616,406 | ||||||

|

|

|

| |||||||

Portfolio holdings are subject to change at any time.

The accompanying notes are an integral part of the financial statements.

20

BRADESCO LATIN AMERICAN EQUITY FUND

Portfolio of Investments

April 30, 2017

| Number of Shares | Value | |||||||

COMMON STOCKS — 80.7% |

| |||||||

Argentina — 0.5% | ||||||||

Adecoagro SA* | 6,500 | $ | 72,085 | |||||

|

| |||||||

Brazil — 48.0% | ||||||||

Alupar Investimento SA | 33,500 | 198,211 | ||||||

Ambev SA, ADR | 58,200 | 333,486 | ||||||

B2W Cia Digital* | 6,618 | 27,418 | ||||||

Banco do Brasil SA | 28,100 | 290,203 | ||||||

BB Seguridade Participacoes SA | 31,100 | 291,987 | ||||||

BM&FBovespa SA - Bolsa de Valores Mercadorias e Futuros | 108,700 | 648,286 | ||||||

BR Malls Participacoes SA | 43,800 | 195,124 | ||||||

CCR SA | 11,900 | 66,135 | ||||||

Cia de Saneamento de Minas Gerais-COPASA | 15,100 | 170,978 | ||||||

Cosan SA Industria e Comercio | 13,700 | 159,140 | ||||||

EcoRodovias Infraestrutura e Logistica SA | 26,534 | 78,581 | ||||||

Energisa SA | 32,300 | 229,984 | ||||||

Ez Tec Empreendimentos e Participacoes SA | 11,900 | 76,183 | ||||||

Hypermarcas SA | 59,000 | 557,833 | ||||||

International Meal Co. Alimentacao SA* | 36,000 | 68,846 | ||||||

Itau Unibanco Holding SA, SP ADR | 97,290 | 1,196,667 | ||||||

Itausa - Investimentos Itau SA* | 5,173 | 16,054 | ||||||

Klabin SA | 44,500 | 221,094 | ||||||

Linx SA | 39,328 | 220,798 | ||||||

Lojas Renner SA | 68,600 | 637,577 | ||||||

| Number of Shares | Value | |||||||

COMMON STOCKS — (Continued) |

| |||||||

Brazil — (Continued) | ||||||||

Multiplan Empreendimentos Imobiliarios SA | 7,913 | $ | 169,344 | |||||

Petroleo Brasileiro SA*. | 46,600 | 210,387 | ||||||

Petroleo Brasileiro SA, SP ADR* | 67,900 | 611,779 | ||||||

Sao Martinho SA | 28,000 | 155,171 | ||||||

Telefonica Brasil SA | 19,547 | 228,045 | ||||||

Vale SA, SP ADR | 53,452 | 438,841 | ||||||

|

| |||||||

| 7,498,152 | ||||||||

|

| |||||||

Chile — 5.2% | ||||||||

Itau CorpBanca | 15,800,000 | 144,031 | ||||||

Parque Arauco SA | 143,439 | 375,445 | ||||||

SACI Falabella | 36,000 | 287,863 | ||||||

|

| |||||||

| 807,339 | ||||||||

|

| |||||||

Colombia — 0.8% | ||||||||

Grupo de Inversiones Suramericana SA | 10,100 | 133,545 | ||||||

|

| |||||||

Mexico — 23.9% | ||||||||

Alsea SAB de CV | 65,700 | 233,655 | ||||||

America Movil SAB de CV, SP ADR, Class L | 46,800 | 720,252 | ||||||

Arca Continental SAB de CV | 44,200 | 325,021 | ||||||

Cemex SAB de CV, SP ADR* | 37,600 | 346,672 | ||||||

Concentradora Fibra Danhos SA de CV, REIT | 61,650 | 105,876 | ||||||

Corp. Inmobiliaria Vesta SAB de CV | 120,000 | 168,795 | ||||||

Grupo Aeroportuario del Centro Norte SAB de CV, ADR | 10,000 | 443,600 | ||||||

The accompanying notes are an integral part of the financial statements.

21

BRADESCO LATIN AMERICAN EQUITY FUND

Portfolio of Investments (Concluded)

April 30, 2017

| Number of Shares | Value | |||||||

COMMON STOCKS — (Continued) |

| |||||||

Mexico — (Continued) | ||||||||

Grupo Cementos de Chihuahua SAB de CV | 35,000 | $ | 166,380 | |||||

Grupo Financiero Banorte SAB de CV, Class O | 109,600 | 632,499 | ||||||

Rassini SAB de CV | 29,277 | 138,475 | ||||||

Wal-Mart de Mexico SAB de CV | 199,700 | 449,783 | ||||||

|

| |||||||

| 3,731,008 | ||||||||

|

| |||||||

Peru — 2.3% | ||||||||

Credicorp Ltd. | 2,400 | 368,784 | ||||||

|

| |||||||

TOTAL COMMON STOCKS |

| 12,610,913 | ||||||

|

| |||||||

PREFERRED STOCKS — 15.9% |

| |||||||

Brazil — 15.1% | ||||||||

Alupar Investimento SA | 28,177 | 55,483 | ||||||

Banco do Estado do Rio Grande do Sul SA, Class B | 14,000 | 63,295 | ||||||

Cia Energetica de Minas Gerais | 21,400 | 59,601 | ||||||

Cia Energetica de Sao Paulo, Class B | 72,400 | 409,895 | ||||||

Gerdau SA | 57,300 | 176,735 | ||||||

Itausa - Investimentos Itau SA | 315,700 | 978,714 | ||||||

Lojas Americanas SA | 59,200 | 312,408 | ||||||

Suzano Papel e Celulose SA, Class A | 71,200 | 299,017 | ||||||

|

| |||||||

| 2,355,148 | ||||||||

|

| |||||||

| Number of Shares | Value | |||||||

PREFERRED STOCKS — (Continued) |

| |||||||

Colombia — 0.8% | ||||||||

Bancolombia SA | 12,600 | $ | 123,002 | |||||

|

| |||||||

TOTAL PREFERRED STOCKS |

| 2,478,150 | ||||||

|

| |||||||

REGISTERED INVESTMENT COMPANY — 4.6% |

| |||||||

Dreyfus Government Cash Management Fund, Institutional Shares, | 713,647 | 713,647 | ||||||

|

| |||||||

TOTAL REGISTERED INVESTMENT |

| 713,647 | ||||||

|

| |||||||

TOTAL INVESTMENTS - 101.2% |

| 15,802,710 | ||||||

LIABILITIES IN EXCESS OF OTHER ASSETS - (1.2)% | (186,304 | ) | ||||||

|

| |||||||

NET ASSETS - 100.0% | $ | 15,616,406 | ||||||

|

| |||||||

| * | Non-income producing. |

| (a) | Rate periodically changes. Rate disclosed is the daily yield on April 30, 2017. |

| ADR | American Depository Receipt |

| REIT | Real Estate Investment Trust |

| SP | ADR Sponsored American Depository Receipt |

The accompanying notes are an integral part of the financial statements.

22

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Portfolio Holdings Summary Table

April 30, 2017

(Unaudited)

The following table presents a summary by security type of the portfolio holdings of the Fund:

| % of Net Assets | Value | |||||||

SECURITY TYPE: | ||||||||

Corporate Bonds and Notes | 80.9 | % | $ | 12,969,293 | ||||

Government Bonds | 8.0 | 1,290,495 | ||||||

Registered Investment Company | 9.3 | 1,489,002 | ||||||

Other Assets in Excess of Liabilities | 1.8 | 280,725 | ||||||

|

|

|

| |||||

NET ASSETS | 100.0 | % | $ | 16,029,515 | ||||

|

|

|

| |||||

Portfolio holdings are subject to change at any time.

The accompanying notes are an integral part of the financial statements.

23

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Portfolio of Investments

April 30, 2017

| Par Value | Value | |||||||

CORPORATE BONDS AND NOTES — 80.9% |

| |||||||

Austria — 0.1% | ||||||||

OAS Investments GmbH | $ | 200,000 | $ | 11,000 | ||||

|

| |||||||

Brazil — 27.8% | ||||||||

Banco Daycoval SA | 200,000 | 205,500 | ||||||

Banco do Brasil SA | 700,000 | 728,000 | ||||||

Banco Votorantim SA | 300,000 | 321,750 | ||||||

BM&FBovespa SA | 500,000 | 526,900 | ||||||

Caixa Economica Federal | 300,000 | 288,000 | ||||||

Centrais Eletricas Brasileiras SA | 500,000 | 512,000 | ||||||

Cia Brasileira de Aluminio | 200,000 | 194,500 | ||||||

Embraer SA | 500,000 | 526,875 | ||||||

Itau Unibanco Holding SA | 200,000 | 212,570 | ||||||

Itau Unibanco Holding SA | 300,000 | 316,878 | ||||||

Itau Unibanco Holding SA | 200,000 | 209,250 | ||||||

Votorantim Cimentos SA | 400,000 | 408,500 | ||||||

|

| |||||||

| 4,450,723 | ||||||||

|

| |||||||

Canada — 1.9% | ||||||||

St Marys Cement, Inc. Canada 5.75%, 01/28/2027(b) | 300,000 | 299,625 | ||||||

|

| |||||||

| Par Value | Value | |||||||

| CORPORATE BONDS AND NOTES — (Continued) | ||||||||

Cayman Islands — 17.7% | ||||||||

BR Malls International Finance Ltd. | $ | 400,000 | $ | 404,400 | ||||

Braskem Finance Ltd. | 250,000 | 272,813 | ||||||

Braskem Finance Ltd. | 200,000 | 210,000 | ||||||

Cosan Overseas Ltd. | 600,000 | 602,700 | ||||||

Fibria Overseas Finance Ltd. | 400,000 | 413,000 | ||||||

Suzano Trading Ltd. | 200,000 | 213,300 | ||||||

Vale Overseas Ltd. | 500,000 | 512,350 | ||||||

Vale Overseas Ltd. | 200,000 | 218,560 | ||||||

|

| |||||||

| 2,847,123 | ||||||||

|

| |||||||

Chile — 1.3% | ||||||||

Itau CorpBanca | 200,000 | �� | 206,310 | |||||

|

| |||||||

Colombia — 2.7% | ||||||||

Bancolombia SA | 400,000 | 440,500 | ||||||

|

| |||||||

Luxembourg — 7.4% | ||||||||

Cosan Luxembourg SA | 400,000 | 417,520 | ||||||

Klabin Finance SA | 360,000 | 364,140 | ||||||

Ultrapar International SA | 400,000 | 401,500 | ||||||

|

| |||||||

| 1,183,160 | ||||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

24

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Portfolio of Investments (Concluded)

April 30, 2017

| Par Value | Value | |||||||

CORPORATE BONDS AND NOTES — (Continued) |

| |||||||

Mexico — 7.9% | ||||||||

Alfa SAB de CV | $ | 500,000 | $ | 528,750 | ||||

America Movil SAB de CV | 300,000 | 322,593 | ||||||

Grupo Bimbo SAB de CV | 400,000 | 422,259 | ||||||

|

| |||||||

| 1,273,602 | ||||||||

|

| |||||||

Netherlands — 10.8% | ||||||||

Petrobras Global Finance BV | 500,000 | 566,250 | ||||||

Petrobras Global Finance BV | 1,000,000 | 1,166,000 | ||||||

|

| |||||||

| 1,732,250 | ||||||||

|

| |||||||

Virgin Islands — 3.3% | ||||||||

Gerdau Trade, Inc. | 500,000 | 525,000 | ||||||

|

| |||||||

TOTAL CORPORATE BONDS AND NOTES (Cost $12,769,195) | 12,969,293 | |||||||

|

| |||||||

GOVERNMENT BONDS — 8.0% |

| |||||||

Brazilian Government International Bond | 300,000 | 320,595 | ||||||

Brazilian Government International Bond | 300,000 | 348,000 | ||||||

| Par Value | Value | |||||||

GOVERNMENT BONDS — (Continued) |

| |||||||

Mexico Government International Bond | $ | 600,000 | $ | 621,900 | ||||

|

| |||||||

TOTAL GOVERNMENT BONDS | 1,290,495 | |||||||

|

| |||||||

| Number of Shares | ||||||||

REGISTERED INVESTMENT COMPANY — 9.3% |

| |||||||

Dreyfus Government Cash Management Fund, Institutional Shares, 0.69%(d) | 1,489,002 | 1,489,002 | ||||||

TOTAL REGISTERED INVESTMENT COMPANY (Cost $1,489,002) | 1,489,002 | |||||||

TOTAL INVESTMENTS - 98.2% (Cost $15,474,348) | 15,748,790 | |||||||

OTHER ASSETS IN EXCESS OF LIABILITIES - 1.8% | 280,725 | |||||||

|

| |||||||

NET ASSETS - 100.0% | $ | 16,029,515 | ||||||

|

| |||||||

| (a) | Investment with a total aggregate value of $11,000 or 0.07% of net assets was in default as of April 30, 2017. |

| (b) | This security is callable. |

| (c) | Security is perpetual. Date shown is next call date. |

| (d) | Rate periodically changes. Rate disclosed is the daily yield on April 30, 2017. |

The accompanying notes are an integral part of the financial statements.

25

BRADESCO FUNDS

Statements of Assets and Liabilities

April 30, 2017

| Bradesco Latin American Equity Fund | Bradesco Latin American Hard Currency Bond Fund | |||||||||

Assets | ||||||||||

Investments, at value (Cost $14,598,400 and $15,474,348, respectively) | $ | 15,802,710 | $ | 15,748,790 | ||||||

Cash | 101 | — | ||||||||

Deposit with Broker | — | 103,500 | ||||||||

Receivable for investments sold | 866,697 | — | ||||||||

Receivable for capital shares sold | 1,000 | 7 | ||||||||

Dividends and interest receivable | 65,072 | 220,067 | ||||||||

Prepaid expenses and other assets | 43,369 | 43,560 | ||||||||

|

|

|

| |||||||

Total assets | 16,778,949 | 16,115,924 | ||||||||

|

|

|

| |||||||

Liabilities | ||||||||||

Payable for investments purchased | 1,071,792 | — | ||||||||

Payable for audit fees. | 37,150 | 36,000 | ||||||||

Payable for administration and accounting fees | 11,060 | 10,893 | ||||||||

Payable for custodian fees | 10,813 | 8,741 | ||||||||

Payable for transfer agent fees | 8,756 | 11,443 | ||||||||

Payable for legal fees. | 8,501 | 10,127 | ||||||||

Payable to Investment Adviser | 7,244 | 5,716 | ||||||||

Payable for printing fees | 6,545 | 2,691 | ||||||||

Payable for distribution fees | 62 | 20 | ||||||||

Accrued expenses | 620 | 778 | ||||||||

|

|

|

| |||||||

Total liabilities | 1,162,543 | 86,409 | ||||||||

|

|

|

| |||||||

Net Assets | $ | 15,616,406 | $ | 16,029,515 | ||||||

|

|

|

| |||||||

Net Assets Consisted of: | ||||||||||

Capital stock, $0.01 par value | $ | 18,741 | $ | 16,340 | ||||||

Paid-in capital | 18,344,038 | 16,507,356 | ||||||||

Accumulated net investment income | 26,848 | 81,844 | ||||||||

Accumulated net realized loss from investments, foreign currency transactions, futures contracts and translation of assets and liabilities denominated in foreign currency | (3,978,364 | ) | (850,467 | ) | ||||||

Net unrealized appreciation on investments and foreign currency translations | 1,205,143 | 274,442 | ||||||||

|

|

|

| |||||||

Net Assets | $ | 15,616,406 | $ | 16,029,515 | ||||||

|

|

|

| |||||||

Institutional Class: | ||||||||||

Net asset value, offering and redemption price per share ($15,313,919 / 1,837,580) and ($15,929,959 / 1,623,872 shares) | $ | 8.33 | $ | 9.81 | ||||||

|

|

|

| |||||||

Retail Class: | ||||||||||

Net asset value, offering and redemption price per share ($302,487 / 36,500) and ($99,556 / 10,123 shares) | $ | 8.29 | $ | 9.83 | ||||||

|

|

|

| |||||||

The accompanying notes are an integral part of the financial statements.

26

BRADESCO FUNDS

Statements of Operations

For the Year Ended April 30, 2017

| Bradesco Latin American Equity Fund | Bradesco Latin American Hard Currency Bond Fund | |||||||||

Investment Income | ||||||||||

Dividends | $ | 444,013 | $ | 1,727 | ||||||

Less: foreign taxes withheld | (40,770 | ) | — | |||||||

Interest | — | 776,817 | ||||||||

|

|

|

| |||||||

Total investment income | 403,243 | 778,544 | ||||||||

|

|

|

| |||||||

Expenses | ||||||||||

Advisory fees (Note 2) | 143,127 | 115,732 | ||||||||

Administration and accounting fees | 74,860 | 73,494 | ||||||||

Registration and filing fees | 28,036 | 28,326 | ||||||||

Transfer agent fees (Note 2) | 24,678 | 27,862 | ||||||||

Custodian fees (Note 2) | 23,046 | 19,052 | ||||||||

Audit fees | 21,429 | 18,499 | ||||||||

Legal fees | 21,151 | 25,818 | ||||||||

Trustees’ and officers’ fees (Note 2) | 18,642 | 21,535 | ||||||||

Printing and shareholder reporting fees | 9,752 | 13,129 | ||||||||

Distribution fees (Retail Class) (Note 2) | 448 | 240 | ||||||||

Other expenses | 20,004 | 20,912 | ||||||||

|

|

|

| |||||||

Total expenses before waivers and reimbursements | 385,173 | 364,599 | ||||||||

|

|

|

| |||||||

Less: waivers and reimbursements (Note 2) | (134,253 | ) | (132,864 | ) | ||||||

|

|

|

| |||||||

Net expenses after waivers and reimbursements | 250,920 | 231,735 | ||||||||

|

|

|

| |||||||

Net investment income | 152,323 | 546,809 | ||||||||

|

|

|

| |||||||

Net realized and unrealized gain/(loss) from investments | ||||||||||

Net realized gain from investments* | 186,192 | 103,778 | ||||||||

Net realized gain from written options** | — | 16,313 | ||||||||

Net realized loss from foreign currency transactions | (60,885 | ) | — | |||||||

Net realized gain from futures contracts** | — | 28,227 | ||||||||

Net change in unrealized appreciation/(depreciation) on investments | 1,586,804 | 733,527 | ||||||||

Net change in unrealized appreciation/(depreciation) on foreign currency translations | 507 | — | ||||||||

|

|

|

| |||||||

Net realized and unrealized gain on investments | 1,712,618 | 881,845 | ||||||||

|

|

|

| |||||||

Net increase in net assets resulting from operations | $ | 1,864,941 | $ | 1,428,654 | ||||||

|

|

|

| |||||||

| * | Includes realized loss on purchased options of $132,891 for the Bradesco Latin American Hard Currency Bond Fund. Primary risk exposure is equity contracts. |

| ** | Primary risk exposure is interest rate contracts. |

The accompanying notes are an integral part of the financial statements.

27

BRADESCO LATIN AMERICAN EQUITY FUND

Statements of Changes in Net Assets

| For the Year Ended April 30, 2017 | For the Year Ended April 30, 2016 | |||||||||

Increase/(Decrease) in net assets from operations: | ||||||||||

Net investment income | $ | 152,323 | $ | 136,551 | ||||||

Net realized gain/(loss) from investments and foreign currency transactions | 125,307 | (2,459,753 | ) | |||||||

Net change in unrealized appreciation/(depreciation) on investments and foreign currency translations | 1,587,311 | 154,864 | ||||||||

|

|

|

| |||||||

Net increase/(decrease) in net assets resulting from operations. | 1,864,941 | (2,168,338 | ) | |||||||

|

|

|

| |||||||

Less Dividends and Distributions to Shareholders: | ||||||||||

Net investment income: | ||||||||||

Institutional Class | (54,684 | ) | — | |||||||

Retail Class | (760 | ) | — | |||||||

|

|

|

| |||||||

Total from net investment income | (55,444 | ) | — | |||||||

|

|

|

| |||||||

Increase in Net Assets Derived from Capital Share Transactions (Note 4) | 228,589 | 27,302 | ||||||||

|

|

|

| |||||||

Total increase/(decrease) in net assets | 2,038,086 | (2,141,036 | ) | |||||||

|

|

|

| |||||||

Net assets | ||||||||||

Beginning of year | 13,578,320 | 15,719,356 | ||||||||

|

|

|

| |||||||

End of year | $ | 15,616,406 | $ | 13,578,320 | ||||||

|

|

|

| |||||||

Accumulated net investment gain/(loss), end of year | $ | 26,848 | $ | (11,810 | ) | |||||

|

|

|

| |||||||

The accompanying notes are an integral part of the financial statements

28

BRADESCO LATIN AMERICAN HARD CURRENCY BOND FUND

Statements of Changes in Net Assets

| For the Year Ended April 30,2017 | For the Year Ended April 30,2016 | |||||||||

Increase/(Decrease) in net assets from operations: | ||||||||||

Net investment income | $ | 546,809 | $ | 478,991 | ||||||

Net realized gain/loss from investments, written options, foreign currency transactions and futures contracts | 148,318 | (874,581 | ) | |||||||

Net change in unrealized appreciation/(depreciation) on investments and foreign currency translations | 733,527 | (322,417 | ) | |||||||

|

|

|

| |||||||

Net increase/decrease in net assets resulting from operations | 1,428,654 | (718,007 | ) | |||||||

|

|

|

| |||||||

Less Dividends and Distributions to Shareholders from: | ||||||||||

Net investment income: | ||||||||||

Institutional Class | (480,850 | ) | (473,674 | ) | ||||||

Retail Class | (2,751 | ) | (2,776 | ) | ||||||

|

|

|

| |||||||

Total from net investment income | (483,601 | ) | (476,450 | ) | ||||||

|

|

|

| |||||||

Increase in Net Assets Derived from Capital Share Transactions (Note 4) | 412,839 | 406,479 | ||||||||

|

|

|

| |||||||

Total increase/(decrease) in net assets | 1,357,892 | (787,978 | ) | |||||||

|

|

|

| |||||||

Net assets | ||||||||||

Beginning of year | 14,671,623 | 15,459,601 | ||||||||

|

|

|

| |||||||

End of year | $ | 16,029,515 | $ | 14,671,623 | ||||||

|

|

|

| |||||||

Accumulated net investment income, end of year | $ | 81,844 | $ | 18,636 | ||||||

|

|

|

| |||||||

The accompanying notes are an integral part of the financial statements.

29

BRADESCO LATIN AMERICAN EQUITY FUND

Financial Highlights

Contained below is per share operating performance data for Institutional Class shares outstanding, total investment return, ratios to average net assets and other supplemental data for each of the respective periods. The total returns in the table represent the rate that an investor would have earned or lost on an investment in the Fund (assuming reinvestment of all dividends and distributions). This information has been derived from information provided in the financial statements and should be read in conjunction with the financial statements and the notes thereto.

| Institutional Class | ||||||||||||||||||||

| For the Year Ended April 30, 2017 | For the Year Ended April 30, 2016 | For the Year Ended April 30, 2015 | For the Period December 20, 2013* to April 30, 2014 | |||||||||||||||||

Per Share Operating Performance | ||||||||||||||||||||

Net asset value, beginning of period | $ | 7.36 | $ | 8.54 | $ | 10.24 | $ | 10.00 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

Net investment income(1) . | 0.08 | 0.07 | 0.06 | 0.06 | ||||||||||||||||

Net realized and unrealized gain/(loss) on investments | 0.92 | (1.25 | ) | (1.75 | )(2) | 0.18 | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

Net increase/(decrease) in net assets resulting from operations | 1.00 | (1.18 | ) | (1.69 | ) | 0.24 | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

Dividends and distributions to shareholders from: | ||||||||||||||||||||

Net investment income | (0.03 | ) | — | (0.01 | ) | — | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

Net asset value, end of period | $ | 8.33 | $ | 7.36 | $ | 8.54 | $ | 10.24 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||||||

Total investment return(3) | 13.63 | % | (13.82 | )% | (16.51 | )%(2) | 2.40 | % | ||||||||||||

Ratio/Supplemental Data | ||||||||||||||||||||

Net assets, end of period (in thousands) | $ | 15,314 | $ | 13,481 | $ | 15,637 | $ | 1,024 | ||||||||||||

Ratio of expenses to average net assets | 1.75 | % | 1.75 | % | 1.75 | % | 1.75 | %(4) | ||||||||||||

Ratio of expenses to average net assets without waivers and expense reimbursements(5) | 2.69 | % | 2.98 | % | 3.27 | % | 23.40 | %(4) | ||||||||||||

Ratio of net investment income to average net assets | 1.07 | % | 1.08 | % | 0.60 | % | 1.70 | %(4) | ||||||||||||