UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant o

Filed by a Party other than the Registrant x

Check the appropriate box:

x Preliminary Proxy Statement

¨ Confidential, for Use of the Commission Only (as permitted by Rule14a-6(e)(2))

¨ Definitive Proxy Statement

o Definitive Additional Materials

o Soliciting Material Under Rule 14a-12

HEARTWARE INTERNATIONAL, INC. |

| (Name of Registrant as Specified in Its Charter) |

ENGAGED CAPITAL MASTER FEEDER I, LP ENGAGED CAPITAL MASTER FEEDER II, LP ENGAGED CAPITAL I, LP ENGAGED CAPITAL I OFFSHORE, LTD. ENGAGED CAPITAL II, LP ENGAGED CAPITAL II OFFSHORE LTD. ENGAGED CAPITAL, LLC ENGAGED CAPITAL HOLDINGS, LLC GLENN W. WELLING SCOTT R. WARD SHAWN T MCCORMICK BRENDAN B. SPRINGSTUBB |

| (Name of Persons(s) Filing Proxy Statement, if Other Than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

x No fee required.

¨ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

(1) Title of each class of securities to which transaction applies:

(2) Aggregate number of securities to which transaction applies:

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

(4) Proposed maximum aggregate value of transaction:

(5) Total fee paid:

¨ Fee paid previously with preliminary materials:

¨ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing.

(1) Amount previously paid:

(2) Form, Schedule or Registration Statement No.:

(3) Filing Party:

(4) Date Filed:

PRELIMINARY COPY SUBJECT TO COMPLETION

DATED JANUARY 7, 2016

ENGAGED CAPITAL, LLC

____________, 2016

Dear Fellow HeartWare Stockholder:

The attached proxy statement and the enclosed WHITE proxy card are being furnished to you, the stockholders of HeartWare International, Inc., a Delaware corporation (“HeartWare” or the “Company”), in connection with the solicitation of proxies by Engaged Capital, LLC (together with its affiliates “Engaged Capital”) for use at the special meeting of stockholders of HeartWare, and at any adjournments or postponements thereof (the “Special Meeting”), relating to the proposed acquisition (the “Acquisition”) of Valtech Cardio, Ltd., a private company incorporated under the laws of Israel (“Valtech”), by HeartWare. In connection with the proposed Acquisition, HeartWare entered into a Business Combination Agreement (the “Business Combination Agreement”), dated as of September 1, 2015, with Valtech, HW Global, Inc., a Delaware corporation and a direct wholly owned subsidiary of HeartWare (“Holdco”), HW Merger Sub, Inc., a Delaware corporation and a direct wholly owned subsidiary of Holdco (“US Merger Sub”), Valor Merger Sub Ltd., a private company incorporated under the laws of Israel and a direct wholly owned subsidiary of Holdco (“ISR Merger Sub”) and Valor Shareholder Representative, LLC, a Delaware limited liability company. Pursuant to the Business Combination Agreement, among other things, (a) U.S. Merger Sub will merge with and into HeartWare, with HeartWare surviving the merger as a wholly owned subsidiary of Holdco, and (b) ISR Merger Sub will merge with and into Valtech, with Valtech surviving the merger as a subsidiary of Holdco.

Pursuant to the attached proxy statement, we are soliciting proxies from holders of shares of HeartWare common stock to vote AGAINST the proposed Acquisition.

The Special Meeting will be held on _________, 2016 at ____, local time, at 200 Clarendon Street, 27th Floor, Boston, Massachusetts 02116.

We urge you to carefully consider the information contained in the attached proxy statement and then support our efforts by signing, dating and returning the enclosed WHITE proxy card today. The attached proxy statement and the enclosed WHITE proxy card are first being furnished to the Company’s stockholders on or about ________ __, 2016.

If you have already voted for management’s proposal relating to the Acquisition, you have every right to change your vote by signing, dating and returning a later dated proxy card.

If you have any questions or require any assistance with your vote, please contact Morrow & Co., LLC (“Morrow”), which is assisting us, at their address and toll-free numbers listed on the following page.

Thank you for your support,

/s/ Glenn W. Welling

Glenn W. Welling

Engaged Capital, LLC

If you have any questions, require assistance in voting your WHITE proxy card, or need additional copies of Engaged Capital’s proxy materials, please contact Morrow & Co., LLC at the phone numbers or email listed below. MORROW & CO., LLC 470 West Avenue Stamford, CT 06902 Call Toll Free: (800) 662-5200 Call Direct: (203) 658-9400 Email: engaged@morrowco.com |

PRELIMINARY COPY SUBJECT TO COMPLETION

DATED JANUARY 7, 2016

SPECIAL MEETING OF STOCKHOLDERS

OF

HEARTWARE INTERNATIONAL, INC.

TO BE HELD ON _________

PROXY STATEMENT

OF

ENGAGED CAPIAL, LLC

SOLICITATION OF PROXIES IN OPPOSITION TO

MATTERS RELATING TO THE PROPOSED

ACQUISITION OF VALTECH CARDIO, LTD. BY HEARTWARE INTERNATIONAL, INC.

PLEASE SIGN, DATE AND MAIL THE ENCLOSED WHITE PROXY CARD TODAY

Engaged Capital, LLC (“Engaged Capital LLC” and together with its affiliates “Engaged Capital” or “we”) are stockholders of HeartWare International, Inc. (“HeartWare” or the “Company”), owning approximately 1.3% of its outstanding shares of common stock, $0.001 par value per share (the “Shares”). Engaged Capital is writing to you in connection with the proposed acquisition (the “Acquisition”) of Valtech Cardio, Ltd., a private company incorporated under the laws of Israel (“Valtech”), by HeartWare. The Board of Directors of HeartWare (the “Board”) has scheduled a special meeting of stockholders for the purpose of approving the proposed Acquisition (the “Special Meeting”). The Special Meeting is scheduled to be held on _________, 2016 at ____, local time, at 200 Clarendon Street, 27th Floor, Boston, Massachusetts 02116. In connection with the proposed Acquisition, HeartWare entered into a Business Combination Agreement (the “Business Combination Agreement”), dated as of September 1, 2015, with Valtech, HW Global, Inc., a Delaware corporation and a direct wholly owned subsidiary of HeartWare (“Holdco”), HW Merger Sub, Inc., a Delaware corporation and a direct wholly owned subsidiary of Holdco (“US Merger Sub”), Valor Merger Sub Ltd., a private company incorporated under the laws of Israel and a direct wholly owned subsidiary of Holdco (“ISR Merger Sub”) and Valor Shareholder Representative, LLC, a Delaware limited liability company. Pursuant to the Business Combination Agreement, among other things, (a) U.S. Merger Sub will merge with and into HeartWare, with HeartWare surviving the merger as a wholly owned subsidiary of Holdco, and (b) ISR Merger Sub will merge with and into Valtech, with Valtech surviving the merger as a subsidiary of Holdco.

Pursuant to this Proxy Statement, Engaged Capital is soliciting proxies from holders of the Shares, in respect of the following proposal to be considered at the Special Meeting, as described in greater detail in the Company’s proxy statement for the Special Meeting (the “Company’s Proxy Statement”):

1. The Company’s proposal to adopt the Business Combination Agreement, dated as of September 1, 2015, by and among HeartWare, Valtech, Holdco, U.S. Merger Sub, ISR Merger Sub and Valor Shareholder Representative, LLC, and approve the transactions contemplated thereby, including, without limitation, (a) the merger of U.S. Merger Sub with and into HeartWare, with HeartWare surviving the merger as a wholly owned subsidiary of Holdco, (b) the merger of ISR Merger Sub with and into Valtech, with Valtech surviving the merger as a subsidiary of Holdco and (c) the other transactions contemplated thereby (collectively, the “Transactions Proposal”).

ENGAGED CAPITAL URGES YOU TO VOTE THE WHITE PROXY CARD “AGAINST” THE TRANSACTIONS PROPOSAL.

The participants in this proxy solicitation are Engaged Capital Master Feeder I, LP, a Cayman Islands exempted limited partnership (“Engaged Capital Master I”), Engaged Capital Master Feeder II, LP, a Cayman Islands exempted limited partnership (“Engaged Capital Master II”), Engaged Capital I, LP, a Delaware limited partnership (“Engaged Capital I”), Engaged Capital I Offshore, Ltd., a Cayman Islands exempted company (“Engaged Capital Offshore”), Engaged Capital II, LP, a Delaware limited partnership (“Engaged Capital II”), Engaged Capital II Offshore Ltd., a Cayman Islands exempted company (“ Engaged Capital Offshore II”), Engaged Capital LLC, a Delaware limited liability company, Engaged Capital Holdings, LLC, a Delaware limited liability company (“Engaged Holdings”), Glenn W. Welling, Scott R. Ward, Shawn T McCormick and Brendan B. Springstubb.

Engaged Capital has submitted a notice of the nomination of Messrs. Ward, McCormick and Springstubb for election as directors at the next annual meeting of the stockholders of the Company.

For additional information concerning the participants in this proxy solicitation, please refer to the information set forth under the heading “Additional Participant Information.” This Proxy Statement and the WHITE proxy card are first being furnished to HeartWare’s stockholders on or about [______], 2016.

The Company has set the close of business on ______, 2016 as the record date for determining stockholders entitled to notice of and to vote at the Special Meeting (the “Record Date”). The principal executive offices of HeartWare are located at 500 Old Connecticut Path, Building A, Framingham, Massachusetts 01701. Stockholders of record at the close of business on the Record Date will be entitled to vote at the Special Meeting. As of the Record Date, there were ________ Shares outstanding and entitled to vote at the Special Meeting. As of [________], 2016, the approximate date on which Engaged Capital expects to mail this Proxy Statement to the stockholders, Engaged Capital, together with all of the participants in this solicitation, are the collective beneficial owners of an aggregate of 230,000 Shares, which represents approximately 1.3% of the Shares outstanding. Of the Shares beneficially owned by Engaged Capital, [_____] of such Shares may be voted by Engaged Capital at the Special Meeting.

According to the Company’s Proxy Statement, the adoption of the Business Combination Agreement will require the affirmative vote of stockholders holding at least a majority of the outstanding Shares entitled to vote as of the close of business on the Record Date.

THIS SOLICITATION IS BEING MADE BY ENGAGED CAPITAL AND NOT ON BEHALF OF THE BOARD OF DIRECTORS OR MANAGEMENT OF HEARTWARE. ENGAGED CAPITAL IS NOT AWARE OF ANY OTHER MATTERS TO BE BROUGHT BEFORE THE SPECIAL MEETING. SHOULD OTHER MATTERS, WHICH ENGAGED CAPITAL IS NOT AWARE OF A REASONABLE TIME BEFORE THIS SOLICITATION, BE BROUGHT BEFORE THE SPECIAL MEETING, THE PERSONS NAMED AS PROXIES IN THE ENCLOSED WHITE PROXY CARD WILL VOTE ON SUCH MATTERS IN THEIR DISCRETION.

ENGAGED CAPITAL URGES YOU TO SIGN, DATE AND RETURN THE WHITE PROXY CARD TO VOTE “AGAINST” THE TRANSACTIONS PROPOSAL.

2

IF YOU HAVE ALREADY SENT A COMPANY PROXY CARD FURNISHED BY HEARTWARE, YOU MAY REVOKE THAT PROXY BY SIGNING, DATING AND RETURNING THE ENCLOSED WHITE PROXY CARD. THE LATEST DATED PROXY IS THE ONLY ONE THAT COUNTS. ANY PROXY MAY BE REVOKED AT ANY TIME PRIOR TO THE SPECIAL MEETING BY DELIVERING A WRITTEN NOTICE OF REVOCATION OR A LATER DATED PROXY FOR THE SPECIAL MEETING TO ENGAGED CAPITAL, C/O MORROW, WHICH IS ASSISTING IN THIS SOLICITATION, OR TO THE SECRETARY OF HEARTWARE, OR BY VOTING IN PERSON AT THE SPECIAL MEETING.

IMPORTANT NOTICE REGARDING AVAILABILITY OF PROXY MATERIALS FOR THE SPECIAL MEETING OF STOCKHOLDERS TO BE HELD ON ______, 2016

The proxy materials are available at [_________]

3

IMPORTANT

Your vote is important, no matter how many or how few Shares you own. Engaged Capital urges you to sign, date, and return the enclosed WHITE proxy card today to vote AGAINST the Transactions Proposal.

Engaged Capital does not believe that the Acquisition is in the best interest of the Company’s stockholders. A vote AGAINST the Transactions Proposal will enable you – as the owners of HeartWare – to send a message to the Board that you do not believe the Acquisition is in stockholders’ best interest and you are committed to protecting your investment.

| ● | If your Shares are registered in your own name, please sign and date the enclosed WHITE proxy card and return it to Engaged Capital, c/o Morrow, in the enclosed envelope today. |

| ● | If your Shares are held in a brokerage account or bank, you are considered the beneficial owner of the Shares, and these proxy materials, together with a WHITE voting form, are being forwarded to you by your broker or bank. As a beneficial owner, you must instruct your broker, trustee or other representative how to vote. Your broker cannot vote your Shares on your behalf without your instructions. |

| ● | Depending upon your broker or custodian, you may be able to vote either by toll-free telephone or by the Internet. Please refer to the enclosed voting form for instructions on how to vote electronically. You may also vote by signing, dating and returning the enclosed voting form. |

If you have any questions, require assistance in voting your WHITE proxy card, or need additional copies of Engaged Capital’s proxy materials, please contact Morrow & Co., LLC at the phone numbers or email listed below. MORROW & CO., LLC 470 West Avenue Stamford, CT 06902 Call Toll Free: (800) 662-5200 Call Direct: (203) 658-9400 Email: engaged@morrowco.com |

4

PROPOSAL NO. 1

APPROVAL OF BUSINESS COMBINATION AGREEMENT

You are being asked by HeartWare to approve the Business Combination Agreement and the transactions contemplated thereby (the “Transactions”). For the reasons discussed below, we oppose the proposed Transactions and Business Combination Agreement. To that end, we are soliciting your proxy to vote AGAINST Proposal No. 1.

We urge you to demonstrate your opposition to the proposed Transactions and to send a message to the HeartWare Board that the Transactions Proposal is not in the best interest of HeartWare stockholders by signing, dating and returning the enclosed WHITE proxy card as soon as possible.

REASONS TO VOTE AGAINST THE TRANSACTIONS PROPOSAL

We strongly believe that the Acquisition of Valtech is detrimental to, and not in the best interest of, the Company’s stockholders. We remain baffled by the decision-making process that led to the Board’s decision to acquire Valtech. We cannot comprehend how the Board came to the conclusion that pursuing a risky, expensive acquisition of a pre-revenue company was a better risk-adjusted alternative than continuing to execute in the Company’s core ventricular assist device (VAD) business or selling the Company at a premium. Moreover, as explained below, the inclusion of certain terms in the Business Combination Agreement (including the acceleration provision) and governance structure of Holdco, the Company’s parent company in the event the Business Combination Agreement is approved, makes us question whether the Board is properly prioritizing the stockholders’ best interests.

We Believe the Company’s Rationale for Pursuing Valtech is Flawed

HeartWare has focused on Valtech’s Cardioband System (“Cardioband”) as the key value-creating asset in the Valtech portfolio that justifies the Acquisition of Valtech, which is not surprising given it is the only device within the Valtech portfolio expected to generate any material revenue for the next five years. Management has cited the performance of Abbott Laboratories’ MitraClip device (“MitraClip”) and the “conventional wisdom” that mitral valve repair is preferable to mitral valve replacement in the treatment of mitral regurgitation (“MR”) as some of the reasons to believe Cardioband will generate significant revenues. As we discuss below, this thesis is based on tenuous assumptions and ignores the significant clinical, competitive and regulatory risks facing the device.

First, brand new clinical data calls into question the thesis that transcatheter repair of MR will continue to be preferred to transcatheter replacement. An article posted to the New England Journal of Medicine website on November 9, 2015 contained updated two year data from the Cardiothoracic Surgical Trials Network’s study comparing mitral valve repair to mitral valve replacement in patients with severe ischemic MR. Significantly, this is the only randomized trial that compares the outcomes of mitral valve repair vs. mitral valve replacement in patients with MR. The results of this study are not supportive of a robust future for mitral valve repair. To quote the authors:

5

“The rate of recurrence of moderate or severe mitral regurgitation over 2 years was higher in the repair group than in the replacement group (58.8% vs. 3.8%, P<0.001). There were no significant between-group differences in rates of serious adverse events and overall readmissions, but patients in the repair group had more serious adverse events related to heart failure (P = 0.05) and cardiovascular readmissions (P = 0.01). On the Minnesota Living with Heart Failure questionnaire, there was a trend toward greater improvement in the replacement group (P = 0.07).” 1

Digging further into the published data reveals that on nearly every measure of cardiovascular adverse events, the replacement arm outperformed the repair arm. Again, to quote the authors:

“…we observed that the recurrence of mitral regurgitation, which was mostly moderate in degree, remained a progressive and excess hazard for patients undergoing mitral-valve repair… This deficiency in the durability of correction of mitral regurgitation is disconcerting, given that recurrence confers a predisposition to heart failure, atrial fibrillation, and repeat interventions and hospitalizations. We found that patients in the repair group had more serious adverse events of heart failure and hospital readmission for cardiovascular causes.”1

Not only did patients in the replacement arm have less cardiovascular adverse events, these patients also had a better quality of life than patients in the repair arm:

“The findings of the Minnesota Living with Heart Failure questionnaire, although not conclusive, were consistent with these clinical events. The 7.9-point difference in average improvement over baseline in favor of the replacement group was not significant (P = 0.07), but the magnitude of change exceeded the 5-point threshold for clinically meaningful improvement used in other studies.”1

Historically, the preference for mitral valve repair over replacement was driven by the presumption that while both were equally effective at correcting MR, repair was the safer procedure. This landmark study – the first of its kind – demonstrates that not only is the safety advantage associated with repair statistically insignificant, repair is clearly inferior to replacement in preventing the recurrence of MR and on many clinical measures, the outcomes for patients receiving repair were inferior at 2 years.

What does this mean for transcatheter mitral valve repair devices like Cardioband? As transcatheter mitral valve replacement devices are developed and refined, it is quite likely any periprocedural safety advantage associated with repair (both surgical and transcatheter) will diminish and may eventually vanish entirely. As such, we find it hard to believe Cardioband will achieve the robust revenues projected by HeartWare management if transcatheter repair offers little, if any, safety advantage and is clearly inferior in durably correcting MR when compared to replacement.

Second, the path to U.S. approval for Cardioband is murky at best. HeartWare management has already begun walking back their initial expectations for a late 2018 U.S. launch of Cardioband, recently saying that a 2019 launch “hopefully is not overly ambitious.”2 Given that management is still “brainstorming”3 potential trial designs and has not yet had any formal meetings with the FDA, a 2019 approval certainly appears to be an optimistic outcome. We need only look to MitraClip – the only transcatheter mitral valve repair device with U.S. approval to date – to observe how long (and risky) the path to U.S. approval may be for Cardioband. MitraClip secured U.S. approval in 2013 – a full 5 ½ years after receiving CE Mark and only after two substantial clinical trials (EVEREST I and EVEREST II) were conducted. Even then, MitraClip barely squeaked by a 5-3 FDA advisory panel vote for approval – which included five out of nine panel members voting against the efficacy of the device4 – and a sizeable post-marketing study was required. Nothing in the limited Cardioband dataset suggests that it is any more efficacious than MitraClip – U.S. approval appears far from certain.

1 Goldstein, Daniel, et al. "Two-year outcomes of surgical treatment of severe ischemic mitral regurgitation." New England Journal of Medicine (2015).

4 http://www.wsj.com/articles/SB10001424127887324103504578372951720541928

6

Even if the Premarket Approval-enabling trial of Cardioband yields data supportive of approval, the timeline for securing FDA approval will likely stretch beyond 2020. The COAPT trial, Abbott Laboratories’ U.S. trial comparing MitraClip to guideline-directed medical therapy (“GDMT”) in surgery-ineligible patients with MR, has been enrolling for over 3 years, and based on the pace of enrollment to date, it will take at least another year to complete enrollment. We are hard-pressed to believe that HeartWare would be quicker than Abbott Laboratories in enrolling patients in a future Cardioband pivotal trial. Assuming it takes six months to finalize a trial design and qualify study sites, 2-4 years to enroll the trial (as fast or faster than both EVEREST II and COAPT enrollment), one year of patient follow-up, 3-6 months to analyze and publish results and 6-9 months of FDA review time, FDA approval of Cardioband – if it is approved at all – would not be secured until sometime between mid-2020 and the end of 2022.

Third, acquiring Valtech would expose HeartWare stockholders to a significant risk that is completely out of the control of HeartWare and Valtech management: the results of the COAPT trial itself. The key opinion leaders who presented at HeartWare’s November 5, 2015 Investor Day (the “Investor Day”) expressed concern that the COAPT trial will miss its ill-specified primary endpoint (superiority in reducing recurrent heart failure hospitalizations vs. GDMT). These same experts also stated that, should this be the case, “reimbursement will disappear… overnight” for MitraClip and any other transcatheter repair device, including Cardioband. Securing reimbursement for Cardioband in the European Union would then likely require positive results from a rigorous, randomized (and risky) clinical trial – which would add years of additional expense and cash burn. Similarly, the consequence of a negative COAPT trial for Cardioband would likely include increased scrutiny and more onerous approval requirements from the FDA.

Fourth, there are numerous potential competitors to Cardioband. HeartWare management has portrayed the transcatheter mitral valve repair market as a two-horse race between MitraClip and Cardioband. Indeed, the financial forecast HeartWare management presented during the Investor Day assumes Cardioband will hold 40% market share in transcatheter repair in the future5. We believe this is, to put it mildly, an overly optimistic view of how the market will develop. Besides MitraClip, there are at least 21 transcatheter mitral valve repair devices under development today, at least ten of which are in human testing and/or are already approved for use in Europe. This number does not consider the internal efforts underway by both Edwards Lifesciences Corporation (“Edwards”) and Medtronic, Inc. (“Medtronic”) to develop transcatheter repair technologies as well.

Finally, we do not believe it is realistic to ascribe meaningful value to any of Valtech’s products outside of Cardioband. Valtech’s Cardiovalve for mitral valve replacement has yet to reach first-in-man, and even then, faces enormous risk in demonstrating it is a viable device. Edwards recently shelved its FORTIS valve for transcatheter mitral valve replacement after a series of adverse events were observed in the first 20 patients receiving the device. With all due respect to the R&D team at Valtech – if Edwards, the unquestionable leader in transcatheter approaches to structural heart repair, with resources and expertise far beyond what Valtech and HeartWare can call upon, could not successfully internally develop a transcatheter mitral valve replacement device, what probability of success can investors realistically assign to Cardiovalve?

7

Even if Cardiovalve successfully overcomes the developmental and clinical hurdles to produce an approvable device, HeartWare will be a late entrant to a highly competitive market. We can identify at least 15 transcatheter mitral valve replacement technologies under development, at least seven of which have achieved first-in-man. In comparison, Valtech’s Cardiovalve device does not yet have a finalized design, and even in a best-case scenario, is 18 months away from first-in-man trials.

Given the relative paucity of clinical data regarding the surgical treatment of tricuspid regurgitation and the absence of any meaningful data on transcatheter techniques to repair the tricuspid valve, we view the opportunity for Cardioband and Cardiovalve in tricuspid repair and replacement as highly uncertain and of limited value. As a result, while HeartWare management may describe Valtech as “quadrupling the number of milestones”6 ahead of the Company, we think the better term to describe these “milestones” is “risks.”

We Believe the Acquisition of Valtech adds Significant Long-term Risks to the Company

Despite the large purchase price, it is clear to us that Valtech is a collection of unproven assets. While Valtech’s valve repair and replacement assets may ultimately have the potential to generate significant revenues, these assets will have to clear numerous clinical and regulatory hurdles before providing any meaningful revenue. In fact, a significant portion of the expected long-term revenue from Valtech is from products that have yet to be fully designed, let alone validated in the clinic. The enormous upfront dilution borne by the Company’s stockholders is incongruous with the significant risk associated with achieving management’s forecast for Valtech’s products. It is entirely possible that stockholders will bear dilution in excess of 30% for an acquisition that never generates any material revenue for the Company.

The seriousness of this risk can be seen in HeartWare’s own limited M&A track record. HeartWare’s only acquisition of note, CircuLite, Inc. and its SYNERGY pump, has experienced numerous delays and design changes despite management’s assurance at the time of the acquisition that it was a “straightforward logical fix”7 to make the design change necessary to bring the SYNERGY pump back into the clinic. Now, nearly two years post-acquisition, there is still no timeline for returning SYNERGY to the market. Management’s failure to execute upon the CircuLite acquisition, a far smaller and less complex asset than Valtech, gives us no confidence that management’s assessment of the clinical and commercial timelines for Valtech will be achieved.

From a strategic standpoint, the Valtech acquisition represents a “poison pill” for many of the logical strategic acquirers of HeartWare. Abbott Laboratories, Edwards and Medtronic have each recently acquired mitral valve replacement companies that will directly compete with Valtech’s valve replacement assets. These companies – all of which are logical acquirers of HeartWare – would assign little to no value to these duplicative assets for which HeartWare is paying hundreds of millions of dollars.

Additionally, these potential competitors all have significantly more resources and expertise than HeartWare. Even if HeartWare is successful in bringing Valtech’s valve replacement assets to market, HeartWare would likely be the fourth or fifth market entrant competing with some of the largest medical device companies in the world; companies with sales and R&D budgets many times that of HeartWare. This is in stark contrast to the Company’s core VAD market, where HeartWare has competed in a virtual duopoly with a similarly-sized peer.

7 HeartWare CEO Douglas Godshall, Acquisition of Circulite Conference Call, December 2, 2013

8

We Believe the Valtech Acquisition Dilutes the Company’s Stockholders and Drains its Cash

The upfront equity dilution to HeartWare stockholders from the Acquisition is approximately 30%, which is equivalent to $425 million based on the closing price of HeartWare prior to the announcement. Additional milestones and equity warrants have the potential to more than double the total cost of the transaction over time.

In our view, the cost of the Acquisition of Valtech goes far beyond the purchase price. In order to bring Valtech’s products to market, HeartWare must invest significant amounts of cash into added R&D expenses. By management’s own admission, Valtech will increase HeartWare’s operating losses by $30 to $40 million annually over the next two years. This is on top of HeartWare’s already significant R&D expense of $120 million over the last twelve months – a sum which represents a staggering 42% of revenue and is $10 million greater than HeartWare’s main competitor, Thoratec Corporation (“Thoratec”), spent in R&D over the same period, despite the fact that Thoratec generated 70% more revenue than HeartWare8.

We believe this cash drain only compounds the risk Valtech presents to HeartWare stockholders. Not only will Valtech take management’s focus away from the core VAD business at a critical juncture, the added R&D burden will compete for HeartWare’s limited cash resources. In a worst case scenario, Valtech-related spending will siphon needed cash from the core VAD business and increase the risk that HeartWare must raise capital at unfavorable rates.

We Believe Management’s Investor Day Forecast for Valtech is Misleading

On October 15, 2015, Holdco filed a registration statement on Form S-4, as amended on November 25, 2015 (the “S-4”) in connection with the Transactions, which included a preliminary proxy statement of HeartWare that also constitutes a preliminary prospectus of Holdco. The S-4 contained four “representative cases” depicting management’s projections of Valtech’s financial performance through 2025. During the Company’s Investor Day, management presented financial projections for Valtech from “Case 2” – the second-most optimistic case – to investors. Typically, when management teams publicly present financial projections, it is safe for investors to assume these forecasts represent management’s best estimate of the expected performance of the business in question. However, this is not true of the forecast HeartWare’s management presented for Valtech at the Investor Day.

During the Investor Day, HeartWare appears to have misled investors by presenting a forecast for Valtech that is nearly 40% above management’s own probability-weighted forecast for the business. The indisputable evidence confirming our assertion is contained within the fairness opinion issued by the Company’s own financial advisors. The fairness opinion issued by Canaccord Genuity Inc. (“Canaccord”) to the Company and published in the S-4 is based upon HeartWare management’s probability-adjusted revenue forecast for Valtech9. It is a simple exercise to derive the revenue forecast supporting Canaccord’s valuation calculations used in the fairness opinion. The chart below illustrates the mismatch between HeartWare management’s probability-adjusted internal forecast for Valtech and the publicly-presented forecast highlighted at the Investor Day.

8 HeartWare Forms 10-Q for the periods ending 9/30/2014, 3/31/2015 and 6/30/2015 and Form 10-K for the period ending 12/31/2014; Thoratec Forms 10-Q for the periods 9/27/2014, 4/4/2015 and 7/4/2015 and Form 10-K for the period ending 1/3/2015

9

It would not surprise us to hear management justify this after the fact by claiming that “Case 2” is now their best forecast for Valtech. Revising long-term revenue and synergy forecasts upward is a common tactic used by management teams to defend contested transactions. Such upward revisions generally lack credibility and are usually discarded as soon as the contest has ended. Management’s upward revision to their Valtech forecast is no exception. We believe it strains credulity to believe that management’s revised forecast of how the mitral valve repair and replacement market will evolve over the next ten years will be any more accurate than the forecasts management provided to their financial advisors just a few months prior. Additionally, we believe the likelihood that HeartWare’s current management team will still be in place ten years from now when the performance of Valtech can actually be judged is low. Management therefore can promise the moon to the Company’s investors knowing full well that they are not very likely to ever be held accountable for, nor will their compensation be tied to, achieving the optimistic forecast presented at the Investor Day.

Finally, even under the most optimistic scenario provided in the S-4, Valtech would generate no meaningful cash flow until 2021. Therefore, the entire value (or lack thereof) of the proposed Acquisition hinges on the performance of Valtech, and the state of the competitive environment, at least 6-10 years from now. No one, not us, not HeartWare management, not Valtech’s competitors and not the treating physicians, can predict with any degree of certainty how the mitral valve repair and replacement market will develop over the next decade, much less predict which companies and devices will succeed. We believe it is the peak of hubris for management to claim otherwise and rationalize taking on the enormous and unnecessary risks associated with Valtech, when there is a clear, lower-risk path to significant stockholder value creation - executing in the Company’s core VAD business.

The Milestone Acceleration Provision of the Business Combination Agreement Effectively Serves as a 10-year Poison Pill

Our conversations with the Company’s stockholders has revealed that many are either unaware, or do not fully appreciate the impact, of the milestone payment acceleration provision that the Board agreed to as part of the Business Combination Agreement. As we detail below, this provision has the potential to serve as a 10-year entrenchment mechanism for HeartWare’s Board and management team by creating a significant barrier to a future sale of the Company. We feel obligated to highlight the significant cost and risk this provision imposes on HeartWare’s stockholders while benefiting the pecuniary interests of the Company’s Board, management team and the current owners of Valtech.

10

The Business Combination Agreement provides that, in the event Holdco is acquired within 10 years post the closing of the Transactions, all of the milestone payments owed to Valtech’s former owners accelerate or become more readily achievable, significantly lowering the consideration HeartWare’s stockholders would otherwise receive in a sale. Specifically:

| 1. | The 700,000-share milestone payment associated with first-in-man trials of Valtech’s Cardioband Tricuspid or Cardiovalve products becomes immediately payable regardless of whether or not either product has achieved first-in-man |

| 2. | The warrants to purchase 850,000 Holdco shares at a strike price of $83.73 that vest upon achieving $75 million in trailing twelve-month (“TTM”) revenues from Valtech products immediately vest regardless of whether or not this level of revenue has been achieved |

| 3. | $175 million of the $375 million milestone payment associated with achieving $450 million in TTM revenues from Valtech products becomes immediately payable |

| 4. | $75 million of the $375 million milestone payment becomes payable at a lowered TTM revenue threshold of $75 million, rather than $450 million |

| 5. | The remaining $125 million of the $375 million milestone payment becomes payable at a lowered TTM revenue threshold of $150 million, rather than $450 million |

It is important that the Company’s directors take time to fully understand the implications of this acceleration provision for stockholders of the Company. The acceleration provision would force Holdco’s acquirer to make milestone payments to Valtech’s former owners regardless of Valtech’s performance. Thus, the raison d'être of utilizing a milestone payment provision – to mitigate the damage to stockholders from the underperformance of an acquired asset – is rendered pointless.

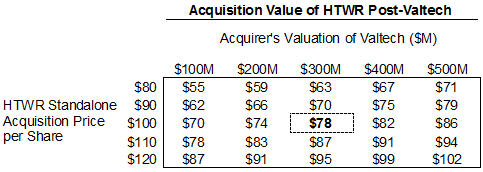

For illustrative purposes, let us assume that a potential acquirer of HeartWare is willing to pay $100 per share for the Company, pre-Valtech. Additionally, assume this same acquirer values the Valtech assets at $300 million. Due to the dilution and milestone acceleration provision associated with the Valtech acquisition, rather than receiving the full $100 per share, HeartWare stockholders would instead only receive $78 per share10 in an acquisition of Holdco, a 22% discount to the pre-Valtech per-share value of the Company. The table below illustrates the price per share the Company’s stockholders would receive in an acquisition based on a range of values for HeartWare as a standalone company and following the Valtech acquisition.

10 See Exhibit 1 to DFAN on Schedule 14A filed by Engaged Capital on January 7, 2016 for calculation

11

In order for the Company’s stockholders to actually receive the full $100 per share in an acquisition of the Company post-Valtech, the acquirer must assign a value to Valtech in excess of $850 million – an amount greater than HeartWare’s current market capitalization. This “breakeven” valuation for Valtech only increases as the value of HeartWare’s core VAD franchise increases.

The ramifications of the acceleration provision are troubling. Since the most logical acquirers of the Company already possess assets that would be either partly or wholly duplicative to Valtech’s portfolio, it is unlikely that these acquirers would assign much value to Valtech. Unfortunately for HeartWare’s stockholders, the acceleration provision would force these potential acquirers of HeartWare to pay full value for the Valtech assets. As a result, this acceleration provision effectively serves, whether intentionally or not, as a ten-year poison pill. Rather than trading with an embedded M&A premium like most of its mid-cap medical device peers, the Acquisition of Valtech will cause Holdco to trade with an M&A discount.

We are Concerned the Acquisition of Valtech Entrenches HeartWare’s Board and Management Team at the Expense of Stockholders

Conversations with numerous bankers and industry executives have supported our assertion that the Company’s acquisition of Valtech makes HeartWare a less attractive acquisition target. The most likely potential acquirers of HeartWare have categorically expressed to us that they would have no interest in acquiring the Company should the Valtech acquisition close. This fact, which directly contradicts claims being made by the Company’s management team, is particularly disheartening as many HeartWare stockholders have an investment thesis predicated upon an eventual sale of the Company to a large strategic acquirer at a significant premium.

While we agree with many of the Company’s stockholders that the ultimate destiny for HeartWare is a sale to a strategic acquirer, let us be clear – we are not advocating for a sale of the Company today. Given the currently depressed share price and uncertainty regarding the restart of the MVAD CE Mark clinical trial, we believe it is unlikely that the Board would be able to negotiate a sale of the Company at a premium that would be acceptable to stockholders today. However, it is unacceptable to the Company’s stockholders to permanently impair a future sale of the Company by acquiring an asset – Valtech – which makes the Company less attractive to the most likely acquirers.

Perhaps the Acquisition of Valtech is a product of misaligned incentives between HeartWare’s insiders and the Company’s stockholders. Troubling to us, the Board and management team have collectively purchased a total of only 4,150 Shares (valued at $300,000) on the open market over the last five years, while selling nearly 680,000 Shares (valued at $56 million) over the same time period11. Given the sparse shareholdings and past trading history of the Board and management team, investors are left to wonder if the Company’s leadership has an incentive to continue receiving (and subsequently selling) significant annual stock grants, rather than positioning the Company for an eventual sale. Unfortunately for stockholders, the Acquisition of Valtech would increase the likelihood that the Company remains independent and the annual stock grants keep flowing.

Furthermore, the approval of the Business Combination Agreement would have the added consequence of disenfranchising current HeartWare stockholders to an extent. Should the Acquisition of Valtech close, Valtech and the Company would become wholly-owned subsidiaries of Holdco. Holdco, as a newly formed company, would not be required to hold a stockholder meeting for the election of directors until the spring of 2017, which would frustrate stockholders’ ability to vote for directors of their choice. Even if Holdco elects to hold its first annual meeting at an earlier date, the Company’s current independent stockholders would have difficulty effecting any strategic or governance changes (including to the composition of Holdco’s board) as current Valtech stockholders and HeartWare insiders would collectively control approximately 25% of Holdco’s shares. Further limiting stockholders’ rights is the fact that Holdco intends to adopt a classified board structure so that only approximately one-third of all directors will be up for election each year. Accordingly, we encourage the Company’s stockholders to exercise their rights to vote against the Transactions Proposal while they still have the power to meaningfully influence the Company’s future.

11 Includes all current directors and named executive officers. Data per the Company’s SEC filings and Factset.

12

We Believe HeartWare is a Desirable and Undervalued Asset

Given the significant amount of Holdco shares to be issued to Valtech stockholders upon the close of the Transactions, any evaluation of the proposed Acquisition of Valtech requires assessing the value of HeartWare’s Shares (as current HeartWare stockholders will have their Shares represent the right to receive Holdco shares on a one-for-one basis upon the closing of the Transactions). We firmly believe the true cost of the Valtech acquisition is not based on the currently-depressed trading value of the Company’s Shares; rather it is based on the risk-adjusted fair value of the Company’s long-term standalone business plan. While the recent disclosure of a handful of adverse events observed in the MVAD CE Mark trial is unfortunate, the attractive fundamentals of the Company’s core VAD franchise are unchanged from this summer, when the Shares were trading well above $80. Barring a catastrophic MVAD pump redesign – which by all accounts is highly unlikely – the Shares should steadily close the gap to fair value as MVAD returns to the clinic.

We believe the fair value of the Shares is significantly greater than the current trading price. During the Investor Day, management provided its long-term forecast for the VAD franchise, projecting revenues of $524 million in 2020. This scenario yields a $141 per share valuation for HeartWare at the end of 201912, representing over 200% upside from today’s levels. Of course, it is only prudent to examine a more conservative scenario for the core business. We believe the Shares are undervalued even if we assume management’s forecast is aggressive. Under a scenario where VAD revenues in 2020 are only $450 million, and revenue growth beyond 2020 is a more modest 10% rather than the 18% projected by management, fair value at the end of 2019 would be $92 per share – a 100% premium from today’s levels13.

We cannot comprehend, if the Board truly believes the forecast presented at the Investor Day, how the Board can justify the Valtech acquisition as being a superior risk-adjusted alternative to simply executing in the Company’s core business – a strategy which would double to triple the value of the Company in four years.

As a result, we believe it is false to portray the Valtech acquisition as being “cheaper” now than it was at the time the Acquisition was initially disclosed – the 30% upfront dilution, additional shares and warrants and $375 million in milestone payments remain unchanged. Even in the downside scenario discussed above, the future value of the consideration offered to Valtech exceeds $900 million in cash and stock – an amount greater than the Company’s current market capitalization.

Additionally, as we have stated previously, we believe the ultimate destination of the Company’s VAD portfolio is in the hands of a larger medical device manufacturer. It is evident to us that the potential acquirers of HeartWare are very familiar with the Company, and would be able to move quickly to evaluate acquiring it should the opportunity present itself, now or in the future.

13 See Exhibit 1 to DFAN on Schedule 14A filed by Engaged Capital on January 7, 2016 for calculation

13

Using the valuation multiple Thoratec commanded in its sale to St. Jude Medical Inc., the value of the Company’s long-term plan in an acquisition is $178 per share at the end of 2019 – a 290% increase from today14 However, for the reasons discussed above, should the Company complete the Acquisition of Valtech, we believe a sale to a strategic acquirer will become unlikely and stockholders will be left to wonder what could have been.

Engaged Capital urges you to vote against the Transactions Proposal by signing, dating and returning the enclosed WHITE proxy card as soon as possible.

14

CONSEQUENCES OF DEFEATING THE TRANSACTIONS PROPOSAL

As more fully described in the Company’s Proxy Statement, Valtech and HeartWare may each terminate the Business Combination Agreement under certain circumstances. In the event the Business Combination Agreement is terminated in accordance with the termination provisions of the Business Combination Agreement, HeartWare would be obligated to make a loan to Valtech in a principal amount equal to $30,000,000 pursuant to a convertible promissory note as Valtech’s sole and exclusive remedy under the Business Combination Agreement.

15

VOTING AND PROXY PROCEDURES

Only stockholders of record on the Record Date will be entitled to notice of and to vote at the Special Meeting. Each Share is entitled to one vote. Stockholders who sell Shares before the Record Date (or acquire them without voting rights after the Record Date) may not vote such Shares. Stockholders of record on the Record Date will retain their voting rights in connection with the Special Meeting even if they sell such Shares after the Record Date. Based on publicly available information, Engaged Capital believes that the only outstanding class of securities of HeartWare entitled to vote at the Special Meeting is the Shares.

Shares represented by properly executed WHITE proxy cards will be voted at the Special Meeting as marked and, in the absence of specific instructions, will be voted AGAINST the adoption of the Business Combination Agreement and in the discretion of the persons named as proxies on all other matters as may properly come before the Special Meeting.

QUORUM; BROKER NON-VOTES; DISCRETIONARY VOTING

A quorum is the minimum number of Shares that must be represented at a duly called meeting in person or by proxy in order to legally conduct business at the meeting. For the Special Meeting, the presence, in person or by proxy, of the holders of at least _______ Shares, which represents a majority of the _________ Shares outstanding as of the Record Date, will be considered a quorum allowing votes to be taken and counted for the matters before the stockholders.

Abstentions will be counted for purposes of determining a quorum. Shares represented by “broker non-votes” will not be counted for purposes of determining the presence of a quorum unless the broker has been instructed to vote on at least one of the proposals to be presented at the Special Meeting in this Proxy Statement. If you hold your Shares in street name and do not provide voting instructions to your broker, your Shares will not be voted on any proposal on which your broker does not have discretionary authority to vote (a “broker non-vote”). Your broker will not have discretionary authority to vote your Shares at the Special Meeting on any proposal.

VOTES REQUIRED FOR APPROVAL

Adoption of the Business Combination Agreement ─ Stockholders may vote “FOR” or “AGAINST” or may “ABSTAIN” from voting on the adoption of the Business Combination Agreement. The adoption of the Business Combination Agreement by the Company’s stockholders requires the affirmative vote of stockholders holding at least a majority of the outstanding Shares entitled to vote as of the close of business on the Record Date. As disclosed in the Company’s Proxy Statement, the failure to vote your Shares, abstentions and “broker non-votes” will have the same effect as a vote “AGAINST” the proposal to adopt the Business Combination Agreement.

To vote, please complete, sign, date and return the enclosed WHITE proxy card or, to appoint a proxy over the Internet or by telephone, follow the instructions provided herein. If you attend the Special Meeting and wish to vote in person, you may withdraw your proxy and vote in person. If your Shares are held in the name of your broker, bank or other nominee, you must obtain a proxy, executed in your favor, from the holder of record to be able to vote at the Special Meeting.

REVOCATION OF PROXIES

Stockholders of HeartWare may revoke their proxies at any time prior to exercise by attending the Special Meeting and voting in person (although attendance at the Special Meeting will not in and of itself constitute revocation of a proxy) or by delivering a written notice of revocation. The delivery of a subsequently dated proxy which is properly completed will constitute a revocation of any earlier proxy. The revocation may be delivered either to Engaged Capital in care of Morrow at the address set forth on the back cover of this Proxy Statement or to HeartWare at 500 Old Connecticut Path, Building A, Framingham, Massachusetts 01701, or any other address provided by HeartWare. Although a revocation is effective if delivered to HeartWare, Engaged Capital requests that either the original or photostatic copies of all revocations be mailed to Engaged Capital in care of Morrow at the address set forth on the back cover of this Proxy Statement so that Engaged Capital will be aware of all revocations and can more accurately determine if and when proxies have been received from the holders of record on the Record Date of a majority of the outstanding Shares. Additionally, Morrow may use this information to contact stockholders who have revoked their proxies in order to solicit later dated proxies against the Company’s proposals in connection with the Acquisition.

16

DISSENTERS’ RIGHT OF APPRAISAL

According to the Company’s Proxy Statement, under Delaware law, holders of Shares are not entitled to appraisal rights in connection with the matters to be acted on at the Special Meeting.

IF YOU WISH TO VOTE AGAINST THE TRANSACTIONS PROPOSAL, PLEASE SIGN, DATE AND RETURN PROMPTLY THE ENCLOSED WHITE PROXY CARD IN THE POSTAGE-PAID ENVELOPE PROVIDED.

17

SOLICITATION OF PROXIES

The solicitation of proxies pursuant to this Proxy Statement is being made by Engaged Capital. Proxies may be solicited by mail, facsimile, telephone, telegraph, Internet, in person and by advertisements.

Engaged Capital has entered into an agreement with Morrow for solicitation and advisory services in connection with this solicitation, for which Morrow will receive a fee not to exceed $[______], together with reimbursement for its reasonable out-of-pocket expenses. Morrow will solicit proxies from individuals, brokers, banks, bank nominees and other institutional holders. Engaged Capital has requested banks, brokerage houses and other custodians, nominees and fiduciaries to forward all solicitation materials to the beneficial owners of the Shares they hold of record. Engaged Capital will reimburse these record holders for their reasonable out-of-pocket expenses in so doing. It is anticipated that Morrow will employ approximately [___] persons to solicit HeartWare’s stockholders for the Special Meeting.

The entire expense of soliciting proxies is being borne by Engaged Capital. Costs of this solicitation of proxies are currently estimated to be approximately $[_________]. Engaged Capital estimates that through the date hereof, its expenses in connection with this solicitation are approximately $[___________].

If Engaged Capital is successful in its solicitation of proxies to defeat the Transactions Proposal at the Special Meeting, then it intends to seek reimbursement from the Company for its expenses incurred in connection therewith.

ADDITIONAL PARTICIPANT INFORMATION

The members of Engaged Capital and Messrs. Ward, McCormick and Springstubb are participants in this solicitation. The principal business of each of Engaged Capital Master I and Engaged Capital Master II is investing in securities. Each of Engaged Capital I and Engaged Capital Offshore is a private investment partnership that serves as a feeder fund of Engaged Capital Master I. Each of Engaged Capital II and Engaged Capital Offshore II is a private investment partnership that serves as a feeder fund of Engaged Capital Master II. Engaged Capital LLC is a registered investment advisor and serves as the investment advisor to each of Engaged Capital Master I, Engaged Capital Master II, Engaged Capital I, Engaged Capital Offshore, Engaged Capital II and Engaged Capital Offshore II. Engaged Holdings serves as the managing member of Engaged Capital LLC. Mr. Welling is the Founder and Chief Investment Officer of Engaged Capital LLC, the sole member of Engaged Holdings and a director of each of Engaged Capital Offshore and Engaged Capital Offshore II. Mr. Ward is the Chairman and Interim Chief Executive Officer of Cardiovascular Systems, Inc; he also serves as Managing Director of SightLine Partners, LLC. Mr. McCormick is the former Chief Financial Officer of Tornier N.V. Mr. Springstubb is a Senior Analyst at Engaged Capital LLC.

Engaged Capital has submitted a notice of the nomination of Messrs. Ward, McCormick and Springstubb for election as directors at the next annual meeting of stockholders of the Company.

The address of the principal office of each of Engaged Capital Master I, Engaged Capital Master II, Engaged Capital Offshore and Engaged Capital Offshore II is c/o Codan Trust Company (Cayman) Ltd., Cricket Square, Hutchins Drive, P.O. Box 2681, Grand Cayman KY1-1111, Cayman Islands. The address of the principal office of each of Engaged Capital I, Engaged Capital II, Engaged Capital LLC, Engaged Holdings and Messrs. Welling and Springstubb is 610 Newport Center Drive, Suite 250, Newport Beach, California 92660. The address of the principal office of Mr. Ward is c/o SightLine Partners, 8500 Normandale Lake Blvd., Suite 1070, Bloomington, Minnesota 55437. The address of the principal office of Mr. McCormick is 3016 137th Ave NE, Ham Lake, Minnesota 55304.

18

As of the date hereof, Engaged Capital Master I beneficially owned 71,800 Shares. As of the date hereof, Engaged Capital Master II beneficially owned 158,200 Shares. Engaged Capital I, as a feeder fund of Engaged Capital Master I, may be deemed the beneficial owner of the 71,800 Shares beneficially owned by Engaged Capital Master I. Engaged Capital Offshore, as a feeder fund of Engaged Capital Master I, may be deemed the beneficial owner of the 71,800 Shares beneficially owned by Engaged Capital Master I. Engaged Capital II, as a feeder fund of Engaged Capital Master II, may be deemed the beneficial owner of the 158,200 Shares beneficially owned by Engaged Capital Master II. Engaged Capital Offshore II, as a feeder fund of Engaged Capital Master II, may be deemed the beneficial owner of the 158,200 Shares beneficially owned by Engaged Capital Master II. Engaged Capital LLC, as the investment adviser to each of Engaged Capital Master I and Engaged Capital Master II, may be deemed to beneficially own the 230,000 Shares owned in the aggregate by Engaged Capital Master I and Engaged Capital Master II. Engaged Holdings, as the managing member of Engaged Capital LLC, may be deemed to beneficially own the 230,000 Shares owned in the aggregate by Engaged Capital Master I and Engaged Capital Master II. Mr. Welling, as the Founder and Chief Investment Officer of Engaged Capital LLC and the sole member of Engaged Holdings, may be deemed to beneficially own the 230,000 Shares owned in the aggregate by Engaged Capital Master I and Engaged Capital Master II. As of the date hereof, Messrs. Ward, McCormick and Springstubb do not beneficially own any Shares.

Each participant in this solicitation is a member of a “group” (the “Group”) with the other participants for the purposes of Section 13(d)(3) of the Exchange Act. The Group may be deemed to beneficially own the 230,000 Shares owned in the aggregate by all of the participants in this solicitation. Each participant in this solicitation disclaims beneficial ownership of the Shares he or it does not directly own. The Shares directly owned by each of Engaged Capital Master I and Engaged Capital Master II were purchased with working capital (which may, at any given time, include margin loans made by brokerage firms in the ordinary course of business).

Except as set forth in this Proxy Statement, no participant in this solicitation has a substantial interest, direct or indirect, by security holdings or otherwise, in any matter to be acted on at the Special Meeting.

19

INFORMATION REGARDING HEARTWARE AND THE PROPOSED TRANSACTIONS

According to the Company’s Proxy Statement, HeartWare is a Delaware corporation with its principal executive office located at 500 Old Connecticut Path, Building A, Framingham, Massachusetts 01701; Telephone No. (508) 739-0950.

HeartWare is subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and in accordance therewith is required to file reports, proxy statements and other information with the SEC. Reports, registration statements, proxy statements and other information filed by HeartWare with the SEC, including the Company’s Proxy Statement, are publicly available at the SEC website: www.sec.gov.

We note that the Company’s Proxy Statement contains information regarding:

| · | the terms of the Business Combination Agreement and the Transactions; |

| · | any reports, opinions and/or appraisals received by HeartWare in connection with the Transactions; |

| · | past contacts, transactions and negotiations by and among the parties to the Transactions and their respective affiliates and advisors; |

| · | federal and state regulatory requirements that must be complied with and approvals that must be obtained in connection with the Transactions; |

| · | the voting agreement by and among Holdco and certain officers, directors and stockholders of Valtech; |

| · | security ownership of certain beneficial owners and management of the Company, including 5% owners; |

| · | the number of Shares outstanding as of the Record Date; |

| · | the establishment of a quorum; |

| · | the vote required for approval; |

| · | the treatment of abstentions and “broker non-votes;” |

| · | the trading prices of HeartWare Shares over time; |

| · | the availability of appraisal rights to the Company’s stockholders; and |

| · | the Company, Valtech and Holdco. |

STOCKHOLDER PROPOSALS

The Company’s Proxy Statement is silent with respect to the Company’s 2016 Annual Meeting of Stockholders (the “2016 Annual Meeting”).

20

If the 2016 Annual Meeting is held, proposals of stockholders intended to be presented at the 2016 Annual Meeting must, in order to be included in the Company’s proxy statement and the form of proxy for the 2016 Annual Meeting, have been delivered to the Company’s Corporate Secretary at 500 Old Connecticut Path, Building A, Framingham, Massachusetts 01701 by January 1, 2016.

Under the Company’s Bylaws, any stockholder intending to present any proposal (other than a proposal made by, or at the direction of, the Board) at the 2016 Annual Meeting, must give written notice of that proposal to the Company’s Secretary not less than 120 days prior to the first anniversary of the date the proxy statement for the preceding year’s annual meeting was released to stockholders (subject to certain exceptions if the annual meeting is advanced a certain number of days). Therefore, to be presented at the 2016 Annual Meeting, such a proposal must have been given on or before January 1, 2016.

The information set forth above regarding the procedures for submitting stockholder proposals for consideration at the 2016 Annual Meeting is based on information contained in the public filings. The incorporation of this information in this Proxy Statement should not be construed as an admission by Engaged Capital that such procedures are legal, valid or binding.

OTHER MATTERS AND ADDITIONAL INFORMATION

Engaged Capital is unaware of any other matters to be considered at the Special Meeting. However, should other matters, which Engaged Capital is not aware of a reasonable time before this solicitation, be brought before the Special Meeting, the persons named as proxies on the enclosed WHITE proxy card will vote on such matters in their discretion.

Engaged Capital has omitted from this Proxy Statement certain disclosure required by applicable law that is already included in the Company’s Proxy Statement. This disclosure includes, among other things, detailed information relating to the background, reasons for, terms and consequences of the Transactions, including risk factors, financial and pro forma information, tax consequences, accounting treatment, description of business conducted by HeartWare, description and share price information of the Shares, and interest of officers and directors of HeartWare in the Transactions.

See Schedule I for information regarding persons who beneficially own more than 5% of the Shares and the ownership of the Shares by the management and directors of HeartWare.

The information concerning HeartWare contained in this Proxy Statement and the Schedule attached hereto has been taken from, or is based upon, publicly available information.

ENGAGED CAPIAL, LLC

[____________], 2016

21

SCHEDULE I

The following table is reprinted from the Company’s definitive proxy statement on filed with the Securities and Exchange Commission on _______, 2016.

IMPORTANT

Tell your Board what you think! Your vote is important. No matter how many Shares you own, please give Engaged Capital your proxy AGAINST the Transactions Proposal by taking three steps:

| ● | SIGNING the enclosed WHITE proxy card, |

| ● | DATING the enclosed WHITE proxy card, and |

| ● | MAILING the enclosed WHITE proxy card TODAY in the envelope provided (no postage is required if mailed in the United States). |

If any of your Shares are held in the name of a brokerage firm, bank, bank nominee or other institution, only it can vote such Shares and only upon receipt of your specific instructions. Accordingly, please contact the person responsible for your account and instruct that person to execute the WHITE proxy card representing your Shares. Engaged Capital urges you to confirm in writing your instructions to Engaged Capital in care of Morrow at the address provided below so that Engaged Capital will be aware of all instructions given and can attempt to ensure that such instructions are followed.

If you have any questions or require any additional information concerning this Proxy Statement, please contact Morrow at the address set forth below.

MORROW & CO., LLC 470 West Avenue Stamford, CT 06902 Call Toll Free: (800) 662-5200 Call Direct: (203) 658-9400 Email: engaged@morrowco.com |

WHITE PROXY CARD

PRELIMINARY COPY SUBJECT TO COMPLETION

DATED JANUARY 7, 2016

HEARTWARE INTERNATIONAL, INC.

SPECIAL MEETING OF STOCKHOLDERS

THIS PROXY IS SOLICITED ON BEHALF OF

ENGAGED CAPIAL, LLC

THE BOARD OF DIRECTORS OF

HEARTWARE INTERNATIONAL, INC.

IS NOT SOLICITING THIS PROXY

P R O X Y

The undersigned appoints Glenn W. Welling and Steve Wolosky, and each of them, attorneys and agents with full power of substitution to vote all shares of common stock of HeartWare International, Inc. (“HeartWare” or the “Company”) which the undersigned would be entitled to vote if personally present at the Special Meeting of Stockholders of the Company, and including at any adjournments or postponements thereof and at any meeting called in lieu thereof (the “Special Meeting”).

The undersigned hereby revokes any other proxy or proxies heretofore given to vote or act with respect to the shares of common stock of the Company held by the undersigned, and hereby ratifies and confirms all action the herein named attorneys and proxies, their substitutes, or any of them may lawfully take by virtue hereof. If properly executed, this Proxy will be voted as directed on the reverse and in their discretion with respect to any other matters as may properly come before the Special Meeting that are unknown to Engaged Capital, LLC (“Engaged Capital”) a reasonable time before this solicitation.

IF NO DIRECTION IS INDICATED WITH RESPECT TO THE PROPOSAL ON THE REVERSE, THIS PROXY WILL BE VOTED AGAINST PROPOSAL 1.

This Proxy will be valid until the sooner of one year from the date indicated on the reverse side and the completion of the Special Meeting.

IMPORTANT: PLEASE SIGN, DATE AND MAIL THIS PROXY CARD PROMPTLY!

CONTINUED AND TO BE SIGNED ON REVERSE SIDE

[X] Please mark vote as in this example

| 1. | The Company’s proposal to adopt the Business Combination Agreement, dated September 1, 2015, by and among HeartWare, Valtech Cardio, Ltd. (“Valtech”), HW Global, Inc. (“Holdco”), HW Merger Sub, Inc. (“U.S. Merger Sub”), Valor Merger Sub Ltd. (“ISR Merger Sub”) and Valor Shareholder Representative, LLC, and approve the transactions contemplated thereby, including, without limitation, (a) the merger of U.S. Merger Sub with and into HeartWare, with HeartWare surviving the merger as a wholly owned subsidiary of Holdco, (b) the merger of ISR Merger Sub with and into Valtech, with Valtech surviving the merger as a subsidiary of Holdco and (c) the other transactions contemplated thereby. |

¨ FOR | ¨ AGAINST | ¨ ABSTAIN |

Engaged Capital recommends a vote “AGAINST” Proposal 1.

IN THEIR DISCRETION, THE PROXIES ARE AUTHORIZED TO VOTE UPON SUCH OTHER MATTERS AS MAY PROPERLY COME BEFORE THE SPECIAL MEETING.

DATED: ____________________________

____________________________________

(Signature)

____________________________________

(Signature, if held jointly)

____________________________________

(Title)

WHEN SHARES ARE HELD JOINTLY, JOINT OWNERS SHOULD EACH SIGN. EXECUTORS, ADMINISTRATORS, TRUSTEES, ETC., SHOULD INDICATE THE CAPACITY IN WHICH SIGNING. PLEASE SIGN EXACTLY AS NAME APPEARS ON THIS PROXY.