Filed pursuant to Rule 424(b)(3)

Registration Statement No. 333-164629

THE FRONTIER FUND

(a Delaware statutory trust)

Supplement

dated January 31, 2012 to the

Prospectus

and Disclosure Document

dated April 30, 2011

THE FRONTIER FUND

FRONTIER DIVERSIFIED SERIES; FRONTIER DYNAMIC SERIES; FRONTIER

LONG/SHORT COMMODITY SERIES; FRONTIER MASTERS SERIES

Supplement dated January 31, 2012 to the Prospectus and Disclosure Document Dated as of April 30, 2011

The following information amends the disclosure in the Prospectus and Disclosure Document dated as of April 30, 2011 (the “Prospectus”). If any statement in this supplement conflicts with a statement in the Prospectus, the statement in this supplement controls.

Closing of the Dynamic Series

On July 15, 2011, Equinox Fund Management, LLC, the managing owner of the Frontier Dynamic Series of The Frontier Fund (the “Dynamic Series”), announced that the Dynamic Series would be closed to outside investors. In addition, all existing outside investors as of July 15, 2011 were redeemed at that date’s net asset value per unit. Accordingly, all references to the Dynamic Series in the Prospectus and the Statement of Additional Information are hereby deleted in their entirety. This change does not affect any other series of The Frontier Fund.

The Trust and Managing Owner

The fifth sentence included in the paragraph entitled “The Trust and Managing Owner” on the cover page of the Prospectus is hereby deleted in its entirety and replaced with the following:

“As of October 31, 2011, the net asset value per unit was: Frontier Diversified Series: $97.72 (Class 1), $101.91 (Class 2); Frontier Masters Series: $98.25 (Class 1), $102.45 (Class 2); and Frontier Long/Short Commodity Series: $122.61 (Class 1a), $127.80 (Class 2a).”

SUMMARY

The Units

The fifth paragraph under the heading “SUMMARY—The Units” is hereby deleted in its entirety and replaced with the following:

“The percent return (and associated dollar amount) that your investment must earn in the indicated series, after taking into account estimated interest income, in order to break-even after one year is as follows (please see the “Break-Even Analysis” on page 16): Frontier Diversified Series: Class 1 – 5.31% ($53.10); Class 2 – 2.98% ($29.80); Class 3 – 2.73% ($27.30); Frontier Masters Series: Class 1 – 6.27% ($62.70); Class 2 – 4.08% ($40.80); Class 3 – 3.83% ($38.30); and Frontier Long/Short Commodity Series: Class 1a – 6.13% ($61.30); Class 2a – 3.94% ($39.40); Class 3a – 3.69% ($36.90).”

2

BREAK-EVEN ANALYSIS

The tables included under the heading “BREAK-EVEN ANALYSIS” are hereby deleted and replaced in their entirety with the following:

FRONTIER DIVERSIFIED SERIES

| Class 1 | Class 2 | Class 3(8) | ||||||||||||||||||||||

| $ | % | $ | % | $ | % | |||||||||||||||||||

Management Fee(1) | 7.50 | 0.75 | 7.50 | 0.75 | 7.50 | 0.75 | ||||||||||||||||||

Service Fee(2) | 20.00 | 2.00 | 2.50 | 0.25 | 0.00 | 0.00 | ||||||||||||||||||

Brokerage Commissions and Investment and Trading Fees and Expenses(3, 9) | 34.50 | 3.45 | 34.50 | 3.45 | 34.50 | 3.45 | ||||||||||||||||||

Incentive Fee(4) | 6.80 | 0.68 | 1.10 | 0.11 | 1.10 | 0.11 | ||||||||||||||||||

Less Interest income (5, 9) | (17.00 | ) | (1.70 | ) | (17.00 | ) | (1.70 | ) | (17.00 | ) | (1.70 | ) | ||||||||||||

Due Diligence and Custodial Fees and Expenses(6, 9) | 1.20 | 0.12 | 1.20 | 0.12 | 1.20 | 0.12 | ||||||||||||||||||

Redemption Fee(7) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||||||||

Trading profit the series must earn for you to recoup your investment after one year | 53.10 | 5.31 | 29.80 | 2.98 | 27.30 | 2.73 | ||||||||||||||||||

FRONTIER MASTERS SERIES

| Class 1 | Class 2 | Class 3(8) | ||||||||||||||||||||||

| $ | % | $ | % | $ | % | |||||||||||||||||||

Management Fee(1) | 20.00 | 2.00 | 20.00 | 2.00 | 20.00 | 2.00 | ||||||||||||||||||

Service Fee(2) | 20.00 | 2.00 | 2.50 | 0.25 | 0.00 | 0.00 | ||||||||||||||||||

Brokerage Commissions and Investment and Trading Fees and Expenses(3, 9) | 33.30 | 3.33 | 33.30 | 3.33 | 33.30 | 3.33 | ||||||||||||||||||

Incentive Fee(4) | 5.20 | 0.52 | 0.80 | 0.08 | 0.80 | 0.08 | ||||||||||||||||||

Less Interest income (5, 9) | (17.00 | ) | (1.70 | ) | (17.00 | ) | (1.70 | ) | (17.00 | ) | (1.70 | ) | ||||||||||||

Due Diligence and Custodial Fees and Expenses(6, 9) | 1.20 | 0.12 | 1.20 | 0.12 | 1.20 | 0.12 | ||||||||||||||||||

Redemption Fee(7) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||||||||

Trading profit the series must earn for you to recoup your investment after one year | 62.70 | 6.27 | 40.80 | 4.08 | 38.30 | 3.83 | ||||||||||||||||||

FRONTIER LONG/SHORT COMMODITY SERIES

| Class 1a | Class 2a | Class 3a(8) | ||||||||||||||||||||||

| $ | % | $ | % | $ | % | |||||||||||||||||||

Management Fee(1) | 20.00 | 2.00 | 20.00 | 2.00 | 20.00 | 2.00 | ||||||||||||||||||

Service Fee(2) | 20.00 | 2.00 | 2.50 | 0.25 | 0.00 | 0.00 | ||||||||||||||||||

Brokerage Commissions and Investment and Trading Fees and Expenses(3, 9) | 31.90 | 3.19 | 31.90 | 3.19 | 31.90 | 3.19 | ||||||||||||||||||

Incentive Fee(4) | 5.20 | 0.52 | 0.80 | 0.08 | 0.80 | 0.08 | ||||||||||||||||||

Less Interest income (5, 9) | (17.00 | ) | (1.70 | ) | (17.00 | ) | (1.70 | ) | (17.00 | ) | (1.70 | ) | ||||||||||||

Due Diligence and Custodial Fees and Expenses(6, 9) | 1.20 | 0.12 | 1.20 | 0.12 | 1.20 | 0.12 | ||||||||||||||||||

Redemption Fee(7) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||||||||

Trading profit the series must earn for you to recoup your investment after one year | 61.30 | 6.13 | 39.40 | 3.94 | 36.90 | 3.69 | ||||||||||||||||||

3

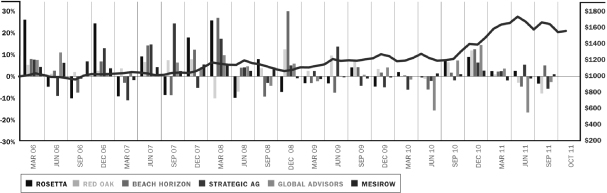

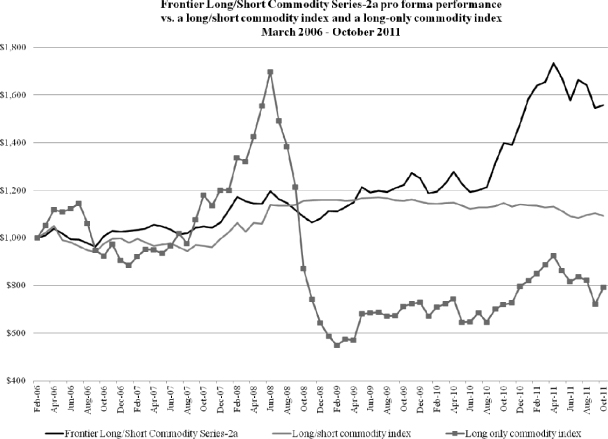

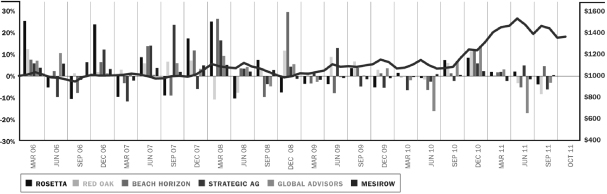

PAST PERFORMANCE OF THE SERIES

The text, table and footnotes included under the heading “PAST PERFORMANCE OF THE SERIES” are deleted in their entirety and replaced with the following:

PAST PERFORMANCE OF THE SERIES

Set forth in Capsules I-III below is the performance record of trading of each currently offered series of the trust from its inception through October 31, 2011.

CAPSULE I | ||||

Series | Frontier Diversified Series Class 1 | Frontier Diversified Series Class 2 | ||

Type of pool | Publicly-Offered; Multi-Advisor; Not Principal-Protected | Publicly-Offered; Multi-Advisor; Not Principal-Protected | ||

Inception of trading | June 9, 2009 | June 9, 2009 | ||

Aggregate subscriptions(1) | $114,796,843.09 | $83,229,109.40 | ||

Current capitalization(1) | $70,380,195.80 | $60,813,389.11 | ||

Worst monthly % drawdown since inception(1)(2) | -3.98% (Jan 2010) | -3.85% (Jan 2010) | ||

Worst month-end peak-to-valley drawdown since inception(1)(3) | -9.82% (Feb 2011 to Aug 2011) | -9.02% (Feb 2011 to Aug 2011) | ||

Monthly performance | ||||

| Month | 2011 | 2010 | 2009 | 2011 | 2010 | 2009 | ||||||||||||||||||

January | 3.53 | % | -3.98 | % | — | 3.69 | % | -3.85 | % | — | ||||||||||||||

February | 0.28 | % | 0.45 | % | — | 0.41 | % | 0.58 | % | — | ||||||||||||||

March | -0.91 | % | 2.28 | % | — | -0.76 | % | 2.44 | % | — | ||||||||||||||

April | 0.56 | % | 2.20 | % | — | 0.70 | % | 2.35 | % | — | ||||||||||||||

May | -2.48 | % | -0.05 | % | — | -2.34 | % | 0.08 | % | — | ||||||||||||||

June | -2.75 | % | -0.03 | % | -1.89 | % | -2.60 | % | 0.12 | % | -1.79 | % | ||||||||||||

July | -0.83 | % | -2.02 | % | -0.74 | % | -0.69 | % | -1.88 | % | -0.59 | % | ||||||||||||

August | -3.78 | % | 4.09 | % | 0.31 | % | -3.63 | % | 4.25 | % | 0.46 | % | ||||||||||||

September | 3.60 | % | 1.25 | % | 1.29 | % | 3.75 | % | 1.40 | % | 1.45 | % | ||||||||||||

October | -2.74 | % | 4.13 | % | 0.08 | % | -2.59 | % | 4.27 | % | 0.22 | % | ||||||||||||

November | -3.76 | % | 1.41 | % | -3.61 | % | 1.57 | % | ||||||||||||||||

December | 2.65 | % | -3.61 | % | 2.81 | % | -3.47 | % | ||||||||||||||||

Year |

| -5.66 (10 months | % ) | 7.00 | % |

| -3.20 (7 months | % ) |

| -4.27 (10 months | % ) | 8.88 | % |

| -2.23 (7 months | % ) | ||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

4

CAPSULE II | ||||

Series | Frontier Masters Series Class 1 | Frontier Masters Series Class 2 | ||

Type of pool | Publicly-Offered; Multi-Advisor; Not Principal-Protected | Publicly-Offered; Multi-Advisor; Not Principal-Protected | ||

Inception of trading | June 9, 2009 | June 9, 2009 | ||

Aggregate subscriptions(1) | $49,931,647.35 | $27,632,383.58 | ||

Current capitalization(1) | $34,493,533.27 | $19,302,731.02 | ||

Worst monthly % drawdown since inception(1)(2) | -5.74% (Dec-2009) | -5.60% (Dec-2009) | ||

Worst month-end peak-to-valley drawdown since inception(1)(3) | -9.41% (Nov-2009 to Feb-2010) | -9.03% (Nov-2009 to Feb-2010) | ||

Monthly performance | ||||

| Month | 2011 | 2010 | 2009 | 2011 | 2010 | 2009 | ||||||||||||||||||

January | 1.20 | % | -3.54 | % | — | 1.36 | % | -3.40 | % | — | ||||||||||||||

February | 0.71 | % | -0.37 | % | — | 0.85 | % | -0.24 | % | — | ||||||||||||||

March | -1.75 | % | 4.32 | % | — | -1.60 | % | 4.48 | % | — | ||||||||||||||

April | 5.07 | % | 0.57 | % | — | 5.22 | % | 0.71 | % | — | ||||||||||||||

May | -4.88 | % | -1.46 | % | — | -4.74 | % | -1.33 | % | — | ||||||||||||||

June | -3.93 | % | -0.20 | % | -2.03 | % | -3.78 | % | -0.04 | % | -1.92 | % | ||||||||||||

July | 3.78 | % | -1.70 | % | -1.64 | % | 3.93 | % | -1.56 | % | -1.49 | % | ||||||||||||

August | 0.25 | % | 4.24 | % | -0.30 | % | 0.41 | % | 4.40 | % | -0.15 | % | ||||||||||||

September | -0.25 | % | 3.56 | % | 2.33 | % | -0.10 | % | 3.73 | % | 2.49 | % | ||||||||||||

October | -4.39 | % | 4.05 | % | -0.57 | % | -4.25 | % | 4.19 | % | -0.47 | % | ||||||||||||

November | -2.92 | % | 2.52 | % | -2.77 | % | 2.67 | % | ||||||||||||||||

December | 2.57 | % | -5.74 | % | 2.72 | % | -5.60 | % | ||||||||||||||||

Year |

| -4.58 (10 months | % ) | 9.00 | % |

| -5.54 (7 months | % ) |

| -3.17 (10 months | % ) | 10.94 | % |

| -4.63 (7 months | % ) | ||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

5

CAPSULE III | ||||

Series | Frontier Long/Short Commodity Series Class 1a | Frontier Long/Short Commodity Series Class 2a | ||

Type of pool | Publicly-Offered; Multi-Advisor; Not Principal-Protected | Publicly-Offered; Multi-Advisor; Not Principal-Protected | ||

Inception of trading | June 9, 2009 | June 9, 2009 | ||

Aggregate subscriptions(1) | $17,863,723.29 | $10,251,741.04 | ||

Current capitalization(1) | $17,309,701.40 | $10,202,399.11 | ||

Worst monthly % drawdown since inception(1)(2) | -6.10% (Sep-2011) | -5.96% (Sep-2011) | ||

Worst month-end peak-to-valley drawdown since inception(1)(3) | -11.61% (Apr-2011 to Sep-2011) | -10.95% (Apr-2011 to Sep-2011) | ||

Monthly performance | ||||

| Month | 2011 | 2010 | 2009 | 2011 | 2010 | 2009 | ||||||||||||||||||

January | 7.08 | % | -5.19 | % | — | 7.24 | % | -5.09 | % | — | ||||||||||||||

February | 3.29 | % | 0.54 | % | — | 3.43 | % | 0.67 | % | — | ||||||||||||||

March | 0.81 | % | 2.66 | % | — | 0.96 | % | 2.82 | % | — | ||||||||||||||

April | 4.65 | % | 3.87 | % | — | 4.80 | % | 4.02 | % | — | ||||||||||||||

May | -3.72 | % | -4.15 | % | — | -3.58 | % | -4.02 | % | — | ||||||||||||||

June | -5.85 | % | -2.83 | % | -2.47 | % | -5.71 | % | -2.67 | % | -2.36 | % | ||||||||||||

July | 5.37 | % | 0.43 | % | 0.52 | % | 5.51 | % | 0.57 | % | 0.64 | % | ||||||||||||

August | -1.44 | % | 0.94 | % | -0.59 | % | -1.28 | % | 1.09 | % | -0.45 | % | ||||||||||||

September | -6.10 | % | 8.03 | % | 1.14 | % | -5.96 | % | 8.18 | % | 1.29 | % | ||||||||||||

October | 0.77 | % | 6.43 | % | 1.00 | % | 0.92 | % | 6.58 | % | 1.17 | % | ||||||||||||

November | -0.74 | % | 3.92 | % | -0.59 | % | 4.07 | % | ||||||||||||||||

December | 6.12 | % | -1.90 | % | 6.28 | % | -1.77 | % | ||||||||||||||||

Year |

| 3.94 (10 months | % ) | 16.22 | % |

| 1.49 (7 months | % ) |

| 5.47 (10 months | % ) | 18.24 | % |

| 2.48 (7 months | % ) | ||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

| (1) | “Aggregate subscriptions,” “Current capitalization,” “Worst monthly % drawdown since inception,” “Worst month-end peak-to-valley drawdown since inception” and “Monthly Performance” are provided for each offered class of investors and include subscriptions and capitalization through October 31, 2011. |

| (2) | “Worst monthly % drawdown since inception” means losses experienced in the net asset value per unit over the specified period and is calculated by dividing the net change in the net asset value per unit by the beginning net asset value per unit for the relevant period. “Decline” is measured on the basis of monthly returns only, and does not reflect intra-month figures. |

| (3) | “Worst month-end peak-to-valley drawdown since inception” is the largest percentage decline in the net asset value per unit over the specified period. This need not be a continuous decline, but can be a series of positive and negative returns where the negative returns are larger than the positive ones. |

6

Performance Summary for Previously Offered Commodity Pools

The table and notes included under the heading “THE MANAGING OWNER—Performance Information—Non-Offered Series” is deleted in its entirety and replaced with the following:

THE FRONTIER FUND

CAPSULE SUMMARY OF PERFORMANCE INFORMATION REGARDING

PREVIOUSLY OFFERED COMMODITY POOLS

| CAPSULE I | CAPSULE II | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Series | Balanced Series Class 1 | Balanced Series Class 2 | Balanced Series Class 1A(1) | Balanced Series Class 2A(2) | Balanced Series Class 3A(3) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Type of pool |

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi- Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Inception of Trading(4) | September 24, 2004 | September 24, 2004 | May 1, 2006 | May 1, 2006 | 4-Jun-09 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Close Date(5) | N/A | N/A | N/A | N/A | N/A | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Aggregate Subscriptions(6) | $409,634,470.42 | $122,225,945.80 | $17,560,608.01 | $3,814,043.79 | $5,070,935.81 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Current Capitalization(7) | $186,658,249.31 | $62,025,396.84 | $3,218,625.87 | $2,771,947.60 | $2,664,919.33 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Monthly Decline-Last 5 Years(8) | -7.02% (July-2007) | -6.77% (July-2007) | -7.06% (July-2007) | -6.81% (July-2007) | -5.48% (August-2011) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Peak-to-Valley Drawdown-Last 5 Years(9) |

| -13.76% (April-2006 to August-2007) |

|

| -12.50% (June-2007 to August-2007) |

|

| -14.76% (April-2006 to August-2007) |

|

| -12.58% (June-2007 to August-2007) |

| | -11.41% (April-2011 to August-2011) | | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Month | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

January | 4.13 | % | -5.56 | % | 1.34 | % | -0.55 | % | 1.20 | % | 3.47 | % | 4.40 | % | -5.34 | % | 1.59 | % | -0.30 | % | 1.47 | % | 3.73 | % | 4.06 | % | -5.62 | % | 1.28 | % | -0.57 | % | 1.14 | % | 3.46 | % | 4.32 | % | -5.39 | % | 1.53 | % | -0.33 | % | 1.41 | % | 3.72 | % | 4.32 | % | -5.39 | % | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

February | 0.21 | % | 1.64 | % | 0.33 | % | 7.52 | % | -4.38 | % | -2.95 | % | 0.44 | % | 1.87 | % | 0.56 | % | 7.78 | % | -4.16 | % | -2.73 | % | 0.10 | % | 1.58 | % | 0.25 | % | 7.50 | % | -4.35 | % | -2.96 | % | 0.33 | % | 1.81 | % | 0.48 | % | 7.77 | % | -4.20 | % | -2.74 | % | 0.33 | % | 1.81 | % | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

March | -0.96 | % | 3.54 | % | -1.62 | % | -0.48 | % | -3.17 | % | 3.62 | % | -0.70 | % | 3.82 | % | -1.36 | % | -0.22 | % | -2.93 | % | 3.89 | % | -1.00 | % | 3.48 | % | -1.71 | % | -0.49 | % | -3.22 | % | 3.61 | % | -0.75 | % | 3.76 | % | -1.45 | % | -0.24 | % | -2.98 | % | 3.88 | % | -0.75 | % | 3.76 | % | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

April | 1.03 | % | 3.48 | % | -2.35 | % | 0.26 | % | 2.77 | % | 1.26 | % | 1.27 | % | 3.74 | % | -2.11 | % | 0.50 | % | 3.03 | % | 1.51 | % | 0.93 | % | 3.42 | % | -2.36 | % | 0.23 | % | 2.72 | % | 1.25 | % | 1.16 | % | 3.68 | % | -2.12 | % | 0.48 | % | 2.98 | % | 1.50 | % | 1.16 | % | 3.68 | % | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

May | -2.66 | % | -0.98 | % | 1.73 | % | 1.11 | % | 5.66 | % | -2.26 | % | -2.41 | % | -0.76 | % | 1.98 | % | 1.36 | % | 5.93 | % | -2.00 | % | -2.76 | % | -1.06 | % | 1.77 | % | 1.10 | % | 5.61 | % | -2.73 | % | -2.51 | % | -0.83 | % | 1.97 | % | 1.34 | % | 5.88 | % | -2.50 | % | -2.51 | % | -0.83 | % | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||

June | -2.73 | % | 0.15 | % | -2.67 | % | 5.50 | % | 0.59 | % | -1.77 | % | -2.48 | % | 0.42 | % | -2.41 | % | 5.81 | % | 0.82 | % | -1.53 | % | -2.86 | % | 0.07 | % | -2.71 | % | 5.53 | % | 0.55 | % | -1.82 | % | -2.61 | % | 0.34 | % | -2.46 | % | 5.79 | % | 0.78 | % | -1.58 | % | -2.61 | % | 0.34 | % | -2.64 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

July | -1.40 | % | -3.30 | % | -1.04 | % | -2.74 | % | -7.02 | % | -1.48 | % | -1.17 | % | -3.06 | % | -0.79 | % | -2.49 | % | -6.77 | % | -1.23 | % | -1.51 | % | -3.38 | % | -1.09 | % | -2.71 | % | -7.06 | % | -1.55 | % | -1.27 | % | -3.14 | % | -0.83 | % | -2.46 | % | -6.81 | % | -1.30 | % | -1.27 | % | -3.14 | % | -0.84 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

August | -5.60 | % | 6.28 | % | 0.22 | % | 0.15 | % | -6.37 | % | -0.85 | % | -5.34 | % | 6.56 | % | 0.48 | % | 0.39 | % | -6.15 | % | -0.59 | % | -5.74 | % | 6.17 | % | 0.16 | % | 0.15 | % | -6.42 | % | -0.88 | % | -5.48 | % | 6.45 | % | 0.42 | % | 0.38 | % | -6.19 | % | -0.63 | % | -5.48 | % | 6.45 | % | 0.43 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

September | 3.79 | % | 2.30 | % | 1.99 | % | 0.50 | % | 5.13 | % | -1.75 | % | 4.04 | % | 2.56 | % | 2.24 | % | 0.76 | % | 5.38 | % | -1.53 | % | 3.66 | % | 2.25 | % | 1.94 | % | 0.44 | % | 5.09 | % | -1.81 | % | 3.92 | % | 2.50 | % | 2.19 | % | 0.70 | % | 5.35 | % | -1.58 | % | 3.92 | % | 2.48 | % | 2.17 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

October | -2.96 | % | 4.63 | % | -0.82 | % | 4.13 | % | 3.04 | % | 0.22 | % | -2.71 | % | 4.88 | % | -0.58 | % | 4.39 | % | 3.32 | % | 0.49 | % | -3.06 | % | 4.47 | % | -0.88 | % | 4.12 | % | 3.01 | % | 0.17 | % | -2.82 | % | 4.72 | % | -0.63 | % | 4.39 | % | 3.28 | % | 0.43 | % | -2.82 | % | 4.72 | % | -0.63 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

November | -4.30 | % | 2.43 | % | 3.39 | % | -1.96 | % | 2.07 | % | -4.05 | % | 2.69 | % | 3.63 | % | -1.72 | % | 2.32 | % | -4.37 | % | 2.36 | % | 3.40 | % | -2.00 | % | 2.00 | % | -4.11 | % | 2.62 | % | 3.64 | % | -1.76 | % | 2.26 | % | 4.10 | % | 2.62 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

December | 3.67 | % | -4.71 | % | 2.85 | % | 0.54 | % | 2.71 | % | 33.94 | % | -4.46 | % | 3.13 | % | 0.80 | % | 2.95 | % | 3.60 | % | -4.78 | % | 2.90 | % | 0.51 | % | 2.67 | % | 3.86 | % | -4.54 | % | 3.18 | % | 0.77 | % | 2.91 | % | -3.86 | % | -4.54 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Year | -7.31 | % | 11.31 | % | -5.30 | % | 23.37 | % | -4.88 | % | 1.99 | % | -4.97 | % | 14.70 | % | -2.41 | % | 27.18 | % | -1.98 | % | 5.08 | % | -8.29 | % | 10.30 | % | -5.88 | % | 23.32 | % | -5.29 | % | 1.08 | % | -5.98 | % | 13.65 | % | -3.04 | % | 27.06 | % | -2.47 | % | 4.11 | % | -5.98 | % | 13.66 | % | -3.58 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

7

| CAPSULE III | CAPSULE IV | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Series | Berkeley/Graham/Tiverton Series Class 1(10) | Berkeley/Graham/Tiverton Series Class 2(11) | Currency Series Class 1 (12) | Currency Series Class 2(13) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Type of pool |

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Inception of Trading(4) | February 14, 2005 | February 14, 2005 | September 24, 2004 | September 24, 2004 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Close Date(5) | N/A | N/A | N/A | N/A | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Aggregate Subscriptions(6) | $93,674,486.01 | $15,537,186.54 | $16,166,751.73 | $6,318,254.17 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Current Capitalization(7) | $ 37,429,127.02 | $4,662,563.63 | $4,316,539.30 | $112,895.31 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Monthly Decline-Last 5 Years(8) | -8.59% (Jul-2007) | -8.34% (Jul-2007) | -7.24% (Sep-2008) | -6.99% (Sep-2008) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Peak-to-Valley Drawdown-Last 5 Years(9) | -18.02% (Feb-2011 to Oct-2011) | -16.35% (Feb-2011 to Oct-2011) | -35.09% (Mar-2008 to Oct-2011) | -27.72% (Mar-2008 to Oct-2011) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Month | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

January | 0.92 | % | -5.29 | % | 0.03 | % | 0.32 | % | 0.23 | % | 1.24 | % | 1.18 | % | -5.06 | % | 0.27 | % | 0.58 | % | 0.50 | % | 1.50 | % | -1.30 | % | -1.19 | % | -3.07 | % | -0.47 | % | 0.02 | % | 0.71 | % | -1.06 | % | -0.95 | % | -2.83 | % | -0.22 | % | 0.29 | % | 0.97 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

February | 2.34 | % | 0.65 | % | 0.35 | % | 4.10 | % | -5.80 | % | -1.21 | % | 2.58 | % | 0.88 | % | 0.58 | % | 4.34 | % | -5.59 | % | -1.00 | % | -1.96 | % | 0.57 | % | -0.51 | % | 3.10 | % | -2.46 | % | 0.14 | % | -1.73 | % | 0.80 | % | -0.28 | % | 3.34 | % | -2.24 | % | 0.37 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

March | -4.79 | % | 1.50 | % | -2.99 | % | 0.69 | % | -3.99 | % | 2.75 | % | -4.54 | % | 1.77 | % | -2.74 | % | 0.94 | % | -3.76 | % | 3.01 | % | -1.23 | % | 2.57 | % | -2.30 | % | 3.11 | % | -0.55 | % | -0.27 | % | -0.98 | % | 2.85 | % | -2.04 | % | 3.37 | % | -0.31 | % | -0.01 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

April | 4.01 | % | 1.08 | % | -2.93 | % | -2.44 | % | 4.25 | % | 1.11 | % | 4.26 | % | 1.33 | % | -2.69 | % | -2.20 | % | 4.51 | % | 1.33 | % | 2.28 | % | 0.10 | % | -2.73 | % | -2.78 | % | 3.41 | % | 0.01 | % | 2.52 | % | 0.34 | % | -2.49 | % | -2.54 | % | 3.67 | % | 0.24 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

May | -7.48 | % | -0.56 | % | 1.91 | % | 1.85 | % | 9.12 | % | -2.90 | % | -7.24 | % | -0.33 | % | 2.15 | % | 2.11 | % | 9.40 | % | -2.64 | % | -2.85 | % | 1.78 | % | 0.90 | % | 0.75 | % | 2.15 | % | -2.05 | % | -2.61 | % | 2.02 | % | 1.14 | % | 1.00 | % | 2.41 | % | -1.79 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

June | -3.56 | % | -0.98 | % | -4.18 | % | 4.52 | % | 4.86 | % | -0.80 | % | -3.32 | % | -0.71 | % | -3.93 | % | 4.79 | % | 5.11 | % | -0.55 | % | -0.48 | % | -1.21 | % | -1.32 | % | -0.38 | % | 1.57 | % | 0.76 | % | -0.23 | % | -0.94 | % | -1.05 | % | -0.13 | % | 1.81 | % | 1.01 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

July | 0.51 | % | -2.02 | % | 0.32 | % | -3.44 | % | -8.59 | % | -1.83 | % | 0.75 | % | -1.77 | % | 0.58 | % | -3.18 | % | -8.34 | % | -1.57 | % | -1.26 | % | 0.74 | % | -3.40 | % | 0.82 | % | -0.58 | % | -0.59 | % | -1.03 | % | 0.99 | % | -3.15 | % | 1.08 | % | -0.32 | % | -0.34 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

August | -1.77 | % | 4.24 | % | -0.23 | % | -0.50 | % | -5.19 | % | -2.08 | % | -1.50 | % | 4.52 | % | 0.02 | % | -0.26 | % | -4.96 | % | -1.81 | % | -3.31 | % | 0.14 | % | -3.31 | % | -1.53 | % | -1.95 | % | 2.03 | % | -3.05 | % | 0.41 | % | -3.07 | % | -1.29 | % | -1.70 | % | 2.29 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

September | -0.80 | % | 2.60 | % | 3.11 | % | 1.07 | % | 3.03 | % | -1.09 | % | -0.56 | % | 2.86 | % | 3.37 | % | 1.33 | % | 3.27 | % | -0.87 | % | 1.05 | % | 0.22 | % | 2.30 | % | -7.24 | % | 0.82 | % | -1.51 | % | 1.30 | % | 0.46 | % | 2.55 | % | -6.99 | % | 1.05 | % | -1.29 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

October | -5.26 | % | 4.01 | % | -1.25 | % | 6.84 | % | 5.60 | % | 1.20 | % | -5.02 | % | 4.26 | % | -1.01 | % | 7.09 | % | 5.90 | % | 1.48 | % | -4.13 | % | 0.27 | % | -2.77 | % | 1.41 | % | 2.15 | % | -0.13 | % | -3.89 | % | 0.51 | % | -2.53 | % | 1.67 | % | 2.42 | % | 0.14 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

November | -2.11 | % | 4.10 | % | 2.82 | % | -3.91 | % | 1.06 | % | -1.85 | % | 4.37 | % | 3.05 | % | -3.69 | % | 1.31 | % | -1.60 | % | -1.24 | % | -2.26 | % | -2.45 | % | 2.49 | % | -1.34 | % | -0.99 | % | -2.03 | % | -2.20 | % | 2.75 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

December | 2.72 | % | -3.32 | % | 3.24 | % | -2.56 | % | 4.91 | % | 2.99 | % | -3.07 | % | 3.51 | % | -2.31 | % | 5.16 | % | -0.93 | % | -3.14 | % | 1.39 | % | -2.37 | % | 2.05 | % | -0.67 | % | -2.90 | % | 1.67 | % | -2.12 | % | 2.29 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Year | -15.32 | % | 5.56 | % | -5.33 | % | 20.28 | % | -4.54 | % | 2.09 | % | -13.18 | % | 8.78 | % | -2.46 | % | 23.90 | % | -1.63 | % | 5.19 | % | -12.59 | % | 1.39 | % | -18.91 | % | -4.45 | % | -0.49 | % | 3.59 | % | -10.39 | % | 4.48 | % | -16.44 | % | -1.53 | % | 2.56 | % | 6.72 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

8

THE FRONTIER FUND

CAPSULE SUMMARY OF PERFORMANCE INFORMATION REGARDING

PREVIOUSLY OFFERED COMMODITY POOLS

| CAPSULE V | CAPSULE VI | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Series | Dunn Series Class 1 | Dunn Series Class 2 | Frontier Long/Short Commodity Series Class 1 | Frontier Long/Short Commodity Series Class 2 | Frontier Long/Short Commodity Series Class 3(3) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Type of pool |

| Closed; Multi-Advisor; Not Principal-Protected |

|

| Closed; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi- Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi- Advisor; Not Principal-Protected |

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Inception of Trading(4) | September 24, 2004 | September 24, 2004 | March 6, 2006 | March 6, 2006 | 1-Jun-09 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Close Date(5) | October 15, 2007(14) | October 15, 2007(14) | N/A | N/A | N/A | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Aggregate Subscriptions(6) | $278,793.00 | $2,151,563.86 | $73,164,273.65 | $14,933,869.84 | $36,968,750.71 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Current Capitalization(7) | $0.00 | $0.00 | $8,500,949.17 | $9,302,559.09 | $24,888,833.22 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Monthly Decline-Last 5 Years(8) | -24.96% (Aug-2007) | -24.76% (Aug-2007) | -6.48% (Sep-2011) | -6.25% (Sep-2011) | -6.25% (Sep-2011) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Peak-to-Valley Drawdown-Last 5 Years(9) | | -57.00% (Nov-2004 to Aug-2007) | | | -53.29% (Nov-2004 to Aug-2007) | | -12.31% (Apr-2011 to Sep-2011) | -11.20% (Apr-2011 to Sep-2011) | | -11.20% (Apr-2011 to Sep-2011) | | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Month | 2007 | 2006 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

January | -0.72 | % | -6.61 | % | -0.45 | % | -6.37 | % | 7.09 | % | -5.22 | % | 2.66 | % | 4.57 | % | 0.07 | % | -- | 7.36 | % | -5.00 | % | 2.91 | % | 4.84 | % | 0.33 | % | -- | 7.36 | % | -5.00 | % | — | |||||||||||||||||||||||||||||||||||||||||

February | -12.64 | % | -2.75 | % | -12.44 | % | -2.53 | % | 3.35 | % | 0.48 | % | -0.37 | % | 4.87 | % | 0.18 | % | -- | 3.59 | % | 0.71 | % | -0.14 | % | 5.13 | % | 0.41 | % | -- | 3.59 | % | 0.71 | % | — | |||||||||||||||||||||||||||||||||||||||||

March | -6.39 | % | 9.19 | % | -6.16 | % | 9.47 | % | 0.96 | % | 2.59 | % | 1.42 | % | -1.83 | % | 0.36 | % | 0.96 | % | 1.22 | % | 2.87 | % | 1.69 | % | -1.58 | % | 0.61 | % | 1.20 | % | 1.22 | % | 2.87 | % | — | |||||||||||||||||||||||||||||||||||||||

April | 3.13 | % | 10.42 | % | 3.39 | % | 10.67 | % | 5.03 | % | 3.81 | % | 1.53 | % | -1.05 | % | 1.24 | % | 2.40 | % | 5.28 | % | 4.07 | % | 1.79 | % | -0.81 | % | 1.50 | % | 2.63 | % | 5.28 | % | 4.07 | % | — | |||||||||||||||||||||||||||||||||||||||

May | 12.16 | % | -5.59 | % | 12.45 | % | -5.33 | % | -4.00 | % | -4.22 | % | 5.40 | % | -0.39 | % | -0.89 | % | -2.22 | % | -3.76 | % | -4.00 | % | 5.55 | % | -0.15 | % | -0.64 | % | -1.95 | % | -3.76 | % | -4.00 | % | — | |||||||||||||||||||||||||||||||||||||||

June | 6.82 | % | -5.82 | % | 7.08 | % | -5.59 | % | -6.04 | % | -2.97 | % | -2.03 | % | 4.54 | % | -1.38 | % | -2.52 | % | -5.80 | % | -2.70 | % | -1.77 | % | 4.81 | % | -1.14 | % | -2.28 | % | -5.80 | % | -2.70 | % | -1.78 | % | ||||||||||||||||||||||||||||||||||||||

July | -18.15 | % | -3.05 | % | -17.92 | % | -2.81 | % | 5.35 | % | 0.34 | % | 0.44 | % | -3.03 | % | -2.20 | % | -0.36 | % | 5.60 | % | 0.59 | % | 0.69 | % | -2.78 | % | -1.94 | % | -0.10 | % | 5.60 | % | 0.59 | % | 0.69 | % | ||||||||||||||||||||||||||||||||||||||

August | -24.96 | % | -2.05 | % | -24.76 | % | -1.80 | % | -1.33 | % | 0.86 | % | -0.58 | % | -1.65 | % | 0.28 | % | -1.83 | % | -1.06 | % | 1.12 | % | -0.32 | % | -1.42 | % | 0.53 | % | -1.58 | % | -1.06 | % | 1.12 | % | -0.32 | % | ||||||||||||||||||||||||||||||||||||||

September | 14.92 | % | -2.27 | % | 15.17 | % | -2.04 | % | -6.48 | % | 8.31 | % | 1.09 | % | -2.76 | % | 1.95 | % | -1.61 | % | -6.25 | % | 8.57 | % | 1.33 | % | -2.50 | % | 2.19 | % | -1.38 | % | -6.25 | % | 8.57 | % | 1.34 | % | ||||||||||||||||||||||||||||||||||||||

October | -3.21 | % | -3.14 | % | -3.08 | % | -2.88 | % | 0.66 | % | 6.79 | % | 1.18 | % | -2.82 | % | 0.38 | % | 4.44 | % | 0.92 | % | 7.04 | % | 1.43 | % | -2.57 | % | 0.65 | % | 4.70 | % | 0.92 | % | 7.04 | % | 1.43 | % | ||||||||||||||||||||||||||||||||||||||

November | 1.83 | % | 2.08 | % | -0.82 | % | 4.12 | % | -2.35 | % | -0.82 | % | 1.93 | % | -0.56 | % | 4.38 | % | -2.13 | % | -0.58 | % | 2.17 | % | -0.56 | % | 4.38 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

December | -0.61 | % | -0.37 | % | 6.61 | % | -2.01 | % | 1.34 | % | 1.95 | % | -0.52 | % | 6.88 | % | -1.76 | % | 1.62 | % | 2.21 | % | -0.28 | % | 6.88 | % | -1.76 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

Year | -34.47 | % | -11.42 | % | -28.81 | % | -8.74 | % | 3.60 | % | 16.66 | % | 13.33 | % | -1.06 | % | 1.04 | % | 0.44 | % | 6.22 | % | 20.21 | % | 16.67 | % | 1.95 | % | 4.13 | % | 2.93 | % | 6.22 | % | 20.21 | % | 3.90 | % | ||||||||||||||||||||||||||||||||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

9

THE FRONTIER FUND

CAPSULE SUMMARY OF PERFORMANCE INFORMATION REGARDING

PREVIOUSLY OFFERED COMMODITY POOLS

| CAPSULE VII | CAPSULE VIII | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Series | Long Only Commodity Series Class 1 | Long Only Commodity Series Class 2 | Long Only Commodity Series Class 3 | Managed Futures Index Series Class 1 | Managed Futures Index Series Class 2 | Managed Class 3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Type of pool | Closed to New Investment; Multi-Advisor; Not Principal-Protected | Closed to New Investment; Multi-Advisor; Not Principal-Protected | Closed to New Multi-Advisor; Not Principal- | Closed to New Investment; Multi-Advisor; Not Principal-Protected | Closed to New Investment; Multi-Advisor; Not Principal-Protected | Closed to New Multi-Advisor; Not Principal- | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Inception of Trading(4) | March 1, 2006 | March 1, 2006 | | January 13, 2011 | | April 25, 2006 | April 25, 2006 | | January 13, 2011 | | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Close Date(5) | N/A | N/A | N/A | N/A | N/A | N/A | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Aggregate Subscript- ions(6) | $8,587,366.70 | $1,612,568.43 | $1,613,778.39 | $3,197,156.50 | $2,283,718.00 | $371,832.66 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Current Capital- | $552,528.01 | $130,255.48 | $839,798.95 | $341,002.37 | $2,922,313.82 | $327,492.18 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Monthly Decline- | -24.11% (Oct-2008) | -23.97% (Oct-2008) | | -15.04% (Sep-2011) | | -11.71% (Oct-2011) | -11.56% (Oct-2011) | | -11.56% (Oct-2011) | | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Peak-to- | -55.54% (Jun-2008 to Feb-2009) | -54.96% (Jun-2008 to Feb-2009) | | -20.59% (Apr-2011 to Sep-2011) | | -21.36% (Dec-2008 to Jun-2011) | -17.38% (Dec-2008 to Jun-2011) | | -11.56% (Sep-2011 | | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Month | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

January | 1.47% | -6.38% | -5.86% | 3.19% | -1.79% | — | 1.64% | -6.24% | -5.70% | 3.36% | -1.61% | — | 1.48% | -1.45% | 1.24% | -1.55% | 5.61% | -0.07% | — | -1.29% | 1.40% | -1.38% | 5.79% | 0.12% | — | 1.02% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

February | 1.97% | 3.60% | -3.63% | 12.31% | 4.05% | — | 2.12% | 3.76% | -3.48% | 12.48% | 4.21% | — | 2.12% | 1.45% | -0.96% | -2.19% | 8.71% | -3.70% | — | 1.60% | -0.81% | -2.04% | 8.89% | -3.55% | — | 1.60% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

March | 2.28% | -1.07% | 3.53% | -4.76% | 1.36% | 3.82% | 2.45% | -0.89% | 3.71% | -4.60% | 1.53% | 4.06% | 2.45% | -4.61% | -1.15% | -2.84% | -3.77% | -3.28% | — | -4.44% | -0.97% | -2.68% | -3.60% | -3.12% | — | -4.44% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

April | 3.03% | 1.22% | 0.70% | 4.39% | -0.92% | 5.72% | 3.18% | 1.39% | 0.87% | 4.56% | -0.75% | 5.88% | 3.20% | 4.75% | -2.53% | -4.23% | -4.11% | 1.56% | 2.48% | 4.92% | -2.37% | -4.11% | -3.95% | 1.73% | 2.63% | 4.92% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

May | -5.21% | -8.28% | 13.48% | 2.31% | -1.12% | -0.60% | -5.05% | -8.13% | 13.66% | 2.48% | -0.95% | -0.42% | -5.04% | -6.68% | 4.79% | 4.15% | 0.17% | 1.61% | 1.51% | -6.52% | 4.95% | 4.32% | 0.34% | 1.79% | 1.69% | -6.52% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

June | -3.48% | 1.00% | -0.44% | 9.85% | 0.43% | 0.33% | -3.32% | 1.19% | -0.27% | 10.04% | 0.59% | 0.49% | -3.32% | -5.48% | 0.95% | -2.06% | 3.16% | 4.79% | -4.47% | -5.32% | 1.13% | -1.89% | 3.33% | 4.95% | -4.32% | -5.32% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

July | 1.58% | 6.32% | 2.14% | -9.60% | 2.83% | 2.87% | 1.74% | 6.50% | 2.31% | -9.43% | 3.01% | 3.04% | 1.74% | 2.09% | -5.08% | -0.45% | -7.22% | 0.83% | -3.29% | 2.25% | -4.92% | -0.28% | -7.04% | 1.01% | -3.13% | 2.25% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

August | -0.10% | -4.09% | -1.12% | -6.00% | -4.87% | -6.65% | 0.08% | -3.92% | -0.96% | -5.85% | -4.71% | -6.49% | 0.08% | 7.21% | 6.66% | -1.19% | 3.12% | -5.82% | 1.99% | 7.41% | 6.84% | -1.02% | 3.25% | -5.66% | 2.16% | 7.41% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

September | -15.18% | 8.02% | 4.25% | -11.13% | 8.21% | -8.82% | -15.04% | 8.20% | 4.42% | -10.98% | 8.37% | -8.68% | -15.04% | 7.94% | -1.61% | -0.93% | -2.46% | 4.73% | -2.96% | 8.12% | -1.45% | -0.76% | -2.36% | 4.89% | -2.81% | 8.12% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

October | 8.24% | 4.02% | 1.08% | -24.11% | 6.55% | 0.11% | 8.43% | 4.19% | 1.24% | -23.97% | 6.75% | 0.29% | 8.43% | -11.71% | 3.78% | -0.86% | 16.07% | 2.12% | -0.83% | -11.56% | 3.95% | -0.70% | 16.36% | 2.31% | -0.66% | -11.56% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

November | -0.07% | 2.19% | -8.51% | -4.37% | 5.15% | 0.10% | 2.37% | -8.38% | -4.21% | 5.33% | -6.14% | 1.41% | 8.46% | 2.52% | 1.66% | -5.97% | 1.58% | 8.35% | 2.69% | 1.83% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

December | 9.29% | 2.31% | -6.54% | 5.58% | -5.39% | 9.47% | 2.48% | -6.41% | 5.76% | -5.24% | 5.70% | -4.92% | 2.17% | -0.80% | 1.01% | 5.88% | -4.76% | 2.41% | -0.63% | 1.17% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Year | -7.07% | 12.59% | 18.88% | -36.54% | 16.07% | -4.55% | -5.51% | 14.86% | 21.27% | -35.28% | 18.43% | -2.89% | -5.66% | -8.08% | 4.82% | -14.86% | 31.40% | 3.98% | -3.15% | -6.54% | 6.94% | -13.19% | 33.79% | 6.09% | -1.69% | -4.35% | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

10

THE FRONTIER FUND

CAPSULE SUMMARY OF PERFORMANCE INFORMATION REGARDING

PREVIOUSLY OFFERED COMMODITY POOLS

| CAPSULE IX | CAPSULE X | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Series | Winton Series Class 1 | Winton Series Class 2 | Winton/Graham Series Class 1 (15) | Winton/Graham Series Class 2 (16) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Type of pool |

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

|

| Closed to New Investment; Multi-Advisor; Not Principal-Protected |

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Inception of Trading(4) | September 24, 2004 | September 24, 2004 | November 22, 2004 | November 22, 2004 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Close Date(5) | N/A | N/A | N/A | N/A | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Aggregate Subscriptions(6) | $63,261,450.81 | $9,975,096.5 | $58,480,838.79 | $18,621,556.33 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Current | $37,916,335.06 | $11,412,342.51 | $26,302,871.97 | $6,223,126.41 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Monthly Decline-Last 5 Years(8) | -7.75% (Feb-2007) | -7.53% (Feb-2007) | -7.00% (Jan-2010) | -6.78% (Jan-2010) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Worst Peak-to-Valley Drawdown-Last 5 Years(9) | -13.31% (Jan-2007 to Mar-2007) | -12.89% (Jan-2007 to Mar-2007) | -26.89% (Dec-2004 to Mar-2007) | -13.67% (Apr-2011 to Oct-2011) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Month | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | 2011 | 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

January | -0.16 | % | -3.27 | % | 0.39 | % | 2.96 | % | 4.12 | % | -- | 0.09 | % | -3.04 | % | 0.63 | % | 3.23 | % | 4.41 | % | -- | -0.45 | % | -7.00 | % | -0.10 | % | 1.42 | % | -1.37 | % | 0.67 | % | -0.19 | % | -6.78 | % | 0.14 | % | 1.68 | % | -1.10 | % | 0.93 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

February | 1.67 | % | 2.83 | % | -0.77 | % | 7.22 | % | -7.75 | % | -- | 1.91 | % | 3.06 | % | -0.54 | % | 7.48 | % | -7.53 | % | -- | 2.17 | % | 1.67 | % | 0.10 | % | 7.20 | % | -6.18 | % | -0.72 | % | 2.41 | % | 1.90 | % | 0.33 | % | 7.46 | % | -5.97 | % | -0.49 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

March | -0.49 | % | 5.48 | % | -1.90 | % | -0.86 | % | -6.03 | % | -- | -0.24 | % | 5.77 | % | -1.64 | % | -0.60 | % | -5.80 | % | -- | -2.63 | % | 5.20 | % | -2.63 | % | 2.46 | % | -3.38 | % | 1.44 | % | -2.39 | % | 5.48 | % | -2.37 | % | 2.73 | % | -3.14 | % | 1.70 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

April | 3.05 | % | 1.75 | % | -3.71 | % | -2.32 | % | 5.33 | % | -- | 3.29 | % | 2.00 | % | -3.47 | % | -2.08 | % | 5.60 | % | -- | 5.14 | % | 2.03 | % | -3.06 | % | -0.39 | % | 5.69 | % | 7.12 | % | 5.39 | % | 2.28 | % | -2.82 | % | -0.14 | % | 5.96 | % | 7.37 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

May | -2.61 | % | -0.99 | % | -2.60 | % | 0.72 | % | 4.43 | % | -- | -2.36 | % | -0.76 | % | -2.37 | % | 0.96 | % | 4.69 | % | -- | -5.03 | % | -0.75 | % | 0.53 | % | 2.72 | % | 14.51 | % | -3.37 | % | -4.79 | % | -0.53 | % | 0.77 | % | 2.97 | % | 14.80 | % | -3.11 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

June | -3.48 | % | 2.10 | % | -1.74 | % | 4.16 | % | 1.41 | % | -- | -3.24 | % | 2.37 | % | -1.48 | % | 4.43 | % | 1.65 | % | -- | -3.92 | % | -0.14 | % | -3.43 | % | 3.28 | % | 4.14 | % | -1.29 | % | -3.67 | % | 0.13 | % | -3.18 | % | 3.54 | % | 4.39 | % | -1.05 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

July | 5.60 | % | -4.19 | % | -2.01 | % | -4.33 | % | -1.90 | % | -- | 5.85 | % | -3.95 | % | -1.76 | % | -4.08 | % | -1.64 | % | -- | 4.52 | % | -3.16 | % | -0.16 | % | - 4.49 | % | - 4.25 | % | - 3.18 | % | 4.77 | % | -2.93 | % | 0.10 | % | -4.25 | % | -4.00 | % | -2.93 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||

August | 1.86 | % | 6.64 | % | -0.04 | % | -2.58 | % | -1.55 | % | 2.57 | % | 2.13 | % | 6.92 | % | 0.21 | % | -2.34 | % | -1.30 | % | 2.72 | % | -2.55 | % | 5.70 | % | 0.69 | % | -2.75 | % | - 3.45 | % | - 3.73 | % | -2.29 | % | 5.98 | % | 0.95 | % | -2.52 | % | -3.21 | % | -3.49 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

September | -0.04 | % | 0.53 | % | 2.69 | % | -1.03 | % | 6.71 | % | -2.20 | % | 0.21 | % | 0.78 | % | 2.94 | % | -0.77 | % | 6.96 | % | -1.99 | % | -2.29 | % | 0.52 | % | 3.67 | % | 0.37 | % | 4.93 | % | 0.69 | % | -2.05 | % | 0.77 | % | 3.93 | % | 0.64 | % | 5.18 | % | 0.92 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

October | -2.89 | % | 2.86 | % | -2.17 | % | 3.09 | % | 1.84 | % | 1.24 | % | -2.65 | % | 3.11 | % | -1.92 | % | 3.36 | % | 2.12 | % | 1.50 | % | -6.37 | % | 5.03 | % | -2.88 | % | 5.78 | % | 5.19 | % | 1.29 | % | -6.14 | % | 5.28 | % | -2.64 | % | 6.05 | % | 5.47 | % | 1.56 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

November | -3.00 | % | 6.05 | % | 5.17 | % | 1.98 | % | 2.25 | % | -2.74 | % | 6.32 | % | 5.41 | % | 2.24 | % | 2.50 | % | -3.54 | % | 6.77 | % | 3.81 | % | 0.44 | % | 1.74 | % | -3.29 | % | 7.04 | % | 4.05 | % | 0.68 | % | 1.99 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

December | 3.86 | % | -4.07 | % | 2.13 | % | -0.03 | % | 1.73 | % | 4.12 | % | -3.82 | % | 2.41 | % | 0.23 | % | 1.97 | % | 3.84 | % | -4.33 | % | 1.44 | % | -2.84 | % | 1.98 | % | 4.10 | % | -4.08 | % | 1.72 | % | -2.59 | % | 2.23 | % | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Year | 2.16 | % | 14.86 | % | -9.84 | % | 14.56 | % | 7.74 | % | 5.64 | % | 4.74 | % | 18.36 | % | -7.10 | % | 18.07 | % | 11.05 | % | 6.81 | % | -11.47 | % | 8.88 | % | -5.27 | % | 22.25 | % | 12.21 | % | 2.17 | % | -9.23 | % | 12.19 | % | -2.35 | % | 26.00 | % | 15.63 | % | 5.26 | % | ||||||||||||||||||||||||||||||||||||||||||||||||

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

11

THE FRONTIER FUND

CAPSULE SUMMARY OF PERFORMANCE INFORMATION REGARDING

PREVIOUSLY OFFERED COMMODITY POOLS

CAPSULE XI | ||||

Series | Frontier Dynamic Series Class 1 | Frontier Dynamic Series Class 2 | ||

Type of pool | Closed; Multi-Advisor; Not Principal-Protected | Closed; Multi-Advisor; Not Principal-Protected | ||

Inception of Trading(4) | June 9, 2009 | June 9, 2009 | ||

Close Date(5) | July 15, 2011(17) | July 15, 2011(17) | ||

Aggregate Subscriptions(6) | $1,627,010.21 | $451,893.90 | ||

Current Capitalization(7) | $0.00 | $0.00 | ||

Worst Monthly Decline- | -2.93% (Jun-2009) | -2.82% (Jun-2009) | ||

Worst Peak-to-Valley Drawdown-Last 5 Years(9) | -11.95% (May-2009 to Jul-2011) | -9.94% (May-2009 to Jul-2010) | ||

| Month | 2011 | 2010 | 2009 | 2011 | 2010 | 2009 | ||||||

| January | 0.59% | -1.18% | — | 0.74% | -1.04% | — | ||||||

| February | -0.37% | -0.05% | — | -0.24% | 0.09% | — | ||||||

| March | -2.63% | 0.34% | — | -2.48% | 0.50% | — | ||||||

| April | 1.49% | 0.01% | — | 1.63% | 0.15% | — | ||||||

| May | -2.04% | -1.09% | — | -1.89% | -0.95% | — | ||||||

| June | 1.17% | 0.17% | -2.93% | 1.32% | 0.33% | -2.82% | ||||||

| July | -2.43% | -1.60% | -0.16% | -2.36% | -1.46% | -0.01% | ||||||

| August | 1.76% | 0.55% | 1.91% | 0.70% | ||||||||

| September | 1.39% | -0.91% | 1.53% | -0.77% | ||||||||

| October | 1.22% | -0.49% | 1.36% | -0.43% | ||||||||

| November | -1.41% | -2.17% | -1.26% | -2.02% | ||||||||

| December | 1.06% | -2.74% | 1.21% | -2.59% | ||||||||

| Year | -4.23% | 0.56% | -8.57% | -3.32% | 2.33% | -7.75% |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

Footnotes to the Frontier Fund Capsule Summary of Performance Information Regarding Previously Offered Commodity Pools

| (1) | The Balanced Series Class 1A performance table sets forth the actual performance of the Balanced Series Class 1A since May 2006 and the pro forma performance of Balanced Series Class 1, adjusted to take into account the fees associated with an investment in Balanced Series Class 1A Units, from September 2004 to April 2006. |

| (2) | The Balanced Series Class 2A performance table sets forth the actual performance of the Balanced Series Class 2A since May 2006 and the pro forma performance of Balanced Series Class 2, adjusted to take into account the fees associated with an investment in Balanced Series Class 2A Units, from September 2004 to April 2006. |

| (3) | Units that have reached the compensation limitations as determined by the managing owner will be designated as class 3 (and in the case of the Frontier Long/Short Commodity Series, class 3a) units for reporting purposes and will not be subject to additional ongoing service fees. |

12

| (4) | “Inception of trading” is the month and year that the pool began trading. |

| (5) | “Close Date” is the month and year that the pool liquidated its assets and stopped doing business. |

| (6) | “Aggregate Subscriptions” is the aggregate of all amounts contributed to the class, including investments that were later redeemed by investors. |

| (7) | “Current Capitalization” is the net asset value of the class as of October 31, 2011, or, in the case of liquidated pools, the net asset value of the class on the Close Date. |

| (8) | “Worst Monthly % Decline-Last 5 Years” means losses experienced in the net asset value per unit over the specified period and is calculated by dividing the net change in the net asset value per unit by the beginning net asset value per unit for the relevant period. “Decline” is measured on the basis of monthly returns only, and does not reflect intra-month figures. |

| (9) | “Worst Peak-to-Valley Drawdown-Last 5 Years” is the largest percentage decline in the net asset value per unit over the specified period, although the peak may have occurred outside of the past five years and year-to-date. This need not be a continuous decline, but can be a series of positive and negative returns where the negative returns are larger than the positive ones. |

| (10) | Prior to June 2008, the Campbell/Graham/Tiverton Series Class 1 performance table sets forth the actual performance of the Campbell/Graham/Tiverton Series Class 1, during a period when it was directed only by Campbell and Graham. The Campbell/Graham/Tiverton Series was originally designated as the “Campbell/Graham Series,” and trading for the Series was directed by Campbell and Graham. |

| (11) | Prior to June 2008, the Campbell/Graham/Tiverton Series Class 2 performance table sets forth the actual performance of the Campbell/Graham/Tiverton Series Class 2, during a period when it was directed only by Campbell and Graham. The Campbell/Graham/Tiverton Series was originally designated as the “Campbell/Graham Series,” and trading for the Series was directed by Campbell and Graham. |

| (12) | The Currency Series Class 1 performance table sets forth the actual performance of the Currency Series Class 1. The Currency Series was originally a single-advisor Series designated as the “C-View Currency Series.” The past performance information presented in the composite performance table from inception through February 1, 2006, represents the past performance of the Currency Series Class 1 under C-View as the single advisor. |

| (13) | The Currency Series Class 2 performance table sets forth the actual performance of the Currency Series Class 2. The Currency Series was originally a single-advisor Series designated as the “C-View Currency Series.” The past performance information presented in the composite performance table from inception through February 1, 2006, represents the past performance of the Currency Series Class 1 under C-View as the single advisor. |

| (14) | Each of the Dunn Series Class 1 and Dunn Series Class 2 ceased trading on October 15, 2007 and had no net asset value as of any subsequent month-end. |

| (15) | Prior to June 2008, the Winton/Graham Series Class 1 performance table sets forth the actual performance of the Winton/Graham Series Class 1 during a period when it was directed solely by Graham. The Winton/Graham Series was originally designated as the “Graham Series,” and trading for the Series was directed by Graham. |

| (16) | Prior to June 2008, the Winton/Graham Series Class 2 performance table sets forth the actual performance of the Winton/Graham Series Class 2 during a period when it was directed solely by Graham. The Winton/Graham Series was originally designated as the “Graham Series,” and trading for the Series was directed by Graham. |

| (17) | Each of the Frontier Dynamic Series Class 1 and the Frontier Dynamic Series Class 2 ceased trading on July 15, 2011 and had no net asset value as of any subsequent month-end. |

13

CLEARING BROKERS

UBS Securities

The disclosure included under the heading “CLEARING BROKERS—UBS Securities” is hereby deleted in its entirety and replaced with the following:

UBS Securities

UBS Securities LLC (“UBS Securities”) principal business address is 677 Washington Blvd, Stamford, CT 06901. UBS Securities is a futures clearing broker for each trading company.UBS Securities is registered in the US with the Financial Industry Regulatory Authority (“FINRA”) as a Broker- Dealer and with the CFTC as a Futures Commission Merchant. UBS Securities is a member of various US futures and securities exchanges. UBS AG, the ultimate parent company to UBS Securities LLC, files annual reports and quarterly reports to the SEC in which it discloses material information about UBS matters, including information about any material litigation or regulatory investigations (http://www.ubs.com/1/e/investors/quarterly_reporting/2011.htm). Actions with respect to UBS Securities’ futures commission merchant business are publicly available on the website of the National Futures Association (http://www.nfa.futures.org/).

On April 29, 2010, the CFTC issued an order with respect to UBS Securities LLC and levied a fine of $200,000. The Order stated that on February 6, 2009, UBS Securities’ employee broker aided and abetted UBS Securities’ customer’s concealment of material facts from the New York Mercantile Exchange (“NYMEX”) in violation of Section 9(a)(4) of the CEA, 7 U.S.C. § 13(a)(4) (2006). Pursuant to NYMEX Rules, a block trade must be reported to NYMEX “within five minutes of the time of execution” consistent with the requirements of NYMEX Rule 6.21C(A)(6). Although the block trade in question was executed earlier in the day, UBS Securities’ employee broker allegedly aided and abetted its customer’s concealment of facts when, in response to the customer’s request to delay reporting the trade until after the close of trading, UBS Securities’ employee did not report the trade until after the close. The fine has been paid and the matter is now closed.

On August 14, 2008 the New Hampshire Bureau of Securities Regulation filed an administrative action against UBS Securities relating to a student loan issuer, the New Hampshire Higher Education Loan Corp. (NHHELCO). The complaint alleged fraudulent and unethical conduct in violation of New Hampshire state statues. On April 14, 2010, UBS entered into a Consent Order resolving all of the Bureau’s claims. UBS paid $750,000 to the Bureau for all costs associated with the Bureau’s investigation. UBS entered a separate civil settlement with NHHELCO and provided a total financial benefit of $20M to NHHELCO.

In the summer of 2008, the Massachusetts Securities Division, Texas State Securities Board, and the New York Attorney General all brought actions against UBS and UBS Financial Services, Inc. (“UBS Financial”), alleging violations of various state law anti-fraud provisions in connection with the marketing and sale of auction rate securities.

On August 8, 2008, UBS Securities and UBS Financial Services reached agreements with the SEC, the NYAG, the Massachusetts Securities Division and other state regulatory agencies represented by the North American Securities Administrators Association (“NASAA”) to restore liquidity to all remaining client’s holdings of auction rate securities by June 30, 2012. On October 2, 2008, UBS Securities and UBS Financial entered into a final consent agreement with the Massachusetts Securities Division settling all allegations in the Massachusetts Securities Division’s administrative proceeding against UBS Securities and UBS Financial with regards to the auction rate securities matter. On December 11, 2008, UBS Securities and UBS Financial executed an Assurance of Discontinuance in the auction rate securities settlement with the NYAG. On the same day, UBS Securities and UBS Financial finalized settlements with the SEC. UBS paid penalties of $75M to NYAG and an additional $75M to be apportioned among the participating NASAA states. In March 2010, UBS and NASAA agreed on final settlement terms, pursuant to which, UBS agreed to provide client liquidity up to an additional $200 million.

14

The Jerome F. Sheldon Trust, et al. v. UBS Securities LLC, et al. is one of a series of consolidated actions filed beginning in 2008 in the Superior Court of California, County of San Francisco relating to Solidus Networks, Inc., d/b/a Pay by Touch (“PBT”), for which UBS served as a placement agent in several offerings by PBT securities. Plaintiffs in the consolidated actions allege, among other things, that UBS and executives of PBT misrepresented the financial condition of PBT and failed to disclose certain legal difficulties of John Rogers (the initial founder and CEO of PBT) including alleged drug use. Plaintiffs’ complaint asserts that these alleged misrepresentations and omissions constituted fraud against certain investors in PBT and violated provisions of California securities law. Plaintiff claims $95 million in damages, plus interest and punitive damages. Trial is scheduled to begin the week of November 21, 2011.

On June 27, 2007, the Securities Division of the Secretary of the Commonwealth of Massachusetts (“Massachusetts Securities Division”) filed an administrative complaint (the “Complaint”) and notice of adjudicatory proceeding against UBS Securities LLC, captioned In The Matter of UBS Securities, LLC, Docket No. E-2007-0049, which alleged that UBS Securities violated the Massachusetts Uniform Securities Act (the “Act”) and related regulations by providing the advisers for certain hedge funds with gifts and gratuities in the form of below market office rents, personal loans with below market interest rates, event tickets, and other perks, in order to induce those hedge fund advisers to increase or retain their level of prime brokerage fees paid to UBS Securities. On November 22, 2010, UBS entered into a Consent Order and Settlement with the Massachusetts Securities Division, pursuant to which UBS agreed to implementing a disclosure policy and retaining an independent consultant to monitor the policy. UBS also paid a $100,000 fine.

UBS Securities will act only as a clearing broker for each trading company and as such will be paid commissions for executing and clearing trades on behalf of each trading company. UBS Securities has not passed upon the adequacy or accuracy of this prospectus. UBS Securities neither will act in any supervisory capacity with respect to the managing owner or the trading advisors nor participate in the management of the trust, the managing owner or the trading companies.

Newedge

The disclosure included under the heading “CLEARING BROKERS—Newedge” is hereby deleted in its entirety and replaced with the following:

Newedge

Currently, Newedge USA, LLC (“Newedge USA”) serves as the Fund’s clearing broker to execute and clear the Fund’s futures and equities transactions and provide other brokerage-related services. Newedge UK Financial Limited (“Newedge UK”) or Newedge Alternative Strategies, Inc. (“NAST”) may execute foreign exchange or other over the counter transactions with the Fund as principal. Newedge USA is a subsidiary of Newedge Group, which was formed on January 2, 2008 as a joint venture by Société Générale and Calyon to combine the brokerage activities previously carried by their respective subsidiaries, which comprised the Fimat Group and the Calyon Financial Group of affiliated entities. Newedge USA is a futures commission merchant and broker dealer registered with the U.S. Commodity Futures Trading Commission (“CFTC”) and the U.S. Securities and Exchange Commission (“SEC”), and is a member of FINRA. Newedge USA is a clearing member of all principal futures exchanges located in the United States as well as a member of the Chicago Board Options Exchange, International Securities Exchange, New York Stock Exchange, Options Clearing Corporation, and Government Securities Clearing Corporation. NAST is an eligible swap participant that is not registered or required to be registered with the CFTC or the SEC, and is not a member of any exchange. Newedge UK is a wholly-owned subsidiary of Newedge Group incorporated in England and Wales with company number 5407520 and whose registered office is at 10 Bishops Square, London, E1 6EG. Newedge is an authorized firm under the Financial Services and Markets Act 2000 (as amended) and is lead-regulated and supervised by the Financial Services Authority.

15

Newedge USA and NAST are headquartered at 550 W. Jackson, Suite 500, Chicago, IL 60661 with branch offices in New York, New York; Kansas City, Missouri; Cypress, Texas, and Montreal Canada. Newedge UK is headquartered at 10 Bishops Square, London E1 6EG.

Prior to January 2, 2008, Newedge USA was known as Fimat USA, LLC. On September 1, 2008, Newedge USA merged with future commission merchant and broker dealer Newedge Financial Inc. (“NFI”) – formerly known as Calyon Financial Inc. Newedge USA was the surviving entity.

In March 2008, NFI settled, without admitting or denying the allegations, a disciplinary action brought by the New York Mercantile Exchange (“NYMEX”) alleging that NFI violated NYMEX rules related to: numbering and time stamping orders by failing properly to record a floor order ticket; wash trading; failure to adequately supervise employees; and violation of a prior NYMEX cease and desist order, effective as of December 5, 2006, related to numbering and time stamping orders and block trades. NFI paid a $100,000 fine to NYMEX in connection with this settlement.

In February 2011, Newedge USA settled, without admitting or denying the allegations, a disciplinary action brought by the CFTC alleging that Newedge USA exceeded speculative limits in the October 2009 live cattle futures contract on the Chicago Mercantile Exchange and failed to provide accurate and timely reports to the CFTC regarding their larger trader positions. Newedge USA paid a $140,000 civil penalty and disgorgement value of $80,910 to settle this matter. In addition, the CFTC Order required Newedge USA to implement and maintain a program designed to prevent and detect reporting violations of the Commodity Exchange Act and CFTC regulations.

In January 2012, Newedge USA settled, without admitting or denying the allegations, a disciplinary action brought by the CFTC alleging that Newedge USA failed to file accurate and timely reports to the CFTC and failed to report certain large trader information to the CFTC. Newedge USA paid a $700,000 civil penalty to settle this matter. In addition, the CFTC Order required Newedge USA to timely submit accurate position reports and notices, and to implement and maintain procedures to prevent and detect reporting violations of the Commodity Exchange Act and CFTC regulations.

Other than the foregoing proceedings, which did not have a material adverse effect upon the financial condition of Newedge USA, there have been no material administrative, civil or criminal actions brought, pending or concluded against Newedge USA or Newedge UK or their principals in the past five years.

Neither Newedge USA, Newedge UK nor any affiliate, officer, director or employee thereof have passed on the merits of this Memorandum or offering, or give any guarantee as to the performance or any other aspect of the Fund.

16

FRONTIER DIVERSIFIED SERIES APPENDIX

The information set forth on pages Frontier Diversified App.—5 through Frontier Diversified App.—7 is hereby deleted in its entirety and replaced with the following:

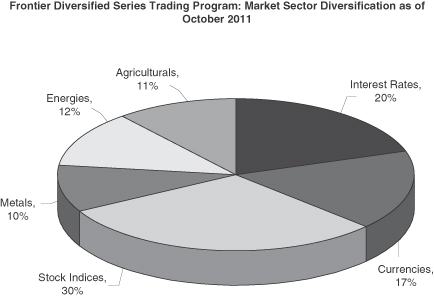

The following table sets forth certain of the markets in which the trading advisors that will receive allocations of the Frontier Diversified Series Assets may trade on behalf of client accounts. Not all markets are part of each trading advisor’s program. Each trading advisor reserves the right to vary the markets and types of instruments it trades without giving prior notice to the trust. The diversification summary below is based on long-term averages as of October 31, 2011.

DIVERSIFICATION SUMMARY

THE FRONTIER FUND—THE FRONTIER DIVERSIFIED SERIES

Frontier Diversified Series Trading | Program | Interest Rates | Currencies | Stock Indices | Metals | Energies | Agriculturals | Total | ||||||||||||||||||||||||

Major Advisors and/or Reference Programs: | ||||||||||||||||||||||||||||||||

Cantab Capital Partners LLP | | Aristarchus Program | | 25 | % | 39 | % | 15 | % | 8 | % | 8 | % | 5 | % | 100 | % | |||||||||||||||

Graham Capital Management, L.P. |

| K4D-15 Program |

| 26 | % | 33 | % | 22 | % | 4 | % | 10 | % | 6 | % | 100 | % | |||||||||||||||

Quantitative Investment Management | Global | 26 | % | 14 | % | 45 | % | 6 | % | 8 | % | 1 | % | 100 | % | |||||||||||||||||

QuantMetrics Capital Management LLP | QM Futures | 9 | % | 20 | % | 65 | % | 1 | % | 4 | % | 1 | % | 100 | % | |||||||||||||||||

Tiverton Trading, Inc. | | Discretionary Trading Methodology Program | | 17 | % | 17 | % | 16 | % | 17 | % | 17 | % | 16 | % | 100 | % | |||||||||||||||

Transtrend B.V. | | Diversified Trend Program -- Enhanced Risk/USD | | 22 | % | 30 | % | 15 | % | 8 | % | 12 | % | 13 | % | 100 | % | |||||||||||||||

Winton Capital Management Ltd.* | Diversified | 28 | % | 18 | % | 20 | % | 15 | % | 13 | % | 6 | % | 100 | % | |||||||||||||||||

Non-Major Advisors and/or Reference Programs | N/A | 18 | % | 9 | % | 31 | % | 11 | % | 14 | % | 18 | % | 100 | % | |||||||||||||||||

Frontier Diversified Series | N/A | 20 | % | 17 | % | 30 | % | 10 | % | 12 | % | 11 | % | 100 | % | |||||||||||||||||

| * | These figures are based on the Winton Futures Fund projected risk of the current trading system and represents Winton’s projected long term risk breakdown and is based on historic market volatilities over the last 10 years. |

17

18

PAST PERFORMANCE OF FRONTIER DIVERSIFIED SERIES-1

The Capsule Performance Table which follows sets forth the past performance of the Frontier Diversified Series-1 during the period covered by the table.

| Month | 2011 | 2010 | 2009 | |||||||||

January | 3.53 | % | -3.98 | % | — | |||||||

February | 0.28 | % | 0.45 | % | — | |||||||

March | -0.91 | % | 2.28 | % | — | |||||||

April | 0.56 | % | 2.20 | % | — | |||||||

May | -2.48 | % | -0.05 | % | — | |||||||

June | -2.75 | % | -0.03 | % | -1.89 | % | ||||||

July | -0.83 | % | -2.02 | % | -0.74 | % | ||||||

August | -3.78 | % | 4.09 | % | 0.31 | % | ||||||

September | 3.60 | % | 1.25 | % | 1.29 | % | ||||||

October | -2.74 | % | 4.13 | % | 0.08 | % | ||||||

November | -3.76 | % | 1.41 | % | ||||||||

December | 2.65 | % | -3.61 | % | ||||||||

Year |

| -5.66 (10 month | % ) | 7.00 | % |

| -3.20 (7 months | % ) | ||||

| Name of pool: | The Frontier Fund | |

This pool is a multi-advisor advisor pool as defined in CFTC Regulation § 4.10(d)(2). | ||

Name of series and class: | Frontier Diversified Series-1 | |

Inception of Trading of Frontier Diversified Series-1: | June 9, 2009 | |

Aggregate Gross Capital Subscriptions for Frontier Diversified Series-1 as of October 31, 2011: | $114,796,843.09 | |

Net Asset Value of Frontier Diversified Series-1 as of October 31, 2011: | $70,380,195.80 | |

Worst Monthly Percentage Draw-down: | -3.98% (Jan 2010) | |

Worst peak-to-valley Draw-down: | -9.82% (Feb 2011 to Aug 2011) |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

The Frontier Diversified Series-1 performance table sets forth the actual performance of the Frontier Diversified Series-1. Actual gross trading performance (gross realized and unrealized gain/loss before deduction for trading commissions and fees, management fees or any other expenses, and before addition of interest income) is adjusted for the trading expenses, management fees, incentive fees, initial service fees, on-going service fees and interest income of the Frontier Diversified Series-1. The asset-based fees, as an annualized percentage calculated monthly on the adjusted beginning of month net asset value, are as follows:

| • | Management fees: 0.75% |

| • | Initial service fees and on-going service fees: 2.00% |

An incentive fee of 25% of New High Net Trading Profits (as defined), earned quarterly, is deducted in the above table. Twenty percent (20%) of any interest income, based upon applying the 90-day Treasury Bill rate for each month to the adjusted beginning of month net asset value, is credited in the above table.

19

| * | “Draw-down” means losses experienced by the applicable class of the applicable series of the pool over a specified period. |

| ** | “Worst peak-to-valley draw-down” means the greatest cumulative percentage decline in month-end net asset value due to losses sustained by the applicable class of the applicable series of the pool during any period in which the initial month-end net asset value is not equaled or exceeded by a subsequent month-end net asset value. |

20

PAST PERFORMANCE OF FRONTIER DIVERSIFIED SERIES-2

The Capsule Performance Table which follows sets forth the past performance of the Frontier Diversified Series-2 during the period covered by the table.

| Month | 2011 | 2010 | 2009 | |||||||||

January | 3.69 | % | -3.85 | % | — | |||||||

February | 0.41 | % | 0.58 | % | — | |||||||

March | -0.76 | % | 2.44 | % | — | |||||||

April | 0.70 | % | 2.35 | % | — | |||||||

May | -2.34 | % | 0.08 | % | — | |||||||

June | -2.60 | % | 0.12 | % | -1.79 | % | ||||||

July | -0.69 | % | -1.88 | % | -0.59 | % | ||||||

August | -3.63 | % | 4.25 | % | 0.46 | % | ||||||

September | 3.75 | % | 1.40 | % | 1.45 | % | ||||||

October | -2.59 | % | 4.27 | % | 0.22 | % | ||||||

November | -3.61 | % | 1.57 | % | ||||||||

December | 2.81 | % | -3.47 | % | ||||||||

Year |

| -4.27 (10 months | % ) | 8.88 | % |

| -2.23 (7 months | % ) | ||||

| Name of pool: | The Frontier Fund | |

This pool is a multi-advisor advisor pool as defined in CFTC Regulation § 4.10(d)(2). | ||

Name of series and class: | Frontier Diversified Series-2 | |

Inception of Trading of Frontier Diversified Series-2: | June 9, 2009 | |

Aggregate Gross Capital Subscriptions for Frontier Diversified Series-2 as of October 31, 2011: | $83,229,109.40 | |

Net Asset Value of Frontier Diversified Series-2 as of October 31, 2011: | $60,813,389.11 | |

Worst Monthly Percentage Draw-down: | -3.85% (Jan 2010) | |

Worst peak-to-valley Draw-down: | -9.02% (Feb 2011 to Aug 2011) |

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

21

FRONTIER DIVERSIFIED SERIES APPENDIX

CANTAB

The disclosures included under the headings “CANTAB—Principals of Cantab” and “CANTAB—Other Principals of Cantab” are hereby deleted in their entirety and replaced with the following:

Principals of Cantab

Dr. Ewan Kirk

Dr. Ewan Kirk is the former head of the Goldman Sachs Fixed Income, Currency, Commodity and Equity Quantitative Strategies group. As the Partner in charge of a group of 110 mathematicians, physicists, statisticians and programmers, Dr. Kirk oversaw and drove the development of the highly respected and profitable quantitative group. Dr. Kirk joined Goldman Sachs, the investment bank, in the commodity strategy group in May 1992 and spent 8 years in the commodity business developing trading algorithms, quantitative models and trading systems before becoming a partner in October 2000 and managing the group until leaving Goldman Sachs in January 2005. Dr. Kirk was between employment from February 2005 to January 2006, when he co-founded Cantab. Dr. Kirk has been listed as a principal of Cantab since April 8, 2008, where his duties are research and development, risk management, managing Cantab’s quantitative team and the overall leadership of the firm, and registered as an associated person of Cantab since June 12, 2008.

Erich Schlaikjer

Erich Schlaikjer is the former Managing Director and Chief Technology Officer for the European Strategies group at Goldman Sachs, the investment bank, from September 1987 to January 2005. Mr. Schlaikjer was personally responsible for designing and building many of the analysis tools which are currently in use at Goldman Sachs. At Cantab, Mr. Schlaikjer runs the team of programmers which designs and builds the analytical tools and infrastructure which enable the mathematicians to develop, test and implement algorithmic trading rules. Mr. Schlaikjer has worked extensively in the FX and Equity markets. Mr. Schlaikjer was between employment from January 2005 to January 2006, when he co-founded Cantab. Mr. Schlaikjer has been listed as a principal of Cantab since June 10, 2008 and registered as an associated person of Cantab since June 12, 2008.

Chris Pugh

Chris Pugh is the former Chief Operating Officer for KBC Alternative Investment Management (“KBC”), an investment management firm, from December 2000 through March 2006, Mr. Pugh was one of the founding members of KBC’s hedge fund, assisting it in its growth from $50 million in 2001 to a peak of $5 billion in 2005. Mr. Pugh was responsible for the operational and financial infrastructure at KBC. Prior to his career at KBC, from September 1995 to December 2000 Mr. Pugh was the Head of Special Projects at D. E. Shaw & Co., an investment management firm. Chris joined Cantab in March 2006. Mr. Pugh has been listed as a principal of Cantab since April 29, 2008, where his duties are overseeing the process, procedure, compliance and control aspects of managing investment funds, and registered as an associated person of Cantab since June 12, 2008.

Dr. Tom Howat

Tom was recently invited to join the partnership in recognition of his outstanding contribution to the firm. Tom heads the team of programmers responsible for Cantab Capital Partners’ ongoing infrastructural development. Much of the framework for the backtesting, trading and real time risk management of our strategies is due to Tom’s innovative design and implementation; from methods for real time signal computation and automated execution, through to ensuring the fairest possible allocations between our managed accounts. Tom joined Cantab Capital Partners at its inception in 2006, prior to which he spent seven years at Trinity College, Cambridge, where he obtained degrees in mathematics and a PhD in mathematical biology. Mr. Howat has been listed as a principal of Cantab since May 23, 2011.

Other Principals of Cantab

Cantab Capital LTIP Limited has been listed as a principal of Cantab since April 26, 2011.

22

The disclosure included under the headings “CANTAB TRADING STRATEGY” and “CANTAB MARKETS TRADED” are hereby deleted in their entirety and replaced with the following:

CANTAB TRADING STRATEGY

Cantab believes that statistically rigorous and robust analysis of markets identifies sources of returns which persist due to inefficiencies and the behavior of market participants.

Cantab uses a strict methodology to postulate these sources of returns initially and then test the hypothesis using real world data out of sample. Cantab’s systematic strategies are un-tuned and are predominately parameter free.

Cantab takes a strictly quantitative approach to all aspects of trading. Strategy selection, portfolio construction, execution and risk control are all specified by algorithmic and systematic processes.

The Strategies

By combining proprietary algorithms with macroeconomic state variables such as the carry or risk premium Cantab has created stable alpha generating strategies.

By executing a correlated basket of futures and forwards, Cantab creates precise risk return profiles for each strategy which enhances the performance of the strategies.

Robust out of sample testing, large consistent data sets and flexible, efficient and rigorous tools are essential in identifying these sources of return and creating the appropriate strategies to capture the return.

Portfolio Construction

Although simple fixed weighting portfolios perform well, by creating a dynamically weighted VAR constrained portfolio, attractive risk profiles can be created. Cantab’s proprietary portfolio algorithms allow Cantab to not only construct an optimal portfolio but to also adapt the portfolio construction in various market states.

CANTAB MARKETS TRADED

Cantab concentrates on the FX, Commodity, Equity Indices, Bond, and Interest Rate markets and implements their approach through the forwards and futures markets.

PAST PERFORMANCE OF CANTAB