PURSUANT TO RULE 13a-16 OR 15d-16 OF THE

For the month of April, 2020

(Commission File No. 001-33356),

Indicate by check mark whether the registrant files or will file

annual reports under cover Form 20-F or Form 40-F.

Form 20-F ___X___ Form 40-F ______

the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1)

Yes ______ No ___X___

Indicate by check mark if the registrant is submitting

the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ______ No ___X___

Indicate by check mark whether by furnishing the information contained in this Form,

the Registrant is also thereby furnishing the information to the Commission pursuant

to Rule 12g3-2(b) under the Securities Exchange Act of 1934:

Yes ______ No ___X___

If “Yes” is marked, indicate below the file number assigned

to the registrant in connection with Rule 12g3-2(b):N/A

Financial Statements

Gafisa S.A.

December 31, 2019

and Independent Auditor’s on the Financial Statements

(A free translation of the original report in Portuguese as published in Brazil)

Gafisa S.A.

Financial Statements

December 31, 2019

Contents

Management Report | 1 |

Independent auditor’s report on the Financial Statements | 8 |

Audited financial statements | |

Statements of financial position | 14 |

Statement of profit or loss | 16 |

Statement of comprehensive income | 17 |

Statement of changes in equity | 18 |

Statement of cash flows | 19 |

Statement of value added | 20 |

Notes to the financial statements | 21 |

Statement of the executive officers about the financial statements | 85 |

Statement of the executive officers about the independent auditors’ report | 86 |

Audit Committee’s meeting minutes | 87 |

Board of Directors’ meeting minutes | 88 |

4Q19 Earnings release | 90 |

| 2019 MANAGEMENT REPORT |

Dear Shareholders,

The year of 2019 has been remarkable in the history of Gafisa, has gone through an in-depth restructuring process, leading to a substantial improvement in our operational performance and financial results.

In terms of cash structuring, we have successful completed two capital increases with total funding of US$ 100 million, resulting in new institutional investors in the Company’s ownership structure.

We have engaged Bain Co., to support us with our Planning, and Falconi Consultores, to implement our working method and the goals to be attained in 2020.

We have decided to not launch any new venture while we do not fully control our operations and, most importantly, our finances.

Leverage, measured by the ratio of net debt to equity, dropped to 34%, down by 118.6 p.p. on the same period of the previous year.

As event after the reporting date, we have also received the approval from Banco do Brazil for renegotiating the debt we had with that institution, which will extend the maturity of short-term liability.

Fixed and variable costs have been reduced by more than R$ 50 million, and 18 ventures had their construction works resumed, two of which have already been delivered to our customers.

We have renegotiated important debts, financial ones and with suppliers, obtained many credit facilities in the market and significantly reduced the accounting provisions.

Moreover, we have resumed the process of relisting our stocks in the US market, to increase our access to new investors.

Our financial results had a significant improvement, considering that our net debt fell to R$ 325 million, a 57% drop in relation to 2018.

Cash and banks have changed from R$ 63 million in the 1Q2019 to R$ 414 million in the 4Q2019.

Our gross margin has substantially improved to approximately 30%, whereas in 2018 it stood at 12%.

Finally, we have reversed an adjusted net loss of (R$ 356 million) in 2018 to (R$ 14 million) in 2019. If we do not consider the divestment of the interest held in Alphaville Urbanismo S.A., the company recorded a profit of R$ 15 million.

Attaining this result is extremely relevant, as the company’s latest profit was recorded in the fourth quarter of 2015.

In December, we have signed a Letter of Intent for acquisition of UPCON, a renowned developer operating in São Paulo market.

With this operation, to be submitted for the approval of our shareholders in next April, we will strengthen Gafisa with both assets and experience and the complementary skills that we will have with their executive team.

We have projects that have already been approved, continue to prospect businesses and land, are capitalized with the important increase in capital made in 2019, and we count on a highly engaged team to launch new ventures in 2020.

Gafisa, relying on a traditional trademark, recognized as benchmark for the Brazilian market and with a business model that has been daily improved, is positioned to begin a new development and growth cycle, resuming its successful history and creating value to our shareholders.

We thank the support of our shareholders, who gave us a vote of absolute confidence in the company’s management, the loyalty of our customers, the partnership of our suppliers, and thecontribution of our team of professionals, who, in a demonstration of full commitment to the company, has been of fundamental importance to rebuild the company and pave this new path.

1

Gafisa’s Management Committee & Executive Board

| OPERATIONAL AND FINANCIAL PERFORMANCE |

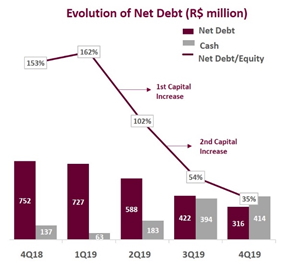

In line with its restructuring process, Gafisa has concentrated its efforts during the year to restructure itself internally. Two capital increases, totaling R$ 405 million, have been fundamental to adjust the Company’s capital structure.

Cash and Banks amounted to R$ 414 million in the 4Q2019, as compared to R$ 63 million in the 1Q2019, reflecting the strict discipline to use the inflow of operating cash to pay the Company’s commitments, preserving the funds obtained in the capital increase as a liquidity cushion and resource that enables us to resume our growth.

During 2019, we have equated a relevant portion of our financial liabilities, adjusting the flow to the monetization curve of the units and often reducing the debt cost. We are in an advanced stage in the renegotiation of other transactions, following the rationale of extending terms and reducing costs. This entire process and the commitment demonstrated by the new Management enabled the Company to reestablish good relationship with the financial markets while seeking new transactions, as well as with major players in the capital markets. In the end of the 4Q2019, net debt has been reduced to R$316.3 million, as compared to R$752 million reported in the previous year.

The net debt-to-equity ratio in the end of the 4Q19 reached 35.3%, down by nearly 58% on the amount reported in the 4Q18 of R$ 752 million.

Chart 1 – Net Debt, Net Debt/Equity, Cash (in millions of reais - R$)

The Company’s decision to not launch new ventures over the year has directly affected sales performance.

Gross sales totaled R$ 292 million in 2019, a drop by 72% in relation to the same period of the previous year (R$ 1.04 billion). Sales over Supply (SoS) over the past 12 months reached 18.2%, a drop by 21.7 p.p. in relation to the same period of the previous year.

Meanwhile, with the renegotiation efforts that have been made with Gafisa’s customers, the contract cancellations reported for the year amounted to R$ 96.4 million, a drop by 57.7% year-on-year. We have noted that the trend downward in contract cancellation has consolidated throughout 2019. In addition, the trend upward in real estate prices in general, noted throughout 2019, combined withthe consolidation of the Contract Cancellation Law, have, in our opinion, also contributed to decrease the incentives for customers to cancel contracts.

2

The market value of the Company’s inventory at the end of the fourth quarter of 2019 totaled R$ 881.7 million.

Deliveries totaled 363 units with a TSV of R$171.3 million, divided into 2 projects or phases in 2019. Moreover, in December 2019, the certificate of occupancy of a venture comprising 63 units and TSV of R$ 37 million has been obtained. In the end of 2019, Gafisa had 17 active construction sites.

Chart 2 - Delivered ventures

Project | Delivery date | Launch date | Venue | % Interest | Units 100%¹ | TSV % R$000² |

Like Aclimação | Feb-19 | Mar-16 | São Paulo, SP | 100% | 136 | 80,079 |

Choice Santo Amaro | May-19 | Jun-16 | São Paulo, SP | 100% | 227 | 91,317 |

Total 2019 |

|

|

|

| 363 | 171,396 |

¹ Number of units equivalent to 100% interest in ventures, net of barter transactions;

² TSV = Total Sales Value of units, net of brokerage and barter transactions.

The TSV passed on amounted to R$ 171 million for the year-to-date. The estimate for 2020 is a significant increase in the TSV passed on, once eight Gafisa ventures are expected to be delivered, with a TSV to be passed on that may exceed R$ 1 billion.

Net revenues totaled R$400.4 million in 2019, a drop by 58.3% in relation to the amount reported in the previous period.

Meanwhile gross profit amounted to R$117.7 million in 2019, above that of 2018 (R$ 115 million), even though revenue was lower. As a result, gross margin for 2019 stood at 29.4%, reflecting the more effective management of the new Management of the Company.

3

Chart 3 – Development of Margins (R$ 000)

| 4Q19 | 3Q19 | Q/Q(%) | 4Q183 | Y/Y (%) | 12M19 | 12M183 | Y/Y (%) |

Net revenue | 116,173 | 89,212 | 30.2% | 192,917 | (39.8%) | 400,465 | 960,891 | (58.3%) |

Gross Profit | 36,259 | 38,104 | (4.8%) | (29,710) | (222.0%) | 117,781 | 114,722 | 2.7% |

Gross margin | 31.21% | 42.71% | -11.5 p.p. | (15.4%) | 46.6 p.p. | 29.41% | 11.90% | 17.5 p.p. |

(-) Financial Costs | 7,920 | (7,147) | (210.8%) | (13,506) | (158.6%) | 30,356 | (112,904) | (126.9%) |

Adjusted Gross Profit ¹ | 44,179 | 45,251 | (2.4%) | 46,942 | (5.9%) | 148,137 | 227,626 | (34.9%) |

Adjusted Gross Margin ¹ | 38.03% | 50.72% | -12.7 p.p. | 24.3% | 13.7 p.p. | 36.99% | 23.7% | 13.3 p.p. |

(-) Inventory and Land Bank | (8,435) | - | - | 63,145 | (113.4%) | (8,435) | 63,145 | (113.4%) |

Recurring Gross Profit ² | 35,744 | 45,251 | (21.0%) | 46,942 | (23.9%) | 139,702 | 290,771 | (52.0%) |

Recurring Adjusted Gross Margin² | 30.77% | 50.72% | -20 p.p. | 24.3% | 6.4 p.p. | 34.88% | 30.3% | 4.6 p.p. |

The adjusted gross margin was 37% in 2019, up 13.3 p.p. on the margin reported in 2018, and up 37.5 p.p. on that reported in 2017.

Recurring general and administrative expenses fell from R$74.4 million in 2018 to R$ 50.6 million in 2019, a saving of R$ 23.6 million, which represents 31.7%. This saving is a direct result of the plan for cutting expenses carried out over the year, with the adjustment of the structure to the new model of the Company.

The adjusted EBITDA reached R$214 million in the end of 2019, a 68.5% increase as compared to the amount reported in the previous year (R$ 127 million).

We have obtained the reversal of the loss of approximately R$ 406 million. The net result for 2019 was negative by R$ 13.7 million, as compared to the net loss of R$419.5 million reported in the previous year. If we exclude the effect of the divestment of Alphaville Urbanismo S.A., we would have obtained a Net Income of R$ 15.1 million.

| HUMAN RESOURCES |

We have an experienced team is at the vanguard of the Brazilian real estate sector and other business types, which positively contributes to the continuous improvement in our processes, customer satisfaction and respect, as well as to attain favorable results to our Company.

In the last year we have made drastic changes in our leadership, which enabled us to form a heterogenous team with complementary competences and engaged to deliver results to our shareholders.

Also, occupational safety and accident are central themes for Gafisa. Therefore, we maintain a continuous program of risk identification, prevention and mitigation, which aims, besides preserving the physical integrity of our direct or indirect staff, to offer a basis for a healthier life. For us, investing in safety is a guarantee of wellness in and out of the work environment. We offer training programs to the team in the field (directly related to construction works), as well as to our collaborators of third-party companies, who provide services in our sites and some ventures.

The Company has 250 employees (base December 2019).

4

| CORPORATE GOVERNANCE |

Gafisa’s Board of Directors is responsible for making decisions and formulating general guidelines and policies for the Company’s business, including its long-term strategies. In addition, the Board also appoints executive officers and supervises their activities.

The decisions of the Board of Directors are taken by the majority vote of its members. In the event of a disagreement, the Chair of the Board of Directors has, in addition to her/his personal vote, to cast a tie-breaking vote.

The current Board is formed by seven members, most of whom are independent (57%). The members serve for a unified term of office of two years*, according to the Listing Rules of Novo Mercado, with reelection and removal being permitted by shareholders in Shareholders’ Meeting.

The members of Board of Directors are shown in the following table.

NAME | DATE OF BIRTH | POSITION | ELECTION DATE |

Leo Julian Simpson | 3.30.1956 | CEO | April 15, 2019 |

Antonio Carlos Romanoski | 2.12.1945 | Effective Member | April 15, 2019 |

Eduardo Larangeira Jácome | 10.15.1955 | Effective Member | April 15, 2019 |

Nelson Sequeiros Rodriguez Tanure | 11.21.1951 | Effective Member | April 15, 2019 |

João Antonio Lopes Filho | 8.12.1963 | Effective Member | February 7, 2020 |

Thomas Cornelius Azevedo Reichenheim | 12.4.1947 | Effective Member | April 15, 2019 |

Denise dos Passos Ramos | 1.30.1975 | Effective Member | July 3, 2019 |

FISCAL COUNCIL

Gafisa’s Articles of Incorporation provide for a non-permanent Fiscal Council, the Shareholders’ Meeting being able to determine its installation and members, as provided in the Law. The Fiscal Council, when installed, will comprise three to five members, and an equal number of alternates.

The operations of the Fiscal Council, when installed, ends in the first Annual Shareholders’ Meeting (ASM) held after its installation, the re-election of its members being permitted. The compensation of fiscal council members is set at the Shareholders’ Meeting that elect them.

The Company’s Fiscal Council is not currently installed.

| EXECUTIVE MANAGEMENT |

The Executive Management is the Company’s body mainly responsible for managing and daily monitoring the general policies and guidelines established at the Shareholders’ Meeting and Board of Directors.

Gafisa’s Executive Management shall be composed of a minimum of two and a maximum of eight members, including the CEO, the CFO and the IR Officer, elected by the Board of Directors for a three-year term of office, reelection being permitted, as established in the Articles of Incorporation. In the current term of office, eight members comprise the Executive Management:

5

NAME | POSITION | DATE OF LAST INVESTITURE | TERM OF OFFICE |

Ian Monteiro de Andrade | CFO and IR Officer | March 2, 2020 | March 2, 2023 |

Saulo Nunes | Statutory Officer | May 17, 2019 | May 16, 2022 |

Cauê Cardoso | Statutory Officer | January 28, 2020 | January 28, 2023 |

Guilherme Luis Presenti e Silva | Statutory Officer | January 28, 2020 | January 28, 2023 |

Luiz Fernando Ortiz | Statutory Officer | January 28, 2020 | January 28, 2023 |

Guilherme Augusto Soares Benevides | COO | March 2, 2020 | March 2, 2023 |

Fabio Freitas Romano | Statutory Officer | March 2, 2020 | March 2, 2023 |

André Ackermann | Statutory Officer | March 2, 2020 | March 2, 2023 |

| COMMITTEES |

| CORPORATE GOVERNANCE AND COMPENSATION COMMITTEE |

The Corporate Governance and Compensation Committee is aimed at periodically analyzing and reporting on matters related to the size, identification, selection, qualification and continuing education of the Board of Directors. It identifies qualified persons to become Board members, nominates to the Manager candidates to be proposed for election in the annual shareholders’ meeting, and to serve on the Board of Directors and leadership positions in the committee.The members are Eduardo Larangeira Jácome, Nelson Sequeiros Rodriguez Tanure, Thomas Cornelius Azevedo Reichenheim and Antônio Carlos Romanoski.

| AUDIT COMMITTEE |

The Audit Committee supervises the Company’s accounting and financial reporting, planning and analysis processes, including those of quarterly and financial reporting. It guides the involvement and disclosure of auditors throughout the auditing process, assuring the full compliance with legal requirements and accounting standards. Moreover, it is responsible for monitoring the internal control and internal auditing processes, and choosing the accounting policies.The members are Gilberto Braga, Pedro Carvalho de Mello and Thomas Cornelius Azevedo Reichenheim.

| DIVIDENDS, SHAREHOLDER RIGHTS AND SHARE DATA |

In order to protect the interest of all shareholders equally, the Company establishes that, according to the effective legislation and the best governance practices, the following rights are entitled to Gafisa’s shareholders:

ü Vote in annual or extraordinary Shareholders' Meeting, and make recommendations and provide guidance to the Board of Directors on decision making;

ü Receive dividends and participate in profit sharing or other share-related distributions, in proportion to their interest in capital;

ü Supervise Gafisa's management, according to its Articles of Incorporation, and step down from the Company in the cases provided in the Brazilian Corporate Law; and

6

ü Receive at least 100% of the price paid for common share of the controlling stake, according to the Listing Rules of Novo Mercado, in case of public offering of shares as a result of the disposal of the Company's control.

Under the terms of article 47, paragraph 2 (b) of Articles of Incorporation, the balance of net income for the year, calculated after the deductions provided in the Articles of Incorporation and adjusted according to article 202, of the Brazilian Corporate Law, will have 25% of it allocated to the payment of mandatory dividend to all shareholders of the Company.

Considering that the Company recognized loss for the year ended December 31, 2019, there is no proposal for allocation of net income and dividend distribution for such year.

| CAPITAL MARKETS |

The Company has diluted capital, its shares are traded in the Brazilian market and abroad through American Depositary Receipt (ADR). From December 17, 2018, Gafisa’s shares are no longer listed on the New York Stock Exchange (NYSE), and its ADRs started to be traded Over the Counter (OTC). The Company’s delisting process was approved in the meeting of the Board of Directors held on November 26, 2018. The rationale behind this decision is supported by the weighing of the costs against the benefits inherent in the ADR program.

Gafisa is currently going through the process for re-listing on the New York Stock Exchange (NYSE), aiming to increase the visibility of the Company and access to new markets.

In 2019, we reached an average daily trading volume of R$2.2 million on B3 and US$ 124.7 thousand on the NYSE/OTC.

The Company’s shares ended the year 2019 quoted at R$8.67 (GFSA3) and US$1.81 (GFASY).

| INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

The Company’s policy on commissioning non-external audit services to independent auditors is based on principles that preserve their autonomy. These internationally accepted principles consist of the following: (a) the auditor cannot audit its own work, (b) the auditor cannot function in the role of management in its client, and (c) the auditor cannot promote the interests of its client.

According to Article 2 of CVM Instruction 381/03, Gafisa informs that BKR Lopes Machado, responsible for general auditing, and BDO Auditores Independentes, responsible for SOx auditing, the independent registered accounting firms of the Company and its subsidiaries, did not provide services other than independent audit in 2019.

| MANAGEMENT STATEMENT |

The Executive Management declares, in compliance with article 25, paragraph 1, items V and VI, of CVM Instruction 480/2009, that it revised, discussed and agrees with the Financial Statements contained in this Report and the opinion issued in the report of Independent Registered Accountants on them.

7

INDEPENDENT AUDITOR’S REPORT ON INDIVIDUAL AND CONSOLIDATED FINANCIAL STATEMENTS

To

Shareholders and Board members of

Gafisa S.A.

São Paulo, SP

Opinion

We have audited the accompanying individual and consolidated financial statements ofGafisa S.A. (“Gafisa” or “Company”), identified as Company and Consolidated, respectively, which comprise the statement of financial position as of December 31, 2019, and the respective statement of profit or loss, statement of comprehensive income, statement of changes in equity, and statement of cash flows for the year then ended, as well as the corresponding explanatory notes, including the summary of significant accounting policies.

Opinion on the individual financial statements

In our opinion, the aforementioned individual financial statements present fairly, in all material respects, the financial position of Gafisa S.A. as of December 31, 2019, and the performance of its operations and cash flows for the year then ended, in accordance with the accounting practices adopted in Brazil, applicable to real estate development entities in Brazil, registered with the Brazilian Securities and Exchange Commission (CVM).

Opinion on the consolidated financial statements

In our opinion, the aforementioned individual financial statements present fairly, in all material respects, the consolidated financial position of Gafisa S.A. as of December 31, 2019, and its consolidated performance of its operations and cash flows for the year then ended, in accordance with the accounting practices adopted in Brazil and the International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB), applicable to real estate development entities in Brazil, registered with the Brazilian Securities and Exchange Commission (CVM).

Basis for opinion on the individual and consolidated financial statements

We conducted our audit in accordance with the Brazilian and International Standards on Auditing. Our responsibilities, according to such standards, are described in the following section, entitled “Auditor’s responsibility for the audit of individual and consolidated financial statements”. We are independent of the Company and its subsidiaries, according to the relevant ethical principles established in the Accountant’s Code of Professional Ethics and the professional standards issued by the Federal Accounting Council (CFC), and comply with other ethical responsibilities according to such standards. We believe that the audit evidence we have obtained is sufficient and appropriate to base our opinion.

8

Emphasis

Accounting practices adopted in Brazil applicable to real estate development entities in Brazil, registered with the CVM

As described in Note 2.1, the individual (Company) and consolidated financial statements have been prepared in accordance with the accounting practices adopted in Brazil and the International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB), applicable to real estate development entities in Brazil, registered with the CVM. Accordingly, the determination of the accounting policy to be adopted by the entity, on recognition of revenue from purchase and sale of real estate unit not yet completed, on aspects related to transfer of control, follows the understanding expressed by CVM in the Circular Letter/CVM/SNC/SEP 02/2018 on the application of NBC TG 47 (IFRS 15). Our opinion does not contain exception in relation to this matter.

Key audit matters

Key audit matters are those that, in our professional judgment, were of most significance in our audit of the current year. These matters were addressed in the context of our audit of the individual and consolidated financial statements as a whole, and in forming our opinion thereon, and, therefore, we do not provide a separate opinion on these matters.

Recognition of revenues

The Company recognizes real estate sales revenue during construction as established in the Circular Letter CVM/SNC/SEP 02/2018, as described in the Notes 2.1 and 2.2.2 to the individual and consolidated financial statements. The recognition of the revenue of the Company and its subsidiaries requires the measurement of progress and satisfaction of performance obligation over time. This measurement requires significant and timely judgment by the Management of the Company and its subsidiaries of the estimate of inputs and expenditures necessary for satisfying the respective performance obligations, considering, for example, the costs to be incurred until the completion of construction works and measurement of the progress of the respective real estate ventures.

Consequently this matter was considered key for our audit because we consider the high risk of subjectivity in the evaluation of the estimates made by the Company’s Management, linked to the relevance and amounts involved in revenue recognition.

How our audit conducted this matter:

Our main audit procedures aimed at the appropriate recognition of the revenue from real estate sales during construction were the following: (i) Evaluation of the effectiveness of the internal controls directly related to the approval and revision of construction costs (incurred and to be incurred), used in the calculation of the percentage of completion of real estate ventures; (ii) On sampling basis, we have obtained budget maps – from the commencement of construction of the qualifiable asset until its latest version - and we compared them with the accounting records. We also compared, on sampling basis, the documents supporting the incurred costs, units sold, and amount of sales contracts used in revenue calculation; (iii) Recalculation of revenue recognized based on information extracted from the budgets approved by the engineer responsible for the venture; (iv) analytical reviews of the estimates of costs incurred and to be incurred; and (v) evaluation of the disclosures in the individual and consolidated financial statements.

Based on the findings of the followed audit procedures, we understand that: (i) the assumptions adopted by Management to estimate the costs to be incurred are acceptable in the context of the individual and consolidated financial statements; and (ii) the calculations made by Managementconcerning the percentage of completion correspond to the criteria established in the Circular Letter CVM/SNC/SEP 02/2018.

9

Provisions and contingent liabilities

According to Note 2.2.1 – item c and 16, the Company and its subsidiaries are parties to lawsuits of tax, civil and labor nature, for which Management estimates the involved amounts and records a provision in the individual and consolidated financial statements for the cases it considers that there will be a probable loss, as established in the accounting standard CPC 25 (IAS 17) - Provisions, Contingent Liabilities and Contingent Assets. Besides the lawsuits considered as probable loss, the Company is party to labor and civil lawsuits in progress, for which no provision is recorded, as losses are considered possible or remote by Management, based on the positions of its legal counsel. The risk evaluation and loss estimates are prepared by management based on available evidences and opinion of the Company’s legal counsel, involving high judgement level, given the complexity of themes. The progress of such lawsuits in the many applicable levels may result in change in the evaluation of risk of loss, and significantly impact the recognized provisions and the profit or loss of the Company and its subsidiaries.

Due to the volume of claims, the criteria established for timely identifying the need for recognizing a provision and the existence of significant judgments involved in the process of evaluation and measurement of provisions and disclosures of contingent liabilities, we considered it a key audit matter.

How our audit conducted this matter:

Our audit procedures included, but were not limited to, the following: (i) obtaining, reading and evaluating the mails of the legal counsel of the Company and its subsidiaries, (ii) matching the total contingent liabilities mentioned by the Company’s legal counsel that are expected to lead to a probable outflow of funds with the existing accounting provision in the individual and consolidated financial statements, (iii) inspecting the Management’s meeting minutes, and (iv) analyzing the disclosures made in the notes to the individual and consolidated financial statements.

During the auditing process, there was the need for adjustments that affected the measurement and disclosure of the provision for contingent liabilities. These adjustments also reveal the need for review and improvement in internal controls.

Divestment of the associate Alphaville Urbanismo e Investimento in the Subsidiary SPE GDU Loteamentos Ltda.

As detailed in notes 1.3 and 9.1(i) to the financial statements, the Company entered with Alphaville Urbanismo S.A. (“Alphaville”), Private Equity AE Investimentos e Participações S.A. (“PEAE”) and PEAE’s affiliates into a Contract for Purchase and Sale, Redemption of Shares, Corporate Structuring and Other Covenants, disposing its 21.20% interest in the associate Alphaville Urbanismo. This transaction was recognized by using the acquisition method, which requires, among other procedures, that the Company determines at the effective control acquisition date, the fair value of the transferred consideration, the fair value of acquired assets and assumed liabilities, and the determination of goodwill or gain from bargain purchase. Such procedures usually involve a high judgement level and the need for developing fair value estimates based on calculations and assumptions related to the future performance of the acquired business and that are subject to a high level of uncertainty. In view of the related high judgement level and the impact that any change in assumptions may have on the financial statements, we consider it a key audit matter.

How our audit conducted this matter:

Our audit procedures included, but were not limited to, the following: (i) obtaining and reading the Purchase Price Allocation (PPA) performed by Specialized Company, and, with the support of ourcorporate finance experts, we analyzed the methodology used for measuring at fair value the assets acquired and the liabilities assumed in the transaction, and we evaluated the reasonableness of the assumptions used in the cash flow projection and the calculations made by comparing, when available, with market information, as well as evaluated the main assumptions used and the impacts of possible changes in such assumptions on the determined fair values and their materiality in relation to the financial statements taken as a whole, (ii) inspecting the Management’s meeting minutes and disclosure of Material Facts of the transaction, (iii) accounting mapping and understanding of the records made for divestment and investment, and (iv) analyzing the disclosures made in the notes to the individual and consolidated financial statements.

10

Based on the findings of the performed audit procedures, we understand that the criteria, assumptions and accounting records used by Management were appropriate, and the disclosures are consistent with the obtained data and information.

Other matters

Statement of value added

The individual and consolidated statements of value added (DVA) for the year ended December 31, 2019, prepared under the responsibility of the Company’s Management, and presented as supplementary information for IFRS purposes, were submitted to the audit procedures performed together with the audit of the financial statements of the Company. To form our opinion, we evaluated whether these statements are reconciled with the financial statements and accounting records, as applicable, and whether their formats and contents follow the criteria established in the NTC TG 09 – Statement of Value Added. In our opinion, the accompanying statements of value added were fairly prepared, in all material respects, according to the criteria established in such Standard and are consistent with the individual and consolidated financial statements taken as a whole.

Audit of the amounts related to the comparative individual and consolidated financial statements for the year ended December 31, 2018

The corresponding individual and consolidated financial statements for the year ended December 31, 2018 were previously audited by other independent auditors, who issued a report dated March 28, 2019 without exception, and containing emphasis related to the accounting practices adopted in Brazil applicable to the real estate development entities in Brazil, registered with the CVM.

Other information that accompany the individual and consolidated financial statements and the auditor’s report

The Company’s Management is responsible for such other information, which comprise the Management Report.

Our opinion on the individual and consolidated financial statements does not include the Management Report, and we do not express any type of audit conclusion on such report.

In connection with the audit of the individual and consolidated financial statements, our responsibility is to read the Management Report, and, in doing so, consider whether such report is, in material respects, inconsistent with the financial statements or with the knowledge we obtained in the audit or otherwise appears to be materially misstated If, based on the work we have performed, we conclude that there is material misstatement in the Management Report, we are required to report such fact. We have nothing to report in this regard.

11

Management’s and governance responsibility for the individual and consolidated financial statements

The Company’s Management is responsible for the preparation and fair presentation of the individual and consolidated financial statements in accordance with the accounting practices adopted in Brazil and the International Financial Reporting Standards (IFRS), applicable to real estate development entities in Brazil, registered with the CVM, and for the internal controls that it deemed necessary to enable the preparation of financial statements free from material misstatement, whether due to fraud or error.

In the preparation of the individual and consolidated financial statements, Management is responsible for assessing the Company’s ability to continue as going concern, disclosing, when applicable, the matters related to its going concern, and the use of this accounting basis in the preparation of the financial statements, unless Management intends to liquidate the Company, or cease its operations, or do not have any realistic alternative to avoid the discontinuance of operations.

Those charged with governance of the Company and its subsidiaries are those with responsibility for supervising the process of preparation of the financial statements.

Independent auditor’s responsibilities for the audit of financial statements

Our objectives are to obtain reasonable assurance about whether the individual and consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report including our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Brazilian and International Standards on Auditing will always detect any existing material misstatements. Misstatements can arise from fraud or error and are considered material if, individually or in aggregate, they could be reasonably expected to influence the economic decisions of users taken on the basis of such financial statements.

As part of the audit in accordance with Brazilian and International Standards on Auditing, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

· Identify and assess risks of material misstatements of the individual and consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide basis for our opinion. The risk of not detecting material misstatement resulting from fraud is higher than for one resulting from error, once fraud may involve collusion, forgery, intentional omissions, misrepresentations and the override of internal control.

· Obtain understanding of internal controls relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the internal controls of the Company and its subsidiaries.

· Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

· Conclusion on the appropriateness of management’s use of the going concern basis of accounting, and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubts on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, then we are required to draw attention in our auditor’s report to the related disclosures in the individual and consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidences obtained up to the date of our auditor’s report. However, future events or conditions may cause the Company to cease to continue as a going concern.

12

· Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the individual and consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

· Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the group to express an opinion on the individual and consolidated financial statements. We are responsible for the direction, supervision and performance of the group audit, and, consequently, the audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in the internal control that we identify during our audit.

We also provide to those charged with governance with a statement that we have complied with relevant ethical requirements, including the applicable independence requirements, and communicate with them all relationships and other matters that may reasonably be thought to bear on our independence and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those that were of most significance in the audit of the financial statements of the current year and are therefore the key audit matters. We describe these matters in our auditor’s report, unless the law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

Rio de Janeiro, March 26, 2020.

![]()

Mário Vieira Lopes |

Accountant - CRC- RJ 060.611/O-0 |

13

Gafisa S.A.

Statement of financial position - Assets

Years ended December 31, 2019 and 2018

(In thousands of Brazilian Reais)

|

| Company | Consolidated | ||

Notes | 2019 | 2018 | 2019 | 2018 | |

|

|

|

|

|

|

Current assets |

| ||||

Cash and cash equivalents | 4.1 | 810 | 29,180 | 12,435 | 32,304 |

Short-term investments | 4.2 | 401,243 | 102,827 | 401,895 | 104,856 |

Trade accounts receivable | 5 | 361,649 | 391,557 | 445,303 | 467,992 |

Properties for sale | 6 | 490,419 | 705,123 | 786,660 | 890,460 |

Receivables from related parties | 21.1 | 23,388 | 26,619 | 77,606 | 64,660 |

Prepaid expenses | - | 1,227 | 2,183 | 1,860 | 2,668 |

Non-current assets held for sale | 8.1 | 3,709 | 74,842 | 7,014 | 78,148 |

Other assets | 7 | 52,455 | 35,396 | 67,395 | 42,283 |

Total current assets | 1,334,900 | 1,367,727 | 1,800,168 | 1,683,371 | |

|

|

|

| ||

Non-current assets |

|

|

| ||

Trade accounts receivable | 5 | 98,368 | 155,421 | 112,135 | 174,017 |

Properties for sale | 6 | 230,049 | 139,804 | 279,207 | 198,941 |

Receivables from related parties | 21.1 | 33,416 | 28,409 | 33,416 | 28,409 |

Other assets | 7 | 107,435 | 92,607 | 166,916 | 95,194 |

469,268 | 416,241 | 591,674 | 496,561 | ||

|

|

|

| ||

Investments in ownership interests | 9 | 681,645 | 1,407,516 | 138,802 | 314,505 |

Property and equipment | 10 | 12,147 | 17,284 | 14,159 | 20,073 |

Intangible assets | 11 | 6,552 | 10,999 | 7,084 | 11,770 |

700,344 | 1,435,799 | 160,045 | 346,348 | ||

|

|

|

| ||

Total non-current assets | 1,169,612 | 1,852,040 | 751,719 | 842,909 | |

|

|

|

| ||

|

|

|

| ||

|

|

| |||

|

|

|

| ||

Total assets | 2,504,512 | 3,219,767 | 2,551,887 | 2,526,280 | |

The accompanying notes are an integral part of these financial statements.

14

Gafisa S.A.

Statement of financial position - Liabilities

Years ended December 31, 2019 and 2018

(In thousands of Brazilian Reais)

|

| Company | Consolidated | ||

Notes | 2019 | 2018 | 2019 | 2018 | |

|

|

|

|

| |

Current liabilities |

| ||||

Loans and financing | 12 | 383,647 | 252,919 | 426,124 | 285,612 |

Debentures | 13 | 158,179 | 62,783 | 158,179 | 62,783 |

Payable for purchase of properties and advances from customers | 17 | 89,825 | 82,264 | 129,353 | 113,355 |

Payables for goods and service suppliers | - | 79,106 | 116,948 | 95,450 | 119,847 |

Taxes and contributions | - | 58,556 | 45,667 | 69,868 | 57,276 |

Salaries, payroll charges and profit sharing | - | 11,963 | 6,128 | 12,291 | 6,780 |

Provision for legal claims and commitments | 16 | 139,623 | 138,201 | 140,735 | 138,201 |

Obligations assumed on the assignment of receivables | 14 | 14,755 | 18,554 | 20,526 | 25,046 |

Payables to related parties | 21.1 | 191,364 | 939,603 | 64,384 | 56,164 |

Other payables | 15 | 110,189 | 156,498 | 135,492 | 173,951 |

Total current liabilities | 1,237,207 | 1,819,565 | 1,252,402 | 1,039,015 | |

|

|

|

| ||

Non-current liabilities |

|

|

| ||

Loans and financing | 12 | 107,029 | 307,680 | 107,029 | 338,135 |

Debentures | 13 | 39,346 | 202,883 | 39,346 | 202,883 |

Payable for purchase of properties and advances from customers | 17 | 68,515 | 151,835 | 93,075 | 196,076 |

Deferred income tax and social contributions | 19 | 12,114 | 49,372 | 12,114 | 49,372 |

Provision for legal claims and commitments | 16 | 123,858 | 152,863 | 123,878 | 155,608 |

Obligations assumed on the assignment of receivables | 14 | 16,463 | 26,090 | 19,835 | 32,140 |

Other payables | 15 | 6,272 | 18,162 | 9,065 | 19,860 |

Total non-current liabilities | 373,597 | 908,885 | 404,342 | 994,074 | |

|

|

|

| ||

Equity |

|

|

| ||

Capital | 18.1 | 2,926,280 | 2,521,319 | 2,926,280 | 2,521,319 |

Treasury shares | 18.1 | (43,517) | (58,950) | (43,517) | (58,950) |

Capital reserves and reserve for granting stock options | - | 337,611 | 337,351 | 337,611 | 337,351 |

Accumulated losses | 18.2 | (2,326,666) | (2,308,403) | (2,326,666) | (2,308,403) |

| 893,708 | 491,317 | 893,708 | 491,317 | |

Non-controlling interests | - | - | 1,435 | 1,874 | |

Total equity | 893,708 | 491,317 | 895,143 | 493,191 | |

Total liabilities and equity | 2,504,512 | 3,219,767 | 2,551,887 | 2,526,280 | |

The accompanying notes are an integral part of these financial statements.

15

Gafisa S.A.

Statement of profit or loss

Years ended December 31, 2019 and 2018

(In thousands of Brazilian Reais, except if stated otherwise)

Company | Consolidated | ||||

Notes | 2019 | 2018 | 2019 | 2018 | |

|

|

|

|

|

|

Continuing operations |

|

|

|

| |

Net operating revenue | 22 | 360,589 | 832,328 | 400,465 | 960,891 |

|

|

|

| ||

Operating costs |

|

|

| ||

Real estate development and sales of properties | 23 | (238,714) | (713,836) | (282,684) | (846,169) |

|

|

|

| ||

Gross profit | 121,875 | 118,492 | 117,781 | 114,722 | |

|

|

|

| ||

Operating (expenses) income |

|

|

| ||

Selling expenses | 23 | (12,020) | (73,233) | (14,889) | (84,431) |

General and administrative expenses | 23 | (46,954) | (41,947) | (54,133) | (57,089) |

Income from equity method investments | 9 | 46,863 | (50,929) | (5,003) | (15,483) |

Depreciation and amortization | 10 and 11 | (12,859) | (19,931) | (14,181) | (21,290) |

Derecognition of goodwill from remeasurement of investment | 9.iii | (161,100) | (112,800) | (161,100) | (112,800) |

Other income (expenses), net | 23 | 79,483 | (181,010) | 141,771 | (186,135) |

|

|

|

| ||

Profit (loss) before finance income and expenses and income tax and social contribution | 15,288 | (361,358) | 10,246 | (362,506) | |

|

|

|

| ||

Finance expenses | 24 | (82,920) | (101,562) | (76,830) | (100,074) |

Finance income | 24 | 16,631 | 18,294 | 17,206 | 19,553 |

|

|

|

| ||

Loss before income tax and social contribution | (51,001) | (444,626) | (49,378) | (443,027) | |

|

|

|

| ||

Current income tax and social contribution | - | - | (1,984) | (3,349) | |

Deferred income tax and social contribution | 37,259 | 25,100 | 37,259 | 25,100 | |

|

|

|

| ||

Total Income tax and social contribution | 19.i | 37,259 | 25,100 | 35,275 | 21,751 |

|

|

|

| ||

Net income (loss) from continuing operations | (13,742) | (419,526) | (14,103) | (421,276) | |

|

|

|

| ||

Net income (loss) from discontinued operations |

| - | - | - | - |

|

|

|

|

|

|

Loss for the year |

| (13,742) | (419,526) | (14,103) | (421,276) |

|

|

|

|

|

|

(-)Attributable to: |

|

|

|

|

|

Noncontrolling interests |

| - | - | (361) | (1,750) |

Owners of the parent | (13,742) | (419,526) | (13,742) | (419,526) | |

|

|

|

| ||

Weighted average number of shares (in thousands) | 27 | 68,584 | 41,147 |

|

|

|

|

|

|

| |

Basic loss per thousand shares - In Reais | 27 | (0.200) | (10.196) | ||

From continuing operations |

| (0.200) | (10.196) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Diluted loss per thousand shares - In Reais | 27 | (0.200) | (10.196) | ||

From continuing operations |

| (0.200) | (10.196) |

|

|

|

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

16

Gafisa S.A.

Statement of comprehensive income (loss)

Years ended December 31, 2019 and 2018

(In thousands of Brazilian Reais, except if stated otherwise)

Company | Consolidated | |||

2019 | 2018 | 2019 | 2018 | |

|

|

|

|

|

Loss for the year | (13,742) | (419,526) | (14,103) | (421,276) |

|

|

|

|

|

Total comprehensive income for the year, net of taxes | (13,742) | (419,526) | (14,103) | (421,276) |

|

|

|

|

|

Attributable to: |

| �� |

|

|

Owners of the parent | (13,742) | (419,526) | (13,742) | (419,526) |

Non-controlling interests | - | - | (361) | (1,750) |

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

17

Gafisa S.A.

Statement of changes in equity

Years ended December 31, 2019 and 2018

(In thousands of Brazilian Reais)

|

|

| ||||||

|

|

|

|

|

| |||

|

| Attributed to Owners of the Parent |

|

| ||||

Notes | Capital | Treasury shares | Reserve for capital and granting shares | Accumulated losses | Total Company | Noncontrolling interests | Total Consolidated | |

Balances as of December 31, 2017 | 2,521,152 | (29,089) | 85,448 | (1,866,289) | 711,222 | 3,847 | 715,069 | |

|

| |||||||

Capital increase | 18.1 | 167 | - | 250,599 | - | 250,766 | - | 250,766 |

Stock option plan | 18.3 | - | - | 1,304 | - | 1,304 | - | 1,304 |

Treasury shares sold | 18.1 | - | 2,351 | - | (1,525) | 826 | - | 826 |

Share repurchase program | 18.1 | - | (32,212) |

| (21,063) | (53,275) | - | (53,275) |

Recognition of reserves | - | - | - | - | - | - | (223) | (223) |

Loss for the year | - | - | - | - | (419,526) | (419,526) | (1,750) | (421,276) |

|

| |||||||

Balances as of December 31, 2018 | 2,521,319 | (58,950) | 337,351 | (2,308,403) | 491,317 | 1,874 | 493,191 | |

|

| |||||||

Capital increase | 18.1 | 404,961 | - | (157) | - | 404,804 | - | 404,804 |

Stock option plan | 18.3 | - | - | 417 |

| 417 | - | 417 |

Treasury shares sold | 18.1 | - | 141 | - | 7 | 148 | - | 148 |

Treasury shares cancelled | 18.1 | - | 5,747 | - | (5,747) | - | - | - |

Treasury shares reissued | 18.1 | - | (20,671) | - | 20,671 | - | - | - |

Share repurchase program | 18.1 | - | 30,216 | - | (19,452) | 10,764 | - | 10,764 |

Recognition of reserves | - | - | - | - | - | - | (78) | (78) |

Loss for the year | - | - | - | - | (13,742) | (13,742) | (361) | (14,103) |

|

|

|

|

|

|

|

|

|

Balances as of December 31, 2019 | 2,926,280 | 43,517 | 337,611 | (2,326,666) | 893,708 | 1,435 | 895,143 | |

The accompanying notes are an integral part of these financial statements.

18

Gafisa S.A.

Cash flow statement

Yearsended December 31, 2019 and 2018

(In thousands of Brazilian Reais)

Company | Consolidated | |||

2019 | 2018 | 2019 | 2018 | |

Operating activities |

|

|

| |

Profit (loss) before income tax and social contribution | (51,001) | (444,626) | (49,378) | (443,027) |

Expenses/(income) not affecting cash and cash equivalents: |

|

|

|

|

Depreciation and amortization (Notes 10 and 11) | 12,859 | 19,931 | 14,181 | 21,290 |

Stock option plan expense (Note 18.3) | (2,366) | 1,927 | (2,366) | 1,927 |

Unrealized interests and charges, net | 3,068 | 4,703 | 5,448 | 11,156 |

Warranty provision (Note 15) | (7,521) | (4,130) | (7,521) | (4,130) |

Provision for legal claims and commitments (Note 16) | 9,990 | 172,103 | 8,300 | 172,432 |

Provision for profit sharing (Note 25 (iii)) | 5,000 | (14,750) | 5,000 | (14,750) |

Allowance for expected credit losses and cancelled contracts (Note 5) | (61,460) | (41,828) | (47,257) | (41,827) |

Provision for realization of non-financial assets: |

|

|

|

|

Properties and land for sale (Note 6 and 8) | (37,394) | 15,479 | (36,913) | (74,689) |

Provision for penalties due to delay in construction works (Note 15) | 3,659 | - | 5,283 | - |

Income from equity method investments (Note 9) | (46,863) | 50,929 | 5,003 | 15,483 |

Financial instruments (Note 20) | - | (763) | - | (763) |

Derecognition of goodwill based on inventory surplus (Notes 6 and 9) | 3,000 | 462 | - | - |

Derecognition of goodwill from remeasurement of investment in associate (Note 9) | 161,100 | 112,800 | 161,100 | 112,800 |

Acquisition of subsidiary (Note 9) | (43,954) | - | - | - |

Goodwill based on inventory surplus and gain from bargain purchase (Note 9) | (39,886) | - | - | - |

Assignment of investment shares (Note 9) | 27,843 | - | 2,759 | 28,289 |

|

|

|

|

|

Decrease/(increase) in operating assets |

|

|

|

|

Trade accounts receivable | 134,996 | (149,919) | 115,003 | (95,740) |

Properties for sale and land available for sale | 232,986 | 290,106 | 131,581 | 339,575 |

Other assets | (36,498) | (24,546) | (98,544) | (15,880) |

Prepaid expenses | 956 | 2,847 | 808 | 2,867 |

|

|

|

|

|

Increase/(decrease) in operating liabilities |

|

|

|

|

Payable for purchase of properties and advances from customers | (75,759) | (35,191) | (87,003) | 597 |

Taxes and contributions | 12,888 | 13,553 | 12,592 | 10,846 |

Payables for goods and service suppliers | (48,714) | 40,983 | (37,750) | 32,732 |

Salaries, payroll charges and profit sharing | 835 | (5,119) | 511 | (6,459) |

Other payables | (87,818) | (2,025) | (76,443) | (3,434) |

Transactions with related parties | (56,408) | (24,379) | 21,608 | (14,497) |

Paid taxes | - | - | (1,983) | (3,348) |

Cash and cash equivalents from (used in) operating activities | 13,538 | (21,453) | 44,019 | 31,450 |

|

|

|

|

|

Financing activities |

|

|

|

|

Acquisition of property and equipment and intangible assets (Notes 10 and 11) | (3,275) | (11,065) | (3,581) | (12,511) |

Increase in short-term investments | (360,294) | (1,036,014) | (387,319) | (1,090,796) |

Redemption of short-term investments | 61,878 | 1,044,131 | 90,280 | 1,104,875 |

Investments | - | (7,629) | - | (4,629) |

Cash from (used in) investing activities | (301,691) | (10,577) | (300,620) | (3,061) |

|

|

|

|

|

Financing activities |

|

|

|

|

Increase in loans, financing and debentures | 113,839 | 367,934 | 122,639 | 412,768 |

Payment of loans, financing and debentures - principal | (200,937) | (415,059) | (229,846) | (528,252) |

Payment of loans, financing and debentures - interest | (54,033) | (101,156) | (56,976) | (111,157) |

Loan transactions with related parties | (11,179) | (1,289) | (11,179) | (1,289) |

Treasury shares repurchase program (Note 18.1) | 7,132 | (47,448) | 7,132 | (47,448) |

Capital increase | 404,962 | 167 | 404,962 | 167 |

Subscription and pay-in of common shares | - | 250,599 | - | 250,599 |

Cash and cash equivalents from (used in) financing activities | 259,784 | 53,748 | 236,732 | (24,612) |

|

|

|

|

|

|

|

|

|

|

Net increase/(decrease) in cash and cash equivalents | (28,369) | 21,718 | (19,869) | 3,777 |

|

|

|

|

|

Cash and cash equivalents |

|

|

|

|

At the beginning of the year | 29,179 | 7,461 | 32,304 | 28,527 |

At the end of the year | 810 | 29,179 | 12,435 | 32,304 |

|

|

|

|

|

Net increase (decrease) in cash and cash equivalents | (28,369) | 21,718 | (19,869) | 3,777 |

The accompanying notes are an integral part of these financial statements.

19

Gafisa S.A.

Statement of value added

Years ended December 31, 2019 and 2018

(In thousands of Brazilian Reais)

Company | Consolidated | |||

|

|

|

| |

2019 | 2018 | 2019 | 2018 | |

|

|

|

|

|

|

|

|

|

|

Revenues | 394,252 | 913,648 | 437,289 | 1,048,145 |

Real estate development and sales of properties | 332,792 | 871,820 | 390,032 | 1,006,317 |

Reversal (recognition) of allowance for doubtful accounts and cancelled contracts | 61,460 | 41,828 | 47,257 | 41,828 |

Inputs acquired from third parties (including taxes on purchases) | (314,103) | (943,711) | (294,610) | (1,075,054) |

Operating costs- Real estate development and sales | (208,823) | (616,400) | (244,409) | (733,265) |

Materials, energy, outsourced labor and other | 39,228 | (214,511) | 94,307 | (228,989) |

Gain from bargain purchase | 16,592 | - | 16,592 | - |

Derecognition of goodwill from remeasurement of investment | (161,100) | (112,800) | (161,100) | (112,800) |

|

|

|

|

|

Gross value added | 80,149 | (30,063) | 142,679 | (26,909) |

|

|

|

| |

Depreciation and amortization | (12,859) | (19,931) | (14,181) | (21,290) |

|

|

|

| |

Net value added produced by the entity | 67,290 | (49,994) | 128,498 | (48,199) |

|

|

|

| |

Value added received on transfer | 63,494 | (32,635) | 12,203 | 4,070 |

Income from equity method investments | 46,863 | (50,929) | (5,003) | (15,483) |

Finance income | 16,631 | 18,294 | 17,206 | 19,553 |

|

|

|

| |

Total value added to be distributed | 130,784 | (82,629) | 140,701 | (44,129) |

|

|

|

| |

Value added distribution | 130,784 | (82,629) | 140,701 | (44,129) |

Personnel and payroll charges | 26,851 | 63,730 | 28,429 | 75,300 |

Taxes and contributions | 1,647 | 69,643 | 7,106 | 81,339 |

Interest and rents | 116,028 | 203,524 | 118,908 | 218,758 |

Retained earnings attributable to noncontrolling interests | - | - | 361 | 1,750 |

Incurred losses | (13,742) | (419,526) | (14,103) | (421,276) |

The accompanying notes are an integral part of these financial statements.

20

Gafisa S.A.

Notes to the financial statements --Continued

December 31, 2019

(In thousands of Brazilian Reais, except if stated otherwise)

1. Operations

Gafisa S.A. ("Gafisa" or "Company") is a publicly traded company with registered office at Avenida Presidente Juscelino Kubitschek, nº 1.830, conjunto comercial nº32, 3o andar, Bloco 2, in the city and state of São Paulo, Brazil, and began its operations in 1997 with the objectives of: (i) promoting and managing all forms of real estate ventures on its own behalf or for third parties (in the latter case, as construction company or proxy); (ii) selling and purchasing real estate properties; (iii) providing civil construction and civil engineering services; (iv) developing and implementing marketing strategies related to its own and third party real estate ventures; and (v) investing in other companies who share similar objectives.

The Company enters into real estate development projects with third parties through specific purpose partnerships (“Sociedades de Propósito Específico” or “SPEs”) or through the formation of consortia and condominiums. The subsidiaries significantly share the managerial and operating structures, and corporate, managerial and operating costs with the Company. The SPEs, condominiums and consortia operate solely in the real estate industry and are linked to specific ventures.

The Company has stocks traded at B3 S.A. – Brasil, Bolsa, Balcão (former BM&FBovespa), reporting its information to the Brazilian Securities and Exchange Commission (CVM) and the U.S. Securities and Exchange Commission (SEC). The ADSs were delisted on the NYSE on December 17, 2018, and are currently traded over the counter (OTC).

1.1 Change in Shareholding Structure

On February 14, 2019, 14,600,000 shares held by the group GWI Asset Management S.A., corresponding to a 33.67% stake in the Company, were auctioned. As a result of this auction, Planner Corretora de Valores S.A., by means of the investment funds it manages, started to hold 8,000,000 common shares, corresponding to 18.45% of total common shares issued by the Company.

1.2 Increase in capital

On June 24, 2019, the Board of Directors ratified the increase in capital approved in its meeting held on April 15, 2019, by subscription and payment of 26,273,962 new common shares, of which 12,170,035 are new shares subscribed and paid-in by the shareholders who exercised their preemptive rights at the price of R$5.12, and 14,103,927 are new shares subscribed and paid-in by the shareholders who subscribed the remaining shares of the capital increase at the price of R$4.96, totaling R$62,310 and R$69,954, respectively.

21

Gafisa S.A.

Notes to the financial statements --Continued

December 31, 2019

(In thousands of Brazilian Reais, except if stated otherwise)

1. Operations --Continued

1.2 Increase in capital--Continued

On October 23, 2019, the Board of Directors ratified the capital increase approved in its meeting held on August 15, 2019, by subscription and payment of 48,968,124 new common shares, of which 45,554,148 are new shares, subscribed and paid-in by the shareholders who exercised their preemptive rights at the price of R$5.58, and 3,413,976 new shares, subscribed and paid-in by the shareholders who subscribed the remaining shares of capital increase at the price of R$5.42, totaling R$254,195 and R$18,504, respectively.

1.3 Divestment of associate

On October 21, 2019, the Company disclosed a Material Fact whereby it informed about the Contract for Purchase, Sale and Redemption of Shares, Corporate Restructuring and Other Covenants, entered into with Alphaville Urbanismo S.A. (“Alphaville”), Private Equity AE Investimentos e Participações S.A. (“PEAE”) and PEAE affiliated companies, aimed at establishing the terms and conditions under which it is implementing the divestment of Gafisa’s 21.20% ownership interest in Alphaville. The reduction in the former interest of 30% is a result of an increase in capital made by PEAE’s affiliated companies. The total amount of the transaction is equivalent to R$100,000, settled by offsetting receivables and receipt of the investee shares against assets, measured at fair value. On December 27, 2019, the Company disclosed a Material Fact informing about the completion of this transaction (Note 9.1).

1.4 Letter of Intent - UPCON Acquisition

On December 16, 2019, the Company disclosed a Material Fact whereby it informed that it entered into a non-binding Letter of Intent with UPCON Incorporadora S.A. (“UPCON”), concerning the acquisition by the Company of the totality of shares issued by UPCON. On March 2, 2020, the Company informed that the Administrative Council for Economic Defense (CADE) approved, without restriction, the merger of the totality of shares of UPCON into the Company. Once the required approval stages are completed, UPCON will become a wholly-owned subsidiary of Gafisa. (Note 31.(i)).

22

Gafisa S.A.

Notes to the financial statements --Continued

December 31, 2019

(In thousands of Brazilian Reais, except if stated otherwise)

2. Presentation of financial statements and summary of significant accounting policies

2.1. Basis of presentation and preparation of individual and consolidated financial statements

On March 26, 2020, the Company’s Board of Directors approved these individual and consolidated financial statements of the Company and authorized their disclosure.

The individual financial statements, identified as “Company”, have been prepared and are being presented according to the accounting practices adopted in Brazil, including the pronouncements issued by the Accounting Pronouncements Committee (CPC), approved by the Brazilian Securities and Exchange Commission (CVM) and are disclosed together with the consolidated financial statements.

The consolidated financial statements of the Company have been prepared and are being presented according to the accounting practices adopted in Brazil, including the pronouncements issued by the CPC, approved by the CVM, and according to the International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB).

The individual financial statements of the Company are not considered in compliance with the IFRS, once they consider the capitalization of interest on qualifying assets of investees in the financial statements of the Company. In view of the fact that there is no difference between the Company’s and the consolidated equity and profit or loss, the Company opted for presenting such individual and consolidated information in only one set.

The consolidated financial statements are specifically in compliance with the IFRS applicable to real estate development entities in Brazil, registered with the CVM. The aspects related to the transfer of control in the sale of real estate units follow the understanding of theCompany’s Management, aligned with that expressed by the CVM inCircular Letter/CVM/SNC/SEP 02/2018 about the application of Technical Pronouncement CPC 47 – Revenue from contracts with customers (IFRS 15).

23

Gafisa S.A.

Notes to the financial statements --Continued

December 31, 2019

(In thousands of Brazilian Reais, except if stated otherwise)

2. Presentation of financial statements and summary of significant accounting policies--Continued

2.1. Basis of presentation and preparation of individual and consolidated financial statements--Continued

All material information characteristic of the financial statements, and only it, is being evidenced, and corresponds to those used by Management in its administration.

The presentation of the individual and consolidated Statement of Value Added (DVA) is required by the Brazilian corporate legislation and the accounting practices adopted in Brazil applicable to publicly-held companies and was prepared according to CVM Resolution557, of November 12, 2008, which approved the accounting pronouncement CPC 09 – Statement of Value Added. The IFRS does not require the presentation of this statement. Consequently, under the IFRS, this statement is presented as additional information, without causing harm to the financial statements as a whole.

The financial statements have been prepared on a going concern basis. Management makes an assessment of the Company’s ability to continue as a going concern when preparing the financial statements.

The individual and consolidated financial statements have been prepared based on historical cost, except for those measured at fair value, when indicated.

All amounts reported in the accompanying financial statements are in thousands of reais, except as otherwise stated.

2.1.1. Consolidated financial statements

The consolidated financial statements of the Company include the financial statements of Gafisa and its direct and indirect subsidiaries. The Company controls an entity when it is exposed or is entitled to variable returns arising from its involvement with the entity and has the ability to affect those returns through the power that it exerts over the entity. The existence and the potential effects of voting rights, which are currently exercisable or convertible, are taken into account when evaluating whether the Company controls other entity. The subsidiaries are fully consolidated from the date the control is transferred and the consolidation is discontinued from the date control ceases.

In the Company’s individual financial statements, the financial statements of direct and indirect subsidiaries are recognized using the equity method.

The accounting practices were uniformly adopted in all subsidiaries included in the consolidated financial statements, and the fiscal year of these companies is the same of the Company. See further details in Note 9.

2.1.2. Functional and presentation currency

The functional and presentation currency of the Company is the Brazilian real, mainly because of its revenues and the incurred costs of operations.

24

Gafisa S.A.

Notes to the financial statements --Continued

December 31, 2019

(In thousands of Brazilian Reais, except if stated otherwise)

2. Presentation of financial statements and summary of significant accounting policies--Continued

2.2. Summary of significant accounting policies

2.2.1. Accounting judgments, estimates and assumptions

Accounting estimates and judgments are evaluated on an ongoing basis based on historical experience and other factors, including expectations on future events, considered reasonable under the circumstances.

The preparation of the individual and consolidated financial statements of the Company requires Management to make judgments, estimates and assumptions that affect the reported amounts of revenue, expenses, assets and liabilities, as well as the disclosure of contingent liabilities, at the reporting date of financial statements.

Assets and liabilities subject to estimates and assumptions include the provision for asset impairment, transactions with share-based payment, provision for legal claims, fair value of financial instruments, measurement of the estimated cost of ventures, deferred tax assets, among others.

The main assumptions related to sources of uncertainty over future estimates and other important sources of uncertainty over estimates at the reporting date of the statement of financial position, which may result in different amounts upon settlement are discussed below:

a) Impairment loss of non-financial assets

An impairment loss exists when the asset’s carrying amount exceeds its recoverable amount, which is the higher of an asset’s fair value less costs to sell and its value in use.

The calculation of the fair value less cost to sell is based on available information on sale transactions of similar assets or market prices less additional costs of disposal. The calculation of the value in use is based on the discounted cash flow model.

Cash flows are derived from the budget for the following five years, and do not include uncommitted restructuring activities or future significant investments that will improve the asset basis of the cash-generating unit being tested. The recoverable amount is sensitive to the discount rate used under the discounted cash flow method, the estimated future cash inflows, and to the growth rate used for purposes of extrapolation.

Indefinite lived intangible assets and goodwill attributable to future economic benefit are tested at least annually, and/or when circumstances indicate a decrease in the carrying value. The main assumptions used for determining the recoverable amount of cash-generating units are detailed in Note 9.

25

Gafisa S.A.

Notes to the financial statements --Continued

December 31, 2019

(In thousands of Brazilian Reais, except if stated otherwise)

2. Presentation of financial statements and summary of significant accounting policies--Continued

2.2. Summary of significant accounting policies--Continued

2.2.1. Accounting judgments, estimates and assumptions --Continued

b) Share-based payment transactions

The Company measures the cost of transactions with employees to be settled with shares based on the fair value of equity instruments on the grant date. For cash-settled share-based transactions, the liability is required to be remeasured at the end of each reporting period through the settlement date, recognizing in profit or loss possible changes in fair value, which requires revaluation of the estimates used at the end of each reporting period. The estimate of the fair value of share-based payments requires the determination of the most adequate pricing model to grant equity instruments, which depends on the grant terms and conditions.

It also requires the determination of the most adequate data for the pricing model, including the expected option life, volatility and dividend income, and the corresponding assumptions. The assumptions and models used for estimating the fair value of share-based payments are disclosed in Note 18.3.

c) Provision for legal claims

The Company is party to many lawsuits and administrative proceedings and recognizes a provision for tax, labor and civil claims (Note 16). Provisions are recognized for all claims related to lawsuits which likelihoods of losses are considered probable. Provisions are reviewed and adjusted to take into account the changes in circumstances, such as applicable statutes of limitations, findings of tax inspections, or additional exposures found based on new court issues or decisions.

Contingent liabilities for which losses are considered possible are only disclosed in a note to financial statements, and those for which losses are considered remote are neither accrued nor disclosed.

Contingent assets are recognized only when there are secured guarantees or final and unappealable favorable court decisions. Contingent assets with probable favorable decision are only disclosed in explanatory note.

There are uncertainties inherent in the interpretation of complex tax rules and in the value and timing of future taxable income. In the ordinary course of business, the Company and its subsidiaries are subject to assessments, audits, legal claims and administrative proceedings in civil, tax and labor matters.

26

Gafisa S.A.

Notes to the financial statements --Continued

December 31, 2019

(In thousands of Brazilian Reais, except if stated otherwise)

2. Presentation of financial statements and summary of significant accounting policies--Continued

2.2. Summary of significant accounting policies--Continued

2.2.1. Accounting judgments, estimates and assumptions--Continued

d) Allowance for expected credit losses

The Company makes an in-depth analysis of the contracts with customers outstanding for recognizing the allowance for expected credit losses for all sale contracts of real estate units, and the amounts are accrued as contra-entry to the recognition of the respective development revenue, based on data history of its current operations and estimates. This allowance is calculated based on the percentage of completion of the construction work, the methodology used for recognizing profit or loss (Note 2.2.2). Such analysis is individually made by sale contract, in line with CPC 48 – Financial Instruments, item 5.5.17 (c).

The Company annually reviews its assumptions for recognizing the loss allowance, in the face of the review of the history of its current operations and improvement in its estimates.

e) Warranty provision

The Company and its subsidiaries record a provision to cover expenditures for repairing construction defects covered during the warranty period, is based on the estimate that considers the history of incurred expenditures adjusted by the future expectation, which is regularly reviewed, except for the subsidiaries that operate with third-party companies, which are the own guarantors of the provided construction services. The warranty term provided is five years from the delivery of the venture.

f) Estimated cost of construction

Estimated costs, mainly comprising the incurred and estimated costs for completing the construction works, are regularly reviewed, based on the progress of construction, and any resulting adjustments are recognized in profit or loss of the Company. The effects of such estimate reviews affect profit or loss.

g) Realization of deferred income tax

The initial recognition and further analysis of the realization of a deferred tax asset is carried out when it is probable that a taxable profit will be available in subsequent years to offset the deferred tax asset, based on projections of results, and supported by internal assumptions and future economic scenarios that enable its total or partial use.

27

Gafisa S.A.

Notes to the financial statements --Continued

December 31, 2019

(In thousands of Brazilian Reais, except if stated otherwise)

2. Presentation of financial statements and summary of significant accounting policies--Continued

2.2. Summary of significant accounting policies--Continued

2.2.1. Accounting judgments, estimates and assumptions--Continued

h) Allowance for contract cancellation

The Company recognizes an allowance for contract cancellation when it identifies cash inflow risks. Contracts are monitored to identify the moment when these conditions are mitigated.

While it does not occur, no revenue or cost is recognized in profit or loss, the amounts only being recorded in asset and liability accounts.

The other provisions recognized in the Company are described in Note 2.2.22.

2.2.2. Recognition of revenue and expenses