Exhibit 99.2

Strategic Merger Investor PresentationAugust 15, 2017

Forward-Looking Statements This presentation contains estimates, predictions, opinions, projections and other "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements often use words such as “anticipate,” “believe,” “contemplate,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “project,” “should” “will,” or other words of similar meaning. You can also identify them by the fact that they do not relate strictly to historical or current facts. Such statements include, without limitation, references to Howard Bancorp, Inc.'s (“Howard”) beliefs, plans, objectives, goals, expectations, anticipations, assumptions, estimates, intensions and future performance, including our growth strategy and expansion plans, including potential acquisitions. Forward-looking statements involve known and unknown risks, uncertainties and other factors, which may be beyond or control, and which may cause our actual results, performance or achievements to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements.In addition to factors previously disclosed in Howard’s reports filed with the U.S. Securities and Exchange Commission (the "SEC") and those identified elsewhere in this document, the following factors among others, could cause actual results to differ materially from forward-looking statements or historical performance: ability to obtain regulatory approvals and meet other closing conditions to the merger, including approval by Howard and First Mariner stockholders on the expected terms and schedule; delay in closing the merger; difficulties and delays in integrating the First Mariner business or fully realizing cost savings and other benefits of the merger; business disruption following the merger; changes in asset quality and credit risk; the inability to sustain revenue and earnings growth; customer acceptance of First Mariner products and services; customer disintermediation; the introduction, withdrawal, success and timing of business initiatives; the inability to realize cost savings or revenues or to implement integration plans and other consequences associated with mergers, acquisitions and divestitures; the impact, extent and timing of technological changes, capital management activities, and other actions of the Federal Reserve Board and legislative and regulatory actions and reforms.Annualized, pro forma, projected and estimated numbers are used for illustrative purpose only, are not forecasts and may not reflect actual results.

In connection with the proposed merger, Howard will file with the SEC a Registration Statement on Form S-4 that will include an information statement of First Mariner and a proxy statement/prospectus of Howard, as well as other relevant documents concerning the proposed transaction. This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote or approval. STOCKHOLDERS OF FIRST MARINER AND HOWARD ARE URGED TO READ THE REGISTRATION STATEMENT AND THE JOINT PROXY AND INFORMATION STATEMENT/PROSPECTUS REGARDING THE MERGER WHEN IT BECOMES AVAILABLE AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC BY HOWARD, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION.A free copy of the joint proxy and information statement/prospectus, as well as other filings containing information about Howard, may be obtained at the SEC's Internet site (http://www.sec.gov), when they are filed by Howard. You will also be able to obtain these documents, when they are filed, free of charge, from Howard at www.howardbank.com under the heading "Investor Relations" and then under "SEC Documents". Copies of the joint proxy and information statement/prospectus can also be obtained, when it becomes available, free of charge, by directing a request to Howard Bancorp, Inc., 6011 University Boulevard, Suite 370, Ellicott City, MD 21043, Attention: George C. Coffman, Telephone: (410) 750-0020 or to First Mariner Bank, 3301 Boston Street, Baltimore, MD 21224, Attention: Robert D. Kunisch, Telephone: (410) 573-9651. Participants in the SolicitationFirst Mariner, Howard, and certain of their respective directors, executive officers and certain other members of their management and employees may be deemed to be participants in the solicitation of proxies in connection with the proposed transaction. Information concerning all of the participants in the solicitation will be included in the joint proxy and information statement/prospectus relating to the proposed transaction when it becomes available. Free copies of this document may be obtained as described in the preceding paragraph. Important Additional information andWhere to find it

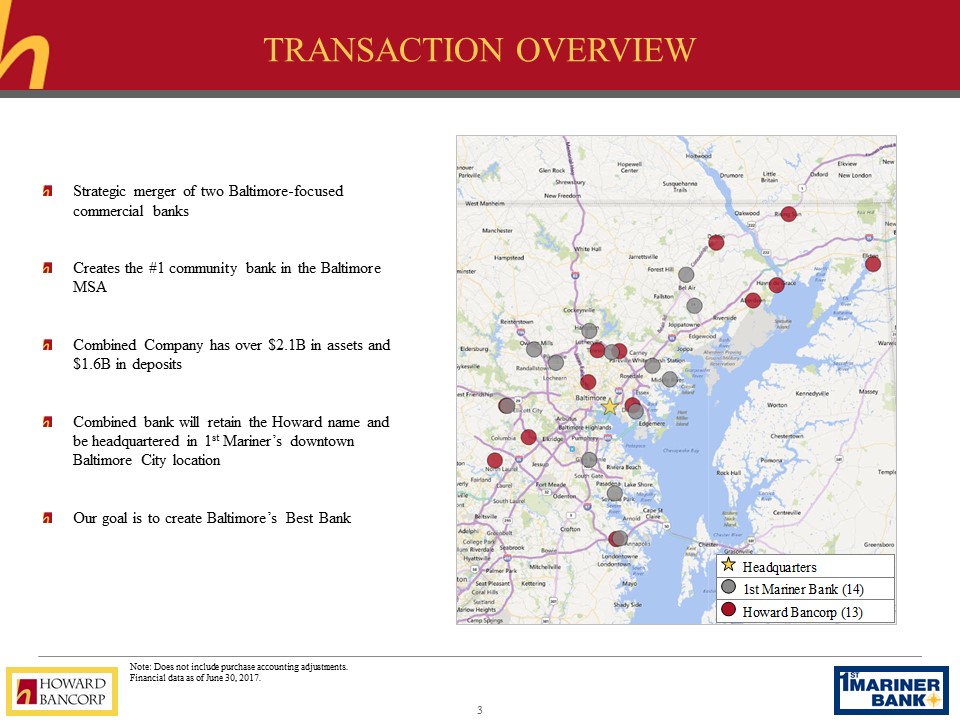

Transaction Overview Strategic merger of two Baltimore-focused commercial banksCreates the #1 community bank in the Baltimore MSACombined Company has over $2.1B in assets and $1.6B in depositsCombined bank will retain the Howard name and be headquartered in 1st Mariner’s downtown Baltimore City locationOur goal is to create Baltimore’s Best Bank Note: Does not include purchase accounting adjustments.Financial data as of June 30, 2017.

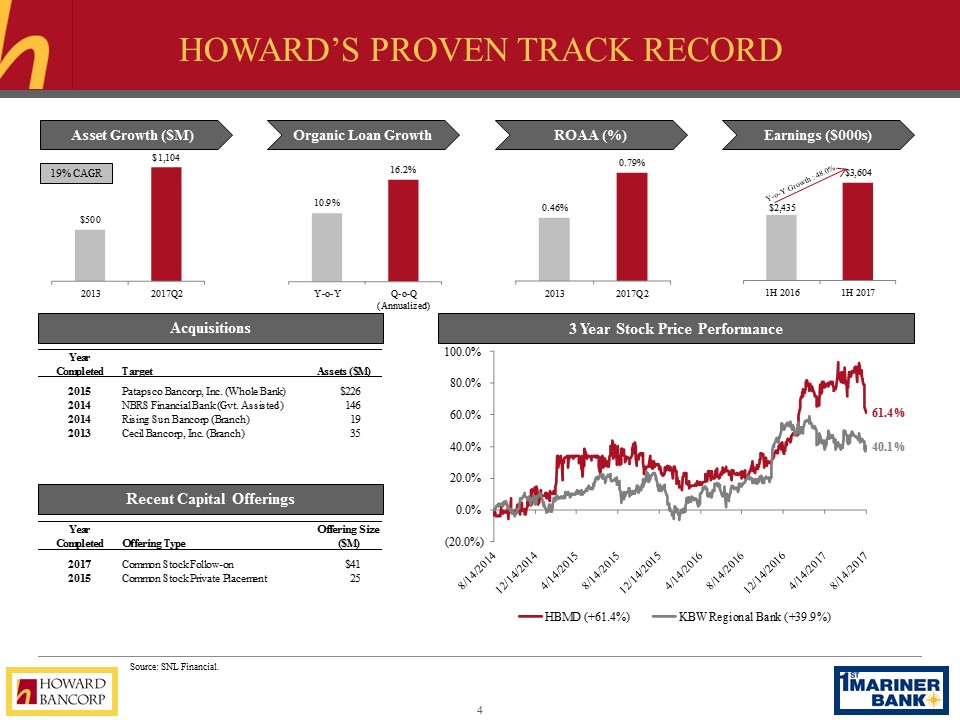

Howard’s Proven Track Record Source: SNL Financial. 3 Year Stock Price Performance Asset Growth ($M) ROAA (%) Earnings ($000s) 19% CAGR Acquisitions Recent Capital Offerings Organic Loan Growth Y-o-Y Growth : 48.0%

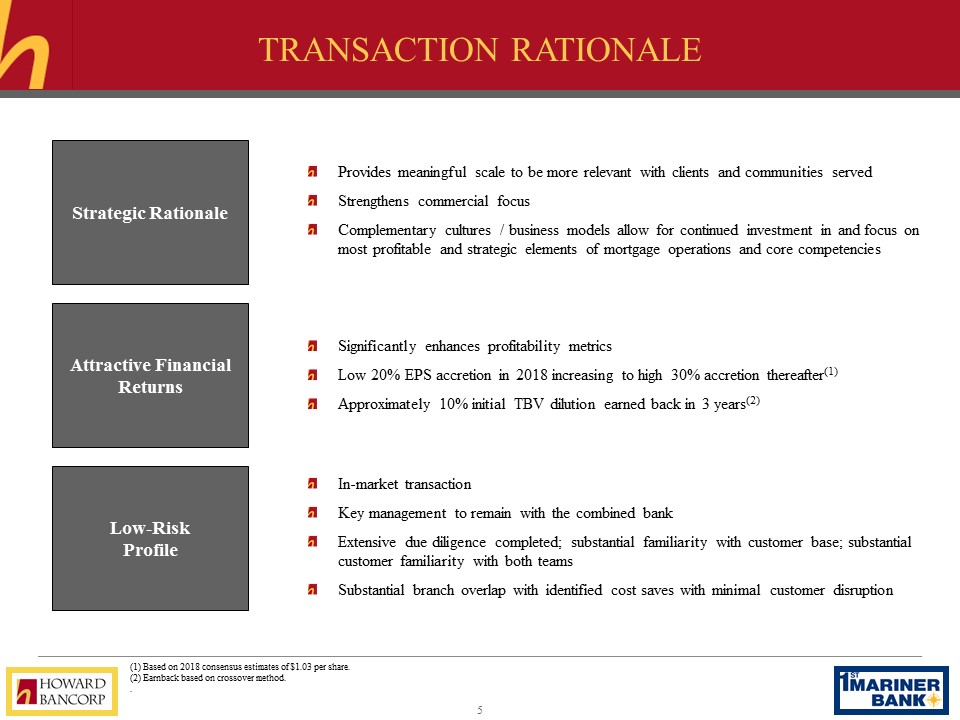

Transaction Rationale Provides meaningful scale to be more relevant with clients and communities servedStrengthens commercial focusComplementary cultures / business models allow for continued investment in and focus on most profitable and strategic elements of mortgage operations and core competencies TBU: Update for most recent financials TBU: New map that fits onto whle right side Strategic Rationale Significantly enhances profitability metricsLow 20% EPS accretion in 2018 increasing to high 30% accretion thereafter(1)Approximately 10% initial TBV dilution earned back in 3 years(2) Attractive Financial Returns In-market transactionKey management to remain with the combined bankExtensive due diligence completed; substantial familiarity with customer base; substantial customer familiarity with both teamsSubstantial branch overlap with identified cost saves with minimal customer disruption Low-Risk Profile (1) Based on 2018 consensus estimates of $1.03 per share.(2) Earnback based on crossover method..

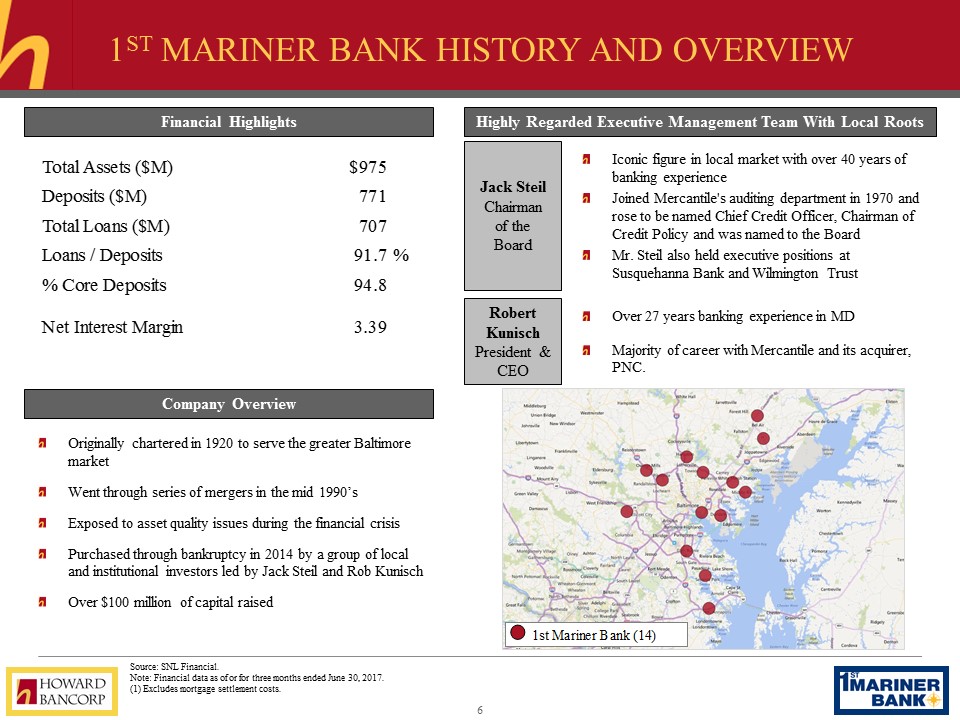

1st mariner bank History and overview Financial Highlights Company Overview Source: SNL Financial.Note: Financial data as of or for three months ended June 30, 2017.(1) Excludes mortgage settlement costs. Originally chartered in 1920 to serve the greater Baltimore marketWent through series of mergers in the mid 1990’sExposed to asset quality issues during the financial crisisPurchased through bankruptcy in 2014 by a group of local and institutional investors led by Jack Steil and Rob KunischOver $100 million of capital raised Highly Regarded Executive Management Team With Local Roots Jack SteilChairman of the Board Iconic figure in local market with over 40 years of banking experienceJoined Mercantile's auditing department in 1970 and rose to be named Chief Credit Officer, Chairman of Credit Policy and was named to the BoardMr. Steil also held executive positions at Susquehanna Bank and Wilmington Trust Robert KunischPresident & CEO Over 27 years banking experience in MDMajority of career with Mercantile and its acquirer, PNC.

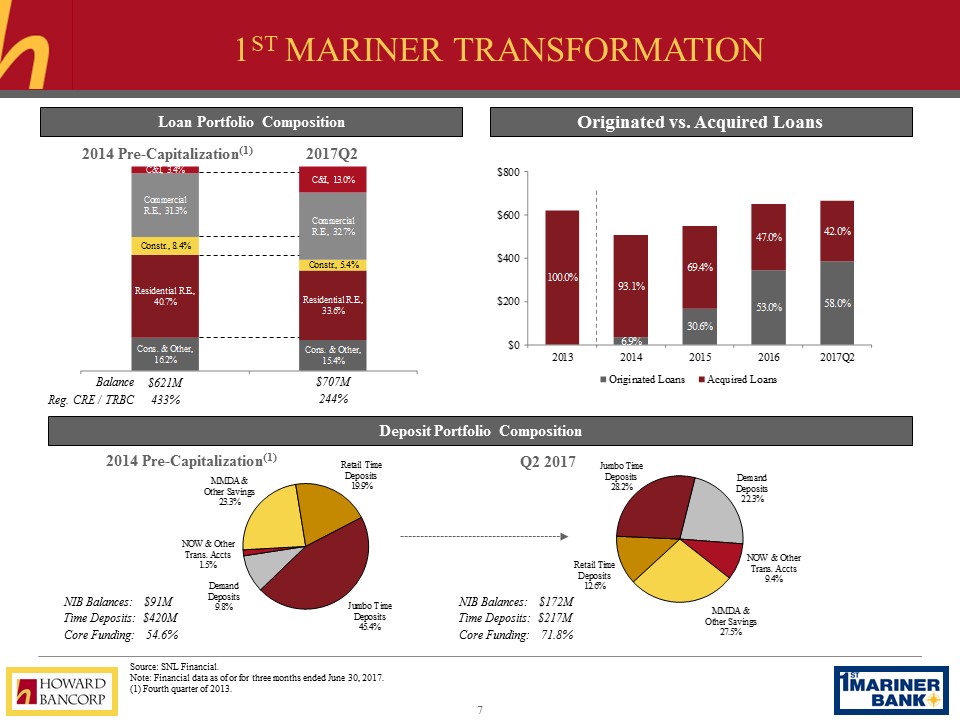

1st Mariner Transformation Source: SNL Financial.Note: Financial data as of or for three months ended June 30, 2017.(1) Fourth quarter of 2013. Loan Portfolio Composition Deposit Portfolio Composition $621M $707M Reg. CRE / TRBC 433% 244% Originated vs. Acquired Loans Q2 2017 2014 Pre-Capitalization(1) Q2 2017 Balance 2017Q2 2014 Pre-Capitalization(1) NIB Balances: $91M 54.6% Core Funding: Time Deposits: $420M NIB Balances: $172M 71.8% Core Funding: Time Deposits: $217M

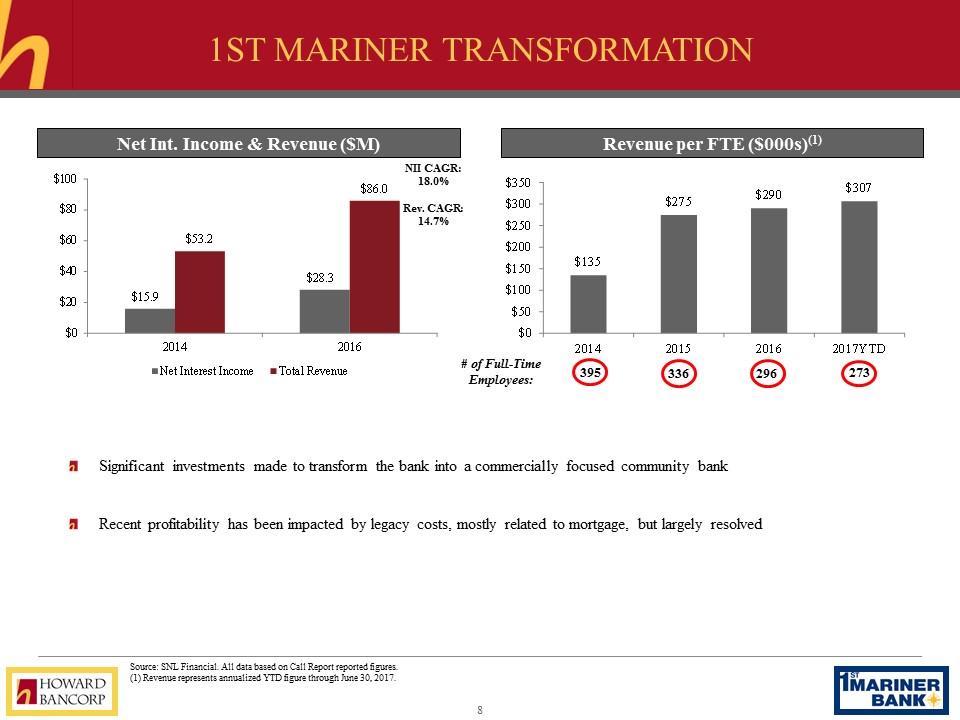

1st Mariner Transformation Source: SNL Financial. All data based on Call Report reported figures.(1) Revenue represents annualized YTD figure through June 30, 2017. Net Int. Income & Revenue ($M) Revenue per FTE ($000s)(1) NII CAGR: 18.0% Rev. CAGR: 14.7% 395 336 296 273 # of Full-Time Employees: Significant investments made to transform the bank into a commercially focused community bankRecent profitability has been impacted by legacy costs, mostly related to mortgage, but largely resolved

Combined Leadership team Name Title YearsExperience Experience Mary Ann Scully Chairman & Chief Executive Officer 37+ Howard Bank, Allfirst, The First National Bank of Maryland; Past President of the Maryland Bankers Association Robert D. Kunisch, Jr. President 27+ 1st Mariner, Wilmington Trust, PNC, Mercantile George Coffman Chief Financial Officer 32+ Howard Bank, Mercantile, Farmers & Mechanics Bank, Sequoia Bank, Citizens Bank of Maryland James D. Witty Chief Commercial Banking Officer 29+ Howard Bank, BB&T, Susquehanna Bank, PNC, Mercantile Robert Altieri Chief Mortgage Officer 32+ Howard Bank, Carrollton Bank / Carrollton Mortgage Services Randy Jones Chief Credit Officer 27+ 1st Mariner, PNC, Mercantile Charles Schwabe Chief Risk Officer 32+ Howard Bank, Allfirst, The First National Bank of Maryland Steve Poynot Chief Administrative Officer 20+ Howard Bank, Mercantile Jack E. Steil Director & Senior Advisor 40+ 1st Mariner, Wilmington Trust, PNC, Mercantile

Combined Board of directors Name Bank Experience Mary Ann Scully - Chairman Howard Howard Bank, Allfirst, The First National Bank of Maryland Robert W. Smith Jr. – Lead Independent Director Howard DLA Piper Richard G. Arnold Howard John E. Ruth Company W. Gary Dorsch 1st Mariner Keyser Capital, Allegiance Capital, Bank of America James T. Dresher, Jr. 1st Mariner Skye Asset Management Howard Feinglass 1st Mariner Priam Capital Michael B. High 1st Mariner Patriot Financial Partners, Harleysville National Corporation John J. Keenan Howard KPMG Robert D. Kunisch, Jr. 1st Mariner 1st Mariner, PNC, Mercantile Paul I. Latta Howard ERIS Technologies, The Rouse Company Kenneth C. Lundeen Howard Environmental Reclamation Company, C.J. Langenfelder & Son Thomas P. O’Neill Howard Hertzbach & Co, Wolpoff & Co, Patapsco Bancorp Donna Hill Staton Howard DLA Piper, Piper & Marbury, Deputy Attorney General - Maryland Jack E. Steil 1st Mariner 1st Mariner, Wilmington Trust, PNC, Mercantile

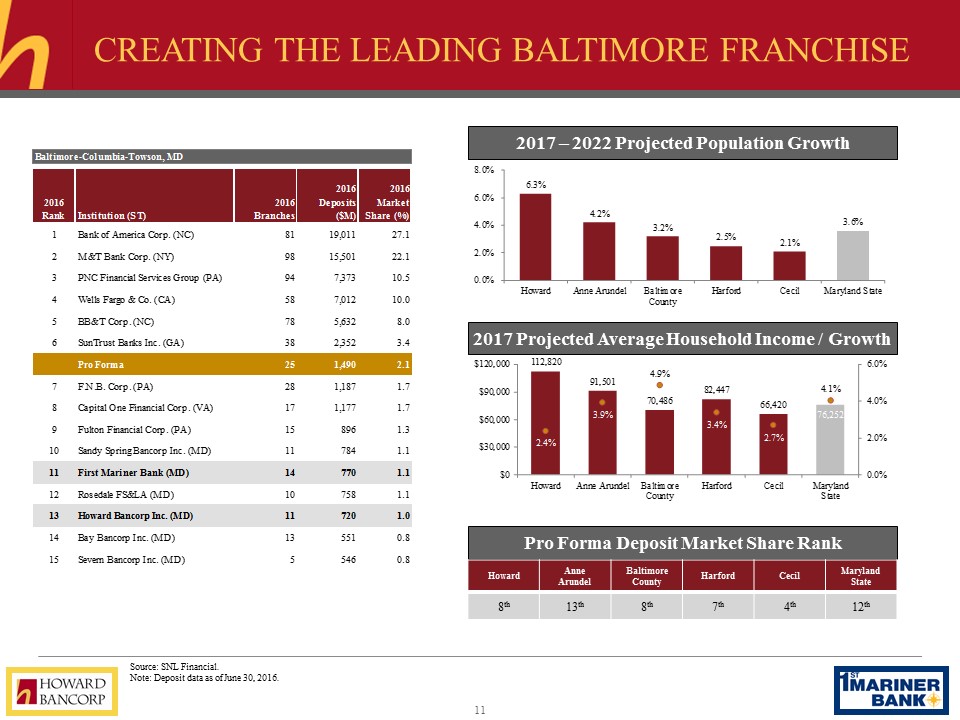

Future results driven by operating leverage Source: SNL Financial. Note: Deposit data as of June 30, 2016. Future results driven by operating leverage Project BBBB Pro Forma Franchise Creating the leading Baltimore franchise 2017 – 2022 Projected Population Growth 2017 Projected Average Household Income / Growth Pro Forma Deposit Market Share Rank Howard Anne Arundel Baltimore County Harford Cecil Maryland State 8th 13th 8th 7th 4th 12th

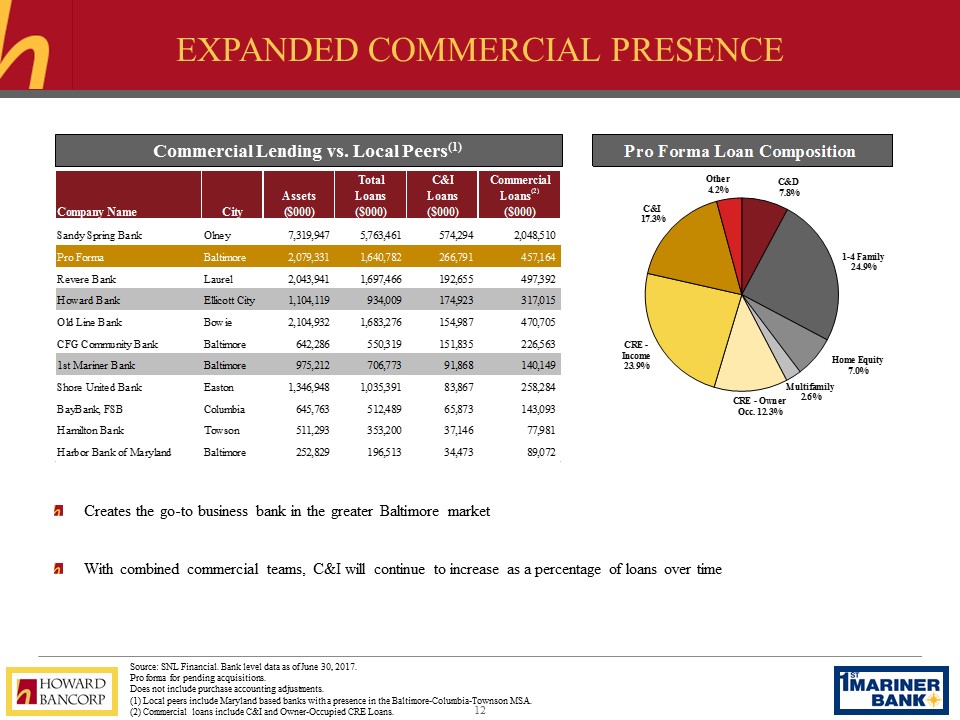

Expanded commercial presence (1) Source: SNL Financial. Bank level data as of June 30, 2017. Pro forma for pending acquisitions.Does not include purchase accounting adjustments.(1) Local peers include Maryland based banks with a presence in the Baltimore-Columbia-Townson MSA.(2) Commercial loans include C&I and Owner-Occupied CRE Loans. Commercial Lending vs. Local Peers(1) Creates the go-to business bank in the greater Baltimore marketWith combined commercial teams, C&I will continue to increase as a percentage of loans over time

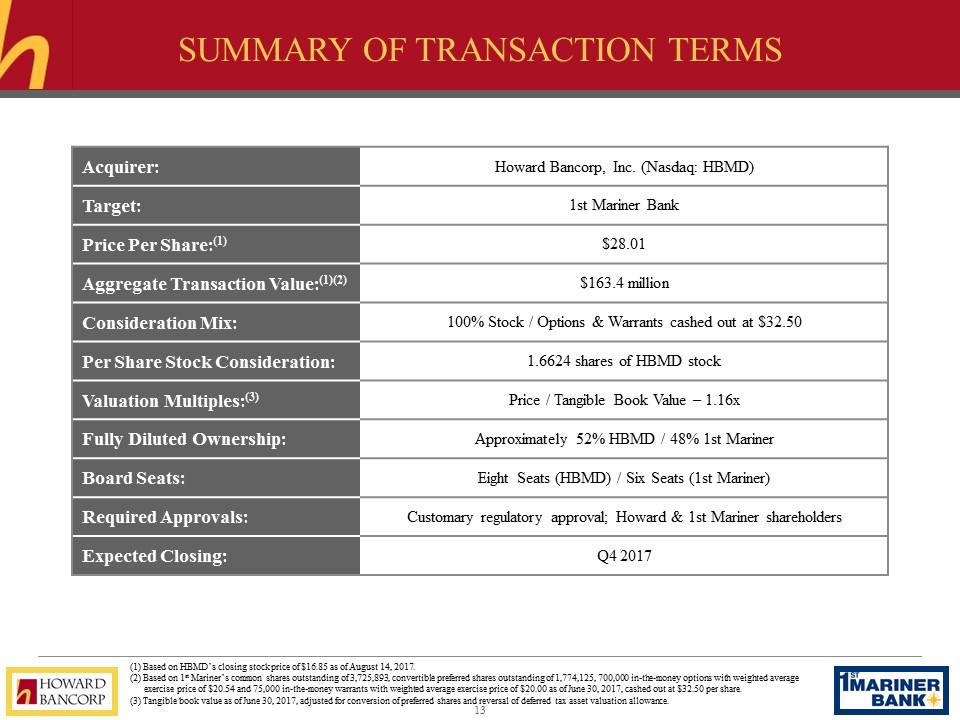

Summary of Transaction Terms (1) Based on HBMD’s closing stock price of $16.85 as of August 14, 2017.(2) Based on 1st Mariner’s common shares outstanding of 3,725,893, convertible preferred shares outstanding of 1,774,125, 700,000 in-the-money options with weighted average exercise price of $20.54 and 75,000 in-the-money warrants with weighted average exercise price of $20.00 as of June 30, 2017, cashed out at $32.50 per share.(3) Tangible book value as of June 30, 2017, adjusted for conversion of preferred shares and reversal of deferred tax asset valuation allowance. Acquirer: Howard Bancorp, Inc. (Nasdaq: HBMD) Target: 1st Mariner Bank Price Per Share:(1) $28.01 Aggregate Transaction Value:(1)(2) $163.4 million Consideration Mix: 100% Stock / Options & Warrants cashed out at $32.50 Per Share Stock Consideration: 1.6624 shares of HBMD stock Valuation Multiples:(3) Price / Tangible Book Value – 1.16x Fully Diluted Ownership: Approximately 52% HBMD / 48% 1st Mariner Board Seats: Eight Seats (HBMD) / Six Seats (1st Mariner) Required Approvals: Customary regulatory approval; Howard & 1st Mariner shareholders Expected Closing: Q4 2017

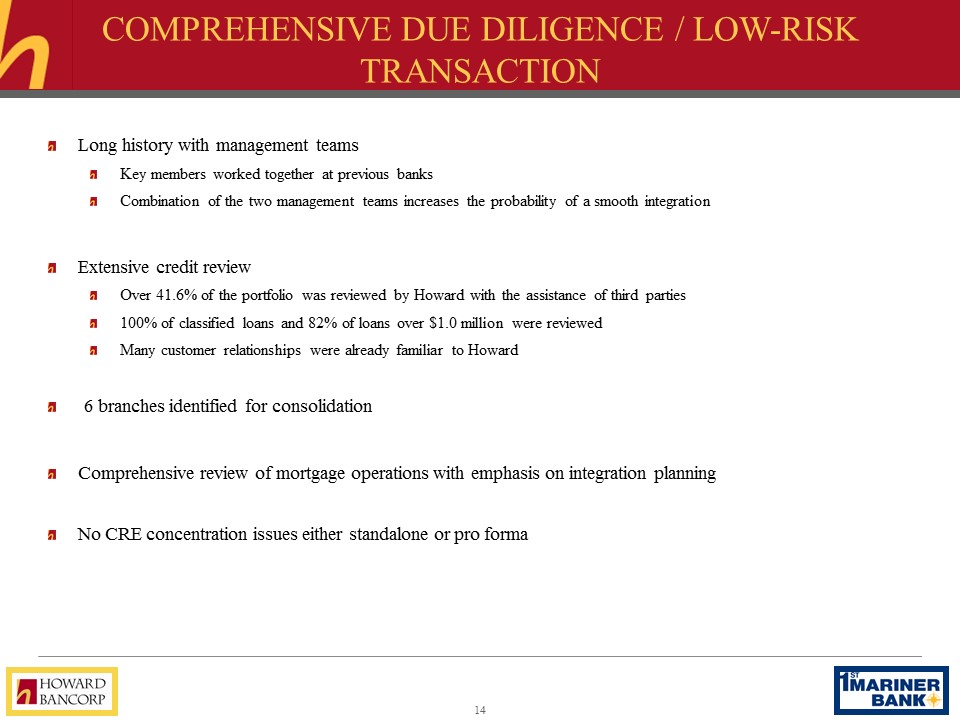

Strong Institutional sponsorship Future results driven by operating leverage Future results driven by operating leverage Project BBBB Pro Forma Franchise Comprehensive due diligence / Low-Risk Transaction Long history with management teamsKey members worked together at previous banksCombination of the two management teams increases the probability of a smooth integrationExtensive credit reviewOver 41.6% of the portfolio was reviewed by Howard with the assistance of third parties100% of classified loans and 82% of loans over $1.0 million were reviewedMany customer relationships were already familiar to Howard6 branches identified for consolidationComprehensive review of mortgage operations with emphasis on integration planningNo CRE concentration issues either standalone or pro forma

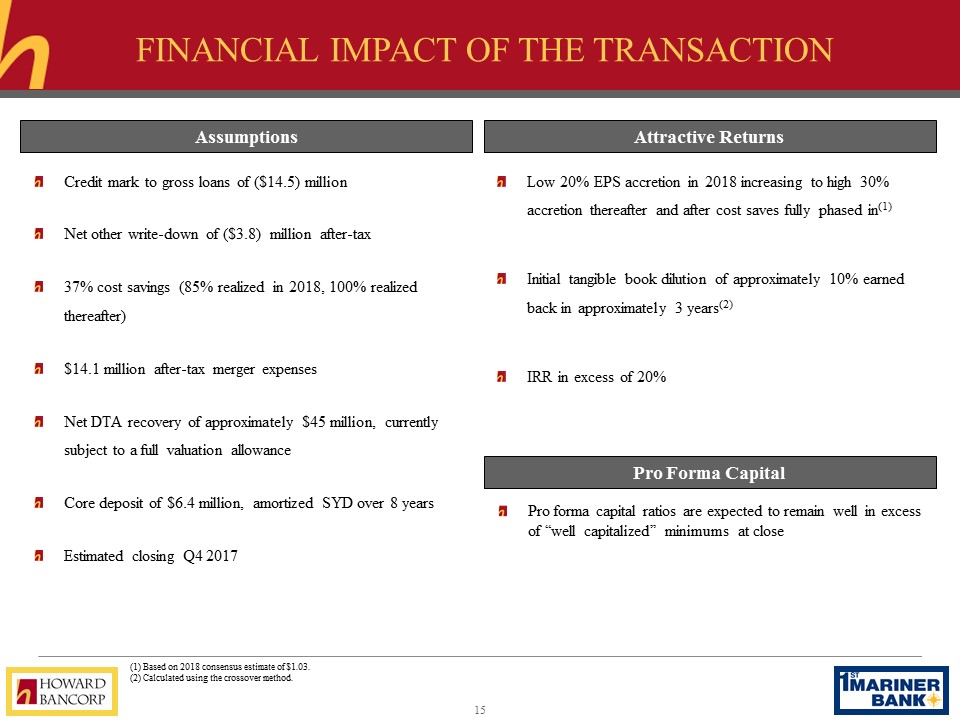

Financial Impact of the transaction Credit mark to gross loans of ($14.5) millionNet other write-down of ($3.8) million after-tax37% cost savings (85% realized in 2018, 100% realized thereafter)$14.1 million after-tax merger expensesNet DTA recovery of approximately $45 million, currently subject to a full valuation allowanceCore deposit of $6.4 million, amortized SYD over 8 yearsEstimated closing Q4 2017 Low 20% EPS accretion in 2018 increasing to high 30% accretion thereafter and after cost saves fully phased in(1)Initial tangible book dilution of approximately 10% earned back in approximately 3 years(2)IRR in excess of 20% Assumptions Attractive Returns Pro Forma Capital Pro forma capital ratios are expected to remain well in excess of “well capitalized” minimums at close (1) Based on 2018 consensus estimate of $1.03.(2) Calculated using the crossover method.

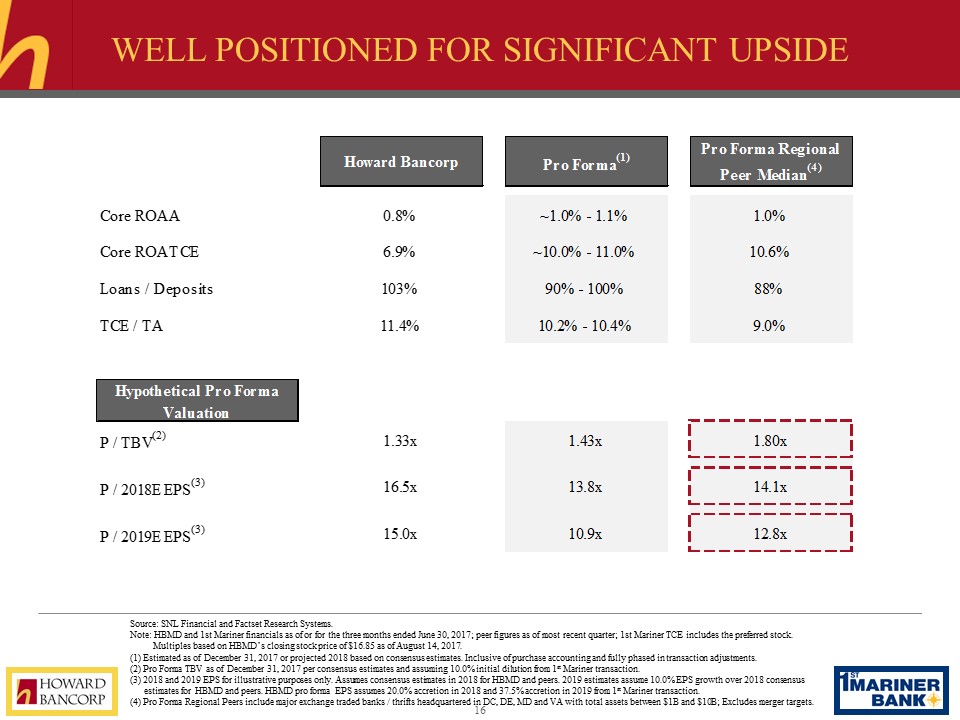

Well Positioned For Significant Upside TBU: Update for most recent financials TBU: New map that fits onto whle right side Source: SNL Financial and Factset Research Systems.Note: HBMD and 1st Mariner financials as of or for the three months ended June 30, 2017; peer figures as of most recent quarter; 1st Mariner TCE includes the preferred stock. Multiples based on HBMD’s closing stock price of $16.85 as of August 14, 2017.(1) Estimated as of December 31, 2017 or projected 2018 based on consensus estimates. Inclusive of purchase accounting and fully phased in transaction adjustments.(2) Pro Forma TBV as of December 31, 2017 per consensus estimates and assuming 10.0% initial dilution from 1st Mariner transaction. (3) 2018 and 2019 EPS for illustrative purposes only. Assumes consensus estimates in 2018 for HBMD and peers. 2019 estimates assume 10.0% EPS growth over 2018 consensus estimates for HBMD and peers. HBMD pro forma EPS assumes 20.0% accretion in 2018 and 37.5% accretion in 2019 from 1st Mariner transaction. (4) Pro Forma Regional Peers include major exchange traded banks / thrifts headquartered in DC, DE, MD and VA with total assets between $1B and $10B; Excludes merger targets.

Concluding Remarks Attractive combination of the two best commercial banks in the Baltimore marketCreates the go-to bank in a sizable metro marketCultural similarity and integration of management teams lowers execution riskFinancially compelling for both sets of shareholders