UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number 1-33332

WABCO Holdings Inc.

(Exact name of Registrant as specified in its charter)

| | |

| Delaware | | 20-8481962 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

Chaussée de Wavre, 1789 1160 Brussels, Belgium | | |

One Centennial Avenue, P.O. Box 6820, Piscataway, NJ | | 08855-6820 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code +32 2 663 98 00

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

Common stock, par value $0.01 per share | | New York Stock Exchange |

| |

Securities registered pursuant to Section 12(g) of the Act: | | |

Title of each class | | |

None | | |

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “non-accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (check one).

| | |

Large Accelerated filer x | | Accelerated filer ¨ |

Non-Accelerated filer ¨ | | Smaller reporting company ¨ |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

The aggregate market value of the voting stock (Common Stock) held by non-affiliates of the Registrant as of the close of business on June 30, 2009 was approximately $1.2 billion based on the closing sale price of the common stock on the New York Stock Exchange on that date. The Registrant does not have any non-voting common equity.

Indicate the number of shares outstanding of the Registrant’s common stock, as of the latest practicable date.

| | |

Common stock, $.01 par value, outstanding at | | |

February 12, 2010 | | 64,087,311 shares |

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information from certain portions of the Registrant’s definitive proxy statement to be filed with the Securities and Exchange Commission within 120 days after the fiscal year end of December 31, 2009.

TABLE OF CONTENTS

i

Information Concerning Forward Looking Statements

Certain of the statements contained in this report (other than the historical financial data and other statements of historical fact), including, without limitation, statements as to management’s expectations and beliefs, are forward-looking statements. These forward-looking statements were based on various facts and were derived utilizing numerous important assumptions and other important factors, and changes in such facts, assumptions or factors could cause actual results to differ materially from those in the forward-looking statements. Forward-looking statements include the information concerning our future financial performance, financial condition, liquidity, business strategy, projected plans and objectives. Statements preceded by, followed by or that otherwise include the words “believes,” “expects,” “anticipates,” “strategies,” “prospects,” “intends,” “projects,” “estimates,” “plans,” “may increase,” “may fluctuate,” and similar expression or future or conditional verbs such as “will,” “should,” “would,” “may” and “could” are generally forward looking in nature and not historical facts. This report includes important information as to risk factors in “Item 1. Business”, “Item 1A. Risk Factors”, and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Many important factors could cause actual results to differ materially from management’s expectations, including:

| | • | | the actual level of commercial vehicle production in our end-markets; |

| | • | | adverse developments in the business of our key customers; |

| | • | | periodic changes to contingent liabilities, including those associated with litigation matters and government investigations; |

| | • | | the amount of the fine assessed by the European Commission and our ability to fund the payment of the fine; |

| | • | | our ability to access credit markets or capital markets on a favorable basis or at all; |

| | • | | continued turmoil and instability in the credit markets; |

| | • | | adverse developments in general business, economic and political conditions or any outbreak or escalation of hostilities on a national, regional or international basis; |

| | • | | changes in international or U.S. economic conditions, such as inflation, interest rate fluctuations, foreign exchange rate fluctuations or recessions in our markets; |

| | • | | unpredictable difficulties or delays in the development of new product technology; |

| | • | | pricing changes to our supplies or products or those of our competitors, and other competitive pressures on pricing and sales; |

| | • | | changes in the environmental regulations that affect our current and future products; |

| | • | | competition in our existing and future lines of business and the financial resources of competitors; |

| | • | | our failure to comply with regulations and any changes in regulations; |

| | • | | our failure to complete potential future acquisitions or to realize benefits from completed acquisitions; |

| | • | | our inability to implement our growth plan; |

| | • | | the loss of any of our senior management; |

| | • | | difficulties in obtaining or retaining the management and other human resource competencies that we need to achieve our business objectives; |

| | • | | risks inherent in operating in foreign countries, including exposure to local economic conditions, government regulation, currency restrictions and other restraints, changes in tax laws, expropriation, political instability and diminished ability to legally enforce our contractual rights. |

We undertake no obligation to release publicly any revisions to any forward-looking statements, to report events or to report the occurrence of unanticipated events unless we are required to do so by law.

1

Overview

Except as otherwise indicated or unless context otherwise requires “WABCO”, “WABCO Holdings Inc.,” “we,” “us,” “our,” and “our company” refer to WABCO Holdings Inc. and its consolidated subsidiaries.

WABCO is a leading provider of electronic, mechanical and mechatronic products for the world’s leading commercial truck, trailer, bus and passenger car manufacturers. We manufacture and sell control systems, including advanced braking, stability, suspension, transmission control and air compressing and processing systems, that improve vehicle performance and safety and reduce overall vehicle operating costs. We estimate that our products are included in approximately two out of three commercial vehicles with advanced vehicle control systems and offered in sophisticated, niche applications in cars and sport utility vehicles (SUVs). We continue to grow in more parts of the world as we provide more components and systems throughout the life of a vehicle, from design and development to the aftermarket.

History of Our Company

WABCO was founded in the United States in 1869 as Westinghouse Air Brake Company. We were purchased by American Standard Companies Inc. (or “American Standard”) in 1968 and operated as the Vehicle Control Systems business division within American Standard until we were spun off from American Standard on July 31, 2007. Subsequent to our spin-off, American Standard changed its name to Trane Inc., which we herein refer to as “Trane”. On June 5, 2008, Trane was acquired in a merger with Ingersoll-Rand Company Limited (“Ingersoll Rand”) and exists today as a wholly owned subsidiary of Ingersoll-Rand.

The Separation of WABCO from Trane

The spin-off by Trane of its Vehicle Control Systems business became effective on July 31, 2007, through a distribution of 100% of the common stock of WABCO to Trane’s shareholders (the “Distribution”). The Distribution was effected through a separation and distribution agreement pursuant to which Trane distributed all of the shares of WABCO common stock as a dividend on Trane common stock, in the amount of one share of WABCO common stock for every three shares of outstanding Trane common stock to each shareholder on the record date. Trane received a private letter ruling from the Internal Revenue Service and an opinion from tax counsel indicating that the spin-off was tax free to the shareholders of Trane and WABCO. Please refer to Item 1A. “Risk Factors” below for information on the tax risks associated with the spin-off from Trane.

Our Relationship with Trane

On July 16, 2007, we entered into definitive agreements with Trane that, among other things, set forth the terms and conditions of our separation from Trane (“Separation”) and provide a framework for the relationship between WABCO and Trane following the Separation. The agreements provide for the allocation between WABCO and Trane of assets, liabilities and obligations attributable to periods prior to the Separation. In addition to the Separation and Distribution Agreement, which contains many of the key provisions related to the Separation of WABCO and the Distribution of WABCO’s common stock to Trane’s shareholders, the parties also entered into a Tax Sharing Agreement, a Transition Services Agreement, an Employee Matters Agreement and an Indemnification and Cooperation Agreement. A summary of the agreements with continued relevance is set forth below:

Separation and Distribution Agreement – sets forth WABCO’s agreements with Trane regarding principal transactions necessary to separate WABCO from Trane. This agreement also sets forth the other agreements that govern certain aspects of WABCO’s relationship with Trane after the completion of the Separation from Trane and provides for the allocation of certain assets to be transferred, liabilities to be assumed and contracts to be assigned to WABCO and Trane as part of the Separation.

Tax Sharing Agreement – governs the parties’ respective rights, responsibilities and obligations after the Distribution with respect to taxes, including ordinary course of business taxes and taxes, if any, incurred as a result of any failure of the Distribution of all of the common shares of WABCO to qualify as a tax-free distribution for U.S. federal income tax purposes within the meaning of Section 355 of the Internal Revenue Code of 1986, as amended.

2

Indemnification and Cooperation Agreement – Pursuant to this agreement, WABCO Europe BVBA (an indirect wholly-owned subsidiary of WABCO), has agreed to be responsible for and to indemnify certain American Standardand Bath and Kitchen companies which were named in a Statement of Objections alleging infringements of European Union competition regulations, as well as their respective affiliates, successors and assigns, against any fines related to the European Commission’s investigation, as outlined in the Statement of Objections received by American Standard and certain of its European subsidiaries on March 28, 2007. For further detail, please refer to Legal Proceedings below and Note 13—Warranties, Guarantees, Commitments and Contingencies in the notes to the consolidated financial statements.

Products and Services

We develop, manufacture and sell advanced braking, stability, suspension and transmission control systems primarily for commercial vehicles. Our largest-selling products are pneumatic anti-lock braking systems (ABS), electronic braking systems (EBS), automated manual transmission systems, air disk brakes, and a large variety of conventional mechanical products such as actuators, air compressors and air control valves for heavy- and medium-sized trucks, trailers and buses. We also supply advanced electronic suspension controls and vacuum pumps to the car and SUV markets in Europe, North America and Asia. In addition, we sell replacement parts, diagnostic tools, training and other services to commercial vehicle aftermarket distributors, repair shops, and fleet operators.

WABCO is a leader in improving highway safety, with products that help drivers prevent accidents by enhancing vehicle responsiveness and stability. For example, we offer a stability control system for trucks and buses that constantly monitors the vehicle’s motion and dynamic stability. If the system detects vehicle instability, such as the driver swerving to avoid another vehicle, it responds by applying the brakes at specific wheels, or slowing the vehicle down to minimize the risk of instability or a rollover. Additionally, we have created the commercial vehicle industry’s first autonomous emergency braking system, OnGuardMAX™, which assists in collision imminent situations with moving or stopped vehicles. This highly technological system fuses data from video and laser sensors, integrates with braking, the engine, transmission and stability control systems to assist the driver in reducing risks of collision.

3

Our key product groups and functions are described below.

| | |

| WABCO KEY PRODUCT GROUPS |

| SYSTEM / PRODUCT | | FUNCTION |

Actuator | | Converts Energy Stored in Compressed Air into Mechanical Force Applied to Foundation Brake to Slow or Stop Commercial Vehicles |

Air Compressor and Air Processing/Air Management System | |

Provides Compressed, Dried Air for Braking, Suspension and other Pneumatic Systems on Trucks, Buses and Trailers |

Foundation Brake | | Transmits Braking Force to a Disc or Drum (Connected to the Wheel) to Slow, Stop or Hold Vehicles |

Anti-lock Braking System (ABS) | | Prevents Wheel Locking during Braking to Ensure Steerability and Stability |

Conventional Braking System | | Mechanical and Pneumatic Devices for Control of Braking Systems in Commercial Vehicles |

Electronic Braking System (EBS) | | Electronic Controls of Braking Systems for Commercial Vehicles |

Electronic and Conventional Air Suspension Systems | | Level Control of Air Springs in Trucks, Buses, Trailers and Cars |

Transmission Automation | | Automates Transmission Gear Shifting for Trucks and Buses |

Vehicle Electronic Architecture (VEA) | | Central Electronic Modules Integrating Multiple Vehicle Control Functions |

Vehicle Electronic Stability Control (ESC) and Roll Stability Support (RSS) | |

Enhances Driving Stability |

Key Markets and Trends

Electronically controlled products and systems are important for the growth of our business. The market for these products is driven primarily by the growing electronics content of control systems in commercial vehicles. The electronics content has been increasing steadily with each successive platform introduction, as original equipment manufacturers (OEMs) look to improve safety and performance through added functionalities, and meet evolving regulatory safety standards. Overall the trends in commercial vehicle design show a shift in demand towards electronics content. Although the pace varies, this is a trend in all major geographies, and braking systems are part of this broader shift from conventional to advanced electronic systems. In addition to increasing safety, improving stopping distances, and reducing installation complexity, advanced EBS also allow for new functionality to be introduced into vehicles at a lower price. The new functionality includes stability control, adaptive cruise control, automated transmission controls, brake performance warning, vehicle diagnostics, driver assistance systems and engine braking/speed control. Adaptive cruise control uses sensors to detect proximity to other vehicles and automatically adjusts speed. Automated transmission controls reduce the amount of gear shifting, resulting in less physical effort and training required for drivers, less component wear, fewer parts, better fuel efficiency, and enhanced driver safety and comfort.

A fundamental driver of demand for our products is commercial truck production. Commercial truck production generally follows a multi-year cyclical pattern. While the number of new commercial vehicles built fluctuates each year, we have over the last five years demonstrated the ability to grow in excess of these fluctuations by increasing the amount of content on each vehicle. Due to the unprecedented decline in the commercial vehicle industry in 2009, WABCO’s European sales to truck and bus (“T&B”) OEM customers were down 58%, which still outperformed Western European T&B production that declined 62% in 2009. During the five year period through

4

2009, WABCO’s European sales to T&B OEM customers, excluding the impact of foreign currency exchange rates, outperformed the rate of Western European T&B production by an average of 3% per year.

| | | | | | | | | | | | | | | |

Year to Year Change | | 2005 | | | 2006 | | | 2007 | | | 2008 | | | 2009 | |

Sales to European T&B OEMs (at a constant FX rate) | | +6 | % | | +10 | % | | +12 | % | | +4 | % | | -58 | % |

Western European T&B Production | | +5 | % | | +5 | % | | +10 | % | | +4 | % | | -62 | % |

Customers

We sell our products primarily to four groups of customers around the world: truck and bus (OEMs), trailer (OEMs), commercial vehicle aftermarket distributors for replacement parts and services, and major car manufacturers. Our largest customer is Daimler, which accounts for approximately 12% of our sales. Other key customers include Arvin Meritor, Ashok Leyland, China National Heavy Truck Corporation (CNHTC), Cummins, Fiat (Iveco), Hino, Hyundai, MAN Nutzfahrzeuge AG (MAN), Meritor WABCO (a joint venture), Nissan Diesel, Paccar (DAF Trucks N.V. (DAF), Kenworth, Leyland and Peterbilt), Otto Sauer Achsenfabrik (SAF), Scania, TATA Motors, Volvo (Mack and Renault) and ZF Friedrichshafen AG (ZF). For the fiscal year ended December 31, 2009, our top 10 customers accounted for approximately 48% of our sales.

The largest group of our customers, representing approximately 55% of sales (62% in 2008), consists of truck and bus OEMs who are large, increasingly global and few in numbers due to industry consolidation. As truck and bus OEMs grow globally, they expect suppliers to grow with them beyond their traditional markets and become reliable partners, especially in the development of new technologies. WABCO has a strong reputation for technological innovation and often collaborates closely with major OEM customers to design and develop the technologies used in their products. Our products play an important role in vehicle safety and there are few other suppliers who compete across the breadth of products that we supply.

The second largest group, representing approximately 32% of sales (21% in 2008), consists of the commercial vehicle aftermarket distributor network that provides replacement parts to commercial vehicle operators. This distributor network is a fragmented and diverse group of customers, covering a broad spectrum from large OE-affiliated or owned distributors to small independent local distributors. The increasing number of commercial trucks in operation world-wide that are equipped with our products continuously increases demand for replacement parts and services, thus generating a growing stream of recurring aftermarket sales. Additionally, we continue to develop an array of service offerings such as diagnostics, training and other services to repair shops and fleet operators that will further enhance our presence and growth in the commercial vehicle aftermarket.

The next largest group, representing approximately 9% of sales (13% in 2008), consists of trailer manufacturers. Trailer manufacturers are also a fragmented group of local or regional players with great diversity in business size, focus and operation. Trailer manufacturers are highly dependent on suppliers such as WABCO to provide technical expertise and product knowledge. Similar to truck and bus OEMs, trailer manufacturers rely heavily on our products for important safety functions and superior technology.

The smallest group, representing approximately 4% of sales (4% in 2008), consists of car and SUV manufacturers to whom WABCO sells electronic air suspension systems and vacuum pumps. Electronic air suspension is a luxury feature with increasing penetration and above market growth. Vacuum pumps are used with diesel and GDI engines and, therefore, enjoy higher than average growth rates associated with increasing diesel and GDI applications in Europe and Asia. These customers are typically large, global, sophisticated and demand high product quality and overall service levels.

We address our customers through a global sales force that is organized around key accounts and customer groups and interfaces with product marketing and management to identify opportunities and meet customer needs across its product portfolio.

Europe represented approximately 65% of our sales in 2009, down from 76% in 2008, and ended the year representing only 60% of sales in the fourth quarter of 2009. The severe decline that occurred in the industry in Europe in 2009, combined with the less severe decline in India and improving market in China drove our sales in Asia to represent approximately 21% of our total sales in the fourth quarter of 2009. The growth in Asia is being

5

enhanced by our strong roots in China and India where we have achieved leading positions in the marketplace through increasingly close connectivity to customers. We are further strengthened in Asia by an outstanding network of suppliers, manufacturing sites and engineering hubs.

| | | | | | | | | | | | | | |

| WABCO SALES | |

| BY GEOGRAPHY | | | MAJOR END-MARKETS | |

| | | FY 2009

% of Sales | | | Q4 2009

% of Sales | | | | | FY 2009

% of Sales | | | Q4 2009

% of Sales | |

• Europe | | 65 | % | | 60 | % | | • Truck & Bus Products (OEMs) | | 55 | % | | 56 | % |

| | | | | | |

• Asia Pacific | | 18 | % | | 21 | % | | • Aftermarket | | 32 | % | | 31 | % |

| | | | | | |

• North America | | 8 | % | | 9 | % | | • Trailer Products | | 9 | % | | 8 | % |

| | | | | | |

• South America | | 6 | % | | 7 | % | | • Car Products | | 4 | % | | 5 | % |

| | | | | | |

• Other | | 3 | % | | 3 | % | | | | | | | | |

Backlog

Information on our backlog is set forth under Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Backlog” of this annual report.

Cyclical and Seasonal Nature of Business

Information on the cyclical and seasonal nature of our business is set forth under Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Cyclical and Seasonal Nature of Business” of this annual report.

Growth Strategy

Our growth strategy is focused on four key platforms: technology innovation, geographic expansion, aftermarket growth and opportunistic automotive application of our products and systems. Drivers of growth for both our aftermarket and advanced car systems are discussed in “Customers” above.

Technology

We continue to drive growth by utilizing our industry-leading expertise in developing electronically controlled systems, including braking, transmission automation, air suspension and air management systems. We have a strong track record of innovation and are responsible for some of the industry’s most important innovations including:

| | • | | First heavy-duty truck anti-lock braking system (ABS); |

| | • | | First electronically controlled air suspension (ECAS) system for commercial vehicles; |

| | • | | First commercial vehicle automated manual transmission (AMT) controls system; |

| | • | | First electronic stability control (ESC) system for commercial vehicles; |

| | • | | First collision safety system with active braking developed for the North American market, based on Adaptive Cruise Control technology (ACC); and |

| | • | | First autonomous emergency braking (AEB) system for commercial vehicles, for collision imminent situations with moving or stopped vehicles. |

We continue to expand our product and technology portfolio by introducing new products and functionalities, and by improving the penetration of recently launched technologies. Advanced products and functionalities are typically developed and adopted first in Europe and then migrate to North America and Asia. Important examples

6

include the adoption of ABS and automated transmission systems that were first widely adopted in European markets before starting to penetrate North America and Asia. Over the last three years, we spent approximately $250 million for research activities, product development and product engineering.

We are also focused on longer-term opportunities, particularly in the area of Advanced Driver Assistance Systems (ADAS). ADAS is a technology concept that involves connecting advanced sensors with truck control devices, such as braking and steering systems as well as engine controls, to improve safety and avoid collisions. During 2008, we launched our OnGuard™ product family, which includes the world’s first autonomous emergency braking system for commercial vehicles that we will begin producing in 2012. This product will allow our customers to comply with upcoming European road safety regulations to be implemented thereafter.

Geographic Expansion

We continue to drive sales in the high growth markets of Eastern Europe, China, India and Brazil. In Eastern Europe, we have been manufacturing products since 2001. The market in Eastern Europe, although experiencing the effects of the global economic slowdown, has historically experienced rapid growth, and we have established relationships with local customers.

China

China is a key long-term growth market for us. The adoption of more advanced braking, safety and other related systems is increasing in China, and the number of trucks built in the country is expected to continue to increase in the longer term. We have been in China since 1996 and are the leading provider of advanced systems like ABS, with a strong brand and established customer relationships. In the short-to medium-term, growth will be driven by the enforcement of existing regulations making ABS mandatory on trucks, buses and trailers, and we are well positioned to take advantage of this growth. Additional near term growth will be driven by introducing other new products into the local market such as our advanced air compressors and our new generation air disc brakes, clutch servos and automated manual transmission (AMT) systems. We have begun to supply our highly advanced modular AMT systems to CNHTC in China, illustrating our ability to grow in this market. To serve the growing demand for products both in China and for export, we have two facilities to manufacture conventional products, advanced systems such as ABS, and new modular air compressors. In addition, we have built a new factory in China to more closely support the long-term supply agreement with CNHTC and are building another facility in China to support the joint venture formed in December 2008 with Guangdong FUWA Heavy Industry Co., Ltd. (FUWA), which will provide for the production of air disc brakes in China. In order to ensure opportunities in Asia receive enough focus and management attention, we have increased our management presence in the region.

India

India is another growth market for us due to its expected volume of truck production and increasing adoption of advanced technology for commercial vehicles. We participate in this market through WABCO-TVS (INDIA) Ltd. (“WABCO-TVS”), which we took a majority ownership position in during the second quarter of 2009, further strengthening the Company’s already well-anchored position in India. With three world class factories in different areas of India, we are the market leader in traditional braking products, while customer demand for advanced braking and control systems is progressing. India also provides a strong base for sourcing and engineering activities, which we are actively developing. WABCO-TVS is a sourcing hub for our global operations by purchasing raw materials locally at best cost and it provides machining capabilities in our factory in Mahindra City to process the metals, castings and electrical motors that are used in our other factories in Europe, North America, Brazil and China to manufacture our products. WABCO-TVS is also a center of mechanical and software engineering activity, as we continue to develop our long-standing relationships in the local engineering community to benefit our global research and development efforts.

Competition

Given the importance of technological leadership, vehicle life-cycle expertise, reputation for quality and reliability, and the growing joint collaboration between OEMs and suppliers to drive new product development, the space in which we mostly operate has not historically had a large number of competitors. Our principal competitors

7

are Knorr-Bremse (Knorr’s U.S. subsidiary is Bendix Commercial Vehicle Systems) and, in certain categories, Haldex. In the advanced electronics categories, automotive players such as Bosch (automotive) and Continental (including Siemens-VDO) have recently been present in some commercial vehicle applications. In the mechanical product categories, several Asian competitors are emerging, primarily in China, who are focused on such products.

Manufacturing and Operations

Most of our manufacturing sites and distribution centers produce and/or house a broad range of products and serve all different types of customers. Currently, over 64% of our manufacturing workforce is located in best cost countries such as China, India and Poland up from approximately 10% in 1999. Facilities in best cost countries have helped reduce costs on the simpler and more labor-intensive products, while the facilities in Western Europe are focused on producing more technologically advanced products. All facilities globally are deploying Six Sigma Lean initiatives to improve productivity and reduce costs. By applying the Six Sigma philosophy and tools we seek to improve quality and predictability of our processes. Lean is geared towards eliminating waste in our supply chain, manufacturing and administrative processes. Both methodologies are customer driven and data based. In addition, our global supply chain team makes decisions on where to manufacture which products taking into account such factors as local and export demand, customer approvals, cost, key supplier locations and factory capabilities.

Our global sourcing organization purchases a wide variety of components including electrical, electro-mechanical, cast aluminum products and steel, as well as copper, rubber and plastic containing components that represent a substantial portion of manufacturing costs. We source products on a global basis from three key regions: Western Europe, Central and Eastern Europe and Asia. To support the continuing shift of manufacturing to best cost countries, we also continue to shift more of our sourcing to best cost regions. Under the leadership of the global sourcing organization, which is organized around commodity and product groups, we identify and develop key suppliers and seek to integrate them as partners into our extended enterprise. Many of our Western European suppliers are accompanying us on our move to best cost countries. Since 1999, the share of our sourcing from best cost regions has increased from 10% to approximately 41%.

We have developed a strong position in the design, development, engineering and testing of products, components and systems. We are generally regarded in the industry as a systems expert, having in-depth technical knowledge and capabilities to support the development of advanced technology applications. Key customers depend on us and will typically involve us very early in the development process as they begin designing next generation platforms. We have approximately 1,250 employees dedicated to developing new products, components and systems as well as supporting and enhancing current applications. Our sales organization hosts application engineers that are based near customers in all regions around the world and are partially resident at some customer locations. We also have significant resources in best cost countries performing functions such as drawings, testing and software component development. We operate test tracks in Germany, Finland (for extreme weather test conditions) and India.

Joint Ventures

We use joint ventures globally to expand and enhance our access to customers. Our important joint ventures are:

| | • | | A majority-owned joint venture (90%) in Japan with Sanwa-Seiki that distributes WABCO’s products in the local market. |

| | • | | A majority-owned (70%) partnership in the U.S. with Cummins Engine Co. (WABCO Compressor Manufacturing Co.), a manufacturing partnership formed to produce air compressors designed by WABCO. |

| | • | | A majority-owned joint venture (70%) in China with Mingshui Automotive Fitting Factory (MAFF) that provides conventional mechanical products to the local market. |

| | • | | A majority-owned joint venture (70%) with Guangdong FUWA Heavy Industry Co., Ltd., (“FUWA”) to produce air disc brakes for commercial trailers in China. FUWA is the largest manufacturer of commercial trailer axles in China and in the world. |

| | • | | A 50 percent owned joint venture in North America with Arvin Meritor Automotive Inc. (Meritor WABCO) that markets ABS and other vehicle control products. |

8

| | • | | A minority equity investment in a joint venture in South Africa, where we have a 49% ownership joint venture with Sturrock & Robson Ltd (WABCO SA), a distributor of braking systems products. |

Employees

We have approximately 8,100 employees. The streamlining actions taken in Europe significantly reduced the numbers of employees in Europe; however this was more than offset by the 1,800 employees added through taking majority ownership of WABCO-TVS in India. Approximately 50% of our employees are salaried and 50% are hourly. Approximately 58% of our workforce is in Europe, 35% is in Asia, and the remaining 7% is in the Americas. Approximately 1,250 employees work in engineering/product development.

Employees located in our sites in Europe, Asia and South America are subject to collective bargaining, with internal company agreements or external agreements at the region or country level. Currently 50% of our workforce is covered by a collective bargaining agreement and nearly all of those agreements expire during 2010. These employees’ right to strike is typically protected by law and union membership is confidential information which does not have to be provided to the employer. The collective bargaining agreements are typically renegotiated on an annual basis. Our U.S. facilities are non-union. We have maintained good relationships with our employees around the world and historically have experienced very few work stoppages.

Intellectual Property

Patents and other proprietary rights are important to our business. We also rely upon trade secrets, manufacturing know-how, continuing technological innovations, and licensing opportunities to maintain and improve our competitive position. We review third-party proprietary rights, including patents and patent applications, as available, in an effort to develop an effective intellectual property strategy, avoid infringement of third-party proprietary rights, identify licensing opportunities, and monitor the intellectual property claims of others.

We own a large portfolio of patents that principally relate to our products and technologies, and we have, from time to time, licensed some of our patents. Patents for individual products and processes extend for varying periods according to the date of patent filing or grant and the legal term of patents in various countries where patent protection is obtained.

The WABCO brand is also protected by trademark registrations throughout the world in the key markets in which our products are sold.

While we consider our patents and trademarks to be valuable assets, we do not believe that our competitive position is materially dependent upon any single patent or group of related patents.

Environmental Regulation

Our operations are subject to local, state, federal and foreign environmental laws and regulations that govern activities or operations that may have adverse environmental effects and which impose liability for clean-up costs resulting from past spills, disposals or other releases of hazardous wastes and environmental compliance. Generally, the international requirements that impact the majority of our operations tend to be no more restrictive than those in effect in the U.S.

Throughout the world, we have been dedicated to being an environmentally responsible manufacturer, neighbor and employer. We have a number of proactive programs under way to minimize our impact on the environment and believe that we are in substantial compliance with environmental laws and regulations. Manufacturing facilities are audited on a regular basis. Twelve of our manufacturing facilities have Environmental Management Systems (EMS), which have been certified as ISO 14001 compliant. These facilities are those located in:

| | | | |

Claye-Souilly, France | | Campinas, Brazil | | Wroclaw, Poland |

Gronau, Germany | | Hannover, Germany | | Jinan, China |

Ambattur, India | | Pyungtaek, Korea | | Qingdao, China |

Meppel, Netherlands | | Mannheim, Germany | | Charleston, United States |

9

A number of our facilities are undertaking responsive actions to address groundwater and soil issues. Expenditures in 2009 to evaluate and remediate these sites were not material.

Additional sites may be identified for environmental remediation in the future, including properties previously transferred and with respect to which the Company may have contractual indemnification obligations.

Available Information

Our web site is located at www.wabco-auto.com. Our periodic reports and all amendments to those reports required to be filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge through the web site. During the period covered by this report, we posted our periodic reports on Form 10-Q and our current reports on Form 8-K and any amendments to those documents to our web site as soon as such reports were filed or furnished electronically with the Securities Exchange Commission (“SEC”). We will continue to post to our web site such reports and amendments as soon as reasonably practicable after such reports are filed with or furnished to the SEC.

Code of Conduct and Ethics

Our Code of Conduct and Ethics, which applies to all employees, including all executive officers and senior financial officers and directors, is posted on our web site www.wabco-auto.com. The Code of Conduct and Ethics is compliant with Item 406 of SEC Regulation S-K and the NYSE corporate governance listing standards. Any changes to the Code of Conduct and Ethics that affect the provisions required by Item 406 of Regulation S-K will also be disclosed on the web site.

Any waivers of the Code of Conduct and Ethics for our executive officers, directors or senior financial officers must be approved by our Audit Committee and those waivers, if any are ever granted, would be disclosed on our web site under the caption “Exemptions to the Code of Conduct and Ethics.” There have been no waivers to the Code of Conduct and Ethics.

Any of the following factors could have a material adverse affect on our future operating results as well as other factors included in “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Information Concerning Forward Looking Statements.”

Risks Relating to Our Business

The credit crisis and global recession have negatively impacted our customers and could continue to result in reduced demand for our products, which could therefore continue to have a significant negative impact on our business.

The credit markets have experienced a period of unprecedented turmoil and upheaval characterized by significantly reduced availability of credit and increased borrowing costs. The disruptions in the credit markets and impact of a more prolonged global recession could continue to negatively impact consumer confidence and spending patterns and cause our customers to reduce truck and bus production. This in turn could have a negative impact on our business and results of operations, our operating cash flows and our financial condition.

We may be unable to pay any significant fine imposed by the European Commission, if we are unable to access our principal credit facility or arrange for alternative sources of capital.

As discussed in greater detail in Item 3. “Legal Proceedings,” Item 7. “Management’s Discussion and Analysis of Results of Operations and Financial Condition – Liquidity with Regard to European Commission Fine,” and Note 13. “Warranties, Guarantees, Commitments and Contingencies,” we are required to indemnify our former parent company, American Standard, now Trane, and Ideal Standard International and their respective owners against any fines that may be imposed by the European Commission (“the Commission”) in connection with a multi-company

10

investigation commenced in 2004 relating to alleged infringement of EU competition rules in the Bath and Kitchen fixtures market. The fine imposed by the Commission could be material to our operating results and cash flows for the year in which the liability would be recognized or the fine paid.

Our principal credit facility contains a number of covenants that require us to maintain certain defined financial metrics associated with our earnings before we can access the funds available under the facility. If the current global industry conditions continue to significantly negatively impact both our customers and the demand for our products in such a way as to continue to depress our earnings, we may continue to be unable to fully access our credit facility due to an inability to meet these financial covenants. If we are unable to fully access our principal credit facility, obtain alternative sources of financing, or obtain some payment relief from the Commission or a suspension of the payment obligation from the General Court (formerly the European Court of First Instance), and the fine exceeds our funding capability, then our financial condition and liquidity would be materially adversely affected.

Our sales could decline due to macro-economic factors, cyclicality of the industry, regulatory changes and other factors outside of our control.

Changes in economic conditions, cyclical downturns in our industry, regulatory changes impacting the purchasing patterns of commercial vehicles, and changes in the local economies of the countries or regions in which we sell our products, such as changes in consumer confidence, increases in interest rates and increases in unemployment, many of which are now occurring as a result of the global recession, are likely to further affect demand for our products, which could negatively affect our business and results of operations.

Demand for new trucks and buses in the markets in which we operate has a significant impact on our sales. While in the last few years leading up to 2009, heavy truck and bus production had increased in our largest market (Western Europe), this market along with others has been significantly affected by the downturn. The Western European market, which accounted for approximately 58% of our total sales, experienced a 62% decline in 2009. Adverse economic conditions in our markets, particularly in Western Europe, has largely contributed to reduced truck and bus production, which has and will continue to have an adverse effect on our results of operations and cash flows.

Our exposure to exchange rate fluctuations on cross border transactions and the translation of local currency results into U.S. dollars could negatively impact our results of operations.

We conduct business through subsidiaries in many different countries, and fluctuations in currency exchange rates have a significant impact on the reported results of our operations, which are presented in U.S. dollars. In 2009, approximately 92% of our combined sales occurred outside of the United States. A significant and growing portion of our products are manufactured in lower-cost locations and sold in various countries. Cross border transactions, both with external parties and intercompany relationships, result in increased exposure to foreign currency exchange effects. Accordingly, significant changes in the exchange rates of the euro, U.S. dollar and other applicable currencies could cause fluctuations in the reported results of our operations that could negatively affect our results of operations. Additionally, our results of operations are translated into U.S. dollars for reporting purposes. The strengthening or weakening of the U.S. dollar results in favorable or unfavorable translation effects as the results of foreign locations are translated into U.S. dollars.

We are subject to general risks associated with our foreign operations.

In addition to the currency exchange risks inherent in operating in many different foreign countries, there are other risks inherent in our international operations.

The risks related to our foreign operations that we more often face in the normal course of business include:

| | • | | changes in non-U.S. tax law, increases in non-U.S. tax rates and the amount of non-U.S. earnings relative to total combined earnings could change and impact our combined tax rate; |

| | • | | foreign earnings may be subject to withholding requirements or the imposition of tariffs, price or exchange controls, or other restrictions; |

11

| | • | | general economic and political conditions in countries where we operate may have an adverse effect on our operations in those countries; and |

| | • | | we may have difficulty complying with a variety of foreign laws and regulations, some of which may conflict with United States law, and the uncertainty created by this legal environment could limit our ability to effectively enforce our rights in certain markets. |

The ability to manage these risks could be difficult and may limit our operations and make the manufacture and distribution of our products internationally more difficult, which could negatively affect our business and results of operations.

If we are unable to obtain component parts or obtain them at reasonable price levels, our ability to maintain existing sales margins may be affected.

We purchase a broad range of materials and components throughout the world in connection with our manufacturing activities. Major items include electronic components and parts containing aluminum, steel, copper, zinc, rubber and plastics. The cost of components and parts, and the raw materials used therein, represents a significant portion of our total costs. Price increases of the underlying commodities may adversely affect our results of operations. Although we maintain alternative sources for components and parts, our business is subject to the risk of price fluctuations and periodic delays in the delivery of certain raw materials. This risk has increased due to the current global recession, which is impacting our supplier base. The sudden inability of a supplier to deliver components or to do so at reasonable prices could have a temporary adverse effect on our production of certain products or the cost at which we can produce those products. Any change in the supply or price of raw materials could materially adversely affect our future business and results of operations.

If we are not able to maintain good relations with our employees, we could suffer work stoppages that could negatively affect our business and results of operations.

Employees located in our sites in Europe, Asia and South America are subject to collective bargaining, with internal company agreements or external agreements at the region or country level. These employees’ right to strike is typically protected by law and union membership is confidential information which does not have to be provided to the employer. Our U.S. facilities are non-union. Any disputes with our employee base could result in work stoppages or labor protests, which could disrupt our operations. Any such labor disputes could negatively affect our business and results of operations.

We are dependent on key customers.

We rely on several key customers. For the fiscal year ending December 31, 2009, sales to our top three customers accounted for approximately 12% (Daimler), 8% and 5%, respectively, of our sales, and sales to our top ten customers accounted for approximately 48% of our sales. This includes sales to our 50%-owned Meritor WABCO joint venture in North America. Many of our customers place orders for products on an as-needed basis and operate in cyclical industries and, as a result, their order levels have varied from period to period in the past and may vary significantly in the future. Such customer orders are dependent upon their markets and customers and may be subject to delays or cancellations. As a result of dependence on our key customers, we have experienced and could experience in the future a material adverse effect on our business and results of operations if any of the following were to occur:

| | • | | the loss of any key customer, in whole or in part; |

| | • | | a declining market in which customers reduce orders or demand reduced prices; or |

| | • | | a strike or work stoppage at a key customer facility, which could affect both their suppliers and customers. |

If there are changes in the environmental or other regulations that affect one or more of our current or future products, it could have a negative impact on our business and results of operations.

We are currently subject to various environmental and other regulations in the U.S. and internationally. A risk of environmental liability is inherent in our current and former manufacturing activities. Under certain environmental

12

laws, we could be held jointly and severally responsible for the remediation of any hazardous substance contamination at our past and present facilities and at third party waste disposal sites and could also be held liable for damages to natural resources and any consequences arising out of human exposure to such substances or other environmental damage. While we have a number of proactive programs underway to minimize the impact of the production and use of our products on the environment and believe that we are in substantial compliance with environmental laws and regulations, we cannot predict whether there will be changes in the environmental regulations affecting our products.

Any changes in the environmental and other regulations which affect our current or future products could have a negative impact on our business if we are unable to adjust our product offering to comply with such regulatory changes. In addition, it is possible that we will incur increased costs as a result of complying with environmental regulations, which could have a material adverse effect on our business, results of operations and financial condition.

We may be subject to product liability and warranty and recall claims, which may increase the costs of doing business and adversely affect our business, financial condition and results of operations.

We are subject to a risk of product liability or warranty claims if our products actually or allegedly fail to perform as expected or the use of our products results, or is alleged to result, in bodily injury and/or property damage. While we maintain reasonable limits of insurance coverage to appropriately respond to such exposures, large product liability claims, if made, could exceed our insurance coverage limits and insurance may not continue to be available on commercially acceptable terms, if at all. We cannot assure you that we will not incur significant costs to defend these claims or that we will not experience any product liability losses in the future. In addition, if any of our designed products are or are alleged to be defective, we may be required to participate in recalls and exchanges of such products. In the past five years, our warranty expense has fluctuated between approximately 1.3% and 2.4% of sales on an annual basis. Individual quarters were above or below the annual averages. The future cost associated with providing product warranties and/or bearing the cost of repair or replacement of our products could exceed our historical experience and have a material adverse effect on our business, financial condition and results of operations.

We are required to plan our capacity well in advance of production and our success depends on having available capacity and effectively using it.

We principally compete for new business at the beginning of the development of our customers’ new products. Our customers’ new product development generally begins significantly prior to the marketing and production of their new products and our supply of our products generally lasts for the life of our customers’ products. Nevertheless, our customers may move business to other suppliers or request price reductions during the life cycle of a product. The long development and sales cycle of our new products, combined with the specialized nature of many of our facilities and the resulting difficulty in shifting work from one facility to another, could result in variances in capacity utilization. In order to meet our customers’ requirements, we may be required to supply our customers regardless of cost and consequently we may suffer an adverse impact on our operating profit margins and results of operations.

We must continue to make technological advances, or we may not be able to successfully compete in our industry.

We operate in an industry in which technological advancements are necessary to remain competitive. Accordingly, we devote substantial resources to improve already technologically complex products and to remain a leader in technological innovation. However, if we fail to continue to make technological improvements or our competitors develop technologically superior products, it could have an adverse effect on our operating results or financial condition.

13

Risks Relating to the Separation

We have agreed to indemnify Trane for taxes and related losses resulting from certain actions that may cause the Distribution to fail to qualify as a tax-free transaction.

Trane has received a private letter ruling from the Internal Revenue Service (“IRS”) substantially to the effect that the Distribution qualifies as tax-free for U.S. federal income tax purposes under Section 355 of the Internal Revenue Code (“the Code”). In addition, Trane has received an opinion of Skadden, Arps, Slate, Meagher & Flom LLP, tax counsel to Trane, substantially to the effect that the Distribution will qualify as tax-free to Trane, us and our shareholders under Section 355 and related provisions of the Code. The ruling and opinion were based on, among other things, certain assumptions as well as on the accuracy of certain factual representations and statements made by Trane and the Company. In rendering its ruling, the IRS also relied on certain covenants that the Company and Trane entered into, including the adherence to certain restrictions on Trane’s and the Company’s future actions.

Notwithstanding receipt by Trane of the private letter ruling and the opinion of counsel, the IRS could assert that the Distribution should be treated as a taxable transaction. If the Distribution fails to qualify for tax-free treatment, then Trane would recognize a gain in an amount equal to the excess of (i) the fair market value of our common stock distributed to the Trane shareholders over (ii) Trane’s tax basis in such common stock. Under the terms of the Tax Sharing Agreement, in the event the Distribution were to fail to qualify as a tax-free reorganization and such failure was not the result of actions taken after the distribution by Trane or any of its subsidiaries or shareholders, we would be responsible for all taxes imposed on Trane as a result thereof. In addition, each Trane shareholder who received our common stock in the Distribution generally would be treated as having received a taxable Distribution in an amount equal to the fair market value of our common stock received (including any fractional share sold on behalf of the shareholder), which would be taxable as a dividend to the extent of the shareholder’s ratable share of Trane’s current and accumulated earnings and profits (as increased to reflect any current income including any gain recognized by Trane on the taxable distribution). The balance, if any, of the Distribution would be treated as a nontaxable return of capital to the extent of the Trane shareholder’s tax basis in its Trane stock, with any remaining amount being taxed as capital gain. Our obligation to indemnify Trane under the Tax Sharing Agreement if the Distribution fails to qualify for tax-free treatment could be substantial if triggered, and could have a material adverse effect on our business, financial condition and results of operations.

We are responsible for certain of Trane’s contingent and other corporate liabilities.

Under the Indemnification and Cooperation Agreement, the Separation and Distribution Agreement and the Tax Sharing Agreement, our wholly-owned subsidiary WABCO Europe BVBA has assumed and is responsible for certain contingent liabilities related to Trane’s business (including certain associated costs and expenses, whether arising prior to, at or after the Distribution) and will indemnify Trane for these liabilities. Among the contingent liabilities against which we will indemnify Trane and the other indemnitees, are liabilities associated with an investigation into alleged infringement of European Union competition regulations, certain non-U.S. tax liabilities and certain U.S. and non-U.S. environmental liabilities associated with certain Trane entities.

We will indemnify Trane, Ideal Standard International, including certain former European subsidiaries and affiliates of the former American Standard group, and their respective owners against any fines associated with an investigation into alleged infringement of European Union competition regulations.

As part of a multi-company investigation, American Standard and certain of its European subsidiaries engaged in the Bath and Kitchen business have been charged by the European Commission for alleged infringements of European Union competition rules relating to the distribution of bathroom fixtures and fittings in a number of European countries. Pursuant to the Indemnification and Cooperation Agreement, WABCO Europe BVBA (an indirect wholly-owned subsidiary of WABCO) will be responsible for, and will indemnify American Standard (now Trane) and Ideal Standard International (including certain subsidiaries engaged, or formerly engaged in the Bath and Kitchen business) and their respective affiliates against any fines related to this investigation. See Item 3. “Legal Proceedings” for additional discussion of the procedural history, response, hearing and appeals process related to the European Commission investigation.

14

Risks Relating to Our Common Stock

Your percentage ownership in WABCO may be diluted in the future.

Your percentage ownership in WABCO may be diluted in the future because of equity awards that have already been granted and that we expect will be granted to our directors and officers in the future. Prior to the Separation and record date for the Distribution, Trane approved an Omnibus Incentive Plan, which provides for the grant of equity-based awards, including restricted stock, restricted stock units, stock options, stock appreciation rights, phantom equity awards and other equity-based awards to our directors, officers and other employees. After the Separation and record date for the Distribution, WABCO has approved its own Omnibus Incentive Plan. In the future, we may issue additional equity securities, subject to limitations imposed by the Tax Sharing Agreement, in order to fund working capital needs, capital expenditures and product development, or to make acquisitions and other investments, which may dilute your ownership interest.

We cannot assure you that we will pay any dividends or repurchase shares.

While we have historically returned value to shareholders in the form of share repurchases and dividends, our ability to repurchase shares and pay dividends is limited by available cash, contingent liabilities, (such as any fine resulting from the alleged infringement discussed above) and surplus. Moreover, all decisions regarding the declaration and payment of dividends and share repurchases will be at the sole discretion of our Board and will be evaluated from time to time in light of our financial condition, earnings, capital requirements of our business, covenants associated with certain debt obligations, legal requirements, regulatory constraints, industry practice and other factors that our Board deems relevant.

Our shareholder rights plan and provisions in our amended and restated certificate of incorporation and amended and restated by-laws, and of Delaware law may prevent or delay an acquisition of our company, which could decrease the trading price of our common stock.

Our amended and restated certificate of incorporation, amended and restated by-laws and Delaware law contain provisions that are intended to deter coercive takeover practices and inadequate takeover bids by making such practices or bids unacceptably expensive to the raider and to encourage prospective acquirers to negotiate with our Board of Directors rather than to attempt a hostile takeover. These provisions include, among others:

| | • | | a Board of Directors that is divided into three classes with staggered terms; |

| | • | | elimination of the right of our shareholders to act by written consent; |

| | • | | rules regarding how shareholders may present proposals or nominate directors for election at shareholder meetings; |

| | • | | the right of our Board to issue preferred stock without shareholder approval; and |

| | • | | limitations on the right of shareholders to remove directors. |

Delaware law also imposes some restrictions on mergers and other business combinations between us and any holder of 15% or more of our outstanding common stock.

On July 13, 2007, our Board adopted a shareholder rights plan, which provides, among other things, that when specified events occur, our shareholders will be entitled to purchase from us a newly created series of junior preferred stock. The preferred stock purchase rights are triggered by the earlier to occur of (i) ten business days (or a later date determined by our Board of Directors before the rights are separated from our common stock) after the public announcement that a person or group has become an “acquiring person” by acquiring beneficial ownership of 15% or more of our outstanding common stock or (ii) ten business days (or a later date determined by our Board before the rights are separated from our common stock) after a person or group begins a tender or exchange offer that, if completed, would result in that person or group becoming an acquiring person. The issuance of preferred stock pursuant to the shareholder rights plan would cause substantial dilution to a person or group that attempts to acquire us on terms not approved by our Board of Directors.

We believe these provisions protect our shareholders from coercive or otherwise unfair takeover tactics by requiring potential acquirers to negotiate with our Board and by providing our Board with more time to assess any

15

acquisition proposal. These provisions are not intended to make our company immune from takeovers. However, these provisions apply even if the offer may be considered beneficial by some shareholders and could delay or prevent an acquisition that our Board determines is not in the best interests of our company and our shareholders.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

As of February 18, 2010, we conducted our manufacturing activities at 16 plants in 10 countries. Construction of one additional plant in Taishan, China has been completed but no manufacturing has taken place to date. In addition, we have a contract in place for the sale of our facility in Leeds, England, which will take place in 2010. This facility continues to fulfill a backlog of customer orders and will continue to manufacture certain products until the sale occurs.

| | |

Location | | Major Products Manufactured at Location |

Campinas, Brazil | | Vehicle control systems |

Leeds, England | | Vacuum pumps |

Claye-Souilly, France | | Vehicle control systems |

Hanover, Germany | | Vehicle control systems |

Mannheim, Germany | | Foundation brakes |

Gronau, Germany | | Compressors and hydraulics |

Meppel, Netherlands | | Actuators |

Wroclaw, Poland | | Vehicle control systems |

Qingdao, China | | Braking systems |

Jinan, China (2 plants) | | Braking systems and Compressors |

Pyungtaek, Korea | | Braking systems |

Ambattur, India | | Vehicle control systems |

Jamshedpur, India | | Vehicle control systems |

Mahindra World City, India | | Vehicle control systems |

Charleston, United States | | Compressors |

We own all of the plants described above, except for Claye-Souilly, France; Jinan, China; Taishan, China; Jamshedpur, India; Mahindra World City, India and Charleston, U.S.; which are leased. Our properties are generally in good condition, are well maintained, and are generally suitable and adequate to carry out our business. In 2009, the manufacturing plants, taken as a whole, met our capacity needs.

We also own or lease warehouse and office space for administrative and sales staff. Our headquarters, located in Brussels, Belgium, and our executive offices, located in Piscataway, New Jersey, are leased.

In addition to the matters described below, we are party to a variety of legal proceedings with respect to environmental related, employee related, product related, and general liability and automotive litigation related matters that arise in the normal course of our business. While the results of these legal proceedings cannot be predicted with certainty, management believes that the final outcome of these proceedings will not have a material adverse effect on our combined results of operations or financial position.

The European Commission Investigation

In November 2004, certain of American Standard’s European subsidiaries were contacted by the European Commission as part of a multi-company investigation into possible infringement of European Union competition regulations relating to the distribution of bathroom fixtures and fittings in certain European countries. In November 2005, the European Commission sent certain of American Standard’s European subsidiaries a written request for information. On March 28, 2007, American Standard and certain of its European subsidiaries engaged in the Bath and Kitchen business received an administrative complaint entitled a Statement of Objections from the European

16

Commission alleging infringements of European Union competition rules by numerous bathroom fixture and fittings companies. As a result of a legal reorganization that occurred in 2007, WABCO Europe BVBA (an indirect wholly-owned subsidiary of WABCO), formerly American Standard Europe BVBA, is responsible for, and is liable to indemnify Trane and Ideal Standard International (representing the successor to the Bath and Kitchen business, and owner of certain of the former American Standard subsidiaries) and their owners against any fines related to this investigation.

American Standard and its charged European subsidiaries responded to the Statement of Objections on July 31, 2007. WABCO Europe BVBA attended a hearing with the European Commission to present evidence regarding the response to the Statement of Objections in November 2007. Since that time, the Commission has made several requests for additional information from WABCO relating to, among other things, historic sales for all of the charged entities for periods prior to and subsequent to the spin-off and the sale of the Bath & Kitchen Division of Trane. A fine would be required to be paid within three months of any decision, unless imposition of any such fine were appealed within two months of the decision. If we elected to appeal, we would be required to pay the fine or to provide a bank guarantee for the full amount of the fine plus interest. The appeals process could take as long as five to seven years during which time WABCO would not have access to such funds or would be required to provide a bank guarantee. The Commission or the General Court (previously known as the Court of First Instance) could agree to waive or suspend this requirement for reasons of financial hardship; however this outcome cannot be assured and will depend on the relevant facts at the time. See Note 13-Warranties, Guarantees, Commitments and Contingencies in the notes to the consolidated financial statements for further detail.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

No matter was submitted to a vote of the Company’s shareholders during the fourth quarter of 2009.

| ITEM 4A. | EXECUTIVE OFFICERS OF THE REGISTRANT |

The following table sets forth certain information as of February 18, 2010 with respect to each person who is an executive officer of the Company:

| | | | |

Name | | Age | | Position(s) |

Jacques Esculier | | 50 | | Chairman of the Board of Directors and Chief Executive Officer |

Ulrich Michel | | 47 | | Chief Financial Officer |

Kevin Tarrant | | 52 | | Chief Human Resources Officer |

Nikhil M. Varty | | 45 | | Vice President, Compression & Braking |

Todd Weinblatt | | 40 | | Vice President and Controller |

Jean-Christophe Figueroa | | 46 | | Vice President, Vehicle Dynamics and Controls |

Alfred Farha | | 47 | | Chief Legal Officer and Secretary |

Each officer of the Company is appointed by the Board of Directors to a term of office expiring on the date of the first Board meeting after the Annual Meeting of Shareholders next succeeding his or her appointment or such officer’s earlier resignation or removal.

Set forth below is the principal occupation of each of the executive officers named above during the past five years.

Jacques Esculier has served as our Chief Executive Officer and director since July 2007. In May 2009, he was appointed Chairman of our Board of Directors. Prior to July 2007, Mr. Esculier served as Vice President of Trane and President of its Vehicle Control Systems business, a position he had held since January 2004. Prior to holding that position, Mr. Esculier served in the capacity of Business Leader for the Trane Commercial Systems’ Europe, Middle East, Africa, India & Asia Region from 2002 through January 2004. Prior to joining Trane in 2002, Mr. Esculier spent more than six years in leadership positions at AlliedSignal/Honeywell. He was Vice President and General Manager of Environmental Control and Power Systems Enterprise based in Los Angeles, and Vice President of Aftermarket Services—Asia Pacific based in Singapore.

Ulrich Michel has served as our Chief Financial Officer since July 2007. Prior to July 2007, Mr. Michel served as Chief Financial Officer of Trane’s Vehicle Control Systems business, a position he had held since April 2005.

17

Prior to holding that position, Mr. Michel served in the capacity of Chief Financial Officer for the Trane Commercial Systems’ EMAIR (Europe, Middle East, Africa & India Region) from 2003 through April 2005. Prior to joining Trane in 2003, Mr. Michel spent more than six years in financial leadership positions at AlliedSignal/Honeywell with areas of focus including mergers and acquisitions, the Specialty Chemicals business, and the Control Products business in Europe. Before joining AlliedSignal/Honeywell, Mr. Michel spent eight years at Price Waterhouse.

Kevin Tarrant has served as our Chief Human Resources Officer since July 2007. Prior to July 2007, Mr. Tarrant served for two years as Vice President, Global Organization Effectiveness for Arrow Electronics in Melville, New York. Prior to that, Mr. Tarrant was Senior Vice President of Human Resources for First Data Resources in Denver, Colorado from 2003 to 2005 after having served as Vice President of Human Resources for First Data’s Western Union International business headquartered in Paris, France from 2002 to 2003. Before joining First Data, Mr. Tarrant spent 10 years at the headquarters and business-unit level working for various Dun & Bradstreet Corporation businesses and six years at the Monsanto Company’s chemical controls businesses.

Nikhil M. Vartyhas served as our Vice President, Compression and Braking since July 2007. Prior to July 2007, Mr. Varty served as Vice President, Compression and Braking of Trane’s Vehicle Control Systems business, a position he has held since January 2005. Prior to holding that position, Mr. Varty served in the capacity of Chief Financial Officer of Trane’s Vehicle Control Systems business. Prior to joining Trane in June 2001, Mr. Varty had more than 10 years of national and international senior level finance roles with Great Lakes Chemical Corp., AlliedSignal/Honeywell and Coopers & Lybrand.

Todd Weinblatt has served as our Vice President and Controller since July 2007. Prior to July 2007, Mr. Weinblatt served as Assistant Controller of Trane, a position he had held since 2004. Before joining Trane, Mr. Weinblatt served as Director—Accounting Policy and External Reporting at The Dun & Bradstreet Corporation. His prior experience includes six years at Lucent Technologies Inc., where he was a Senior Manager of Accounting Policy and Mergers and Acquisitions. He began his career with Coopers & Lybrand, where he spent five years as an auditor.

Jean-Christophe Figueroahas served as our Vice President, Vehicle Dynamics and Controls since July 2007. Prior to July 2007, Mr. Figueroa served in a similar capacity within Trane’s Vehicle Control Systems business. Mr. Figueroa joined Trane in 2005 from tier-1 automotive supplier Valeo where he had been Group Vice President, Purchasing, based in Paris, France. Mr. Figueroa spent 13 years in senior management business and purchasing positions for Valeo, including leadership of the Automotive Climate Control business in both Mexico and subsequently Western Europe. Prior to joining Valeo, Mr. Figueroa spent seven years with Pierburg, Mexico, in various leadership positions in logistics, purchasing and program management.

Alfred Farha has served as our Chief Legal Officer and Secretary since July 2008. Prior to July 2008, Mr. Farha served as the General Counsel, Europe of Flextronics for four years, with additional global responsibility for Flextronics’s automotive business segment. Previously, Mr. Farha was Senior Corporate Counsel at Cisco Systems from 2000-2004, and at Unisys Corporation, from 1996-2000. Prior to his in-house career, he gained diverse experience with leading corporate international law firms in Europe, the US, Japan and Venezuela. He is a member of the Bar of the State of New York.

18

PART II

| ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

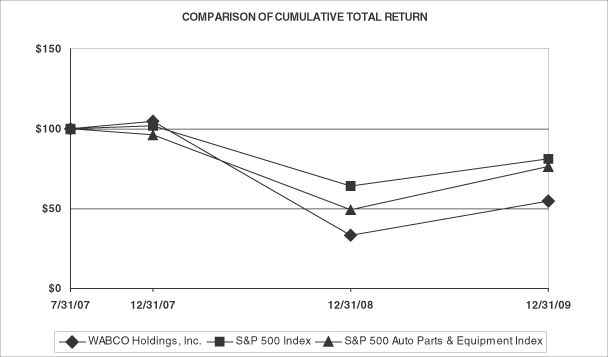

Our common stock is listed on NYSE under the symbol “WBC.” The common stock was first traded “regular way” on the NYSE on August 1, 2007, concurrent with our spin-off from Trane.

Our Certificate of Incorporation, as amended, authorizes the Company to issue up to 400,000,000 shares of common stock, par value $.01 per share, and 4,000,000 shares of preferred stock, par value $.01 per share, all of which have been designated by our Board of Directors as a series of Junior Participating Cumulative Preferred Stock. We also have a rights agreement. Pursuant to the rights agreement, when triggered in certain takeover situations, one preferred stock purchase right will be issued for each outstanding share of our common stock.