Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☒ | Definitive Proxy Statement |

| ☐ | Definitive Additional Materials |

| ☐ | Soliciting Material under §240.14a-12 |

WABCO Holdings Inc.

(Name of registrant as specified in its charter)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which the transaction applies: |

| (2) | Aggregate number of securities to which the transaction applies: |

| (3) | Per unit price or other underlying value of the transaction computed pursuant to Exchange ActRule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of the transaction: |

| (5) | Total fee paid: |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Table of Contents

WABCO Holdings Inc.

| Notice of Annual Meeting |

| of Shareholders and |

| Proxy Statement |

| May 24, 2018 |

| McDermott Will & Emery |

340 Madison Avenue, New York, NY 10173-1922 |

Table of Contents

|

Global Headquarters | |

Chaussée de la Hulpe 166 1170 Brussels Belgium Phone +322 663 98 00 |

Jacques Esculier

Chairman and Chief Executive Officer

April 12, 2018

Dear Shareholder:

I invite you to the Annual Meeting of Shareholders of WABCO Holdings Inc. This year’s meeting will be held on Thursday, May 24, 2018, at 10:00 a.m. at the New York offices of McDermott Will & Emery, 340 Madison Avenue, New York, NY 10173-1922.

Our directors and representatives of our senior management will attend the meeting. We will consider the items of business listed in the attached formal notice of meeting and proxy statement. Our 2017 Annual Report accompanies this proxy statement.

Your vote is very important, regardless of the number of shares you hold. Whether or not you plan to attend the meeting in person, please cast your vote, as instructed in the Notice Regarding Internet Availability of Proxy Materials or proxy card, over the Internet or by telephone, as promptly as possible. If you received only a Notice Regarding Internet Availability of Proxy Materials in the mail or by electronic mail, you may also request a paper proxy card to submit your vote by mail, if you prefer. However, we encourage you to vote over the Internet because it is convenient and will save printing costs and postage fees, as well as natural resources.

On behalf of the management team and your Board of Directors, thank you for your continued support and interest in WABCO Holdings Inc.

Sincerely,

Jacques Esculier

Chairman and Chief Executive Officer

Table of Contents

WABCO Holdings Inc.

Notice of 2018 Annual Meeting of Shareholders

and Proxy Statement

To the Shareholders of

WABCO Holdings Inc.:

The Annual Meeting of Shareholders of WABCO Holdings Inc. will be held at the New York offices of McDermott Will & Emery, 340 Madison Avenue, New York, NY 10173-1922, on Thursday, May 24, 2018, at 10:00 a.m. to consider and vote upon the following proposals:

1. Election of three directors to Class II with terms expiring at the 2021 Annual Meeting of Shareholders.

2. Ratification of the appointment of Ernst & Young Bedrijfsrevisoren BCVBA/Reviseurs d’Entreprises SCCRL (“Ernst &Young Belgium”) as the company’s independent registered public accounting firm for the year ending December 31, 2018.

3. Advisory approval of the company’s executive compensation(“Say-on-Pay”).

4. Approval of the Amended and Restated WABCO Holdings Inc. 2009 Omnibus Incentive Plan.

We may also transact any other business as may properly come before the meeting and any adjournments or postponements thereof.

Shareholders of record of the company’s common stock as of the close of business on March 29, 2018 are entitled to receive notice of the Annual Meeting of Shareholders and to vote. Shareholders who hold shares in street name may vote through their brokers, banks or other nominees.

Regardless of the number of shares you own, please vote. All shareholders of record can vote (i) over the Internet, (ii) by toll-free telephone (please see the proxy card for instructions), (iii) by written proxy by signing and dating the proxy card and returning it, or (iv) by attending the Annual Meeting of Shareholders in person. These various options for voting are described in the Notice Regarding Internet Availability of Proxy Materials and on the proxy card.

We encourage you to receive all proxy materials in the future electronically to help us save printing costs and postage fees, as well as natural resources in producing and distributing these materials. If you wish to receive these materials electronically next year, please follow the instructions on the proxy card.

By order of the Board of Directors,

Lisa J. Brown

Chief Legal Officer and Company Secretary

Brussels, Belgium

April 12, 2018

Table of Contents

| Page | ||||

| 1 | ||||

| 4 | ||||

| 5 | ||||

| 5 | ||||

| 6 | ||||

| 6 | ||||

Class III Directors Continuing in Office—Terms Expiring at the 2019 Annual Meeting of Shareholders | 7 | |||

Class I Directors Continuing in Office—Terms Expiring at the 2020 Annual Meeting of Shareholders | 8 | |||

| 11 | ||||

| 11 | ||||

| 11 | ||||

| 13 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 15 | ||||

| 15 | ||||

CERTAIN RELATIONSHIPS OR RELATED PERSON TRANSACTIONS AND SECTION 16 REPORTING COMPLIANCE | 16 | |||

| 16 | ||||

| 16 | ||||

| 17 | ||||

| 17 | ||||

| 18 | ||||

PROPOSAL 2—RATIFICATION OF APPOINTMENT OF THE INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | 19 | |||

| 19 | ||||

| 20 | ||||

| 21 | ||||

| 21 | ||||

| 25 | ||||

Executive Compensation Philosophy; Compensation Program Objectives | 25 | |||

| 26 | ||||

| 27 | ||||

| 28 | ||||

| 28 | ||||

| 29 | ||||

| 35 | ||||

| 36 | ||||

| 36 | ||||

| 36 | ||||

| 36 | ||||

| 37 | ||||

REPORT OF THE COMPENSATION, NOMINATING AND GOVERNANCE COMMITTEE | 38 | |||

| 39 | ||||

| 39 | ||||

| 40 | ||||

Table of Contents

| Page | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 44 | ||||

| 44 | ||||

| 49 | ||||

| 50 | ||||

| 50 | ||||

PROPOSAL 4—APPROVAL OF THE AMENDED AND RESTATED 2009 OMNIBUS INCENTIVE PLAN | 51 | |||

| 51 | ||||

| 52 | ||||

| 53 | ||||

| 55 | ||||

| 57 | ||||

| 57 | ||||

| 58 | ||||

| 60 | ||||

| 60 | ||||

| 61 | ||||

| 61 | ||||

| 62 | ||||

COMMON STOCK OWNERSHIP OF OFFICERS, DIRECTORS AND SIGNIFICANT SHAREHOLDERS | 63 | |||

Ownership of Common Stock by Directors and Executive Officers | 63 | |||

Ownership of Common Stock by Certain Significant Shareholders | 64 | |||

| 65 | ||||

Shareholder Proposals for the 2019 Annual Meeting of Shareholders | 65 | |||

| 65 | ||||

| 66 | ||||

| 66 | ||||

| A-1 | ||||

| B-1 | ||||

Appendix C— Amended and Restated WABCO Holdings Inc. 2009 Omnibus Incentive Plan | C-1 | |||

Table of Contents

ABOUT THE ANNUAL MEETING OF SHAREHOLDERS

Why have I received these materials?The Board of Directors is soliciting proxies for use at the Annual Meeting of Shareholders of the company to be held on May 24, 2018.

Who may vote?You are entitled to vote if our records show you held one or more shares of the company’s common stock at the close of business on March 29, 2018 which we refer to as the record date. At that time, there were 53,596,522 shares of common stock outstanding and entitled to vote. Each share will entitle you to one vote at the Annual Meeting of Shareholders. For ten days prior to the Annual Meeting of Shareholders, during normal business hours, a complete list of all shareholders on the record date will be available for examination by any shareholder at the company’s offices at 2770 Research Drive, Rochester Hills, Michigan 48309-3511. The list of shareholders will also be available at the Annual Meeting of Shareholders.

How do I vote shares registered in my name?Under rules adopted by the U.S. Securities and Exchange Commission, we are primarily furnishing proxy materials to our shareholders on the Internet, rather than mailing paper copies of the materials (including our 2017 Annual Report to Shareholders (“annual report”)) to each shareholder. If you received only a Notice Regarding Internet Availability of Proxy Materials (the “Notice”) by mail or electronic mail, you will not receive a paper copy of these proxy materials unless you request one. Instead, the Notice will instruct you as to how you may access and review the proxy materials on the Internet. The Notice will also instruct you as to how you may access your proxy card to vote over the Internet. If you received a Notice by mail or electronic mail and would like to receive a paper copy of our proxy materials, free of charge, please follow the instructions included in the Notice.

We anticipate that the Notice will be mailed to our shareholders on or about April 12, 2018, and will be sent by electronic mail to our shareholders who have opted for such means of delivery on or about April 16, 2018. The Internet and telephone voting facilities for shareholders of record will close at 11:59 p.m., Eastern Daylight Time, on May 23, 2018.

About the proxy statement.The words “company,” “WABCO,” “we,” “us” and “our” refer to WABCO Holdings Inc., a Delaware corporation. We refer to the U.S. Securities and Exchange Commission as the “SEC” and the New York Stock Exchange as the “NYSE.” We were spun off from American Standard on July 31, 2007. We refer to this event as the“Spin-off.” Lastly, the words “common stock,” “stock” and “shares” refer to the company’s common stock, par value $.01 per share, which trades on the NYSE under the symbol WBC.

How will the company representatives vote for me?The company representatives, Jacques Esculier, Mazen Mazraani, Alexander De Bock and Lisa J. Brown or anyone else they choose as their substitutes, have been chosen to vote in your place as your proxies at the Annual Meeting of Shareholders. Whether you vote by proxy card, Internet or telephone, the company representatives will vote your shares as you instruct them. If you do not indicate how you want your shares voted, the company representatives will vote as the Board recommends. If there is an interruption or adjournment of the Annual Meeting of Shareholders before the agenda is completed, the company representatives may still vote your shares when the meeting resumes. If a broker, bank or other nominee holds your common stock, they will ask you for instructions and instruct the company representatives to vote the shares held by them in accordance with your instructions.

Can I change my vote after I have returned my proxy card or given instructions over the Internet or telephone?Yes. After you have submitted a proxy, you may change your vote at any time before the proxy is exercised by submitting a notice of revocation or a proxy bearing a later date. Whether or not you vote using a traditional proxy card, through the Internet or by telephone, you may use any of those three methods to change your vote. Accordingly, you may change your vote either by submitting a proxy card prior to or at the Annual Meeting of Shareholders or by voting again before 11:59 p.m., Eastern Daylight Time, on May 23, 2018, the time at which the Internet and telephone voting facilities close. The later submitted vote will be recorded and the earlier vote revoked.

1

Table of Contents

How do I vote shares held by a broker?If a broker, bank or other nominee holds shares of common stock for your benefit, and the shares are not in your name on the company’s stock transfer records, then you are considered a “beneficial owner” of those shares. Shares held this way are sometimes referred to as being held in “street name.” In that case, if you have previously elected to receive a paper copy of your proxy materials, this proxy statement and a proxy card have been sent to the broker. You may have received this proxy statement directly from your broker, together with instructions as to how to direct the broker to vote your shares. If you desire to have your vote counted, it is important that you return your voting instructions to your broker.

Rules of the NYSE determine whether proposals presented at shareholder meetings are “routine” or“non-routine.” If a proposal is routine, a broker or other entity holding shares for an owner in street or beneficial name may vote on the proposal without voting instructions from the owner. If a proposal isnon-routine, the broker or other entity may vote on the proposal only if the owner has provided voting instructions. A “brokernon-vote” occurs when the broker or other entity is unable to vote on a proposal because the proposal isnon-routine and the owner does not provide instructions. Proposal 1, the proposal to elect directors, Proposal 3, the“Say-on-Pay” advisory vote and Proposal 4, the proposal to approve the Amended and Restated 2009 Omnibus Incentive Plan, are considerednon-routine proposals under the rules of the NYSE. As a result, brokers or other entities holding shares for an owner in street name will not be able to vote on Proposals 1, 3 or 4 unless such broker or entity receives voting instructions from the beneficial owner of the shares. We believe that Proposal 2, the proposal to ratify the appointment of Ernst & Young Belgium as the independent registered public accounting firm for the company for fiscal year 2018, is considered a routine proposal under the rules of the NYSE. As a result, brokers or other entities holding shares for an owner in street name should be able to vote on Proposal 2, even if no voting instructions are provided by the beneficial owner of the shares. See “The effect of abstentions and brokernon-votes” below.

Votes required for approval.Provided that a quorum is present, the nominees for director receiving a plurality of the votes cast at the meeting in person or by proxy will be elected. However, as discussed further in Proposal 1, we have implemented a majority voting standard in uncontested director elections which requires that incumbent directors submit an irrevocable resignation contingent upon (i) the receipt of more “withheld” than “for” votes, and (ii) the acceptance of such resignation by the Board. Approval of Proposals 2, 3 and 4 require the affirmative vote of a majority of shares present or represented by proxy and entitled to vote at the Annual Meeting of Shareholders.

The effect of abstentions and brokernon-votes.Abstentions are not counted as votes “for” or “against” a proposal, but are counted in determining the number of shares present or represented on a proposal for purposes of establishing a quorum. However, since approval of Proposals 2, 3 and 4 require the affirmative vote of a majority of the shares of common stock present or represented at the Annual Meeting of Shareholders and entitled to vote, abstentions will have the same effect as a vote “against” those Proposals.

As discussed above under “How do I vote shares held by a broker?”, a “brokernon-vote” occurs if you fail to vote shares held by a broker in respect of a proposal that is considerednon-routine, and thus the broker cannot use its own discretion in casting the vote. If you hold your shares in street name, it is critical that you submit your proxy if you want your vote to count in the election of directors (Proposal 1), in the“Say-on-Pay” advisory vote (Proposal 3) and in the proposal to approve the Amended and Restated 2009 Omnibus Incentive Plan (Proposal 4). In the past, if you held your shares in street name and you did not indicate how you wanted your shares voted in the election of directors, your bank or broker was allowed to vote those shares on your behalf in the election of directors as they felt appropriate. Changes in the rules have taken away the ability of your bank or broker to vote your uninstructed shares in the election of directors on a discretionary basis. Thus, if you hold your shares in street name and you do not instruct your bank or broker how to vote in the election of directors (Proposal 1), in the“Say-on-Pay” advisory vote (Proposal 3) or in the proposal to approve the Amended and Restated 2009 Omnibus Incentive Plan (Proposal 4), your shares will be deemed brokernon-votes and no votes will be cast on your behalf on those Proposals. In tabulating the voting results for Proposals 1, 3 and 4, shares that constitute brokernon-votes are not considered entitled to vote on those Proposals. Thus, brokernon-votes will not affect the

2

Table of Contents

outcomes of Proposals 1, 3 and 4. Similarly, with respect to the company’s majority voting standard for Proposal 1, brokernon-votes are not considered as votes “for” or “withheld” in the election of directors. Thus, brokernon-votes will also not affect the outcome of Proposal 1 under the company’s majority voting standard.

What constitutes a quorum for purposes of the Annual Meeting of Shareholders?There is a quorum when the holders of a majority of the company’s outstanding common stock are present in person or represented by proxy. Withheld votes for the election of directors, proxies marked as abstentions and brokernon-votes are treated as present in determining a quorum.

Who pays for this solicitation?The expense of preparing, printing and mailing this proxy statement and the accompanying material will be borne by WABCO Holdings Inc. Solicitation of individual shareholders may be made by mail, personal interviews, telephone, facsimile, electronic delivery or other telecommunications by officers and regular employees of the company who will receive no additional compensation for those activities. We will reimburse brokers and other nominees for their expenses in forwarding solicitation material to beneficial owners.

What happens if other business not discussed in this proxy statement comes before the meeting?The company does not know of any business to be presented at the Annual Meeting of Shareholders other than the four proposals in this proxy statement. If other business comes before the meeting and is proper under Delaware law, the company representatives will use their discretion in casting all of the votes they are entitled to cast.

3

Table of Contents

BOARD RECOMMENDATIONS ON VOTING FOR PROPOSALS

The Board’s recommendation for each proposal is set forth in this proxy statement together with the description of each proposal. In summary, the Board recommends a vote:

| • | FOR Proposal 1 to elect three Class II directors. |

| • | FOR Proposal 2 to ratify the appointment of Ernst & Young Belgium as the company’s independent registered public accounting firm for the year ending December 31, 2018. |

| • | FOR Proposal 3 to approve, on an advisory basis, the compensation paid to the company’s named executive officers(“Say-on-Pay”). |

| • | FOR Proposal 4 to approve the Amended and Restated 2009 Omnibus Incentive Plan. |

4

Table of Contents

PROPOSAL 1—ELECTION OF DIRECTORS

The company has three classes of directors. The number of directors is split among the three classes as equally as possible. The term of each directorship is three years so that one class of directors is elected each year. All directors are elected for three-year terms and until their successors are duly elected and qualified. The total number of directors established by resolution of the Board of Directors is nine.

At this Annual Meeting of Shareholders, the shareholders will vote tore-elect three current Class II directors: Jean-Paul L. Montupet, D. Nick Reilly and Michael T. Smith. The Class II directors will have a term expiring at the 2021 Annual Meeting of Shareholders.

Our amended and restatedby-laws(“by-laws”) provide for a majority voting standard in uncontested director elections. Ourby-laws require that, in order for an incumbent director to be eligible forre-election, he or she must submit to the Board an irrevocable resignation that is contingent upon (i) the nominee’s receipt of a greater number of votes “withheld” from his or her election than votes “for” his or her election (with “brokernon-votes” not counted as a vote “withheld” from or “for” such person’s election) (a “Majority Withheld Vote”), and (ii) the acceptance of such resignation by the Board of Directors. If an incumbent nominee receives a Majority Withheld Vote, then the company’s Compensation, Nominating and Governance Committee (the “CNG Committee”) will make a recommendation to the Board on whether to accept or reject the previously submitted resignation. The Board of Directors will then act on the recommendation of the CNG Committee within 90 days after the certification of the shareholder vote, and the company will disclose the Board’s decision in a Current Report on Form8-K filed with the SEC promptly thereafter.

The Board of Directors has no reason to believe that any of the nominees will not serve if elected. If a nominee should become unavailable to serve as a director, and if the Board designates a substitute nominee, the company representatives named on the proxy card will vote for the substitute nominee designated by the Board unless you submit a proxy withholding your vote from the nominee being substituted. Under theby-laws, vacancies are filled by the Board of Directors.

The Board of Directors unanimously recommends that shareholders vote FOR Proposal 1, the election of Jean-Paul L. Montupet, D. Nick Reilly and Michael T. Smith, as Class II directors.

5

Table of Contents

Nominees for Election for Class II Directors—Terms Expiring at the 2018 Annual Meeting of Shareholders

Jean-Paul L. Montupet—Age 70

Director since April 2012

Mr. Montupet serves as an Advisory Director of Emerson Electric Co. He served as President of Emerson Europe SA until December 2012, and had served as an Executive Vice President of Emerson Electric Co. since 1990 where he was responsible for its Industrial Automation Business. From 2002 to March 2016, Mr. Montupet served on the Board of PartnerRe Ltd., a leading global reinsurer; he served asnon-Executive Chairman from 2010 to March 2016 and was also Chairman of the Nominating and Governance Committee and a member of the Risk and Finance Committee. Mr. Montupet served as a member of the board of directors of Lexmark International Inc., a leading provider of imaging products and services until November 2016. In addition, Mr. Montupet is a director of IHS Markit Ltd. and Assurant, Inc.

The Board of Directors concluded that the following experience, qualifications and skills qualified Mr. Montupet to serve as director of the company: significant executive management experience gained as an executive officer at a global Fortune 500 company publicly traded on the New York Stock Exchange; strong international experience gained as an executive officer of Emerson Electric Co., a company with more than 129,000 employees and 250 manufacturing locations worldwide; financial expertise acquired as a president and as a chief financial officer and serving on the audit committees of two publicly-traded companies; strong educational background with an advanced business degree from HEC Paris, one of the top business schools in Europe; and additional experience gained as a director of another publicly-traded company listed on the NYSE and the Paris Stock Exchange.

D. Nick Reilly, CBE—Age 68

Director since December 2014

Since 2012 Mr. Reilly has served on the Advisory Board of MSXI Inc., a privately held company that provides engineering and staffing services to clients mainly in the automotive industry. Prior to his role on the Advisory Board, he served as Chairman, Asia Pacific for MSXI Inc. From 2012 to 2016, Mr. Reilly has also served as a strategic adviser to UkrAuto Corporation, a Ukrainian importer of cars that owns the largest network of manufacturing and assembling facilities, service stations and auto dealerships in Ukraine. From 2012 until March 2016, Mr. Reilly served as Vice Chairman of erae Automotive (previously Korea Delphi Automotive Components) a privately held company that develops, manufactures and sells automotive components in South Korea and internationally. Prior to 2012, Mr. Reilly spent 37 years with General Motors Corporation (“General Motors” “GM”), and held several international executive roles , such as President, GM Europe from 2009 to 2012, President, GM International from 2008 to 2009 and President, GM Asia Pacific from 2006 to 2008 and President, GM Daewoo from 2001 to 2006. Prior to General Motors, Mr. Reilly worked for three years in the finance and investment community.

The Board of Directors concluded that the following experience, qualifications and skills qualified Mr. Reilly to serve as a director of the company: extensive international executive experience with General Motors, including significant experience in finance, manufacturing, quality control, purchasing, sales and aftermarket sales of automotive equipment and significant experience in evaluating new business opportunities as a strategic adviser to three companies in the international automotive industry.

6

Table of Contents

Michael T. Smith—Age 74

Director since July 2007

Mr. Smith served as the Chairman of the Board and Chief Executive Officer of Hughes Electronics Corporation from 1997 to 2001, before retiring in 2001. Prior to those positions, Mr. Smith had been Vice Chairman of Hughes Electronics and Chairman of the Hughes Aircraft Company. Mr. Smith joined Hughes Electronics in 1985 as Senior Vice President and Chief Financial Officer after spending nearly 20 years with General Motors in a variety of financial management positions. In 1992 he was elected Vice Chairman of Hughes Electronics and President of Hughes Missile Systems Group, and in 1995 he was elected Chairman of Hughes Aircraft Company. Mr. Smith was also a member of the Board of Directors of Alliant Techsystems until 2009 and Ingram Micro, Inc. until 2014. Mr. Smith is a member of the Board of Directors of Teledyne Technologies, Inc., FLIR Systems, Inc. and Zero Gravity Solutions, Inc.

The Board of Directors concluded that the following experience, qualifications and skills qualified Mr. Smith to serve as a director of the company: significant executive management experience gained as an executive officer of a Fortune 500 company that is publicly traded on the NYSE; strong international experience gained as the Chairman of the Board and Chief Executive Officer of Hughes Electronics Corporation; financial expertise acquired as Chief Financial Officer of Hughes Electronics and by holding various financial management positions with General Motors; and board experience gained as a member of the board of directors of three publicly-held companies. In summary, Mr. Smith has leadership and financial management abilities that substantially strengthen the company due to his multinational knowledge of the global automotive sector and his understanding of the strategic needs of major original equipment manufacturers.

Class III Directors Continuing in Office—Terms Expiring at the 2019 Annual Meeting of Shareholders

Jacques Esculier—Age 58

Director since July 2007 and Chairman since May 2009

Jacques Esculier has served as our Chief Executive Officer and Director since July 2007. Since May 2009, he has also served as our Chairman of the Board. Prior to July 2007, Mr. Esculier served as Vice President of American Standard Companies Inc. and President of its Vehicle Control Systems business, a position he had held since January 2004. Prior to holding that position, Mr. Esculier served in the capacity of Business Leader for American Standard’s Trane Commercial Systems’ Europe, Middle East, Africa, India & Asia Region from 2002 through January 2004. Prior to joining American Standard in 2002, Mr. Esculier spent more than six years in leadership positions at AlliedSignal/Honeywell. He was Vice President and General Manager of Environmental Control and Power Systems Enterprise based in Los Angeles and Vice President of Aftermarket Services—Asia Pacific based in Singapore. Mr. Esculier is a member of the Board of Directors of Pentair plc.

The Board of Directors concluded that the following experience, qualifications and skills qualified Mr. Esculier to serve as our Chairman and Chief Executive Officer: significant executive management experience gained as an executive officer at two Fortune 500 companies publicly traded on the New York Stock Exchange; strong international experience gained as an executive officer of American Standard; and financial expertise acquired as chief executive officer with the chief financial officer as a direct report and by holding several senior management positions. In summary, Mr. Esculier has multi-cultural leadership and outstanding strategic abilities to steward and sustain the company’s performance as it maintains its position as an industry innovation leader while pursuing global expansion and excellence in execution.

Thomas S. Gross—Age 63

Director since March 2016

Mr. Gross served from 2009 to 2015 as Vice Chairman and Chief Operating Officer of the Electrical Sector at Eaton Corporation plc, a global power management company, before retiring in 2015. Prior to that, at Eaton Corporation, he was President, Power Quality and Control Business; President, Power Quality Solutions; and

7

Table of Contents

Vice President, Eaton Business System. After joining Eaton in 2003, Mr. Gross gained senior executive experience through businesses that supply technological solutions globally for a range of industrial power systems and controls. Previously, Mr. Gross held senior executive positions at Danaher Corporation, a global science and technology company serving a variety of industries, and at Xycom, a technology company serving the industrial automation and control sector. He began his career at Rockwell Automation in 1977, earning increased responsibilities over two decades, and was ultimately promoted to President, Rockwell Software. Mr. Gross currently serves on the Board of RPM International Inc., a world leader in specialty coatings and sealants. Mr. Gross served as Director of Celestica Inc., a leading manufacturer of electronic and electro-mechanical solutions, until November 2017. Mr. Gross holds a Master of Business Administration degree from the University of Michigan and a Bachelor of Science degree from the University of Wisconsin, both located in the United States.

The Board of Directors concluded that the following experience, qualifications and skills qualified Mr. Gross to serve as director of the company: significant executive management experience gained as an executive officer at Eaton Corporation plc, Danaher Corporation and Rockwell Automation; extensive experience in finance, capital allocation, compensation, management development, and acquisitions; and board experience gained as a director of another publicly-held company.

Henry R. Keizer—Age 61

Director since July 2015

Mr. Henry R. Keizer served from 2010 to 2012 as Deputy Chairman and Chief Operating Officer of KPMG LLP, one of the world’s largest accounting and professional services firms, before retiring in 2012. Prior to that, for five years, he was Global Head of Audit at KPMGI, a consortium of more than 100 KPMG firms operating in over 140 countries. During his 35 years at KPMG, Mr. Keizer held a range of senior executive leadership roles of increasing responsibility, advising clients engaged in finance, manufacturing and technology, among other sectors.

Mr. Keizer currently serves as a trustee of BlackRock Funds. He also serves as thenon-executive chairman and a director of Hertz Global Holdings, Inc., a global rental car company, a director of Sealed Air Corporation (NYSE:SEE) and as a director of Park Indemnity Ltd., a captive insurer affiliated with KPMGI. Previously, Mr. Keizer served on the boards of MUFG Americas Holding Corporation, MUFG Union Bank and Montpelier Re Holdings, Ltd, a global property and casualty reinsurance company and the American Institute of Certified Public Accountants. He holds a bachelor’s degree in accounting, summa cum laude, from Montclair State University, New Jersey, U.S.A.

The Board of Directors concluded that the following experience, qualifications and skills qualified Mr. Keizer to serve as a director of the company: significant executive management experience gained as Chief Operating Officer at KPMG; financial expertise acquired by holding various financial positions of increasing responsibility; strong international experience gained as Global Head of Audit at KPMGI; and board experience gained as a director of publicly-held companies.

Class I Directors Continuing in Office—Terms Expiring at the 2020 Annual Meeting of Shareholders

G. Peter D’Aloia—Age 73

Director since July 2007

Mr. D’Aloia served as Senior Vice President and Chief Financial Officer of American Standard Companies Inc., a position he held since 2000, before retiring in 2008. Before joining American Standard, Mr. D’Aloia worked for Honeywell where he most recently served as Vice President—Business Development. He spent 27 years with Honeywell’s predecessor company, AlliedSignal, in diverse finance management positions. During his career with AlliedSignal, he served as Vice President—Taxes; Vice President and Treasurer; Vice President and

8

Table of Contents

Controller; and Vice President and Chief Financial Officer for the Engineered Materials Sector. Early in his career, he worked as a tax attorney for the accounting firm, Arthur Young and Company. Mr. D’Aloia served as a director of ITT Inc. from October 2011 until May 2017. Mr. D’Aloia is a director of FMC Corporation.

The Board of Directors concluded that the following experience, qualifications and skills qualified Mr. D’Aloia to serve as a director of the company: significant executive management experience gained as an executive officer of two Fortune 500 companies, both publicly traded on the New York Stock Exchange; strong international experience gained as Vice President and Chief Financial Officer for American Standard; financial expertise acquired as Chief Financial Officer of American Standard and by holding diverse financial management positions with AlliedSignal and working as a tax attorney for the accounting firm, Arthur Young and Company; and board experience gained as a member of the board of directors of two publicly-held companies. In summary, Mr. D’Aloia has financial management abilities, including multinational legal, tax and banking expertise, that significantly contribute to the company’s success as a globally operating entity while taking full advantage of business opportunities in developed as well as emerging economies.

Juergen W. Gromer—Age 73

Director since July 2007

Dr. Gromer is the retired President and CEO of Tyco Electronics, a position that he held from April 1999 until December 31, 2007. Dr. Gromer formerly held senior management positions from 1983 to 1998 at AMP (acquired by Tyco in April 1999) including Senior Vice President of Worldwide Sales and Services, President of the Global Automotive Division, and Vice President of Central and Eastern Europe, and General Manager of AMP Germany. Dr. Gromer has over 20 years of AMP and Tyco Electronics experience, serving in a wide variety of regional and global assignments. Before working for Tyco Electronics and AMP, Dr. Gromer held management positions at ZF Friedrichshafen, ITT and Procter & Gamble. Dr. Gromer served as a member of the board of directors of TE Connectivity (formerly Tyco Electronics) from June 2007 until March 2017, Marvell Technology Group Ltd. from October 2007 until November 2016, and RWE Rhein Ruhr AG from 2000 to 2009. He is also Chairman of the Board of the Society for Economic Development of the District Bergstrasse/Hessen and from 1992 to 2016 a director of the American Chamber of Commerce in Germany. Dr. Gromer served as a member of the Advisory Board of Commerzbank from 1992 to 2015.

The Board of Directors concluded that the following experience, qualifications and skills qualified Dr. Gromer to serve as a director of the company: significant executive management experience gained as an executive officer of a Fortune 500 company publicly traded on the New York Stock Exchange; strong international experience gained as President of Tyco Electronics; financial expertise acquired as a President of Tyco Electronics and through various senior management positions and also as a member of the Advisory Board of Commerzbank; and board experience gained as a director of publicly-held companies. In summary, Dr. Gromer has global leadership abilities, as well as deep connections with European corporate culture, and he strongly contributes to the company’s strategy of geographic expansion while maintaining a leading technology and industry position in Europe.

Mary L. Petrovich—Age 55

Director since November 2011

Mary Petrovich has served as the Executive Chairman of AxleTech International, a supplier ofoff-highway and specialty vehicle drive train systems and components, since January 2015 and as Senior Advisor to The Carlyle Group since June 2011. Prior to rejoining AxleTech as its Executive Chairman, Ms. Petrovich was Chairman and CEO of AxleTech from 2001 to December 2011. Prior to AxleTech, in 2000, Ms. Petrovich was President of the Driver Controls Division of Dura Automotive, possessing management responsibility for 7,600 employees. From 2011 to 2014, Ms. Petrovich served as a director on the boards of Modine Manufacturing Company, a global provider of thermal management technology and systems, and GT Advanced Technologies Inc. Ms. Petrovich currently serves on the board of directors of Woodward, Inc., a leading manufacturer and service provider of energy controls for global infrastructure equipment.

9

Table of Contents

The Board of Directors concluded that the following experience, qualifications and skills qualified Ms. Petrovich to serve as a director of the company: extensive experience with mergers, acquisitions and the integration of acquired businesses in the automotive,off-highway and transportation industries; extensive operational experience with Six Sigma lean manufacturing techniques and supply chain management; significant experience in evaluating new business opportunities; and board experience gained as a director of publicly-held companies.

10

Table of Contents

Board Matters and Committee Membership

Our business, property and affairs are managed under the direction of our Board of Directors. Members of our Board are kept informed of our business through discussions with our Chairman and Chief Executive Officer and other officers and employees, by reviewing materials provided to them during visits to our offices and plants and by participating in meetings of the Board and its committees.

The Board of Directors held a total of 12 meetings in 2017. The standing committees of the Board of Directors are the Audit Committee and the CNG Committee.All directors attended 75% or more of the combined total number of meetings of the Board of Directors and the Board committees on which they served during 2017.

The table below provides committee assignments and 2017 meeting information for each of the Board committees:

Name | Audit Committee | Compensation, Nominating and Governance Committee | ||||||||

G. Peter D’Aloia | X | |||||||||

Juergen W. Gromer | X | |||||||||

Jean-Paul L. Montupet | X | |||||||||

Michael T. Smith | X | |||||||||

Jacques Esculier | ||||||||||

Mary L. Petrovich | X | |||||||||

D. Nick Reilly | X | (1) | ||||||||

Henry R. Keizer | X | * | ||||||||

Thomas S. Gross | X | *(2) | ||||||||

2017 Meetings | 9 | 6 | ||||||||

| * | Indicates Committee Chair |

| (1) | Mr. Reilly served on the CNG Committee until March 23, 2017, at which time he was reassigned to the Audit Committee. |

| (2) | Mr. Gross served on the Audit Committee until March 23, 2017, at which time he was reassigned to the CNG Committee and appointed as Chair in replacement of Mr. Montupet, who was appointed Lead Director on March 23, 2017 and remains a member of the CNG Committee. |

Audit Committee

The Audit Committee has been established in accordance with Section 3(a)(58)(A) of the Securities Exchange Act of 1934, as amended. Each member of the Audit Committee is independent as defined by the NYSE listing standards and the company’s independence standards. The Audit Committee’s responsibilities, as set forth in its charter, include:

| • | reviewing the scope of internal and independent audits; |

| • | reviewing the company’s quarterly and annual financial statements and Annual Report on Form10-K; |

| • | reviewing the adequacy of management’s implementation of internal controls; |

| • | reviewing with management and the independent auditors the company’s actions and activities concerning risk assessment and risk management; |

| • | reviewing the company’s accounting policies and procedures and significant changes in accounting policies; |

11

Table of Contents

| • | appointing the independent auditors and reviewing their independence and performance and the reasonableness of their fees; and |

| • | reviewing compliance with the company’s Code of Conduct and Ethics, major litigation, compliance with environmental standards and the investment performance and funding of the company’s retirement plans. |

The Board of Directors has determined that Mr. Keizer, chair of the Audit Committee, is an audit committee financial expert as defined by the SEC. In addition, the Board has determined that each member of the Audit Committee is financially literate as defined by the NYSE.

Compensation, Nominating and Governance Committee

Our Board of Directors has delegated its compensation, nominating and governance functions to a single standing committee, the CNG Committee. Each member of the CNG Committee is independent as defined by the NYSE listing standards and the company’s independence standards. The CNG Committee’s responsibilities, as set forth in its charter, include:

| • | identifying individuals qualified to become members of the Board and recommending to the Board director nominees to be presented at the annual meeting of shareholders as well as nominees to fill vacancies on the Board; |

| • | recommending Board committee memberships, including committee chairpersons; |

| • | considering and making recommendations concerning director nominees proposed by shareholders; |

| • | developing and recommending to the Board corporate governance principles for the company and processes for Board evaluations; |

| • | reviewing and making recommendations concerning compensation of directors; |

| • | reviewing and making recommendations concerning executive officers’ salaries and employee benefit and executive compensation plans and administering certain of those plans, including the company’s incentive compensation and stock incentive plans; |

| • | reviewing and approving performance goals and objectives for all executive officers, evaluating performance against objectives and based on its evaluation, approving base and incentive compensation for all executive officers except for the Chairman and Chief Executive Officer, whose base and incentive compensation is recommended by the CNG Committee and approved by the independent members of the Board; and |

| • | evaluating executive succession plans, the quality of management, and leadership and management development. |

For a description of the CNG Committee’s responsibility in determining executive compensation, see “Compensation Discussion and Analysis—Role of the CNG Committee in the Compensation Process” in this proxy statement.

Our Board of Directors includes several directors with European and international leadership experience which we believe provides the diversity of perspective necessary for a European-based company listed in the United States with increasingly global operations and sales. While international leadership experience is important to our CNG Committee in considering potential director nominees, as described in “Other Matters—Director Nominations” below, our CNG Committee will also consider judgment, age, skills, gender, ethnicity, race, culture, diversity of thought, geography and other measures to ensure that the Board as a whole reflects a range of viewpoints, backgrounds, skills, experience and expertise.

12

Table of Contents

The Board has determined that all members of the Compensation Committee are“non-employee directors” (within the meaning of Rule16b-3 under the Securities Exchange Act of 1934, as amended) and “outside directors” (within the meaning of Section 162(m) of the Internal Revenue Code).

Our Board of Directors oversees risk management and risk assessment both directly and indirectly through the board committees. Board oversight is enterprise-wide, with a particular focus on five primary areas of risk: strategic, operational, financial, IT and compliance and governance. To organize its risk oversight responsibilities, our Board of Directors reviews a comprehensive risk governance scorecard that identifies all of the material risk categories within these five primary areas and identifies a responsible person or “owner” among our senior management for managing that risk. Each risk category is then assigned to the full Board of Directors or to one or more of the board committees for primary monitoring responsibility. Both the company processes for managing the risk and the Board’s (or committee’s) processes for monitoring the risk are clearly set forth in the risk governance scorecard and both these processes and the delegation of responsibilities in the scorecard is reviewed annually by our full Board of Directors.

Our Audit Committee focuses on financial risk, including internal controls, and receives regular reports from members of senior management, including our Chief Financial Officer, Controller, Chief Legal Officer and Company Secretary, Treasurer, Vice President, Taxes and Internal Audit Director. Our CNG Committee focuses on the risks associated with leadership assessment, management succession planning, corporate governance and executive compensation programs and policies, and receives regular reports from members of senior management, including our Chief Executive Officer, Chief Human Resources Officer and Chief Legal Officer and Company Secretary. Each of these committees regularly reports to the full Board of Directors. In addition, our Board of Directors oversees the company’s strategic planning and receives reports at the beginning of each year regarding our annual operating plan (our “Operating Plan”) and budget as well as our long-term planning and strategy.

Risk Assessment of our Compensation Program

In designing our compensation program for our executive officers, including our named executive officers, our CNG Committee structures such programs to balance reward and risk, while mitigating the incentive for excessive risk-taking. The possibility of excessive risk-taking is limited by the following measures:

| • | Base salaries are fixed amounts at market competitive levels; |

| • | Annual and long-term incentive plans are based on a balanced mix of complementary general corporate financial measures and do not take into consideration any specific/individual results of business units; |

| • | Maximum payouts under our annual and long-term incentive plans are capped; |

| • | Our long-term incentive plan is comprised of a balanced portfolio of performance-based cash incentive awards, performance-based stock units (“PSUs”) and time-vested restricted stock units (“RSUs”) that vest over multiple years, or after multiple years (i.e., cliff vesting for PSUs), which aligns our named executive officers’ interests with our shareholders’ interests; |

| • | Cash and equity incentive awards are subject to forfeiture upon termination; |

| • | Members of the CNG Committee approve the final incentive awards after reviewing the executive and corporate performance achievements and may utilize negative discretion; |

| • | The company adopted an incentive pay recoupment policy, also referred to as a “clawback,” that requires recovery from executive officers of any annual incentive plan awards for 2012 and later years, if such compensation was received during the three-year period preceding the date of a restatement of any financial statements due to materialnon-compliance with the financial reporting rules; |

13

Table of Contents

| • | All of our directors and officers, including our named executive officers, are subject to stock ownership guidelines, as described below; and |

| • | Our policy is to prohibit our officers and directors from pledging, hypothecating, or otherwise encumbering our common stock as collateral for indebtedness, and we also prohibit our officers and directors from holding our common stock in a margin account, or purchasing any financial instrument or entering into any transaction that is designed to hedge or offset any decrease in the market value of our common stock (including, but not limited to, prepaid variable forward contracts, equity swaps, collars, or exchange funds). |

Our CNG Committee has determined that our executive as well as employee compensation programs, policies and practices are not reasonably likely to have a material adverse effect on our company. The CNG Committee will continue to periodically oversee and monitor risk in our compensation program.

Compensation Committee Interlocks and Insider Participation

None.

Board Attendance at the Annual Meeting of Shareholders

In accordance with our Corporate Governance Guidelines, all directors are expected to attend the Annual Meeting of Shareholders. While the Board understands that there may be situations that prevent a director from attending, the Board strongly encourages all directors to make attendance at all annual meetings of shareholders a priority. All of our directors at the time attended the company’s 2017 Annual Meeting of Shareholders.

Independence Standards for Board Service

The Board of Directors has adopted a definition of director independence fornon-management directors that serve on the company’s Board of Directors which meet and in some areas exceed the NYSE listing standards. Each director, other than Jacques Esculier, the company’s Chairman and Chief Executive Officer, satisfies the definition of director independence adopted and accordingly has no material relationship with the company (either directly or indirectly as a partner, shareholder or officer of an organization that has a relationship with the company) other than serving as a director of, and owning stock in, the company. A copy of our definition of director independence is attached to this proxy statement as Appendix A and is also available on our web sitewww.wabco-auto.com, by following the links “Investor Relations—Corporate Governance—Definition of Director Independence.” In addition, none of the company’s directors and executive officers participated in any related person transactions nor were any other transactions considered by the Board in determining directors’ independence. For a discussion of the company’s policy on related person transactions, please see “Certain Relationships or Related Person Transactions and Section 16 Reporting Compliance—Certain Relationships and Related Person Transactions” in this proxy statement.

From August 2007 through May 2009, the positions of Chairman of the Board and Chief Executive Officer were held by separate people, due in part to the fact that the company was a newly independent stand-alone public company after theSpin-off, and also due to the fact that the Board was newly constituted and, in large part, unfamiliar with the Chief Executive Officer. Based in part on the strong governance structure established by our thennon-executive Chairman of the Board, the Board’s increasing familiarity and comfort with the Chief Executive Officer and in recognition of the potential efficiencies of having the Chief Executive Officer also serve in the role of Chairman of the Board, the Board decided to revise its structure. In 2009, our Board of Directors unanimously approved a proposal to combine the Chairman of the Board and Chief Executive Officer roles and appointed Jacques Esculier as Chairman of the Board. Michael T. Smith served as our Lead Director from May 2012 until March 2017. Jean-Paul Montupet was appointed as Lead Director in March 2017.

14

Table of Contents

As the Chairman of the Board, Mr. Esculier provides leadership to the Board and works with the Board to define its structure and activities in fulfillment of its responsibilities. Our Lead Director’s duties include presiding at all meetings of the company’snon-management directors and, in consultation with the Chairman of the Board, developing the agendas for the board meetings and determining the appropriate scheduling for board meetings. Our Lead Director also acts as a liaison between the company’s Chairman of the Board and the company’snon-management directors and assists the company’s independent directors in discharging their duties to the company and its shareholders. A more detailed description of the role of our Lead Director is included in our Corporate Governance Guidelines.

Communication with the Company’s Board of Directors

Our Lead Director presides over all executive sessions of thenon-management directors. Shareholders or other interested parties wishing to communicate with our Board of Directors can communicate with our Board of Directors by writing to: Chief Legal Officer and Company Secretary, c/o WABCO Holdings Inc., 2770 Research Drive, Rochester Hills, Michigan 48309-3511. Your message will not be screened or edited before it is delivered to the Lead Director. The Lead Director will determine whether to relay your message to other Board members. See “Other Matters—Director Nominations” below for a description of how shareholders may submit the names of candidates for director nominees to our Board of Directors.

Availability of Corporate Governance Materials

The company’s Code of Conduct and Ethics and Governance Principles, including our definition of director independence, as well as the charters for the Audit Committee and the CNG Committee are available on our web sitewww.wabco-auto.comunder the caption “Investor Relations—Corporate Governance.” The foregoing information is available in print to any shareholder who requests it. Requests should be addressed to Chief Legal Officer and Company Secretary, WABCO Holdings Inc., 2770 Research Drive, Rochester Hills, Michigan 48309-3511.

15

Table of Contents

CERTAIN RELATIONSHIPS OR RELATED PERSON TRANSACTIONS AND SECTION 16 REPORTING COMPLIANCE

Certain Relationships and Related Person Transactions

The Audit Committee of the Board of Directors has adopted a written policy governing the review and approval or ratification of related person transactions. Under the policy, a related person transaction is any transaction exceeding $120,000 in which the company or a subsidiary, on the one hand, and an executive officer, director, holder of 5% or more of the company’s voting securities or an immediate family member of such person, on the other hand, had or will have a direct or indirect material interest.

No related person transaction shall be approved or ratified if such transaction is contrary to the best interest of the company. Unless determined otherwise by the Audit Committee, any related person transaction must be on terms that are no less favorable to the company than would be obtained in a similar transaction with an unaffiliated third party under the same or similar circumstances.

Unless the Audit Committee determines otherwise, any proposed related person transaction directly between the company and an executive officer, director or immediate family member should be reviewed prior to the time the transaction is entered into. In addition, the policy provides that ordinary course transactions are not considered related person transactions, and therefore do not require approval under the company’s related person transaction policy. An ordinary course transaction means a transaction that occurs between the company or any of its subsidiaries and any entity (i) for which any related person serves as an executive officer, partner, principal, member or in any similar executive or governing capacity, or (ii) in which such related person has an economic interest that does not afford such related person control over such entity, and such transaction occurs in the ordinary course of business on terms and conditions that are no less favorable to the company or, if applicable, a subsidiary than would otherwise apply to a similar transaction with an unrelated party. In addition, all immaterial relationships and transactions identified in the Instructions to Item 404(a) of RegulationS-K are incorporated into the policy, and accordingly, all such immaterial relationships or transactions are not related person transactions and do not require approval under the policy.

The Chief Legal Officer and Company Secretary is responsible for making the initial determination as to whether any transaction constitutes a related person or ordinary course of business transaction and for taking all reasonable steps to ensure that all related person transactions required to be disclosed pursuant to Item 404(a) of RegulationS-K are presented to the Audit Committee forpre-approval or ratification. If a related person transaction involves the Chief Legal Officer and Company Secretary, the Chief Financial Officer shall perform the responsibilities under the policy.

The Audit Committee reviews and assesses the adequacy of the policy annually.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Securities Exchange Act of 1934, as amended, requires our directors, certain executive officers, and persons who own more than 10% of the Company’s outstanding common stock to file reports of ownership and changes in ownership with the SEC and the NYSE. Those “reporting persons” are required by SEC regulation to furnish the Company with copies of all Section 16(a) forms they file.

SEC regulations require the company to identify anyone who failed to file a required report or filed a late report during the most recent fiscal year. Based upon a review of those filings and other information furnished by the reporting persons, we believe that, with respect to the fiscal year ended December 31, 2017, all applicable filings were timely filed, except that, in each case, one late Form 4 reflecting one transaction was filed on behalf of each of Messrs. D’Aloia, Gromer, Montupet, Smith, Reilly, Keizer and Gross as well as Ms. Petrovich.

16

Table of Contents

Audit CommitteePre-Approval Policies and Procedures

The Audit Committee is directly responsible for the appointment, compensation, retention and oversight of the work of Ernst & Young Belgium, our independent registered public accounting firm (“independent auditor”). The independent auditor reports directly to the Audit Committee. As part of its responsibility, the Audit Committee established a policy topre-approve all Audit Services and permissibleNon-Audit Services performed by the independent auditor. Inpre-approving services, the Audit Committee considers whether such services are consistent with the SEC’s rules on auditor independence.

The Audit Committee also considers whether the independent auditor is best positioned to provide the most effective and efficient service, for reasons such as its understanding and knowledge of the company’s business, people, culture, accounting systems, risk profile and other factors, and whether the service might enhance the company’s ability to manage or control risk or improve audit quality.

The Audit Committee is mindful of the relationship between fees for Audit and permissibleNon-Audit Services in deciding whether topre-approve any such services and may determine, for each fiscal year, the appropriate relationship between the total amount of fees for Audit and Audit-Related Services and the total amount of fees for Tax Services and certain permissibleNon-Audit Services classified as “All Other Services.” Prior to the engagement of the independent auditor for an upcomingaudit/non-audit service period, defined as a twelve-month timeframe, Ernst & Young Belgium submits to the Audit Committee for approval a detailed list of services expected to be rendered during that period as well as an estimate of the associated fees for each of the following four categories of services:

Audit Servicesconsist of services rendered by an external auditor for the audit of the company’s annual consolidated financial statements (including tax services performed to fulfill the auditor’s responsibility under generally accepted auditing standards), the audit of internal control over financial reporting performed in conjunction with the audit of the annual consolidated financial statements and reviews of financial statements included in Form10-Qs. Audit Services includes services that generally only an external auditor can reasonably provide, such as comfort letters, statutory audits, attest services, consents and assistance with and review of documents filed with the SEC.

Audit-Related Servicesconsist of assurance and related services (e.g., due diligence) by an external auditor that are reasonably related to the audit or review of financial statements, including employee benefit plan audits, due diligence related to mergers and acquisitions, employee benefit plan audits, accounting consultations and audits in connection with proposed or consummated acquisitions, internal control reviews, attest services related to financial reporting that are not required by statute or regulation, audit-related litigation advisory services and consultation concerning financial accounting and reporting standards, including compliance with Section 404 of the Sarbanes-Oxley Act.

Tax Servicesconsist of services performed by the independent auditor’s tax personnel except those included in Audit Services above. Tax Services include those services rendered by an external auditor for tax compliance, tax consulting, tax planning, expatriate tax services, transfer pricing studies, tax planning, and tax issues related to stock compensation.

OtherNon-Audit Servicesare any other permissible work that is not an Audit, Audit-Related or Tax Service and includenon-audit-related litigation advisory services and administrative assistance related to expatriate services.

For each type of service, details of the service as well as estimated fees are reviewed andpre-approved by the Audit Committee as either an annual amount or specified stand-alone activity.Pre-approval of such services is used as the basis for establishing the spend level, and the Audit Committee requires the independent auditor to report detailed actual/projected fees versus the budget periodically throughout the year by category of service and by specific project.

17

Table of Contents

Circumstances may arise during the twelve-month period when it may become necessary to engage the independent auditor for additional services or additional effort not contemplated in the originalpre-approval. In those instances, the Audit Committee requires specificpre-approval before engaging the independent auditor.

This review is typically done in formal Audit Committee meetings; however, the Audit Committee may delegatepre-approval authority to one or more of its members. The member to whom such authority is delegated must report anypre-approval decisions to the Audit Committee at its next scheduled meeting.

Fees billed to the company by Ernst & Young Belgium for services rendered in 2017 and 2016 were as follows:

Type of Service(1) | 2017 | 2016 | ||||||

| (in thousands) | ||||||||

Audit | $ | 4,699 | $ | 2,737 | ||||

Audit-Related | $ | 288 | $ | 50 | ||||

Tax | $ | 265 | $ | 297 | ||||

All Other | — | — | ||||||

|

|

|

| |||||

Total | $ | 5,252 | $ | 3,084 | ||||

|

|

|

| |||||

| (1) | For a description of the types of services, see “Audit Committee Matters—Audit CommitteePre-Approval Policies and Procedures,” above. |

18

Table of Contents

PROPOSAL 2—RATIFICATION OF APPOINTMENT OF THE

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Audit Committee of the Board of Directors has appointed Ernst & Young Belgium as the company’s independent registered public accounting firm to examine the consolidated financial statements of the company for fiscal year 2018 upon terms set by the Audit Committee. The Board of Directors recommends that this appointment be ratified by the shareholders. If the appointment of Ernst & Young Belgium is not ratified by the shareholders, the Audit Committee will give consideration to the appointment of other independent registered public accounting firms.

Representatives of Ernst & Young Belgium will be present at the Annual Meeting of Shareholders, will have the opportunity to make a statement if they desire to do so and are expected to be available to respond to appropriate questions.

The Board of Directors unanimously recommends that shareholders vote FOR Proposal 2, the ratification of the appointment of Ernst & Young Belgium as the company’s independent registered public accounting firm for the year ending December 31, 2018.

19

Table of Contents

The Audit Committee oversees the company’s financial reporting process on behalf of the Board of Directors. In fulfilling its responsibilities, the committee has reviewed and discussed the audited financial statements in the Annual Report with the company’s management and independent auditors.

Management has the primary responsibility for the financial statements and the reporting process including the internal controls systems, and has represented to the Audit Committee that such financial statements were prepared in accordance with generally accepted accounting principles. The independent auditors are responsible for expressing an opinion on the conformity of those audited financial statements with generally accepted accounting principles.

The Audit Committee has discussed with the independent auditor the matters required to be discussed by Auditing Standard No. 1301, Communications with Audit Committees issued by the Public Company Accounting Oversight Board. In addition, the committee has discussed with the independent auditor, the auditor’s independence, including the matters in the written disclosures and letter which were received by the committee from the independent auditors, as required by Independence Standards Board Standard No. 1, Independence Discussions with Audit Committees. The Audit Committee has also considered whether the independent auditor’s provision ofnon-audit services to the company is compatible with maintaining the auditor’s independence.

The committee discussed with the company’s internal and independent auditors the overall scope and plans for their respective audits. The committee meets with the internal and independent auditors, with and without management present, to discuss the results of their examinations, their evaluations of the company’s internal controls, and the overall quality of the company’s financial reporting.

Based on the reviews and discussions referred to above, the committee recommended to the Board of Directors that the audited financial statements be included in the Annual Report on Form10-K for the year ended December 31, 2017, for filing with the U.S. Securities and Exchange Commission.

Members of the Audit Committee:

Henry R. Keizer, Chairman

G. Peter D’Aloia

Dr. Juergen W. Gromer

D. Nick Reilly

20

Table of Contents

COMPENSATION DISCUSSION AND ANALYSIS

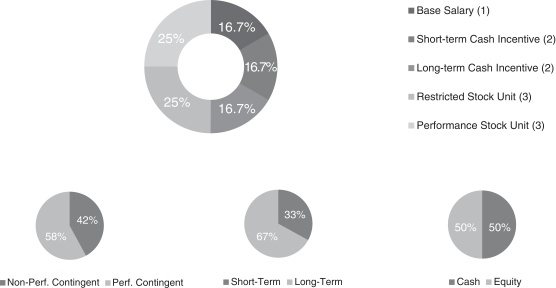

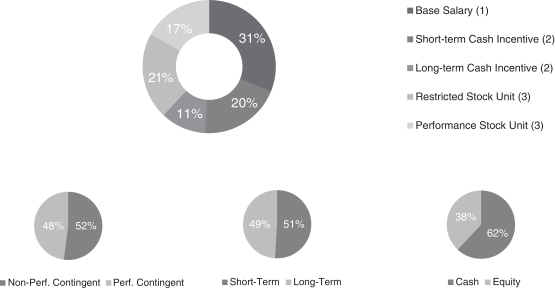

We seek to closely align the interests of our named executive officers (“NEOs”) with the interests of our shareholders. Our compensation programs are designed to reward our NEOs for achieving short-term and long- term strategic and operational goals and increasing total shareholder returns, while at the same time avoiding incentives that encourage unnecessary or excessive risk-taking. Our NEOs’ total compensation is comprised of a mix of base salary, annual cash incentive awards and long-term incentive awards that include both performance-based cash and equity awards.

For 2017, our NEOs were:

• Jacques Esculier | Chairman of the Board and Chief Executive Officer (“CEO”) | |

• Alexander De Bock | Chief Financial Officer (interim)* | |

• Nick Rens | President, Trailer Systems, Aftermarket & Off Highway Division | |

• Jorge Solis | President, Truck, Bus & Car Original Equipment Manufacturers Division | |

• Nicolas Bardot | Chief Supply Chain Officer | |

• Prashanth Mahendra-Rajah | Former Chief Financial Officer* | |

| * | Mr. De Bock started his interim tenure on September 1, 2017 and Mr. Mahendra-Rajah left on September 30, 2017. |

2017 Performance(1)

Fiscal 2017 was another strong year of performance for WABCO. Specific achievements in 2017 included:

| • | Sales/Sales Growth:WABCO continued to strongly perform in the global truck and bus production market in 2017. Global production of trucks and buses greater than six tons increased during 2017 by approximately 19% globally as compared to 2016. WABCO’s 2017 sales increased by 17.6% (16.0% excluding foreign currency translation effects) as compared with 2016, of which 2.6% is attributable to our acquisitions. Our global aftermarket sales increased by 11.8% (9.4% excluding foreign currency translation effects) over this same period. |

| • | Performance Gross Profit Margin: We maintained strong performance gross profit margin levels at 30% or higher for three consecutive years. Our 2017 performance gross profit margin was 31.1%, compared to 31.7% in 2016. On a GAAP basis, our 2017 gross profit margin was 30.7%, compared to 31.3% in 2016. |

| • | Performance Operating Income: WABCO reported 2017 performance operating income of $492.1 million, versus $411.7 million in 2016, or a 19.5% increase. On a GAAP basis, our 2017 operating income was $435.0 million, versus $381.9 million in 2016. Excludingyear-on-year currency transactional effects, WABCO delivered incremental operating margin in 2017 of 20% (Incremental operating margin represents the ratio of the increase in our performance operating income over WABCO’s growth in sales during 2017. |

| (1) | The summary of our 2017 financial performance includes certainnon-GAAP financial measures. Performance gross profit margin, performance operating income, performance earnings before taxes, performance net income, and performance earnings per share arenon-GAAP financial measures that exclude items for separation, streamlining and acquisition, discrete andone-time tax items, and other items that may mask the underlying operating results of the company, as appropriate. These measures should be considered in addition to, not as a substitute for, GAAP measures. Management believes that presenting thesenon-GAAP measures is useful to shareholders because it enhances their understanding of how management assesses the operating performance of the company’s business. The definitions for thesenon-GAAP measures are the same as in 2016. See Appendix B for reconciliation to the most comparable GAAP measures. |

21

Table of Contents

| • | Performance Earnings Before Taxes(Pre-Tax Income): WABCO reported 2017 Performance Earnings Before Taxes (PerformancePre-Tax Income) of $448.7 million, versus $390.6 million in 2016, or a 14.9% increase. On a GAAP basis, our 2017 Earnings Before Taxes(Pre-Tax Income) was $406.1 million, versus $223.0 million in 2016. |

| • | Performance Net Income and Performance Earnings Per Share (“EPS”):WABCO reported 2017 performance net income attributable to the company of $371.6 million or $6.86 of performance EPS, versus $324.6 million or $5.80 of performance EPS in 2016, resulting in an 18.3% increase in performance EPS. In particular, WABCO’s performance EPS of $6.86 represents a new annual record in delivering value for our shareholders. On a GAAP basis, our 2017 net income attributable to the company and EPS were $406.1 million and $7.50, respectively, versus $223.0 million and $3.98, respectively, in 2016. |

| • | Gross Material Productivity: WABCO’s Operating System continued to provide fast and flexible responses to major market changes, delivering $83.2 million of materials productivity. Gross material productivity in 2017 represented 5.3% of total materials cost with the impact of commodity inflation decreasing net materials productivity to 4.3%. This commodity inflation covers the cost increase of U.S. Dollar denominated commodities, partially offset by the U.S. Dollar weakening versus most of the currencies that we purchase in. Conversion productivity in our factories in 2017 represented 8.1%, a new annual record for WABCO. |

| • | Strategic Acquisitions: WABCO completed several strategic acquisitions and investments, including the acquisition of Meritor Inc.’s stake in our North American joint venture and the acquisition of R. H. Sheppard Co., Inc. |

In summary, 2017 marked another strong year with double-digit sales growth and record performance EPS, demonstrating top line growth with incremental bottom line profitability.

Pay-for-Performance

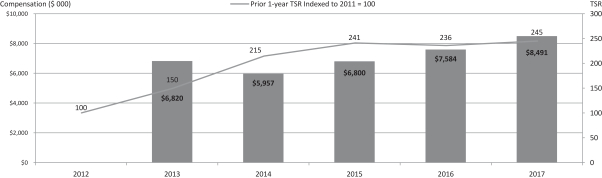

We believe that the levels of executive pay based on our financial results are reasonable over the long term in light of our actual performance for shareholders. The following graph illustrates the trend over the last five completed fiscal years of our CEO executive compensation and our total shareholder return (“TSR”). Note that our equity grants are typically made during the first quarter based on prior-year performance.

22

Table of Contents

CEO Pay Index Year

CEO Pay Index Year(1) | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | ||||||||||||||||||

CEO Pay Measure ($ 000) | ||||||||||||||||||||||||

Reported Pay1-Year (FX each year) | $ | 6,820 | $ | 5,957 | $ | 6,800 | $ | 7,584 | $ | 8,491 | ||||||||||||||

% Change | -12.6 | % | 13.8 | % | 11.9 | % | 11.9 | % | ||||||||||||||||

TSR Index Year(2) | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||||

TSR Index Measure | ||||||||||||||||||||||||

Prior1-Year TSR Indexed to 2011=100 | 100 | 150 | 215 | 241 | 236 | 245 | ||||||||||||||||||

1-Year TSR % | 50.2 | % | 43.3 | % | 12.2 | % | -2.4 | % | 3.8 | % | ||||||||||||||

| (1) | CEO Pay (in $000s) includes (i) base salary and annual incentive awards earned during the applicable year, (ii) the cash-based long-term incentive plan (“Cash LTIP”) award with a performance period ending in the applicable year, (iii) the fair value of restricted stock unit (RSU) and performance share unit (PSU) awards or RSU and option awards (prior to 2013) granted during the applicable year as determined under ASC Topic 718 and (iv) all other compensation reported for the applicable year. |

| (2) | TSR = stock price appreciation plus reinvested dividends. TSR is indexed to December 31, 2011, in the graph and table above since equity awards are typically granted during the first calendar quarter when prior-year TSR results are known. |

Overview of 2017 Compensation Decisions and Actions

The decisions made by our CNG Committee and our Board of Directors in 2017 reflect our company’s continued strong performance for 2017. The following compensation actions were taken in 2017 by the CNG Committee, or by the independent members of the Board of Directors in the case of CEO compensation actions:

| • | Base Salary: In May 2017, we increased the base salaries of each of our NEOs by between 2.7% and 4.2%, excluding an increase of 8.9% for Mr. De Bock, and no salary increase for our Chairman and Chief Executive Officer. These salary adjustments reflect the Committee’s review of market data as well as individual factors as discussed in “Components of 2017 Executive Compensation—Base Salary.” |

| • | Annual Incentives: The CNG Committee approved a 2017 annual incentive plan achievement of 157.0% of target. Our CEO was granted a discretionary individual adjustment of an additional 15% to recognize his leadership and greater responsibility for delivering shareholder value. Since Mr. Mahendra-Rajah left the company prior to end of fiscal 2017, he forfeited his entire 2017 AIP award. These award levels for all our NEOs reflect corporate performance in all of thepre-established financial and quantitative,non-financial goals. See “Components of 2017 Executive Compensation—Fiscal Year 2017Annual Incentive Plan.” |

| • | Long-Term Incentives: |