UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(a)

OF THE SECURITIES EXCHANGE ACT OF 1934

Filed by the Registrant¨ Filed by a Party other than the Registrantþ

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, For Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| þ | Definitive Additional Materials |

| ¨ | Soliciting Materials Pursuant to Section 240.14a-12 |

INTERNATIONAL ELECTRONICS, INC.

(Name of Registrant as Specified in its Charter)

RISCO LTD.

ROKONET INDUSTRIES, U.S.A., INC.

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| þ | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11 |

| 1.) | Title of each class of securities to which the transaction applies: |

| 2.) | Aggregate number of securities to which transaction applies: |

| 3.) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| 4.) | Proposed maximum aggregate value of transaction: |

| 5.) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| 1.) | Amount Previously Paid: |

| 2.) | Form, Schedule or Registration Statement No.: |

| 3.) | Filing Party: |

| 4.) | Date Filed: |

Presentation for Presentation for The following is a slide presentation presented to Institutional Shareholder Services by RISCO Ltd. on May 10, 2007. |

2 Company Overview - Risco Company Overview - Risco Established in 1979 and privately owned Headquartered in Israel with operations in Europe and North America A leading provider of innovative integrated security systems and solutions Growing rapidly, highly profitable and well capitalized Successful acquirer and integrator of complimentary businesses Over 600 employees Seasoned management team |

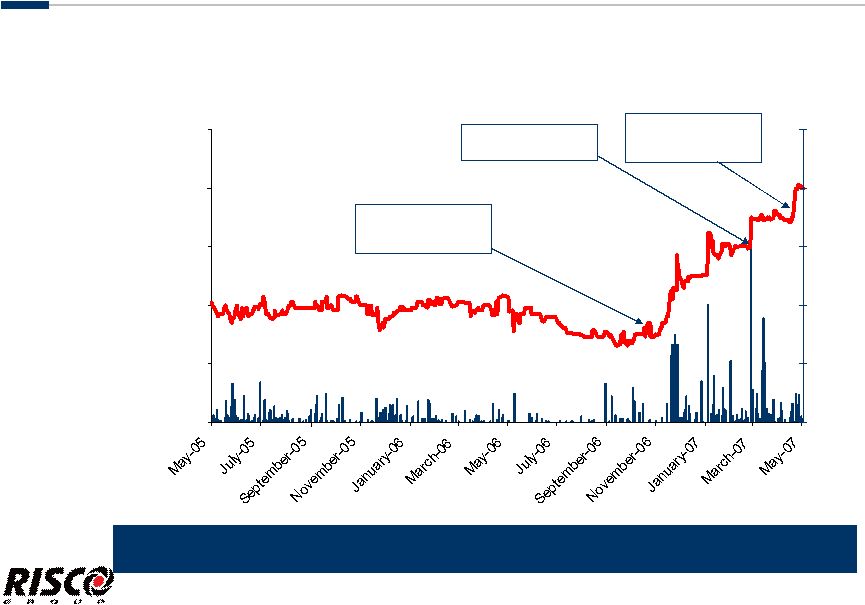

3 IEIB – Stock Price Performance & Volume IEIB – Stock Price Performance & Volume Stock Price & Volume Performance, May 09, 2005 - May 09, 2007 $0.0 $1.0 $2.0 $3.0 $4.0 $5.0 0 50,000 100,000 150,000 200,000 250,000 10/31/06 - Risco issues bear hug letter to IEIB - $1.70 International Electronics Inc Average Price and Volume – May 09, 2005 – Oct 30, 2006 Average Price: $1.84 Average Volume: 3,200 3/6/07 - Risco issues tender offer - $2.98 4/30/07 - Risco increases offer price to $4.00 - $3.53 IEIB’s stock had been stagnant until recent overtures by Risco |

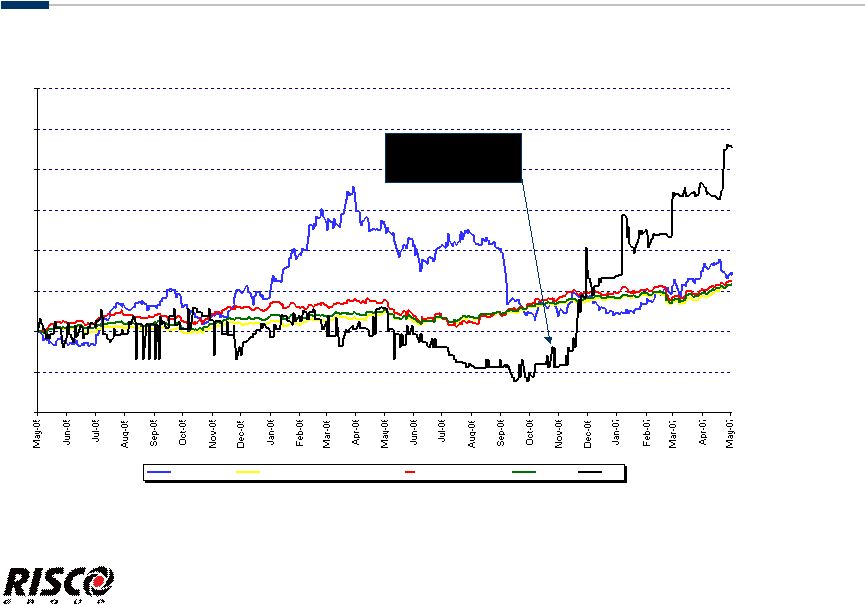

4 Market Indices Performance Market Indices Performance From May 2005 until end of year 2006, IEIB underperformed its peers as well as the broader market indices. Security index includes Magal Security Systems Ltd, Napco Security Systems Inc and Vicon Industries Inc 50 75 100 125 150 175 200 225 250 Security Index Dow Jones Industrial Average NASDAQ Composite S&P 500 IEIB 10/31/06 - Risco issues bear hug letter to IEIB - $1.70 |

5 IEIB Financial Performance IEIB Financial Performance Management of IEIB has failed to create value for shareholders 2004 2005 2006 2007 (1) Revenue 11,393,708 $ 12,646,997 $ 14,120,979 $ 8,492,499 $ Cost of Sales 6,626,589 6,978,820 7,663,956 4,656,630 Gross Profit 4,767,119 5,668,177 6,457,023 3,835,869 Gross Margin 41.8% 44.8% 45.7% 45.2% Research & Development Expenses 1,177,463 1,228,920 1,292,096 671,410 Selling, General & Administrative Expenses 4,257,437 5,162,954 5,617,400 2,870,698 Total Operating Expenses 5,434,900 6,391,874 6,909,496 3,542,108 Operating Profit (Loss) (667,781) (723,697) (452,473) 293,761 Net Income (Loss) (1,125,482) (720,027) (406,821) 254,249 Net Income (Loss) Per Share (0.68) (0.42) (0.23) 0.14 (1) Represents results for the first six months of 2007 IEIB has incurred significant losses in the past three years – Aggregate per share losses for FY 2004-2006 equal $1.33 per share – At an earnings rate of $0.28 per share, IEIB will need 4.75 years to recoup previous losses Management has not put forth a clear strategy that articulates how they can recoup these losses with such limited resources at their disposal |

6 IEIB Management Comments IEIB Management Comments Management’s guidance have been overly optimistic and have not delivered on prior commitments to create shareholder value “We look forward to the efforts that have been made in both product development and expansion of our channels of distribution to pay dividends in fiscal 2006.” – John Waldstein, Chairman & CEO, November 28, 2005 “The Company continues to believe that the markets and the opportunities afforded it by the development of the eMerge™ and the Powerkey™ product lines are significant.” – John Waldstein, Chairman & CEO, January 17, 2006 “Our flagship product line, the eMerge Browser Managed Security Platform, continues to do well as more dealers adopt it as their product of choice in security management.” – John Waldstein, Chairman & CEO, July 13, 2006 |

7 Relative Size – IEIB vs Access Control Market Relative Size – IEIB vs Access Control Market ($ in millions) IEIB remains a niche and marginal player in an industry dominated by large security product providers $14.1 $4,400.0 IEIB U.S. Electronic Access Control Industry |

8 IEIB Issues IEIB Issues Marginal player with very limited product offering – IEIB does not own the IP for its “flagship” product Weak management team that has consistently failed to deliver – John Waldstein is the Chairman, CEO, President, CFO and Treasurer Weak corporate governance structure – Unaccountable management team and Board – BOD does not have a governance or nominating committee – Audit committee composed of only 2 members – Board has 4 members including one insider Limited liquidity and institutional shareholder base – The company has been traded on the over-the-counter market since July of 2005 – Average recent (1) daily trading volume is 3,200 – Two institutional shareholders representing 10.4% of the outstanding shares – Management has given no indication that it is working to get IEI shares re- listed on Nasdaq and create liquidity for stockholders (1) Trading volume from May of 2005 to October of 2006 |

9 IEIB Issues IEIB Issues Limited financial wherewithal to embark on growth and strategic initiatives – As of February 28, 2007, IEIB had $1.1mm in cash – The company does not have adequate financial resources to augment its product offerings and develop a robust sales and distribution channel required to compete in today’s competitive marketplace – The company continues to squander its limited financial resources by resisting to consider a full and fair proposal by Risco IEIB’s claim that Risco’s offer is “substantially less” than other offers is undocumented IEIB has proven to be unwilling to consider the interests of its shareholders and negotiate a consensual transaction IEIB is not well positioned to create near or long-term shareholder value |

10 Risco Offer for IEIB Risco Offer for IEIB Risco’s offer for IEIB does not include conditionalities that are often found in similar proposals including: – Financing contingencies – Completion of due diligence – Approval by Buyer’s stockholders – Tender by sufficient stockholders for “back end” merger – Registration of Buyer securities in non-cash deal Risco’s only “unique” conditions are: – 50.1% tender – Approval of voting rights – Satisfaction of business combination statute Risco’s offer for IEIB minimizes uncertainties |

11 Risco Offer for IEIB Risco Offer for IEIB A significant premium All cash High degree of certainty No financing or other contingencies Risco believes that the proposal it has put forward for IEIB is adequate and is in the best interest of shareholders |