UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of report (date of earliest event reported): January 18, 2008

SEMGROUP ENERGY PARTNERS, L.P.

(Exact name of Registrant as specified in its charter)

| | | | |

| DELAWARE | | 001-33503 | | 20-8536826 |

(State of incorporation or organization) | | (Commission file number) | | (I.R.S. employer identification number) |

| | |

| |

Two Warren Place 6120 South Yale Avenue, Suite 500 Tulsa, Oklahoma | | 74136 |

| (Address of principal executive offices) | | (Zip code) |

Registrant’s telephone number, including area code: (918) 524-5500

(Former name or former address, if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

| ¨ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ¨ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ¨ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ¨ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Item 7.01. Regulation FD Disclosure.

On January 18, 2008, SemGroup Energy Partners, L.P. (the “Partnership”) issued a press release announcing that it has filed with the Securities and Exchange Commission a registration statement for an underwritten public offering of 6,000,000 of its common units representing limited partner interests (the “Offering”). A copy of the press release is furnished as an exhibit to this Current Report.

The Partnership has previously announced that its subsidiary, SemGroup Energy Partners Operating, L.L.C., entered into a Purchase and Sale Agreement (the “Purchase Agreement”) pursuant to which it will acquire land, receiving infrastructure, machinery, pumps and piping and large liquid asphalt cement and residual fuel oil terminals and storage tanks (the “Acquired Assets”) from SemMaterials, L.P., a subsidiary of SemGroup, L.P. (“SemGroup”). Set forth below is a description of the Acquired Assets and as well as certain risk factors that are presented as if the Partnership has completed the acquisition.

In accordance with General Instruction B.2 of Form 8-K, the information set forth in this Item 7.01 and in the attached exhibit shall be deemed to be “furnished” and not be deemed to be “filed” for purposes of the Securities and Exchange Act of 1934, as amended (the “Exchange Act”).

The Acquired Assets

Overview of the Acquisition

The Acquired Assets include 46 terminals in 23 states with an aggregate shell storage capacity of approximately 6.6 million barrels. The Partnership will acquire the terminalling and storage assets associated with the terminals other than equipment used exclusively for processing and marketing operations, which SemGroup will retain. SemGroup will also retain certain domestic leased terminals that are used for storage and processing and marketing of finished asphalt products, as well as its operations in Mexico. The acquisition is expected to close concurrently with the closing of the Offering.

After the Partnership’s acquisition of the Acquired Assets, it will provide liquid asphalt cement storage and terminalling services to SemGroup and third parties. The Partnership’s liquid asphalt cement terminalling and storage operations will allow SemGroup and third parties to store liquid asphalt cement so that they may process and market various finished asphalt products during the periods of highest demand.

The Partnership believes the acquisition of the Acquired Assets will provide several key strategic benefits. The acquisition will enhance the Partnership’s ability to generate stable and predictable cash flows and broaden its service capabilities consistent with its business strategies. In addition, the acquisition will increase the scale of the Partnership’s operations as well as expand and diversify the geographic markets and the lines of business in which it operates.

The Acquired Assets will be engaged in providing terminalling and storage services to the asphalt and residual fuel oil industries. Both liquid asphalt cement and residual fuel oil are products produced from the distillation of crude oil by refiners. The Acquired Assets will generally serve as intermediate storage for the various products as they are transported from the supply sources to their end customers.

The Asphalt Industry

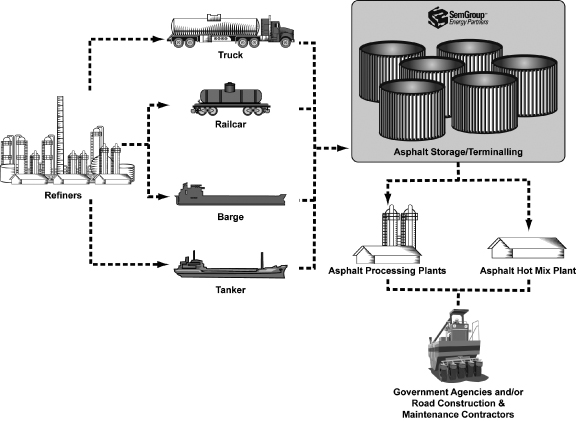

Liquid asphalt cement is one of the oldest engineering materials. Liquid asphalt cement’s adhesive and waterproofing properties have been used for building structures, waterproofing ships, mummification and numerous other applications. More than 100 million tons of asphalt are consumed annually worldwide. In the United States, approximately 90% of liquid asphalt cement consumed is used for road paving and approximately 10% is used for roofing products, with other specialty applications accounting for only a very small fraction of consumption. As reported by the Asphalt Institute, total sales of liquid asphalt paving products in the United States averages nearly 30 million tons per year. It is estimated that approximately 80% of all paving grade liquid asphalt cement is sold to the public sector. The following graphic depicts the asphalt industry from production through its end use, and highlights the areas in which the Partnership will operate following the acquisition of the Acquired Assets.

2

Production of liquid asphalt cement begins with the production of crude oil. Liquid asphalt cement is a dark brown to black cementitious material that is primarily produced by petroleum distillation. When crude oil is separated in distillation towers at a refinery, the heaviest hydrocarbons with the highest boiling points settle at the bottom. These tar-like fractions, called residuum, require relatively little additional processing to become products such as asphalt base or residual fuel oil. Liquid asphalt cement production represents only a small portion of the total crude oil refining process and generally does not have a significant impact on the gross margins realized by refineries. The higher gross margin refined products such as gasoline, kerosene and other light to medium distillates are the main drivers of a refinery’s profitability, with liquid asphalt cement often treated as a by-product. As such, the main concern of most refineries is simply “clearing” the liquid asphalt cement barrels. The liquid asphalt cement produced by petroleum distillation can be sold by the refinery either directly into the wholesale and retail liquid asphalt cement markets or to a liquid asphalt cement marketer.

In its normal state, asphalt cement is too viscous a liquid to be used at ambient temperatures. For paving applications, asphalt cement can be heated (as for hot mix asphalt), diluted or cut back with petroleum solvents (cutback asphalts), or emulsified in a water base with emulsifying chemicals by a colloid mill (asphalt emulsions). Approximately 90% of the road paving liquid asphalt cement in the United States is used for hot mix asphalt. Hot mix asphalt is manufactured by mixing hot asphalt cement and heated aggregate (stone, sand and/or gravel). The hot mix asphalt is loaded into trucks for transport to the paving site, where it is placed on the road surface by paving machines and compacted by rollers. Hot mix asphalt is used for new construction, reconstruction and for thin maintenance overlays on existing roads.

Asphalt emulsions and cutback asphalts are used for a variety of applications including spraying as a tack coat between an old pavement and a new hot mix asphalt overlay, cold mix pothole patching material, and preventive maintenance surface applications such as chip seals. Asphalt emulsions are also used for fog seal,

3

slurry seal, scrub seal, sand seal and microsurfacing maintenance treatments, for warm mix emulsion/aggregate mixtures, base stabilization and both central plant and in-place recycling. Asphalt emulsions and cutback asphalts are generally sold directly to government agencies but are also sold to contractors for use in applications such as chip seals.

Funding for road construction comes from a variety of federal, state and local government sources and from the private sector. Federal funds typically require the states to match some portion of the federal contribution as an incentive to spend more on road construction and maintenance. Motor fuel tax and other user fees account for approximately one-half of transportation revenues. In addition, as lawmakers look to improve road conditions, state and local transportation taxes have been instituted or increased as a source of funds for transportation projects. Historically, nearly 50% of disbursements by government agencies have been for new capital projects with approximately 25% spent on maintenance and services. However, agencies are increasingly allocating more funds to pavement preservation, thus generating more demand for maintenance products such as asphalt emulsions. Asphalt emulsions are most frequently utilized for preservation projects while asphalt cement is more commonly used for new construction and rehabilitation projects.

The asphalt industry in the United States is characterized by a high degree of seasonality. Much of this seasonality is due to the impact that weather conditions have on road construction schedules, particularly in cold weather states. Refineries produce liquid asphalt cement year round, but the peak asphalt demand season is during the warm weather months when most of the road construction activity in the United States takes place. As a result, liquid asphalt cement prices can vary dramatically from the winter to summer months. Liquid asphalt cement marketers and finished asphalt product producers with access to extensive storage capacity possess the inherent advantage of being able to purchase supply from refineries at low prices in the low demand winter months and then sell finished asphalt products at higher prices in the peak summer demand season.

People rely almost exclusively on motor vehicles for mobility in the United States with travel in private vehicles accounting for over 90% of all person miles of travel. The United States has nearly four million miles of roads, 64% of which are paved. Asphalt is used in construction of approximately 94% of the 2.5 million miles of paved roads in the United States. Since 1973, highway travel has increased dramatically while road capacity has only increased by slightly over 5%. In addition, approximately 84% of all goods shipped in the United States are transported on its highways. Various studies indicate that over 60% of the United States’ major roads are in fair to poor condition with nearly 40% of the United States’ major urban roads severely congested.

The liquid asphalt cement market is largely a commodity market with price functioning as the primary decision-making criterion. The markets for polymer modified asphalt cement and asphalt emulsions are more specialized with an emphasis on product specification and functionality. Liquid asphalt cement is a relatively small component of road construction cost (5% by weight of hot mix asphalt material). Due to its relatively small share of total construction cost, demand for asphalt products is generally not highly correlated to the price of crude oil or the price of liquid asphalt cement. Recent advances such as polymer modification and performance-based grading specifications have significantly improved the quality of liquid asphalt cement (e.g., durable elasticity, resistance to rutting and resistance to thermal cracking).

The Residual Fuel Oil Industry

Like asphalt cement, residual fuel oil is another by-product of the crude oil distillation process. Residual fuel oil is primarily used as a burner fuel in numerous industrial and commercial business applications including the utility industry, the shipping and paper industry, steel mills, tire manufacturing, schools and food processors. Approximately 45% of the residual fuel oil demand in the United States is in the utility industry, with 35% to the ship bunker fuel market with industrial and commercial markets consuming the remainder.

The residual fuel oil industry in the United States is characterized by a high degree of seasonality with much of the seasonality driven by the impact of weather on the need to produce power for heating and cooling

4

applications. The residual fuel oil market is largely a commodity market with price functioning as the primary decision-making criterion. However, many customers have unique product specifications driven by their particular business applications that require the blending of various components to meet those specifications.

Residual fuel oil is purchased from a variety of refiners by SemGroup and transported to the Partnership’s terminalling and storage facilities via numerous transportation methods including rail tank car, barge, ship and truck. SemGroup will use the Acquired Assets to service its residual fuel oil business.

The Partnership’s Liquid Asphalt Cement Terminalling and Storage Services

With approximately 6.6 million barrels of liquid asphalt cement storage capacity, the Partnership will be able to provide SemGroup and other customers the ability to effectively manage their liquid asphalt cement inventories and significant flexibility in their processing and marketing activities. The Partnership’s 46 terminals are located in 23 states and as such are well positioned to provide liquid asphalt cement terminalling and storage services in the market areas they serve throughout the continental United States.

SemGroup or other customers will purchase liquid asphalt cement from various suppliers including domestic and foreign refiners such as CHS, Inc., ConocoPhillips Company, Exxon Mobil Corporation, Valero Energy Corporation, Flint Hills Resources, L.P., Marathon Petroleum Company, Navajo Refining Company, Suncor Energy Inc., Irving Oil Corporation and Husky Energy Inc. Liquid asphalt cement purchased by SemGroup or other customers from these and other suppliers is transported via numerous transportation methods including rail tank car, barge, ship and truck to the Partnership’s facilities. The Acquired Assets include the logistics assets, such as docks and rail spurs and the piping and pumping equipment necessary, to facilitate the unloading of liquid asphalt cement into the Partnership’s terminalling and storage facilities. After initial unloading, the liquid asphalt cement is moved via heat traced pipelines into large storage tanks. These tanks are insulated and contain heating elements that allow the asphalt cement to be stored in a heated state. The liquid asphalt cement can then be directly sold by the Partnership’s customers to end users or used by its customers as a raw material for the processing of asphalt emulsions, asphalt cutbacks, polymer modified asphalt cement and related finished asphalt products. The Partnership will terminal and store the liquid asphalt cement until it delivers these products to SemGroup or other third parties for their further processing and/or sale to end users including private companies and governmental agencies.

The Partnership will not take title to, or marketing responsibility for, the liquid asphalt cement that it will terminal and store. As a result, the Partnership’s liquid asphalt cement terminalling and storage operations will have minimal direct exposure to changes in commodity prices, but the volumes of liquid asphalt cement it will terminal or store will be indirectly affected by commodity prices. In the Partnership’s liquid asphalt cement business, it will generate revenues by charging a fee for services provided as liquid asphalt cement is terminalled and stored in its facilities. SemGroup will be the Partnership’s primary customer and, pursuant to the Terminalling Agreement, SemGroup will pay the Partnership a fee based on the number of barrels the Partnership terminals or stores and will commit to utilize the Partnership’s services at certain minimum levels.

5

The following table outlines the location of each terminalling and storage facility included in the Acquired Assets and their respective storage capacity as of December 31, 2007:

| | | | |

Location | | Number of

Tanks | | Shell Capacity (Barrels) |

St. Louis, MO | | 13 | | 499,550 |

Newport News, VA | | 15 | | 497,000 |

Saginaw, TX | | 26 | | 494,668 |

Gloucester City, NJ | | 8 | | 455,524 |

Halstead, KS | | 11 | | 341,394 |

Memphis, TN | | 17 | | 327,929 |

Catoosa, OK* | | 8 | | 291,116 |

Spokane, WA* | | 19 | | 273,644 |

Las Vegas, NV | | 13 | | 272,005 |

Port of Catoosa, OK* | | 9 | | 269,500 |

Boise, ID | | 16 | | 261,398 |

Muskogee, OK | | 15 | | 229,520 |

Lubbock, TX | | 15 | | 228,340 |

Bay City, MI | | 6 | | 181,571 |

Denver, CO* | | 6 | | 173,905 |

Salt Lake City, UT | | 17 | | 165,538 |

New Madrid, MO | | 10 | | 150,468 |

Warsaw, IN | | 10 | | 134,032 |

Morehead City, NC | | 9 | | 128,552 |

Chicago, IL | | 4 | | 127,195 |

Parsons, TN | | 7 | | 114,214 |

Grand Island, NE | | 6 | | 111,600 |

Pasco, WA | | 8 | | 103,223 |

Pekin, IL | | 2 | | 102,090 |

Billings, MT | | 8 | | 100,000 |

Woods Cross, UT | | 12 | | 98,592 |

Dodge City, KS | | 9 | | 84,699 |

Pueblo, CO | | 11 | | 75,146 |

Grand Junction, CO | | 11 | | 68,161 |

Ennis, TX | | 11 | | 63,895 |

Fontana, CA | | 10 | | 52,913 |

Spokane, WA* | | 4 | | 43,277 |

Columbus, OH | | 4 | | 26,524 |

Northumberland, PA | | 8 | | 23,333 |

Reading, PA | | 7 | | 11,810 |

Catoosa, OK* | | 4 | | 9,063 |

Austin, TX | | 4 | | 8,568 |

Garden City, GA | | 5 | | 8,214 |

Denver, CO* | | 5 | | 8,167 |

Little Rock, AR | | 4 | | 6,722 |

Sedalia, MO | | 3 | | 6,271 |

El Dorado, KS | | 4 | | 5,619 |

Salina, KS | | 5 | | 5,590 |

Lawton, OK | | 5 | | 4,935 |

Memphis, TN | | 4 | | 3,095 |

Ardmore, OK | | 3 | | 2,090 |

| | | | |

Total | | 411 | | 6,650,662 |

| * | Denotes locations that have more than one facility. |

6

The Acquired Assets range in age from one year to over thirty years and the Partnership expects that the storage tanks will have an average remaining life of in excess of 20 years when the Partnership acquire them. The Acquired Assets have been well maintained.

The asphalt industry is highly fragmented and regional in nature. Participants range in size from major oil companies to small family-owned proprietorships. SemGroup’s competitors in the asphalt business include: refiners such as BP p.l.c., Flint Hills Resources, L.P., CHS, Inc., Exxon Mobil Corporation, ConocoPhillips Company, NuStar Energy L.P., Ergon, Inc., Marathon Petroleum Company LLC, Alon USA LP, Suncor Energy Inc. and Valero Energy Corporation; resellers such as NuStar Energy L.P., Idaho Asphalt Supply, Inc. and Asphalt Materials, Inc.; and large road construction firms such as OldCastle Materials, Inc., APAC, Inc. and Colas SA. The Partnership will compete with national, regional and local liquid asphalt cement terminalling and storage companies including the major integrated oil companies and a variety of others including KinderMorgan Energy Partners, International-Matex Tank Terminals and Houston Fuel Oil Terminal Company.

SemGroup acquired the majority of the Acquired Assets from Koch Materials Company in April 2005. Since that time, the Acquired Assets have been operated by SemMaterials, L.P., a wholly owned subsidiary of SemGroup.

Terminalling Agreement

In connection with the acquisition of the Acquired Assets, the Partnership will enter into a Terminalling and Storage Agreement (the “Terminalling Agreement”) with SemGroup. A substantial portion of the Partnership’s revenues will be derived from services provided to the finished asphalt product processing and marketing operations of SemGroup pursuant to this agreement. Under this agreement, the Partnership will provide the following services to SemGroup:

| | • | | Terminalling and Storage Services. The Partnership will provide services relating to the terminalling and storage of liquid asphalt cement for SemGroup in its liquid asphalt cement storage facilities. The Partnership will also provide services to deliver liquid asphalt cement to the finished asphalt product processing and marketing assets owned by SemGroup. The Partnership’s storage services will enable SemGroup to purchase and store liquid asphalt cement and sell it at later dates. |

| | • | | Minimum Throughput and Storage Requirements. The terminalling and storage services will be subject to minimum throughput requirements each month, regardless of the amount of such services actually used by SemGroup in a given month. If SemGroup uses these services in excess of the minimum throughput requirements, SemGroup will pay the Partnership a premium for such services. In addition, SemGroup will commit to use five million barrels of the Partnership’s total storage capacity per month. SemGroup will be obligated, regardless of the amount of storage services actually used by it in a given month, to pay the Partnership a fee per barrel for five million barrels of the Partnership’s storage capacity. If SemGroup utilizes any of these storage services in excess of these minimum storage requirements, SemGroup will pay the Partnership a fee for such services equal to at least 110% of the per barrel base charge for the applicable services. However, the Partnership will be permitted to contract with other customers for services in excess of these minimum commitments and the Partnership will not be obligated to provide any services in excess of the minimum requirements to SemGroup. |

Based on these minimum throughput and storage requirements, SemGroup is obligated to pay the Partnership minimum monthly fees totaling $58.9 million annually for its liquid asphalt cement terminalling and storage services.

The Partnership will not take title to, or marketing responsibility for, the liquid asphalt cement that it terminals and stores. The Terminalling Agreement contains a Consumer Price Index adjustment that may offset a portion of any increased costs that the Partnership incurs. If new laws or regulations that affect these services generally are enacted that require the Partnership to make substantial and unanticipated capital expenditures, the Partnership will have the right to negotiate an upfront payment or monthly surcharge to be paid by SemGroup for the use of the Partnership’s services to cover SemGroup’s

7

pro rata portion of the cost of complying with these laws or regulations, after the Partnership has made efforts to mitigate their effect. The Partnership and SemGroup are obligated to negotiate in good faith to agree on the level of the monthly surcharge. The surcharge will not apply in respect of routine capital expenditures.

SemGroup’s obligations may be temporarily suspended during the occurrence of a force majeure event that renders performance of services impossible with respect to an asset for at least 30 consecutive days. If a force majeure event results in a diminution in the services the Partnership is able to provide to SemGroup pursuant to the Terminalling Agreement, SemGroup’s minimum service usage commitment would be reduced proportionately for the duration of the force majeure event. If such a force majeure event continues for twelve consecutive months or more, the Partnership and SemGroup will each have the right to terminate their rights and obligations with respect to the affected services under the Terminalling Agreement.

The Terminalling Agreement has an initial term that expires on December 31, 2014 with additional automatic one-year renewals unless either party terminates the agreement upon one year’s prior notice. The Terminalling Agreement may be assigned by SemGroup only with the Partnership’s consent.

The Terminalling Agreement will not apply to any services the Partnership may provide to customers other than SemGroup.

Access and Use Agreement

In connection with the acquisition of the Acquired Assets, the Partnership will enter into a Terminal Access and Use Agreement (the “Access and Use Agreement”) with SemGroup and its affiliates. The Acquired Assets include facilities and real property where the finished asphalt product processing and marketing operations retained by SemGroup will continue to be located. Pursuant to the Access and Use Agreement, SemGroup will reserve the right to access facilities used for both terminalling and storage of liquid asphalt cement and processing of finished asphalt products. In addition, pursuant to the Access and Use Agreement the Partnership will be indemnified for any losses that occur from SemGroup’s operations at or relating to the Acquired Assets.

Amended Omnibus Agreement

Concurrently with the closing of the acquisition of the Acquired Assets, the Partnership will amend and restate the Omnibus Agreement that it entered into with SemGroup, the Partnership’s general partner and others (the “Amended Omnibus Agreement”). Any or all of the provisions of the Amended Omnibus Agreement, other than the indemnification provisions described below, are terminable by SemGroup at its option if the Partnership’s general partner is removed without cause and units held by the Partnership’s general partner and its affiliates are not voted in favor of that removal. The Amended Omnibus Agreement will also terminate in the event of a change of control of the Partnership or the Partnership’s general partner.

Reimbursement of General and Administrative Expenses

Under the Amended Omnibus Agreement, the Partnership will reimburse SemGroup for the payment of certain operating expenses and for the provision of various general and administrative services for the Partnership’s benefit with respect to the Partnership’s crude oil business and the Acquired Assets. SemGroup performs centralized corporate functions for the Partnership, such as legal, accounting, treasury, insurance administration and claims processing, risk management, health, safety and environmental, information technology, human resources, credit, payroll, internal audit, taxes, engineering and marketing. The Partnership pays its general partner and SemGroup a fixed administrative fee for providing general and administrative services to the Partnership, which was initially fixed at $5.0 million per year but will be increased under the Amended Omnibus Agreement to $7.0 million per year for the three years following the completion of the Offering, subject to annual increases based on increases in the Consumer Price Index and subject to further

8

increases in connection with expansions of the Partnership’s operations through the acquisition or construction of new assets or businesses with the concurrence of the Partnership’s conflicts committee. After the three-year anniversary of the completion of the Offering, the Partnership’s general partner will determine the general and administrative expenses to be allocated to the Partnership in accordance with the Partnership’s partnership agreement.

The Partnership is also obligated to reimburse SemGroup for operating expenses, which are not included in the $7.0 million annual fixed administrative fee, to the extent incurred by SemGroup on the Partnership’s behalf. Such operating expenses primarily include compensation of operational personnel performing services for the Partnership’s benefit and the cost of their employee benefits and insurance coverage expenses SemGroup incurs with respect to the Partnership’s business and operations.

Non-Competition

Under the Amended Omnibus Agreement, SemGroup and its affiliates will agree, so long as the Terminalling Agreement is in effect, not to engage in, or acquire or invest in an entity that engages in, the business of terminalling and storing liquid asphalt cement within 50 miles of the Partnership’s liquid asphalt cement facilities. These non-competition provisions will not apply to:

| | • | | SemGroup’s ownership and operation of finished asphalt product processing and marketing assets; |

| | • | | SemGroup’s provision of finished asphalt product processing, marketing and distributing services; |

| | • | | SemGroup’s purchase and ownership of not more than 9.9% of any class of securities of an entity that provides liquid asphalt cement terminalling and storage services; |

| | • | | SemGroup’s acquisition or construction of liquid asphalt cement terminalling and storage assets that have a fair market value of less than $5 million; |

| | • | | SemGroup’s conduct of any restricted business with the approval of the conflicts committee of the Partnership’s general partner; |

| | • | | SemGroup’s provision of refining and marketing of other products that do not produce qualifying income; and |

| | • | | SemGroup’s operation of certain leased liquid asphalt cement terminalling and storage assets. |

In addition, the Partnership will agree, so long as the Terminalling Agreement is in effect, not to engage in, or acquire or invest in an entity that engages in, the business of processing, marketing and distributing liquid asphalt cement and finished asphalt products within 50 miles of the Partnership’s liquid asphalt cement facilities. These non-competition provisions will not apply to:

| | • | | the Partnership’s ownership and operation of the Acquired Assets; |

| | • | | the Partnership’s provision of liquid asphalt cement terminalling and storage services; |

| | • | | the Partnership’s purchase and ownership of not more than 9.9% of any class of securities of an entity that provides liquid asphalt cement processing, marketing and distributing services; |

| | • | | the Partnership’s acquisition or construction of liquid asphalt cement processing assets that have a fair market value of less than $5 million; and |

| | • | | the Partnership’s conduct of any restricted business with the approval of SemGroup. |

Right of First Refusal

Under the Amended Omnibus Agreement SemGroup will have, so long as the Terminalling Agreement is in effect, a right of first refusal to purchase the liquid asphalt cement terminalling and storage assets owned by the Partnership if

9

the Partnership proposes to transfer such assets to a third party. In addition, the Partnership will have, so long as the Terminalling Agreement is in effect, a right of first refusal to purchase the finished asphalt product processing assets owned by SemGroup if SemGroup proposes to transfer such assets to a third party. Before the Partnership enters into any contract to sell the Partnership’s liquid asphalt cement terminalling and storage assets or SemGroup enters into any contract to sell its finished asphalt product processing assets, the selling party must give the other party written notice of the terms of such proposed sale. The notice must set forth the name of the third party purchaser, the assets to be sold, the purchase price, reasonable details of the payment terms, an estimate of the fair value of any non-cash consideration and all other material terms and conditions of the offer. To the extent the third party offer consists of consideration other than cash (or in addition to cash), the purchase price shall be deemed equal to the amount of any such cash plus the fair market value of such non-cash consideration. The Partnership or SemGroup, as applicable, will have the option for a period of 45 days following receipt of the notice, to purchase the subject assets on the terms set forth in the notice.

Indemnification

Under the Amended Omnibus Agreement, SemGroup indemnifies the Partnership for five years after the closing of the Partnership’s initial public offering against certain potential environmental claims, losses and expenses associated with the operation of the Partnership’s crude oil business occurring before the contribution of the crude oil business to the Partnership. SemGroup’s maximum liability for this indemnification obligation will not exceed $7.5 million and SemGroup will not have any obligation under this indemnification until the Partnership’s aggregate losses exceed $250,000. The Partnership has agreed to indemnify SemGroup against environmental liabilities relating to the crude oil business arising or occurring after the contribution of the crude oil business to the Partnership.

Additionally, SemGroup will indemnify the Partnership for losses attributable to rights-of-way, certain consents or governmental permits and income taxes attributable to operations of the crude oil business before its contribution to the Partnership. The Partnership will indemnify SemGroup for all losses attributable to the post-contribution operations of the crude oil business. SemGroup’s obligations under this additional indemnification will survive for five years after the closing of the Partnership’s initial public offering, except that the indemnification obligation with respect to income tax liabilities will terminate upon the expiration of the applicable statute of limitations.

Risk Factors Related to The Partnership’s Business

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which the Partnership are subject are similar to those that would be faced by a corporation engaged in a similar business. If any of the following risks were actually to occur, the Partnership’s business, financial condition, or results of operations could be materially adversely affected. In that case, the Partnership might not be able to pay distributions on the Partnership’s common units and the trading price of the Partnership’s common units could decline.

The following risks are presented as if the Partnership has completed the acquisition of the Acquired Assets.

The Partnership may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to the Partnership’s general partner, to enable it to make cash distributions to holders of the Partnership’s common units and subordinated units at the initial distribution rate under the Partnership’s cash distribution policy.

In order to make the Partnership’s cash distributions at the Partnership’s initial distribution rate of $0.3125 per common unit and subordinated unit per complete quarter, or $1.25 per unit per year, the Partnership will require available cash of approximately $10.5 million per quarter, or $42.0 million per year, based on the common units and subordinated units outstanding immediately after completion of the Offering ($10.8 million or $43.2 million, respectively, if the underwriters exercise their over-allotment option in full). The Partnership may not have sufficient available cash from operating surplus each quarter to enable it to make cash distributions at the initial distribution rate under the Partnership’s cash distribution policy. The amount of cash the Partnership can distribute on the Partnership’s units principally depends upon the amount of cash the Partnership generates from its operations, which will fluctuate from quarter to quarter based on, among other things, the risks described in this section.

In addition, the actual amount of cash the Partnership will have available for distribution will depend on other factors, including:

| | • | | the level of capital expenditures the Partnership makes; |

| | • | | the cost of acquisitions; |

| | • | | the Partnership’s debt service requirements and other liabilities; |

| | • | | fluctuations in the Partnership’s working capital needs; |

| | • | | the Partnership’s ability to borrow funds and access capital markets; |

| | • | | restrictions contained in the Partnership’s credit facility or other debt agreements; and |

| | • | | the amount of cash reserves established by the Partnership’s general partner. |

The Partnership depends upon SemGroup for substantially all of the Partnership’s revenues and any reduction in these revenues would have a material adverse effect on the Partnership’s results of operations and the Partnership’s ability to make distributions to its unitholders.

Because the Partnership utilizes substantially all of the operating capacity of its crude oil and liquid asphalt cement assets to provide services to SemGroup pursuant to the Throughput Agreement and the Terminalling Agreement,

10

the Partnership does not expect to materially increase its revenues from third-party customers in the near term unless the Partnership undertakes significant acquisition or construction projects. Therefore, the Partnership expects its dependence on SemGroup for substantially all of its revenues to continue. If SemGroup is unable to make to the Partnership the payments required by it under the Throughput Agreement or the Terminalling Agreement for any reason, the Partnership’s revenues would decline and the Partnership’s ability to make distributions to the Partnership’s unitholders would be reduced. Therefore, the Partnership is indirectly subject to the business risks of SemGroup, many of which are similar to the business risks the Partnership faces. In particular, these business risks include the following:

| | • | | the inability of SemGroup to generate adequate gross margins from the purchase, transportation, storage and marketing of petroleum products; |

| | • | | material reductions in the supply of crude oil, liquid asphalt cement and petroleum products; |

| | • | | a material decrease in the demand for crude oil, finished asphalt and petroleum products in the markets served by SemGroup; |

| | • | | the inability of SemGroup to manage its commodity price risk resulting from its ownership of crude oil, liquid asphalt cement and petroleum products; |

| | • | | contract non-performance by SemGroup’s customers; and |

| | • | | various operational risks to which SemGroup’s business is subject. |

The Partnership is exposed to the credit risk of SemGroup and any material nonperformance by SemGroup could reduce the Partnership’s ability to make distributions to its unitholders.

The Partnership is party to the Terminalling Agreement with SemGroup pursuant to which the Partnership provides certain liquid asphalt cement terminalling and storage services to SemGroup. The Partnership is also party to the Throughput Agreement with SemGroup pursuant to which the Partnership provide certain crude oil gathering, transportation, terminalling and storage services to SemGroup. In addition, the Partnership has entered into the Amended Omnibus Agreement and other agreements with SemGroup that addresses, among other things, the provision of general and administrative and operating services to the Partnership and indemnification matters. As of January 14, 2008, Moody’s assigned SemGroup a corporate family rating of Ba3 and Fitch Ratings assigned SemGroup’s senior unsecured indebtedness rating of B+, both of which are speculative ratings. These speculative ratings signify a higher risk that SemGroup will default on its obligations, including its obligations to the Partnership, than does an investment grade credit rating. Any material nonperformance under the Amended Omnibus Agreement, the Throughput Agreement or the Terminalling Agreement by SemGroup could materially and adversely impact the Partnership’s ability to operate and make distributions to the Partnership’s unitholders.

Though the Partnership will have no indebtedness rated by any credit rating agency at the closing of the Offering, the Partnership may have rated debt in the future. Credit rating agencies such as Moody’s and Fitch Ratings may consider SemGroup’s debt ratings when assigning the Partnership’s, because of SemGroup’s ownership interest in and control of the Partnership, the strong operational links between SemGroup and the Partnership, and the Partnership’s reliance on SemGroup for substantially all of the Partnership’s revenues. If one or more credit rating agencies were to downgrade the outstanding indebtedness of SemGroup, the Partnership could experience an increase in the Partnership’s borrowing costs or difficulty accessing capital markets. Such a development could adversely affect the Partnership’s ability to grow the Partnership’s business and to make distributions to its unitholders.

SemGroup’s obligations under the Throughput Agreement and the Terminalling Agreement may be reduced or suspended in some circumstances, which would reduce the Partnership’s ability to make distributions to its unitholders.

Some of the circumstances under which SemGroup’s obligations under the Throughput Agreement and the Terminalling Agreement may be permanently reduced are within the exclusive control of SemGroup. Any such permanent reduction would reduce the Partnership’s ability to make distributions to its unitholders. For example, under the Throughput Agreement, if the Partnership and SemGroup cannot agree on an upfront payment or ratable fee surcharge to cover substantial and unanticipated capital expenditures at any of the Partnership’s facilities in order to comply with new laws

11

or regulations, and if the Partnership is not able to direct the affected crude oil to mutually acceptable storage or gathering and transportation assets that the Partnership owns, either party will have the right to remove the affected facility from the Throughput Agreement, and SemGroup’s minimum monthly payment obligation will be correspondingly reduced. SemGroup’s minimum monthly payment obligation may also be temporarily suspended under the Throughput Agreement or the Terminalling Agreement to the extent that the occurrence of a force majeure event that is outside the control of the parties prevents the Partnership from making the Partnership’s services available to SemGroup and the affected services under the Throughput Agreement or the Terminalling Agreement, as applicable, may be terminated if the force majeure event prevents performance for more than twelve months.

The amount of cash the Partnership has available for distribution to holders of the Partnership’s common units and subordinated units depends primarily on the Partnership’s cash flow and not solely on earnings reflected in the Partnership’s financial statements. Consequently, even if the Partnership is profitable, the Partnership may not be able to make cash distributions to holders of the Partnership’s common units and subordinated units.

Unitholders should be aware that the amount of cash the Partnership has available for distribution depends primarily upon the Partnership’s cash flow and not solely on earnings reflected in the Partnership’s financial statements, which will be affected by non-cash items. As a result, the Partnership may make cash distributions during periods when the Partnership records losses for financial accounting purposes and may not make cash distributions during periods when the Partnership records net earnings for financial accounting purposes.

A significant decrease in demand for crude oil and/or finished asphalt products in the areas served by the Partnership’s storage facilities and pipelines would reduce the Partnership’s ability to make distributions to its unitholders.

A sustained decrease in demand for crude oil and/or finished asphalt products in the areas served by the Partnership’s storage facilities and pipelines could significantly reduce the Partnership’s revenues and, therefore, reduce the Partnership’s ability to make or increase distributions to its unitholders. Factors that could lead to a decrease in market demand for crude oil and finished asphalt products include:

| | • | | lower demand by consumers for refined products, including finished asphalt products, as a result of recession or other adverse economic conditions or due to high prices caused by an increase in the market price of crude oil or higher fuel taxes or other governmental or regulatory actions that increase, directly or indirectly, the cost of gasolines or other refined products; |

| | • | | a shift by consumers to more fuel-efficient or alternative fuel vehicles or an increase in fuel economy of vehicles, whether as a result of technological advances by manufacturers, governmental or regulatory actions or otherwise; and |

| | • | | fluctuations in demand for crude oil, such as those caused by refinery downtime or shutdowns, could also significantly reduce the Partnership’s revenues and, therefore, reduce the Partnership’s ability to make distributions to its unitholders. |

Certain of the Partnership’s field and pipeline operating costs and expenses are fixed and do not vary with the volumes the Partnership gathers and transports. These costs and expenses may not decrease ratably or at all should the Partnership experience a reduction in the volumes gathered or transmitted by the Partnership’s gathering and transportation operations. As a result, the Partnership may experience declines in its margin and profitability if its volumes decrease.

A material decrease in the production of crude oil from the oil fields served by the Partnership’s pipelines could materially reduce the Partnership’s ability to make distributions to its unitholders.

The throughput on the Partnership’s crude oil pipelines depends on the availability of attractively priced crude oil produced from the oil fields served by such pipelines, or through connections with pipelines owned by third parties. Crude oil production may decline for a number of reasons, including natural declines due to depleting wells, a material decrease in the price of crude oil, or the inability of producers to obtain necessary drilling or

12

other permits from applicable governmental authorities. If the Partnership is unable to replace volumes lost due to a temporary or permanent material decrease in production from the oil fields served by the Partnership’s crude oil pipelines, the Partnership’s throughput could decline, reducing its revenue and cash flow and adversely affecting the Partnership’s ability to make distributions to its unitholders. In addition, it is difficult to attract producers to a new gathering system if the producer is already connected to an existing system. As a result, SemGroup or third-party shippers on the Partnership’s pipeline systems may experience difficulty acquiring crude oil at the wellhead in areas where there are existing relationships between producers and other gatherers and purchasers of crude oil.

A material decrease in the production of liquid asphalt cement could materially reduce the Partnership’s ability to make distributions to its unitholders.

The throughput at the Acquired Assets depends on the availability of attractively priced liquid asphalt cement produced from the various liquid asphalt cement producing refineries. Liquid asphalt cement production may decline for a number of reasons, including refiners processing more light, sweet crude oil or refiners installing coker units that further refine heavy residual fuel oil bottoms such as liquid asphalt cement. If the Partnership is unable to replace volumes lost due to a temporary or permanent material decrease in production from the suppliers of liquid asphalt cement, the Partnership’s throughput could decline, reducing its revenue and cash flow and adversely affecting the Partnership’s ability to make distributions to its unitholders.

The Partnership faces intense competition in its gathering, transportation, terminalling and storage activities. Competition from other providers of crude oil gathering, transportation, terminalling and storage services that are able to supply SemGroup and the Partnership’s other customers with those services at a lower price could reduce the Partnership’s ability to make distributions to its unitholders.

The Partnership is subject to competition from other crude oil gathering, transportation, terminalling and storage operations that may be able to supply SemGroup and the Partnership’s other customers with the same or comparable services on a more competitive basis. The Partnership competes with national, regional and local gathering, storage, terminalling and pipeline companies, including the major integrated oil companies, of widely varying sizes, financial resources and experience. Some of these competitors are substantially larger than the Partnership, have greater financial resources, and control substantially greater storage capacity than the Partnership does. With respect to the Partnership’s gathering and transportation services, these competitors include TEPPCO Partners, L.P., Plains All American Pipeline, L.P., ConocoPhillips, Sunoco Logistics Partners L.P. and National Cooperative Refinery Association, among others. With respect to the Partnership’s storage and terminalling services, these competitors include BP plc, Enbridge Energy Partners, L.P. and Plains All American Pipeline, L.P. Some of these competitors have greater capital resources and control greater supplies of crude oil than SemGroup. Several of the Partnership’s competitors conduct portions of their operations through publicly traded partnerships with structures similar to the Partnership’s, including Plains All American Pipeline, L.P., TEPPCO Partners, L.P., Sunoco Logistics Partners L.P. and Enbridge Energy Partners, L.P.

The Partnership’s ability to compete could be harmed by numerous factors, including:

| | • | | the perception that another company can provide better service; and |

| | • | | the availability of alternative supply points, or supply points located closer to the operations of SemGroup’s customers. |

In addition, SemGroup will continue to own midstream assets upon completion of the Offering and may engage in competition with the Partnership, subject to certain restrictions on SemGroup’s ability to acquire and construct liquid asphalt cement terminalling and storage assets. If the Partnership is unable to compete with services offered by other midstream enterprises, including SemGroup, its ability to make distributions to its unitholders may be adversely affected.

13

Some of the Partnership’s pipeline systems are dependent upon their interconnections with other crude oil pipelines to reach end markets.

Some of the Partnership’s pipeline systems are dependent upon their interconnections with other crude oil pipelines to reach end markets. Reduced throughput on these interconnecting pipelines as a result of testing, line repair, reduced operating pressures or other causes could result in reduced throughput on the Partnership’s pipeline systems that would adversely affect the Partnership’s revenue and cash flow and the Partnership’s ability to make distributions to its unitholders.

The Partnership will use the proceeds of the Offering, together with borrowings under the Partnership’s amended credit facility, to purchase the Acquired Assets. If the Acquired Assets do not perform as expected, the Partnership’s future financial performance may be negatively impacted.

The Partnership’s acquisition of the Acquired Assets will significantly increase the size of the Partnership and diversify the geographic areas and lines of business in which the Partnership operates. The Partnership cannot assure its unitholders that it will achieve the desired profitability from the Acquired Assets. In addition, the Partnership’s failure to successfully integrate the Acquired Assets into the Partnership’s business could adversely affect the Partnership’s financial condition and results of operations.

The Partnership will face certain challenges as the Partnership works to integrate the Acquired Assets into the Partnership’s business. In particular, the acquisition of the Acquired Assets will, by adding 46 terminals in 23 states, expand the Partnership’s operations and the types of business in which the Partnership engages, significantly expanding the Partnership’s geographic scope and increasing the number of employees involved in the Partnership’s operations, thereby presenting the Partnership with significant challenges as the Partnership works to manage the increase in scale resulting from the acquisition. Delays in this process could have a material adverse effect on the Partnership’s revenues, expenses, operating results and financial condition. In addition, events outside of the Partnership’s control, including changes in state and federal regulation and laws as well as economic trends, also could adversely affect the Partnership’s ability to realize the anticipated benefits from the acquisition of the Acquired Assets.

Further, the liquid asphalt cement operations may not perform in accordance with the Partnership’s expectations, the Partnership may lose key employees and the Partnership’s expectations with regards to integration and synergies may not be fully realized. The Partnership’s failure to successfully integrate and operate the Acquired Assets, and to realize the anticipated benefits of the acquisition could adversely affect the Partnership’s operating and financial results.

The Partnership’s debt levels may limit the Partnership’s ability to make distributions and the Partnership’s flexibility in obtaining additional financing and in pursuing other business opportunities.

Upon completion of the Offering, the Partnership expects to have approximately $310 million of debt outstanding under the Partnership’s amended credit facility. The Partnership’s level of debt could have important consequences for the Partnership, including the following:

| | • | | the Partnership’s ability to obtain additional financing, if necessary, for working capital, capital expenditures, acquisitions or other purposes may be impaired or such financing may not be available on favorable terms; |

| | • | | the Partnership will need a substantial portion of its cash flow to make principal and interest payments on its debt, reducing the funds that would otherwise be available for operations, future business opportunities and distributions to unitholders; |

| | • | | the Partnership’s debt level will make the Partnership more vulnerable to competitive pressures or a downturn in the Partnership’s business or the economy generally; and |

| | • | | the Partnership’s debt level may limit the Partnership’s flexibility in responding to changing business and economic conditions. |

The Partnership’s ability to service its debt will depend upon, among other things, the Partnership’s future financial and operating performance, which will be affected by prevailing economic conditions and financial, business, regulatory and other factors. The Partnership’s ability to service debt under its amended credit facility also will depend on market interest rates, since the interest rates applicable to the Partnership’s borrowings will fluctuate with the London Interbank Offered Rate,

14

or LIBOR, or the prime rate. If the Partnership’s operating results are not sufficient to service the Partnership’s current or future indebtedness, the Partnership will be forced to take actions such as reducing distributions, reducing or delaying the Partnership’s business activities, acquisitions, investments or capital expenditures, selling assets, restructuring or refinancing the Partnership’s debt, or seeking additional equity capital. The Partnership may not be able to effect any of these actions on satisfactory terms, or at all.

Restrictions in the Partnership’s amended credit facility may prevent the Partnership from engaging in some beneficial transactions or paying distributions to its unitholders.

The Partnership’s amended credit facility contains covenants limiting the Partnership’s ability to make distributions to its unitholders. In addition, the Partnership’s amended credit facility contains various covenants that limit, among other things, the Partnership’s ability to incur indebtedness, grant liens or enter into a merger, consolidation or sale of assets. Furthermore, the Partnership’s amended credit facility contains covenants requiring the Partnership to maintain certain financial ratios and tests. Any subsequent refinancing of the Partnership’s current debt may have similar or greater restrictions.

If the Partnership borrows funds to make the Partnership’s quarterly distributions, the Partnership’s ability to pursue acquisitions and other business opportunities may be limited and the Partnership’s operations may be materially adversely effected.

Available cash for the purpose of making distributions to unitholders includes working capital borrowings. If the Partnership borrows funds to pay one or more quarterly distributions, such amounts will incur interest and must be repaid in accordance with the terms of the Partnership’s credit facility. In addition, any amounts borrowed for distributions to the Partnership’s unitholders will reduce the funds available to the Partnership for other purposes under the Partnership’s amended credit facility, including amounts available for use in connection with acquisitions and other business opportunities. If the Partnership is unable to pursue its growth strategy due to its limited ability to borrow funds, the Partnership’s operations may be materially adversely effected.

A principal focus of the Partnership’s business strategy is to grow and expand the Partnership’s business through acquisitions. If the Partnership does not make acquisitions on economically acceptable terms, the Partnership’s future growth may be limited.

A principal focus of the Partnership’s business strategy is to grow and expand its business through acquisitions. The Partnership’s ability to grow depends, in part, on the Partnership’s ability to make acquisitions that result in an increase in the cash generated per unit from operations. If the Partnership is unable to make these accretive acquisitions, either because the Partnership is (1) unable to identify attractive acquisition candidates or negotiate acceptable purchase contracts with them, (2) unable to obtain financing for these acquisitions on economically acceptable terms or (3) outbid by competitors, then the Partnership’s future growth and ability to increase distributions will be limited. Furthermore, even if the Partnership does make acquisitions that it believes will be accretive, these acquisitions may nevertheless result in a decrease in the cash generated from operations per unit.

Any acquisition involves potential risks, including, among other things:

| | • | | mistaken assumptions about volumes, revenues and costs, including synergies; |

| | • | | an inability to integrate successfully the businesses the Partnership acquires; |

| | • | | an inability to hire, train or retain qualified personnel to manage and operate the Partnership’s business and assets; |

| | • | | the assumption of unknown liabilities; |

| | • | | limitations on rights to indemnity from the seller; |

| | • | | mistaken assumptions about the overall costs of equity or debt; |

| | • | | the diversion of management’s and employees’ attention from other business concerns; |

| | • | | unforeseen difficulties operating in new product areas or new geographic areas; and |

| | • | | customer or key employee losses at the acquired businesses. |

15

If the Partnership consummates any future acquisitions, the Partnership’s capitalization and results of operations may change significantly, and unitholders will not have the opportunity to evaluate the economic, financial and other relevant information that the Partnership will consider in determining the application of these funds and other resources.

The Partnership’s acquisition strategy is based, in part, on its expectation of ongoing divestitures of energy assets by industry participants. A material decrease in such divestitures would limit the Partnership’s opportunities for future acquisitions and could adversely affect the Partnership’s operations and cash flows available for distribution to its unitholders.

The Partnership’s growth strategy includes acquiring midstream entities or assets that are distinct and separate from the Partnership’s existing terminalling, storage, gathering and transportation operations, which could subject the Partnership to additional business and operating risks.

The Partnership may acquire midstream assets that have operations in new and distinct lines of business from the Partnership’s crude oil or liquid asphalt cement operations. Integration of a new business is a complex, costly and time-consuming process. Failure to timely and successfully integrate acquired entities’ new lines of business with the Partnership’s existing operations may have a material adverse effect on the Partnership’s business, financial condition or results of operations. The difficulties of integrating a new business with the Partnership’s existing operations include, among other things:

| | • | | operating distinct businesses that require different operating strategies and different managerial expertise; |

| | • | | the necessity of coordinating organizations, systems and facilities in different locations; |

| | • | | integrating personnel with diverse business backgrounds and organizational cultures; and |

| | • | | consolidating corporate and administrative functions. |

In addition, the diversion of the Partnership’s attention and any delays or difficulties encountered in connection with the integration of a new business, such as unanticipated liabilities or costs, could harm the Partnership’s existing business, results of operations, financial conditions and prospects. Furthermore, new lines of business will subject the Partnership to additional business and operating risks. For example, the Partnership may in the future determine to acquire businesses that are subject to significant risks due to fluctuations in commodity prices. These new business and operating risks could have a material adverse effect on the Partnership’s financial condition or results of operations.

Expanding the Partnership’s business by constructing new assets subjects the Partnership to risks that projects may not be completed on schedule, and that the costs associated with projects may exceed the Partnership’s expectations, which could cause the Partnership’s cash available for distribution to its unitholders to be less than anticipated.

The construction of additions or modifications to the Partnership’s existing assets, and the construction of new assets, involves numerous regulatory, environmental, political, legal and operational uncertainties and requires the expenditure of significant amounts of capital. If the Partnership undertakes these types of projects, they may not be completed on schedule or at all or at the budgeted cost. In addition, the Partnership’s revenues may not increase immediately upon the expenditure of funds on a particular project. Moreover, the Partnership may construct facilities to capture anticipated future growth in demand in a market in which such growth does not materialize.

The Partnership is exposed to the credit risks of the Partnership’s third-party customers in the ordinary course of the Partnership’s gathering activities. Any material nonpayment or nonperformance by the Partnership’s third-party customers could reduce the Partnership’s ability to make distributions to its unitholders.

In addition to the Partnership’s dependence on SemGroup, the Partnership is subject to risks of loss resulting from nonpayment or nonperformance by the Partnership’s third-party customers. Some of the Partnership’s customers may be highly leveraged and subject to their own operating and regulatory risks. In addition, any material nonpayment or nonperformance by the Partnership’s customers could require the Partnership to pursue substitute customers for its affected assets or provide alternative services. Any such efforts may not be successful or may not provide similar fees. These events could reduce the Partnership’s ability to make distributions to its unitholders.

16

The Partnership’s revenues from third-party customers are generated under contracts that must be renegotiated periodically and that allow the customer to reduce or suspend performance in some circumstances, which could cause the Partnership’s revenues from those contracts to decline and reduce the Partnership’s ability to make distributions to its unitholders.

Some of the Partnership’s contract-based revenues from customers other than SemGroup are generated under contracts with terms which allow the customer to reduce or suspend performance under the contract in specified circumstances, such as the occurrence of a catastrophic event to the Partnership’s or the customer’s operations. The occurrence of an event which results in a material reduction or suspension of a customer’s performance could reduce the Partnership’s ability to make distributions to its unitholders.

Many of the Partnership’s contracts with third-party customers for producer field services have terms of one year or less. As these contracts expire, they must be extended and renegotiated or replaced. The Partnership may not be able to extend, renegotiate or replace these contracts when they expire, and the terms of any renegotiated contracts may not be as favorable as the contracts they replace. In particular, the Partnership’s ability to extend or replace contracts could be harmed by numerous competitive factors, such as those described above under “—The Partnership faces intense competition in its gathering, transportation, terminalling and storage activities. Competition from other providers of crude oil gathering, transportation, terminalling and storage services that are able to supply SemGroup and the Partnership’s other customers with those services at a lower price could reduce the Partnership’s ability to make distributions to its unitholders.” Additionally, the Partnership may incur substantial costs if modifications to the Partnership’s terminals are required in order to attract substitute customers or provide alternative services. If the Partnership cannot successfully renew significant contracts or must renew them on less favorable terms, or if the Partnership incurs substantial costs in modifying its terminals, the Partnership’s revenues from these arrangements could decline and the Partnership’s ability to make distributions to its unitholders could suffer.

The Partnership may incur significant costs and liabilities as a result of pipeline integrity management program testing and any necessary pipeline repair, or preventative or remedial measures, which could have a material adverse effect on the Partnership’s results of operations.

The United States Department of Transportation, or DOT, has adopted regulations requiring pipeline operators to develop integrity management programs for transportation pipelines located where a leak or rupture could do the most harm in “high consequence areas”, including high population areas, areas that are sources of drinking water, ecological resource areas that are unusually sensitive to environmental damage from a pipeline release and commercially navigable waterways, unless the operator effectively demonstrates by risk assessment that the pipeline could not affect the area. The regulations require operators of covered pipelines to:

| | • | | perform ongoing assessments of pipeline integrity; |

| | • | | identify and characterize threats to pipeline segments that could impact a high consequence area; |

| | • | | improve data collection, integration and analysis; |

| | • | | repair and remediate the pipeline as necessary; and |

| | • | | implement preventive and mitigating actions. |

In addition to these adopted regulations, in September 2006, the DOT proposed amendment of existing pipeline safety standards including its integrity management programs to broaden the scope of coverage to include certain rural onshore hazardous liquid and low-stress pipeline systems found near “unusually sensitive areas,” including non-populated areas requiring extra protection because of the presence of sole source drinking water resources, endangered species, or other ecological resources. Also, in December 2006, the Pipeline Inspection, Protection, Enforcement and Safety Act of 2006 was enacted. This act reauthorizes and amends the DOT’s pipeline safety programs and includes a provision eliminating the regulatory exemption for hazardous liquid pipelines operated at low stress. Adoption of new or more stringent pipeline safety regulations affecting the Partnership’s gathering or low-stress pipelines could result in more rigorous and costly integrity management planning requirements being imposed on those lines, which could have a material adverse effect on the Partnership’s results of operations.

17

The Partnership does not have any officers or employees and relies solely on officers of the Partnership’s general partner and employees of SemGroup. Failure of such officers and employees to devote sufficient attention to the management and operation of the Partnership’s business may adversely affect the Partnership’s financial results and the Partnership’s ability to make distributions to its unitholders.

The officers of the Partnership’s general partner are employees of the Partnership’s general partner and are also employed by SemGroup. Pursuant to the Amended Omnibus Agreement with SemGroup, SemGroup operates the Partnership’s assets and performs other administrative services for the Partnership such as accounting, legal, regulatory, development, finance, land and engineering. Affiliates of SemGroup conduct businesses and activities of their own in which the Partnership has no economic interest, including businesses and activities relating to SemGroup. As a result, there is material competition for the time and effort of the officers and employees who provide services to the Partnership’s general partner and SemGroup. If the officers of the Partnership’s general partner and the employees of SemGroup do not devote sufficient attention to the management and operation of the Partnership’s business, the Partnership’s financial results may suffer and the Partnership’s ability to make distributions to its unitholders may be reduced.

The Partnership’s operations are subject to environmental and worker safety laws and regulations that may expose the Partnership to significant costs and liabilities. Failure to comply with these laws and regulations could adversely affect the Partnership’s ability to make distributions to its unitholders.

The Partnership’s midstream crude oil gathering, transportation, terminalling and storage operations, together with the liquid asphalt cement terminalling and storage assets the Partnership is acquiring from SemGroup, are subject to stringent federal, state and local laws and regulations relating to the protection of the environment. Various governmental authorities, including the United States Environmental Protection Agency, have the power to enforce compliance with these laws and regulations and the permits issued under them, and violators are subject to administrative, civil and criminal penalties, including civil fines, injunctions or both. Joint and several strict liability may be incurred without regard to fault or the legality of the original conduct under the Comprehensive Environmental Response, Compensation, and Liability Act, as amended, the Resource Conservation and Recovery Act, as amended, and analogous state laws for the remediation of contaminated areas. Private parties, including the owners of properties located near the Partnership’s terminalling and storage facilities or through which the Partnership’s pipeline systems pass, also may have the right to pursue legal actions to enforce compliance, as well as seek damages for non-compliance with environmental laws and regulations or for personal injury or property damage. Moreover, new stricter laws, regulations or enforcement policies could be implemented that significantly increase the Partnership’s compliance costs and the cost of any remediation that may become necessary, some of which may be material.

In performing midstream operations and liquid asphalt cement terminalling services, the Partnership incurs environmental costs and liabilities in connection with the handling of hydrocarbons and solid wastes. The Partnership currently owns, operates or leases properties that for many years have been used for midstream activities, including properties in and around the Cushing Interchange, and with respect to the Acquired Assets, for liquid asphalt cement terminalling and storage activities. Activities by the Partnership or prior owners, lessees or users of these properties over whom the Partnership had no control may have resulted in the spill or release of hydrocarbons or solid wastes on or under them. Additionally, some sites the Partnership owns or operates are located near current or former storage, terminal and pipeline operations, and there is a risk that contamination has migrated from those sites to the Partnership’s. Increasingly strict environmental laws, regulations and enforcement policies as well as claims for damages and other similar developments could result in significant costs and liabilities, and the Partnership’s ability to make distributions to its unitholders could suffer as a result.

In addition, the workplaces associated with the storage facilities and pipelines the Partnership operates are subject to the requirements of the federal Occupational Safety and Health Act, as amended, or OSHA, and comparable state statutes that regulate the protection of the health and safety of workers. The OSHA hazard communication standard requires that the Partnership maintain information about hazardous materials used or produced in the Partnership’s operations and that the Partnership provide this information to employees, state and local government authorities, and local residents. Failure to comply with OSHA requirements, including general industry standards, recordkeeping requirements and

18

monitoring of occupational exposure to regulated substances, could subject the Partnership to fines or significant compliance costs and adversely affect the Partnership’s ability to make distributions to its unitholders.

The Partnership’s business involves many hazards and operational risks, including adverse weather conditions, which could cause the Partnership to incur substantial liabilities.

The Partnership’s operations are subject to the many hazards inherent in the transportation and storage of crude oil and the storage of liquid asphalt cement, including:

| | • | | explosions, fires, accidents, including road and highway accidents involving the Partnership’s tanker trucks; |

| | • | | extreme weather conditions, such as hurricanes which are common in the Gulf Coast and tornadoes and flooding which are common in the Midwest; |

| | • | | damage to the Partnership’s pipelines, storage tanks, terminals and related equipment; |

| | • | | leaks or releases of crude oil into the environment; and |

| | • | | acts of terrorism or vandalism. |

If any of these events were to occur, the Partnership could suffer substantial losses because of personal injury or loss of life, severe damage to and destruction of property and equipment, and pollution or other environmental damage resulting in curtailment or suspension of the Partnership’s related operations. In addition, mechanical malfunctions, faulty measurement or other errors may result in significant costs or lost revenues.

The Partnership is not fully insured against all risks incident to the Partnership’s business, and could incur substantial liabilities as a result.

The Partnership may not be able to maintain or obtain insurance of the type and amount the Partnership desires at reasonable rates. As a result of changing market conditions, premiums and deductibles for certain of the Partnership’s insurance policies may increase substantially in the future. In some instances, certain insurance could become unavailable or available only for reduced amounts of coverage. If the Partnership were to incur a significant liability for which it was not fully insured, it could have a material adverse effect on the Partnership’s financial position and ability to make distributions to its unitholders.

The Partnership shares some insurance policies, including the Partnership’s general liability policy, with SemGroup. These policies contain caps on the insurer’s maximum liability under the policy, and claims made by either SemGroup or the Partnership are applied against the caps and deductibles. The possibility exists that, in an event in which the Partnership wishes to make a claim under a shared insurance policy, the Partnership’s claim could be denied or only partially satisfied due to claims made by SemGroup against the policy cap. Further, where events occur that would entitle both SemGroup and the Partnership to benefits under these insurance policies, the full deductible may be borne by the first claimant under the policy. In addition, claims made by SemGroup could affect the Partnership’s premiums and the Partnership’s ability to obtain insurance in the future.

If the Partnership’s general partner fails to develop or maintain an effective system of internal controls, then the Partnership may not be able to accurately report the Partnership’s financial results or prevent fraud. As a result, current and potential unitholders could lose confidence in the Partnership’s financial reporting, which would harm the Partnership’s business and the trading price of the Partnership’s common units.