Table of Contents

| PROSPECTUS | Filed Pursuant to Rule 424(b)(3) | |

| Registration No. 333-141465 |

(Proposed holding company for Bank of New Orleans)

Up to 6,095,000 Shares of Common Stock

(Anticipated Maximum)

Louisiana Bancorp, Inc. is offering shares of its common stock for sale in connection with the conversion of Bank of New Orleans from the mutual to the stock form of ownership. Louisiana Bancorp, Inc. will be the holding company for Bank of New Orleans. After the offering, all of Bank of New Orleans’ outstanding common stock will be owned by Louisiana Bancorp, Inc. We expect that the common stock of Louisiana Bancorp, Inc. will be quoted on the Nasdaq Global Market under the symbol “LABC.” Sandler O’Neill & Partners, L.P. will use its best efforts to assist us in Louisiana Bancorp’s selling efforts, but is not required to purchase any of the common stock that is being offered for sale. All shares offered for sale are being offered at a price of $10.00 per share. Purchasers will not pay a commission to purchase shares of common stock in the offering.

| • | If you are a current or former depositor of Bank of New Orleans you may have priority rights to purchase shares. |

| • | If you are not a current or former depositor of Bank of New Orleans, you may have an opportunity to purchase shares of common stock after priority orders are filled. |

We are offering up to 6,095,000 shares of common stock for sale on a best efforts basis, subject to certain conditions. We must sell a minimum of 4,505,000 shares to complete the offering. If, as a result of regulatory considerations, demand for the shares or changes in market or financial conditions, the independent appraiser determines our market value has increased, we may sell up to 7,009,250 shares without giving you further notice or the opportunity to change or cancel your order. The offering is expected to close at 4:00 p.m., Central time, on June 14, 2007. We may extend this close date without notice to you until July 29, 2007, unless the Office of Thrift Supervision approves a later date, which will not be beyond June 27, 2009.

The minimum purchase is 25 shares. Once submitted, orders are irrevocable unless the offering is terminated or extended beyond July 29, 2007. If the offering is extended beyond July 29, 2007, subscribers will be notified and will be given the right to confirm, change or cancel their orders, and funds will be returned promptly to subscribers who do not respond to this notice. Funds received before completion of the offering up to the minimum of the offering range will be maintained at Bank of New Orleans. Funds received in excess of the minimum of the offering range may be maintained at Bank of New Orleans, or at our discretion, in an escrow account at an independent insured depository institution. In either case, we will pay interest on all funds received at a rate equal to Bank of New Orleans’ passbook rate, which is currently 0.5% per annum. If we do not sell the minimum number of shares or if we terminate the offering for any other reason, we will promptly return your funds with interest at Bank of New Orleans’ passbook rate.

The Office of Thrift Supervision has conditionally approved our plan of conversion. However, such approval does not constitute a recommendation or endorsement of this offering.

This investment involves a degree of risk, including the possible loss of principal.

Please read “Risk Factors” beginning on page 13.

Table of Contents

OFFERING SUMMARY

Price per Share: $10.00

| Minimum | Maximum | Maximum, As Adjusted | |||||||

Number of shares | 4,505,000 | 6,095,000 | 7,009,250 | ||||||

Gross offering proceeds | $ | 45,050,000 | $ | 60,950,000 | $ | 70,092,500 | |||

Estimated offering expenses(1) | $ | 900,000 | $ | 900,000 | $ | 900,000 | |||

Selling agent fees and expenses | $ | 391,000 | $ | 537,000 | $ | 622,000 | |||

Estimated net proceeds | $ | 43,759,000 | $ | 59,513,000 | $ | 68,571,000 | |||

Estimated net proceeds per share | $ | 9.71 | $ | 9.76 | $ | 9.78 | |||

| (1) | Excludes selling agent fees and expenses payable to Sandler O’Neill & Partners, LP. in connection with the offering. |

These securities are not deposits or accounts and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Neither the Securities and Exchange Commission, the Office of Thrift Supervision, nor any state securities regulator has approved or disapproved of these securities or determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is May 14, 2007

Table of Contents

Table of Contents

| Page | ||

| 1 | ||

| 13 | ||

| 19 | ||

| 19 | ||

| 21 | ||

| 21 | ||

Bank of New Orleans Meets All of Its Regulatory Capital Requirements | 22 | |

| 24 | ||

| 26 | ||

| 30 | ||

| 32 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 35 | |

Business of Bank of New Orleans | 48 | |

| 67 | ||

| 74 | ||

| 76 | ||

| 87 | ||

| 88 | ||

Restrictions on Acquisition of Louisiana Bancorp and Bank of New Orleans and Related Anti-Takeover Provisions | 105 | |

| 111 | ||

| 112 | ||

| 113 | ||

| 113 | ||

| 114 | ||

Table of Contents

This summary highlights selected information from this document and may not contain all the information that is important to you. To understand the stock offering and the reorganization fully, you should read this entire document carefully, including the financial statements and the notes to the financial statements of Bank of New Orleans.

THE COMPANIES

Louisiana Bancorp, Inc.

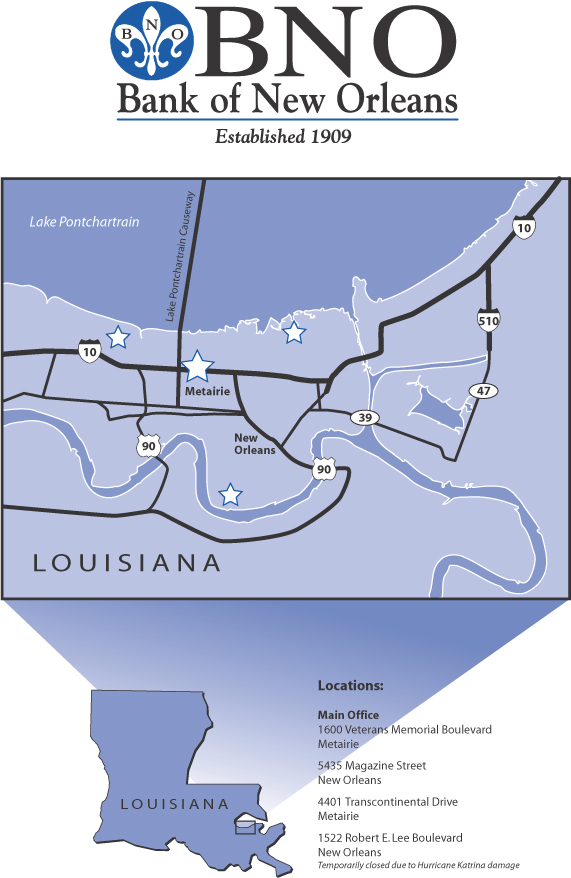

This offering is being made by Louisiana Bancorp, Inc., a Louisiana corporation recently formed by Bank of New Orleans to be its holding company. Louisiana Bancorp has not yet commenced operations and has no assets. Following the completion of this offering, Louisiana Bancorp will be a savings and loan holding company and parent corporation for Bank of New Orleans. The common stock of Louisiana Bancorp is being sold as part of the mutual-to-stock conversion of Bank of New Orleans, with a preference to certain depositors and employee benefit plans of the bank. We expect the common stock of Louisiana Bancorp to be publicly traded on the Nasdaq Global Market. The executive offices of Louisiana Bancorp, Inc. are located at the bank’s headquarters, 1600 Veterans Memorial Boulevard, Metairie, Louisiana. You may visit our website at www.bankofneworleans.com.

Bank of New Orleans

Bank of New Orleans is a federally chartered mutual savings bank which was originally organized in 1909. As of December 31, 2006, the bank had $219.7 million in assets, $150.3 million in deposits and $29.2 million in equity capital. We operate out of our headquarters in Metairie, Louisiana, approximately eight miles from downtown New Orleans, and three branch offices, although one of our branches remains temporarily closed due to flooding suffered during Hurricane Katrina in August 2005. Bank of New Orleans is a community oriented savings bank offering a variety of deposit products as well as providing single-family residential loans, commercial real estate and multi-family residential loans and, to a lesser degree, consumer loans, primarily to individuals, families and small to mid-sized businesses located in the greater New Orleans market area as well as other areas in southern Louisiana and coastal Mississippi. As of December 31, 2006, $45.6 million or 49.6% of the Bank’s total loan portfolio consisted of one-to four-family residential mortgage loans and $34.0 million or 37.0% consisted of multi-family residential, commercial real estate and land loans.

The devastating effects of Hurricane Katrina continue to significantly impact southern Louisiana. However, total non-performing loans of Bank of New Orleans, which amounted to $3.5 million or 3.8% of total loans at December 31, 2005, improved to $184,000 or 0.2% of total loans at December 31, 2006. As of December 31, 2006, Bank of New Orleans maintained an allowance for loan losses of $2.3 million, or 2.5% of total loans.

Bank of New Orleans’ mission is to operate and grow a profitable community focused financial institution while protecting its franchise through prudent operating standards. We plan to achieve this by executing our strategy of:

| • | growing our loan portfolio; |

| • | expanding our market area; |

| • | maintaining high asset quality; and |

| • | providing exceptional service to attract and retain customers. |

We believe our mutual-to-stock conversion will assist us in implementing our business strategy by increasing our capital base which will support continuing growth in our lending operations and facilitate the expansion of our franchise through the opening of additionalde novo branch offices or possible acquisitions of other financial institutions. We believe it is an opportune time for us to convert so that we can grow. After our

1

Table of Contents

conversion, we will also be able to use stock-related incentive programs to attract and retain executive and other personnel, which we expect will permit us to expand our lending capabilities. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Business Strategy” on page 36.

The Conversion

The conversion involves a series of transactions by which we will convert from our current status as a mutual savings bank to a stock savings bank and become a subsidiary of Louisiana Bancorp. As a stock savings bank, we will implement our business strategy focused on loan growth and geographic expansion of our franchise. After the conversion, we will continue to be subject to the regulation and supervision of the Office of Thrift Supervision and the Federal Deposit Insurance Corporation. See “The Conversion and Offering” at page 88.

At present, our depositors are voting members of Bank of New Orleans. When we complete the conversion, our depositors will cease to be voting members and Louisiana Bancorp will have all of the voting rights in Bank of New Orleans since it will be the bank’s sole shareholder. Exclusive voting rights with respect to Louisiana Bancorp will be vested in the holders of our common stock.

The conversion will permit our customers and possibly other members of the local community and of the general public to become equity owners and to share in our future. The conversion also will provide additional funds for lending and investment activities and enhance our ability to diversify and to grow our operations. The conversion to stock form is subject to approval by our members entitled to vote on the matter.

The Offering

We are offering between 4,505,000 shares and 6,095,000 shares of our common stock for sale at a purchase price of $10.00 per share. All investors will pay the same cash price per share in the offering. Subject to regulatory approval, we may increase the amount of stock to be sold to 7,009,250 shares without any further notice to you if, as a result of regulatory conditions, demand for the shares or changes in market or financial conditions, the independent appraiser determines that the market value has increased.

Reasons for the Offering

We are pursuing the offering for the following reasons:

| • | The additional funds resulting from the offering will support future growth and geographic expansion of our banking operations, as well as increase Bank of New Orleans’ loans-to-one borrower limits and provide increased lending capability. |

| • | To enhance our future profitability and earnings through reinvesting and leveraging the proceeds, primarily through traditional funding and lending activities. |

| • | To enhance our current compensation programs through the addition of stock-based benefit plans, which we expect will help us to attract and retain qualified directors, officers and employees. |

| • | The offering will facilitate our ability to make acquisitions of other institutions in the future (although we do not currently have any plans, agreements or understandings regarding any acquisition transactions). |

We believe that this is the right time for Bank of New Orleans to convert to the stock form. After Hurricane Katrina, our primary focus initially was on damage assessment and re-opening the bank, contacting our customers to assess their needs and ability to repay outstanding loans and analyzing our allowance for loan losses and making additional provisions for loan losses in light of the devastation caused by the storm and the uncertain future of the market area. After this initial assessment period, our board of directors and management carefully considered various strategies for operating the bank in the post-Katrina environment. We determined that, while there are considerable risks and uncertainties relating to the business environment and future viability of the

2

Table of Contents

metropolitan New Orleans market, there also were unique opportunities to grow and expand our franchise as a participant in the rebuilding process in southern Louisiana. We believe that we can grow our loan portfolio, particularly in the commercial real estate and construction areas. The increased capital from the offering proceeds will enable us to make larger loans than we have been able to in the past. In order to capitalize on these opportunities we plan to hire several additional commercial lending officers who will focus on increasing our commercial real estate loan portfolio. We believe that, as a stock-form institution, we may be in a better position to attract and retain quality loan officers. In addition, we plan to expand our banking franchise by opening additional branch offices in areas to the north and west of our current offices. We expect that such areas will continue to grow and be developed in future years and that, by expanding the geographic market area we serve, we may reduce somewhat the risk we currently face as a result of our business concentration in metropolitan New Orleans. We plan to open one additional branch in the first year after the offering and then one branch every 18 months over the next three to five years, although we have no specific branch office locations in the planning or development-stage at this time. We hope to be able to use these new branches to enhance our commercial lending efforts in the areas in which we open new offices. We also may use a portion of the net proceeds received to purchase loans and loan participation interests outside of our traditional market area. We expect this will facilitate our loan growth and returns and, again, help to reduce the geographic concentration risk in our portfolio. In addition, we believe that there may be opportunities to make acquisitions of other financial institutions in the future, as some institutions may determine they cannot continue to operate effectively as independent entities in the post-Katrina climate, although we do not currently have any plans, agreements or understanding regarding any acquisition transactions. The proceeds from the offering as well as the stock form of ownership will facilitate our ability to consider acquisitions in the future.

Conditions to Completion of the Offering

We cannot complete the offering unless:

| • | Our members approve the conversion at the special meeting to be held onJune 27, 2007; |

| • | We sell at least the minimum number of shares offered; and |

| • | We receive the final approval of the Office of Thrift Supervision to complete the conversion and the offering. |

How We Determined the Price Per Share and the Offering Range

The offering range is based on an independent appraisal by Feldman Financial Advisors, Inc., an appraisal firm experienced in appraisals of savings institutions. The pro forma market value is the estimated market value of our common stock assuming the sale of shares in this offering. Feldman Financial Advisors has indicated that in its opinion as of March 13, 2007, the estimated pro forma market value of our common stock was between $45.1 million and $61.0 million, with a midpoint of $53.0 million. The appraisal was based in part upon our financial condition and operations and the effect of the additional capital we will raise from the sale of common stock in the offering.

In preparing its appraisal, Feldman Financial Advisors considered the information in this prospectus, including our financial statements. Feldman Financial Advisors also considered the following factors, among others:

| • | our historical, present and projected operating results including, but not limited to, historical income statement information such as return on assets, return on equity, net interest margin trends, operating expense ratios, levels and sources of non-interest income, and levels of loan loss provisions; |

| • | our historical, present and projected financial condition including, but not limited to, historical balance sheet size, composition and growth trends, loan portfolio composition and trends, liability composition and trends, credit risk measures and trends, and interest rate risk measures and trends; |

3

Table of Contents

| • | the economic, demographic and competitive characteristics of Bank of New Orleans’ primary market area after Hurricane Katrina including, but not limited to, employment by industry type, unemployment trends, size and growth of the population, trends in household and per capita income, deposit market share and largest competitors by deposit market share; |

| • | a comparative evaluation of our operating and financial statistics with those of other similarly situated institutions, which included a comparative analysis of balance sheet composition, income statement ratios, credit risk, interest rate risk and loan portfolio composition; |

| • | the impact of the stock offering on our equity and earning potential including, but not limited to, the increase in equity resulting from the offering, the estimated increase in earnings resulting from the reinvestment of the net proceeds of the offering, the estimated impact on the equity and earnings resulting from adoption of the employee benefit plans and the effect of higher consolidated equity on our future operations; and |

| • | the trading market for securities of comparable institutions and general conditions in the market for such securities. |

Subject to regulatory approval, we may increase the amount of common stock offered by up to 15%. Accordingly, at the minimum of the offering range, we are offering 4,505,000 shares, and at the maximum, as adjusted, of the offering range we are offering 7,009,250 shares in the subscription offering. The appraisal will be updated before the offering is completed. If the pro forma market value of the common stock at that time is either below $45.1 million or above $70.1 million, we may terminate the stock offering and promptly return all funds; promptly return all funds, set a new offering range and give all subscribers the opportunity to modify or rescind their purchase orders for shares of Louisiana Bancorp’s common stock; or take such other actions as may be permitted by the Office of Thrift Supervision and the Securities and Exchange Commission. See “The Conversion and Offering – How We Determined the Price Per Share and the Offering Range” for a description of the factors and assumptions used in determining the stock price and offering range.

Feldman Financial Advisors relied primarily on a comparative market value methodology in determining the pro forma market value of our common stock. In applying this methodology, Feldman Financial Advisors analyzed financial and operational comparisons of Bank of New Orleans with a selected peer group of publicly traded savings institutions. The pro forma market value of our common stock was determined by Feldman Financial Advisors based on the market pricing ratios of the peer group, subject to certain valuation adjustments based on fundamental differences between Bank of New Orleans and the institutions comprising the peer group. Specifically, Feldman Financial Advisors took into account that, on a pro forma basis compared solely to our peer group, we had a relatively higher capital level, higher concentration of investment in securities and a lower concentration of loans and that, based on the twelve-month period preceding their appraisal, we had higher profitability compared to the peer group. Additionally, Feldman Financial Advisors took into account the economic conditions and outlook for the metropolitan New Orleans market area in which Bank of New Orleans operates and the after market pricing characteristics of recently converted savings institutions. Feldman Financial advisors utilized the results of this overall analysis to establish pricing ratios that resulted in the determination of our pro forma market value.

Two of the measures investors use to analyze whether a stock might be a good investment are the ratio of the offering price to the issuer’s “book value” and the ratio of the offering price to the issuer’s annual net income. Feldman Financial Advisors considered these ratios, among other factors, in preparing its appraisal. Book value is the same as total equity, and represents the difference between the issuer’s assets and liabilities. Feldman Financial Advisors’ appraisal also incorporates an analysis of a peer group of publicly traded companies that Feldman Financial Advisors considered to be comparable to us.

The following table presents a summary of selected pricing ratios for the peer group companies and for us on a reported basis as utilized by Feldman Financial Advisors in its appraisal. These ratios are based on earnings for the twelve months ended December 31, 2006 and book value as of December 31, 2006. Compared to the average pricing ratios of the peer group at the maximum of the offering range, our stock would be priced at a premium of 16.5% to the peer group on a price-to-earnings basis and a discount of 29.0% to the peer group on a price-to book

4

Table of Contents

basis. This means that, at the maximum of the offering range, a share of our common stock would be more expensive than the peer group based on an earnings per share basis and less expensive than the peer group based on a book value per share basis. See “Pro Forma Data” for the assumptions used to derive these pricing ratios.

| Price To Earnings Multiple | Price to Tangible Book Value Ratio | |||||

Louisiana Bancorp (pro forma) | ||||||

Minimum | 18.2 | x | 66.7 | % | ||

Maximum | 23.3 | 74.9 | ||||

Peer group companies as of March 13, 2007 | ||||||

Average | 20.0 | x | 111.1 | % | ||

Median | 16.8 | 130.5 |

The independent appraisal does not indicate market value. You should not assume or expect that the valuation described above means that our common stock will trade at or above the $10.00 purchase price after the offering.

After Market Performance of Other Recently Converted Institutions

The following table provides information regarding the after-market performance of the conversion offerings completed from January 1, 2005 through March 13, 2007. As part of its appraisal of our pro forma market value, Feldman Financial Advisors considered the after-market performance of mutual-to-stock conversions completed in the three months prior to March 13, 2007, which was the date of its appraisal report. Feldman Financial Advisors considered information regarding the new issue market for converting thrifts as part of its consideration of the market for thrift stocks.

| Appreciation From Initial Offering Price | ||||||||||||||

Issuer (Market/Symbol) | Date of IPO | After 1 Day | After 1 Week | After 1 Month | Through 03/13/07 | |||||||||

Hampden Bancorp, Inc. (Nasdaq: HBNK) | 01/17/07 | 28.2 | % | 24.5 | % | 23.4 | % | 22.5 | % | |||||

Chicopee Bancorp, Inc. (Nasdaq: CBNK) | 07/20/06 | 44.96 | 44.7 | 45.2 | 51.3 | |||||||||

Newport Bancorp, Inc. (Nasdaq: NFSB) | 07/07/06 | 28.0 | 28.6 | 31.7 | 38.5 | |||||||||

Legacy Bancorp, Inc. (Nasdaq: LEGC) | 10/26/05 | 30.3 | 34.8 | 32.0 | 56.0 | |||||||||

Bank Financial Corp (Nasdaq: BFIN) | 06/24/05 | 36.0 | 33.3 | 36.0 | 64.4 | |||||||||

Benjamin Franklin Bancorp, Inc. (Nasdaq: BFBC) | 04/05/05 | 0.6 | 3.6 | 3.4 | 47.7 | |||||||||

OC Financial, Inc. (OTCBB: OCFL) | 04/01/05 | 20.0 | 10.0 | 10.0 | 9.5 | |||||||||

Royal Financial, Inc. (OTCBB: RYFL) | 01/21/05 | 16.0 | 25.5 | 25.4 | 67.0 | |||||||||

Average - all transactions | 25.5 | 25.6 | 25.9 | 44.6 | ||||||||||

Median - all transactions | 28.1 | 27.1 | 28.6 | 49.5 | ||||||||||

This table is not intended to be indicative of how our stock may perform. Furthermore, this table presents only short-term price performance with respect to several companies that only recently completed their initial public offerings and may not be indicative of the longer-term stock price performance of these companies. Stock price appreciation is affected by many factors, including, but not limited to: general market and economic conditions; the interest rate environment; the amount of proceeds a company raises in its offering; and numerous

5

Table of Contents

factors relating to the specific company, including the experience and ability of management, historical and anticipated operating results, the nature and quality of the company’s assets, and the company’s market area. The companies listed in the table above may not be similar to Louisiana Bancorp, the pricing ratios for their stock offerings were in some cases different from the pricing ratios for Louisiana Bancorp’s common stock and the market conditions in which these offering were completed were, in some cases, different from current market conditions. Any or all of these differences may cause our stock to perform differently from these other offerings. Before you make an investment decision, we urge you to carefully read this prospectus, including, but not limited to, the “Risk Factors” section beginning on page 13.

You should be aware that, in certain market conditions, stock prices of thrift initial public offerings have decreased. We can give you no assurance that our stock will not trade below the $10.00 purchase price or that our stock will perform similarly to other recent mutual-to-stock conversions.

6

Table of Contents

Use of Proceeds from the Sale of Our Common Stock

We will use the proceeds from the offering as follows:

Use of Proceeds | Amount, at the minimum | Amount, at the maximum | Percentage of net offering proceeds at the maximum | ||||||

Loan to our employee stock ownership plan | $ | 3,604,000 | $ | 4,876,000 | 8.2 | % | |||

Repurchase of shares for recognition and retention plan | $ | 1,802,000 | $ | 2,438,000 | 4.1 | % | |||

Investment in equity of Bank of New Orleans | $ | 21,879,500 | $ | 29,756,500 | 50.0 | % | |||

General corporate purposes – investments, dividend payments, possible acquisitions and stock repurchases | $ | 16,473,500 | $ | 22,442,500 | 37.7 | % | |||

Half of the net proceeds from the offering will be used by Louisiana Bancorp to buy the common stock of Bank of New Orleans. Bank of New Orleans will use the portion of the cash proceeds it receives for general corporate purposes. The net proceeds received by Bank of New Orleans will further strengthen our capital position, which already exceeds all regulatory requirements, and will provide us with additional flexibility to grow and diversify. The proceeds invested in Bank of New Orleans, in addition to funding new loans and being invested in equity securities, may ultimately be used to finance the expansion of our banking operations through the opening of additional branch offices or possible acquisitions of other financial institutions or branch offices, although no such transactions are specifically being considered at this time.

The remaining portion of the net proceeds after the loan to our employee stock ownership plan and the investment in Bank of New Orleans will be retained by Louisiana Bancorp and will be available for general corporate purposes. We may initially use the remaining net proceeds to invest in deposits at Bank of New Orleans, U.S. Government and federal agency securities of various maturities, Federal funds, mortgage-backed securities, or a combination thereof. In addition, assuming shareholder approval of the recognition and retention plan, we intend to contribute sufficient funds to the trust so that it can purchase a number of shares equal to an aggregate of 4% of the common stock issued in the conversion. The net proceeds retained by Louisiana Bancorp may ultimately be used to:

| • | support the future expansion of operations through establishment of additional branch offices or other customer facilities for Bank of New Orleans, acquisition of other financial institutions or branch offices, expansion into other lending markets or diversification into other banking related businesses, although no such transactions are specifically being considered at this time; |

| • | invest in deposits at Bank of New Orleans or securities; or |

| • | fund repurchases of our common stock or serve as a source of possible payments of cash dividends. |

Our Dividend Policy

We have not determined whether we will pay dividends on the common stock. After the offering, we will consider a policy of paying regular cash dividends. Our ability to pay dividends will depend on a number of factors, including capital requirements, regulatory limitations and our operating results and financial condition. Initially, our ability to pay dividends will be limited to the net proceeds retained by Louisiana Bancorp and earnings from the investment of such proceeds, as well as dividends from Bank of New Orleans, if any. At the maximum of the offering range, Louisiana Bancorp will retain approximately $29.8 million of the net proceeds. Additionally, funds could be contributed from Bank of New Orleans through dividends; however, the ability of Bank of New Orleans to dividend funds to Louisiana Bancorp is subject to regulatory limitations described in more detail in “Dividends” on page 21.

7

Table of Contents

Benefits to Management from the Offering

Our employees, officers and directors will benefit from the offering due to various stock-based benefit plans.

| • | Full-time employees, including officers, will be participants in our employee stock ownership plan which will purchase shares of common stock in the offering; |

| • | Subsequent to completion of the offering, we intend to implement a: |

| • | stock recognition and retention plan; and |

| • | stock option plan |

which will benefit our employees and directors.

| • | Employee Stock Ownership Plan. The employee stock ownership plan will provide retirement benefits to all eligible employees of Bank of New Orleans. The plan will purchase 8.0% of Louisiana Bancorp’s common stock sold in the offering, with the proceeds of a loan from Louisiana Bancorp. As the loan is repaid and shares are released from collateral, the shares will be allocated to the accounts of participants based on a participant’s compensation as a percentage of total plan compensation. Non-employee directors are not eligible to participate in the employee stock ownership plan. We will incur additional compensation expense as a result of this plan. See “Pro Forma Data” for an illustration of the effects of this plan. |

| • | Stock Option and Stock Recognition and Retention Plans. We intend to implement a stock option plan and stock recognition and retention plan no earlier than six months after the offering and conversion. Under these plans, we may award stock options and shares of restricted stock to employees and directors. Shares of restricted stock will be awarded at no cost to the recipient. Stock options will be granted at an exercise price equal to 100% of the fair market value of our common stock on the option grant date. We will incur additional compensation expense as a result of both plans. See “Pro Forma Data” for an illustration of the effects of these plans. Under the stock option plan, we may grant stock options in an amount up to 10.0% of Louisiana Bancorp’s common stock sold in the offering. Under the stock recognition and retention plan, we may award restricted stock in an amount equal to 4.0% of Louisiana Bancorp’s common stock sold in the offering. The plans will comply with all applicable Office of Thrift Supervision regulations. Implementation of the stock option plan and stock recognition and retention plan will be subject to approval by the shareholders of Louisiana Bancorp. If the plans are implemented within one year of the conversion and offering, they must be approved by a majority of the total votes eligible to be cast by our shareholders. If the plans are implanted more than one year after the conversion, they must be approved by a majority of the total votes cast. |

The following table presents the total value of all shares expected to be available for restricted stock awards under the stock recognition and retention plan, based on a range of market prices from $8.00 per share to $14.00 per share. Ultimately, the value of the grants will depend on the actual trading price of our common stock, which depends on numerous factors.

| Value of | ||||||||||||

Share Price | 180,200 Shares Awarded at Minimum of Range | 212,000 Shares Awarded at Midpoint of Range | 243,800 Shares Awarded at Maximum of Range | 280,370 Shares Awarded at 15% Above Maximum of Range | ||||||||

$8.00 | $ | 1,441,600 | $ | 1,696,000 | $ | 1,950,400 | $ | 2,242,960 | ||||

10.00 | 1,802,000 | 2,120,000 | 2,438,000 | 2,803,700 | ||||||||

12.00 | 2,162,400 | 2,544,000 | 2,925,600 | 3,364,440 | ||||||||

14.00 | 2,522,800 | 2,968,000 | 3,413,200 | 3,925,180 | ||||||||

8

Table of Contents

The following table presents the total value of all stock options expected to be made available for grant under the proposed stock option plan, based on a range of market prices from $8.00 per share to $14.00 per share. For purposes of this table, the value of the stock options was determined using the Black-Scholes option-pricing formula. See “Pro Forma Data.” Ultimately, financial gains can be realized on a stock option only if the market price of the common stock increases above the price at which the option is granted.

| Value of | |||||||||||||||

Exercise Price | Option Value | 450,500 Options Granted at Minimum of Range | 530,000 Options Granted at Midpoint of Range | 609,500 Options Granted at Maximum of Range | 700,925 Options Granted at 15% Above Maximum of Range | ||||||||||

$8.00 | $ | 3.24 | $ | 1,459,620 | $ | 1,717,200 | $ | 1,974,780 | $ | 2,270,997 | |||||

10.00 | 4.05 | 1,824,525 | 2,146,500 | 2,468,475 | 2,838,746 | ||||||||||

12.00 | 4.86 | 2,189,430 | 2,575,800 | 2,962,170 | 3,406,496 | ||||||||||

14.00 | 5.67 | 2,554,335 | 3,005,100 | 3,455,865 | 3,974,245 | ||||||||||

The following table summarizes, at the maximum of the offering range, the total number and value of the shares of common stock that the employee stock ownership plan expects to acquire and the total value of all restricted stock awards and stock options that are expected to be available under the stock recognition and retention plan and stock option plan, respectively. At the maximum of the offering range, we will sell 6,095,000 shares.

| Number of Shares to be Granted or Purchased | As a % of Common Stock Sold in the Offering(1) | Total Estimated Value of Grants | ||||||||

Employee stock ownership plan | 487,600 | (2) | 8.0 | % | $ | 4,876,000 | (4) | |||

Restricted stock awards | 243,800 | 4.0 | 2,438,000 | (4) | ||||||

Stock options | 609,500 | (3) | 10.0 | 2,468,475 | (5) | |||||

Total | 1,340,900 | 22.0 | % | $ | 9,782,475 | |||||

| (1) | Based on shares to be sold at maximum of offering range. |

| (2) | Represents the number of shares of common stock of Louisiana Bancorp to be outstanding based on the maximum of the offering range multiplied by 8.0%. |

| (3) | Represents the number of shares of common stock of Louisiana Bancorp to be outstanding based on the maximum of the offering range multiplied by 10.0%. |

| (4) | Assumes the value of Louisiana Bancorp’s common stock is $10.00 per share for purposes of determining the total estimated value of the grants under the employee stock ownership plan and the recognition and retention plan. |

| (5) | Assumes the value of a stock option is $4.05 per share, which was determined using the Black-Scholes option-pricing formula. See “Pro Forma Data.” |

Market For Common Stock

We have applied to have the common stock of Louisiana Bancorp listed for trading on the Nasdaq Global Market under the symbol “LABC.” We cannot assure you that our common stock will be approved for listing. Sandler O’Neill & Partners, L.P. currently intends to become a market maker in the common stock, but it is under no obligation to do so. We cannot assure you that other market markers will be obtained or that an active and liquid trading market for our common stock will develop or, if developed, will be maintained.

Federal and State Income Tax Consequences

We have received an opinion from our federal income tax counsel, Elias, Matz, Tiernan & Herrick L.L.P., that, under federal income tax law and regulation, the tax basis to the shareholders of the common stock purchased in the offering will be the amount paid for the common stock, and that the conversion will not be a taxable event for us. This opinion, however, is not binding on the Internal Revenue Service. We also have received an opinion that the reorganization should not be a taxable event under Louisiana income tax law, see “The Conversion and Offering – Tax Aspects” (page 103). The full texts of the opinions are filed as exhibits to the registration statement of which

9

Table of Contents

this document is a part, and copies may be obtained from the SEC. See “Where You Can Find Additional Information” on page 113.

In its opinion, Elias, Matz, Tiernan & Herrick L.L.P. notes that the subscription rights will be granted at no cost to the recipients, will be legally nontransferable and of short duration, and will provide the recipients with the right only to purchase shares of common stock at the same price to be paid by members of the general public in any community offering. Elias, Matz, Tiernan & Herrick L.L.P. has also noted that Feldman Financial Advisors has issued a letter stating that the subscription rights will have no ascertainable market value. In addition, no cash or property will be given to recipients of the subscription rights in lieu of such rights or to those recipients who fail to exercise such rights. In addition, the IRS was requested in 1993 in a private letter ruling to address the federal tax treatment of the receipt and exercise of nontransferable subscription rights in another reorganization but declined to express any opinion. Elias, Matz, Tiernan & Herrick L.L.P. believes because of such factors that it is more likely than not that the nontransferable subscription rights to purchase common stock will have no ascertainable value at the time the rights are granted. In addition, neither we nor Elias, Matz, Tiernan & Herrick L.L.P. is aware of any instance where the IRS has determined that subscription rights of the type provided in our conversion have any ascertainable value.

Restrictions on the Acquisition of Louisiana Bancorp and Bank of New Orleans

Federal regulation, as well as provisions contained in the articles of incorporation and bylaws of Louisiana Bancorp, contain certain restrictions on acquisitions of Louisiana Bancorp or its capital stock. These restrictions include the requirement that a potential acquirer of common stock obtain the prior approval of the Office of Thrift Supervision before acquiring in excess of 10% of the stock of Louisiana Bancorp.

In addition, the articles of incorporation of Louisiana Bancorp include a provision that prohibit any person from acquiring or offering to acquire the beneficial ownership of more than 10% of any class of equity security of Louisiana Bancorp. For further information, see “Restrictions on Acquisition of Louisiana Bancorp and Bank of New Orleans and Related Anti-Takeover Provisions.”

The Amount of Stock You May Purchase

The minimum purchase is 25 shares. You may purchase no more than $250,000 of common stock offered in any single priority category. The maximum amount of shares that a person together with any associates or group of persons acting in concert with such person may purchase is 1.0% of the common stock being offered (60,950 shares). Your associates are the following persons:

| • | persons on joint accounts with you; |

| • | relatives living in your house; |

| • | other persons who have the same address as you on our records; |

| • | companies, trusts or other entities in which you have a controlling interest or hold a position; or |

| • | other persons who may be acting together with you. |

We may decrease or increase the maximum purchase limitation without notifying you. For additional information, see “The Conversion and Offering – Limitations on Common Stock Purchases” at page 97.

How We Will Prioritize Orders If We Receive Orders for More Shares Than Are Available for Sale

You might not receive any or all of the shares you order. If we receive orders for more shares than are available, we will allocate stock to the following persons or groups.

10

Table of Contents

| PRIORITY 1: | ELIGIBLE ACCOUNT HOLDERS (Bank of New Orleans depositors with a balance of at least $50 at the close of business on December 31, 2005). | |

| PRIORITY 2: | OUR EMPLOYEE STOCK OWNERSHIP PLAN. | |

| PRIORITY 3: | SUPPLEMENTAL ELIGIBLE ACCOUNT HOLDERS (Bank of New Orleans depositors with a balance of at least $50 at the close of business onMarch 31, 2007). | |

| PRIORITY 4: | OTHER MEMBERS (Bank of New Orleans depositors at the close of business onApril 30, 2007). | |

If the above persons do not subscribe for all of the shares offered in the subscription offering, we will offer the remaining shares to the general public in the community offering, giving preference to natural persons who reside in Jefferson and Orleans Parishes, Louisiana.

How to Order Shares in the Offering

If you want to place an order for shares in the offering, you must complete an original stock order and certification form and send it to us, together with full payment. You must sign the certification that is on the reverse side of the stock order and certification form. We must receive your stock order and certification form before the end of the subscription offering or the end of the community offering, as appropriate. Once we receive your order, you cannot cancel or change it.

To ensure that we properly identify your subscription rights, you must list all of your deposit accounts as of the eligibility date on the stock order and certification form. If you fail to do so, your subscription may be reduced or rejected if the offering is oversubscribed. To preserve your purchase priority, you must register the shares only in the name or names of eligible purchasers at the applicable date of eligibility. You may not add the names of others who were not eligible to purchase common stock in the offering on the applicable date of eligibility.

We may, in our sole discretion, reject orders received in the community offering either in whole or in part. For example, we may reject an order submitted by a person who we believe is making false representations or who we believe is attempting to violate, evade or circumvent the terms and conditions of the plans of reorganization and additional stock issuance. If your order is rejected in part, you cannot cancel the remainder of your order.

How Shares Can Be Paid For

In the offering, subscribers may pay for shares by:

| • | personal check, bank check or money order; or |

| • | authorizing Bank of New Orleans to withdraw money from the subscriber’s deposit account(s) maintained with Bank of New Orleans (we will waive any applicable penalties for early withdrawals from certificate of deposit accounts). |

Owners of self-directed IRAs may use the assets of such IRAs to purchase shares of common stock in the subscription and community offerings. Persons with IRAs maintained at Bank of New Orleans must have their accounts transferred to an unaffiliated institution or broker to purchase shares of common stock in the subscription and community offerings. Any interested parties wishing to use IRA funds for stock purchases are advised to contact the conversion center for additional information and allow sufficient time for the account to be transferred as required.

Bank of New Orleans cannot lend funds to anyone for the purpose of purchasing shares.

11

Table of Contents

Deadline for Orders of Stock

For those depositors of Bank of New Orleans with subscription rights who wish to purchase shares in the offering, a properly completed stock order form, together with payment for the shares, must be received by Bank of New Orleans no later than 4:00 p.m., Central time, on June 14, 2007, unless this deadline is extended by us. Subscribers may submit order forms by mail using the return envelope provided, by overnight courier to the indicated address on the order form, or by bringing their order forms to our main office, located at 1600 Veterans Memorial Boulevard, Metairie, Louisiana, during regular business hours. Stock order forms will not be accepted at any of our branch offices. Once submitted, orders are irrevocable unless the offering is terminated or extended beyond July 29, 2007.

Termination of the Offering

The subscription offering will expire at 4:00 p.m., Central time, on June 14, 2007. In the event that there is a community offering in addition to the subscription offering, we anticipate that such direct community offering would expire not later than 45 days subsequent to the expiration of the subscription offering. We may extend this expiration date without notice to you, until July 29, 2007, unless the Office of Thrift Supervision approves a later date. If the subscription offering and/or community offering extends beyond July 29, 2007, we will notify all subscribers and give them the opportunity to confirm, change or cancel their orders. We will promptly return funds with interest to any subscriber who does not respond to this notice. All further extensions, in the aggregate, may not last beyond June 27, 2009.

Your Subscription Rights Are Not Transferable

You may not assign or sell your subscription rights. Any transfer of subscription rights is prohibited by law. If you exercise subscription rights, you will be required to certify that you are purchasing shares solely for your own account and that you have no agreement or understanding regarding the sale or transfer of shares. We intend to pursue any and all legal and equitable remedies if we learn of the transfer of any subscription rights. We will reject orders that we determine to involve the transfer of subscription rights. With the exception of purchases through individual retirement accounts, Keogh accounts and 401(k) plan accounts, shares purchased in the subscription offering must be registered in the names of all depositors on the qualifying account(s). Deleting names of depositors or adding non-depositors or otherwise altering the form of beneficial ownership of a qualifying account will result in the loss of your subscription rights.

Conversion Center

If you have any questions regarding the offering or our reorganization, please call the conversion center at (504) 836-8160. The conversion center is open Monday through Friday, except bank holidays, from 10:00 a.m. to 4:00 p.m., Central time.

To ensure that each purchaser in the subscription and community offering receives a prospectus at least 48 hours before the expiration date of the subscription and community offering in accordance with federal law, no prospectus will be mailed any later than five days before the expiration date, sent via overnight delivery any later than three days before the expiration date or hand delivered any later than two days before the expiration date. Order forms will be distributed only when preceded or accompanied by a prospectus.

12

Table of Contents

You should consider carefully the following risk factors before purchasing Louisiana Bancorp common stock.

Risks Related to Our Business

Hurricane Katrina has resulted in a significant reduction of population in metropolitan New Orleans which may limit future business opportunities and which has adversely affected our ability to retain staff and increased our compensation costs.

Hurricane Katrina hit the greater New Orleans area in August 2005. The hurricane caused widespread property damage, required the relocation of an unprecedented number of residents and business operations, and severely disrupted normal economic activity in the impacted areas. Prior to Hurricane Katrina, the New Orleans SMSA was estimated to have a population of approximately 1.34 million, of which approximately 458,000 persons were estimated to live in the City of New Orleans. Post Katrina, the population for metropolitan New Orleans in December 2006 is estimated at approximately 1.03 million, a decline of approximately 300,000 residents. The population of the City of New Orleans was estimated at 200,500 people for December 2006. If the population of metropolitan New Orleans does not rebound, economic activity in the area may stagnate, which could limit our future business opportunities such as new loan originations. This could reduce our income in the future. The lower population levels also may adversely affect our ability to attract and retain deposits in a cost efficient manner. Consistent with the population decline, the number of our total employees has decreased from 74 at December 31, 2004 to 58 at December 31, 2006. As a result of the exodus from metropolitan New Orleans, the pool of available employees has shrunk dramatically. In addition, some employers have offered significantly higher wages in order to fill vacant positions. This has adversely affected our ability to attract and retain qualified personnel and has increased our employee costs as we have increased the compensation we pay in response to the market. While rebuilding efforts are underway, there is a great deal of uncertainty as to the economic climate for the New Orleans metropolitan area given the need to address the multitude of interdependent problems. As a result, significant uncertainty remains regarding the impact Hurricane Katrina will continue to have on the business, financial condition and results of operations of Bank of New Orleans.

Our Market Area is susceptible to additional hurricanes and tropical storms in the future which could adversely affect the banking business in southern Louisiana.

Our primary market area is Metairie, Louisiana and the greater New Orleans metropolitan area, an area which is susceptible to hurricanes and tropical storms. Basic services, such as water, gas, electricity, health care and the transportation network, as well as the flood prevention system, have been severely strained and may not withstand another hurricane or tropical storm. This could have a severe adverse effect on us as well as the banking business in southern Louisiana as a whole. Any new storm could have effects similar to Hurricane Katrina, which, among other things, resulted in a complete cessation of business in New Orleans for several weeks, affected loan portfolios by damaging properties pledged as collateral and impaired the ability of certain borrowers to repay their loans.

Metropolitan New Orleans may never fully recover from the effects of Hurricane Katrina which could have long-term adverse effects on the banking business in southern Louisiana.

The devastation of Hurricane Katrina on metropolitan New Orleans was pervasive. There is considerable uncertainty whether the area will fully recover. Businesses, including banking, have been adversely affected by the population decline, the continuing problems with basic services in the area, fundamental differences on how the rebuilding should proceed and the exodus of many firms. Tourism, which has been the largest single employment sector in metropolitan New Orleans, has declined dramatically since August 2005. If the area does not recover, it could have a long-term adverse effect on us as well as the banking business in southern Louisiana as a whole.

13

Table of Contents

There are increased risks involved with commercial real estate and construction lending activities.

Our lending activities include loans secured by commercial real estate and multi-family residential mortgage loans. In addition, we originate loans for the construction of residential and commercial use properties. We have increased our emphasis on originating commercial and multi-family real estate loans and construction loans in recent years, and such loans have increased as a proportion of our loan portfolio from 13.5% at December 31, 2002 to 37.0% at December 31, 2006. Commercial real estate, multi-family residential and construction lending generally is considered to involve a higher degree of risk than single-family residential lending due to a variety of factors, including generally larger loan balances, the dependency on successful completion or operation of the project for repayment, the difficulties in estimating construction costs and loan terms which often do not require full amortization of the loan over its term and, instead, provide for a balloon payment at stated maturity. As a result of the larger loan balances typically involved in these loans, an adverse development with respect to one loan or one credit relationship can expose us to greater risk of loss compared to an adverse development with respect to a one- to four-family residential mortgage loan. As of December 31, 2006, our 10 largest commercial real estate, multi-family residential and land loans had an aggregate outstanding balance of $19.4 million, or 56.9% of total commercial real estate, multi-family residential and land loans and 21.1% of our total loan portfolio at such date. In addition, our relatively recent emphasis on increasing our originations of commercial real estate and multi-family residential loans means that our portfolio of these loans is significantly weighted with loans which are not well seasoned, and thus, are generally perceived to be more susceptible to adverse economic conditions than older loans. Construction loans generally have a higher risk of loss than single-family residential mortgage loans due primarily to the critical nature of the initial estimates of a property’s value upon completion of construction compared to the estimated costs, including interest, of construction as well as other assumptions. If the estimates upon which construction loans are made prove to be inaccurate, we may be confronted with projects that, upon completion, have values which are below the loan amounts. The net proceeds from the offering will increase our capital and facilitate our ability to make larger commercial real estate and construction loans by increasing our internal loans to one borrower limits. We expect to make larger commercial real estate and construction loans and to increase our construction lending activity upon completion of the conversion and the offering.

We may not succeed at our plan to grow which could reduce future profitability.

We intend to grow our branch system by opening additional offices. In addition, we may seek to either acquire other financial institutions and/or branch offices. Bank of New Orleans has never acquired another banking institution and we cannot assure you that we will be able to grow through acquisitions or, if we do, successfully integrate other financial institutions or branch offices. Our ability to successfully acquire other institutions depends on our ability to identify, acquire and integrate such institutions into our franchise. Currently, we have no agreements or understandings with anyone regarding an acquisition. Our ability to grow organically by establishing newde novobranch offices depends on whether we can identify advantageous locations and generate new deposits and loans from those locations that will create an acceptable level of net income. In addition, our ability to grow will be dependent on our ability to hire additional qualified officers and staff. Following Hurricane Katrina and given the decline in population in metropolitan New Orleans, the pool of available, qualified job candidates is limited and no assurance can be given that we will be able to attract and hire the additional personnel needed for our growth plans. Our ability to grow also will be affected by local economic conditions. There continues to be considerable uncertainty regarding the long-term economic prospects for southern Louisiana after Hurricane Katrina. If the economy of New Orleans does not rebound, it could negatively affect our ability to originate new loans and generate deposits. Because of the continuing uncertainties regarding the New Orleans metropolitan area, we intend to focus our growth strategy in contiguous markets. However, we have never operated a branch office outside metropolitan New Orleans, and no assurance can be given that we can successfully implement our business plan in a different market area. There will be additional costs associated with any expansion of our branch network, and no assurance can be given that any new offices will be profitable. There also is a risk that, as we geographically expand our lending area, we may not be as successful in assessing the credit risks which are inherent in different markets. We cannot assure you that we will be successful in our plan to grow.

14

Table of Contents

The loss of our President and Chief Executive Officer or Chief Financial Officer could hurt our operations.

We rely heavily on our President and Chief Executive Officer, Lawrence J. LeBon, III, and our Chief Financial Officer, John LeBlanc. The loss of either of these executive officers could have an adverse effect on us. Mr. LeBon is central to virtually all aspects of our business operations and management. Mr. LeBlanc is critical to our financial reporting function, and he also works closely with Mr. LeBon on virtually all other aspects of our operations. In addition, as a small community bank, we have fewer management-level personnel who are in position to succeed and assume the responsibilities of either Messrs. LeBon or LeBlanc. We intend to enter into three-year employment agreements with Messrs. LeBon and LeBlanc. We do not maintain key man life insurance on either Mr. Le Bon or Mr. LeBlanc. For further discussion, see “Management.”

Our business is geographically concentrated in southern Louisiana, which makes us vulnerable in the local economy.

Most of our loans are to individuals and businesses located generally in southern Louisiana and, more particularly, metropolitan New Orleans. Regional economic conditions affect the demand for our products and services as well as the ability of our customers to repay loans. The concentration of our business operations in southern Louisiana makes us vulnerable to downturns in the local economy. Declines in local real estate values could adversely affect the value of property used as collateral for the loans we make. The regional economic outlook remains uncertain after Hurricane Katrina and no assurance can be given that, given the geographic concentration of our business, we will not suffer from future adverse developments in the region. The region is susceptible to hurricanes and tropical storms. Any new hurricanes or storms could severely test the infrastructure of the markets we operate in, negatively affect the local economy or disrupt our operations, which would have an adverse effect on our business and results of operations. In addition, certain property insurers operating in metropolitan New Orleans have indicated their intention to cease writing policies on properties in the market or have dramatically increased insurance premiums. In addition, the inventory of unsold housing in the region has been increasing in recent periods. These factors could depress market values, reduce the value of the collateral securing our loans and may adversely affect our ability to originate new real estate loans in New Orleans.

Changes in interest rates could have a material adverse effect on our operations.

The operations of financial institutions such as us are dependent to a large extent on net interest income, which is the difference between the interest income earned on interest-earning assets such as loans and investment securities and the interest expense paid on interest-bearing liabilities such as deposits and borrowings. Changes in the general level of interest rates can affect our net interest income by affecting the difference between the weighted average yield earned on our interest-earning assets and the weighted average rate paid on our interest-bearing liabilities, or interest rate spread, and the average life of our interest-earning assets and interest-bearing liabilities. Changes in interest rates also can affect our ability to originate loans; the value of our interest-earning assets and our ability to realize gains from the sale of such assets; our ability to obtain and retain deposits in competition with other available investment alternatives; the ability of our borrowers to repay adjustable or variable rate loans; and the fair value of the derivatives carried on our balance sheet, derivative hedge effectiveness testing and the amount of ineffectiveness recognized in our earnings. Interest rates are highly sensitive to many factors, including governmental monetary policies, domestic and international economic and political conditions and other factors beyond our control. Although we believe that the estimated maturities of our interest-earning assets currently are well balanced in relation to the estimated maturities of our interest-bearing liabilities (which involves various estimates as to how changes in the general level of interest rates will impact these assets and liabilities), there can be no assurance that our profitability would not be adversely affected during any period of changes in interest rates. Our net interest margin, which is net interest income as a percentage of average interest-earning assets, declined to 2.97% for the quarter ended March 31, 2007 compared to 3.07% for the year ended December 31, 2006. In light of the continuing flat yield curve and that our cost of funds has been increasing as we have seen an outflow of certain lower costing deposits received after Hurricane Katrina, we may experience continued compression of our net interest margin which could reduce net income in future periods.

15

Table of Contents

Our results of operations are significantly dependent on economic conditions and related uncertainties.

The operations of savings associations are affected, directly and indirectly, by domestic and international economic and political conditions and by governmental monetary and fiscal policies. Conditions such as inflation, recession, unemployment, volatile interest rates, real estate values, government monetary policy, international conflicts, the actions of terrorists and other factors beyond our control may adversely affect our results of operations. Changes in interest rates, in particular, could adversely affect our net interest income and have a number of other adverse effects on our operations. Adverse economic conditions also could result in an increase in loan delinquencies, foreclosures and nonperforming assets and a decrease in the value of the property or other collateral which secures our loans, all of which could adversely affect our results of operations. We are particularly sensitive to changes in economic conditions and related uncertainties in the metropolitan New Orleans area because we derive the vast majority of our loans, deposits and other business from this area. Accordingly, we remain subject to the risks associated with prolonged declines in our local economy.

Our allowance for losses on loans may not be adequate to cover probable losses.

We have established an allowance for loan losses which we believe is adequate to offset probable losses on our existing loans. There can be no assurance that any future declines in real estate market conditions, general economic conditions or changes in regulatory policies will not require us to increase our allowance for loan losses, which would adversely affect our results of operations.

We are subject to extensive regulation which could adversely affect our business and operations.

We are subject to extensive federal governmental supervision and regulation, which are intended primarily for the protection of depositors. In addition, we are subject to changes in federal and state laws, as well as changes in regulations, governmental policies and accounting principles. The effects of any such potential changes cannot be predicted but could adversely affect the business and our operations in the future.

We face strong competition which may adversely affect our profitability.

We are subject to vigorous competition in all aspects and areas of our business from banks and other financial institutions, including savings and loan associations, savings banks, finance companies, credit unions and other providers of financial services, such as money market mutual funds, brokerage firms, consumer finance companies and insurance companies. We also compete with non-financial institutions, including retail stores that maintain their own credit programs and governmental agencies that make available low cost or guaranteed loans to certain borrowers. Certain of our competitors are larger financial institutions with substantially greater resources, lending limits, larger branch systems and a wider array of commercial banking services. Competition from both bank and non-bank organizations will continue.

Our ability to successfully compete may be reduced if we are unable to make technological advances.

The banking industry is experiencing rapid changes in technology. In addition to improving customer services, effective use of technology increases efficiency and enables financial institutions to reduce costs. As a result, our future success will depend in part on our ability to address our customers’ needs by using technology. We cannot assure you that we will be able to effectively develop new technology-driven products and services or be successful in marketing these products to our customers. Many of our competitors have far greater resources than we have to invest in technology.

Risks Related to this Offering

Additional Expenses Following the Offering From New Equity Benefit Plans Will Adversely Affect Our Net Income.

Following the offering, we will recognize additional annual employee compensation and benefit expenses stemming from options and shares granted to employees, directors and executives under new benefit plans. These

16

Table of Contents

additional expenses will adversely affect our net income. We cannot determine the actual amount of these new stock-related compensation and benefit expenses at this time because applicable accounting practices generally require that they be based on the fair market value of the options or shares of common stock at the date of the grant; however, we expect them to be significant. We will recognize expenses for our employee stock ownership plan when shares are committed to be released to participants’ accounts and will recognize expenses for restricted stock awards and stock options generally over the vesting period of awards made to recipients. These benefit expenses in the first year following the offering have been estimated to be approximately $989,000 at the maximum of the offering range as set forth in the pro forma financial information under “Pro Forma Data” assuming the $10.00 per share purchase price as fair market value. Actual expenses, however, may be higher or lower, depending on the price of our common stock at that time. For further discussion of these plans, see “Management – New Stock Benefit Plans.”

Our Return on Equity May Negatively Impact Our Stock Price.

Return on equity, which equals net income divided by average equity, is a ratio used by many investors to compare the performance of a particular company with other companies. Bank of New Orleans’ return on average equity was 7.2% for the year ended December 31, 2006. This is lower than returns on equity for many comparable publicly traded financial institutions. We expect our return on equity ratio will not increase substantially, due in part to our increased capital level upon completion of the offering. Consequently, you should not expect a competitive return on equity in the near future. Failure to attain a competitive return on equity ratio may make an investment in our common stock unattractive to some investors which might cause our common stock to trade at lower prices than comparable companies with higher returns on equity. The net proceeds from the stock offering, which may be as much as $68.6 million, will significantly increase our equity. On a pro forma basis and based on net income for the year ended December 31, 2006, our return on equity ratio, assuming shares are sold at the maximum of the offering range, would be approximately 2.7%. Based on trailing 12-month data for the most recent publicly available financial information (December 31, 2006), the 12 companies comprising our peer group in the independent appraisal prepared by Feldman Financial Advisors and all publicly traded savings banks had average ratios of returns on equity of 5.44% and 5.41%, respectively.

We Have Broad Discretion in Allocating the Proceeds of the Offering.

We intend to contribute 50% of the net proceeds of the offering to Bank of New Orleans. Louisiana Bancorp may use the portion of the proceeds that it retains to, among other things, invest in securities, pay cash dividends or repurchase shares of common stock, subject to regulatory restriction. Bank of New Orleans initially intends to use the net proceeds it retains to originate new loans and to purchase investment and mortgage-backed securities.In the future, Bank of New Orleans may use the portion of the proceeds that it receives to open new branches, invest in securities and expand its business activities. Louisiana Bancorp and Bank of New Orleans may also use the proceeds of the offering to diversify their business and acquire other companies, although we have no specific plans to do so at this time. We have not allocated specific amounts of proceeds for any of these purposes, and we will have significant flexibility in determining how much of the net proceeds we apply to different uses and the timing of such applications. There is a risk that we may fail to effectively use the net proceeds which could have a negative effect on our future profitability ratios.

Our Employee Stock Benefit Plans Will Be Dilutive.

If the offering is completed and shareholders subsequently approve a stock recognition and retention plan and a stock option plan, we will allocate stock to our officers, employees and directors through these plans. If the shares for the stock recognition and retention plan are issued from our authorized but unissued stock, the ownership percentage of outstanding shares of Louisiana Bancorp would be diluted by approximately 3.8%. However, it is our intention to purchase shares of our common stock in the open market to fund the stock recognition and retention plan. Assuming the shares of our common stock to be awarded under the stock recognition and retention plan are purchased at a price equal to the offering price in the offering, the reduction to shareholders’ equity from the stock recognition and retention plan would be between $1.8 million and $2.8 million at the minimum and the maximum, as adjusted, of the offering range. The ownership percentage of Louisiana Bancorp shareholders would also decrease by approximately 9.1% if all potential stock options under our proposed stock option plan are exercised and are

17

Table of Contents

filled using shares issued from authorized but unissued stock, assuming the offering closes at the maximum of the offering range. See “Pro Forma Data” for data on the dilutive effect of the stock recognition and retention plan and the stock option plan and “Management – New Stock Benefit Plans” for a description of the plans.

Our Stock Price May Decline When Trading Commences.

We cannot guarantee that if you purchase shares in the offering that you will be able to sell them at or above the $10.00 purchase price. The trading price of the common stock will be determined by the marketplace, and will be influenced by many factors outside of our control, including prevailing interest rates, investor perceptions, securities analyst research reports and general industry, geopolitical and economic conditions. Publicly traded stock, including stocks of financial institutions, often experience substantial market price volatility. These market fluctuations might not be related to the operating performance of particular companies whose shares are traded.

There May Be a Limited Market For Our Common Stock, Which May Adversely Affect Our Stock Price.

Although we have applied to have our shares of common stock traded on the Nasdaq Global Market, there is no guarantee that the shares will be actively traded. If an active trading market for our common stock does not develop, you may not be able to sell all of your shares of common stock in an efficient manner and the sale of a large number of shares at one time could temporarily depress the market price. There also may be a wide spread between the bid and asked price for our common stock. When there is a wide spread between the bid and asked price, the price at which you may be able to sell our common stock may be significantly lower than the price at which you could buy it at that time.

We Intend to Remain Independent Which May Mean You Will Not Receive a Premium for Your Common Stock.

We intend to remain independent for the foreseeable future. Because we do not plan on seeking possible acquirors, it is unlikely that we will be acquired in the foreseeable future. Accordingly, you should not purchase our common stock with any expectation that a takeover premium will be paid to you in the near term.

Our Stock Value May Suffer from Anti-Takeover Provisions That May Impede Potential Takeovers That Management Opposes.

Provisions in our corporate documents, as well as certain federal regulations, may make it difficult and expensive to pursue a tender offer, change in control or takeover attempt that our board of directors opposes. As a result, our shareholders may not have an opportunity to participate in such a transaction, and the trading price of our stock may not rise to the level of other institutions that are more vulnerable to hostile takeovers. Anti-takeover provisions contained in our corporate documents include:

| • | restrictions on acquiring more than 10% of our common stock by any person and limitations on voting rights; |

| • | the election of members of the board of directors to staggered three-year terms; |

| • | the absence of cumulative voting by shareholders in the election of directors; |

| • | provisions restricting the calling of special meetings of shareholders; and |

| • | our ability to issue preferred stock and additional shares of common stock without shareholder approval. |

See “Restrictions on Acquisition of Louisiana Bancorp and Bank of New Orleans and Related Anti-Takeover Provisions” for a description of anti-takeover provisions in our corporate documents and federal regulations.

18

Table of Contents

This document contains forward-looking statements, which can be identified by the use of such words as “estimate,” “project,” “believe,” “intend,” “anticipate,” “plan,” “seek,” “expect” and similar expressions. These forward-looking statements include:

| • | statements of goals, intentions and expectations; |

| • | statements regarding prospects and business strategy; |

| • | statements regarding asset quality and market risk; and |

| • | estimates of future costs, benefits and results. |

These forward-looking statements are subject to significant risks, assumptions and uncertainties, including, among other things, the factors discussed under the heading “Risk Factors” beginning at page 13 that could affect the actual outcome of future events.

Because of these and other uncertainties, our actual future results may be materially different from the results indicated by these forward-looking statements and you should not rely on such statements.

The following table shows how we intend to use the net proceeds of the offering. The actual net proceeds will depend on the number of shares of common stock sold in the offering and the expenses incurred in connection with the offering. Payments for shares made through withdrawals from deposit accounts at Bank of New Orleans will reduce Bank of New Orleans’ deposits and will not result in the receipt of new funds for investment. See “Pro Forma Data” for the assumptions used to arrive at these amounts.

Minimum of Offering Range | Midpoint of Offering Range | Maximum of Offering Range | 15% Above Maximum of Offering Range | |||||||||||||||||||||

| 4,505,000 Shares at $10.00 Per Share | Percent of Net Proceeds | 5,300,000 Shares at $10.00 Per Share | Percent of Net Proceeds | 6,095,000 Shares at $10.00 Per Share | Percent of Net Proceeds | 7,009,250 Shares at $10.00 Per Share | Percent of Net Proceeds | |||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||

Offering proceeds | $ | 45,050,000 | 103.0 | % | $ | 53,000,000 | 102.6 | % | $ | 60,950,000 | 102.4 | % | $ | 70,092,500 | 102.2 | % | ||||||||