UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811‑22044

Eaton Vance Risk-Managed Diversified Equity Income Fund

(Exact Name of Registrant as Specified in Charter)

One Post Office Square, Boston, Massachusetts 02109

(Address of Principal Executive Offices)

Deidre E. Walsh

One Post Office Square, Boston, Massachusetts 02109

(Name and Address of Agent for Services)

(617) 482‑8260

(Registrant’s Telephone Number)

December 31

Date of Fiscal Year End

December 31, 2024

Date of Reporting Period

Item 1. Reports to Stockholders

Eaton Vance

Risk-Managed Diversified Equity Income Fund (ETJ)

Annual Report

December 31, 2024

Commodity Futures Trading Commission Registration. The Commodity Futures Trading Commission (“CFTC”) has adopted regulations that subject registered investment companies and advisers to regulation by the CFTC if a fund invests more than a prescribed level of its assets in certain CFTC-regulated instruments (including futures, certain options and swap agreements) or markets itself as providing investment exposure to such instruments. The investment adviser has claimed an exclusion from the definition of “commodity pool operator” under the Commodity Exchange Act with respect to its management of the Fund. Accordingly, neither the Fund nor the adviser with respect to the operation of the Fund is subject to CFTC regulation. Because of its management of other strategies, the Fund’s adviser is registered with the CFTC as a commodity pool operator. The adviser is also registered as a commodity trading advisor.

Managed Distribution Plan. Pursuant to an exemptive order issued by the Securities and Exchange Commission (Order), the Fund is authorized to distribute long-term capital gains to shareholders more frequently than once per year. Pursuant to the Order, the Fund’s Board of Trustees approved a Managed Distribution Plan (MDP) pursuant to which the Fund makes monthly cash distributions to common shareholders, stated in terms of a fixed amount per common share.

The Fund currently distributes monthly cash distributions equal to $0.0651 per share in accordance with the MDP. You should not draw any conclusions about the Fund’s investment performance from the amount of these distributions or from the terms of the MDP. The MDP will be subject to regular periodic review by the Fund’s Board of Trustees and the Board may amend or terminate the MDP at any time without prior notice to Fund shareholders. However, at this time there are no reasonably foreseeable circumstances that might cause the termination of the MDP.

The Fund may distribute more than its net investment income and net realized capital gains and, therefore, a distribution may include a return of capital. A return of capital distribution does not necessarily reflect the Fund’s investment performance and should not be confused with “yield” or “income.” With each distribution, the Fund will issue a notice to shareholders and a press release containing information about the amount and sources of the distribution and other related information. The amounts and sources of distributions contained in the notice and press release are only estimates and are not provided for tax purposes. The amounts and sources of the Fund’s distributions for tax purposes will be reported to shareholders on Form 1099-DIV for each calendar year.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

Annual Report December 31, 2024

Eaton Vance

Risk-Managed Diversified Equity Income Fund

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

Management’s Discussion of Fund Performance†

Economic and Market Conditions

For U.S. equity investors, the 12-month period ended December 31, 2024, was a banner year. The S&P 500® Index returned 25.02% -- the broad-market benchmark’s second year in a row above 20% -- as U.S. equities outpaced stocks in most areas of the world. The signal event of the period was the start of long-anticipated federal fund rate cuts by the U.S. Federal Reserve (the Fed) in September 2024 -- the central bank’s first reduction since it began raising rates in 2022 to quell inflation.

As the period opened in January 2024, U.S. stocks were in the midst of a rally that had begun in November 2023. Rally drivers included strong corporate profits, excitement over the nascent artificial intelligence (AI) boom, strong hiring, robust consumer spending, and confidence that the Fed was done raising interest rates.

In April 2024, however, stock prices retreated after the U.S. Labor Department reported three straight months of persistent inflation. That changed in May when the Personal Consumption Expenditures Price Index (PCE) -- the Fed’s preferred inflation gauge -- showed inflation had fallen to 2.7% year-over-year. In response, stocks erased April’s losses and the U.S. equity rally resumed.

In late July and early August 2024, stock prices dipped briefly as the Fed failed to cut interest rates and July job creation came in below expectations. From August 8 through most of October, equities rallied again, encouraged by additional decreases in the PCE.

On September 18, 2024, the Fed announced a half-point interest-rate cut, adding fuel to the U.S. stock rally. Late October brought a pause in the rally as investors fretted over weak third-quarter earnings and uncertainties about the upcoming U.S. presidential election. In mid-November, however, equities enjoyed a post-election bump that lasted through mid-December, buoyed by the prospects of deregulation and lower corporate taxes under a new Trump administration.

On December 18, 2024, the Fed brought the rally to a halt. Although the central bank delivered an expected quarter-point rate cut, it surprised investors by reducing its projected 2025 rate cuts from four to two. After inflation rose modestly in October and November, Fed Chair Jerome Powell noted that “For additional cuts, we’re going to be looking for further progress on inflation.” In response, stock prices largely declined during the final weeks of the period, although most major U.S. indexes delivered strong performance for the period as a whole.

Fund Performance

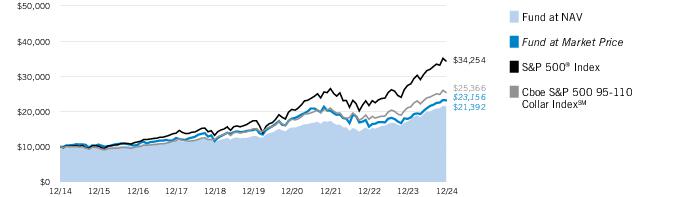

For the 12-month period ended December 31, 2024, Eaton Vance Risk-Managed Diversified Equity Income Fund (the Fund) returned 24.90% at net asset value of its common shares (NAV), underperforming its equity benchmark, the S&P 500® Index (the Index), which returned 25.02%; and outperforming its options benchmark, the Cboe S&P 500 95-110 Collar IndexSM, which returned 20.51%.

The Fund’s collared-options strategy (the options strategy) was the largest detractor from Fund performance versus the Index during the period. The options strategy may be beneficial during times of market weakness and higher volatility, but may detract from performance relative to the Index during periods of market strength, since it seeks to buy downside protection at the expense of upside potential.

For much of the period, the Index moved higher with a few sudden pullbacks due to changing market events. Market volatility -- as measured by the Cboe Volatility Index®, or VIX -- was largely subdued during the first part of the period. However, in August 2024, equity markets experienced a historic spike in volatility, with a market sell-off attributed to a surprise interest-rate hike by the Bank of Japan. While the Fund’s downside protection was helpful during this market pullback, the stock market’s overall strength during the period created net losses within the Fund’s options strategy.

Meanwhile, the Fund’s common stock portfolio outperformed the Index during the period, contributing to Index-relative returns. On an individual stock basis, the largest contributor to performance versus the Index was an overweight position in NVIDIA Corp. (NVIDIA), a leading supplier of graphics processing unit microchips that have helped power the artificial intelligence boom. NVIDIA’s share price more than doubled during the period as the chipmaker reported strong earnings and profits.

On a sector basis, stock selections and an overweight position in the information technology sector, stock selections in the health care sector, and stock selections and an underweight position in the consumer staples sector all contributed to Fund performance versus the Index during the period.

In contrast, the largest individual stock detractor from performance relative to the Index was an overweight position in health insurance provider Elevance Health Inc. (Elevance). The company’s share price fell during the period amid a decline in subscribers and higher-than-projected costs in its Medicare business. By period-end, Elevance was sold from the Fund.

On a sector basis, stock selections in the energy sector detracted from Fund performance versus the Index during the period.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees and other expenses by determining the percentage change in net asset value (NAV) or market price (as applicable) with all distributions reinvested in accordance with the Fund’s Dividend Reinvestment Plan. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Performance at market price will differ from performance at NAV due to variations in the Fund’s market price versus NAV, which may reflect factors such as fluctuations in supply and demand for Fund shares, changes in Fund distributions, shifting market expectations for the Fund’s future returns and distribution rates, and other considerations affecting the trading prices of closed-end funds. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Risk-Managed Diversified Equity Income Fund

December 31, 2024

Management’s Discussion of Fund Performance† — continued

Fund Distributions

Pursuant to an exemptive order issued by the Securities and Exchange Commission (the Order), the Fund is authorized to distribute long-term capital gains to shareholders more frequently than once per year. Pursuant to the Order, the Fund’s Board of Trustees approved a Managed Distribution Plan (MDP) pursuant to which the Fund makes monthly cash distributions to common shareholders. The Fund’s MDP had no effect on the Fund’s investment strategy during the most recent fiscal year and is not expected to have an effect in future periods, but distributions in excess of Fund returns will cause its per share NAV to erode. Investors should not draw any conclusions about the Fund’s investment performance from the amount of its distribution or from the terms of its MDP.

For the period from January 1, 2024 to March 31, 2024, the Fund made monthly distributions of $0.0579 per share and, for the period from April 1, 2024 to December 31, 2024, the Fund made monthly distributions of $0.0651 per share. The Fund’s distributions may be comprised of amounts characterized for federal income tax purposes as qualified and non-qualified ordinary dividends, capital gains and non-dividend distributions, also known as return of capital distributions. The federal income tax character of distributions is determined after the end of the calendar year and reported to shareholders on the Internal Revenue Service’s form 1099-DIV. For additional information, see Note 2 in the Notes to Financial Statements herein.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees and other expenses by determining the percentage change in net asset value (NAV) or market price (as applicable) with all distributions reinvested in accordance with the Fund’s Dividend Reinvestment Plan. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Performance at market price will differ from performance at NAV due to variations in the Fund’s market price versus NAV, which may reflect factors such as fluctuations in supply and demand for Fund shares, changes in Fund distributions, shifting market expectations for the Fund’s future returns and distribution rates, and other considerations affecting the trading prices of closed-end funds. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

Performance

Portfolio Manager(s) Charles B. Gaffney and Douglas R. Rogers, CFA, CMT

| % Average Annual Total Returns1 | Inception Date | One Year | Five Years | Ten Years |

| Fund at NAV | 07/31/2007 | 24.90% | 10.44% | 7.89% |

| Fund at Market Price | — | 29.42 | 9.49 | 8.75 |

|

| S&P 500® Index | — | 25.02% | 14.51% | 13.09% |

| Cboe S&P 500 95-110 Collar IndexSM | — | 20.51 | 10.93 | 9.75 |

| % Premium/Discount to NAV2 | |

| As of period end | (4.32)% |

| Distributions3 | |

| Total Distributions per share for the period | $0.76 |

| Distribution Rate at NAV | 8.03% |

| Distribution Rate at Market Price | 8.39 |

Growth of $10,000

This graph shows the change in value of a hypothetical investment of $10,000 in the Fund for the period indicated. For comparison, the same investment is shown in the indicated index.

See Endnotes and Additional Disclosures in this report.

Past performance is no guarantee of future results. Returns are historical and are calculated net of management fees and other expenses by determining the percentage change in net asset value (NAV) or market price (as applicable) with all distributions reinvested in accordance with the Fund’s Dividend Reinvestment Plan. Furthermore, returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Performance at market price will differ from performance at NAV due to variations in the Fund’s market price versus NAV, which may reflect factors such as fluctuations in supply and demand for Fund shares, changes in Fund distributions, shifting market expectations for the Fund’s future returns and distribution rates, and other considerations affecting the trading prices of closed-end funds. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance for periods less than or equal to one year is cumulative. Performance is for the stated time period only; due to market volatility, current Fund performance may be lower or higher than the quoted return. For performance as of the most recent month-end, please refer to eatonvance.com.

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

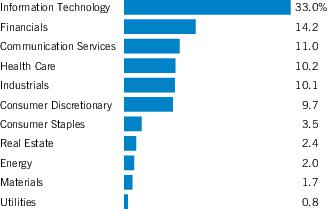

| Sector Allocation (% of total investments)1 |

| Top 10 Holdings (% of total investments)1 |

| Apple, Inc. | 7.6% |

| Microsoft Corp. | 7.5 |

| NVIDIA Corp. | 7.3 |

| Amazon.com, Inc. | 5.3 |

| Alphabet, Inc., Class C | 4.4 |

| Broadcom, Inc. | 3.6 |

| Meta Platforms, Inc., Class A | 3.1 |

| Eli Lilly & Co. | 2.3 |

| Visa, Inc., Class A | 2.1 |

| ConocoPhillips | 2.0 |

| Total | 45.2% |

Footnotes:

| 1 | Depictions do not reflect the Fund’s option positions. Excludes cash and cash equivalents. |

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

The Fund's Investment Objectives, Principal Strategies and Principal Risks‡

Investment Objectives. The Fund’s primary investment objective is to provide current income and gains, with a secondary objective of capital appreciation. In pursuing its investment objectives, the Fund evaluates returns on an after-tax basis, seeking to minimize and defer shareholder federal income taxes.

Principal Strategies. Under normal market conditions, the Fund’s investment program consists primarily of owning a diversified portfolio of common stocks and employing a variety of options strategies. The Fund seeks to earn high levels of tax-advantaged income and gains by (1) investing in stocks that pay dividends that qualify for favorable federal income tax treatment, (2) writing (selling) put options on individual stocks deemed attractive for purchase, and/or (3) writing (selling) stock index call options with respect to a portion of its common stock portfolio value. To reduce the Fund’s risk of loss due to a decline in the value of the general equity market, the Fund intends to purchase index put options with respect to a substantial portion of the value of its common stock holdings and stocks subject to written put options.

Under normal market conditions, the Fund invests at least 80% of its total assets in a combination of (1) dividend-paying common stocks, (2) common stocks the value of which is subject to written put options on individual stocks, and (3) common stocks the value of which is subject to written index call options. In addition, under normal market conditions, the Fund purchases index put options with respect to at least 80% of the value of its investments in common stocks. The Fund may consider investments in stocks that pay dividends that qualify for federal income taxation at rates applicable to long-term capital gains. The Fund generally intends to buy put options and write call options on one or more broad-based stock indices that the investment adviser believes collectively approximate the characteristics of its common stock portfolio (or that portion of its portfolio against which options are purchased and written). The Fund intends to buy put options and write call options primarily on the S&P 500® Index (the “S&P 500”), and may also buy put options and write call options on other domestic and foreign stock indices. The Fund’s current options strategy consists of purchasing out-of-the-money S&P 500 put options and selling out-of-the-money S&P 500 call options on all or substantially all of the value of the Fund’s common stock portfolio. Purchasing index put options provides protection against loss of principal value during periods of market weakness and selling index call options generates premium income. The Fund generally intends to purchase short-dated (generally 28-day) index put options and sell index call options of the same term, staggering roll dates across the options portfolio. The indices on which the Fund buys put options and writes call options may vary as a result of changes in the availability and liquidity of various listed index options, changes in stock portfolio holdings, the Adviser’s evaluation of equity market conditions and other factors. The buying of index put options will reduce the Fund’s cash available for distribution from other sources, including from selling put options on individual stocks and index call options.

The Fund invests primarily in common stocks of United States issuers. The Fund may invest up to 40% of its total assets in securities of foreign issuers, including securities evidenced by American Depositary Receipts (“ADRs”), Global Depositary Receipts (“GDRs”) and European Depositary Receipts (“EDRs”). The Fund may invest up to 5% of its total assets in securities of emerging market issuers. The Fund expects that its assets will normally be invested across a broad range of industries and market sectors. The Fund may not invest 25% or more of its total assets in the securities of issuers in any single industry. Eaton Vance generally considers mid-capitalization companies to be those companies having market capitalizations within the range of capitalizations for the S&P MidCap 400® Index (the “S&P MidCap 400® ”). As of December 31, 2024, the median market capitalization of companies in the S&P MidCap 400® was approximately $7 billion. Market capitalizations of companies within the S&P MidCap 400® are subject to change.

During unusual market circumstances, the Fund may invest up to 100% of assets in cash or cash equivalents temporarily, which may be inconsistent with the Fund’s investment objective and other policies.

Principal Risks

Market Discount Risk. As with any security, the market value of the common shares may increase or decrease from the amount initially paid for the common shares. The Fund’s common shares have traded both at a premium and at a discount relative to NAV. The shares of closed-end management investment companies frequently trade at a discount from their NAV. This is a risk separate and distinct from the risk that the Fund’s NAV may decrease.

Investment and Market Risk. An investment in common shares is subject to investment risk, including the possible loss of the entire principal amount invested. An investment in common shares represents an indirect investment in the securities owned by the Fund, which are generally traded on a securities exchange or in the over-the-counter markets. The value of these securities, like other market investments, may move up or down, sometimes rapidly and unpredictably. Because the Fund may sell stock index call options on a portion of its common stock portfolio value, the Fund’s appreciation potential from equity market performance may be more limited than if the Fund did not engage in selling stock index call options. Because the Fund may sell put options on individual stocks, the Fund’s exposure to loss from a decline in the value of such stocks may increase. To the extent that the individual stocks held by the Fund and/or the stocks subject to written put options decrease in value more than the index or indices on which the Fund has purchased put options, the strategy of purchasing index put options will provide only limited protection with respect to the value of the Fund’s assets and may result in worse performance for the Fund than if it did not buy index put options. The common shares at any point in time may be worth less than the original investment, even after taking into account any reinvestment of distributions.

The value of investments held by the Fund may increase or decrease in response to social, economic, political, financial, public health crises or other disruptive events (whether real, expected or perceived) in the U.S. and global markets and include events such as war, natural disasters, epidemics and pandemics, terrorism, conflicts and social unrest. These events may negatively impact broad segments of businesses and populations and may exacerbate pre-existing risks to the Fund. The frequency and magnitude of resulting changes in the value of the Fund’s investments cannot be predicted. Certain securities and other investments held by the Fund may experience increased volatility, illiquidity, or other potentially adverse effects in reaction to changing

See Endnotes and Additional Disclosures in this report.

6

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

The Fund's Investment Objectives, Principal Strategies and Principal Risks‡ — continued

market conditions. Monetary and/or fiscal actions taken by U.S. or foreign governments to stimulate or stabilize the global economy may not be effective and could lead to high market volatility. No active trading market may exist for certain investments held by the Fund, which may impair the ability of the Fund to sell or to realize the current valuation of such investments in the event of the need to liquidate such assets.

Issuer Risk. The value of securities held by the Fund may decline for a number of reasons that directly relate to the issuer, such as management performance, financial leverage and reduced demand for the issuer’s goods and services.

Equity Securities Risk. The value of equity securities and related instruments may decline in response to adverse changes in the economy or the economic outlook; deterioration in investor sentiment; interest rate, currency, and commodity price fluctuations; adverse geopolitical, social or environmental developments; issuer and sector-specific considerations; unexpected trading activity among retail investors; or other factors. Market conditions may affect certain types of stocks to a greater extent than other types of stocks. If the stock market declines in value, the value of the Fund’s equity securities will also likely decline. Although prices can rebound, there is no assurance that values will return to previous levels.

Limitations on Equity Market Risk Management Strategy. To manage the risk of a decline in the value of the general equity market, the Fund purchases index put options on a substantial portion of the value of its common stock holdings. As the purchaser of an index put option, the Fund would pay to the writer (seller) of the option cash (the premium), and the Fund has the right to receive from the seller the amount by which the cash value of the index is below the exercise price as of the valuation date of the option. If the Fund exercises the index put option, the seller would pay the Fund the difference between the exercise price and the value of the index. There are a number of limitations on the extent to which common shareholders of the Fund may benefit from this risk management strategy.

First, holding an index put option generally provides a hedge against a decline in the applicable index to levels below the exercise price on the option. A decline in the index to a level above the exercise price would result in the option expiring worthless if held until expiration. Generally, the Fund intends to buy index put options that are “out-of-the-money” (i.e., the exercise price generally is below the current level of the applicable index when the option is purchased). Options that are more “out-of-the-money” provide the Fund with less protection against a decline in the applicable index.

Second, there is a risk that the value of the stock indices subject to purchased put options will not correlate with the value of the Fund’s portfolio holdings. The Fund intends to buy put options on one or more broad-based stock indices that the Adviser believes collectively approximate the characteristics of the Fund’s common stock portfolio (or that portion of its portfolio against which put options are acquired). The Fund will not, however, hold stocks that fully replicate the indices on which it buys put options. Due to tax considerations, the Fund intends to generally limit the overlap between its stock holdings (and any subset thereof) and each index on which it has outstanding options positions to less than 70% on an ongoing basis. The Fund’s stock holdings will normally include stocks not included in the indices on which it buys put options. Accordingly, the value of the indices may remain flat or increase in value at times when the Fund’s portfolio holdings are decreasing in value. Similarly, the indices may decrease in value but to a lesser extent than the Fund’s portfolio holdings. In such cases, the index put options would provide only a limited hedge against a decline in the value of the Fund’s portfolio holdings and may result in worse performance for the Fund than if it did not buy index put options. The use of index put options cannot serve as a complete hedge since the price movement of the indices underlying the options will not necessarily follow the price movements of the Fund’s portfolio holdings. Correlation risks are also presented in connection with the Fund’s selling of put options on individual stocks and purchasing index puts to hedge the associated increase in market risk. Purchasing index put options with respect to single stock put options written does not protect the Fund against the risk that the stocks against which put options are written decrease in value relative to the index on which put options are purchased and may result in greater costs and losses to the Fund than a strategy that does not involve such hedging.

Third, the Fund may in certain circumstances hold stock index put options with respect to only a portion of the value of its common stock holdings, subject to the condition that, under normal market conditions, the Fund will hold index put options with respect to at least 80% of the value of its investments in common stocks. The portion of the Fund’s portfolio value against which index put options are not acquired will not benefit from this risk management strategy.

Index put options can be highly volatile instruments. This may cause options positions held to react to market changes differently than the Fund’s portfolio securities and stocks subject to written put options. A put option acquired by the Fund and not sold prior to expiration will expire worthless if the price of the index at expiration exceeds the exercise price of the option, thereby causing the Fund to lose its entire investment in the option. If restrictions on exercise were imposed, the Fund might be unable to exercise an option it had purchased. If the Fund were unable to close out an option that it had purchased, it would have to exercise the option in order to realize any profit or the option may expire worthless.

Option Strategy Risk. The Fund’s option strategy seeks to take advantage of, and its effectiveness is dependent on, a general excess of option price implied volatilities for the S&P 500 over realized index volatilities. This market observation is often attributed to an excess of natural buyers over natural sellers of S&P 500 options. There can be no assurance that this imbalance will apply in the future over specific periods or generally. It is possible that the imbalance could decrease or be eliminated by actions of investors, including the Fund, that employ strategies seeking to take advantage of the imbalance, which could have an adverse effect on the Fund’s ability to achieve its investment objective.

Risk of Selling Index Call Options. The purchaser of an index call option has the right to any appreciation in the value of the index over the exercise price of the call option as of the valuation date of the option. Because their exercise is settled in cash, sellers of index call options such as the Fund cannot provide in advance for their potential settlement obligations by acquiring and holding the underlying securities. The Fund intends to mitigate the risks of its options activities by holding a diversified portfolio of stocks that the Fund’s investment adviser believes collectively approximate the characteristics of the

See Endnotes and Additional Disclosures in this report.

7

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

The Fund's Investment Objectives, Principal Strategies and Principal Risks‡ — continued

indices on which options are written. The Fund will not, however, hold stocks that fully replicate the indices on which it writes call options. Due to tax considerations, the Fund intends to limit the overlap between its stock holdings (and any subset thereof) and each index on which it has outstanding options positions to less than 70% on an ongoing basis. The Fund’s stock holdings will normally include stocks not included in the indices on which it writes call options. Consequently, the Fund bears the risk that the performance of its stock portfolio will vary from the performance of the indices on which it writes call options. As the writer of index call options, the Fund will forgo, during the option’s life, the opportunity to profit from increases in the value of the applicable index above the sum of the option premium received and the exercise price of the call option, but retains the risk of loss, minus the option premium received, should the value of the applicable index decline. When a call option is exercised, the Fund will be required to deliver an amount of cash determined by the excess of the value of the applicable index at contract termination over the exercise price of the option. If the value of the index increases over the option’s life, the premium income generated from selling the index call option may not be enough to compensate for the difference between the exercise price of the index call option and the increased index value. Thus, the exercise of index call options sold by the Fund may require the Fund to sell portfolio securities to generate cash at inopportune times or for unattractive prices and the Fund may lose money. The trading price of options may be adversely affected if the market for such options becomes less liquid or smaller. The Fund may close out a call option by buying the option instead of letting it expire or be exercised. There can be no assurance that a liquid market will exist when the Fund seeks to close out a call option position by buying the option.

Risks of Selling Put Options on Individual Stocks. The Fund may write put options on individual stocks that the Adviser believes are attractive for purchase at prices at or above the exercise price of the put options written. The purchaser of a put option assumes the right to sell (put) the stock to the seller of the option at a specified price (the exercise price) on or before the expiration date of the option. If the value of the stock on the option expiration date is at or below the exercise price of the option, the Fund may be obligated to purchase the stock at the exercise price. In the event of a substantial depreciation in the value of the underlying stock, the Fund may incur a substantial loss.

Options Risks Generally. A decision as to whether, when and how to use options involves the exercise of skill and judgment, and even a well-conceived and well-executed options program may be adversely affected by market behavior or unexpected events. Successful options strategies may require the anticipation of future movements in securities prices, interest rates and other economic factors. No assurances can be given that the Adviser’s judgments in this respect will be correct.

The trading price of options may be adversely affected if the market for such options becomes less liquid or smaller. The Fund may close out a written option position by buying the option instead of letting it expire or be exercised. Similarly, the Fund may close out a purchased option position by selling the option instead of holding until exercise. There can be no assurance that a liquid market will exist when the Fund seeks to close out an option position by buying or selling the option. Reasons for the absence of a liquid secondary market on an exchange include the following: (i) there may be insufficient trading interest in certain options; (ii) restrictions may be imposed by an exchange on opening transactions or closing transactions or both; (iii) trading halts, suspensions or other restrictions may be imposed with respect to particular classes or series of options; (iv) unusual or unforeseen circumstances may interrupt normal operations on an exchange; (v) the facilities of an exchange or the Options Clearing Corporation (the “OCC”) may not at all times be adequate to handle current trading volume; or (vi) one or more exchanges could, for economic or other reasons, decide or be compelled to discontinue the trading of options (or a particular class or series of options) at some future date. If trading were discontinued, the secondary market on that exchange (or in that class or series of options) would cease to exist. However, outstanding options on that exchange that had been issued by the OCC as a result of trades on that exchange would continue to be exercisable in accordance with their terms.

The Fund’s options positions will be marked to market daily. The hours of trading for options may not conform to the hours during which common stocks held by the Fund are traded. To the extent that the options markets close before the markets for securities, significant price and rate movements can take place in the securities markets that would not be reflected concurrently in the options markets. The value of index options is affected by changes in the value and dividend rates of the securities represented in the underlying index, changes in interest rates, changes in the actual or perceived volatility of the associated index and the remaining time to the options’ expiration, as well as trading conditions in the options market. Similarly, the value of single stock options is affected by changes in the value and dividend rate of the underlying stock, changes in interest rates, changes in the actual or perceived volatility of the associated stock and the remaining time to the options’ expiration, as well as options market trading conditions.

The Fund’s options transactions will be subject to limitations established by each of the exchanges, boards of trade or other trading facilities on which such options are traded. These limitations govern the maximum number of options in each class which may be written or purchased by a single investor or group of investors acting in concert, regardless of whether the options are written or purchased on the same or different exchanges, boards of trade or other trading facilities or are held or written in one or more accounts or through one or more brokers. Thus, the number of options which the Fund may write or purchase may be affected by options written or purchased by other investment advisory clients of the Adviser. An exchange, board of trade or other trading facility may order the liquidation of positions found to be in excess of these limits, and may impose certain other sanctions. The Fund will not write “naked” or uncovered call options.

To the extent that the Fund buys or writes options on indices based upon foreign stocks, the Fund generally intends to buy or sell options on broad-based foreign country and/or regional stock indices that are listed for trading in the United States or which otherwise qualify as “section 1256 contracts” under the Code. Options on foreign indices that are listed for trading in the United States or which otherwise qualify as “section 1256 contracts” under the Code may trade in substantially lower volumes and with substantially wider bid-ask spreads than other options contracts on the same or similar indices that

See Endnotes and Additional Disclosures in this report.

8

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

The Fund's Investment Objectives, Principal Strategies and Principal Risks‡ — continued

trade on other markets outside the United States. To implement its options program most effectively, the Fund may buy or sell index options that do not qualify as “section 1256 contracts” under the Code. Gain or loss on index options not qualifying as “section 1256 contracts” under the Code would be realized upon disposition, lapse or settlement of the positions and, generally, would be treated as short-term gain or loss.

OTC Options Risks. OTC options involve risk that the issuer or counterparty will fail to perform its contractual obligations. Participants in these markets are typically not subject to credit evaluation and regulatory oversight as are members of “exchange based” markets. Options traded in OTC markets will not be issued, guaranteed or cleared by the OCC. By engaging in option transactions in these markets, the Fund may take a credit risk with regard to parties with which it trades and also may bear the risk of settlement default. These risks may differ materially from those involved in exchange-traded transactions, which generally are characterized by clearing organization guarantees, daily marking-to-market and settlement, and segregation and minimum capital requirements applicable to intermediaries. Transactions entered into directly between two counterparties generally do not benefit from these protections, which in turn may subject the Fund to the risk that a counter-party will not settle a transaction in accordance with agreed terms and conditions because of a dispute over the terms of the contract or because of a credit or liquidity problem. Such “counterparty risk” is increased for contracts with longer maturities when events may intervene to prevent settlement. The ability of the Fund to transact business with any one or any number of counterparties, the lack of any independent evaluation of the counterparties or their financial capabilities, and the absence of a regulated market to facilitate a settlement may increase the potential for losses to the Fund.

Derivatives Risk. The Fund’s exposure to derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other investments. The use of derivatives can lead to losses because of adverse movements in the price or value of the security, instrument, index, currency, commodity, economic indicator or event underlying a derivative (“reference instrument”), due to failure of a counterparty or due to tax or regulatory constraints. Derivatives may create leverage in the Fund, which represents a non-cash exposure to the underlying reference instrument. Leverage can increase both the risk and return potential of the Fund. Derivatives risk may be more significant when derivatives are used to enhance return or as a substitute for a cash investment position, rather than solely to hedge the risk of a position held by the Fund. Use of derivatives involves the exercise of specialized skill and judgment, and a transaction may be unsuccessful in whole or in part because of market behavior or unexpected events. Changes in the value of a derivative (including one used for hedging) may not correlate perfectly with the underlying reference instrument. Derivative instruments traded in over-the-counter markets may be difficult to value, may be illiquid, and may be subject to wide swings in valuation caused by changes in the value of the underlying reference instrument. If a derivative’s counterparty is unable to honor its commitments, the value of Fund shares may decline and the Fund could experience delays in (or be unable to achieve) the return of collateral or other assets held by the counterparty. The loss on derivative transactions may substantially exceed the initial investment. A derivative investment also involves the risks relating to the reference instrument underlying the investment.

Tax-Sensitive Investing Risk. The Fund may hold a security in order to achieve more favorable tax-treatment or to sell a security in order to create tax losses. The Fund’s utilization of various tax-management techniques may be curtailed or eliminated by tax legislation, regulation or interpretations. The Fund may not be able to minimize taxable distributions to shareholders and a portion of the Fund’s distributions may be taxable.

Tax Risk. Although the Fund seeks to minimize and defer the federal income taxes incurred by common shareholders in connection with their investment in the Fund, there can be no assurance that it will be successful in this regard. The tax treatment and characterization of the Fund’s distributions may change over time due to changes in the Fund’s mix of investment returns and changes in the federal tax laws, regulations and administrative and judicial interpretations, potentially with retroactive effect. The Fund’s investment program and the tax treatment of Fund distributions may be affected by IRS interpretations of the Code and future changes in tax laws and regulations. While the Fund generally intends to use a variety of techniques and strategies designed to minimize and defer the federal income taxes incurred by common shareholders in connection with their investment in the Fund, certain of the Fund’s investment practices are subject to complex federal income tax provisions that may, among other things, cause common shareholders to pay more tax than they otherwise would have, or to accelerate common shareholders’ recognition of taxable income or gains.

Risks of Investing in Smaller and Mid-Sized Companies. The Fund may make investments in stocks of companies whose market capitalization is considered middle sized or “mid-cap.” Smaller and mid-sized companies are generally subject to greater price fluctuations, limited liquidity, higher transaction costs and higher investment risk than the stocks of larger, more established companies. Such companies may have limited product lines, markets or financial resources, may be dependent on a limited management group, and may lack substantial capital reserves or an established performance record. There may be generally less publicly available information about such companies than for larger, more established companies. Stocks of these companies frequently have lower trading volumes making them more volatile and potentially more difficult to value.

Foreign Investment Risk. Foreign investments can be adversely affected by political, economic and market developments abroad, including the imposition of economic and other sanctions by the United States or another country against a particular country or countries, organizations, entities and/or individuals. There may be less publicly available information about foreign issuers because they may not be subject to reporting practices, requirements or regulations comparable to those to which United States companies are subject. Adverse changes in investment regulations, capital requirements or exchange controls could adversely affect the value of the Fund’s investments. Foreign markets may be smaller, less liquid and more volatile than the major markets in the United States, and as a result, Fund share values may be more volatile. Trading in foreign markets typically involves higher expense than trading in the United States. The Fund may have difficulties enforcing its legal or contractual rights in a foreign country. Depositary receipts are subject to many of the risks associated with investing directly in foreign instruments, including the political and economic risks of the underlying issuer’s country and, in the case of depositary receipts traded on foreign markets, currency risk.

See Endnotes and Additional Disclosures in this report.

9

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

The Fund's Investment Objectives, Principal Strategies and Principal Risks‡ — continued

Emerging Markets Investment Risk. Investment markets within emerging market countries are typically smaller, less liquid, less developed and more volatile than those in more developed markets like the United States, and may be focused in certain sectors. Emerging market securities often involve greater risks than developed market securities. The information available about an emerging market issuer may be less reliable than for comparable issuers in more developed capital markets.

Focused Investment Risk. To the extent the Fund has substantial investments in a relatively small number of securities or issuers, or a particular market, industry, group of industries, country, region, group of countries, asset class or sector, the Fund’s performance will be more susceptible to any single economic, market, political, or regulatory occurrence affecting those particular securities or issuers or that particular market, industry, group of industries, country, region, group of countries, assets class, or sector than a fund that invests more broadly.

Currency Risk. Exchange rates for currencies fluctuate daily. The value of foreign investments may be affected favorably or unfavorably by changes in currency exchange rates in relation to the U.S. dollar. Currency markets generally are not as regulated as securities markets and currency transactions are subject to settlement, custodial and other operational risks.

Interest Rate Risk. The premiums from writing options and amounts available for distribution from the Fund’s options activities may decrease in declining interest rate environments. The value of the Fund’s common stock investments may also be influenced by changes in interest rates. Higher yielding stocks and stocks of issuers whose businesses are substantially affected by changes in interest rates may be particularly sensitive to interest rate risk.

Liquidity Risk. The Fund is exposed to liquidity risk when trading volume, lack of a market maker or trading partner, large position size, market conditions, or legal restrictions impair its ability to sell particular investments or to sell them at advantageous market prices. Consequently, the Fund may have to accept a lower price to sell an investment or continue to hold it or keep the position open, sell other investments to raise cash or abandon an investment opportunity, any of which could have a negative effect on the Fund’s performance. These effects may be exacerbated during times of financial or political stress.

Inflation Risk. Inflation risk is the risk that the purchasing power of assets or income from investments is worth less in the future as inflation decreases the value of money. As inflation increases, the real value of the common shares and distributions thereon can decline.

Counterparty Risk. A financial institution or other counterparty with whom the Fund does business (such as trading or as a derivatives counterparty), or that underwrites, distributes or guarantees any instruments that the Fund owns or is otherwise exposed to, may decline in financial condition and become unable to honor its commitments. This could cause the value of Fund shares to decline or could delay the return or delivery of collateral or other assets to the Fund. Counterparty risk is increased for contracts with longer maturities.

Leverage Risk. Certain Fund transactions may give rise to leverage. Leverage can result from a non-cash exposure to an underlying reference instrument. Leverage can increase both the risk and return potential of the Fund. Leverage can also result from borrowings or issuance of preferred shares. The use of leverage may cause the Fund to liquidate portfolio positions when it may not be advantageous to do so to satisfy its obligations. Leverage may cause the Fund’s NAV to be more volatile than if it had not been leveraged, as certain types of leverage may exaggerate the effect of any increase or decrease in the Fund’s portfolio securities. The Fund may not be able to adjust its use of leverage rapidly enough to respond to interest rate volatility, inflation, and other changing market conditions. As a result, the Fund’s use of leverage may have a negative impact on the Fund’s performance from time to time. The loss on leveraged investments may substantially exceed the initial investment.

Risks Associated with Active Management. The success of the Fund’s investment strategy depends on portfolio management’s successful application of analytical skills and investment judgment. Active management involves subjective decisions and there is no guarantee that such decisions will produce the desired results or expected returns.

Recent Market Conditions. Both U.S. and international markets have experienced significant volatility in recent months and years. As a result of such volatility, investment returns may fluctuate significantly. National economies are substantially interconnected, as are global financial markets, which creates the possibility that conditions in one country or region might adversely impact issuers in a different country or region. However, the interconnectedness of economies and/or markets may be diminishing, which may impact such economies and markets in ways that cannot be foreseen at this time.

The U.S. government and the U.S. Federal Reserve, as well as certain foreign governments and central banks, have from time to time taken steps to support financial markets. The U.S. government and the U.S. Federal Reserve may, conversely, reduce market support activities, including by taking action intended to increase certain interest rates. This and other government intervention may not work as intended, particularly if the efforts are perceived by investors as being unlikely to achieve the desired results. Changes in government activities in this regard, such as changes in interest rate policy, can negatively affect financial markets generally, increase market volatility and reduce the value and liquidity of securities in which the Fund invests.

Some countries, including the United States, have adopted more protectionist trade policies. Slowing global economic growth, the rise in protectionist trade policies, changes to some major international trade agreements, risks associated with the trade agreement between the United Kingdom and the European Union, and the risks associated with trade negotiations between the United States and China, could affect the economies of many nations in ways that cannot necessarily be foreseen at the present time. In addition, the current strength of the U.S. dollar may decrease foreign demand for U.S. assets, which could have a negative impact on certain issuers and/or industries.

See Endnotes and Additional Disclosures in this report.

10

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

The Fund's Investment Objectives, Principal Strategies and Principal Risks‡ — continued

Regulators in the United States have proposed and adopted a number of changes to regulations involving the markets and issuers, some of which apply to the Fund. The full effect of various newly adopted regulations is not currently known. Additionally, it is not currently known whether any of the proposed regulations will be adopted. However, due to the scope of regulations being proposed and adopted, certain of these changes to regulation could limit the Fund’s ability to pursue its investment strategies or make certain investments, may make it more costly for it to operate, or adversely impact performance.

Tensions, war, or open conflict between nations, such as between Russia and Ukraine, in the Middle East, or in eastern Asia could affect the economies of many nations, including the United States. The duration of ongoing hostilities and any sanctions and related events cannot be predicted. Those events present material uncertainty and risk with respect to markets globally and the performance of the Fund and its investments or operations could be negatively impacted.

There is widespread concern about the potential effects of global climate change on property and security values. Certain issuers, industries and regions may be adversely affected by the impact of climate change in ways that cannot be foreseen. The impact of legislation, regulation and international accords related to climate change may negatively impact certain issuers and/or industries.

Cybersecurity Risk. With the increased use of technologies by Fund service providers to conduct business, such as the Internet, the Fund is susceptible to operational, information security and related risks. In general, cyber incidents can result from deliberate attacks or unintentional events. Cybersecurity failures by or breaches of the Fund’s investment adviser or administrator and other service providers (including, but not limited to, the custodian or transfer agent), and the issuers of securities in which the Fund invests, may disrupt and otherwise adversely affect their business operations. This may result in financial losses to the Fund, impede Fund trading, interfere with the Fund’s ability to calculate its net asset value, interfere with the Fund’s ability to transact business or cause violations of applicable privacy and other laws, regulatory fines, penalties, reputational damage, reimbursement or other compensation costs, or additional compliance costs.

Market Disruption. Global instability, war, geopolitical tensions and terrorist attacks in the United States and around the world have previously resulted, and may continue to result in market volatility and may have long-term effects on the United States and worldwide financial markets and may cause further economic uncertainties in the United States and worldwide. The Fund cannot predict the effects of significant future events on the global economy and securities markets. A similar disruption of the financial markets could impact interest rates, auctions, secondary trading, ratings, credit risk, inflation and other factors relating to the common shares.

Anti-Takeover Provisions. The Fund’s Agreement and Declaration of Trust (the “Declaration of Trust”) and Amended and Restated By-Laws (the “By-Laws”) include provisions that could have the effect of making it more difficult to acquire control of the Fund and/or to change the composition of its Board.

General Fund Investing Risks. The Fund is not a complete investment program and there is no guarantee that the Fund will achieve its investment objective. It is possible to lose money by investing in the Fund. An investment in the Fund is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

There have been no material changes to the Fund’s investment objective or principal investment strategies since December 31, 2023.

Important Notice to Shareholders

On January 26, 2023, the Fund’s Board of Trustees voted to exempt, on a going forward basis, all prior and, until further notice, new acquisitions of Fund shares that otherwise might be deemed “Control Share Acquisitions” under the By-Laws from the provisions of the By-Laws addressing “Control Share Acquisitions” (the “Control Share Provisions”). On October 10, 2024, the Board adopted Amendment No. 1 to the By-Laws to formally eliminate the Control Share Provisions and to make certain related conforming changes.

See Endnotes and Additional Disclosures in this report.

11

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

Endnotes and Additional Disclosures

| † | The views expressed in this report are those of the portfolio manager(s) and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance and the Fund(s) disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. This commentary may contain statements that are not historical facts, referred to as “forward-looking statements.” The Fund’s actual future results may differ significantly from those stated in any forward-looking statement, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund shares, the continuation of investment advisory, administrative and service contracts, and other risks discussed from time to time in the Fund’s filings with the Securities and Exchange Commission. |

| ‡ | The information contained herein is provided for informational purposes only and does not constitute a solicitation of an offer to buy or sell Fund shares. Common shares of the Fund are available for purchase and sale only at current market prices in secondary market trading. |

| | |

| 1 | S&P 500® Index is an unmanaged index of large-cap stocks commonly used as a measure of U.S. stock market performance. S&P Dow Jones Indices are a product of S&P Dow Jones Indices LLC (“S&P DJI”) and have been licensed for use. S&P® and S&P 500® are registered trademarks of S&P DJI; Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); S&P DJI, Dow Jones and their respective affiliates do not sponsor, endorse,

sell or promote the Fund, will not have any liability with respect thereto and do not have any liability for any errors, omissions, or interruptions of the S&P Dow Jones Indices. Cboe S&P 500 95–110 Collar IndexSM is an unmanaged index of the S&P 500® stocks with a collar option strategy of buying put options and selling call options. Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. |

| 2 | The shares of the Fund often trade at a discount or premium to their net asset value. The discount or premium may vary over time and may be higher or lower than what is quoted in this report. For up-to-date premium/discount information, please refer to https://funds.eatonvance.com/closed-end-fund-prices.php. |

| 3 | The Distribution Rate is based on the Fund’s last regular distribution per share in the period (annualized) divided by the Fund’s NAV or market price at the end of the period. The Fund’s distributions may be comprised of amounts characterized for federal income tax purposes as qualified and non-qualified ordinary dividends, capital gains and nondividend distributions, also known as return of capital. For additional information about nondividend distributions, please refer to Eaton Vance Closed-End Fund Distribution Notices (19a) posted on our website, eatonvance.com. The Fund will determine the federal income tax character of distributions paid to a shareholder after the end of the calendar year. This is reported on the IRS form 1099-DIV and provided to the shareholder shortly after each year-end. For information about the tax character of distributions made in prior |

| | calendar years, please refer to Performance-Tax Character of Distributions on the Fund’s webpage available at eatonvance.com. In recent years, a significant portion of the Fund’s distributions has been characterized as a return of capital. The Fund’s distributions are determined by the investment adviser based on its current assessment of the Fund’s long-term return potential. Fund distributions may be affected by numerous factors including changes in Fund performance, the cost of financing for leverage, portfolio holdings, realized and projected returns, and other factors. As portfolio and market conditions change, the rate of distributions paid by the Fund could change. |

| | Fund profile subject to change due to active management. |

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

| Security | Shares | Value |

| Aerospace & Defense — 0.9% |

| HEICO Corp.(1) | | 26,162 | $ 6,219,754 |

| | | | $ 6,219,754 |

| Automobiles — 0.5% |

| Tesla, Inc.(1)(2) | | 8,158 | $ 3,294,527 |

| | | | $ 3,294,527 |

| Biotechnology — 1.7% |

| AbbVie, Inc.(1) | | 61,667 | $ 10,958,226 |

| | | | $ 10,958,226 |

| Broadline Retail — 5.3% |

| Amazon.com, Inc.(1)(2) | | 159,188 | $ 34,924,255 |

| | | | $ 34,924,255 |

| Building Products — 1.1% |

| Carrier Global Corp.(1) | | 103,057 | $ 7,034,671 |

| | | | $ 7,034,671 |

| Capital Markets — 6.9% |

| Blue Owl Capital, Inc.(1) | | 428,181 | $ 9,959,490 |

| Intercontinental Exchange, Inc.(1) | | 55,684 | 8,297,473 |

| S&P Global, Inc.(1) | | 18,644 | 9,285,271 |

| Stifel Financial Corp.(1) | | 65,528 | 6,951,210 |

| Tradeweb Markets, Inc., Class A(1) | | 80,595 | 10,551,498 |

| | | | $ 45,044,942 |

| Chemicals — 0.7% |

| Linde PLC(1) | | 10,942 | $ 4,581,087 |

| | | | $ 4,581,087 |

| Commercial Services & Supplies — 1.1% |

| Waste Connections, Inc.(1) | | 40,503 | $ 6,949,505 |

| | | | $ 6,949,505 |

| Communications Equipment — 0.6% |

| Arista Networks, Inc.(1)(2) | | 32,880 | $ 3,634,226 |

| | | | $ 3,634,226 |

| Consumer Staples Distribution & Retail — 3.5% |

| BJ's Wholesale Club Holdings, Inc.(1)(2) | | 122,046 | $ 10,904,810 |

| Security | Shares | Value |

| Consumer Staples Distribution & Retail (continued) |

| Walmart, Inc.(1) | | 134,091 | $ 12,115,122 |

| | | | $ 23,019,932 |

| Containers & Packaging — 0.9% |

| AptarGroup, Inc.(1) | | 39,606 | $ 6,222,103 |

| | | | $ 6,222,103 |

| Electrical Equipment — 1.5% |

| AMETEK, Inc.(1) | | 53,381 | $ 9,622,459 |

| | | | $ 9,622,459 |

| Entertainment — 3.0% |

| Liberty Media Corp.-Liberty Formula One, Class C(1)(2) | | 54,435 | $ 5,043,947 |

| Netflix, Inc.(1)(2) | | 13,812 | 12,310,912 |

| Spotify Technology SA(1)(2) | | 5,400 | 2,415,852 |

| | | | $ 19,770,711 |

| Financial Services — 4.1% |

| Mr. Cooper Group, Inc.(1)(2) | | 42,426 | $ 4,073,320 |

| Shift4 Payments, Inc., Class A(1)(2) | | 87,432 | 9,073,693 |

| Visa, Inc., Class A(1) | | 43,741 | 13,823,906 |

| | | | $ 26,970,919 |

| Ground Transportation — 1.3% |

| Uber Technologies, Inc.(1)(2) | | 139,776 | $ 8,431,288 |

| | | | $ 8,431,288 |

| Health Care Equipment & Supplies — 3.3% |

| Abbott Laboratories(1) | | 56,643 | $ 6,406,890 |

| Edwards Lifesciences Corp.(1)(2) | | 94,528 | 6,997,908 |

| Intuitive Surgical, Inc.(1)(2) | | 15,386 | 8,030,876 |

| | | | $ 21,435,674 |

| Health Care Providers & Services — 1.8% |

| UnitedHealth Group, Inc.(1) | | 23,242 | $ 11,757,198 |

| | | | $ 11,757,198 |

| Hotels, Restaurants & Leisure — 1.2% |

| Marriott International, Inc., Class A(1) | | 28,702 | $ 8,006,136 |

| | | | $ 8,006,136 |

| Insurance — 3.3% |

| Allstate Corp.(1) | | 67,404 | $ 12,994,817 |

| Arthur J. Gallagher & Co.(1) | | 29,400 | 8,345,190 |

| | | | $ 21,340,007 |

13

See Notes to Financial Statements.

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

Portfolio of Investments — continued

| Security | Shares | Value |

| Interactive Media & Services — 7.5% |

| Alphabet, Inc., Class C(1) | | 152,734 | $ 29,086,663 |

| Meta Platforms, Inc., Class A(1) | | 34,419 | 20,152,669 |

| | | | $ 49,239,332 |

| IT Services — 1.2% |

| Gartner, Inc.(1)(2) | | 16,883 | $ 8,179,307 |

| | | | $ 8,179,307 |

| Life Sciences Tools & Services — 1.2% |

| Thermo Fisher Scientific, Inc.(1) | | 14,698 | $ 7,646,341 |

| | | | $ 7,646,341 |

| Machinery — 0.9% |

| Parker-Hannifin Corp.(1) | | 9,415 | $ 5,988,222 |

| | | | $ 5,988,222 |

| Media — 0.4% |

| Trade Desk, Inc., Class A(1)(2) | | 24,961 | $ 2,933,666 |

| | | | $ 2,933,666 |

| Multi-Utilities — 0.8% |

| Sempra(1) | | 57,384 | $ 5,033,724 |

| | | | $ 5,033,724 |

| Oil, Gas & Consumable Fuels — 2.0% |

| ConocoPhillips(1) | | 134,808 | $ 13,368,909 |

| | | | $ 13,368,909 |

| Pharmaceuticals — 2.3% |

| Eli Lilly & Co.(1) | | 19,587 | $ 15,121,164 |

| | | | $ 15,121,164 |

| Professional Services — 3.4% |

| Automatic Data Processing, Inc.(1) | | 21,586 | $ 6,318,870 |

| Booz Allen Hamilton Holding Corp.(1) | | 23,917 | 3,078,118 |

| TransUnion(1) | | 136,427 | 12,648,147 |

| | | | $ 22,045,135 |

| Real Estate Management & Development — 2.4% |

| CoStar Group, Inc.(1)(2) | | 89,547 | $ 6,410,670 |

| FirstService Corp. | | 51,888 | 9,392,766 |

| | | | $ 15,803,436 |

| Semiconductors & Semiconductor Equipment — 13.7% |

| Analog Devices, Inc.(1) | | 37,583 | $ 7,984,884 |

| Security | Shares | Value |

| Semiconductors & Semiconductor Equipment (continued) |

| Broadcom, Inc.(1) | | 101,823 | $ 23,606,645 |

| Lam Research Corp.(1) | | 144,130 | 10,410,510 |

| NVIDIA Corp.(1) | | 356,380 | 47,858,270 |

| | | | $ 89,860,309 |

| Software — 10.0% |

| Fair Isaac Corp.(1)(2) | | 4,173 | $ 8,308,151 |

| Microsoft Corp.(1) | | 116,881 | 49,265,341 |

| Palo Alto Networks, Inc.(1)(2) | | 42,626 | 7,756,227 |

| | | | $ 65,329,719 |

| Specialty Retail — 2.7% |

| Burlington Stores, Inc.(1)(2) | | 31,986 | $ 9,117,929 |

| TJX Cos., Inc.(1) | | 69,062 | 8,343,380 |

| | | | $ 17,461,309 |

| Technology Hardware, Storage & Peripherals — 7.6% |

| Apple, Inc.(1) | | 198,626 | $ 49,739,923 |

| | | | $ 49,739,923 |

Total Common Stocks

(identified cost $357,989,940) | | | $646,968,116 |

| Short-Term Investments — 0.6% |

| Security | Shares | Value |

| Morgan Stanley Institutional Liquidity Funds - Government Portfolio, Institutional Class, 4.43%(3) | | 4,185,156 | $ 4,185,156 |

Total Short-Term Investments

(identified cost $4,185,156) | | | $ 4,185,156 |

Total Purchased Put Options — 0.8%

(identified cost $2,989,337) | | | $ 5,106,405 |

Total Investments — 100.2%

(identified cost $365,164,433) | | | $656,259,677 |

Total Written Call Options — (0.1)%

(premiums received $3,180,359) | | | $ (853,123) |

| Other Assets, Less Liabilities — (0.1)% | | | $ (469,258) |

| Net Assets — 100.0% | | | $654,937,296 |

14

See Notes to Financial Statements.

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

Portfolio of Investments — continued

| The percentage shown for each investment category in the Portfolio of Investments is based on net assets. |

| (1) | Security (or a portion thereof) has been pledged as collateral for written options. |

| (2) | Non-income producing security. |

| (3) | May be deemed to be an affiliated investment company (see Note 7). The rate shown is the annualized seven-day yield as of December 31, 2024. |

| Purchased Put Options (Exchange-Traded) — 0.8% |

| Description | Number of

Contracts | Notional

Amount | Exercise

Price | Expiration

Date | Value |

| S&P 500 Index | 87 | $ | 51,170,181 | $ | 5,955 | 1/3/25 | $ 661,200 |

| S&P 500 Index | 87 | | 51,170,181 | | 5,940 | 1/6/25 | 605,085 |

| S&P 500 Index | 87 | | 51,170,181 | | 5,925 | 1/8/25 | 582,465 |

| S&P 500 Index | 88 | | 51,758,344 | | 5,900 | 1/10/25 | 521,840 |

| S&P 500 Index | 88 | | 51,758,344 | | 5,920 | 1/13/25 | 638,880 |

| S&P 500 Index | 88 | | 51,758,344 | | 5,890 | 1/15/25 | 564,960 |

| S&P 500 Index | 89 | | 52,346,507 | | 5,620 | 1/17/25 | 103,685 |

| S&P 500 Index | 89 | | 52,346,507 | | 5,675 | 1/21/25 | 171,770 |

| S&P 500 Index | 88 | | 51,758,344 | | 5,810 | 1/22/25 | 412,720 |

| S&P 500 Index | 89 | | 52,346,507 | | 5,750 | 1/24/25 | 328,855 |

| S&P 500 Index | 89 | | 52,346,507 | | 5,650 | 1/27/25 | 208,705 |

| S&P 500 Index | 88 | | 51,758,344 | | 5,700 | 1/29/25 | 306,240 |

| Total | | | | | | | $5,106,405 |

| Written Call Options (Exchange-Traded) — (0.1)% |

| Description | Number of

Contracts | Notional

Amount | Exercise

Price | Expiration

Date | Value |

| S&P 500 Index | 87 | $ | 51,170,181 | $ | 6,210 | 1/3/25 | $ (653) |

| S&P 500 Index | 87 | | 51,170,181 | | 6,180 | 1/6/25 | (1,305) |

| S&P 500 Index | 87 | | 51,170,181 | | 6,200 | 1/8/25 | (870) |

| S&P 500 Index | 88 | | 51,758,344 | | 6,175 | 1/10/25 | (3,080) |

| S&P 500 Index | 88 | | 51,758,344 | | 6,200 | 1/13/25 | (2,860) |

| S&P 500 Index | 88 | | 51,758,344 | | 6,175 | 1/15/25 | (7,700) |

| S&P 500 Index | 89 | | 52,346,507 | | 6,025 | 1/17/25 | (151,745) |

| S&P 500 Index | 89 | | 52,346,507 | | 6,060 | 1/21/25 | (103,685) |

| S&P 500 Index | 88 | | 51,758,344 | | 6,125 | 1/22/25 | (40,920) |

| S&P 500 Index | 89 | | 52,346,507 | | 6,085 | 1/24/25 | (100,570) |

| S&P 500 Index | 89 | | 52,346,507 | | 6,020 | 1/27/25 | (250,535) |

| S&P 500 Index | 88 | | 51,758,344 | | 6,060 | 1/29/25 | (189,200) |

| Total | | | | | | | $(853,123) |

15

See Notes to Financial Statements.

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

Statement of Assets and Liabilities

| | December 31, 2024 |

| Assets | |

| Unaffiliated investments, at value (identified cost $360,979,277) | $652,074,521 |

| Affiliated investments, at value (identified cost $4,185,156) | 4,185,156 |

| Dividends receivable | 234,430 |

| Dividends receivable from affiliated investments | 11,472 |

| Receivable for investments sold | 184,666 |

| Receivable for premiums on written options | 257,245 |

| Tax reclaims receivable | 17,068 |

| Trustees' deferred compensation plan | 121,256 |

| Total assets | $657,085,814 |

| Liabilities | |

| Written options outstanding, at value (premiums received $3,180,359) | $853,123 |

| Payable for investments purchased | 260,979 |

| Payable to affiliates: | |

| Investment adviser fee | 565,355 |

| Trustees' fees | 9,950 |

| Trustees' deferred compensation plan | 121,256 |

| Payable for custodian fee | 134,066 |

| Payable for printing and postage | 116,833 |

| Accrued expenses | 86,956 |

| Total liabilities | $2,148,518 |

| Net Assets | $654,937,296 |

| Sources of Net Assets | |

| Common shares, $0.01 par value, unlimited number of shares authorized | $673,018 |

| Additional paid-in capital | 366,054,952 |

| Distributable earnings | 288,209,326 |

| Net Assets | $654,937,296 |

| Common Shares Issued and Outstanding | 67,301,787 |

| Net Asset Value Per Common Share | |

| Net assets ÷ common shares issued and outstanding | $9.73 |

16

See Notes to Financial Statements.

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

| | Year Ended |

| | December 31, 2024 |

| Investment Income | |

| Dividend income (net of foreign taxes withheld of $12,758) | $5,461,714 |

| Dividend income from affiliated investments | 211,088 |

| Total investment income | $5,672,802 |

| Expenses | |

| Investment adviser fee | $6,301,085 |

| Trustees’ fees and expenses | 47,315 |

| Custodian fee | 222,659 |

| Transfer and dividend disbursing agent fees | 18,054 |

| Legal and accounting services | 85,844 |

| Printing and postage | 172,311 |

| Miscellaneous | 67,454 |

| Total expenses | $6,914,722 |

| Deduct: | |

| Waiver and/or reimbursement of expenses by affiliates | $6,030 |

| Total expense reductions | $6,030 |

| Net expenses | $6,908,692 |

| Net investment loss | $(1,235,890) |

| Realized and Unrealized Gain (Loss) | |

| Net realized gain (loss): | |

| Investment transactions | $47,493,894 |

| Written options | (15,303,247) |

| Net realized gain | $32,190,647 |

| Change in unrealized appreciation (depreciation): | |

| Investments | $98,924,201 |

| Written options | 5,116,181 |

| Net change in unrealized appreciation (depreciation) | $104,040,382 |

| Net realized and unrealized gain | $136,231,029 |

| Net increase in net assets from operations | $134,995,139 |

17

See Notes to Financial Statements.

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

Statements of Changes in Net Assets

| | Year Ended December 31, |

| | 2024 | 2023 |

| Increase (Decrease) in Net Assets | | |

| From operations: | | |

| Net investment income (loss) | $(1,235,890) | $1,387,706 |

| Net realized gain | 32,190,647 | 37,324,830 |

| Net change in unrealized appreciation (depreciation) | 104,040,382 | 41,641,292 |

| Net increase in net assets from operations | $134,995,139 | $80,353,828 |

| Distributions to shareholders | $(30,372,308) | $(43,357,343) |

| Tax return of capital to shareholders | $(20,750,130) | $(3,403,939) |

| Net increase in net assets | $83,872,701 | $33,592,546 |

| Net Assets | | |

| At beginning of year | $571,064,595 | $537,472,049 |

| At end of year | $654,937,296 | $571,064,595 |

18

See Notes to Financial Statements.

Eaton Vance

Risk-Managed Diversified Equity Income Fund

December 31, 2024

| | Year Ended December 31, |

| | 2024 | 2023 | 2022 | 2021 | 2020 |

| Net asset value — Beginning of year | $8.49 | $7.99 | $10.38 | $10.08 | $9.34 |

| Income (Loss) From Operations | | | | | |

| Net investment income (loss)(1) | $(0.02) | $0.02 | $0.04 | $0.04 | $0.07 |

| Net realized and unrealized gain (loss) | 2.02 | 1.17 | (1.56) | 1.16 | 1.58 |

| Total income (loss) from operations | $2.00 | $1.19 | $(1.52) | $1.20 | $1.65 |

| Less Distributions | | | | | |

| From net investment income | $— | $(0.02) | $(0.03) | $(0.04) | $(0.08) |

| From net realized gain | (0.45) | (0.62) | (0.55) | (0.18) | (0.19) |

| Tax return of capital | (0.31) | (0.05) | (0.30) | (0.69) | (0.64) |

| Total distributions | $(0.76) | $(0.69) | $(0.88) | $(0.91) | $(0.91) |

| Premium from common shares sold through shelf offering (see Note 5)(1) | $— | $— | $0.01 | $0.01 | $— |

| Net asset value — End of year | $9.73 | $8.49 | $7.99 | $10.38 | $10.08 |

| Market value — End of year | $9.31 | $7.84 | $7.50 | $10.69 | $10.37 |

| Total Investment Return on Net Asset Value(2) | 24.90% | 15.94% | (14.93)% | 12.35% | 18.78% |

| Total Investment Return on Market Value(2) | 29.42% | 14.05% | (22.46)% | 12.47% | 22.33% |

| Ratios/Supplemental Data | | | | | |

| Net assets, end of year (000’s omitted) | $654,937 | $571,065 | $537,472 | $677,045 | $643,771 |

| Ratios (as a percentage of average daily net assets):(3) | | | | | |

| Total expenses | 1.10% | 1.13% | 1.12% | 1.10% | 1.11% |

| Net expenses | 1.10%(4) | 1.13%(4) | 1.12%(4) | 1.10% | 1.11% |