As filed with the Securities and Exchange Commission on February 11, 2013

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

VERSO PAPER HOLDINGS LLC

(Exact name of registrant as specified in its charter)

| | | | |

| DELAWARE | | 2621 | | 56-2597634 |

(State or other jurisdiction of Incorporation or organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification No.) |

6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436

(901) 369-4100

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

VERSO PAPER INC.

(Exact name of registrant as specified in its charter)

| | | | |

| DELAWARE | | 2621 | | 56-2597640 |

(State or other jurisdiction of Incorporation or organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification No.) |

6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436

(901) 369-4100

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

SEE TABLE OF ADDITIONAL REGISTRANTS

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Peter H. Kesser, Esq.

Senior Vice President, General Counsel and Secretary

6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436

(901) 369-4100

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a copy to:

David S. Huntington, Esq.

Paul, Weiss, Rifkind, Wharton & Garrison LLP

1285 Avenue of the Americas

New York, New York 10019-6064

(212) 373-3000

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement becomes effective.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | | | | |

| Large accelerated filer | | ¨ | | Accelerated filer | | ¨ |

| Non-accelerated filer | | x (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ¨

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ¨

CALCULATION OF REGISTRATION FEE

| | | | | | | | |

|

Title of each Class of Securities to be Registered | | Amount to be Registered | | Proposed Maximum Offering Price Per Note | | Proposed Maximum Aggregate Offering Price(1) | | Amount of Registration Fee(2) |

11.75% Senior Secured Notes due 2019 | | $72,882,000 | | 100% | | $72,882,000 | | $9,941.10 |

Guarantee of 11.75% Senior Secured Notes due 2019(3) | | — | | — | | — | | (4) |

|

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended (the “Securities Act”). |

| (2) | Calculated pursuant to Rule 457(f) of the rules and regulations of the Securities Act. |

| (3) | Each of Verso Paper Holdings LLC’s domestic 100% owned subsidiaries, as of the date of this Registration Statement, except Verso Paper Inc., Bucksport Leasing LLC and Verso Quinnesec REP LLC, guarantees the 11.75% Senior Secured Notes due 2019. |

| (4) | See the Table of Additional Registrants on the inside facing page for table of additional registrant guarantors. Pursuant to Rule 457(n) of the rules and regulations under the Securities Act, no separate fee for the guarantees are payable. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission (“SEC”), acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANTS

| | | | | | | | |

Guarantor | | State or Other

Jurisdiction of

Incorporation or

Organization | | Address of Registrants’ Principal

Executive Offices | | Primary

Standard

Industrial

Classification

Code No. | | IRS

Employer

Identification

Number |

Verso Paper LLC | | Delaware | | 6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436

(901) 369-4100 | | 2621 | | 75-3217399 |

| | | | |

Verso Androscoggin LLC | | Delaware | | 6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436 (901) 369-4100 | | 2621 | | 75-3217400 |

| | | | |

Verso Bucksport LLC | | Delaware | | 6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436 (901) 369-4100 | | 2621 | | 75-3217402 |

| | | | |

Verso Sartell LLC | | Delaware | | 6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436 (901) 369-4100 | | 2621 | | 75-3217406 |

| | | | |

Verso Quinnesec LLC | | Delaware | | 6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436 (901) 369-4100 | | 2621 | | 75-3217404 |

| | | | |

Verso Maine Energy LLC | | Delaware | | 6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436 (901) 369-4100 | | 2621 | | 26-1857446 |

| | | | |

Verso Fiber Farm LLC | | Delaware | | 6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436 (901) 369-4100 | | 2621 | | 75-3217398 |

| | | | |

nexTier Solutions Corporation | | California | | 6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436 (901) 369-4100 | | 2621 | | 33-0901108 |

| | | | |

Verso Quinnesec REP Holding Inc. | | Delaware | | 6775 Lenox Center Court, Suite 400

Memphis, Tennessee 38115-4436 (901) 369-4100 | | 2621 | | 27-4272864 |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated February 11, 2013

PRELIMINARY PROSPECTUS

Verso Paper Holdings LLC

Verso Paper Inc.

Exchange Offer for $72,882,000

11.75% Senior Secured Notes due 2019

The Notes and the Guarantees

| | • | | Verso Paper Holdings LLC and Verso Paper Inc. (the “Issuers”) are offering to exchange for $72,882,000 of our outstanding 11.75% Senior Secured Notes due 2019 and certain related guarantees, which we refer to collectively as the “additional senior secured notes,” a like aggregate amount of our registered 11.75% Senior Secured Notes due 2019 and certain related guarantees, which we refer to collectively as the “additional exchange notes.” The additional senior secured notes were issued on January 31, 2013. The additional exchange notes will be issued under the indenture dated as of March 21, 2012, as amended and supplemented by the First Supplemental Indenture dated as of March 29, 2012 and as further amended and supplemented by the Second Supplemental Indenture dated as of January 31, 2013. We refer to the additional senior secured notes and the additional exchange notes collectively as the “additional notes.” |

| | • | | On December 19, 2012, we exchanged $344,318,000 aggregate principal amount of our 11.75% Senior Secured Notes due 2019 and certain related guarantees, which we refer to as the “existing senior secured notes,” for a like aggregate principal amount of our registered 11.75% Senior Secured Notes due 2019 and certain related guarantees, which we refer to as the “existing exchange notes.” The additional exchange notes will bear the same CUSIP as the existing exchange notes. The additional exchange notes and the existing exchange notes will have identical terms, except as stated herein. We refer collectively to the additional senior secured notes, the additional exchange notes, the initial senior secured notes and the existing exchange notes as the “notes.” |

| | • | | The additional exchange notes will mature on January 15, 2019. We will pay interest on the additional exchange notes semi-annually on January 15 and July 15 of each year, commencing on July 15, 2013, at a rate of 11.75% per annum, to holders of record on the January 1 or July 1 immediately preceding the interest payment date. |

| | • | | The additional exchange notes will be guaranteed by Verso Paper Holdings LLC’s wholly owned domestic restricted subsidiaries (except Verso Paper Inc., Bucksport Leasing LLC and Verso Quinnesec REP LLC) that guarantee the ABL Facility and the Cash Flow Facility, each as defined herein. |

| | • | | The additional exchange notes and the related guarantees will be secured by (i) first-priority security interests in the “Notes Priority Collateral” (which generally includes most fixed assets of the Issuers and the guarantors) and (ii) second-priority security interests in the “ABL Priority Collateral” (which generally includes most inventory and accounts receivable of the Issuers and guarantors), in each case subject to certain permitted liens and as described herein. |

Terms of the Exchange Offer

| | • | | The exchange offer will expire at 11:59 p.m., New York City time, on , 2013, unless we extend it. |

| | • | | If all the conditions to this exchange offer are satisfied, we will exchange all of our additional senior secured notes that are validly tendered and not withdrawn for the additional exchange notes. |

| | • | | You may withdraw your tender of additional senior secured notes at any time before the expiration of this exchange offer. |

| | • | | The additional exchange notes that we will issue you in exchange for your additional senior secured notes will be substantially identical to your additional senior secured notes except that, unlike your additional senior secured notes, the additional exchange notes will have no transfer restrictions or registration rights. |

| | • | | The additional exchange notes that we will issue you in exchange for your additional senior secured notes are new securities with no established market for trading. |

Before participating in this exchange offer, please refer to the section in this prospectus entitled “Risk Factors” beginning on page 17.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We have not applied, and do not intend to apply, for listing the notes on any national securities exchange or automated quotation system.

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of those exchange notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for additional senior secured notes where those additional senior secured notes were acquired by that broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 180 days after the expiration date, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See “Plan of Distribution.”

The date of this prospectus is , 2013.

TABLE OF CONTENTS

We have not authorized anyone to give you any information or to make any representations about us or the transactions we discuss in this prospectus other than those contained in this prospectus. If you are given any information or representations about these matters that is not discussed in this prospectus, you must not rely on that information. This prospectus is not an offer to sell or a solicitation of an offer to buy securities anywhere or to anyone where or to whom we are not permitted to offer or sell securities under applicable law. The delivery of this prospectus does not, under any circumstances, mean that there has not been a change in our affairs since the date of this prospectus. Subject to our obligation to amend or supplement this prospectus as required by law and the rules of the SEC the information contained in this prospectus is correct only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of these securities.

Until , 2013 (90 days after the date of this prospectus), all dealers that effect transactions in the additional exchange notes, whether or not participating in the exchange offer, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Each prospective purchaser of the additional exchange notes must comply with all applicable laws and regulations in force in any jurisdiction in which it purchases, offers or sells the notes or possesses or distributes this prospectus and must obtain any consent, approval or permission required by it for the purchase, offer or sale by it of the additional exchange notes under the laws and regulations in force in any jurisdiction to which it is subject or in which it makes such purchases, offers or sales, and we shall not have any responsibility therefor.

i

SUMMARY

This summary highlights important information about our business and about this exchange offer. It does not include all information you should consider before making a decision to participate in the exchange offer. For a more complete understanding of the Issuers, we urge you to carefully read this prospectus in its entirety, including the sections entitled “Risk Factors,” “Cautionary Statement Concerning Forward-Looking Statements,” and “Where You Can Find More Information” and our financial statements and the related notes. Unless otherwise noted, the terms “we,” “us” and “our” refer collectively to Verso Paper Holdings LLC, a Delaware limited liability company, and its subsidiaries. The term “Company” refers to Verso Paper Holdings LLC only and does not include any of its subsidiaries. Our definition of “Adjusted EBITDA” and other financial terms are described in footnote 3 under “—Summary Historical Financial Data.”

Our Company

We are a leading North American supplier of coated papers to catalog and magazine publishers. The coating process adds a smooth uniform layer in the paper, which results in superior color and print definition. As a result, coated paper is used primarily in media and marketing applications, including catalogs, magazines, and commercial printing applications, such as high-end advertising brochures, annual reports, and direct mail advertising.

We are one of North America’s largest producers of coated groundwood paper, which is used primarily for catalogs and magazines. We are also a low cost producer of coated freesheet paper, which is used primarily for annual reports, brochures, and magazine covers. We also produce and sell market kraft pulp, which is used to manufacture printing and writing paper grades and tissue products. Our net sales by product line for the nine months ended September 30, 2012 were approximately $889 million, $104 million and $120 million for coated paper, hardwood market pulp and other, respectively.

We currently operate eight paper machines at three mills located in Maine and Michigan. We believe our coated paper mills are among the most efficient and lowest cost coated paper mills in the world based on the cash cost of delivery to Chicago. We attribute our manufacturing efficiency, in part, to the significant historical investments made in our mills. Our mills have a combined annual production capacity of approximately 1,290,000 tons of coated paper, 165,000 tons of ultra-lightweight specialty and uncoated papers, and 930,000 tons of kraft pulp. Of the pulp that we produce, we consume approximately 635,000 tons internally and sell the rest. Our facilities are strategically located within close proximity to major publication printing customers, which affords us the ability to more quickly and cost-effectively deliver our products. The facilities also benefit from convenient and cost-effective access to northern softwood fiber, which is required for the production of lightweight and ultra-lightweight coated papers.

We sell and market our products to approximately 125 customers that comprise approximately 700 end-user accounts. We have long-standing relationships with many leading magazine and catalog publishers, commercial printers, specialty retail merchandisers and paper merchants. Our relationships with our ten largest coated paper customers average more than 20 years. We reach our end-users through several distribution channels, including direct sales, commercial printers, paper merchants, and brokers. Many of our customers provide us with forecasts of their paper needs, which allows us to plan our production runs in advance, optimizing production over our integrated mill system and thereby reducing costs and increasing overall efficiency. Our key customers include leading magazine publishers such as Condé Nast Publications, Inc., Hearst Corporation, and Time Inc.; leading catalog producers such as Uline Inc. and Sears Holdings Corporation; leading commercial printers such as Quad/Graphics, Inc., and RR Donnelley & Sons Company and leading paper merchants and brokers, such as A.T. Clayton & Co., xpedx, and Clifford Paper, Inc.

1

As of September 30, 2012, we had approximately 2,200 employees. For the fiscal years ended December 31, 2011, 2010, and 2009, we had net sales of $1,722.5 million, $1,605.3 million and $1,360.9 million, respectively. We had net losses of $122.5 million and $125.5 million in fiscal years 2011 and 2010, respectively, and net income of $80.7 million in fiscal year 2009. For the nine months ended September 30, 2012, we had net sales of $1,113.6 million and a net loss of $194.6 million.

Recent Developments

On January 31, 2013, the Issuers issued 11.75% Senior Secured Notes due 2019 (the “additional senior secured notes”) to certain lenders (the “Holdco Lenders”) under the credit agreement (the “Holdco Credit Agreement”) of Verso Paper Finance Holdings LLC and Verso Paper Finance Holdings Inc. (together, the “Holdco Borrowers”), in exchange for approximately $85.8 million of aggregate principal amount of the outstanding loans under the Holdco Credit Agreement (the “Holdco Loans”) and net accrued interest thereon through the closing date, at an exchange rate of 85%, pursuant to exchange agreements entered into among the Holdco Borrowers, the Issuers, the Guarantors, and the Holdco Lenders. The Issuers issued the additional senior secured notes to the Holdco Lenders in exchange for the assignment to the Holdco Borrowers of their Holdco Loans and the cancellation of such Holdco Loans. We refer to these exchange transactions collectively as the “Refinancing Transactions.”

Additional Information

Our principal executive offices are located at 6775 Lenox Center Court, Suite 400, Memphis, Tennessee 38115-4436. Our telephone number is (901) 369-4100. Our website address iswww.versopaper.com. Information on or accessible through our website is not part of, and is not incorporated by reference into, this prospectus.

2

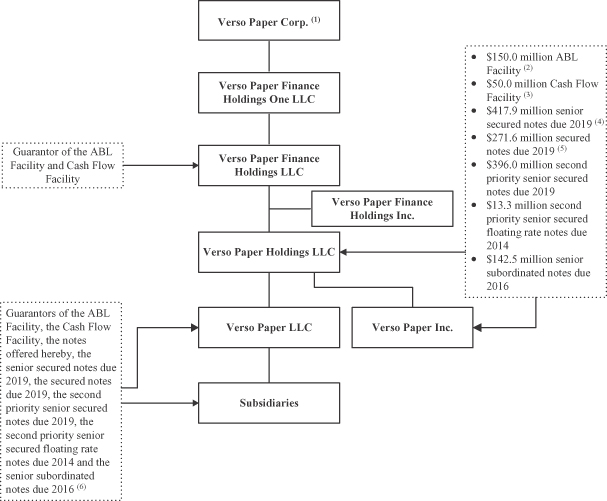

Corporate Structure

The chart below is a summary of the organizational structure of the Issuers and their parents and subsidiaries and illustrates the long-term debt that was outstanding as of September 30, 2012, after giving effect to the Refinancing Transactions.

| (1) | Certain intermediate holding companies without material assets or obligations are not shown. |

| (2) | As of September 30, 2012, there was $35.0 million of debt outstanding under the ABL Facility, $43.3 million in letters of credit issued and $71.7 million available for future borrowing. |

| (3) | As of September 30, 2012, there was no debt outstanding under the Cash Flow Facility and $50.0 million available for future borrowing. |

| (4) | Including the $72.9 million of the additional senior secured notes being exchanged. |

| (5) | Secured by liens that are junior in priority to the additional senior secured notes. |

| (6) | Guarantors of the ABL Facility, the Cash Flow Facility, the notes, the secured notes, the second priority senior secured notes, the second priority senior secured floating rate notes and the senior subordinated notes include all of the domestic wholly owned operating subsidiaries of Verso Paper Holdings LLC, except Verso Paper Inc., Bucksport Leasing LLC and Verso Quinnesec REP LLC, as of the date of this prospectus, but do not include any of our future foreign subsidiaries. |

3

Summary of the Exchange Offer

In connection with the closing of the offering of the additional senior secured notes, we entered into a registration rights agreement (as more fully described below) with Citigroup Global Markets Inc., on behalf of the holders of the additional senior secured notes. You are entitled to exchange in the exchange offer your additional senior secured notes for additional exchange notes, which are identical in all material respects to the additional senior secured notes except that:

| | • | | the additional exchange notes have been registered under the Securities Act and will be freely tradable by persons who are not affiliated with us; |

| | • | | the additional exchange notes are not entitled to the registration rights applicable to the additional senior secured notes under the registration rights agreement; and |

| | • | | our obligation to pay additional interest on the additional senior secured notes due to the failure to consummate the exchange offer by a prior date does not apply to the additional exchange notes. |

Exchange Offer | We are offering to exchange up to $72,882,000 aggregate principal amount of our additional exchange notes for a like aggregate principal amount of our additional senior secured notes. |

| | In order to exchange your additional senior secured notes, you must properly tender them and we must accept your tender. We will exchange all outstanding additional senior secured notes that are validly tendered and not validly withdrawn. Additional senior secured notes may be exchanged only in denominations of $2,000 and integral multiples of $1,000 in excess thereof. |

Expiration Date | This exchange offer will expire at 11:59 p.m., New York City time, on , 2013, unless we decide to extend it. We do not currently intend to extend the expiration date. |

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, some of which we may waive, that include the following conditions: |

| | • | | there is no change in the laws and regulations which would impair our ability to proceed with this exchange offer, |

| | • | | there is no change in the current interpretation of the staff of the SEC permitting resales of the additional exchange notes, |

| | • | | there is no stop order issued by the SEC which would suspend the effectiveness of the registration statement which includes this prospectus or the qualification of the additional exchange notes under the Trust Indenture Act of 1939, |

| | • | | there is no litigation or threatened litigation which would impair our ability to proceed with this exchange offer, and |

| | • | | we obtain all the governmental approvals we deem necessary to complete this exchange offer. |

| | Please refer to the section in this prospectus entitled “The Exchange Offer—Conditions to the Exchange Offer.” |

4

Procedures for Tendering Additional Senior Secured Notes | To participate in this exchange offer, you must complete, sign and date the letter of transmittal or its facsimile and transmit it, together with your additional senior secured notes to be exchanged and all other documents required by the letter of transmittal, to Wilmington Trust, National Association, as exchange agent, at its address indicated under “The Exchange Offer—Exchange Agent.” In the alternative, you can tender your additional senior secured notes by book-entry delivery following the procedures described in this prospectus. For more information on tendering your additional senior secured notes, please refer to the section in this prospectus entitled “The Exchange Offer—Procedures for Tendering Additional Senior Secured Notes.” |

Special Procedures for Beneficial Owners | If you are a beneficial owner of additional senior secured notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender your additional senior secured notes in the exchange offer, you should contact the registered holder promptly and instruct that person to tender on your behalf. |

Guaranteed Delivery Procedures | If you wish to tender your additional senior secured notes and you cannot get the required documents to the exchange agent on time, you may tender your additional senior secured notes by using the guaranteed delivery procedures described under the section of this prospectus entitled “The Exchange Offer—Procedures for Tendering Additional Senior Secured Notes—Guaranteed Delivery Procedure.” |

Withdrawal Rights | You may withdraw the tender of your additional senior secured notes at any time before 11:59 p.m., New York City time, on the expiration date of the exchange offer. To withdraw, you must send a written or facsimile transmission notice of withdrawal to the exchange agent at its address indicated under “The Exchange Offer—Exchange Agent” before 11:59 p.m., New York City time, on the expiration date of the exchange offer. |

Acceptance of Additional Senior Secured Notes and Delivery of Exchange Notes | If all the conditions to the completion of this exchange offer are satisfied, we will accept any and all additional senior secured notes that are properly tendered in this exchange offer on or before 11:59 p.m., New York City time, on the expiration date. We will return any initial note that we do not accept for exchange to you without expense promptly after the expiration date. We will deliver the additional exchange notes to you promptly after the expiration date and acceptance of your additional senior secured notes for exchange. Please refer to the section in this prospectus entitled “The Exchange Offer—Acceptance of Additional Senior Secured Notes for Exchange; Delivery of Exchange Notes.” |

5

Federal Income Tax Considerations Relating to the Exchange Offer | Exchanging your additional senior secured notes for additional exchange notes will not be a taxable event to you for United States federal income tax purposes. Please refer to the section of this prospectus entitled “Certain U.S. Federal Income Tax Considerations.” |

Exchange Agent | Wilmington Trust, National Association is serving as exchange agent in the exchange offer. |

Fees and Expenses | We will pay all expenses related to this exchange offer. Please refer to the section of this prospectus entitled “The Exchange Offer—Fees and Expenses.” |

Use of Proceeds | We will not receive any proceeds from the issuance of the additional exchange notes. We are making this exchange offer solely to satisfy certain of our obligations under our registration rights agreement entered into in connection with the offering of the additional senior secured notes. |

Consequences to Holders Who Do Not Participate in the Exchange Offer | All untendered additional senior secured notes will continue to be subject to the restrictions on transfer provided for in the additional senior secured notes and in the indenture. In general, the additional senior secured notes may not be offered or sold unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register under the Securities Act any additional senior secured notes that remain outstanding after completion of the exchange offer. |

| | Please refer to the section of this prospectus entitled “The Exchange Offer—Your Failure to Participate in the Exchange Offer Will Have Adverse Consequences.” |

Resales of the Additional Exchange Notes | Based on an interpretation by the staff of the SEC set forth in no-action letters issued to third parties, we believe that the additional exchange notes issued pursuant to the exchange offers in exchange for additional senior secured notes may be offered for resale, resold and otherwise transferred by you (unless you are our “affiliate” within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that you: |

| | • | | are acquiring the additional exchange notes in the ordinary course of business; and |

| | • | | have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person or entity, including any of the Issuers’ affiliates, to participate in, a distribution of the additional exchange notes. |

6

| | In addition, each participating broker-dealer that receives exchange notes for its own account pursuant to the exchange offers in exchange for additional senior secured notes that were acquired as a result of market-making or other trading activity must also acknowledge that it will deliver a prospectus in connection with any resale of the additional exchange notes. For more information, see “Plan of Distribution.” Any holder of additional senior secured notes, including any broker-dealer, who |

| | • | | does not acquire the additional exchange notes in the ordinary course of its business, or |

| | • | | tenders in the exchange offers with the intention to participate, or for the purpose of participating, in a distribution of exchange notes, |

| | cannot rely on the position of the staff of the SEC expressed in Exxon Capital Holdings Corporation, Morgan Stanley & Co., Incorporated or similar no-action letters and, in the absence of an exemption, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with the resale of the additional exchange notes. |

| | Please refer to the sections of this prospectus entitled “The Exchange Offer—Procedures for Tendering Additional Senior Secured Notes—Proper Execution and Delivery of Letters of Transmittal,” “Risk Factors—Risks Related to the Exchange Offer—Some persons who participate in the exchange offer must deliver a prospectus in connection with resales of the additional exchange notes” and “Plan of Distribution.” |

7

Summary of Terms of the Additional Exchange Notes

The summary below describes the principal terms of the additional exchange notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The “Description of Additional Exchange Notes” section of this prospectus contains more detailed descriptions of the terms and conditions of the additional exchange notes.

Issuers | Verso Paper Holdings LLC, a Delaware limited liability company (the “Company”), and Verso Paper Inc., a Delaware corporation. Verso Paper Inc. is a wholly owned subsidiary of the Company and was incorporated in Delaware for the sole purpose of serving as co-issuer of the notes, our secured notes, our second priority senior secured notes, our second priority senior secured floating rate notes and our senior subordinated notes. Investors in the additional exchange notes should not expect Verso Paper Inc. to have the ability to service the interest and principal obligations on the additional exchange notes. When used in this prospectus, “Issuers” refers to the Company and Verso Paper Inc. |

Notes Offered | $72,882,000 aggregate principal amount of 11.75% Senior Secured Notes due 2019. |

Maturity Date | January 15, 2019;provided, however, that, if as of 45 days prior to the maturity dates of our 11.375% Senior Subordinated Notes due 2016, more than $100,000,000 of such senior subordinated notes remains outstanding, the notes will mature on that day. |

Interest Rate | The additional exchange notes will accrue interest from January 15, 2013 at the rate of 11.75% per annum and will be payable in cash. |

Interest Payment Dates | January 15 and July 15 of each year, commencing on July 15, 2013. |

Denominations | Minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof; provided that notes may be issued in denominations of less than $2,000 solely to accommodate book-entry positions that have been created by a DTC participant in denominations of less than $2,000. |

Guarantees | Our obligations under the notes will be fully and unconditionally guaranteed by the Company’s direct and indirect restricted subsidiaries (other than Verso Paper Inc., Bucksport Leasing LLC and Verso Quinnesec REP LLC) that are wholly owned domestic subsidiaries on the issue date and guarantee indebtedness under the asset based revolving facility (“ABL Facility”) and the cash flow facility (“Cash Flow Facility”). |

Ranking | The notes are our senior secured obligations and: |

| | • | | rank senior in right of payment to all of the Issuers’ and the guarantors’ existing and future subordinated indebtedness; |

8

| | • | | rank equally in right of payment with all of the Issuers’ and the guarantors’ existing and future senior indebtedness, including our ABL Facility and our Cash Flow Facility; |

| | • | | are effectively senior to all of the Issuers’ and the guarantors’ indebtedness under the ABL Facility, to the extent of the value of the Notes Priority Collateral; |

| | • | | are effectively junior to all of the Issuers’ and the guarantors’ indebtedness under the ABL Facility, to the extent of the value of the ABL Priority Collateral; |

| | • | | are effectively senior to all of the Issuers’ and the guarantors’ indebtedness under the secured notes, second priority senior secured notes and related guarantees and the second priority senior secured floating rate notes and related guarantees, to the extent of the value of the collateral securing the additional exchange notes, and to all unsecured indebtedness of the Issuers and the guarantors; |

| | • | | are effectively pari passu with all of the Issuers’ and the guarantors’ indebtedness under the Cash Flow Facility and all future Other First-Priority Lien Obligations (as defined in the “Description of Additional Exchange Notes”), to the extent of the value of the Notes Priority Collateral; and |

| | • | | are effectively subordinated in right of payment to all existing and future indebtedness, preferred stock and other liabilities of our non-guarantor subsidiaries (other than indebtedness, preferred stock and liabilities held by an Issuer or a guarantor). |

| | As of September 30, 2012, after giving effect to the Refinancing Transactions, the notes would have been: |

| | • | | senior to $271.6 million of secured notes and $409.3 million of existing second-lien notes, to the extent of the value of the collateral securing the additional exchange notes, and contractually senior in right of payment to $142.5 million of our senior subordinated notes; and |

| | • | | effectively junior to $35.0 million outstanding borrowings under our ABL Facility, to the extent of the value of the ABL Priority Collateral, with $43.3 million of letters of credit outstanding, leaving $71.7 million available for borrowing (based on a borrowing base of $150.7 million and a maximum committed amount of $150.0 million). |

Collateral | The additional exchange notes are secured by first-priority security interests in the “Notes Priority Collateral” (which generally included most fixed assets of the Issuers and the guarantors) and by second-priority interests in the “ABL Priority Collateral” (which generally |

9

| | includes most inventory and accounts receivable of the Issuers and the guarantors), in each case subject to Permitted Liens (as defined in the “Description of Additional Exchange Notes”) and as described herein. The Cash Flow Facility and the existing notes (and any Other First Priority Lien Obligations) are secured by security interests in the same collateral securing the additional exchange notes and related guarantees. The security interest securing the Cash Flow Facility (and any Other First-Priority Lien Obligations) rank equal in priority with those securing the additional exchange notes and the guarantees. |

| | Upon an enforcement action or insolvency proceedings, the proceeds from ABL Priority Collateral will be applied first to repay amounts owing under the ABL Facility before being used to repay the notes, the Cash Flow Facility or any Other First-Priority Lien Obligations, while proceeds from our Notes Priority Collateral would be first applied to repay the notes, the Cash Flow Facility and any Other First-Priority Lien Obligations. |

| | See “Description of Additional Exchange Notes—Security for the Notes.” |

Intercreditor Agreements | The right of holders of the notes and the guarantees to receive the proceeds of collateral will be contractually equal to the rights of holders of all of our obligations under the Cash Flow Facility (and any Other First-Priority Lien Obligations). The First-Lien Revolving Facility Collateral Agent (as defined in the “Description of Additional Exchange Notes”) will have the exclusive right (subject to limited exceptions) to exercise remedies and take enforcement actions on behalf of the holders of the First-Priority Lien Obligations (as defined in the “Description of Additional Exchange Notes”) relating to the collateral until such date as the principal amount of commitments outstanding under the Cash Flow Facility is less than $30.0 million. Thereafter, the Authorized First-Lien Collateral Agent (as defined in the “Description of Additional Exchange Notes”) will be appointed by holders of a majority in aggregate outstanding principal amount of the series of First-Priority Lien Obligations that is the largest principal amount of any such series, subject to the First-Lien Revolving Facility Collateral Agent continuing as the Authorized First-Lien Collateral Agent in certain cases. |

| | The collateral agent, on behalf of the holders of the notes, the First-Lien Revolving Facility Collateral Agent and the collateral agent under the ABL Facility have entered into an intercreditor agreement as to the relative priorities of their respective security interests in the ABL Priority Collateral and the Notes Priority Collateral and certain other matters relating to the administration of security interests. So long as first-priority liens on the collateral securing the ABL Facility are outstanding, holders of the notes or lenders under the Cash Flow Facility are not entitled to enforce their security interest under the second-priority lien on such collateral. |

10

| | See “Description of Additional Exchange Notes—Intercreditor Agreements.” |

Optional Redemption | We may redeem the notes, in whole or part, at any time before January 15, 2015, at a redemption price equal to 100% of the principal amount thereof, plus the make-whole premium described in this prospectus, plus accrued and unpaid interest on the date of redemption. |

| | We may redeem the notes, in whole or part, at any time on or after January 15, 2015, at the following redemption prices (expressed as a percentage of principal amount), plus accrued and unpaid interest and additional interest, if any, to the redemption date (subject to the right of holders of record on the relevant record date to receive interest due on the relevant interest payment date), if redeemed during periods set forth below: |

| | | | |

January 15, 2015 through January 14, 2016 | | | 108.813% | |

January 15, 2016 through January 14, 2017 | | | 105.875% | |

January 15, 2017 through January 14, 2018 | | | 102.938% | |

January 15, 2018 and thereafter | | | 100.000% | |

| | In addition, prior to January 15, 2015 we may redeem during each 12-month period up to 10% of the aggregate principal amount of the notes at a redemption price equal to 103% of the principal amount of the notes redeemed, and we may redeem up to 35% of the original aggregate principal amount of the notes with the proceeds of qualified equity offerings at a redemption price equal to 111.75% of the principal amount of the notes redeemed, plus accrued and unpaid interest. |

Change of Control | If we experience a change of control, we may be required to offer to purchase the notes at a purchase price equal to 101% of the principal amount, plus accrued and unpaid interest. |

| | We might not be able to pay you the required price for the notes you present us at the time of a change of control because our ABL Facility or our Cash Flow Facility or other indebtedness may prohibit payment or we might not have enough funds at that time. |

Certain Covenants | The indenture governing the notes contains covenants that, among other things, limits our ability and the ability of our subsidiaries to, among other things: |

| | • | | incur additional indebtedness; |

| | • | | pay dividends or make other distributions or repurchase or redeem our stock; |

11

| | • | | enter into agreements restricting out subsidiaries’ ability to pay dividends; |

| | • | | enter into transactions with affiliates; and |

| | • | | consolidate, merge or sell all or substantially all of our assets. |

| | These covenants are subject to important exceptions and qualifications, which are described under the heading “Description of Additional Exchange Notes” in this prospectus and will not apply so long as the notes are rated investment grade by both rating agencies. |

Book-Entry Form | The additional exchange notes will be issued in registered book-entry form represented by one or more global notes to be deposited with or on behalf of DTC or its nominee. Transfers of the additional exchange notes will only be effected through facilities of DTC. Beneficial interests in the global notes may not be exchanged for certificated notes except in limited circumstances. See “Book-Entry; Delivery and Form.” |

Risk Factors | You should consider all of the information contained in this prospectus before making an investment in the additional exchange notes. In particular, you should consider the risks described under “Risk Factors.” |

12

Summary Historical Financial Data

The following table presents our summary historical financial data as of and for the periods presented. The following information is only a summary and should be read in conjunction with the financial statements included in this prospectus.

The summary historical financial data for the years ended December 31, 2009, 2010 and 2011 have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). The summary historical financial data as of December 31, 2009, 2010 and 2011, and for the years ended December 31, 2009, 2010 and 2011 have been derived from, and should be read in conjunction with, our audited consolidated financial statements. The summary historical financial data as of and for the nine months ended September 30, 2011 and September 30, 2012 and the twelve months ended September 30, 2012, are derived from our unaudited consolidated financial statements and, in the opinion of our management, include all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of the information set forth herein. Interim financial statements are not necessarily indicative of results that may be experienced for the fiscal year or any future reporting period.

13

You should read the following summary historical financial data in conjunction with the Management’s Discussion and Analysis of Results of Operation and Financial Condition with respect to the relevant periods.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year ended

December 31, | | | Nine months ended

September 30, | | | Twelve months

ended

September 30,

2012 | |

| (Dollars and tons in millions) | | 2009 | | | 2010 | | | 2011 | | | 2011 | | | 2012 | | |

Statement of Operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net sales | | $ | 1,360.9 | | | $ | 1,605.3 | | | $ | 1,722.5 | | | $ | 1,272.2 | | | $ | 1,113.6 | | | $ | 1,563.9 | |

Costs and expenses: | | | | | | | | | | | | | | | | | | | | | | | | |

Cost of products sold (exclusive of depreciation, amortization, and depletion) | | | 1,242.7 | | | | 1,410.8 | | | | 1,460.3 | | | | 1,066.5 | | | | 962.3 | | | | 1,356.1 | |

Depreciation, amortization, and depletion | | | 132.7 | | | | 127.4 | | | | 125.3 | | | | 94.2 | | | | 91.3 | | | | 122.4 | |

Selling, general and administrative expenses | | | 61.7 | | | | 70.9 | | | | 78.0 | | | | 59.8 | | | | 56.3 | | | | 74.5 | |

Goodwill impairment | | | — | | | | — | | | | 10.5 | | | | — | | | | — | | | | 10.5 | |

Restructuring and other charges | | | 1.0 | | | | — | | | | 24.5 | | | | — | | | | 97.0 | | | | 121.5 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Operating income (loss) | | | (77.2 | ) | | | (3.8 | ) | | | 23.9 | | | | 51.7 | | | | (93.3 | ) | | | (121.1 | ) |

Interest income | | | (0.2 | ) | | | (0.1 | ) | | | (1.6 | ) | | | (1.2 | ) | | | (1.1 | ) | | | (1.5 | ) |

Interest expense | | | 116.1 | | | | 122.5 | | | | 122.2 | | | | 91.5 | | | | 94.9 | | | | 125.6 | |

Other (income) expense, net(1) | | | (273.8 | ) | | | (0.7 | ) | | | 25.8 | | | | 25.9 | | | | 7.5 | | | | 7.4 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) | | $ | 80.7 | | | $ | (125.5 | ) | | $ | (122.5 | ) | | $ | (64.5 | ) | | $ | (194.6 | ) | | $ | (252.6 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Balance Sheet Data (at period end): | | | | | | | | | | | | | | | | | | | | | | | | |

Working capital | | $ | 210.4 | | | $ | 162.3 | | | $ | 142.9 | | | $ | 164.9 | | | $ | 79.4 | | | $ | 79.4 | |

Property, plant and equipment, net | | | 1,022.6 | | | | 972.7 | | | | 934.7 | | | | 949.4 | | | | 818.7 | | | | 818.7 | |

Total assets | | | 1,560.3 | | | | 1,530.5 | | | | 1,444.4 | | | | 1,465.2 | | | | 1,215.8 | | | | 1,215.8 | |

Total debt | | | 1,118.3 | | | | 1,172.7 | | | | 1,201.1 | | | | 1,200.0 | | | | 1,221.9 | | | | 1,221.9 | |

Total equity (deficit) | | | 198.0 | | | | 71.4 | | | | (61.2 | ) | | | 6.8 | | | | (247.0 | ) | | | (247.0 | ) |

| | | | | | |

Statement of Cash Flows Data: | | | | | | | | | | | | | | | | | | | | | | | | |

Cash provided by (used in) operating activities | | $ | 180.1 | | | $ | 75.8 | | | $ | 14.6 | | | $ | (47.6 | ) | | $ | (37.0 | ) | | $ | 25.2 | |

Cash used in investing activities | | | (34.1 | ) | | | (98.3 | ) | | | (66.2 | ) | | | (47.2 | ) | | | (44.6 | ) | | | (63.6 | ) |

Cash (used in) provided by financing activities | | | (115.8 | ) | | | 25.4 | | | | (6.3 | ) | | | (6.2 | ) | | | (3.1 | ) | | | (3.2 | ) |

| | | | | | |

Other Financial and Operating Data: | | | | | | | | | | | | | | | | | | | | | | | | |

EBITDA(2) | | $ | 329.3 | | | $ | 124.3 | | | $ | 123.4 | | | $ | 120.0 | | | $ | (9.5 | ) | | $ | (6.1 | ) |

Adjusted EBITDA(3) | | | 76.9 | | | | 132.0 | | | | 202.8 | | | | 155.0 | | | | 99.0 | | | | 146.8 | |

Capital expenditures | | | (34.2 | ) | | | (73.6 | ) | | | (90.3 | ) | | | (67.8 | ) | | | (46.8 | ) | | | (69.3 | ) |

Total tons sold | | | 1,724.5 | | | | 2,063.6 | | | | 2,023.4 | | | | 1,493.0 | | | | 1,358.8 | | | | 1,889.2 | |

| (1) | Other income was $273.8 million for the year ended December 31, 2009, which includes $238.9 million in net benefits from alternative fuel mixture tax credits provided by the U.S. government for our use of black liquor in alternative fuel mixtures and $31.3 million in net gains related to the early retirement of debt. |

| (2) | EBITDA consists of earnings before interest, taxes, depreciation, and amortization. EBITDA is a measure commonly used in our industry, and we present EBITDA to enhance your understanding of our operating performance. We use EBITDA as a way of evaluating our performance relative to that of our peers. We believe that EBITDA is an operating performance measure, and not a liquidity measure, that provides investors and analysts with a measure of operating results unaffected by differences in capital structures, capital investment cycles and ages of related assets among otherwise comparable companies. However, EBITDA is not a measurement of financial performance under GAAP, and our EBITDA may not be comparable to similarly titled measures of other companies. You should consider our EBITDA in addition to and not as a substitute for, or superior to, our operating or net income determined in accordance with GAAP or cash flows from operating activities, determined in accordance with GAAP. |

14

The following table reconciles net income (loss) to EBITDA for the periods presented:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year ended

December 31, | | | Nine months ended

September 30, | | | Twelve months

ended

September 30,

2012 | |

| (Dollars in millions) | | 2009 | | | 2010 | | | 2011 | | | 2011 | | | 2012 | | |

Reconciliation of net income (loss) to EBITDA: | | | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) | | $ | 80.7 | | | $ | (125.5 | ) | | $ | (122.5 | ) | | $ | (64.5 | ) | | $ | (194.6 | ) | | $ | (252.6 | ) |

Interest expense, net | | | 115.9 | | | | 122.4 | | | | 120.6 | | | | 90.3 | | | | 93.8 | | | | 124.1 | |

Depreciation, amortization, and depletion | | | 132.7 | | | | 127.4 | | | | 125.3 | | | | 94.2 | | | | 91.3 | | | | 122.4 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

EBITDA | | $ | 329.3 | | | $ | 124.3 | | | $ | 123.4 | | | $ | 120.0 | | | $ | (9.5 | ) | | $ | (6.1 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| (3) | Adjusted EBITDA is a non-GAAP financial measure. Adjusted EBITDA is EBITDA further adjusted to eliminate the impact of certain items that we do not consider to be indicative of the performance of our ongoing operations and other pro forma adjustments permitted in calculating covenant compliance under the indentures governing our notes. You are encouraged to evaluate each adjustment and to consider whether the adjustment is appropriate. In addition, in evaluating adjusted EBITDA, you should be aware that in the future, we may incur expenses similar to the adjustments included in the presentation of adjusted EBITDA. We believe that Adjusted EBITDA is an important measure that supplements discussions and analysis of our results of operations. We believe that it is useful to investors to provide disclosures of our results of operations on the same basis as that used by management. Management relies upon Adjusted EBITDA as a primary measure to review and assess operating performance of our business and the management team. Adjusted EBITDA is also used to determine compliance with certain covenants contained in our ABL Facility and Cash Flow Facility, the notes and our other existing notes that restrict our ability to incur additional debt, make certain restricted payments or make certain acquisitions if we cannot meet specified ratios of Adjusted EBITDA to total net first-lien indebtedness and Adjusted EBITDA to fixed charges. Management and investors review both the overall performance (GAAP net income) and operating performance (Adjusted EBITDA) of our business. Adjusted EBITDA is not a measure of financial performance under GAAP, and you should consider Adjusted EBITDA in addition to and not as a substitute for, or superior to, our operating or net income determined in accordance with GAAP or cash flows from operating activities, determined in accordance with GAAP. Because Adjusted EBITDA is not a measurement determined in accordance with GAAP and is susceptible to varying calculations, Adjusted EBITDA, as presented, may not be comparable to other similarly titled measures presented by other companies. There may also be additional adjustments to Adjusted EBITDA under the agreements governing our material debt obligations. |

15

The following table reconciles cash flow from operations to Adjusted EBITDA for the periods presented:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year ended

December 31, | | | Nine months ended

September 30, | | | Twelve months

ended

September 30,

2012 | |

| (Dollars in millions) | | 2009 | | | 2010 | | | 2011 | | | 2011 | | | 2012 | | |

Reconciliation of cash flows to EBITDA and Adjusted EBITDA: | | | | | | | | | | | | | | | | | | | | | | | | |

Cash flow from operating activities | | $ | 180.1 | | | $ | 75.8 | | | $ | 14.6 | | | $ | (47.6 | ) | | $ | (37.0 | ) | | $ | 25.2 | |

Amortization of debt issuance costs | | | (5.3 | ) | | | (5.3 | ) | | | (5.0 | ) | | | (3.8 | ) | | | (3.7 | ) | | | (4.9 | ) |

Accretion of discount on long-term debt | | | (2.1 | ) | | | (3.7 | ) | | | (4.1 | ) | | | (3.1 | ) | | | (1.3 | ) | | | (2.3 | ) |

Interest income | | | (0.2 | ) | | | (0.1 | ) | | | (1.6 | ) | | | (1.2 | ) | | | (1.1 | ) | | | (1.5 | ) |

Interest expense | | | 116.1 | | | | 122.5 | | | | 122.2 | | | | 91.5 | | | | 94.9 | | | | 125.6 | |

Gain (loss) on early extinguishment | | | 31.3 | | | | 0.3 | | | | (26.1 | ) | | | (26.1 | ) | | | (8.2 | ) | | | (8.2 | ) |

Goodwill impairment | | | — | | | | — | | | | (10.5 | ) | | | — | | | | — | | | | (10.5 | ) |

Asset impairment | | | — | | | | — | | | | — | | | | — | | | | (75.7 | ) | | | (75.7 | ) |

Equity award expense | | | (0.6 | ) | | | (1.7 | ) | | | (2.4 | ) | | | (1.8 | ) | | | (2.3 | ) | | | (2.9 | ) |

Other, net | | | (28.4 | ) | | | 4.7 | | | | (1.3 | ) | | | 0.8 | | | | 2.8 | | | | 0.7 | |

Changes in assets and liabilities, net | | | 38.4 | | | | (68.2 | ) | | | 37.6 | | | | 111.3 | | | | 22.1 | | | | (51.6 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

EBITDA | | $ | 329.3 | | | $ | 124.3 | | | $ | 123.4 | | | $ | 120.0 | | | $ | (9.5 | ) | | $ | (6.1 | ) |

Alternative fuel tax credit(1) | | | (238.9 | ) | | | — | | | | — | | | | — | | | | — | | | | — | |

Loss (gain) on early extinguishment of debt, net(2) | | | (31.3 | ) | | | (0.3 | ) | | | 26.1 | | | | 26.1 | | | | 8.2 | | | | 8.2 | |

Goodwill impairment(3) | | | — | | | | — | | | | 10.5 | | | | — | | | | — | | | | 10.5 | |

Restructuring and other charges(4) | | | 1.0 | | | | — | | | | 24.5 | | | | — | | | | 97.0 | | | | 121.5 | |

Hedge losses (gains)(5) | | | — | | | | — | | | | 7.5 | | | | — | | | | (3.6 | ) | | | 3.9 | |

Equity award expense(6) | | | 0.6 | | | | 1.7 | | | | 2.4 | | | | 1.8 | | | | 2.3 | | | | 2.9 | |

Other items, net(7) | | | 16.2 | | | | 6.3 | | | | 8.4 | | | | 7.1 | | | | 4.6 | | | | 5.9 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Adjusted EBITDA before pro forma effects of profitability program | | $ | 76.9 | | | $ | 132.0 | | | $ | 202.8 | | | $ | 155.0 | | | $ | 99.0 | | | $ | 146.8 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Represents earnings from the federal government’s program which provides incentives for the use of alternative fuels. |

| (2) | Represents net losses (gains) related to debt refinancing. |

| (3) | Represents impairment of goodwill allocated to the coated paper segment. |

| (4) | Represents costs in 2012 related to the closure of the Sartell mill, costs in 2011 associated with the shut-down of three paper machines and transition costs in 2009 related to the acquisition of our business from International Paper Company. |

| (5) | Represents unrealized losses (gains) on energy-related derivative contracts. |

| (6) | Represents amortization of non-cash incentive compensation. |

| (7) | Represents earnings adjustments for product development costs and other miscellaneous items. |

16

RISK FACTORS

Investing in the additional exchange notes in this exchange offer involves a high degree of risk. You should carefully consider the risk factors set forth below, as well as the other information contained in this prospectus, before participating in the exchange offer. Any of the following risks could materially and adversely affect our business, financial condition or results of operations. In addition, the risks described below are not the only risks that we face. Additional risks and uncertainties not currently known to us or those that we currently view to be immaterial could also materially and adversely affect our business, financial condition or results of operations. In any such case, you may lose all or a part of your original investment. As used herein, “existing notes” refers to our outstanding initial senior secured notes, existing exchange notes, secured notes, second priority senior secured notes, second priority senior secured floating rate notes and our senior subordinated notes.

Risks Related to the Exchange Offer

If you do not properly tender your additional senior secured notes, you will continue to hold unregistered additional senior secured notes and be subject to the same limitations on your ability to transfer additional senior secured notes.

We will only issue exchange notes in exchange for additional senior secured notes that are timely received by the exchange agent together with all required documents, including a properly completed and signed letter of transmittal. Therefore, you should allow sufficient time to ensure timely delivery of the additional senior secured notes and you should carefully follow the instructions on how to tender your additional senior secured notes. Neither we nor the exchange agent are required to tell you of any defects or irregularities with respect to your tender of the additional senior secured notes. If you are eligible to participate in the exchange offer and do not tender your additional senior secured notes or if we do not accept your additional senior secured notes because you did not tender your additional senior secured notes properly, then, after we consummate the exchange offer, you will continue to hold additional senior secured notes that are subject to the existing transfer restrictions and will no longer have any registration rights or be entitled to any additional interest with respect to the additional senior secured notes. In addition:

| | • | | if you tender your additional senior secured notes for the purpose of participating in a distribution of the additional exchange notes, you will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale of the additional exchange notes; and |

| | • | | if you are a broker-dealer that receives exchange notes for your own account in exchange for additional senior secured notes that you acquired as a result of market-making activities or any other trading activities, you will be required to acknowledge that you (i) have not entered into any arrangement or understanding with the Issuers or an affiliate of the Issuers to distribute those exchange notes and (ii) will deliver a prospectus in connection with any resale of those exchange notes. |

We have agreed that, for a period of 180 days after the exchange offer is consummated, we will make this prospectus available to any broker-dealer for use in connection with any resales of the additional exchange notes.

You may have difficulty selling the additional senior secured notes that you do not exchange.

If you do not exchange your additional senior secured notes for exchange notes in the exchange offer, you will continue to be subject to the restrictions on transfer of your additional senior secured notes described in the legend on your additional senior secured notes. The restrictions on transfer of your additional senior secured notes arise because we issued the additional senior secured notes under exemptions from, or in transactions not subject to, the registration requirements of the Securities Act and applicable state securities laws. In general, you may only offer or sell the additional senior secured notes if they are registered under the Securities Act and applicable state securities laws, or offered and sold under an exemption from these requirements. Except as

17

required by the registration rights agreements, we do not intend to register the additional senior secured notes under the Securities Act. The tender of additional senior secured notes under the exchange offer will reduce the principal amount of the currently outstanding additional senior secured notes. Due to the corresponding reduction in liquidity, this may have an adverse effect upon, and increase the volatility of, the market price of any currently outstanding additional senior secured notes that you continue to hold following completion of the exchange offer. See “The Exchange Offer—Your Failure to Participate in the Exchange Offer Will Have Adverse Consequences.”

The issuance of the additional exchange notes may adversely affect the market for the additional senior secured notes.

To the extent the additional senior secured notes are tendered and accepted in the exchange offer, the trading market for the untendered and tendered but unaccepted additional senior secured notes could be adversely affected. Because we anticipate that most holders of the additional senior secured notes will elect to exchange their additional senior secured notes for exchange notes due to the absence of restrictions on the resale of exchange notes under the Securities Act, we anticipate that the liquidity of the market for any additional senior secured notes remaining after the completion of this exchange offer may be substantially limited. Please refer to the section in this prospectus entitled “The Exchange Offer—Your Failure to Participate in the Exchange Offer Will Have Adverse Consequences.”

Some persons who participate in the exchange offer must deliver a prospectus in connection with resales of the additional exchange notes.

Based on interpretations of the staff of the SEC contained in Exxon Capital Holdings Corp., SEC no-action letter (April 13, 1988), Morgan Stanley & Co. Inc., SEC no-action letter (June 5, 1991) and Shearman & Sterling, SEC no-action letter (July 2, 1983), we believe that you may offer for resale, resell or otherwise transfer the additional exchange notes without compliance with the registration and prospectus delivery requirements of the Securities Act. However, in some instances described in this prospectus under “Plan of Distribution,” you will remain obligated to comply with the registration and prospectus delivery requirements of the Securities Act to transfer your additional exchange notes. In these cases, if you transfer any additional exchange note without delivering a prospectus meeting the requirements of the Securities Act or without an exemption from registration of your additional exchange notes under the Securities Act, you may incur liability under the Securities Act. We do not and will not assume, or indemnify you against, this liability.

You must comply with the exchange offer procedures in order to receive new, freely tradable exchange notes.

Delivery of exchange notes in exchange for additional senior secured notes tendered and accepted for exchange pursuant to the exchange offer will be made only after timely receipt by the exchange agent of book-entry transfer of additional senior secured notes into the exchange agent’s account at DTC, as depositary, including an agent’s message (as defined herein). We are not required to notify you of defects or irregularities in tenders of additional senior secured notes for exchange notes. Additional senior secured notes that are not tendered or that are tendered but we do not accept for exchange will, following consummation of the exchange offer, continue to be subject to the existing transfer restrictions under the Securities Act and, upon consummation of the exchange offer, certain registration and other rights under the registration rights agreements will terminate. See “The Exchange Offer—Procedures for Tendering Additional Senior Secured Notes” and “The Exchange Offer—Your Failure to Participate in the Exchange Offer Will Have Adverse Consequences.”

There is no public market for the additional exchange notes, and we do not know if a market will ever develop or, if a market does develop, whether it will be sustained. If an active market does not develop for the additional exchange notes, you may not be able to resell your exchange notes at a particular time or at favorable prices.

We cannot assure you that a liquid market for the additional exchange notes will develop or, if developed, that it will continue or that you will be able to sell your exchange notes at a particular time or that the prices that

18

you receive when you sell the additional exchange notes will be favorable. Historically, the market for non-investment grade debt has been subject to disruptions that have caused substantial volatility in the prices of securities similar to the additional exchange notes and we cannot assure you that any such disruptions may not adversely affect the prices at which you may sell your exchange notes.

We do not intend to apply for listing or quotation of the additional exchange notes on any securities exchange or automated quotation system. The liquidity of any market for the additional exchange notes is subject to a number of factors, including:

| | • | | the number of holders of exchange notes; |

| | • | | our operating performance and financial condition; |

| | • | | our ability to complete the offer to exchange the additional senior secured notes for the additional exchange notes; |

| | • | | the market for similar securities; |

| | • | | the interest of securities dealers in making a market in the additional exchange notes; and |

| | • | | prevailing interest rates. |

Risks Related to Our Indebtedness

Our substantial indebtedness could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry, expose us to interest rate risk to the extent of our variable rate debt and prevent us from meeting our obligations under these exchange notes and our other indebtedness.

We are a highly leveraged company. As of September 30, 2012, after giving effect to the Refinancing Transactions, the principal amount of our total indebtedness was $1,299.6 million (including a $23.3 million loan from Verso Paper Finance Holdings LLC (“Verso Finance Holdings”) to Chase NMTC Verso Investment Fund). Our high degree of leverage could have important consequences, including:

| | • | | making it more difficult for us to satisfy our obligations with respect to the additional exchange notes; |

| | • | | increasing our vulnerability to general adverse economic and industry conditions; |

| | • | | requiring us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures, research and development efforts and other general corporate purposes; |

| | • | | increasing our vulnerability to and limiting our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| | • | | exposing us to the risk of increased interest rates as borrowings under our ABL Facility and our Cash Flow Facility and our second priority senior secured floating rate notes are subject to variable rates of interest; |

| | • | | placing us at a competitive disadvantage compared to our competitors that have less debt; and |

| | • | | limiting our ability to borrow additional funds. |

The indentures governing the notes and our other existing notes, our Cash Flow Facility and our ABL Facility contain financial and other restrictive covenants that limit our ability to engage in activities that may be in our long-term best interests. Our failure to comply with those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of all of our debts.

In addition, our ability to make distributions to our parent is subject to restrictions in our various debt instruments. For example, the additional exchange notes and our existing notes generally limit the amount of

19

“restricted payments,” including dividends, that we can make to an amount generally equal to 50% of our consolidated net income (as defined in the indentures governing the notes and our other existing notes) since July 1, 2006, subject to satisfaction of certain other tests and certain exceptions. Our ABL Facility and the Cash Flow Facility will only permit dividends to fund debt service of our parent from a “cumulative credit” basket built from proceeds of equity, certain cash flow and certain other items or when certain other payment conditions are met. In addition, the indenture governing the notes and our other existing notes provide certain exceptions to this to permit additional dividends. Our ability to generate net income will depend upon various factors that may be beyond our control. A portion of our debt bears variable rates of interest so our interest expense could increase further in the future. We may not generate sufficient cash flow from operations or be permitted by the terms of our debt instruments to pay dividends or distributions to our parent in amounts sufficient to allow it to pay cash interest on its debt. If Verso Finance Holdings is unable to meet its debt service obligations, it could attempt to restructure or refinance its indebtedness or seek additional equity capital. We cannot assure you that our parent will be able to accomplish these actions on satisfactory terms, if at all.

We will require a significant amount of cash to service our indebtedness and make planned capital expenditures. Our ability to generate cash or refinance our indebtedness depends on many factors beyond our control, including general economic conditions.

Our ability to make payments on and to refinance our indebtedness, including the additional exchange notes, and to fund planned capital expenditures and research and development efforts will depend on our ability to generate cash flow in the future and our ability to borrow under our ABL Facility and our Cash Flow Facility to the extent of available borrowings. This, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control. If adverse regional and national economic conditions persist, worsen, or fail to improve significantly, we could experience decreased revenues from our operations attributable to decreases in wholesale and consumer spending levels and could fail to generate sufficient cash to fund our liquidity needs or fail to satisfy the restrictive covenants and borrowing limitations which we are subject to under our indebtedness. Additionally, until December 31, 2009, the United States government provided an excise tax credit to taxpayers for the use of alternative fuel mixtures. As a result of our use of an alternative fuel mixture containing “black liquor,” a byproduct of pulp production, at our Androscoggin and Quinnesec mills, we recognized $238.9 million of alternative fuel mixture tax credits in the year ended December 31, 2009, including approximately $10 million for claims pending at December 31, 2009. The amount recognized in fiscal 2009 includes amounts received for claims for use of the alternative fuel mixture from September 2008 through December 2009. The tax credit, as it relates to liquid fuels derived from biomass, expired on December 31, 2009.

Based on our current and expected level of operations, we believe our cash flow from operations, available cash and available borrowings under our ABL Facility and our Cash Flow Facility, will be adequate to meet our future liquidity needs for at least the next year.

We cannot assure you, however, that our business will generate sufficient cash flow from operations or that future borrowings will be available to us under our ABL Facility and our Cash Flow Facility, or otherwise in an amount sufficient to enable us to pay our indebtedness, including the notes or to fund our other liquidity needs.

Restrictive covenants in the indentures governing the notes and our other existing notes, our ABL Facility and our Cash Flow Facility may restrict our ability to pursue our business strategies.

The indenture governing the notes and our other existing notes, our ABL Facility and our Cash Flow Facility limit our ability, among other things, to:

| | • | | incur additional indebtedness; |

| | • | | pay dividends or make other distributions or repurchase or redeem our stock; |

| | • | | prepay, redeem or repurchase certain of our indebtedness; |

20

| | • | | sell assets, including capital stock of restricted subsidiaries; |

| | • | | enter into agreements restricting our subsidiaries’ ability to pay dividends; |

| | • | | consolidate, merge, sell or otherwise dispose of all or substantially all of our assets; |

| | • | | enter into transactions with our affiliates; and |

The Cash Flow Facility requires us to maintain a maximum total net first-lien leverage ratio of not more than 3.50 to 1.00 at any time that any portion of the facility is drawn (including outstanding letters of credit). In addition, the ABL Facility will require us to maintain a minimum fixed charge coverage ratio at any time when the average availability (defined as the lesser of the availability under the ABL Facility and the borrowing base at such time, net of any unrestricted cash) is less than the greater of (a) 10% of the lesser of (i) the borrowing base at such time and (ii) the aggregate amount of ABL Facility commitments at such time, and (b) $10.0 million. In that event, we must satisfy a minimum fixed charge coverage ratio of 1.0 to 1.0. The ABL Facility also contains certain other customary affirmative covenants and events of default. Although, on a pro forma basis, after giving effect to the Refinancing Transactions, the fixed charge coverage ratio is not in effect, even after giving effect to the Refinancing Transaction, we are in compliance with the covenant. As of September 30, 2012 and after giving effect to the Refinancing Transactions, we were not subject to the above described financial maintenance covenants.

A breach of any of these restrictive covenants could result in a default under the indentures governing the notes, our other existing notes, the Cash Flow Facility or the ABL Facility. If a default occurs, the holders of these instruments may elect to declare all borrowings thereunder outstanding, together with accrued interest and other fees, to be immediately due and payable. The lenders under our Cash Flow Facility and the ABL Facility would also have the right in these circumstances to terminate any commitments they have to provide further borrowings. If we are unable to repay our indebtedness when due or declared due, the lenders thereunder will also have the right to proceed against the collateral pledged to them to secure the indebtedness. If such indebtedness were to be accelerated, we cannot assure you that our assets would be sufficient to repay in full our indebtedness, including the additional exchange notes, and we could be forced into bankruptcy or liquidation.

Despite our current indebtedness levels, we and our subsidiaries may still be able to incur substantially more debt. This could further exacerbate the risks associated with our substantial leverage.