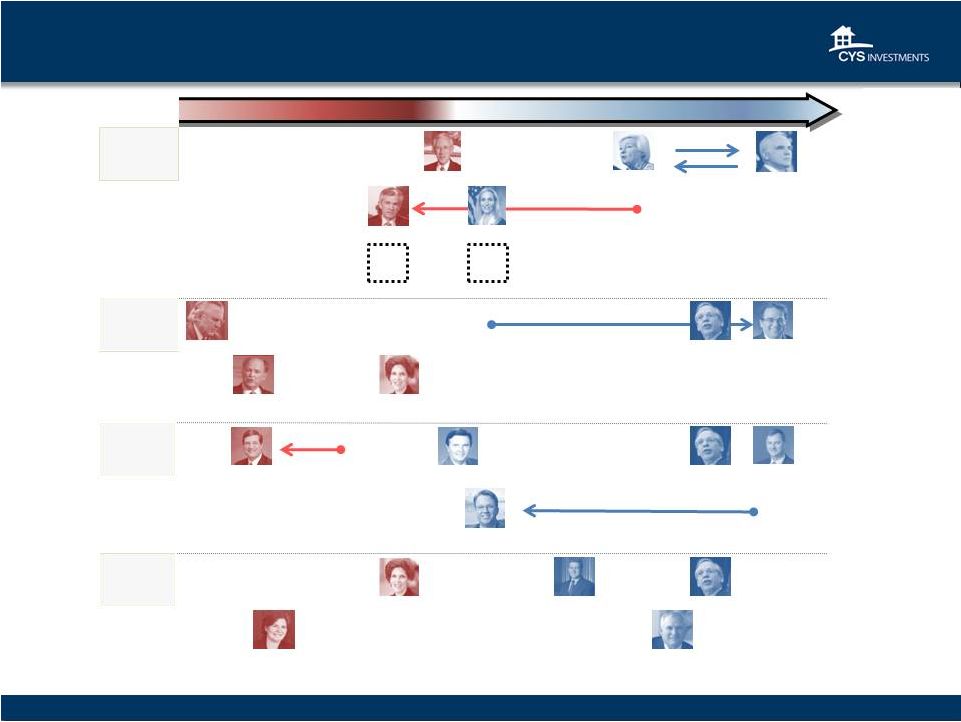

GSE Reform “Headway” Legislative Level of GSE Credit Risk Proposal Government Involvement Implication Sharing Status Corker-Warner Bill Limited: Only under catastrophic scenarios where losses on a pool of mortgages exceeds 10% Completely wound down over 5 years 10% first-loss piece is sold to private entities Corker-Warner under committee discussion but not yet put to vote. Either may become the front runner from the Senate side but both will likely have private capital in the first loss place with several mechanisms for risk sharing Senate Banking Committee voted in favor of the bill 13-9 on May 15. Insufficient support to allow the bill to be brought to the Senate floor for debate/vote. Johnson - Crapo Bill Based on Corker-Warner, limited: only on scenarios where losses on a pool of mortgages exceeds a 10% private loss position. GSE’s wound down over 5 year period, replaced by FMIC. Similar to Corker-Warner, 10% first-loss piece is sold to private entities. PATH Act Very limited: dissolves the GSEs completely and reduces the scope of the FHA/VA guarantee Placed into receivership and completely liquidated with Initially, a 10% risk-sharing program on new GSE and FHA business, although private market securitization is intended eventually to replace GSEs No news. In early 2013, the Path Act seemed to be the clear front-runner on the House side. The final housing finance reform, if it happens, could be a compromise between the PATH Act and whatever comes out of the Senate Delaney-Carney-Himes Limited: Ginnie Mae is required to provide an explicit government guarantee once the 5% risk slice is eroded when one of the private monoline insurers defaults GSEs will be slowly wound down and eventually converted into private reinsurers with limited capacities to take on mortgage credit risk 5% first-loss piece on each new Ginnie Mae securitization, as well as a 10% pro-rata risk slice on the top 95% of each Ginnie Mae securitization Source: Barclays, CYS 12 |