UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-22056

John Hancock Tax-Advantaged Global Shareholder Yield Fund

(Exact name of registrant as specified in charter)

200 Berkeley Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Salvatore Schiavone

Treasurer

200 Berkeley Street

Boston, Massachusetts 02116

(Name and address of agent for service)

Registrant's telephone number, including area code:617-663-4497

| Date of fiscal year end: | October 31 |

| Date of reporting period: | October 31, 2019 |

ITEM 1. REPORTS TO STOCKHOLDERS.

John Hancock

Tax-Advantaged Global Shareholder Yield Fund

Ticker: HTY

Annual report 10/31/19

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the fund's shareholder reports such as this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the transfer agent or from your financial intermediary. Instead, the reports will be made available on our website, and you will be notified by mail each time a report is posted and be provided with a website link to access the report.

If you have already elected to receive shareholder reports electronically, you will not be affected by this change and you do not need to take any action. You may elect to receive shareholder reports and other communications electronically by calling the transfer agent, Computershare, at 800-852-0218, by going to "Communication Preferences" at computershare.com/investor, or by contacting your financial intermediary.

You may elect to receive all reports in paper, free of charge, at any time. You can inform the transfer agent or your financial intermediary that you wish to continue receiving paper copies of your shareholder reports by following the instructions listed above. Your election to receive reports in paper will apply to all funds held with John Hancock Investment Management or your financial intermediary.

A message to shareholders

Dear shareholder,

It was a volatile time for global stock investors during the 12 months ended October 31, 2019, although many segments of the market delivered attractive absolute returns for the period. Uncertainty surrounding global trade, a slowdown in China, sluggish growth in Europe, and the latest Brexit developments led to some dramatic swings in performance. Central banks introduced stimulative measures late in the period, with the U.S. Federal Reserve cutting interest rates three times and the European Central Bank rolling out a sweeping package of monetary and fiscal support for the eurozone economy.

Economic fundamentals around the globe are relatively mixed today, with the United States appearing fairly healthy, Europe on decidedly less stable footing, and emerging economies on divergent paths. With an uncertain outlook, it's safe to say there are sure to be patches of market turbulence as the year goes on. As always, your best resource in unpredictable markets is your financial advisor, who can help position your portfolio so that it's sufficiently diversified to meet your long-term objectives and to withstand the inevitable bouts of market volatility along the way.

On behalf of everyone at John Hancock Investment Management, I'd like to take this opportunity to welcome new shareholders and thank existing shareholders for the continued trust you've placed in us.

Sincerely,

Andrew G. Arnott

President and CEO,

John Hancock Investment Management

Head of Wealth and Asset Management,

United States and Europe

This commentary reflects the CEO's views as of this report's period end and are subject to change at any time. Diversification does not guarantee investment returns and does not eliminate risk of loss. All investments entail risks, including the possible loss of principal. For more up-to-date information, you can visit our website at jhinvestments.com.

John Hancock

Tax-Advantaged Global Shareholder Yield Fund

Table of contents

| 2 | Your fund at a glance | |

| 5 | Manager's discussion of fund performance | |

| 7 | Fund's investments | |

| 12 | Financial statements | |

| 15 | Financial highlights | |

| 16 | Notes to financial statements | |

| 23 | Report of independent registered public accounting firm | |

| 24 | Tax information | |

| 25 | Additional information | |

| 28 | Continuation of investment advisory and subadvisory agreements | |

| 35 | Trustees and Officers | |

| 39 | More information |

INVESTMENT OBJECTIVE

The fund seeks to provide total return consisting of a high level of current income and gains and long-term capital appreciation. The fund will seek to achieve favorable after-tax returns for shareholders by seeking to minimize the U.S. federal income tax consequences on income and gains generated by the fund.

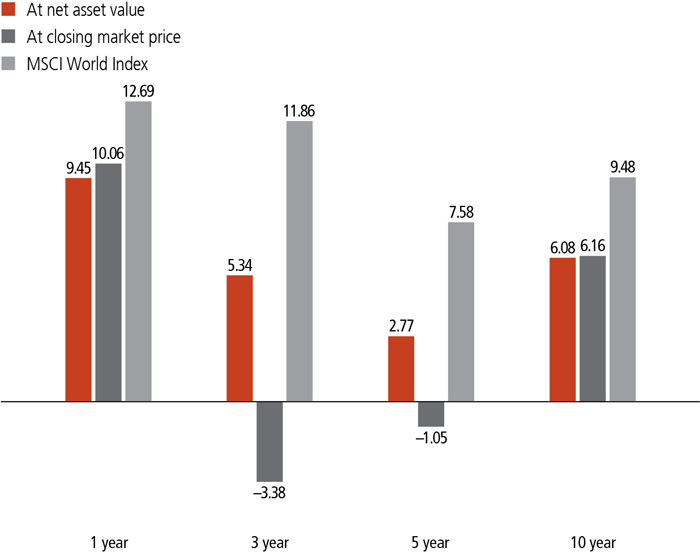

AVERAGE ANNUAL TOTAL RETURNS AS OF 10/31/19 (%)

The MSCI World Index is a free float-adjusted capitalization-weighted index that is designed to measure the equity market performance of developed markets.

It is not possible to invest directly in an index. Index figures do not reflect expenses or sales charges, which would result in lower returns.

The performance data contained within this material represents past performance, which does not guarantee future results.

Investment returns and principal value will fluctuate and a shareholder may sustain losses. Further, the fund's performance at net asset value (NAV) is different from the fund's performance at closing market price because the closing market price is subject to the dynamics of secondary market trading. Market risk may be augmented when shares are purchased at a premium to NAV or sold at a discount to NAV. Current month-end performance may be higher or lower than the performance cited. The fund's most recent performance can be found at jhinvestments.com or by calling 800-852-0218.

PERFORMANCE HIGHLIGHTS OVER THE LAST TWELVE MONTHS

Accommodative policy supported equity gains

Global stocks delivered solid performance amid increased volatility, with easing monetary policy from central banks overcoming an ongoing trade war and slowing global economic growth.

Limited exposure to growth sectors affected performance

The fund had a positive return at NAV but underperformed its comparative index, the MSCI World Index, due to stock selection in the consumer staples and communication services sectors, an overweight in energy, and lower exposure to information technology.

Utilities and financial stocks had a positive influence

Stock selection in the utilities and financials sectors and an overweight in utilities contributed the most to relative results.

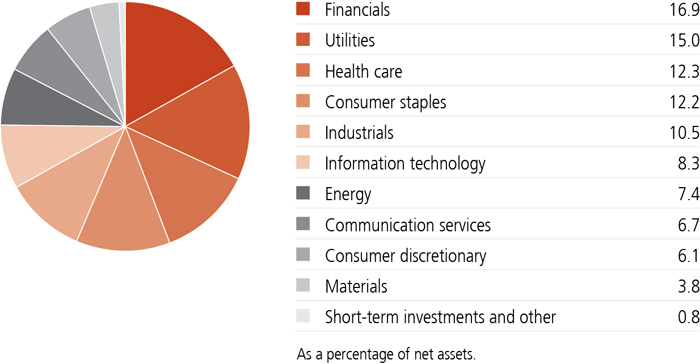

SECTOR COMPOSITION AS OF 10/31/19 (%)

A note about risks

As is the case with all exchange-listed closed-end funds, shares of this fund may trade at a discount or a premium to the fund's net asset value (NAV). An investment in the fund is subject to investment and market risks, including the possible loss of the entire principal invested. The value of a company's equity securities is subject to changes in its financial condition and overall market and economic conditions. Foreign investing, especially in emerging markets, has additional risks, such as currency and market volatility and political and social instability. There is no guarantee prior distribution levels will be maintained, and distributions may include a substantial return of capital. For the fiscal year ended October 31, 2019, the fund's aggregate distributions included a tax return of capital of $0.22 per share, or 34% of aggregate distributions, which may increase the potential tax gain or decrease the potential tax loss of a subsequent sale of shares of the fund. See the financial highlights and notes to the financial statements for details of the return of capital and risks associated with distributions made by the fund. Fixed-income investments are subject to interest-rate and credit risk; their value will normally decline as interest rates rise or if an issuer, grantor, or counterparty is unable or unwilling to make principal, interest, or settlement payments. Investments in higher-yielding, lower-rated securities are subject to a higher risk of default. An issuer of securities held by the fund may default, have its credit rating downgraded, or otherwise perform poorly, which may affect fund performance. Liquidity—the extent to which a security may be sold or a derivative position closed without negatively affecting its market value—may be impaired by reduced trading volume, heightened volatility, rising interest rates, and other market conditions. Focusing on a particular industry or sector may increase the fund's volatility and make it more susceptible to market, economic, and regulatory risks as well as other factors affecting those industries or sectors. Derivatives transactions, such as hedging and other strategic transactions, may increase a fund's volatility and could produce disproportionate losses, potentially more than the fund's principal investment. Cybersecurity incidents may allow an unauthorized party to gain access to fund assets, customer data, or proprietary information, or cause a fund or its service providers to suffer data corruption or lose operational functionality. Similar incidents affecting issuers of fund securities may negatively impact performance.

Global equities withstood increasing periods of volatility to deliver solid returns. A continued trade standoff between the United States and China, as well as signs of slowing global growth, centered in manufacturing, were the primary risks during the period. Global monetary policy, meanwhile, turned accommodative, with the U.S. Federal Reserve reducing its interest-rate target three times and the European Central Bank announcing plans to resume quantitative easing. The fund's benchmark, the MSCI World Index, advanced 12.7%, led by the income-oriented real estate and utilities sectors as well as information technology, communication services, and industrials; financials and healthcare lagged the market.

How did the fund respond to these market conditions?

Amid a backdrop of increased volatility and slowing global growth, the yield-oriented companies that we favor outperformed, and while the fund produced a positive return, it underperformed its benchmark. Asset allocation detracted from relative performance while stock selection contributed. Stock selection in the financials, utilities, and consumer discretionary sectors and an overweight in utilities were the primary contributors. Stock selection in the consumer staples and communication services sectors as well as an overweight in energy and an underweight in information technology hurt performance.

What were the main areas of weakness?

Kraft Heinz Company, a North American packaged food and beverage company, was among the leading detractors following disappointing results and an abrupt

| TOP 10 HOLDINGS AS OF 10/31/19 (%) | TOP 10 COUNTRIES AS OF 10/31/19 (%) | |||

| Eaton Corp. PLC | 2.5 | United States | 54.0 | |

| MetLife, Inc. | 2.0 | United Kingdom | 10.8 | |

| Unilever PLC | 1.9 | France | 7.4 | |

| Allianz SE | 1.9 | Canada | 6.2 | |

| AXA SA | 1.8 | Germany | 6.1 | |

| Duke Energy Corp. | 1.8 | Italy | 3.3 | |

| BCE, Inc. | 1.8 | Switzerland | 2.9 | |

| Texas Instruments, Inc. | 1.8 | Australia | 1.8 | |

| Verizon Communications, Inc. | 1.7 | Japan | 1.7 | |

| Entergy Corp. | 1.7 | Netherlands | 1.4 | |

| TOTAL | 18.9 | TOTAL | 95.6 | |

| As a percentage of net assets. | As a percentage of net assets. | |||

| Cash and cash equivalents are not included. | Cash and cash equivalents are not included. | |||

change in its capital allocation policy. Occidental Petroleum Corp., a global oil and natural gas exploration and production company, underperformed as deteriorating trade negotiations led to investor concerns on global oil demand and falling oil and gas prices.

Which holdings contributed the most to performance?

Utilities were among the top individual contributors for the period, led by Entergy Corp., a U.S.-based power producer. Shares outperformed as market volatility increased, interest rates declined, and investors gained further confidence in its exit of unregulated merchant power generation businesses. Munich Re, a global company engaged in reinsurance and primary insurance across life and property and casualty markets, was also among the leading contributors due to a better pricing environment and outlook for reinsurers.

What changes did you make during the period?

We added more than 10 new positions, including CenterPoint Energy, Inc., a U.S. utility involved in electricity generation and natural gas distribution that generates cash flow from regulated and nonutility businesses, and Darden Restaurants, Inc., which sustains cash flows through market leadership and scale of its eight U.S. dining brands. We also closed more than 10 positions, including Vodafone Group, PLC, a global provider of telecommunication services, which lowered its dividend due to increased competition, and risk management firm Arthur J. Gallagher & Company, where share price appreciation compressed the dividend yield.

MANAGED BY

| The Tax-Advantaged Global Shareholder Yield fund is jointly managed by a team of portfolio managers from Epoch Investment Partners, Inc. and Wells Capital Management Incorporated. |

![]()

![]()

| Fund’s investments |

| Shares | Value | ||||

| Common stocks 99.2% | $82,609,149 | ||||

| (Cost $80,156,084) | |||||

| Australia 1.8% | 1,500,872 | ||||

| Commonwealth Bank of Australia | 8,600 | 466,293 | |||

| Macquarie Group, Ltd. | 5,586 | 515,797 | |||

| Westpac Banking Corp. | 26,720 | 518,782 | |||

| Canada 6.2% | 5,172,882 | ||||

| BCE, Inc. | 32,100 | 1,522,745 | |||

| Nutrien, Ltd. | 15,223 | 727,507 | |||

| Pembina Pipeline Corp. | 23,500 | 827,344 | |||

| Rogers Communications, Inc., Class B | 14,600 | 687,378 | |||

| Royal Bank of Canada | 7,400 | 596,899 | |||

| TELUS Corp. | 22,800 | 811,009 | |||

| France 7.4% | 6,185,947 | ||||

| AXA SA | 58,189 | 1,540,333 | |||

| Cie Generale des Etablissements Michelin SCA | 6,000 | 730,543 | |||

| Sanofi | 10,874 | 1,002,442 | |||

| SCOR SE | 13,100 | 552,547 | |||

| TOTAL SA | 23,419 | 1,238,120 | |||

| Vinci SA | 10,000 | 1,121,962 | |||

| Germany 6.1% | 5,085,387 | ||||

| Allianz SE | 6,353 | 1,551,546 | |||

| BASF SE | 11,600 | 881,823 | |||

| Deutsche Post AG | 19,500 | 690,788 | |||

| Muenchener Rueckversicherungs-Gesellschaft AG | 4,600 | 1,278,062 | |||

| Siemens AG | 5,920 | 683,168 | |||

| Italy 3.3% | 2,771,378 | ||||

| Assicurazioni Generali SpA | 34,300 | 695,518 | |||

| Snam SpA | 218,700 | 1,122,785 | |||

| Terna Rete Elettrica Nazionale SpA | 144,200 | 953,075 | |||

| Japan 1.7% | 1,382,475 | ||||

| Takeda Pharmaceutical Company, Ltd. | 22,400 | 809,380 | |||

| Tokio Marine Holdings, Inc. | 10,600 | 573,095 | |||

| Netherlands 1.4% | 1,141,893 | ||||

| Royal Dutch Shell PLC, ADR, Class A (A) | 19,698 | 1,141,893 | |||

| Norway 0.9% | 763,180 | ||||

| Orkla ASA | 79,400 | 763,180 | |||

| South Korea 0.8% | 695,911 | ||||

| Samsung Electronics Company, Ltd., GDR (B) | 651 | 695,911 | |||

| SEE NOTES TO FINANCIAL STATEMENTS | ANNUAL REPORT | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | 7 |

| Shares | Value | ||||

| Spain 0.7% | $534,003 | ||||

| Naturgy Energy Group SA | 19,600 | 534,003 | |||

| Sweden 0.5% | 424,394 | ||||

| Svenska Handelsbanken AB, A Shares | 42,288 | 424,394 | |||

| Switzerland 2.9% | 2,441,977 | ||||

| Nestle SA | 5,000 | 534,907 | |||

| Novartis AG | 11,803 | 1,031,289 | |||

| Roche Holding AG | 2,910 | 875,781 | |||

| Taiwan 0.7% | 577,017 | ||||

| Taiwan Semiconductor Manufacturing Company, Ltd., ADR | 11,176 | 577,017 | |||

| United Kingdom 10.8% | 8,944,260 | ||||

| AstraZeneca PLC, ADR (A) | 17,231 | 844,836 | |||

| BAE Systems PLC | 156,700 | 1,170,504 | |||

| British American Tobacco PLC | 21,600 | 755,479 | |||

| British American Tobacco PLC, ADR | 7,746 | 270,800 | |||

| Coca-Cola European Partners PLC (New York Stock Exchange) | 8,100 | 433,431 | |||

| GlaxoSmithKline PLC | 38,200 | 874,969 | |||

| Imperial Brands PLC | 38,400 | 842,322 | |||

| Lloyds Banking Group PLC | 855,100 | 629,017 | |||

| Micro Focus International PLC | 25,783 | 353,877 | |||

| National Grid PLC | 99,750 | 1,166,305 | |||

| Unilever PLC | 26,766 | 1,602,720 | |||

| United States 54.0% | 44,987,573 | ||||

| 3M Company | 3,200 | 527,968 | |||

| AbbVie, Inc. | 8,600 | 684,130 | |||

| Altria Group, Inc. (A) | 22,700 | 1,016,733 | |||

| Ameren Corp. (A) | 6,200 | 481,740 | |||

| American Electric Power Company, Inc. (A) | 7,600 | 717,364 | |||

| Amgen, Inc. | 2,400 | 511,800 | |||

| AT&T, Inc. (A) | 29,800 | 1,147,002 | |||

| BB&T Corp. | 11,928 | 632,780 | |||

| BlackRock, Inc. (A) | 1,100 | 507,870 | |||

| Broadcom, Inc. | 1,545 | 452,453 | |||

| CenterPoint Energy, Inc. | 21,164 | 615,237 | |||

| Chevron Corp. | 6,055 | 703,228 | |||

| Cisco Systems, Inc. (A) | 15,628 | 742,486 | |||

| CME Group, Inc. (A) | 2,298 | 472,814 | |||

| Darden Restaurants, Inc. | 3,814 | 428,198 | |||

| Dominion Energy, Inc. (A) | 14,200 | 1,172,210 | |||

| Dow, Inc. | 17,606 | 888,927 | |||

| Duke Energy Corp. (A) | 16,300 | 1,536,438 | |||

| Eaton Corp. PLC | 24,268 | 2,113,985 | |||

| Emerson Electric Company (A) | 10,120 | 709,918 | |||

| 8 | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Shares | Value | ||||

| United States (continued) | |||||

| Entergy Corp. (A) | 11,384 | $1,382,928 | |||

| Exxon Mobil Corp. (A) | 11,800 | 797,326 | |||

| FirstEnergy Corp. (A) | 26,400 | 1,275,648 | |||

| Hanesbrands, Inc. (A) | 36,982 | 562,496 | |||

| IBM Corp. | 6,156 | 823,242 | |||

| Intel Corp. | 9,931 | 561,399 | |||

| Johnson & Johnson (A) | 5,525 | 729,521 | |||

| Kimberly-Clark Corp. (A) | 5,400 | 717,552 | |||

| KLA Corp. | 3,358 | 567,636 | |||

| Las Vegas Sands Corp. | 14,800 | 915,232 | |||

| Leggett & Platt, Inc. | 13,800 | 707,940 | |||

| Lockheed Martin Corp. (A) | 1,532 | 577,074 | |||

| LyondellBasell Industries NV, Class A | 7,200 | 645,842 | |||

| McDonald's Corp. (A) | 2,600 | 511,420 | |||

| Merck & Company, Inc. (A) | 12,600 | 1,091,916 | |||

| MetLife, Inc. (A) | 34,934 | 1,634,562 | |||

| Microsoft Corp. (A) | 4,398 | 630,541 | |||

| Occidental Petroleum Corp. (A) | 13,600 | 550,800 | |||

| People's United Financial, Inc. (A) | 54,700 | 884,499 | |||

| PepsiCo, Inc. | 5,200 | 713,284 | |||

| Pfizer, Inc. (A) | 32,375 | 1,242,229 | |||

| Philip Morris International, Inc. (A) | 12,700 | 1,034,288 | |||

| Phillips 66 | 8,022 | 937,130 | |||

| PPL Corp. (A) | 27,800 | 931,022 | |||

| Target Corp. | 6,100 | 652,151 | |||

| Texas Instruments, Inc. (A) | 12,900 | 1,522,071 | |||

| The Coca-Cola Company (A) | 14,900 | 811,007 | |||

| The Home Depot, Inc. | 2,400 | 562,992 | |||

| The Procter & Gamble Company (A) | 5,300 | 659,903 | |||

| United Parcel Service, Inc., Class B | 4,800 | 552,816 | |||

| UnitedHealth Group, Inc. | 2,300 | 581,210 | |||

| Verizon Communications, Inc. (A) | 23,500 | 1,421,045 | |||

| Watsco, Inc. | 3,492 | 615,640 | |||

| WEC Energy Group, Inc. (A) | 6,081 | 574,046 | |||

| Wells Fargo & Company | 10,573 | 545,884 | |||

| Yield (%) | Shares | Value | |||

| Short-term investments 0.9% | $732,778 | ||||

| (Cost $732,778) | |||||

| Money market funds 0.3% | 237,778 | ||||

| State Street Institutional Treasury Money Market Fund, Premier Class | 1.7364(C) | 237,778 | 237,778 | ||

| SEE NOTES TO FINANCIAL STATEMENTS | ANNUAL REPORT | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | 9 |

| Par value^ | Value | ||||

| Repurchase agreement 0.6% | 495,000 | ||||

| Repurchase Agreement with State Street Corp. dated 10-31-19 at 0.550% to be repurchased at $495,008 on 11-1-19, collateralized by $505,000 U.S. Treasury Notes, 1.875% due 1-31-22 (valued at $509,820, including interest) | 495,000 | 495,000 | |||

| Total investments (Cost $80,888,862) 100.1% | $83,341,927 | ||||

| Other assets and liabilities, net (0.1%) | (48,098) | ||||

| Total net assets 100.0% | $83,293,829 | ||||

| The percentage shown for each investment category is the total value of the category as a percentage of the net assets of the fund unless otherwise indicated. | |

| ^All par values are denominated in U.S. dollars unless otherwise indicated. | |

| Security Abbreviations and Legend | |

| ADR | American Depositary Receipt |

| GDR | Global Depositary Receipt |

| (A) | All or a portion of this security is segregated as collateral for options. Total collateral value at 10-31-19 was $25,051,698. |

| (B) | These securities are exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may be resold, normally to qualified institutional buyers, in transactions exempt from registration. |

| (C) | The rate shown is the annualized seven-day yield as of 10-31-19. |

| 10 | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Options on index | ||||||||

| Counterparty (OTC)/ Exchange- traded | Name of issuer | Exercise price | Expiration date | Number of contracts | Notional amount | Premium | Value | |

| Calls | ||||||||

| Exchange-traded | NASDAQ 100 Index | USD | 7,875.00 | Nov 2019 | 1 | 100 | $21,519 | $(24,500) |

| Exchange-traded | Russell 2000 Index | USD | 1,535.00 | Nov 2019 | 15 | 1,500 | 49,429 | (62,850) |

| Exchange-traded | S&P 500 Index | USD | 3,005.00 | Nov 2019 | 8 | 800 | 17,194 | (28,200) |

| Exchange-traded | S&P 500 Index | USD | 3,050.00 | Nov 2019 | 8 | 800 | 8,634 | (8,800) |

| Exchange-traded | S&P 500 Index | USD | 3,225.00 | Nov 2019 | 42 | 4,200 | 10,290 | (630) |

| Exchange-traded | S&P 500 Index | USD | 1,275.00 | Nov 2019 | 64 | 6,400 | 289,406 | (494,720) |

| Exchange-traded | S&P 500 Index | USD | 3,040.00 | Nov 2019 | 8 | 800 | 12,714 | (18,720) |

| Exchange-traded | S&P 500 Index | USD | 3,085.00 | Nov 2019 | 8 | 800 | 7,273 | (8,400) |

| Exchange-traded | S&P 500 Index | USD | 1,330.00 | Dec 2019 | 8 | 800 | 28,474 | (30,640) |

| Exchange-traded | S&P 500 Index | USD | 1,430.00 | Dec 2019 | 38 | 3,800 | 10,330 | (3,800) |

| $455,263 | $(681,260) | |||||||

| Derivatives Currency Abbreviations | |

| USD | U.S. Dollar |

| Derivatives Abbreviations | |

| OTC | Over-the-counter |

| SEE NOTES TO FINANCIAL STATEMENTS | ANNUAL REPORT | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | 11 |

| Financial statements |

| Assets | |

| Unaffiliated investments, at value (Cost $80,888,862) | $83,341,927 |

| Foreign currency, at value (Cost $36) | 36 |

| Dividends and interest receivable | 758,601 |

| Receivable for investments sold | 186,206 |

| Other assets | 60,836 |

| Total assets | 84,347,606 |

| Liabilities | |

| Written options, at value (Premiums received $455,263) | 681,260 |

| Due to custodian | 185,798 |

| Payable for fund shares repurchased | 69,227 |

| Payable to affiliates | |

| Accounting and legal services fees | 7,123 |

| Trustees' fees | 147 |

| Other liabilities and accrued expenses | 110,222 |

| Total liabilities | 1,053,777 |

| Net assets | $83,293,829 |

| Net assets consist of | |

| Paid-in capital | $105,308,987 |

| Total distributable earnings (loss) | (22,015,158) |

| Net assets | $83,293,829 |

| Net asset value per share | |

| Based on 10,938,436 shares of beneficial interest outstanding - unlimited number of shares authorized with $0.01 par value | $7.61 |

| 12 | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Investment income | |

| Dividends | $6,073,453 |

| Interest | 28,818 |

| Less foreign taxes withheld | (325,640) |

| Total investment income | 5,776,631 |

| Expenses | |

| Investment management fees | 790,988 |

| Accounting and legal services fees | 18,331 |

| Transfer agent fees | 20,344 |

| Trustees' fees | 43,690 |

| Custodian fees | 48,456 |

| Printing and postage | 49,481 |

| Professional fees | 117,167 |

| Stock exchange listing fees | 21,515 |

| Other | 9,485 |

| Total expenses | 1,119,457 |

| Less expense reductions | (6,123) |

| Net expenses | 1,113,334 |

| Net investment income | 4,663,297 |

| Realized and unrealized gain (loss) | |

| Net realized gain (loss) on | |

| Unaffiliated investments and foreign currency transactions | (3,654,652) |

| Written options | (986,492) |

| (4,641,144) | |

| Change in net unrealized appreciation (depreciation) of | |

| Unaffiliated investments and translation of assets and liabilities in foreign currencies | 7,185,666 |

| Written options | (453,937) |

| 6,731,729 | |

| Net realized and unrealized gain | 2,090,585 |

| Increase in net assets from operations | $6,753,882 |

| SEE NOTES TO FINANCIAL STATEMENTS | ANNUAL REPORT | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | 13 |

| Year ended 10-31-19 | Year ended 10-31-18 | |

| Increase (decrease) in net assets | ||

| From operations | ||

| Net investment income | $4,663,297 | $4,494,980 |

| Net realized loss | (4,641,144) | (2,453,114) |

| Change in net unrealized appreciation (depreciation) | 6,731,729 | (6,922,809) |

| Increase (decrease) in net assets resulting from operations | 6,753,882 | (4,880,943) |

| Distributions to shareholders | ||

| From earnings | (4,667,477) | (4,509,993) |

| From tax return of capital | (2,386,247) | (4,540,867) |

| Total distributions | (7,053,724) | (9,050,860) |

| Fund share transactions | ||

| Issued pursuant to Dividend Reinvestment Plan | — | 85,293 |

| Repurchased | (720,881) | — |

| Total from fund share transactions | (720,881) | 85,293 |

| Total decrease | (1,020,723) | (13,846,510) |

| Net assets | ||

| Beginning of year | 84,314,552 | 98,161,062 |

| End of year | $83,293,829 | $84,314,552 |

| Share activity | ||

| Shares outstanding | ||

| Beginning of year | 11,044,437 | 11,034,238 |

| Issued pursuant to Dividend Reinvestment Plan | — | 10,199 |

| Shares repurchased | (106,001) | — |

| End of year | 10,938,436 | 11,044,437 |

| 14 | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | ANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| Financial highlights |

| Period ended | 10-31-19 | 10-31-18 | 10-31-17 | 10-31-16 | 10-31-15 |

| Per share operating performance | |||||

| Net asset value, beginning of period | $7.63 | $8.90 | $8.77 | $10.07 | $11.44 |

| Net investment income1 | 0.42 | 0.41 | 0.44 | 0.52 | 0.64 |

| Net realized and unrealized gain (loss) on investments | 0.19 | (0.86) | 0.66 | (0.57) | (0.75) |

| Total from investment operations | 0.61 | (0.45) | 1.10 | (0.05) | (0.11) |

| Less distributions | |||||

| From net investment income | (0.42) | (0.41) | (0.44) | (0.52) | (0.75) |

| From tax return of capital | (0.22) | (0.41) | (0.54) | (0.76) | (0.53) |

| Total distributions | (0.64) | (0.82) | (0.98) | (1.28) | (1.28) |

| Anti-dilutive impact of repurchase plan | 0.012 | — | — | — | — |

| Anti-dilutive impact of shelf offering | — | — | 0.01 | 0.03 | 0.02 |

| Net asset value, end of period | $7.61 | $7.63 | $8.90 | $8.77 | $10.07 |

| Per share market value, end of period | $6.93 | $6.91 | $8.97 | $10.35 | $9.51 |

| Total return at net asset value (%)3,4 | 9.45 | (5.45) | 12.95 | (1.28) | (0.65) |

| Total return at market value (%)3 | 10.06 | (15.04) | (3.54) | 23.37 | (14.74) |

| Ratios and supplemental data | |||||

| Net assets, end of period (in millions) | $83 | $84 | $98 | $96 | $106 |

| Ratios (as a percentage of average net assets): | |||||

| Expenses before reductions | 1.35 | 1.35 | 1.32 | 1.32 | 1.27 |

| Expenses including reductions | 1.34 | 1.34 | 1.31 | 1.32 | 1.26 |

| Net investment income | 5.60 | 4.90 | 4.96 | 5.60 | 6.01 |

| Portfolio turnover (%) | 260 | 208 | 220 | 253 | 261 |

| 1 | Based on average daily shares outstanding. |

| 2 | The repurchase plan was completed at an average repurchase price of $6.80 for 106,001 shares for the periods ended 10-31-19. |

| 3 | Total return based on net asset value reflects changes in the fund’s net asset value during each period. Total return based on market value reflects changes in market value. Each figure assumes that distributions from income, capital gains and tax return of capital, if any, were reinvested. |

| 4 | Total returns would have been lower had certain expenses not been reduced during the applicable periods. |

| SEE NOTES TO FINANCIAL STATEMENTS | ANNUAL REPORT | JOHN HANCOCK Tax-Advantaged Global Shareholder Yield Fund | 15 |

| Notes to financial statements |

| 16 | JOHN HANCOCK Tax-Advantaged Global Shareholder Yield Fund | ANNUAL REPORT |

| Total value at 10-31-19 | Level 1 quoted price | Level 2 significant observable inputs | Level 3 significant unobservable inputs | |

| Investments in securities: | ||||

| Assets | ||||

| Common stocks | ||||

| Australia | $1,500,872 | — | $1,500,872 | — |

| Canada | 5,172,882 | $5,172,882 | — | — |

| France | 6,185,947 | — | 6,185,947 | — |

| Germany | 5,085,387 | — | 5,085,387 | — |

| Italy | 2,771,378 | — | 2,771,378 | — |

| Japan | 1,382,475 | — | 1,382,475 | — |

| Netherlands | 1,141,893 | 1,141,893 | — | — |

| Norway | 763,180 | — | 763,180 | — |

| South Korea | 695,911 | — | 695,911 | — |

| Spain | 534,003 | — | 534,003 | — |

| Sweden | 424,394 | — | 424,394 | — |

| Switzerland | 2,441,977 | — | 2,441,977 | — |

| Taiwan | 577,017 | 577,017 | — | — |

| United Kingdom | 8,944,260 | 1,549,067 | 7,395,193 | — |

| United States | 44,987,573 | 44,987,573 | — | — |

| ANNUAL REPORT | JOHN HANCOCK Tax-Advantaged Global Shareholder Yield Fund | 17 |

| Total value at 10-31-19 | Level 1 quoted price | Level 2 significant observable inputs | Level 3 significant unobservable inputs | |

| Short-term investments | $732,778 | $237,778 | $495,000 | — |

| Total investments in securities | $83,341,927 | $53,666,210 | $29,675,717 | — |

| Derivatives: | ||||

| Liabilities | ||||

| Written options | $(681,260) | $(681,260) | — | — |

| 18 | JOHN HANCOCK Tax-Advantaged Global Shareholder Yield Fund | ANNUAL REPORT |

| October 31, 2019 | October 31, 2018 | |

| Ordinary income | $4,667,477 | $4,509,993 |

| Return of capital | 2,386,247 | 4,540,867 |

| Total | $7,053,724 | $9,050,860 |

| ANNUAL REPORT | JOHN HANCOCK Tax-Advantaged Global Shareholder Yield Fund | 19 |

| Risk | Statement of assets and liabilities location | Financial instruments location | Assets derivatives fair value | Liabilities derivatives fair value |

| Equity | Written options, at value | Written options | — | $(681,260) |

| 20 | JOHN HANCOCK Tax-Advantaged Global Shareholder Yield Fund | ANNUAL REPORT |

| Statement of operations location - Net realized gain (loss) on: | |

| Risk | Written options |

| Equity | $(986,492) |

| Statement of operations location - Change in net unrealized appreciation (depreciation) of: | |

| Risk | Written options |

| Equity | $(453,937) |

| ANNUAL REPORT | JOHN HANCOCK Tax-Advantaged Global Shareholder Yield Fund | 21 |

| 22 | JOHN HANCOCK Tax-Advantaged Global Shareholder Yield Fund | ANNUAL REPORT |

| ANNUAL REPORT | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | 23 |

| Tax information (Unaudited) |

| 24 | JOHN HANCOCK TAX-ADVANTAGED GLOBAL SHAREHOLDER YIELD FUND | ANNUAL REPORT |

Unaudited

Investment objective and policy

The fund is a diversified, closed-end management investment company, common shares of which were initially offered to the public in 2007. The fund's investment objective is to provide total return consisting of a high level of current income and gains and long term capital appreciation. In pursuing its investment objective of total return, the fund will seek to emphasize high current income. The fund will seek to achieve favorable after-tax returns for its shareholders by seeking to minimize the U.S. federal income tax consequences on income and gains generated by the fund. Under normal market conditions, the fund will invest at least 80% of its total assets in a diversified portfolio of dividend-paying securities of issuers located throughout the world. The fund will notify shareholders at least 60 days prior to any change in this 80% investment policy. The fund also intends to write (sell) call options on a variety of both U.S. and non-U.S. broad-based indices.

Dividends and distributions

During the year ended October 31, 2019, distributions from net investment income totaling $0.6400 per share were paid to shareholders. The dates of payments and the amounts per share were as follows:

| Payment Date | Income Distributions* |

| December 31, 2018 | $0.1600 |

| March 29, 2019 | 0.1600 |

| June 28, 2019 | 0.1600 |

| September 30, 2019 | 0.1600 |

| Total | $0.6400 |

* A portion of the distributions may be deemed a tax return of capital at the fiscal year end.

Dividend reinvestment plan

The fund's Dividend Reinvestment Plan (the Plan) provides that distributions of dividends and capital gains are automatically reinvested in common shares of the fund by Computershare Trust Company, N.A. (the Plan Agent). Every shareholder holding at least one full share of the fund is entitled to participate in the Plan. In addition, every shareholder who became a shareholder of the fund after June 30, 2011, and holds at least one full share of the fund will be automatically enrolled in the Plan. Shareholders may withdraw from the Plan at any time and shareholders who do not participate in the Plan will receive all distributions in cash.

If the fund declares a dividend or distribution payable either in cash or in common shares of the fund and the market price of shares on the payment date for the distribution or dividend equals or exceeds the fund's net asset value per share (NAV), the fund will issue common shares to participants at a value equal to the higher of NAV or 95% of the market price. The number of additional shares to be credited to each participant's account will be determined by dividing the dollar amount of the distribution or dividend by the higher of NAV or 95% of the market price. If the market price is lower than NAV, or if dividends or distributions are payable only in cash, then participants will receive shares purchased by the Plan Agent on participants' behalf on the NYSE or otherwise on the open market. If the market price exceeds NAV before the Plan Agent has completed its purchases, the average per share purchase price may exceed NAV, resulting in fewer shares being acquired than if the fund had issued new shares.

There are no brokerage charges with respect to common shares issued directly by the fund. However, whenever shares are purchased or sold on the NYSE or otherwise on the open market, each participant will pay a pro rata portion of

brokerage trading fees, currently $0.05 per share purchased or sold. Brokerage trading fees will be deducted from amounts to be invested.

The reinvestment of dividends and net capital gains distributions does not relieve participants of any income tax that may be payable on such dividends or distributions.

Shareholders participating in the Plan may buy additional shares of the fund through the Plan at any time in amounts of at least $50 per investment, up to a maximum of $10,000, with a total calendar year limit of $100,000. Shareholders will be charged a $5 transaction fee plus $0.05 per share brokerage trading fee for each order. Purchases of additional shares of the fund will be made on the open market. Shareholders who elect to utilize monthly electronic fund transfers to buy additional shares of the fund will be charged a $2 transaction fee plus $0.05 per share brokerage trading fee for each automatic purchase. Shareholders can also sell fund shares held in the Plan account at any time by contacting the Plan Agent by telephone, in writing or by visiting the Plan Agent's website at www.computershare.com/investor. The Plan Agent will mail a check (less applicable brokerage trading fees) on settlement date. Pursuant to regulatory changes, effective September 5, 2017, the settlement date is changed from three business days after the shares have been sold to two business days after the shares have been sold. If shareholders choose to sell shares through their stockbroker, they will need to request that the Plan Agent electronically transfer those shares to their stockbroker through the Direct Registration System.

Shareholders participating in the Plan may withdraw from the Plan at any time by contacting the Plan Agent by telephone, in writing or by visiting the Plan Agent's website at www.computershare.com/investor. Such termination will be effective immediately if the notice is received by the Plan Agent prior to any dividend or distribution record date; otherwise, such termination will be effective on the first trading day after the payment date for such dividend or distribution, with respect to any subsequent dividend or distribution. If shareholders withdraw from the Plan, their shares will be credited to their account; or, if they wish, the Plan Agent will sell their full and fractional shares and send the shareholders the proceeds, less a transaction fee of $5 and less brokerage trading fees of $0.05 per share. If a shareholder does not maintain at least one whole share of common stock in the Plan account, the Plan Agent may terminate such shareholder's participation in the Plan after written notice. Upon termination, shareholders will be sent a check for the cash value of any fractional share in the Plan account, less any applicable broker commissions and taxes.

Shareholders who hold at least one full share of the fund may join the Plan by notifying the Plan Agent by telephone, in writing or by visiting the Plan Agent's website at www.computershare.com/investor. If received in proper form by the Plan Agent before the record date of a dividend, the election will be effective with respect to all dividends paid after such record date. If shareholders wish to participate in the Plan and their shares are held in the name of a brokerage firm, bank or other nominee, shareholders should contact their nominee to see if it will participate in the Plan. If shareholders wish to participate in the Plan, but their brokerage firm, bank or other nominee is unable to participate on their behalf, they will need to request that their shares be re-registered in their own name, or they will not be able to participate. The Plan Agent will administer the Plan on the basis of the number of shares certified from time to time by shareholders as representing the total amount registered in their name and held for their account by their nominee.

Experience under the Plan may indicate that changes are desirable. Accordingly, the fund and the Plan Agent reserve the right to amend or terminate the Plan. Participants generally will receive written notice at least 90 days before the effective date of any amendment. In the case of termination, participants will receive written notice at least 90 days before the record date for the payment of any dividend or distribution by the fund.

Effective November 1, 2013, the Plan was revised to provide that Computershare Trust Company, N.A. no longer provides mail loss insurance coverage when shareholders mail their certificates to the fund's administrator.

All correspondence or requests for additional information about the Plan should be directed to Computershare Trust Company, N.A., at the address stated below, or by calling 800-852-0218, 201-680-6578 (For International Telephone Inquiries) and 800-952-9245 (For the Hearing Impaired (TDD)).

Shareholder communication and assistance

If you have any questions concerning the fund, we will be pleased to assist you. If you hold shares in your own name and not with a brokerage firm, please address all notices, correspondence, questions or other communications regarding the fund to the transfer agent at:

Regular Mail:

Computershare

P.O. Box 505000

Louisville, KY 40233

Registered or Overnight Mail:

Computershare

462 South 4th Street, Suite 1600

Louisville, KY 40202

If your shares are held with a brokerage firm, you should contact that firm, bank or other nominee for assistance.

Continuation of Investment Advisory and Subadvisory Agreements

Evaluation of Advisory and Subadvisory Agreements by the Board of Trustees

This section describes the evaluation by the Board of Trustees (the Board) of John Hancock Tax-Advantaged Global Shareholder Yield Fund (the fund) of the Advisory Agreement (the Advisory Agreement) with John Hancock Investment Management, LLC (the Advisor, formerly John Hancock Advisers, LLC) and the Subadvisory Agreements (the Subadvisory Agreements) with Epoch Investment Partners, Inc. and Wells Capital Management Incorporated (formerly known as Analytic Investors, LLC) (collectively, the Subadvisors). The Advisory Agreement and Subadvisory Agreements are collectively referred to as the Agreements. Prior to the June23-26, 2019 in-person meeting at which the Agreements were approved, the Board also discussed and considered information regarding the proposed continuation of the Agreements at an in-person meeting held on May28-30, 2019.

Approval of Advisory and Subadvisory Agreements

At in-person meetings held on June 23-26, 2019, the Board, including the Trustees who are not parties to any Agreement or considered to be interested persons of the fund under the Investment Company Act of 1940, as amended (the 1940 Act) (the Independent Trustees), reapproved for an annual period the continuation of the Advisory Agreement between the fund and the Advisor and the Subadvisory Agreements between the Advisor and the Subadvisors with respect to the fund.

In considering the Advisory Agreement and the Subadvisory Agreements, the Board received in advance of the meetings a variety of materials relating to the fund, the Advisor and the Subadvisors, including comparative performance, fee and expense information for a peer group of similar funds prepared by an independent third-party provider of fund data, performance information for an applicable benchmark index; and other pertinent information, such as the market premium and discount information, and, with respect to the Subadvisors, comparative performance information for comparably managed accounts, as applicable, and other information provided by the Advisor and the Subadvisors regarding the nature, extent and quality of services provided by the Advisor and the Subadvisors under their respective Agreements, as well as information regarding the Advisor's revenues and costs of providing services to the fund and any compensation paid to affiliates of the Advisor. At the meetings at which the renewal of the Advisory Agreement and Subadvisory Agreements are considered, particular focus is given to information concerning fund performance, comparability of fees and total expenses, and profitability. However, the Board noted that the evaluation process with respect to the Advisor and the Subadvisors is an ongoing one. In this regard, the Board also took into account discussions with management and information provided to the Board (including its various committees) at prior meetings with respect to the services provided by the Advisor and the Subadvisors to the fund, including quarterly performance reports prepared by management containing reviews of investment results and prior presentations from the Subadvisors with respect to the fund. The information received and considered by the Board in connection with the May and June meetings and throughout the year was both written and oral. The Board also considered the nature, quality, and extent of non-advisory services, if any, to be provided to the fund by the Advisor's affiliates, including distribution services. The Board considered the Advisory Agreement and the Subadvisory Agreements separately in the course of its review. In doing so, the Board noted the respective roles of the Advisor and Subadvisors in providing services to the fund.

Throughout the process, the Board asked questions of and requested additional information from management. The Board is assisted by counsel for the fund and the Independent Trustees are also separately assisted by independent legal counsel throughout the process. The Independent Trustees also received a memorandum from their independent legal counsel discussing the legal standards for their consideration of the proposed continuation of the Agreements

and discussed the proposed continuation of the Agreements in private sessions with their independent legal counsel at which no representatives of management were present.

Approval of Advisory Agreement

In approving the Advisory Agreement with respect to the fund, the Board, including the Independent Trustees, considered a variety of factors, including those discussed below. The Board also considered other factors (including conditions and trends prevailing generally in the economy, the securities markets, and the industry) and did not treat any single factor as determinative, and each Trustee may have attributed different weights to different factors. The Board's conclusions may be based in part on its consideration of the advisory and subadvisory arrangements in prior years and on the Board's ongoing regular review of fund performance and operations throughout the year.

Nature, extent, and quality of services. Among the information received by the Board from the Advisor relating to the nature, extent, and quality of services provided to the fund, the Board reviewed information provided by the Advisor relating to its operations and personnel, descriptions of its organizational and management structure, and information regarding the Advisor's compliance and regulatory history, including its Form ADV. The Board also noted that on a regular basis it receives and reviews information from the fund's Chief Compliance Officer (CCO) regarding the fund's compliance policies and procedures established pursuant to Rule 38a-1 under the 1940 Act. The Board observed that the scope of services provided by the Advisor, and of the undertakings required of the Advisor in connection with those services, including maintaining and monitoring its own and the fund's compliance programs, risk management programs, liquidity management programs and cybersecurity programs, had expanded over time as a result of regulatory, market and other developments. The Board considered that the Advisor is responsible for the management of the day-to-day operations of the fund, including, but not limited to, general supervision of and coordination of the services provided by the Subadvisors, and is also responsible for monitoring and reviewing the activities of the Subadvisors and other third-party service providers. The Board also considered the significant risks assumed by the Advisor in connection with the services provided to the fund including entrepreneurial risk in sponsoring new funds and ongoing risks including investment, operational, enterprise, litigation, regulatory and compliance risks with respect to all funds.

The Board also considered the differences between the Advisor's services to the fund and the services it provides to other clients that are not closed-end funds, including, for example, the differences in services related to the regulatory and legal obligations of closed-end funds.

In considering the nature, extent, and quality of the services provided by the Advisor, the Trustees also took into account their knowledge of the Advisor's management and the quality of the performance of the Advisor's duties, through Board meetings, discussions and reports during the preceding year and through each Trustee's experience as a Trustee of the fund and of the other funds in the John Hancock group of funds complex (the John Hancock Fund Complex).

In the course of their deliberations regarding the Advisory Agreement, the Board considered, among other things:

| (a) | the skills and competency with which the Advisor has in the past managed the fund's affairs and its subadvisory relationships, the Advisor's oversight and monitoring of the Subadvisors' investment performance and compliance programs, such as the Subadvisors' compliance with fund policies and objectives, review of brokerage matters, including with respect to trade allocation and best execution and the Advisor's timeliness in responding to performance issues; |

| (b) | the background, qualifications and skills of the Advisor's personnel; |

The Board concluded that the Advisor may reasonably be expected to continue to provide a high quality of services under the Advisory Agreement with respect to the fund.

Investment performance.In considering the fund's performance, the Board noted that it reviews at its regularly scheduled meetings information about the fund's performance results. In connection with the consideration of the Advisory Agreement, the Board:

| (a) | reviewed information prepared by management regarding the fund's performance; |

| (b) | considered the comparative performance of an applicable benchmark index; |

| (c) | considered the performance of comparable funds, if any, as included in the report prepared by an independent third-party provider of fund data; |

| (d) | took into account the Advisor's analysis of the fund's performance; and |

| (e) | considered the fund's share performance and premium/discount information. |

The Board noted that while it found the data provided by the independent third-party generally useful it recognized its limitations, including in particular that the data may vary depending on the end date selected and the results of the performance comparisons may vary depending on the selection of the peer group. The Board noted that, based on its net asset value, the fund underperformed its benchmark index for the one-, three- five- and ten-year periods ended December 31, 2018. The Board also noted that, based on its net asset value, the fund outperformed its peer group average for the one-year period and underperformed its peer group average for the three-, five- and ten-year periods ended December 31, 2018. The Board took into account management's discussion of the fund's performance, including the impact of current market conditions on the fund's investment strategy and the favorable performance relative to the peer group for the one-year period. The Board concluded that the fund's performance is being monitored and reasonably addressed, where appropriate.

Fees and expenses. The Board reviewed comparative information prepared by an independent third-party provider of fund data, including, among other data, the fund's contractual and net management fees (and subadvisory fees, to the extent available) and total expenses as compared to similarly situated investment companies deemed to be comparable to the fund in light of the nature, extent and quality of the management and advisory and subadvisory services provided by the Advisor and the Subadvisors. The Board considered the fund's ranking within a smaller group of peer funds chosen by the independent third-party provider, as well as the fund's ranking within a broader group of

funds. In comparing the fund's contractual and net management fees to those of comparable funds, the Board noted that such fees include both advisory and administrative costs. The Board noted that net management fees for the fund are lower than the peer group median and that net total expenses for the fund are lower than the peer group median.

The Board took into account management's discussion with respect to the overall management fee and the fees of the Subadvisors, including the amount of the advisory fee retained by the Advisor after payment of the subadvisory fees, in each case in light of the services rendered for those amounts and the risks undertaken by the Advisor. The Board also noted that the Advisor pays the subadvisory fees and that such fees are negotiated at arm's length with respect to the Subadvisors. In addition, the Board took into account that management had agreed to implement an overall fee waiver across the complex, including the fund, which is discussed further below. The Board reviewed information provided by the Advisor concerning the investment advisory fee charged by the Advisor or one of its advisory affiliates to other clients (including other funds in the John Hancock Fund Complex) having similar investment mandates, if any. The Board considered any differences between the Advisor's and Subadvisors' services to the fund and the services they provide to other comparable clients or funds. The Board concluded that the advisory fee paid with respect to the fund is reasonable in light of the nature, extent and quality of the services provided to the fund under the Advisory Agreement.

Profitability/Fall out benefits. In considering the costs of the services to be provided and the profits to be realized by the Advisor and its affiliates from the Advisor's relationship with the fund, the Board:

| (a) | reviewed financial information of the Advisor; |

| (b) | reviewed and considered information presented by the Advisor regarding the net profitability to the Advisor and its affiliates with respect to the fund; |

| (c) | received and reviewed profitability information with respect to the John Hancock Fund Complex as a whole and with respect to the fund; |

| (d) | received information with respect to the Advisor's allocation methodologies used in preparing the profitability data and considered that the Advisor hired an independent third-party consultant to provide an analysis of the Advisor's allocation methodologies; |

| (e) | considered that the Advisor also provides administrative services to the fund on a cost basis pursuant to an administrative services agreement; |

| (f) | noted that the Advisor also derives reputational and other indirect benefits from providing advisory services to the fund; |

| (g) | noted that the subadvisory fees for the fund are paid by the Advisor, and are negotiated at arm's length; |

| (h) | considered the Advisor's ongoing costs and expenditures necessary to improve services, meet new regulatory and compliance requirements, and adapt to other challenges impacting the fund industry; and |

| (i) | considered that the Advisor should be entitled to earn a reasonable level of profits in exchange for the level of services it provides to the fund and the risks that it assumes as Advisor, including entrepreneurial, operational, reputational, litigation and regulatory risk. |

Based upon its review, the Board concluded that the level of profitability, if any, of the Advisor and its affiliates from their relationship with the fund was reasonable and not excessive.

Economies of scale. In considering the extent to which the fund may realize any economies of scale and whether fee levels reflect these economies of scale for the benefit of the fund shareholders, the Board noted that the fund has a

limited ability to increase its assets as a closed-end fund. The Board took into account management's discussions of the current advisory fee structure, and, as noted above, the services the Advisor provides in performing its functions under the Advisory Agreement and in supervising the Subadvisors.

The Board also considered potential economies of scale that may be realized by the fund as part of the John Hancock Fund Complex. Among them, the Board noted that the Advisor has contractually agreed to waive a portion of its management fee and/or reimburse expenses for certain funds of the John Hancock Fund Complex, including the fund (the participating portfolios). This waiver is based upon aggregate net assets of all the participating portfolios. The amount of the reimbursement is calculated daily and allocated among all the participating portfolios in proportion to the daily net assets of each fund. The Board also considered the Advisor's overall operations and its ongoing investment in its business in order to expand the scale of, and improve the quality of, its operations that benefit the fund. The Board determined that the management fee structure for the fund was reasonable.

Approval of Subadvisory Agreements

In making its determination with respect to approval of the Subadvisory Agreements, the Board reviewed:

| (1) | information relating to the Subadvisors' business, including current subadvisory services to the fund (and other funds in the John Hancock Fund Complex); |

| (2) | the historical and current performance of the fund and comparative performance information relating to an applicable benchmark index and comparable funds; |

| (3) | the subadvisory fees for the fund and to the extent available, comparable fee information prepared by an independent third party provider of fund data; and |

| (4) | information relating to the nature and scope of any material relationships and their significance to the fund's Advisor and the Subadvisors. |

Nature, extent, and quality of services. With respect to the services provided by the Subadvisors, the Board received information provided to the Board by the Subadvisors, including the Subadvisors' respective Form ADV, as well as took into account information presented throughout the past year. The Board considered each Subadvisor's current level of staffing and its overall resources, as well as received information relating to each Subadvisor's compensation program. The Board reviewed each Subadvisor's history and investment experience, as well as information regarding the qualifications, background, and responsibilities of each Subadvisor's investment and compliance personnel who provide services to the fund. The Board also considered, among other things, each Subadvisor's compliance program and any disciplinary history. The Board also considered each Subadvisor's risk assessment and monitoring process. The Board reviewed each Subadvisor's regulatory history, including whether it was involved in any regulatory actions or investigations as well as material litigation, and any settlements and amelioratory actions undertaken, as appropriate. The Board noted that the Advisor conducts regular, periodic reviews of each Subadvisor and its operations, including regarding investment processes and organizational and staffing matters. The Board also noted that the fund's CCO and his staff conduct regular, periodic compliance reviews with each Subadvisor and present reports to the Independent Trustees regarding the same, which includes evaluating the regulatory compliance systems of each Subadvisor and procedures reasonably designed to assure compliance with the federal securities laws. The Board also took into account the financial condition of each Subadvisor.

The Board considered each Subadvisor's investment process and philosophy. The Board took into account that each Subadvisor's responsibilities include the development and maintenance of an investment program for the fund that is consistent with the fund's investment objective, the selection of investment securities and the placement of orders for

the purchase and sale of such securities, as well as the implementation of compliance controls related to performance of these services. The Board also received information with respect to each Subadvisor's brokerage policies and practices, including with respect to best execution and soft dollars.

Subadvisor compensation. In considering the cost of services to be provided by each Subadvisor and the profitability to each Subadvisor of its relationship with the fund, the Board noted that the fees under each Subadvisory Agreement are paid by the Advisor and not the fund. The Board also relied on the ability of the Advisor to negotiate the Subadvisory Agreements and the fees thereunder at arm's length. As a result, the costs of the services to be provided and the profits to be realized by the Subadvisors from its relationship with the fund were not a material factor in the Board's consideration of Subadvisory Agreements.

The Board also received information regarding the nature and scope (including their significance to the Advisor and its affiliates and the Subadvisors) of any material relationships with respect to the Subadvisors, which include arrangements in which a Subadvisor or its affiliates provide advisory, distribution, or management services in connection with financial products sponsored by the Advisor or its affiliates, and may include other registered investment companies, a 529 education savings plan, managed separate accounts and exempt group annuity contracts sold to qualified plans. The Board also received information and took into account any other potential conflicts of interest the Advisor might have in connection with the Subadvisory Agreements.

In addition, the Board considered other potential indirect benefits that the Subadvisors and its affiliates may receive from the Subadvisors' relationship with the fund, such as the opportunity to provide advisory services to additional funds in the John Hancock Fund Complex and reputational benefits.

Subadvisory fees. The Board considered that the fund pays an advisory fee to the Advisor and that, in turn, the Advisor pays subadvisory fees to the Subadvisors. As noted above, the Board also considered the fund's subadvisory fees as compared to similarly situated investment companies deemed to be comparable to the fund as included in the report prepared by the independent third party provider of fund data, to the extent available. The Board noted that the limited size of the Lipper peer group was not sufficient for comparative purposes. The Board also took into account the subadvisory fees paid by the Advisor to the Subadvisors with respect to the fund and compared them to fees charged by the Subadvisors to manage other subadvised portfolios and portfolios not subject to regulation under the 1940 Act, as applicable.

Subadvisor performance. As noted above, the Board considered the fund's performance as compared to the fund's peer group and the benchmark index and noted that the Board reviews information about the fund's performance results at its regularly scheduled meetings. The Board noted the Advisor's expertise and resources in monitoring the performance, investment style and risk-adjusted performance of the Subadvisors. The Board was mindful of the Advisor's focus on the Subadvisors' performance. The Board also noted the Subadvisors' long-term performance record for similar accounts, as applicable.

The Board's decision to approve the Subadvisory Agreements was based on a number of determinations, including the following:

| (1) | the Subadvisors have extensive experience and demonstrated skills as a manager; |

| (2) | the fund's performance, based on net asset value, is being monitored and reasonably addressed, where appropriate; and |

| (3) | the subadvisory fees are reasonable in relation to the level and quality of services being provided under the Subadvisory Agreements. |

* * *

Based on the Board's evaluation of all factors that the Board deemed to be material, including those factors described above, the Board, including the Independent Trustees, concluded that renewal of the Advisory Agreement and the Subadvisory Agreements would be in the best interest of the fund and its shareholders. Accordingly, the Board, and the Independent Trustees voting separately, approved the Advisory Agreement and Subadvisory Agreements for an additional one-year period.

This chart provides information about the Trustees and Officers who oversee your John Hancock fund. Officers elected by the Trustees manage the day-to-day operations of the fund and execute policies formulated by the Trustees.

Independent Trustees

| Name, year of birth Position(s) held with fund Principal occupation(s) and other directorships during past 5 years | Trustee of the Trust since1 | Number of John Hancock funds overseen by Trustee |

| Hassell H. McClellan, Born: 1945 | 2012 | 207 |

| Trustee and Chairperson of the Board Director/Trustee, Virtus Funds (since 2008); Director, The Barnes Group (since 2010); Associate Professor, The Wallace E. Carroll School of Management, Boston College (retired 2013). Trustee (since 2005) and Chairperson of the Board (since 2017) of various trusts within the John Hancock Fund Complex. | ||

| Charles L. Bardelis,2 Born: 1941 | 2012 | 207 |

| Trustee Director, Island Commuter Corp. (marine transport). Trustee of various trusts within the John Hancock Fund Complex (since 1988). | ||

| James R. Boyle,Born: 1959 | 2015 | 207 |

| Trustee Chief Executive Officer, Foresters Financial (since 2018); Chairman and Chief Executive Officer, Zillion Group, Inc. (formerly HealthFleet, Inc.) (healthcare) (2014-2018); Executive Vice President and Chief Executive Officer, U.S. Life Insurance Division of Genworth Financial, Inc. (insurance) (January 2014-July 2014); Senior Executive Vice President, Manulife Financial, President and Chief Executive Officer, John Hancock (1999-2012); Chairman and Director, John Hancock Investment Management LLC, John Hancock Investment Management Distributors LLC, and John Hancock Variable Trust Advisers LLC (2005-2010). Trustee of various trusts within the John Hancock Fund Complex (2005-2014 and since 2015). | ||

| Peter S. Burgess,2 Born: 1942 | 2012 | 207 |

| Trustee Consultant (financial, accounting, and auditing matters) (since 1999); Certified Public Accountant; Partner, Arthur Andersen (independent public accounting firm) (prior to 1999); Director, Lincoln Educational Services Corporation (since 2004); Director, Symetra Financial Corporation (2010-2016); Director, PMA Capital Corporation (2004-2010). Trustee of various trusts within the John Hancock Fund Complex (since 2005). | ||

| William H. Cunningham, Born: 1944 | 2007 | 207 |

| Trustee Professor, University of Texas, Austin, Texas (since 1971); former Chancellor, University of Texas System and former President of the University of Texas, Austin, Texas; Chairman (since 2009) and Director (since 2006), Lincoln National Corporation (insurance); Director, Southwest Airlines (since 2000); former Director, LIN Television (2009-2014). Trustee of various trusts within the John Hancock Fund Complex (since 1986). | ||

| Grace K. Fey, Born: 1946 | 2012 | 207 |

| Trustee Chief Executive Officer, Grace Fey Advisors (since 2007); Director and Executive Vice President, Frontier Capital Management Company (1988-2007); Director, Fiduciary Trust (since 2009). Trustee of various trusts within the John Hancock Fund Complex (since 2008). | ||

Independent Trustees (continued)

| Name, year of birth Position(s) held with fund Principal occupation(s) and other directorships during past 5 years | Trustee of the Trust since1 | Number of John Hancock funds overseen by Trustee |

| Deborah C. Jackson, Born: 1952 | 2008 | 207 |

| Trustee President, Cambridge College, Cambridge, Massachusetts (since 2011); Board of Directors, Massachusetts Women's Forum (since 2018); Board of Directors, National Association of Corporate Directors/New England (since 2015); Board of Directors, Association of Independent Colleges and Universities of Massachusetts (2014-2017); Chief Executive Officer, American Red Cross of Massachusetts Bay (2002-2011); Board of Directors of Eastern Bank Corporation (since 2001); Board of Directors of Eastern Bank Charitable Foundation (since 2001); Board of Directors of American Student Assistance Corporation (1996-2009); Board of Directors of Boston Stock Exchange (2002-2008); Board of Directors of Harvard Pilgrim Healthcare (health benefits company) (2007-2011). Trustee of various trusts within the John Hancock Fund Complex (since 2008). | ||

| James M. Oates,2Born: 1946 | 2012 | 207 |

| Trustee Managing Director, Wydown Group (financial consulting firm) (since 1994); Chairman and Director, Emerson Investment Management, Inc. (2000-2015); Independent Chairman, Hudson Castle Group, Inc. (formerly IBEX Capital Markets, Inc.) (financial services company) (1997-2011); Director, Stifel Financial (since 1996); Director, Investor Financial Services Corporation (1995-2007); Director, Connecticut River Bancorp (1998-2014); Director/Trustee, Virtus Funds (since 1988). Trustee (since 2004) and Chairperson of the Board (2005-2016) of various trusts within the John Hancock Fund Complex. | ||

| Steven R. Pruchansky, Born: 1944 | 2007 | 207 |

| Trustee and Vice Chairperson of the Board Managing Director, Pru Realty (since 2017); Chairman and Chief Executive Officer, Greenscapes of Southwest Florida, Inc. (since 2014); Director and President, Greenscapes of Southwest Florida, Inc. (until 2000); Member, Board of Advisors, First American Bank (until 2010); Managing Director, Jon James, LLC (real estate) (since 2000); Partner, Right Funding, LLC (2014-2017); Director, First Signature Bank & Trust Company (until 1991); Director, Mast Realty Trust (until 1994); President, Maxwell Building Corp. (until 1991). Trustee (since 1992), Chairperson of the Board (2011-2012), and Vice Chairperson of the Board (since 2012) of various trusts within the John Hancock Fund Complex. | ||

| Gregory A. Russo, Born: 1949 | 2008 | 207 |

| Trustee Director and Audit Committee Chairman (since 2012), and Member, Audit Committee and Finance Committee (since 2011), NCH Healthcare System, Inc. (holding company for multi-entity healthcare system); Director and Member (2012-2018) and Finance Committee Chairman (2014-2018), The Moorings, Inc. (nonprofit continuing care community); Vice Chairman, Risk & Regulatory Matters, KPMG LLP (KPMG) (2002-2006); Vice Chairman, Industrial Markets, KPMG (1998-2002); Chairman and Treasurer, Westchester County, New York, Chamber of Commerce (1986-1992); Director, Treasurer, and Chairman of Audit and Finance Committees, Putnam Hospital Center (1989-1995); Director and Chairman of Fundraising Campaign, United Way of Westchester and Putnam Counties, New York (1990-1995). Trustee of various trusts within the John Hancock Fund Complex (since 2008). | ||

Non-Independent Trustees3

| Name, year of birth Position(s) held with fund Principal occupation(s) and other directorships during past 5 years | Trustee of the Trust since1 | Number of John Hancock funds overseen by Trustee |

| Andrew G. Arnott, Born: 1971 | 2017 | 207 |

| President and Non-Independent Trustee Head of Wealth and Asset Management, United States and Europe, for John Hancock and Manulife (since 2018); Executive Vice President, John Hancock Financial Services (since 2009, including prior positions); Director and Executive Vice President, John Hancock Investment Management LLC (since 2005, including prior positions); Director and Executive Vice President, John Hancock Variable Trust Advisers LLC (since 2006, including prior positions); President, John Hancock Investment Management Distributors LLC (since 2004, including prior positions); President of various trusts within the John Hancock Fund Complex (since 2007, including prior positions). Trustee of various trusts within the John Hancock Fund Complex (since 2017). | ||

| Marianne Harrison, Born: 1963 | 2018 | 207 |

| Non-Independent Trustee President and CEO, John Hancock (since 2017); President and CEO, Manulife Canadian Division (2013-2017); Member, Board of Directors, CAE Inc. (since 2019); Member, Board of Directors, MA Competitive Partnership Board (since 2018); Member, Board of Directors, American Council of Life Insurers (ACLI) (since 2018); Member, Board of Directors, Communitech, an industry-led innovation center that fosters technology companies in Canada (2017-2019); Member, Board of Directors, Manulife Assurance Canada (2015-2017); Board Member, St. Mary's General Hospital Foundation (2014-2017); Member, Board of Directors, Manulife Bank of Canada (2013-2017); Member, Standing Committee of the Canadian Life & Health Assurance Association (2013-2017); Member, Board of Directors, John Hancock USA, John Hancock Life & Health, John Hancock New York (2012-2013). Trustee of various trusts within the John Hancock Fund Complex (since 2018). | ||

Principal officers who are not Trustees

| Name, year of birth Position(s) held with fund Principal occupation(s) during past 5 years | Officer of the Trust since |

| Francis V. Knox, Jr.,Born: 1947 | 2005 |

| Chief Compliance Officer Vice President, John Hancock Financial Services (since 2005); Chief Compliance Officer, various trusts within the John Hancock Fund Complex, John Hancock Investment Management LLC, and John Hancock Variable Trust Advisers LLC (since 2005). | |

| Charles A. Rizzo, Born: 1957 | 2007 |

| Chief Financial Officer Vice President, John Hancock Financial Services (since 2008); Senior Vice President, John Hancock Investment Management LLC and John Hancock Variable Trust Advisers LLC (since 2008); Chief Financial Officer of various trusts within the John Hancock Fund Complex (since 2007). | |

| Salvatore Schiavone, Born: 1965 | 2010 |

| Treasurer Assistant Vice President, John Hancock Financial Services (since 2007); Vice President, John Hancock Investment Management LLC and John Hancock Variable Trust Advisers LLC (since 2007); Treasurer of various trusts within the John Hancock Fund Complex (since 2007, including prior positions). | |

Principal officers who are not Trustees (continued)

| Name, year of birth Position(s) held with fund Principal occupation(s) during past 5 years | Officer of the Trust since |

| Christopher (Kit) Sechler,Born: 1973 | 2018 |

| Chief Legal Officer and Secretary Vice President and Deputy Chief Counsel, John Hancock Investments (since 2015); Assistant Vice President and Senior Counsel (2009-2015), John Hancock Investment Management; Chief Legal Officer and Secretary of various trusts within the John Hancock Fund Complex (since 2018); Assistant Secretary of John Hancock Investment Management LLC and John Hancock Variable Trust Advisers LLC (since 2009). | |

The business address for all Trustees and Officers is 200 Berkeley Street, Boston, Massachusetts 02116-5023.

| 1 | Mr. Boyle, Mr. Cunningham, Ms. Fey, Mr. McClellan and Mr. Russo serve as Trustees for a term expiring in 2020; Mr. Bardelis, Mr. Burgess and Ms. Harrison serve as Trustees for a term expiring in 2021; Mr. Arnott, Ms. Jackson, Mr. Oates and Mr. Pruchansky serve as Trustees for a term expiring in 2022; Mr. Boyle has served as Trustee at various times prior to date listed in the table. |

| 2 | Member of the Audit Committee. |

| 3 | The Trustee is a Non-Independent Trustee due to current or former positions with the Advisor and certain of its affiliates. |

Trustees Hassell H. McClellan,Chairperson Officers Andrew G. Arnott Francis V. Knox, Jr. Charles A. Rizzo Salvatore Schiavone Christopher (Kit) Sechler | Investment advisor John Hancock Investment Management LLC Subadvisors Epoch Investment Partners, Inc. (Epoch) Portfolio Managers The Investment Team at Epoch and WellsCap Distributor John Hancock Investment Management Distributors LLC Custodian State Street Bank and Trust Company Transfer agent Computershare Shareowner Services, LLC Legal counsel K&L Gates LLP Independent registered public accounting firm PricewaterhouseCoopers LLP Stock symbol Listed New York Stock Exchange: HTY |

* Member of the Audit Committee

† Non-Independent Trustee

For shareholder assistance refer to page 6

| You can also contact us: | |||

| 800-852-0218 jhinvestments.com | Regular mail: Computershare | Express mail: Computershare | |

The fund's proxy voting policies and procedures, as well as the fund's proxy voting record for the most recent twelve-month period ended June 30, are available free of charge on the Securities and Exchange Commission (SEC) website at sec.gov or on our website.

All of the fund's holdings as of the end of the third month of every fiscal quarter are filed with the SEC on Form N-PORT within 60 days of the end of the fiscal quarter. The fund's Form N-PORT filings are available on our website and the SEC's website, sec.gov.

We make this information on your fund, as well asmonthly portfolio holdings, and other fund details available on our website at jhinvestments.com or by calling 800-852-0218.

The report is certified under the Sarbanes-Oxley Act, which requires closed-end funds and other public companies to affirm that, to the best of their knowledge, the information in their financial reports is fairly and accurately stated in all material respects.

John Hancock family of funds