S- 2 | |

S- 3 | |

S- 3 | |

S- 4 | |

S- 4 | |

S- 5 | |

S- 5 |

Prospectus | |

Prospectus Summary | 1 |

Summary of Risks | 5 |

Summary of Fund Expenses | 8 |

Financial Highlights | 10 |

Market and Net Asset Value Information | 12 |

The Fund | 12 |

Use of Proceeds | 12 |

Investment Objective | 13 |

Principal investment strategies | 13 |

Risk Factors | 21 |

Management of the Fund | 29 |

Custodian and Transfer Agent | 31 |

Determination of Net Asset Value | 32 |

Distribution Policy | 33 |

Dividend Reinvestment Plan | 34 |

Closed-End Fund Structure | 35 |

U.S. Federal Income Tax Matters | 35 |

Plan of Distribution | 38 |

Description of Capital Structure | 39 |

Certain Provisions in the Declaration of Trust and By-Laws | 41 |

Reports to Shareholders | 43 |

Independent Registered Public Accounting Firm | 43 |

Legal and Regulatory Matters | 43 |

Incorporation by Reference | 43 |

Additional Information | 43 |

Table of Contents of the Statement of Additional Information | 44 |

The Fund’s Privacy Policy | 44 |

Shareholder Transaction Expenses (%) | |

Sales load (as a percentage of offering price) (1) | 1.00 |

Offering expenses (as a percentage of offering price) (2) | 1.55 |

Dividend Reinvestment Plan fees (3) | None |

Annual Expenses (Percentage of Net Assets Attributable to Common Shares) (%) | |

Management fees (4) | 0.90 |

Other expenses | 0.70 |

Total Annual Operating Expenses | 1.60 |

Contractual Expense Reimbursement (5) | (0.01 ) |

Total Annual Fund Operating Expenses After Expense Reimbursements | 1.59 |

1 Year | 3 Years | 5 Years | 10 Years | |

Total Expenses | $41 | $75 | $110 | $211 |

As of October 31, 2023 (audited) | As of February 14, 2024 (unaudited) | Pro Forma (unaudited) | |

Actual | Actual | As Adjusted | |

Net assets ($) | 53,163,196 | 57,149,121 | 58,912,009 |

Common Shares of beneficial interest outstanding — unlimited number of shares authorized with $0.01 par value | 10,921,751 | 10,921,751 | 11,277,753 |

Paid-in capital ($) | 90,668,867 | 94,751,175 | 96,514,063 |

Total distributable earnings (loss) | (37,505,671 ) | (37,602,054 ) | (37,602,054 ) |

Net assets ($) | 53,163,196 | 57,149,121 | 58,912,009 |

Net asset value per share ($) | 4.87 | 5.23 | 5.22 |

Market Price | NAV per Share on Date of Market Price High and Low | Premium/(Discount) on Date of Market Price High and Low | ||||

Fiscal Quarter Ended | High ($) | Low ($) | High ($) | Low ($) | High (%) | Low (%) |

January 31, 2022 | 6.74 | 6.11 | 6.60 | 6.32 | 2.12 | (3.32 ) |

April 30, 2022 | 6.85 | 6.05 | 6.40 | 6.06 | 7.03 | (0.17 ) |

July 31, 2022 | 6.21 | 5.05 | 6.27 | 5.49 | (0.96 ) | (8.01 ) |

October 31, 2022 | 5.54 | 4.36 | 5.91 | 4.95 | (6.26 ) | (11.92 ) |

January 31, 2023 | 5.26 | 4.63 | 5.63 | 5.33 | (6.57 ) | (13.13 ) |

April 30, 2023 | 5.50 | 4.70 | 5.70 | 5.21 | (3.51 ) | (9.79 ) |

July 31, 2023 | 4.87 | 4.49 | 5.47 | 5.30 | (10.97 ) | (15.28 ) |

October 31, 2023 | 4.79 | 4.04 | 5.48 | 4.80 | (12.59 ) | (15.83 ) |

January 31, 2024 | 5.14 | 4.13 | 5.28 | 4.92 | (2.65 ) | (16.06 ) |

Title of Class | Amount Authorized | Amount Held by the Fund or for its Account | Amount Outstanding |

Common Shares | Unlimited | 0 | 10,921,751 |

Shareholder Transaction Expenses (%) | |

Sales load (as a percentage of offering price) 1 | |

Offering expenses (as a percentage of offering price) 1 | |

Dividend Reinvestment Plan fees 2 | None |

Annual Expenses (Percentage of Net Assets Attributable to Common Shares) (%) | |

Management fees | 0.90 |

Other expenses | 0.70 |

Total Annual Operating Expenses | 1.60 |

Contractual expense reimbursement 3 | (0.01 ) |

Total annual fund operating expenses after expense reimbursements | 1.59 |

1 Year | 3 Years | 5 Years | 10 Years | |

Total Expenses | $16 | $50 | $87 | $189 |

Period ended | 10-31-23 | 10-31-22 | 10-31-21 | 10-31-20 | 10-31-19 |

Per share operating performance | |||||

Net asset value, beginning of period | $5.31 | $6.47 | $5.78 | $7.61 | $7.63 |

Net investment income 1 | 0.27 | 0.30 | 0.32 | 0.36 | 0.42 |

Net realized and unrealized gain (loss) on investments | (0.07 ) | (0.82 ) | 1.01 | (1.55 ) | 0.19 |

Total from investment operations | 0.20 | (0.52 ) | 1.33 | (1.19 ) | 0.61 |

Less distributions | |||||

From net investment income | (0.27 ) | (0.29 ) | (0.32 ) | (0.35 ) | (0.42 ) |

From tax return of capital | (0.37 ) | (0.35 ) | (0.32 ) | (0.29 ) | (0.22 ) |

Total distributions | (0.64 ) | (0.64 ) | (0.64 ) | (0.64 ) | (0.64 ) |

Anti-dilutive impact of repurchase plan | — | — | — | — 2,3 | 0.01 3 |

Net asset value, end of period | $4.87 | $5.31 | $6.47 | $5.78 | $7.61 |

Per share market value, end of period | $4.10 | $4.71 | $6.37 | $4.75 | $6.93 |

Total return at net asset value (%) 4,5 | 4.75 | (8.16 ) | 23.93 | (14.79 ) | 9.45 |

Total return at market value (%) 4 | (0.58 ) | (17.26 ) | 48.48 | (23.10 ) | 10.06 |

Ratios and supplemental data | |||||

Net assets, end of period (in millions) | $53 | $58 | $71 | $63 | $83 |

Ratios (as a percentage of average net assets): | |||||

Expenses before reductions | 1.60 | 1.38 | 1.42 | 1.32 | 1.35 |

Expenses including reductions | 1.59 | 1.37 | 1.42 | 1.31 | 1.34 |

Net investment income | 4.97 | 4.93 | 4.85 | 5.43 | 5.60 |

Portfolio turnover (%) | 308 | 311 | 302 | 301 | 260 |

Period ended | 10-31-18 | 10-31-17 | 10-31-16 | 10-31-15 | 10-31-14 |

Per share operating performance | |||||

Net asset value, beginning of period | $8.90 | $8.77 | $10.07 | $11.44 | $12.25 |

Net investment income 1 | 0.41 | 0.44 | 0.52 | 0.64 | 0.80 |

Net realized and unrealized gain (loss) on investments | (0.86 ) | 0.66 | (0.57 ) | (0.75 ) | (0.36 ) |

Total from investment operations | (0.45 ) | 1.10 | (0.05 ) | (0.11 ) | 0.44 |

Less distributions | |||||

From net investment income | (0.41 ) | (0.44 ) | (0.52 ) | (0.75 ) | (1.28 ) |

From tax return of capital | (0.41 ) | (0.54 ) | (0.76 ) | (0.53 ) | — |

Total distributions | (0.82 ) | (0.98 ) | (1.28 ) | (1.28 ) | (1.28 ) |

Anti-dilutive impact of shelf offering | — | 0.01 | 0.03 | 0.02 | 0.03 |

Net asset value, end of period | $7.63 | $8.90 | $8.77 | $10.07 | $11.44 |

Per share market value, end of period | $6.91 | $8.97 | $10.35 | $9.51 | $12.59 |

Total return at net asset value (%) 2,3 | (5.45 ) | 12.95 | (1.28 ) | (0.65 ) | 3.65 |

Total return at market value (%) 2 | (15.04 ) | (3.54 ) | 23.37 | (14.74 ) | 10.55 |

Ratios and supplemental data | |||||

Net assets, end of period (in millions) | $84 | $98 | $96 | $106 | $117 |

Ratios (as a percentage of average net assets): | |||||

Expenses before reductions | 1.35 | 1.32 | 1.32 | 1.27 | 1.32 |

Expenses including reductions | 1.34 | 1.31 | 1.32 | 1.26 | 1.32 |

Net investment income | 4.90 | 4.96 | 5.60 | 6.01 | 6.60 |

Portfolio turnover (%) | 208 | 220 | 253 | 261 | 228 |

Market Price | NAV per Share on Date of Market Price High and Low | Premium/(Discount) on Date of Market Price High and Low | ||||

Fiscal Quarter Ended | High ($) | Low ($) | High ($) | Low ($) | High (%) | Low (%) |

January 31, 2022 | 6.74 | 6.11 | 6.60 | 6.32 | 2.12 | (3.32 ) |

April 30, 2022 | 6.85 | 6.05 | 6.40 | 6.06 | 7.03 | (0.17 ) |

July 31, 2022 | 6.21 | 5.05 | 6.27 | 5.49 | (0.96 ) | (8.01 ) |

October 31, 2022 | 5.54 | 4.36 | 5.91 | 4.95 | (6.26 ) | (11.92 ) |

January 31, 2023 | 5.26 | 4.63 | 5.63 | 5.33 | (6.57 ) | (13.13 ) |

April 30, 2023 | 5.50 | 4.70 | 5.70 | 5.21 | (3.51 ) | (9.79 ) |

July 31, 2023 | 4.87 | 4.49 | 5.47 | 5.30 | (10.97 ) | (15.28 ) |

October 31, 2023 | 4.79 | 4.04 | 5.48 | 4.80 | (12.59 ) | (15.83 ) |

January 31, 2024 | 5.14 | 4.13 | 5.28 | 4.92 | (2.65 ) | (16.06 ) |

Title of Class | Amount Authorized | Amount Held by the Fund or for its Account | Amount Outstanding |

Common Shares | Unlimited | 0 | 10,921,751.00 |

Page | |

Organization of the Fund | 2 |

Additional Investment Policies and Risks | 2 |

Investment Restrictions | 11 |

Portfolio Turnover | 12 |

Those Responsible for Management | 12 |

Shareholders of the Fund | 21 |

Investment Advisory and Other Services | 21 |

Determination of Net Asset Value | 25 |

Portfolio Brokerage | 27 |

Additional Information Concerning Taxes | 28 |

Other Information | 32 |

Custodian and Transfer Agent | 33 |

Independent Registered Public Accounting Firm | 33 |

Reports to Shareholders | 33 |

Incorporation by Reference | 33 |

Codes of Ethics | 34 |

Additional Information | 34 |

Appendix A: Description of Bond Ratings | A-1 |

Appendix B: Proxy Voting Policies and Procedures | B-1 |

Name (Birth Year) | Current Position(s) with the Trust 1 | Principal Occupation(s) and Other Directorships During the Past 5 Years | Number of Funds in John Hancock Fund Complex Overseen by Trustee |

Non-Independent Trustees | |||

Andrew G. Arnott 2 (1971) | Trustee (since 2017) | Global Head of Retail for Manulife (since 2022); Head of Wealth and Asset Management, United States and Europe, for John Hancock and Manulife (2018-2023); Director and Chairman, John Hancock Investment Management LLC (2005-2023, including prior positions); Director and Chairman, John Hancock Variable Trust Advisers LLC (2006-2023, including prior positions); Director and Chairman, John Hancock Investment Management Distributors LLC (2004-2023, including prior positions); President of various trusts within the John Hancock Fund Complex (2007-2023, including prior positions). Trustee of various trusts within the John Hancock Fund Complex (since 2017). | 177 |

Paul Lorentz 2 (1968) | Trustee (since 2022) | Global Head, Manulife Wealth and Asset Management (since 2017); General Manager, Manulife, Individual Wealth Management and Insurance (2013–2017); President, Manulife Investments (2010–2016). Trustee of various trusts within the John Hancock Fund Complex (since 2022). | 175 |

Name (Birth Year) | Current Position(s) with the Trust 1 | Principal Occupation(s) and Other Directorships During the Past 5 Years | Number of Funds in John Hancock Fund Complex Overseen by Trustee |

Independent Trustees | |||

James R. Boyle (1959) | Trustee (since 2015) 3 | Board Member, United of Omaha Life Insurance Company (since 2022). Board Member, Mutual of Omaha Investor Services, Inc. (since 2022). Foresters Financial, Chief Executive Officer (2018–2022) and board member (2017–2022). Manulife Financial and John Hancock, more than 20 years, retiring in 2012 as Chief Executive Officer, John Hancock and Senior Executive Vice President, Manulife Financial. Trustee of various trusts within the John Hancock Fund Complex (2005–2014 and since 2015). | 175 |

William H. Cunningham (1944) | Trustee (since 2007) | Professor, University of Texas, Austin, Texas (since 1971); former Chancellor, University of Texas System and former President of the University of Texas, Austin, Texas; Director (since 2006), Lincoln National Corporation (insurance); Director, Southwest Airlines (since 2000). Trustee of various trusts within the John Hancock Fund Complex (since 1986). | 177 |

Name (Birth Year) | Current Position(s) with the Trust 1 | Principal Occupation(s) and Other Directorships During the Past 5 Years | Number of Funds in John Hancock Fund Complex Overseen by Trustee |

Independent Trustees | |||

Noni L. Ellison (1971) | Trustee, each Trust (since 2022) | Senior Vice President, General Counsel & Corporate Secretary, Tractor Supply Company (rural lifestyle retailer) (since 2021); General Counsel, Chief Compliance Officer & Corporate Secretary, Carestream Dental, L.L.C. (2017–2021); Associate General Counsel & Assistant Corporate Secretary, W.W. Grainger, Inc. (global industrial supplier) (2015–2017); Board Member, Goodwill of North Georgia, 2018 (FY2019)–2020 (FY2021); Board Member, Howard University School of Law Board of Visitors (since 2021); Board Member, University of Chicago Law School Board of Visitors (since 2016); Board member, Children’s Healthcare of Atlanta Foundation Board (2021–2023). Trustee of various trusts within the John Hancock Fund Complex (since 2022). | 175 |

Grace K. Fey (1946) | Trustee (since 2012) | Chief Executive Officer, Grace Fey Advisors (since 2007); Director and Executive Vice President, Frontier Capital Management Company (1988–2007); Director, Fiduciary Trust (since 2009). Trustee of various trusts within the John Hancock Fund Complex (since 2008). | 179 |

Dean C. Garfield (1968) | Trustee, each Trust (since 2022) | Vice President, Netflix, Inc. (since 2019); President & Chief Executive Officer, Information Technology Industry Council (2009–2019); NYU School of Law Board of Trustees (since 2021); Member, U.S. Department of Transportation, Advisory Committee on Automation (since 2021); President of the United States Trade Advisory Council (2010–2018); Board Member, College for Every Student (2017–2021); Board Member, The Seed School of Washington, D.C. (2012–2017); Advisory Board Member of the Block Center for Technology and Society (since 2019). Trustee of various trusts within the John Hancock Fund Complex (since 2022). | 175 |

Deborah C. Jackson (1952) | Trustee (since 2008) | President, Cambridge College, Cambridge, Massachusetts (2011–2023); Board of Directors, Amwell Corporation (since 2020); Board of Directors, Massachusetts Women’s Forum (2018–2020); Board of Directors, National Association of Corporate Directors/New England (2015–2020); Chief Executive Officer, American Red Cross of Massachusetts Bay (2002–2011); Board of Directors of Eastern Bank Corporation (since 2001); Board of Directors of Eastern Bank Charitable Foundation (since 2001); Board of Directors of Boston Stock Exchange (2002–2008); Board of Directors of Harvard Pilgrim Healthcare (health benefits company) (2007–2011). Trustee of various trusts within the John Hancock Fund Complex (since 2008). | 177 |

Hassell H. McClellan (1945) | Trustee (since 2012) and Chairperson of the Board (since 2017) | Trustee of Berklee College of Music (since 2022); Director/Trustee, Virtus Funds (2008–2020); Director, The Barnes Group (2010–2021); Associate Professor, The Wallace E. Carroll School of Management, Boston College (retired 2013). Trustee (since 2005) and Chairperson of the Board (since 2017) of various trusts within the John Hancock Fund Complex. | 179 |

Name (Birth Year) | Current Position(s) with the Trust 1 | Principal Occupation(s) and Other Directorships During the Past 5 Years | Number of Funds in John Hancock Fund Complex Overseen by Trustee |

Independent Trustees | |||

Steven R. Pruchansky (1944) | Trustee (since 2007) and Vice Chairperson of the Board (since 2012) | Managing Director, Pru Realty (since 2017); Chairman and Chief Executive Officer, Greenscapes of Southwest Florida, Inc. (2014–2020); Director and President, Greenscapes of Southwest Florida, Inc. (until 2000); Member, Board of Advisors, First American Bank (until 2010); Managing Director, Jon James, LLC (real estate) (since 2000); Partner, Right Funding, LLC (2014–2017); Director, First Signature Bank & Trust Company (until 1991); Director, Mast Realty Trust (until 1994); President, Maxwell Building Corp. (until 1991). Trustee (since 1992), Chairperson of the Board (2011–2012), and Vice Chairperson of the Board (since 2012) of various trusts within the John Hancock Fund Complex. | 175 |

Frances G. Rathke (1960) | Trustee (since 2020) | Director, Audit Committee Chair, Oatly Group AB (plant-based drink company) (since 2021); Director, Audit Committee Chair and Compensation Committee Member, Green Mountain Power Corporation (since 2016); Director, Treasurer and Finance & Audit Committee Chair, Flynn Center for Performing Arts (since 2016); Director and Audit Committee Chair, Planet Fitness (since 2016); Chief Financial Officer and Treasurer, Keurig Green Mountain, Inc. (2003–retired 2015). Trustee of various trusts within the John Hancock Fund Complex (since 2020). | 175 |

Gregory A. Russo (1949) | Trustee (since 2008) | Director and Audit Committee Chairman (2012–2020), and Member, Audit Committee and Finance Committee (2011–2020), NCH Healthcare System, Inc. (holding company for multi-entity healthcare system); Director and Member (2012–2018), and Finance Committee Chairman (2014–2018), The Moorings, Inc. (nonprofit continuing care community); Global Vice Chairman, Risk & Regulatory Matters, KPMG LLP (KPMG) (2002–2006); Vice Chairman, Industrial Markets, KPMG (1998–2002). Trustee of various trusts within the John Hancock Fund Complex (since 2008). | 175 |

Name (Birth Year) | Current Position(s) with the Trust 1 | Principal Occupation(s) During the Past 5 Years |

Kristie M. Feinberg (1975) | President (since 2023) | Head of Wealth & Asset Management, U.S. and Europe, for John Hancock and Manulife (since 2023); Director and Chairman, John Hancock Investment Management LLC (since 2023); Director and Chairman, John Hancock Variable Trust Advisers LLC (since 2023); Director and Chairman, John Hancock Investment Management Distributors LLC (since 2023); CFO and Global Head of Strategy, Manulife Investment Management (2021–2023, including prior positions); CFO Americas & Global Head of Treasury, Invesco, Ltd., Invesco US (2019–2020, including prior positions); Senior Vice President, Corporate Treasurer and Business Controller, OppenheimerFunds (2001–2019, including prior positions); President of various trusts within the John Hancock Fund Complex (since 2023). |

Charles A. Rizzo (1957) | Chief Financial Officer (since 2007) | Vice President, John Hancock Financial Services (since 2008); Senior Vice President, John Hancock Investment Management LLC and John Hancock Variable Trust Advisers LLC (since 2008); Chief Financial Officer of various trusts within the John Hancock Fund Complex (since 2007). |

Salvatore Schiavone (1965) | Treasurer (since 2010) | Assistant Vice President, John Hancock Financial Services (since 2007); Vice President, John Hancock Investment Management LLC and John Hancock Variable Trust Advisers LLC (since 2007); Treasurer of various trusts within the John Hancock Fund Complex (since 2007, including prior positions). |

Christopher (Kit) Sechler (1973) | Secretary and Chief Legal Officer (since 2018) | Vice President and Deputy Chief Counsel, John Hancock Investment Management (since 2015); Assistant Vice President and Senior Counsel (2009–2015), John Hancock Investment Management; Assistant Secretary of John Hancock Investment Management LLC and John Hancock Variable Trust Advisers LLC (since 2009); Chief Legal Officer and Secretary of various trusts within the John Hancock Fund Complex (since 2009, including prior positions). |

Trevor Swanberg (1979) | Chief Compliance Officer (since 2020) | Chief Compliance Officer, John Hancock Investment Management LLC and John Hancock Variable Trust Advisers LLC (since 2020); Deputy Chief Compliance Officer, John Hancock Investment Management LLC and John Hancock Variable Trust Advisers LLC (2019–2020); Assistant Chief Compliance Officer, John Hancock Investment Management LLC and John Hancock Variable Trust Advisers LLC (2016–2019); Vice President, State Street Global Advisors (2015–2016); Chief Compliance Officer of various trusts within the John Hancock Fund Complex (since 2016, including prior positions). |

Name of Trustee | Total Compensation from Trust ($) | Total Compensation from Trust and the John Hancock Fund Complex ($) 2 |

Independent Trustees | ||

James R. Boyle | 4,000 | 455,000 |

Peter S. Burgess 3 | 4,000 | 22,000 |

William H. Cunningham | 4,000 | 530,000 |

Noni L. Ellison | 4,000 | 435,000 |

Grace K. Fey | 4,000 | 630,000 |

Dean C. Garfield | 4,000 | 435,000 |

Deborah C. Jackson | 4,000 | 535,000 |

Patricia Lizarraga 4 | 4,000 | 413,000 |

Hassell H. McClellan | 4,000 | 826,000 |

Steven R. Pruchansky | 4,000 | 455,000 |

Frances G. Rathke | 4,000 | 455,000 |

Gregory A. Russo | 4,000 | 475,000 |

Non-Independent Trustees | ||

Andrew G. Arnott | ||

Marianne Harrison 5 | ||

Paul Lorentz | ||

Trust/Funds | Tax-Advantaged Global Shareholder Yield Fund | Total – John Hancock Fund Complex |

Independent Trustees | ||

James R. Boyle | $10,001 - $50,000 | Over $100,000 |

William H. Cunningham | $10,001 - $50,000 | Over $100,000 |

Noni L. Ellison | None | Over $100,000 |

Grace K. Fey | $10,001 - $50,000 | Over $100,000 |

Dean C. Garfield 1 | None | Over $100,000 |

Deborah C. Jackson | $1 - $10,000 | Over $100,000 |

Hassell H. McClellan | $10,001 - $50,000 | Over $100,000 |

Steven R. Pruchansky | $1 - $10,000 | Over $100,000 |

Frances G. Rathke | $10,001 - $50,000 | Over $100,000 |

Gregory A. Russo | $10,001 - $50,000 | Over $100,000 |

Non-Independent Trustees | ||

Andrew G. Arnott | None | Over $100,000 |

Paul Lorentz | None | None |

Name and Address of Owner | Amount | Percent |

SIT Investment Associates Inc. 3300 IDS Center 80 South Eighth Street Minneapolis, MN 55402 | 1,099,678 | 9.99% 1 |

First Trust Portfolios LP 120 East Liberty Drive Suite 400 Wheaton, IL 60187 | 784,895 | 7.18% 2 |

October 31, 2023 | October 31, 2022 | October 31, 2021 |

$530,440 | $591,923 | $674,141 |

October 31, 2023 | October 31, 2022 | October 31, 2021 |

$12,264 | $10,026 | $10,998 |

Portfolio Manager | Other Registered Investment Companies | Other Pooled Investment Vehicles | Other Accounts | |||

Number of Accounts | Total Assets ($millions) | Number of Accounts | Total Assets ($millions) | Number of Accounts | Total Assets ($millions) | |

William W. Priest, CFA 1 | 7 | 4,501 | 28 | 7,530 | 57 | 4,279 |

-* | -* | 1* | 47* | 7* | 429* | |

Kera Van Valen, CFA | 6 | 4,373 | 12 | 2,124 | 11 | 1,599 |

-* | -* | -* | -* | -* | -* | |

John Tobin, Ph.D., CFA | 6 | 4,373 | 12 | 2,124 | 11 | 1,599 |

-* | -* | -* | -* | -* | -* | |

Michael A. Welhoelter, CFA | 8 | 4,694 | 38 | 9,826 | 60 | 4,377 |

-* | -* | 1* | 47* | 7* | 429* | |

Portfolio Manager | Range of Beneficial Ownership in the Fund | Range of Beneficial Ownership in Similarly Managed Accounts |

William W. Priest, CFA 1 | $100,001 $500,000 | none |

John Tobin, Ph.D., CFA | none | $10,001–$50,000 |

Kera Van Valen, CFA | none | $10,001–$50,000 |

Michael A. Welhoelter, CFA | none | $100,001 $500,000 |

October 31, 2023 | October 31, 2022 | October 31, 2021 |

$131,603 | $101,305 | $127,178 |

Fund | Short-term Losses | Long-term Losses | Total |

John Hancock Tax-Advantaged Global Shareholder Yield Fund | $0 | $20,402,462 | $20,402,462 |

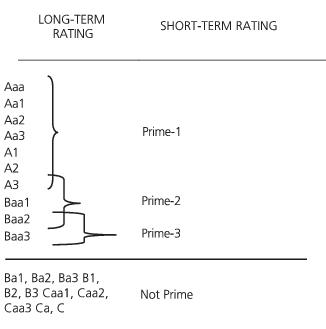

US Municipal Short-Term Versus Long-Term Ratings | ||

NOTES | LONG-TERM RATING | DEMAND OBLIGATIONS WITH CONDITIONAL LIQUIDITY SUPPORT |

MIG 1 | Aaa Aa1 Aa2 Aa3 A1 A2 | VMIG 1 |

MIG 2 | A3 | VMIG 2 |

MIG 3 | Baa1 Baa2 Baa3 | VMIG 3* SG |

SG | Ba1, Ba2, Ba3 B1, B2, B3 Caa1, Caa2, Caa3 Ca, C | |

5E: Proxy Voting Policies and Procedures for the Adviser

General Compliance Policies for Trust & Adviser

Section 5: Fiduciary Standards & Affiliated Persons Issues

| Applies to | Adviser | |

| Risk Theme | Proxy Voting | |

| Policy Owner | Jim Interrante | |

| Effective Date | 12-1-2019 |

5E. Advisers Proxy Voting Policy

Overview

The SEC adopted Rule 206(4)-6 under the Advisers Act, which requires investment advisers with voting authority to adopt and implement written policies and procedures that are reasonably designed to ensure that the investment adviser votes client securities in the best interest of clients. The procedures must include how the investment adviser addresses material conflicts that may arise between the interests of the investment adviser and those of its clients. The Advisers are registered investment advisers under the Advisers Act and serve as the investment advisers to the Funds. The Advisers generally retain one or more sub-advisers to manage the assets of the Funds, including voting proxies with respect to a Fund’s portfolio securities. From time to time, however, the Advisers may elect to manage directly the assets of a Fund, including voting proxies with respect to such Fund’s portfolio securities, or a Fund’s Board may otherwise delegate to the Advisers authority to vote such proxies. Rule 206(4)-6 under the Advisers Act requires that a registered investment adviser adopt and implement written policies and procedures reasonably designed to ensure that it votes proxies with respect to a client’s securities in the best interest of the client.

Firms are required by Advisers Act Rule 204-2(c)(2) to maintain records of their voting policies and procedures, a copy of each proxy statement that the investment adviser receives regarding client securities, a record of each vote cast by the investment adviser on behalf of a client, a copy of any document created by the investment adviser that was material to making a decision how to vote proxies on behalf of a client, and a copy of each written client request for information on how the adviser voted proxies on behalf of the client, as well as a copy of any written response by the investment adviser to any written or oral client request for information on how the adviser voted that client’s proxies.

Investment companies must disclose information about the policies and procedures used to vote proxies on the investment company’s portfolio securities and must file the fund’s proxy voting record with the SEC annually on Form N-PX.

Pursuant thereto, the Advisers have adopted and implemented these proxy voting policies and procedures (the “Proxy Procedures”).

Policy

It is the Advisers’ policy to comply with Rule 206(4)-6 and Rule 204-2(c)(2) under the Advisers Act as described above. In general, the Advisers delegate proxy voting decisions to the sub-advisers managing the funds. If an instance occurs where a conflict of interest arises between the shareholders and a particular sub-adviser, however, the Adviser retains the right to influence and/or direct the conflicting proxy voting decisions.

Regulatory Requirement

Rule 206(4)-6 under the Advisers Act

Reporting

Form N-PX

Advisers will provide the Board with notice and a copy of any amendments or revisions to the Procedures and will report quarterly to the Board all material changes to these Proxy Procedures.

The CCO’s annual written compliance report to the Board will contain a summary of material changes to the Proxy Procedures during the period covered by the report.

If the Advisers or the Designated Person vote any proxies in a manner inconsistent with either these Proxy Procedures or a Fund’s proxy voting policies and procedures, the CCO will provide the Board with a report detailing such exceptions.

Procedure

Fiduciary Duty

The Advisers have a fiduciary duty to vote proxies on behalf of a Fund in the best interest of the Fund and its shareholders.

Voting of Proxies—Advisers

The Advisers will vote proxies with respect to a Fund’s portfolio securities when authorized to do so by the Fund and subject to the Fund’s proxy voting policies and procedures and any further direction or delegation of authority by the Fund’s Board. The decision on how to vote a proxy will be made by the person(s) to whom the Advisers have from time to time delegated such responsibility (the “Designated Person”). The Designated Person may include the Fund’s portfolio manager(s) or a Proxy Voting Committee, as described below.

When voting proxies with respect to a Fund’s portfolio securities, the following standards will apply:

| • | The Designated Person will vote based on what it believes is in the best interest of the Fund and its shareholders and in accordance with the Fund’s investment guidelines. |

| • | Each voting decision will be made independently. To assist with the analysis of voting issues and/or to carry out the actual voting process the Designated Person may enlist the services of (1) reputable professionals (who may include persons employed by or otherwise associated with the Advisers or any of its affiliated persons) or (2) independent proxy evaluation services such as Institutional Shareholder Services. However, the ultimate decision as to how to vote a proxy will remain the responsibility of the Designated Person. |

| • | The Advisers believe that a good management team of a company will generally act in the best interests of the company. Therefore, the Designated Person will take into consideration as a key factor in voting proxies with respect to securities of a company that are held by the Fund the quality of the company’s management. In general, the Designated Person will vote as recommended by company management except in situations where the Designated Person believes such recommended vote is not in the best interests of the Fund and its shareholders. |

| • | As a general principle, voting with respect to the same portfolio securities held by more than one Fund should be consistent among those Funds having substantially the same investment mandates. |

| • | The Advisers will provide the Fund, from time to time in accordance with the Fund’s proxy voting policies and procedures and any applicable laws and regulations, a record of the Advisers’ voting of proxies with respect to the Fund’s portfolio securities. |

Material Conflicts of Interest

In carrying out its proxy voting responsibilities, the Advisers will monitor and resolve potential material conflicts (“Material Conflicts”) between the interests of (a) a Fund and (b) the Advisers or any of its affiliated persons. Affiliates of the Advisers include Manulife Financial Corporation and its subsidiaries. Material Conflicts may arise, for example, if a proxy vote relates to matters involving any of these companies or other issuers in which the Advisers or any of their affiliates has a substantial equity or other interest.

5E. Advisers Proxy Voting Policy

If the Advisers or a Designated Person become aware that a proxy voting issue may present a potential Material Conflict, the issue will be referred to the Advisers’ Legal Department and/or the Office of the CCO. If the Legal Department and/or the Office of the CCO, as applicable determines that a potential Material Conflict does exist, a Proxy Voting Committee will be appointed to consider and resolve the issue. The Proxy Voting Committee may make any determination that it considers reasonable and may, if it chooses, request the advice of an independent, third-party proxy service on how to vote the proxy.

Voting Proxies of Underlying Funds of a Fund of Funds

The Advisers or the Designated Person will vote proxies with respect to the shares of a Fund that are held by another Fund that operates as a Fund of Funds”) in the manner provided in the proxy voting policies and procedures of the Fund of Funds (including such policies and procedures relating to material conflicts of interest) or as otherwise directed by the board of trustees or directors of the Fund of Funds.

Proxy Voting Committee(s)

The Advisers will from time to time, and on such temporary or longer-term basis as they deem appropriate, establish one or more Proxy Voting Committees. A Proxy Voting Committee shall include the Advisers’ CCO and may include legal counsel. The terms of reference and the procedures under which a Proxy Voting Committee will operate will be reviewed from time to time by the Legal and Compliance Department. Records of the deliberations and proxy voting recommendations of a Proxy Voting Committee will be maintained in accordance with applicable law, if any, and these Proxy Procedures. Requested shareholder proposals or other Shareholder Advocacy must be submitted for consideration pursuant to the Shareholder Advocacy Policy and Procedures.

Voting of Proxies - SubAdvisers

In the case of proxies voted by a sub-adviser to a Fund pursuant to the Fund’s proxy voting procedures, the Advisers will request the sub-adviser to certify to the Advisers that the sub-adviser has voted the Fund’s proxies as required by the Fund’s proxy voting policies and procedures and that such proxy votes were executed in a manner consistent with these Proxy Procedures and to provide the Advisers with a report detailing any instances where the sub-adviser voted any proxies in a manner inconsistent with the Fund’s proxy voting policies and procedures. The COO of the Advisers will then report to the Board on a quarterly basis regarding the sub-adviser certification and report to the Board any instance where the sub-adviser voted any proxies in a manner inconsistent with the Fund’s proxy voting policies and procedures.

The Fund Administration Department maintains procedures affecting all administration functions for the mutual funds. These procedures detail the disclosure and administration of the Trust’s proxy voting records.

The Trust’s Chief Legal Counsel is responsible for including, in the SAI of each Trust, information about the proxy voting of the Advisers and each sub-adviser.

Reporting to Fund Boards

The CCO of the Advisers will provide the Board with a copy of these Proxy Procedures, accompanied by a certification that represents that the Proxy Procedures have been adopted by the Advisers in conformance with Rule 206(4)-6 under the Advisers Act. Thereafter, the Advisers will provide the Board with notice and a copy of any amendments or revisions to the Procedures and will report quarterly to the Board all material changes to these Proxy Procedures.

The CCO’s annual written compliance report to the Board will contain a summary of material changes to the Proxy Procedures during the period covered by the report.

If the Advisers or the Designated Person vote any proxies in a manner inconsistent with either these Proxy Procedures or a Fund’s proxy voting policies and procedures, the CCO will provide the Board with a report detailing such exceptions

Key Contacts

Investment Compliance

Escalation/Reporting Violations

All John Hancock employees are required to report any known or suspected violation of this policy to the CCO of the Funds.

Related Policies and Procedures

N/A

Document Retention Requirements

The Advisers will retain (or arrange for the retention by a third party of) such records relating to proxy voting pursuant to these Proxy Procedures as may be required from time to time by applicable law and regulations, including the following:

| 1. | These Proxy Procedures and all amendments hereto; |

| 2. | All proxy statements received regarding Fund portfolio securities; |

| 3. | Records of all votes cast on behalf of a Fund; |

| 4. | Records of all Fund requests for proxy voting information; |

| 5. | Any documents prepared by the Designated Person or a Proxy Voting Committee that were material to or memorialized the basis for a voting decision; |

| 6. | All records relating to communications with the Funds regarding Conflicts; and |

| 7. | All minutes of meetings of Proxy Voting Committees. |

The Office of the CCO, and/or the Legal Department are responsible for maintaining the documents set forth above as needed and deemed appropriate. Such documents will be maintained in the Office of the CCO, and/or the Legal Department for the period set forth in the Records Retention Schedule.

Version History | ||||

| Date | Effective Date | Approving Party | ||

| 1 | 01-01-2012 | |||

| 2 | 02-01-2015 | |||

| 3 | Sept. 2015 | |||

| 4 | 05-01-2017 | |||

| 5 | 12-01-2019 | |||

JOHN HANCOCK FUNDS

PROXY VOTING POLICIES AND PROCEDURES

(Updated December 10, 2019)

Overview

Each fund of the Trust or any other registered investment company (or series thereof) (each, a “fund”) is required to disclose its proxy voting policies and procedures in its registration statement and, pursuant to Rule 30b1-4 under the 1940 Act, file annually with the Securities and Exchange Commission and make available to shareholders its actual proxy voting record.

Investment Company Act

An investment company is required to disclose in its SAI either (a) a summary of the policies and procedures that it uses to determine how to vote proxies relating to portfolio securities or (b) a copy of its proxy voting policies.

A fund is also required by Rule 30b1-4 of the Investment Company Act of 1940 to file Form N-PX annually with the SEC, which contains a record of how the fund voted proxies relating to portfolio securities. For each matter relating to a portfolio security considered at any shareholder meeting, Form N-PX is required to include, among other information, the name of the issuer of the security, a brief identification of the matter voted on, whether and how the fund cast its vote, and whether such vote was for or against management. In addition, a fund is required to disclose in its SAI and its annual and semi-annual reports to shareholders that such voting record may be obtained by shareholders, either by calling a toll-free number or through the fund’s website, at the fund’s option.

Advisers Act

Under Advisers Act Rule 206(4)-6, investment advisers are required to adopt proxy voting policies and procedures, and investment companies typically rely on the policies of their advisers or sub-advisers.

Policy

The Majority of the Independent Board of Trustees (the “Board”) of each registered investment company of the Trusts, has adopted these proxy voting policies and procedures (the “Trust Proxy Policy”).

It is the Advisers’ policy to comply with Rule 206(4)-6 of the Advisers Act and Rule 30b1-4 of the 1940 Act as described above. In general, Advisers defer proxy voting decisions to the sub-advisers managing the Funds. It is the policy of the Trusts to delegate the responsibility for voting proxies relating to portfolio securities held by a Fund to the Fund’s respective Adviser or, if the Fund’s Adviser has delegated portfolio management responsibilities to one or more investment sub-adviser(s), to the fund’s sub-adviser(s), subject to the Board’s continued oversight. The sub-adviser for each Fund shall vote all proxies relating to securities held by each Fund and in that connection, and subject to any further policies and procedures contained herein, shall use proxy voting policies and procedures adopted by each sub-adviser in conformance with Rule 206(4)-6 under the Advisers Act.

If an instance occurs where a conflict of interest arises between the shareholders and the designated sub-adviser, however, Advisers retain the right to influence and/or direct the conflicting proxy voting decisions in the best interest of shareholders.

Delegation of Proxy Voting Responsibilities

It is the policy of the Trust to delegate the responsibility for voting proxies relating to portfolio securities held by a fund to the fund’s investment adviser (“adviser”) or, if the fund’s adviser has delegated portfolio management responsibilities to one or more investment sub-adviser(s), to the fund’s sub-adviser(s), subject to the Board’s continued oversight. The sub-adviser for each fund shall vote all proxies relating to securities held by each fund and in that connection, and subject to any further policies and procedures contained herein, shall use proxy voting policies and procedures adopted by each sub-adviser in conformance with Rule 206(4)-6 under the Investment Advisers Act of 1940, as amended (the “Advisers Act”).

Except as noted below under Material Conflicts of Interest, the Trust Proxy Policy with respect to a Fund shall incorporate that adopted by the Fund’s sub-adviser with respect to voting proxies held by its clients (the “Sub-adviser Proxy Policy”). Each Sub-adviser Policy, as it may be amended from time to time, is hereby incorporated by reference into the Trust Proxy Policy. Each sub-adviser to a Fund is directed to comply with these policies and procedures in voting proxies relating to portfolio securities held by a fund, subject to oversight by the Fund’s adviser and by the Board. Each Adviser to a Fund retains the responsibility, and is directed, to oversee each sub- adviser’s compliance with these policies and procedures, and to adopt and implement such additional policies and procedures as it deems necessary or appropriate to discharge its oversight responsibility. Additionally, the Trust’s Chief Compliance Officer (“CCO”) shall conduct such monitoring and supervisory activities as the CCO or the Board deems necessary or appropriate in order to appropriately discharge the CCO’s role in overseeing the sub-advisers’ compliance with these policies and procedures.

The delegation by the Board of the authority to vote proxies relating to portfolio securities of the funds is entirely voluntary and may be revoked by the Board, in whole or in part, at any time.

Voting Proxies of Underlying Funds of a Fund of Funds

A. Where the Fund of Funds is not the Sole Shareholder of the Underlying Fund

With respect to voting proxies relating to the shares of an underlying fund (an “Underlying Fund”) held by a Fund of the Trust operating as a fund of funds (a “Fund of Funds”) in reliance on Section 12(d)(1)(G) of the 1940 Act where the Underlying Fund has shareholders other than the Fund of Funds which are not other Fund of Funds, the Fund of Funds will vote proxies relating to shares of the Underlying Fund in the same proportion as the vote of all other holders of such Underlying Fund shares.

B. Where the Fund of Funds is the Sole Shareholder of the Underlying Fund

In the event that one or more Funds of Funds are the sole shareholders of an Underlying Fund, the Adviser to the Fund of Funds or the Trusts will vote proxies relating to the shares of the Underlying Fund as set forth below unless the Board elects to have the Fund of Funds seek voting instructions from the shareholders of the Funds of Funds in which case the Fund of Funds will vote proxies relating to shares of the Underlying Fund in the same proportion as the instructions timely received from such shareholders.

1. Where Both the Underlying Fund and the Fund of Funds are Voting on Substantially Identical Proposals

In the event that the Underlying Fund and the Fund of Funds are voting on substantially identical proposals (the “Substantially Identical Proposal”), then the Adviser or the Fund of Funds will vote proxies relating to shares of the Underlying Fund in the same proportion as the vote of the shareholders of the Fund of Funds on the Substantially Identical Proposal.

2. Where the Underlying Fund is Voting on a Proposal that is Not Being Voted on by the Fund of Funds

(a) Where there is No Material Conflict of Interest Between the Interests of the Shareholders of the Underlying Fund and the Adviser Relating to the Proposal

In the event that the Fund of Funds is voting on a proposal of the Underlying Fund and the Fund of Funds is not also voting on a substantially identical proposal and there is no material conflict of interest between the interests of the shareholders of the Underlying Fund and the Adviser relating to the Proposal, then the Adviser will vote proxies relating to the shares of the Underlying Fund pursuant to its Proxy Voting Procedures.

(b) Where there is a Material Conflict of Interest Between the Interests of the Shareholders of the Underlying Fund and the Adviser Relating to the Proposal

In the event that the Fund of Funds is voting on a proposal of the Underlying Fund and the Fund of Funds is not also voting on a substantially identical proposal and there is a material conflict of interest between the interests of the shareholders of the Underlying Fund and the Adviser relating to the Proposal, then the Fund of Funds will seek voting instructions from the shareholders of the Fund of Funds on the proposal and will vote proxies relating to shares of the Underlying Fund in the same proportion as the instructions timely received from such shareholders. A material conflict is generally defined as a proposal involving a matter in which the Adviser or one of its affiliates has a material economic interest.

Material Conflicts of Interest

If (1) a sub-adviser to a Fund becomes aware that a vote presents a material conflict between the interests of (a) shareholders of the Fund; and (b) the Fund’s Adviser, sub-adviser, principal underwriter, or any of their affiliated persons, and (2) the sub-adviser does not propose to vote on the particular issue in the manner prescribed by its Sub-adviser Proxy Policy or the material conflict of interest procedures set forth in its Sub-adviser Proxy Policy are otherwise triggered, then the sub-adviser will follow the material conflict of interest procedures set forth in its Sub-adviser Proxy Policy when voting such proxies.

If a Sub-adviser Proxy Policy provides that in the case of a material conflict of interest between Fund shareholders and another party, the sub-adviser will ask the Board to provide voting instructions, the sub-adviser shall vote the proxies, in its discretion, as recommended by an independent third party, in the manner prescribed by its Sub-adviser Proxy Policy or abstain from voting the proxies.

Proxy Voting Committee(s)

The Advisers will from time to time, and on such temporary or longer-term basis as they deem appropriate, establish one or more Proxy Voting Committees. A Proxy Voting Committee shall include the Advisers’ CCO and may include legal counsel. The terms of reference and the procedures under which a Proxy Voting Committee will operate will be reviewed from time to time by the Legal and Compliance Department. Records of the deliberations and proxy voting recommendations of a Proxy Voting Committee will be maintained in accordance with applicable law, if any, and these Proxy Procedures. Requested shareholder proposals or other Shareholder Advocacy in the name of a Fund must be submitted for consideration pursuant to the Shareholder Advocacy Policy and Procedures.

Securities Lending Program

Certain of the Funds participate in a securities lending program with the Trusts through an agent lender. When a Fund’s securities are out on loan, they are transferred into the borrower’s name and are voted by the borrower, in its discretion. Where a sub-adviser determines, however, that a proxy vote (or other shareholder action) is materially important to the client’s account, the sub-adviser should request that the agent recall the security prior to the record date to allow the sub-adviser to vote the securities.

Disclosure of Proxy Voting Policies and Procedures in the Trust’s Statement of Additional Information (“SAI”)

The Trust shall include in its SAI a summary of the Trust Proxy Policy and of the Sub-adviser Proxy Policy included therein. (In lieu of including a summary of these policies and procedures, the Trust may include each full Trust Proxy Policy and Sub-adviser Proxy Policy in the SAI.)

Disclosure of Proxy Voting Policies and Procedures in Annual and Semi-Annual Shareholder Reports

The Trusts shall disclose in annual and semi-annual shareholder reports that a description of the Trust Proxy Policy, including the Sub- adviser Proxy Policy, and the Trusts’ proxy voting record for the most recent 12 months ended June 30 are available on the Securities and Exchange Commission’s (“SEC”) website, and without charge, upon request, by calling a specified toll-free telephone number. The Trusts will send these documents within three business days of receipt of a request, by first-class mail or other means designed to ensure equally prompt delivery. The Fund Administration Department is responsible for preparing appropriate disclosure regarding proxy voting for inclusion in shareholder reports and distributing reports. The Legal Department supporting the Trusts is responsible for reviewing such disclosure once it is prepared by the Fund Administration Department.

Filing of Proxy Voting Record on Form N-PX

The Trusts will annually file their complete proxy voting record with the SEC on Form N-PX. The Form N-PX shall be filed for the twelve months ended June 30 no later than August 31 of that year. The Fund Administration department, supported by the Legal Department supporting the Trusts, is responsible for the annual filing.

Regulatory Requirement

Rule 206(4)-6 of the Advisers Act and Rule 30b1-4 of the 1940 Act

Reporting

Disclosures in SAI: The Trusts shall disclose in annual and semi-annual shareholder reports that a description of the Trust Proxy Policy, including the Sub-adviser Proxy Policy, and the Trusts’ proxy voting record for the most recent 12 months ended June 30.

Form N-PX: The proxy voting service will file Form N-PX for each twelve-month period ending on June 30. The filing must be submitted to the SEC on or before August 31 of each year.

Procedure

Review of Sub-advisers’ Proxy Voting The Trusts have delegated proxy voting authority with respect to Fund portfolio securities in accordance with the Trust Policy, as set forth above.

Consistent with this delegation, each sub-adviser is responsible for the following:

1. Implementing written policies and procedures, in compliance with Rule 206(4)-6 under the Advisers Act, reasonably designed to ensure that the sub-adviser votes portfolio securities in the best interest of shareholders of the Trusts.

2. Providing the Advisers with a copy and description of the Sub-adviser Proxy Policy prior to being approved by the Board as a sub-adviser, accompanied by a certification that represents that the Sub-adviser Proxy Policy has been adopted in conformance with Rule 206(4)-6 under the Advisers Act. Thereafter, providing the Advisers with notice of any amendment or revision to that Sub-adviser Proxy Policy or with a description thereof. The Advisers are required to report all material changes to a Sub-adviser Proxy Policy quarterly to the Board. The CCO’s annual written compliance report to the Board will contain a summary of the material changes to each Sub-adviser Proxy Policy during the period covered by the report.

3. Providing the Adviser with a quarterly certification indicating that the sub-adviser did vote proxies of the funds and that the proxy votes were executed in a manner consistent with the Sub-adviser Proxy Policy. If the sub-adviser voted any proxies in a manner inconsistent with the Sub-adviser Proxy Policy, the sub-adviser will provide the Adviser with a report detailing the exceptions.

Adviser Responsibilities The Trusts have retained a proxy voting service to coordinate, collect, and maintain all proxy-related information, and to prepare and file the Trust’s reports on Form N-PX with the SEC.

The Advisers, in accordance with their general oversight responsibilities, will periodically review the voting records maintained by the proxy voting service in accordance with the following procedures:

1. Receive a file with the proxy voting information directly from each sub-adviser on a quarterly basis.

2. Select a sample of proxy votes from the files submitted by the sub-advisers and compare them against the proxy voting service files for accuracy of the votes.

3. Deliver instructions to shareholders on how to access proxy voting information via the Trust’s semi-annual and annual shareholder reports.

The Fund Administration Department, in conjunction with the Legal Department supporting the Trusts, is responsible for the foregoing procedures.

Proxy Voting Service Responsibilities Proxy voting services retained by the Trusts are required to undertake the following procedures:

| • | Aggregation of Votes: |

The proxy voting service’s proxy disclosure system will collect fund-specific and/or account-level voting records, including votes cast by multiple sub- advisers or third-party voting services.

| • | Reporting: |

The proxy voting service’s proxy disclosure system will provide the following reporting features:

1. multiple report export options;

2. report customization by fund-account, portfolio manager, security, etc.; and

3. account details available for vote auditing.

| • | Form N-PX Preparation and Filing: |

The Advisers will be responsible for oversight and completion of the filing of the Trusts’ reports on Form N-PX with the SEC. The proxy voting service will prepare the EDGAR version of Form N-PX and will submit it to the adviser for review and approval prior to filing with the SEC. The proxy voting service will file Form N-PX for each twelve-month period ending on June 30. The filing must be submitted to the SEC on or before August 31 of each year. The Fund Administration Department, in conjunction with the Legal Department supporting the Trusts, is responsible for the foregoing procedures.

The Fund Administration Department in conjunction with the CCO oversees compliance with this policy.

The Fund Administration Department maintains operating procedures affecting the administration and disclosure of the Trusts’ proxy voting records.

The Trusts’ Chief Legal Counsel is responsible for including in the Trusts’ SAI information regarding the Advisers’ and each sub-advisers proxy voting policies as required by applicable rules and form requirements.

Key Contacts

Investment Compliance

Escalation/Reporting Violations

All John Hancock employees are required to report any known or suspected violation of this policy to the CCO of the Funds.

Related Policies and Procedures

7B Registration Statements and Prospectuses

Document Retention Requirements

The Fund Administration Department and The CCO’s Office is responsible for maintaining all documentation created in connection with this policy. Documents will be maintained for the period set forth in the Records Retention Schedule. See Compliance Policy: Books and Records.

Proxy Voting and Class Action Monitoring

Policy

Epoch maintains proxy voting authority for Client accounts, unless otherwise instructed by the client. Epoch votes proxies in a manner that it believes is most likely to enhance the economic value of the underlying securities held in Client accounts. Epoch maintains a Proxy Voting Group comprised of investment team, operations and compliance representatives that meet at least on a quarterly basis. Epoch will not respond to proxy solicitor requests unless Epoch determines that it is in the best interest of Clients to do so.

In light of Epoch’s fiduciary duty to its Clients, and given the complexity of the issues that may be raised in connection with proxy votes, the Firm has retained Institutional Shareholder Services (“ISS”). ISS is an independent adviser that specializes in providing a variety of fiduciary-level proxy-related services to institutional investment managers. The services provided to the Firm include in-depth research, voting recommendations, vote execution and recordkeeping. Epoch requires ISS to notify the Company if ISS experiences a material conflict of interest in the voting of Clients’ proxies.

ISS will pre-populate the Firm’s votes on the ISS’s electronic voting platform with ISS’s recommendations based on the Firm’s voting instructions to ISS. To the extent Epoch becomes aware that an issuer that is the subject of ISS’s voting recommendation intends to file or has filed additional solicitating materials (“Additional Information”) after the Firm has received the ISS’s voting recommendation, but before the proxy submission deadline, and the Additional Information would reasonably be expected to affect the Adviser’s voting determination, Epoch will consider the Additional Information prior to exercising voting authority to confirm that the Firm is voting in its client’s best interest.

Notwithstanding the foregoing, the Firm will use its best judgment to vote proxies in the manner it deems to be in the best interests of its Clients. In the event that judgment differs from that of ISS, or that investment teams within Epoch wish to vote differently with respect to the same proxy in light of their specific strategy, the Firm will memorialize the reasons supporting that judgment and retain a copy of those records for the Firm’s files. The Compliance Department will periodically review the voting of proxies to ensure that votes which have diverged from the judgment of ISS, were voted consistent with the Firm’s fiduciary duties.

On at least an annual basis, the CCO or a designee will review this Proxy Voting and Class Action Monitoring policy.

Procedures for Lent Securities and Issuers in Share-blocking Countries

At times, neither Epoch nor ISS will be allowed to vote proxies on behalf of Clients when those Clients have adopted a securities lending program. The Firm recognizes that Clients who have adopted securities lending programs have made a general determination that the lending program provides a greater economic benefit than retaining the ability to vote proxies. Notwithstanding this fact, in the event that the Firm becomes aware of a proxy voting matter that would enhance the economic value of the client’s position and that position is lent out, the Firm will make reasonable efforts to inform the Client that neither the Firm nor ISS is able to vote the proxy until the Client recalls the lent security.

In certain markets where share blocking occurs, shares must be “frozen” for trading purposes at the custodian or sub-custodian in order to vote. During the time that shares are blocked, any pending trades will not settle. Depending on the market, this period can last from one day to three weeks. Any sales that must be executed will settle late and potentially be subject to interest charges or other punitive fees. For this reason, in blocking markets, the Firm retains the right to vote or not, based on the determination of the Firm’s Investment Personnel. If the decision is made to vote, the Firm will process votes through ISS unless other action is required as detailed in this policy.

Effective Date - October 1, 2022

Procedures for Conflicts of Interest

Epoch has identified the following potential conflicts of interest:

| • | Whether there are any business or personal relationships between Epoch, or an employee of Epoch, and the officers, directors or shareholder proposal proponents of a company whose securities are held in Client accounts that may create an incentive to vote in a manner that is not consistent with the best interests of Epoch’s Clients; |

| • | Whether Epoch has any other economic incentive to vote in a manner that is not consistent with the best interests of its Clients; or |

| • | Whether a proxy relates to a company that is a Client of Epoch.1 |

If a conflict of interest has been identified (as outlined above), then Epoch shall bring the proxy voting issue first to the attention of the Proxy Voting Group. The Proxy Voting Group may engage affected Clients and/or Epoch employees to ensure the relevant proxies are voted in a manner that is consistent with Epoch’s fiduciary duties.

Procedures for Proxy Solicitation

In the event that any officer or employee of Epoch receives a request to reveal or disclose Epoch’s voting intention on a specific proxy event, then the officer or employee must forward the solicitation to the CCO.

Procedures for Voting Disclosure

Upon request, Epoch will provide Clients with their specific proxy voting history.

Initial and Ongoing Diligence of Proxy Service Provider

The Operations Department will conduct additional diligence on ISS to ensure the provider continues to have the capacity and competency to adequately analyze proxy issues on an annual basis. As part of the due diligence process, the Head of Operations, or a designee, obtains a completed questionnaire from ISS that assists Epoch in evaluating ISS’s services and any potential conflicts of interest that may exist.

Recordkeeping

Epoch must maintain the documentation described in the following section for a period of not less than five (5) years, the first two (2) years at its principal place of business. The Firm will be responsible for the following procedures and for ensuring that the required documentation is retained.

Client Request to Review Proxy Votes

If a Client requests to review the proxy votes, the Relationship Management team will:

| • | Record the identity of the Client, the date of the request, and the disposition (e.g., provided a written or oral response to Client’s request, referred to third party, not a proxy voting Client, other dispositions, etc.) in a suitable place. |

| • | Furnish the information requested, free of charge, to the Client within a reasonable time period (within 10 business days). Maintain a copy of the written record provided in response to client’s written (including e-mail) or oral request. |

| 1 | Compliance (with assistance from Operations and Client Services) will seek to identify instances where a proxy vote relates to a company that is a Client of Epoch’s and escalate to the Proxy Voting Group as necessary. |

Effective Date - October 1, 2022

Proxy Voting Records

The proxy voting record is periodically provided to Epoch by ISS. Included in these records are:

| • | Documents prepared or created by Epoch that were material to making a decision on how to vote, or that memorialized the basis for the decision. |

| • | Documentation or notes or any communications received from third parties, other industry analysts, third party service providers, company’s management discussions, etc. that were material in the basis for the decision. |

Disclosure

Epoch includes a description of its policies and procedures regarding proxy voting and class actions in Part 2 of Form ADV, along with a statement that Clients and Investors contact Epoch at 212 303-7200 to obtain a copy of these policies and procedures and information about how Epoch voted with respect to the Client’s securities. Any request for information about proxy voting or class actions should be promptly forwarded to Epoch at the number above and we will respond to any such requests.

The CCO will ensure that Part 2A of Form ADV is updated as necessary to reflect: (i) all material changes to this policy; and (ii) regulatory requirements related to proxy voting disclosure.

As a matter of policy, Epoch does not disclose how it expects to vote on upcoming proxies. Additionally, Epoch does not disclose the way it voted proxies to unaffiliated third parties without a legitimate need to know such information.

Class Action Litigation Settlement

Generally, Epoch does not have responsibility to file proofs of claim or engage in class action litigation.

Epoch does not complete proofs-of-claim on behalf of Clients for current or historical holdings; however, Epoch will assist Clients with collecting information relevant to filing proofs-of-claim when such information is in the possession of Epoch.

Effective Date - October 1, 2022

| Manulife Investment Management global proxy voting policy and procedures |  |

INTERNAL

Global Proxy Voting Policy and Procedures

Applicable Business Unit: Manulife Investment Management Public Markets

Applicable Legal Entity(ies): Refer to Appendix A

Committee Approval: Manulife IM Public Markets Operating Committee

Business Owner: Manulife IM Public Markets

Policy Sponsor: Chief Compliance Officer, Manulife IM Public Markets

Policy Last Updated/Reviewed: April 2021

Policy Next Review Date: April 2024

Policy Original Issue Date: February 2011

Review Cycle: Three (3) years

Company policy documents are for internal use only and may not be shared outside the Company, in whole or part, without prior approval from the Global Chief Compliance Officer (or local Chief Compliance Officer if policy is only entity-applicable) who will consult, as appropriate with, the Policy Sponsor and legal counsel when deciding whether to approve and the conditions attached to any approval.

INTERNAL

Manulife Investment Management global proxy voting policy and procedures

Executive summary

Each investment team at Manulife Investment Management (Manulife IM)1 is responsible for investing in line with its investment philosophy and clients’ objectives. Manulife IM’s approach to proxy voting aligns with its organizational structure and encourages best practices in governance and management of environmental and social risks and opportunities. Manulife IM has adopted and implemented proxy voting policies and procedures to ensure that proxies are voted in the best interests of its clients for whom it has proxy voting authority.

This global proxy voting policy and procedures (policy) applies to each of the Manulife IM advisory affiliates listed in Appendix A. In seeking to adhere to local regulatory requirements of the jurisdiction in which an advisory affiliate operates, additional procedures specific to that affiliate may be implemented to ensure compliance, where applicable. The policy is not intended to cover every possible situation that may arise in the course of business, but rather to act as a decision-making guide. It is therefore subject to change and interpretation from time to time as facts and circumstances dictate.

Statement of policy

| • | The right to vote is a basic component of share ownership and is an important control mechanism to ensure that a company is managed in the best interests of its shareholders. Where clients delegate proxy voting authority to Manulife IM, Manulife IM has a fiduciary duty to exercise voting rights responsibly. |

| • | Where Manulife IM is granted and accepts responsibility for voting proxies for client accounts, it will seek to ensure proxies are received and voted in the best interests of the client with a view to maximize the economic value of their equity securities unless it determines that it is in the best interests of the client to refrain from voting a given proxy. |

| • | If there is any potential material proxy-related conflict of interest between Manulife IM and its clients, identification and resolution processes are in place to provide for determination in the best interests of the client. |

| • | Manulife IM will disclose information about its proxy voting policies and procedures to its clients. |

| • | Manulife IM will maintain certain records relating to proxy voting. |

| 1 | Manulife Investment Management is the unified global brand for Manulife’s global wealth and asset management business, which serves individual investors and institutional clients in three businesses: retirement, retail, and institutional asset management (Public markets and private markets). |

| INTERNAL | April 2021 2 |

Manulife Investment Management global proxy voting policy and procedures

Philosophy on sustainable investing

Manulife IM’s commitment to sustainable investment 2 is focused on protecting and enhancing the value of our clients’ investments and, as active owners in the companies in which we invest, we believe that voting at shareholder meetings can contribute to the long-term sustainability of our investee companies. Manulife IM will seek to exercise the rights and responsibilities associated with equity ownership, on behalf of its clients, with a focus on maximizing long-term shareholder returns, as well as enhancing and improving the operating strength of the companies to create sustainable value for shareholders.

Manulife IM invests in a wide range of securities across the globe, ranging from large multinationals to smaller early-stage companies, and from well-developed markets to emerging and frontier markets. Expectations of those companies vary by market to reflect local standards, regulations, and laws. Manulife IM believes, however, that successful companies across regions are generally better positioned over the long term if they have:

| • | Robust oversight, including a strong and effective board with independent and objective leaders working on behalf of shareholders; |

| • | Mechanisms to mitigate risk such as effective internal controls, board expertise covering a firm’s unique risk profile, and routine use of key performance indicators to measure and assess long-term risks; |

| • | A management team aligned with shareholders through remuneration structures that incentivize long- term performance through the judicious and sustainable stewardship of company resources; |

| • | Transparent and thorough reporting of the components of the business that are most significant to shareholders and stakeholders with focus on the firm’s long-term success; and |

| • | Management focused on all forms of capital, including environmental, social, and human capital. |

The Manulife Investment Management voting principles (voting principles) outlined in Appendix B provide guidance for our voting decisions. An active decision to invest in a firm reflects a positive conviction in the investee company and we generally expect to be supportive of management for that reason. Manulife IM may seek to challenge management’s recommendations, however, if they contravene these voting principles or Manulife IM otherwise determines that doing so is in the best interest of its clients.

| 2 | Further information on Sustainable Investing at Manulife IM can be found at manulifeim.com/institutional. |

| INTERNAL | April 2021 3 |

Manulife Investment Management global proxy voting policy and procedures

Manulife IM also regularly engages with boards and management on environmental, social, or corporate governance issues consistent with the principles stipulated in our sustainable investing statement and our ESG engagement policy. Manulife IM may, through these engagements, request certain changes of the portfolio company to mitigate risks or maximize opportunities. In the context of preparing for a shareholder meeting, Manulife IM will review progress on requested changes for those companies engaged. In an instance where Manulife IM determines that the issuer has not made sufficient improvements on an issue, then we may take voting action to demonstrate our concerns.

In rare circumstances, Manulife IM may consider filing, or co-filing, a shareholder resolution at an investee company. This may occur where our team has engaged with management regarding a material sustainability risk or opportunity, and where we determine that the company has not made satisfactory progress on the matter within a reasonable time period. Any such decision will be in the sole discretion of Manulife IM and acted on where we believe filing, or co-filing, a proposal is in the best interests of our clients.

Manulife IM may also divest of holdings in a company where portfolio managers are dissatisfied with company financial performance, strategic direction, and/or management of material sustainability risks or opportunities.

Procedures

Receipt of ballots and proxy materials

Proxies received are reconciled against the client’s holdings, and the custodian bank will be notified if proxies have not been forwarded to the proxy service provider when due.

Voting proxies

Manulife IM has adopted the voting principles contained in Appendix B of this policy.

Manulife IM has deployed the services of a proxy voting services provider to ensure the timely casting of votes, and to provide relevant and timely proxy voting research to inform our voting decisions. Through this process, the proxy voting services provider populates initial recommended voting decisions that are aligned with the Manulife IM voting principles outlined in Appendix B. These voting recommendations are then submitted, processed, and ultimately tabulated. Manulife IM retains the authority and operational functionality to submit different voting instructions after these initial recommendations from the proxy voting services provider have been submitted, based on Manulife IM’s assessment of each situation. As Manulife IM reviews voting recommendations and decisions, as articulated below, Manulife IM will often change voting instructions based on those reviews. Manulife IM periodically reviews the detailed policies created by the proxy voting service provider to ensure consistency with our voting principles, to the extent this is possible.

| INTERNAL | April 2021 4 |

Manulife Investment Management global proxy voting policy and procedures

Manulife IM also has procedures in place to review additional materials submitted by issuers often in response to voting recommendations made by proxy voting service providers. Manulife IM will review additional materials related to proxy voting decisions in those situations where Manulife IM becomes aware of those additional materials, is considering voting contrary to management, and where Manulife IM owns 2% or more of the subject issuer as aggregated across the funds.

| INTERNAL | April 2021 5 |

Manulife Investment Management global proxy voting policy and procedures

Portfolio managers actively review voting options and make voting decisions for their holdings. Where Manulife IM holds a significant ownership position in an issuer, the rationale for a portfolio manager’s voting decision is specifically recorded, including whether the vote cast aligns with the recommendations of the proxy voting services provider or has been voted differently. A significant ownership position in an investment is defined as those cases where Manulife IM holds at least 2% of a company’s issued share capital in aggregate across all Manulife IM client accounts.

The Manulife IM ESG research and integration team (ESG team) is an important resource for portfolio management teams on proxy matters. This team provides advice on specific proxy votes for individual issuers if needed. ESG team advice is supplemental to the research and recommendations provided by our proxy voting services provider. In particular, ESG analysts actively review voting resolutions for companies in which:

| • | Manulife IM’s aggregated holdings across all client accounts represent 2% or greater of issued capital; |

| • | A meeting agenda includes shareholder resolutions related to environmental and social risk management issues, or where the subject of a shareholder resolution is deemed to be material to our investment decision; or |

Manulife IM may also review voting resolutions for issuers where an investment team engaged with the firm within the previous two years to seek a change in behavior.

After review, the ESG team may provide research and advice to investment staff in line with the voting principles.

Manulife IM also has an internal proxy voting working group (working group) comprising senior managers from across Manulife IM including the equity investment team, legal, compliance, and the ESG team. The working Group operates under the auspices of the Manulife IM Public Markets Sustainable Investing Committee. The Working group regularly meets to review and discuss voting decisions on shareholder proposals or instances where a portfolio manager recommends a vote different than the recommendation of the proxy voting services provider.

Manulife IM clients retain the authority and may choose to lend shareholdings. Manulife IM, however, generally retains the ability to restrict shares from being lent and to recall shares on loan in order to preserve proxy voting rights. Manulife IM is focused in particular on preserving voting rights for issuers where funds hold 2% or more of an issuer as aggregated across funds. Manulife IM has a process in place to systematically restrict and recall shares on a best efforts basis for those issuers where we own an aggregate of 2% or more.

| INTERNAL | April 2021 6 |

Manulife Investment Management global proxy voting policy and procedures

Manulife IM may refrain from voting a proxy where we have agreed with a client in advance to limit the situations in which we will execute votes. Manulife IM may also refrain from voting due to logistical considerations that may have a detrimental effect on our ability to vote. These issues may include, but are not limited to:

| • | Costs associated with voting the proxy exceed the expected benefits to clients; |

| INTERNAL | April 2021 7 |

Manulife Investment Management global proxy voting policy and procedures

| • | Underlying securities have been lent out pursuant to a client’s securities lending program and have not been subject to recall; |

| • | Short notice of a shareholder meeting; |

| • | Requirements to vote proxies in person; |

| • | Restrictions on a nonnational’s ability to exercise votes, determined by local market regulation; |

| • | Restrictions on the sale of securities in proximity to the shareholder meeting (i.e., share blocking); |

| • | Requirements to disclose commercially sensitive information that may be made public (i.e., reregistration); |

| • | Requirements to provide local agents with power of attorney to facilitate the voting instructions (such proxies are voted on a best-efforts basis); or |

| • | The inability of a client’s custodian to forward and process proxies electronically. |

If a Manulife IM portfolio manager believes it is in the best interest of a client to vote proxies in a manner inconsistent with the policy, the portfolio manager will submit new voting instructions to a member of the ESG team with rationale for the new instructions. The ESG team will then support the portfolio manager in developing voting decision rationale that aligns with this policy and the voting principles. The ESG team will then submit the vote change to the working group. The working group will review the change and ensure that the rationale is sound, and the decision will promote the long-term success of the issuer.