1 OSI at a Glance OSI Services (98% of LTM Revenue) OSI Portfolio Management (2% of LTM Revenue) ARM Provider of early stage contract management services and late stage collection services of accounts receivables to the telecommunications, utilities, education, healthcare and financial services industries 70% First-Party (Non-Contingency Fee) 30% Third-Party (Contingency Fee) $415MM LTM 9/30/07 Revenue $27MM LTM 9/30/07 Adjusted EBITDA Strong track record in purchasing delinquent accounts receivable portfolios including credit card, telecom, health club and consumer loan receivables $9MM LTM 9/30/07 Revenue $0MM LTM 9/30/07 Adjusted ...EBTIDA Exhibit 99.1 |

2 Managing NCPM Through a Challenging Economic Climate New Purchase Opportunities Maintain existing IRR goals and reduce price to off-set down-turn in collections Committed Purchase Opportunities Board portfolios with reduced IRR since price is committed Maintains profitability while lowering risk of future impairment Existing Portfolios Analyze portfolios for impairments in order to maintain original IRR as required by GAAP Current expectation is Q4 2007 impairment between $20.0MM– $25.0MM (8%- 10% of carrying value) Reduce future collection expectations (modify “look back” period) Re-segment portfolios based on current consumer behavior trends Review and modify collection and recovery strategies (sub-contractors, letters, and sales) |

3 Company Overview OSI is a leading provider of Business Process Outsourcing (BPO) services for the strategic management of consumer receivables across the entire cash-to-credit cycle 2 First-party Collection / Billing Services (69% of LTM revenue) 2 Third-party Collection Services (29% of LTM revenue) 2 Portfolio Management (2% of LTM revenue) History 2 Formed in 1995 by McCown DeLeeuw & Co. 2 Built business through acquisitions 2 Sold to Madison Dearborn Partners by McCown DeLeeuw in 1999 for $800MM $575MM of new and assumed debt $225MM of equity 2 Business continued to grow through acquisitions and leverage 2 Filed for bankruptcy in May 2005 and emerged seven months later 2 Returned to profitability nine months after emerging from bankruptcy Purchase multiple of 5.6x based on 2008 estimated annualized EBITDA |

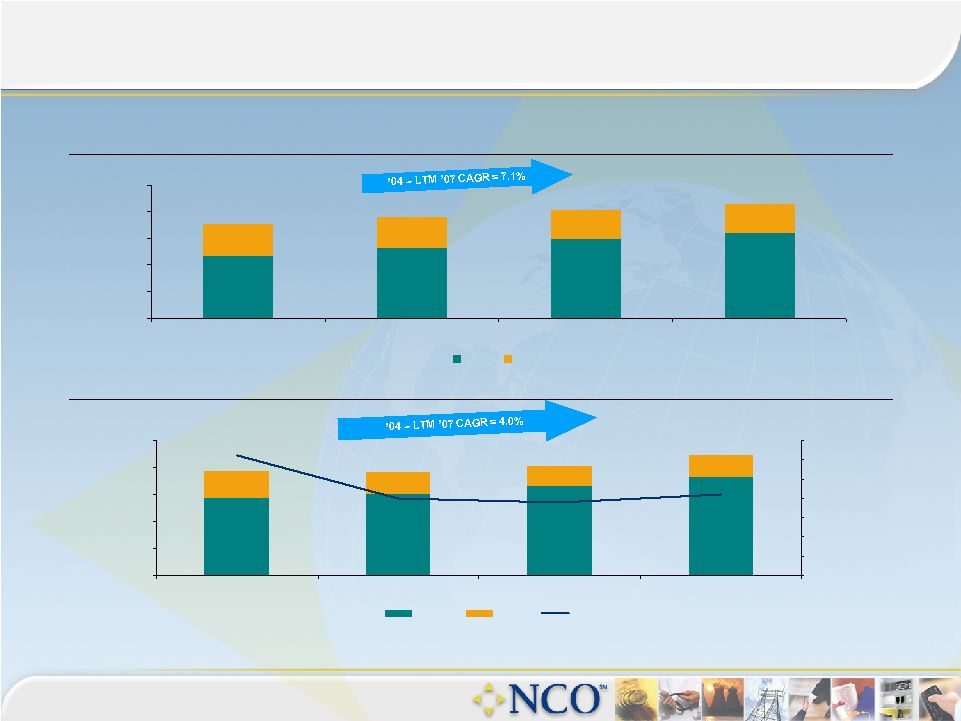

4 NCO / OSI – Financial Summary Revenues ($MM) 940 1,052 1,190 1,286 477 473 442 424 $0 $400 $800 $1,200 $1,600 $2,000 2004 2005 2006 LTM 9/30/07 NCO OSI Adj. EBITDA (1) ($MM) 143 149 164 182 49 42 38 41 14% 13% 12% 13% $0.0 $50.0 $100.0 $150.0 $200.0 $250.0 2004 2005 2006 LTM 9/30/07 10.50% 11.00% 11.50% 12.00% 12.50% 13.00% 13.50% 14.00% NCO OSI Margin (1) Pro forma LTM 9/30/07 Adjusted EBITDA includes SST acquisition for NCO and OSI synergies of $13.9MM for OSI. $193 $191 $222 $203 $1,417 $1,525 $1,710 $1,632 (1) (1) |