Exhibit 99.1

Presented to

Accredited Members

Conference

Conference

April 21, 2010

Certain statements contained in this presentation, which are not based on historical facts, are forward-

looking statements as the term is defined in the Private Securities Litigation Reform Act of 1995 and, as

such, are subject to substantial uncertainties and risks that may cause actual results to materially differ

from projections. Although the Company believes that the expectations expressed herein are based on

reasonable assumptions within the bounds of the Company’s knowledge of its businesses, operations,

business plans, budgets and internal financial projections, there can be no assurance that actual results

will not differ materially from the expectations expressed herein. Important factors currently known to

management that could cause actual results to differ materially from those in forward-looking statements

include the Company's ability to (i) properly execute its business model, (ii) raise additional capital to

sustain its business model, (iii) attract and retain personnel, including highly qualified executives,

management and operational personnel, (iv) negotiate favorable current debt and future capital raises,

(v) manage the inherent risks associated with operating a diversified business to achieve and maintain

positive cash flow and net profitability, and (vi) get back into compliance, and remain in compliance, with

its current senior secured credit facility with PNC Bank, N.A. as well as the other risks detailed from time

to time in the SEC reports of Best Energy Services, Inc., including its annual report on Form 10-K/A for the

transition period from February 1, 2008 to December 31, 2008 and its quarterly reports on Form 10-Q for

the three months ended March 31, 2009, June 30, 2009 and September 30, 2009. In light of these risks

and uncertainties, there can be no assurance that the forward-looking information contained in this

presentation will, in fact, occur. The forward-looking statements made herein speak only as of the date

hereof and Best Energy disclaims any obligation to update these forward-looking statements.

looking statements as the term is defined in the Private Securities Litigation Reform Act of 1995 and, as

such, are subject to substantial uncertainties and risks that may cause actual results to materially differ

from projections. Although the Company believes that the expectations expressed herein are based on

reasonable assumptions within the bounds of the Company’s knowledge of its businesses, operations,

business plans, budgets and internal financial projections, there can be no assurance that actual results

will not differ materially from the expectations expressed herein. Important factors currently known to

management that could cause actual results to differ materially from those in forward-looking statements

include the Company's ability to (i) properly execute its business model, (ii) raise additional capital to

sustain its business model, (iii) attract and retain personnel, including highly qualified executives,

management and operational personnel, (iv) negotiate favorable current debt and future capital raises,

(v) manage the inherent risks associated with operating a diversified business to achieve and maintain

positive cash flow and net profitability, and (vi) get back into compliance, and remain in compliance, with

its current senior secured credit facility with PNC Bank, N.A. as well as the other risks detailed from time

to time in the SEC reports of Best Energy Services, Inc., including its annual report on Form 10-K/A for the

transition period from February 1, 2008 to December 31, 2008 and its quarterly reports on Form 10-Q for

the three months ended March 31, 2009, June 30, 2009 and September 30, 2009. In light of these risks

and uncertainties, there can be no assurance that the forward-looking information contained in this

presentation will, in fact, occur. The forward-looking statements made herein speak only as of the date

hereof and Best Energy disclaims any obligation to update these forward-looking statements.

OUR VISION:

We are building our business in two complementary directions:

§ By continuing to provide a single point source for all our customer’s

needs:

needs:

üSuperior Safety Record

üValue Pricing in All Markets

üA long history of Performance

üAnd Soon - Capital.

§ By expanding our area:

üUsing our Customer-Centric approach

üMoving into other basins where legacy companies and

their practices invite our competitive presence.

their practices invite our competitive presence.

OUR VISION:

OUR HISTORY:

§ Q1 2008 -- Formed with Three Acquisitions

üBest Well Services (established in 1991)

üBob Beeman Drilling

üCertain Housing Accommodation assets

§Q4 2008 -- Board Mandated Management Changes

üAnticipated significant commodity price and

activity decline

activity decline

üDiscontinued rig redeployment model

üCut annual G&A from $ 5.4MM to $960K

üImplemented new profit models, to gauge business

unit viability

unit viability

§Q4 2009 -- Discontinued Drilling and Housing business units

§Q1 2010 -- Established Customer-Centric Growth Model

Our Leadership: Accomplished & Respected

Mark Harrington, Chairman and CEO

•Founding board member; Appointed CEO December 2008

•30 years experience - Oil & Gas Exploration, Development and

Finance

Finance

•Prior Chairman/President - Seven, Energy and Private Equity

Companies

Companies

•Featured on CNBC, Canada AM, Dow Jones News & Bloomberg

Eugene Allen, President and COO

• A second generation oilman with 4o years hand-on experience in

the oil and gas industry.

the oil and gas industry.

• 16 Years at Best Well Services.

•Prior Experience: Pool Well Service, Pride Petroleum and KMA

Well Service

Well Service

•Executing the operations of BWS and orderly liquidation of non-

strategic assets from discontinued business units.

strategic assets from discontinued business units.

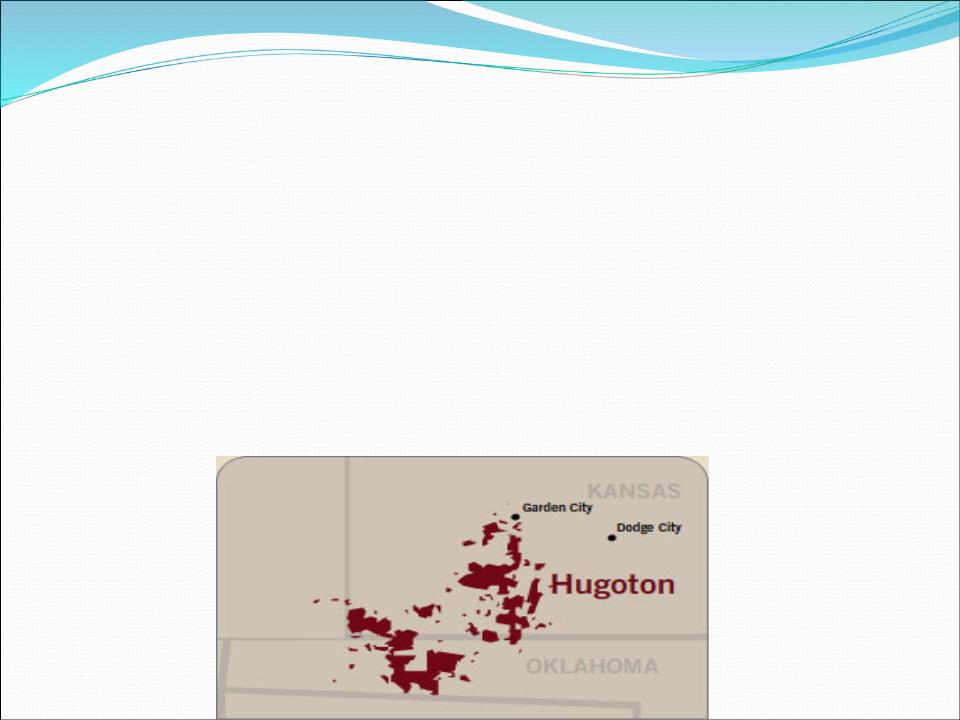

Our Platform

Current Operations: Hugoton Basin

Rife with Opportunity

Ø 24 Trillion Cubic Feet Produced since 1930

Ø 12 Trillion Cubic Feet Remaining to be Produced

Ø 12,000+ Active Wells in the Basin

Ø 50+ Active Operators

Our Strengths Define Who We Are

Ø Longevity - BWS established in 1991

Ø Sustainability - Grew steadily from 1 rig to 25 rigs

Ø Reputation - A coveted book of business

Ø Customer Centric - A history of value pricing and service to

our customers

our customers

Ø Management - Significant depth of management and

continuity of key employees

continuity of key employees

Why Our Customers Choose Best

Ø“Safety First”

• An Exceptional Safety Record - well over a year, with no lost time due to a

safety incident

safety incident

• Rank at the highest level among our customer’s providers

Ø Value Pricing- always Fair and Competitive

•Market Peak: BWS $240/hour Competitors $360/hour

•Today’s Pricing: BWS $210/hour Competitors $240/hour

Ø Reputation and Performance

• Continuity in our Crews- Historical turnover <5%, industry norm >40%

• Superior Depth of Knowledge and Experience- Faster execution times

for our customers

for our customers

Ø Soon to Come: A delivery mechanism for our customers’ greatest need- Capital.

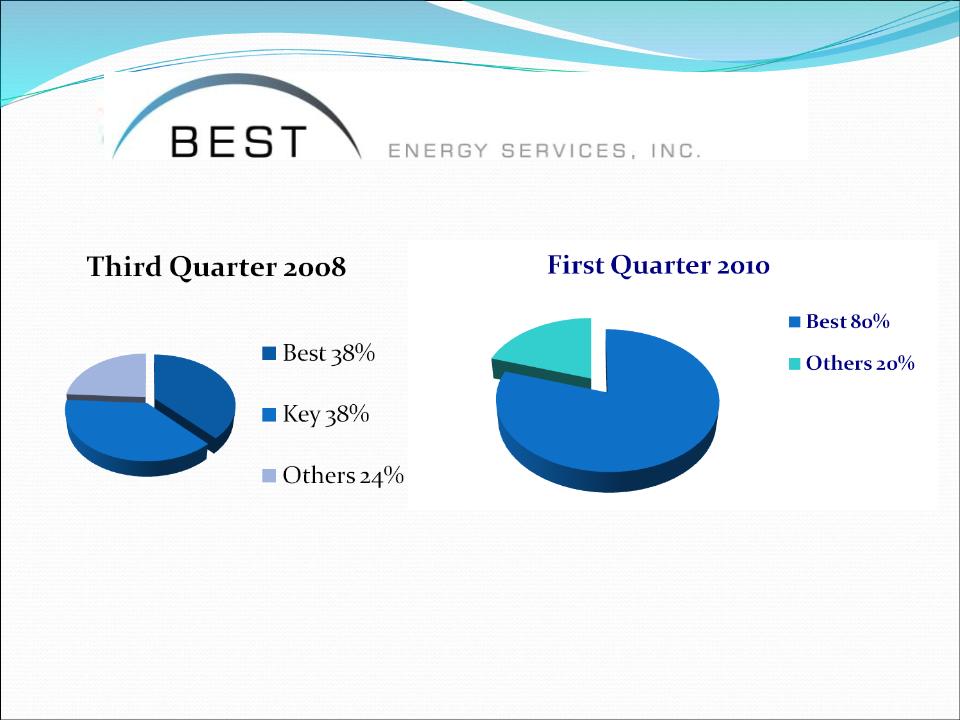

The Results : Success in Growth Market Share

Our Customers Include:

Anadarko | Dominion | Linn Energy | Oxy USA |

Arena | Ellora Energy | Marlin Oil | Pioneer |

Bengalia L&C | Enervest | Merit Energy | Pride Energy |

Cleary | EOG | Midwestern | Samson |

Devon | Kaiser-Francis | Noble | XTO |

Building on Our Platform

•Hugoton Basin Financing Partners

•Basin-Specific Scaling

Hugoton Basin Financing Partners:

A Compelling Financing Option for Our Customers

Ø Shut-in wells Financially Damage the Customer

•No cash flow to support area G&A

•Reduces Borrowing Base through Absent Cash Flow and Degradation of

Reserve Category

Reserve Category

Ø HBFP allows Customers to Focus Capital Allocations on Highest Impact

Areas:

Areas:

•Gulf of Mexico

•Shale plays

•International

Ø Earn-In structure is Bank Friendly for the Customer

•No bank capital required

•No sub or senior debt taken-on

•No inter-creditor agreements

•Not a sale of a liened property

•Enhances Credit Quality by increasing Operators cash flow

Ø Customer Retains Operations and Cash Flows to Support Regional G&A

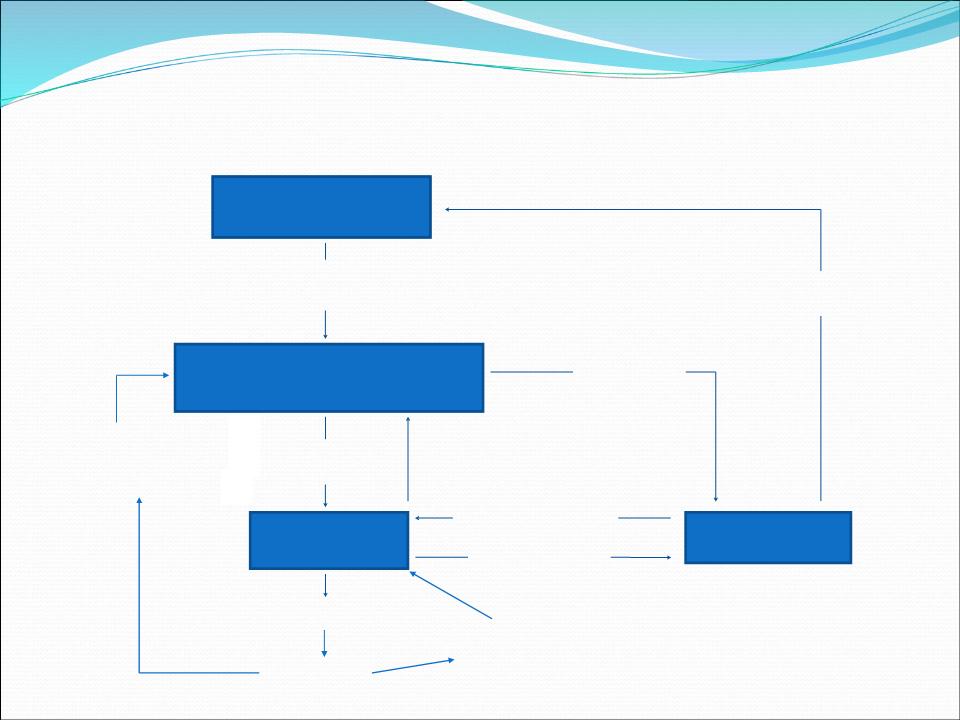

Institutional

Investor

$5 Million

Commitment

Commitment

Hugoton Basin

Financing Partners

Best���s

Customers

Customers

Rejuvenated Wells

Preferred Cash

Recoupment +

Premium

$ For

Rejuvenation

BEST

Work Contract

Payment for

Services

Share in

Fund’s

Fund’s

Production

Warrants

Negotiated

Back- in APO

Back- in APO

Cash Flow

100% Cash Flow

After HBFP Payback

After HBFP Payback

HBFP: A First Of Its Kind Financing Product

Created by a Former Customer - - Best’s CEO

HBFP Has Connected the Dots

Ø Operators Gain Access to Much Needed Capital

•Unavailable from Corporate Allocation

•Unavailable from Lenders/Capital Markets

Ø Institutional Investor Gains High Quality and Closable

Deal Flow

Deal Flow

•Earn-in Structure Obviates Disconnect in Buyer/

Seller Expectations

Seller Expectations

•Best’s leading position in the Hugoton makes us the

Preeminent Intelligence Network for Accessing

Candidates

Preeminent Intelligence Network for Accessing

Candidates

Basin-Specific Scaling: What We Look For

— Low per unit F & D costs

— Rising activity level

— Connective Customer Entrée

— Competitor pricing invites our Presence

Report Card on First Target:

South Texas Eagle Ford Shale

ü Low F & D Costs - Economics Maintained to $3/Mcf gas

IRR on Type Well - - Varied Natural Gas Pricing ($/Mcf) | |||

Shale Play | $3.00/Mcf | $4.00/Mcf | $5.00/Mcf |

Eagle Ford Shale | 25-35% | 45-60% | 65-90% |

Barnett Shale | 0% | 0-10% | 5-15% |

Fayetteville | 5% | 15% | 25% |

Haynesville | 9% | 28% | 51% |

Marcellus | 18% | 35% | 54% |

Source: various trade publications and company data | |||

Report Card on First Target:

South Texas Eagle Ford Shale

P Rising Activity Level - Permits up 40% over 2009

ü Connective Customer Entrée - Long-standing

Hugoton Basin Customers hold 500,000+acres in

the play

Hugoton Basin Customers hold 500,000+acres in

the play

P Competitor Pricing Invites our Entry - Their prices

are at a 30% premium to Best

are at a 30% premium to Best

Financial Considerations

•Scaling Revenue

•Deleveraging

•Financial Performance Drivers

•Rig Count Break Points

•Annualized Upside Scenarios

•Share Capitalization

•Investment Consideration

Scaling Revenue - - A Work in Progress

Ø STEP ONE: Capture Existing Market Share (Initiated Q1 2009)

•Accomplished

üNow at 80%+ vs. 38% in 2008

Ø STEP TWO: Capture New Projects (Secured Q4 2009)

•Accomplished

üAwarded coveted 6 rig contract from major oil company

üCredited to safety record and historical performance for customer

Ø STEP THREE: Game-changing revenue creation model (Q1 2010)

•Hugoton Basin Financing Partners

üMarket Potential-- $20MM+ annually

üMarries proprietary financial product to asset base

• Redeploy/Add/Scale into other Basins

üValue Pricing model= Pricing Power

ü Customer Connectivity

Deleveraging

ØTerm Debt level is too high at $16.8 million

ØThough terms are favorable

•LIBOR +4%

•Amortizes $1.5mm over next 12 months

ØNon-Dilutive Solutions:

• Sale of equipment from discontinued operations

• Target $4MM in next 120 days

• $1.2MM sold to date

• Periodic Sales of “Production Tails” from HBFP

• Ramp-up in free cash flows

Financial Drivers

Ø Operating and Overhead Expense Containment Completed

•G&A to remain <$1mm/year

•Very nominal increase to indirect costs

ØThree Revenue Drivers For 2010-2012

•Market Conditions in Hugoton

o Natural gas prices at wellhead

o Capital Allocations by customers

o Potential impact from HBFP product

•Scaling of HBFP

o Rig activity in Hugoton

o Rig activities in other basins

o Bundled services

•Expansions into other Basins

o Customers welcome value-pricing, reputation and

performance

performance

Rig Count Break Points:

•Positive EBITDA 10 Rigs

•1:1 coverage on debt service - 15 Rigs

•Annual EBITDA $3.2MM+ - 20 Rigs

•Annual EBITDA $5.0MM+ - 25Rigs

•Annual EBITDA $8.5MM+ - 35 Rigs

Note:

•12 Rigs running as of April 2010

•Figures exclude added revenues from HBFP

Annualized Upside Scenarios

20-Rig Case | 25-Rig Case | 35-Rig Case | |

Revenue | $ 11,900 | $ 15,600 | $ 23,000 |

Expenses (Direct and Indirect) | $ 7,740 | $ 9,640 | $ 13,570 |

Operating Income | $ 4,160 | $ 5,960 | $ 9,430 |

Corporate G&A | $ 960 | $ 960 | $ 960 |

EBITDA | $ 3,200 | $ 5,000 | $ 8,470 |

Interest (Cash & Non-Cash) | $ 1,076 | $ 1,076 | $ 1,076 |

Depreciation | $ 1,724 | $ 1,724 | $ 2,224 |

Net Income | $ 400 | $ 2,200 | $ 5,170 |

Share Capitalization: Treasury Method Dilution

As of 4/1/2010* | ||

Current shares issued | 35,544,409 | |

Undiluted shares after offering | 35,544,409 | |

Total dilution at $0.25 | 56,780,184 | |

Total dilution at $0.50 | 70,730,084 | |

Total dilution at $0.75 | 75,546,724 | |

Fully diluted | 89,505,877 | |

*post equity offering

Investment Considerations

ØSuccessful Turn-around Executed by New Management

• G&A reduced from $5.4MM in 2008 to less than $960,000

• Discontinued 3 of 4 unprofitable lines of business

• EBITDA positive beginning Q1 2010

ØSound Fundamentals in Hugoton Basin

• Largest conventional natural gas basin in U.S.

• 12,000+ active wells

• 12 TCF of gas left to be produced

ØExcellent Business Platform in Workover Services

• 50%+ gross margins

• Unblemished 19 year reputation

• Strong continuity of management

• Low employee turnover <5% vs industry norm of 45%

• First in class safety record

• History of value pricing to customers—up markets and down

Ø Doubled Market Share in Core Business In Down

Market

Market

• 80% share vs. 35% two years ago

• Demonstrated reputational and pricing prowess of BWS

• Coveted Book of Business Expanding

Ø A “Customer-Centric” Approach

• Safety first

• Value pricing

• Performance and reputation

• Soon to come—capital delivery to the customers

Ø Two Potentially Significant Growth Engines

• Hugoton Basin Financing Partners

o First of its kind financing

o Connects the Dots between Customer Capital Needs and

Financing

Financing

o Customer friendly and customer fair

• Basin- Specific Scaling

o Value pricing = pricing power

o Active growth in shale gas in target basin

Ø Significant Upside on Execution

— Positive EBITDA at 10 rig count

— Positive net income at 20 rig count

— Potential on successful HBFP execution

— Scalability of HBFP to other basins

— Potential deployment in Eagle Ford Basin

�� A Firmly Committed Management Team

— CEO signed on to 3 year contract

— Interests fully aligned with shareholders

— Significant option positions for ALL key employees

— 2/3 of options vest only on hitting $5MM EBITDA-- full 25 rig

deployment for 1 year

deployment for 1 year

Corporate Headquarters

5433 Westheimer Avenue, Suite 825

Houston, Texas 77056

Phone: 713-933-2600