Investor Presentation

May 20, 2008

This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of

1933 and Section 21E of the Securities Exchange Act of 1934, which reflect our current views with respect to,

among other things, our operations and financial performance. In some cases, you can identify these forward-

looking statements by the use of words such as “outlook”, “believes”, “expects”, “potential”, “continues”, “may”,

“will”, “should”, “seeks”, “approximately”, “predicts”, “intends”, “plans”, “estimates”, “anticipates” or the negative

version of these words or other comparable words. All statements other than statements of historical fact included

in this presentation are forward-looking statements and are based on various underlying assumptions and

expectations and are subject to known and unknown risks, uncertainties and assumptions, and may include

projections of our future financial performance based on our growth strategies and anticipated trends in our

business. Such forward-looking statements are subject to various risks and uncertainties. Accordingly, there are

or will be important factors that could cause actual outcomes or results to differ materially from those indicated in

these statements. We believe these factors include, but are not limited to, those described under “Risk Factors”

discussed in our Form 10-K filed with the SEC on March 26, 2008. These factors should not be construed as

exhaustive and should be read in conjunction with the other cautionary statements that are included in this

discussion. In addition, new risks and uncertainties emerge from time to time, and it is not possible for us to

predict all risks and uncertainties, nor can we assess the impact of all factors on our business or the extent to

which any factor, or combination of factors, may cause actual results to differ materially from those contained in

any forward-looking statements. Accordingly, you should not rely upon forward-looking statements as a prediction

of actual results and we do not assume any responsibility for the accuracy or completeness of any of these

forward-looking statements. We undertake no obligation to publicly update or review any forward-looking

statement, whether as a result of new information, future developments or otherwise.

Forward Looking Statements

2

Introduction to Duff & Phelps

Positioned to capitalize on key industry trends

Uniquely qualified to succeed

Broad and well-balanced service offerings for all markets

Benefiting from today’s volatile market environment

Strong financial performance

Significant growth opportunities

Investment Highlights

4

Positioned to Capitalize on Key Industry Trends

“Investors have been clamoring for more use

of fair value in financial statements, because

they think it provides a more accurate picture

of the company’s balance sheet than

historical cost figures.” – Reuters, September

2006

“Turnaround firms, faced with increasing

demand for their service…, are beefing up

staffs in anticipation of an increase in

corporate restructurings and bankruptcies

this year.” – Wall Street Journal, May 2007

“Companies often hire small, independent

boutiques to provide deal advice that

counterbalances input from bulge-bracket

firms . . . that may have many internal

competing agendas.” – Wall Street Journal,

September 2007

Corporate Restructuring

Fair Value Accounting

Independent Advice

5

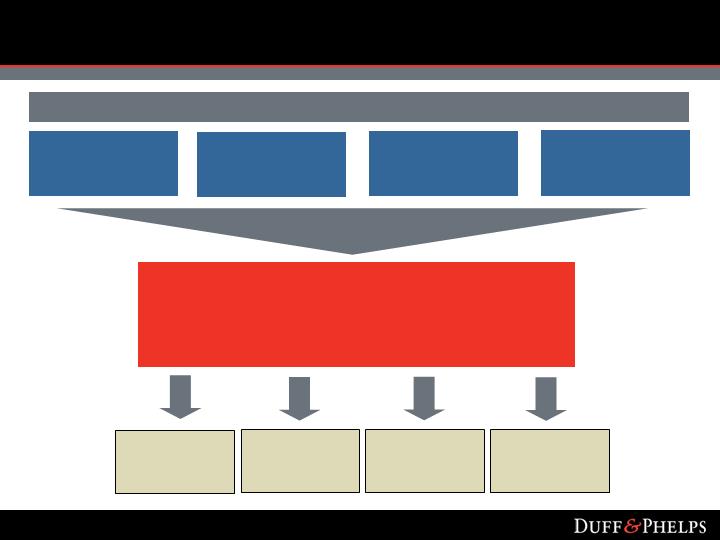

Valuation Services are the Foundation of Our Business

Fair Value

Accounting

Transparency

Corporate

Restructuring

Independence

VALUATION SERVICES

- Financial Reporting - Portfolio Valuation

- Transaction Opinions - Tax Valuation

- General Business Valuations - Financial Engineering

Specialty

Tax

Dispute

Consulting

M&A

Restructuring

Technical Expertise

Market Trends

6

Long-Standing, Diverse Client Base

Approximately one-third of the S&P 500 companies

Leading multi-national firms

Top-tier private equity firms and hedge funds

Client diversification

7

Technical Expertise

Independence

Scale

Brand

Culture

What Makes Duff & Phelps Unique?

8

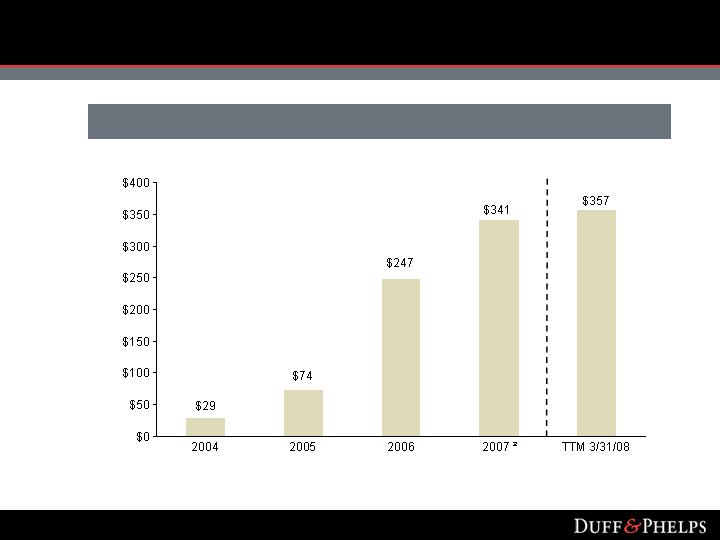

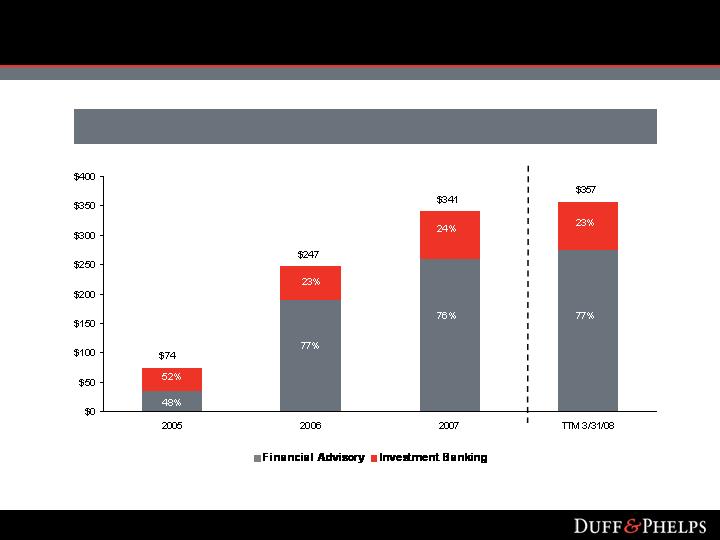

Financial Highlights

1 Total revenue excludes reimbursable expenses.

2 Revenue represents Aggregated Successor and Predecessor results.

3 TTM 3/31/08 represents the Trailing Twelve Months Ended March 31, 2008.

Duff & Phelps Revenue1

($ in millions)

3

9

Broad & Well-Balanced Service Portfolio

Counter-Cyclical

Restructuring Advisory

Dispute Consulting

FAS 142 (goodwill

impairment)

Strong Secular

Trends / Non-Cyclical

Portfolio Valuation

Financial Engineering

Transfer Pricing

Property Tax

General Valuation

International

M&A Driven

FAS 141

M&A Advisory

Transaction Opinions

M&A Due Diligence

M&A Driven

Counter-

Cyclical

10

Impact of Today’s Credit Environment

Duff & Phelps is benefiting from the market dislocation

Hired by multiple global financial institutions to provide independent valuation

assessments of their loan and CDO portfolios

Hired to provide multiple transaction opinions and related advice with respect to

distressed bail-out situations in the financial services sector

Hired as a restructuring advisor in connection with a distressed sub-prime

situation

Major corporate clients are hiring D&P to value their investment portfolios,

particularly given their typical concentrations in money-market, municipals and

CDO-related investments

FAS 142 impairment valuation practice seeing lift in today’s environment

11

Growth Strategy

International expansion

Complementary / new service offerings

Cross-selling

Brand building

Focus on balance

12

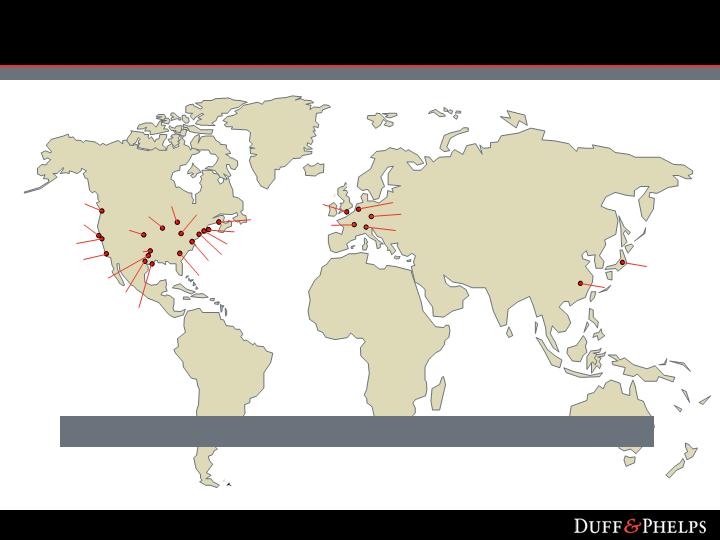

Expanding Global Platform

Tokyo

Silicon Valley

San Francisco

Seattle

Detroit

Chicago

Houston

Dallas

Los Angeles

Denver

Austin

Amsterdam

London

Munich

Zurich

Paris

Plano

Cincinnati

Boston

New York

Morristown

Philadelphia

Atlanta

Washington, DC Metro

Significant International Growth Opportunities

Shanghai

13

Expanding Global Platform

Increased global restructuring capability by adding

experienced restructuring professionals in Paris

Continued expansion in Asia through the opening of a

Shanghai office

Strategic relationship with Shinsei Bank in Japan supports

platform for further Asian market penetration

Continued growth throughout Europe and Asia

14

Our Culture

Unconflicted

Dynamic

Environment

Multiple Growth

Channels

Cross-selling

75 Year History

Partnership

Heritage

Global Presence

Blue Chip Clients

Diverse Portfolio

Collaborative, Team-Oriented Culture

LARGE, STABLE

ORGANIZATION

HIGH GROWTH

FIRM

15

Operational and Financial Highlights

Delivering Solutions

Financial Advisory

Valuation Advisory

Corporate Finance

Consulting

Specialty Tax

Dispute & Legal

Management

Consulting

Investment Banking

Transaction Opinions

M&A Advisory

Restructuring

17

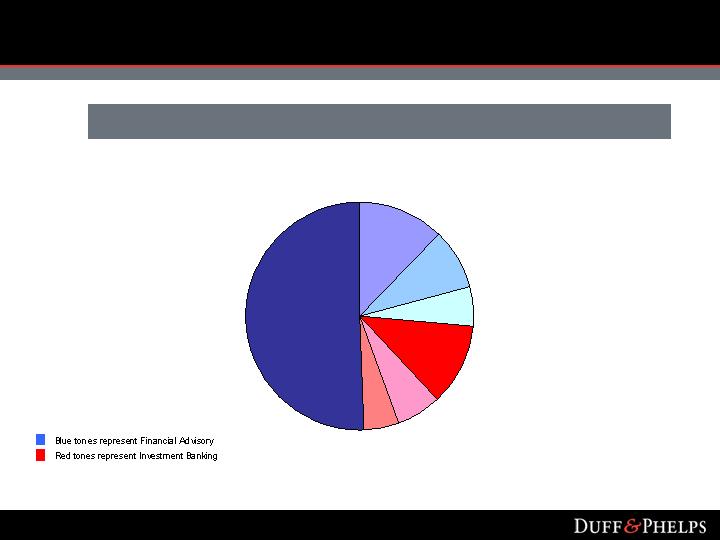

Financial Highlights

Revenue1 Snapshot by Service Category

¹ Represents revenue for the Trailing Twelve Months Ended March 31, 2008.

Corporate Finance Consulting 12%

Valuation Advisory Services 51%

Specialty Tax 8%

Dispute and Legal Management 6%

Transaction Opinions 12%

M&A Advisory 6%

Restructuring 5%

18

Business Model Diversification

Pricing

Key Metrics

Financials

Rates & Hours

Utilization

Rate per Hour

Mid 40% Gross Margin

More Predictable

Big 4

Specialty consulting

Retainer / Success Fee

Revenue per Professional

Backlog / Pipeline

High 40% Gross Margin

Transaction Based

Boutique investment banks

FINANCIAL

ADVISORY

INVESTMENT

BANKING

23%

Technical Expertise in Financial Analysis & Valuation

77%

Competition

19

Selected Operating Metrics

Financial Advisory

Investment Banking

Total

2005

2006

2007 2

425

84

509

746

98

844

($000s)

Financial Advisory

Investment Banking

Total

$344

$424

$377

$374

$651

$415

$409

$808

$464

Utilization

Rate per hour ($)

71.4%

$264

68.1%

$300

69.0%

$323

1 Revenue per professional calculated by dividing total segment revenue by average headcount for the given period of time.

2 Revenue used for calculation represents Aggregated Successor and Predecessor results and excludes reimbursable expenses.

3 Excludes approximately 60 professionals and approximately $1.6 million and $2.0 million of revenue associated with Rash & Associates in 2007 and Q1 2008, respectively.

Q1 2008

66.1%

$326

$95

$187

$105

807

109

916

553

118

671

Q1 2007

591

100

691

67.5%

$314

$102

$174

$114

20

Client Service Professionals

Sources of Growth

Financial Advisory1

52% of growth in headcount associated with Specialty Tax of which approximately 30%

resulted from the acquisition of Rash & Associates

25% of growth from additional domestic hiring across other service lines

23% of growth from hiring internationally

Investment Banking

Nine client service professionals hired in our Paris office to build a restructuring

business

Since the end of the quarter, we have built this restructuring practice to over 20 client

service professionals, including three managing directors

1 Between the quarters ended March 31, 2007 and March 31, 2008.

21

Financial Highlights

¹ 2007 represents Aggregated Successor and Predecessor results. TTM 3/31/08 represents the Trailing Twelve Months Ended March 31, 2008.

Revenue1

($ in millions)

22

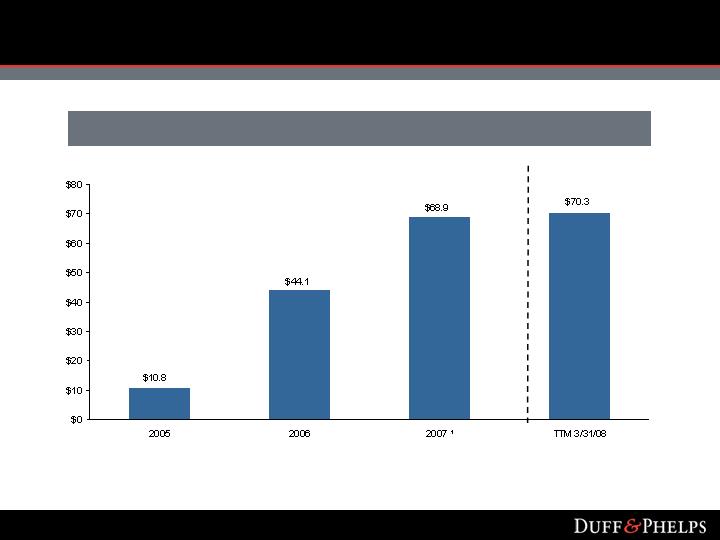

Financial Highlights

¹ Represents Aggregated Successor and Predecessor results.

2 Represents Trailing Twelve Months Ended March 31, 2008.

Adjusted EBITDA

($ in millions)

2

23

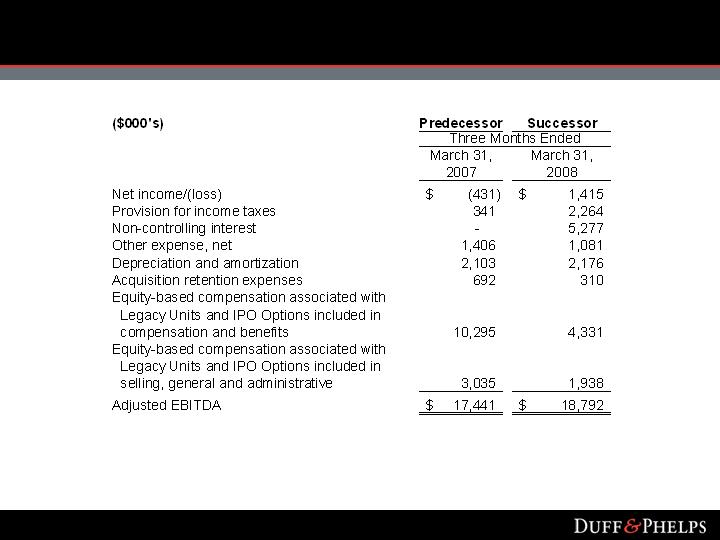

Adjusted EBITDA Reconciliation

24

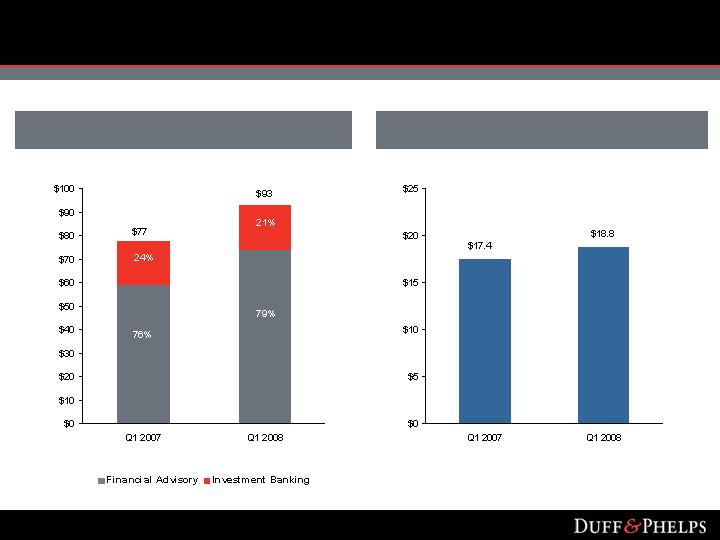

Q1 Adjusted EBITDA

Q1 Revenue

Financial Highlights

($ in millions)

25

Adjusted EBITDA Reconciliation

26

Long-Term Financial Objectives

15-20% Total Revenue Growth

Mix of organic and acquired revenue

19-20% Adjusted EBITDA Margin

Gross margin leverage (productivity improvement, business mix)

Utilization

SG&A leverage

20% Adjusted Pro Forma EPS Growth

On a fully exchanged, fully diluted basis

Low-to-mid single digit % annual share count growth

Primarily with respect to Restricted Stock Awards granted in connection with ongoing equity

compensation

Excludes material acquisitions or additional share offerings

Note: The foregoing does not represent projections for any period, but rather long-term objectives that management utilizes

as goals in managing the business. Results for any particular period will reflect the impact of the business cycle and various

other factors, including those discussed under "Risk Factors" in our Form 10-K for the year ended December 31, 2007.

27

Conclusion

Positioned to capitalize on key industry trends

Uniquely qualified to succeed

Broad and well-balanced service offerings for all markets

Benefiting from today’s volatile market environment

Strong financial performance

Significant growth opportunities

Investment Highlights

29