|

|

| OMB APPROVAL |

| OMB Number: 3235-0570 |

| Expires: August 31, 2011 |

| Estimated average burden hours |

| per response. . . . . . . . . . . . . . . . .18.9 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22067

| AGIC Global Equity & Convertible Income Fund |

| (Exact name of registrant as specified in charter) |

|

|

|

| 1345 Avenue of the Americas, New York, | NY 10105 |

| (Address of principal executive offices) | (Zip code) |

| Lawrence G. Altadonna – 1345 Avenue of the Americas, New York, NY 10105 |

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: 212-739-3371

Date of fiscal year: August 31, 2010

Date of reporting period: August 31, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-2001. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

ITEM 1: REPORT TO SHAREHOLDERS

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Annual Report |

|

August 31, 2010

AGIC Global Equity & Convertible Income Fund

(formerly Nicholas-Applegate Global Equity & Convertible Income Fund)

|

|

|

Contents |

|

|

|

|

|

| 2–3 | |

|

|

|

| 4 | |

|

|

|

| 5 | |

|

|

|

| 6–18 | |

|

|

|

| 19 | |

|

|

|

| 20 | |

|

|

|

| 21 | |

|

|

|

| 22–30 | |

|

|

|

| 31 | |

|

|

|

| 32 | |

|

|

|

Annual Shareholder Meeting Results/ |

| 33 |

|

|

|

| 34–36 | |

|

|

|

| 37 | |

|

|

|

Proxy Voting Policies & Procedures/ |

| 38 |

|

|

|

| 39 | |

|

|

|

| 40 | |

|

|

|

| 41 |

8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 1

The fiscal year ended August 31, 2010 encompassed two different stories. The first eight months were characterized by solid gains for convertible bonds and U.S. and global stocks, as the rally that began in March 2009 continued. However, during the last few months of the reporting period, slowing economic growth, global debt concerns and fears of a double-dip recession combined to make a significant portion of those gains evaporate.

In contrast, the Morgan Stanley Capital International (“MSCI”) All Country World Index, an unmanaged global index generally reflective of developed equity markets, advanced 3.49% in U.S. dollar terms. The Merrill Lynch All-Convertible Index, an unmanaged index generally representative of the convertible securities market, gained 14.27%. The S&P 500 Index, an unmanaged index that is generally representative of the U.S. stock market, rose 4.91% and the Barclays Capital U.S. Treasury Bond Index advanced 8.13% for the fiscal year.

Between October and December 2009, the economy, as measured by gross domestic product (“GDP”), grew at an annual rate of 5.0%. This slowed to 3.7% between January and March 2010 and 1.6% between April and June. In July and August, plunging home sales, tepid consumer spending and high unemployment instilled little confidence that growth would revive soon.

Abroad, there were fears that a handful of European governments could default on their debt. A European Union bailout of approximately $1 trillion calmed the markets initially, though some critics pointed out this was not a permanent fix. In China, the government took measures to throttle back the country’s booming economy.

The net effect of these factors was a rush for the exits by investors into the perceived safe haven of U.S. Treasury bonds. Prices surged and, as the Fund’s fiscal year drew to a close, the yield on the benchmark 10-year bond fell to 2.47%. Corporate bonds were perceived as risky and fell, as did stocks.

In this “unusually uncertain” period – to quote Federal Reserve (the “Fed”) Chairman Ben Bernanke – interest rates remained low. The Fed maintained the Federal Funds Rate – the interest rate banks charge to lend federal funds to other banks – in the 0.0% to 0.25% range. The discount rate – the interest rate charged

2 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10

to banks for direct loans – ended the fiscal year at 0.75%, after an increase of 25 basis points in February. The Fed also lowered expectations for economic growth, indicating that it could take until 2016 for conditions to return to what policymakers considered “normal.”

|

|

|

For specific information on the Fund and its performance, please refer to the following pages. If you have any questions regarding the information provided, we encourage you to contact your financial advisor or call the Fund’s shareholder servicing agent at (800) 254-5197. In addition, a wide range of information and resources is available on our website, www.allianzinvestors.com/closedendfunds. |

| Receive this report electronically and eliminate paper mailings. To enroll, go to www.allianzinvestors.com/ edelivery. |

Together with Allianz Global Investors Fund Management LLC, the Fund’s investment manager, and Allianz Global Investors Capital LLC, the Fund’s sub-adviser, we thank you for investing with us.

We remain dedicated to serving your investment needs.

Sincerely,

|

|

|

|

|

|

|

|

|

Hans W. Kertess |

| Brian S. Shlissel |

8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 3

|

August 31, 2010 (unaudited) |

|

|

• | For the fiscal year ended August 31, 2010, AGIC Global Equity & Convertible Income Fund returned 6.71% on NAV and 17.66% on market price. |

|

|

• | Global equities ended modestly higher for the reporting period with gains in emerging markets, North America and the Pacific region offsetting declines in Europe and Japan. A robust stock rally lost momentum in late spring and equity indexes slumped through summer, taking back most of the period’s early gains. Within the MSCI All Country World Index, companies in the consumer staples, consumer discretionary and materials sectors delivered the highest average returns. Share prices declined, on average, for index constituents in the financials and energy sectors. |

|

|

• | The convertible market, as measured by the Merrill Lynch All-Convertible Index, experienced positive performance during the reporting period, exceeding the returns of many domestic equity benchmarks. |

|

|

• | The high risk-aversion of 2008 and 2009 gradually subsided during the reporting period. Companies seeking debt financing experienced a highly accommodative corporate bond market. The easing of the credit crunch coincided with rising bond prices and a tightening of credit spreads. |

|

|

• | Except for a brief early-summer spike in volatility, The Chicago Board Options Exchange Volatility Index (VIX) remained subdued throughout the period, despite multiple directional changes for stocks. Domestic call writing for the Fund was opportunistic. Volatility in European and Japanese equities spiked at the beginning of May from March lows and then fell into a more stable range, creating opportunities for international covered call-writing on a tactical basis. |

|

|

• | Within the convertible universe, performance was broadly positive during the fiscal year. Securities in every sector recorded gains on average. Bond-like or busted convertibles rose in price despite the companies’ deteriorated operating fundamentals. Busted convertible securities trade like fixed-income investments because the market price of the common stock they convert to has fallen low enough to render the conversion feature valueless. Ultimately, improving credit conditions played the most significant role in the recovery of the convertible market. |

|

|

• | In absolute terms, the Fund’s equity positions in the consumer discretionary, consumer staples and industrials sectors contributed most significantly to gains during the fiscal year. Fund positions in energy and utilities sector stocks detracted from performance. The Fund’s convertible weightings in the financials, utilities and materials sector contributed positively to returns versus the benchmark. Exposure to convertible securities in the energy, technology and health care sectors detracted from relative returns. |

|

|

• | International markets, as measured by the MSCI EAFE Index, declined on average during the fiscal year. Weakness in Japan and in the European Union countries outweighed the relative strength of the Nordic countries, Switzerland and the developed Pacific markets of Hong Kong, Singapore and Australia. |

|

|

• | Signs of weak but emerging economic growth sparked recovery in the ailing consumer discretionary and materials sectors during the period. In this environment, the Fund’s equity positions in carmaker Ford and online retailer Amazon contributed positively to returns. Ford provided upbeat guidance on profits early in the period and made progress throughout the fiscal year at improving its balance sheet and sharpening its focus on core businesses. Amazon shares posted sharp gains early in the period when the company provided guidance for substantial earnings growth ahead of the holiday shopping season. |

|

|

• | Stock selection decisions among financials companies and an underweighting of the sector contributed to the Fund’s posting of gains in an area that declined for the Merrill Lynch All Convertibles All Quality Index. Positions in Commonwealth Bank and Challenger Financial Services, both based in Australia, benefited from a regional recovery and contributed positively to returns. |

|

|

• | Equities in Europe remained weak amid concerns about the national debts of some of the countries using the euro currency. Greece, Spain, Ireland, Italy, and Portugal all contributed to an onslaught of headlines on the collective instability of the region’s monetary system. The Fund’s position in Spanish telecommunications company Telefonica declined on these concerns, detracting from returns during the period. France Telecom saw its share price drop in this environment, as the company’s efforts rebuild morale internally and its image externally ran up against a general feeling of angst among European consumers and investors. |

4 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10

|

AGIC Global Equity & Convertible Income Fund Performance & Statistics |

August 31, 2010 (unaudited) |

|

|

|

|

|

|

|

Total Return (1): |

| Market Price |

| NAV | ||

1 Year |

| 17.66 | % |

| 6.71 | % |

Commencement of Operations (9/28/07) to 8/31/10 |

| (8.59 | )% |

| (6.84 | )% |

Commencement of Operations (9/28/07) to 8/31/10

|

|

|

|

|

Market Price/NAV: |

|

|

|

|

Market Price |

|

| $14.10 |

|

NAV |

|

| $14.54 |

|

Discount to NAV |

|

| (3.03 | )% |

Market Price Yield(2) |

|

| 7.20 | % |

|

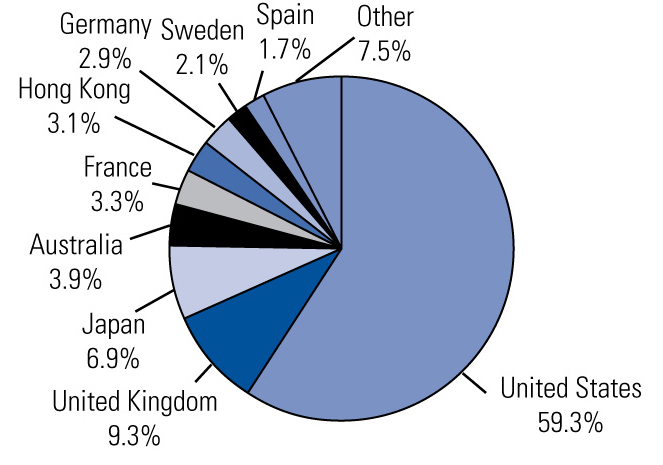

Investment Allocation |

| |

(1) | Past performance is no guarantee of future results. Total return is calculated by determining the percentage change in NAV or market price (as applicable) in the specified period. The calculation assumes that all income dividends, capital gain and return of capital distributions, if any, have been reinvested. Total returns do not reflect the deduction of taxes that a shareholder would pay on a Fund’s distributions or the redemption of a Fund’s shares. Total return does not reflect broker commissions or sales charges. Total return for a period of more than one year represents the average annual total return. |

| |

| Performance at market price will differ from its results at NAV. Although market price returns typically reflect investment results over time, during shorter periods returns at market price can also be influenced by factors such as changing views about the Fund, market conditions, supply and demand for the Fund’s shares, or changes in the Fund’s dividends. |

| |

| An investment in the Fund involves risk, including the loss of principal. Total return, market price, market yield and NAV will fluctuate with changes in market conditions. This data is provided for information purposes only and is not intended for trading purposes. Closed-end funds, unlike open-end funds, are not continuously offered. There is a onetime public offering and once issued, shares of closed-end funds are sold in the open market through a stock exchange. NAV is equal to total assets less total liabilities divided by the number of shares outstanding. Holdings are subject to change daily. |

| |

(2) | Market Price Yield is determined by dividing the annualized current quarterly per share dividend (comprised of net investment income and net capital gains, if any) payable to shareholders by the market price per share at August 31, 2010. |

8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 5

|

|

Schedule of Investments | |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

| COMMON STOCK—80.3% |

|

|

|

| ||

|

|

| Australia—3.2% |

|

|

|

|

|

|

| Airlines—0.3% |

|

|

|

|

| 152,554 |

| Qantas Airways Ltd. (a) |

| $ | 342,656 |

|

|

|

| Biotechnology—0.5% |

|

|

|

|

| 17,462 |

| CSL Ltd. (b) |

|

| 513,564 |

|

|

|

| Commercial Banks—0.9% |

|

|

|

|

| 19,579 |

| Commonwealth Bank of Australia |

|

| 880,316 |

|

|

|

| Construction & Engineering—0.4% |

|

|

|

|

| 14,173 |

| Leighton Holdings Ltd. |

|

| 388,676 |

|

|

|

| Diversified Financial Services—0.5% |

|

|

|

|

| 139,994 |

| Challenger Financial Services Group Ltd. |

|

| 471,289 |

|

|

|

| Metals & Mining—0.6% |

|

|

|

|

| 13,924 |

| BHP Billiton Ltd. |

|

| 462,151 |

|

| 58,602 |

| OneSteel Ltd. |

|

| 151,222 |

|

|

|

|

|

|

| 613,373 |

|

|

|

| Austria—0.1% |

|

|

|

|

|

|

| Building Products—0.0% |

|

|

|

|

| 3,027 |

| Wienerberger AG (a) |

|

| 39,259 |

|

|

|

| Metals & Mining—0.1% |

|

|

|

|

| 2,316 |

| Voestalpine AG |

|

| 68,709 |

|

|

|

| Belgium—0.1% |

|

|

|

|

|

|

| Chemicals—0.1% |

|

|

|

|

| 5,374 |

| Tessenderlo Chemie NV |

|

| 152,003 |

|

|

|

| Brazil—0.9% |

|

|

|

|

|

|

| Metals & Mining—0.9% |

|

|

|

|

| 32,439 |

| Vale S.A. - Cl. B — ADR |

|

| 867,743 |

|

|

|

| Canada—0.4% |

|

|

|

|

|

|

| Communications Equipment—0.4% |

|

|

|

|

| 9,100 |

| Research In Motion Ltd. (a) |

|

| 390,026 |

|

|

|

| China—0.2% |

|

|

|

|

|

|

| Electronic Equipment, Instruments—0.1% |

|

|

|

|

| 30,500 |

| Kingboard Chemical Holdings Ltd. |

|

| 144,531 |

|

|

|

| Independent Power Producers—0.1% |

|

|

|

|

| 38,000 |

| China Resources Power Holdings Co., Ltd. |

|

| 84,359 |

|

|

|

| Denmark—0.1% |

|

|

|

|

|

|

| Construction & Engineering—0.1% |

|

|

|

|

| 2,000 |

| FLSmidth & Co. AS |

|

| 117,819 |

|

|

|

| Finland—0.3% |

|

|

|

|

|

|

| Communications Equipment—0.1% |

|

|

|

|

| 7,353 |

| Nokia Oyj |

|

| 62,838 |

|

|

|

| Food & Staples Retailing—0.2% |

|

|

|

|

| 4,984 |

| Kesko Oyj - Cl. B |

|

| 193,456 |

|

6 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

| France—2.6% |

|

|

|

|

|

|

| Airlines—0.1% |

|

|

|

|

| 4,355 |

| Air France - - KLM (a) |

| $ | 57,314 |

|

|

|

| Automobiles—0.3% |

|

|

|

|

| 9,874 |

| Peugeot S.A. (a) |

|

| 258,777 |

|

| 1,838 |

| Renault S.A. (a) |

|

| 74,466 |

|

|

|

|

|

|

| 333,243 |

|

|

|

| Commercial Banks—0.5% |

|

|

|

|

| 4,922 |

| BNP Paribas |

|

| 305,815 |

|

| 12,598 |

| Credit Agricole S.A. |

|

| 157,831 |

|

|

|

|

|

|

| 463,646 |

|

|

|

| Diversified Telecommunication—0.9% |

|

|

|

|

| 47,233 |

| France Telecom S.A. (b) |

|

| 962,894 |

|

|

|

| Electrical Equipment—0.2% |

|

|

|

|

| 4,912 |

| Alstom S.A. |

|

| 234,027 |

|

|

|

| Household Durables—0.1% |

|

|

|

|

| 2,043 |

| SEB S.A. |

|

| 150,236 |

|

|

|

| Metals & Mining—0.1% |

|

|

|

|

| 3,088 |

| ArcelorMittal |

|

| 89,763 |

|

|

|

| Oil, Gas & Consumable Fuels—0.4% |

|

|

|

|

| 8,490 |

| Total S.A. |

|

| 396,060 |

|

|

|

| Germany—2.3% |

|

|

|

|

|

|

| Airlines—0.4% |

|

|

|

|

| 23,665 |

| Deutsche Lufthansa AG (a) |

|

| 374,174 |

|

|

|

| Automobiles—1.0% |

|

|

|

|

| 17,212 |

| Daimler AG (a)(b) |

|

| 835,148 |

|

| 3,950 |

| Porsche Automobile Holding SE |

|

| 184,769 |

|

|

|

|

|

|

| 1,019,917 |

|

|

|

| Chemicals—0.4% |

|

|

|

|

| 7,688 |

| K+S AG |

|

| 402,016 |

|

|

|

| Industrial Conglomerates—0.3% |

|

|

|

|

| 2,992 |

| Siemens AG |

|

| 272,010 |

|

|

|

| Metals & Mining—0.1% |

|

|

|

|

| 1,548 |

| Salzgitter AG |

|

| 94,358 |

|

|

|

| Multi-Utilities—0.0% |

|

|

|

|

| 568 |

| RWE AG |

|

| 37,286 |

|

|

|

| Semiconductors & Semiconductor Equipment—0.1% |

|

|

|

|

| 2,911 |

| Aixtron AG |

|

| 72,099 |

|

| 15,947 |

| Infineon Technologies AG (a) |

|

| 88,690 |

|

|

|

|

|

|

| 160,789 |

|

|

|

| Greece—0.0% |

|

|

|

|

|

|

| Commercial Banks—0.0% |

|

|

|

|

| 4,039 |

| National Bank of Greece S.A. (a) |

|

| 50,294 |

|

8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 7

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

| Hong Kong—2.5% |

|

|

|

|

|

|

| Airlines—0.5% |

|

|

|

|

| 197,000 |

| Cathay Pacific Airways Ltd. |

| $ | 488,607 |

|

|

|

| Diversified Financial Services—0.1% |

|

|

|

|

| 8,000 |

| Hong Kong Exchanges & Clearing Ltd. |

|

| 126,204 |

|

|

|

| Electric Utilities—0.2% |

|

|

|

|

| 59,000 |

| Cheung Kong Infrastructure Holdings Ltd. |

|

| 227,979 |

|

|

|

| Industrial Conglomerates—0.2% |

|

|

|

|

| 3,600 |

| Jardine Matheson Holdings Ltd. |

|

| 156,451 |

|

|

|

| Marine—0.1% |

|

|

|

|

| 10,500 |

| Orient Overseas International Ltd. |

|

| 84,918 |

|

|

|

| Paper & Forest Products—0.1% |

|

|

|

|

| 112,000 |

| Lee & Man Paper Manufacturing Ltd. |

|

| 78,309 |

|

|

|

| Real Estate Management & Development—1.1% |

|

|

|

|

| 41,000 |

| Hang Lung Group Ltd. |

|

| 247,359 |

|

| 118,000 |

| New World Development Ltd. |

|

| 190,328 |

|

| 56,000 |

| Swire Pacific Ltd. - Cl. A |

|

| 677,320 |

|

|

|

|

|

|

| 1,115,007 |

|

|

|

| Semiconductors & Semiconductor Equipment—0.1% |

|

|

|

|

| 16,500 |

| ASM Pacific Technology Ltd. |

|

| 134,592 |

|

|

|

| Specialty Retail—0.1% |

|

|

|

|

| 19,981 |

| Esprit Holdings Ltd. |

|

| 112,737 |

|

|

|

| Ireland—0.0% |

|

|

|

|

|

|

| Banks—0.0% |

|

|

|

|

| 20,740 |

| Anglo Irish Bank Corp. PLC (a)(c) |

|

| 264 |

|

|

|

| Insurance—0.0% |

|

|

|

|

| 9,738 |

| Irish Life & Permanent PLC (a) |

|

| 17,905 |

|

|

|

| Italy—0.7% |

|

|

|

|

|

|

| Electric Utilities—0.3% |

|

|

|

|

| 54,358 |

| Enel SpA |

|

| 258,708 |

|

|

|

| Household Durables—0.1% |

|

|

|

|

| 14,735 |

| Indesit Co. SpA |

|

| 141,885 |

|

|

|

| Oil, Gas & Consumable Fuels—0.3% |

|

|

|

|

| 13,395 |

| ENI SpA |

|

| 265,432 |

|

|

|

| Japan—5.5% |

|

|

|

|

|

|

| Auto Components—0.1% |

|

|

|

|

| 5,800 |

| Tokai Rika Co., Ltd. |

|

| 90,342 |

|

|

|

| Commercial Banks—0.3% |

|

|

|

|

| 169,000 |

| Hokuhoku Financial Group, Inc. |

|

| 295,519 |

|

|

|

| Computers & Peripherals—0.1% |

|

|

|

|

| 13,000 |

| Toshiba Corp. (a) |

|

| 61,134 |

|

|

|

| Consumer Finance—0.1% |

|

|

|

|

| 490 |

| ORIX Corp. |

|

| 36,863 |

|

| 13,600 |

| Promise Co., Ltd. |

|

| 106,092 |

|

|

|

|

|

|

| 142,955 |

|

8 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

| Japan—(continued) |

|

|

|

|

|

|

| Diversified Telecommunication—0.1% |

|

|

|

|

| 2,100 |

| Nippon Telegraph & Telephone Corp. |

| $ | 90,338 |

|

|

|

| Electronic Equipment, Instruments—0.4% |

|

|

|

|

| 3,500 |

| FUJIFILM Holdings Corp. |

|

| 106,270 |

|

| 5,500 |

| Mitsumi Electric Co., Ltd. |

|

| 77,048 |

|

| 23,000 |

| Nippon Chemi-Con Corp.(a) |

|

| 91,947 |

|

| 14,000 |

| Star Micronics Co., Ltd. |

|

| 120,192 |

|

|

|

|

|

|

| 395,457 |

|

|

|

| Health Care Equipment & Supplies—0.2% |

|

|

|

|

| 7,000 |

| Olympus Corp. |

|

| 167,397 |

|

|

|

| Household Durables—0.4% |

|

|

|

|

| 13,300 |

| Sony Corp. |

|

| 372,950 |

|

|

|

| Leisure Equipment & Products—0.5% |

|

|

|

|

| 5,000 |

| Nikon Corp. |

|

| 83,365 |

|

| 7,900 |

| Sankyo Co., Ltd. |

|

| 399,809 |

|

|

|

|

|

|

| 483,174 |

|

|

|

| Machinery—0.2% |

|

|

|

|

| 5,000 |

| Glory Ltd. |

|

| 106,864 |

|

| 4,700 |

| Shima Seiki Manufacturing Ltd. |

|

| 88,004 |

|

|

|

|

|

|

| 194,868 |

|

|

|

| Marine—0.5% |

|

|

|

|

| 71,000 |

| Mitsui OSK Lines Ltd. |

|

| 446,502 |

|

| 32,000 |

| Nippon Yusen KK |

|

| 123,314 |

|

|

|

|

|

|

| 569,816 |

|

|

|

| Metals & Mining—0.4% |

|

|

|

|

| 4,300 |

| JFE Holdings, Inc. |

|

| 126,940 |

|

| 43,000 |

| Nippon Steel Corp. |

|

| 141,943 |

|

| 56,000 |

| Sumitomo Metal Industries Ltd. |

|

| 131,268 |

|

|

|

|

|

|

| 400,151 |

|

|

|

| Pharmaceuticals—0.2% |

|

|

|

|

| 6,000 |

| Chugai Pharmaceutical Co., Ltd. |

|

| 102,629 |

|

| 3,300 |

| Daiichi Sankyo Co., Ltd. |

|

| 65,963 |

|

|

|

|

|

|

| 168,592 |

|

|

|

| Real Estate Management & Development—0.1% |

|

|

|

|

| 2,000 |

| Daito Trust Construction Co., Ltd. |

|

| 114,906 |

|

|

|

| Road & Rail—0.1% |

|

|

|

|

| 1,700 |

| East Japan Railway Co. |

|

| 109,995 |

|

|

|

| Software—0.1% |

|

|

|

|

| 300 |

| Nintendo Co., Ltd. |

|

| 83,209 |

|

|

|

| Specialty Retail—0.0% |

|

|

|

|

| 3,000 |

| Aoyama Trading Co., Ltd. |

|

| 41,373 |

|

|

|

| Tobacco—0.0% |

|

|

|

|

| 16 |

| Japan Tobacco, Inc. |

|

| 49,729 |

|

8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 9

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

| Japan—(continued) |

|

|

|

|

|

|

| Trading Companies & Distribution—1.5% |

|

|

|

|

| 54,000 |

| ITOCHU Corp. |

| $ | 440,435 |

|

| 70,000 |

| Marubeni Corp. |

|

| 360,562 |

|

| 26,000 |

| Mitsui & Co., Ltd. |

|

| 338,616 |

|

| 36,900 |

| Sumitomo Corp. |

|

| 422,913 |

|

|

|

|

|

|

| 1,562,526 |

|

|

|

| Wireless Telecommunication Services—0.2% |

|

|

|

|

| 50 |

| KDDI Corp. |

|

| 241,248 |

|

|

|

| Netherlands—0.1% |

|

|

|

|

|

|

| Diversified Financial Services—0.1% |

|

|

|

|

| 14,541 |

| ING Groep NV (a) |

|

| 128,780 |

|

|

|

| New Zealand—0.1% |

|

|

|

|

|

|

| Construction Materials—0.1% |

|

|

|

|

| 27,259 |

| Fletcher Building Ltd. |

|

| 143,782 |

|

|

|

| Norway—0.5% |

|

|

|

|

|

|

| Chemicals—0.4% |

|

|

|

|

| 10,500 |

| Yara International ASA |

|

| 420,073 |

|

|

|

| Energy Equipment & Services—0.1% |

|

|

|

|

| 3,400 |

| TGS Nopec Geophysical Co. ASA |

|

| 45,543 |

|

|

|

| Singapore—1.2% |

|

|

|

|

|

|

| Airlines—0.4% |

|

|

|

|

| 40,000 |

| Singapore Airlines Ltd. |

|

| 446,667 |

|

|

|

| Commercial Banks—0.2% |

|

|

|

|

| 36,000 |

| Oversea-Chinese Banking Corp. |

|

| 230,999 |

|

|

|

| Distributors—0.2% |

|

|

|

|

| 9,000 |

| Jardine Cycle & Carriage Ltd. |

|

| 216,484 |

|

|

|

| Electronic Equipment, Instruments—0.2% |

|

|

|

|

| 26,000 |

| Venture Corp. Ltd. |

|

| 167,123 |

|

|

|

| Real Estate Management & Development—0.1% |

|

|

|

|

| 71,000 |

| Wing Tai Holdings Ltd. |

|

| 85,112 |

|

|

|

| Transportation Infrastructure—0.1% |

|

|

|

|

| 29,200 |

| SATS Ltd. |

|

| 60,233 |

|

|

|

| Spain—1.4% |

|

|

|

|

|

|

| Construction & Engineering—0.4% |

|

|

|

|

| 9,221 |

| ACS Actividades de Construccion y Servicios S.A. |

|

| 382,896 |

|

| 2,822 |

| Sacyr Vallehermoso S.A. (a) |

|

| 12,712 |

|

|

|

|

|

|

| 395,608 |

|

|

|

| Diversified Telecommunication—1.0% |

|

|

|

|

| 45,274 |

| Telefonica S.A. |

|

| 1,003,561 |

|

|

|

| Sweden—1.7% |

|

|

|

|

|

|

| Commercial Banks—0.2% |

|

|

|

|

| 19,000 |

| Nordea Bank AB |

|

| 169,920 |

|

| 4,200 |

| Swedbank AB (a) |

|

| 46,959 |

|

|

|

|

|

|

| 216,879 |

|

10 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

| Sweden—(continued) |

|

|

|

|

|

|

| Household Durables—0.1% |

|

|

|

|

| 5,400 |

| Electrolux AB |

| $ | 104,027 |

|

|

|

| Machinery—0.5% |

|

|

|

|

| 20,200 |

| Sandvik AB |

|

| 239,019 |

|

| 16,000 |

| Trelleborg AB - Cl. B |

|

| 106,212 |

|

| 14,200 |

| Volvo AB - Cl. B (a) |

|

| 164,183 |

|

|

|

|

|

|

| 509,414 |

|

|

|

| Specialty Retail—0.9% |

|

|

|

|

| 26,400 |

| Hennes & Mauritz AB - Cl. B |

|

| 862,806 |

|

|

|

| Switzerland—1.3% |

|

|

|

|

|

|

| Biotechnology—0.2% |

|

|

|

|

| 5,878 |

| Actelion Ltd. (a) |

|

| 251,798 |

|

|

|

| Capital Markets—0.1% |

|

|

|

|

| 2,773 |

| Credit Suisse Group AG |

|

| 121,423 |

|

|

|

| Insurance—0.8% |

|

|

|

|

| 3,450 |

| Zurich Financial Services AG (b) |

|

| 767,582 |

|

|

|

| Textiles, Apparel & Luxury Goods—0.2% |

|

|

|

|

| 656 |

| Swatch Group AG |

|

| 210,694 |

|

|

|

| United Kingdom—7.5% |

|

|

|

|

|

|

| Aerospace & Defense—0.0% |

|

|

|

|

| 11,929 |

| BAE Systems PLC |

|

| 53,819 |

|

|

|

| Capital Markets—0.1% |

|

|

|

|

| 17,856 |

| 3i Group PLC |

|

| 71,170 |

|

|

|

| Commercial Banks—0.5% |

|

|

|

|

| 50,729 |

| Barclays PLC |

|

| 233,391 |

|

| 18,343 |

| Lloyds TSB Group PLC (a) |

|

| 19,349 |

|

| 51,937 |

| Royal Bank of Scotland Group PLC (a) |

|

| 35,249 |

|

| 9,470 |

| Standard Chartered PLC |

|

| 253,433 |

|

|

|

|

|

|

| 541,422 |

|

|

|

| Commercial Services & Supplies—0.3% |

|

|

|

|

| 13,579 |

| Aggreko PLC |

|

| 295,008 |

|

|

|

| Food & Staples Retailing—0.4% |

|

|

|

|

| 92,742 |

| WM Morrison Supermarkets PLC (b) |

|

| 412,091 |

|

|

|

| Industrial Conglomerates—0.1% |

|

|

|

|

| 4,961 |

| Cookson Group PLC (a) |

|

| 31,813 |

|

| 4,730 |

| Smiths Group PLC |

|

| 82,891 |

|

|

|

|

|

|

| 114,704 |

|

|

|

| Insurance—0.6% |

|

|

|

|

| 253,484 |

| Old Mutual PLC |

|

| 493,660 |

|

| 45,432 |

| Standard Life PLC |

|

| 141,588 |

|

|

|

|

|

|

| 635,248 |

|

|

|

| Machinery—0.2% |

|

|

|

|

| 17,900 |

| Charter International PLC |

|

| 167,250 |

|

8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 11

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

| United Kingdom—(continued) |

|

|

|

|

|

|

| Metals & Mining—1.6% |

|

|

|

|

| 6,416 |

| Anglo American PLC |

| $ | 229,319 |

|

| 36,554 |

| BHP Billiton PLC (b) |

|

| 1,021,492 |

|

| 5,372 |

| Rio Tinto PLC |

|

| 270,774 |

|

| 4,527 |

| Xstrata PLC |

|

| 70,795 |

|

|

|

|

|

|

| 1,592,380 |

|

|

|

| Multiline Retail—0.8% |

|

|

|

|

| 26,858 |

| Marks & Spencer Group PLC |

|

| 142,207 |

|

| 21,928 |

| Next PLC |

|

| 664,485 |

|

|

|

|

|

|

| 806,692 |

|

|

|

| Oil, Gas & Consumable Fuels—1.8% |

|

|

|

|

| 16,993 |

| BG Group PLC |

|

| 272,749 |

|

|

|

| Royal Dutch Shell PLC, |

|

|

|

|

| 16,201 |

| Class A |

|

| 429,974 |

|

| 45,399 |

| Class B (b) |

|

| 1,159,546 |

|

|

|

|

|

|

| 1,862,269 |

|

|

|

| Professional Services—0.1% |

|

|

|

|

| 14,108 |

| Michael Page International PLC |

|

| 85,743 |

|

|

|

| Specialty Retail—0.1% |

|

|

|

|

| 72,326 |

| Galiform PLC (a) |

|

| 69,652 |

|

| 16,621 |

| Game Group PLC |

|

| 16,849 |

|

|

|

|

|

|

| 86,501 |

|

|

|

| Tobacco—0.5% |

|

|

|

|

| 14,650 |

| British American Tobacco PLC (b) |

|

| 497,439 |

|

|

|

| Wireless Telecommunication Services—0.4% |

|

|

|

|

| 165,068 |

| Vodafone Group PLC |

|

| 397,178 |

|

|

|

| United States—47.6% |

|

|

|

|

|

|

| Aerospace & Defense—0.7% |

|

|

|

|

| 10,300 |

| L-3 Communications Holdings, Inc. |

|

| 685,980 |

|

|

|

| Auto Components—0.8% |

|

|

|

|

| 31,200 |

| Johnson Controls, Inc. |

|

| 827,736 |

|

|

|

| Automobiles—1.1% |

|

|

|

|

| 101,700 |

| Ford Motor Co. (a) |

|

| 1,148,193 |

|

|

|

| Beverages—2.2% |

|

|

|

|

| 20,100 |

| Coca-Cola Co. |

|

| 1,123,992 |

|

| 15,600 |

| Molson Coors Brewing Co. - Cl. B |

|

| 679,536 |

|

| 7,600 |

| PepsiCo, Inc. |

|

| 487,768 |

|

|

|

|

|

|

| 2,291,296 |

|

|

|

| Biotechnology—0.7% |

|

|

|

|

| 22,800 |

| Gilead Sciences, Inc. (a) |

|

| 726,408 |

|

|

|

| Capital Markets—1.0% |

|

|

|

|

| 31,248 |

| Lazard Ltd. - Cl. A |

|

| 976,813 |

|

12 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

| United States—(continued) |

|

|

|

|

|

|

| Communications Equipment—3.4% |

|

|

|

|

| 5,266 |

| Aviat Networks, Inc.(a) |

| $ | 20,748 |

|

| 44,800 |

| Cisco Systems, Inc.(a) |

|

| 898,240 |

|

| 5,984 |

| EchoStar Corp. - Cl. A (a) |

|

| 111,661 |

|

| 21,200 |

| Harris Corp. |

|

| 891,884 |

|

| 34,200 |

| Juniper Networks, Inc. (a) |

|

| 930,240 |

|

| 17,000 |

| Qualcomm, Inc. |

|

| 651,270 |

|

|

|

|

|

|

| 3,504,043 |

|

|

|

| Computers & Peripherals—3.0% |

|

|

|

|

| 4,275 |

| Apple, Inc. (a) |

|

| 1,040,407 |

|

| 61,000 |

| EMC Corp. (a)(b) |

|

| 1,112,640 |

|

| 7,500 |

| International Business Machines Corp. |

|

| 924,225 |

|

|

|

|

|

|

| 3,077,272 |

|

|

|

| Diversified Financial Services—0.9% |

|

|

|

|

| 24,837 |

| JP Morgan Chase & Co. |

|

| 903,073 |

|

|

|

| Diversified Telecommunication Services—0.9% |

|

|

|

|

| 6,769 |

| Frontier Communications Corp. |

|

| 52,324 |

|

| 28,200 |

| Verizon Communications, Inc. |

|

| 832,182 |

|

|

|

|

|

|

| 884,506 |

|

|

|

| Electric Utilities—1.1% |

|

|

|

|

| 13,855 |

| Entergy Corp. |

|

| 1,092,328 |

|

|

|

| Electronic Equipment, Instruments & Components—0.6% |

|

|

|

|

| 14,000 |

| Amphenol Corp. - Cl. A |

|

| 570,080 |

|

|

|

| Energy Equipment & Services—2.1% |

|

|

|

|

| 9,700 |

| Diamond Offshore Drilling, Inc. |

|

| 564,346 |

|

| 11,600 |

| National Oilwell Varco, Inc. |

|

| 436,044 |

|

| 21,700 |

| Schlumberger Ltd. |

|

| 1,157,261 |

|

|

|

|

|

|

| 2,157,651 |

|

|

|

| Food Products—0.6% |

|

|

|

|

| 20,500 |

| Archer-Daniels-Midland Co. |

|

| 630,990 |

|

|

|

| Health Care Equipment & Supplies—1.6% |

|

|

|

|

| 15,600 |

| Baxter International, Inc. |

|

| 663,936 |

|

| 3,680 |

| Intuitive Surgical, Inc. (a) |

|

| 975,310 |

|

|

|

|

|

|

| 1,639,246 |

|

|

|

| Health Care Providers & Services—2.2% |

|

|

|

|

| 23,000 |

| CIGNA Corp. |

|

| 741,060 |

|

| 15,000 |

| McKesson Corp. |

|

| 870,750 |

|

| 14,600 |

| Medco Health Solutions, Inc. (a) |

|

| 634,808 |

|

|

|

|

|

|

| 2,246,618 |

|

|

|

| Hotels, Restaurants & Leisure—1.1% |

|

|

|

|

| 15,000 |

| McDonald’s Corp. (b) |

|

| 1,095,900 |

|

|

|

| Household Durables—0.4% |

|

|

|

|

| 7,690 |

| Stanley Black & Decker, Inc. |

|

| 412,492 |

|

|

|

| Household Products—1.0% |

|

|

|

|

| 16,500 |

| Procter & Gamble Co. |

|

| 984,555 |

|

8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 13

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Value |

| ||

|

|

| United States—(continued) |

|

|

|

|

|

|

| Independent Power Producers & Energy Traders—1.1% |

|

|

|

|

| 12,500 |

| Constellation Energy Group, Inc. |

| $ | 366,625 |

|

| 38,461 |

| NRG Energy, Inc. (a) |

|

| 781,528 |

|

|

|

|

|

|

| 1,148,153 |

|

|

|

| Industrial Conglomerates—1.7% |

|

|

|

|

| 62,026 |

| General Electric Co. |

|

| 898,137 |

|

| 45,800 |

| Textron, Inc. |

|

| 781,806 |

|

|

|

|

|

|

| 1,679,943 |

|

|

|

| Insurance—2.1% |

|

|

|

|

| 46,000 |

| Genworth Financial, Inc. - Cl. A (a) |

|

| 498,180 |

|

| 11,760 |

| MetLife, Inc. |

|

| 442,176 |

|

| 17,000 |

| Prudential Financial, Inc. |

|

| 859,690 |

|

| 19,230 |

| XL Group PLC - Cl. A |

|

| 344,409 |

|

|

|

|

|

|

| 2,144,455 |

|

|

|

| Internet Software & Services—0.9% |

|

|

|

|

| 2,000 |

| Google, Inc. - - Cl. A (a) |

|

| 900,040 |

|

|

|

| Machinery—2.5% |

|

|

|

|

| 18,700 |

| AGCO Corp. (a) |

|

| 618,035 |

|

| 14,200 |

| Deere & Co. |

|

| 898,434 |

|

| 18,600 |

| Joy Global, Inc. (b) |

|

| 1,055,364 |

|

|

|

|

|

|

| 2,571,833 |

|

|

|

| Media—0.5% |

|

|

|

|

| 29,919 |

| DISH Network Corp. - Cl. A |

|

| 537,046 |

|

|

|

| Metals & Mining—1.2% |

|

|

|

|

| 17,550 |

| Freeport—McMoRan Copper & Gold, Inc. |

|

| 1,263,249 |

|

|

|

| Multiline Retail—1.0% |

|

|

|

|

| 19,500 |

| Target Corp. |

|

| 997,620 |

|

|

|

| Multi-Utilities—1.3% |

|

|

|

|

| 28,169 |

| PG&E Corp. |

|

| 1,317,182 |

|

|

|

| Oil, Gas & Consumable Fuels—1.7% |

|

|

|

|

| 5,500 |

| Occidental Petroleum Corp. |

|

| 401,940 |

|

| 23,900 |

| Peabody Energy Corp. |

|

| 1,022,920 |

|

| 18,800 |

| Valero Energy Corp. |

|

| 296,476 |

|

|

|

|

|

|

| 1,721,336 |

|

|

|

| Pharmaceuticals—4.4% |

|

|

|

|

| 16,000 |

| Abbott Laboratories |

|

| 789,440 |

|

| 43,300 |

| Bristol-Myers Squibb Co. |

|

| 1,129,264 |

|

| 18,224 |

| Johnson & Johnson |

|

| 1,039,132 |

|

| 43,391 |

| Merck & Co., Inc. |

|

| 1,525,628 |

|

|

|

|

|

|

| 4,483,464 |

|

|

|

| Semiconductors & Semiconductor Equipment—1.6% |

|

|

|

|

| 48,000 |

| Intel Corp. |

|

| 850,560 |

|

| 33,900 |

| Texas Instruments, Inc. |

|

| 780,717 |

|

|

|

|

|

|

| 1,631,277 |

|

14 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10

|

|

AGIC Global Equity & Convertible Income Fund Schedule of Investments | |

August 31, 2010 | |

|

|

|

|

|

|

|

|

|

|

Shares |

|

|

|

|

| Value |

| ||

|

|

| United States—(continued) |

|

|

|

|

|

|

|

|

| Software—2.2% |

|

|

|

|

|

|

| 44,500 |

| Microsoft Corp. |

|

|

| $ | 1,044,860 |

|

| 53,000 |

| Oracle Corp. |

|

|

|

| 1,159,640 |

|

|

|

|

|

|

|

|

| 2,204,500 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Common Stock (cost—$133,505,002) |

|

|

|

| 81,736,101 |

|

|

|

|

|

|

|

|

|

|

|

CONVERTIBLE PREFERRED STOCK—12.7% | |||||||||

|

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Credit Rating |

|

|

|

| |

|

|

| Airlines—0.1% |

|

|

|

|

|

|

| 2 |

| Continental Airlines Finance Trust II, 6.00%, 11/15/30 |

| Caa1/NR |

|

| 71,638 |

|

|

|

| Automobiles—0.4% |

|

|

|

|

|

|

| 60 |

| General Motors Corp., 6.25%, 7/15/33, Ser. C (a) |

| WR/NR |

|

| 441,000 |

|

|

|

| Banks—0.2% |

|

|

|

|

|

|

| 4 |

| Barclays Bank PLC, 10.00%, 3/15/11 |

| A1/A+ |

|

| 198,393 |

|

|

|

| Capital Markets—0.3% |

|

|

|

|

|

|

|

|

| Lehman Brothers Holdings, Inc. (c)(d)(e), |

|

|

|

|

|

|

| 42 |

| 6.00%, 10/12/10, Ser. GIS (General Mills, Inc.) |

| WR/NR |

|

| 135,833 |

|

| 9 |

| 28.00%, 3/6/09, Ser. RIG (Transocean, Inc.) |

| WR/NR |

|

| 126,771 |

|

|

|

|

|

|

|

|

| 262,604 |

|

|

|

| Commercial Banks—0.4% |

|

|

|

|

|

|

| 2 |

| Fifth Third Bancorp, 8.50%, 6/30/13, Ser. G (f) |

| Ba1/BB |

|

| 211,080 |

|

| — | (j) | Wells Fargo & Co., 7.50%, 3/15/13, Ser. L (f) |

| Ba1/A- |

|

| 246,750 |

|

|

|

|

|

|

|

|

| 457,830 |

|

|

|

| Commercial Services & Supplies—1.2% |

|

|

|

|

|

|

| 9 |

| Avery Dennison Corp., 7.875%, 11/15/20 |

| NR/BB+ |

|

| 346,500 |

|

| 29 |

| United Rentals, Inc., 6.50%, 8/1/28 |

| Caa2/CCC |

|

| 918,938 |

|

|

|

|

|

|

|

|

| 1,265,438 |

|

|

|

| Consumer Finance—0.4% |

|

|

|

|

|

|

| 1 |

| SLM Corp., 7.25%, 12/15/10 |

| Ba3/BB- |

|

| 388,537 |

|

|

|

| Diversified Financial Services—2.1% |

|

|

|

|

|

|

| 5 |

| AMG Capital Trust I, 5.10%, 4/15/36 |

| NR/BB |

|

| 185,633 |

|

|

|

| Bank of America Corp., |

|

|

|

|

|

|

| 1 |

| 7.25%, 1/30/13, Ser. L (f) |

| Ba3/BB |

|

| 475,000 |

|

| 7 |

| 10.00%, 2/24/11, Ser. SLB (Schlumberger Ltd.) (d) |

| A2/A |

|

| 388,790 |

|

| 4 |

| Citigroup, Inc., 7.50%, 12/15/12 |

| NR/NR |

|

| 480,690 |

|

| 41 |

| JP Morgan Chase & Co., 10.00%, 1/20/11 |

|

|

|

|

|

|

|

|

| (Symantec Corp.) (d) |

| Aa3/A+ |

|

| 596,366 |

|

|

|

|

|

|

|

|

| 2,126,479 |

|

|

|

| Food Products—1.3% |

|

|

|

|

|

|

| 11 |

| Archer-Daniels-Midland Co., 6.25%, 6/1/11 |

| NR/BBB+ |

|

| 467,628 |

|

| 10 |

| Bunge Ltd., 4.875%, 12/1/11 (f) |

| Ba1/BB |

|

| 835,000 |

|

|

|

|

|

|

|

|

| 1,302,628 |

|

8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 15

|

|

AGIC Global Equity & Convertible Income Fund Schedule of Investments | |

August 31, 2010 | |

|

|

|

|

|

|

|

|

|

|

Shares |

|

|

| Credit Rating |

| Value |

| ||

|

|

| Household Durables—0.2% |

|

|

|

|

|

|

| 4 |

| Newell Financial Trust I, 5.25%, 12/1/27 |

| WR/BB |

| $ | 165,660 |

|

|

|

| Insurance—0.8% |

|

|

|

|

|

|

| 22 |

| American International Group, Inc., 8.50%, 8/1/11 |

| Ba2/NR |

|

| 158,670 |

|

| 5 |

| Assured Guaranty Ltd., 8.50%, 6/1/12 |

| NR/NR |

|

| 343,408 |

|

| 14 |

| XL Group Ltd., 10.75%, 8/15/11 |

| Baa2/BBB- |

|

| 370,859 |

|

|

|

|

|

|

|

|

| 872,937 |

|

|

|

| Multi-Utilities—1.4% |

|

|

|

|

|

|

| 30 |

| AES Trust III, 6.75%, 10/15/29 |

| B3/B |

|

| 1,410,000 |

|

|

|

| Oil, Gas & Consumable Fuels—0.8% |

|

|

|

|

|

|

| 5 |

| ATP Oil & Gas Corp., 8.00%, 10/1/14 (f)(g)(h) |

| NR/NR |

|

| 287,875 |

|

| 7 |

| Chesapeake Energy Corp., 5.00%, 11/15/10 (f) |

| NR/B |

|

| 528,463 |

|

|

|

|

|

|

|

|

| 816,338 |

|

|

|

| Pharmaceuticals—0.4% |

|

|

|

|

|

|

| — | (j) | Mylan, Inc., 6.50%, 11/15/10 |

| NR/B |

|

| 392,767 |

|

|

|

| Real Estate Investment Trust—1.4% |

|

|

|

|

|

|

| 11 |

| Alexandria Real Estate Equities, Inc., 7.00%, 4/20/13 (f) |

| NR/NR |

|

| 248,240 |

|

| 60 |

| FelCor Lodging Trust, Inc., 1.95%, 12/31/49, Ser. A (a)(f) |

| Caa3/C |

|

| 1,186,800 |

|

|

|

|

|

|

|

|

| 1,435,040 |

|

|

|

| Wireless Telecommunication Services—1.3% |

|

|

|

|

|

|

| 23 |

| Crown Castle International Corp., 6.25%, 8/15/12 |

| NR/NR |

|

| 1,350,781 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Convertible Preferred Stock (cost—$19,538,002) |

|

|

|

| 12,958,070 |

|

|

|

|

|

|

|

|

|

|

|

CONVERTIBLE BONDS & NOTES—6.5% |

| ||||||||

|

|

|

|

|

|

|

|

|

|

Principal |

|

|

|

|

|

|

|

| |

|

|

| Auto Components—0.5% |

|

|

|

|

|

|

| $ 325 |

| BorgWarner, Inc., 3.50%, 4/15/12 |

| NR/BBB |

|

| 468,000 |

|

|

|

| Commercial Services & Supplies—0.6% |

|

|

|

|

|

|

| 650 |

| Bowne & Co., Inc., 6.00%, 10/1/33 (i) |

| B3/CCC+ |

|

| 643,500 |

|

|

|

| Electrical Equipment—1.1% |

|

|

|

|

|

|

| 400 |

| EnerSys, 3.375%, 6/1/38 (i) |

| B2/BB |

|

| 382,500 |

|

| 785 |

| JA Solar Holdings Co., Ltd., 4.50%, 5/15/13 |

| NR/NR |

|

| 713,369 |

|

|

|

|

|

|

|

|

| 1,095,869 |

|

|

|

| Energy Equipment & Services—0.3% |

|

|

|

|

|

|

| 375 |

| Hornbeck Offshore Services, Inc., 1.625%, 11/15/26 (i) |

| NR/B+ |

|

| 313,125 |

|

|

|

| Household Durables—0.5% |

|

|

|

|

|

|

| 475 |

| Stanley Black & Decker, Inc., zero coupon, 5/17/12, VRN |

| Baa1/A- |

|

| 510,625 |

|

|

|

| Internet Software & Services—0.3% |

|

|

|

|

|

|

| 275 |

| VeriSign, Inc., 3.25%, 8/15/37 |

| NR/NR |

|

| 280,156 |

|

|

|

| IT Services—0.5% |

|

|

|

|

|

|

| 475 |

| Alliance Data Systems Corp., 1.75%, 8/1/13 |

| NR/NR |

|

| 457,187 |

|

|

|

| Machinery—0.3% |

|

|

|

|

|

|

| 250 |

| Titan International, Inc., 5.625%, 1/15/17 (g)(h) |

| NR/NR |

|

| 298,750 |

|

16 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 | |

|

|

|

|

|

|

|

|

|

|

Principal |

|

|

| Credit Rating |

| Value |

| ||

|

|

| Media—0.7% |

|

|

|

|

|

|

| $ 310 |

| Liberty Media LLC, 3.125%, 3/30/23 |

| B1/BB- |

| $ | 338,675 |

|

| 400 |

| Regal Entertainment Group, 6.25%, 3/15/11 (g)(h) |

| NR/NR |

|

| 405,500 |

|

|

|

|

|

|

|

|

| 744,175 |

|

|

|

| Pharmaceuticals—0.6% |

|

|

|

|

|

|

| 365 |

| Biovail Corp., 5.375%, 8/1/14 (g)(h) |

| NR/NR |

|

| 599,513 |

|

|

|

| Real Estate Investment Trust—0.4% |

|

|

|

|

|

|

| 400 |

| Health Care REIT, Inc., 4.75%, 12/1/26 |

| Baa2/BBB- |

|

| 438,000 |

|

|

|

| Semiconductors & Semiconductor Equipment—0.5% |

|

|

|

|

|

|

| 600 |

| Micron Technology, Inc., 1.875%, 6/1/14 |

| NR/B |

|

| 519,750 |

|

|

|

| Thrifts & Mortgage Finance—0.2% |

|

|

|

|

|

|

| 200 |

| MGIC Investment Corp., 5.00%, 5/1/17 |

| NR/CCC+ |

|

| 194,750 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Convertible Bonds & Notes (cost—$6,892,126) |

|

|

|

| 6,563,400 |

|

|

|

|

|

|

|

|

|

|

|

WARRANTS (a)—0.0% | |||||||||

|

|

|

|

|

|

|

|

|

|

Units |

|

|

|

|

|

|

|

| |

|

|

| Electronic Equipment, Instruments—0.0% |

|

|

|

|

|

|

| 3,050 |

| Kingboard Chemical Holdings Ltd., expires 10/31/12 (cost—$361) |

|

|

|

| 1,341 |

|

|

|

|

|

|

|

|

|

|

|

SHORT-TERM INVESTMENT—0.4% | |||||||||

|

|

|

|

|

|

|

|

|

|

Principal |

|

|

|

|

|

|

|

| |

|

|

| Time Deposit—0.4% |

|

|

|

|

|

|

| $ 444 |

| Citibank - London, 0.03%, 9/1/10 (cost-$443,834) |

|

|

|

| 443,834 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Investments before call options written |

|

|

|

| 101,702,746 |

|

|

|

|

|

|

|

|

|

|

|

CALL OPTIONS WRITTEN (a)—(0.1)% | |||||||||

|

|

|

|

|

|

|

|

|

|

Contracts |

|

|

|

|

|

|

|

| |

|

|

| Dow Jones Euro Stoxx 50 Price Index, OTC, |

|

|

|

|

|

|

| 1,945 |

| strike price €2,743, expires 9/17/10 |

|

|

|

| (36,225 | ) |

|

|

| Joy Global, Inc., |

|

|

|

|

|

|

| 85 |

| strike price $65, expires 9/18/10 |

|

|

|

| (1,700 | ) |

|

|

| McDonald’s Corp., |

|

|

|

|

|

|

| 105 |

| strike price $75, expires 9/18/10 |

|

|

|

| (3,675 | ) |

|

|

| NIKKEI 225 Index, OTC, |

|

|

|

|

|

|

| 43,186 |

| strike price ¥9,687, expires 9/10/10 |

|

|

|

| (80 | ) |

|

|

| Total Call Options Written (premiums received—$85,226) |

|

|

|

| (41,680 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

| Total Investments net of call options written |

|

|

|

| 101,661,066 |

|

|

|

| Other assets less other liabilities—0.2% |

|

|

|

| 183,796 |

|

|

|

| Net Assets—100.0% |

|

|

| $ | 101,844,862 |

|

8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 17

|

|

AGIC Global Equity & Convertible Income Fund | Schedule of Investments |

August 31, 2010 |

|

|

|

| |

Notes to Schedule of Investments: | |

|

|

* | Unaudited. |

(a) | Non-income producing. |

(b) | All or partial amount segregated for the benefit of the counterparty as collateral for call options written. |

(c) | Fair-Valued—Securities with an aggregate value of $262,868, representing 0.3% of net assets. See Note 1(a) and Note 1(b) in the Notes to Financial Statements. |

(d) | Securities exchangeable or convertible into securities of an entity different than the issuer or structured by the issuer to provide exposure to securities of an entity different than the issuer. Such entity is identified in the parenthetical. |

(e) | In default. |

(f) | Perpetual maturity. Maturity date shown is the first call date. |

(g) | Private Placement—Restricted as to resale and may not have a readily available market. Securities with an aggregate value of $1,591,638, representing 1.6% of net assets. |

(h) | 144A—Exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, typically to qualified institutional buyers. Unless otherwise indicated, these securities are not considered to be illiquid. |

(i) | Step Bond—Coupon is a fixed rate for an initial period then resets at a specific date and rate. |

(j) | Less than 500 shares. |

(k) | Securities with an aggregrate value of $31,059,896, representing 30.5% of net assets, were valued utilizing modeling tools provided by a third-party vendor as described in Note 1(a) in the Notes to Financial Statements. |

|

|

Glossary:

|

€ — Euro |

¥ — Japanese Yen |

ADR — American Depository Receipt |

NR — Not Rated |

OTC — Over the Counter |

REIT — Real Estate Investment Trust |

|

|

VRN — | Variable Rate Note. Instruments whose interest rates change on specified date (such as a coupon date or interest payment date) and/or whose interest rates vary with changes in a designated base rate (such as the prime interest rate). The interest rate disclosed reflects the rate in effect on August 31, 2010. |

|

WR — Withdrawn Rating |

18 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10 | See accompanying Notes to Financial Statements

|

|

AGIC Global Equity & Convertible Income Fund | |

August 31, 2010 |

|

|

|

|

|

|

|

|

|

|

|

Assets: |

|

|

|

|

Investments, at value (cost—$160,379,325) |

| $101,702,746 |

| |

Foreign currency (cost—$64,122) |

|

| 62,591 |

|

Dividends and interest receivable (net of foreign withholding taxes) |

|

| 365,405 |

|

Prepaid expenses |

|

| 11,511 |

|

Total Assets |

|

| 102,142,253 |

|

|

|

|

|

|

Liabilities: |

|

|

|

|

Investment management fees payable |

|

| 89,320 |

|

Call options written, at value (premiums received—$85,226) |

|

| 41,680 |

|

Accrued expenses |

|

| 166,391 |

|

Total Liabilities |

|

| 297,391 |

|

Net Assets |

|

| $101,844,862 |

|

|

|

|

|

|

Composition of Net Assets: |

|

|

|

|

Common Shares: |

|

|

|

|

Par value ($0.00001 per share, applicable to 7,004,189 shares issued and outstanding) |

|

| $70 |

|

Paid-in-capital in excess of par |

|

| 161,751,731 |

|

Dividends in excess of net investment income |

|

| (321,825 | ) |

Accumulated net realized loss |

|

| (948,711 | ) |

Net unrealized depreciation of investments, call options written |

|

| (58,636,403 | ) |

Net Assets |

| $101,844,862 |

| |

Net Asset Value Per Share |

|

| $14.54 |

|

See accompanying Notes to Financial Statements | 8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 19

|

|

AGIC Global Equity & Convertible Income Fund | |

Year ended August 31, 2010 | |

|

|

|

|

|

|

|

|

|

|

Investment Income: |

|

|

|

|

Dividends (net of foreign withholding taxes of $83,076) |

|

| $2,816,820 |

|

Interest |

|

| 386,011 |

|

Other income |

|

| 91,251 |

|

Total Investment Income |

|

| 3,294,082 |

|

|

|

|

|

|

Expenses: |

|

|

|

|

Investment management fees |

|

| 1,085,135 |

|

Custodian and accounting agent fees |

|

| 99,516 |

|

Shareholder communications fees |

|

| 85,080 |

|

Audit and tax services |

|

| 54,642 |

|

Transfer agent fees |

|

| 32,816 |

|

New York Stock Exchange listing fees |

|

| 21,278 |

|

Legal fees |

|

| 12,118 |

|

Trustees’ fees and expenses |

|

| 10,170 |

|

Miscellaneous expenses |

|

| 6,919 |

|

Total Expenses |

|

| 1,407,674 |

|

|

|

|

|

|

Net Investment Income |

|

| 1,886,408 |

|

|

|

|

|

|

Realized and Change in Unrealized Gain (Loss): |

|

|

|

|

Net realized gain on: |

|

|

|

|

Investments |

|

| 3,850,291 |

|

Call options written |

|

| 651,753 |

|

Foreign currency transactions |

|

| 2,835 |

|

Net change in unrealized appreciation/depreciation of: |

|

|

|

|

Investments |

|

| 695,932 |

|

Call options written |

|

| 114,425 |

|

Foreign currency transactions |

|

| (3,735 | ) |

Net realized and change in unrealized gain on investments, |

|

| 5,311,501 |

|

Net Increase in Net Assets Resulting from Investment Operations |

|

| $7,197,909 |

|

20 AGIC Global Equity & Convertible Income Fund Annual Report | 8.31.10 | See accompanying Notes to Financial Statements

|

|

AGIC Global Equity & Convertible Income Fund |

|

|

|

|

|

|

|

|

|

|

| Year ended August 31, |

| |||||

|

| 2010 |

|

| 2009 |

| ||

|

|

|

|

|

|

|

|

|

Investment Operations: |

|

|

|

|

|

|

|

|

Net investment income |

| $ | 1,886,408 |

|

| $ | 3,129,043 |

|

Net realized gain on investments, call options written |

|

| 4,504,879 |

|

|

| 518,764 |

|

Net change in unrealized appreciation/depreciation of investments, |

|

| 806,622 |

|

|

| (21,046,022 | ) |

Net increase (decrease) in net assets resulting from investment operations |

|

| 7,197,909 |

|

|

| (17,398,215 | ) |

|

|

|

|

|

|

|

|

|

Dividends and Distributions to Shareholders from: |

|

|

|

|

|

|

|

|

Net investment income |

|

| (2,276,643 | ) |

|

| (3,854,964 | ) |

Net realized gains |

|

| (4,834,030 | ) |

|

| (3,826,551 | ) |

Return of capital |

|

| (1,294,354 | ) |

|

| (3,808,857 | ) |

Total dividends and distributions to shareholders |

|

| (8,405,027 | ) |

|

| (11,490,372 | ) |

Total decrease in net assets |

|

| (1,207,118 | ) |

|

| (28,888,587 | ) |

|

|

|

|

|

|

|

|

|

Net Assets: |

|

|

|

|

|

|

|

|

Beginning of year |

|

| 103,051,980 |

|

|

| 131,940,567 |

|

End of year (including dividends in excess of net investment income |

| $ | 101,844,862 |

|

| $ | 103,051,980 |

|

See accompanying Notes to Financial Statements | 8.31.10 | AGIC Global Equity & Convertible Income Fund Annual Report 21

|

|

AGIC Global Equity & Convertible Income Fund | |

August 31, 2010 | |

The Fund’s investment objective is to seek total return comprised of capital appreciation, current income and gains. Under normal market conditions the Fund pursues its investment objective by investing in a diversified, global portfolio of equity securities and income-producing convertible securities. The Fund also employ a strategy of writing (selling) call options on stocks held as well as on equity indexes in an attempt to generate gains from option premiums. There is no guarantee that the Fund will meet its stated objective.

The preparation of the financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts and disclosures in the Fund’s financial statements. Actual results could differ from these estimates.

In the normal course of business, the Fund enters into contracts that contain a variety of representations which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred.

The following is a summary of significant accounting policies consistently followed by the Fund: