UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

[Mark One]

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

| OR |

| | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13(a) OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

| | For the fiscal year ended: June 30, 2015 | Commission File Number: 001-33514 |

TRANSITION THERAPEUTICS INC.

(Exact name of Registrant as specified in its charter)

Ontario, Canada

(Jurisdiction of incorporation or organization)

101 College Street, Suite 220

Toronto, Ontario, Canada

M5G 1L7

(416) 260-7770

(Address and telephone number of Registrant’s principal executive offices)

Nicole Rusaw

Chief Financial Officer

101 College Street, Suite 220

Toronto, Ontario, Canada

M5G 1L7

(416) 260-7770 Tel.

(416) 260-2886 Fax

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of each exchange on which registered |

| Common Shares, no par value | | The NASDAQ Stock Market LLC |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: As of June 30, 2015: 38,878,879 shares of Common Shares were outstanding.

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.¨ Yesx No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.¨ Yesx No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.x Yes¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files).¨ Yes¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ¨ | International Financial Reporting Standards as issued by

the International Accounting Standards Board x | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.¨ Item 17¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).¨ Yesx No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST

FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by acourt.¨ Yes¨ No

Table of Contents

Introduction

In this annual report, where “we”, “us”, “our”, “Transition”, “Corporation” or the “Company” is used, it is referring to Transition Therapeutics Inc. and its wholly-owned subsidiaries, unless otherwise indicated. All amounts are in Canadian dollars, unless otherwise indicated.

Additional information relating to the Corporation, including the Corporation’s most recently filed Annual Information Form, can be found on SEDAR at www.sedar.com.

Presentation of Financial Information

Unless we indicate otherwise, financial information in this annual report has been prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board. IFRS differs in some respects from United States generally accepted accounting principles, or United States GAAP, and thus our financial statements may not be comparable to the financial statements of United States companies.

Percentages and some amounts in this annual report have been rounded for ease of presentation. Any discrepancies between totals and the sums of the amounts listed are due to rounding.

Currency Translation

We present our historical financial statements in Canadian dollars, which is the reporting currency of the Corporation. All figures reported in this annual report are in Canadian dollars, except where we indicate otherwise, and are referenced as “CAD$,” “$” and “dollars”. This annual report contains a translation of some Canadian dollar amounts into United States dollars at specified exchange rates solely for your convenience. See “Exchange Rate Data” below for certain information about the rates of exchange between Canadian dollars and United States dollars.

Exchange Rate Data

The following table sets forth, for each period indicated, the low and high exchange rates for Canadian dollars expressed in United States dollars and the average of such exchange rates on the last day of each month during such period, based on the inverse of the noon buying rate in the City of New York for cable transfers in Canadian dollars as certified for customs purposes by the Federal Reserve Bank of New York. The source of the exchange rate data is the H.10 statistical release of the Federal Reserve Board. The exchange rates set forth below demonstrate trends in exchange rates, but the actual exchange rates used throughout this Annual Report may vary.

| | | Exchange Rate | |

| | | High | | | Average (1) | | | Low | |

| | | (US$ per CAD$1.00) | |

| Last Five Fiscal Years | | | | | | | | | | | | |

| Fiscal Year Ended June 30, 2011 | | | 1.0542 | | | | 1.0013 | | | | 0.9392 | |

| Fiscal Year Ended June 30, 2012 | | | 1.0584 | | | | 0.9977 | | | | 0.9430 | |

| Fiscal Year Ended June 30, 2013 | | | 1.03 | | | | 0.9920 | | | | 0.9495 | |

| Fiscal Year Ended June 30, 2014 | | | 0.9769 | | | | 0.9336 | | | | 0.8888 | |

| Fiscal Year Ended June 30, 2015 | | | 0.9388 | | | | 0.8438 | | | | 0.7811 | |

| | | | | | | | | | | | | |

| Last Six Months | | | | | | | | | | | | |

| March 2015 | | | 0.8039 | | | | | | | | 0.7811 | |

| April 2015 | | | 0.8365 | | | | | | | | 0.7930 | |

| May 2015 | | | 0.8368 | | | | | | | | 0.8011 | |

| June 2015 | | | 0.8193 | | | | | | | | 0.7970 | |

| July 2015 | | | 0.7962 | | | | | | | | 0.7658 | |

| August 2015 | | | 0.7708 | | | | | | | | 0.7518 | |

Notes:

| (1) | For the years indicated, the average exchange rates are determined by averaging the exchange rates on the last business day of each month during the relevant period. |

Cautionary Statement Concerning Forward-Looking Statements

This annual report contains and incorporates by reference certain forward looking statements within the meaning of applicable securities laws. Forward-looking information typically contains statements with words such as “anticipate”, “believe”, “expect”, “plan”, “estimate”, “intend”, “may” or similar words suggesting future outcomes.

Forward-looking statements in this annual report include, but are not limited to statements with respect to: the clinical study phases of the Company’s product candidates which the Company expects to complete in fiscal 2016 and beyond; the ability of the Company’s business model to maximize shareholder returns; the potential for ELND005 to slow the progression of Alzheimer’s disease and improve symptoms; the potential for ELND005 to be effective for the treatment of agitation and or aggression in patients with Alzheimer’s disease; the potential for ELND005 to be effective for the treatment of Down syndrome; the timing and manner of future clinical development, if any, of ELND005; the global population size of those affected by Alzheimer’s disease; the demand for a product that can slow or reverse the progression of Alzheimer’s disease; the demand for a product that can reduce the emergence or severity of neuropsychiatric symptoms like depression, anxiety, agitation and aggression in Alzheimer’s disease; the potential clinical benefit of ELND005 in the treatment of other disease indications; the development of TT401 and the series of preclinical compounds in-licensed from Eli Lilly and Company (“Lilly”) and their potential benefit in type 2 diabetes patients and obese individuals; the timing and manner of future clinical development of TT401 performed by Lilly; TT701 development plans and timelines for individuals with androgen deficiency or other disease indications; the potential clinical benefit of TT701 to increase lean body mass, improve functional and sexual outcomes or improve other symptoms associated with androgen deficiency; the engagement of third party manufacturers to produce the Company’s drug substances and products; the potential future in-licensing of additional drug candidates to expand the development pipeline; the intention of the Company to make collaborative arrangements for the marketing and distribution of its products and the impact of human capital on the growth and success of the Company.

Some of the assumptions, risks and factors which could cause future outcomes to differ materially from those set forth in the forward-looking information include, but are not limited to: (i) the assumption that the Company will be able to obtain sufficient and suitable financing to support operations, clinical trials and commercialization of products, (ii) the risk that the Company may not be able to capitalize on partnering and acquisition opportunities, (iii) the assumption that the Company will obtain favourable clinical trial results in the expected timeframe, (iv) the assumption that the Company will be able to adequately protect proprietary information and technology from competitors, (v) the risks relating to the uncertainties of the regulatory approval process, (vi) the impact of competitive products and pricing and the assumption that the Company will be able to compete in the targeted markets, and (vii) the risk that the Company may be unable to retain key personnel or maintain third party relationships, including relationships with key collaborators.

By its nature, forward looking information involves numerous assumptions, inherent risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts, projections or other forward looking statements will not occur. Prospective investors should carefully consider the information contained under the heading “Risk Factors” and all other information included in or incorporated by reference in this annual report before making investment decisions with regard to the securities of the Corporation.

The section entitled “Risks Factors” discusses risks, uncertainties and factors that our management believes could cause actual results or events to differ materially from the forward-looking statements. Although we have attempted to identify important risks, uncertainties and other factors that could cause actual results or events to differ materially from those expressed or implied in the forward-looking information, there may be other factors that cause actual results or events to differ from those expressed or implied in the forward-looking information.

Forward-looking statements contained in this annual report are made as of the dates hereof, and such forward-looking statements are based on the beliefs, expectations and opinions of our management as of such date. We disclaim any obligation to update any forward-looking statements.

Part I

| Item 1. | Identity of Directors, Senior Management and Advisers |

Not applicable.

| Item 2. | Offer Statistics and Expected Timetable |

Not applicable.

| A. | Selected Financial Data |

The following information should be read in conjunction with the Corporation’s audited consolidated financial statements for the year ended June 30, 2015 and the related notes, which are prepared in accordance with IFRS. The selection of financial information includes financial information derived from the annual audited consolidated financial statements.

The following table is a summary of selected audited consolidated financial information of the Corporation for each of the five most recently completed financial years. The information presented is presented in accordance with IFRS:

| | | June 30, 2015 | | | June 30, 2014 | | | June 30, 2013 | | | June 30, 2012 | | | June 30, 2011 | |

| Revenue | | $ | — | | | $ | — | | | $ | 17,933,500 | | | $ | — | | | $ | 10,251,394 | |

| Net income (loss)(1) | | | (51,339,528 | ) | | | (21,782,255 | ) | | | 23,297 | | | | (12,269,846 | ) | | | (5,689,613 | ) |

| Basic and diluted net income ( loss) per share | | | (1.41 | ) | | | (0.72 | ) | | | 0.00 | | | | (0.48 | ) | | | (0.25 | ) |

| Total assets | | | 49,649,085 | | | | 68,907,236 | | | | 37,807,955 | | | | 37,093,030 | | | | 43,179,488 | |

| Total long-term liabilities | | | 3,503,344 | | | | 3,849,718 | | | | 1,457,821 | | | | 1,469,253 | | | | 1,480,685 | |

| Shareholders’ equity | | | 36,737,589 | | | | 59,094,260 | | | | 33,154,612 | | | | 32,123,489 | | | | 38,432,070 | |

| Common shares outstanding | | | 38,878,879 | | | | 35,303,913 | | | | 26,930,634 | | | | 26,921,302 | | | | 23,217,599 | |

| Cash dividends declared per share | | | — | | | | — | | | | — | | | | — | | | | — | |

Notes:

| (1) | Net income (loss) before discontinued operations and extraordinary items was equivalent to the net income (loss) for such periods. |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

Investing in our securities involves a high degree of risk. Before making an investment decision, you should carefully consider the following risk factors, in addition to the other information provided in this annual report and the Corporation’s other disclosure documents filed with the U.S. Securities and Exchange Commission onwww.sec.gov.

The Company will require significant additional financing and it may not have access to sufficient capital.

The Company anticipates that it will need additional financing in the future to fund its ongoing research and development programs and for general corporate requirements. The Company may choose to seek additional funding through public or private offerings, corporate collaborations or partnership arrangements. The amount of financing required will depend on many factors including the financial requirements of the Company to fund its research and clinical trials, and the ability of the Company to secure partnerships and achieve partnership milestones as well as to fund other working capital requirements. The Company’s ability to access the capital markets or to enlist partners is mainly dependent on the progress of its research and development and regulatory approval of its products. There is no assurance that additional funding will be available on acceptable terms, if at all.

The Company has a history of losses, and it has not generated any product revenue to date. It may never achieve or maintain profitability.

Since inception, the Company has incurred significant losses each year and expects to incur significant operating losses as the Company continues product research and development and clinical trials. There is no assurance that the Company will ever successfully commercialize or achieve revenues from sales of its therapeutic products if they are successfully developed or that profitability will ever be achieved or maintained. Even if profitability is achieved, the Company may not be able to sustain or increase profitability.

The Company is an early stage development company in an uncertain industry.

The Company is at an early stage of development. Preclinical and clinical trial work must be completed before our products could be ready for use within the markets we have identified. We may fail to develop any products, to obtain regulatory approvals, to enter clinical trials or to commercialize any products. The Company does not know whether any of our potential product development efforts will prove to be effective, meet applicable regulatory standards, obtain the requisite regulatory approvals or be capable of being manufactured at a reasonable cost. If the Company’s products are approved for sale, there can be no assurance that the products will gain market acceptance among consumers, physicians, patients and others in the medical community. A failure to gain market acceptance may adversely affect the revenues of the Company.

The Company is subject to a strict regulatory environment.

None of the Company’s product candidates have received regulatory approval for commercial sale.

Numerous statutes and regulations govern human testing and the manufacture and sale of human therapeutic products in Canada, the United States and other countries where the Company intends to market its products. Such legislation and regulation bears upon, among other things, the approval of protocols and human testing, the approval of manufacturing facilities, testing procedures and controlled research, review and approval of manufacturing, preclinical and clinical data prior to marketing approval including adherence to Good Manufacturing Practices (“GMP”) during production and storage as well as regulation of marketing activities including advertising and labelling.

The completion of the clinical testing of our product candidates and the obtaining of required approvals are expected to take years and require the expenditure of substantial resources. There can be no assurance that clinical trials will be completed successfully within any specified period of time, if at all. Furthermore, clinical trials may be delayed or suspended at any time by the Company or by regulatory authorities if it is determined at any time that patients may be or are being exposed to unacceptable health risks, including the risk of death, or that compounds are not manufactured under acceptable GMP conditions or with acceptable quality. Any failure or delay in obtaining regulatory approvals would adversely affect the Company’s ability to utilize its technology thereby adversely affecting operations. No assurance can be given that the Company’s product candidates or lead compounds will prove to be safe and effective in clinical trials or that they will receive the requisite protocol approval or regulatory approval. Furthermore, no assurance can be given that current regulations relating to regulatory approval will not change or become more stringent. There are no assurances the Company can scale-up, formulate or manufacture any compound in sufficient quantities with acceptable specifications for the regulatory agencies to grant approval or not require additional changes or additional trials be performed. The agencies may also require additional trials be run in order to provide additional information regarding the safety, efficacy or equivalency of any compound for which the Company seeks regulatory approval. Similar restrictions are imposed in foreign markets other than the United States and Canada. Investors should be aware of the risks, problems, delays, expenses and difficulties which may be encountered by the Company in light of the extensive regulatory environment in which the Company’s business operates.

Even if a product candidate is approved by the FDA or any other regulatory authority, the Company may not obtain approval for an indication whose market is large enough to recoup its investment in that product candidate. The Company may never obtain the required regulatory approvals for any of its product candidates.

The Company is faced with uncertainties related to its research.

The Company’s research programs are based on scientific hypotheses and experimental approaches that may not lead to desired results. In addition, the timeframe for obtaining proof of principle and other results may be considerably longer than originally anticipated, or may not be possible given time, resource, financial, strategic and collaborator scientific constraints. Success in one stage of testing is not necessarily an indication that the particular program will succeed in later stages of testing and development. It is not possible to predict, based upon studies in in-vitro models and in animals, whether any of the compounds made for these programs will prove to be safe, effective, and suitable for human use. Each compound will require additional research and development, scale-up, formulation and extensive clinical testing in humans. Decisions regarding future development activities may be based on results from completed studies or interim results from on-going studies or projections derived from interim or administrative analyses of studies not yet completed. Development of these compounds will require investigations into the mechanism of action of the molecules as these are not fully understood. Unsatisfactory results obtained from a particular study relating to a program may cause the Company to abandon its commitment to that program or to the lead compound or product candidate being tested. The discovery of unexpected toxicities, lack of sufficient efficacy, poor physiochemical properties, unacceptable ADME (absorption, distribution, metabolism and excretion) and DMPK (drug metabolism and pharmacokinetics), pharmacology, inability to increase scale of manufacture, market attractiveness, regulatory hurdles, competition, as well as other factors, may make the Company’s targets, lead compounds or product candidates unattractive or unsuitable for human use, and the Company may abandon its commitment to that program, target, lead compound or product candidate. In addition, preliminary results seen in animal and/or limited human testing may not be substantiated in larger controlled clinical trials.

If difficulties are encountered enrolling patients in the Company’s clinical trials, the Company’s trials could be delayed or otherwise adversely affected.

Clinical trials for the Company’s product candidates require that the Company identify and enroll a large number of patients with the disorder under investigation. The Company may not be able to enroll a sufficient number of patients to complete its clinical trials in a timely manner. Patient enrolment is a function of many factors including, but not limited to, design of the study protocol, size of the patient population, eligibility criteria for the study, the perceived risks and benefits of the therapy under study, the patient referral practices of physicians and the availability of clinical trial sites. If the Company has difficulty enrolling a sufficient number of patients to conduct the Company’s clinical trials as planned, it may need to delay or terminate ongoing clinical trials.

Even if regulatory approvals are obtained for the Company’s product candidates, the Company will be subject to ongoing government regulation.

Even if regulatory authorities approve any of the Company’s human therapeutic product candidates, the manufacture, marketing and sale of such products will be subject to strict and ongoing regulation. Compliance with such regulation may be expensive and consume substantial financial and management resources. If the Company, or any future marketing collaborators or contract manufacturers, fail to comply with applicable regulatory requirements, it may be subject to sanctions including fines, product recalls or seizures, injunctions, total or partial suspension of production, civil penalties, withdrawal of regulatory approvals and criminal prosecution. Any of these sanctions could delay or prevent the promotion, marketing or sale of the Company’s products.

The Company may not achieve its projected development goals in the time frames announced and expected.

The Company sets goals for and makes public statements regarding the timing of the accomplishment of objectives material to its success, such as the commencement and completion of clinical trials, anticipated regulatory submission and approval dates and time of product launch. The actual timing of these events can vary dramatically due to factors such as delays or failures in the Company’s clinical trials, the uncertainties inherent in the regulatory approval process and delays in achieving manufacturing or marketing arrangements sufficient to commercialize its products.

There can be no assurance that the Company’s clinical trials will be completed, that the Company will make regulatory submissions or receive regulatory approvals as planned. If the Company fails to achieve one or more of these milestones as planned, the price of the Common Shares would likely decline.

If the Company fails to obtain acceptable prices or adequate reimbursement for its human therapeutic products, its ability to generate revenues will be diminished.

The Company’s ability to successfully commercialize its human therapeutic products will depend significantly on its ability to obtain acceptable prices and the availability of reimbursement to the patient from third-party payers, such as government and private insurance plans. While the Company has not commenced discussions with any such parties, these third-party payers frequently require companies to provide predetermined discounts from list prices, and they are increasingly challenging the prices charged for pharmaceuticals and other medical products. The Company’s human therapeutic products may not be considered cost-effective, and reimbursement to the patient may not be available or sufficient to allow the Company to sell its products on a competitive basis. The Company may not be able to negotiate favourable reimbursement rates for its human therapeutic products.

In addition, the continuing efforts of third-party payers to contain or reduce the costs of healthcare through various means may limit the Company’s commercial opportunity and reduce any associated revenue and profits. The Company expects proposals to implement similar government control to continue. In addition, increasing emphasis on managed care will continue to put pressure on the pricing of pharmaceutical and biopharmaceutical products. Cost control initiatives could decrease the price that the Company or any current or potential collaborators could receive for any of its human therapeutic products and could adversely affect its profitability. In addition, in Canada and in many other countries, pricing and/or profitability of some or all prescription pharmaceuticals and biopharmaceuticals are subject to government control.

If the Company fails to obtain acceptable prices or an adequate level of reimbursement for its products, the sales of its products would be adversely affected or there may be no commercially viable market for its products.

The Company may not obtain adequate protection for its products through its intellectual property.

The Company’s success depends, in large part, on its ability to protect its competitive position through patents, trade secrets, trademarks and other intellectual property rights. The patent positions of pharmaceutical and biopharmaceutical firms, including the Company, are uncertain and involve complex questions of law and fact for which important legal issues remain unresolved. The patents issued or to be issued to the Company may not provide the Company with any competitive advantage. The Company’s patents may be challenged by third parties in patent litigation, which is becoming widespread in the biopharmaceutical industry. In addition, it is possible that third parties with products that are very similar to the Company’s will circumvent its patents by means of alternate designs or processes. The Company may have to rely on method of use protection for its compounds in development and any resulting products, which may not confer the same protection as compounds per se. The Company may be required to disclaim part of the term of certain patents. There may be prior applications of which the Company is not aware that may affect the validity or enforceability of a patent claim. There also may be prior applications which are not viewed by the Company as affecting the validity or enforceability of a claim, but which may, nonetheless ultimately be found to affect the validity or enforceability of a claim. No assurance can be given that the Company’s patents would, if challenged, be held by a court to be valid or enforceable or that a competitor’s technology or product would be found by a court to infringe the Company’s patents. Applications for patents and trademarks in Canada, the United States and in foreign markets have been filed and are being actively pursued by the Company. Pending patent applications may not result in the issuance of patents, and the Company may not develop additional proprietary products which are patentable.

Patent applications relating to or affecting the Company’s business have been filed by a number of pharmaceutical and biopharmaceutical companies and academic institutions. A number of the technologies in these applications or patents may conflict with the Company’s technologies, patents or patent applications, and such conflict could reduce the scope of patent protection which the Company could otherwise obtain. The Company could become involved in interference proceedings in the United States in connection with one or more of its patents or patent applications to determine priority of invention. The Company’s granted patents could also be challenged and revoked in opposition proceedings in certain countries outside the United States.

In addition to patents, the Company relies on trade secrets and proprietary know-how to protect its intellectual property. The Company generally requires its employees, consultants, outside scientific collaborators and sponsored researchers and other advisors to enter into confidentiality agreements. These agreements provide that all confidential information developed or made known to the individual during the course of the individual’s relationship with the Company is to be kept confidential and not disclosed to third parties except in specific circumstances. In the case of the Company’s employees, the agreements provide that all of the technology which is conceived by the individual during the course of employment is the Company’s exclusive property. These agreements may not provide meaningful protection or adequate remedies in the event of unauthorized use or disclosure of the Company’s proprietary information. In addition, it is possible that third parties could independently develop proprietary information and techniques substantially similar to those of the Company or otherwise gain access to the Company’s trade secrets.

The Company currently has the right to use certain technology under license agreements with third parties. The Company’s failure to comply with the requirements of material license agreements could result in the termination of such agreements, which could cause the Company to terminate the related development program and cause a complete loss of its investment in that program.

As a result of the foregoing factors, the Company may not be able to rely on its intellectual property to protect its products in the marketplace.

The Company may infringe the intellectual property rights of others.

The Company’s commercial success depends significantly on its ability to operate without infringing the patents and other intellectual property rights of third parties. There could be issued patents of which the Company is not aware that its products infringe or patents, that the Company believes it does not infringe, but that it may ultimately be found to infringe. Moreover, patent applications are in some cases maintained in secrecy until patents are issued. The publication of discoveries in the scientific or patent literature frequently occurs substantially later than the date on which the underlying discoveries were made and patent applications were filed. Because patents can take many years to issue, there may be currently pending applications of which the Company is unaware that may later result in issued patents that its products infringe.

The biopharmaceutical industry has produced a proliferation of patents, and it is not always clear to industry participants, including the Company, which patents cover various types of products. The coverage of patents is subject to interpretation by the courts, and the interpretation is not always uniform. The Company is aware of, and has reviewed, third party patents relating to the treatment of Alzheimer’s disease, diabetes and other relevant indication areas. In the event of infringement or violation of another party’s patent, the Company may not be able to enter into licensing arrangements or make other arrangements at a reasonable cost. Any inability to secure licenses or alternative technology could result in delays in the introduction of the Company’s products or lead to prohibition of the manufacture or sale of the products.

Patent litigation is costly and time consuming and may subject the Company to liabilities.

The Company’s involvement in any patent litigation, interference, opposition or other administrative proceedings will likely cause the Company to incur substantial expenses, and the efforts of its technical and management personnel will be significantly diverted. In addition, an adverse determination in litigation could subject the Company to significant liabilities.

The Company operates in a fiercely competitive business environment.

The biopharmaceutical industry is highly competitive. Competition comes from healthcare companies, pharmaceutical companies, large and small biotech companies, specialty pharmaceutical companies, universities, government agencies and other public and private companies. Research and development by others may render the Company’s technology or products non-competitive or obsolete or may result in the production of treatments or cures superior to any therapy the Company is developing or will develop. In addition, failure, unacceptable toxicity, lack of sales or disappointing sales or other issues regarding competitors’ products or processes could have a material adverse effect on the Company’s product candidates, including its clinical candidates or its lead compounds.

The market price of the Company’s Common Shares may experience a high level of volatility due to factors such as the volatility in the market for biotechnology stocks generally, and the short-term effect of a number of possible events.

The Company is a public growth company in the biotechnology sector. As frequently occurs among these companies, the market price for the Company’s Common Shares may experience a high level of volatility. For example, in the last year, the Company’s stock price has ranged from a low of US$1.77 to a high of US$9.30. Numerous factors, including many over which the Company has no control, may have a significant impact on the market price of Common Shares including, among other things, (i) clinical and regulatory developments regarding the Company’s products and product candidates and those of its competitors, (ii) arrangements or strategic partnerships by the Company, (iii) other announcements by the Company or its competitors regarding technological, product development, sales or other matters, (iv) patent or other intellectual property achievements or adverse developments, (v) arrivals or departures of key personnel; (vi) government regulatory action affecting the Company’s product candidates in the United States, Canada and foreign countries, (vii) actual or anticipated fluctuations in the Company’s revenues or expenses, (viii) general market conditions and fluctuations for the emerging growth and biopharmaceutical market sectors, (ix) reports of securities analysts regarding the expected performance of the Company, and (x) events related to threatened, new or existing litigation. Listing on NASDAQ and the TSX may increase share price volatility due to various factors including, (i) different ability to buy or sell the Company’s Common Shares, (ii) different market conditions in different capital markets; and (iii) different trading volume.

In addition, the stock market in recent years has experienced extreme price and trading volume fluctuations that often have been unrelated or disproportionate to the operating performance of individual companies. These broad market fluctuations may adversely affect the price of Common Shares, regardless of the Company’s operating performance. In addition, sales of substantial amounts of Common Shares in the public market after any offering, or the perception that those sales may occur, could cause the market price of Common Shares to decline.

Furthermore, shareholders may initiate securities class action lawsuits if the market price of the Company’s stock drops significantly, which may cause the Company to incur substantial costs and could divert the time and attention of its management.

The Company is highly dependent on third parties.

The Company is or may in the future be dependent on third parties for certain raw materials, product manufacture, marketing and distribution and, like other biotechnology and pharmaceutical companies, upon medical institutions to conduct clinical testing of its potential products. Although the Company does not anticipate any difficulty in obtaining any such materials and services, no assurance can be given that the Company will be able to obtain such materials and services.

The Company is subject to intense competition for its skilled personnel, and the loss of key personnel or the inability to attract additional personnel could impair its ability to conduct its operations.

The Company is highly dependent on its management and its clinical, regulatory and scientific staff, the loss of whose services might adversely impact its ability to achieve its objectives. Recruiting and retaining qualified management and clinical, scientific and regulatory personnel is critical to the Company’s success. Competition for skilled personnel is intense, and the Company’s ability to attract and retain qualified personnel may be affected by such competition.

The Company’s business involves the use of hazardous materials which requires the Company to comply with environmental regulation.

The Company’s discovery and development processes involve the controlled use of hazardous materials. The Company is subject to federal, provincial and local laws and regulations governing the use, manufacture, storage, handling and disposal of such materials and certain waste products. The risk of accidental contamination or injury from these materials cannot be completely eliminated. In the event of such an accident, the Company could be held liable for any damages that result, and any such liability could exceed the Company’s resources. The Company may not be adequately insured against this type of liability. The Company may be required to incur significant costs to comply with environmental laws and regulations in the future, and its operations, business or assets may be materially adversely affected by current or future environmental laws or regulations.

Legislative actions, potential new accounting pronouncements and higher insurance costs are likely to impact the Company’s future financial position or results of operations.

Compliance with changing regulations regarding corporate governance and public disclosure, notably with respect to internal controls over financial reporting, may result in additional expenses. Changing laws, regulations and standards relating to corporate governance and public disclosure are creating uncertainty for companies such as ours, and insurance costs are increasing as a result of this uncertainty.

Future healthcare reforms may produce adverse consequences.

Healthcare reform and controls on healthcare spending may limit the price the Company can charge for any products and the amounts thereof that it can sell. In particular, in the United States, the federal government and private insurers have considered ways to change, and have changed, the manner in which healthcare services are provided. Potential approaches and changes in recent years include controls on healthcare spending and the creation of large purchasing groups. In the future, the U.S. government may institute further controls and different reimbursement schemes and limits on Medicare and Medicaid spending or reimbursement. These controls, reimbursement schemes and limits might affect the payments the Company could collect from sales of any of its products in the United States. Uncertainties regarding future health care reform and private market practices could adversely affect the Company’s ability to sell any products profitably in the United States. Election of new or different political or government officials in large market countries could lead to dramatic changes in pricing, regulatory approval legislation and reimbursement which could have material impact on product approvals and commercialization.

The Company faces an unproven market for its future products.

The Company believes that there will be many different applications for products successfully derived from its technologies and that the anticipated market for products under development will continue to expand. No assurance, however, can be given that these beliefs will prove to be correct due to competition from existing or new products and the yet to be established commercial viability of the Company’s products. Physicians, patients, formularies, third party payers or the medical community in general may not accept or utilize any products that the Company or its collaborative partners may develop.

The Company may be faced with future lawsuits related to secondary market liability.

Securities legislation in Canada has recently changed to make it easier for shareholders to sue. These changes could lead to frivolous law suits which could take substantial time, money, resources and attention or force the Company to settle such claims rather than seek adequate judicial remedy or dismissal of such claims.

The Company may encounter unforeseen emergency situations and information technology breaches.

Despite the implementation of security measures, any of the Company’s, its collaborators’ or its third party service providers’ internal computer systems are vulnerable to damage from computer viruses, unauthorized access, natural disasters, terrorism, war and telecommunication and electrical failure. Any resulting system failure, accident or security breach could result in a material disruption of the Company’s operations. Likewise, data privacy or security breaches by employees and others with permitted access to our systems, including in some cases third-party service providers to which we may outsource certain business functions, may pose a risk that sensitive data, including intellectual property or personal information, may be exposed to unauthorized persons or to the public. While we have invested in the protection of data and information technology, there can be no assurance that our efforts will prevent service interruptions, or identify breaches in our systems, that could adversely affect our business and/or result in the loss of critical or sensitive information, which could result in financial, legal, business or reputational harm to us.

The Company’s technologies may become obsolete.

The pharmaceutical industry is characterized by rapidly changing markets, technology, emerging industry standards and frequent introduction of new products. The introduction of new products embodying new technologies, including new manufacturing processes, and the emergence of new industry standards may render the Company’s technologies obsolete, less competitive or less marketable.

Our product candidates may cause undesirable serious adverse events during clinical trials that could delay or prevent their regulatory authorization, approval or other permission to conduct further testing or commence commercialization.

Our product candidates in clinical development, including ELND005 can potentially cause adverse events. In 2010, together with our collaborator, Elan, we completed a Phase 2 study that evaluated three dose groups of ELND005 and a placebo group in mild to moderate Alzheimer’s disease patients. The study included four treatment arms: placebo, 250mg bid, 1000mg bid and 2000mg bid. The two high dose ELND005 groups were electively discontinued in 2009 by the companies due to an observed imbalance of serious adverse events, including deaths. No causal relationship could be determined between these higher doses and the events.

Of the 351 subjects who received study drug, a total of 171 subjects received either 250mg bid or placebo, the rest were in the two discontinued high dose groups. The overall incidence of adverse events in the 250mg bid and placebo groups was 87.5% versus 91.6%; and the incidence of withdrawals due to adverse events was 10.2% versus 9.6%, respectively. The incidence of serious adverse events in the 250mg bid and placebo groups was 21.6% versus 13.3%, but the incidence of serious adverse events that were considered drug related was 2.3% and 2.4%, respectively. The total number of deaths in the study was five and four in the 1000mg bid and 2000mg bid dose groups versus one and zero in the 250mg bid and placebo groups, respectively. These deaths occurred between August 2008 and November 2009. The study’s independent safety monitoring committee reviewed the final safety results and continued to conclude that a causal relationship between the deaths and drug could not be determined.

The most common adverse events in the 250mg bid group that were >5% in incidence and double the placebo rate were: falls (12.5% vs. placebo 6%), depression (11.4% vs. placebo 4.8%), and confusional state (8% vs. placebo 3.6%). Because our product candidates have been tested in relatively small patient populations and for limited durations, additional adverse events may be observed as their development progresses.

Adverse events caused by any of our product candidates could cause us or regulatory authorities to interrupt, delay or halt clinical trials and could result in the denial of regulatory approval by the FDA or other non-U.S. regulatory authorities for any or all targeted indications. This, in turn, could prevent the commercialization of our product candidates and the generation of revenues from their sale. In addition, if our product candidates receive authorization, marketing approval or other permission and we or others later identify adverse events caused by the product, the material adverse consequences that may arise, include, but are not limited to:

| • | regulatory authorities may withdraw their authorization, approval, or other permission to test or market the candidate product; |

| • | we may be required to recall the product, change the way the product is administered, conduct additional clinical trials or change the labeling of the product; |

| • | a product may become less competitive and product sales may decrease; or |

| • | our reputation may suffer. |

Any one or a combination of these events could prevent us from achieving or maintaining market acceptance or could substantially increase the costs and expenses of commercializing the product candidate, which in turn could delay or prevent us from generating significant revenues from the sale of such products.

The Company may be subject to costly product liability claims and may not have adequate insurance.

The conduct of clinical trials in humans involves the potential risk that the use of our product candidates will result in adverse effects. The Company currently maintains product liability insurance for their clinical trials; however, such liability insurance may not be adequate to fully cover any liabilities that arise from clinical trials of our product candidates. The Company may not have sufficient resources to pay for any liabilities resulting from a claim excluded from, or beyond the limit of, our insurance coverage.

Clinical Study Results from our product candidates may not support further clinical development.

The clinical studies performed to evaluate the safety, tolerability and efficacy of our product candidates, including ELND005, can yield study results that may or may not support further clinical development. In June 2015, the Company announced that a Phase 2/3 study of neuropsychiatric drug candidate ELND005 did not meet its primary efficacy endpoint. In the study, both the treatment and placebo groups showed a significant, but similar, reduction in agitation and aggression relative to baseline. There was a greater than expected reduction in agitation and aggression observed in the placebo group as measured in weeks 4, 8 and 12 in the study. The safety and tolerability profile of ELND005 was consistent with previous studies in AD at the 250mg bid dose. The Phase 2/3 clinical study evaluated the efficacy, safety and tolerability of ELND005 over 12 weeks of treatment in patients with mild to severe AD, who were experiencing at least moderate levels of agitation/aggression. The randomized, double-blind, placebo-controlled study enrolled 350 AD patients (175 subjects per study arm). The primary efficacy endpoint of the study was the change from baseline in the Neuropsychiatric Inventory – Clinician (“NPI-C”) scale of agitation and aggression. An analysis of the full study dataset is being performed. A group of expert external clinical advisors is being consulted to determine any future development of ELND005. The results of this data analysis and clinical advisory interaction may or may not support the further development of ELND005. Future development may include evaluating ELND005 as a treatment of neuropsychiatric symptoms such as agitation and aggression in Alzheimer’s disease patients or potentially narrower patient populations or other disease indications. Any ELND005 development plan will be strategically focused to advance the drug candidate in the targeted patient population and therefore may differ from previously proposed development plans. Further, interactions with regulatory authorities including the FDA may or may not support proposed ELND005 clinical plans. Regulatory interactions may also result in modifications to the ELND005 development plan potentially increasing the time and cost of clinical development activities.

U.S. holders of our Common Shares may suffer adverse tax consequences if we are characterized as a Passive Foreign Investment Company (“PFIC”).

There is a risk that we will be classified as a PFIC for U.S. federal income tax purposes. Our status as a PFIC could result in a reduction in the after-tax return to U.S. Holders of our Common Shares and may cause a reduction in the value of such shares. We will be classified as a PFIC for any taxable year in which (i) at least 75% of our gross income is passive income or (ii) at least 50% of the average value of all of our assets produce or are held for the production of passive income. For this purpose, passive income includes dividends, interest, and royalties and rents that are not derived in the active conduct of a trade or business, as well as gains from the sale of assets that produce passive income. Based on the composition of our income and valuation of our assets, we do not believe we were a PFIC for the taxable year ended June 30, 2015. However, there is no assurance that we will not be classified as a PFIC in subsequent taxable years. If we are classified as a PFIC, U.S. Holders of our common shares could be subject to greater U.S. income tax liability than might otherwise apply, imposition of U.S. income tax in advance of when tax would otherwise apply, and detailed tax filing requirements that would not otherwise apply. Subject to certain exceptions, once a U.S. Holder’s shares are treated as shares in a PFIC, they remain shares in a PFIC. Dividends received by a U.S. Holder from a PFIC will not constitute qualified dividend income qualifying for lower tax rates. The PFIC rules are complex and U.S. Holders of our common shares are urged to consult their own tax advisors regarding the possible application of the PFIC rules to them in their particular circumstances. See “Taxation—United States Federal Income Taxation.”

| Item 4. | Information on the Corporation |

Name, Address and Incorporation

Transition Therapeutics Inc. was incorporated pursuant to the Business Corporations Act (Ontario) on July 6, 1998 as “Transition Therapeutics and Diagnostics Inc.” The Corporation filed articles of amendment on October 12, 2000 and on October 19, 2000 to create a class of non-voting shares (the “Class B Shares”) and to amend certain attributes of its Common Shares. On November 2, 2000, the Corporation filed articles of amendment to delete its private company restrictions. On December 14, 2000, the Corporation filed articles of amendment to change its name to “Transition Therapeutics Inc.” and effect a split of its issued and outstanding Common Shares on the basis of 3.25649 Common Shares for each previously issued and outstanding Common Share. On December 14, 2004, the Corporation filed articles of amendment to eliminate the Class B Shares from its authorized capital. In July 2007, the Corporation completed the consolidation of its issued and outstanding Common Shares on the basis of one (1) post-consolidation Common Share for every nine (9) pre-consolidation Common Shares.

The Corporation’s principal and registered office is located at 101 College Street, Suite 220, Toronto, Ontario, Canada, M5G 1L7, and its telephone number is (416) 260-7770. The Corporation’s agent for service of process in the United States is CT Corporation System located at 111 Eighth Avenue, New York, NY 10011.

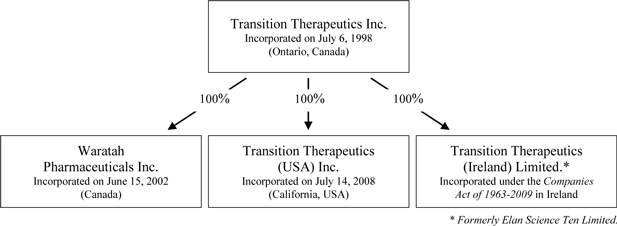

Intercorporate Relationships

The Corporation has three wholly-owned material subsidiaries: Waratah Pharmaceuticals Inc. (“Waratah”), which is incorporated under the Canada Business Corporations Act, Transition Therapeutics Ireland Limited (“Transition Ireland”) (formerly Elan Science Ten Limited) which is incorporated under the Companies Acts of 1963 to 2009 in Dublin, Ireland and Transition Therapeutics (USA) Inc. (“Transition USA”), which is incorporated under the laws of the State of California.

The chart below illustrates the corporate structure:

General Development of the Business

Three Year History

On August 30, 2012, the Corporation announced that Elan Pharma International Limited (“Elan”) had dosed the first patient in a Phase 2 clinical study of ELND005 in bipolar disorder. The study is a placebo-controlled, safety and efficacy study of oral ELND005 as an adjunctive maintenance treatment in patients with Bipolar 1 Disorder to delay the time to occurrence of mood episodes. As the first patient has been dosed in the study, the Corporation received a milestone payment of US$11 million from Elan.

On November 28, 2012, Transition announced that Elan had enrolled the first patient in a Phase 2 study of ELND005 for the treatment of agitation/aggression in patients with moderate to severe Alzheimer's disease.

On April 30, 2013, Transition announced the results of a five-week proof of concept clinical study of TT401 in type 2 diabetic and obese non-diabetic subjects. In the study, TT401, a once-weekly administered peptide, demonstrated significant improvements in glycemic control and reductions in body weight.

On June 17, 2013, Transition announced that Eli Lilly and Company (“Lilly”) had exercised its option to assume all development and commercialization rights to type 2 diabetes drug candidate TT401. In conjunction with this assumption of rights, Transition received a US$7 million milestone payment from Lilly.

On July 17, 2013, Transition announced that the US Food and Drug Administration (“FDA”) has granted Fast Track Designation to the development program for ELND005 which was submitted for the treatment of Neuropsychiatric Symptoms (“NPS”) in Alzheimer's disease (“AD”). The FDA concluded that the development program for ELND005 for the treatment of NPS in AD meets their criteria for Fast Track Designation.

On July 23, 2013, Transition announced the exclusive licensing of worldwide rights to a novel small molecule transcriptional regulator ("TT601") from Lilly for the treatment of osteoarthritis ("OA") pain.

On August 15, 2013, the Corporation announced the closing of its private placement financing issuing 2,625,300 units of the Corporation to certain existing shareholders, board members and management at a price of US$4.19 per unit, raising gross proceeds of US$11.0 million. Each unit consists of (i) one common share, (ii) 0.325 Common Share purchase warrant with a purchase price of US$4.60 per whole warrant and (iii) 0.4 Common Share purchase warrant with a purchase price of US$6.50 per whole warrant. Each whole warrant will entitle the holder, within two years of the closing date, to purchase one additional common share in the capital of the Corporation. If and when all of the warrants are exercised, the Corporation may realize up to an additional US$10.7 million in proceeds.

On September 4, 2013, Transition announced the first patient was dosed in a Phase 2a study of ELND005 in Down syndrome. Study ELND005-DS201 will evaluate the safety and pharmacokinetics of two doses of ELND005 and placebo in young adults with Down syndrome without dementia, and will also include select cognitive and behavioural measures.

On December 18, 2013 Perrigo Company plc “(Perrigo”) completed its acquisition of Elan Company plc and all of its subsidiaries. With this acquisition, Perrigo acquired all of the rights and obligations of Elan under the collaboration agreement (“ELND005 Agreement”) between Waratah, a wholly-owned subsidiary of the Corporation, and Elan for the development and commercialization of ELND005.

On February 28, 2014 Transition announced the acquisition of an Irish domiciled company, the holder of all the development and commercialization rights of neuropsychiatric drug candidate, ELND005. Going forward, Transition’s wholly owned subsidiary, Transition Therapeutics Ireland Limited, will be responsible for all future development and commercialization activities of the ELND005 drug candidate. In parallel with this acquisition, Perrigo has invested US$15 million and received 2,255,640 Transition common shares representing approximately a 7% ownership stake in Transition. Perrigo will also be eligible to receive up to US$40 million in approval and commercial milestone payments and a 6.5% royalty on net sales of ELND005 products and sublicense fees received. As a result of the transaction, Perrigo transferred its rights under the ELND005 Agreement to Transition Ireland.

On April 7, 2014, Transition provided a clinical development update and announced the decision to focus ELND005 development on the completion of current Phase 2 clinical studies in Agitation and Aggression in Alzheimer’s disease and a Phase 2a study in Down syndrome. A decision was also made to discontinue the clinical study of bipolar subjects following a commercial assessment of the size and length of the bipolar study, and costs and timelines for its completion. This decision was not based on any analysis of efficacy data and there were no adverse safety findings that contributed to this decision. Transition also announced that a Phase 2 study of TT401 is in the final preparation stage with dosing expected to commence in calendar Q2 2014 and that there would be no further development of osteoarthritis preclinical candidate, TT601. This decision was made after expanded toxicology study data and regulatory interactions revealed the development plan for TT601 would be restricted and timelines delayed.

On May 15, 2014, Transition announced the dosing of the first patient in a Phase 2 clinical study of TT401 (LY2944876), a drug candidate for the treatment of type 2 diabetes. The study is expected to enroll up to 375 type 2 diabetes subjects and will be performed by Transition's development partner, Lilly. The objectives of the study will be to evaluate the safety and effectiveness of TT401 compared to once-weekly exenatide extended release and placebo.

On June 23, 2014, the Corporation announced the closing of its private placement financing through which 3,195,487 units of the Corporation were purchased by certain existing shareholders, board members and management of the Corporation at a price of US$5.32 per unit for gross proceeds of $18,319,000 (US$17.0 million). Each unit consisted of one common share and 0.61 Common Share purchase warrant with a purchase price of US$7.10 per whole warrant. Each whole warrant will entitle the holder, within two years of the closing date, to purchase one additional common share in the capital of the Corporation. If and when all of the warrants are exercised, the Corporation will realize an additional US$13.8 million in proceeds.

On July 11, 2014, the Corporation announced that Carl Damiani has been appointed Chief Operating Officer of Transition.

On November 4, 2014, Transition announced findings from a Phase 2 study of neuropsychiatric drug candidate, ELND005, as an adjunctive maintenance treatment for bipolar disorder type I patients (BPD). Overall, ELND005 had an acceptable safety and tolerability profile in the study, and showed numerical differences in the number of mood event recurrences favoring ELND005.

On November 20, 2014, the Corporation announced the results of a clinical study of neuropsychiatric drug candidate ELND005 in young adults with Down syndrome. TTIL completed this first study in Down syndrome subjects without dementia to allow optimal dose selection for future larger studies. The study enrolled 23 Down syndrome subjects in three study arms over a four-week treatment period. At the doses evaluated, ELND005 was determined to have an acceptable safety and tolerability profile and there were no serious adverse events reported.

On November 24, 2014, Transition announced results from a thorough QT (tQT) study in which no QT effects were observed at supra-therapeutic single doses of neuropsychiatric drug candidate, ELND005. A tQT study is a specialized clinical trial required by the FDA for the approval of most drugs in development. From a safety perspective, drugs that have no QT prolongation effects are particularly desirable for administration to an elderly Alzheimer’s disease (“AD”) population.

In December, 2014, TT401 diabetes drug candidate development partner Lilly informed Transition that the 70% patient enrollment milestone had been achieved triggering the payment of the third and final milestone payment which in aggregate totalled US$14 million. The Corporation has no additional funding obligations related to this Phase 2 clinical study.

On February 18, 2015, the Corporation announced the closing of a public offering of US$23 million of common shares equivalent to an aggregate of 3,538,461 common shares at a price to the public of US$6.50 per share, including 461,538 common shares issued upon the exercise of the underwriters’ over-allotment option. Cowen and Company, LLC was the sole book-running manager and Canaccord Genuity Inc., H.C. Wainwright & Co., LLC, and LifeSci Capital LLC were the co-managers for the offering.

In February, 2015, development partner Lilly informed Transition that 420 type 2 diabetic subjects have been enrolled in the current Phase 2 study thereby completing the enrollment phase of the study.

On March 2, 2015, the Corporation announced that its wholly owned subsidiary, Transition Ireland completed enrolment of 350 patients in the Phase 2 clinical study evaluating neuropsychiatric drug candidate ELND005 as a treatment for agitation and aggression in patients with Alzheimer’s disease (“AD”). The objectives of the Phase 2 clinical study (“Harmony AD Study”) are to evaluate the efficacy, safety and tolerability of ELND005 over 12 weeks of treatment in patients with mild to severe AD, who are experiencing at least moderate levels of agitation/aggression.

On March 26, 2015, Transition announced results from two phase 1 clinical studies of neuropsychiatric drug candidate ELND005. These studies, an absorption-metabolism-excretion (“AME”) study and a renal clearance study, are specialized clinical pharmacology trials that are required by the United States Food and Drug Administration (“FDA”) for the approval of most drugs in development.

On May 6, 2015, the Corporation announced its wholly-owned subsidiary, Transition Ireland has exclusively licensed worldwide rights to a novel small molecule drug candidate (“TT701”) from Lilly.

On June 16, 2015, Transition announced that Carl Damiani has been appointed as President and Chief Operating Officer of Transition.

On June 24, 2015, the Corporation announced results of Clinical Study of ELND005 in Agitation and Aggression in Patients with Alzheimer’s Disease. The Phase 2/3 clinical study of neuropsychiatric drug candidate ELND005 did not meet its primary efficacy endpoint. In the study, both the treatment and placebo groups showed a significant, but similar, reduction in agitation and aggression relative to baseline. There was a greater than expected reduction in agitation and aggression observed in the placebo group as measured in weeks 4, 8 and 12 in the study. The safety and tolerability profile of ELND005 was consistent with previous studies in Alzheimer’s disease at the 250mg bid dose.

Business of the Corporation

Market sizes appearing in this annual report are estimates of potential markets only. The Corporation makes no claim that such figures represent sales figures actually anticipated should the Corporation successfully develop and receive approval for any of its product candidates.

General

The Corporation’s principal business activity is the researching and developing of therapeutic agents.

The Corporation has two entities (Transition Ireland and Waratah) that are developing novel pharmaceuticals for disease indications with large markets. The Corporation’s other two entities, (Transition Therapeutics Inc. and Transition Therapeutics USA) provide development services to support the clinical and non-clinical activities of Transition Ireland and Waratah. The Corporation’s entities each perform different activities and have different business models.

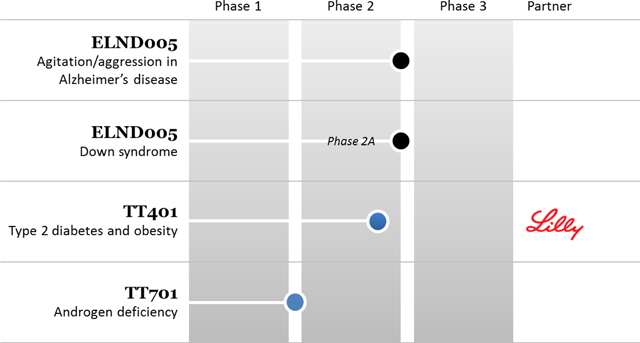

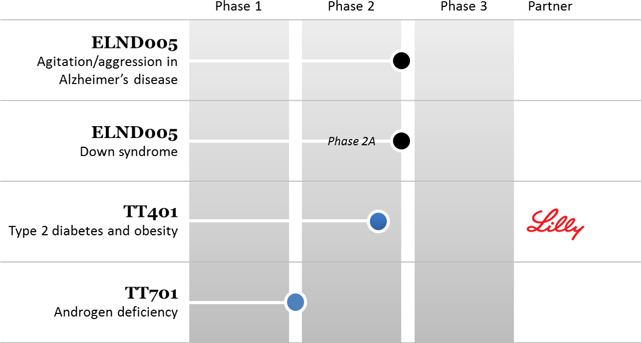

Transition Ireland is developing two drug candidates; neuropsychiatric candidate ELND005 and androgen deficiency candidate TT701. In the recently completed Phase 2/3 study in Alzheimer’s disease patients, ELND005 did not meet the study’s primary efficacy endpoint. Transition Ireland is currently conducting a thorough review of all data from the studies with external clinical advisors to determine the potential future development path for this asset. Transition Ireland is also developing TT701 toward a Phase 2 clinical study expected to commence in fiscal 2016. TT701 is a selective androgen receptor modulator (“SARM”) that has been shown in a Phase 2 study to significantly increase lean body mass and a measurement of muscle strength in male subjects.

Waratah’s lead development asset is diabetes drug candidate TT401. Currently, Waratah’s development partner Lilly, is performing a 420 patient, Phase 2 clinical study of TT401 in type 2 diabetes individuals.

Transition Therapeutics Inc. and Transition USA provide development services in support of the clinical and non-clinical activities of Transition Ireland and Waratah. The Corporation operates in one operating segment, the research and development of therapeutic agents.

The Corporation’s strategic focus is on building shareholder value. To effectively achieve this, the Corporation has established a core business model based on the following steps: 1) identifying attractive early stage technologies targeting large markets; 2) moving these products through the clinic to provide validation; 3) considering additional product opportunities; 4) identifying partners with the infrastructure and resources to complete late stage clinical development and product commercialization; and 5) identifying new product opportunities to expand the Corporation’s product pipeline.

In addition to this business model, Transition Ireland has a separate and distinct business. Transition Ireland acquired the development and commercialization rights to the late stage neuropsychiatric asset, ELND005. Transition Ireland’s business model is to perform later stage clinical development, including late stage Phase 2 and Phase 3 clinical studies for this asset and potentially other drug candidates, including TT701 which was acquired from Lilly in May, 2015. Transition Ireland has contracted development services from contract research organizations, Transition Therapeutics Inc., Transition Therapeutics USA and third parties to perform the development activities of ELND005. The development of un-partnered assets, such as ELND005, will allow Transition Ireland to access the economics associated with advancing assets to regulatory approval.

Technology

The Corporation’s technologies in development are as follows: (i) Transition Ireland is developing ELND005 for the treatment of Alzheimer’s disease and Down syndrome as well as TT701 for the treatment of androgen deficiencies and (ii) Waratah is developing TT401for the treatment of diabetes.

ELND005 for Alzheimer`s Disease

The Corporation’s subsidiary, Transition Ireland, is developing small molecule therapeutics that act by preventing the formation of and breaking down amyloid beta peptide aggregates. The accumulation of amyloid beta has been connected to several diseases including Alzheimer’s disease, AA Amyloidosis and others.

The Product

ELND005, scyllo-inositol, is an orally bioavailable small molecule that is being investigated for neuropsychiatric indications on the basis of its proposed dual mechanism of action, which includes β-amyloid anti-aggregation and regulation of brain myo-inositol levels. An extensive clinical program of Phase 1 and Phase 2 studies have been completed with ELND005. The Phase 2 study (ELND005-AD201) which evaluated ELND005 in more than 350 mild to moderate AD patients was published in the peer-reviewed journal,Neurology. TheNeurology article was entitled “A Phase 2 randomized trial of ELND005, scyllo-inositol, in mild-moderate Alzheimer’s disease”.

On July 17, 2013, the FDA granted Fast Track Designation to the development program for ELND005 which was submitted for the treatment of Neuropsychiatric Symptoms (“NPS”) in Alzheimer's disease. The FDA concluded that the development program for ELND005 for the treatment of NPS in AD meets their criteria for Fast Track Designation.

On June 24, 2015, the Corporation reported that a Phase 2/3 study of ELND005 in Alzheimer’s disease patients with at least moderate levels of agitation/aggression did not meet its primary endpoint. In the study, both the treatment and placebo groups showed a significant, but similar, reduction in agitation and aggression relative to baseline. There was a greater than expected reduction in agitation and aggression observed in the placebo group as measured in weeks 4, 8 and 12 in the study. The safety and tolerability profile of ELND005 was consistent with previous studies in AD at the 250mg bid dose. The Company is performing a thorough review of the data from the completed study in agitation and aggression. An external clinical advisory board is working with the Company to evaluate the data and consider potential future clinical development paths for ELND005.

Alzheimer’s Disease – The Disease and the Market Opportunity

Alzheimer’s disease is a progressive brain disorder that gradually destroys a person’s memory and ability to learn, reason, make judgments, communicate and carry out daily activities. As Alzheimer’s disease progresses, individuals may also experience changes in personality and behaviour, such as anxiety, suspiciousness or agitation, as well as delusions or hallucinations. In late stages of the disease, individuals need help with dressing, personal hygiene, eating and other basic functions. People with Alzheimer’s disease die an average of eight years after first experiencing symptoms, but the duration of the disease can vary from three to 20 years.

The disease mainly affects individuals over the age of 65 and it is estimated over 18 million people are suffering from Alzheimer’s disease worldwide. The likelihood of developing late-onset Alzheimer’s approximately doubles every five years after age 65. By age 85, the risk reaches nearly 50 percent. In the United States, Alzheimer’s disease is the sixth leading cause of death and current direct/indirect costs of caring for an estimated 5.4 million Alzheimer’s disease patients are at least US$100 billion annually. Scientists have so far discovered one gene that increases risk for late-onset of the disease.

Current FDA approved Alzheimer’s disease medications may temporarily delay memory decline for some individuals, but none of the currently approved drugs are known to stop the underlying degeneration of brain cells. With no approved therapies for neuropsychiatric symptoms of Alzheimer’s disease, certain drugs approved to treat other illnesses may sometimes help with the emotional and behavioural symptoms of Alzheimer’s disease.

Neuropsychiatric symptoms associated with Alzheimer’s disease are a significant problem for Alzheimer’s disease patients and their caregivers. Approximately 90% of Alzheimer’s disease patients develop neuropsychiatric symptoms, and up to 60% develop agitation/aggression over the course of their disease. Agitation/aggression are among the most disruptive neuropsychiatric symptoms in Alzheimer’s disease and are associated with increased morbidity and caregiver burden. With an aging population, there is a great need for new therapies that can effectively reduce or delay the neuropsychiatric symptoms associated with Alzheimer’s disease.

ELND005 for Down Syndrome

On November 20, 2014, the Corporation announced the results of a clinical study of neuropsychiatric drug candidate ELND005 in young adults with Down syndrome. Transition’s wholly-owned subsidiary, Transition Therapeutics Ireland Limited (“TTIL”) completed this first study in Down syndrome subjects without dementia to allow optimal dose selection for future larger studies.

The study enrolled 23 Down syndrome subjects in three study arms over a four-week treatment period: placebo (n=6), 250mg once daily (QD) (n=5), and 250mg twice daily (BID) (n=12). ELND005, at the doses evaluated, was determined to have an acceptable safety and tolerability profile and there were no serious adverse events reported in the study. Treatment emergent adverse events were reported in seven of the subjects receiving ELND005 and all were deemed to be mild in severity. The two ELND005 doses achieved the plasma levels expected in pharmacokinetic modeling and will inform the selection of a higher dose in a future clinical study.

The Product

Excess activity of genes on chromosome 21, such as amyloid precursor protein (APP) and sodium-myo-inositol active transporter (SMIT), are thought to play a role in the cognitive dysfunction of DS. Life-long exposure to increased amyloid and myo-inositol levels in the brain are thought to lead to synaptic dysfunction and cognitive disability. ELND005 may have the potential to improve cognition in DS by decreasing amyloid levels and regulating myo-inositol-dependent neuronal signaling.

Down Syndrome – The Disease and the Market Opportunity

Down syndrome (DS, Trisomy 21), caused by an extra copy of chromosome 21, is the most common genetic form of intellectual disability with a prevalence of approximately 1 in 700 live births in the US. Children with DS exhibit developmental delay and various degrees of intellectual disability, while adults are at increased risk of Alzheimer’s dementia. There are currently no drugs approved for the treatment of cognitive dysfunction in DS.

TT401 for Type 2 Diabetes

In March, 2010, the Corporation acquired the rights to a series of preclinical compounds from Lilly in the area of diabetes. Under the licensing and collaboration agreement, the Corporation receives exclusive worldwide rights to develop and potentially commercialize a class of compounds.

The Product

In preclinical diabetes models, the lead compound, TT401 has shown potential to provide glycemic control and other beneficial effects including weight loss. In June, 2012, the Corporation announced the results of the Phase 1 clinical study of type 2 diabetes drug candidate, TT401. The Phase 1, double-blind, placebo-controlled randomized study enrolled 48 non-diabetic obese subjects in six cohorts evaluating six escalating subcutaneous single doses of TT401. TT401 demonstrated an acceptable safety and tolerability profile in non-diabetic obese subjects in the study. TT401 exhibited the expected pharmacological effect on glucose and pharmacodynamic biomarkers at doses that were safe and tolerable. The pharmacokinetic profile, assessed over 28 days, demonstrated a half-life consistent with once-weekly dosing.