Financial Results for the Fiscal Year Ended December 31, 2016 [US GAAP] [Consolidated]

February 14, 2017

|

| |

| Company name | Kubota Pharmaceutical Holdings Co., Ltd. |

| Stock exchange listing | Tokyo Stock Exchange Mothers Market |

| Code number | 4596 |

| URL | www.kubotaholdings.co.jp/en/ |

| Representative | Dr. Ryo Kubota |

| | Title: Chairman, President and Chief Executive Officer |

| Contact | Yasuo Ishikawa, Director of Financial Reporting |

| | Japan Office, Acucela Inc. |

| | (Telephone: 03-5789-5872) |

| Scheduled date of general shareholders meeting | May 25, 2017 |

| Scheduled date of annual securities report submission | March 15, 2017 |

| Scheduled date of dividend payment commencement | — |

| Supplementary materials for financial results | Yes |

| Earnings announcement for financial results | Yes |

1. Financial Results for FY2016 (January 1, 2016 to December 31, 2016)

(1) Consolidated Operating Results

(Unit: in millions, % change from the previous fiscal year)

|

| | | | | | | | | | | | | | | | | | | | |

| | Revenue from collaborations | Loss from operations | Income (loss) before income tax | Net loss attributable to common shareholders |

| | $ | 8 |

| | $ | (36 | ) | | $ | (35 | ) | | $ | (35 | ) | |

| FY2016 | ¥ | 870 |

| NA |

| ¥ | (4,121 | ) | NA |

| ¥ | (3,953 | ) | NA |

| ¥ | (3,953 | ) | NA |

|

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

| |

| FY2015 | ¥ | — |

| — |

| ¥ | — |

| — |

| ¥ | — |

| — |

| ¥ | — |

| — |

|

(Note) Comprehensive loss: FY2016 - JPY ¥3,601 million (US $34.1 million);

(Unit: ¥ or $, except for %) |

| | | | | | | | | | | | | |

| | | Basic loss per share | Diluted loss per share | Net income (loss) to equity ratio | Ratio of income before income tax to total assets | Ratio of operating income to revenues from collaborations |

| |

| | | $ | (0.92 | ) | $ | (0.92 | ) | | | |

| | FY2016 | ¥ | (105.64 | ) | ¥ | (105.64 | ) | (23.9 | )% | (23.0 | )% | (473.6 | )% |

| | | $ | — |

| $ | — |

| | | |

| | FY2015 | ¥ | — |

| ¥ | — |

| — |

| — |

| — |

|

(2) Consolidated Financial Position

(Unit: in millions, except for % and per share data)

|

| | | | | | | | | | | | | | | |

| | | Total assets | Net assets | Shareholders’ equity | Shareholders’ equity ratio | Shareholders' equity per share |

| |

| | | $ | 147 |

| $ | 142 |

| $ | 142 |

| | $ | 3.74 |

|

| | As of December 31, 2016 | ¥ | 17,169 |

| ¥ | 16,520 |

| ¥ | 16,520 |

| 96.2 | % | ¥ | 436.14 |

|

| | | $ | — |

| $ | — |

| $ | — |

| | |

| | As of December 31, 2015 | ¥ | — |

| ¥ | — |

| ¥ | — |

| — |

| ¥ | — |

|

(3) Consolidated Cash Flows

(Unit: in millions)

|

| | | | | | | | | | | | |

| | Cash flows from operating activities | Cash flows from investing activities | Cash flows from financing activities | Cash and cash equivalents—end of year |

| | $ | (28 | ) | $ | 28 |

| $ | 3 |

| $ | 9 |

|

| FY2016 | ¥ | (3,154 | ) | ¥ | 3,210 |

| ¥ | 385 |

| ¥ | 1,042 |

|

| | $ | — |

| $ | — |

| $ | — |

| $ | — |

|

| FY2015 | ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

|

2. Dividends

(Unit: in millions, except for %)

|

| | | | | | | | | | | | | | | | | | | | | | |

| | Annual dividend per share | Total Dividend Paid | Payout Ratio | Ratio of Total Amount of Dividends to Net Assets |

| First Quarter | Second Quarter | Third Quarter | Year-end | Total |

| | $ | — |

| $ | — |

| $ | — |

| $ | — |

| $ | — |

| $ | — |

| — | % | — | % |

| FY2015 | ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

| — | % | — | % |

| | $ | — |

| $ | — |

| $ | — |

| $ | — |

| $ | — |

| $ | — |

| — | % | — | % |

| FY2016 | ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

| — | % | — | % |

| | $ | — |

| $ | — |

| $ | — |

| $ | — |

| $ | — |

| $ | — |

| — | % | — | % |

| FY2017 (forecast) | ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

| ¥ | — |

| — | % | — | % |

3. Projected Consolidated Financial Results for FY2017 (January 1, 2017 to December 31, 2017)

(Unit: US$ and ¥ in millions, except for % and per share data)

|

| | | | | | | | | | | | | | | |

| | Revenue from collaborations | Loss from operations | Income (loss) before income tax | Net loss | Net loss per share (low)1 |

| Full Year 2017 Forecast | $ | — |

| $ | (39 | ) | $ | (38 | ) | $ | (38 | ) | $ | (1.00 | ) |

| ¥ | — |

| ¥ | (4,290 | ) | ¥ | (4,180 | ) | ¥ | (4,180 | ) | ¥ | (110.00 | ) |

| Percentage Change (%) - omitted where not meaningful | — | % | — | % | — | % | — | % | — | % |

1 - Net income (loss) per share was computed for Full Year 2017 Forecast using 37,877,705 weighted average shares for expected basic and diluted shares outstanding.

Note: Earnings forecast of the Company is based on US dollar amounts. Amounts as to the earnings forecast for FY2017 are converted amounts (Japanese Yen (¥) in thousands except for per share amounts) at the rate of 1 US Dollars = ¥110 which is the rate use to forecast 2017 for the sake of convenience.

4. Others

(1) Changes in significant subsidiaries during the period (changes in specified subsidiaries resulting in a change in scope of consolidation): A new consolidated subsidiary Acucela Inc.

(2) Changes in accounting principles, procedures, and the method of presentation

(i) Changes caused by revision of accounting standards, etc: None

(ii) Changes other than (i) None

(3) Number of shares issued and outstanding (common stock)

1) Number of shares issued and outstanding as of the end of the reporting period (including treasury stock):

|

| | |

| Number of Common Shares |

| As of December 31, 2016 | 37,877,705 |

|

| As of December 31, 2015 | — |

|

2) Number of shares of treasury stock as of the end of the reporting period:

|

| | |

| Number of Treasury Shares |

| As of December 31, 2016 | 70 |

|

| As of December 31, 2015 | none |

|

3) Average number of shares outstanding during the reporting period:

|

| | |

| Weighted Average Number of Common Shares |

| FY 2016 | 37,416,848 |

|

| FY 2015 | — |

|

(Reference) Overview of Non-Consolidated Financial Results

1. Non-Consolidated Financial Results for FY2016 (January 1, 2016 to December 31, 2016)

(1) Non-Consolidated Operating Results

(Unit: US$ and ¥ in millions, except for % and per share data)

|

| | | | | | | | | | | | | | | | | | | | |

| Revenue | Operating loss | Ordinary loss | Net loss |

| $ | — |

| — |

| $ | — |

| — |

| $ | — |

| — |

| $ | — |

| — |

|

| FY2016 | ¥ | — |

| ― |

| ¥ | (483 | ) | ― |

| ¥ | (484 | ) | ― |

| ¥ | (484 | ) | ― |

|

| $ | — |

| — |

| $ | — |

| — |

| $ | — |

| — |

| $ | — |

| — |

|

| FY2015 | ¥ | — |

| ― |

| ¥ | — |

| ― |

| ¥ | (1 | ) | ― |

| ¥ | (1 | ) | ― |

|

(Unit: ¥, $)

|

| | | | | | |

| Net loss per share | Diluted net loss per share |

| $ | — |

| $ | — |

|

| FY2016 | ¥ | (12.78 | ) | ¥ | — |

|

| $ | — |

| $ | — |

|

| FY2015 | ¥ | (0.02 | ) | ¥ | — |

|

(2) Non-Consolidated Financial Position

(Unit: in millions, except for % and per share data)

|

| | | | | | | | | | | |

| | Total assets | Net assets | Equity ratio | Net assets per share |

| | — |

| — |

| — |

| — |

|

| FY2016 | ¥ | 21 |

| ¥ | (3 | ) | (2,168.5 | )% | ¥ | (11.80 | ) |

| | — |

| — |

| — |

| — |

|

| FY2015 | ¥ | 1 |

| ¥ | — |

| (38.7 | )% | ¥ | (0.01 | ) |

(Note) Equity: FY 2016 ¥(447) million; FY 2015 ¥(0) million

* Implementation status of audit procedures

This financial results report is not subject to audit procedures by independent auditors under Japan’s Financial Instruments and Exchange Act, or the Act. At the time of release of this report, audit procedures in accordance under the Act have not yet been completed.

* Disclaimer Regarding Forward-Looking Statements and Other Items of Note

Effective December 1, 2016, we completed a triangular merger (the Redomicile Transaction), pursuant to which Acucela Inc., the former parent company of Kubota Holdings (the Company), merged with and into Acucela North America Inc., a wholly owned subsidiary of the Company established on March 24, 2016, as a surviving corporation. Under such transaction, the shares of common stock of the Company were allocated and issued to the shareholders of Acucela Inc. in exchange for the common stock of such company. The Company listed on Tokyo Stock Exchange Mothers Market on December 6, 2016. Therefore, the Company has prepared the consolidated financial statements since this fiscal year.

Forecasts and other forward-looking statements included in this report are based on information currently available and certain assumptions that the Company deems reasonable. Actual performance and other results may differ significantly due to various factors. Please see "1. Business Results - (1) Analysis of Business Results" and “1. Business Results - (4) Risk Factors of Operation" below for the details.

* Investors Meeting

The Company will actively hold Investors Meetings for investors. Please visit our website (http://www.kubotaholdings.co.jp/en/) for the schedule.

TABLE OF CONTENTS

1. Business Results

(1) Analysis of Business Results

Effective December 1, 2016, we completed a triangular merger (the Redomicile Transaction), pursuant to which Acucela Inc., the former parent company of Kubota Holdings (the Company), merged with and into Acucela North America Inc., a wholly owned subsidiary of the Company established on March 24, 2016, as a surviving corporation. Under such transaction, the shares of common stock of the Company were allocated and issued to the shareholders of Acucela Inc. in exchange for the common stock of such company. As for the analysis below, figures of the former Acucela Inc. are used for FY 2015 for the sake of convenience of our shareholders.

FY2016 compared to FY2015

Revenue from collaborations. Revenues from collaborations for the year ended December 31, 2016 totaled approximately ¥870 million ($7.6 million), representing a decrease of approximately ¥2,033 million ($16.5 million), or 70.0%, over the same period in 2015.

By program, revenues were as follows (in thousands JPY (¥), except for %):

|

| | | | | | | | | | | | | | |

| | Year Ended December 31, | | 2015 to 2016

¥ Change | | 2015 to 2016

% Change |

| | 2016 | | 2015 | |

| Emixustat | ¥ | 868,572 |

| | ¥ | 2,902,397 |

| | ¥ | (2,033,825 | ) | | (70.1 | )% |

| OPA-6566 | 1,626 |

| | 324 |

| | 1,302 |

| | 401.9 | % |

| Total | ¥ | 870,198 |

| | ¥ | 2,902,721 |

| | ¥ | (2,032,523 | ) | | (70.0 | )% |

By program, revenues were as follows (in thousands US$, except for %):

|

| | | | | | | | | | | | | | |

| | Year Ended December 31, | | 2015 to 2016

$ Change | | 2015 to 2016

% Change |

| | 2016 | | 2015 | |

| Emixustat | $ | 7,592 |

| | $ | 24,064 |

| | $ | (16,472 | ) | | (68.5 | )% |

| OPA-6566 | 14 |

| | 3 |

| | 11 |

| | 366.7 | % |

| Total | $ | 7,606 |

| | $ | 24,067 |

| | $ | (16,461 | ) | | (68.4 | )% |

Revenues from clinical programs under the Emixustat Agreement decreased in 2016 compared to 2015. The decrease in revenue from collaborations was primarily due to billing fewer full-time employees as a result of the completion of the Emixustat clinical trial during the year and wind-down activities related to Emixustat following the termination of our collaboration with Otsuka. Wind-down activities related to Emixustat were completed in December 2016.

Our Phase 2b/3 clinical trial results related to Emixustat for the treatment of geographic atrophy was completed in May 2016. We do not expect to generate any revenue from the terminated collaboration with Otsuka related to Emixustat in the future.

Our clinical program related to Otsuka's proprietary compound for potential treatment of glaucoma, which was the subject of the OPA-6566 Agreement between us and Otsuka, was terminated in 2016. We do not expect to generate any revenue from the collaboration related to OPA-6566 in the future.

Research and development.

We anticipate that potential product candidates developed under our Strategic Plan may be developed independently, and our expenditures on such programs will not be funded by collaborative partners. As a consequence, we expect our total research and development expenses to increase in absolute dollars as we pursue development of our product candidates in multiple indications and execute in-licensing transactions resulting in potential upfront and milestone payments.

Research and development expense for the year ended December 31, 2016 totaled approximately ¥2,370 million ($20.7 million), representing a decrease of approximately ¥360 million ($1.9 million), or 13.2%, over the same period in 2015.

By program, our research and development expenses were as follows (in thousands JPY (¥), except for %):

|

| | | | | | | | | | | | | | |

| | Year Ended December 31, | | 2015 to 2016

¥ Change | | 2015 to 2016

% Change |

| | 2016 | | 2015 | |

| Emixustat | ¥ | 1,324,661 |

| | ¥ | 2,540,027 |

| | ¥ | (1,215,366 | ) | | (47.8 | )% |

| Internal Research | 1,044,622 |

| | 189,962 |

| | 854,660 |

| | 449.9 | % |

| OPA-6566 | 1,080 |

| | 139 |

| | 941 |

| | 677.0 | % |

| Total | ¥ | 2,370,363 |

| | ¥ | 2,730,128 |

| | ¥ | (359,765 | ) | | (13.2 | )% |

By program, our research and development expenses were as follows (in thousands US$, except for %):

|

| | | | | | | | | | | | | | |

| | Year Ended December 31, | | 2015 to 2016

$ Change | | 2015 to 2016

% Change |

| | 2016 | | 2015 | |

| Emixustat | $ | 11,576 |

| | $ | 21,060 |

| | $ | (9,484 | ) | | (45.0 | )% |

| Internal Research | 9,122 |

| | 1,575 |

| | 7,547 |

| | 479.2 | % |

| OPA-6566 | 9 |

| | 1 |

| | 8 |

| | 800.0 | % |

| Total | $ | 20,707 |

| | $ | 22,636 |

| | $ | (1,929 | ) | | (8.5 | )% |

Research and development expense related to clinical programs under the Emixustat Agreement decreased in 2016 compared to 2015. The decrease was due to the completion of the Phase 2b/3 clinical trial and related wind-down in activities related to such clinical trial following the termination of the Emixustat Agreement.

Due to the termination of the OPA-6566/Glaucoma Agreement with Otsuka in 2016 and the results of a Phase 1/2 clinical study evaluating OPA-6566 in 2012, we do not expect to incur any research and development expenses related to this program in the future.

Research and development expenses incurred through our internal research activities increased in 2016 compared to 2015, mainly due to new product development. This increase included an upfront non-refundable fee of ¥572 million ($5.0 million), paid to YouHealth in the first quarter of 2016 in connection with the option and license agreement for lanosterol technology.

General and administrative.

The general and administrative expenses were as follows (in thousands JPY (¥), except for %):

|

| | | | | | | | | | | | | | |

| | Year Ended December 31, | | 2015 to 2016

¥ Change | | 2015 to 2016

% Change |

| | 2016 | | 2015 | |

| General and administrative | ¥ | 2,620,904 |

| | ¥ | 3,375,512 |

| | ¥ | (754,608 | ) | | (22.4 | )% |

The general and administrative expenses were as follows (in thousands US$, except for %):

|

| | | | | | | | | | | | | | |

| | Year Ended December 31, | | 2015 to 2016

$ Change | | 2015 to 2016

% Change |

| | 2016 | | 2015 | |

| General and administrative | $ | 22,895 |

| | $ | 27,987 |

| | $ | (5,092 | ) | | (18.2 | )% |

General and administrative expenses decreased ¥755 million ($5.1 million) in 2016 compared to 2015. Excluding stock based compensation, general and administrative expenses decreased ¥358 million ($2.1 million) in 2016 compared to 2015 primarily due to the following:

| |

| • | the Company recognized less stock based compensation expense related to accelerated vesting upon termination by former employees of the Company than in the prior year by ¥396 million ($3.0 million); |

| |

| • | the Company did not incur ¥271 million ($2.2 million) in charges related to the one-time May 2015 special meeting of the shareholders and related transaction costs; |

| |

| • | the Company incurred fewer charges related to bonus and retention payments of ¥151 million ($1.2 million); |

| |

| • | the Company paid ¥139 million ($1.1 million) less in severance to former officers and employees in the current year; and |

| |

| • | the Company paid ¥107 million ($0.8 million) less in accounting and compliance services related to implementing a new general ledger system, audit and equity compliance; |

These changes were offset by the increase in 2016 of corporate legal expenses and charges related to the Redomicile Transaction of ¥372 million ($3.3 million).

Prospects for the upcoming fiscal year:

Discussion in the summary section 3. Projected Financial Results for FY2017 (January 1, 2017 to December 31, 2017) is as follows.

During 2017, the Company will pursue a strategy of advancing the development of a portfolio of product candidates. In prior years the Company’s principal development activities were done in connection with its collaborations with Otsuka, through which the Company earned development revenue. Starting in 2017, the Company is independently developing its product candidates. By pursuing a broad portfolio of product candidates, the Company believes there will be multiple opportunities to demonstrate clinical proof of concept and pursue commercial success.

As the development programs advance, the Company will evaluate engaging collaboration partners to provide funding for later stage development and assist with commercialization. Until collaboration partners and associated collaboration revenues are secured, the Company will self-fund its operations, resulting in net losses.

Revenue from collaborations:

Due to the termination of the agreement with Otsuka Pharmaceutical in June 2016, the Company does not expect revenue in FY2017. The Company is required by the TSE to generate revenue five years after the IPO. Currently, the Company is pursuing various partnering efforts and is expecting to generate revenue in the future through collaboration with strategic partners.

Loss from Operations:

The operating loss for FY2017 is mainly due to the increase in internal research and development efforts, as the Company will self-fund the development of its product candidate portfolio and intends to continue to expand its pipeline. The Company expects G&A costs to decline compared to FY2016 due to the completion of the Redomicile Transaction as of December 2016.

(2) Analysis of Financial Condition

Cash and cash equivalents include all short-term, highly liquid investments with an original maturity date of three months or less as of the date of purchase. Cash equivalents consist of money market funds. Investments with maturities between three months and one year at the date of purchase are classified as short-term investments. Short-term investments are comprised of corporate debt securities, commercial paper, US government agency securities, and certificates of deposit.

As of December 31, 2016 and December 31, 2015, we had cash, cash equivalents and investments of ¥16,459 million ($141.3 million) and ¥20,085 million ($166.5 million), respectively. Amounts on deposit with third-party financial institutions may exceed the US Federal Deposit Insurance Corporation and the Securities Investor Protection Corporation insurance limits, as applicable.

We believe that our existing cash, cash equivalents and investment balances will be sufficient to fund our ongoing operating activities, working capital, capital expenditures and other capital requirements for at least the next 12 months. Our future capital requirements will depend on many factors, including the expansion of our research and development activities, and our ability to successfully in-license or acquire additional technologies. Other than our exclusive option to purchase the assets related to our collaboration agreement with EyeMedics, we are not currently a party to any agreement or letter of intent regarding potential investments in, or acquisitions of, complementary businesses, applications or technologies. We may enter into these types of arrangements, which could require us to seek additional equity or debt financing.

The following table shows a summary of our cash flows for the years ended December 31, 2016 and 2015, (in US$ and JPY¥ thousands):

|

| | | | | | | | | | | | | | | |

| | Cash flows from operating activities | Cash flows from investing activities | Cash flows from financing activities | Effect of exchange rate change on cash and cash equivalents | Cash and cash equivalents—end of period |

| | $ | (27,526 | ) | $ | 28,022 |

| $ | 3,365 |

| $ | — |

| $ | 8,949 |

|

| FY2016 | ¥ | (3,154,251 | ) | ¥ | 3,210,098 |

| ¥ | 384,829 |

| ¥ | (11,880 | ) | ¥ | 1,042,474 |

|

| | $ | (16,871 | ) | $ | 4,341 |

| $ | (1,160 | ) | $ | — |

| $ | 5,088 |

|

| FY2015 | ¥ | (2,034,811 | ) | ¥ | 523,583 |

| ¥ | (139,908 | ) | ¥ | — |

| ¥ | 613,678 |

|

Cash Flows from Operating Activities

Net cash used in operating activities was ¥3,154 million ($27.5 million) and ¥2,035 million ($16.9 million) for the years ended December 31, 2016 and 2015, respectively. The change in net cash used in operating activities is related to an increase of ¥171 million ($0.4 million) in cash payments for operating expenses and a decrease of ¥1,290 million ($10.2 million) in cash collections of accounts receivable from collaborations.

Cash Flows from Investing Activities

Net cash provided by investing activities was ¥3,210 million ($28.0 million) and ¥524 million ($4.3 million) for the years ended December 31, 2016 and 2015, respectively. Net cash inflows increased from 2015 to 2016 due to an increase of ¥2,613 million ($27.7 million) in maturities of marketable securities held as available for sale offset by an increase of ¥31 million ($4.3 million) in purchases of marketable securities available for sale.

Cash Flows from Financing Activities

Net cash provided by financing activities was ¥385 million ($3.4 million) and net cash used by financing activities was ¥140 million ($1.2 million) for the years ended December 31, 2016 and 2015, respectively. During 2016, cash inflows from financing activities was primarily the result of ¥1,304 million ($11.4 million) of proceeds related to the issuance of common stock related to current and former employees exercising their stock options during the year. This was partially offset by ¥919 million ($8.0 million) related to employee tax withholdings for equity awards. During 2015, cash outflows from financing activities related to employee tax withholdings for equity awards.

(Reference) Indicators

|

| | | | | |

| | FY2015 |

| | FY2016 |

|

| Shareholders’ equity ratio (%) | 94.6 | % | | 96.2 | % |

| Shareholders’ equity ratio based on market prices (%) | 143.4 | % | | 230.3 | % |

| Debt to annual cash flow ratio (%) | — |

| | — |

|

| Interest coverage ratio (times) | — |

| | — |

|

Shareholders' equity ratio: stockholders' equity / total assets

Shareholders' equity ratio based on market prices: market capitalization / total assets

Debt to annual cash flow ratio: interest bearing liabilities / operating cash flows

Interest coverage ratio: operating cash flows / interest payments

(Notes)

1. These indexes are calculated using U.S. GAAP figures.

2. Market capitalization is calculated based on issued and outstanding shares excluding treasury stock.

3. Operating cash flows are the cash flows provided by operating activities on the statements of cash flows.

4. Interest-bearing liabilities include all liabilities on the balance sheets that incur interest.

(3) Basic Policy on Distribution of Profits and Distribution for FY2016 and Distribution Forecast for FY2017

We have not declared or paid a cash dividend on our capital stock and do not intend to pay cash dividends for the foreseeable future. We intend to retain all available funds and any future earnings to fund the development and growth of our business. Any future determinations to pay dividends on our capital stock would depend on our results of operations, our financial condition and liquidity requirements, restrictions that may be imposed by applicable law or our contracts, and any other factors that our board of directors in its sole discretion may consider relevant.

Distribution forecast for 2017 - The Company does not plan for distribution at this time.

(4) Risk Factors of Operations

Risks Related to Our Business and Industry

We do not have any products that are approved for commercial sale.

We are a clinical stage ophthalmology company with no products approved for commercial sale. All of the products we are developing or may develop in the future require additional research or development. None of our product candidates have received regulatory approval for marketing in any country and failure to receive such approvals could materially harm our business. To date, we have not generated any product revenue and have funded our operations through proceeds from our IPO, private sales of our equity and debt securities and from our collaboration agreements with Otsuka. We will not receive revenues from sales of any drug candidate unless we succeed, either independently or with third parties, in developing and obtaining regulatory approval and marketing drugs with commercial potential. We may never succeed in these activities, and may not generate sufficient revenues to continue our operations.

We cannot be certain that our product candidates or devices will achieve success in clinical trials, secure regulatory approval, or be successfully commercialized.

We have invested significant time and financial resources in the development of Emixustat, the lead investigational drug candidate emerging from our internally-developed VCM compounds. VCM is an emerging technology and its long-term safety and efficacy is unknown, and thus, there can be no assurance that our drug candidates will achieve regulatory approval. In May 2016, we announced the top-line results of our completed Phase 2b/3 study of Emixustat in patients with GA secondary to dry AMD. The study did not meet its primary endpoint and in June 2016, Otsuka terminated the Emixustat Agreement pertaining to our prior collaboration. We intend to continue development of Emixustat for the treatment of retinal disorders other than GA secondary to dry AMD. There can be no assurance that our development efforts will be successful. Clinical development is a long, expensive and uncertain process and subject to delays or additional requirements. We may also encounter delays or rejections based on our inability to enroll enough subjects to complete our clinical trials in a timely manner. It may take several years and require the expenditure of substantial resources to complete the testing of product candidates or devices, and failure can occur at any stage of testing. Interim results of clinical or non-clinical studies may not necessarily predict their final results, and product candidates that appear promising at early stages of development may ultimately fail. We may not be able to obtain marketing approval or may obtain approval for indications that are not as broad as intended. Our product development costs will also increase if we experience delays in testing or approvals. Significant clinical trial delays could allow our competitors to bring products to market before we do and impair our ability to commercialize products. If we are unable to successfully develop, obtain regulatory approval, sell and distribute or recognize revenues from our product candidates, the results of our business operations will be adversely affected.

Revenues from research and development activities in collaboration with Otsuka represented all of our revenues during the year ended December 31, 2016, and the loss of these revenues will adversely affect our business.

Revenues from research and development activities under our collaboration agreements with Otsuka were our only source of revenues in 2015 and 2016. In June 2016, Otsuka terminated our existing collaboration agreements, including the Emixustat Agreement, due to Emixustat’s failure to meet its primary endpoints in the concluded Phase 2b/3 clinical trial in GA secondary to AMD. Following the expiration of a six month wind-down period under the Emixustat Agreement, our revenue has significantly decreased. The loss of revenue derived from research and development activities on behalf of Otsuka will have an adverse impact on our business. In addition, Otsuka’s termination of its relationship with us could harm our reputation.

We may face competition from alternative product offerings with superior risk-benefit profiles.

Ophthalmology is a fast growing market with many established and emerging companies heavily investing in research, development and commercialization of novel products. Those products may offer a superior risk-benefit profile, including but not limited to, a superior economic value to payers, such that their products will be preferred therapies over our future product offerings. This may negatively impact our future revenue from such product sales or impact our ability to commercialize the product in a specific market or geography.

We incurred losses in both the last fiscal year and the year ended December 31, 2016, and will continue to incur losses in the future.

We incurred a net loss of ¥3,953 million ($34.5 million) during the year ended December 31, 2016, and as of December 31, 2016, we had an accumulated deficit of ¥7,496 million ($65.5 million). We expect to incur net losses for the next several years as we continue to develop our product candidates and over the long-term if we expand our research and development programs and acquire or in-license additional products, technologies or businesses that are

complementary to our own. As a result of these losses, we may exhaust our financial resources and be unable to complete the development of our product candidates. If we fail to raise capital as needed, we may curtail or cease operations in the future. There can be no assurances that there will be adequate financing available to us in the future on acceptable terms, or at all.

Exchange rate fluctuations may affect our operating results.

Our main business of research and development activities is currently based in its U.S. subsidiary, Acucela Inc. The functional currency of Acucela is the U.S. dollar, and its financial statements are also prepared in U.S. dollar. Therefore, since consolidated financial statements are translated into Japanese yen for the reporting purpose in Japan, substantial exchange rate fluctuations may have a material impact on our business results and financial position of consolidated financial statements.

We have never generated any revenue from product sales and our ability to generate revenue from product sales and become profitable depends significantly on our success in executing on a number of factors.

We have no products approved for commercial sale, have not generated any revenue from product sales, and do not anticipate generating any revenue from product sales until sometime after we have received regulatory approval for the commercial sale of a product candidate. Our ability to generate revenue and achieve profitability depends significantly on our success in executing on many factors, including completing research and development, obtaining regulatory approvals and marketing authorizations, accessing sustainable and scalable manufacturing processes, launching and commercializing product candidates, and achieving market acceptance.

We anticipate incurring significant costs in commercializing any approved product. Our expenses could increase beyond expectations and if we are not able to generate sufficient revenue from product sales, we may never become profitable.

The pharmaceutical market is intensely competitive. Even if we are successful in obtaining approval of any of our drug candidates, we may be unable to compete effectively with other drugs, new treatment methods and technologies.

The pharmaceutical market is intensely competitive. Many large pharmaceutical and biotechnology companies, academic institutions, governmental agencies and other public and private research organizations are pursuing the development of novel therapies for the same indications that we are targeting or expect to target.

If our product candidates are approved for commercialization, we anticipate competition to vary depending on the approved indication. Currently there are no FDA approved treatments for Stargardt Disease or RP, though there are various low vision aids to assist the daily living of patients with these diseases. Although there are multiple FDA approved treatments for cataracts, there is no FDA approved pharmacological therapy to prevent, reverse or slow the progression of cataracts though various competitive products are in development. However in Japan, multiple therapies are approved for the treatment of wet AMD and diabetic retinopathy. Consequently, we will have to establish an improved risk/benefit, convenience or pricing profile for ACU-6151 to gain significant market acceptance.

Many of our competitors have much greater financial, technical and human resources, more extensive experience in non-clinical testing, conducting clinical trials, obtaining regulatory approvals, manufacturing and marketing pharmaceutical products, drug candidates based on previously tested or accepted technologies, approved products or investigational drug candidates in late stages of development, and collaboration arrangements in our target markets.

Our competitors may obtain patent protection or receive regulatory approval for drugs or devices for the same indications before we do. Competing drugs or devices may be more effective or marketed and sold more effectively than products we develop. Moreover, physicians frequently prescribe therapies for uses that are not described in the product’s labeling and that differ from those tested in clinical studies and approved by regulatory authorities. These unapproved, or “off-label,” uses are common across medical specialties and may represent a potential source of competition to our drug candidates. Competitive therapies, including surgical procedures and medical devices, may make our drug candidates obsolete or noncompetitive before we can recover the expenses of development and commercialization.

Market acceptance of any potential product we develop in the future may be limited.

The commercial success of the products for which we may obtain marketing approval from regulatory authorities will depend upon the acceptance of these products by the medical community and third-party payors as clinically useful, cost-effective and safe. Even if a potential product displays a favorable efficacy and safety profile in clinical trials, market acceptance of the product will not be known until after it is commercially launched.

Our operating results may fluctuate in the future, which could cause our stock price to decline.

Our quarterly and annual results of operations may fluctuate in the future due to a variety of factors, many of which are outside of our control. The revenues we generate, if any, and our operating results will be affected by numerous factors, including, the terms of any future collaboration agreement, particularly, the timing of any milestone payments to be paid or received by us under such agreements, regulatory approvals, competing technologies and products, the timing and magnitude of internal development efforts, and general and industry specific economic conditions.

If our operating results fall below the expectations of investors or securities analysts, the price of our common stock could decline substantially. Furthermore, any fluctuations in our operating results and cash flows may cause the price of our stock to fluctuate substantially. Comparisons of our historical financial results may not be an indication of future results.

We have limited in-house sales and marketing capabilities and will need to invest significantly to develop these capabilities if our product candidates are successfully developed.

In order to exploit any potential future commercialization opportunities for our product candidates, we believe we will need to develop our own sales and marketing infrastructure. We cannot make assurances that we will be able to do this on a timely basis or at all. The failure to do so would harm our ability to generate product revenues. If we cannot or choose not to use internal resources for the marketing, sales or distribution of any product candidates, we intend to rely on collaboration partners or licensees. We may be unable to establish or maintain such relationships. If we work with collaboration partners or other third parties for marketing, sales and distribution, any revenues we receive will depend upon their efforts. Such efforts may not be successful, and we will not be able to control the amount and timing of resources that our licensees or collaborators or other third parties devote to our products.

We may not be successful in our efforts to expand our portfolio of product candidates.

We are seeking to further expand our portfolio of product candidates through internal development and by licensing or partnering with other pharmaceutical, biotechnology or device companies, or universities.

Our internal research programs involve unproven technologies. Identifying research programs for new disease targets and product candidates requires substantial technical, financial and human resources. Our research programs may initially show promise in identifying potential compounds, yet fail to yield product candidates.

We may attempt to license or acquire product candidates and be unable to do so for a number of reasons. In particular, the licensing and acquisition of pharmaceutical products is a competitive area. We may be unable to license or acquire the relevant intellectual property rights on terms that would allow us to earn an appropriate return. Companies that perceive us to be their competitors may be unwilling to assign or license their product rights to us. If we are successful in expanding our portfolio of product candidates, we may be unable to successfully develop such candidates or find a suitable collaborator. Even if we identify suitable new product candidates, such product candidates may not achieve proof of concept in a cost-effective manner or at all. The occurrence of any of these risks could materially and adversely impact our business.

Relying on third-party manufacturers may result in delays in our clinical trials and product introductions.

We have limited experience in, and we do not own facilities for, manufacturing and we do not intend to develop facilities for the manufacture of product candidates for clinical trials or commercial purposes in the foreseeable future. While there are likely competitive sources available to manufacture our product candidates, entering into new arrangements may cause delays and additional expenditures, which we cannot estimate.

The risks inherent in pharmaceutical manufacturing could affect the ability of third-party manufacturers to meet our requirements or the requirements of regulators, which could result in delays. If we do not have adequate manufacturing capacity, our ability to develop and commercialize our products could be adversely impacted.

We are dependent on our management team and if we are unable to retain and motivate our key management and scientific staff, our development programs may be delayed and we may be unable to successfully develop or commercialize our product candidates.

We are dependent on our management team. The relationships and reputation that our management team has cultivated within the ophthalmology community are critical for our continued access to technologies and developments in this field.

Our success depends on our ability to attract, retain and motivate highly qualified management and scientific personnel. We face competition for experienced scientists and other professionals from numerous companies and academic and other research institutions.

If any products we develop become subject to third-party reimbursement practices, unfavorable pricing regulations or healthcare reform initiatives, our business could be harmed.

Reimbursement by governmental and other third-party payors of healthcare services affect the market for our potential products. These payors continually attempt to limit or reduce the costs of healthcare by challenging the prices charged for medical products and services. We cannot be sure that reimbursement will be available for any future product candidates and reimbursement amounts, if any, may reduce the demand for, or the price of, our future products.

Obtaining approvals from governmental and other third-party payors of healthcare services is time-consuming and expensive. Because our product candidates are under development, we are unable at this time to determine the level or method of reimbursement. Our business would be materially adversely affected if we do not receive approval for adequate reimbursement of any product candidates that obtain marketing approval.

We may need to grow the size of our organization, and we may experience difficulties in managing this growth.

As we advance our product candidates through clinical development and develop our related commercialization plans and strategies, we may need to hire employees for managerial, operational, sales, marketing, financial, human resources and other functional areas. Competition for these employees is intense and we may be unable to hire additional qualified personnel in a timely manner or on reasonable terms. While we attempt to provide competitive compensation packages to attract and retain key personnel, many of our competitors are likely to have greater resources and more experience than we have, and we have had difficulty competing successfully for key personnel.

We face the risk of product liability claims and may not be able to obtain insurance, and we may have exposure to significant contingent liabilities.

Our business exposes us to the risk of product liability claims. If our products harm people, we may be subject to costly and damaging product liability claims. We have product liability insurance for our clinical trials up to a $10 million annual aggregate limit. We intend to expand our insurance coverage to include the sale of commercial products if we obtain marketing approval for any of the products that we may develop. Insurance coverage is increasingly expensive and may not be available on reasonable terms, if at all. If we are unable to obtain insurance at an acceptable cost or otherwise protect against potential product liability claims, we will be exposed to significant liabilities, which may materially and adversely affect our business and financial position.

We may need additional financing, which may be difficult to obtain. Our failure to obtain necessary financing or doing so on unattractive terms could adversely affect our development programs and other operations.

As of December 31, 2016, we had cash, cash equivalents and investments of ¥16,459 million ($141.3 million) and working capital of ¥14,294 million ($122.7 million). We believe that our cash, cash equivalents and investments will be sufficient to meet our working capital and capital expenditure requirements for at least the next 12 months. However, our future working capital and capital expenditure requirements will depend on many factors, including the success of our development efforts and commercialization of product candidates and our ability to raise additional funding through partnering, out-licensing and other means.

Additional financing may not be available to us on favorable terms when we need it. If we are unable to obtain adequate financing, we may be required to significantly curtail one or more of our development, licensing or acquisition programs. If we raise additional funds by issuing equity securities or securities convertible into equity, our then-existing shareholders will experience dilution and the terms of any new equity securities or securities convertible into equity may have preferences over our common stock. If we raise additional funds through the incurrence of indebtedness we would have payment obligations and, potentially be subjected to certain restrictive covenants.

Our computer systems may fail or suffer security breaches.

Despite the implementation of security measures, our computer systems are vulnerable to damage from computer viruses and unauthorized access. Although to our knowledge we have not experienced a material system failure or security breach, if such an event were to occur and cause interruptions in our operations, it could result in a material disruption of our development programs and our business operations.

We maintain confidential and proprietary information on our computer networks. Although we have employed security measures to protect this information from unauthorized access, security breaches may occur as a result of third-party action, including computer hackers, employee error, malfeasance or otherwise, that could result in someone obtaining unauthorized access. Because the techniques employed by hackers to obtain unauthorized access or to sabotage systems change frequently, we may be unable to anticipate these techniques or to implement adequate preventative measures. Any security breach could result in disclosure of our trade secrets or disclosure of confidential supplier or employee data. Our systems and external backup measures may also be vulnerable to damage or breach due to natural disasters or other unexpected events. If this should happen, we could be exposed to potentially significant legal liability, remediation expense, harm to our reputation and other harm to our business.

If we use hazardous or biological materials in a manner that causes injury or violates applicable law, we may be liable for damages.

Our research and development activities may involve potentially hazardous chemical and biological materials and our operations may produce hazardous waste products. We are subject to laws and regulations governing the use of hazardous materials. We believe that we comply with legally prescribed standards pertaining to these hazardous materials, however we may incur significant additional costs to comply with applicable laws in the future. We cannot completely eliminate the risk of contamination or injury resulting from hazardous materials and we may incur liability as a result of any such contamination or injury. In the event of an accident, we could be held liable for damages or penalized with fines, and the liability could exceed our resources. Compliance with applicable environmental laws and regulations is expensive, and current or future environmental regulations may impair our research, development and production efforts, which could harm our business, operating results and financial condition.

We are an “emerging growth company,” and any decision on our part to comply only with certain reduced disclosure requirements applicable to emerging growth companies could make our common stock less attractive to investors.

We are an emerging growth company, as defined in Section 2(a) of the Securities Act of 1933, as amended, of the Securities Act, and, while we maintain such status, may choose to take advantage of certain exemptions from various reporting requirements applicable to other public companies, including, but not limited to, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation. We could be an emerging growth company until the end of 2019 or until the market value of our common stock that is held by non-affiliates exceeds $700 million as of June 30th of any year. Investors may find our common stock less attractive if we choose to rely on these exemptions.

Risks Related to Our Recently Completed Redomicile Transaction

The anticipated benefits of the Redomicile Transaction may not be realized.

We may not realize the benefits we anticipate from the Redomicile Transaction, particularly as the realization of those benefits are in many important respects subject to factors that we do not control. These factors would include such things as the reactions of third parties with whom we enter into contracts and do business and the reactions of investors and analysts, the positions taken by Japanese and U.S. taxing authorities with respect to the Redomicile Transaction and the taxation of Kubota Holdings following the Redomicile Transaction, and other factors discussed in these risk factors. For example, the increased availability, quantity and prominence of information about our Company for Japanese investors and the increased number of Tokyo Stock Exchange-focused institutional investors that will be able to invest in us following the Redomicile Transaction may not lead to increased demand for our listed securities. Even if there is increased demand for our listed securities, we cannot assure investors that equity research analysts will initiate or maintain research coverage of Kubota Holdings. The failure to realize any of these anticipated benefits could have an adverse impact on the price of Kubota Holdings’ common stock.

Completion of the Redomicile Transaction may also fail to provide us with additional business opportunities in Japan, including initiation of new collaborations with Japanese pharmaceutical companies. Any such business opportunities will be significantly influenced by factors that will not be directly impacted by the Redomicile Transaction, including our technology, product candidates and the interests of Japanese pharmaceutical companies in pursuing collaborations with Kubota Holdings.

If any of these benefits or other anticipated business opportunities are not realized, our business, results of operation or financial condition could be adversely impacted.

The National Tax Agency may disagree with our conclusions on tax treatment of the Redomicile Transaction and the National Tax Agency has not provided (and we have not requested) a ruling on the Japanese tax aspects of the Redomicile Transaction.

We expect that the Redomicile Transaction will not result in any material Japanese tax liability to Japanese shareholders, as the Redomicile Transaction should be treated as a qualified merger for Japanese tax purposes. However, if the National Tax Agency, or NTA, disagrees with this view, it may take the position that material Japanese income or corporation tax liabilities or amounts on account thereof are payable by Japanese shareholders as a result of the Redomicile Transaction. The NTA has not provided (and we have not requested) a ruling on the Japanese tax aspects of the Redomicile Transaction. There can be no assurance that the NTA will agree with our interpretation of the tax aspects of the Redomicile Transaction or any related matters associated therewith.

We are subject to United States and Japanese corporation taxes following the Redomicile Transaction.

Following the Redomicile Transaction, Kubota Holdings is generally resident and subject to tax in both the United States and Japan. While we believe our dual status for tax purposes will not result in material amounts of additional corporation tax, tax authorities may challenge our application and/or interpretation of relevant tax laws, regulations or treaties, valuations and methodologies or other supporting documentation, and, if they are successful in doing so, we may experience adverse tax consequences. Even if we are successful in maintaining our tax positions, we may incur significant expense in contesting these positions or other claims made by tax authorities. In addition, the holding company structure of Kubota Holdings will introduce other operational issues, including a limited ability to transfer cash from Acucela US to Kubota Holdings without incurring a tax imposed by Japanese authorities on the value of the funds transferred in certain cases.

Kubota Holdings’ dual tax status may adversely affect a future liquidity event.

In the event of an acquisition of Kubota Holdings, an acquirer would inherit Kubota Holdings’ dual tax status, which may decrease the likelihood that Kubota Holdings is acquired or may adversely affect the valuation of Kubota Holdings in the event of such an acquisition.

In the event of a sale of Acucela US by Kubota Holdings, the acquirer would not inherit Kubota Holdings’ dual tax status. However, in that case, Kubota Holdings would potentially be subject to both United States and Japanese corporation tax on any gain from the sale of Acucela US, and the holders of Kubota Holdings common stock would additionally be subject to tax on the distribution of proceeds from such a sale. Consequently, Kubota Holdings does not anticipate consummating any such sale of Acucela US, although it is impossible to predict the precise form of a future liquidity event.

Holders of Kubota Holdings common stock may be subject to double tax on dividends.

The gross amount of dividends paid to U.S. shareholders from Kubota Holdings on Kubota Holdings common stock generally will be included in gross income as dividend income for U.S. federal income tax purposes. Such dividends generally also will be subject to Japanese withholding tax. However, such dividends will not constitute foreign source income for U.S. foreign tax credit limitation purposes because Kubota Holdings, even though organized as a Japanese joint stock corporation, will be treated as a U.S. corporation for U.S. federal income tax purposes. Therefore, U.S. shareholders may not be able to claim a U.S. foreign tax credit for Japanese withholding tax on any dividends received from Kubota Holdings unless such U.S. shareholders have sufficient other foreign source income.

Also, the gross amount of dividends paid to Japanese shareholders from Kubota Holdings on Kubota Holdings common stock will generally be treated as taxable income for Japanese tax purposes, subject to certain exceptions for corporate shareholders. Such dividends generally also will be subject to U.S. withholding tax. However, the U.S. withholding tax may not be a creditable tax to offset against Japanese taxes because under the Japanese foreign tax credit system, only foreign taxes allowed to be levied by a contracting state under a tax treaty are creditable in principle. In addition, even if the U.S. withholding tax is considered a creditable tax, dividends paid by Kubota Holdings may not constitute foreign source income for Japanese tax credit purposes because Kubota Holdings is a Japanese corporation, so the U.S. withholding tax may not generally be creditable. Therefore, Japanese shareholders may not be able to claim a Japanese foreign tax credit for any U.S. withholding tax. The Japanese withholding tax should be creditable against a Japanese shareholder’s Japanese income tax in principle or be refundable to a Japanese shareholder in appropriate cases.

Holders of Kubota Holdings common stock who are not U.S. or Japanese shareholders will generally be subject to both U.S. and Japanese withholding tax.

If the Company decides to pay a dividend it may attempt to take measures in advance to avoid double tax on dividends. However, there can be no assurance that such measures would eliminate such double tax with respect to any particular holder of shares of Kubota Holdings common stock.

The renaming and rebranding of our business may not be successful and our operating results and business prospects may suffer if we are unable to successfully transition our brand

In connection with the Redomicile Transaction, Kubota Pharmaceutical Holdings Co., Ltd. became the publicly traded parent company of Acucela Inc. Renaming our business has resulted in additional expenditures for updating our logos and graphics and increased marketing costs to inform our collaborators, suppliers, service providers and other third parties. In addition, challenges to our new brand could also result in incremental operating expenses. If these incremental expenses exceed customary and expected costs, there could be a material adverse impact on our business. In addition, following the renaming and rebranding, we may experience loss of goodwill and some of our existing and potential collaborators, suppliers, service providers and other third parties may not recognize our new corporate names. The renaming and rebranding also may negatively impact our ability to recruit qualified personnel due to lack of name recognition. We may need to expend significant resources to develop our new brand names in the marketplace, and if we fail to build strong brand recognition, our business relationships, recruiting efforts and business prospects may suffer.

Negative publicity resulting from the Redomicile Transaction could adversely affect our business and the price of Kubota Holdings common stock.

Reincorporations have generated significant press coverage in the United States, much of which has been negative. Negative publicity generated by the Redomicile Transaction could cause our employees, particularly those in the United States, to perceive uncertainty regarding their future opportunities. In addition, negative publicity could cause some of our vendors, collaborators and other third parties to be more reluctant to do business with us. Either of these events could have a significant adverse impact on our business. Negative publicity could also cause some Kubota Holdings shareholders to sell their shares or decrease the demand for new investors to purchase Kubota Holdings shares.

Regulatory Risks

We may not be able to obtain regulatory approval for any of the products resulting from our development efforts. Failure to obtain these approvals could materially harm our business.

None of our product candidates have received regulatory approval for marketing in the United States or elsewhere. We will be required to obtain an effective Investigational New Drug Application, or IND, or an Investigational Device Exemption, or IDE, prior to initiating new human clinical trials in the United States, and must submit a New Drug Application, or NDA, Premarket Approval, or PMA, or 510(k) application to obtain marketing approval prior to commercializing any product in the United States. This process is expensive, highly uncertain and lengthy, often taking years until a product is approved for marketing, if at all. Outside of the United States, approval procedures vary among countries and can involve additional product testing, administrative review periods and agreements with pricing authorities. Approval policies or regulations may change and the regulatory authorities have substantial discretion in the product approval process, including the ability to delay, limit, or deny approval of a product candidate for many reasons. Regulatory authorities may disagree with the design or implementation of our clinical trials and we may be unable to demonstrate to the satisfaction of regulatory authorities that a product candidate is safe and effective. Accordingly, there can be no assurance that regulatory authorities will approve any product that we develop.

Our products could be subject to “post-approval” restrictions or withdrawal from the market and we may be subject to penalties if we fail to comply with regulatory requirements, or if we experience problems with our products, when and if any of them are approved.

Any product for which we obtain marketing approval will be subject to continual requirements, review and periodic inspections by applicable regulatory bodies. Even if regulatory approval is granted, the approval may be subject to limitations on the indicated uses for which the product may be marketed. The approval may contain conditions or requirements for costly post-marketing testing and surveillance to monitor the safety or efficacy. Post-approval discovery of previously unknown problems with our products or manufacturing processes, or failure to comply with regulatory requirements, may result in product recall or withdrawal from the market, manufacturing restrictions, suspension of product approval, or fines and penalties.

We may be subject, directly or indirectly, to federal and state healthcare fraud and abuse laws, false claims laws, physician payment transparency laws and health information privacy and security laws. If we are unable to comply, or have not fully complied, with such laws, we could face substantial penalties.

If we obtain FDA approval for any of our product candidates and begin commercializing those products in the United States, our operations may be directly or indirectly, through our customers, subject to various federal and state fraud and abuse laws, including, without limitation, the federal Anti-Kickback Statute, the federal False Claims Act, and physician sunshine laws and regulations. These laws may impact, among other things, our proposed sales, marketing, and education programs. In addition, we may be subject to patient privacy regulation by both the federal government and the states in which we conduct our business. Efforts to ensure that our business arrangements will comply with applicable healthcare laws may involve substantial costs and it is possible that governmental authorities may conclude that our business practices violate applicable law.

If any such actions are instituted against us, and we are not successful in defending ourselves or asserting our rights, those actions could have a significant negative impact on our business.

Risks Relating to Intellectual Property and Other Legal Matters

If our efforts to protect the proprietary nature of the intellectual property related to our product candidates are not adequate, we may be unable to compete effectively in our markets.

The strength of our patents involves complex legal, scientific and bioengineering issues and can be uncertain. In addition to the rights we obtain from our collaborators or licensing partners, we rely upon our own intellectual property, including patents, patent applications and trade secrets. Our patent applications may be challenged or fail to result in issued patents and our existing or future patents may be too narrow to prevent third parties from developing or designing around these patents. Further, there is no uniform, global policy regarding the subject matter and scope of claims allowable in pharmaceutical patents and the criteria applied by patent offices throughout the world to grant patents are not always predictable or uniform.

There is no guarantee that the patent applications we file or in-license will be granted or that the patents we hold would be found valid and enforceable if challenged. Third parties may challenge their validity, enforceability or scope, which may result in such patents being narrowed or invalidated. We may lose our rights to the patents and patent applications we license in the event of a breach or termination of any of our collaboration agreements. Moreover, as a licensee of third parties, we rely on these third parties to file and prosecute patent applications and maintain patents and otherwise protect the licensed intellectual property under some of our license agreements. We have not had and do not have primary control over these activities for certain of our patents or patent applications. We cannot be certain that such activities by third parties have been or will be conducted in compliance with applicable laws and regulations or will result in valid and enforceable patents or other intellectual property rights. Manufacturers may also seek to obtain approval to sell generic or biosimilar versions, or similar designs of our product candidates prior to the expiration of the relevant licensed patents. If the sufficiency of the breadth or strength of protection provided by the patents we license with respect to our product candidates is threatened, it could dissuade others from collaborating with us to develop, and threaten our ability to commercialize, our other product candidates. Further, if we encounter delays in our clinical trials or our development activities are otherwise impeded, the period of time during which we could market our product candidates under patent protection would be reduced. Once the patent life has expired for a product, we may be subject to competition from generic, biosimilar or design knock-offs.

If we are unable to protect the confidentiality of our proprietary information and know-how, the value of our technology and products could be adversely affected.

We rely on a combination of patent, copyright and trade secret protection, nondisclosure agreements and licensing arrangements to establish, protect and enforce our proprietary information and rights. Trade secret protection and confidentiality agreements protect certain proprietary know-how that is not patentable, for processes for which patents are difficult to enforce and for any other elements of our development processes with respect to our product candidates that involve proprietary know-how, information and technology that is not covered by patent applications. Although, we continue to implement protective measures and intend to defend our proprietary rights vigorously, these efforts may not be successful.

Third-party claims of intellectual property infringement may prevent or delay our discovery, development and commercialization efforts with respect to our product candidates.

Our commercial success depends, in part, on avoiding infringement of the patents and proprietary rights of third parties. Although we are not currently aware of any litigation or other proceedings or third-party claims of intellectual property infringement, the biotechnology and pharmaceutical industries are characterized by extensive litigation regarding patents and other intellectual property rights. Other parties may allege that our activities infringe their patents or that we are employing their proprietary technology without authorization. We may not have identified all the patents, patent applications or published literature that affect our business either by blocking our ability to commercialize our product, by preventing the patentability of one or more aspects of our products or those of our licensors or by covering the same or similar technologies that may affect our ability to market our product candidates. Defense of these claims, regardless of their merit, would involve substantial litigation expense and would be a substantial diversion of resources from our business. In the event of a successful claim of infringement against us, we may have to pay substantial damages, obtain one or more licenses from third parties or pay royalties, or we may be enjoined from further developing or commercializing our product candidates and technologies.

We may become involved in lawsuits to protect or enforce our patents or the patents of our licensors, which could be expensive, time consuming and unsuccessful.

Competitors may infringe our patents or the patents of our licensors. To the extent we rely on third parties for our proprietary rights, we will have limited control over the protection and defense of such rights. To counter infringement or unauthorized use, we may be required to file infringement claims, which can be expensive and time consuming. In addition, in an infringement proceeding, a court may decide that a patent of ours or our licensors is not valid or enforceable, or may find that our patents do not cover the technology in question. An adverse result in any litigation or defense proceedings could put one or more of our patents at risk of being invalidated or interpreted narrowly and could put our patent applications at risk of not issuing.

Interference proceedings brought by the U.S. Patent and Trademark Office may be necessary to determine the priority of inventions with respect to our patents and patent applications or those of our collaborators or licensors. An unfavorable outcome could require us to cease using the technology or to attempt to license rights to it from the prevailing party. Litigation or interference proceedings may fail and, even if successful, may result in substantial costs and distraction of our management and other employees.

Because of the substantial amount of discovery required for intellectual property litigation, some of our confidential information could be compromised by disclosure during the litigation proceedings. In addition, there could be public announcements of the results of hearings, motions or other interim proceedings or developments. If securities analysts or investors perceive these results to be negative, it could have a substantial adverse effect on the price of our common stock.

Risks Related to Ownership of Our Common Stock

As the successor issuer to Acucela Inc., a United States public reporting company with shares previously listed on the Tokyo Stock Exchange, Kubota Holdings is subject to a variety of financial and other reporting and corporate governance requirements that may be difficult to satisfy, will raise our costs and may divert resources and management attention from operating our business.

As a public company whose shares of common stock are both registered under the Exchange Act in the United States and listed for trading on the Mothers market of the Tokyo Stock Exchange, or the TSE, in Japan, we have incurred and will continue to incur significant legal, accounting and other expenses related to various financial reporting and corporate governance requirements in both the United States and Japan. Specifically, we are subject to the continued listing standards of the TSE in Japan as well as the disclosure requirements of the Exchange Act in the United States, which together impose significant compliance obligations upon us. These rules and regulations have increased and have made our legal, accounting and financial compliance efforts and costs more time-consuming and costly. These rules and regulations could also make it more difficult for us to attract and retain qualified persons to serve on our board of directors or our board committees or as executive officers.

A limited number of shareholders have the ability to influence the outcome of director elections and other matters requiring shareholder approval.

As of December 31, 2016, Dr. Ryo Kubota, one of our largest shareholders, as an individual, and our directors and executive officers and their affiliates, as a group, beneficially owned approximately 28.1% and 28.7% of our outstanding common stock, respectively, and entities affiliated with SBI Holdings, Inc., collectively SBI Group, own approximately 38.1% of our outstanding common stock.

As a result of their significant holdings of our common stock, Dr. Ryo Kubota and SBI Group, or other future large shareholders, individually have the ability to exert substantial influence over matters requiring approval by our shareholders and can control the outcome of matters requiring approval by our shareholders if they vote together, including electing directors and approving mergers, acquisitions or other business combination or corporate restructuring transactions. This concentration of ownership may discourage, delay or prevent a change in control of our company, which could deprive our shareholders of an opportunity to receive a premium for their stock as part of a sale of our company and might reduce our stock price. These actions may be taken even if they are opposed by our other shareholders. Dr. Kubota acting alone or with these other shareholders, could exert substantial influence over matters requiring approval by Kubota Holdings’ shareholders, including electing directors and approving mergers, acquisitions or other business combination transactions. This concentration of ownership may discourage, delay or prevent a change of control of the Company, which could deprive Kubota Holdings’ shareholders of an opportunity to receive a premium for their stock as part of a sale of the Company and might reduce Kubota Holdings’ stock price. These actions may be taken even if they are opposed by our other shareholders.

Under the Japanese Companies Act, certain material matters require approval of at least two thirds of the shares present or represented by proxy at a duly convened meeting of shareholders at which at least one third of the total number of shares entitled to vote are present or represented by a proxy. If SBI Group is present or represented by proxy at a meeting where matters requiring two-thirds voting requirement are addressed, SBI Group could block the approval of such action. For matters requiring approval of at least a majority of the shares present or represented by proxy at a duly convened meeting of shareholders, SBI Group may be able to prevent attainment of the requisite approvals depending on the level of shareholder participation in such a meeting. As a result of SBI Holdings’ ownership stake, future proposed actions requiring approval of Kubota Holdings’ shareholders may be blocked, which could have a material and adverse effect on Kubota Holdings’ stock price.

Our redomicile to Japan could discourage a takeover attempt, which may reduce or eliminate the likelihood of a change of control transaction and, therefore, the ability of Kubota Holdings’ shareholders to sell their shares for a premium.

Hostile takeovers are rarely attempted in Japan. While Japanese law does not have anti-takeover statutes and the Japan Articles do not include any specific protections against a hostile takeover, such as a shareholder rights plan, certain factors, such as negative social perception and the nature of shareholder bases for Japanese corporations, may make it difficult to complete a hostile takeover, which may reduce or eliminate the likelihood of a change of control transaction and the ability of Kubota Holdings’ shareholders to sell their shares for a potential premium.

Kubota Holdings does not expect to pay dividends in the foreseeable future. As a result, you must rely on stock appreciation for any return on your investment.

Kubota Holdings does not anticipate paying cash dividends on its common stock in the foreseeable future. Any payment of cash dividends will also depend on financial condition, results of operations, capital requirements and other factors and will be at the discretion of the board of directors of Kubota Holdings. Accordingly, you will have to rely on capital appreciation, if any, to earn a return on your investment in Kubota Holdings common stock.

2. Management Policy

(1) Basic Management Policy

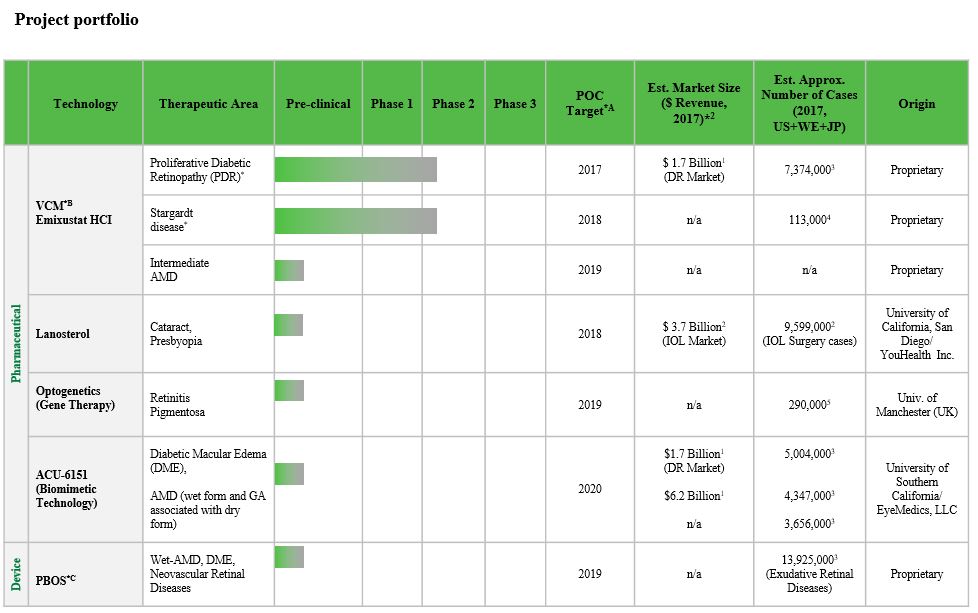

We are a clinical stage ophthalmology company that is committed to translating innovation into a diverse portfolio of drugs and devices to preserve and restore vision for millions worldwide. We have a broad product candidate portfolio of multiple technologies in the preclinical and clinical development stages intended to provide solutions to ophthalmic disorders affecting millions of people worldwide. We are pursuing development of our product candidates for indications such as diabetic retinopathy/diabetic macular edema, cataract, age-related macular degeneration, and blinding orphan retinal diseases such as retinitis pigmentosa and Stargardt disease which primarily affect young adults.

(2) Target Financial Index

The Company believes that it is not appropriate to use a financial index as a target in the light of business administration at this time.

(3) Strategy

Our long-term strategy is to commercialize drugs and devices that will benefit people living with debilitating ophthalmological conditions. To this end, we will pursue research and development opportunities that fulfill the following selection criteria:

| |

| • | product candidates must have significant market potential as assessed by disease prevalence and/or incidence, pricing and reimbursement opportunity, patent protection and competitive positioning; |

| |

| • | pharmaceutical and biotechnology product candidates must interact with a molecular target strongly linked by robust, scientific data to a targeted disease and the link must be validated by external experts in order to enhance the scientific likelihood of success. Device product candidates must have a compelling link between the engineering technology and a mode of action to deliver an anticipated outcome; and |

| |