FORM 10

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 4 TO

FORM 10-SB

ON

FORM 10

General Form For Registration of Securities

of Small Business Issuers

Under Section 12(b) or 12(g) of The Securities Exchange Act of 1934

Dominion Minerals Corp.

(Name of Small Business Issuer in Its Charter)

File No. 000-52696

| Delaware | 22-3091075 |

| (State or Other Jurisdiction of | (I.R.S. Employer Identification Number) |

| Incorporation or Organization) | |

| 410 Park Avenue, 15th Floor, New York, NY | 10022 |

| (Address of Principal Executive Offices) | (Zip Code) |

(212) 231-8171

Issuer's Telephone Number

Securities to be registered pursuant to Section 12(b) of the Act:

Title of Each Class Name of Each Exchange on Which

to be so Registered Each Class is to be Registered

None

Securities to be registered pursuant to Section 12(g) of the Act:

Common Stock $0.0001 Per Share Par Value

AMENDMENT NO. 4 TO FORM 10-SB

This Amendment No. 4 to Form 10-SB on Form 10 amends our Registration Statement on Amendment No. 3 to Form 10-SB as previously filed with the Securities and Exchange Commission on November 21, 2007.

As described in Note 3 to the Company’s financial statements included herein, the Company has restated its financial statements as of and for the periods ended June 30, 2007 and September 30, 2007, to revise the accounting for common stock issued in connection with the conversion on April 1, 2007 of a promissory note previously issued by the Company and services that the Company expected to receive from the holders of the promissory note. As described in Note 3, the Company filed suit on December 23, 2008 in an effort to recover the shares of common stock issued and reached a settlement agreement on February 11, 2009, under which a portion of the shares issued were cancelled or returned to the Company. The Company has re-stated its accounting for the issuance of the shares and has recorded a non-cash charge to income of $2,205,492 in the quarter ended June 30, 2007 related to the shares that will not be returned to the Company and for which the Company will not receive the services it expected.

The restatement of the Company’s financial statements of June 30, 2007 and September 30 2007, as described in Note 3, reduced the Company’s net income for the periods ended June 30, 2007 and September 30, 2007 by $2,205,492. The restatement reduced the total amount of Shareholders’ Equity by $3,230 and increased Current Liabilities by $3,230, as of June 30, 2007 and September 30, 2007. Except for these effects and the inclusion of Note 3 and related revisions to Note 1, paragraph (g), Note 7, paragraph (a), Note 9, paragraph (f), and Note 10, this Amendment No. 4 and the Company’s financial statements included herein are unchanged from the Report previously filed.

This Amendment contains the complete text of the original report with the corrected information appearing in the financial statements.

PART I

The Issuer, Empire Minerals Corp., a Delaware corporation "Company", is electing to furnish the information required in this PART I by supplying the information required by Items 6-12 of Model B of Form 1-A under Alternative 2 of Form 10-SB.

The Company has a wholly-owned subsidiary, Empire Minerals Corp., a Nevada corporation ("Nevada Subsidiary"). When used herein the terms "we", "us" and/or "our" shall mean the Company, and/or the Nevada Subsidiary in the context in which they appear.

This Registration Statement contains forward-looking statements that involve a number of risks and uncertainties. Such forward-looking statements are not historical facts and constitute or rely upon projections, forecasts, assumptions or other forward-looking information. Generally these statements may be identified by the use of forward-looking words or phrases such as "believes", "expects", "anticipates", "intends", "plans", "estimates", "may", and "should". These statements are inherently subject to known and unknown risks, uncertainties and assumptions. Our future results could differ materially from those expected or anticipated in the forward-looking statements. Specific factors that might cause such differences include factors described and discussed in the Description of Business in Item 1 below.

Item 1 Description of Business.

(Item 6. of Model B of Form 1A)

General

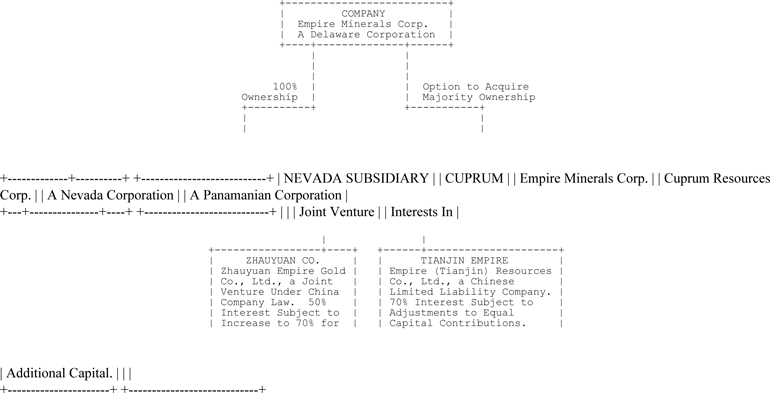

The Company is engaged in the acquisition, exploration, development and operation of mineral and natural resource properties and prospects. The present activities are concentrated on mineral prospects and properties located in the Republic of Panama and in the People's Republic of China.

The Company has entered into an agreement with Bellhaven Copper & Gold, Inc., a British corporation and its wholly owned subsidiary, Cuprum Resources, Corp., a Panamanian corporation. Under this agreement, the Company may acquire a majority ownership interest in Cuprum Resources, Corp. Cuprum holds a mineral Concession from the Republic of Panama on a copper prospect located in the Guariviara Area of Panama.

The Nevada Subsidiary has entered into two joint venture agreements involving mineral properties and/or prospects located within China. These properties are primarily regarded as gold prospects or properties. One of the Chinese joint venture agreements of the Nevada Subsidiary is with Zhaoyuan Dongxing Gold Minerals Co., Ltd, an entity organized under the China Company Law. Under this agreement, the parties have formed Zhaoyuan Empire Gold Corp., Ltd., a Chinese entity in which they each own a 50% interest subject to future adjustment. This jointly held entity holds three mining leases from the Chinese government on gold prospects located in the Shandong Province of China along with certain mining and mill equipment. The other joint venture agreement of the Nevada Subsidiary is with the Tianjin Institute of Geology, a Chinese legal entity. Under this agreement the parties have formed a Chinese limited liability company named Empire (Tianjin) Resources Co., Ltd. This entity was formed to acquire mineral interests in and explore, develop and, if warranted, conduct mining operations on mineral properties located in the Inner Mongolian Autonomous Region of Tianjin Province in the Peoples Republic of China. The Nevada Subsidiary holds a 70% interest in this entity subject to future adjustment to reflect the parties' respective capital contributions.

2

The following chart sets out our present organizational structure:

The proposed operations of the two Chinese Joint Ventures and the acquisition of the majority interest in the Cuprum Resources, Corp. and operations on the Panamanian prospect will require our expenditure of materially more capital than is presently available to us. Our proposed operations include:

o Supervising, and if necessary providing or procuring additional financing for, the operations of the two Chinese Joint Ventures;

o Acquiring the majority interest in the Panamanian corporation holding the mineral concession and providing financing for and supervising its operations;

o Exploring and evaluating additional mineral and natural resource acquisitions; and

o Seeking the necessary additional capital to finance activities.

The following subsections set out information on our history and present and proposed operations and certain of the risk factors associated with us and our securities.

History of the Company

The Company was formed as a Delaware corporation on January 4, 1996 under the name ObjectSoft Corporation. On May 9, 2005, The Company changed its name to Nanergy, Inc. On June 5, 2006, its name was changed to Xacord Corp. On January 3, 2007, the Company changed it's name to Empire Minerals Corp.

We were originally formed in January of 1996 to acquire the business of a predecessor company, Object Soft Corporation, a New Jersey Corporation. This acquisition was completed in the form of a corporate business combination effective January 31, 1996. The acquired business involved the provision of retail Kiosks, which were internet-connected, advertising-interactive Kiosks. The Kiosks were public access terminals that offered terminals that offered information entertainment and the ability to execute financial transactions via a touch screen. This business was unsuccessful and in July of 2001, we filed a Bankruptcy Petition in the Bankruptcy Court for the District of New Jersey. None of our present officers, directors or significant employees were associated with us at the time of or involved in any way in our bankruptcy proceeding. In November of 2004, we exited the Bankruptcy case with no assets, one liability in the form of a convertible promissory note with a principal balance of $100,000.00 and outstanding stock of 195 shares of common stock. We then operated as a shell corporation seeking a new business opportunity either through a corporate business combination or an acquisition of assets.

In September of 2005, we were a party to a business combination in which we acquired the ownership of a New Jersey corporation holding licenses, patents and developments to certain photovoltaic processes. In this transaction, the Company issued 99,455 shares of our common stock. The Company also agreed to issue additional shares of common stock and stock options, if certain economic milestones were met by December 31, 2006. These economic milestones were not met. In 2006, we abandoned our efforts to develop the involved processes.

4

During the period from June 17, 2005 to the date of this Registration Statement, the Company effected three reverse stock splits of its outstanding common stock by amending its Certificate of Incorporation. On June 17, 2005, each outstanding 100 shares was reversed into one share. On August 11, 2006, each 20 outstanding shares were reversed into one share. On January 22, 2007, each 20 outstanding shares were reversed into one share. In all three reverse splits, all fractional shares due to be issued were rounded up to the next full share. Unless otherwise indicated, all references to a number of shares of the Company's common stock have been adjusted to give effect to the applicable stock splits.

On February 20, 2007 we completed a business combination in which we acquired all of the outstanding stock of the Nevada Subsidiary in exchange for shares of our common stock. The combination was structured as a three-party merger in which:

o The Company acquired all of the outstanding stock of the Nevada Subsidiary;

o A Nevada corporation named Xacord Acquisitions Sub Corp. formed and wholly owned by the Company to be used as a vehicle for the transaction was merged into the Nevada Subsidiary;

o The outstanding shares of the common stock of the Nevada Subsidiary as of the Effective Time of the merger were converted into shares of the common stock of the Company on a share for share basis with a total of 26,504,000 shares of the Company's stock issued in this conversion;

o The Company assumed four warrants issued by the Nevada Subsidiary to purchase up to a total of 4,500,000 shares of the Company's Common Stock at $0.10 per share during a three year term. These warrants were held as follows: (i) a warrant for 2,000,000 shares was held by Saddle River Associates, Inc., a financial and business consultant to the Company; (ii) an additional warrant for 500,000 shares was held by Saddle River Associates, Inc.; (iii) a warrant for 1,500,000 shares was held by Pinchas Althaus, President and a director of the Company; and (iv) a warrant for 50,000 shares was held by Chaya Schreiber, a former shareholder of the Nevada Subsidiary. The warrant to purchase 50,000 shares was exercised on March 2, 2007. The remaining three warrants for 4,000,000 were canceled by mutual agreement of the parties on June 1, 2007.

o The Company assumed a contingent obligation of the Nevada Subsidiary to issue warrants to Saddle River Associates, Inc. to purchase up to 500,000 shares of the Company's Common Stock at $0.50 per share during a five-year term from issuance, if the Company obtains specified amounts of additional capital; and

o The Company acquired the rights of the Nevada Subsidiary under a Letter of Intent to enter into the agreements relating to the acquisition of the majority interest in the Panamanian corporation holding the concession to the copper prospect.

o The management of the parties at the time of the business combination consisted of: (i) Diego Roca was the sole officer and director of the Company and of Xacord Acquisition Sub Corp.; and (ii) Pinchas Althaus, Diego Roca and Bruce Minsky were the officers and directors of the Nevada Subsidiary. Messrs. Althaus, Roca and Minsky became the three directors and three of the officers of the Company and the Nevada Subsidiary upon completion of the business combination.

5

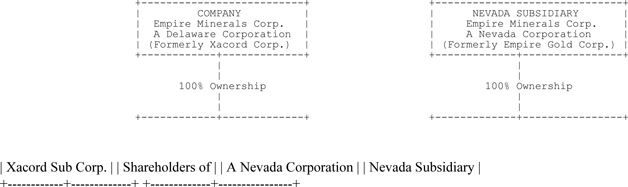

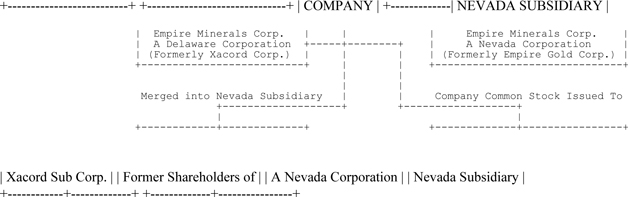

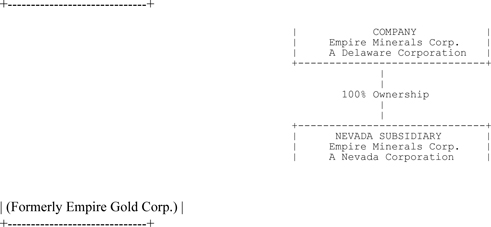

The following diagrams set forth the organizational status of the Company and the Nevada Subsidiary before and after the completion of their business combination.

Status Before Business Combination:

Actions in Business Combination:

6

Status After Business Combination:

Present and Proposed Operations

Dongxing Venture

In 2006, the Nevada Subsidiary entered into a joint venture arrangement with Zhaoyuan Dongxing Gold Minerals Co., Ltd., a Chinese legal entity formed under the laws of the People's Republic of China ("Dongxing"). The control person of Dongxing was at the formation of the joint venture and now is Quizhi Liu, its Chairman and President, who was and is not affiliated with the Company or the Nevada Subsidiary. Under this arrangement, and after receiving the necessary business license in December of 2006, Dongxing and the Nevada Subsidiary formed a Chinese entity for the venture under the China Company Law. The entity is named Zhaoyuan Empire Gold Co., Ltd. ("Zhaoyuan Co."). As set out below, the results of the exploration work on the properties of Zhaoyuan Co. were less than anticipated and these properties are not presently considered material by the Nevada Subsidiary. Unless Zhaoyuan Co. acquires other mineral prospects or additional geological work or its present properties produce beneficial results, we do not plan to invest any material amount of additional funds in this venture. Under the present circumstances, it is unlikely we can salvage or recoup any material amount of this investment. The material terms of the arrangements of this joint venture and the material related events to date of this Amendment No. 3 to the Registration Statement are:

o The formation of Zhaoyuan Co., in which the Nevada Subsidiary and Dongxing each have a 50% equity interest;

7

o Dongxing contributed to Zhaoyuan Co. three Mining Licenses granted by the Shandong Land and Resources Administration Bureau on mineral properties located in the Shandong Province of China, along with certain mining equipment and instruments;

o The Nevada Subsidiary contributed $500,000.00 (USD) to Zhaoyuan Co.;

o The Nevada Subsidiary has exercised its right to appoint three of the five directors of Zhaoyuan Co. including the Chief Director and to appoint the General Manager and Chief Financial Officer and Dongxing has exercised its right to appoint the other two directors;

o The joint venture has a term of 15 years commencing in December of 2006;

o The Nevada Subsidiary has the right and option to contribute an additional $500,000.00 (USD) to the equity capital of Zhaoyuan Co. as the mining activities progress, in which case the Nevada Subsidiary's equity interest in Zhaoyuan Co. would increase to 70% and Dongxing's equity interest would decrease to 30%;

o If the Nevada Subsidiary has invested a total of $1,000,000 in Zhaoyuan Co.and either Dongxing or the Nevada Subsidiary invest any additional capital in Zhaoyuan, the investment would be in the form of non-interest bearing contributed capital which the investing party would have the right to recover from Zhaoyuan Co.'s tax free profit before any sharing of profit would be allocated to the Nevada Subsidiary or Dongxing;

o The arrangement defines an area of mutual interest including all potential mineral properties in Zhaoyuan City in the Shandong Province other than the three properties contributed to Zhaoyuan Co. by Dongxing and a specific property therein on which an independent third party presently holds an Exploration License; and

o The Nevada Subsidiary has the final control over the selection of personnel and operations, provided that Dongxing has a preferential right to provide exploration services to Zhaoyuan Co. to the extent it can do so at comparable market rates.

Following its formation as the joint venture company in December of 2006, Zhaoyuan Co.initiated a program for the renovation, exploration and development of the Dongxing mine. The previous operations on this property involved mining production down to the 150 meter level. Our completed renovation program included:

o General clean-up of the property, de-watering the mine and installation of underground electric and air systems;

o Renovation and upgrading of the concentration mill located on the property;

8

o Expansion of mine cross drifts at the 150 meter level; and

o Completion of safety upgrades to the property followed by the acquisition of safety approvals from local authorities.

Zhaoyuan Co. then conducted an exploration program which included a 1,896.3 meter drill program initiated on May 5, 2007. The program consisted of four holes that were to test the downward potential of gold bearing vein systems observed and previously mined from 0 to 150 meters depth. The target depth of this investigation was between 250m and 500m.

The drilling was completed on July 1, 2007. A thorough cleanup was done, post drilling, to minimize the environmental footprint. The drill core was logged and some sections were split and analyzed by a local state run laboratory. Anomalous gold, between 0.1 and 0.4 g/t was encountered in several sericitic alteration zones. These results were significantly lower than expected and it was concluded to reevaluate our strategy regarding this property.

Of the $500,000 invested by the Company, approximately $461,000 was expended in the renovation of the property and exploration program.

Zhaoyuan Co. is presently exploring the possibility of acquiring additional mineral prospective properties in the area and plans to do additional geological modeling work on the present property. However, unless these efforts are successful, the Company does not plan to invest any material amount of additional funds in this venture, as it will not consider the present property to have material prospects.

The concentration mill located on the present property has a capacity of 60 tons a day. It consists of a jaw crusher, conveyor systems, a ball mill and a flotation cell system. The mill reduces a gold and silver concentrate. Any concentrate produced would be sent to the refinery located in the area. This refinery presently custom-processes such concentrates and retains the silver recovered from the concentrate as payment for the refining fee. We have renovated the mill facilities and achieved successful concentrate results in test mill runs. However, unless Zhaoyuan Co. can acquire and develop a property with sufficient ore reserves, the mill will have no material value. As of November 19, 2007, the Company has not recorded any impairment expense related to this project.

Tianjin Empire Venture

On November 21, 2006, the Nevada Subsidiary entered into a Joint Venture Contract with the Tianjin Institute of Geology, and Mineral Resources, a Chinese legal entity ("Institute") for the formation and operation of a mining joint venture in the form of a Chinese limited liability company to be named Empire (Tianjin) Resources Co., Ltd. ("Tianjin Empire"). Tianjin Empire is to be formed to conduct mineral exploration, development, and, if warranted, mining operations in the Inner Mongolia Autonomous Region of Tianjin Province in the People's Republic of China ("Cooperation Area"). As set out below, the Institute has not yet transferred to Tianjin Empire the mineral properties the Institute is to contribute to the capital of Tianjin Empire. Until mineral properties with a valuation satisfactory to us are contributed to Tianjin Empire by the Institute, the properties proposed for transfer are not considered to be material properties by us. The material terms of this contract and the related material events to the date of this Amendment No. 4 to the Registration Statement are:

9

o The execution of the contract on November 21, 2006 followed by the application for the required business license for Tianjin Empire for its formation and operation which license was granted in April of 2007;

o The Institute is to contribute capital to Tianjin Empire in the amount of Renminbi (the main currency used in China) totaling approximately $300,000.00. It is intended that the Institute's capital contribution will be made in the form of the transfer to Tianjin Empire of mineral resources exploration licenses on properties located in the Cooperation Area. Any properties transferred will be valued for purposes of the Institute's capital contribution by mutual agreement of the Institute and the Nevada Subsidiary. The Institute is obligated to transfer the properties for its capital contribution to Tianjin Empire. The Institute has not presented its valuation on the prospective properties for contribution purposes. The Institute has not timely presented the mineral properties and their valuations for transfer to Tianjin Empire under the terms of the agreement for this venture. We have agreed with the Institute to extend the deadline for the completion of the property transfers by the Institute for its capital contribution and for the payment by the Nevada Subsidiary of the $500,000.00 balance to February 28, 2008.

o The Institute will contribute to Tianjin Empire the mineral information and data held by Licenses on properties located in the Cooperation Area along with the mineral data had by it on that region;

o The Nevada Subsidiary shall contribute a total of $1,000,000.00 (USD) to Tianjin Empire as follows: (i) $200,000.00 paid on July 5, 2007; (ii) $300,000 paid on September 5, 2007; and (iii) $500,000.00 to be paid on or before February 28, 2008;

o The Nevada Subsidiary shall own 70% of Tianjin Empire and the Institute shall own 30%; subject to adjustment so that the respective ownership interests will be equal to the respective capital contributions of the parties;

o Any additional increase in the capital of Tianjin Empire shall be under terms decided by its Board of Directors subject to a first right of refusal by the party agreeing to contribute to a proposed capital increase contribution share not made by the non-contributing party and ownership interests of the parties shall be adjusted to reflect the actual ratio of capital contributions of the parties;

o The Institute shall have a preferential right to provide exploration services to Tianjin Empire at a fair market price;

10

o The Nevada Subsidiary and the Institute shall each have a pre-emptive right of first refusal to purchase all or any part of the other's interest in Tianjin Empire except for transfer of an interest to an affiliate of the transferor;

o Tianjin Empire shall have a five member Board of Directors with the Nevada Subsidiary having the right to appoint three members, including the Chairman, and the Institute having the right to appoint two members, including the Vice-Chairman, and these appointments have been made;

o Certain activities of Tianjin Empire's Board of Directors require unanimous assent of the directors, including: (i) amendment to its Articles of Association; (ii) increase or reduction of its registered capital; (iii) its dissolution; (iv) mortgage or pledge of its assets; or (iv) merger, division or change of form of organization of Tianjin Empire;

o Subject to approval of the Board of Directors, the Nevada Subsidiary shall nominate Tianjin Empire's General Manager and Chief Financial Officer and the Institute shall nominate its Deputy General Manager, which nominations have been completed;

o The contract sets out provisions and guidelines for the operations of Tianjin Empire; and

o The duration of Tianjin Empire shall be for a term of 30 years from the granting of its original business licenses.

The Institute (through an affiliate) received its business license on four mineral prospects on April 13 2007. However, the Institute has not completed all the valuations of the properties for purposes of transferring the properties to Tianjin Empire to make its capital contribution. The Institute and the Nevada Subsidiary have agreed to extend the deadline for the property transfers at a valuation mutually agreed upon by the parties to complete the Institute's capital contribution to February 28, 2008. If the Institute's capital contribution is not timely made, it is the intention of the Company to terminate its participation in the Tianjin Empire venture.

Although Tianjin Empire has preliminary plans to develop an exploration program for the properties covered by the business license issued to the Institute, until the properties are transferred to Tianjin Empire, the Company does not consider the properties to be material.

11

On March 27, 2006, the Nevada Subsidiary entered into an agreement with Universal Gold Corp., a New York corporation ("Universal"). Universal is controlled by Walter Reissman, its Chief Executive Officer, and there were no preexisting affiliations between him or Universal, with the Company or the Nevada Subsidiary. Universal is engaged in the business of providing facilitating services and information to persons and entities desiring to acquire, explore, develop and operate mineral properties in China. The agreement with Universal was related to the Tianjin joint venture in that Universal introduced to the Institute and provided information on mineral properties and prospects in the area of interest. Under this agreement, the Nevada Subsidiary purchased from Universal certain business relationships, due diligence, know-how and research and development in process, and all related relevant and technical information whether tangible or intangible, including without limitation any data, designs, calculations, computer source codes (human readable format), specifications, test and installation, instructions, service and maintenance notes, technical, operating and service and maintenance manuals, user documentation, training materials, and other data, information, know-how and all goodwill associated therewith, in each case which are in the possession of, owned by, developed and/or licensed to Universal which relate to, and are necessary or desirable to enhance, develop, manufacture, assemble, service, maintain, install, operate, use or test and/or explore, mine and/or produce precious metals/minerals, not limited to gold, in China. The Nevada Subsidiary paid Universal $350,000.00 under the agreement. The total payment under the agreement of $350,000 was expensed when paid during the year ended December 31, 2006 as research and development expenses and no value was placed on the purchased assets.

Chinese Regulations

Under the amended "Mineral Resources Law of the PRC", which became effective as of January 1, 1997, all mineral resources of the PRC are owned by the State. The Ministry of Land and Resources ("MLR") is responsible for the supervision and administration of the mining and exploration of mineral resources nationwide. The geology and mineral resources departments of the Chinese Government in the respective provinces, autonomous regions and municipalities are responsible for the supervision and administration of the exploration, development and mining of mineral resources within their own jurisdictions. The companies engaged in the mining or exploration of mineral resources must obtain mining and exploration licenses, as the case may be, which are transferable for consideration only in certain circumstances as provided under PRC laws, subject to approval by relevant administrative authorities.

According to the relevant PRC laws, before the exploration and mining activities relating to mineral resources can commence, the project company must first obtain the exploration license and the mining license, which generally entitles the project company to the exploration and mining rights attached to the relevant mining project. Furthermore, if the mining activities involve gold resources, the Gold Operating Permit must also be obtained.

Holders of exploration licenses and holders of mining licenses are subject to exploration right usage fees and mining right usage fees, respectively. In accordance with the "Administrative Measures on Registration of Mineral Resources Exploitation", mining right usage fees are payable on an annual basis. The rate of mining right usage fee is RMB1,000 per sq.km. of mining area p.a. On the other hand, in accordance with the "Administrative Measures on Registration of Tenement of Mineral Resources Exploration and Survey", exploration right usage fees are calculated according to the size of the exploration area and are payable on an annual basis. The rate of exploration right usage fees for the first year to the third year of exploration is RMB100 per sq.km. of exploration area p.a. From the fourth year of exploration onwards, the rate increases by RMB100 per sq.km of exploration area p.a. However, the annual maximum rate may not exceed RMB500 per sq.km. of exploration area. In addition, according to the amended "Administration Regulation for Collection of Mineral Resource Compensation Fee"), which became effective as of July 3, 1997, holders of mining licenses are subject to mineral resource compensation fees, which accounts for a certain percentage of the sales revenue of such holders. The mineral resource compensation fee is paid on a half-yearly basis.

12

An exploration license must be obtained before carrying out exploration activities. In accordance with the "Administrative Measures on Registration of Tenement of Mineral Resources Exploration and Survey", the applicant must submit the following documents to the MLR or its local branch for the exploration license: (i) an application form for registration and a drawing or map indicating the scope of the blocks for which the applicant is applying; (ii) a copy of the certificate validating the qualification of the exploration unit;

(iii) an exploration working plan and an exploration contract or documents evidencing that the exploration unit and project are entrusted by the State;

(iv) an implementation proposal for the exploration, and its appendixes thereto;

(v) documents of proof showing the source of the funds for the exploration project; and (vi) materials otherwise required by the relevant authority.

After all related documents required by the authority have been provided and submitted, the competent authority shall make a decision within 40 days and notify the applicant of the result. If the application is approved, the applicant must pay the exploration right usage fee before obtaining the exploration license, which is calculated according to the size of the exploration area. The fee is payable on an annual basis.

The maximum valid period of the initial term of the exploration license is three years. An application must be submitted to the original competent registration authority for renewal of such exploration license at least 30 days prior to the expiration date stipulated thereon. Each renewal of valid term cannot exceed two years. If the holder of an exploration license fails to renew the same, such license is automatically annulled upon expiration.

During the term of an exploration license, the holder of such exploration license has the privileged priority to obtain mining rights to the mineral resources in the exploration area, provided that the holder of the exploration license meets the qualifying conditions for mining rights owners. The holder of the exploration license has the rights, among others, to: (i) explore without interference within the area under license during the license term, (ii) construct exploration facilities, and (iii) pass through other exploration areas and adjacent ground to access the licensed area.

13

The holder of an exploration license is obliged to, among other things: (i) begin exploration within the prescribed term, (ii) explore according to a prescribed exploration work scheme, (iii) comply with Chinese laws and regulations regarding labor safety, water and soil conservation, land reclamation and environmental protection, (iv) make detailed reports to local and other licensing authorities, (v) close and occlude the wells arising from exploration work, (vi) take other measures to protect against safety concerns after the exploration work is completed, and (vii) complete minimum exploration expenditures as required by the Administrative Measures on Registration of Tenement of Mineral Resources Exploration and Survey.

In accordance with the "Administrative Measures on Registration of Mineral Resources Exploitation", to apply for the mining license, the applicant must submit the following documents to the MLR or its local branch: (i) an application form for registration and a drawing or map indicating the scope of the mining area; (ii) certificate validating the qualification of the applicant;

(iii) a plan for development and utilization of the mineral resources; (iv) approval documents for establishment of the mining company; (v) an environment influence evaluation report for the exploitation of the mineral resources; and

(vi) materials otherwise required by the relevant authority.

After all related documents required by the authority have been provided and submitted, the competent authority shall make a decision within 40 days and notify the applicant of the result. If the application is approved, the applicant must pay the mining right usage fee before obtaining the mining license, which is calculated according to the size of the mining area and must be paid on an annual basis.

The maximum valid period of the initial term of the mining license is determined according to the construction scale of the mine. For a large size mine, the term may be as long as 30 years, for a middle size mine, 20 years, and for a small size mine, 10 years. An application may be submitted to the original competent registration authority for renewal of such license at least 30 days prior to its expiration date. If the holder of a mining license fails to renew the same, such license is automatically annulled upon expiration.

The holder of a mining license has the rights, among others, to: (i) conduct mining activities during the term and within the mining area prescribed by the mining license, (ii) sell mineral products (except for mineral products that the State Council has identified for unified purchase by designated units),

(iii) construct production and living facilities within the mine area, and (iv) use the land necessary for production and construction, in accordance with applicable laws.

The holder of a mining license is required to, among other things: (i) conduct mine construction or mining activities within a defined time period,

(ii) conduct efficient production, rational mining and comprehensive use of the mineral resources, (iii) pay resources tax and mineral resources compensation (royalties) pursuant to applicable laws, (iv) comply with State laws and regulations regarding labor safety, water and soil conservation, land reclamation and environmental protection, (v) be subject to the supervision and management by the departments in charge of geology and mineral resources, and

(vi) complete and present mineral reserves forms and mineral resource development and use statistics reports, in accordance with applicable law.

14

The holder of an exploration or mining license may transfer its exploration or mining license to others, subject to the approval of MLR.

An exploration license may only be transferred if the transferor has: (i) held the exploration license for two years as of the issue date, or discovered minerals in the exploration area, which are able to be explored or mined further, (ii) held a valid and subsisting exploration license, (iii) completed the stipulated minimum exploration expenditures, (iv) paid the user fees and the price for exploration rights pursuant to the relevant regulations, and (v) obtained the necessary approval from the authorized department in charge of the minerals.

A mining license may only be transferred if the transferor needs to change the ownership of such mining rights because it is: (i) engaging in a merger or split, (ii) entering into equity or cooperative joint ventures with others,

(iii) selling its company's assets, or (iv) engaging in a similar transaction that will result in an alteration of the property ownership of the company.

Additionally, when state-owned assets or state funds are involved in a transfer of exploration licenses and mining licenses, the related state-owned assets rules and regulations apply and a proper evaluation report must be completed and filed with the MLR.

Following documents must be submitted to MLR or its local branch to transfer an exploration or mining license: (i) a transfer application form; (ii) transfer agreement signed between the transferor and transferee; (iii) qualification certificates of the transferee; (iv) certificates proving that the transferor has meet the relevant requirements for transferring exploration license or mining license; (v) report regarding the exploration or mining status of the mineral resources; and (vi) materials otherwise required by the relevant authority. Additionally, when state-owned company transfers its mining license, approval document regarding the mining license transfer issued by its governing authorities should also be submitted.

Speculation in exploration and mining rights is prohibited. The penalties for speculation are that the rights of the speculator may be revoked, illegal income from speculation confiscated and a fine levied.

According to the "Provisions on the Administration of Gold Operating Permit", the applicant for mining of gold minerals must submit the following documents to the National Development Reform Commission ("NDRC"): (i) an application form for exploitation of gold minerals; (ii) a formal map indicating the scope of the mining area; (iii) file records or the approval documents regarding the ore reserves report; (iv) an environment influence evaluation report approved by competent environment protection authorities; (v) the contract and the articles of association of the company and the approval for establishment of the company, if the applicant is a company limited by shares; and (vi) the awards rendered by relevant authorities in respect of any boundary dispute concerning the mining area.

15

The valid period for a Gold Operating Permit varies from five years to 15 years, depending upon the production size of the mine. An application must be submitted to the NDRC for renewal of the Gold Operating Permit at least 30 days prior to the expiration date stipulated thereon.

The holder of a Gold Operating Permit is entitled to exploit gold mineral resources in the areas specified in the Gold Operating Permit, subject to obtaining a corresponding mining license.

Our Chinese operations are subject to the laws governing foreign investments in China, laws governing exploration and mining activities and laws on environmental issues, including the following:

o Foreign Investment in China:

(a) Catalogue of Industries for Guiding Foreign Investments;

(b) Company Law;

(c) Regulation on Company Registration and Administration; and

(d) Laws of the Chinese - Foreign Equity Joint Venture and its Implementation Regulations.

o Exploration/mining activities:

(a) Mineral Resource Law;

(b) Procedures for Administration of Registration of Mining of the Mineral Resources;

(c) Procedures for Administration of Registration of Exploring Area of the Mineral Resources;

(d) Administration Rules on the Transfer of Exploration Rights and Mining Rights;

(e) Safety Production Law;

(f) Regulation of Safety Production License; and

(g) Implementation Rules for the Safety Production License of Non-coal Mines Enterprise.

o Environmental Issues:

(a) Environmental Protection Law;

(b) Law of the Prevention and Control of Environmental Pollution by Solid Waste;

(c) Law of the Prevention and Control of Water Pollution;

(d) Law of Appraising of the Environmental Impacts;

(e) Administration Regulation for Environmental Protection of Construction Projects;

16

(f) Administrative Provisions for Environmental Protection of Construction Projects; and

(g) Administrative Provisions on the Completion-Based Check and Acceptance of Construction Projects.

Panamanian Venture

On March 6, 2007, the Company entered into an Exploration Development Agreement with Bellhaven Copper & Gold, Inc., a corporation organized in British Columbia, Canada ("Bellhaven") and Bellhaven's wholly owned Nevada Subsidiary, Cuprum Resources Corp., a corporation organized in the Republic of Panama ("Cuprum"). Cuprum is the holder of a Mineral Concession from the Republic of Panama on a copper prospect located in the Guariviara area of Panama. This agreement grants the Company an option to acquire up to 75% of the authorized and outstanding stock of Cuprum.

The material terms of this agreement and the material events related to it as of the date of this Registration Statement are:

o The Company is granted the option to acquire up to 75% of Cuprum outstanding stock;

o To acquire 65% of Cuprum's stock the Company must: (i) pay to Cuprum or Bellhaven $2,000,000.00; (ii) issue to Bellhaven shares of the Company common stock as valued under an escrow agreement with a total value of $4,000,000.00; and (iii) expend $15,000.000.00 in exploration and development work on the copper prospect underlying Cuprum's prospect underlying Cuprum's Mineral Concession;

o The first $500,000.00 was paid on March 30, 2007. The 4,000,000 shares of the Company's common stock were deposited into escrow on May 14, 2007. The remaining $1,500,000.00 is payable by the Company in three $500,000.00 annual installments due on March 6, 2008, 2009 and 2010;

o The escrow agreement under which the 4,000,000 shares of the Company's common stock issued to Bellhaven and deposited provides: (i) for the immediate release and delivery to Bellhaven of one-third of the shares (1,333,334); (ii) the release and delivery to Bellhaven of an additional one-third of the shares on each of March 6, 2008 and 2009;

(iii) the adjustment of total shares to be issued to Bellhaven by valuing the shares at the price received by the Company for the first $1,000,000 raised by the sale of the Company's common stock or securities convertible into the common stock sold to non-affiliates of the Company after March 6, 2007, so that, if that price is less than $1.00 the shares to Bellhaven would be increased and if more than $1.00 the total shares to Bellhaven would be decreased; and (iv) the Company has agreed to file a Registration Statement under the U.S. Securities Act of 1933 for the shares of its common stock released to Bellhaven by November 3, 2007 or to include these shares on a "piggy-back" in any Registration Statement filed prior thereto by the Company. During the period from June 25 through July 2, 2007, the Company raised $1,100,000.00 through the sale of notes convertible into shares of its common stock at $1.00 per share, thereby setting the number of shares to be issued to Bellhaven at the total of the 4,000,000 shares already issued and deposited in escrow;

17

o The expenditure by the Company of the $15,000,000.00 for exploration and development work shall be made: (i) $2,000,000.00 by March 5, 2008; of which $1,044,189 has been expended by September 17, 2007;

(ii) a total of $9,000,000.00 by March 5, 2009; and (iii) a total of $15,000,000.00 by March 5, 2010. The Company may, at its discretion, pay any of the required amounts directly to Cuprum, in lieu of funding exploration or development work;

o If the Company pays less than all of the $17,000,000 cash payments and funding due under the agreement but at least 50% of it, the Company will earn an interest in the Cuprum shares which will be proportionately reduced from the 65% total;

o If the Company has earned the full 65% of the Cuprum shares by paying or expending the total $17,000,000.00, it shall have the option to earn an additional 10% of the outstanding stock of Cuprum by completing a Bankable Feasibility Study for the subject property. If this study is not completed, the Company by March 5, 2010, the Company will have to expend an additional $1,000,000.00 for exploration and development work for each successive six month period to keep the agreement in force to enable it to earn the additional 10% interest in Cuprum;

o When the Company has made all of the required payments the operations of Cuprum will continue under the terms of an operating agreement of the three parties;

o If the Company introduces a third party mining company, acceptable to Bellhaven and Cuprum, which agrees to complete the Company's payment and expenditure obligations under the agreement including the one to complete Bankable Feasibility Study, the Company will earn its full 75% interest in Cuprum, Bellhaven's interest will reduce to 25% and the interests of the Company, Bellhaven in Cuprum will then be proportionately reduced by the amount of the interest acquired by the third party;

o If the price of copper on the London Metals Exchange falls below $1.25 for 20 consecutive trading days, all activities and funding under the agreement shall be suspended for up to one year or until that price rises above $1.25 for 90 days, whichever occurs first;

18

o Cuprum is the designated operator to manage and supervise the exploration and development work under budgets and exploration plans jointly agreed upon prior to any implementation of work on the property and Empire shall have sole final approval of all exploration budgets and spending. Empire shall, at its sole discretion, have the right to terminate Cuprum as operator at any time with or without cause after it has acquired a 50% equity position in the property. Empire shall give Cuprum 30 days notice of its intent to terminate Cuprum as operator; and

o The interest of all parties to the agreement are subject to a right of refusal by the other parties to any sale or disposal of an interest in the agreement.

The Cerro Chorcha concession consists of 24,241.91 hectares (ha) in five rectangular blocks and is located in Chiriqui and Bocas Del Toro Provinces of Panama straddling the continental divide about 290 km west of Panama City as shown in the following map.

[MAP]

19

The closest city to Cerro Chorcha is David, Panama's third largest city, which is about 40 km to the southwest of the concession site. Travel from Panama City to David requires approximately six hours by car along a paved two-lane highway. There are a number of daily commercial flights between these two cities.

To both the north and south of the concession site there are a number of small towns and villages all connected by a system of roads and trails. A north-south paved mad passes within the northwest portion of the Cerro Chorcha concession, however this highway occurs on the opposite side of the Continental divide to the main camp which is accessible only by helicopter or on foot.

Currently helicopter flights to the main Cerro Chorcha camp and work area arc out of Rambala a small town 31 kilometers north of the camp. There is a dirt road from Rambala to the village of Soloy. A foot trail leads from Soloy to the Cerro Chorcha camp. This route requires one day and a half to traverse by auto and foot.

Elevations on the property range from about 600 m to 2213 m at the top of Cerro Chorcha and slopes are steep. The higher elevations near the Continental Divide are often cloud covered generated by warm, moist Caribbean air that is lifted daily to cooler heights by air currents. Due to the weather effects, access to the concession site by helicopter is best achieved in the early morning and in the late afternoon.

The mountain terrain is covered in high altitude rain forest with annual rainfall reported to be up to about six meters. Temperatures in this locality average 20(degree) C to 25(degree) C but during some months temperatures can dip down to 5(degree)C at night. Work on the concession site can be undertaken at any time of the year.

The main Chorcha exploration camp consists of four large all-weather buildings powered by a diesel generator. Within the region, personnel, supplies, fuel, water and sufficient space for a mining operation are readily available.

The Cerro Chorcha Mineral Exploration Concession (Contract # 006,2005) at Cerro Chorcha was granted to Cuprum on April 4, 2006. This exploration concession is currently valid and in force.

The area falls under the local jurisdictions of the District of San Lorenzo in Chiriqui Province and the District of Chirqui Grande in the Province of Betas Del Toro.

Mineral title to Cerro Chorcha was previously held under Exploration Concession 93-71 (Geo-Minas, S.A.). These concessions expired in 1999 and were officially cancelled by publication in the Official Gazette (No. 25,029) on April 15, 2004. An application for a new concession (CRC-EXPL 2004-05) was accepted on May 17, 2004 in the name of Cuprum.

Table 1 lists the coordinates of the corner points of the individual five blocks.

20

| Block | Longitude | Latitude | Area | ||

| (hectares) | |||||

| 1 | 82(degree) | 40"' 8(degree) | 408.61" | 10,302.92 | |

| 82(degree) | 47"' 8(degree) | 408.61" | |||

| 82(degree) | 47"' 8(degree) | 354.2" | |||

| 82(degree) | 40"' 8(degree) | 354.2" | |||

| 2 | 82(degree) | 47"' 8(degree) | 403.5" | 2,250.95 | |

| 82(degree) | 003.4"8(degree) | 403.5" | |||

| 82(degree) | 03A" 8(degree) | 39' | 37" | ||

| 82(degree) | 47"' 8(degree) | 39' | 37" | ||

| 3 | 82(degree) | 003.4"8(degree) | 403.5" | 4,705.87 | |

| 82(degree) | 021.4"8(degree) | 403.5" | |||

| 82(degree) | 021.4"8(degree) | 354.2" | |||

| 82(degree) | 003.4"8(degree) | 354.2" | |||

| 4 | 82(degree) | 47"' 8(degree) | 354.2" | 4,480.77 | |

| 82(degree) | 021.4"8(degree) | 354.2" | |||

| 82(degree) | 021.4"8(degree) | 327.7" | |||

| 82(degree) | 47"' 8(degree) | 327.7" | |||

| 5 | 82(degree) | 47"' 8(degree) | 337" | 2,501.40 | |

| 82(degree) | 0.34" 8(degree) | 337" | |||

| 82(degree) | 0.34" 8(degree) | 354.2" | |||

| 82(degree) | 47"' 8(degree) | 354.2" |

The owners of the former concession lodged legal complaints objecting to the cancellation of their concession and the re-application by Cuprum. All legal complaints opposing the cancellation of the concession have been rejected by the Supreme Court of Panama. The new metallic mineral concession at Cerro Chorcha was granted to Cuprum and published in the Official Gazette (No. 25,517) on April 4, 2006. A metallic mineral exploration concession is valid for four years, with extensions available for another four. There are various reporting requirements and a tax on the exploration concessions which begins at US$0.50 per ha the first year and increases to US$1.50 per ha in year five.

The owner of the exploration mineral concession has an exclusive right to the application of an exploitation concession. The terms under which major projects proceed are negotiated with the government.

A portion of the Chorcha concession occurs on an autonomous aboriginal land reserve (Comarca) of the Ngobe-Bugle (see figure 2). There are no permanent habitations in the area of concession.

Cuprum signed an exclusive mineral exploration agreement (the "Agreement") with the Comarca on July 28, 2004. The Agreement grants Cuprum the exclusive rights to explore for minerals and to negotiate a new agreement with the Comarca for the "next phase of activity" upon completion of the exploration phase. The Agreement is valid until the expiration of the Exploration Concession and strictly follows the Panama Mining Code whereby an exploitation concession is granted once the presence of commercial ore is demonstrated.

21

The Agreement (resolution #1 Feb 12, 2006) was signed by the President of the Regional Congress of the NoKribo Region (Mr. Enrique Pineda), the Chief of the NoKribo Region (Mr. Johnny Bonilla), and the president of the Local Congress of the Kanicintti District of the NoKribo Region (Mr. Julian Palacio) and, for Cuprum, the General Manager and Secretary of the Board of Directors (Mr. Alfredo Burgos).

Among the issues covered by the Agreement are: work progress, budgets and reporting; employment and training; land rentals and leasing; development programs; environment, education and culture; force majeure; settlement of conflicts; notification, continuity and applicable laws.

A joint committee was created by Cuprum and the peoples of the Comarca. Monthly meetings of the committee are held to review development and to ensure continued mutual support. All work planned by the Company and Cuprum to date been formally reviewed by and the approved by the operating committee.

The north western portion of the Concession is in the watershed of the Fortuna Hydroelectric Project. Significant development in the hydra-electric reserve area would require approval from Fortuna S.A. (a corporation composed equally of Americas Generation Corp. and the State of Panama) which purchased the publicly owned Institute deRecursos Hidro-electricos y Electrificacion (IE) in 1998.

The mineralized area, as presently known, is far outside of reserve, in fact it is on the other side of the Continental Divide from the Fortuna Project and therefore does not affect the catchment area.

Exploration work can be performed within the boundaries of the hyrdo-electric reserve, as long as we present the plan and procedures that adhere to the respective regulations they will not affect the watershed. A portion of the Palo Seco Reserve Forestal (Forestry Reserve) enters the concession from the north and extends to within about one kilometer north of the main mineralized zone, although legal survey of this has not yet been done.

ANAM (Autoridad Nacional del Ambiente), Panama's environmental agency, is responsible for the administration of the forest reserve.

The Palo Seco Reserve, Forestal is divided into various sub-zones, each of which has a different level of protection. The current management plan does not specifically address mineral exploration and development, however the portion of the Palo Seco Forest Reserve nearest the Chorcha Project is assigned to a highly protected status with entry permitted only for scientific research. In the past exploration has been permitted within the limits of forest reserves, however damages must be mitigated.

22

Prior exploration work on Cerro Chorcha has not resulted in anything that could be considered to be an environmental liability.

Most of Panama consists of island arc assemblages of Cretaceous to Recent age which have resulted from the subduction of the Cocos tectonic plate underneath the Caribbean plate.

In western Panama, where Cerro Chorcha is located, Miocene andesitic to basaltic flows and volcaniclastic rocks of the Caflazas Group have been intruded by Pliocene to Miocene granodiorite and monzonitic rocks of the Tabasara.

The Porphyry copper deposits in Panama are associated with calc-alkaline intrusives. Panama hosts two 'world class' mineralized systems at Cerro Colorado and at Petal Pine, each containing in excess of one billion tonnes of mineralized rock.

At Cerro Chorcha the main area of interest occurs within a composite intrusion, consisting of diorite, quartz diorite, and lesser amounts of monzodiorite. Small bodies and dykes of quartz feldspar porphyry and mafic dykes cut the various intrusive phases and are considered to he post-mineral.

The Cerro Chorcha project contains porphyry copper mineralization with related gold and some reported molybdenum. Oxide and hypogene copper zones are present.

Distal propylitic (chlorite, epidote, and actinolite) alteration surrounds proximal phyllic (sericitie and silicic) zones. Much of the chalcopyrite and bornite mineralization occurs in a quartz-magnetite stockwork and vein facies within the intrusive.

There is a strong structural component to the more or less east-west trending mineralized body which is cut by conjugate NE-SW and NW-SE trending faults.

By analogy with the Cerro Colorado porphyry copper deposit only 35 km to the ESE it is thought that the porphyry copper mineralization at Cerro Chorcha is between three and five million years old.

There are scattered mineralized showings over the entire 242 square kilometer Cerro Chorcha concession.

Porphyry copper (Cu) mineralization with associated gold, silver and molybdenum occur at the main Cerro Chorcha zone (the Guariviara Zone) over an area measuring 1.1 kilometers by 500 meters.

Much of the mineralization is structurally controlled and is related to quartz-magnetite sulphide veining and stockwork zones within the intrusive rocks. Laterally outward from the quartz-magnetite zones, sericite-altered intrusive rock contain fracture/veinlet controlled sulphides. The alteration outward from the phyllic, sericitic and siliceous material is predominantly propylitic.

23

Minerals encountered in the hypogene zone consist of magnetite, chalcopyrite, pyrite, bornite and minor sphalerite and molybdenite. Only minor supergene mineralization has been observed.

Exploration by previous operators has included regional stream sediment geochemistry, prospecting, trenching, soil and rock chip sampling, aerial and ground geophysics, and the drilling of 35 drill holes aggregating 7036 in.

ASARCO Exploration Company of Canada Ltd. discovered the Gu.viviara Zone during a regional stream sediment program initiated in 1969. In 1976, exploration efforts included sampling, mapping and trenching resulted in defining porphyry copper mineralization grading greater than 0.2% Cu over an area of 600 meters by 300 meters.

ASARCO mobilized a drill onto the property. Negotiations with the Government to improve the terms of the concession agreement failed and the company abandoned the project without drilling. A total of over 400 samples were taken and assayed during the ASARCO tenure.

In the period 1990 to 1992 Consultores Geologicos S.A. obtained a concession and confirmed the importance of the zone discovered by ASARCO.

In 1993 the original concession was grouped together in a land package measuring 24,350 ha in an agreement between Consultores Geologicos and GeoRecursos International S.A. and the concession was transferred to Geo-Minas, S.A.

During 1993 a north-south grid was cut with 200m line spacing. A total of sixty-seven soil, 30 rock and 64 chip samples were taken as part of a regional prospecting program.

In the period 1994 and 1995 GeoRecursos International S.A. and Arlo Resources (Arlo) expanded the grid, performed geochemical, geological, and magnetic surveys and regional prospecting work.

GeoRecursos and Arlo completed 27 helicopter-supported diamond drill holes on the Guariviara Zone for a total of 5,765metres.

During 1997 and 1998 Cyprus Minera de Panama (Cyprus) obtained an option on the property. Cyprus expanded the grids, refined the geology of the deposit, mapped and sampled outlying zones, conducted airborne radiometric and magnetic surveys and drilled nine diamond drill holes for a total of 1271 meters. Cyprus left Panama and the concession remained dormant, finally being officially cancelled April 15, 2004.

Following approval of the new Chorcha mineral concession Cuprum and Belhaven undertook the construction of the Chorcha exploration camp and conducted a short program of geologic mapping and one-meter channel samples were collected from several zones of structurally-controlled quartz-magnetite stockwork that appears to host the high-grade copper-gold-silver mineralization. Reported grades within the stockwork zone, returned a total of 61 meters at an average grade of 1.89% Cu, 1.44 g/t Au, and 23.28 g/t Ag.

24

Based upon exploration work on the Cerro Chorcha, Bellhaven and Cuprum have procured a technical report on the property which was prepared in compliance with the National Instrument (NI) 43-101, "Standards of Disclosure For Mineral Projects" adopted by Canadian securities regulatory authorities. However, a company reporting under the U.S. Securities Exchange Act of 1934 may not report resources designated under NI 43-101 based upon a pre-feasibility study. In addition, to designate reserves under the Industry Guide 7 of the U.S. Securities and Exchange Commission a final or bankable feasibility study is required. Accordingly, while Bellhaven, Cuprum and the Company have used the NI 43-101 report in their evaluation of the property, they are not claiming or asserting any reserves for the Cerro Chorcha and it must be considered as an exploration property without any known resources. The proposed program for the Cerro Chorcha is exploratory in nature.

Unless changes are required, the three phase program of geologic investigation will be conducted with Cuprum serving as the operator. Apart from direct geologic work, each phase of the program includes the funding of some social program with the local indigenous groups.

Phase One will include surface prospecting, surface geologic mapping, trenching and sampling as well as an 11-hole, 3,600 meter diamond drill program. The phase one program commenced in March 2007 and has a mutually approved annual budget of 2.1 million dollars.

A contract with Cabo Drilling Corp. (Cabo), of Vancouver, B.C. Canada was signed to perform the drill program on March 14, 2007. In preparation for the drill program, the Company and Cuprum built drill pads and fuel storage facilities. The 3,600 meter drill program was commenced in June 2007. As of November 10, 2007, ten drill holes and 3,441 meters have been drilled with encouraging results.

The first drill hole, CH-07-01, was drilled to test a structurally- controlled quartz-magnetite-sulphide stockwork zone that hosts higher grade copper-gold-silver mineralization than what is observed within the larger mineralized Chorcha porphyry system.

The main zone of mineralization in Hole CH-07-01 begins at the surface, and is the thickest and the highest grade thus far encountered within the Cerro Chorcha porphyry copper deposit.

25

Highlights from Hole CH-07-01 include:

| From/To | Length | Copper | Gold | Silver | ||||||||||

| 0 to 239.4 m | 239.4 meters | 1.20 | % | 0.23 g/t | 6.1 g/t | |||||||||

| including | ||||||||||||||

| 0 to 114m | 114 meters | 2.01 | % | 0.43 g/t | 11.3 g/t | |||||||||

| including | ||||||||||||||

| 52 to 90 m | 38 meters | 2.88 | % | 0.73 g/t | 14.3 g/t | |||||||||

| including detailed analyses | ||||||||||||||

| 52 to 54 m | 2 meters | 3.43 | % | 1.29 g/t | 23.3 g/t | |||||||||

| 54 to 56 m | 2 meters | 2.77 | % | 0.82 g/t | 12.1 g/t | |||||||||

| 56 to 58 m | 2 meters | 2.70 | % | 0.50 g/t | 8.6 g/t | |||||||||

| 58 to 59.6 m | 1.6 meters | 2.83 | % | 0.49 g/t | 7.6 g/t | |||||||||

| 59.6 to 62 m | 2.4 meters | 0.61 | % | 0.11 g/t | 3.7 g/t | |||||||||

| 62 to 64 m | 2 meters | 0.74 | % | 0.09 g/t | 2.4 g/t | |||||||||

| 64 to 65.05 m | 1.05 meters | 1.13 | % | 0.14 g/t | 5.5 g/t | |||||||||

| 65.05 to 66 m | 0.95 meters | 3.67 | % | 0.93 g/t | 15.2 g/t | |||||||||

| 66 to 68 m | 2 meters | 2.02 | % | 0.84 g/t | 9.2 g/t | |||||||||

| 68 to 70 m | 2 meters | 4.26 | % | 2.22 g/t | 28.1 g/t | |||||||||

| 70 to 71.23 m | 1.23 meters | 1.42 | % | 0.44 g/t | 6.1 g/t | |||||||||

| 71.23 to 72.75 m | 1.52 meters | 3.88 | % | 1.19 g/t | 22.5 g/t | |||||||||

| 72.75 to 74 m | 1.25 meters | 3.59 | % | 0.92 g/t | 14.3 g/t | |||||||||

| 74 to 76 m | 2 meters | 3.32 | % | 0.62 g/t | 22.6 g/t | |||||||||

| 76 to 78 m | 2 meters | 3.31 | % | 1.57 g/t | 14.7 g/t | |||||||||

| 78 to 80 m | 2 meters | 2.51 | % | 0.57 g/t | 9.7 g/t | |||||||||

| 80 to 82 m | 2 meters | 3.28 | % | 0.54 g/t | 14.9 g/t | |||||||||

| 82 to 84 m | 2 meters | 4.11 | % | 0.70 g/t | 20.7 g/t | |||||||||

| 84 to 86 m | 2 meters | 3.34 | % | 0.35 g/t | 11.2 g/t | |||||||||

| 86 to 88 m | 2 meters | 3.43 | % | 0.50 g/t | 17.4 g/t | |||||||||

| 88 to 90 m | 2 meters | 4.11 | % | 0.40 g/t | 26.8 g/t | |||||||||

Gold values are by fire assay prep and ICP-MS finish, and copper and silver values by multi-acid digestion and ICP-MS analysis. Analyses were performed by ACME Labs in Vancouver.

Hole CH-07-01 is located about 50 meters east of a 1995 Arlo diamond drill hole, G95-10. Hole G95-10 (north azimuth, -60 inclined) cored 309.1 meters (1014.1 feet) of 0.78 % copper and 0.07 g/t gold.

Hole CH-07-01 is a northwest directed -60 degree angle hole that has encountered extensive quartz-magnetite-sulphide stockwork veins and breccias that host the high grade copper-gold-silver mineralization. The entire drill hole (0 to 239.4 meters) (785.43 feet) averages 1.2 % copper, 0.23 grams per tonne of gold and 6.1 grams per tonne of silver. The hole indicates a vector toward greater thickness and grade at depth.

26

The zone of higher grade copper-gold-silver mineralization in Hole CH-07-01 is associated with stockwork veins, breccias and disseminations hosted in a quartz diorite to quartz monzodiorite porphyry of probable late Tertiary age within the Cerro Chorcha porphyry intrusive complex. The quartz-magnetite- sulphide stockwork zones appear to be a late,structurally-controlled mineralizing event within the porphyry center. Strong silicification and sericite-chlorite-magnetite alteration are closely associated with quartz-magnetite-sulphide stockwork veining and silica-flooded breccia zones with copper sulphide (chalcopyrite and bornite) mineralization. Minor supergene mineralization (covellite, chalcocite, and native copper) occurs within several meters of the surface and along fault zones at depth. The copper and gold mineralization is hosted in both the oxide and sulfide portions of the stockwork, and is open to the northeast, southeast, southwest, and at depth. The true thickness of the mineralized stockwork zone remains unknown as it is in a porphyry/stockwork environment.

Hole CH-07-02 was drilled to test a structurally-controlled quartz-magnetite-sulphide stockwork zone that hosts higher grade copper-gold-silver mineralization than what is observed within the larger mineralized Chorcha porphyry system.

Highlights from Hole CH-07-02 include:

| Length | Copper | Gold | Silver | |||||||||||||

| 5.1 to 246 m | 240.9m | 0.81 | % | 0.08 g/t | 2.9 g/t | |||||||||||

| 16.7 to 807 ft | 790.4 ft | |||||||||||||||

| including | ||||||||||||||||

| 124.9m | 1.32 | % | 0.15 g/t | 4.8 g/t | ||||||||||||

| 16.7 to 426.5 ft | 409.8 ft | |||||||||||||||

Gold values are by fire assay prep and ICP-MS finish, and copper and silver values by multi-acid digestion and ICP-MS analysis. Analyses were performed by ACME Labs in Vancouver.

Hole CH-07-02 is a southeast directed -60 degree angle hole drilled from the same site as Hole CH-07-01 (northwest directed, -60 degree angle hole). Hole CH-07-02 has encountered an extensive quartz-magnetite-sulphide stockwork of veins and breccias that host the higher grade copper-gold-silver mineralization. This stockwork zone is similar to the style of mineralization in Hole CH-07-01, but differs in vein density, alteration intensity and the ratio of chalcopyrite to bornite. The apparent thickness of the stockwork zone in Hole CH-07-02 is about 65 meters. The stockwork zone in Hole CH-07-01 has an apparent thickness of 57 meters. The true thicknesses of the mineralized stockwork zones remain unknown as they are in a porphyry/stockwork environment.

27

The zone of higher grade copper-gold-silver mineralization in Hole CH-07-02 is associated with stockwork veins, breccias and disseminations hosted in a quartz diorite to quartz monzodiorite porphyry within the Cerro Chorcha porphyry intrusive complex. The quartz-magnetite-sulphide stockwork zones appear to be a late, structurally-controlled mineralizing event within the porphyry center. Strong silicification and sericite-chlorite-magnetite alteration are closely associated with quartz-magnetite-sulphide stockwork veining with copper sulphide (chalcopyrite and bornite) mineralization. Supergene mineralization (chalcocite and native copper) occurs within several meters of the surface and along fault zones at depth.

Hole CH-07-03 was drilled to test the continuation of structurally- controlled quartz-magnetite-sulphide stockwork zones that have been observed on-surface and in the two previous drill holes. The stockwork zones typically host higher grade copper-gold-silver mineralization than what is observed within the much larger mineralized Chorcha porphyry system. To date eight drill holes have been completed.

Highlights from Hole CH-07-03 include:

| From/To | Length | Copper | Gold | Silver | |||||||||

| 4 to 319.9 m | 313.9 | m | 0.46 | % | pending | 1.1 g/t | |||||||

| 13 to 1047 ft | 1030 ft | ||||||||||||

| including | |||||||||||||

| 122 to 154 m | 32 | m | 0.82 | % | pending | 2.2 g/t | |||||||

| 400 to 505 ft | 105 ft | ||||||||||||

| 224 to 242 m | 18 | m | 1.04 | % | pending | 2.1 g/t | |||||||

| 735 to 794 ft | 59 ft | ||||||||||||

| 286 to 319.9 m | 33.9 | m | 0.62 | % | pending | 1.3 g/t | |||||||

| 938 to 1047 ft | 109 ft | ||||||||||||

Copper and silver values are by multi-acid digestion and ICP-MS analysis. Gold values by fire assay prep and ICP-MS finish are pending final laboratory results. Analyses were performed by ACME Labs in Vancouver.

Hole CH-07-03 is a southeast directed -60 degree angle hole drilled from a site approximately 130 meters northeast of Holes CH-07-01 and CH-07-02. Hole CH-07-03 has encountered three (3) zones of quartz-magnetite-sulphide stockwork veins and breccias that host the higher grade copper-gold-silver mineralization. These stockwork zones are similar to the style of mineralization in Holes CH-07-01 and CH-07-02, but differ in vein density and alteration intensity. The combined total thickness and grade of the three (3) stockwork zones in Hole CH-07-03 is 74 meters of 0.84 % copper. The true thicknesses of the mineralized stockwork zones remain unknown as they are in a porphyry/stockwork environment.

The copper mineralization at Chorcha is commonly found directly at surface. The bulk of the mineralization in Hole CH-07-03 was associated with the phyllic altered quartz diorite to quartz monzodiorite porphyry that is widespread within the Cerro Chorcha porphyry complex. From previous drill efforts it is known that the mineralization may continues to a depth of over 500 meters. It is interesting to note that the final 33.9 meters of Hole CH-07-03 averaged slightly higher grade (0.62% Copper).

28

Results for Holes CH-07-04, CH-07-05, CH-07-06, CH-07-07, CH-07-08, CH-07-09 and CH-07-10 are pending. Currently, holes CH-07-04 through CH-07-09 are at analytical laboratories pending completion of assay results. In an effort to expedite the turnaround time for drill core assay results, management has retained, in addition to Acme labs of Canada, the services of an additional ISO certified laboratory (SGS Labs) in Peru.

The on-going phase one drill program will serve to test the mineralization at Cerro Chorcha which has a known surface expression of over 1 kilometer in length and over 600meters in width.

Phase Two will include the creation of access road into the Chorcha main zone This phase will include a 15,000 meter drill program of systematic drilling utilizing several diamond drill rigs.

Phase Three will concentrate on the completion of a bankable feasibility study by conducting the appropriate meters of drilling necessary to complete this task.

Throughout the exploration all samples will be prepared and analyzed by an independent 1S0 certified laboratory.

Cuprum and Empire's exploration work on the Cerro Chorcha project is supervised by Michael D. Druecker, Ph.D., P.Geo a Qualified Person as defined in NI 43-101. Mr. Druecker has verified that trench and drill results have been accurately summarized from the official assay certificates provided to the Company.

Cuprum and Empire's drilling sampling procedures follow the Exploration Best Practices Guidelines outlined by the Mining Standards Task Force and adopted by the Toronoto Stock Exchange. Samples have been analyzed by ICP (inductively coupled plasma/mass spectrometry), and gold analysis has been by fire assay with gravimetric finish on a 30gram split.

Quality control measures, including check duplicates and sample standard-assaying are being implemented. A chain of custody review has been completed to ensure the integrity of all sample data. Samples were assayed by Acme Analytical Laboratories, independent of Cuprum and Empire.

On March 1, 2007, the Company entered into an agreement with Silver Global, SA, a Panamanian corporation ("Silver"). Silver is controlled by Mr. Abraham Crocamo, its President. There was no previous affiliation between Mr. Crocamo and the Company or the Nevada Subsidiary. This agreement provides that Silver will perform consulting services for the Company related to the identification, location, definition of mineral business opportunities in Panama and introductions to persons or entities holding potential acquisition properties involving Panama Mineral Concessions and related services. Under this agreement:

o The Company paid Silver a consultancy fee for $75,000.00 for services through February 29, 2008;

29

o The Company may extend the agreement for a one-year term for each year after February 29, 2008 by paying a consultancy fee of $150,000.00 per year;

o In addition to the cash consultancy fees the Company will pay Silver a non-cash transaction fee for any transaction the Company makes involving acquisition of an interest in a Panamanian Mineral Concession, directly or indirectly in any form, with a party introduced to the Company by Silver. Each transaction will be as agreed between then and in the form of a percentage interest in the Mineral Concession interest acquired by the Company and/or stock of the Company; and

o For the transaction fee for the Company, Bellhaven and Cuprum transaction the Company has paid Silver 1,000,000 shares of the Company's common stock (issued as "restricted securities") and if the Company completes its acquisition of the 65% interest in Cuprum, it will transfer to Silver 7.5% of Cuprum's outstanding stock. If the Company earns the additional 10% interest in Cuprum by obtaining the Bankable Feasibility Study, the Company will transfer to Silver 5% of Cuprum's outstanding stock. If the Company completes more than 50% of the full payment due to Bellhaven and Cuprum but not all and thus earns a reduced interest in Cuprum, the balance of the transaction fee to Silver will be proportionally reduced.

Panamanian Regulations

The operations being conducted on the Cerro Chorcha project by Cuprum are subject to the supervisory and administrative laws of Panama which govern mining activities. In addition, these activities are governed by the terms and conditions of the exclusive mineral exploration agreement between Cuprum and the Regional Congress of the NoKaibo Region, the Chief of the NoKaibo Region and the Local Congress of the Kanicintti District of the NoKaibo Region as set out above. The major Panamanian statutes applicable to these operations are the "Code of Mineral Resources," the "General Corporation Law" and the "General Environmental Law."

Environmental Issues

Although our mineral activities are outside the United States of America and not subject to Federal, state or local provisions regarding discharge of material into the environment, they are subject to all the environmental regulations of their respective locales. However, since our proposed activities for the next several years are exploratory in nature, the effect of the regulations regarding the discharge of materials into the environment will not have a material effect upon the capital expenditures, earnings and competitive position of the Company and the Nevada Subsidiary.

30

Plan of Operation

During the 12 month period commencing September 1, 2007, the Company will concentrate its efforts on the Panamanian copper prospect and the two Chinese mineral ventures, and in obtaining additional capital necessary to finance its operations. It will also continue to evaluate additional mineral acquisitions.

The Zhaoyuan Co. will explore the acquisition of other mineral prospects in the general area of its present property and continue to geologically evaluate its present property to determine if any further exploration on it is warranted. If the efforts are unsuccessful, the Company intends to terminate the venture. If Zhaoyuan acquires another prospect or evidence of other promising mineral targets on the present property, the Company will evaluate whether or not to provide additional $500,000 for any future exploration program.