UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM20-F

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2018 |

OR

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number:1-33659

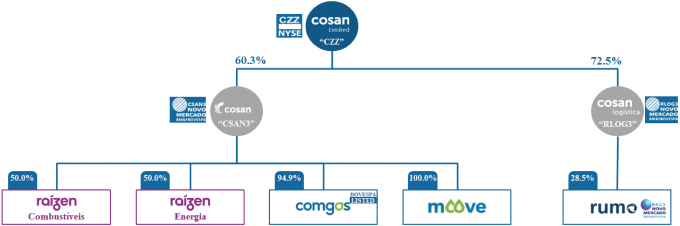

COSAN LIMITED

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Bermuda

(Jurisdiction of incorporation or organization)

Av. Faria Lima, 4,100 – 16th floor

São Paulo – SP,04543-011, Brazil

(55)(11) 3897-9797

(Address of principal executive offices)

Marcelo Eduardo Martins

(55)(11) 3897-9797

ri@cosan.com

Av. Faria Lima, 4,100 – 16th floor

São Paulo – SP,04543-011, Brazil

(Name, Telephone,E-Mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

| Class A Common Shares | | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

The number of outstanding shares as of December 31, 2018 was:

| | |

Title of Class | | Number of Shares Outstanding |

Class A Common Shares, par value $.01 per share | | 148,343,668 |

Class B – series 1 – Common Shares, par value $.01 per share | | 96,332,044 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☒ No ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐ No ☒

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of RegulationS-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, anon-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer ☒ AcceleratedFiler ☐ Non-accelerated Filer ☐ Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule12b-2 of the Exchange Act).

Yes ☐ No ☒

TABLE OF CONTENTS

i

ii

Presentation of Financial and Other Information

We present our consolidated financial statements in accordance with International Financial Reporting Standards, or “IFRS,” as issued by the International Accounting Standards Board, or “IASB,” for Securities and Exchange Commission, or “SEC,” filings.

The consolidated financial statements are presented in Brazilianreais. However, the functional currency of Cosan Limited is the U.S. dollar. The Brazilian real is the currency of the primary economic environment in which Cosan S.A., or “Cosan” or “Cosan S.A.,” Cosan Logística S.A., or “Cosan Logística,” and their respective subsidiaries and jointly-controlled entities, located in Brazil, operate and generate and expend cash. The functional currency for the subsidiaries located outside Brazil is the U.S. dollar, British pound or the Euro. Cosan Limited, Cosan S.A., Cosan Logística and its subsidiaries are collectively referred to as the “Company.”

We have presented our consolidated financial statements for the years ended December 31, 2018, 2017 and 2016, in accordance with IFRS as issued by the IASB. Our consolidated financial statements as of December 31, 2018, 2017 and 2016 and for the years then ended have been audited by KPMG Auditores Independentes, or “KPMG.” KPMG is an independent registered public accounting firm, whose report is included herein.

On June 1, 2011, we and Shell Brazil Holdings B.V., or “Shell,” formed two joint ventures, or the “Joint Venture,” for a combined 50/50 investment, under the names Raízen Combustíveis S.A., or “Raízen Combustíveis” and Raízen Energia e Participações S.A. (currently Raízen Energia S.A.), or “Raízen Energia,” collectively referred to as “Raízen.” Our management evaluates the results of Raízen Energia and Raízen Combustíveis on the same basis as they are evaluated by the management of Raízen, which is on a 100% basis. Accordingly, unless the context requires otherwise, operational information pertaining to Raízen Energia and Raízen Combustíveis included in this annual report refers to 100% of the operations of these businesses. Upon the application of IFRS11- Joint Arrangements, or “IFRS 11,” the Company retrospectively changed the accounting for its investments in Raízen Combustíveis and Raízen Energia, classifying them as investments in joint ventures. As disclosed in “Item 5. Operating and Financial Review and Prospects,” following the adoption of IFRS 11, starting in April 2013 Cosan S.A. no longer proportionally consolidates Raízen Energia and Raízen Combustíveis in its consolidated statement of financial position, statement of profit or loss and comprehensive income and statement of cash flows, and the results of these investments have been presented using the equity method of accounting in accordance with IAS 28R—“Investments in Associates and Joint Ventures.” For further details, see note 9 to our financial statements.

On April 1, 2015, Cosan S.A., through its then subsidiary Rumo Logística Operadora Multimodal S.A. or “Rumo Logística,” acquired 100% of the common shares of ALL – América Latina Logística S.A., or “ALL.” Accordingly, we began consolidating ALL’s results within our own results of operations as from that date.

On September 30, 2016, Cosan S.A. entered into a Share Purchase Agreement with Mansilla Participações Ltda. (a vehicle of TIAA Teachers Insurance and Annuity Association of America), another shareholder in Radar Propriedades Agrícolas S.A. and Radar II Propriedades Agrícolas S.A., or “Radar and Radar II,” through which Cosan S.A. sold part of its shares in Radar and Radar II for an amount of R$1,053.8 million. The consideration was received on November 4, 2016. As a result of this transaction, Cosan S.A. reduced its equity interest in Radar and Radar II from 37.7% to 3.0%. Cosan S.A. retains significant influence over Radar and Radar II through a shareholders’ agreement as described in “Item 7. Major Shareholders and Related Party Transactions.” The criteria used to measure the remaining stake of the investment was the equity method, in accordance with IAS 28, although it is not consolidated due to the limitation on Cosan S.A.’s decision-making power set forth the shareholders’ agreement. The comparative consolidated statement of profit or loss and statements of cash flows have been restated to show the discontinued operation separately from continuing operations.

On October 8, 2016, ALL – América Latina Logística S.A. changed its corporate name to Rumo S.A. or “Rumo.” Subsequently, on December 31, 2016, Rumo Logística was merged into its wholly-owned subsidiary Rumo, as a result of which Rumo S.A. is the successor entity to Rumo Logística.

In 2016, amendments to IAS 16 and IAS 41 changed the accounting requirements for biological assets that fall within the definition of “bearer plants.” These amendments substantially impact Raízen Energia, and the following line items: “Investments in Joint Ventures” in our statement of financial position and “Equity in Earnings of Joint Ventures” in our statement statements of profit or loss.

iii

Furthermore, during 2016, Cosan S.A. identified an immaterial error related to the recognition of tax installment liabilities, related to federal taxes other than income tax, referring to 2011. Cosan S.A. has determined that it was appropriate to revise its financial statements for the years ended December 31, 2016, 2015 and 2014. The revisions to correct the error in the applicable fiscal years are reflected in the financial information herein and will be reflected in future filings containing such information.

On December 12, 2017, we exercised a put option with Shell relating to shares in Companhia de Gás de São Paulo – COMGÁS, or “Comgás,” and bought a total of 21,805,645 shares, which represents 16.77% of Comgás’s share capital for R$1,042 million. As part of the payment, we delivered to Shell 17,187,937 common shares issued by Cosan S.A., representing 4.21% of its capital stock, and also made a cash payment of R$208.7 million. Additionally, we recognized accounts payable referring to the second installment to be settled within one year after the closing of the transaction in the amount of R$208.7 million (plus interest accruing at rate of 3% per year). As a result, Shell ceased to be a shareholder in Comgás.

On December 22, 2017, Cosan S.A. entered into a definitive agreement with Jus Capital Gestão de Recursos Ltda. and Farallon Latin America Investimentos Ltda., for the purchase and sale of credit rights arising from severance claims filed against the Brazilian federal government, which was required to pay compensation for material damages resulting from the fixing of sugar and alcohol prices below their cost of production, in a total amount of R$1,340 million. In addition to the acquisition price, Cosan S.A. will be entitled to receive certain additional payments which are contingent upon the purchaser’s actual receipts from the receivables.

On March 19, 2018, CLE entered into an agreement with ExxonMobil pursuant to which CLE has received exclusive production, import, distribution and marketing rights in Brazil, Bolivia, Paraguay and Uruguay for lubricants and certain other related products under the Mobil brand until November 30, 2038. This agreement came into force on December 1, 2018.

On April 24, 2018, Raízen Combustíveis and its subsidiary Raízen Argentina Holdings S.A.U. entered into a contract for the acquisition of Shell’s downstream business in Argentina. Pursuant to the above-mentioned agreement, Raízen Argentina Holdings S.A.U. acquired 100% of the outstanding share capital of Shell Compañía Argentina de Petróleo S.A and Energina Compañía Argentina de Petróleo S.A., or “Shell Argentina,” for an amount of U.S.$916 million. The acquisition process was completed on October 1, 2018.

On December 21, 2018, Cosan Lubes Investments Limited, or “CLI,” and CVC Fund VII, or “CVC,” entered into an investment agreement pursuant to which CVC will subscribe for shares in Moove’s capital in a total amount of R$562 million (which is equivalent to approximately 30% of Moove’s capital). Following the satisfaction of the applicable conditions provided in the investment agreement, the transaction closed on March 29, 2019. As a result and pursuant to the terms of the investment agreement, Moove received R$434 million at the closing of the transaction and may receive up to approximately R$128 million until 2021, if certain targets set forth in the investment agreement are met.

Forward-Looking Statements

This annual report contains estimates and forward-looking statements, mainly under “Item 3. Key Information—D. Risk Factors,” “Item 4. Information on the Company—B. Business Overview” and “Item 5. Operating and Financial Review and Prospects.” Some of the matters discussed concerning our business and financial performance include estimates and forward-looking statements.

Our estimates and forward-looking statements are mainly based on our current expectations and estimates on projections of future events and trends, which affect or may affect our businesses and results of operations. Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to several risks and uncertainties and are made in light of information currently available to us. Our estimates and forward-looking statements may be influenced by the following factors, among others:

| | • | | general economic, political, demographic and business conditions in Brazil and in the world and the cyclicality affecting our selling prices; |

| | • | | the effects of global financial and economic crises in Brazil; |

iv

| | • | | our ability to implement our expansion strategy in other regions of Brazil and international markets through organic growth, acquisitions or Joint Ventures; |

| | • | | our ability to successfully compete in all segments and geographical markets where we currently conduct business or may conduct businesses in the future; |

| | • | | competitive developments in the segments in which we operate; |

| | • | | our ability to implement our capital expenditure plan, including our ability to arrange financing when required and on reasonable terms; |

| | • | | government intervention resulting in changes in the economy, taxes and tariffs affecting the markets in which we operate; |

| | • | | price of natural gas, ethanol and other fuels, as well as sugar; |

| | • | | equipment failure and service interruptions; |

| | • | | our ability to compete and conduct our businesses in the future; |

| | • | | adverse weather conditions; |

| | • | | changes in customer demand; |

| | • | | changes in our businesses; |

| | • | | our ability to work together successfully with our partners to operate our partnerships (such as the Joint Venture); |

| | • | | technological advances in the natural gas sector, including developments of natural gas for use in other applications, and advances in the development of alternatives to natural gas; |

| | • | | technological advances in the ethanol sector and advances in the development of alternatives to ethanol; |

| | • | | changes in global energy usage; |

| | • | | government intervention and trade barriers, resulting in changes in the economy, taxes, rates, prices or regulatory environment including in relation to our regulated businesses such as Comgás and Rumo; |

| | • | | inflation, depreciation, appreciation and depreciation of thereal; |

| | • | | other factors that may affect our financial condition, liquidity and results of our operations; and |

| | • | | other risk factors discussed under “Item 3. Key Information–D. Risk Factors.” |

The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect” and similar words are intended to identify estimates and forward-looking statements. Estimates and forward-looking statements speak only as of the date they were made, and we undertake no obligation to update or to review any estimate and/or forward-looking statement because of new information, future events or other factors. Estimates and forward-looking statements involve risks and uncertainties and are not guarantees of future performance. Our future results may differ materially from those expressed in these estimates and forward-looking statements. In light of the risks and uncertainties described above, the estimates and forward-looking statements discussed in this annual report might not occur and our future results and our performance may differ materially from those expressed in these forward-looking statements due to but not limited to, the factors mentioned above. Because of these uncertainties, you should not make any investment decision based on these estimates and forward-looking statements.

v

Market Data

We obtained market and competitive position data, including market forecasts, used throughout this annual report from market research, publicly available information and industry publications, as well as internal surveys. We include data from reports prepared by LMC International Ltd., the Central Bank of Brazil (Banco Central do Brasil), or the “Brazilian Central Bank,” the Sugarcane Agroindustry Association of the state of São Paulo (União da Agroindústria Canavieira de São Paulo), or “UNICA,” the Brazilian Ministry of Agriculture, Livestock, and Supply (Ministério da Agricultura, Pecuária e Abastecimento), or “MAPA,” the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística), or “IBGE,” the Brazilian Ministry of Development, Industry and Foreign Trade (Ministério do Desenvolvimento e do Comércio Exterior), or “MDIC,” the Food and Agriculture Organization of the United Nations, or “FAO,” the National Traffic Agency (Departamento Nacional de Trânsito—DENATRAN), the Brazilian Association of Vehicle Manufactures (Associação Nacional dos Fabricantes de Veículos Automotores—ANFAVEA), Datagro Publicações Ltda., F.O. Licht, Czarnikow, Apoio e Vendas Procana Comunicações Ltda., the São Paulo Stock, Commodities and Futures Exchange (B3 S.A. – Brasil, Bolsa, Balcão), or “B3,” the International Sugar Organization, the Brazilian National Economic and Social Development Bank (Banco Nacional de Desenvolvimento Econômico e Social), or “BNDES,” the New York Board of Trade, or “NYBOT,” the New York Stock Exchange, or “NYSE,” the Brazilian Agricultural Research Corporation (Empresa Brasileira de Pesquisa Agropecuária), or “Embrapa,” the Brazilian Secretariat for Foreign Trade (Secretaria de Comércio Exterior), or “Secex,” the National Supply Company (Companhia Nacional de Abastecimento), or “Conab,” the London Stock Exchange, the National Agency of Petroleum, Natural Gas and Biofuels (ANP—Agência Nacional do Petróleo, Gás Natural e Biocombustíveis), or “ANP,” the Brazilian antitrust authority (Superintendência-Geral do Conselho Administrativo de Defesa Econômica), or “CADE,” the National Union of Distributors of Fuels and Lubricants (Associação Nacional das Distribuidoras de Combustíveis, Lubrificantes, Logística e Conveniência), or “Plural,” the Sanitation and Energy Regulatory Agency for the state of São Paulo (Agência Reguladora de Energia de São Paulo), or “ARSESP,” the Brazilian Gas Distributors Association (Associação Brasileira das Empresas Distribuidoras de Gás), or “ABEGÁS,” the Agriculture School of the University of São Paulo (Escola Superior de Agricultura Luiz de Queiroz), or “ESALQ,” the National Waterway Transportation Agency (Agência Nacional de Transportes Aquaviários), or “ANTAQ,” and the National Electric Energy Agency (Agência Nacional de Energia Elétrica), or “ANEEL.” We believe that all market data in this annual report is reliable, accurate and complete.

Terms Used in This Annual Report

In this annual report, we present information in gallons, liters and cubic meters (m³). In addition, we also present information in tons. In this annual report, references to “ton” or “tonne” refer to the metric tonne, which is equal to 1,000 kilograms.

All references in this annual report to “TSR” are to total sugar recovered, which represents the total amount of sugar content in a given quantity of sugarcane.

All references in this annual report to “RTK” mean revenue ton kilometer.

All references in this annual report to “U.S. dollars,” “dollars” or “U.S.$” are to U.S. dollars. All references to the “real,” “reais” or “R$” are to the Brazilianreal, the official currency of Brazil.

Rounding

We have rounding adjustments to reach some of the figures included in this annual report. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

vi

PART I

| Item 1. | Identity of Directors, Senior Management and Advisers |

Not applicable.

| Item 2. | Offer Statistics and Expected Timetable |

Not applicable.

| A. | Selected Financial Data |

The following tables present selected historical financial and operating data for the Company derived from our audited consolidated financial statements. You should read the following information in conjunction with our audited consolidated financial statements and related notes, and the information under “Item 5. Operating and Financial Review and Prospects” in this annual report.

The financial data at and for the fiscal years ended December 31, 2018, 2017, 2016, 2015 and 2014 have been derived from our audited consolidated financial statements prepared in accordance with IFRS as issued by the IASB, unless otherwise stated.

Business Segments and Presentation of Segment Financial Data

We present the following reportable segments:

(1) Raízen Energia: production and marketing of a variety of products derived from sugar cane, including raw sugar (Very High Polarization, or “VHP”), anhydrous and hydrated ethanol, and activities related to energy cogeneration from sugarcane bagasse. In addition, this segment holds interests in companies engaged in research and development on new technology;

(2) Raízen Combustíveis: distribution and marketing of fuels, mainly through a franchised network of service stations under the “Shell” brand throughout Brazil, petroleum refining, the operation of fuel resellers, the manufacture and sale of automotive and industrial lubricants, and the production and sale of liquefied petroleum gas throughout Argentina;

(3) Comgás: distribution of piped natural gas in part of the state of São Paulo to customers in the industrial, residential, commercial, automotive and cogeneration sectors;

(4) Cosan Logística: logistics services for rail transportation, storage and port loading of commodities, mainly for grains and sugar, leasing of locomotives, wagons and another railway equipment;

(5) Moove, consisting of Cosan Lubrificantes e Especialidades S.A., or “CLE,” Stanbridge Group Limited, or “Stanbridge,” Moove Lubricants Limited, or “Moove Lubricants,” (previously known as Comma Oil Chemicals Limited), TTA—SAS Techniques et Technologie Appliquées, or “TTA,” LubrigrupoII, S.A., or “LubrigrupoII,” Cosan Lubrificantes S.R.L, or “Cosan S.R.L” and Commercial Lubricants, LLC (d/b/a Metrolube), or “Metrolube”: production and distribution of lubricants under the Mobil brand in Brazil, Argentina, Bolivia, Uruguay, Paraguay, the United States of America and Europe, as well as in the European and Asian markets under the Comma trademark; and

1

Reconciliation

(6) Cosan Corporate: an online payment services platform and other investments, in addition to the corporate activities of the Company. The Cosan corporate segment includes the financing subsidiaries for the Cosan group.

Following the adoption of IFRS 11, as of April 1, 2013 Cosan S.A. no longer proportionally consolidates Raízen Energia and Raízen Combustíveis in its consolidated statement of financial position, consolidated statement of profit or loss and comprehensive income and consolidated cash flows, and the results from these businesses are accounted for under the line item “Interest in earnings of joint ventures” in our consolidated statement of profit or loss and other comprehensive income.

| | | | | | | | | | | | | | | | | | | | |

| | | As of and for the fiscal year ended December 31, | |

| | | 2018 | | | 2017 | | | 2016 | | | 2015 | | | 2014 | |

| | | (in millions of reais, except where otherwise indicated) | |

Consolidated Profit or Loss Data: | | | | | | | | | | | | | | | | | | | | |

Net sales | | | 16,843.9 | | | | 13,582.5 | | | | 12,518.1 | | | | 12,355.5 | | | | 8,904.7 | |

Cost of sales | | | (12,119.9 | ) | | | (9,232.2 | ) | | | (8,317.5 | ) | | | (8,645.7 | ) | | | (6,353.1 | ) |

| | | | | | | | | | | | | | | | | | | | |

Gross profit | | | 4,724.0 | | | | 4,350.3 | | | | 4,200.6 | | | | 3,709.8 | | | | 2,551.6 | |

| | | | | | | | | | | | | | | | | | | | |

Selling expenses | | | (1,023.5 | ) | | | (1,068.7 | ) | | | (1,037.5 | ) | | | (900.7 | ) | | | (881.5 | ) |

General and administrative expenses | | | (981.8 | ) | | | (935.3 | ) | | | (1,000.7 | ) | | | (911.7 | ) | | | (632.1 | ) |

Other income (expense), net | | | 738.1 | | | | 877.6 | | | | (116.3 | ) | | | 252.3 | | | | (152.8 | ) |

Total operations expenses | | | (1,267.1 | ) | | | (1,126.4 | ) | | | (2,154.5 | ) | | | (1,560.1 | ) | | | (1,666.5 | ) |

| | | | | | | | | | | | | | | | | | | | |

Income before equity in earnings of investees and finance results | | | 3,456.9 | | | | 3,223.9 | | | | 2,046.1 | | | | 2,149.7 | | | | 885.1 | |

Interest in earnings of investees | | | 997.8 | | | | 1,002.3 | | | | 1,565.7 | | | | 703.1 | | | | 580.0 | |

Finance results | | | (1,610.9 | ) | | | (2,751.5 | ) | | | (3,055.8 | ) | | | (2,184.5 | ) | | | (996.8 | ) |

| | | | | | | | | | | | | | | | | | | | |

Profit before taxes | | | 2,843.8 | | | | 1,474.7 | | | | 556.0 | | | | 668.3 | | | | 468.3 | |

Income tax (expense) benefit: | | | | | | | | | | | | | | | | | | | | |

Current | | | (464.9 | ) | | | (134.5 | ) | | | (228.6 | ) | | | (167.7 | ) | | | (143.3 | ) |

Deferred | | | (295.6 | ) | | | (293.9 | ) | | | 166.9 | | | | 198.1 | | | | 119.7 | |

| | | | | | | | | | | | | | | | | | | | |

| | | (760.5 | ) | | | (428.4 | ) | | | (61.7 | ) | | | 30.4 | | | | (23.6 | ) |

Profit from continuing operations | | | 2,083.3 | | | | 1,046.3 | | | | 494.2 | | | | 698.7 | | | | 444.7 | |

(Loss) profit from discontinued operation, net of tax | | | — | | | | — | | | | (35.3 | ) | | | 100.9 | | | | 180.6 | |

| | | | | | | | | | | | | | | | | | | | |

Profit for the period | | | 2,083.3 | | | | 1,046.3 | | | | 458.9 | | | | 799.6 | | | | 625.3 | |

Net income for the period attributable tonon-controlling interests | | | (1,107.7 | ) | | | (495.3 | ) | | | (181.2 | ) | | | (394.0 | ) | | | (465.1 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net income for the period attributable to owners of the parent (including discontinued operations) | | | 975.5 | | | | 551.0 | | | | 277.8 | | | | 405.6 | | | | 160.2 | |

| | | | | | | | | | | | | | | | | | | | |

Consolidated Statement of Financial Position Data: | | | | | | | | | | | | | | | | | | | | |

Cash and cash equivalents | | | 3,621.8 | | | | 4,555.2 | | | | 4,499.6 | | | | 3,505.8 | | | | 1,649.3 | |

Marketable securities | | | 4,202.8 | | | | 3,853.3 | | | | 1,291.6 | | | | 605.5 | | | | 149.7 | |

Inventories | | | 716.3 | | | | 663.1 | | | | 630.8 | | | | 656.9 | | | | 353.7 | |

Property, plant and equipment | | | 12,417.8 | | | | 11,681.6 | | | | 10,726.4 | | | | 9,805.9 | | | | 1,435.9 | |

Intangible assets and goodwill | | | 17,190.4 | | | | 16,973.6 | | | | 17,109.4 | | | | 17,309.7 | | | | 10,286.4 | |

Total assets | | | 56,360.7 | | | | 55,624.5 | | | | 50,469.9 | | | | 52,249.2 | | | | 29,696.3 | |

Current liabilities | | | 6,240.8 | | | | 9,022.3 | | | | 6,629.1 | | | | 6,922.6 | | | | 2,970.9 | |

Non-current liabilities | | | | | | | | | | | | | | | | | | | | |

Loans, borrowings and debentures | | | 22,574.3 | | | | 21,688.9 | | | | 18,338.5 | | | | 18,829.2 | | | | 8,502.6 | |

Preferred shareholders payable in subsidiaries | | | 1,097.5 | | | | 1,442.7 | | | | 1,769.6 | | | | 2,042.9 | | | | 1,926.9 | |

Provision for legal proceedings | | | 1,363.2 | | | | 1,348.2 | | | | 1,268.6 | | | | 1,193.9 | | | | 657.8 | |

Equity attributable to owners of the parent | | | 6,614.4 | | | | 6,038.8 | | | | 6,272.5 | | | | 5,913.7 | | | | 5,795.4 | |

Equity attributable tonon-controlling interests | | | 11,355.0 | | | | 11,020.7 | | | | 9,737.3 | | | | 10,275.5 | | | | 7,615.0 | |

| | | | | | | | | | | | | | | | | | | | |

Total shareholders’ equity | | | 17,969.4 | | | | 17,059.5 | | | | 16,009.8 | | | | 16,189.2 | | | | 13,410.4 | |

| | | | | | | | | | | | | | | | | | | | |

2

| | | | | | | | | | | | | | | | | | | | |

| | | As of and for the fiscal year ended December 31, | |

| | | 2018 | | | 2017 | | | 2016 | | | 2015 | | | 2014 | |

| | | (in millions of reais, except where otherwise indicated) | |

Consolidated Other Financial Data: | | | | | | | | | | | | | | | | | | | | |

Depreciation and amortization | | | 2,061.3 | | | | 1,938.4 | | | | 1,735.3 | | | | 1,178.1 | | | | 678.1 | |

Net debt(1) | | | 13,324.1 | | | | 13,675.9 | | | | 13,861.8 | | | | 15,073.0 | | | | 8,073.3 | |

Working capital(2) | | | 5,718.8 | | | | 4,011.6 | | | | 2,139.9 | | | | (87.4 | ) | | | 594.2 | |

Cash flow provided by (used in): | | | | | | | | | | | | | | | | | | | | |

Operating activities | | | 5,377.9 | | | | 4,088.1 | | | | 3,635.4 | | | | 3,350.6 | | | | 1,117.2 | |

Investing activities | | | (1,498.8 | ) | | | (3,577.4 | ) | | | (727.0 | ) | | | (1,003.1 | ) | | | (308.5 | ) |

Financing activities | | | (5,106.4 | ) | | | (565.7 | ) | | | (1,819.3 | ) | | | (542.6 | ) | | | (658.6 | ) |

Basic earnings per share from continuing operations | | | R$4.00 | | | | R$2.10 | | | | R$1.23 | | | | R$ 1.44 | | | | R$ 0.46 | |

Diluted earnings per share from continuing operations | | | R$3.83 | | | | R$2.05 | | | | R$1.16 | | | | R$ 1.38 | | | | R$ 0.40 | |

Basic earnings/(loss) per share from discontinued operations | | | — | | | | — | | | | (R$0.18 | ) | | | R$ 0.09 | | | | R$ 0.15 | |

Diluted earnings/(loss) per share from discontinued operations | | | — | | | | — | | | | (R$0.18 | ) | | | R$ 0.09 | | | | R$ 0.15 | |

Number of shares outstanding | | | 270,687,385 | | | | 270,687,385 | | | | 270,687,385 | | | | 270,687,385 | | | | 270,687,385 | |

Declared dividends (millions of reais) | | | 425.5 | | | | 792.1 | | | | 975.4 | | | | 531.5 | | | | 445.5 | |

Declared dividends (millions of U.S. dollars) | | | U.S.$ 109.8 | | | | U.S.$ 239.5 | | | | U.S.$ 299.3 | | | | U.S.$ 136.1 | | | | U.S.$ 167.7 | |

Declared dividends per share (reais) | | | R$1.7390 | | | | R$3.2572 | | | | R$3.6851 | | | | R$2.0080 | | | | R$1.6832 | |

Declared dividends per share (U.S. dollars) | | | U.S.$ 0.4488 | | | | U.S.$0.9846 | | | | U.S.$1.1307 | | | | U.S.$ 0.5142 | | | | U.S.$0.6337 | |

Other Operating Data: | | | | | | | | | | | | | | | | | | | | |

Crushed sugarcane (in million tons) | | | 60.1 | | | | 60.7 | | | | 62.2 | | | | 59.9 | | | | 57.1 | |

Sugar production (in million tons) | | | 3.7 | | | | 4.3 | | | | 4.4 | | | | 4.1 | | | | 4.1 | |

Ethanol production (in billion liters) | | | 2.6 | | | | 2.2 | | | | 2.1 | | | | 2.1 | | | | 2.1 | |

Volume of fuel sold (in million liters)(3) | | | 27,521.2 | | | | 25,560.2 | | | | 24,831.5 | | | | 25,076 | | | | 25,027.8 | |

Volume loaded (Cosan Logística)

(in million tons) | | | 10.8 | | | | 13.1 | | | | 13.1 | | | | 11.7 | | | | 11.1 | |

Transported volume (Cosan Logística)

(in million RTK) | | | 56,351.5 | | | | 49,690.5 | | | | 40,270.4 | | | | 44,908.8 | | | | — | |

Natural gas (Comgás) (in million m³) | | | 4,543.3 | | | | 4,292.9 | | | | 4,323.0 | | | | 5,210.9 | | | | 5,458.7 | |

Volume of lubricants and base oil sold

(in million liters) | | | 345.9 | | | | 347.8 | | | | 328.9 | | | | 316.9 | | | | 319.8 | |

| (1) | Net debt consists of current andnon-current debt (including preferred shareholders payable in subsidiaries), net of cash and cash equivalents, marketable securities and derivatives on debt recorded in our consolidated financial statements as othernon-current assets. Net debt is anon-GAAP measure. |

| (2) | Working capital consists of total current assets less total current liabilities. |

| (3) | Starting from 2015 the reported volumes are based on a methodology developed by Sindicom (Sindicato Nacional das Empresas Distribuidoras de Combustíveis e de Lubrificantes), an association of fuel distributors, which excludes volumes sold to other distributors. |

3

The information in the table below presents a reconciliation of Net debt, anon-GAAP financial measure, the most directly comparable IFRS financial measure. Our calculation of these Net debt may differ from the calculation of similarly titled measures used by other companies. Our management believes that disclosure of Net Debt is useful to potential investors as it helps to give them a clearer understanding of our financial liquidity. Net Debt is also used to calculate certain leverage ratios. However, Net Debt is not a measure under IFRS and should not be considered as a substitute for measures of indebtedness determined in accordance with IFRS.

| | | | | | | | | | | | | | | | | | | | |

| | | As of and for the fiscal year ended December 31, | |

| | | 2018 | | | 2017 | | | 2016 | | | 2015 | | | 2014 | |

| | | (in millions ofreais, except where otherwise indicated) | |

Current loans, borrowings and debentures | | | 2,115.3 | | | | 3,903.4 | | | | 2,404.0 | | | | 2,775.5 | | | | 1,056.4 | |

Non-current loans, borrowings and debentures | | | 20,459.0 | | | | 17,785.5 | | | | 15,934.7 | | | | 16,053.7 | | | | 7,446.2 | |

Preferred shareholders payable in subsidiaries | | | 1,097.5 | | | | 1,442.7 | | | | 1,769.6 | | | | 2,042.9 | | | | 1,926.9 | |

Total | | | 23,671.8 | | | | 23,131.6 | | | | 20,108.3 | | | | 20,872.1 | | | | 10,429.5 | |

Cash and cash equivalents | | | (3,621.8 | ) | | | (4,555.2 | ) | | | (4,499.6 | ) | | | (3,505.8 | ) | | | (1,649.3 | ) |

Marketable securities | | | (4,202.8 | ) | | | (3,853.3 | ) | | | (1,291.6 | ) | | | (605.5 | ) | | | (149.7 | ) |

Total | | | (7,824.6 | ) | | | (8,408.5 | ) | | | (5,791.2 | ) | | | (4,111.3 | ) | | | (1,799.0 | ) |

Derivatives on debt | | | (2,523.1 | ) | | | (1,047.2 | ) | | | (455.3 | ) | | | (1,687.8 | ) | | | (557.2 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net debt(1) | | | 13,324.1 | | | | 13,675.9 | | | | 13,861.8 | | | | 15,073.0 | | | | 8,073.3 | |

| | | | | | | | | | | | | | | | | | | | |

| (1) | The Company’s covenants consider preferred shareholders payable in subsidiaries in the calculation of net debt. |

Exchange Rates

The Brazilian foreign exchange system allows the purchase and sale of foreign currency and the international transfer ofreais by any person or legal entity, regardless of the amount, subject to certain regulatory procedures.

Since 1999, the Brazilian Central Bank has allowed thereal/U.S. dollar exchange rate to float freely, which resulted in increasing exchange rate volatility. Until early 2003, thereal declined against the U.S. dollar. Between 2004 and 2008, thereal strengthened against the U.S. dollar, except in the most severe periods of the global economic crisis. Given the recent turmoil in international markets and the current Brazilian macroeconomic outlook, thereal depreciated against the U.S. dollar frommid-2011 to early 2016. Beginning in early 2016 through the end of 2016, thereal appreciated against the U.S. dollar, primarily as a result of Brazil’s changing political conditions. In 2017 and 2018, thereal depreciated 1.5% and 17.1% against the U.S. dollar, respectively. In 2019, to April 26, 2019, thereal depreciated 1.96% against the U.S. dollar. In the past, the Brazilian Central Bank has intervened occasionally to control high volatility in the foreign exchange rates. We cannot predict whether the Brazilian Central Bank or the Brazilian government will continue to permit thereal to float freely or will intervene in the exchange rate market through the return of a currency band system or otherwise. In the future, thereal may fluctuate substantially against the U.S. dollar.

Furthermore, Brazilian law provides that, whenever there is a serious imbalance in Brazil’s balance of payments or there are compelling reasons to foresee a serious imbalance, temporary restrictions may be imposed on remittances of foreign capital abroad. Any such restrictions on remittances of foreign capital abroad may limit our ability to receive dividends from our subsidiaries Cosan S.A. and Cosan Logística S.A. We cannot assure you that such measures will not be taken by the Brazilian government in the future. Exchange rate fluctuation will affect the U.S. dollar value of any distributions we receive from our subsidiaries Cosan S.A. and Cosan Logística S.A., which will be made inreais. See “—D. Risk Factors—Risks Related to Brazil.”

The following tables set forth the selling rate, expressed inreais per U.S. dollar (R$/U.S.$), for the periods indicated:

| | | | | | | | | | | | | | | | |

Year | | Period-end | | | Average(1) | | | Low | | | High | |

2014 | | | 2.656 | | | | 2.354 | | | | 2.197 | | | | 2.740 | |

2015 | | | 3.905 | | | | 3.330 | | | | 2.575 | | | | 4.195 | |

2016 | | | 3.259 | | | | 3.512 | | | | 3.119 | | | | 4.156 | |

2017 | | | 3.308 | | | | 3.193 | | | | 3.051 | | | | 3.381 | |

2018 | | | 3.875 | | | | 3.653 | | | | 3.139 | | | | 4.188 | |

4

| | | | | | | | | | | | | | | | |

Month | | Period-end | | | Average(2) | | | Low | | | High | |

October 2018 | | | 3.718 | | | | 3.756 | | | | 3.637 | | | | 4.027 | |

November 2018 | | | 3.863 | | | | 3.775 | | | | 3.697 | | | | 3.893 | |

December 2018 | | | 3.875 | | | | 3.884 | | | | 3.829 | | | | 3.933 | |

January 2019 | | | 3.652 | | | | 3.747 | | | | 3.652 | | | | 3.860 | |

February 2019 | | | 3.739 | | | | 3.720 | | | | 3.669 | | | | 3.776 | |

March 2019 | | | 3.897 | | | | 3.844 | | | | 3.776 | | | | 3.968 | |

April 2019 (through April 26, 2019) | | | 3.935 | | | | 3.892 | | | | 3.835 | | | | 3.973 | |

Source: Brazilian Central Bank.

| (1) | Represents the average of the exchange rates on the closing of each day during the year. |

| (2) | Represents the average of the exchange rates on the closing of each day during the month. |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

This section is intended to be a summary of more detailed discussion contained elsewhere in this annual report. Our business, financial condition or results of operations could be materially and adversely affected by any of the risks and uncertainties described below. As a result, the market price of our shares could decline, and you could lose all or part of your investment. Additional risks not presently known to us, or that we currently deem immaterial, may also impair our financial condition and business operations.

Risks Related to Our Businesses, the Operations of Our Joint Venture, and Industries in Which We Operate

We may not be successful in reducing operating costs and increasing operating efficiencies.

As part of our strategy, we continue to seek to reduce operating costs and increase operating efficiencies to improve our future financial performance. We may not be able to achieve the cost savings that we expect to achieve as a result of several factors, including increases in the price of our raw materials and other cost inputs. Given the highly competitive markets in which we operate, with prices often being defined based on global supply and demand, it is highly likely that we will not pass on material cost increases, which would materially and adversely affect our financial performance.

The expansion of our business through acquisitions and strategic alliances creates risks that may reduce the benefits we anticipate from these transactions.

We have grown substantially through acquisitions. We may continue to expand by acquiring or investing, directly or indirectly, from time to time, in businesses considered suitable by our management that are consistent with our values and that are expected to generate positive returns. We may also enter into strategic alliances to increase our competitiveness. However, our management is unable to predict whether or when any prospective acquisitions or strategic alliances will occur, or the likelihood of any particular transaction being completed on favorable terms and conditions. Our ability to continue to expand our business through acquisitions or alliances depends on many factors, including our ability to identify acquisitions or access capital markets on acceptable terms. Even if we are able to identify acquisition targets and obtain the necessary financing to make these acquisitions, we could financially overextend ourselves.

Acquisitions, especially involving sizeable enterprises, may present financial, managerial and operational challenges, including diversion of management attention from existing business and difficulties in integrating operations and personnel. Any failure by us to integrate new businesses or manage any new alliances successfully could adversely affect our business and financial performance. Some of our major competitors may be pursuing growth through acquisitions and alliances, which may reduce the likelihood that we will be successful in completing acquisitions and alliances. In addition, any major acquisition we consider may be subject to antitrust and other regulatory approvals. We may not be successful in obtaining required approvals on a timely basis or at all.

5

Acquisitions also pose the risk that we may be exposed to successor liability relating to prior actions involving an acquired company, or contingent liabilities incurred before the acquisition. Due diligence conducted in connection with an acquisition, and any contractual guarantees or indemnities that we receive from sellers of acquired companies, may not be sufficient to protect us from, or compensate us for, actual liabilities. A material liability associated with an acquisition, such as labor or environmental liability, could adversely affect our reputation and financial performance and reduce the benefits of the acquisition.

We may engage in hedging transactions, which involve risks that can harm our financial performance.

We are exposed to market risks arising from the conduct of our business activities—in particular, market risks arising from changes in commodity prices, exchange rates or interest rates. In an attempt to minimize the effects of the volatility of sugar prices and exchange rates on our cash flows and results of operations, we engage in hedging transactions involving commodities and exchange rate futures, options, forwards and swaps. We also engage in interest rate-related hedging transactions from time to time. Hedging transactions expose us to the risk of financial loss in situations where the counterparty to the hedging contract defaults on its contract or there is a change in the expected differential between the underlying price in the hedging agreement and the actual price of commodities or exchange rate. We may incur significant hedging-related losses in the future. We hedge against market price fluctuations by fixing the prices of our sugar export volumes and exchange rates. Since we record derivatives at fair value, to the extent that the market prices of our products exceed the fixed price under our hedging policy, our results will be lower than they would have been if we had not engaged in such transactions as a result of the relatednon-cash derivative expenses. As a result, our financial performance would be adversely affected during periods in which commodities prices increase. Alternatively, we may choose not to engage in hedging transactions in the future, which could have a material adverse effect on our financial performance during periods in which commodities prices decrease.

The costs of complying with current and future legislation related to environmental protection, health and safety, and the contingencies arising from environmental damage and affected third parties may have a material adverse effect on our business, results of operations as well as on our financial condition.

The judicial and administrative penalties, including criminal sanctions, imposed on those who fail to comply with environmental laws are applied irrespective of whether there exists any obligation on such persons to repair any damage caused to the environment. Furthermore, the obligation to repair environmental damage caused may be imposed upon all parties deemed to be involved in such damage, whether directly or indirectly and regardless of such parties’ actual culpability. As a result, when we hire third parties to perform work for us, such as the disposal of waste or vegetation suppression, we are not exempt from liability for any environmental damage caused by these independent contractors. In addition, we can be held liable for any and all consequences arising from the exposure of people to harmful substances or other environmental damage. The costs of complying with current and future legislation related to environmental protection, health and safety, and the contingencies arising from environmental damage and from the imposition of fines and other penalties by environmental agencies and regulators as well as compensation sought by affected third parties may have a material adverse effect on our business, results of operations as well as on our financial condition.

We may be required to expend significant financial resources in order to remedy or contain environmental damage or failures to comply with certain environmental and social obligations. In addition, any such damage ornon-compliance may result in interruptions to our operations pursuant to orders from governmental authorities or restrictions on obtaining financing from government-owned institutions. Any of these developments could have a significant financial impact on us. In addition, the enactment of new regulations may require us to expend significant resources in order to comply with our environmental obligations.

The extensive environmental regulation to which we are subject may also lead to delays in the implementation of new projects given the considerable administrative procedures, and time, that are required to obtain environmental licenses from governmental bodies.

Technological advances could affect demand for our products or require substantial capital expenditures for us to remain competitive.

The development and implementation of new technologies may result in a significant reduction in the costs of sugar and ethanol production. We cannot predict when new technologies may become available, the rate of acceptance of new technologies by our competitors or the costs associated with such new technologies. Advances in the development of alternatives to sugar and ethanol also could significantly reduce demand or eliminate the need for sugar and ethanol as a fuel oxygenate. Any advances in technology which require significant capital expenditures to remain competitive or which otherwise reduce demand for sugar and ethanol will have a material adverse effect on our business and financial performance.

6

We may be unable to implement our growth strategy successfully.

Our future growth and financial performance will depend, in part, on the successful implementation of our business strategy, including: (1) our ability to attract new clients or increase volume from existing clients in specific markets and locations, (2) our capacity to finance investments (through indebtedness or otherwise), (3) our ability to increase our operational capacity and expand our current capacity to supply to new markets, (4) our ability to maintain and renew our existing concessions, (5) our ability to reduce our operating costs and increase operating efficiency, (6) our ability to lead with regards to new technologies and market demands and (7) our ability to integrate our businesses. We cannot assure you that we will be able to achieve these objectives and/or strategies successfully or at all. Our failure to achieve any of these objectives and/or strategies as a result of competitive difficulties, cost increases or restrictions on our ability to invest, among others, may limit our ability to implement our growth strategy successfully. We may need to incur additional indebtedness in order to finance new investments to implement our growth strategy. Unfavorable economic conditions in Brazil and in the global credit markets, such as high interest rates on new loans, reduced liquidity or reduced interest of financial institutions in granting loans, may limit our access to new credit. Furthermore, failure to achieve our expected growth may have a material adverse effect on our business, financial conditions, results of operations and our ability to repay our debt obligations.

We may face conflicts of interest in transactions with related parties.

We engage in business and financial transactions with our controlling shareholder and other shareholders that may create conflicts of interest between our Company and these shareholders. Commercial and financial transactions between our affiliates and us, even if entered into on anarm’s-length basis, create the potential for, or could result in, conflicts of interests.

Lack of service providers for our expansion projects could adversely affect our business.

We are engaged in a number of expansion projects within our concession area that will require a significant number of service providers, which may not be available. Consequently, if we are unable to contract the necessary services due to service industry shortages or a lack of providers with the technical ability to provide the services we require, this could have an adverse effect on our expansion projects or lead to delays in the execution of our expansion projects as new service providers go through an approval process and develop the technical qualification to commence operations. Any delay or failure to commence or continue our expansion projects within our projected timeframe or budget could have a material adverse effect on our business, financial condition and results of operations.

We depend on our information technology systems, and any failure of these systems could adversely affect our business.

We depend on information technology systems for significant elements of our operations, including the storage of data and retrieval of critical business information. Our information technology systems are vulnerable to damage from a variety of sources, including network failures, malicious human acts, and natural disasters. Moreover, despite network security andback-up measures, some of our servers are potentially vulnerable to physical or electronicbreak-ins, computer viruses, and similar disruptive problems. Failures or significant disruptions to our information technology systems or those used by our third-party service providers could prevent us from conducting our general business operations. Any disruption or loss of information technology systems on which critical aspects of our operations depend could have an adverse effect on our business, results of operations, and financial condition.

Further, we store highly confidential information on our information technology systems, including information related to our products. If our servers or the servers of the third party on which our data is stored are attacked by a physical or electronicbreak-in, computer virus or other malicious human action, our confidential information could be stolen or destroyed. Any security breach involving the misappropriation, loss or other unauthorized disclosure or use of confidential information of our suppliers, customers, or others, whether by us or a third party, could have an adverse impact on our business, financial condition and results of operations.

In addition, the ability of our payment services(e-wallet) subsidiary, Payly Soluções de Pagamentos S.A., or “Payly,” to process online payments and provide high quality customer experience depends on the effective uninterrupted operation of internal and third party information technology systems in an integrated manner. Payly also holds certain highly confidential personal and financial data relating to its customers in its information technology systems. Any failures in the information technology systems on which Payly depends or any breaches resulting in the unauthorized disclosure of the personal or financial data of Payly’s customers may adversely affect Payly’s business, financial condition, results of operation and reputation.

7

We could be the target of attempted cyber threats in the future and they could adversely affect our business.

We may be subject to potential fraud and theft by cyber criminals, who are becoming increasingly sophisticated, seeking to obtain unauthorized access to or exploit weaknesses that may exist in our systems. We continuously monitor and develop our information technology networks and infrastructure. We also conduct yearly tests to prevent, detect, address and mitigate the risk of unauthorized access, misuse, computer viruses and other events that could have a security impact on us. Although these measures are taken to ensure that we are protected, to the extent possible, against cyber risks and security breaches, they may not be effective in protecting us against cyber-attacks and other related breaches of our information technology systems. The techniques used to obtain unauthorized, improper or illegal access to our systems, our data or our customers’ data, to disable or degrade service, or to sabotage systems are constantly evolving, may be difficult to detect quickly, and often are not recognized until used against a target. Unauthorized parties may attempt to gain access to our systems or facilities through various means, including, among others, hacking into our systems or those of our customers, partners or vendors, or attempting to fraudulently induce our employees, customers, partners, vendors or other users of our systems to disclose user names, passwords, financial information or other sensitive information, which may in turn be used to access our information technology systems. Certain third-party efforts to access our information technology systems may be supported by significant financial and technological resources, making them even more sophisticated and difficult to detect. Any disruption or loss of information technology systems, on which critical aspects of our operations depend, could have an adverse effect on our business, results of operations and financial condition.

Further, we store highly confidential information on our information technology systems, including information related to our products and customers’ personal data, including financial information. If our servers or the servers of the third parties on which our data is stored are the subject of a physical or electronicbreak-in, computer virus or other cyber risks, our confidential information could be stolen or destroyed. Any security breach involving the misappropriation, loss or other unauthorized disclosure or use of confidential information of our suppliers, customers, or others, whether by us or a third party, could (1) subject us to civil and criminal penalties, (2) have a negative impact on our reputation or (3) expose us to liability to our suppliers, customers, other third parties or government authorities.

We cannot assure you that our information technology systems will not suffer attacks in the future or that we will be able to safeguard the confidential information which we hold adequately. Any failure by us to adequately protect our information technology systems and the confidential data which we hold could have a material adverse effect on our business, financial condition and results of operations.

We are subject to the application of data protection laws. Compliance with such data protection laws could require changes to certain of our business practices, thereby increasing our costs, and noncompliance with the terms of such laws could adversely affect our business. In addition, we may be subject to penalties if we fail to comply with data protection rules.

We operate in a complex regulatory and legal environment that exposes us to compliance and litigation risks that could materially affect our business, financial condition and results of operations. These laws may change, sometimes significantly, as a result of political, economic or social events.

The European Union has adopted a comprehensive overhaul of its data protection regime from the current national legislative approach to a single European Economic Area Privacy Regulation, the General Data Protection Regulation, or the “GDPR,” which came into effect in 2018, and some aspects of our operations or business are subject to the GDPR’s privacy and personal data protection provisions. The EU data protection regime extends the scope of the EU data protection law to all foreign companies processing data of EU residents and imposes heightened requirements on controllers that engage in activities that are within scope of this regulation. It imposes a strict data protection compliance regime with severe penalties of up to the greater of 4% of worldwide turnover or €20 million and, in the case of a data breach, the organization may be required to notify potentially affected individuals.

In addition, on August 14, 2018, the President of Brazil approved Law No. 13,709/2018, a comprehensive data protection law establishing general principles and obligations that apply across multiple economic sectors and contractual relationships (Lei Geral de Proteção de Dados), or the “LGPD.” The LGPD establishes detailed rules for the collection, use, processing and storage of personal data and will affect all economic sectors, including the relationship between customers and suppliers of goods and services, employees and employers and other relationships in which personal data is collected, whether in a digital or physical environment. The obligations established by LGPD will become effective within 18 months from the date of publication of the LGPD, by which date all legal entities will be required to adapt their data processing activities to these new rules. The data protection regime imposes more stringent data protection standards on Brazilian residents. Any breaches of the LGPD may subject us to penalties of up to R$50 million and a requirement to notify parties whose data has been affected.

8

We are currently evaluating the GDPR, the LGPD, their requirements and their potential effect on our business.Implementation of the GDPR and the LGPD could require changes to certain of our business practices, thereby increasing our costs, and noncompliance with their terms could adversely affect our business. Moreover, additional data protection laws may be enacted in Brazil or in other jurisdictions in which we operate. Any such additional laws may require us to make additional changes to our business practices and may expose us to additional penalties fornon-compliance.

Any of these developments could have a material adverse effect on our business, financial condition and results of operations.

Our performance depends on favorable labor relations with our employees and our compliance with labor laws. Any deterioration of those relations or increase in labor costs could adversely affect our business.

All of our employees are represented by labor unions. Our relationships with these organizations are governed by labor agreements or collective bargaining agreements which we negotiate with labor unions. Upon the expiry of such agreements, we are required to renegotiate new agreements with the applicable labor union. As part of these renegotiations, new terms and conditions may be established. In certain cases, these agreements may not be renewed, which could lead to strikes and/or stoppages in our activities and have an adverse impact on our business, financial condition and results of operations. Furthermore, since the enactment of Law No. 13,467/2017, labor agreements and collective bargaining agreements prevail over certain provisions of labor legislation, as stated in items I to XV, of Article611-A, of the Consolidation of Brazilian Labor Laws (Consolidação das Leis do Trabalho), such as, working time arrangements and the manner in which these are recorded, work breaks, and certain employer-specific internal rules, among others. As a result, employers may expand or reduce certain labor rights, provided this is done pursuant to the terms of labor agreements negotiated with unions and/or individual agreements negotiated with the respective employees.

We operate in industries in which the supply, demand and the market price for our products are cyclical and are affected by general economic conditions in Brazil and globally.

The ethanol and sugar industries, globally and in Brazil, have historically been cyclical and sensitive to domestic and international changes in supply and demand. Our sugar production depends on the volume and sucrose content of the sugarcane that we cultivate or is provided to us by farmers located near our plants. Crop yields and sucrose content of the sugarcane mainly depend on weather conditions, such as rainfall and temperature, which may vary and may be influenced by global climate change.

Weather conditions have caused volatility in the ethanol and sugar sectors and, consequently, in our operational results by causing crop failures or reduced harvests. Floods, droughts and frosts, which can be influenced by global climate change, may affect the supply and prices of the agricultural commodities we sell and use in our business. Future climate conditions may reduce the quantity of sugar and sugarcane that we can obtain in a given crop or the sucrose content of the sugarcane. In addition, our production of sugar and ethanol is contingent on our ability to incur capital expenditures to renew sugarcane crops.

Historically, the international sugar market has experienced periods of limited supply, causing sugar prices and industry profit margins to increase, followed by an expansion in the industry that results in oversupply, causing declines in sugar prices and industry profit margins. In addition, fluctuations in prices for ethanol or sugar may occur, for various other reasons, including factors beyond our control, such as:

| | • | | reduced demand for motor vehicles powered by internal combustion engines; |

| | • | | fluctuations in gasoline prices; |

| | • | | variances in the production capacities of our competitors; and |

| | • | | the availability of substitute goods for the ethanol and sugar products we produce. |

The prices we are able to obtain for sugar depend, in large part, on prevailing market conditions. These market conditions, both in Brazil and internationally, are beyond our control. The wholesale price of sugar has a significant impact on our profits. Like other agricultural commodities, sugar is subject to price fluctuations resulting from weather, natural disasters, harvest levels, agricultural investments, government policies and programs for the agricultural sector, domestic and foreign trade policies, shifts in supply and demand, increasing purchasing power, global production of similar or competing products, and other factors beyond our control. In addition, a significant portion of the total worldwide sugar production is traded on exchanges and thus is subject to speculation, which could affect the price of sugar and our results of operations.

9

The price of sugar, in particular, is also affected by producers’ compliance with sugar export requirements and the resulting effects on domestic supply. As a consequence, sugar prices have been subject to high historical volatility. Competition from alternative sweeteners, including saccharine and high fructose corn syrup, known as “HFCS,” changes in Brazilian or international agricultural or trade policies or developments relating to international trade, including those under the World Trade Organization, are factors that can directly or indirectly result in lower domestic or global sugar prices. Any prolonged or significant decrease in sugar prices could have a material adverse effect on our business and financial performance.

Ethanol is marketed as a fuel additive to reduce vehicle emissions from gasoline, as an enhancer to improve the octane rating of gasoline with which it is blended or as a substitute fuel for gasoline. As a result, ethanol prices are influenced by the supply of and demand for gasoline, and our business and financial performance may be materially adversely affected by fluctuations in the demand for and/or price of gasoline. The increase in the production and sale of flex fuel vehicles (hybrid vehicles, that run with ethanol or gasoline or both combined in any proportion) has resulted, in part, from lower taxation, since 2002, of such vehicles compared to gasoline only cars. This favorable tax treatment may be eliminated and the production of flex fuel vehicles may decrease, which could adversely affect demand for ethanol.

If we are unable to maintain sales at generally prevailing market prices for sugar and ethanol in Brazil and internationally, or if we are unable to export sufficient quantities of ethanol and sugar to assure an appropriate domestic market balance, our ethanol and sugar business as well as our cash flow may be adversely affected.

Ethanol prices are directly influenced by sugar and gasoline prices, so that a decline in those prices will adversely affect both our ethanol and sugar businesses.

The price of ethanol generally is closely associated with the price of sugar and is increasingly becoming correlated to gasoline prices in local market. A vast majority of ethanol in Brazil is produced at sugarcane mills that produce both ethanol and sugar. Because sugarcane millers are able to alter their product mix in response to the relative prices of ethanol and sugar, this results in the prices of both products being directly correlated, and the correlation between them may increase over time. In addition, sugar prices in Brazil are determined by prices in the world market, so that there is a correlation between Brazilian ethanol prices and world sugar prices.

Because flex fuel vehicles allow consumers to choose between gasoline and ethanol at the pump rather than at the showroom, ethanol prices are now becoming increasingly correlated to gasoline prices and, consequently, oil prices. We believe that the correlation among the three products will increase over time. Accordingly, a decline in sugar prices will have an adverse effect on the financial performance of our ethanol and sugar businesses, and a decline in oil prices may have an adverse effect on that of our ethanol business, including on its cash flows.

We may not successfully implement our plans to sell energy from our cogeneration projects, and the Brazilian government’s regulation of the energy sector may adversely affect our business and financial performance.

Our current total installed energy cogeneration capacity is used to generate energy for our own industrial operations and to sell surplus energy to the Brazilian energy grid. The Brazilian government regulates the energy sector extensively. We may not be able to satisfy all the requirements necessary to enter into new contracts or to otherwise comply with Brazilian energy regulation. Changes to the current energy regulation or federal authorization programs, and the creation for more stringent criteria for qualification in future public energy auctions, in addition to lower prices, may adversely affect our results of operations from our cogeneration business.

Any failure in the implementation of these plans may have a material adverse effect on our business, financial condition and results of operations.

10

A reduction in market demand for ethanol or a change in governmental policies requiring ethanol be added to gasoline may have a material adverse effect on our business.

We produce and sell three different types of ethanol: hydrous ethanol, anhydrous ethanol for fuel and industrial ethanol. The primary type of ethanol consumed in Brazil is hydrous ethanol, which is used as an alternative to gasoline for flex fuel vehicles (as opposed to anhydrous ethanol which is used as an additive to gasoline).

Governmental authorities of several countries, including Brazil and the United States, currently require the use of anhydrous ethanol as an additive to gasoline. Since 1997, the Brazilian Sugar and Alcohol Inter-ministerial Council (Conselho Interministerial do Açúcar e Álcool), or “CIMA,” has set the percentage of anhydrous ethanol that must be used as an additive to gasoline. According to CIMA Resolution No. 1 dated March 4, 2015, the current anhydrous ethanol percentage for regular gasoline is 27% and for additive/premium gasoline is 25%. Approximatelyone-half of all fuel ethanol in Brazil is used to fuel automobiles that run on a blend of anhydrous ethanol and gasoline; the remainder is used in either flex fuel vehicles or vehicles powered by hydrous ethanol alone. Other countries have similar governmental policies requiring various blends of anhydrous ethanol and gasoline. In addition, flex fuel vehicles in Brazil are currently taxed at lower levels than gasoline-only vehicles, which has contributed to the increase in the production and sale of flex fuel vehicles. Any reduction in the percentage of ethanol required to be added to gasoline or increase in the levels at which flex fuel vehicles are taxed in Brazil, as well as growth in the demand for natural gas and other fuels as an alternative to ethanol, lower gasoline prices or an increase in gasoline consumption (versus ethanol), may cause demand for ethanol to decline and affect our business. In addition, ethanol prices are influenced by the supply and demand for gasoline; therefore, a reduction in oil prices resulting in a decrease in gasoline prices and an increase in gasoline consumption (versus ethanol), may have a material adverse effect on our business, results of operations and financial condition.

Government policies and regulations could have a material adverse effect on our operations and profitability.

Government policies in Brazil and elsewhere, in each case whether at the federal, state or local level, may adversely affect the supply, and demand for, and prices of, our products or restrict our ability to do business in our existing and target markets, which could adversely affect our financial performance.

Agricultural production and trade flows are significantly affected by Brazilian federal, state and municipal, as well as foreign, government policies and regulations. Governmental policies affecting the agricultural industry, such as taxes, tariffs, duties, subsidies and import and export restrictions on agricultural commodities and commodity products, may influence industry profitability, the planting of certain crops versus others, the uses of agricultural resources, the location and size of crop production, the trading levels for unprocessed versus processed commodities, and the volume and types of imports and exports.

Our gas distribution operations are currently concentrated in the state of São Paulo. Any changes affecting governmental policies and regulations regarding natural gas in the state of São Paulo (at the federal, state or municipal level) may have a material adverse effect on our business and financial performance.

In addition, petroleum and petroleum products have historically been subject to price controls in Brazil. Currently there is no legislation or regulation in force giving the Brazilian government the power to set prices for petroleum, petroleum products, ethanol or vehicular natural gas. However, given that Petrobras, the only supplier ofoil-based fuels in Brazil, is a government-controlled company, prices of petroleum and petroleum products are subject to government influence, resulting in potential inconsistencies between international prices and internal oil derivative prices that affect our business and our financial results.

As a payment institution (instituição de pagamento) and payment scheme settlor (instituidor de arranjo de pagamento) in Brazil, Payly is subject to Brazilian laws and regulations relating to electronic payments in Brazil, comprised of Brazilian Federal Law No. 12,865/13 and related rules and regulations. Any failure by Payly to comply with such legislation could result in disciplinary or punitive action by the relevant regulators. Furthermore, we cannot assure you that Payly will be able to obtain and maintain all required operating licenses. Any of these developments could have a material adverse effect on Payly’s business, financial condition and results of operations.

11

Raízen Energia, Raízen Combustíveis and Moove are subject to the application of regulatory penalties in the event ofnon-compliance with the terms and conditions of their respective authorizations, including the possible revocation of such authorizations.

Raízen Energia performs generation activities in accordance with the regulation applicable to the energy sector and with the terms and conditions of authorizations granted by the Brazilian government through ANEEL. The duration of such authorizations varies from 20 to 35 years.

ANEEL may apply regulatory penalties to Raízen Energia in the event ofnon-compliance with the authorizations or with the regulations applicable to the energy sector. Such penalties may include, depending on the seriousness of the infraction, warnings, fines (in some cases up to 2% of our revenues for the last 12 months), restrictions on Raízen Energia’s operations, temporary suspension from participating in public bidding procedures to obtain new permissions, authorizations and concessions, prohibition from contracting with ANEEL, and revocation of its authorizations.

In addition, Raízen Combustíveis conducts its fuel distribution activities and Moove manufactures and distributes lubricants and base oil in accordance with the rules and regulations applicable to the oil and gas sector in Brazil as well as with the terms of the licenses and permits granted to them by the Brazilian government acting through the ANP. Failure to comply with the applicable rules and regulations or with the terms of the relevant licenses and permits may result in fines and other penalties (including confiscation or destruction of products, cancellation of product registrations, bans on certain facilities, and revocation of existing licenses and permits, among others). The applicable fines vary between R$5 thousand and R$5 million, depending on the gravity of the infraction.

Furthermore, the electricity trading operations of WX Energy Comercializadora de Energia Ltda., or “WX Energy,” which Bioenergia Barra Ltda., a wholly-owned subsidiary of Raízen Energia, acquired on July 5, 2018, are highly regulated and supervised by the Brazilian government, including through ANEEL as well as other regulatory authorities. Such regulatory authorities have discretionary authority to implement and change policies, interpretation and rules applicable to different aspects of WX Energy’s business, especially its operations, maintenance, safety, compensation and inspection. Any significant regulatory measure implemented by the competent authorities may impose a significant burden on WX Energy’s activities.

Raízen Energia, Raízen Combustíveis, Moove and WX Energy cannot assure that they will not be penalized by ANEEL, ANP or other regulatory authorities, as applicable, nor can they assure you that they will comply with all terms and conditions of their authorizations and with the regulation applicable to their respective businesses, which may have a material adverse effect on our business, results of operations and financial condition.

We face significant competition, which may have a material adverse effect on our market share and profitability.