UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the Quarterly Period Ended March 31, 2009 | ||

| OR | ||

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to

Commission File No. 000-52934

ZST DIGITAL NETWORKS, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 20-8057756 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

Building 28, Huzhu Road

Zhongyuan District, Zhengzhou, People’s Republic of China

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES)(ZIP CODE)

(86) 371-6771-6850

(COMPANY’S TELEPHONE NUMBER, INCLUDING AREA CODE)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | |

Non-accelerated filer o | Smaller reporting company x | |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The number of shares outstanding of the registrant’s Common Stock, par value $0.0001 per share, was 17,455,000 as of June 12, 2009.

ZST DIGITAL NETWORKS, INC.

FORM 10-Q

For the Quarterly Period Ended March 31, 2009

INDEX

| Part I | Financial Information | 3 | |

| Item 1. | Financial Statements | 3 | |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 4 | |

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 12 | |

| Item 4. | Controls and Procedures | 12 | |

| Part II | Other Information | 13 | |

| Item 1. | Legal Proceedings | 13 | |

| Item 1A. | Risk Factors | 13 | |

| Item 2. | Unregistered Sale of Equity Securities and Use of Proceeds | 13 | |

| Item 3. | Default Upon Senior Securities | 14 | |

| Item 4. | Submission of Matters to a Vote of Security Holders | 14 | |

| Item 5. | Other Information | 14 | |

| Item 6. | Exhibits | 14 | |

| Signatures | 15 | ||

2

The accompanying unaudited financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America for interim financial information and with the instructions to Form 10-Q. Accordingly, they do not include all of the information and footnotes required by generally accepted accounting principles for complete financial statements. The accompanying unaudited financial statements reflect all adjustments that, in the opinion of management, are considered necessary for a fair presentation of the financial position, results of operations, and cash flows for the periods presented. The results of operations for such periods are not necessarily indicative of the results expected for the full fiscal year or for any future period. The accompanying unaudited financial statements should be read in conjunction with the audited financial statements of ZST Digital Networks, Inc. as contained in its Annual Report for the fiscal year ended December 31, 2008 on Form 10-K as filed with the Securities and Exchange Commission on March 31, 2009.

3

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

FINANCIAL STATEMENTS

MARCH 31, 2009

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

INDEX

| PAGE | |

| CONSOLIDATED BALANCE SHEETS | F-2 |

| CONSOLIATED STATEMENTS OF OPERATIONS | F-3 |

| CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY AND COMPREHENSIVE INCOME | F-4 |

| CONSOLIDATED STATEMENTS OF CASH FLOWS | F-5 |

| NOTES TO CONSOLIDATED FINANCIAL STATEMENTS | F-6 - F-25 |

F-1

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Consolidated Balance Sheets

(In U.S. Dollars)

| March 31, | December 31, | |||||||

| 2009 | 2008 | |||||||

| (unaudited) | ||||||||

| Assets | ||||||||

| Current assets | ||||||||

| Cash and cash equivalents | $ | 1,881,304 | $ | 1,134,954 | ||||

| Trade receivables, net (Note 3) | 22,846,271 | 12,322,099 | ||||||

| Employee advances (Note 5) | 6,065 | 6,307 | ||||||

| Inventories, net (Note 4) | 469,785 | 775,185 | ||||||

| Advances to suppliers (Note 10) | 798,410 | 3,024,668 | ||||||

| Prepaid expenses and other receivables | 1,374 | 6,968 | ||||||

| Total current assets | 26,003,209 | 17,270,181 | ||||||

| Property and equipment, net (Note 6) | 29,021 | 34,148 | ||||||

| Total assets | $ | 26,032,230 | $ | 17,304,329 | ||||

| Liabilities & Stockholders' Equity | ||||||||

| Current liabilities | ||||||||

| Accounts payable - trade | $ | 6,968,449 | $ | 1,270,096 | ||||

| Customer deposit | 1,466 | 1,467 | ||||||

| Accrued liabilities and other payable | 806,762 | 501,176 | ||||||

| Various taxes payable | 400,802 | 188,539 | ||||||

| Short-term loans (Note 7) | 3,712,025 | 3,931,991 | ||||||

| Employee security deposit payable | 7,508 | 8,911 | ||||||

| Wages payable | 65,442 | 59,501 | ||||||

| Corporate tax payable (Note 12) | 250,440 | - | ||||||

| Due to related parties (Note 9) | - | 2,359,728 | ||||||

| Total current liabilities | 12,212,894 | 8,321,409 | ||||||

| Commitments and contingencies (Note 11) | - | - | ||||||

Preferred Stock Series A Convertible, $0.0001 par value, 3,750,000 shares | ||||||||

| authorized, 2,242,523 and 0 shares issued and outstanding at March 31, 2009 | ||||||||

| and December 31, 2008, respectively. Liquidation preference and redemption | ||||||||

| value of $3,585,902 at March 31, 2009 (Note 16) | 2,946,440 | - | ||||||

| Stockholders' Equity | ||||||||

| Common stock $0.0001 par value, 100,000,000 shares authorized, 17,455,000 and | ||||||||

| 14,515,000 shares issued and outstanding at March 31, 2009 | ||||||||

| and December 31, 2008, respectively (Note 15) | 1,746 | 1,452 | ||||||

| Additional paid-in capital | 4,294,426 | 1,488,062 | ||||||

| Accumulated other comprehensive income | 168,175 | 590,839 | ||||||

| Statutory surplus reserve fund (Note 8) | 1,491,963 | 1,491,963 | ||||||

| Retained earnings (unrestricted) | 6,656,962 | 5,410,604 | ||||||

| Subscription receivable (Note 9) | (1,740,376 | ) | - | |||||

| Total stockholders' equity | 10,872,896 | 8,982,920 | ||||||

| Total Liabilities & Stockholders' Equity | $ | 26,032,230 | $ | 17,304,329 | ||||

The accompanying notes are an integral part of these consolidated financial statements.

F-2

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Consolidated Statements of Operations

(In U.S. Dollars)

| For the Three Months Ended | ||||||||

| March 31, | ||||||||

| 2009 | 2008 | |||||||

| (unaudited) | (unaudited) | |||||||

| Revenue | $ | 17,760,628 | $ | 13,515,031 | ||||

| Cost of goods sold | 14,844,279 | 10,816,256 | ||||||

| Gross Profit | 2,916,349 | 2,698,775 | ||||||

| Operating Costs and Expenses | ||||||||

| Selling expenses | - | 52,929 | ||||||

| Depreciation | 5,085 | 4,439 | ||||||

| General and administrative | 369,266 | 247,902 | ||||||

| Merger cost | 566,654 | - | ||||||

| Total operating costs and expenses | 941,005 | 305,270 | ||||||

| Income from operations | 1,975,344 | 2,393,505 | ||||||

| Other income (expenses) | ||||||||

| Interest income | 106 | 8,526 | ||||||

| Interest expense | (50,087 | ) | (104,434 | ) | ||||

| Imputed interest | (31,400 | ) | (17,728 | ) | ||||

| Sundry income (expense), net | 3,004 | 335 | ||||||

| Total other income (expenses) | (78,377 | ) | (113,301 | ) | ||||

| Income before income taxes | 1,896,967 | 2,280,204 | ||||||

| Income taxes (Note 12) | (650,609 | ) | (557,582 | ) | ||||

| Net income | $ | 1,246,358 | $ | 1,722,622 | ||||

| Basic earnings per share | $ | 0.07 | $ | 0.12 | ||||

| Weighted average shares outstanding, basic | 17,193,667 | 14,515,000 | ||||||

| Diluted earnings per share | $ | 0.07 | $ | 0.12 | ||||

| Weighted average shares outstanding, diluted | 17,576,333 | 14,515,000 | ||||||

The accompanying notes are an integral part of these consolidated financial statements.

F-3

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Consolidated Statements of Changes in Stockholders’ Equity and Comprehensive Income

For the three months ended March 31, 2009 (unaudited)

(In U.S. Dollars)

| Accumulated | ||||||||||||||||||||||||||||||||||||

| Additional | Statutory | Other | Retained | Total | ||||||||||||||||||||||||||||||||

| Capital | Paid-in | Reserve | Comprehensive | Earnings | Subscription | Stockholders' | Comprehensive | |||||||||||||||||||||||||||||

Shares | Amount | Capital | Fund | Income | (Unrestricted) | Receivable | Equity | Income | ||||||||||||||||||||||||||||

| Balance at December 31, 2008 | 14,515,000 | $ | 1,452 | $ | 1,488,062 | $ | 1,491,963 | $ | 590,839 | $ | 5,410,604 | $ | - | $ | 8,982,920 | |||||||||||||||||||||

| Reverse merger adjustment | 2,940,000 | 294 | 2,774,964 | - | - | - | - | 2,775,258 | ||||||||||||||||||||||||||||

| Imputed interest allocated | - | - | 31,400 | - | - | - | - | 31,400 | ||||||||||||||||||||||||||||

| Subscription receivable | - | - | - | - | - | - | (1,740,376 | ) | (1,740,376 | ) | ||||||||||||||||||||||||||

| Foreign currency translation adjustment | - | - | - | - | (422,664 | ) | - | - | (422,664 | ) | $ | (422,664 | ) | |||||||||||||||||||||||

Net income for the three months ended March 31, 2009 | - | - | - | - | - | 1,246,358 | - | 1,246,358 | 1,246,358 | |||||||||||||||||||||||||||

| Comprehensive income | - | - | - | - | - | - | - | - | $ | 823,694 | ||||||||||||||||||||||||||

| Balance at March 31, 2009 | 17,455,000 | $ | 1,746 | $ | 4,294,426 | 1,491,963 | $ | 168,175 | $ | 6,656,962 | $ | (1,740,376 | ) | $ | 10,872,896 | |||||||||||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

F-4

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Statements of Cash Flows

(In U.S. Dollars)

| For the Three Months Ended | ||||||||

| March 31, | ||||||||

| 2009 | 2008 | |||||||

| (unaudited) | (unaudited) | |||||||

| Cash Flows From Operating Activities | ||||||||

| Net income | $ | 1,246,358 | $ | 1,722,622 | ||||

| Adjustments to reconcile net income to net cash provided | ||||||||

| (used) by operating activities: | ||||||||

| Depreciation | 5,085 | 4,439 | ||||||

| Imputed interest | 31,400 | 17,728 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Account receivable-trade, net | (10,524,172 | ) | (66,631 | ) | ||||

| Contract receivable | - | (4,231 | ) | |||||

| Prepaid expenses and other receivables | 5,594 | 4,459 | ||||||

| Inventories, net | 305,400 | 4,355,811 | ||||||

| Advances | 2,226,258 | (340,532 | ) | |||||

| Accounts payable and accrued liabilities | 6,003,939 | 5,255,776 | ||||||

| Deposits and other payables | (1,404 | ) | - | |||||

| Billings in excess of costs on uncompleted projects | - | 776 | ||||||

| Various taxes payable and taxes recoverable | 212,263 | (233,847 | ) | |||||

| Wages payable | 5,941 | 9,234 | ||||||

| Corporate tax payable | 250,440 | - | ||||||

| Net cash provided (used) by operating activities | (232,898 | ) | 10,725,604 | |||||

| Cash Flows From Investing Activities | ||||||||

| Payment to ZST PRC shareholders | (1,740,376 | ) | - | |||||

| Net cash used by investing activities | (1,740,376 | ) | - | |||||

| Cash Flows From Financing Activities | ||||||||

| Proceeds from short-term demand loans receivable | 242 | 190,608 | ||||||

| Repayment of short-term demand loans payable | (219,966 | ) | (406,676 | ) | ||||

| Sale of preferred stock | 2,946,440 | - | ||||||

| Due from related parties | - | 68,548 | ||||||

| Due to related parties | - | (23,405 | ) | |||||

| Net cash provided (used) by financing activities | 2,726,716 | (170,925 | ) | |||||

| Effect of exchange rate changes on cash | (7,092 | ) | 254,665 | |||||

| Net increase in cash and cash equivalents | 746,350 | 10,809,344 | ||||||

| Cash and cash equivalents, beginning of period | 1,134,954 | 1,125,804 | ||||||

| Cash and cash equivalents, end of period | $ | 1,881,304 | $ | 11,935,148 | ||||

| Supplemental disclosure information: | ||||||||

| Interest expense paid | $ | 50,087 | $ | 104,434 | ||||

| Income taxes paid | $ | 400,164 | $ | 557,582 | ||||

| Non cash investing and financing activities: | ||||||||

| Shares issued for related parties' debt | $ | 2,359,728 | $ | - | ||||

| Shares issued for subscription receivable | $ | 1,740,376 | $ | - | ||||

The accompanying notes are an integral part of these consolidated financial statements.

F-5

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 1 – DESCRIPTION OF BUSINESS AND ORGANIZATION

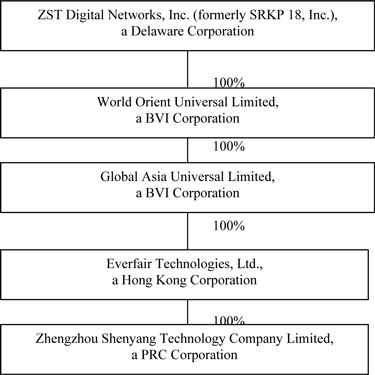

ZST Digital Networks, Inc. (“ZST Digital”, formerly SRKP 18, Inc.) was incorporated in the State of Delaware on December 7, 2006. ZST Digital was originally organized as a “blank check” shell company to investigate and acquire a target company or business seeking the perceived advantages of being a publicly held corporation. On January 9, 2009, we closed a share exchange transaction (the “Share Exchange”) pursuant to which ZST Digital (i) issued 1,985,000 shares of its common stock to acquire 100% equity ownership of World Orient Universal Limited (“World Orient”), which is the 100% parent of Global Asia Universal Limited (“Global Asia”), which is the 100% parent of Everfair Technologies Limited (“Everfair”), which is the 100% parent of Zhengzhou Shenyang Technology Company Limited (“ZST PRC”), (ii) assumed the operations of World Orient and its subsidiaries, and (iii) changed ZST Digital’s name from SRKP 18, Inc. to its current name. Subsequent to the closing of the Share Exchange, on January 14, 2009, Zhong Bo, our Chief Executive Officer and Chairman of the Board, Wu Dexiu, Huang Jiankang, Sun Hui and Li Yuting (the "ZST Management"), each entered into a Common Stock Purchase Agreement pursuant to which the Company issued and the ZST Management agreed to purchase an aggregate of 12,530,000 shares of our common stock at a per share purchase price of $0.2806 (the "Purchase Right") and obtained control of the Company. The purchase price for the shares was paid in full on May 25, 2009. The restructuring of the Company is further discussed below.

World Orient was incorporated in British Virgin Islands (“BVI”) on August 12, 2008. As at December 31, 2008, World Orient had 50,000 capital shares authorized with $1.00 par value and 50,000 shares issued and outstanding. In November 2008, World Orient acquired 100% ownership of Global Asia.

Global Asia was incorporated in BVI on August 12, 2008. As at December 31, 2008, Global Asia had 50,000 capital shares authorized with $1.00 par value and 50,000 shares issued and outstanding. In October 2008, Global Asia acquired 100% ownership of Everfair.

Everfair is a holding company incorporated in November 26, 2007 in Hong Kong, PRC with the original sole shareholder Kuk Kok Sun. Everfair had 10,000 capital shares authorized with 1.00 HKD par value and 10,000 shares issued and outstanding. Pursuant to a share transfer agreement, Global Asia agreed to paid Kuk Kok Sun 10,000 HKD for the ownership transfer.

In October 2008, Everfair entered an ownership transfer agreement with the original owners of ZST PRC. Pursuant to the ownership transfer agreement, Everfair agreed to pay the original owners 12,000,000 RMB for the ownership transfer within three months of the approval of a new business license. This transfer was completed in January, 2009 after the closing of the Share Exchange and exercise of the purchase rights by the shareholders of ZST PRC.

ZST PRC was established on May 20, 1996 as a private domestic corporation in Zhengzhou, Henan Province, PRC with an authorized capital of RMB 1.5 million. On April 8, 1999, the Company increased its authorized capital from RMB 1.5 million to RMB 8 million. On July 27, 2004, the Company further increased its authorized capital to RMB 18 million. On March 15, 2007, the Company decreased its authorized and invested capital to RMB 11.5 million. In February 2009, ZST PRC increased its authorized capital to RMB 17 million.

ZST PRC’s primary revenues were from sales of broadcasting equipment, hi-tech optical transmission devices, and telecommunication products. ZST PRC is principally engaged in supplying digital and optical network equipment to cable system operators in the Henan Province of China. It has developed a line of internet protocol television (“IPTV”) set-top boxes that are used to provide bundled cable television, Internet and telephone services to residential and commercial customers. At present, ZST PRC’s main clients are broadcasting TV bureaus and cable network operators serving various cities and counties. In the near future, the Company plans to joint venture with cable network operators to provide bundled television programming, Internet and telephone services to residential customers in cities and counties located in the Henan Province of China.

ZST Digital and its subsidiaries, World Orient, Global Asia, Everfair, and ZST PRC shall be collectively referred throughout as the “Company”.

F-6

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 1 – DESCRIPTION OF BUSINESS AND ORGANIZATION (continued)

Pursuant to PRC rules and regulations relating to mergers of PRC companies with foreign entities, an offshore company controlled by PRC citizens that intends to merge with a PRC company will be subject to strict examination by the relevant PRC foreign exchange authorities. To enable ZST PRC to go public, ZST management made the following restructuring arrangements: (i) established Everfair as a Hong Kong holding company owned by a non-PRC citizen and indirectly controlled the operations of Everfair, (ii) had Everfair enter into an equity transfer agreement with ZST PRC by paying 12,000,000 RMB to ZST Management, (iii) established World Orient as a BVI holding company owned by a non PRC-citizen, (iv) had World Orient and its wholly owned subsidiary Global Asia, its subsidiary Everfair, and its subsidiary ZST PRC enter into a share exchange agreement with ZST Digital, (v) concurrently conducted a private investment in a public company (“PIPE”) financing, and (vi) used proceeds from the PIPE transaction to pay 12,000,000 RMB to ZST Management pursuant to the ownership transfer agreement.

Upon consummation of the Share Exchange and the Purchase Right, ZST Management owns a majority of the issued and outstanding shares of common stock of ZST Digital and Zhong Bo was appointed as Chairman of the Board and Chief Executive Officer of ZST Digital.

For accounting purposes, this transaction is being accounted for as a reverse merger. The transaction has been treated as a recapitalization of World Orient and its subsidiaries, with ZST Digital (the legal acquirer of World Orient and its subsidiaries including ZST PRC) considered the accounting acquiree and ZST PRC, the only operating company, and whose management took control of ZST Digital (the legal acquiree of ZST Digital) is considered the accounting acquirer. The Company did not recognize goodwill or any intangible assets in connection with the transaction.

To summarize the paragraphs above, the organization and ownership structure of the Company is currently as follows:

F-7

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The consolidated financial statements have been prepared in accordance with U.S. GAAP for interim financial information and the instructions to Form 10-Q and Article 10 of Regulation SX. Accordingly, they do not include all of the information and footnotes required by generally accepted accounting principles for complete financial statements. These consolidated financial statements should be read in conjunction with the consolidated financial statements of the Company for the year ended December 31, 2008 and notes thereto contained in the Report on Form 10-K of the Company as filed with the United States Securities and Exchange Commission (the “SEC”). Interim results are not necessarily indicative of the results for the full year.

In the opinion of the management, the consolidated financial statements reflect all adjustments (which include only normal recurring adjustments) necessary to present fairly the financial position of the Company as of March 31, 2009 and December 31, 2008, and the results of operations and cash flows for the three months ended March 31, 2009 and 2008, respectively.

Basis of Consolidation

The consolidated financial statements include the accounts of the Company and its subsidiaries. All significant inter-company transactions have been eliminated in consolidation.

Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting year. Because of the use of estimates inherent in the financial reporting process, actual results could differ from those estimates.

Fair Value of Financial Instruments

Statement of Financial Accounting Standards (“SFAS”) No. 107, “Disclosures About Fair Value of Financial Instruments,” defines financial instruments and requires fair value disclosures of those financial instruments. On January 1, 2008, the Company adopted SFAS No. 157, “Fair Value Measurements,” which defines fair value, establishes a three-level valuation hierarchy for disclosures of fair value measurement and enhances disclosures requirements for fair value measures. Current assets and current liabilities qualified as financial instruments and management believes their carrying amounts are a reasonable estimate of fair value because of the short period of time between the origination of such instruments and their expected realization and if applicable, their current interest rate is equivalent to interest rates currently available. The three levels are defined as follow:

| · | Level 1 — inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets. |

| · | Level 2 — inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the assets or liability, either directly or indirectly, for substantially the full term of the financial instruments. |

| · | Level 3 — inputs to the valuation methodology are unobservable and significant to the fair value. |

As of the balance sheet date, the estimated fair values of the financial instruments were not materially different from their carrying values as presented due to the short maturities of these instruments and that the interest rates on the borrowings approximate those that would have been available for loans of similar remaining maturity and risk profile at respective period-ends. Determining which category an asset or liability falls within the hierarchy requires significant judgment. The Company evaluates the hierarchy disclosures each quarter.

Cash and Cash Equivalents

Cash and cash equivalents include cash on hand, cash on deposit with various financial institutions in PRC, and all highly-liquid investments with original maturities of three months or less at the time of purchase. Banks and other financial institutions in PRC do not provide insurance for funds held on deposit.

F-8

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Accounts Receivable

Accounts receivable are carried at original invoice amount less an estimate made for doubtful accounts based on a review of all outstanding amounts on a monthly basis. The Company analyzes the aging of accounts receivable balances, historical bad debts, customer concentrations, customer credit-worthiness, current economic trends and changes in our customer payment terms. Significant changes in customer concentration or payment terms, deterioration of customer credit-worthiness or weakening in economic trends could have a significant impact on the collectability of receivables and our operating results. The Company has not provided a bad debt allowance based upon its historical collection experience. There were no bad debts written off during the periods ended March 31, 2009 and 2008.

Inventories

Inventories, which are primarily comprised of raw materials and finished goods, are stated at the lower of cost or net realizable value, using the first-in first-out (FIFO) method. Cost is determined on the basis of a moving average. The Company evaluates the need for reserves associated with obsolete, slow-moving and non-salable inventory by reviewing net realizable values on a periodic basis.

Property and Equipment

Property and equipment are recorded at cost and depreciated using the straight-line method, with an estimated 5% salvage value of original cost, over the estimated useful lives of the assets as follows:

| Machinery and equipment | 5 years | |

| Office equipment | 5 years | |

| Automobile | 5 years | |

| Other equipment | 10 years |

Expenditures for repairs and maintenance, which do not improve or extend the expected useful lives of the assets, are expensed as incurred while major replacements and improvements are capitalized.

When property or equipment is retired or disposed of, the cost and accumulated depreciation are removed from the accounts, with any resulting gains or losses being included in net income or loss in the year of disposition.

Impairment of Long-Lived Assets

The Company accounts for impairment of plant and equipment and amortizable intangible assets in accordance with SFAS No. 144, “Accounting for Impairment of Long-Lived Assets and Long-Lived Assets to be Disposed Of”, which requires the Company to evaluate a long-lived asset for recoverability when there is event or circumstance that indicate the carrying value of the asset may not be recoverable. An impairment loss is recognized when the carrying amount of a long-lived asset or asset group is not recoverable (when carrying amount exceeds the gross, undiscounted cash flows from use and disposition) and is measured as the excess of the carrying amount over the fair value of the asset or asset group.

F-9

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Revenue Recognition

The Company recognizes product sales revenue when the significant risks and rewards of ownership have been transferred pursuant to PRC law, including such factors as when persuasive evidence of an arrangement exists, delivery has occurred, the sales price is fixed or determinable, sales and value-added tax laws have been complied with, and collectability is reasonably assured. The Company generally recognizes revenue when its products are shipped.

The IPTV device sales contracts include a one-year quality assurance warranty for defects. According to the sales contract terms, customers are able to hold back 10% of the total contract balance payable to the Company for one year. This deferred payment obligation is not contingent on resale of the product. In accordance with SFAS FASB No. 48, "Revenue Recognition When Right of Return Exists", the Company records the holdback as revenue at the time of sale when its products are shipped to customers. Costs related to quality assurance fulfillment are mainly the costs of materials used for repair or replacement of damaged or defective products and are expensed as incurred. As the costs associated with such assurance were immaterial in monetary terms, no assurance liability is accrued for all periods. The Company incurred quality assurance costs of $0 and $0 for the period ended March 31, 2009 and 2008, respectively. These costs incurred represent 0% and 0% of 2009 and 2008 IPTV box sales, respectively. In the event of defective product returns, the Company has the right to seek replacement of such returned units from its supplier.

Revenues from fixed-price construction contracts are recognized on the completed-contract method. This method is used because most of the construction and engineering contracts are completed within six months or less and financial position and results of operations do not vary significantly from those which would result from using the percentage-of-completion method. A contract is considered complete when all costs have been incurred and the installation is operating according to specifications or has been accepted by the customer.

Contract costs include all direct material and labor costs and those indirect costs related to contract performance, such as indirect labor, suppliers, tools, repairs, and depreciation costs. General and administrative costs are charged to expenses as incurred. Provisions for estimated losses on uncompleted contracts are made in the period in which such losses are determined. Claims are included in revenues when received.

Comprehensive Income

The Company has adopted SFAS No. 130, “Reporting Comprehensive Income”, which establishes standards for reporting and displaying comprehensive income, its components, and accumulated balances in a full-set of general-purpose financial statements. Accumulated other comprehensive income represents the accumulated balance of foreign currency translation adjustments.

Related Parties

A party is considered to be related to the Company if the party directly or indirectly or through one or more intermediaries, controls, is controlled by, or is under common control with the Company. Related parties also include principal owners of the Company, its management, members of the immediate families of principal owners of the Company and its management and other parties with which the Company may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting parties might be prevented from fully pursuing its own separate interests. A party which can significantly influence the management or operating policies of the transacting parties or if it has an ownership interest in one of the transacting parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully pursuing its own separate interests is also a related party.

Income Taxes

The Company accounts for income taxes in accordance with SFAS No. 109, "Accounting for Income Taxes". SFAS No. 109 requires an asset and liability approach for financial accounting and reporting for income taxes and allows recognition and measurement of deferred tax assets based upon the likelihood of realization of tax benefits in future years. Under the asset and liability approach, deferred taxes are provided for the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. A valuation allowance is provided for deferred tax assets if it is more likely than not these items will either expire before the Company is able to realize their benefits, or that future deductibility is uncertain.

F-10

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Research and Development

Research and development costs are expensed to operations as incurred. The Company spent $0 and $0, on direct research and development (“R&D”) efforts in the three months ended March 31, 2009 and 2008, respectively.

Advertising Costs

The Company expenses advertising costs as incurred. The Company did not incur any advertising expenses for the years ended March 31, 2009 and 2008, respectively.

Foreign Currency Translation

The functional currency of ZST PRC is RMB, the functional currencies of World Orient, Global Asia, and Everfair are HKD, and the functional currency of ZST Digital is USD. The Company maintains its financial statements using the functional currency. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency at rates of exchange prevailing at the balance sheet dates. Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction. Exchange gains or losses arising from foreign currency transactions are included in the determination of net income (loss) for the respective periods.

For financial reporting purposes, the financial statements of each subsidiary, which are prepared in either RMB or HKD, are translated into the Company’s reporting currency, USD. Balance sheet accounts are translated using the closing exchange rate in effect at the balance sheet date and income and expense accounts are translated using the average exchange rate prevailing during the reporting period. Adjustments resulting from the translation, if any, are included in accumulated other comprehensive income (loss) in the owners’ equity.

Foreign Currency Translation (Continued)

The exchange rates used for foreign currency translation were as follows (USD$1 = RMB):

| Period Covered | Balance Sheet Date Rates | Average Rates | ||||||

| Three Months Ended March 31, 2009 | 6.82560 | 6.82547 | ||||||

| Three Months Ended March 31, 2008 | 7.00220 | 7.15461 | ||||||

The exchange rates used for foreign currency translation were as follows (USD$1 = HKD):

| Period Covered | Balance Sheet Date Rates | Average Rates | ||||||

| Three Months Ended March 31, 2009 | 7.74999 | 7.75374 | ||||||

| Three Months Ended March 31, 2008 | 7.77965 | 7.79423 | ||||||

F-11

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Recently Adopted Accounting Pronouncements

In the first quarter of 2009, the Company adopted Statement of Financial Accounting Standards (SFAS) No. 141 (revised 2007), “Business Combinations” (SFAS No. 141(R) as mended by FASB staff position FSP 141(R)-1, “Accounting for Assets Acquired and Liabilities Assumed in a Business Combination.” SFAS No. 141(R) generally requires an entity to recognize the assets acquired, liabilities assumed, contingencies, and contingent consideration at their fair value on the acquisition date. In circumstances where the acquisition-date fair value for a contingency cannot be determined during the measurement period and it is concluded that it is probable that an asset or liability exists as of the acquisition date and the amount can be reasonably estimated, a contingency is recognized as of the acquisition date based on the estimated amount. It further requires that acquisition related costs be recognized separately from the acquisition and expensed as incurred, restructuring costs generally be expensed in periods subsequent to the acquisition date, and changes in accounting for deferred tax asset valuation allowances and acquired income tax uncertainties after the measurement period impact income tax expenses. In addition, acquired in-process research and development is capitalized as an intangibles asset and amortized over its estimated useful life. SFAS No. 141(R) is applicable to business combinations on a prospective basis beginning in the first quarter of 2009. The Company adopted SFAS No. 141(R) for its business combination during the quarter ended March 31, 2009.

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements” (“SFAS 157”). SFAS 157 defines fair value, establishes a framework and gives guidance regarding the methods used for measuring fair value, and expands disclosures about fair value measurements. In February 2008, the FASB issued FASB Staff Position 157-1, “Application of FASB Statement No. 157 to FASB Statement No. 13 and Other Accounting Pronouncements That Address Fair Value Measurements for Purposes of Lease Classification or Measurement under Statement 13 (“FSP 157-1”) and FASB Staff Position 157-2, “Effective Date of FASB Statement No. 157” (“FSP 157-2”). FSP 157-1 amends SFAS 157 to remove certain leasing transactions from its scope. FSP 157-2 delays the effective date of SFAS 157 for all non-financial assets and non-financial liabilities, except for items that are recognized or disclosed at fair value in the financial statements on a recurring basis (at least annually), until fiscal years beginning after November 15, 2008. SFAS 157 is effective for financial statements issued for fiscal years beginning after November 15, 2007, and interim periods within those fiscal years. The Company adopted SFAS 157 effective January 1, 2008 for all financial assets and liabilities as required. The adoption of SFAS 157 was not material to the Company’s financial statements or results of operations.

Effective January 1, 2009, the Company adopted the provisions of EITF 07-5, "Determining Whether an Instrument (or Embedded Feature) is Indexed to an Entity’s Own Stock” (“EITF 07-5”). EITF 07-5 applies to any freestanding financial instruments or embedded features that have the characteristics of a derivative, as defined by SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities,” and to any freestanding financial instruments that are potentially settled in an entity’s own common stock. The adoption of EITF 07-5 was not material to the Company's financial statements or results of operations.

In July 2006, the FASB issued FASB Interpretation (“FIN”) No. 48, “Accounting for Uncertainty in Income Taxes,” which prescribes a comprehensive model for how a company should recognize, measure, present and disclose in its financial statements uncertain tax positions that the company has taken or expects to take on a tax return (including a decision whether to file or not to file a return in a particular jurisdiction). The accounting provisions of FIN No. 48 are effective for fiscal years beginning after December 15, 2006. The adoption of this Interpretation had no impact on the Company’s financial position or results of operations.

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial Liabilities — Including an Amendment of FASB Statement No. 115,” (“SFAS 159”) which is effective for fiscal years beginning after November 15, 2007. SFAS 159 is an elective standard which permits an entity to choose to measure many financial instruments and certain other items at fair value at specified election dates. Subsequent unrealized gains and losses on items for which the fair value option has been elected will be reported in earnings. The Company has not elected the fair value option for any assets or liabilities under SFAS 159.

F-12

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Recent Issued Accounting Pronouncements

In April 2009, the FASB issued FSP FAS 157-4, “Determining Fair Value When the Volume and Level of Activity for the Asset or Liability Have Significantly Decreased and Identifying Transactions That Are Not Orderly” (FSP FAS 157-4). FSP FAS 157-4 amends SFAS 157 and provides additional guidance for estimating fair value in accordance with SFAS 157 when the volume and level of activity for the asset or liability have significantly decreased and also includes guidance on identifying circumstances that indicate a transaction is not orderly for fair value measurements. This FSP shall be applied prospectively with retrospective application not permitted. This FSP shall be effective for interim and annual periods ending after June 15, 2009, with early adoption permitted for periods ending after March 15, 2009. An entity early adopting this FSP must also early adopt FSP FAS 115-2 and FAS 124-2, “Recognition and Presentation of Other-Than-Temporary Impairments” (FSP FAS 115-2 and FAS 124-2). Additionally, if an entity elects to early adopt either FSP FAS 107-1 and APB 28-1, “Interim Disclosures about Fair Value of Financial Instruments” (FSP FAS 107-1 and APB 28-1) or FSP FAS 115-2 and FAS 124-2, it must also elect to early adopt this FSP. The Company is currently evaluating this new FSP but do not believe that it will have a significant impact on the determination or reporting of the Company’s financial results.

In April 2009, the FASB issued FSP FAS 115-2 and FAS 124-2, “Recognition and Presentation of Other-Than-Temporary Impairment” (FSP 115-2/124-2). FSP 115-2/124-2 amends the requirements for the recognition and measurement of other-than-temporary impairment for debt securities by modifying the pre-existing “intent and ability” indicator. Under FSP 115-2/124-2, an other-than-temporary impairment is triggered when there is an intent to sell the security, it is more likely then not that the security will be required to be sold before recovery, or the security is not expected to recover the entire amortized cost basis of the security. Additionally, FSP 115-2/124-2 changes the presentation of an other-than-temporary impairment in the income statement for those impairments involving credit losses. The credit loss component will be recognized in earnings and the remainder of the impairment will be recorded in other comprehensive income. FSP 115-2/124-2 is effective for the Company beginning in the second quarter of fiscal year 2009. Upon implementation at the beginning of the second quarter of 2009, FSP 115-2/124-2 is not expected to have a significant impact on the Company’s consolidated financial statements.

In April 2009, the FASB issued FSP FAS 107-1 and APB 28-1, “Interim Disclosure about Fair Value of Financial Instruments” (“FSP 107-1/APB 28-1”). FSP 107-1/APB 28-1 requires interim disclosures regarding the fair values of financial instruments that are within the scope of FAS 107, “Disclosures about the Fair Value of Financial Instruments,” Additionally, FSP 107-1/APB 28-1 requires disclosures of the methods and significant assumptions used to estimate the fair value of financial instruments on an interim basis as well as changes in the methods and significant assumptions from prior periods. FSP 107-1/APB 28-1 does not change the accounting treatment for these financial instruments and is effective for the Company beginning in the second quarter of fiscal year 2009.

F-13

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 3 – TRADE RECEIVABLES, NET

Trade receivables consist of the following:

| March 31, 2009 | December 31, 2008 | |||||||

| Trade receivables | $ | 22,846,271 | $ | 12,322,099 | ||||

The Company has not provided a bad debt allowance based upon its historical collection experience. There were no bad debts written off for the three months ended March 31, 2009 and 2008.

NOTE 4 – INVENTORIES, NET

Inventory consists of the following:

| March 31, 2009 | December 31, 2008 | |||||||

| Products for sale | $ | 469,785 | $ | 775,185 | ||||

The Company sold its production lines in 2006 and has operated as a distributor since that time. There was no reserve for obsolete inventory for all the periods as the Company has purchased inventory based on customers’ orders.

Since 2008, the Company focuses on sales of IPTV devices and ordered products according to sales contracts. Thus, the ending balance of inventory decreased.

NOTE 5 – EMPLOYEE ADVANCES

Employee advances consist of the following:

| March 31, 2009 | December 31, 2008 | |||||||

| Employee advances | $ | 6,065 | $ | 6,307 | ||||

Employee advances for business operating expenses and were deducted from their monthly wages.

NOTE 6 – PROPERTY AND EQUIPMENT, NET

Property and equipment consist of the following:

| March 31, 2009 | December 31, 2008 | |||||||

| Machinery and equipment | $ | 89,354 | $ | 89,463 | ||||

| Office equipment | 32,408 | 32,447 | ||||||

| Automobiles | 101,703 | 101,827 | ||||||

| Accumulated depreciation | (194,444 | ) | (189,589 | ) | ||||

| Total | $ | 29,021 | $ | 34,148 | ||||

The depreciation expenses are $5,085 and $4,439 in the three months ended March 31, 2009 and 2008, respectively.

F-14

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 7 – SHORT-TERM DEMAND LOANS PAYABLE

Since 2005, the Company had several outstanding short-term demand loans which were used primarily for general working capital purposes. These short-term unsecured loans were borrowed from long-term relationship customers bearing no interest. The balances of such short-term demand loans as of March 31, 2009 and December 31, 2008, were $0 and $0, respectively. The imputed interests are assessed as an expense to the business operation and addition to the paid-in capital. The calculation is performed monthly by annual rate in the rage from 5.58 to7.30% with the reference to the one-year loan rate from The People’s Bank of China. The imputed interests for the three months ended March 31, 2009 and 2008 were $0 and $17,728, respectively.

In 2006 and 2007, the Company secured one-year bank loans from Bank of Communication and Austria Central Cooperation Bank. These loans carried at an annual interest rate of 6.7275% for loans from Bank of Communication and 6.6975% for loans from Austria Central Cooperation Bank Beijing Branch. Both loans are secured by accounts receivable of the Company. The balances of such short-term demand loans as of March 31, 2009 and December 31, 2008 were $3,712,025 and $3,931,991, respectively.

The outstanding loans are as follows:

| Bank Loan: | March 31, 2009 | December 31, 2008 | ||||||

| Austria Central Cooperation Bank | $ | 3,712,025 | $ | 3,931,991 | ||||

Interest expense incurred for the above short-term bank loans for the three months ended March 31, 2009 and 2008 was $50,087 and $104,434, respectively.

NOTE 8 – STATUTORY RESERVES

As stipulated by the relevant laws and regulations for enterprises operating in PRC, the subsidiaries of the Company are required to make annual appropriations to a statutory surplus reserve fund. Specifically, the subsidiaries of the Company are required to allocate 10% their profits after taxes, as determined in accordance with the PRC accounting standards applicable to the subsidiaries of the Company, to a statutory surplus reserve until such reserve reaches 50% of the registered capital of the subsidiaries of the Company.

NOTE 9 – RELATED PARTIES TRANSACTIONS

Due to related parties

For the year then ended December 31, 2008, the Company had an outstanding payable to Mr. Zhong, Ms. Sen, Mr. Huang, Ms. Wu, and Ms. Li totaling $2,102,178, $13,759, $21,152, $211,814 and $10,825, respectively. These amounts are non-secured, non interest bearing, and are considered to be short-term within five months starting from October 6, 2008 to March 5, 2009. These payables were exchanged for common stock during the quarter ended March 31, 2009 as part of the Purchase Rights Agreement with the management of ZST PRC.

Due to related parties consist of the following:

| March 31, 2009 | December 31, 2008 | |||||||

| Sen, Hui (shareholder) | $ | - | $ | 13,759 | ||||

| Zhong, Bo (CEO) | - | 2,102,178 | ||||||

| Huang, Jenkang (VP) | - | 21,152 | ||||||

| Wu, Dexio (Warehousing, CEO's Wife) | - | 211,814 | ||||||

| Li, Yuting (Executive Secretary to CEO) | - | 10,825 | ||||||

| Total | $ | - | $ | 2,359,728 | ||||

The imputed interest for the three months ended March 31, 2009 and 2008 was $31,400 and $0, respectively.

F-15

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 9 – RELATED PARTIES TRANSACTIONS (continued)

Subscription receivable

Pursuant to relevant laws and regulations of China and the ownership transfer agreement with the original owners of ZST PRC, the Company, through its Everfair subsidiary, agreed to pay approximately $1.7 million (RMB 12,000,000) to acquire the assets of ZST PRC. As part of the Purchase Rights Agreement the original owners agreed to use these proceeds to complete the exercise of the Purchase Rights to purchase the Company’s shares and obtain control of the Company. As of March 31, 2009, the Company had an outstanding subscription receivable from Mr. Zhong, Ms. Sen, Mr. Huang, Ms. Wu, and Ms. Li in the amount of $1,740,376. The subscription receivable was paid on May 25, 2009.

Subscription receivable consists of the following:

| March 31, 2009 | December 31, 2008 | |||||||

| Sen, Hui (shareholder) | $ | 3,860 | $ | - | ||||

| Zhong, Bo (CEO) | 1,571,381 | - | ||||||

| Huang, Jenkang (VP) | 14,488 | - | ||||||

| Wu, Dexio (Warehousing, CEO's Wife) | 144,589 | - | ||||||

| Li, Yuting (Executive Secretary to CEO) | 6,058 | - | ||||||

| Total | $ | 1,740,376 | $ | - | ||||

NOTE 10 – ADVANCES

In accordance with the purchase contracts, the Company is required to make an advance to its suppliers to purchase the IPTV materials and add on process work. The advance is applied to the total invoice balance upon satisfaction of the delivered goods.

NOTE 11 – COMMITMENTS AND CONTINGENCIES

Office lease commitments

The Company has entered into two office lease agreements. The Company’s commitments for minimum lease payments under these leases for the next five years and thereafter are as follows as follows:

| Year Ending December 31, | ||||

| 2010 | $ | 8,251 | ||

| 2011 | - | |||

| Thereafter | - | |||

| $ | 8,251 | |||

Lack of insurance

The Company could be exposed to liabilities or other claims for which the Company would have no insurance protection. The Company does not currently maintain any business interruption insurance, products liability insurance, or any other comprehensive insurance policy except for property insurance policies with limited coverage. For example, because the Company does not carry products liability insurance, a failure of any of the products marketed by the Company may subject it to the risk of product liability claims and litigation arising from injuries allegedly caused by the improper functioning or design of its products. The Company cannot assure that it will have enough funds to defend or pay for liabilities arising out of a products liability claim. To the extent the Company incurs any product liability or other litigation losses, its expenses could materially increase substantially. There can be no assurance that the Company will have sufficient funds to pay for such expenses, which could end its operations. There can be no guarantee that the Company will be able to obtain additional insurance coverage in the future, and even if it can obtain additional coverage, the Company may not carry sufficient insurance coverage to satisfy potential claims. Any purchasers of the Company’s common stock could lose their entire investment should uninsured losses occur.

F-16

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 12 – INCOME TAXES

The Company is registered in PRC and has no tax advantages granted by local government for corporate income taxes and sales taxes because it is a domestic corporation.

Beginning January 1, 2008, the new Enterprise Income Tax (“EIT”) law has replaced the old laws for Domestic Enterprises (“DES”) and Foreign Invested Enterprises (“FIEs”). The new standard EIT rate of 25% replaces the 33% rate applicable to both DES and FIEs, except for High Tech companies that pay a reduced rate of 15%, subject to government verification for Hi-Tech company status in every three years. For companies established before March 16, 2007 continue to enjoy tax holiday treatment approved by local government for a grace period of either for the next 5 years or until the tax holiday term is completed, whichever is sooner.

The provision for taxes on earnings consisted of:

| March 31, 2009 | March 31, 2008 | |||||||

| PRC Corporate Income Tax | $ | 650,609 | $ | 557,582 | ||||

A reconciliation between the income tax computed at the PRC statutory rate and the Company’s provision for income taxes for the period ended March 31, 2009 and 2008 is as follows:

| March 31, 2009 | March 31, 2008 | |||||||

| PRC Corporate Income Tax Rate | 25 | % | 25 | % | ||||

The PRC tax authority conducts periodic and ad hoc tax filing reviews on business enterprises operating in the PRC after those enterprises have completed their relevant tax filings, hence the Company’s tax filings may not be finalized. It is therefore uncertain as to whether the PRC tax authority may take different views about the Company’s tax filings which may lead to additional tax liabilities.

F-17

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 13 – SEGMENT INFORMATION

SFAS No. 131, “Disclosures About Segments of an Enterprise and Related Information”, requires certain financial and supplementary information to be disclosed on an annual and interim basis for each reportable segment of an enterprise. The Company believes that it operates in one business segment (research, development, production, marketing and sales of electronic products) and in one geographical segment (China), as all of the Company’s current operations are carried out in China.

The Company’s revenues, costs and gross profits were broken into the following categories:

Product Sales:

| March 31, 2009 | March 31, 2008 | |||||||

| Sales revenues | $ | 17,760,628 | $ | 12,920,736 | ||||

| Cost of sales | 14,844,279 | 10,783,570 | ||||||

| Gross Profit | $ | 2,916,349 | $ | 2,173,166 | ||||

| Gross Margin | 16.42 | % | 16.54 | % | ||||

| Technical Support Revenues: | ||||||||

| March 31, 2009 | March 31, 2008 | |||||||

| Sales revenues | $ | - | $ | 594,295 | ||||

| Service cost | - | 32,686 | ||||||

| Gross Profit | $ | - | $ | 561,609 | ||||

| Gross Margin | - | 94.50 | % | |||||

| Total Revenues: | ||||||||

| March 31, 2009 | March 31, 2008 | |||||||

| Total revenues | $ | 17,760,628 | $ | 13,515,031 | ||||

| Total costs | 14,844,279 | 10,816,256 | ||||||

| Gross Profit | $ | 2,916,349 | $ | 2,698,775 | ||||

| Gross Margin | 16.42 | % | 19.97 | % | ||||

F-18

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 14 – OPERATING RISK

Concentration of credit risk

The Company maintains cash balances at various financial institutions in the PRC that do not provide insurance for amounts on deposit. The Company operates principally in the PRC and grants credit to its customers. Although the PRC is economically stable, it is always possible that unanticipated events both domestically and in foreign countries could disrupt the operations of the Company or its customers.

Country risk

The Company has significant investments in the PRC. The operating results of the Company may be adversely affected by changes in the political and social conditions in the PRC and by changes in Chinese government policies with respect to laws and regulations, anti-inflationary measures, currency conversion, international remittances and rates and methods of taxation, among other things. The Company can give no assurance that those changes in political and other conditions will not result in have a material adverse effect upon the Company’s business and financial condition.

NOTE 15 – COMMON STOCK

On January 9, 2009, ZST Digital closed a share exchange transaction (the “Share Exchange”) pursuant to which ZST Digital (i) issued 1,985,000 shares of its common stock to acquire 100% equity ownership of World Orient Universal Limited (“World Orient”), which is the 100% parent of Global Asia Universal Limited (“Global Asia”), which is the 100% parent of Everfair Technologies Limited ("Everfair”), which is a 100% parent of Zhengzhou Shenyang Technology Company Limited (“ZST PRC”), (ii) assumed the operations of World Orient and its subsidiaries, and (iii) changed ZST Digital’s name from SRKP 18, Inc. to its current name.

Immediately after the closing of the Share Exchange but prior to the Private Placement (described below), ZST Digital had outstanding 9,081,390 shares of common stock, no shares of preferred stock, no options, and warrants to purchase 7,096,390 shares of common stock at an exercise price of $0.0001 per share. Pursuant to the terms of the Share Exchange, ZST Digital agreed to register a total of 2,940,000 shares of common stock and 420,000 shares of common stock issuable upon the exercise of outstanding warrants held by stockholders of ZST Digital immediately prior to the Share Exchange. Of the shares, 600,055 shares of common stock and 85,723 shares of common stock underlying the warrants would be covered by the registration statement filed in connection with the Private Placement and 2,339,945 shares of common stock and 334,277 shares of common stock underlying the warrants will be included in a subsequent registration statement filed by us within 10 days after the end of the 6-month period that immediately follows the date on which ZST Digital files the registration statement to register the shares issued in the Private Placement. Also in connection with the Share Exchange, we paid $350,000 to WestPark Capital, Inc., the placement agent for the Private Placement (“WestPark”), and $125,000 to a third party unaffiliated with ZST Digital, SRKP 18 or WestPark. Immediately after the closing of the Share Exchange, on January 9, 2009, the Company changed its corporate name from “SRKP 18, Inc.” to “ZST Digital Networks, Inc.”

On January 14, 2009, Zhong Bo, our Chief Executive Officer and Chairman of the Board, Wu Dexiu, Huang Jiankang, Sun Hui and Li Yuting (the “ZST Management”), each entered into a Common Stock Purchase Agreement pursuant to which the Company issued and the ZST Management agreed to purchase an aggregate of 12,530,000 shares of our common stock at a per share purchase price of $0.2806 (the “Purchase Right”). The purchase price for the shares was paid in full on May 25, 2009. Each of the shareholders and warrantholders of the Company prior to the Share Exchange agreed to cancel 0.3317 shares of common stock and warrants to purchase 0.5328 shares of common stock held by each of them for each one (1) share of common stock purchased by the ZST Management pursuant to the Purchase Right (the “Share and Warrant Cancellation”). Pursuant to the Share and Warrant Cancellation, an aggregate of 4,156,390 shares of common stock and warrants to purchase 6,676,390 shares of common stock held by certain of our stockholders and warrantholders prior to the Share Exchange were cancelled.

F-19

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 16 – SERIES A PREFERRED STOCK

The Company is authorized to issue 10,000,000 shares of preferred stock.

On January 5, 2009, the Company filed a Certificate of Designations, Preferences and Rights (the “Certificate”) whereby it designated 3,750,000 shares of its preferred stock, $0.0001 par value per share, as Series A Convertible Preferred Stock, (the “Preferred Stock”). Each share of Preferred Stock has a stated value of $1.60. Each share of Preferred Stock is convertible, at the option of the holder at any time and from time to time after the original issue date of the Preferred Stock, into one share of Common Stock, at a conversion price equal to the per share purchase price, subject to adjustment as more fully described in the Certificate. Each share of Preferred Stock has the right to one vote per share of Common Stock issuable upon conversion of the shares of Preferred Stock.

In 2009, the Company conducted five closings of a private placement transaction (the “Private Placement”) of which three closings occurred in the three months ended March 31, 2009. As of March 31, 2009, pursuant to subscription agreements entered into with the investors, the Company sold an aggregate of 2,242,523 shares of Series A Convertible Preferred Stock at $1.60 per share for gross proceeds of $3,585,902. Each share of Preferred Stock shall be convertible at the option of the holder thereof, at any time and from time to time from and after the Original Issue Date into that number of shares of Common Stock determined by dividing the Stated Value of $1.60 of such share of Preferred Stock by the Conversion Price of $1.60.

On January 9, 2009, the Company conducted an initial closing of the Private Placement. Pursuant to subscription agreements entered into with investors, the Company sold an aggregate of 1,097,500 shares of Series A Convertible Preferred Stock at $1.60 per share. As a result, the Company received gross proceeds in the amount of $1,750,902. In connection with the initial closing of the Private Placement, the Company issued a promissory note in the principal amount of $170,000, bearing no interest, to WestPark Capital Financial Services, LLC, the parent company of WestPark, the placement agent for the Private Placement (the “Note”).

On January 23, 2009, the Company conducted a second closing of the Private Placement. Pursuant to subscription agreements entered into with investors, the Company sold an aggregate of 325,563 shares of Series A Convertible Preferred Stock at $1.60 per share. As a result, the Company received gross proceeds in the amount of $525,000, of which $170,000 was used to repay the Note in full.

On February 13, 2009, the Company conducted a third closing of the Private Placement. Pursuant to subscription agreements entered into with investors, the Company sold an aggregate of 819,460 shares of Series A Convertible Preferred Stock at $1.60 per share. As a result, the Company received gross proceeds in the amount of $1,310,000.

In accordance with Emerging Issues Task Force (‘‘EITF’’) 98-5 and EITF 00-27, the Series A convertible preferred stock does not have an embedded beneficial conversion feature (BCF) because the effective conversion price of such shares equals the fair value of the Company’s common stock. The Company determined that the fair value of the common stock at $1.60 per share based on the fact that (1) the common stock is not readily tradable in an open market at the time of issuance, and (2) the Company has recently sold the convertible preferred stock that is convertible into common stock at 1:1 ratio for $1.60 per share in a private placement, therefore the market price of the common stock is $1.60 per share.

| Value Allocated to Preferred Stocks: | ||||

| Proceeds from issuance | $ | 3,585,902 | ||

| Less value allocated to warrants | - | |||

Value allocated to preferred stocks | $ | 3,585,902 | ||

| Market Value of Shares Issuable Upon Conversion: | ||||

| Shares issuable upon conversion of the preferred stocks | 2,242,523 | |||

| Market value of stock on preferred stock issuance date | $ | 1.60 | ||

| Market value of shares issuable upon conversion | $ | 3,585,902 | ||

| Beneficial Conversion Feature: | ||||

| Market value of shares issuable upon conversion | $ | 3,585,902 | ||

| Less value allocated to preferred stocks | 3,585,902 | |||

| Value of beneficial conversion feature | $ | - | ||

F-20

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 16 – SERIES A PREFERRED STOCK (continued)

The Company evaluated whether or not the Series A convertible preferred stock contained any embedded conversion features that meet the definition of derivatives under SFAS 133, “Accounting for Derivative Instruments and Hedging Activities” and related interpretations. Paragraph 12 of SFAS 133 states that an embedded derivative instrument shall be separated from the host contract and accounted for as a derivative instrument pursuant to the statement if and only if all the following criteria are met:

| a. | The economic characteristics and risks of the embedded derivative instrument are not clearly and closely related to the economic characteristic and the risks to the host contact. (Additional guidance on applying this criterion to various contracts containing embedded derivative instrument s is included in Appendix A of this statement.) |

| b. | The contract that embodies both the embedded derivative instrument and the host contract are not measured at fair value under otherwise applicable generally accepted accounting principles with changes in fair value reported in earnings as they occur. |

| c. | A separate instrument with the same terms as the embedded derivative instrument would, pursuant to paragraph 6-11, be a derivative instrument subject to the requirements of this statement. However, this criterion is not met if the separate instrument with the same terms as the embedded derivative instrument would be classified as a liability (or an asset in some circumstance) under the provisions of Statement 150 but would be classified in stockholders’ equity absent the provisions in Statement 150. |

The Series A Preferred Stock has a fixed conversion provision of 1 preferred share for 1 common share and is convertible at the option of the holder and automatically based upon certain events happening. Based upon the above requirement of paragraph 12 of SFAS 133, it is clear that any potential embedded derivatives in the Series A Preferred Stock are clearly and closely related and do not require bifurcation from the host.

The Company evaluated whether or not the convertible preferred stock should be classified as a liability or equity under SFAS 150, “Accounting for Certain Financial Instruments with Characteristics of Both Liabilities and Equity” and Topic D-98 “Classification and Measurement of Redeemable Securities”. The Company concluded that under EITF Topic D-98, preferred securities that are redeemable for cash or other assets are to be classified outside of permanent equity if they are redeemable (i) at a fixed or determinable price on a fixed or determinable date, (ii) at the option of the holder, or (iii) upon the occurrence of an event that is not solely within the control of the issuer. Accordingly, the Company classified the Series A Preferred Stock outside of permanent equity based on the rights of the Series A Preferred Stock in a deemed liquidation.

NOTE 17 – EARNINGS PER SHARE

Basic net income per share is computed by dividing net income by the weighted-average number of shares outstanding during the period.

Diluted net income per share is computed by using the weighted-average number of shares of common stock outstanding and, when dilutive, potential shares from options and warrants to purchase common stock, using the treasury stock method.

The following table illustrates the computation of basic and dilutive net income per share and provides a reconciliation of the number of weighted-average basic and diluted shares outstanding:

| March 31, | ||||||||

| 2009 | 2008 | |||||||

| Net income | $ | 1,246,358 | $ | 1,722,622 | ||||

| Denominator: | ||||||||

| Basic weighted-average shares outstanding | 17,193,667 | 14,515,000 | ||||||

| Effect of dilutive warrants | 382,666 | - | ||||||

| Basic weighted-average shares outstanding | 17,576,333 | 14,515,000 | ||||||

| Net income per share: | ||||||||

| Basic | $ | 0.07 | $ | 0.12 | ||||

| Diluted | $ | 0.07 | $ | 0.12 | ||||

F-21

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 18 – COMMON STOCK WARRANTS

In January 2007, the Company sold to its original shareholders warrants to purchase 7,096,390 shares of common stock at an exercise price of $0.0001. On January 14, 2009, these shareholders canceled an aggregate of 6,676,390 warrants such that the shareholders held an aggregate of 420,000 warrants immediately after the Share Exchange. The warrant has a 5 year term and is not exercisable until at least one year from the date of Share Exchange.

The following is a summary of outstanding warrants at March 31, 2009:

Warrants | Average Exercise Price | |||

| 420,000 | $ | 0.0001 | ||

NOTE 19 – SUBSEQUENT EVENTS

On April 15, 2009, the Company conducted a fourth closing of the Private Placement. Pursuant to subscription agreements entered into with investors, the Company sold an aggregate of 501,949 shares of Series A Convertible Preferred Stock at $1.60 per share. As a result, the Company received gross proceeds in the amount of $693,200 and subscription receivables of $110,800, which were subsequently received.

On May 5, 2009, the Company conducted a fifth closing of the Private Placement. Pursuant to subscription agreements entered into with investors, the Company sold an aggregate of 366,128 shares of Series A Convertible Preferred Stock at $1.60 per share. As a result, the Company received gross proceeds in the amount of $587,051.

On January 14, 2009, Zhong Bo, our Chief Executive Officer and Chairman of the Board, Wu Dexiu, Huang Jiankang, Sun Hui and Li Yuting (the "ZST Management"), each entered into a Common Stock Purchase Agreement pursuant to which the Company issued and the ZST Management agreed to purchase an aggregate 12,530,000 shares of our common stock at a per share purchase price of $0.2806 (the "Purchase Right"). The purchase price for the shares was paid in full on May 25, 2009.

NOTE 20 - CONDENSED PARENT COMPANY FINANCIAL INFORMATION

Basis of Presentation

The condensed parent company financial statements have been prepared in accordance with Rule 12-04, Schedule I of Regulation S-X, as the restricted net assets of the subsidiaries of ZST Digital Networks, Inc. exceed 25% of the consolidated net assets of ZST Digital Networks, Inc. The ability of our Chinese operating subsidiaries to pay dividends may be restricted due to the foreign exchange control policies and availability of cash balances of the Chinese operating subsidiaries. Because substantially all of our operations are conducted in China and a substantial majority of our revenues are generated in China, a majority of our revenue being earned and currency received are denominated in Renminbi (RMB). RMB is subject to the exchange control regulation in China, and, as a result, we may be unable to distribute any dividends outside of China due to PRC exchange control regulations that restrict our ability to convert RMB into US Dollars.

The condensed parent company financial statements have been prepared using the same accounting principles and policies described in the notes to the consolidated financial statements, with the only exception being that the parent company accounts for its subsidiaries using the equity method. Refer to the consolidated financial statements and notes presented above for additional information and disclosures with respect to these financial statements.

F-22

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 20 - CONDENSED PARENT COMPANY FINANCIAL INFORMATION (continued)

ZST Digital Networks, Inc.

(Formerly SRKP 18, Inc.)

CONDENSED PARENT COMPANY BALANCE SHEETS

(Dollars in Thousands)

| March 31, | December 31, | |||||||

| 2009 | 2008 | |||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

| Investment in subsidiaries, at equity in net assets | $ | 14,200 | $ | 8,983 | ||||

| Total Assets | 14,200 | 8,983 | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) | ||||||||

| CURRENT LIABILITIES | ||||||||

| Accrued liabilities and other payable | 381 | - | ||||||

| Total Current Liabilities | 381 | - | ||||||

| COMMITMENTS AND CONTINGENCIES | ||||||||

Preferred Stock Series A Convertible, $0.0001 par value, 3,750,000 shares authorized, 2,242,523 and 0 shares issued and outstanding at March 31, 2009 and December 31, 2008, respectively. Liquidation preference and redemption value of $3,591,000 at March 31, 2009 | 2,946 | - | ||||||

| STOCKHOLDERS’ EQUITY (DEFICIT): | ||||||||

| Common stock, $0.0001 par value, 100,000,000 shares authorized,17,455,000 and 14,515,000 shares issued and outstanding at March 31, 2009 and December 31, 2008, respectively | 2 | 1 | ||||||

| Additional paid in capital | 4,294 | 1,488 | ||||||

| Accumulated other comprehensive income | 168 | 591 | ||||||

| Statutory surplus reserve fund | 1,492 | 1,492 | ||||||

| Retained earnings (unrestricted) | 6,657 | 5,411 | ||||||

| Subscription receivable | (1,740 | ) | - | |||||

| Total Stockholders’ Equity (Deficit) | 10,873 | 8,983 | ||||||

| Total Liabilities & Shareholders' Equity | $ | 14,200 | $ | 8,983 | ||||

F-23

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 20 - CONDENSED PARENT COMPANY FINANCIAL INFORMATION (continued)

ZST Digital Networks, Inc.

(Formerly SRKP 18, Inc.)

CONDENSED PARENT COMPANY STATEMENTS OF OPERATIONS

(Dollars in Thousands)

| For the | For the | |||||||

Three Months Ended | Three Months Ended | |||||||

| March 31, | March 31, | |||||||

| 2009 | 2008 | |||||||

| Unaudited | Unaudited | |||||||

| Revenue | $ | - | $ | - | ||||

| Merger cost | 555 | - | ||||||

| Other general and administrative | 50 | - | ||||||

| Total Expenses | 605 | - | ||||||

| Equity in undistributed income of subsidiaries | 1,851 | 1,723 | ||||||

| Income before income taxes | 1,246 | 1,723 | ||||||

| Provision for income tax | - | - | ||||||

| Net income | $ | 1,246 | $ | 1,723 | ||||

F-24

ZST DIGITAL NETWORKS, INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(Amounts and disclosures for the three months ended March 31, 2009 and 2008 are unaudited)

NOTE 20 - CONDENSED PARENT COMPANY FINANCIAL INFORMATION (continued)

ZST Digital Networks, Inc.

(Formerly SRKP 18, Inc.)

CONSDENSED PARENT COMPANY STATEMENTS OF CASH FLOWS

(Dollars in Thousands)

| For the | For the | |||||||

Three Months Ended | Three Months Ended | |||||||

| March 31, | March 31, | |||||||

| 2009 | 2008 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Cash Flows from Operating Activities: | ||||||||