UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

[X] | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |

|

| |

| For the Fiscal Year Ended December 31, 2012 | |

|

| |

[ ] | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |

|

| |

| For the Transition Period from __________ to | |

|

| |

Commission File Number: 333-145088 | ||

|

| |

SPINDLE, INC. | ||

(Name of small business issuer in its charter) | ||

| ||

Nevada | 20-8242820 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. employer identification number) | |

|

| |

18835 North Thompson Peak Parkway, Suite 210 Scottsdale, Arizona 85255 | 85251 | |

(Address of principal executive offices) | (Zip code) | |

|

| |

Issuer’s telephone number: (480) 335-7351 | ||

| ||

Securities Registered Pursuant to Section 12(b) of the Act: | ||

| ||

Title of each class | Name of each exchange on which registered | |

|

| |

None | None | |

|

| |

|

| |

|

| |

Securities Registered Pursuant to Section 12(g) of the Act: | ||

| ||

None | ||

(Title of class) | ||

| ||

| ||

(Title of class) | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [X] No [ ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ ] No [X]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [X]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.:

Large accelerated filer [ ] | Accelerated filer [ ] |

Non-accelerated filer [ ] (Do not check if a smaller reporting company) | Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act)

Yes [ ] No [X]

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the most recent price at which the common equity was sold: $19,908,140 as of July 19, 2013.

The number of shares outstanding of each of the issuer's classes of common equity, as of July 19, 2013 was 25,078,858.

DOCUMENTS INCORPORATED BY REFERENCE

If the following documents are incorporated by reference, briefly describe them and identify the part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) any annual report to security holders; (2) any proxy or information statement; and (3) any prospectus filed pursuant to Rule 424(b) or (c) of the Securities Act of 1933 ("Securities Act"). The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1990).

2

SPINDLE, INC.

FORM 10-K

For the year ended December 31, 2012

TABLE OF CONTENTS

3

FORWARD LOOKING STATEMENTS

This Annual Report contains forward-looking statements about our business, financial condition and prospects that reflect our management’s assumptions and beliefs based on information currently available. We can give no assurance that the expectations indicated by such forward-looking statements will be realized. If any of our assumptions should prove incorrect, or if any of the risks and uncertainties, underlying such expectations should materialize; our actual results may differ materially from those indicated by the forward-looking statements.

The key factors that are not within our control and that may have a direct bearing on operating results include, but are not limited to, acceptance of our services, our ability to expand its customer base, managements’ ability to raise capital in the future, the retention of key employees and changes in the regulation of our industry.

There may be other risks and circumstances that management may be unable to predict. When used in this Report, words such as, "believes," "expects," "intends," "plans," "anticipates," "estimates" and similar expressions are intended to identify and qualify forward-looking statements, although there may be certain forward-looking statements not accompanied by such expressions.

PART I

ITEM 1 - DESCRIPTION OF BUSINESS

History

Spindle, Inc., a Nevada corporation ("Spindle," "SPDL," "we," "us," or the "Company"), was originally incorporated in the State of Nevada on January 8, 2007 as “Coyote Hills Golf, Inc.” We were previously an online retailer of golf-related apparel, equipment and supplies and generated minimal revenues from that line of business.

On December 2, 2011, we acquired certain assets and intellectual property from Spindle Mobile, Inc. ("Spindle Mobile"), a Delaware corporation in the business of data processing, mobile payments fields and other related fields, in exchange for approximately 80% of the issued and outstanding common stock of the Company, which shares were distributed to the stockholders of Spindle Mobile, pursuant to the terms and conditions of an Asset Purchase Agreement, dated December 2, 2011 (the "Spindle Mobile Agreement").

Concurrent with the closing of the Spindle Mobile Agreement, we amended our articles of incorporation to change our name from "Coyote Hills Golf, Inc." to "Spindle, Inc." Additionally, we increased our authorized capital from 200,000,000 shares of common stock, $0.001 par value, and 100,000,000 shares of preferred stock, $0.001 par value to 300,000,000 shares of common stock, $0.001 par value, and 50,000,000 preferred stock, $0.001 par value. The actions were approved on November 11, 2011, by the consent of the majority stockholders who represent 90% of our issued and outstanding common stock, and effective on of December 2, 2011.

On October 11, 2012, pursuant to Article XII of the Company’s Articles of Incorporation, the Board of Directors amended the Company’s bylaws to (i) include the Chief Executive Officer as a person who may call a meeting of the Board of Directors and a special meeting of the Board of Directors; (ii) allow a quorum of the Board of Directors to be set by resolution of the Board of Directors; (iii) amend the description of the offices of Chief Executive Officer/President; (iii) set the annual meeting of shareholders at a time to be fixed by the Board of Directors; and (iv) allow for the election of Directors by a plurality of the votes cast in an election. Amendments to the bylaws were approved by the stockholders holding of a majority of the shares of entitled to vote thereon on October 29, 2012.

On December 31, 2012 (the “Parallel Acquisition Closing Date”), pursuant to that certain Asset Purchase Agreement (the “Parallel Agreement”) by and between the Company and Parallel Solutions Inc., a Nevada corporation (“Parallel”), the Company acquired substantially all of Parallel’s assets used in connection with its business of facilitating electronic payment processing services to merchants (the “Parallel Assets”), assumed certain specified assumed liabilities consisting of approximately $46,225 in outstanding accounts payable and residual liabilities of Parallel (as more specifically described in the Parallel Agreement), and hired seven employees of Parallel in exchange for 538,570 restricted shares (the “Aggregate Share Consideration”) of common stock, of which 53,857 shares (the "Indemnification Escrow") and 100,000 shares (the "Deferred Consent Escrow") were deposited in escrow with our transfer agent. The Indemnification Escrow will be held for a period of one year from the Closing Date and will be available to compensate the Company pursuant to the indemnification obligations of Parallel under the Parallel Agreement, and for any necessary accounts receivable adjustment after the Parallel Acquisition Closing Date.

4

The Deferred Consent Escrow will be held for a period of up to five years after the Closing Date and will be released to Parallel or its legally permitted assign(s) incrementally as and when certain specified contract assignments or residual revenue streams are properly assigned to the Company or the residual revenue streams in respect of such specified contracts are bought out by the applicable third party, and otherwise the Deferred Consent Escrow is subject to cancellation to the extent such specified assignments or buy-outs fail to occur during such five year period, all as more particularly set forth in the Parallel Agreement.

On March 20, 2013 (the “MeNetwork Closing Date”), the Company assumed certain liabilities and acquired substantially all the assets of MeNetwork, Inc. (“MeNetwork”) used in connection with its business of developing, marketing and licensing a mobile marketing platform for use by merchants and consumers (the “MeNetwork Assets”), pursuant to an Asset Purchase Agreement, dated March 1, 2013, by and between Spindle and MeNetwork (the “MeNetwork Agreement”). As consideration for the assumption of such liabilities and the acquisition of the MeNetwork Assets, the Company issued an aggregate of 2,750,000 shares of common stock to the stockholders of MeNetwork, of which 350,000 shares are being held in escrow for a period of one year from the MeNetwork Closing Date for the purposes of satisfying any indemnification claims. In addition, upon the earlier of 180 days following the MeNetwork Closing Date or a change in control of the Company, the Company shall issue an additional 750,000 shares of common stock to Ashton Craig Page, the director and Chief Operating Officer of MeNetwork and a current director of the Company.

Financial Restatement, Regulatory Reviews and Other Significant Recent Events

On February 6, 2013, the Company’s Board of Directors, after consultation with management, determined that the Company’s financial statements for the fiscal year ended December 31, 2011 (the "2011 Fiscal Year") as included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2011 (the "2011 Annual Report"), and the financial statements, as included in the Company’s Quarterly Reports on Form 10-Q for the fiscal quarters ended March 31, 2012, June 30, 2012 and September 30, 2012 (the "2012 Fiscal Quarters", together with the 2011 Fiscal Year, the “Restatement Periods”) should no longer be relied upon and should be restated because of the Company’s characterization of the acquisition of the Spindle Mobile Asset as an asset acquisition instead of a reverse capitalization. Accordingly, as of the date hereof, the restatement of the Restatement Periods has not yet been completed.

Overview of Our Business

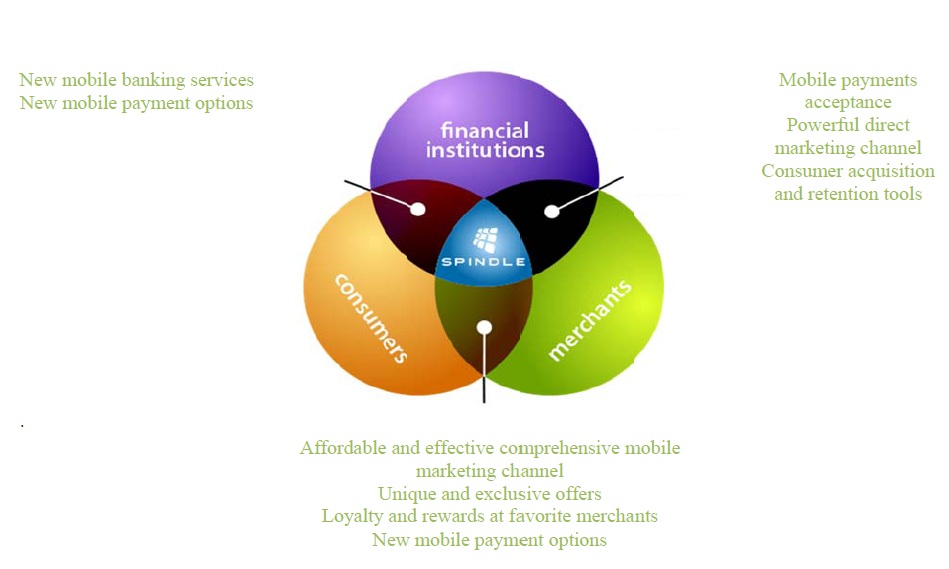

Spindle has developed a comprehensive mobile commerce platform for consumers and merchants. The Company generates revenue through the processing of electronic payments and delivery of mobile advertising and marketing services through mobile phones and connected devices. We believe that Spindle enables a trusted relationship between buyers and sellers, consumers and merchants, and third party partners through our secure payments processes, incentives, and promotions, which include marketing coupons and vouchers, offers, loyalty programs, and consumer feedback on merchants, products, and services. Spindle provides the platform for the secure movement of funds between parties and the requisite conversion tools for brands, merchants, and partners to deliver a seamless, hassle-free (what we term “frictionless”) mobile commerce ecosystem.

Numerous research reports predict rapid growth in mobile payment transactions over the next several years. For example, IE Market Research projects mobile payment transactions rising to $945 billion globally and $260 billion in North America by 2015 (IE Research - 2013 Global Mobile Payment Market Forecast 2009 - 2017). With mobile communications and cloud-enabled services entering every aspect of our daily life, we believe that the service providers that can tie together mobility, convenience, universal access to payments and marketing stand to gain significantly by serving the instant needs of our fast-paced economy.

Spindle Services

Spindle has developed an ecosystem that combines the benefits of a full-function mobile marketing platform and a secure full-function mobile payment platform. It is the combination of these two services that we believe separates Spindle from the other entrenched payments companies and the newly minted mobile marketing companies. Spindle has built a services platform that we call our ‘Ecosystem’ where buyers and sellers come together to establish a ‘Community’.

5

Spindle users can select their favorite merchant, receive real-time and relevant offers, join brand loyalty programs, and make instant one-click purchases from their mobile phone or connected devices. Through integration with Facebook, LinkedIn, and phone contacts, customers are able to send money, recommend a merchant, share a coupon, or write a review that will be posted on the Spindle platform and shared with social media channels. Spindle's solution enables consumers to establish their user profile where favorite merchants, merchant interaction preferences, and location-based offer preferences are kept.

For merchants, we believe that the Spindle suite of products - a broad spectrum of payment services and customer engagement tools - chosen individually or in concert with one another - offer a better way to extend the life of environmental, internet, mobile, and other networked marketing and advertising campaigns. Spindle products are device- and hardware-agnostic, focusing instead on enterprise, banking, and brand-centric solutions that streamline the transactional process in a highly secure space. A basic tenet behind our “frictionless” finance concept is our commitment to providing easy-to-use enterprise class solutions for any size company.

Spindle’s solution includes a full-function cloud-based wallet where customers will link their credit cards, debit cards, and Demand Deposit Accounts (DDA), and deposit checks with their mobile phone or connected devices. It is expected that the Spindle solution will also indirectly offer a proprietary micro-credit facility for use with participating merchants and a sub-account that will allow users to earn interest income. We plan for these services to be collectively made available to consumers through partnerships with banking institutions, wireless carriers, and/or specialized affinity groups like sports teams, political organizations, or large brands.

The Mobile Payments Market

Each of the two primary mobile wallet solutions - Near Field Communications (NFC) and cloud-based approaches require changes to the Point Of Sale (POS). NFC requires new hardware, which of negative consequence, requires investment by both the merchant and consumer to transmit confidential payment data between devices. The standard cloud-based approach requires only a software change at the point of sale. Within our Cloud based platform no payment data is exchanged at the point of sale allowing the secure payment networks to move funds between the buyer and sellers account in a secure and global environment. We believe for mobile commerce to be successful there has to be an end-to-end solution offered by service providers and their partners. We also believe that wallet adoption by consumers will be dependent on the secure access to payment accounts, acceptance of wallet payments at the POS, and tangible benefit for both consumers and merchants. In today’s environment, there is essentially no critical mass adoption on either side of buyer-seller relationship. Merchants and consumers demand a value-added experience when using a mobile wallet as compared to traditional card swipe methods of payment. Separately, risk management and fraud controls are critical to maintaining momentum of any new payment service provider.

Given the size and growth prospects of the mobile commerce market, we anticipate many potential competitors. As we survey the competitive environment we believe that few suppliers, if any, presently offer the comprehensive platform that Spindle provides, and some of the larger, more visible and brand centric competitors are focused on enabling legacy or traditional services through the addition of a mobile application.

Against this backdrop, we believe we enjoy several competitive advantages. First, we offer a white-label solution enabling our partners to enter the mobile commerce marketplace under their own brand. We also offer an end-to-end universal payment processing capability. To add critical value to the buyer and seller, we layer our core platform with a full service mobile marketing and loyalty platform that allows merchants to establish and foster direct communication with consumers via their mobile and cloud aware devices. Finally, we have assembled a strong team of payments industry and mobile marketing professionals that provide responsiveness and attention to our channel partners.

Numerous research reports predict rapid growth in mobile payment transactions over the next several years. For example, IE Market Research projects mobile payment transactions rising to $945 billion globally and $260 billion in North America by 2015 (IE Research - 2013 Global Mobile Payment Market Forecast 2009 - 2017). With mobile communications and cloud-enabled services entering many aspects of our daily life, we believe that the service providers that can tie together mobility, convenience, universal access to payments and marketing stand to gain significantly by serving the instant needs of our fast-paced society.

Spindle set out at the onset to create a solution for the mobile marketplace that offered the best of the mobile marketing and advertising solutions coupled with a mobile enabled payment solution that delivered a seamless experience for our customers.

6

To our company promise, Spindle offers a solution where merchants come to a single portal to conduct all of their mobile business regardless of size or scope. MeNetwork allows merchants to create custom marketing messages, using a simple merchant interface, and syndicate those messages to anyone carrying a mobile phone, either through the MeNetwork free iPhone and iPad applications (App), free Android applications, or via SMS/text. MeNetwork forges a direct and measurable connection between a merchants business and the consumers targeted, and allows merchants to instantly vary messages and offers on the fly based on a business’s needs and market conditions. The MeNetwork also allows merchants to inexpensively stay in touch with their most loyal customers and keep them up-to-date on latest deals and special offers, enables mobile payment acceptance, purchases of both virtual and physical goods and services, and referrals via integrated social media including Facebook and Twitter.

We currently support thousands of merchants on our systems supplying these merchants a range of solutions for traditional retail, mobile retail, and e-commerce using Spindle services for mobile marketing, advertising, and payment processing services. Spindle services are delivered to merchants using the newest Software as a Service (SaaS) and Mobile Point of Sale (POS) technology as well as traditional cloud aware Point of Sale (POS) solutions.

Our Growth Strategy

We believe that Spindle differs from most of its competitors in a fundamental way: Spindle offers services to banking institutions and non-bank third parties who are interested in offering mobile commerce services to their retail and commercial customers under their brand as a white-labeled solution. Spindle relies heavily on a strategy of selling services through strategic alliances and affiliations (Channels) in the implementation of our business plan. We intend to leverage our branding partners with established consumer brands to offer the white-labeled or co-branded versions of our products to their customers. We believe that these relationships will help us acquire our target users in a cost-effective manner and enable our channels to drive customer acquisition and retention by better serving their customers.

Spindle has embraced the white-label model, which enables market leaders in any industry to effectively offer a comprehensive and competitive mobile commerce service to their customers. For bank partners this enables them to keep their customers’ funds in their bank by using the bank’s Demand Deposit Account (DDA) as the funding account, as opposed to moving money into a PayPal account. It allows non-bank partners to offer mobile solutions to their customers and participate in the revenue from a service that today is out of reach.

We believe that a principal benefit Spindle offers our branding partners is an ability to tailor our product offerings to match their specific customer’s needs. By offering a comprehensive and flexible platform, we expect our partners to realize the benefits of competitive fees, lower administrative costs, lower transactional costs, and higher customer retention.

Our Revenue Model

On the consumer side, our MeNetwork consumer facing mobile application, which works in concert with the virtual marketing interface, is free to users. Our channel partners cover branding and integration costs, with network transaction fees covered by the bank or branding partner.

On the merchant side, we generate revenue through payments processing and MeNet marketing platform services. For payment services, we offer competitive payment processing rates as a percentage of transaction volume. We offer a flat rate pricing plan as well as completive-tiered pricing for merchant acquiring services for credit card, check, and ACH processing services. Spindle is a full-service merchant acquirer registered under Visa and MasterCard, and sponsored by Bank of America Merchant Services (our processing partner). Flexible payment processing rates allow us to offer completive solutions through our channels who service merchants in many of the popular markets such as Mobile phone based POS (MPOS), SaaS based POS, traditional ecommerce (Web), retail, and restaurant. Our MeNetwork mobile marketing and loyalty platform carries a Monthly fee based on three pricing tiers. Additionally, we charge a transaction fee when payments are cleared through the payment-processing platform, which is integrated into the MeNetwork marketing portal. This allows customers to seamlessly make purchases for goods and services offered by our merchants.

7

Business Status

Our first service in the unattended or Vending market segment has been generating revenues from vending machine operations since May 2012. We are excited about our relationship with Bank of America, which works with us to provide payment services for vending machines nationwide. Development of our full service as a Payment Service Provider (PSP) was completed in November 2012. Post-completion, we received PCI Service Provider Level 1 certification, which enabled us to process a full range of payment transaction under our registration as a Payment Service Provider and Payment Facilitator (PSP / PF). Additionally, Spindle processes checks and ACH transactions for our merchants and sub-merchants.

We have completed iOS and Android development of both our MeNetwork mobile marketing and loyalty solution and our Mobile POS solution for mobile merchant acquiring. Development of our fully integrated consumer wallet app is targeted for completion in Q3 of 2013. This new app combines exiting Spindle payments functionality with existing MeNetwork mobile marketing functionality in a full-featured mobile commerce solution.

Via the MeNetwork platform, Spindle currently offers services in 85 US cities and 20 international cities. We are working to add payments capabilities for our international partners to leverage the integrated and seamless nature of the Spindle mobile commerce capabilities.

Spindle offers merchants an all-in-one solution

The tug of war between technologies also referred to as “wallet wars” is underway. There are numerous technology providers vying for relevance in the market. The large players are Visa, MasterCard, Google, and ISIS, to name a few. Their solutions provide a component of the transaction stream that is focused on a technical aspect of passing payment card or payment account information from buyer to seller using a mobile phone and an enabled Point of Sale (POS) system to accept the secure Near Field Communications (NFC) transaction. While the Spindle solution is compatible with these wallets, we believe that the evolution of payments will ultimately move to a cloud or network-based solution. In support of this evolution, Spindle solutions enable payment though “authenticated” cloud-based processes that we project will reduce the risk and uncertainty of the payment process.

Spindle’s solution includes a full function cloud-based wallet where customers will be able to link their credit cards, debit cards, and DDA accounts, and deposit checks with their mobile phone. It is expected that the Spindle solution will also indirectly offer a proprietary micro-credit facility for use with participating merchants and a sub-account that will allow users to earn interest income. We plan for these services to be made available to consumers through partnerships with banking institutions, wireless carriers, and/or specialized affinity groups like sports teams, political organizations, or large advertisers.

Spindle’s Marketing solutions reach the marketplace

Spindle has developed an ecosystem that combines the benefits of a full-function mobile marketing platform and a secure full-function mobile payment platform. It is the combination of these two services that we believe separates Spindle from the other entrenched payments companies and the newly minted mobile marketing companies. Spindle has built a services platform that we call our ‘Ecosystem’ where buyers and sellers come together to establish a ‘Community’.

Spindle users will be able to select their favorite merchant, receive targeted offers, join their loyalty program, and make instant one-click purchases from their mobile phone. Through integration with Facebook and phone contacts, customers will be able to send money, recommend a merchant, share a coupon, or write a review that can be posted on the Spindle platform and shared with social media channels. Spindle's solution will enable consumers to establish their user profile where favorite merchants, merchant interaction preferences, and location-based offer preferences are kept.

For merchants, we believe that the Spindle suite of products - a broad spectrum of payment services and customer engagement tools - chosen individually or in concert with one another will offer a better way to extend the life of environmental, internet, mobile, and other networked marketing and advertising campaigns. Spindle products are device and hardware agnostic, focusing instead on enterprise, banking, and brand-centric solutions that streamline the transactional process in a highly secure space. A basic tenet behind our “frictionless finance” concept is our commitment to providing easy-to-use enterprise class solutions for any size company.

8

Spindle enables a new combination of services for the market. It enhances the interaction between the money centers (the banks and Financial Institutions) and their customers both Consumer and Commercial. Spindle drive innovation through the channel and delivers new revenue opportunities and enhanced customer retention. Spindle puts the financial institution firmly in the value chain of the mobile commerce market.

Regulation

Regulation of the payments industry, including regulations applicable to us and our channel partners, have increased significantly in the last several years. These changes include new requirements in the Patriot Act, Dodd-Frank, Durban, and similar legal developments. The recent economic cycle has exposed risks in the banking and payment market. As a result we anticipate a continued active regulatory environment in the US and Europe that could impact the services we provide.

We are subject to regulations that affect the financial services and payment industry in which our services are used. In particular, our partner banks and financial institutions are subject to regulations applicable in the United States and abroad. Consequently, Spindle is affected by such regulations. Spindle is covered by, or touches, regulation for Banking, Money Services, and consumer laws like uniform commercial code. Spindle must complete with US Patriot Act, Bank Secrecy Act, and a variety of related laws. Spindle is careful to comply with and conducts internally and externally reviews. Externally we are periodically reviewed by our processing sponsors, and auditors related to their areas of expertise.

Spindle is also covered by Payment Card Industry (PCI) data protection policies. Spindle employs an external PCI audit firm to ensure we are following best practices and have the required system reviews. Spindle is currently certified to operate as a Service Provider at Level 1, which is the highest possible certification.

Competition

Spindle is positioned in the market as both a payment processing solution provider and a mobile marketing solution provider. As such, we have competition with both solutions. As Spindle completes the full integration of our services, we find ourselves with a unique capability to deliver an integrated marketing and payment solution that joins the two markets. We currently find little to no competition with this combined solution. We certainly anticipate this is the direction other companies will pursue and they may in fact be doing so now.

9

General Purpose Payment Card Industry. Within the general-purpose payment card industry there is substantial and increasingly intense competition worldwide from suppliers who offer payment processing for Visa, MasterCard, American Express, and Discover card. Spindle has positioned itself as a supplier of processing services by engaging in the market as both a Payment Services Provider (PSP) under Visa, and Payment Facilitator (PF) under MasterCard. This is a relatively new category for registration for with the card brands and today there are a variety of like suppliers in the market. Most are of which are focused on specific verticals, but some do offer services similar to Spindle.

Competition in the payments card industry ranges from new mobile wallet technology with NFC (near field communication), to closed-loop payment solutions, to Software-as-a-Service (SaaS) based Point of Sale (POS) services. These are the categories in which Spindle is collaborating to offer our cloud-based payment processing services. With our ability to underwrite and approve merchants and bundle marketing services through a single Application Programming Interface (API), Spindle seeks to engage these emerging technologies by enabling their efficient connection with the legacy payment networks, simplification of PCI requirements, and turnkey settlement services.

Spindle has also contracted with approximately 130 sales agents in the payments market to offer our payment services to merchants and third parties suppliers in the market. With the combination of marketing and payment solutions combined with our ability to underwrite and service merchants with these new PSP/PF capabilities, ACH and check services, Spindle continues to offer competitive solutions and attract new sales agents.

Specific companies are usually mentioned when we are in the market selling services. Once such company is PayPal, which has established a strong brand both domestically and internationally. PayPal not only provides a private payment services using funds within the PayPal network. They also support payment processing of open-loop cards for traditional payment acceptance. In addition, PayPal has recently engaged in a ‘cooperative’ arrangement with Discover Card extending access to PayPal funds beyond their original in network merchants.

Another company usually mentioned by our potential channel partners is Square. Square functions as micro merchant acquirers and is registered as a PSP/PF focused on servicing the needs of this underserved market. While Spindle does not directly compete with Square, our technology is used to deliver a substantially similar service to our channel partners who do so under their brands. Square has recently expanded their service to include a service targeted at the small to mid-sized merchant which is in line with the market segment that Spindle targets. Spindle today provides a broader service than Square however, with their access to funds and growing brand awareness Spindle may find Square more involved with our target markets than exists today.

We have been told by speakers at recent industry conferences that there are nearly 140 digital wallet suppliers in the market. While we have no way to verify, nor do we have a list of such suppliers, it demonstrates the great fracture present in the market. Spindle has components of a digital wallet built into our consumer marketing application as delivered by our MeNetwork solution. While offering a wallet technology to the market is not the focus of Spindle, we do use our homegrown wallet technology to services customer who wish to make purchased from merchants who advertise. It is the acceptance of mobile payments that spindle is working to solve. By becoming a processor of mobile payments, we hope to enable these wallet technology providers to succeed in the market through standardizing mobile transaction technology and growing merchant payment acceptance through our platform.

Mobile Marketing, Advertising and Loyalty industry. Spindle’s solution in the mobile marketing segment is delivered through our MeNetwork marketing platform, which is focused on providing our merchant the ability to publish offers, events and coupons to subscribers of the MeNet mobile application for iOS and Android phones and tablets. Additionally the MeNetwork platform includes a full function loyalty capability to help our merchant customer attract and retain customers through repeat business, special events, earned discounts, and more.

Competitors in this space, while not offering a complete completive technology, are companies such as Groupon, Living Social, and FourSquare. Each of which started with adjacent solution but now moving into payment enabled marketing services.

We believe Spindle’s capability weight our merchant facing marketing and full service payment process is unique we certainly expect others to more closely match our solution over time. First person marketing defines are very targeted ads, appears to be gaining a significant advantage over the more traditional third party group distribution advertising. Spindle has always believed that “timely and relevant” ads were what consumers wanted and we constructed our system to achieve this objective. As such, there is a clear migration away from “daily deals” and group promotions that target the broader group. This movement is evident by the actions of other suppliers in the market.

10

Although we believe that Spindle has a real competitive advantage in these areas, we are a small company competing against a number of large, established competitors. As such, our competitive advantage could erode as we prove the advantages of a service like ours. Today Spindle generates revenue from both payment solutions and mobile marketing. While our revenue is greatly enhanced by plan to become a processor of mobile payments for the Mobile Wallets and Mobile Marketing suppliers in the market, our revenue forecast and ability to become cash flow positive is not reliant on that success.

Company Management

Management Team Employees are key to the success of any business. Great technology and good ideas only go so far. To ensure spindle had the horsepower to put our evolutionally idea in to place we have assembled a team of proven industry executives.

·

William Clark - CEO, 25+ years of expertise. 17 years Executive with First Data responsible for $350M in annual revenues. EVP/GM Apriva LLC for 6 years grew to leader in space and $30M in annual revenues. 2 years with Spindle.

·

Tom Lineen - EVP, 13+ year’s ecommerce payments expertise. Founder and CEO Parallel Solutions acquired by Spindle in 2012. Previously success with Authorize.net and Cynergy Online.

·

Michael Stevens - SVP Marketing and Innovation. 18+ year career in advertising producing award-winning campaigns digital work for clients like Apple, Porsche, Air France, Weber, and Vail Resorts.

·

John Tharpe - SVP Strategy & Business Development, 22+ year’s expertise. VP of strategic partnerships at BAMS, responsible for BAMS’ mobile wallet, 3rd party payment gateway, professional sports acquiring and mobile payments strategies. Previous success as a cofounder of Trust Commerce.

·

Kevin McNish - VP, Product Development, 15 years expertise. First Data Merchant Services. Holds several payments related patents. Focused on merchant facing Pont-of-Sale solutions both internationally and U.S.

·

Sean Tate - VP, Engineering and chief architect, 15 years of experience in developing enterprise class distributed payment processing systems for companies such as Allied Wallet LLC, L&G Mortgagebanc LLC, and Advanced Financial Services, Inc.

Technology Spindle has leveraged the combined experience of card issuing, Merchant acquiring, Payment gateway, Ecommerce and marketing to develop a system designed for mobile. Spindle’s systems leverage leading technology frameworks and run in Amazon’s AWS infrastructure.

Intellectual Property

Spindle’s intellectual property portfolio supports and enhances our enterprise payment solutions, which is developed both internally and through acquisition. Spindle owns 4 patents and it has an additional 3 patent applications pending with the United States Patent & Trademark Office (U.S.P.T.O).

Spindle’s initial patent portfolio plays an integral role in technology platforms and services and the movement of value over networks. We believe that the patents are foundational to the methods used in networked payments. The patent portfolio includes one continuation patent in a family of patents related to “Processing Payment on the Internet” now pending with the U.S.P.T.O.

Number of total employees and number of full time employees

As of July 19, 2013, we employed 14 individuals all of whom are full time employees

11

Reports to Security Holders

We are a reporting issuer with the Securities and Exchange Commission. We voluntarily file periodic reports, with the Securities and Exchange Commission to maintain the fully reporting status. We will furnish shareholders with annual financial reports certified by our independent registered public accountants. The public may read and copy any materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Our SEC filings will be available on the SEC Internet site, located at http://www.sec.gov.

ITEM 1A - RISK FACTORS.

Risks Related to Our Business

We have incurred losses since our inception and cannot assure you that we will achieve profitability.

The Company has incurred net losses since inception. Coyote Hills Golf, Inc. was originally incorporated in the State of Nevada on January 8, 2007. Spindle Mobile was incorporated in the State of Delaware on January 14, 2011. On December 2, 2012, Coyote Hills and Spindle Mobile consummated a reverse acquisition whereby Spindle mobile was deemed the accounting acquirer and Coyote Hills the legal acquire resulting in a recapitalization of Spindle Mobile. Simultaneous to the reverse acquisition Coyote Hills Golf, Inc. effected a name change to Spindle, Inc. Coyote Hills Golf, Inc. was previously an online retailer of golf-related apparel, equipment and supplies. As shown in the accompanying financial statements, the Company has incurred a net loss of $2,616,613 for the period from January 14, 2011 (inception) to December 31, 2012. The extent of our future operating losses and the timing of profitability are highly uncertain and we may never achieve or sustain profitability. We cannot assure you that we will ever generate sufficient revenues from our operations to achieve profitability. If revenues grow slower than we anticipate, or if operating expenses exceed our expectations or cannot be adjusted accordingly, we may not ever achieve profitability and the value of your investment could decline significantly.

These factors create a substantial doubt about our ability to continue as a going concern and our auditors have included a going concern qualification in their report on our audited financial statements.

We are in the early stages of our life cycle and have limited operating history. Therefore, there is limited historical or current operating information upon which an investor can base its investment decision.

We have limited operating history on which to base an evaluation of our business and prospects. To date, we have engaged primarily in research, development and partnering agreements, securing rights to essential technology, product testing, engaging markets and distribution sources, and making other arrangements necessary to begin operations. As an early stage company, we have no prior experience in implementing and managing our planned business in an operational setting. Accordingly, there can be no assurance that we will be able to successfully implement our business plans or strategies.

We cannot provide any assurance that we will be successful in addressing the risks that we may encounter, and our failure to do so could have a material adverse effect on our business, prospects, financial condition and results of operations.

If we are unable to obtain additional capital, we may be unable to proceed with our long-term business plan, and we may be forced to curtail or cease our operations.

We require additional working capital to support our long-term business plan, which includes identifying suitable targets for horizontal or vertical mergers or acquisitions, so as to enhance the overall productivity and benefit from economies of scale. We expect to pursue acquisitions of, or investments in, businesses and assets in new markets that complement or expand our existing business. Our working capital requirements and the cash flow provided by future operating activities, if any, will vary greatly from quarter to quarter, depending on the volume of business during the period and payment terms with our channel partners. We may not be able to obtain adequate levels of additional financing, whether through equity financing, debt financing or other sources. Additional financings could result in significant dilution to our earnings per share or the issuance of securities with rights superior to our current outstanding securities. In addition, we may grant registration rights to investors purchasing our equity or debt securities in the future. If we are unable to raise additional financing, we may be unable to implement our long-term business plan, develop or enhance our products and services, take advantage of future opportunities or respond to competitive pressures on a timely basis, if at all. In addition, a lack of additional financing could force us to substantially curtail or cease operations.

12

Pressures from competitors with more resources may limit our market share, profitability, and growth.

We face aggressive competition from numerous and varied competitors in all of our markets, making it difficult to maintain market share, remain profitable, and grow. Even if we are able to maintain or increase our market share for a particular product, revenue or profitability could decline due to pricing pressures, increased competition from other types of products, or because the product is in a maturing industry.

Our competitors may be able to more quickly develop or adapt to new or emerging technologies, better respond to changes in the requirements or preferences of our channel partners, or devote greater resources to the development, promotion, and sale of their products. Some of our competitors have, in relation to us, longer operating histories, larger customer bases, longer standing relationships with customers, greater name recognition, and significantly greater financial, technical, marketing, customer service, public relations, distribution, or other resources. Some of our competitors are also significantly larger and have increased their presence in our markets in recent years through internal development, partnerships, and acquisitions. There has also been significant consolidation among our competitors, which has improved the competitive position of several of these companies and enabled new competitors to emerge in all of our markets. In addition, we may face competition from solutions developed internally by our channel partners. To the extent we cannot compete effectively, our market share and, therefore, results of operations, could be materially adversely affected.

Because price and related terms are key considerations for many of our channel partners, we may have to accept less-favorable payment terms, lower the prices of our products and services, and/or reduce our cost structure, including reducing headcount or investment in research and development, in order to remain competitive. Certain of our competitors have become increasingly aggressive in their pricing strategy, particularly in markets where they are trying to establish a foothold. If we are forced to take these kinds of actions to maintain market share, our revenue and profitability may suffer or we may adversely influence our longer-term ability to execute or compete.

Our growth is dependent upon our ability to attract channel partners.

Our performance depends on successfully selling our services to channel partners such as banks, cellular carriers, and other third party companies looking to offer a mobile solution by purchasing our Software as a Service platform rather than building an in-house solution. This is a dual risk that the market does not support outsourcing of mobile payment solutions and that we can effectively sell against our competitors, some of whom sell an outsource solution as defined in the previous paragraph.

Our business is dependent upon our ability to attract and retain skilled personnel.

Our performance depends on successfully attracting and retaining talented and qualified employees, including sales and marketing personnel. The market for highly skilled personnel in our industry is extremely competitive. If we are less successful in our recruiting efforts, or if we are unable to retain key employees, our ability to develop and deliver successful products and services may be adversely affected. Effective succession planning is also important to our long-term success. Failure to ensure effective transfer of knowledge and smooth transitions involving key employees could hinder our strategic planning and execution.

The Wall Street Reform and Consumer Protection Act may have a material adverse impact on our revenue, our prospects for future growth and our overall business, financial condition and results of operations.

The Wall Street Reform and Consumer Protection Act recently enacted in the United States establishes regulation and oversight by the U.S. Federal Reserve Board of debit interchange rates and certain other network industry practices. Among other things, it requires debit and prepaid “interchange transaction fees” (referred to in the Wall Street Reform and Consumer Protection Act as fees established, charged or received by a payment card network for the purpose of compensating an issuer for its involvement in an electronic debit transaction) to be “reasonable and proportional to the cost incurred by the issuer with respect to the transaction.” At this time the law is published and we believe our payment service is exempt. Should that change there would be an impact on our business model due to the costs of compliance with such law.

13

Additionally, the Wall Street Reform and Consumer Protection Act provides that neither an issuer nor a payment card network may establish exclusive debit network arrangements or inhibit the ability of a merchant to choose among different networks for routing debit transactions. Under alternative rules proposed by the Federal Reserve, either (1) a debit card would meet the requirements of the Wall Street Reform and Consumer Protection Act as long as it could be used in at least two unaffiliated networks, or (2) each debit card would be required to function in at least two unaffiliated networks for each method of authorization that the cardholder could use for transactions (i.e., two signature and/or two PIN networks). Some of Spindle services will use a debit card or prepaid card product for consumer funds.

The Wall Street Reform and Consumer Protection Act also created two new independent regulatory bodies in the Financial Reserve System. The Bureau will have significant authority to regulate consumer financial products, including consumer credit, deposit, payment, and similar products; although it is not clear whether and/or to what extent the Bureau will be authorized to regulate broader aspects of payment card network operations. The Council is tasked, among other responsibilities, with identifying “systemically important” payment, clearing and settlement systems that will be subject to new regulation, supervision and examination requirements, although it is not clear whether Spindle would be deemed “systemically important” under the applicable statutory standard. If Spindle were deemed “systemically important,” it could be subject to new risk management regulations relating to its payment, clearing, and settlement activities. New regulations could address areas such as risk management policies and procedures; collateral requirements; participant default policies and procedures; the ability to complete timely clearing and settlement of financial transactions; and capital and financial resource requirements. In addition, a “systemically important” payment system could be required to obtain prior approval from the U.S. Board of Governors of the Federal Reserve System or another federal agency for changes to its system rules, procedures or operations that could materially affect the level of risk presented by that payment system. These developments or actions could increase the cost of operating our business and may make payment card transactions less attractive to card issuers, as well as consumers. This could result in a reduction in our payments volume and revenues.

If issuers, acquirers and/or merchants modify their business operations or otherwise take actions in response to this legislation which have the result of reducing the number of debit transactions we process or the network fees we collect, the Wall Street Reform and Consumer Protection Act could have a material adverse impact on our revenue, our prospects for future growth and our overall business, financial condition and results of operations. Failure by our channel partners or by us to adjust our strategies successfully to compete in the new environment would increase this impact.

The payments industry is the subject of increasing global regulatory focus, which may result in the imposition of costly new compliance burdens on us and our channel partners and may lead to increased costs and decreased transaction volumes and revenues.

The regulatory environment has seen rapid chance in recent years. These changes range for new requirements in the Patriot Act, Frank-Dodd, Durban, and more. We are subject to regulations that affect the payment industry in which our service is used. In particular, our partner banks and financial institutions are subject to regulations applicable in the United States and abroad, and, consequently, Spindle is at times affected by such regulations. Regulation of the payments industry, including regulations applicable to us and our channel partners, has increased significantly in the last several years.

Increased regulatory focus on us, such as in connection with the matters discussed above, may result in costly compliance burdens and/or may otherwise increase our costs, which could materially and adversely influence our financial performance. Similarly, increased regulatory focus on our channel partners may cause such partners to reduce the volume of transactions processed through our systems, which could reduce our revenues materially and adversely influence our financial performance. Finally, failure to comply with the laws and regulations discussed above to which we are subject could result in fines, sanctions or other penalties, which could materially and adversely affect our results of operations and overall business, as well as have an impact on our reputation.

General economic and global political conditions may adversely affect trends in consumer spending, which may materially and adversely impact our revenue and profitability.

The global payments industry depends heavily upon the overall level of consumer, business and government spending. General economic conditions (such as unemployment, housing and changes in interest rates) and other political conditions (such as devaluation of currencies and government restrictions on consumer spending) in key countries in which we operate may adversely affect our financial performance by reducing the number or average purchase amount of transactions involving payment cards carrying our brands. In addition, as we are principally based in the United States, a negative perception of the United States could impact the perception of our company, which could adversely affect our business prospects and growth.

14

If our transaction processing systems are disrupted or we are unable to process transactions efficiently or at all, our revenue or profitability would be materially reduced.

Our processing systems may experience service interruptions as a result of process or other technological malfunction, fire, natural or man-made disasters, power loss, disruptions in long distance or local telecommunications access, fraud, terrorism, accident or other catastrophic events, the probability or severity of which cannot be determined or predicted by the Company. A disaster or other problem at our primary and/or back-up facilities or our other owned or leased facilities could interrupt our services. Our visibility in the global payments industry may also attract terrorists, activists or hackers to attack our facilities or systems, leading to service interruptions, increased costs or data security compromises. Additionally, we rely on third-party service providers for the timely transmission of information across our global data transportation network. Inadequate infrastructure in lesser developed markets could also result in service disruptions, which could impact our ability to do business in those markets. If one of our service providers fails to provide the communications capacity or services we require, as a result of natural disaster, operational disruption, terrorism or any other reason, the failure could interrupt our services, adversely affect the perception of our brands’ reliability and materially reduce our revenue or profitability.

Account data breaches involving card data stored by third parties or us could adversely affect our reputation and revenue.

We, our channel partners, merchants, and other third parties store cardholder account and other information in connection with payment cards bearing our brands. In addition, our channel partners may sponsor third-party processors to process transactions generated by cards carrying our brands and merchants may use third parties to provide services related to card use. Although the Company uses what it believes to be industry standard, reasonable security precautions and protections, a breach of the systems on which sensitive cardholder data and account information are stored could lead to fraudulent activity involving cards carrying our brands, damage the reputation of our brands and lead to claims against us. In recent years, there have been several high-profile account data compromise events involving merchants and third party payment processors that process, store or transmit payment card data, which affected millions of MasterCard, Visa, Discover and American Express cardholders. As a result of such data security breaches, we may be subject to lawsuits involving payment cards carrying our brands. While most of these lawsuits do not involve direct claims against us, in certain circumstances, we could be exposed to damage claims, which, if upheld, could materially and adversely affect our profitability.

Any damage to our reputation or that of our brands resulting from an account data breach could decrease the use and acceptance of our cards, which in turn could have a material adverse impact on our transaction volumes, revenue and prospects for future growth, or increase our costs by leading to additional regulatory burdens being imposed upon us.

If we are not able to keep pace with the rapid technological developments in our industry to provide customers, merchants and cardholders with new and innovative payment programs and services, the use of our cards could decline, which could reduce our revenue and income or limit our future growth.

The payment card industry is subject to rapid and significant technological changes, including continuing developments of technologies in the areas of smart cards, radio frequency and proximity payment devices (such as contactless cards), electronic commerce and mobile commerce, among others. We cannot predict the effect of technological changes on our business. We rely in part on third parties, including some of our competitors and potential competitors, for the development of and access to new technologies. We expect that new services and technologies applicable to the payments industry will continue to emerge, and these new services and technologies may be superior to, or render obsolete, the technologies we currently use in our card programs and services. In addition, our ability to adopt new services and technologies that we develop may be inhibited by a need for industry-wide standards, by resistance from customers or merchants to such changes, by the complexity of our systems or by intellectual property rights of third parties. We have received, and we may in the future receive, notices or inquiries from other companies suggesting that we may be infringing a pre-existing patent or that we need to license use of their patents to avoid infringement. Such notices may, among other things, threaten litigation against us. Our future success will depend, in part, on our ability to develop or adapt to technological changes and evolving industry standards.

15

Changes to payment card networks or bank fees, rules, or practices could harm our business.

Spindle does not directly access payment card networks, such as Visa and MasterCard, which enable Spindle's acceptance of credit cards and debit cards (including some types of prepaid cards). As a result, Spindle must rely on banks or other payment processors to process transactions, and must pay fees for this service. From time to time, payment card networks have increased, and may increase in the future, the interchange fees and assessments that they charge for each transaction using one of their cards. Spindle's payment card processors have the right to pass any increases in interchange fees and assessments on to Spindle as well as increase such processor’s own fees for processing. Changes in interchange fees and assessments could increase Spindle's operating costs and reduce its profit margins. In addition, in some jurisdictions, governments have required Visa and MasterCard to reduce interchange fees, or have opened investigations as to whether Visa or MasterCard's interchange fees and practices violate antitrust law. In the United States, the financial reform law enacted in 2010 authorizes the Federal Reserve Board to regulate debit card interchange rates and debit card network exclusivity provisions, and in June 2011, the Federal Reserve Board issued a final rule capping debit card interchange fees at significantly lower rates than Visa or MasterCard previously charged. Any material reduction in credit or debit card interchange rates in the United States or other markets could jeopardize Spindle's competitive position against traditional credit and debit card processors. While the regulations adopted by the Federal Reserve Board in June 2011 do not treat Spindle as a “payment card network,” future changes to those regulations or to Spindle's business could potentially cause Spindle to be treated as a payment card network, which could subject Spindle to additional regulation and require Spindle to change its business practices, which could reduce Spindle's revenue and adversely affect Spindle's business. Contemporaneously, any changes to payment card networks or bank fees, rules, or practices could provide similar or equal harm to all or the majority payment industry participants.

Spindle is required by its processors to comply with payment card network operating rules, and Spindle has agreed to reimburse its processors for any fines they are assessed by payment card networks as a result of any rule violations by Spindle or Spindle's channel partners. The payment card networks set and interpret the card rules. Payment card networks could adopt new operating rules or re-interpret existing rules that Spindle or its processors might find difficult or even impossible to follow, or costly to implement. As a result, Spindle could lose its ability to give customers the option of using payment cards to fund their payments. If Spindle were unable to accept payment cards, its business would be seriously damaged.

Spindle is also required to comply with payment card networks' special operating rules for payment service provider and payment facilitators. Spindle and its payment card processors have implemented specific business processes for merchant customers in order to comply with these rules, but any failure to comply could result in fines, the amount of which would be within the payment card networks' discretion. Spindle also could be subject to fines from payment card networks if it fails to detect that merchants are engaging in activities that are illegal or that are considered “high risk,” primarily the sale of certain types of digital content. For “high risk” merchants, Spindle must either prevent such merchants from using Spindle or register such merchants with payment card networks and conduct additional monitoring with respect to such merchants.

System failures or slowdowns, security breaches and other problems could harm our reputation and business, cause us to lose our channel partners and revenue, and expose us to customer liability.

Our business is based upon our ability to securely, rapidly and reliably receive and transmit data through our systems. One or more of our platforms could slow down significantly or fail, or be breached, for a variety of reasons, including:

1.

failure of third party equipment, software or services utilized by us,

2.

undetected defects or errors in our software programs, especially when first integrated into production,

3.

unexpected problems encountered when integrating changes, enhancements or upgrades of third party equipment or software with our systems,

4.

computer viruses,

5.

In ability to secure Payment Card Industry (PCI) compliance certification at the required level to operate as a registered PSP/PF

6.

natural or man-made disasters disrupting power or telecommunications systems generally, and

7.

damage to, or failure of, our systems due to human error or intentional disruption such as physical or electronic break-in, sabotage, acts of vandalism and similar events.

16

We may not have sufficient redundant systems or backup telecommunications facilities to allow us to receive and transmit data in the event of significant system failures. Any significant security breach degradation or failure of one or more of the sub-systems on which we rely, including the networks of our vendors and customers could disrupt the operation of our network and cause our channel partners to suffer delays in transaction processing, which could damage our reputation, increase our service costs, or cause us to lose channel partners and revenues.

If we are exposed to, or threatened with, litigation relating to our intellectual property, we may suffer adverse consequences to our operations.

Our intellectual property may be exposed to, or threatened with, litigation by third parties alleging that products infringe their intellectual property rights. If one of these patents was found to cover a component of our operations or one of our patents was successfully challenged, we could be enjoined by a court, required to pay damages and be unable to commercialize or continue development of our products unless a license to the patent or other intellectual property right is obtained. A license may not be available to such patents on acceptable terms or at all. Furthermore, such litigation is costly and could impair our operations, require us to raise additional cash sooner than we originally anticipated and distract our management team from the operation of our business.

Risks Related to our Common Stock

Because we were a shell company prior to the acquisition of the assets of Spindle Mobile, holders of our Common Stock may be unable to sell their shares under Rule 144.

Our Common Stock is subject to risks arising from restrictions on reliance on Rule 144 by shell companies or former shell companies. The SEC defines a shell company as a company that has (a) no or nominal operations and (b) either (i) no or nominal assets, (ii) assets consisting solely of cash and cash equivalents; or (iii) assets consisting of any amount of cash and cash equivalents and nominal other assets. Under Rule 144, a person who has beneficially owned restricted securities of an issuer and who is not an affiliate of that issuer may sell them without registration under the Securities Act provided that certain conditions have been met. One of these conditions is that such person has held the restricted securities for a prescribed period, which can be 6 months or 1 year, depending on various factors. However, when the reporting company has previously been a shell company, as we were prior to the acquisition of assets from Spindle Mobile, Rule 144 is unavailable for the resale of securities until the following conditions have been met:

·

The issuer of the securities that was formerly a shell company has ceased to be a shell company; and

·

At least one year has elapsed from the time that the issuer filed current comprehensive disclosure with the SEC reflecting its status as an entity that is not a shell company, including audited financial statements ("Form 10 Information").

Since the Company has determined that the transactions contemplated by the Spindle Mobile Agreement should be accounted for as a reverse capitalization, requiring the filing of the audited financial statements of Spindle Mobile, the Company will not be deemed to have filed Form 10 Information until the audited financial statements of Spindle Mobile have been filed. As a result, stockholders who receive our restricted securities will not be able to sell them pursuant to Rule 144 without registration until at least one year following the date on which the Spindle Mobile audited financial statements have been filed with the SEC (the “One Year Anniversary Date”), and then only if and for so long as we have complied with our reporting requirements in the 12 months immediately prior to the One Year Anniversary Date. No assurance can be given that we will meet these requirements or that, if we have met them, we will continue to do so. Furthermore, we have no obligation to register any securities of the Company.

The Restatements have increased our costs and expenses and could materially adversely affect our business, financial condition, results of operations, and liquidity.

We have incurred substantial cost and expenses for legal and accounting services due to the Restatements, which could have an adverse impact on our business, results of operations, financial condition and liquidity.

17

We are subject to the “seasoning” requirements imposed by the NYSE Euronext and the NASDAQ Stock Market which will make us ineligible to list and trade on a national exchange until we have traded in the over-the-counter markets (or some other national or foreign regulated exchange) for at least one year following the filing with the SEC of all required information about the reverse capitalization with Spindle Mobile, including audited financial statements for the combined entity and filing our Form 10-K for the fiscal year ended December 31, 2014, unless we are able to complete a firm commitment underwritten public offering with gross proceeds of at least $40 million.

Because of our status as a former SEC-reporting shell company, we are subject to SEC rules which require companies that have completed a reverse merger to (1) trade in the over-the-counter markets (or some other national or foreign regulated exchange) for at least one year following the filing with the SEC of all required information about the reverse merger, including audited financial statements for the combined entity and (2) to timely file all required periodic reports with the SEC, including one annual report that includes audited financial statements for a full fiscal year commencing after filing the required information about the reverse merger, before seeking to “uplist” to a national securities exchange like NASDAQ or NYSE Euronext. This means we will not be eligible to apply for listing on such exchanges until we have traded on the over the counter market for at least one year after filing the audited statements of Spindle Mobile in connection with the restatement of our 2011 Annual Report. We may only bypass the requirements set forth above if we can complete a firm commitment underwritten public offering with gross proceeds of at least $40 million. As a result, our stockholders may find it more difficult to dispose of shares or obtain accurate quotations as to the market value of our common stock. In addition, we would be subject to an SEC rule that, in the event we failed to meet the criteria set forth in such rule, it would impose various practice requirements on broker-dealers who sell securities governed by the rule to persons other than established customers and accredited investors. Consequently, such rule may deter broker-dealers from recommending or selling our common stock, which may further affect its liquidity. This would also make it more difficult for us to raise additional working capital through subsequent financings. In the event we do seek the listing of our common stock on a national securities exchange such as NASDAQ or NYSE Euronext, we cannot assure you that we will be able to meet the initial listing standards of either of those or any other stock exchange, or that we will be able to maintain a listing of our common stock on either of those or any other stock exchange.

The price of our Common Stock may be depressed by sales of outstanding shares of free-trading securities held by the original stockholders of the Company.

A material portion of our issued and outstanding shares of Common Stock, were issued in a registered offering or are eligible for an exemption from registration in connection with a resale, and such shares are currently freely tradable. The Company does not have a current relationship with the holders of such shares, nor are such shares are subject to any contractual restrictions, which would limit trading. The sale of these shares could depress the price of the Company’s Common Stock and could result in the price per share falling below $1.00. In addition, if a substantial number of such shares are sold, such sales could saturate the market, making it difficult for holders of our Common Stock to liquidate their holdings once their shares are eligible for resale.

Our shares of Common Stock are subject to penny stock regulation.

The SEC has adopted rules that regulate broker/dealer practices in connection with transactions in penny stocks. Penny stocks generally are equity securities with a price of less than $5.00 (other than securities registered on certain national securities exchanges or quoted on the NASDAQ system, provided that current price and volume information with respect to transactions in such securities is provided by the exchange system). The penny stock rules require a broker/dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document prepared by the SEC that provides information about penny stocks and the nature and level of risks in the penny stock market. The broker/dealer also must provide the customer with bid and offer quotations for the penny stock, the compensation of the broker/dealer, and its salesperson in the transaction, and monthly account statements showing the market value of each penny stock held in the customer's account. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from such rules, the broker/dealer must make a special written determination that a penny stock is a suitable investment for the purchaser and receive the purchaser's written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in any secondary market for a stock that becomes subject to the penny stock rules, and accordingly, customers in Company securities may find it difficult to sell their securities, if at all.

18

We have not paid any cash dividends and do not intend to pay any cash dividends for the foreseeable future.

We have never declared or paid any cash dividends on our common stock. For the foreseeable future, we intend to reinvest any earnings in the development and expansion of our business, and do not anticipate paying any cash dividends on our common stock. Any future determination to pay dividends will be at the discretion of the Board of Directors and will be dependent upon then existing conditions, including our financial condition and results of operations, capital requirements, contractual restrictions, business prospects and other factors that the board of directors considers relevant. Therefore, there can be no assurance that any dividends on the common stock will ever be paid.

Future issuances of our preferred stock could dilute the voting and other rights of holders of our common stock.

Our Board of Directors has the authority to issue shares of preferred stock in any series and may establish, from time to time, various designations, powers, preferences and rights of the shares of each such series of preferred stock. Any issuances of preferred stock would have priority over the common stock with respect to dividend or liquidation rights. Any future issuance of preferred stock may have the effect of delaying, deferring or preventing a change in control of our Company and may adversely affect the voting and other rights of the holders of common stock.

As a result of the Restatements, there is a presumption that Company’s internal control over financial reporting as of December 31, 2011, as well as the quarters ended March 31, 2012, June 30, 2012 and September 30, 2012 were ineffective.