Registration No. 333-191839

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2 to

FORM S-4

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

REVETT MINERALS INC.

(Exact Name of Registrant as Specified in Its Charter)

| Canada* | 1040 | Not Applicable** |

| (State or Other Jurisdiction | (Primary Standard Industrial | (IRS Employer Identification |

| of Incorporation) | Classification Code Number) | Number) |

11115 East Montgomery Drive, Suite G

Spokane Valley, Washington 99206

(509) 921-2294

(Address, including zip code, and telephone number, including area

code, of Registrant’s principal executive offices)

John G. Shanahan

11115 East Montgomery Drive, Suite G

Spokane Valley, Washington 99206

(509) 921-2294

with a copy to:

Douglas J. Siddoway, Esq.

Randall | Danskin, P.S.

1500 Bank of America Financial Center

601 West Riverside Avenue

Spokane, Washington 99201-0653

(509) 747-2052

(Name, address, including zip code, and telephone number, including

area code, of agent for service)

Approximate date of commencement of proposed sale to the public:As soon as practicable after this Registration Statement becomes effective and the consummation of the domestication transaction covered hereby.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. [ ]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earliest effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer [ ] | Accelerated filer [X] |

| Non-accelerated filer [ ] | Smaller reporting company [ ] |

| (Do not check if a smaller reporting company) |

CALCULATION OF REGISTRATION FEE

| Proposed | Proposed | |||

| Title of each class of | Amount to be | maximum offering | maximum aggregate | Amount of |

| securities to be registered | registered | price per unit | offering price | registration fee |

| common stock | 34,596,387(1) | $0.61(2) | $21,103,796(2) | $2,879 |

(1) Represents shares of common stock of Revett Mining Company, Inc., a to-be-formed Delaware corporation, being registered in connection with the domestication of Revett Minerals Inc., a corporation organized under the federal laws of Canada. Assumes the proposed domestication is approved by the registrant’s shareholders and thereafter consummated.

(2) Estimated pursuant to Rule 457(c) solely for the purpose of calculating the registration fee based on the average of the high and low prices of the registrant’s common stock as reported on the New York Stock Exchange Market Division on October 18, 2013.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant files a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

____________________

*The registrant intends to change its jurisdiction of incorporation from the federal jurisdiction of Canada to the State of Delaware in the United States of America through a continuance under Section 188 of the Canada Business Corporations Act, or CBCA. The change in jurisdiction is sometimes referred to herein as the “domestication” and is subject to shareholder approval.

**The registrant intends to obtain an employer identification number at such time as the domestication is effected and the registrant is incorporated in the State of Delaware.

(ii)

The information contained herein is subject to completion or amendment. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This document shall not constitute an offer to sell or the solicitation of any offer to buy nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

PRELIMINARY – SUBJECT TO COMPLETION – DATED NOVEMBER __, 2013

REVETT MINERALS INC.

PROPOSED DOMESTICATION – YOUR VOTE IS VERY IMPORTANT

Dear Shareholders:

We are furnishing this management proxy circular to shareholders of Revett Minerals Inc. in connection with the solicitation of proxies by our management for use at a Special Meeting of our shareholders to be held on December__, 2013 at 10:00 a.m. (Spokane Valley, Washington time), at our executive offices, 11115 East Montgomery, Suite G, Spokane Valley, Washington.

The purpose of the Special Meeting is to obtain shareholder approval to change our jurisdiction of incorporation from the federal jurisdiction of Canada to the State of Delaware in the United States of America. We refer to this transaction as the “domestication” throughout this letter and the management proxy circular/prospectus that accompanies it.

We are pursuing the domestication for a number of reasons, the foremost being that we have no significant presence in Canada. Our corporate offices and operations are located in the United States and most of our shareholders reside there. The principal market for our common shares, the New York Stock Exchange Market Division, is also in the United States. In addition, domiciling in the United States will eventually enable us to eliminate one level of holding company ownership and streamline our corporate structure. We believe this will reduce our overall professional fees and could lead to better acceptance in the capital markets and greater shareholder value.

We chose the State of Delaware to be our domicile principally because the Delaware General Corporation Law, or DGCL, expressly accommodates a continuance authorized by Section 188 of the CBCA. We also chose the State of Delaware because of the substantial body of case law that has evolved over the years interpreting various provisions of the DGCL. We believe the domestication will not only unambiguously establish us as a U.S. corporation, it will help us achieve our strategic goals.

If we complete the domestication, we will continue our legal existence in Delaware as if we had originally been incorporated under Delaware law. In addition, each outstanding common share of Revett Minerals Inc. as a Canadian corporation will then represent one share of common stock of Revett Mining Company, Inc. as a Delaware corporation. Our common shares are currently traded on the New York Stock Exchange Market Division and the Toronto Stock Exchange under the symbol “RVM” and on the Frankfurt Stock Exchange under the symbol “37RN”. Upon the completion of our domestication, our common stock will continue to be listed on such exchanges under such symbols. Further, our management will be comprised of the same directors and executive officers who served in such capacities immediately prior to the domestication.

The record date for the determination of shareholders entitled to receive notice of, and to vote at the Special Meeting is November 1, 2013. At such date, 34,596,387 common shares were outstanding. The holders of at least two-thirds of our common shares present at the Special Meeting in person or by proxy (and assuming a quorum of our outstanding common shares are represented at the Special Meeting in person or by proxy) must vote to approve the domestication proposal. Dissenting shareholders have the right to be paid the fair value of their shares under Section 190 of the CBCA. If approved by our shareholders, the domestication is expected to become effective on December 31, 2013 or as soon as practicable after the Special Meeting. Our board of directors has reserved the right to terminate or abandon our domestication at any time prior to its effectiveness, notwithstanding shareholder approval, if it determines for any reason that the consummation of our domestication would be inadvisable or not in our best interests.

Your existing certificates representing your Revett Minerals Inc. common shares will represent the same number of shares of Revett Mining Company, Inc. common stock after the domestication without any action on your part. You will not have to exchange any share certificates. We will issue new certificates to you representing shares of common stock of Revett Mining Company, Inc. as a Delaware corporation upon a transfer of the shares by you or at your request.

The accompanying management proxy circular provides a detailed description of our proposed domestication and other information to assist you in considering the proposals on which you are asked to vote. We urge you to review this information carefully and, if you require assistance, to consult with your financial, tax or other professional advisers.

Our board of directors unanimously recommends that you vote FOR approval of our domestication.

Your vote is very important. Whether or not you plan to attend the Special Meeting, we ask that you indicate the manner in which you wish your shares to be voted and sign and return your proxy as promptly as possible in the enclosed envelope so that your vote may be recorded. If your shares are registered in your name, you may vote your shares in person if you attend the meeting, even if you send in your proxy.

We appreciate your continued interest in our company.

Very truly yours,

/s/ John G. Shanahan

President and Chief Executive Officer

2

These securities involve a high degree of risk. See “Risk Factors” beginning on page 34 of this proxy circular/prospectus for a discussion of specified matters that should be considered.

Neither the Securities and Exchange Commission nor any state securities commission or similar authority in Canada has approved or disapproved of these securities or determined if this proxy circular/prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This proxy circular/prospectus is dated November __, 2013 and is first being mailed to shareholders on or about November __, 2013.

____________________

REVETT MINERALS INC.

11115 East Montgomery Drive, Suite G

Spokane Valley, Washington 99206

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To our Shareholders:

NOTICE IS HEREBY GIVEN that a special meeting of shareholders (the “Special Meeting”) of REVETT MINERALS INC. (the “Corporation”) will be held on December __, 2013, at the hour of 10:00 a.m. (Spokane Valley, Washington time) at our executive offices, 11115 East Montgomery, Suite G, Spokane Valley, Washington for the following purposes:

1. to consider, and if deemed advisable, approve a special resolution authorizing the Corporation to make an application under Section 188 of the CBCA to change its jurisdiction of incorporation from the federal jurisdiction of Canada to the State of Delaware, United States of America, and to approve the certificate of incorporation authorized in the special resolution to be effective as of the date of the Corporation’s domestication (Proposal 1); and

2. to transact such other business as is proper at such meeting or any adjournment thereof.

A shareholder wishing to be represented by proxy at the Special Meeting or any postponement or adjournment thereof must deposit his or her duly executed form of proxy with the Corporation’s transfer agent and registrar, Computershare Investor Services Inc., 8th Floor, 100 University Avenue, Toronto, Ontario, M5J 2Y1, Attention: Proxy Department, or by facsimile to (416) 263-9524 or 1-866-249-7775 not later than 10:00 a.m. (Spokane Valley, Washington time) on December __, 2013 or, if the Special Meeting is adjourned, 48 hours (excluding Saturdays and holidays) before any postponement or adjournment of the Meeting. The time limit for the deposit of proxies may be waived by the chair of the Special Meeting at his discretion, without notice. A shareholder may also vote by telephone or via the Internet by following the instructions on the form of proxy. If a shareholder votes by telephone or via the Internet, completion or return of the proxy form is not needed.

The directors of the Corporation have fixed the close of business on November 1, 2013 as the record date for the determination of the shareholders of the Corporation entitled to receive notice of the Special Meeting and to vote at the Special Meeting. At such date, 34,596,387 common shares were outstanding. The holders of at least two-thirds of our common shares present at the Special Meeting in person or by proxy (and assuming a quorum of our outstanding common shares are represented at the Special Meeting in person or by proxy) must vote to approve the domestication proposal. No cumulative voting rights are authorized. A proxy circular/prospectus and form of proxy accompany this Notice.

DATED at Spokane Valley, Washington this ____ day of November, 2013.

/s/ Monique Hayes

Monique Hayes, Secretary

MANAGEMENT PROXY CIRCULAR

TABLE OF CONTENTS

REVETT MINERALS INC.

PROXY CIRCULAR/PROSPECTUS

(All dollar amounts expressed herein are U.S. dollars)

SUMMARY

This summary highlights selected information appearing elsewhere in this proxy circular/prospectus (the “Circular”) and does not contain all the information that you should consider in making a decision with respect to the proposals described herein. You should read this summary, together with the more detailed information, including our financial statements and the related notes appearing elsewhere in this Circular, and the exhibits attached hereto. You should carefully consider, among other things, the matters discussed in “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which are included in this Circular. You should read this Circular in its entirety.

Unless otherwise provided in this Circular, references to the “Corporation,” “Revett Minerals,” “we,” “us” and “our” refer to Revett Minerals Inc., a Canadian corporation, prior to the change of jurisdiction. References to “Revett Mining” and “Revett Mining Company, Inc.” refer to Revett Mining Company, Inc., a Delaware corporation, as of the effective time of the change in jurisdiction.

Revett Minerals Inc.

Revett Minerals was incorporated under the Canada Business Corporations Act (“CBCA”) in August 2004 to acquire Revett Silver Company, a Montana corporation, and undertake a public offering of its common shares in Canada, transactions that were completed in February 2005. Revett Silver Company was organized in April 1999 to acquire the Troy mine (“Troy”) and the Rock Creek project (“Rock Creek”) from ASARCO Incorporated and Kennecott Montana Company, transactions that were completed in October 1999 and February 2000, respectively.

Troy is an underground silver and copper mine. ASARCO operated the mine from 1981 to 1993, and then placed it on care and maintenance. We resumed mining operations in January 2005 and produced ore more or less continuously since then until December 2012, when we suspended mining operations due to unstable ground conditions in portions of the mine. We continued to assess these conditions until October 2013, when we concluded that we could not use an existing haulage route to resume operations but would instead have to construct a deeper decline to the C Bed and previously undeveloped I Bed deposits at Troy, a process that commenced in November 2013, following receipt of MSHA approval, and will take a minimum of twelve months to complete, at a cost of approximately $12 million. Rock Creek is a large development-stage underground silver and copper project.

Our principal executive office is located at 11115 East Montgomery, Suite G, Spokane Valley, Washington 99206, and our telephone number at that address is (509) 921-2294. Our registered office in Canada is located at 1 First Canadian Place, 100 King Street West, Suite 1600, Toronto, Ontario, Canada M5X 1G5.

Significant additional information about Revett Minerals is set forth in the section of this Circular entitled “Information Concerning the Corporation,” beginning at page 8.

Set forth below in a question and answer format is general information regarding the Special Meeting of Shareholders (the “Special Meeting”) to which this Circular relates. This general information regarding the Special Meeting is followed by a more detailed summary of the process relating to, reasons for and effects of our proposed change in jurisdiction of incorporation from Canada to Delaware in the United States (Proposal 1 in the Notice of Special Meeting), which we refer to in this Circular as the domestication.

1

Questions and Answers About the Domestication

Q. What is the purpose of the Special Meeting?

A. The purpose of the Special Meeting is to vote on the proposal to approve a special resolution authorizing us to make an application to change our jurisdiction of incorporation to Delaware and adopt a certificate of incorporation of Revett Mining Company, Inc. to be effective as of the date of our domestication, and to transact such other business as is proper at the Special Meeting.

Q. Where will the Special Meeting be held?

A. The Special Meeting will be held at our executive offices, 11115 East Montgomery, Suite G, Spokane Valley, Washington on December __, 2013, at the hour of 10:00 a.m. (Spokane Valley, Washington time).

Q. Who is soliciting my vote?

A. Our management is soliciting your proxy to vote at the Special Meeting. This Circular and form of proxy were first mailed to our shareholders on or about November __, 2013. Your vote is important. We encourage you to vote as soon as possible after carefully reviewing this Circular.

Q. Who is entitled to vote?

A. The record date for the determination of shareholders entitled to receive notice of the Special Meeting is November 1, 2013. In accordance with the provisions of the CBCA, we will prepare a list of our registered holders of common shares (the “common shareholders”) as of the record date. If you were a common shareholder as of the record date, you will be entitled to vote to approve the special resolution authorizing the change of jurisdiction and approval of the certificate of incorporation of Revett Mining Company, Inc. to be effective as of the date of our domestication (Proposal 1 in the Notice of Special Meeting) and any other matter that is properly submitted for shareholder vote at the Special Meeting.

Q. What am I voting on?

A. The common shareholders are entitled to vote on a special resolution authorizing us to make an application under Section 188 of the CBCA to change our jurisdiction of incorporation from the federal jurisdiction of Canada to the State of Delaware, United States of America, by way of a continuance under Section 188 of the CBCA and a domestication under Section 388 of the Delaware General Corporation Law (“DGCL”), and to approve the certificate of incorporation of Revett Mining Company, Inc. authorized in the special resolution to be effective as of the date of our domestication.

Q. What is the voting recommendation of the Board of Directors?

A. he board of directors recommends a vote FOR the special resolution authorizing us to make an application under Section 188 of the CBCA to change our jurisdiction of incorporation from the federal jurisdiction of Canada to the State of Delaware, United States of America, by way of a continuance, and to approve the certificate of incorporation of Revett Mining Company, Inc. authorized in the special resolution to be effective as of the date of our domestication.

2

Q. Will any other matters be voted on?

A. The board of directors does not intend to present any other matters at the Special Meeting. The board of directors does not know of any other matters that will be brought before our shareholders for a vote at the Special Meeting. If any other matter is properly brought before the Special Meeting, your signed proxy card gives authority to John G. Shanahan and, failing him, Timothy R. Lindsey, as proxies, with full power of substitution, to vote on such matters at their discretion.

Q. How many votes do I have?

A. Common shareholders are entitled to one vote for each Common Share held as of the close of business on the record date.

Q. What is the difference between holding shares as a shareholder of record and as a beneficial owner?

A. Many shareholders hold their shares through a stock broker or bank (“Intermediaries”) rather than directly in their own names. As summarized below, there are some distinctions between shares held of record and those owned beneficially.

Shareholder of Record – If your shares are registered directly in your name with our transfer agent, you are considered, with respect to those shares, the “shareholder of record,” and these Circular materials are being sent directly to you by us. You may vote the shares registered directly in your name by completing and mailing the proxy card or by voting in person at the Special Meeting.

Beneficial Owner – Non-registered holders who have not objected to their Intermediary disclosing certain ownership information about themselves to the Corporation are referred to as “NOBOs”. Those non-registered holders who have objected to their Intermediary disclosing ownership information about themselves to the Corporation are referred to as “OBOs”. The Corporation has elected to send the Notice, this Circular and the form of proxy (collectively, the “meeting materials”) directly to the NOBOs, to the extent possible, and indirectly through Intermediaries to the OBOs. The Intermediaries (or their service companies) are responsible for forwarding the meeting materials to each OBO, unless the OBO has waived the right to receive them. Intermediaries will frequently use service companies to forward the meeting materials to non-registered holders.

Q. How do I vote?

A. If you are a shareholder of record, there are two ways to vote: By completing and mailing your proxy card; or by voting in person at the Special Meeting. If you return your proxy card but you do not indicate your voting preferences, the proxies will vote your shares FOR Proposal 1 and on any other matter that is properly submitted for shareholder vote at the Special Meeting.

Generally, anon-registered holder who has not waived the right to receive meeting materials will either:

(i) be given a voting instruction form (“VIF”) which is not signed by the Intermediary, and which, when properly completed and signed by the non-registered holder and returned to the Intermediary or its service company, will constitute voting instructions which the Intermediary must follow; or

(ii) less frequently, be given a form of proxy which has already been signed by the Intermediary (typically by a facsimile, stamped signature), which is restricted as to the number of common shares beneficially owned by the non-registered holder and must be completed, but not signed, by the non-registered holder and deposited with the Corporation’s transfer agent, Computershare Investor Services Inc.

3

These meeting materials are being sent to both registered shareholders and non-registered holders. If you are a non-registered holder, and the Corporation or its agent has sent these meeting materials to you, your name and address and information about your holdings of securities have been obtained in accordance with applicable securities regulatory requirements from the Intermediary holding securities on your behalf. By choosing to send these meeting materials to you directly, the Corporation (and not the Intermediary holding securities on your behalf) has assumed responsibility for delivering these materials to you and executing your proper voting instructions. Please return your voting instructions as specified in the request for voting instruction.

VIFs, whether provided by the Corporation or by an Intermediary, should be completed and returned in accordance with the specific instructions noted on the VIF, including those regarding where and by when the VIF is to be delivered.The purpose of this procedure is to permit non-registered holders to direct the voting of the common shares that they beneficially own.

Should a non-registered holder who receives a VIF wish to attend the Special Meeting or have someone else attend on his or her behalf, the non-registered holder should follow the instructions set forth in the VIF.

Q. Can I change my vote or revoke my proxy?

A. A Common shareholder who has given a proxy has the power to revoke it by depositing an instrument in writing executed by the shareholder or by the shareholder’s attorney authorized in writing either at our registered office at any time up to and including the last business day preceding the day of the Special Meeting, or any adjournment thereof, or with the chairman of the Special Meeting on the day of the Special Meeting or any adjournment thereof, or in any other manner permitted by law. A common shareholder who has given a proxy may also revoke it by signing a form of proxy bearing a later date and depositing it by the time specified in the Notice or by delivering a written statement revoking the proxy. The written statement must be delivered to the Corporate Secretary of the Corporation at 11115 East Montgomery, Suite G, Spokane Valley, Washington, U.S.A. 99206 no later than 5:00 p.m. (Spokane Valley, Washington time) on the last business day prior to the date of the Special Meeting or any adjournment of the Special Meeting, or to the chairman of the Special Meeting on the day of the Special Meeting or any adjournment thereof.

Q. How are votes counted?

A. We will appoint a scrutineer at the Special Meeting, who will collect all proxies and ballots and tabulate the results. The scrutineer is typically a representative of our transfer agent.

Q. Who pays for soliciting proxies?

A. We will bear the cost of soliciting proxies from the shareholders. It is planned that the solicitation will be initially by mail, but proxies may also be solicited by our employees by telephone or email. These persons will receive no additional compensation for such services but will be reimbursed for reasonable out-of-pocket expenses. Arrangements will also be made with brokerage houses and other custodians, nominees and fiduciaries for the forwarding of solicitation materials to the beneficial owners of shares held of record by these persons, and we will reimburse them for their reasonable out-of-pocket expenses. The cost of such solicitation, estimated to be approximately $100,000, will be borne by us.

Q. What is the quorum requirement of the Special Meeting?

A. A quorum for the consideration of Proposal 1 shall be common shareholders present in person or by proxy representing not less than one-third of the total outstanding common shares.

4

Q. What are broker non-votes?

A. Broker non-votes occur when holders of record, such as banks and brokers holding shares on behalf of beneficial owners, do not receive voting instructions from the beneficial holders at least ten days before the Special Meeting. Broker non-votes will not affect the outcome of the matters being voted on at the Special Meeting, assuming that a quorum is obtained.

Q. What is the vote required to approve the domestication?

A. Our change of jurisdiction from Canada to Delaware requires the affirmative vote, in person or by proxy, of two-thirds of the votes cast by the common shareholders at the Special Meeting if a quorum, or one-third of the total outstanding common shares, is present.

Q. Multiple shareholders live in my household, and together we received only one copy of this Circular. How can I obtain my own separate copy of this document for the Special Meeting?

A. You may pick up copies in person at the Special Meeting or download them from our Internet web site,www.revettminerals.com(click on the link to the Investor Relations page). If you want copies mailed to you and are a beneficial owner, you must request them from your broker, bank or other nominee. If you want copies mailed to you and are a shareholder of record, we will mail them promptly if you request them from our corporate office by phone at (509) 921-2294 or by mail to 11115 East Montgomery Drive, Suite G, Spokane Valley, Washington 99206, Attention: Monique Hayes. We cannot guarantee you will receive mailed copies before the Special Meeting.

Q. Who can help answer my questions?

A. If you have questions about the Special Meeting you should contact Monique Hayes at (509) 921-2294 or by emailing her at hayes@revettminerals.com. You may also obtain additional information about us from documents filed with the SEC or with Canadian securities regulatory authorities by following the instructions in the section entitled “Where You Can Find More Information.”

5

The Domestication Proposal

Our board of directors is proposing to change our jurisdiction of incorporation from the federal jurisdiction of Canada to the State of Delaware through a transaction called a “continuance” under Section 188 of the CBCA and a “domestication” under Section 388 of the DGCL. Under the DGCL, a corporation becomes domesticated in Delaware by filing a certificate of corporate domestication and a certificate of incorporation with the Secretary of State of the State of Delaware. The domesticated corporation, which will be called Revett Mining Company, Inc., will become subject to the DGCL on the date of its domestication, but will be deemed for the purposes of the DGCL to have commenced its existence in Delaware on the date it originally commenced existence in Canada. The board of directors has unanimously approved the domestication, believes it to be in our best interests, and unanimously recommends approval.

Our board of directors has determined to pursue the domestication for a number of reasons, the foremost being that we have no significant presence in Canada. Our corporate offices and operations are located in the United States, most of our shareholders reside there, and the principal market for our common shares is the New York Stock Exchange Market Division. In addition, domiciling in the United States will eventually enable us to eliminate one level of holding company ownership (by merging our wholly-owned Revett Silver Company subsidiary with and into Revett Mining Company, Inc.) and streamline our corporate structure. We believe this will lead to greater acceptance in the capital markets, lower accounting and legal fees, and greater shareholder value. We chose the State of Delaware to be our domicile principally because the DGCL expressly accommodates continuances under the CBCA, and also because of the comprehensive body of case law interpreting the DGCL that has evolved over the years, including case law interpreting the duties and obligations of directors and officers. We believe the domestication will unambiguously establish us as a U.S. corporation and help us achieve our strategic goals.

The domestication will change the corporate laws that apply to our shareholders from the federal jurisdiction of Canada to the State of Delaware. There are material differences between the CBCA and the DGCL. Our shareholders may have more or fewer rights under Delaware law depending on the specific set of circumstances.

We plan to complete the proposed domestication as soon as possible following approval by our shareholders. The domestication will be effective on the date set forth in the certificate of corporate domestication and certificate of incorporation, as filed with the Secretary of State of the State of Delaware. Thereafter, Revett Mining Company, Inc. will be subject to the certificate of incorporation filed in Delaware. We will be discontinued in Canada as of the date shown on the certificate of discontinuance issued by the Director appointed under the CBCA, which is expected to be the same date as the date of the filing of the certificate of corporate domestication and certificate of incorporation in Delaware. However, the board of directors may decide to delay the domestication or not to proceed with the domestication after receiving approval from our shareholders if it determines that the domestication is no longer advisable. The Board of directors has not considered any alternative action if the domestication is not approved or if it decides to abandon the domestication.

The domestication will not interrupt our corporate existence, our operations, our outstanding agreements and obligations, or the trading market of our common shares. Each outstanding common share at the time of the domestication will remain issued and outstanding as a share of common stock of Revett Mining Company, Inc. after our corporate existence is continued from Canada under the CBCA and domesticated in Delaware under the DGCL. Following the completion of the domestication, Revett Mining Company, Inc.’s common stock will continue to be listed on the New York Stock Exchange Market Division and the Toronto Stock Exchange under the symbol “RVM” and will continue to be listed on the Frankfurt Stock Exchange under the symbol “37RN”.

Regulatory and Other Approvals

The continuance is subject to the authorization of the director appointed under the CBCA. The director is empowered to authorize the continuance if, among other things, he is satisfied that the continuance will not adversely affect our creditors or shareholders.

6

Tax Consequences of the Domestication

U.S. Federal Income Tax Consequences. We believe that the change in our jurisdiction of incorporation will constitute a tax-free reorganization within the meaning of Section 368(a) of the United States Internal Revenue Code and, generally, neither we nor Revett Mining Company, Inc. should recognize any gain or loss for U.S. federal income tax purposes as a result of the domestication, other than as described later herein in “United States Federal Income Tax Consequences.” If, for any reason, we determine that the domestication would not qualify as a tax-free reorganization, we will abandon the domestication.

For U.S. shareholders, the domestication also would generally be tax-free, however, Internal Revenue Code Section 367 has the effect of potentially imposing income tax on such holders in connection with such transactions. Pursuant to the Treasury Regulations under Internal Revenue Code Section 367, any U.S. holder that owns, directly or through attribution, 10% or more of the combined voting power of all classes of our stock (which we refer to as a 10% shareholder) will have to recognize a deemed dividend on the domestication equal to the “all earnings and profits amount,” within the meaning of Treasury Regulation Section 1.367(b) -2, attributable to such holder’s shares in the Corporation. Any U.S. shareholder that is not a 10% shareholder and whose shares have a fair market value of less than $50,000 on the date of the domestication, will recognize no gain or loss as a result of the domestication. A U.S. shareholder that is not a 10% shareholder but whose shares have a fair market value of at least $50,000 on the date of the domestication must generally recognize gain (but not loss) on the domestication equal to the difference between the fair market value of the Revett Mining Company, Inc. common stock received at the time of the domestication over the shareholder’s tax basis in our shares. Such a shareholder, however, instead of recognizing gain, may elect to include in income as a deemed dividend the “all earnings and profits amount” attributable to his shares in the Corporation which we refer to as a “Deemed Dividend Election.”

Based on all available information, we believe that no U.S. shareholder of the Corporation should have a positive “all earnings and profits amount” attributable to such shareholder’s shares in the Corporation, and that we are not a “passive foreign investment company” as that term is defined in the Internal Revenue Code of 1986, as amended, or the Code, and accordingly no U.S. shareholder should be subject to tax on the domestication. Our belief with respect to the “all earnings and profits amount” results from detailed calculations performed by a nationally recognized accounting firm based on information provided to them by us. Our earnings and profits for this purpose were calculated in conformity with the relevant provisions of the Code and the Treasury Proposed and Final Regulations in force as of the date of this Circular, the current administrative rulings and practices of the Internal Revenue Service, or the IRS and judicial decisions as they relate to those statutes and regulations.

Based on our limited activity at the holding company level and the size of our existing earnings and profits deficit, we do not believe that a U.S. shareholder should have a positive “all earnings and profits” amount attributable to such shareholder’s shares in the Corporation. As a result, we believe that no U.S. shareholder should be required to include any such amount in income as a result of the domestication. However , no assurance can be given that the IRS will agree with us. If it does not agree, then a U.S. shareholder may be subject to adverse U.S. federal income tax consequences. A U.S. shareholder’s tax basis in the shares of common stock of Revett Mining Company, Inc. received in the exchange will be equal to such shareholder’s tax basis in the shares of the Corporation, increased by the amount of gain (if any) recognized in connection with the domestication or the amount of the “all earnings and profits amount” included in income by such U.S. shareholder. A U.S. shareholder’s holding period in the shares of common stock of Revett Mining Company, Inc. should include the period of time during which such shareholder held his shares in the Corporation, provided that the shares of the Corporation were held as capital assets.

Canadian Federal Income Tax Consequences. Under the Income Tax Act (Canada), or Tax Act, the change in our jurisdiction from Canada to the United States will cause our tax year to end immediately before the domestication. Furthermore, we will be deemed to have disposed of all of our property immediately before the continuance for proceeds of disposition equal to the fair market value of the property at that time. We will be subject to a separate corporate emigration tax imposed equal to the amount by which the fair market value of all of our property (principally consisting of all of the outstanding shares of capital stock of our United States operating subsidiary, Revett Silver Company) immediately before the continuance exceeds the aggregate of our liabilities at that time (other than dividends payable and taxes payable in connection with the emigration tax) and the amount of paid-up capital on all of our outstanding common shares.

7

We have reviewed our assets, liabilities, paid-up capital and other tax balances with the assistance of our professional advisors. Based on our calculations, if the market price of our common shares does not exceed $2.25 per share and the exchange rate of the Canadian dollar to the U.S. dollar remains relatively constant at CDN $1.00 equals $0.97, then we should not incur any Canadian income taxation arising on the domestication. This conclusion is based in part on determinations of factual matters, including determinations regarding the fair market value of our assets and tax attributes, any or all of which could change prior to the effective time of the domestication. If the market price of our common shares exceeds such amount, however, or if the exchange rate of the Canadian dollar to the U.S. dollar appreciably changes, then we could incur Canadian income taxation as a result of the domestication.

Our shareholders who hold our common shares after the domestication will not be considered to have disposed of their shares by reason only of the domestication. Accordingly, the domestication will not cause Canadian resident shareholders to realize a capital gain or loss on their shares and there will be no effect on the adjusted cost base of their shares.

The foregoing is a brief summary of the principal income tax considerations only and is qualified in its entirety by the more detailed description of income tax considerations in “United States and Canadian Tax Considerations” in this Circular, which shareholders are urged to read. This summary does not discuss all aspects of United States and Canadian tax consequences that may apply in connection with the domestication. Shareholders should consult their own tax advisors as to the tax consequences of the domestication applicable to them. In addition, please note that other tax consequences may arise under applicable law in other countries.

Accounting Treatment of the Domestication

Our domestication as a Delaware corporation represents a transaction between entities under common control. Assets and liabilities transferred between entities under common control are accounted for at carrying value. Accordingly, the assets and liabilities of Revett Mining Company, Inc. will be reflected at their carrying value to us. Any of our shares that we acquire from dissenting shareholders will be treated as an acquisition of treasury stock at the amount paid for the shares.

Dissent Rights of Shareholders

If you wish to dissent and do so in compliance with Section 190 of the CBCA, and we proceed with the domestication, you will be entitled to be paid the fair value of the common shares you hold. Fair value is determined as of the close of business on the day before the domestication is approved by our common shareholders. If you wish to dissent, you must send written objection to the domestication to us at or before the Special Meeting. If you vote in favor of the domestication, you in effect lose your rights to dissent. If you withhold your vote or vote against the domestication, you preserve your dissent rights to the extent you comply with Section 190 of the CBCA.

However, it is not sufficient to vote against the domestication or to withhold your vote. You must also provide a separate dissent notice at or before the Special Meeting. If you grant a proxy and intend to dissent, the proxy must instruct the proxy holder to vote against the domestication in order to prevent the proxy holder from voting such shares in favor of the domestication and thereby voiding your right to dissent. Under the CBCA, you have no right of partial dissent. Accordingly, you may only dissent as to all your common shares. Section 190 of the CBCA is reprinted in its entirety as Exhibit E to this Circular.

Comparison of Shareholder Rights

Upon completion of the domestication, our shareholders will be holders of common stock of Revett Mining Company, Inc., a Delaware corporation, and their rights will be governed by the DGCL as well as Revett Mining Company, Inc.’s certificate of incorporation and bylaws. Shareholders should be aware that the rights they currently have under the CBCA may, with respect to certain matters, be different than the rights they will have as stockholders under the DGCL. For example, under the CBCA, a company has the authority to issue an unlimited number of shares whereas, under the DGCL, a Delaware corporation may only issue the number of shares that is authorized by its certificate of incorporation and stockholder approval must be obtained to amend the certificate of incorporation to authorize the issuance of additional shares. We refer you to the section entitled “The Domestication – Comparison of Shareholder Rights” for a more detailed description of the material differences between the rights of Canadian shareholders and Delaware stockholders.

8

INFORMATION CONCERNING THE CORPORATION

Narrative Description of Business.

Troy.Troy is an underground silver and copper mine located in Lincoln County, Montana, approximately fifteen miles south of the town of Troy. The mine comprises 24 patented lode-mining claims, 510 unpatented lode-mining claims, approximately 850 acres of fee land and 394 acres of patented claim land. The patented claims were legally surveyed in 1983. ASARCO operated the mine from 1981 to 1993, and then placed it on care and maintenance. We resumed mining operations in January 2005 and produced ore more or less continuously until December 2012, when we voluntarily suspended operations because of underground geotechnical conditions.

Ore from the mine is extracted using a “room and pillar” method and is processed on site using standard flotation technology. The resulting silver/copper concentrate is sold under contract to a third party and is shipped by rail from a load out facility located in Libby, Montana. The Troy concentrate typically contains between 35% and 40% copper, and between 80 to 120 ounces of silver per ton. During 2012, Troy produced 7.6 million pounds of copper and 1.1 million ounces of silver contained in concentrate. At December 31, 2012, the estimated proven and probable reserves at Troy were 11.0 million tons grading 1.01 ounces per ton silver and 0.39% copper using a net smelter return cut off of $29.99 per ton.

We operate Troy through Troy Mine, Inc., a wholly-owned Montana subsidiary of Revett Silver. Troy Mine, Inc. is also the record holder of the patented and unpatented mining claims and fee lands comprising the mine. In December 2012 we suspended mining operations at Troy because of concerns with underground geotechnical conditions. As previously noted, we concluded in October 2013 that we could not use an existing haulage route to resume operations but would instead have to construct a deeper decline to the C Bed and previously undeveloped I Bed deposits at Troy, a process that commenced in November 2013, following receipt of MSHA approval, and will take a minimum of twelve months to complete, at a cost of approximately $12 million.

Once mining has ceased and reclamation has taken place, we intend to transfer 394 acres of patented mining claims and approximately 750 acres of fee land at Troy to the Revett Foundation, an affiliated not-for profit corporation organized, among other things, to acquire title to these properties and see that they are administered and used as wildlife habitat, corridor linkage and other similar public purposes.

Rock Creek.Rock Creek is a development-stage silver and copper deposit located in Sanders County, Montana, approximately five miles northeast of Noxon, Montana and sixteen air miles southeast of Troy. The project comprises 99 patented lode-mining claims, 370 unpatented lode-mining claims, five tunnel site claims, 85 mill site claims and 754 acres of fee land. The patented claims lying within the Cabinet Mountain Wilderness Area convey mineral rights only; the claims lying outside the wilderness area convey both mineral and surface rights. The patented claims were legally surveyed in 1983 and occupy an area of approximately 1,809 acres.

We conduct our development activities at Rock Creek through RC Resources Inc., a wholly-owned Montana subsidiary of Revett Silver. RC Resources Inc. is also the record holder of the patented and unpatented mining claims comprising the project.

Our proposed development of Rock Creek will occur in several phases. The first phase is a two year evaluation program, estimated to cost between $25 million to $30 million, to define the economic and technical viability of the project. The evaluation program will include the development of an evaluation adit to collect additional technical information on the deposit, additional infill drilling to establish and confirm reserve and resource estimates, geotechnical design studies and bulk sampling of the mineralization for use in metallurgical testing. The evaluation program is subject to receipt of permits and approvals from the various federal and state agencies having jurisdiction over the project. The Corporation will also be required to satisfy grizzly bear mitigation and reclamation bonding requirements, design and construct a water treatment facility, and upgrade and improve the road leading to the proposed evaluation adit site.

9

The permitting process is complex. The Rock Creek deposit is partially located on United States Forest Service (the “Forest Service”) land (within the Kootenai National Forest) and under the Cabinet Mountains Wilderness Area, and federal and state approval is required to explore and develop it. In 2001, the Forest Service issued a final environmental impact statement (“final EIS”) under theNational Environmental Policy Act (“NEPA”). In 2003, the Forest Service and the Montana Department of Environmental Quality (the “DEQ”) issued a joint administrative decision approving our proposed plan of operations at Rock Creek(the “Record of Decision”). The Record of Decision was based primarily on the findings in the Final EIS and a companion biological opinion (the “Biological Opinion”) issued by the U.S. Fish and Wildlife Service (“USFWS”) in 2003 pursuant to the requirements of theEndangered Species Act (“ESA”). The project has been challenged by several regional and national conservation groups, culminating in a November 2011 decision by the Ninth Circuit Court of Appeals affirming a Montana federal district court decision that upheld the Biological Opinion against ESA challenges but remanded the final EIS to the Forest Service to address several NEPA procedural deficiencies. We are currently working with the Forest Service to develop a supplemental EIS to comply with the district court’s decision.

Other Properties. We also own two unpatented claim groups, the Vermillion River and the Sims Creek properties, which comprise approximately 1,660 acres and are located approximately 25 miles southeast of Rock Creek. Limited drilling was conducted by the previous owner of the Vermillion River claim group. The Sims group is untested. These claims are held by Revett Exploration, Inc., a wholly-owned Montana subsidiary of Revett Silver. In addition, we own approximately 673 acres of fee land at Rock Creek that will be used primarily for mitigation as the project is developed. This land and other proposed holdings that are not essential to our day to day mining operations are held by Revett Holdings, Inc., a wholly-owned Montana subsidiary of Revett Silver.

The Copper and Silver Markets.Copper and silver are internationally traded metals whose prices are determined by global economic conditions of supply and demand.

Historically, copper prices have been volatile. The following table sets forth the average annual prices of copper on the London Metal Exchange since 2008, as reported by the exchange. During this period, average annual copper prices have ranged from a low of $2.34 per pound in 2009 to a high of $4.00 per pound in 2011.

LME Average Cash Official Price (US$/Pound)

| 2012 | 2011 | 2010 | 2009 | 2008 |

| 3.61 | 4.00 | 3.42 | 2.34 | 3.15 |

We believe copper prices will remain favorable in the long term because of the continued lack of investment in exploration and mine development during the past decade. This has resulted in low to modest growth rates in supplies, compared to increasing consumption rates in the developed economies of North America and Europe, and rapid industrialization and emergence of consumer product markets in countries such as China and India.

Silver prices are also highly volatile. The following table illustrates the average annual London Bullion Market Association Silver Fix since 2008. These average annual prices have ranged from a low of $14.38 per ounce in 2009 to a high of $35.11 per ounce in 2011.

London Average Fix (US$/Ounce)

| 2012 | 2011 | 2010 | 2009 | 2008 |

| 31.15 | 35.11 | 20.16 | 14.38 | 15.03 |

10

We believe silver prices will remain generally favorable in the long term because of strong demand in the electronics industry and consistent demand from institutions that purchase and hold silver for investment purposes.

Financial Information about Segments.

Our operations comprise a single business segment, located in the United States. Information concerning our revenues, profits and losses, and total assets, liabilities and equity for the years ended December 31, 2012, 2011 and 2010 is included in the consolidated financial statements that appear elsewhere in this Circular.

Environmental Matters.

All mining companies doing business in the United States are subject to a variety of federal, state and local statutes, rules and regulations designed to protect the quality of the air and water, and threatened or endangered species in the vicinity of its mining operations. These include permitting or pre-operating approval requirements designed to ensure the environmental integrity of a proposed mining facility, operating requirements designed to mitigate the effects of discharges into the environment during mining operations, and reclamation or post-operation requirements designed to ensure water quality and to remediate the lands affected by mining activities once commercial operations have ceased. These laws are administered and enforced by various federal and state agencies operating under parallel statutes and regulations. The principal environmental laws affecting our current and proposed operations at Troy and Rock Creek are set forth below:

The Federal Clean Water Act and the Montana Water Quality Act. The federal Clean Water Act and the Montana Water Quality Act are the principal water quality laws regulating our operations at Troy and Rock Creek. The federal act imposes limitations on water discharges into waters of the United States, including discharges from point sources such as mine facilities, and is administered by the US Environmental Protection Agency. The Montana act imposes similar limitations on discharges into state waters and is administered by the DEQ.

The Endangered Species Actrequires federal agencies to ensure that any action authorized, funded or carried out by such agency is not likely to jeopardize the continued existence of any endangered or threatened species. ESA’s definition of “species” includes any distinct population segment of any vertebrate fish or wildlife that interbreeds when mature. In order to facilitate the conservation of listed species, ESA establishes an interagency consultation process. When a federal agency proposes an action that “may affect” a listed species, which in the case of Rock Creek includes grizzly bears and bull trout, the Forest Service must provide a “biological assessment” of the effects of the proposed action. Unless the USFWS determines that the proposed action will have no adverse effect on listed species, it must review all of the information provided by the action agency, as well as any other relevant information, and prepare a “biological opinion” setting forth the effects of the proposed action. In preparing such an opinion, the USFWS must use the best available scientific and economic data to determine whether the proposed action is likely to jeopardize the species, the amount and extent of any incidental “taking” or harm to the species that may result from the action, and whether it should identify any conservation measures to promote the recovery of the listed species. ESA also provides that, once the interagency consultation process has been initiated, neither the federal agency nor the permit or license applicant (in this case, the Corporation) may make any irreversible commitment of resources with respect to the proposed agency action that would have the effect of foreclosing the formulation or implementation of any reasonable or prudent measures to avoid jeopardizing the listed species.

As previously noted, the USFWS issued a Biological Opinion in May 2003, which concluded that the proposed development of Rock Creek would not jeopardize the continued existence of grizzly bears or bull trout. The opinion was subsequently challenged by several conservation organizations on ESA grounds in a lawsuit brought in federal district court in Montana and was later remanded to the USFWS for further study. In October 2006 the USFWS issued a revised Biological Opinion reaffirming its earlier decision. The revised opinion was also challenged in federal district court. In May 2010, the district court issued a decision dismissing the groups’ ESA challenge. The conservation groups appealed that dismissal to the Ninth Circuit Court of Appeals, which issued an opinion in November 2011 affirming the district court’s decision and upholding the USFWS’s determination that the mine would entail “no adverse modification” to bull trout critical habitat and would result in “no jeopardy” to grizzly bears.

11

The Wilderness Act of 1964 created a National Wilderness Preservation System composed of federally owned areas designated by Congress as “wilderness areas.” Wilderness is generally defined in the Act as “an area where the earth and its community of life are untrammelled by man, where man himself is a visitor who does not remain.” Once included in the system, the Act requires that these areas be administered by the federal department or agency having prior jurisdiction in the system in such a manner as to preserve their wilderness character and leave them unimpaired for future use and enjoyment as wilderness. The Cabinet Mountains Wilderness Area overlays Rock Creek and was included in the National Wilderness Preservation System in 1964. TheWilderness Act does not affect mineral leasing activities conducted prior to 1983, however it does authorize the Secretary of Agriculture (through the Forest Service) to impose such reasonable stipulations as are necessary to protect the wilderness character of the land for the purposes for which they are leased, permitted or licensed. In the case of Rock Creek, these stipulations have been the focus of public opposition to the development of the project.

The Clean Air Actlimits the ambient air discharge of certain materials deemed to be hazardous and establishes a federal air quality permitting program for such discharges.

The Montana Air Quality Act imposes limitations and permitting requirements similar to those of the Clean Air Act. Hazardous materials are defined in both acts and in their enabling regulations to include various metals. We holds all of the required air quality permits pertaining to its operations at Troy.

The National Environmental Policy Act and the Montana Environmental Policy Act requires all governmental agencies to consider the impact of major federal actions on the human environment. The state act mandates similar considerations with respect to major state actions. Because Rock Creek is located on federal lands, we were required to prepare and file an EIS outlining the environmental effects of its proposed operations and our plans to limit the effects of Rock Creek’s operations. The final EIS for Rock Creek was issued in 2001, and the Forest Service, the lead government agency on the project, released its Record of Decision on the Corporation’s proposed operating plan in June 2003. The Corporation is working with the Forest Service to develop a supplemental EIS as required by the district court’s May 4, 2010 decision.

The Federal Comprehensive Environmental Response, Compensation and Liability Act and the Montana Metal Mine Reclamation Act (“CERCLA”) imposes clean-up and reclamation obligations stemming from unlawful discharges into the environment, and establishes significant criminal and civil penalties against those persons who are primarily responsible for such discharges.

The Montana Metal Mine Reclamation Act (“MMRA”) is similar to CERCLA in principle, but focuses principally on the cleanup and reclamation of mining properties and unlawful discharges from mining operations. CERCLA is jointly administered and enforced by the Environmental Protection Agency and the DEQ. MMRA is administered and enforced by the DEQ.

The Multiple-Use Sustained Yield Act of 1960(“MUSYA”) andThe National Forest Management Act of 1974directs the Secretary of the U.S. Department of Agriculture to administer Forest Service and other federal lands in ways that promote multiple uses of these resources (such as outdoor recreation, grazing, timber harvesting and mining) and are protective of watersheds, fish and wildlife, and to implement regulations that are consistent with MUSYA’s objectives.

The Resource Conservation and Recovery Act was designed and implemented to regulate the disposal of hazardous wastes. It mandates that such wastes be treated, disposed of or stored, and requires those doing so to obtain permits from the Environmental Protection Agency or the authorized state regulatory authority.

Employees.

We had 63 full-time employees and no part-time employees at November 21, 2013. Fifty-six of these employees work at Troy in production and management capacities, and the remaining seven employees work in management and administrative capacities at our corporate office. None of our employees are represented by a collective bargaining unit.

12

Properties.

We acquired our interests in Troy and Rock Creek in February 2005 through our acquisition of Revett Silver. Revett Silver, in turn, acquired Troy and Rock Creek from ASARCO and Kennecott in October 1999 and February 2000. Revett Silver holds Troy through its wholly-owned subsidiary Troy Mine Inc., and it holds Rock Creek through its wholly-owned subsidiary RC Resources Inc. Both properties are located in northwestern Montana. In 2012, we formed two additional subsidiaries of Revett Silver, Revett Exploration Inc., which holds the Sims Creek and Vermillion River mineral claims located in Montana and Revett Holdings Inc., which holds the mitigation lands located in Montana formerly owned by RC Resources Inc.

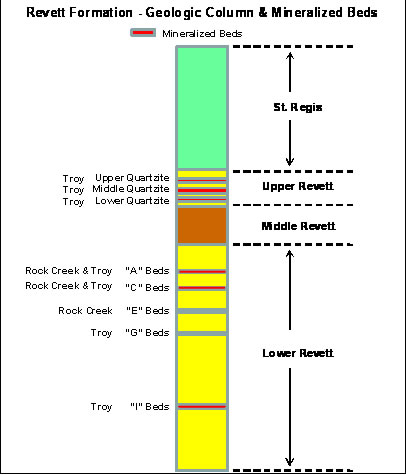

Geology. The geology of the region is characterized by a thick sedimentary sequence, Proterozoic in age, containing four major conformable groups: the Lower Belt, Ravalli, Middle Belt Carbonate and Missoula Groups. The Troy and Rock Creek deposits are found within the Ravalli Group, specifically in the Revett Formation. This Formation represents a mature, clastic, metamorphosed sandstone sequence of varying thicknesses with the sulfide mineralization being stratabound and disseminated; minor secondary enriched mineralization also occurs as fracture-fillings. Varying degrees of copper and silver mineralization occurs within favorable beds throughout the Revett Formation (in excess of 2,000 feet thick) as depicted in the following diagram.

Base and precious metals mineralization is associated with sulfide dissemination within selected portions of the Precambrian Belt Supergroup, and more specifically within the Revett Formation. This type of mineralization, referred to as stratabound disseminated copper deposits, results from the migration of metal-bearing solutions through unconsolidated porous sediments prior to or during diagenesis. Considerable research has been undertaken to understand the genesis of these deposits and determine the fundamental controls on ore distribution. All of the deposits are similar and appear to exhibit lateral metal and mineral zoning which were interpreted to derive from primary ore-forming processes.

13

Copper is found in the sulfide minerals bornite and chalcocite, and most often occurs as fine-grained disseminations with concentrations of less than six percent of the total sulfide along fractures, veinlets and bedding planes. The main copper sulfide zones are the chalcocite-chlorite and the bornite-calcite zones. Significant amounts of silver are found in these zones within the copper sulfides and as enriched native silver. The thickness of these zones and their copper and silver grades are generally quite continuous across large areas, while locally there are segments that are thinner or of lower grade. Enveloping the chalcocite-chlorite and bornite-calcite zones are four additional concentric mineral zones that generally have no economic value. The chalcopyrite-ankerite zone is on the proximal side of the ore zones. The other three mineral zones are chalcopyrite-calcite, galena-calcite and pyrite-calcite which are sequentially located on the distal side of the ore zones.

Physiography, Climate and Infrastructure.The Cabinet Mountains are a rugged, northwest-trending mountain range. Maximum relief in the area ranges from 2,200 feet in the valleys to 7,700 feet at the peaks. The area’s topography is controlled by the underlying rock types and structural features. The talus slopes and hogback ridges of the area are typically formed by the more erosion resistant quartzite and limestone rocks.

The major land-forming features were created by the Rocky Mountain uplift that was active approximately 60 million years ago, and were subsequently modified by shifts in the earth’s crust, alpine glaciation and alluvial deposits. Topography in the area of the projects has been influenced by Pleistocene-age glaciation. In the northern part of the project area, Pleistocene alpine glaciers carved the landscape into a series of cirques, and horns characterized by nearly vertical cliffs, ledges, steep colluvial slopes and talus fields. Pleistocene-age glaciation scoured some lower elevation areas and created a veneer of glacial deposits. Glacial lake bed deposit, silt and clay accumulations approximately 1,000 feet in thickness were deposited in the low-elevation drainages.

The climate of the area is characterized by a combination of Pacific maritime and continental climates. The maritime influences are strongest in the winter when relatively warm, moist air from the Pacific Ocean is cooled as it is lifted over the mountains and mixes with colder Arctic air moving south. This results in snowfall with significant accumulations in the higher elevations. Continental influences are more prevalent in the summer with thundershowers during May and June followed by hot, dry weather into mid-September. Annual precipitation totals vary from about 30 inches along the Clark Fork River valley to about 80 inches at the highest elevations in the Cabinet Mountains. Temperatures in the area are moderate. During the summer months, minimum night-time temperatures are in the 50 to 60 degrees Fahrenheit range. Winter cold waves occur, but mild weather is more common. The long-term annual average temperature is about 45 degrees Fahrenheit. The warmest month, July, averages 65 degrees Fahrenheit and the coldest month, January, averages 24 degrees Fahrenheit.

Troy is located in Lincoln County, Montana which is sparsely inhabited with several rural communities. Libby, the county seat, is located approximately 32 miles northeast of the mine. The mine site is accessed by a seven mile paved mine road which connects to Montana Highway 56, a paved all-weather road connecting Montana Highway 200 to U.S. Highway 2. The copper-silver concentrates from Troy are trucked to a leased load out facility and rail siding in Libby for rail shipment to a port as designated by our concentrate purchaser. The mine is connected to the local power grid managed by a local electric cooperative.

Rock Creek is located in Sanders County, Montana, approximately five miles northeast of the town of Noxon. Thompson Falls, the county seat, is located approximately 37 miles southeast of Noxon along Montana Highway 200. An active railway line parallels Highway 200 and would connect directly to a copper-silver concentrate load out facility at the project site. Electrical service is available throughout the area including a high voltage power line which passes through the project area. Rock Creek is ideally situated from an infrastructure standpoint as all major services (power, highway, rail and water) are available within four miles of the planned project site.

The Vermillion River and the Sims Creek properties consist of two unpatented claim groups located approximately 25 miles southeast of Rock Creek.

The local economy is based primarily on agriculture and tourism and, to a lesser extent, logging and the production of wood products. Unemployment in Lincoln and Sanders Counties is high relative to state and national unemployment rates.

14

Development History. Troy and Rock Creek have long histories dating back to 1963 when the Bear Creek Mining Company, a subsidiary of Kennecott Copper Corp., now a subsidiary of Rio Tinto PLC, discovered stratabound copper and silver mineralization in the Cabinet Mountains of northwestern Montana. Over the next two decades, extensive exploration activity delineated both the Troy and Rock Creek deposits. The Troy and Rock Creek deposits share many similarities in geology, geochemistry, and physiology.

In 1973, ASARCO leased the Troy project from Kennecott and began permitting and development of the Troy mine. Production commenced in August 1981 and continued until April 1993, when operations were placed on care and maintenance due mainly to low metal prices. During the twelve year period of production, the mine produced approximately 4.0 million ounces of silver and 34 million pounds of copper per year.

ASARCO also acquired the Rock Creek claims from Kennecott in 1973 and commenced an exploration program comprising 121 boreholes. According to a final exploration report prepared by ASARCO in 1989, the Rock Creek deposit contained a mineral resource estimated at 143.76 million tons grading an average of 0.68% copper and 1.65 ounces of silver per ton using a polygonal method.

In 1982 and 1983, U.S. Borax and Chemical Corporation, also now a subsidiary of Rio Tinto PLC, explored the lateral extensions of Rock Creek deposit on adjacent claims. In 1984 U.S. Borax estimated the mineral inventory of 48 million tons grading 0.54% Cu and 1.66 opt Ag in three satellite zones, referred to as the “Adjacent Properties,” using a polygonal methodology. This mineral inventory and methodology has not been audited. Revett Silver acquired the Adjacent Properties in 2000 as part of the Kennecott transaction.

Revett Silver subsequently acquired the mineral rights to two other exploration stage stratabound copper/silver prospects located south of, and on trend with Rock Creek, these being the Vermilion River and Sims Creek projects.

In 2010, Troy Mine Inc. acquired a total 152 unpatented claims from Kennecott located east and north of Troy. These claims expand the Corporation’s holdings by approximately 3,000 acres and provide important new ground for exploration that potentially could extend the mine life of Troy.

In 2011 RC Resources Inc. acquired 8 unpatented claims (the JE claims) and staked an additional 200 unpatented claims (the Lost Girl claims) northwest of Rock Creek expanding the property position at Rock Creek by approximately 4,000 acres.

Troy.Troy is an underground “room and pillar” silver and copper mine with a conventional flotation mill located in Lincoln County, Montana. ASARCO developed the mine in 1980 and 1981, at a cost of approximately $100 million. Troy comprises 24 patented lode-mining claims and approximately 511 unpatented lode-mining claims. We re-opened Troy in December 2004 at a cost of approximately $8 million and have operated it since then. Copper concentrate high in silver content is shipped by rail from a load out facility in Libby, Montana under a renewable long term contract. The Troy concentrates typically contain 35% to 40% copper and 80 to 120 troy ounces of silver per ton. The Troy concentrates are considered high grade and clean with no deleterious elements.

The Troy Deposit. Economically significant mineralization occurs at Troy within a number of distinct stratigraphically adjacent quartzite sub-units. The Upper, Middle and Lower Quartzites are located within the Upper Member of the Revett Formation and the “A”, “C” and “I” Beds are contained in the Lower Member of the Revett Formation. In plan view, the stratiform deposit measures approximately 7,500 feet by 1,800 feet. In the vicinity of the mine, the stratigraphy is generally flat with a shallow dip of four degrees (7% grade). There are two styles of faults in the mine area. Northwest trending faults are brittle-ductile structures with common clay gouge as exemplified by the East Fault. The East Fault displays a close spatial relationship with the copper-silver mineralization. The second type of faults are late brittle and generally open faults with sandy infill, as typified by the Cross Fault which separates the north and south ore bodies. These faults trend east northeast to east southeast and have steep southerly dips. These faults are late structures offsetting the mineralized sedimentary units. The Cross Fault also offsets the East Fault.

15

The Troy deposit has been subdivided into three separate mining areas; the North Ore Body (“NOB”), South Ore Body (“SOB”) and the East Ore Body (“EOB”), delineated primarily by the Cross Fault and the East Fault dissecting the mineralized quartzite sub-units (see following diagram). The main mining quartzite sub-unit has been the middle quartzite which averages approximately sixty feet thick. The NOB and SOB are mined in both the Lower and Middle Quartzite while the Middle and Upper Quartzite sub-units are mined in the EOB. No economic copper and silver mineralization was delineated in the Upper Quartzite west of the East Fault and similarly in the Lower Quartzite east of the East Fault (which represents the eastern boundary of the NOB and SOB). The South fault delineates the southern margin of the SOB. All other lateral ore boundaries are assay delimited and do not represent hard geological boundaries. Both the A and C Beds are mined in the South Ore Body.

The Corporation conducted exploration drilling between 2006 and 2012 that delineated additional mineralization and new ore bodies in the “C Beds” and the “A” and “I” Beds of the South Ore Body. These deposits comprise a portion of Troy’s probable reserves.

Troy Reserve Estimates (December 31, 2012)

| Ag | ||||||

| Grade | Cu Grade | Contained | Contained | |||

| Category | Area | Million Tons | (Opt) | (%) | Ag (Moz) | Cu (Mlbs) |

| Proven Reserves | North Ore Body | 1.38 | 1.42 | 0.70 | 1.95 | 19.30 |

| South Ore Body | 0.60 | 1.55 | 0.81 | 0.94 | 9.72 | |

| East Ore Body | 0.08 | 1.26 | 0.63 | 0.09 | 0.95 | |

| Lower Revett - A Bed | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| Lower Revett - C Bed | 0.09 | 1.54 | 0.66 | 0.14 | 1.19 | |

| Lower Revett - I Bed | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| Total | Proven Reserves | 2.14 | 1.46 | 0.73 | 3.12 | 31.17 |

| Probable Reserves | North Ore Body | 0.36 | 0.62 | 0.33 | 0.23 | 2.36 |

| South Ore Body | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| East Ore Body | 0.90 | 1.39 | 0.60 | 1.25 | 10.89 | |

| Lower Revett - A Bed | 0.60 | 0.88 | 0.26 | 0.53 | 3.13 | |

| Lower Revett - C Bed | 0.39 | 0.95 | 0.31 | 0.37 | 2.43 | |

| Lower Revett - I Bed | 6.66 | 0.85 | 0.28 | 5.64 | 36.96 | |

| Total | Probable Reserves | 8.93 | 0.90 | 0.31 | 8.02 | 55.77 |

| Proven & Probable | North Ore Body | 1.74 | 1.25 | 0.62 | 2.18 | 21.67 |

| South Ore Body | 0.60 | 1.55 | 0.81 | 0.94 | 9.72 | |

| East Ore Body | 0.98 | 1.38 | 0.61 | 1.35 | 11.84 | |

| Lower Revett - A Bed | 0.60 | 0.88 | 0.26 | 0.53 | 3.13 | |

| Lower Revett - C Bed | 0.48 | 1.06 | 0.37 | 0.51 | 3.62 | |

| Lower Revett - I Bed | 6.66 | 0.85 | 0.28 | 5.64 | 36.96 | |

| Total | Proven & Probable Reserves | 11.07 | 1.01 | 0.39 | 11.14 | 86.94 |

The following key factors were used in determining the foregoing reserves:

| Key Factors / Parameters | Silver | Copper | Other/Total |

| Metal Prices (prior 3 year averages) | $28.83 | $3.67 | |

| NSR Cutoff (Incl. Royalty) | $29.99 / Ton | ||

| Mining Recovery | 100% | ||

| Dilution (Incl. Reserve Calc.) | 0% | ||

| Metallurgical Recoveries – LOM Avg. | 85.86% | 84.18% |

16

Troy Resources Estimate (December 31, 2012)

| Category | Area | Million Tons | Ag Grade (Opt) | Cu Grade (%) |

| Measured Resource | North Ore Body | 27.76 | 1.32 | 0.66 |

| South Ore Body | 17.65 | 1.40 | 0.69 | |

| East Ore Body | 3.15 | 1.13 | 0.52 | |

| Lower Revett - A Bed | 0.78 | 0.84 | 0.27 | |

| Lower Revett - C Bed | 1.36 | 1.41 | 0.60 | |

| Lower Revett - I Bed | 0.00 | 0.00 | 0.00 | |

| Total Measured Resource | Total | 50.69 | 1.33 | 0.65 |

| Indicated Resource | North Ore Body | 0.54 | 0.62 | 0.33 |

| South Ore Body | 2.62 | 0.96 | 0.27 | |

| East Ore Body | 2.73 | 1.34 | 0.61 | |

| Lower Revett - A Bed | 0.39 | 0.84 | 0.27 | |

| Lower Revett - C Bed | 0.59 | 0.95 | 0.31 | |

| Lower Revett - I Bed | 10.00 | 0.85 | 0.28 | |

| Total Indicated Resource | Total | 16.88 | 0.94 | 0.33 |

| Measured & Indicated | North Ore Body | 28.30 | 1.31 | 0.65 |

| South Ore Body | 20.28 | 1.35 | 0.63 | |

| East Ore Body | 5.88 | 1.23 | 0.56 | |

| Lower Revett - A Bed | 1.17 | 0.84 | 0.27 | |

| Lower Revett - C Bed | 1.95 | 1.27 | 0.51 | |

| Lower Revett - I Bed | 11.50 | 0.83 | 0.28 | |

| Total Measured & Indicated | Total | 69.07 | 1.24 | 0.57 |

| Total Inferred (Troy Property) | Lower Revett – I Bed | 1.50 | 0.71 | 0.30 |

| (Pillars Incl. in Meas. & Ind.) | Total | (49.31) | (1.33) | (0.65) |

| Total Inferred (JF Property)1 | Total | 11.00 | 1.40 | 0.40 |