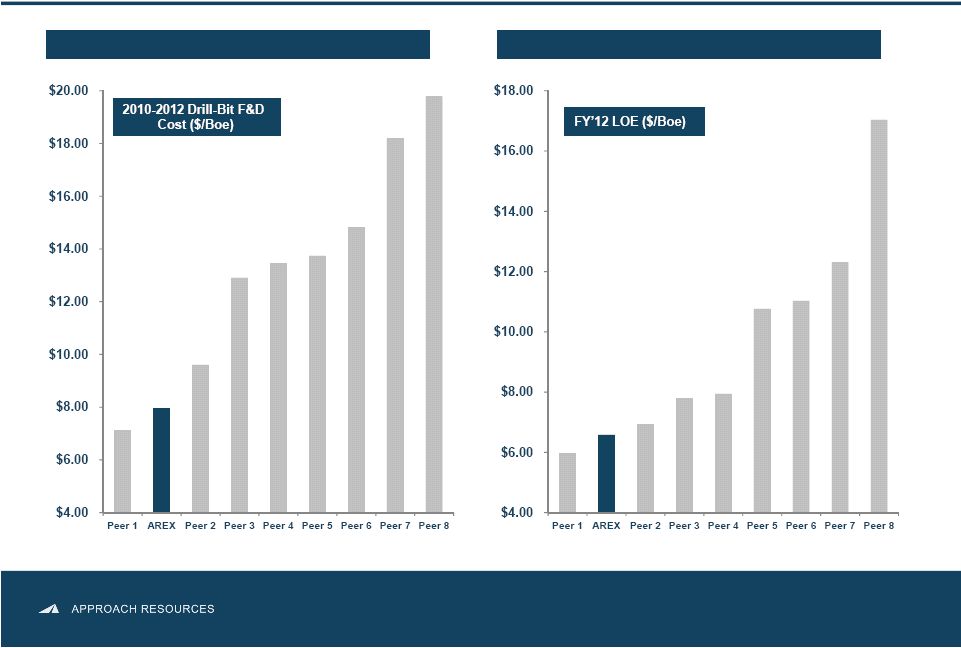

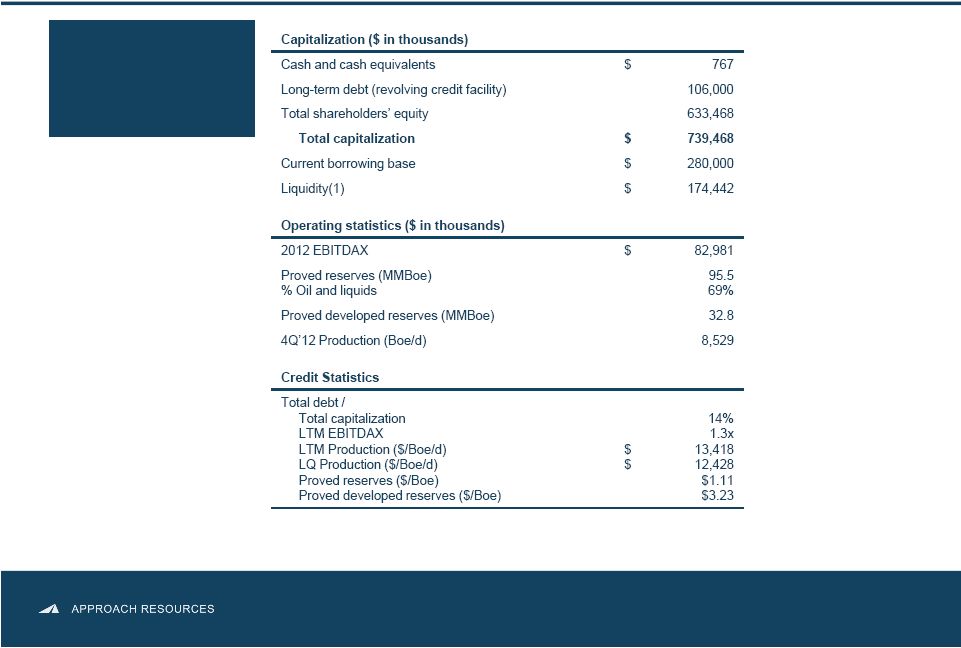

F&D Costs Reconciliation (unaudited) 28 We believe that providing measures of finding and development, or F&D, cost is useful to assist an evaluation of how much it costs the Company, on a per Boe basis, to add proved reserves. However, these measures are provided in addition to, and not as an alternative for, and should be read in conjunction with, the information contained in our financial statements prepared in accordance with GAAP (including the notes), included in our SEC filings and posted on our website. Due to various factors, including timing differences, F&D costs do not necessarily reflect precisely the costs associated with particular reserves. For example, exploration costs may be recorded in periods before the periods in which related increases in reserves are recorded and development costs may be recorded in periods after the periods in which related increases in reserves are recorded. In addition, changes in commodity prices can affect the magnitude of recorded increases (or decreases) in reserves independent of the related costs of such increases. As a result of the above factors and various factors that could materially affect the timing and amounts of future increases in reserves and the timing and amounts of future costs, including factors disclosed in our filings with the SEC, we cannot assure you that the Company’s future F&D costs will not differ materially from those set forth above. Further, the methods we use to calculate F&D costs may differ significantly from methods used by other companies to compute similar measures. As a result, our F&D costs may not be comparable to similar measures provided by other companies. The following tables reflect the reconciliation of our estimated finding and development costs to the information required by paragraphs 11 and 21 of ASC 932-235. 2012 Reserve summary (MBoe) Balance – 12/31/2011 76,975 Extensions & discoveries 38,861 Revisions (17,469) Production (2,888) Balance – 12/31/2012 95,479 Cost summary ($M) Acquisition costs $ 7,742 Exploration costs 4,550 Development costs 285,039 Total 297,331 Finding & development costs ($/Boe) All-in F&D costs $ 13.90 Drill-bit F&D cost $ 7.45 Reserve replacement ratio (%) Extensions & discoveries (MBoe) 38,861 2012 Production (MBoe) (2,888) Reserve replacement 1,346% 3-Year Reserve summary (MBoe) Balance – 12/31/2009 36,488 Extensions & discoveries 68,182 Purchases 12,456 Revisions (14,866) Production (6,781) Balance – 12/31/2012 95,479 Cost summary ($M) Acquisition costs $ 131,189 Exploration costs 17,415 Development costs 524,476 Total 673,080 Finding & development costs ($/Boe) 3-YR All-in F&D costs $ 10.23 3-YR Drill-bit F&D cost $ 7.95 Reserve replacement ratio (%) Extensions & discoveries (MBoe) 68,182 3-YR Production (MBoe) (6,781) Reserve replacement 1,005% |