Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on February 29, 2016

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

FORM 20-F

o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | ||

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

for the fiscal year ended December 31, 2015 | ||

OR | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | ||

o | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission file number 001-33632

BROOKFIELD INFRASTRUCTURE PARTNERS L.P.

(Exact name of Registrant as specified in its charter)

Bermuda

(Jurisdiction of incorporation or organization)

73 Front Street

Hamilton, HM 12, Bermuda

(Address of principal executive offices)

Jane Sheere

73 Front Street

Hamilton, HM 12, Bermuda

+1-441-294-3309

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered pursuant to Section 12(b) of the Act:

| Title of class | Name of each exchange on which registered | |

|---|---|---|

| Limited Partnership Units | New York Stock Exchange; Toronto Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report:

162,163,205 Limited Partnership Units as of December 31, 2015

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| o U.S. GAAP | ý International Financial Reporting Standards as issued by the International Accounting Standards Board | o Other |

If "Other" has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow. Item 17 o Item 18 o

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

i

| | | | PAGE | |||||

|---|---|---|---|---|---|---|---|---|

| 10.H | DOCUMENTS ON DISPLAY | 206 | ||||||

| 10.I | SUBSIDIARY INFORMATION | 206 | ||||||

Item 11. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT NON-PRODUCT RELATED MARKET RISK | 207 | ||||||

Item 12. | DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 207 | ||||||

PART II | 208 | |||||||

Item 13. | DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES | 208 | ||||||

Item 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 208 | ||||||

Item 15. | CONTROLS AND PROCEDURES | 208 | ||||||

Item 16A. | AUDIT COMMITTEE FINANCIAL EXPERT | 209 | ||||||

Item 16B. | CODE OF ETHICS | 209 | ||||||

Item 16C. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 209 | ||||||

Item 16D. | EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEE | 210 | ||||||

Item 16E. | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASER | 210 | ||||||

Item 16F. | CHANGE IN REGISTRANT'S CERTIFYING ACCOUNTANT | 211 | ||||||

Item 16G. | CORPORATE GOVERNANCE | 211 | ||||||

Item 16H. | MINE SAFETY DISCLOSURES | 211 | ||||||

PART III | 212 | |||||||

Item 17. | FINANCIAL STATEMENTS | 212 | ||||||

Item 18. | FINANCIAL STATEMENTS | 212 | ||||||

Item 19. | EXHIBITS | 212 | ||||||

ii

INTRODUCTION AND USE OF CERTAIN TERMS

Unless otherwise specified, information provided in this annual report on Form 20-F is as of December 31, 2015.

Unless the context requires otherwise, when used in this annual report on Form 20-F, the terms "Brookfield Infrastructure", "we", "us" and "our" refer to Brookfield Infrastructure Partners L.P., collectively with its subsidiary entities and the operating entities (as defined below). All dollar amounts contained in this annual report on Form 20-F are expressed in U.S. dollars and references to "dollars", "$", "US$" or "USD" are to U.S. dollars, all references to "C$" or "CAD" are to Canadian dollars, all references to "A$" or "AUD" are to Australian dollars, all references to "CLP" are to Chilean pesos, all references to "COP" are to Colombian pesos, all references to "reais", "BRL" or "R$" are to Brazilian reais, all references to "rupees", "INR" or "I$" are to Indian rupees, and all references to "UF" are to Unidad de Fomento which is an inflation indexed Chilean peso monetary unit that is set daily, on the basis of the prior month's inflation rate. In addition, all references to "£" or "GBP" are to pound sterling, all references to "NZD" are to New Zealand dollars, all references to "€" or "EUR" are to Euros, and unless the context suggests otherwise, references to:

- •

- an "affiliate" of any person are to any other person that, directly or indirectly through one or more intermediaries, controls, is controlled by or is under common control with such person;

- •

- "Asciano Acquisition" means the proposed transaction whereby our partnership and its institutional partners may acquire shares in, or individual assets from, Asciano Limited ("Asciano");

- •

- "Brookfield" are to Brookfield Asset Management and any affiliate of Brookfield Asset Management, other than us;

- •

- "Brookfield Asset Management" are to Brookfield Asset Management Inc.;

- •

- our "current operations" are to the businesses in which we hold an interest as set out in Item 4.B "Business Overview";

- •

- our "communications infrastructure operations" are to our interest in French communication tower infrastructure operations, as described in Item 4.B "Business Overview—Current Operations—Communications Infrastructure Operations—Overview";

- •

- our "energy operations" are to our interest in North American gas transmission operations in the U.S., European energy distribution operations in the Channel Islands and Isle of Man, North American natural gas storage operations in the U.S. and Canada, North American district energy operations in the U.S. and Canada and Australian energy distribution operations, as described in Item 4.B "Business Overview—Current Operations—Energy Operations—Overview";

- •

- "Gammon Acquisition" means the transaction pursuant to which our partnership and its institutional partners have entered into agreements to acquire a portfolio of six toll roads located in India from Gammon Infrastructure Project Limited ("Gammon"), which is expected to complete during the first quarter of 2016, subject to satisfaction of customary closing conditions.

- •

- our "General Partner" are to Brookfield Infrastructure Partners Limited, which serves as our partnership's general partner;

- •

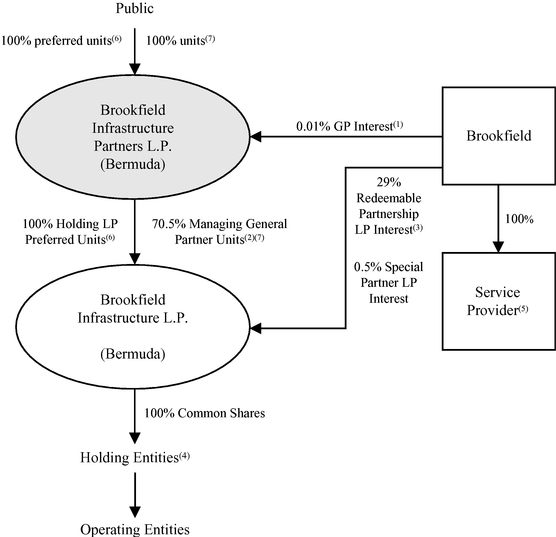

- "Holding Entities" are to certain subsidiaries of the Holding LP, from time-to-time, through which we hold all of our interests in the operating entities;

- •

- the "Holding LP" are to Brookfield Infrastructure L.P.;

Brookfield Infrastructure 1

- •

- the "Infrastructure General Partner" are to Brookfield Infrastructure Special GP Limited, which serves as the general partner of the Infrastructure Special LP;

- •

- the "Infrastructure Special LP" are to Brookfield Infrastructure Special L.P., which is a special limited partner of the Holding LP;

- •

- "Licensing Agreements" are to the licensing agreements described in Item 7.B "Related Party Transactions—Licensing Agreements";

- •

- our "Limited Partnership Agreement" are to the amended and restated limited partnership agreement of our partnership, as amended from time to time;

- •

- the "managing general partner" are to our partnership in its capacity as managing general partner of the Holding LP;

- •

- "Master Services Agreement" are to the amended and restated master services agreement dated as of March 13, 2015, among the Service Recipients, Brookfield Asset Management, the Service Provider and others, as described in Item 6.A "Directors and Senior Management—Our Master Services Agreement";

- •

- "Merger Transaction" are to our acquisition of the ownership interests in Prime that were not already held by us, which was completed on December 8, 2010;

- •

- "operating entities" are to the entities which directly or indirectly hold our current operations and assets that we may acquire in the future, including any assets held through joint ventures, partnerships and consortium arrangements;

- •

- our "partnership" are to Brookfield Infrastructure Partners L.P.;

- •

- "Prime" are to Prime Infrastructure, known collectively as Babcock & Brown Infrastructure Limited and Babcock & Brown Infrastructure Trust, or BBI, prior to its recapitalization on November 20, 2009;

- •

- "rate base" are to a regulated or notionally stipulated asset base;

- •

- the "Redemption-Exchange Mechanism" are to the mechanism by which Brookfield may request redemption of its limited partnership interests in the Holding LP in whole or in part in exchange for cash, subject to the right of our partnership to acquire such interests (in lieu of such redemption) in exchange for units of our partnership, as more fully set forth in Item 10.B "Memorandum and Articles of Association—Description of the Holding LP's Limited Partnership Agreement—Redemption-Exchange Mechanism";

- •

- "Redeemable Partnership Unit" is a unit of the Holding LP that has the rights of the Redemption-Exchange Mechanism. See Item 10.B "Memorandum and Articles of Association—Description of the Holding LP's Limited Partnership Agreement—Units";

- •

- "Relationship Agreement" are to the amended and restated relationship agreement dated as of March 28, 2014, as amended from time to time, by and among our partnership, the Holding LP, the Holding Entities, the Service Provider and Brookfield Asset Management, as described in Item 7.B "Related Party Transactions—Relationship Agreement";

- •

- the "Service Provider" are to Brookfield Infrastructure Group L.P., Brookfield Asset Management Private Institutional Capital Adviser (Canada), LP, Brookfield Asset Management Barbados Inc., Brookfield Global Infrastructure Advisor Limited, Brookfield Infrastructure Group (Australia) Pty Limited and, unless the context otherwise requires, includes any other affiliate of Brookfield Asset Management that provides services to us pursuant to the Master Services Agreement or any other service agreement or arrangement;

2 Brookfield Infrastructure

- •

- "Service Recipients" are to our partnership, the Holding LP and certain of the Holding Entities;

- •

- "spin-off" are to the issuance of the special dividend by Brookfield Asset Management to its shareholders of 23,344,508 of our units on January 31, 2008;

- •

- our "transport operations" are to our interests in Australian rail operations, port operations in the U.S., the UK, and in Europe, toll road operations in Chile, Brazil and, subject to completion of the Gammon Acquisition, India, and Brazilian rail operations, as described in Item 4.B "Business Overview—Our Operations—Transport—Overview";

- •

- our "units" are to the limited partnership units in our partnership other than the preferred units, references to our "preferred units" are to preferred limited partnership units in our partnership and references to our "unitholders" and "preferred unitholders" are to the holders of our units and preferred units, respectively;

- •

- "Class A Preferred Units", "Series 1 Preferred Units", "Series 2 Preferred Units", "Series 3 Preferred Units" and "Series 4 Preferred Units" are to cumulative class A preferred limited partnership units, cumulative class A preferred limited partnership units, series 1, cumulative class A preferred limited partnership units, series 2, cumulative class A preferred limited partnership units, series 3 and cumulative class A preferred limited partnership units, series 4, in our partnership, respectively;

- •

- our "utilities operations" refer to our interests in Australian regulated terminal operation, South American electricity transmission operation in Chile and distribution operation in Colombia, North American electricity transmission operations in Canada, Australian energy distribution operation, and European energy distribution operation in the UK, as described in Item 4.B "Business Overview—Current Operations—Utilities—Overview"; and

- •

- "Voting Agreements" are to the voting arrangements described in Item 7.B "Related Party Transactions—Voting Agreements".

This annual report on Form 20-F contains certain forward-looking statements and information concerning our business and operations. The forward-looking statements and information also relate to, among other things, our objectives, goals, strategies, intentions, plans, beliefs, expectations and estimates and anticipated events or trends. In some cases, you can identify forward-looking statements by terms such as "anticipate," "believe," "could," "estimate," "expect," "intend," "may," "plan," "potential," "should," "objective," "will" and "would" or the negative of those terms or other comparable terminology.

Although we believe that our anticipated future results, performance or achievements expressed or implied by the forward-looking statements and information are based on reasonable assumptions and expectations, the reader should not place undue reliance on forward-looking statements and information because they involve assumptions, known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to differ materially from anticipated future results, performance or achievements expressed or implied by the forward-looking statements and information.

The following factors could cause our actual results to differ materially from our forward looking statements and information:

- •

- our assets are or may become highly leveraged and we intend to incur indebtedness above the asset level;

Brookfield Infrastructure 3

- •

- our partnership is a holding entity that relies on its subsidiaries to provide the funds necessary to pay our distributions and meet our financial obligations;

- •

- future sales and issuances of our units or preferred units, or the perception of such sales or issuances, could depress the trading price of our units or preferred units;

- •

- acquisitions may subject us to additional risks and the expected benefits of our acquisitions may not materialize;

- •

- foreign currency risk and risk management activities;

- •

- our partnership may become regulated as an investment company under theU.S. Investment Company Act of 1940 ("Investment Company Act"), as amended;

- •

- we are exempt from certain requirements of Canadian securities laws and we are not subject to the same disclosure requirements as a U.S. domestic issuer;

- •

- we may be subject to the risks commonly associated with a separation of economic interest from control or the incurrence of debt at multiple levels within an organizational structure;

- •

- effectiveness of our internal controls over financial reporting;

- •

- general economic conditions and risks relating to the economy;

- •

- commodity risks;

- •

- availability and cost of credit;

- •

- government policy and legislation changes;

- •

- exposure to uninsurable losses and force majeure events;

- •

- infrastructure operations may require substantial capital expenditures;

- •

- labour disruptions and economically unfavourable collective bargaining agreements;

- •

- exposure to occupational health and safety related accidents;

- •

- exposure to increased economic regulation and adverse regulatory decisions;

- •

- exposure to environmental risks, including increasing environmental legislation and the broader impacts of climate change;

- •

- high levels of regulation upon many of our operating entities;

- •

- First Nations claims to land, adverse claims or governmental claims may adversely affect our infrastructure operations;

- •

- the competitive market for acquisition opportunities and the inability to identify and complete acquisitions as planned;

- •

- our ability to renew existing contracts and win additional contracts with existing or potential customers;

- •

- timing and price for the completion of unfinished projects;

- •

- some of our current operations are held in the form of joint ventures or partnerships or through consortium arrangements;

- •

- our infrastructure business is at risk of becoming involved in disputes and possible litigation;

- •

- some of our businesses operate in jurisdictions with less developed legal systems and could experience difficulties in obtaining effective legal redress and create uncertainties;

4 Brookfield Infrastructure

- •

- actions taken by national, state, or provincial governments, including nationalization, or the imposition of new taxes, could materially impact the financial performance or value of our assets;

- •

- reliance on technology;

- •

- customers may default on their obligations;

- •

- reliance on tolling and revenue collection systems;

- •

- our ability to finance our operations due to the status of the capital markets;

- •

- changes in our credit ratings;

- •

- our operations may suffer a loss from fraud, bribery, corruption or other illegal acts;

- •

- Brookfield's influence over our partnership and our partnership's dependence on the Service Provider;

- •

- the lack of an obligation of Brookfield to source acquisition opportunities for us;

- •

- our dependence on Brookfield and its professionals;

- •

- interests in our General Partner may be transferred to a third party without unitholder or preferred unitholder consent;

- •

- Brookfield may increase its ownership of our partnership;

- •

- our Master Services Agreement and our other arrangements with Brookfield do not impose on Brookfield any fiduciary duties to act in the best interests of unitholders or preferred unitholders;

- •

- conflicts of interest between our partnership, our preferred unitholders and our unitholders, on the one hand, and Brookfield, on the other hand;

- •

- our arrangements with Brookfield may contain terms that are less favourable than those which otherwise might have been obtained from unrelated parties;

- •

- our General Partner may be unable or unwilling to terminate the Master Services Agreement;

- •

- the limited liability of, and our indemnification of, the Service Provider;

- •

- our unitholders and preferred unitholders do not have a right to vote on partnership matters or to take part in the management of our partnership;

- •

- market price of our units and preferred units may be volatile;

- •

- dilution of existing unitholders;

- •

- adverse changes in currency exchange rates;

- •

- investors may find it difficult to enforce service of process and enforcement of judgments against us;

- •

- we may not be able to continue paying comparable or growing cash distributions to unitholders in the future;

- •

- changes in tax law and practice; and

- •

- other factors described in this annual report on Form 20-F, including, but not limited to, those described under Item 3.D "Risk Factors" and elsewhere in this annual report on Form 20-F.

Brookfield Infrastructure 5

In light of these risks, uncertainties and assumptions, the events described by our forward-looking statements and information might not occur. We qualify any and all of our forward-looking statements and information by these cautionary factors. Please keep this cautionary note in mind as you read this annual report on Form 20-F. We disclaim any obligation to update or revise publicly any forward-looking statements or information, whether as a result of new information, future events or otherwise, except as required by applicable law.

CAUTIONARY STATEMENT REGARDING THE USE OF NON-IFRS ACCOUNTING MEASURES

FFO

To measure performance, among other measures, we focus on net income as well as funds from operations ("FFO").

We define FFO as net income excluding the impact of depreciation and amortization, deferred income taxes, breakage and transaction costs, non-cash valuation gains or losses and other items. FFO is a measure of operating performance that is not calculated in accordance with, and does not have any standardized meaning prescribed by, International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB"). FFO is therefore unlikely to be comparable to similar measures presented by other issuers. FFO has limitations as an analytical tool. See Item 5 "Management's Discussion and Analysis of Financial Condition and Results of Operations—Reconciliation of Non-IFRS Financial Measures" for more information on this measure, including a reconciliation to the most directly comparable IFRS measure.

AFFO

In addition, we use adjusted funds from operations ("AFFO") as a measure of long-term sustainable cash flow.

We define AFFO as FFO less maintenance capital expenditures. AFFO is a measure of operating performance that is not calculated in accordance with, and does not have any standardized meaning prescribed by, IFRS. AFFO is therefore unlikely to be comparable to similar measures presented by other issuers. AFFO has limitations as an analytical tool. See Item 5 "Management's Discussion and Analysis of Financial Condition and Results of Operations—Reconciliation of Non-IFRS Financial Measures" for more information on this measure, including a reconciliation to the most directly comparable IFRS measure.

Adjusted EBITDA

In addition to FFO and AFFO, we focus on "adjusted EBITDA", which we define as FFO excluding the impact of interest expense, cash taxes and other cash income or expenses. Like FFO, adjusted EBITDA is a measure of operating performance that is not calculated in accordance with, and does not have any standardized meaning prescribed by, IFRS. Adjusted EBITDA is therefore unlikely to be comparable to similar measures presented by other issuers. Adjusted EBITDA has limitations as an analytical tool. See Item 5 "Management's Discussion and Analysis of Financial Condition and Results of Operations—Reconciliation of Non-IFRS Financial Measures" for more information on this measure, including a reconciliation to the most directly comparable IFRS measure.

6 Brookfield Infrastructure

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

The following table presents financial data for Brookfield Infrastructure as of and for the periods indicated:

| | For the Year Ended December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

MILLIONS | 2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||

Statements of Operating Results—Key Metrics | ||||||||||||||||

Revenue | $ | 1,855 | $ | 1,924 | $ | 1,826 | $ | 1,524 | $ | 1,115 | ||||||

Direct operating costs | (798 | ) | (846 | ) | (823 | ) | (766 | ) | (561 | ) | ||||||

General and administrative expenses | (134 | ) | (115 | ) | (110 | ) | (95 | ) | (61 | ) | ||||||

Depreciation and amortization expense | (375 | ) | (380 | ) | (329 | ) | (230 | ) | (126 | ) | ||||||

Interest expense | (367 | ) | (362 | ) | (362 | ) | (322 | ) | (253 | ) | ||||||

Share of earnings (losses) from investments in associates and joint ventures | 69 | 50 | (217 | ) | 1 | 76 | ||||||||||

Mark-to-market on hedging items | 83 | 38 | 19 | (49 | ) | (35 | ) | |||||||||

Gain on sale of associates | — | — | 53 | — | — | |||||||||||

Other income (expenses) | 54 | (1 | ) | (35 | ) | 8 | 10 | |||||||||

Income before income tax | 387 | 308 | 22 | 71 | 165 | |||||||||||

Current income tax expense | (22 | ) | (30 | ) | (3 | ) | (12 | ) | (2 | ) | ||||||

Deferred income tax recovery (expense) | 26 | (49 | ) | 1 | 42 | (12 | ) | |||||||||

Net income from continuing operations | 391 | 229 | 20 | 101 | 151 | |||||||||||

Income from discontinued operations, net of income tax(1) | — | — | 45 | 190 | 289 | |||||||||||

Net income | 391 | 229 | 65 | 291 | 440 | |||||||||||

Net income (loss) attributable to partnership(2) | 298 | 184 | (58 | ) | 106 | 187 | ||||||||||

Net income (loss) per limited partnership unit | 1.04 | 0.67 | (0.43 | ) | 0.47 | 1.13 | ||||||||||

Funds from operations (FFO)(3) | 808 | 724 | 682 | 462 | 392 | |||||||||||

Per unit FFO(4) | 3.59 | 3.45 | 3.30 | 2.41 | 2.41 | |||||||||||

Per unit distributions | 2.12 | 1.92 | 1.72 | 1.50 | 1.32 | |||||||||||

- (1)

- The timber segment was reported as part of continuing operations until the second quarter of 2013 and has since been classified as discontinued operations for the comparative periods. Our Canadian and U.S. freehold timberlands were disposed of in the second and third quarter of 2013, respectively.

- (2)

- Net income (loss) attributable to partnership includes net income (loss) attributable to non-controlling interests—Redeemable Partnership Units held by Brookfield, general partner and limited partners.

- (3)

- FFO is defined as net income excluding the impact of depreciation and amortization, deferred income taxes, breakage and transaction costs, non-cash valuation gains or losses and other items. FFO is a measure of operating performance that is not calculated in accordance with, and does not have any standardized meaning prescribed by IFRS. Please see Item 5 "Management's Discussion and Analysis of Financial Condition and Results of Operations—Reconciliation of Non-IFRS Financial Measures" for a discussion of FFO and its limitations as a measure of our operating performance.

- (4)

- During 2015, on average there were 224.9 million units outstanding (2014: 210.1 million, 2013: 206.7 million, 2012: 191.5 million, 2011: 162.5 million).

Brookfield Infrastructure 7

| | As of December 31, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

MILLIONS | 2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||

Statements of Financial Position Key Metrics | ||||||||||||||||

Cash and cash equivalents | $ | 199 | $ | 189 | $ | 538 | $ | 263 | $ | 153 | ||||||

Total assets | 17,735 | 16,495 | 15,682 | 19,718 | 13,269 | |||||||||||

Corporate borrowings | 1,380 | 588 | 377 | 946 | — | |||||||||||

Non-recourse borrowings | 5,852 | 6,221 | 5,790 | 6,993 | 4,885 | |||||||||||

Partnership capital—attributable to limited partners | 3,838 | 3,533 | 3,751 | 3,632 | 3,049 | |||||||||||

Non-controlling interest—Redeemable Partnership Units held by Brookfield | 1,518 | 1,321 | 1,408 | 1,365 | 1,133 | |||||||||||

Non-controlling interest—in operating subsidiaries | 1,608 | 1,444 | 1,419 | 2,784 | 1,683 | |||||||||||

Partnership capital—attributable to general partner | 23 | 24 | 27 | 27 | 24 | |||||||||||

Partnership capital—attributable to preferred unitholders | 189 | — | — | — | — | |||||||||||

The following table reconciles FFO, a non-IFRS financial metric, to the most directly comparable IFRS measure, which is net income (loss) attributable to partnership(2):

| | For the Year Ended December 31 | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

MILLIONS, EXCEPT PER UNIT AMOUNTS(1) | 2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||

Net income (loss) attributable to partnership(2) | $ | 298 | $ | 184 | $ | (58 | ) | $ | 106 | $ | 187 | |||||

Add back or deduct the following: | ||||||||||||||||

Depreciation and amortization | 506 | 481 | 400 | 300 | 203 | |||||||||||

Impairment charge | — | — | 275 | 16 | — | |||||||||||

Deferred income taxes | (53 | ) | (2 | ) | 65 | (37 | ) | 73 | ||||||||

Gain on sale of associate | — | — | (53 | ) | — | — | ||||||||||

Mark-to-market on hedging items | (63 | ) | (39 | ) | (7 | ) | 50 | 26 | ||||||||

Valuation losses (gains) and other | 120 | 100 | 60 | 27 | (97 | ) | ||||||||||

FFO | $ | 808 | $ | 724 | $ | 682 | $ | 462 | $ | 392 | ||||||

- (1)

- Please see Item 5 "Management's Discussion and Analysis of Financial Condition and Results of Operations—Reconciliation of Non-IFRS Financial Measures" for a detailed reconciliation of Brookfield Infrastructure's proportionate results to our partnership's consolidated statements of operating results.

- (2)

- Net income (loss) attributable to partnership includes net income (loss) attributable to non-controlling interest—Redeemable Partnership Units held by Brookfield, general partner and limited partners.

3.B CAPITALIZATION AND INDEBTEDNESS

Not applicable.

3.C REASONS FOR THE OFFER AND USE OF PROCEEDS

Not applicable.

You should carefully consider the following factors in addition to the other information set forth in this annual report on Form 20-F. If any of the following risks actually occur, our business, financial condition and results of operations and the value of our units and preferred units would likely suffer.

8 Brookfield Infrastructure

Risks Relating to Us and Our Partnership

Brookfield Infrastructure and our operating entities use leverage and such indebtedness may result in Brookfield Infrastructure or our operating entities being subject to certain covenants which restrict our ability to engage in certain types of activities or to make distributions to equity.

The Holding LP and many of our Holding Entities and operating entities have entered into credit facilities or have incurred other forms of debt, including for the purposes of acquisitions and investments as well as for general corporate purposes. The total quantum of exposure to debt within Brookfield Infrastructure is significant, and we may become more highly leveraged in the future. Some facilities are fully drawn, while some have amounts of principal which are undrawn.

Highly leveraged assets are inherently more sensitive to declines in revenues, increases in expenses and interest rates and adverse economic, market and industry developments. A leveraged company's income and net assets also tend to increase or decrease at a greater rate than would otherwise be the case if money had not been borrowed. As a result, the risk of loss associated with a leveraged company, all other things being equal, is generally greater than for companies with comparatively less debt. In addition, the use of indebtedness in connection with an acquisition may give rise to negative tax consequences to certain investors. Leverage may also result in a requirement for short-term liquidity, which may force the sale of assets at times of low demand and/or prices for such assets. This may mean that we are unable to realize fair value for the assets in a sale.

Our credit facilities also contain covenants applicable to the relevant borrower and events of default. Covenants can relate to matters including limitations on financial indebtedness, dividends, investments, or minimum amounts for interest coverage, adjusted EBITDA, cash flow or net worth. If an event of default occurs, or minimum covenant requirements are not satisfied, this can result in a requirement to immediately repay any drawn amounts or the imposition of other restrictions including a prohibition on the payment of distributions to equity.

Our credit facilities or other debt or debt-like instruments may or may not be rated. Should such debt or debt-like instruments be rated, a credit downgrade may have an adverse impact on the cost of such debt.

Our partnership is a holding entity and currently we rely on the Holding LP and, indirectly, the Holding Entities and our operating entities to provide us with the funds necessary to pay distributions and meet our financial obligations.

Our partnership is a holding entity and its sole material asset is its managing general partnership interest and preferred limited partnership interest in the Holding LP, which owns all of the common shares of the Holding Entities, through which we hold all of our interests in the operating entities. Our partnership has no independent means of generating revenue. As a result, we depend on distributions and other payments from the Holding LP and, indirectly, the Holding Entities and our operating entities to provide us with the funds necessary to pay distributions on our units and preferred units and to meet our financial obligations. The Holding LP, the Holding Entities and our operating entities are legally distinct from us and some of them are or may become restricted in their ability to pay dividends and distributions or otherwise make funds available to us pursuant to local law, regulatory requirements and their contractual agreements, including agreements governing their financing arrangements, such as the Holding LP's credit facilities and other indebtedness incurred by the Holding Entities and operating entities. Any other entities through which we may conduct operations in the future will also be legally distinct from us and may be similarly restricted in their ability to pay dividends and distributions or otherwise make funds available to us under certain conditions. The Holding LP, the Holding Entities and our operating entities will generally be required to service their debt obligations before making distributions to us or their parent entities, as applicable, thereby reducing the amount of our cash flow available to pay distributions, fund working capital and satisfy other needs.

Brookfield Infrastructure 9

Our partnership anticipates that the only distributions that it will receive in respect of our partnership's managing general partnership interest in the Holding LP will consist of amounts that are intended to assist our partnership in making distributions to our unitholders in accordance with our partnership's distribution policy and to allow our partnership to pay expenses as they become due. Distributions received in respect of our partnership's preferred limited partnership interest in the Holding LP will consist of amounts that are intended to assist our partnership in making distributions to our preferred unitholders in accordance with the terms of our preferred units. The declaration and payment of cash distributions by our partnership is at the discretion of our General Partner. Our partnership is not required to make such distributions and neither our partnership nor our General Partner can assure you that our partnership will make such distributions as intended.

While we plan to review our partnership's distributions to our unitholders periodically, there is no guarantee that we will be able to increase, or even maintain the level of distributions that are paid. Historically, as a result of this review, we decided to increase distributions in February 2011, February 2012, February 2013, February 2014, February 2015 and February 2016, respectively. However, such historical increases in distribution payments may not be reflective of any future increases in distribution payments which will be subject to review by the board of directors of our General Partner taking into account prevailing circumstances at the relevant time. Although we intend to make distributions on our units in accordance with our distribution policy, our partnership is not required to pay distributions on our units and neither our partnership nor our General Partner can assure you that our partnership will be able to increase or even maintain the level of distributions on our units that are made in the future.

Future sales or issuances of our units or preferred units in the public markets, or the perception of such sales or issuances, could depress the trading price of our units and/or preferred units.

The sale or issuance of a substantial number of our units, preferred units or other equity related securities of our partnership in the public markets, or the perception that such sales or issuances could occur, could depress the market price of our units or preferred units and impair our ability to raise capital through the sale of additional units or preferred units. We cannot predict the effect that future sales or issuances of our units, preferred units or other equity-related securities would have on the market price of our units or preferred units.

Acquisitions may subject us to additional risks and the expected benefits of our acquisitions may not materialize.

A key part of Brookfield Infrastructure's strategy involves seeking acquisition opportunities. Acquisitions may increase the scale, scope and diversity of our operations. We depend on the diligence and skill of Brookfield's professionals to manage us, including integrating all of the acquired business' operations with our existing operations. These individuals may have difficulty managing the additional operations and may have other responsibilities within Brookfield's asset management business. If Brookfield does not effectively manage the additional operations, our existing business, financial condition and results of operations may be adversely affected.

10 Brookfield Infrastructure

Acquisitions will likely involve some or all of the following risks, which could materially and adversely affect our business, financial condition or results of operations: the difficulty of integrating the acquired operations and personnel into our current operations; the ability to achieve potential synergies; potential disruption of our current operations; diversion of resources, including Brookfield's time and attention; the difficulty of managing the growth of a larger organization; the risk of entering markets in which we have little experience; the risk of becoming involved in labour, commercial or regulatory disputes or litigation related to the new enterprise; the risk of environmental or other liabilities associated with the acquired business; and the risk of a change of control resulting from an acquisition triggering rights of third parties or government agencies under contracts with, or authorizations held by the operating business being acquired. While it is our practice to conduct extensive due diligence investigations into businesses being acquired, it is possible that due diligence may fail to uncover all material risks in the business being acquired, or to identify a change of control trigger in a material contract or authorization, or that a contractual counterparty or government agency may take a different view on the interpretation of such a provision to that taken by us, thereby resulting in a dispute. The discovery of any material liabilities subsequent to an acquisition, as well as the failure of an acquisition to perform according to expectations, could have a material adverse effect on Brookfield Infrastructure's business, financial condition and results of operations. In addition, if returns are lower than anticipated from acquisitions, we may not be able to achieve growth in our distributions in line with our stated goals and the market value of our units may decline.

We are subject to foreign currency risk and our risk management activities may adversely affect the performance of our operations.

A significant portion of our current operations are in countries where the U.S. dollar is not the functional currency. These operations pay distributions in currencies other than the U.S. dollar, which we must convert to U.S. dollars prior to making distributions, and certain of our operations have revenues denominated in currencies different from our expense structure, thus exposing us to currency risk. Fluctuations in currency exchange rates could reduce the value of cash flows generated by our operating entities or could make it more expensive for our customers to purchase our services and consequently reduce the demand for our services. In addition, a significant depreciation in the value of such foreign currencies may have a material adverse effect on our business, financial condition and results of operations.

When managing our exposure to such market risks, we may use forward contracts, options, swaps, caps, collars and floors or pursue other strategies or use other forms of derivative instruments. The success of any hedging or other derivative transactions that we enter into generally will depend on our ability to structure contracts that appropriately offset our risk position. As a result, while we may enter into such transactions in order to reduce our exposure to market risks, unanticipated market changes may result in poorer overall investment performance than if the derivative transaction had not been executed. Such transactions may also limit the opportunity for gain if the value of a hedged position increases.

Brookfield Infrastructure 11

Our partnership is not, and does not intend to become, regulated as an investment company under the Investment Company Act (and similar legislation in other jurisdictions) and if our partnership was deemed an "investment company" under the Investment Company Act, applicable restrictions could make it impractical for us to operate as contemplated.

The Investment Company Act (and similar legislation in other jurisdictions) provide certain protections to investors and impose certain restrictions on companies that are required to be regulated as investment companies. Among other things, such rules limit or prohibit transactions with affiliates, impose limitations on the issuance of debt and equity securities and impose certain governance requirements. Our partnership has not been and does not intend to become regulated as an investment company and our partnership intends to conduct its activities so it will not be deemed to be an investment company under the Investment Company Act (and similar legislation in other jurisdictions). In order to ensure that we are not deemed to be an investment company, we may be required to materially restrict or limit the scope of our operations or plans. We will be limited in the types of acquisitions that we may make, and we may need to modify our organizational structure or dispose of assets of which we would not otherwise dispose. Moreover, if anything were to happen which causes our partnership to be deemed an investment company under the Investment Company Act, it would be impractical for us to operate as contemplated. Agreements and arrangements between and among us and Brookfield would be impaired, the type and amount of acquisitions that we would be able to make as a principal would be limited and our business, financial condition and results of operations would be materially adversely affected. Accordingly, we would be required to take extraordinary steps to address the situation, such as the amendment or termination of the Master Services Agreement, the restructuring of our partnership and the Holding Entities, the amendment of our Limited Partnership Agreement or the termination of our partnership, any of which could materially adversely affect the value of our units and preferred units. In addition, if our partnership were deemed to be an investment company under the Investment Company Act, it would be taxable as a corporation for U.S. federal income tax purposes, and such treatment could materially adversely affect the value of our units and preferred units.

Our partnership is an "SEC foreign issuer" under Canadian securities regulations and is exempt from certain requirements of Canadian securities laws and a "foreign private issuer" under U.S. securities laws and as a result is subject to disclosure obligations different from requirements applicable to U.S. domestic registrants listed on the New York Stock Exchange ("NYSE").

Although our partnership is a reporting issuer in Canada, it is an "SEC foreign issuer" and is exempt from certain Canadian securities laws relating to disclosure obligations and proxy solicitation, subject to certain conditions. Therefore, there may be less publicly available information in Canada about our partnership than would be available if we were a typical Canadian reporting issuer.

Although our partnership is subject to the periodic reporting requirement of theU.S. Securities Exchange Act of 1934, as amended, and the rules and regulations promulgated thereunder ("Exchange Act"), the periodic disclosure required of foreign private issuers under the Exchange Act is different from periodic disclosure required of U.S. domestic registrants. Therefore, there may be less publicly available information about our partnership than is regularly published by or about other public limited partnerships in the U.S. Our partnership is exempt from certain other sections of the Exchange Act to which U.S. domestic issuers are subject, including the requirement to provide our unitholders with information statements or proxy statements that comply with the Exchange Act. In addition, insiders and large unitholders of our partnership are not obligated to file reports under Section 16 of the Exchange Act, and certain corporate governance rules imposed by the NYSE are inapplicable to our partnership.

12 Brookfield Infrastructure

We may be subject to the risks commonly associated with a separation of economic interest from control or the incurrence of debt at multiple levels within an organizational structure.

Our ownership and organizational structure is similar to structures whereby one company controls another company which in turn holds controlling interests in other companies; thereby, the company at the top of the chain may control the company at the bottom of the chain even if its effective equity position in the bottom company is less than a controlling interest. Brookfield is the sole shareholder of our General Partner and, as a result of such ownership of our General Partner, Brookfield is able to control the appointment and removal of our General Partner's directors and, accordingly, exercises substantial influence over us. In turn, we often have a majority controlling interest or a significant influence in our investments. Even though Brookfield currently has an effective economic interest in our business of approximately 29.3% as a result of ownership of our units and the Redeemable Partnership Units, over time Brookfield may reduce this economic interest while still maintaining its controlling interest, and, therefore, Brookfield may use its control rights in a manner that conflicts with the economic interests of our other unitholders and preferred unitholders. For example, despite the fact that we have a conflicts protocol in place, which addresses the requirement for independent approval and other requirements for transactions in which there is greater potential for a conflict of interest to arise, including transactions with affiliates of Brookfield, because Brookfield will be able to exert substantial influence over us, and, in turn, over our investments, there is a greater risk of transfer of assets of our investments at non-arm's length values to Brookfield and its affiliates. In addition, debt incurred at multiple levels within the chain of control could exacerbate the separation of economic interest from controlling interest at such levels, thereby creating an incentive to leverage us and our investments. Any such increase in debt would also make us more sensitive to declines in revenues, increases in expenses and interest rates, and adverse market conditions. The servicing of any such debt would also reduce the amount of funds available to pay distributions to us and ultimately to our unitholders and preferred unitholders.

Our failure to maintain effective internal controls could have a material adverse effect on our business in the future and the price of our units and preferred units.

Any failure to maintain adequate internal controls over financial reporting or to implement required, new or improved controls, or difficulties encountered in their implementation, could cause us to report material weaknesses or other deficiencies in our internal controls over financial reporting and could result in errors or misstatements in our consolidated financial statements that could be material. If we or our independent registered public accounting firm were to conclude that our internal controls over financial reporting were not effective, investors could lose confidence in our reported financial information and the price of our units and preferred units could decline. Our failure to achieve and maintain effective internal controls could have a material adverse effect on our business in the future, our access to the capital markets and investors' perception of us. In addition, material weaknesses in our internal controls could require significant expense and management time to remediate.

Brookfield Infrastructure 13

Risks Relating to Our Operations and the Infrastructure Industry

All of our operating entities are subject to general economic conditions and risks relating to the economy.

Many industries, including the industries in which we operate, are impacted by adverse events in financial markets, which may have a profound effect on global or local economies. Some key impacts of general financial market turmoil include contraction in credit markets resulting in a widening of credit spreads, devaluations and enhanced volatility in global equity, commodity and foreign exchange markets and a general lack of market liquidity. A slowdown in the financial markets or other key measures of the global economy or the local economies of the regions in which we operate, including, but not limited to, new home construction, employment rates, business conditions, inflation, fuel and energy costs, commodity prices, lack of available credit, the state of the financial markets, interest rates and tax rates may adversely affect our growth and profitability.

The demand for services provided by our operating entities are, in part, dependent upon and correlated to general economic conditions and economic growth of the regions applicable to the relevant asset. Poor economic conditions or lower economic growth in a region or regions may, either directly or indirectly, reduce demand for the services provided by an asset.

For example, a credit/liquidity crisis, such as the global crisis experienced in 2008/2009, could materially impact the cost and availability of financing and overall liquidity; the volatility of commodity output prices and currency exchange markets could materially impact revenues, profits and cash flow; volatile energy, commodity input and consumables prices and currency exchange rates could materially impact production costs; poor local or regional economic conditions could materially impact the level of traffic on our toll roads or volume of commodities transported on our rail network and/or shipped through our ports; our UK regulated distribution business earns connection revenues that would be negatively impacted by an economic recession and a reduction of housing starts in the UK; and the devaluation and volatility of global stock markets could materially impact the valuation of our units and preferred units. Any one of these factors could have a material adverse effect on our business, financial condition and results of operations. If such increased levels of volatility and market turmoil were to continue, our operations and the trading price of our units and preferred units may be further adversely impacted.

Some of our operations depend on continued strong demand for commodities, such as natural gas or minerals, for their financial performance. Material reduction in demand for these key commodities can potentially result in reduced value for assets, or in extreme cases, a stranded asset.

Some of our operations are critically linked to the transport or production of key commodities. For example, our Australian regulated terminal operation relies on demand for coal exports, our Australian rail operation relies on demand for iron ore for steel production and our North American gas transmission operation relies on demand for natural gas and benefits from higher gas prices. While we endeavor to protect against short to medium term commodity demand risk wherever possible by structuring our contracts in a way that minimizes volume risk (e.g. minimum guaranteed volumes and 'take-or-pay' arrangements), these contract terms are finite and in some cases contracts contain termination or suspension rights for the benefit of the customer. Accordingly, a long-term and sustained downturn in the demand for or price of a key commodity linked to one of our operations may result in termination, suspension or default under a key contract, or otherwise have a material adverse impact on the financial performance or growth prospects of that particular operation, notwithstanding our efforts to maximize contractual protections.

If a critical upstream or downstream business ceased to operate, this could materially impact our financial performance or the value of one or more of our operating businesses. In extreme cases, our infrastructure could become redundant, resulting in an inability to recover a return on or of capital and potentially triggering covenants and other terms and conditions under associated debt facilities.

14 Brookfield Infrastructure

General economic and business conditions that impact the debt or equity markets could impact Brookfield Infrastructure's ability to access credit markets.

General economic and business conditions that impact the debt or equity markets could impact the availability of credit to, and cost of credit for, Brookfield Infrastructure. Brookfield Infrastructure has revolving credit facilities and other short-term borrowings. The amount of interest charged on these will fluctuate based on changes in short-term interest rates. Any economic event that affects interest rates or the ability to refinance borrowings could materially adversely impact Brookfield Infrastructure's financial condition. Movements in interest rates could also affect the discount rates used to value Brookfield Infrastructure's assets, which in turn could cause their valuations calculated under IFRS to be reduced resulting in a material reduction in Brookfield Infrastructure's equity value.

In addition, some of our operations either currently have a credit rating or may have a credit rating in the future. A credit rating downgrade may result in an increase in the cost of debt for the relevant businesses and reduced access to debt markets.

Some assets in our portfolio have a requirement for significant capital expenditure. For other assets, cash, cash equivalents and short-term investments combined with cash flow generated from operations are believed to be sufficient for it to make the foreseeable required level of capital investment. However, no assurance can be given that additional capital investments will not be required in these businesses. If Brookfield Infrastructure is unable to generate enough cash to finance necessary capital expenditures through operating cash flow, then Brookfield Infrastructure may be required to issue additional equity or incur additional indebtedness. The issue of additional equity would be dilutive to existing unitholders at the time. Any additional indebtedness would increase the leverage and debt payment obligations of Brookfield Infrastructure, and may negatively impact its business, financial condition and results of operations.

Our business relies on continued access to capital to fund new investments and capital projects. While we aim to prudently manage our capital requirements and ensure access to capital is always available, it is possible we may overcommit ourselves or misjudge the requirement for capital or the availability of liquidity. Such a misjudgment may require capital to be raised quickly and the inability to do so could result in negative financial consequences or in extreme cases bankruptcy.

All of our operating entities are subject to changes in government policy and legislation.

Our financial condition and results of operations could also be affected by changes in economic or other government policies or other political or economic developments in each country or region, as well as regulatory changes or administrative practices over which we have no control such as: the regulatory environment related to our business operations, concession agreements and periodic regulatory resets; interest rates; currency fluctuations; exchange controls and restrictions; inflation; liquidity of domestic financial and capital markets; policies relating to climate change or policies relating to tax; and other political, social, economic, and environmental and occupational health and safety developments that may occur in or affect the countries in which our operating entities are located or conduct business or the countries in which the customers of our operating entities are located or conduct business or both.

Brookfield Infrastructure 15

In addition, operating costs can be influenced by a wide range of factors, many of which may not be under the control of the owner/operator, including the need to comply with the directives of central and local government authorities. For example, in the case of our utility, transport and energy operations, we cannot predict the impact of future economic conditions, energy conservation measures, alternative fuel requirements, or governmental regulation all of which could reduce the demand for or availability of commodities our transport and energy operations rely upon, most notably coal and natural gas. It is difficult to predict government policies and what form of laws and regulations will be adopted or how they will be construed by the relevant courts, or to the extent which any changes may adversely affect us.

We may be exposed to natural disasters, weather events, uninsurable losses and force majeure events.

Force majeure is the term generally used to refer to an event beyond the control of the party claiming that the event has occurred, including but not limited to acts of God, fires, floods, earthquakes, wars and labour strikes. The assets of our infrastructure businesses are exposed to unplanned interruptions caused by significant catastrophic events such as cyclones, landslides, explosions, terrorist attacks, war, floods, earthquakes, fires, major plant breakdowns, pipeline or electricity line ruptures, accidents, extreme weather events or other disasters. Operational disruption, as well as supply disruption, could adversely affect the cash flow available from these assets. In addition, the cost of repairing or replacing damaged assets could be considerable and could give rise to third-party claims. In some cases, project agreements can be terminated if the force majeure event is so catastrophic as to render it incapable of remedy within a reasonable time period. Repeated or prolonged interruption may result in a permanent loss of customers, substantial litigation, damage, or penalties for regulatory or contractual non-compliance. Moreover, any loss from such events may not be recoverable in whole or in part under relevant insurance policies. Business interruption insurance is not always available, or available on reasonable economic terms to protect the business from these risks.

Given the nature of the assets operated by our operating entities, we may be more exposed to risks in the insurance market that lead to limitations on coverage and/or increases in premium. For example, many components of our South American electricity transmission operations and toll roads are not insured or not fully insured against losses from earthquakes and our North American gas transmission operation, our Australian distribution operations and our European regulated distribution operations self-insure the majority of their line and pipe assets. Therefore, the occurrence of a major or uninsurable event could have a material adverse effect on financial performance. Even if such insurance were available, the cost may be prohibitive. The ability of the operating entities to obtain the required insurance coverage at a competitive price may have an impact on the returns generated by them and accordingly the returns we receive.

For example, our regulated energy distribution businesses generate revenue based on the volume transmitted through their systems. Weather that deviates materially from normal conditions could impact these businesses. A number of our businesses may be adversely impacted by extreme weather. Our Australian rail operation transports grain on its system, for which it is contracted on a volume basis. A drought could have a material negative impact on revenue from grain transportation.

All of our infrastructure operations may require substantial capital expenditures in the future.

Our utilities, transport and energy operations are capital intensive and require substantial ongoing expenditures for, among other things, additions and improvements, and maintenance and repair of plant and equipment related to our operations. Any failure to make necessary capital expenditures to maintain our operations in the future could impair the ability of our operations to serve existing customers or accommodate increased volumes. In addition, we may not be able to recover such investments based upon the rates our operations are able to charge.

16 Brookfield Infrastructure

In some of the jurisdictions in which we have utilities, transport or energy operations, certain maintenance capital expenditures may not be covered by the regulatory framework. If our operations in these jurisdictions require significant capital expenditures to maintain our asset base, we may not be able to recover such costs through the regulatory framework. In addition, we may be exposed to disallowance risk in other jurisdictions to the extent that capital expenditures and other costs are not fully recovered through the regulatory framework.

Performance of our operating entities may be harmed by future labour disruptions and economically unfavourable collective bargaining agreements.

Several of our current operations or other business operations have workforces that are unionized or that in the future may become unionized and, as a result, are required to negotiate the wages, benefits and other terms with many of their employees collectively. If an operating entity were unable to negotiate acceptable contracts with any of its unions as existing agreements expire, it could experience a significant disruption of its operations, higher ongoing labour costs and restrictions on its ability to maximize the efficiency of its operations, which could have a material adverse effect on its business, financial condition and results of operations.

In addition, in some jurisdictions where we have operations, labour forces have a legal right to strike which may have an impact on our operations, either directly or indirectly, for example if a critical upstream or downstream counterparty was itself subject to a labour disruption which impacted our ability to operate.

Our operations are exposed to occupational health and safety and accident risks.

Infrastructure projects and operational assets are highly exposed to the risk of accidents that may give rise to personal injury, loss of life, disruption to service and economic loss. Some of the tasks undertaken by employees and contractors are inherently dangerous and have the potential to result in serious injury or death.

Our operating entities are subject to laws and regulations governing health and safety matters, protecting both members of the public and their employees and contractors. Occupational health and safety legislation and regulations differ in each jurisdiction. Any breach of these obligations, or serious accidents involving our employees, contractors or members of the public could expose them to adverse regulatory consequences, including the forfeit or suspension of operating licenses, potential litigation, claims for material financial compensation, reputational damage, fines or other legislative sanction, all of which have the potential to impact the results of our operating entities and our ability to make distributions. Furthermore, where we do not control a business, we have a limited ability to influence health and safety practices and outcomes.

Brookfield Infrastructure 17

Many of our operations are subject to economic regulation and may be exposed to adverse regulatory decisions.

Due to the essential nature of some of the services provided by our assets and the fact that some of these services are provided on a monopoly or near monopoly basis, many of our operations are subject to forms of economic regulation. This regulation can involve different forms of price control and can involve ongoing commitments to economic regulators and other governmental agencies. The terms upon which access to our facilities is provided, including price, can be determined or amended by a regulator periodically. Future terms to apply, including access charges that our operations are entitled to charge, cannot be determined with any certainty, as we do not have discretion as to the amount that can be charged. New legislation, regulatory determinations or changes in regulatory approaches may result in regulation of previously unregulated businesses or material changes to the revenue or profitability of our operations. In addition, a decision by a government or regulator to regulate non-regulated assets may significantly and negatively change the economics of these businesses and the value or financial performance of Brookfield Infrastructure. For example, in 2010 regulatory action taken by the Federal Energy Regulatory Commission ("FERC") saw a significant reduction in annual cashflow expectations of our North American gas transmission operations.

Our operating entities are exposed to the risk of environmental damage.

Many of Brookfield Infrastructure's assets are involved in using, handling or transporting substances that are toxic, combustible or otherwise hazardous to the environment. Furthermore, some of our assets have operations in or in close proximity to environmentally sensitive areas or densely populated communities. There is a risk of a leak, spillage or other environmental emission at one of these assets, which could cause regulatory infractions, damage to the environment, injury or loss of life. Such an incident if it occurred could result in fines or penalties imposed by regulatory authorities, revocation of licenses or permits required to operate the business or the imposition of more stringent conditions in those licenses or permits, or legal claims for compensation (including punitive damages) by affected stakeholders. In addition, some of our assets may be subject to regulations or rulings made by environmental agencies that conflict with existing obligations we have under concession or other permitting agreements. Resolution of such conflicts may lead to uncertainty and increased risk of delays or cost over-runs on projects. All of these have the potential to significantly impact the value or financial performance of Brookfield Infrastructure.

Our operating entities are exposed to the risk of increasing environmental legislation and the broader impacts of climate change.

With an increasing global focus and public sensitivity to environmental sustainability and environmental regulation becoming more stringent, Brookfield Infrastructure's assets could be subject to increasing environmental responsibility and liability. For example, many jurisdictions in which Brookfield Infrastructure operates are considering implementing, or have implemented, schemes relating to the regulation of carbon emissions. As a result, there is a risk that the consumer demand for some of the energy sources supplied by Brookfield Infrastructure will be reduced. For example, the United Kingdom's phasing out of analog meters and use of gas as a source of heating for residential customers could lead to a reduction in revenue and growth at our UK utility business. The nature and extent of future regulation in the various jurisdictions in which Brookfield Infrastructure's operations are situated is uncertain, but is expected to become more complex and stringent.

18 Brookfield Infrastructure

It is difficult to assess the impact of any such changes on Brookfield Infrastructure. These schemes may result in increased costs to our operations that may not be able to be passed onto our customers and may have an adverse impact on prospects for growth of some businesses. To the extent such regimes (such as carbon emissions schemes or other carbon emissions regulations) become applicable to the operations of Brookfield Infrastructure (and the costs of such regulations are not able to be fully passed on to consumers), its financial performance may be impacted due to costs applied to carbon emissions and increased compliance costs.

Our operating entities are also subject to laws and regulations relating to the protection of the environment and pollution. Standards are set by these laws and regulations regarding certain aspects of environmental quality and reporting, provide for penalties and other liabilities for the violation of such standards, and establish, in certain circumstances, obligations to remediate and rehabilitate current and former facilities and locations where our operations are, or were, conducted. These laws and regulations may have a detrimental impact on the financial performance of our infrastructure operations and projects through increased compliance costs or otherwise. Any breach of these obligations, or even incidents relating to the environment that do not amount to a breach, could adversely affect the results of our operating entities and their reputations and expose them to claims for financial compensation or adverse regulatory consequences.

Our operations may also be exposed directly or indirectly to the broader impacts of climate change, including extreme weather events, export constraints on commodities, increased resource prices and restrictions on energy and water usage.

Our operating entities may be exposed to higher levels of regulation than in other sectors and breaches of such regulations could expose our operating entities to claims for financial compensation and adverse regulatory consequences.

In many instances, our ownership and operation of infrastructure assets involves an ongoing commitment to a governmental agency. The nature of these commitments exposes the owners of infrastructure assets to a higher level of regulatory control than typically imposed on other businesses. For example, several of our utilities, transport and energy operations are subject to government safety and reliability regulations that are specific to their industries. The risk that a governmental agency will repeal, amend, enact or promulgate a new law or regulation or that a governmental authority will issue a new interpretation of the law or regulations, could affect our operating entities substantially.

Sometimes commitments to governmental agencies, for example, under toll road concession arrangements, involve the posting of financial security for performance of obligations. If obligations are breached these financial securities may be called upon by the relevant agency.

There is also the risk that our operating entities do not have, might not obtain, or may lose permits necessary for their operations. Permits or special rulings may be required on taxation, financial and regulatory related issues. Even though most permits and licenses are obtained before the commencement of operations, many of these licenses and permits have to be renewed or maintained over the life of the business. The conditions and costs of these permits, licenses and consents may be changed on any renewal, or, in some cases, may not be renewed due to unforeseen circumstances or a subsequent change in regulations. In any event, the renewal or non-renewal could have a material adverse effect on our business, financial condition and results of operations.

The risk that a government will repeal, amend, enact or promulgate a new law or regulation or that a regulator or other government agency will issue a new interpretation of the law or regulations, may affect our operations or a project substantially. This may also be due to court decisions and actions of government agencies that affect these operations or a project's performance or the demand for its services. For example, a government policy decision may result in adverse financial outcomes for us through directions to spend money to improve security, safety, reliability or quality of service.

Brookfield Infrastructure 19

The lands used for our infrastructure assets may be subject to adverse claims or governmental or First Nations rights.

Our operations require large areas of land on which to be constructed and operated. The rights to use the land can be obtained through freehold title, leases and other rights of use. Although we believe that we have valid rights to all material easements, licenses and rights of way for our infrastructure operations, not all of our easements, licenses and rights of way are registered against the lands to which they relate and may not bind subsequent owners. Additionally, different jurisdictions have adopted different systems of land title and in some jurisdictions it may not be possible to ascertain definitively who has the legal right to enter into land tenure arrangements with the asset owner. In some jurisdictions where we have operations, it is possible to claim indigenous or aboriginal rights to land and the existence or declaration of native title may affect the existing or future activities of our utilities, transport or energy operations and impact on their business, financial condition and results of operations.

In addition, a government, court, regulator, or indigenous or aboriginal group may make a decision or take action that affects an asset or project's performance or the demand for its services. In particular, a regulator may restrict our access to an asset, or may require us to provide third parties with access, or may affect the pricing structure so as to lower our revenues and earnings. In Australia, native title legislation provides for a series of procedures that may need to be complied with if native title is declared on relevant land. In Canada, for example, courts have recognized that First Nations peoples may possess rights at law in respect of land used or occupied by their ancestors where treaties have not been concluded to deal with these rights. In either case, the claims of a First Nations group may affect the existing or future activities of our operations, impact on our business, financial condition and results of operations, or require that compensation be paid.

20 Brookfield Infrastructure

We operate in a highly competitive market for acquisition opportunities and we may be unable to identify and complete acquisitions as planned.