Exhibit 99.2

July 23, 2019

Fellow Calix stockholders:

Our mission is to connect everyone and everything. Calix platforms empower our customers to build new business models, rapidly deploy new services and make the promise of the smart home and business a reality.

Our second quarter of 2019 reinforced our view that our platforms and services position us to ride the coming wave of disruption in the communications industry. Demand in all our customer segments was strong except for our medium-sized, publicly-traded Incumbent Local Exchange Carrier (ILEC) customer base. The headwinds coming from these ILEC customers, which we discussed on our first quarter earnings call, have continued albeit slowly diminishing. We believe these headwinds will continue and diminish through the remainder of this year. Our supply chain performed according to plan in the quarter. We stated last quarter that we believed we would likely achieve demand-supply equilibrium in the third quarter of 2019. We can now confirm that will be the case.

The value of our all-platform product offerings continues to resonate, and demand for our platforms continues to grow. Our expanding addressable market was demonstrated yet again this quarter as we added 33 new customers, bringing our trailing four quarter new customer count to 114. As has been the trend over the past several quarters, well more than half of these new customers came from emerging customer verticals. This continued expansion of our customer base is fundamental to our transformation and will create a foundation for predictable, profitable growth for years to come.

Riding the Wave of Disruption

Our vision is focused on providing the platforms and services that enable innovative service providers to create services at a DevOps pace and provide their subscribers with an exceptional experience.

Service providers achieve this objective by building their infrastructure and service offerings on platforms. The ongoing wave of disruption sweeping across the communications space remains unprecedented in our experience. We continue to see traditional business models being disrupted as service providers of all types learn to adapt to the needs of the device-enabled subscriber. As the market continues to disrupt, the gap between subscriber needs and service provider supply continues to grow. New service providers are being created to address this unmet need, and capital is being formed to support them. We see this pace accelerating in the market, and it is well aligned with our mission; and we see the pace of existing providers transforming to address this need hastening as well. For Calix, these shifts have been significant, creating headwinds and unpredictability in our business. A few years ago, the publicly traded ILECs represented a large majority of our revenue … today they represent only a small minority. This dynamic stems from the absolute decline in revenue from these customers as well as our success in winning new customers and diversifying our customer base. We believe that in 2020 the ILEC customer base will no longer pose a meaningful risk to the predictability of our business. And, as these service providers realign their investments, we are finding areas where our platforms can help them succeed and even grow. In short, when a service provider of any type chooses to own the subscriber experience, we are well positioned to help them succeed.

Continued Transformation to an All Platform Company

Our relentless focus on the transformation of Calix into a communications cloud and software platform, systems and services business yielded further progress in the second quarter despite the lower revenue relative to the year ago quarter. As we stated in our prior letters to stockholders, we continue to believe this transformation will manifest in improved financial performance across four measurable metrics over the long term:

| |

| • | Disciplined operating expense investment |

| |

| • | Deliberate revenue growth |

| |

| • | Increased predictability |

In the second quarter of 2019, we made progress on these metrics, and we expect these metrics will continue to improve as our platforms increase as a percentage of our total business.

Examples of our progress made in the quarter were:

| |

| • | Added 33 new customers in the quarter from all segments of the market. |

| |

| • | Continued rapid expansion of the Calix Cloud platform as customers now using Calix Cloud analytics more than tripled year-over-year. |

| |

| • | Generated another strong quarter of bookings and shipments for our EXOS-powered next generation GigaSpire systems as bookings more than doubled in the quarter sequentially. |

| |

| • | Continued rapid growth of AXOS and AXOS systems as bookings more than doubled year-over-year. |

| |

| • | Light Reading recognized the AXOS Intelligent Access Edge solution as the Most Innovative Telecoms Product at their annual Leading Lights Awards. |

Our focus remains on finding like-minded customers regardless of their type, size or location. Our execution is aligned with continuing the ramp of our all-platform offerings, aligning our investments and maintaining strong discipline over our operating expenses. Over the long-term, we believe this focus will drive continuous improvement in our financial performance.

Second Quarter 2019 Financial Results

|

| | | |

| Actual GAAP | Actual Non-GAAP | Guidance Non-GAAP |

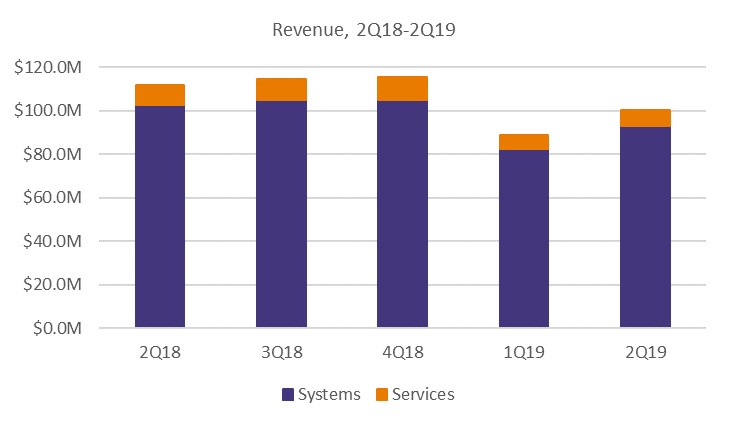

| Revenue | $100.3M | $100.3M | $95M - $105M |

| Gross margin | 44.5% | 46.6% | 45.0 - 47.0% (1) |

| Operating expenses | $49.6M | $47.2M | $47M - $49M (1) |

| Net loss per diluted common share | ($0.09) | ($0.01) | ($0.08) - $0.00 (1) |

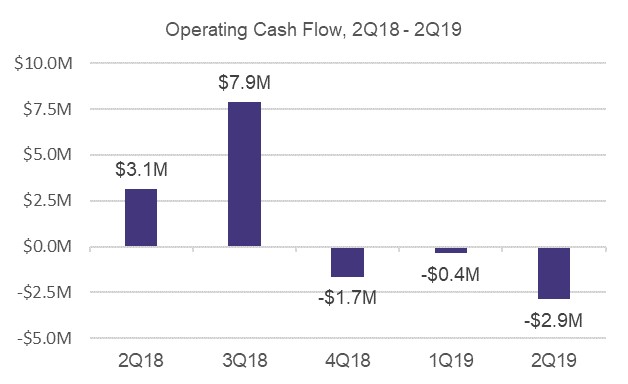

| Operating cash flow | ($2.9M) | Negative | Negative |

(1) Excludes the impact from non-GAAP items such as stock-based compensation and U.S. tariff and tariff-related costs. See GAAP to non-GAAP reconciliations beginning on page 13.

Top and bottom-line results were in-line with our financial guidance. Total revenue decreased relative to the year ago quarter as another strong quarter of demand for our platforms, ramps of new offerings and increased customer diversity were offset by declines within our large, North America-based customers as well as our medium-sized, ILEC customer base. Non-GAAP gross margin was at the high end of our guidance due to favorable customer mix, while operating expenses were at the low end of our guidance due to our continued financial discipline.

Systems revenue decreased 9% compared to the year ago period due to the continued pressure on our legacy systems revenue. We saw continued traction with our Calix Cloud, EXOS and AXOS platforms. Compared to the prior quarter, systems revenue increased sequentially by 13% due to both seasonal increases as well as mitigation of the systems supply shortages. Services revenue decreased 18% compared to the year ago quarter as a continued ramp in our next generation services offerings was

more than offset by lower professional services work related to CAF deployments. We continued to align our services business with our all-platform model through the creation of higher differentiated value services. Compared to the prior quarter, services revenue increased 7% due to normal seasonality.

Domestic revenue was 86% of total revenue for the quarter and decreased 7% compared to the year ago period due to lower demand for our legacy products. Revenue from large customers decreased significantly compared to the year ago period primarily due to lower shipments to a couple of large, North America-based service providers. The principal driver of the lower shipments was lower demand for our legacy products and to a lesser extent the timing of shipments between quarters. Revenue from medium-sized ILEC customers decreased relative to the year ago period due to challenges that some of these customers face. Revenue from small customers increased compared to the year ago quarter due to strength in Calix Cloud and AXOS platforms. International revenue was 14% of total revenue and decreased 24% year-over-year due to the timing of network builds by several customers. Across the board, the team continues to focus on finding strategically-aligned customers for our all-platform business.

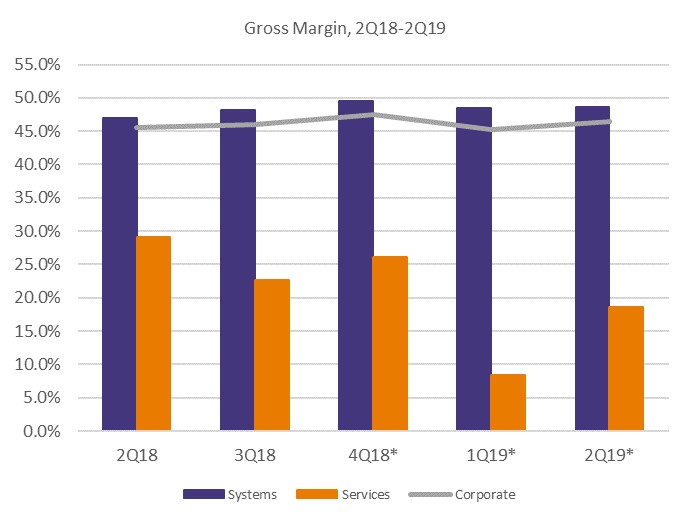

* Systems gross margin excludes 3.0%, 2.6% and 1.9% for 4Q18, 1Q19 and 2Q19, respectively, of U.S. tariff and tariff-related costs. See GAAP to non-GAAP reconciliations on page 13.

Excluding the impact from tariff and tariff-related expenses incurred during the second quarter of 2019, overall GAAP and non-GAAP gross margin improved in the quarter compared to the year ago quarter owing to favorable systems and customer mix as well as the benefit our platforms provide as they continue to increase as a portion of our revenue mix. We saw benefits from continued customer diversification and improved systems mix driven by our all-platform offerings. Systems gross margin on a GAAP basis decreased approximately 40 basis points compared to the year ago quarter despite absorbing 190 basis points of tariff and tariff-related costs, reflecting improved mix and the benefit of platforms as they increase as a percentage of the overall mix. Non-GAAP systems gross margin increased more than 160 basis points year-over-year, respectively. The principal drivers of the year-over-year improvement in systems gross margin were continued growth in our all-platform offerings, customer diversification and mix. Services gross margin decreased compared to the year ago quarter owing to the lower level of revenue in the quarter. Sequentially, services gross margin increased this quarter due to favorable mix within services and lower services costs.

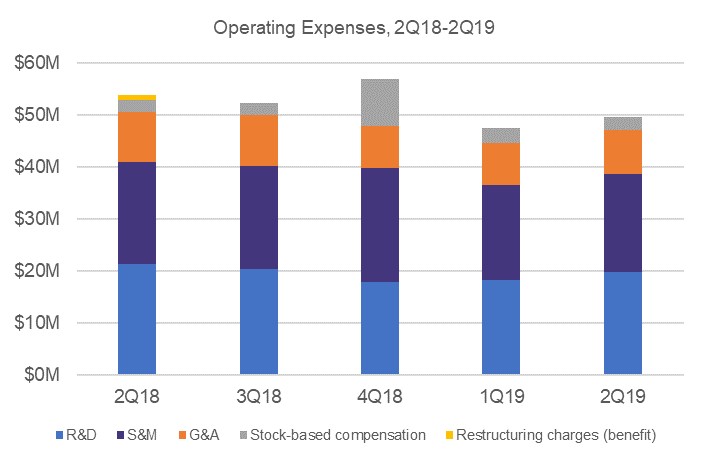

Operating expenses for the second quarter were at the low-end of guidance on a non-GAAP basis due to maintaining disciplined investment decisions. On a GAAP basis, operating expenses were down nearly 8% compared to the year ago quarter as a result of our restructuring actions over a year ago as well as a focus on disciplined expense investment. We saw declines across all operating expense areas compared to the year ago period as we continue to benefit from the leverage within our all-platform offering. In particular, the decrease in overall R&D expense did not impact our level of platform innovations allowing us to introduce new offerings at a DevOps pace. As demonstrated this quarter with our all-platform model, we expect to maintain our operating expense leverage, while maintaining our pace of innovation.

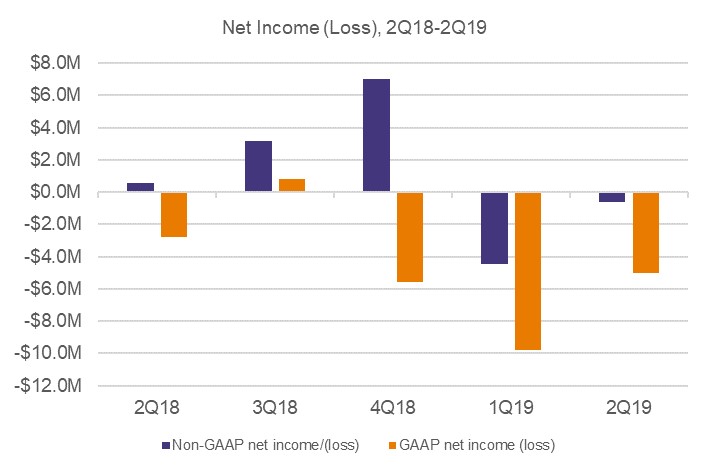

Despite lower revenue of $11.4 million compared to the year ago quarter, our non-GAAP net loss was at a nearly breakeven level, demonstrating the benefits of our all platform offering and the benefits from restructuring actions taken over a year ago. Compared to the year ago quarter, the decrease in our net profit and increase in our net loss on both a GAAP and non-GAAP basis was driven by the lower level of revenue only partially offset by the ramp of our new offerings and lower operating expenses. Our net loss on a GAAP basis increased by $2.2 million year-over-year from a net loss of $2.8 million to a net loss of $5.0 million. This net loss includes $1.9 million of U.S. tariff and tariff-related costs incurred in the second quarter of 2019. Sequentially, our GAAP net loss improved due to the higher level of revenue and increased gross margin partially offset by higher operating expenses. As a reminder, our GAAP results include stock-based compensation, restructuring charges (benefit) and U.S. tariff and tariff-related costs. See GAAP to non-GAAP reconciliations on page 13.

Balance Sheet and Cash Flow

We ended the quarter with cash of $34.9 million, a sequential decrease of $9.1 million. The sequential decrease in our cash was primarily the result of lower borrowings on our line of credit of $5.0 million and capital expenditures of $4.5 million. Compared to the year ago quarter, our cash decreased by $13.2 million primarily due to capital investments of $17.0 million and lower borrowings of $5.0 million partially offset by proceeds from equity-based employee benefit plans of $8.3 million. The decrease in operating cash flow in the quarter of $2.9 million was due to the increased working capital needed to support our supply chain realignment efforts. We expect to generate cash from operations in the third quarter.

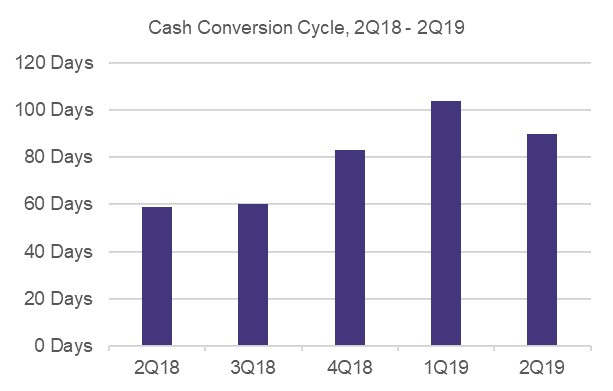

Our team remains focused on operational excellence and customer satisfaction. During the second quarter of 2019, we made improvements in our working capital management despite the negative impact from our supply chain realignment activities. Accounts receivable days sales outstanding at quarter end were 55 days, flat with the prior quarter and down 2 days from the prior year. Inventory turns were 3.9 at quarter end, compared to 3.4 turns in the prior quarter and 9.0 turns in the year ago quarter as we carried a higher than normal level of inventory to support our supply chain realignment. Accounts payable days at quarter end were 59 days up 1 day from the prior quarter and up 20 days from the year ago quarter as we look to keep our cash conversion cycle within our expected range. Our cash conversion cycle declined to 90 days compared to 104 days in the prior quarter and increased from 59 days in the year ago quarter. Over the next few quarters, we expect our cash conversion cycle to return to historical levels as the higher inventory levels caused by the supply chain realignment abate.

Third Quarter 2019 Guidance

|

| | |

| |

Guidance Non-GAAP | Guidance Reconciled to GAAP |

| Revenue | $110M - $114M | $110M - $114M |

| Gross margin | 45.0 - 47.0% (1) | 44.2 - 46.2% |

| Operating expenses | $48M - $50M (1) | $50.5M - $52.5M |

| Net income (loss) per diluted common share | $0.02 - $0.06 (1) (2) | ($0.04) - $0.00 (2) |

| Operating cash flow | Positive | Positive |

| |

| (1) | Excludes the impact from non-GAAP items such as stock-based compensation and U.S. tariff and tariff-related costs. See GAAP to non-GAAP reconciliations on page 14. |

| |

| (2) | Based on 55.7 million weighted-average diluted common shares outstanding. |

Our guidance for the third quarter of 2019 reflects our expectations as of the date of this letter. Relative to the year ago quarter and the second quarter of 2019, we expect to see positive benefits in the third quarter of 2019 from the continued ramp of our all-platform offerings. We continue to expect shipments in the quarter to several large customers as they rollout next generation networks. Even with this anticipated growth, systems demand from our legacy ILEC customer base is expected to be lower than previously anticipated. We see this trend continuing, although diminishing, throughout the remainder of 2019 as these customers work through a number of issues including bankruptcy proceedings, merger integration and asset dispositions.

As of the date of this letter, our key manufacturing partners are now largely at production-demand parity, and our mitigation efforts associated with the U.S. tariffs on goods imported from China are complete. As of June 30, 2019, we have approximately $0.7 million of U.S. tariffs in inventory that are expected to impact gross margin in the third quarter of 2019, which is considered in our GAAP gross margin guidance. Our non-GAAP gross margin guidance for next quarter reflects consistent systems and customer mix.

Our non-GAAP operating expense guidance for next quarter reflects growth in revenue and our continued focus on investment discipline.

Finally, we expect positive operating cash flow next quarter as we anticipate some normalization in our working capital requirements and improved profitability.

Importantly, we remain committed to our long-term financial model. As a reminder, our long-term model produces a better than 10% operating margin at an annual revenue level of $600 million.

Summary

Strong demand for our platforms along with rapid expansion of our customer base continues to demonstrate the progress we made towards our mission in the second quarter. As we remain focused on execution, we expect to see our performance over the long-term continue to improve. Similar to previous quarters, we grew our customer base, expanded our gross margin compared to the year ago quarter and continued to demonstrate discipline in operating expense investment, all despite lower revenue compared to the year ago quarter.

Based on improving trends in bookings, a very positive reception to new service offerings across a broad segment of our customer base and the strong pipeline of platform opportunities ahead of us, we see many innovative service providers looking to Calix to provide the solutions and services to enable them to improve their subscribers’ experience, thereby driving their revenue higher, lowering their churn and increasing ROI. With an expanding pipeline of opportunities spanning service providers of every type, we believe we are well placed to continue building Calix … an all-platform company … that is positioned in front of the largest wave of disruption our industry has experienced. We remain committed to our vision, and we sincerely thank our employees, customers and stockholders for their continued support as we capitalize on this opportunity.

Sincerely,

|

| |

Carl Russo President & CEO |

Cory Sindelar CFO |

Conference Call

In conjunction with this announcement, Calix will host a conference call tomorrow, July 24, 2019, at 5:30 a.m. Pacific Time (8:30 a.m. Eastern Time) to answer questions regarding our second quarter 2019 financial results. A live audio webcast and replay of the call will be available in the Investor Relations section of the Calix website at http://investor-relations.calix.com.

Live call access information: Dial-in number: (877) 407-4019 (U.S.) or (201) 689-8337 (outside the U.S.)

The conference call and webcast will include forward-looking information.

Investor Inquiries

Thomas J. Dinges, CFA

Director of Investor Relations

408-474-0080

Tom.Dinges@calix.com

About Calix

Calix, Inc. (NYSE: CALX) - Innovative communications service providers rely on Calix platforms to help them master and monetize the complex infrastructure between their subscribers and the cloud. Calix is the leading global provider of the cloud and software platforms, systems and services required to deliver the unified access network and smart premises of tomorrow. Our platforms and services help our customers build next generation networks by embracing a DevOps operating model, optimize the subscriber experience by leveraging big data analytics and turn the complexity of the smart home and business into new revenue streams.

Forward-Looking Statements

Statements made in this stockholder letter and the earnings call referencing the stockholder letter that are not statements of historical fact are forward-looking statements. Forward-looking statements are subject to the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements relate to, but are not limited to, statements about potential customer or market opportunities, growth and pipeline opportunities, statements about customer anticipated purchase trends or anticipated adoption of our platforms, systems or services offerings, industry, market and customer trends, opportunities with existing and prospective customers, the anticipated benefits from and effectiveness of our supply-chain reengineering activities and ongoing management of our global supply-chain, the future impact, financial or otherwise, of the U.S. tariffs or any other tariffs or trade regulations that may be imposed whether by the United States or other countries, as well as our ability to effectively mitigate such impacts, and future financial performance (including the outlook for the third quarter of 2019). Forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from expectations, including but not limited to fluctuations in the Company’s financial and operating results, the capital spending decisions of its customers, changes and disruptions in the market and industry, changes in regulations and/or government sponsored programs, competition, its ability to achieve market acceptance of new systems and solutions, its ability to grow its customer base, fluctuations in costs associated with its systems and services including higher costs due to project delays and changes, third party dependencies for production and resource management associated with our global supply-chain that may cause delays in production and unavailability of systems to meet customer orders, which may be substantial, cost overruns and other unanticipated factors, as well as the risks and uncertainties described in its annual reports on Form 10-K and its quarterly reports on Form 10-Q, each as filed with the SEC and available at www.sec.gov, particularly in the sections titled “Risk Factors.” Forward-looking statements speak only as of the date the statements are made and are based on information available to the Company at the time those statements are made and/or management’s good faith belief as of that time with respect to future events. Calix assumes no obligation to update forward-looking statements to reflect actual performance or results, changes in assumptions or changes in other factors affecting forward-looking information, except to the extent required by applicable securities laws. Accordingly, investors should not place undue reliance on any forward-looking statements.

Use of Non-GAAP Financial Information

The Company uses certain non-GAAP financial measures in this stockholder letter to supplement its consolidated financial statements, which are presented in accordance with GAAP. These non-GAAP measures include non-GAAP gross margin, non-GAAP operating expenses, non-GAAP net income (loss) and non-GAAP net income (loss) per diluted common share. These non-GAAP measures are provided to enhance the reader’s understanding of the Company’s operating performance as they primarily exclude certain non-cash charges for stock-based compensation, gain on sale of product line, restructuring charges (benefit) and U.S. tariff and tariff-related costs, which the Company believes are not indicative of its core operating results.

Management believes that the non-GAAP measures used in this stockholder letter provide investors with important perspectives into the Company’s ongoing business performance and management uses these non-GAAP measures to evaluate financial results and to establish operational goals. The presentation of these non-GAAP measures is not meant to be a substitute for results presented in accordance with GAAP, but rather should be evaluated in conjunction with those GAAP results. A reconciliation of the non-GAAP results to the most directly comparable GAAP results is provided in this stockholder letter. The non-GAAP financial measures used by the Company may be calculated differently from, and therefore may not be comparable to, similarly titled measures used by other companies.

|

| | | | | | | | | | | | | | | | | | | |

| Calix, Inc. |

| Condensed Consolidated Statements of Operations |

| (Unaudited, in thousands, except per share data) |

| | | | | | | | | | | | |

| | | | | Three Months Ended | | Six Months Ended | |

| | | | | June 29, | | June 30, | | June 29, | | June 30, | |

| | | | | 2019 | | 2018 | | 2019 | | 2018 | |

| Revenue: | | | | | | | |

| | Systems | | $ | 92,833 |

| | $ | 102,563 |

| | $ | 175,193 |

| | $ | 195,854 |

| |

| | Services | | 7,471 |

| | 9,139 |

| | 14,461 |

| | 15,251 |

| |

| | | Total revenue | | 100,304 |

| | 111,702 |

| | 189,654 |

| | 211,105 |

| |

| Cost of revenue: | | | | | | | | | |

| | Systems (1) | | 49,561 |

| | 54,363 |

| | 94,162 |

| | 105,996 |

| |

| | Services (1) | | 6,075 |

| | 6,473 |

| | 12,481 |

| | 12,184 |

| |

| | | Total cost of revenue | | 55,636 |

| | 60,836 |

| | 106,643 |

| | 118,180 |

| |

| Gross profit | | 44,668 |

| | 50,866 |

| | 83,011 |

| | 92,925 |

| |

| Operating expenses: | | | | | | | | | |

| | Research and development (1) | | 20,700 |

| | 22,101 |

| | 40,030 |

| | 47,637 |

| |

| | Sales and marketing (1) | | 19,734 |

| | 20,527 |

| | 39,073 |

| | 40,428 |

| |

| | General and administrative (1) | | 9,165 |

| | 10,371 |

| | 17,952 |

| | 19,466 |

| |

| | Restructuring charges | | — |

| | 793 |

| | — |

| | 6,133 |

| |

| | Gain on sale of product line | | — |

| | — |

| | — |

| | (6,704 | ) | |

| | | Total operating expenses | | 49,599 |

| | 53,792 |

| | 97,055 |

| | 106,960 |

| |

| Loss from operations | | (4,931 | ) | | (2,926 | ) | | (14,044 | ) | | (14,035 | ) | |

| Interest and other income (expense), net: | | | | | | | | | |

| | Interest expense, net | | (142 | ) | | (165 | ) | | (250 | ) | | (388 | ) | |

| | Other income (expense), net | | 123 |

| | 456 |

| | (268 | ) | | 162 |

| |

| | | Total interest and other income (expense), net | | (19 | ) | | 291 |

| | (518 | ) | | (226 | ) | |

| Loss before provision for income taxes | | (4,950 | ) | | (2,635 | ) | | (14,562 | ) | | (14,261 | ) | |

| Provision for income taxes | | 95 |

| | 158 |

| | 250 |

| | 268 |

| |

| Net loss | | $ | (5,045 | ) | | $ | (2,793 | ) | | $ | (14,812 | ) | | $ | (14,529 | ) | |

| Net loss per common share: | | | | | | | | | |

| | | Basic and diluted | | $ | (0.09 | ) | | $ | (0.05 | ) | | $ | (0.27 | ) | | $ | (0.28 | ) | |

| Weighted average number of shares used to compute net loss per common share: | | | | | | | | |

| | | Basic and diluted | | 54,624 |

| | 52,290 |

| | 54,339 |

| | 51,952 |

| |

| | | | | | | | | | | | |

(1) | Includes stock-based compensation as follows: | | | | | | | | | |

| | Cost of revenue: | | | | | | | | | |

| | | Systems | | $ | 123 |

| | $ | 141 |

| | $ | 278 |

| | $ | 253 |

| |

| | | Services | | 93 |

| | 90 |

| | 192 |

| | 167 |

| |

| | Research and development | | 873 |

| | 814 |

| | 1,889 |

| | 1,797 |

| |

| | Sales and marketing | | 814 |

| | 785 |

| | 1,888 |

| | 1,635 |

| |

| | General and administrative | | 666 |

| | 714 |

| | 1,467 |

| | 1,449 |

| |

|

| | | | | | | | |

| Calix, Inc. |

| Condensed Consolidated Balance Sheets |

| (Unaudited, in thousands) |

| | | | | |

| | | June 29, | | December 31, |

| | | 2019 | | 2018 |

| ASSETS |

| Current assets: | | | | |

| Cash and cash equivalents | | $ | 34,942 |

| | $ | 49,646 |

|

| Restricted cash | | 628 |

| | 628 |

|

| Accounts receivable, net | | 60,186 |

| | 67,026 |

|

| Inventory | | 45,360 |

| | 50,151 |

|

| Prepaid expenses and other current assets | | 7,094 |

| | 7,306 |

|

| Total current assets | | 148,210 |

| | 174,757 |

|

| Property and equipment, net | | 29,105 |

| | 24,945 |

|

| Right-of-use operating leases | | 16,422 |

| | — |

|

| Goodwill | | 116,175 |

| | 116,175 |

|

| Other assets | | 1,336 |

| | 1,203 |

|

| | | $ | 311,248 |

| | $ | 317,080 |

|

| LIABILITIES AND STOCKHOLDERS’ EQUITY |

| Current liabilities: | | | | |

| Accounts payable | | $ | 37,522 |

| | $ | 40,209 |

|

| Accrued liabilities | | 47,657 |

| | 57,869 |

|

| Deferred revenue | | 18,528 |

| | 15,600 |

|

| Line of credit | | 25,000 |

| | 30,000 |

|

| Total current liabilities | | 128,707 |

| | 143,678 |

|

| Long-term portion of deferred revenue | | 17,792 |

| | 17,496 |

|

| Operating leases | | 15,045 |

| | — |

|

| Other long-term liabilities | | 2,498 |

| | 3,972 |

|

| Total liabilities | | 164,042 |

| | 165,146 |

|

| Stockholders’ equity: | | | | |

| Common stock | | 1,520 |

| | 1,482 |

|

| Additional paid-in capital | | 886,076 |

| | 876,073 |

|

| Accumulated other comprehensive loss | | (710 | ) | | (753 | ) |

| Accumulated deficit | | (699,694 | ) | | (684,882 | ) |

| Treasury stock | | (39,986 | ) | | (39,986 | ) |

| Total stockholders’ equity | | 147,206 |

| | 151,934 |

|

| | | $ | 311,248 |

| | $ | 317,080 |

|

|

| | | | | | | | |

| Calix, Inc. |

| Condensed Consolidated Statements of Cash Flows |

| (Unaudited, in thousands) |

| | | | | |

| | | Six Months Ended |

| | | June 29, | | June 30, |

| | | 2019 | | 2018 |

| Operating activities: | | | | |

| Net loss | | $ | (14,812 | ) | | $ | (14,529 | ) |

| Adjustments to reconcile net loss to net cash used in operating activities: | | | | |

| Stock-based compensation | | 5,714 |

| | 5,301 |

|

| Depreciation and amortization | | 4,644 |

| | 4,942 |

|

| Loss on retirement of property and equipment | | 138 |

| | 247 |

|

| Gain on sale of product line | | — |

| | (6,704 | ) |

| Changes in operating assets and liabilities: | | | | |

| Accounts receivable, net | | 6,840 |

| | 11,348 |

|

| Inventory | | 4,791 |

| | 9,524 |

|

| Prepaid expenses and other assets | | 1,697 |

| | (1,066 | ) |

| Accounts payable | | (2,676 | ) | | (10,315 | ) |

| Accrued liabilities | | (10,314 | ) | | (2,589 | ) |

| Deferred revenue | | 3,223 |

| | 1,180 |

|

| Other long-term liabilities | | (2,496 | ) | | (17 | ) |

| Net cash used in operating activities | | (3,251 | ) | | (2,678 | ) |

| Investing activities: | | | | |

| Purchases of property and equipment | | (9,538 | ) | | (2,955 | ) |

| Proceeds from sale of product line | | — |

| | 10,350 |

|

| Net cash provided by (used in) investing activities | | (9,538 | ) | | 7,395 |

|

| Financing activities: | | | | |

| Proceeds from exercise of stock options | | 326 |

| | 51 |

|

| Proceeds from employee stock purchase plans | | 4,157 |

| | 3,836 |

|

| Taxes paid for awards vested under equity incentive plan | | (156 | ) | | (7 | ) |

| Payments related to financing arrangements | | (1,267 | ) | | — |

|

| Proceeds from line of credit | | 89,000 |

| | 288,064 |

|

| Repayment of line of credit | | (94,000 | ) | | (288,064 | ) |

| Net cash provided by (used in) financing activities | | (1,940 | ) | | 3,880 |

|

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | | 25 |

| | (197 | ) |

| Net increase (decrease) in cash, cash equivalents and restricted cash | | (14,704 | ) | | 8,400 |

|

| Cash, cash equivalents and restricted cash at beginning of period | | 50,274 |

| | 39,775 |

|

| Cash, cash equivalents and restricted cash at end of period | | $ | 35,570 |

| | $ | 48,175 |

|

|

| | | | | | | | | | | | | | | | | | | | | | | |

| Calix, Inc. |

| Reconciliation of GAAP to Non-GAAP Results |

| (Unaudited, dollars in thousands, except per share data) |

| | | Three Months Ended

March 30, 2019 | | Three Months Ended

June 30, 2018 | | Three Months Ended December 31, 2018 | | | | | | | | |

| | | | | | Three Months Ended June 29, 2019 |

| | | Systems Gross Margin | | Systems Gross Margin | | Systems Gross Margin | | Gross Margin | | Systems Gross Margin | | Operating Expenses | | Net Loss Per Diluted Common Share |

| GAAP amount | | 45.8 | % | | 47.0 | % | | 46.5 | % | | 44.5 | % | | 46.6 | % | | $ | 49,599 |

| | $ | (0.09 | ) |

| Adjustments to GAAP amounts: | | | | | | | | | | | | | | |

| Stock-based compensation | | 0.2 |

| | 0.1 |

| | 0.5 |

| | 0.2 |

| | 0.1 |

| | (2,353 | ) | | 0.05 |

|

| U.S. tariff and tariff-related costs | | 2.6 |

| | — |

| | 3.0 |

| | 1.9 |

| | 2.0 |

| | — |

| | 0.03 |

|

| Non-GAAP amount | | 48.6 | % | | 47.1 | % | | 50.0 | % | | 46.6 | % | | 48.7 | % | | $ | 47,246 |

| | $ | (0.01 | ) |

| | | | | | | | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | |

| Calix, Inc. |

| Reconciliation of GAAP to Non-GAAP Results |

| (Unaudited, in thousands) |

| | | | |

| | | Three Months Ended | |

| | | June 29, | | March 30, | | December 31, | | September 29, | | June 30, | |

| | | 2019 | | 2019 | | 2018 | | 2018 | | 2018 | |

| GAAP net income (loss) | | $ | (5,045 | ) | | $ | (9,767 | ) | | $ | (5,578 | ) | | $ | 809 |

| | $ | (2,793 | ) | |

| Adjustments to GAAP amounts: | | | | | | | | | | | |

| Stock-based compensation | | 2,569 |

| | 3,145 |

| | 9,674 |

| | 2,499 |

| | 2,544 |

| |

| Restructuring charges (benefit) | | — |

| | — |

| | (271 | ) | | (157 | ) | | 793 |

| |

| U.S. tariff and tariff-related costs | | 1,855 |

| | 2,151 |

| | 3,195 |

| | — |

| | — |

| |

| Non-GAAP net income (loss) | | $ | (621 | ) | | $ | (4,471 | ) | | $ | 7,020 |

| | $ | 3,151 |

| | $ | 544 |

| |

| | | | | | | | | | | | |

|

| | | | | | | | |

| Calix, Inc. |

| Reconciliation of GAAP to Non-GAAP Guidance |

| (Unaudited, dollars in thousands, except per share data) |

| Three Months Ending September 28, 2019 |

| | | | | | | | | |

| Outlook | | GAAP | | Stock-Based Compensation | | U.S. Tariff and Tariff-related Costs | | Non-GAAP |

| Gross margin | | 44.2% - 46.2% | | 0.2% | | 0.6% | | 45.0% - 47.0% |

| Operating expenses | | $ 50,500 - $ 52,500 | | $ (2,500) | | $ - | | $ 48,000 - $ 50,000 |

Net income (loss) per diluted common share(1) | | $ (0.04) - $ 0.00 | | $ 0.05 | | $ 0.01 | | $ 0.02 - $ 0.06 |

(1) Based on 55.7 million weighted-average diluted common shares outstanding.