UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2015

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-36895

FRANKLIN FINANCIAL NETWORK, INC.

(Exact name of registrant as specified in its charter)

| | |

| Tennessee | | 20-8839445 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| |

722 Columbia Avenue Franklin, Tennessee | | 37064 |

| (Address of principal executive offices) | | (Zip Code) |

615-236-2265

(Registrant’s telephone number, including area code)

N/A

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | | | | |

| Large accelerated filer | | ¨ | | Accelerated filer | | ¨ |

| | | |

| Non-accelerated filer | | ¨ (Do not check if a smaller reporting company) | | Smaller reporting company | | x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The number of shares outstanding of the registrant’s common stock, no par value per share, as of November 9, 2015, was 10,525,680.

TABLE OF CONTENTS

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains “forward-looking statements” as defined under U.S. federal securities laws. These statements reflect management’s current knowledge, assumptions, beliefs, estimates, and expectations and express management’s current views of future performance, results, and trends and may be identified by their use of terms such as “may,” “would,” “could,” “should,” “will,” “expect,” “anticipate,” “predict,” “project,” “potential,” “continue,” “contemplate,” “seek,” “assume,” “believe,” “intend,” “plan,” “forecast,” “goal,” and “estimate,” and other similar terms. Forward-looking statements are subject to a number of risks and uncertainties that could cause our actual results to differ materially from those described in the forward-looking statements. Readers should not place undue reliance on forward-looking statements. Such statements are made as of the date of this Quarterly Report on Form 10-Q, and we undertake no obligation to update such statements after this date.

Risks and uncertainties that could cause our actual results to differ materially from those described in forward-looking statements include those discussed in our filings with the Securities and Exchange Commission (“SEC”), including those described in our prospectus filed with the SEC pursuant to Rule 424(b) under the Securities Act of 1933, as amended (the “Securities Act”), on March 27, 2015 (the “Prospectus”) and those described in Item 1A of Part II of our Quarterly Reports on Form 10-Q for the quarters ended March 31, 2015 and June 30, 2015 and Part II of this Quarterly Report on Form 10-Q.

1

PART I FINANCIAL INFORMATION

ITEM 1. CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FRANKLIN FINANCIAL NETWORK, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

September 30, 2015 and December 31, 2014

(Dollar amounts in thousands, except share and per share data)

| | | | | | | | |

| | | September 30,

2015 | | | December 31,

2014 | |

| | | (Unaudited) | | | | |

ASSETS | | | | | | | | |

Cash and due from financial institutions | | $ | 47,658 | | | $ | 49,347 | |

Certificates of deposit at other financial institutions | | | 250 | | | | 250 | |

Securities available for sale | | | 624,420 | | | | 395,705 | |

Securities held to maturity (fair value 2015—$134,028 and 2014—$53,741) | | | 132,134 | | | | 53,332 | |

Loans held for sale, at fair value | | | 14,666 | | | | 18,462 | |

Loans | | | 1,123,826 | | | | 787,188 | |

Allowance for loan losses | | | (9,744 | ) | | | (6,680 | ) |

| | | | | | | | |

Net loans | | | 1,114,082 | | | | 780,508 | |

| | | | | | | | |

Restricted equity securities, at cost | | | 7,691 | | | | 5,349 | |

Premises and equipment, net | | | 9,360 | | | | 9,664 | |

Accrued interest receivable | | | 6,108 | | | | 3,545 | |

Bank owned life insurance | | | 22,452 | | | | 11,664 | |

Deferred tax asset | | | 5,980 | | | | 6,780 | |

Buildings held for sale | | | — | | | | 4,080 | |

Foreclosed assets | | | 206 | | | | 715 | |

Servicing rights, net | | | 3,415 | | | | 3,053 | |

Goodwill | | | 9,124 | | | | 9,124 | |

Core deposit intangible, net | | | 2,199 | | | | 2,698 | |

Other assets | | | 2,793 | | | | 1,551 | |

| | | | | | | | |

Total assets | | $ | 2,002,538 | | | $ | 1,355,827 | |

| | | | | | | | |

LIABILITIES AND SHAREHOLDERS’ EQUITY | | | | | | | | |

Deposits | | | | | | | | |

Non-interest bearing | | $ | 177,452 | | | $ | 150,337 | |

Interest bearing | | | 1,537,142 | | | | 1,021,896 | |

| | | | | | | | |

Total deposits | | | 1,714,594 | | | | 1,172,233 | |

Federal funds purchased and repurchase agreements | | | 37,618 | | | | 39,078 | |

Federal Home Loan Bank advances | | | 57,000 | | | | 19,000 | |

Accrued interest payable | | | 587 | | | | 421 | |

Other liabilities | | | 5,129 | | | | 3,296 | |

| | | | | | | | |

Total liabilities | | | 1,814,928 | | | | 1,234,028 | |

Shareholders’ equity | | | | | | | | |

Senior non-cumulative preferred stock, no par value, $10,000 liquidation value: Series A, 1,000,000 shares authorized; 10,000 shares issued and outstanding at September 30, 2015 and December 31, 2014, respectively | | | 10,000 | | | | 10,000 | |

Common stock, no par value; 20,000,000 shares authorized; 10,524,630 and 7,756,411 shares issued and outstanding at September 30, 2015 and December 31 2014, respectively | | | 146,645 | | | | 94,251 | |

Retained earnings | | | 26,713 | | | | 15,372 | |

Accumulated other comprehensive income | | | 4,252 | | | | 2,176 | |

| | | | | | | | |

Total shareholders’ equity | | | 187,610 | | | | 121,799 | |

| | | | | | | | |

Total liabilities and shareholders’ equity | | $ | 2,002,538 | | | $ | 1,355,827 | |

| | | | | | | | |

See accompanying notes to condensed consolidated financial statements.

2

FRANKLIN FINANCIAL NETWORK, INC.

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

Three and Nine Months Ended September 30, 2015 and 2014

(Dollar amounts in thousands, except share and per share data)

(Unaudited)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Interest income and dividends | | | | | | | | | | | | | | | | |

Loans, including fees | | $ | 14,744 | | | $ | 10,168 | | | $ | 38,071 | | | $ | 22,466 | |

Securities: | | | | | | | | | | | | | | | | |

Taxable | | | 3,462 | | | | 2,395 | | | | 9,084 | | | | 6,932 | |

Tax-exempt | | | 966 | | | | 20 | | | | 1,155 | | | | 60 | |

Dividends on restricted equity securities | | | 100 | | | | 84 | | | | 250 | | | | 175 | |

Federal funds sold and other | | | 29 | | | | 25 | | | | 80 | | | | 57 | |

| | | | | | | | | | | | | | | | |

Total interest income | | | 19,301 | | | | 12,692 | | | | 48,640 | | | | 29,690 | |

| | | | | | | | | | | | | | | | |

Interest expense | | | | | | | | | | | | | | | | |

Deposits | | | 2,417 | | | | 1,446 | | | | 5,963 | | | | 3,808 | |

Federal funds purchased and repurchase agreements | | | 69 | | | | 39 | | | | 232 | | | | 123 | |

Federal Home Loan Bank advances | | | 79 | | | | 80 | | | | 225 | | | | 189 | |

| | | | | | | | | | | | | | | | |

Total interest expense | | | 2,565 | | | | 1,565 | | | | 6,420 | | | | 4,120 | |

| | | | | | | | | | | | | | | | |

Net interest income | | | 16,736 | | | | 11,127 | | | | 42,220 | | | | 25,570 | |

Provision for loan losses | | | 1,724 | | | | 664 | | | | 3,154 | | | | 1,489 | |

| | | | | | | | | | | | | | | | |

Net interest income after provision for loan losses | | | 15,012 | | | | 10,463 | | | | 39,066 | | | | 24,081 | |

| | | | | | | | | | | | | | | | |

Noninterest income | | | | | | | | | | | | | | | | |

Service charges on deposit accounts | | | 44 | | | | 13 | | | | 78 | | | | 37 | |

Other service charges and fees | | | 679 | | | | 600 | | | | 1,987 | | | | 1,149 | |

Net gains on sale of loans | | | 2,463 | | | | 1,875 | | | | 5,573 | | | | 4,226 | |

Loan servicing fees, net of amortization of servicing assets | | | 84 | | | | 73 | | | | 187 | | | | 173 | |

Gain on sales and calls of securities | | | 5 | | | | 22 | | | | 529 | | | | 93 | |

Net gain (loss) on foreclosed assets | | | 3 | | | | (3 | ) | | | 30 | | | | 28 | |

Wealth management | | | 327 | | | | 287 | | | | 914 | | | | 364 | |

Other | | | 193 | | | | 407 | | | | 566 | | | | 1,055 | |

| | | | | | | | | | | | | | | | |

Total noninterest income | | | 3,798 | | | | 3,274 | | | | 9,864 | | | | 7,125 | |

| | | | | | | | | | | | | | | | |

Noninterest expense | | | | | | | | | | | | | | | | |

Salaries and employee benefits | | | 6,208 | | | | 6,144 | | | | 17,960 | | | | 13,494 | |

Occupancy and equipment | | | 1,683 | | | | 1,443 | | | | 4,961 | | | | 3,238 | |

FDIC assessment expense | | | 362 | | | | 181 | | | | 792 | | | | 420 | |

Marketing | | | 277 | | | | 224 | | | | 695 | | | | 470 | |

Professional fees | | | 516 | | | | 961 | | | | 1,382 | | | | 1,594 | |

Amortization of core deposit intangible | | | 160 | | | | 184 | | | | 499 | | | | 184 | |

Indirect expenses related to public offering | | | — | | | | — | | | | 314 | | | | — | |

Other | | | 1,647 | | | | 1,252 | | | | 4,443 | | | | 2,559 | |

| | | | | | | | | | | | | | | | |

Total noninterest expense | | | 10,853 | | | | 10,389 | | | | 31,046 | | | | 21,959 | |

| | | | | | | | | | | | | | | | |

Income before income tax expense | | | 7,957 | | | | 3,348 | | | | 17,884 | | | | 9,247 | |

Income tax expense | | | 2,807 | | | | 1,333 | | | | 6,468 | | | | 3,668 | |

| | | | | | | | | | | | | | | | |

Net income | | | 5,150 | | | | 2,015 | | | | 11,416 | | | | 5,579 | |

Dividends paid on Series A preferred stock | | | (25 | ) | | | (25 | ) | | | (75 | ) | | | (75 | ) |

| | | | | | | | | | | | | | | | |

Net income available to common shareholders | | $ | 5,125 | | | $ | 1,990 | | | $ | 11,341 | | | $ | 5,504 | |

| | | | | | | | | | | | | | | | |

Earnings per share: | | | | | | | | | | | | | | | | |

Basic | | $ | 0.49 | | | $ | 0.26 | | | $ | 1.17 | | | $ | 0.94 | |

Diluted | | | 0.46 | | | | 0.25 | | | | 1.12 | | | | 0.91 | |

See accompanying notes to condensed consolidated financial statements.

3

FRANKLIN FINANCIAL NETWORK, INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

Three and Nine Months Ended September 30, 2015 and 2014

(Dollar amounts in thousands, except share and per share data)

(Unaudited)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Net income | | $ | 5,150 | | | $ | 2,015 | | | $ | 11,416 | | | $ | 5,579 | |

Other comprehensive income (loss), net of tax: | | | | | | | | | | | | | | | | |

Unrealized gains/losses on securities: | | | | | | | | | | | | | | | | |

Unrealized holding gain (loss) arising during the period | | | 7,871 | | | | (623 | ) | | | 4,006 | | | | 7,445 | |

Reclassification adjustment for gains included in net income | | | (5 | ) | | | (22 | ) | | | (529 | ) | | | (93 | ) |

| | | | | | | | | | | | | | | | |

Net unrealized gains (losses) | | | 7,866 | | | | (645 | ) | | | 3,477 | | | | 7,352 | |

Tax effect | | | (3,090 | ) | | | 247 | | | | (1,401 | ) | | | (2,815 | ) |

| | | | | | | | | | | | | | | | |

Total other comprehensive income (loss) | | | 4,776 | | | | (398 | ) | | | 2,076 | | | | 4,537 | |

| | | | | | | | | | | | | | | | |

Comprehensive income | | $ | 9,926 | | | $ | 1,617 | | | $ | 13,492 | | | $ | 10,116 | |

| | | | | | | | | | | | | | | | |

See accompanying notes to condensed consolidated financial statements.

4

FRANKLIN FINANCIAL NETWORK, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

Nine Months Ended September 30, 2015 and 2014

(Dollar amounts in thousands, except share and per share data)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Preferred

| | | Common Stock | | | Retained

| | | Accumulated

Other

Comprehensive

| | | Total

Shareholders’

| |

| | | Stock | | | Shares | | | Amount | | | Earnings | | | Income (Loss) | | | Equity | |

Balance at December 31, 2013 | | $ | 10,000 | | | | 4,862,875 | | | $ | 52,638 | | | $ | 7,058 | | | $ | (4,533 | ) | | $ | 65,163 | |

Exercise of common stock options | | | — | | | | 6,508 | | | | 56 | | | | — | | | | — | | | | 56 | |

Dividends paid on Series A preferred stock | | | — | | | | — | | | | — | | | | (75 | ) | | | — | | | | (75 | ) |

Issuance of restricted stock, net of forfeitures | | | — | | | | 83,725 | | | | — | | | | — | | | | — | | | | — | |

Stock based compensation expense | | | — | | | | — | | | | 457 | | | | — | | | | — | | | | 457 | |

Stock issued in conjunction with 401(k) employer match | | | — | | | | 20,345 | | | | 275 | | | | — | | | | — | | | | 275 | |

Stock and stock options (137,280 options) issued related to MidSouth Bank acquisition, net of stock issuance costs of $514 | | | | | | | 2,766,191 | | | | 40,462 | | | | | | | | | | | | 40,462 | |

Net income | | | — | | | | — | | | | — | | | | 5,579 | | | | — | | | | 5,579 | |

Other comprehensive income | | | — | | | | — | | | | — | | | | — | | | | 4,537 | | | | 4,537 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Balance at September 30, 2014 | | $ | 10,000 | | | | 7,739,644 | | | $ | 93,888 | | | $ | 12,562 | | | $ | 4 | | | $ | 116,454 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

Balance at December 31, 2014 | | $ | 10,000 | | | | 7,756,411 | | | $ | 94,251 | | | $ | 15,372 | | | $ | 2,176 | | | $ | 121,799 | |

Exercise of common stock options | | | — | | | | 80,331 | | | | 780 | | | | — | | | | — | | | | 780 | |

Exercise of common stock warrants | | | — | | | | 4,970 | | | | 60 | | | | — | | | | — | | | | 60 | |

Dividends paid on Series A preferred stock | | | — | | | | — | | | | — | | | | (75 | ) | | | — | | | | (75 | ) |

Issuance of restricted stock, net of forfeitures | | | | | | | 28,229 | | | | — | | | | — | | | | — | | | | — | |

Stock based compensation expense, net of forfeitures | | | — | | | | — | | | | 619 | | | | — | | | | — | | | | 619 | |

Stock issued related to initial public offering, net of stock issuance costs of $5,017 | | | — | | | | 2,640,000 | | | | 50,423 | | | | — | | | | — | | | | 50,423 | |

Stock issued in conjunction with 401(k) employer match, net of distributions | | | — | | | | 14,689 | | | | 365 | | | | — | | | | — | | | | 365 | |

Excess tax benefit from exercise of stock options | | | — | | | | — | | | | 147 | | | | — | | | | — | | | | 147 | |

Net income | | | — | | | | — | | | | — | | | | 11,416 | | | | — | | | | 11,416 | |

Other comprehensive income | | | — | | | | — | | | | — | | | | — | | | | 2,076 | | | | 2,076 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Balance at September 30, 2015 | | $ | 10,000 | | | | 10,524,630 | | | $ | 146,645 | | | $ | 26,713 | | | $ | 4,252 | | | $ | 187,610 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

See accompanying notes to condensed consolidated financial statements.

5

FRANKLIN FINANCIAL NETWORK, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

Nine Months Ended September 30, 2015 and 2014

(Dollar amounts in thousands, except share and per share data)

(Unaudited)

| | | | | | | | |

| | | Nine Months Ended

September 30, | |

| | | 2015 | | | 2014 | |

Cash flows from operating activities | | | | | | | | |

Net income | | $ | 11,416 | | | $ | 5,579 | |

Adjustments to reconcile net income to net cash from operating activities | | | | | | | | |

Depreciation and amortization on premises and equipment | | | 996 | | | | 616 | |

Accretion of purchase accounting adjustments | | | (1,551 | ) | | | (831 | ) |

Net amortization of securities | | | 3,426 | | | | 1,928 | |

Amortization of loan servicing right asset | | | 644 | | | | 547 | |

Amortization of core deposit intangible | | | 499 | | | | 184 | |

Provision for loan losses | | | 3,154 | | | | 1,489 | |

Excess tax benefit related to the exercise of stock options | | | (147 | ) | | | — | |

Origination of loans held for sale | | | (236,831 | ) | | | (191,142 | ) |

Proceeds from sale of loans held for sale | | | 245,194 | | | | 186,618 | |

Net gain on sale of loans | | | (5,573 | ) | | | (4,226 | ) |

Gain on sale of available for sale securities | | | (380 | ) | | | (93 | ) |

Gain on call of held to maturity securities | | | (149 | ) | | | — | |

Income from bank owned life insurance | | | (444 | ) | | | (203 | ) |

(Gain) loss on sale of foreclosed assets | | | (22 | ) | | | (28 | ) |

Stock-based compensation expense | | | 619 | | | | 457 | |

Compensation expense related to common stock issued to 401(k) plan | | | 356 | | | | 294 | |

Recognition of deferred gain on sale of loans | | | (27 | ) | | | (31 | ) |

Recognition of deferred gain on sale of foreclosed assets | | | (8 | ) | | | (2 | ) |

Net change in: | | | | | | | | |

Accrued interest receivable and other assets | | | (4,406 | ) | | | 101 | |

Accrued interest payable and other liabilities | | | 2,190 | | | | (705 | ) |

| | | | | | | | |

| | |

Net cash from operating activities | | | 18,956 | | | | 552 | |

Cash flows from investing activities | | | | | | | | |

Available for sale securities: | | | | | | | | |

Sales | | | 52,064 | | | | 34,087 | |

Purchases | | | (467,067 | ) | | | (118,611 | ) |

Maturities, prepayments and calls | | | 187,222 | | | | 69,465 | |

Held to maturity securities: | | | | | | | | |

Purchases | | | (88,550 | ) | | | (8,601 | ) |

Maturities, prepayments and calls | | | 9,394 | | | | 8,655 | |

Net change in loans | | | (335,238 | ) | | | (114,676 | ) |

Purchase of bank owned life insurance | | | (10,344 | ) | | | — | |

Proceeds from sale of buildings held for sale | | | 4,080 | | | | — | |

Purchase of restricted equity securities | | | (2,342 | ) | | | (745 | ) |

Proceeds from sale of foreclosed assets | | | 531 | | | | 634 | |

Purchases of premises and equipment, net | | | (692 | ) | | | (2,941 | ) |

Net cash received from acquisition | | | — | | | | 12,197 | |

| | | | | | | | |

| | |

Net cash from investing activities | | | (650,942 | ) | | | (120,536 | ) |

Cash flows from financing activities | | | | | | | | |

Increase in deposits | | | 542,422 | | | | 125,903 | |

Increase (decrease) in federal funds purchased and repurchase agreements | | | (1,460 | ) | | | 9,054 | |

Proceeds from Federal Home Loan Bank advances | | | 157,000 | | | | 15,000 | |

Repayment of Federal Home Loan Bank advances | | | (119,000 | ) | | | (11,000 | ) |

Proceeds from exercise of common stock warrants | | | 60 | | | | — | |

Proceeds from exercise of common stock options, including excess tax benefit | | | 927 | | | | 56 | |

Proceeds from issuance of common stock, net of offering costs | | | 50,423 | | | | (514 | ) |

Dividends paid on preferred stock | | | (75 | ) | | | (75 | ) |

| | | | | | | | |

| | |

Net cash from financing activities | | | 630,297 | | | | 138,424 | |

| | | | | | | | |

| | |

Net change in cash and cash equivalents | | | (1,689 | ) | | | 18,440 | |

Cash and cash equivalents at beginning of period | | | 49,347 | | | | 18,217 | |

| | | | | | | | |

| | |

Cash and cash equivalents at end of period | | $ | 47,658 | | | $ | 36,657 | |

| | | | | | | | |

| | |

Supplemental information: | | | | | | | | |

Interest paid | | $ | 6,254 | | | $ | 3,905 | |

Income taxes paid | | | 6,339 | | | | 4,546 | |

Non-cash supplemental information: | | | | | | | | |

Transfers from loans to foreclosed assets | | $ | — | | | $ | 1,315 | |

Fair value of stock and stock options issued related to MidSouth Bank acquisition | | $ | — | | | $ | 40,976 | |

See accompanying notes to condensed consolidated financial statements.

6

FRANKLIN FINANCIAL NETWORK, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Dollar amounts in thousands, except share and per share data)

(Unaudited)

NOTE 1—BASIS OF PRESENTATION

The accompanying unaudited consolidated financial statements of Franklin Financial Network, Inc. (“FFN”), and its wholly owned subsidiaries, Franklin Synergy Bank and BCG Consulting Group, Inc. (“BCG”), together referred to as “the Company,” have been prepared in accordance with instructions to Form 10-Q and therefore do not include all information and footnotes necessary for a fair presentation of financial position, results of operations, and cash flows in conformity with U.S. generally accepted accounting principles (U.S. GAAP). All adjustments which are, in the opinion of management, necessary for a fair presentation of the results for the periods reported have been included as required by Regulation S-X, Rule 10-01. All such adjustments are of a normal recurring nature. It is suggested that these interim consolidated financial statements and notes be read in conjunction with the financial statements and accompanying notes included in the Company’s Annual Report on Form 10-K filed with the SEC on March 11, 2015.

NOTE 2—ACQUISITIONS

Acquisition of MidSouth Bank

On July 1, 2014 the Company completed the acquisition of MidSouth Bank (“MidSouth”), pursuant to the terms of the Agreement and Plan of Reorganization and Bank Merger (the “merger agreement”) dated November 19, 2013.

The acquisition was accounted for under the acquisition method of accounting in accordance with ASC Topic 805,Business Combinations. The Company recognized goodwill on this acquisition of $9,124, which is nondeductible for tax purposes as this acquisition was a nontaxable transaction. The goodwill was calculated based on the fair values of the assets acquired and liabilities assumed as of the acquisition date.

At September 30, 2015, there were no circumstances or significant changes that have occurred since July 1, 2014 related to the acquisition of MidSouth that, in management’s assessment, would necessitate recording impairment of goodwill.

In the acquisition, the Company purchased $184,345 of loans at fair value, net of $7,347, or 3.8%, estimated discount to the outstanding principal balance, representing 38.0% of the Company’s total loans at September 30, 2014. Of the total loans acquired, management identified loans totaling $5,527 as having credit deficiencies. All loans that were on non-accrual status and all loan relationships that were identified as substandard or impaired as of the acquisition date were considered by management to be credit-impaired and are accounted for pursuant to ASC Topic 310-30. The table below summarizes the total contractually required principal and interest cash payments, management’s estimate of expected total cash payments and fair value of the loans as of July 1, 2014 for purchased credit-impaired (“PCI”) loans. Contractually required principal and interest payments have been adjusted for estimated prepayments.

| | | | |

Contractually required principal and interest | | $ | 8,510 | |

Non-accretable difference | | | (1,745 | ) |

| | | | |

Cash flows expected to be collected | | | 6,765 | |

Accretable yield | | | (1,238 | ) |

| | | | |

Total purchased credit-impaired loans acquired | | $ | 5,527 | |

| | | | |

In its assumption of the deposit liabilities, the Company believed the deposits assumed from the acquisition had an intangible value. The Company applied ASC Topic 805, which prescribes the accounting for goodwill and other intangible assets such as core deposit intangibles, in a business combination. The Company determined the estimated fair value of the core deposit intangible asset totaled $3,060, which is being amortized utilizing an accelerated amortization method over an estimated economic life of 8.2 years. Through September 30, 2015, the Company has recorded amortization of core deposit intangibles totaling $861.

7

Pro forma information

Pro forma data for the nine-month period ended September 30, 2014 listed in the table below presents pro forma information as if the MidSouth acquisition occurred at the beginning of 2014. Because the MidSouth transaction closed on July 1, 2014, and its actual results are included in the Company’s actual operating results for the three-month periods ended September 30, 2014 and 2015 and for the nine-month period ended September 30, 2015, there is no pro forma information for those periods.

| | | | |

| | | Nine Months Ended

Sept 30, 2014 | |

Net interest income | | $ | 31,619 | |

Net income available to common shareholders | | | 6,353 | |

| |

Earnings per share—basic | | $ | 0.82 | |

Earnings per share—diluted | | $ | 0.80 | |

Supplemental pro forma earnings for the nine months ended September 30, 2014 were adjusted to exclude acquisition-related costs that were incurred during the nine months ended September 30, 2014 of $2,112. Supplemental pro forma earnings for the nine months ended September 30, 2014 were adjusted to include discount accretion and premium amortization related to the fair value adjustments to acquisition date assets and liabilities, as appropriate.

During the nine months ended September 30, 2014, the acquisition of MidSouth increased pro forma net interest income by approximately $6,049 and net income available to common shareholders by approximately $849.

NOTE 3—SECURITIES

The following table summarizes the amortized cost and fair value of the available for sale securities portfolio at September 30, 2015 and December 31, 2014 and the corresponding amounts of gross unrealized gains and losses recognized in accumulated other comprehensive income.

| | | | | | | | | | | | | | | | |

| | | Amortized

Cost | | | Gross

Unrealized

Gains | | | Gross

Unrealized

Losses | | | Fair

Value | |

September 30, 2015 | | | | | | | | | | | | | | | | |

U.S. government sponsored entities and agencies | | $ | 14,211 | | | $ | 253 | | | $ | (46 | ) | | $ | 14,418 | |

Mortgage-backed securities: residential | | | 508,817 | | | | 6,868 | | | | (1,086 | ) | | | 514,599 | |

Mortgage-backed securities: commercial | | | 20,169 | | | | 161 | | | | — | | | | 20,330 | |

State and political subdivisions | | | 74,220 | | | | 896 | | | | (43 | ) | | | 75,073 | |

| | | | | | | | | | | | | | | | |

Total | | $ | 617,417 | | | $ | 8,178 | | | $ | (1,175 | ) | | $ | 624,420 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| | | Amortized

Cost | | | Gross

Unrealized

Gains | | | Gross

Unrealized

Losses | | | Fair

Value | |

December 31, 2014 | | | | | | | | | | | | | | | | |

U.S. government sponsored entities and agencies | | $ | 30,070 | | | $ | 417 | | | $ | (314 | ) | | $ | 30,173 | |

U.S. Treasury securities | | | 20,000 | | | | — | | | | — | | | | 20,000 | |

Mortgage-backed securities: residential | | | 335,677 | | | | 4,593 | | | | (1,203 | ) | | | 339,067 | |

Mortgage-backed securities: commercial | | | 6,432 | | | | 33 | | | | — | | | | 6,465 | |

| | | | | | | | | | | | | | | | |

Total | | $ | 392,179 | | | $ | 5,043 | | | $ | (1,517 | ) | | $ | 395,705 | |

| | | | | | | | | | | | | | | | |

The amortized cost and fair value of the held to maturity securities portfolio at September 30, 2015 and December 31, 2014 and the corresponding amounts of gross unrecognized gains and losses were as follows:

| | | | | | | | | | | | | | | | |

| | | Amortized

Cost | | | Gross

Unrecognized

Gains | | | Gross

Unrecognized

Losses | | | Fair

Value | |

September 30, 2015 | | | | | | | | | | | | | | | | |

U.S. government sponsored entities and agencies | | $ | 3,301 | | | $ | 13 | | | $ | (42 | ) | | $ | 3,272 | |

Mortgage backed securities: residential | | | 31,691 | | | | 658 | | | | (318 | ) | | | 32,031 | |

State and political subdivisions | | | 97,142 | | | | 1,605 | | | | (22 | ) | | | 98,725 | |

| | | | | | | | | | | | | | | | |

Total | | $ | 132,134 | | | $ | 2,276 | | | $ | (382 | ) | | $ | 134,028 | |

| | | | | | | | | | | | | | | | |

8

| | | | | | | | | | | | | | | | |

| | | Gross

Amortized

Cost | | | Gross

Unrecognized

Gains | | | Gross

Unrecognized

Losses | | | Fair

Value | |

December 31, 2014 | | | | | | | | | | | | | | | | |

U.S. government sponsored entities and agencies | | $ | 5,550 | | | $ | 162 | | | $ | (87 | ) | | $ | 5,625 | |

Mortgage backed securities: residential | | | 38,587 | | | | 555 | | | | (562 | ) | | | 38,580 | |

State and political subdivisions | | | 9,195 | | | | 351 | | | | (10 | ) | | | 9,536 | |

| | | | | | | | | | | | | | | | |

Total | | $ | 53,332 | | | $ | 1,068 | | | $ | (659 | ) | | $ | 53,741 | |

| | | | | | | | | | | | | | | | |

Sales and calls of available for sale securities were as follows:

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Proceeds | | $ | 19,776 | | | $ | 9,767 | | | $ | 54,064 | | | $ | 34,087 | |

Gross gains | | | 95 | | | | 31 | | | | 485 | | | | 256 | |

Gross losses | | | (90 | ) | | | (9 | ) | | | (105 | ) | | | (163 | ) |

Calls of held to maturity securities were as follows:

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Proceeds | | $ | — | | | $ | — | | | $ | 2,300 | | | $ | — | |

Gross gains | | | — | | | | — | | | | 149 | | | | — | |

Gross losses | | | — | | | | — | | | | — | | | | — | |

The amortized cost and fair value of the investment securities portfolio are shown by contractual maturity. Securities not due at a single maturity date, primarily mortgage-backed securities, are shown separately.

| | | | | | | | |

| | | September 30, 2015 | |

| | | Amortized

Cost | | | Fair

Value | |

Available for sale | | | | | | | | |

Three months or less | | $ | — | | | $ | — | |

Over three months through one year | | | — | | | | — | |

Over one year through five years | | | — | | | | — | |

Over five years through ten years | | | 7,761 | | | | 8,009 | |

Over ten years | | | 80,670 | | | | 81,482 | |

Mortgage-backed securities: residential | | | 508,817 | | | | 514,599 | |

Mortgage-backed securities: commercial | | | 20,169 | | | | 20,330 | |

| | | | | | | | |

Total | | $ | 617,417 | | | $ | 624,420 | |

| | | | | | | | |

Held to maturity | | | | | | | | |

Three months or less | | $ | — | | | $ | — | |

Over three months through one year | | | — | | | | — | |

Over one year through five years | | | 1,307 | | | | 1,366 | |

Over five years through ten years | | | 3,024 | | | | 3,091 | |

Over ten years | | | 96,112 | | | | 97,540 | |

Mortgage-backed securities: residential | | | 31,691 | | | | 32,031 | |

| | | | | | | | |

Total | | $ | 132,134 | | | $ | 134,028 | |

| | | | | | | | |

Securities pledged at September 30, 2015 and December 31, 2014 had a carrying amount of $467,080 and $366,764 and were pledged to secure public deposits and repurchase agreements.

At September 30, 2015 and December 31, 2014, there were no holdings of securities of any one issuer, other than the U.S. government-sponsored entities and agencies, in an amount greater than 10% of shareholders’ equity.

9

The following table summarizes the securities with unrealized and unrecognized losses at September 30, 2015 and December 31, 2014, aggregated by major security type and length of time in a continuous unrealized loss position:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Less Than 12 Months | | | 12 Months or Longer | | | Total | |

| | | Fair

Value | | | Unrealized

Losses | | | Fair

Value | | | Unrealized

Losses | | | Fair

Value | | | Unrealized

Losses | |

September 30, 2015 | | | | | | | | | | | | | | | | | | | | | | | | |

Available for sale | | | | | | | | | | | | | | | | | | | | | | | | |

U.S. government sponsored entities and agencies | | $ | — | | | $ | — | | | $ | 1,654 | | | $ | (46 | ) | | $ | 1,654 | | | $ | (46 | ) |

Mortgage-backed securities: residential | | | 77,224 | | | | (620 | ) | | | 26,253 | | | | (466 | ) | | | 103,477 | | | | (1,086 | ) |

State and political subdivisions | | | 2,981 | | | | (43 | ) | | | — | | | | — | | | | 2,981 | | | | (43 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total available for sale | | $ | 80,205 | | | $ | (663 | ) | | $ | 27,907 | | | $ | (512 | ) | | $ | 108,112 | | | $ | (1,175 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| | | Less Than 12 Months | | | 12 Months or Longer | | | Total | |

| | | Fair

Value | | | Unrecognized

Losses | | | Fair

Value | | | Unrecognized

Losses | | | Fair

Value | | | Unrecognized

Losses | |

Held to maturity | | | | | | | | | | | | | | | | | | | | | | | | |

U.S. government sponsored entities and agencies | | $ | 1,979 | | | $ | (21 | ) | | $ | 979 | | | $ | (21 | ) | | $ | 2,958 | | | $ | (42 | ) |

Mortgage-backed securities: residential | | | 1,800 | | | | (6 | ) | | | 5,690 | | | | (312 | ) | | | 7,490 | | | | (318 | ) |

State and political subdivisions | | | 4,671 | | | | (22 | ) | | | — | | | | — | | | | 4,671 | | | | (22 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total held to maturity | | $ | 8,450 | | | $ | (49 | ) | | $ | 6,669 | | | $ | (333 | ) | | $ | 15,119 | | | $ | (382 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| | | Less Than 12 Months | | | 12 Months or Longer | | | Total | |

| | | Fair

Value | | | Unrealized

Losses | | | Fair

Value | | | Unrealized

Losses | | | Fair

Value | | | Unrealized

Losses | |

December 31, 2014 | | | | | | | | | | | | | | | | | | | | | | | | |

Available for sale | | | | | | | | | | | | | | | | | | | | | | | | |

U.S. government sponsored entities and agencies | | $ | 9,999 | | | $ | (1 | ) | | $ | 8,232 | | | $ | (313 | ) | | $ | 18,231 | | | $ | (314 | ) |

Mortgage-backed securities: residential | | | 59,078 | | | | (323 | ) | | | 41,939 | | | | (880 | ) | | | 101,017 | | | | (1,203 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total available for sale | | $ | 69,077 | | | $ | (324 | ) | | $ | 50,171 | | | $ | (1,193 | ) | | $ | 119,248 | | | $ | (1,517 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| | | Less Than 12 Months | | | 12 Months or Longer | | | Total | |

| | | Fair

Value | | | Unrecognized

Losses | | | Fair

Value | | | Unrecognized

Losses | | | Fair

Value | | | Unrecognized

Losses | |

Held to maturity | | | | | | | | | | | | | | | | | | | | | | | | |

U.S. government sponsored entities and agencies | | $ | — | | | $ | — | | | $ | 2,913 | | | $ | (87 | ) | | $ | 2,913 | | | $ | (87 | ) |

Mortgage-backed securities: residential | | | 5,246 | | | | (25 | ) | | | 13,001 | | | | (537 | ) | | | 18,247 | | | | (562 | ) |

State and political subdivisions | | | 507 | | | | (1 | ) | | | 592 | | | | (9 | ) | | | 1,099 | | | | (10 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total held to maturity | | $ | 5,753 | | | $ | (26 | ) | | $ | 16,506 | | | $ | (633 | ) | | $ | 22,259 | | | $ | (659 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Unrealized losses on debt securities have not been recognized into income because the issuers bonds are of high credit quality (rated AA or higher), management does not intend to sell and it is likely that management will not be required to sell the securities prior to their anticipated recovery, and the decline in fair value is largely due to changes in interest rates and other market conditions. The fair value is expected to recover as the bonds approach maturity.

10

NOTE 4—LOANS

Loans at September 30, 2015 and December 31, 2014 were as follows:

| | | | | | | | |

| | | September 30,

2015 | | | December 31,

2014 | |

Loans that are not PCI loans | | | | | | | | |

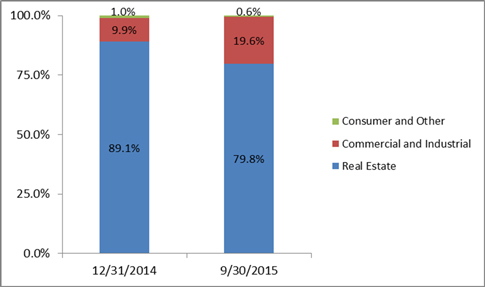

Construction and land development | | $ | 334,208 | | | $ | 239,225 | |

Commercial real estate: | | | | | | | | |

Nonfarm, nonresidential | | | 303,657 | | | | 240,975 | |

Other | | | 9,478 | | | | 5,377 | |

Residential real estate: | | | | | | | | |

Closed-end 1-4 family | | | 144,080 | | | | 130,631 | |

Other | | | 104,371 | | | | 83,129 | |

Commercial and industrial | | | 219,341 | | | | 76,570 | |

Consumer and other | | | 6,893 | | | | 8,025 | |

| | | | | | | | |

Loans before net deferred loan fees | | | 1,122,028 | | | | 783,932 | |

Deferred loan fees, net | | | (2,115 | ) | | | (1,059 | ) |

| | | | | | | | |

Total loans that are not PCI loans | | | 1,119,913 | | | | 782,873 | |

| | | | | | | | |

PCI loans | | | | | | | | |

Construction and land development | | $ | 77 | | | $ | 77 | |

Commercial real estate: | | | | | | | | |

Nonfarm, nonresidential | | | 1,452 | | | | 1,798 | |

Other | | | — | | | | — | |

Residential real estate: | | | | | | | | |

Closed-end 1-4 family | | | 707 | | | | 706 | |

Other | | | 2 | | | | 108 | |

Commercial and industrial | | | 1,675 | | | | 1,624 | |

Consumer and other | | | — | | | | 2 | |

| | | | | | | | |

Total PCI loans | | | 3,913 | | | | 4,315 | |

| | | | | | | | |

Allowance for loan losses | | | (9,744 | ) | | | (6,680 | ) |

| | | | | | | | |

Total loans, net of allowance for loan losses | | $ | 1,114,082 | | | $ | 780,508 | |

| | | | | | | | |

The following table presents the activity in the allowance for loan losses by portfolio segment for the three month periods ended September 30, 2015 and 2014:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Construction

and Land

Development | | | Commercial

Real

Estate | | | Residential

Real

Estate | | | Commercial

and

Industrial | | | Consumer

and

Other | | | Total | |

Three Months Ended September 30, 2015 | | | | | | | | | | | | | | | | | | | | | | | | |

Allowance for loan losses: | | | | | | | | | | | | | | | | | | | | | | | | |

Beginning balance | | $ | 2,567 | | | $ | 2,321 | | | $ | 1,739 | | | $ | 1,324 | | | $ | 65 | | | $ | 8,016 | |

Provision (credit) for loan losses | | | 461 | | | | 135 | | | | (71 | ) | | | 1,253 | | | | (54 | ) | | | 1,724 | |

Loans charged-off | | | — | | | | — | | | | (15 | ) | | | (15 | ) | | | (33 | ) | | | (63 | ) |

Recoveries | | | — | | | | — | | | | 6 | | | | — | | | | 61 | | | | 67 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total ending allowance balance | | $ | 3,028 | | | $ | 2,456 | | | $ | 1,659 | | | $ | 2,562 | | | $ | 39 | | | $ | 9,744 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Three Months Ended September 30, 2014 | | | | | | | | | | | | | | | | | | | | | | | | |

Allowance for loan losses: | | | | | | | | | | | | | | | | | | | | | | | | |

Beginning balance | | $ | 1,910 | | | $ | 1,740 | | | $ | 1,560 | | | $ | 508 | | | $ | 53 | | | $ | 5,771 | |

Provision (credit) for loan losses | | | 231 | | | | 173 | | | | 192 | | | | 72 | | | | (4 | ) | | | 664 | |

Loans charged-off | | | — | | | | (540 | ) | | | (11 | ) | | | (4 | ) | | | — | | | | (555 | ) |

Recoveries | | | — | | | | — | | | | 3 | | | | — | | | | — | | | | 3 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total ending allowance balance | | $ | 2,141 | | | $ | 1,373 | | | $ | 1,744 | | | $ | 576 | | | $ | 49 | | | $ | 5,883 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

11

There was $5 in allowance for loan losses for PCI loans for the three months ended September 30, 2015. There was no allowance for loan losses for the three months ended September 30, 2014.

The following table presents the activity in the allowance for loan losses by portfolio segment for the nine-month periods ended September 30, 2015 and 2014:

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Construction

and Land

Development | | | Commercial

Real

Estate | | | Residential

Real

Estate | | | Commercial

and

Industrial | | | Consumer

and

Other | | | Total | |

Nine Months Ended September 30, 2015 | | | | | | | | | | | | | | | | | | | | | | | | |

Allowance for loan losses: | | | | | | | | | | | | | | | | | | | | | | | | |

Beginning balance | | $ | 2,690 | | | $ | 1,494 | | | $ | 1,791 | | | $ | 650 | | | $ | 55 | | | $ | 6,680 | |

Provision (credit) for loan losses | | | 338 | | | | 962 | | | | (114 | ) | | | 1,927 | | | | 41 | | | | 3,154 | |

Loans charged-off | | | — | | | | — | | | | (32 | ) | | | (15 | ) | | | (121 | ) | | | (168 | ) |

Recoveries | | | — | | | | — | | | | 14 | | | | — | | | | 64 | | | | 78 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total ending allowance balance | | $ | 3,028 | | | $ | 2,456 | | | $ | 1,659 | | | $ | 2,562 | | | $ | 39 | | | $ | 9,744 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Nine Months Ended September 30, 2014 | | | | | | | | | | | | | | | | | | | | | | | | |

Allowance for loan losses: | | | | | | | | | | | | | | | | | | | | | | | | |

Beginning balance | | $ | 1,552 | | | $ | 1,511 | | | $ | 1,402 | | | $ | 337 | | | $ | 98 | | | $ | 4,900 | |

Provision (credit) for loan losses | | | 589 | | | | 402 | | | | 304 | | | | 243 | | | | (49 | ) | | | 1,489 | |

Loans charged-off | | | — | | | | (540 | ) | | | (11 | ) | | | (4 | ) | | | — | | | | (555 | ) |

Recoveries | | | — | | | | — | | | | 49 | | | | — | | | | — | | | | 49 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total ending allowance balance | | $ | 2,141 | | | $ | 1,373 | | | $ | 1,744 | | | $ | 576 | | | $ | 49 | | | $ | 5,883 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

There was $5 in allowance for loan losses for PCI loans for the nine months ended September 30, 2015. There was no allowance for loan losses for the nine months ended September 30, 2014.

The following table presents the balance in the allowance for loan losses and the recorded investment in loans by portfolio segment and based on impairment method as of September 30, 2015 and December 31, 2014. For purposes of this table, recorded investment in loans excludes accrued interest receivable and loan fees, net due to immateriality.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Construction

and Land

Development | | | Commercial

Real

Estate | | | Residential

Real

Estate | | | Commercial

and

Industrial | | | Consumer

and

Other | | | Total | |

September 30, 2015 | | | | | | | | | | | | | | | | | | | | | | | | |

Allowance for loan losses: | | | | | | | | | | | | | | | | | | | | | | | | |

Ending allowance balance attributable to loans: | | | | | | | | | | | | | | | | | | | | | | | | |

Individually evaluated for impairment | | $ | — | | | $ | — | | | $ | — | | | $ | 80 | | | $ | — | | | $ | 80 | |

Collectively evaluated for impairment | | | 3,028 | | | | 2,451 | | | | 1,659 | | | | 2,482 | | | | 39 | | | | 9,659 | |

Purchased credit-impaired loans | | | — | | | | 5 | | | | — | | | | — | | | | — | | | | 5 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total ending allowance balance | | $ | 3,028 | | | $ | 2,456 | | | $ | 1,659 | | | $ | 2,562 | | | $ | 39 | | | $ | 9,744 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Loans: | | | | | | | | | | | | | | | | | | | | | | | | |

Individually evaluated for impairment | | $ | — | | | $ | 914 | | | $ | 709 | | | $ | 102 | | | $ | 25 | | | $ | 1,750 | |

Collectively evaluated for impairment | | | 334,208 | | | | 312,221 | | | | 247,742 | | | | 219,239 | | | | 6,868 | | | | 1,120,278 | |

Purchased credit-impaired loans | | | 77 | | | | 1,452 | | | | 709 | | | | 1,675 | | | | — | | | | 3,913 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total ending loans balance | | $ | 334,285 | | | $ | 314,587 | | | $ | 249,160 | | | $ | 221,016 | | | $ | 6,893 | | | $ | 1,125,941 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

12

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Construction

and Land

Development | | | Commercial

Real

Estate | | | Residential

Real

Estate | | | Commercial

and

Industrial | | | Consumer

and

Other | | | Total | |

December 31, 2014 | | | | | | | | | | | | | | | | | | | | | | | | |

Allowance for loan losses: | | | | | | | | | | | | | | | | | | | | | | | | |

Ending allowance balance attributable to loans: | | | | | | | | | | | | | | | | | | | | | | | | |

Individually evaluated for impairment | | $ | — | | | $ | — | | | $ | — | | | $ | 18 | | | $ | — | | | $ | 18 | |

Collectively evaluated for impairment | | | 2,690 | | | | 1,494 | | | | 1,791 | | | | 632 | | | | 55 | | | | 6,662 | |

Purchased credit-impaired loans | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total ending allowance balance | | $ | 2,690 | | | $ | 1,494 | | | $ | 1,791 | | | $ | 650 | | | $ | 55 | | | $ | 6,680 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Loans: | | | | | | | | | | | | | | | | | | | | | | | | |

Individually evaluated for impairment | | $ | — | | | $ | 835 | | | $ | 93 | | | $ | 18 | | | $ | — | | | $ | 946 | |

Collectively evaluated for impairment | | | 239,225 | | | | 245,517 | | | | 213,667 | | | | 76,552 | | | | 8,025 | | | | 782,986 | |

Purchased credit-impaired loans | | | 77 | | | | 1,798 | | | | 814 | | | | 1,624 | | | | 2 | | | | 4,315 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total ending loans balance | | $ | 239,302 | | | $ | 248,150 | | | $ | 214,574 | | | $ | 78,194 | | | $ | 8,027 | | | $ | 788,247 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Loans collectively evaluated for impairment reported at September 30, 2015 include certain loans acquired from MidSouth on July 1, 2014. The acquired loans were recorded at estimated fair value at date of acquisition, which included an estimated credit discount. On July 1, 2014, acquired non-PCI loans were recorded at an estimated fair value of $178,818, comprised of contractually unpaid principal totaling $183,832 net of estimated discounts totaling $5,014 which included both credit and interest rate discount components. At September 30, 2015, acquired non-PCI loans were recorded at $104,853, comprised of contractually unpaid principal totaling $107,563 net of discounts totaling $2,710. Management evaluated these loans for credit deterioration since acquisition and determined that no allowance for loan losses was necessary at September 30, 2015.

The following table presents information related to impaired loans by class of loans as of September 30, 2015 and December 31, 2014:

| | | | | | | | | | | | |

| | | Unpaid

Principal

Balance | | | Recorded

Investment | | | Allowance for

Loan Losses

Allocated | |

September 30, 2015 | | | | | | | | | | | | |

With no allowance recorded: | | | | | | | | | | | | |

Commercial real estate: | | | | | | | | | | | | |

Nonfarm, nonresidential | | $ | 2,501 | | | $ | 914 | | | $ | — | |

Residential real estate: | | | | | | | | | | | | |

Other | | | 709 | | | | 709 | | | | — | |

Commercial and industrial | | | 22 | | | | 22 | | | | — | |

Consumer and other | | | 25 | | | | 25 | | | | — | |

| | | | | | | | | | | | |

Subtotal | | | 3,257 | | | | 1,670 | | | | — | |

With an allowance recorded: | | | | | | | | | | | | |

Commercial and industrial | | | 80 | | | | 80 | | | | 80 | |

| | | | | | | | | | | | |

Subtotal | | | 80 | | | | 80 | | | | 80 | |

| | | | | | | | | | | | |

Total | | $ | 3,337 | | | $ | 1,750 | | | $ | 80 | |

| | | | | | | | | | | | |

December 31, 2014 | | | | | | | | | | | | |

With no allowance recorded: | | | | | | | | | | | | |

Commercial real estate: | | | | | | | | | | | | |

Nonfarm, nonresidential | | $ | 2,422 | | | $ | 835 | | | $ | — | |

Residential real estate: | | | | | | | | | | | | |

Closed-end 1-4 family | | | 93 | | | | 93 | | | | — | |

| | | | | | | | | | | | |

Subtotal | | | 2,515 | | | | 928 | | | | — | |

| | | | | | | | | | | | |

With an allowance recorded: | | | | | | | | | | | | |

Commercial and industrial | | | 18 | | | | 18 | | | | 18 | |

| | | | | | | | | | | | |

Subtotal | | | 18 | | | | 18 | | | | 18 | |

| | | | | | | | | | | | |

Total | | $ | 2,533 | | | $ | 946 | | | $ | 18 | |

| | | | | | | | | | | | |

13

The following table presents the average recorded investment of impaired loans by class of loans for the three and nine months ended September 30, 2015 and 2014:

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

Average Recorded Investment | | 2015 | | | 2014 | | | 2015 | | | 2014 | |

With no allowance recorded: | | | | | | | | | | | | | | | | |

Construction and land development | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

Commercial real estate: | | | | | | | | | | | | | | | | |

Nonfarm, nonresidential | | | 918 | | | | 211 | | | | 873 | | | | 71 | |

Residential real estate: | | | | | | | | | | | | | | | | |

Closed-end 1-4 family | | | 33 | | | | — | | | | 188 | | | | — | |

Other | | | 712 | | | | — | | | | 317 | | | | — | |

Commercial and industrial | | | 23 | | | | — | | | | 77 | | | | — | |

Consumer and other | | | 25 | | | | — | | | | 8 | | | | — | |

| | | | | | | | | | | | | | | | |

Subtotal | | | 1,711 | | | | 211 | | | | 1,463 | | | | 71 | |

| | | | | | | | | | | | | | | | |

With an allowance recorded: | | | | | | | | | | | | | | | | |

Construction and land development | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

Commercial real estate: | | | | | | | | | | | | | | | | |

Nonfarm, nonresidential | | | — | | | | 1,194 | | | | — | | | | 837 | |

Residential real estate: | | | | | | | | | | | | | | | | |

1-4 family | | | — | | | | — | | | | — | | | | 476 | |

Commercial and industrial | | | 90 | | | | 64 | | | | 50 | | | | 65 | |

Consumer and other | | | 16 | | | | — | | | | 10 | | | | — | |

| | | | | | | | | | | | | | | | |

Subtotal | | | 106 | | | | 1,258 | | | | 60 | | | | 1,378 | |

| | | | | | | | | | | | | | | | |

Total | | $ | 1,817 | | | $ | 1,469 | | | $ | 1,523 | | | $ | 1,449 | |

| | | | | | | | | | | | | | | | |

The impact on net interest income for these loans was not material to the Company’s results of operations for the three and nine months ended September 30, 2015 and 2014.

The following table presents the recorded investment in nonaccrual and loans past due over 90 days still on accrual by class of loans as of September 30, 2015 and December 31, 2014:

| | | | | | | | |

| | | Nonaccrual | | | Loans Past Due

Over 90 Days | |

September 30, 2015 | | | | | | | | |

Commercial real estate: | | | | | | | | |

Nonfarm, nonresidential | | $ | 835 | | | $ | — | |

| | | | | | | | |

Total | | $ | 835 | | | $ | — | |

| | | | | | | | |

December 31, 2014 | | | | | | | | |

Commercial real estate: | | | | | | | | |

Nonfarm, nonresidential | | $ | 835 | | | $ | — | |

Residential real estate: | | | | | | | | |

Closed-end 1-4 family | | | — | | | | 316 | |

| | | | | | | | |

Total | | $ | 835 | | | $ | 316 | |

| | | | | | | | |

Nonaccrual loans and loans past due 90 days still on accrual include both smaller balance homogeneous loans that are collectively evaluated for impairment and individually classified impaired loans.

14

The following table presents the aging of the recorded investment in past due loans as of September 30, 2015 and December 31, 2014 by class of loans:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 30-59

Days

Past Due | | | 60-89

Days

Past Due | | | Greater

Than 89

Days

Past Due | | | Total

Past Due | | | Loans

Not

Past Due | | | PCI

Loans | | | Total | |

September 30, 2015 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Construction and land development | | $ | 1,358 | | | $ | — | | | $ | — | | | $ | 1,358 | | | $ | 332,850 | | | $ | 77 | | | $ | 334,285 | |

Commercial real estate: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Nonfarm, nonresidential | | | — | | | | — | | | | 835 | | | | 835 | | | | 302,822 | | | | 1,452 | | | | 305,109 | |

Other | | | — | | | | — | | | | — | | | | — | | | | 9,478 | | | | — | | | | 9,478 | |

Residential real estate: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Closed-end 1-4 family | | | 839 | | | | — | | | | — | | | | 839 | | | | 143,241 | | | | 707 | | | | 144,787 | |

Other | | | — | | | | — | | | | — | | | | — | | | | 104,371 | | | | 2 | | | | 104,373 | |

Commercial and industrial | | | 123 | | | | — | | | | — | | | | 123 | | | | 219,218 | | | | 1,675 | | | | 221,016 | |

Consumer and other | | | 1 | | | | — | | | | — | | | | 1 | | | | 6,892 | | | | — | | | | 6,893 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | $ | 2,321 | | | $ | — | | | $ | 835 | | | $ | 3,156 | | | $ | 1,118,872 | | | $ | 3,913 | | | $ | 1,125,941 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

December 31, 2014 | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Construction and land development | | $ | 354 | | | $ | — | | | $ | — | | | $ | 354 | | | $ | 238,871 | | | $ | 77 | | | $ | 239,302 | |

Commercial real estate: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Nonfarm, nonresidential | | | — | | | | — | | | | 835 | | | | 835 | | | | 240,140 | | | | 1,798 | | | | 242,773 | |

Other | | | — | | | | — | | | | — | | | | — | | | | 5,377 | | | | — | | | | 5,377 | |

Residential real estate: | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Closed-end 1-4 family | | | 299 | | | | 165 | | | | 316 | | | | 780 | | | | 129,851 | | | | 706 | | | | 131,337 | |

Other | | | 52 | | | | — | | | | — | | | | 52 | | | | 83,077 | | | | 108 | | | | 83,237 | |

Commercial and industrial | | | — | | | | 212 | | | | — | | | | 212 | | | | 76,358 | | | | 1,624 | | | | 78,194 | |

Consumer and other | | | — | | | | — | | | | — | | | | — | | | | 8,025 | | | | 2 | | | | 8,027 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | $ | 705 | | | $ | 377 | | | $ | 1,151 | | | $ | 2,233 | | | $ | 781,699 | | | $ | 4,315 | | | $ | 788,247 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Credit Quality Indicators:The Company categorizes loans into risk categories based on relevant information about the ability of borrowers to service their debt such as: current financial information, historical payment experience, credit documentation, public information, and current economic trends, among other factors. The Company analyzes loans individually by classifying the loans as to credit risk. This analysis includes non-homogeneous loans, such as commercial and commercial real estate loans as well as non-homogeneous residential real estate loans. This analysis is performed on a quarterly basis. The Company uses the following definitions for risk ratings:

Special Mention.Loans classified as special mention have a potential weakness that deserves management’s close attention. If left uncorrected, these potential weaknesses may result in deterioration of the repayment prospects for the loan or of the institution’s credit position at some future date.

Substandard.Loans classified as substandard are inadequately protected by the current net worth and paying capacity of the obligor or of the collateral pledged, if any. Loans so classified have a well-defined weakness or weaknesses that jeopardize the liquidation of the debt. They are characterized by the distinct possibility that the institution will sustain some loss if the deficiencies are not corrected.

15

Loans not meeting the criteria above that are analyzed individually as part of the above described process are considered to be pass-rated loans. The following table includes PCI loans, which are included in the “Substandard” column. Based on the most recent analysis performed, the risk category of loans by class of loans is as follows as of September 30, 2015 and December 31, 2014:

| | | | | | | | | | | | | | | | |

| | | Pass | | | Special

Mention | | | Substandard | | | Total | |

September 30, 2015 | | | | | | | | | | | | | | | | |

Construction and land development | | $ | 334,208 | | | $ | — | | | $ | 77 | | | $ | 334,285 | |

Commercial real estate: | | | | | | | | | | | | | | | | |

Nonfarm, nonresidential | | | 302,387 | | | | — | | | | 2,722 | | | | 305,109 | |

Other | | | 9,478 | | | | — | | | | — | | | | 9,478 | |

Residential real estate: | | | | | | | | | | | | | | | | |

Closed-end 1-4 family | | | 143,564 | | | | — | | | | 1,223 | | | | 144,787 | |

Other | | | 103,663 | | | | — | | | | 710 | | | | 104,373 | |

Commercial and industrial | | | 219,522 | | | | — | | | | 1,494 | | | | 221,016 | |

Consumer and other | | | 6,868 | | | | — | | | | 25 | | | | 6,893 | |

| | | | | | | | | | | | | | | | |

| | $ | 1,119,690 | | | $ | — | | | $ | 6,251 | | | $ | 1,125,941 | |

| | | | | | | | | | | | | | | | |

December 31, 2014 | | | | | | | | | | | | | | | | |

Construction and land development | | $ | 239,225 | | | $ | — | | | $ | 77 | | | $ | 239,302 | |

Commercial real estate: | | | | | | | | | | | | | | | | |

Nonfarm, nonresidential | | | 239,584 | | | | — | | | | 3,189 | | | | 242,773 | |

Other | | | 5,377 | | | | — | | | | — | | | | 5,377 | |

Residential real estate: | | | | | | | | | | | | | | | | |

Closed-end 1-4 family | | | 128,869 | | | | — | | | | 2,468 | | | | 131,337 | |

Other | | | 83,129 | | | | — | | | | 108 | | | | 83,237 | |

Commercial and industrial | | | 76,552 | | | | — | | | | 1,642 | | | | 78,194 | |

Consumer and other | | | 8,025 | | | | — | | | | 2 | | | | 8,027 | |

| | | | | | | | | | | | | | | | |

| | $ | 780,761 | | | $ | — | | | $ | 7,486 | | | $ | 788,247 | |

| | | | | | | | | | | | | | | | |

Purchased Credit-Impaired (“PCI”) Loans

Income is recognized on PCI loans pursuant to ASC Topic 310-30. A portion of the fair value discount has been recognized as an accretable yield that is accreted into interest income over the estimated remaining life of the loans. The remaining non-accretable difference represents cash flows not expected to be collected.

The table below summarizes the total contractually required principal and interest cash payments, management’s estimate of expected total cash payments and carrying value of the loans as of September 30, 2015 and December 31, 2014. Contractually required principal and interest payments have been adjusted for estimated prepayments.

| | | | | | | | |

| | | Sept 30, 2015 | | | Dec 31, 2014 | |

Contractually required principal and interest | | $ | 5,872 | | | $ | 6,532 | |

Non-accretable difference | | | (307 | ) | | | (1,270 | ) |

| | | | | | | | |

Cash flows expected to be collected | | | 5,565 | | | | 5,262 | |

Accretable yield | | | (1,652 | ) | | | (947 | ) |

| | | | | | | | |

Carrying value of acquired loans | | | 3,913 | | | | 4,315 | |

Allowance for loan losses | | | (5 | ) | | | — | |

| | | | | | | | |

Carrying value less allowance for loan losses | | $ | 3,908 | | | $ | 4,315 | |

| | | | | | | | |

16

Management adjusted estimates of future expected losses, cash flows and renewal assumptions during the nine months ended September 30, 2015. These adjustments resulted in a decrease in expected cash flows and accretable yield, and a decrease in the non-accretable difference. The table below summarizes the changes in total contractually required principal and interest cash payments, management’s estimate of expected total cash payments and carrying value of the loans during the three- and nine-month periods ended September 30, 2015.

| | | | | | | | | | | | | | | | | | | | |

Activity during the three-month period ended September 30, 2015 | | Jun 30, 2015 | | | Effect of

Acquisitions | | | Income

Accretion | | | All other

Adjustments | | | Sept 30, 2015 | |

Contractually required principal and interest | | $ | 6,000 | | | $ | — | | | $ | — | | | $ | (128 | ) | | $ | 5,872 | |

Non-accretable difference | | | (973 | ) | | | — | | | | 839 | | | | (173 | ) | | | (307 | ) |

| | | | | | | | | | | | | | | | | | | | |

Cash flows expected to be collected | | | 5,027 | | | | — | | | | 839 | | | | (301 | ) | | | 5,565 | |

Accretable yield | | | (749 | ) | | | — | | | | 447 | | | | (1,350 | ) | | | (1,652 | ) |

| | | | | | | | | | | | | | | | | | | | |

Carrying value of acquired loans | | $ | 4,278 | | | $ | — | | | $ | 1,286 | | | $ | (1,651 | ) | | $ | 3,913 | |

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

Activity during the nine-month period ended September 30, 2015 | | Dec 31, 2014 | | | Effect of

Acquisitions | | | Income

Accretion | | | All other

Adjustments | | | Sept 30, 2015 | |

Contractually required principal and interest | | $ | 6,532 | | | $ | — | | | $ | — | | | $ | (660 | ) | | $ | 5,872 | |

Non-accretable difference | | | (1,270 | ) | | | — | | | | 839 | | | | 124 | | | | (307 | ) |

| | | | | | | | | | | | | | | | | | | | |

Cash flows expected to be collected | | | 5,262 | | | | — | | | | 839 | | | | (536 | ) | | | 5,565 | |

Accretable yield | | | (947 | ) | | | — | | | | 637 | | | | (1,342 | ) | | | (1,652 | ) |

| | | | | | | | | | | | | | | | | | | | |

Carrying value of acquired loans | | $ | 4,315 | | | $ | — | | | $ | 1,476 | | | $ | (1,878 | ) | | $ | 3,913 | |

| | | | | | | | | | | | | | | | | | | | |

Troubled Debt Restructurings

The Company’s loan portfolio contains no loans that have been modified in a troubled debt restructuring.

NOTE 5—LOAN SERVICING

Loans serviced for others are not reported as assets. The principal balances of these loans at September 30, 2015 and December 31, 2014 are as follows:

| | | | | | | | |

| | | September 30,

2015 | | | December 31,

2014 | |

Loan portfolios serviced for: | | | | | | | | |

Federal Home Loan Mortgage Corporation | | $ | 461,121 | | | $ | 414,222 | |

Other | | | 3,613 | | | | 3,986 | |

The components of net loan servicing fees for the three and nine months ended September 30, 2015 and 2014 were as follows:

| | | | | | | | | | | | | | | | |

| | | Three Months Ended

September 30, | | | Nine Months Ended

September 30, | |

| | | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Loan servicing fees, net: | | | | | | | | | | | | | | | | |

Loan servicing fees | | $ | 287 | | | $ | 253 | | | $ | 831 | | | $ | 720 | |

Amortization of loan servicing fees | | | (203 | ) | | | (180 | ) | | | (644 | ) | | | (547 | ) |

Change in impairment | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

Total | | $ | 84 | | | $ | 73 | | | $ | 187 | | | $ | 173 | |

| | | | | | | | | | | | | | | | |

The fair value of servicing rights was estimated by management to be approximately $4,264 at September 30, 2015. Fair value for September 30, 2015 was determined using a weighted average discount rate of 10.5% and a weighted average prepayment speed of 11.5%. At December 31, 2014, the fair value of servicing rights was estimated by management to be approximately $4,180. Fair value for December 31, 2014 was determined using weighted average discount rate of 10.5% and a weighted average prepayment speed of 10.8%.

17

The weighted average amortization period is 6.77 years. Estimated amortization expense for each of the next three years is:

| | | | |

2015 | | $ | 782 | |

2016 | | | 552 | |

2017 | | | 552 | |

NOTE 6—SHARE-BASED PAYMENTS

In connection with the Company’s 2010 private offering, 32,425 warrants were issued to shareholders, one warrant for every twenty shares of common stock purchased. Each warrant allows the shareholders to purchase an additional share of common stock at $12.00 per share. The warrants were issued with an effective date of March 30, 2010 and will be exercisable in whole or in part up to seven years following the date of issuance. The warrants are detachable from the common stock. There were 4,970 warrants exercised during the nine months ended September 30, 2015, for which the Company received cash proceeds of $60. The exercised warrants had an aggregate intrinsic value of $46 at the date of exercise. No warrants were exercised during the nine months ended September 30, 2014. At September 30, 2015, there were 26,907 outstanding warrants associated with the 2010 offering.

Since the common stock of the Company has been registered under the Securities Act and has been traded on a national securities exchange at $15.00 or more for forty-five (45) consecutive days, the Company may redeem the 2010 warrants at any time with not less than thirty (30) days’ written notice to the holder of such 2010 warrant, in whole or in part, at a redemption price of $1.00 per warrant; provided, however, that the holder of the 2010 warrant may exercise the 2010 warrant, in whole or in part, during such thirty (30) day period.

Stock Option Plan: The Company’s 2007 Stock Option Plan (“stock option plan” or the “Plan”), which was shareholder-approved, permitted the grant of stock options to its employees, organizers and directors for up to 551,250 shares of common stock. The Plan was amended during April 2010 to increase the number of shares available for issuance to 1,000,000. In April 2013, the Plan was amended to offer additional forms of equity compensation, to change the Plan’s name to the Franklin Financial Network, Inc. 2007 Omnibus Equity Incentive Plan, and to increase the number of authorized shares to 1,500,000. Shareholders approved amendments to the Company’s 2007 Stock Option Plan (“stock option plan” or the “Plan”) to increase the number of authorized shares to 2,000,000 in June 2014 and to 4,000,000 in February 2015. At September 30, 2015, there were 2,364,492 authorized shares available for issuance.

Employee, organizer and director awards are granted with an exercise price equal to the market price of the Company’s common stock at the date of grant; those option awards have a vesting period of 3 to 5 years and have a 10-year contractual term. The Company assigns discretion to its Board of Directors to make grants either as qualified incentive stock options or as non-qualified stock options. All employee grants are intended to be treated as qualified incentive stock options, if allowable. All other grants are expected to be treated as non-qualified.

On July 1, 2014, 322,300 MidSouth common stock options were converted into 137,280 options to purchase shares of FFN common stock with an exercise price of $8.57 per option pursuant to the terms of the merger agreement (see Note 2). Using the Black-Scholes option valuation model, the grant date fair value was estimated to be $6.31 per converted option based on the $14.50 fair value per share of FFN common stock at July 1, 2014. No compensation expense was required related to the converted options.

The fair value of each option award is estimated on the date of grant using a closed form option valuation (Black-Scholes) model that uses the assumptions noted in the table below. Expected stock price volatility is based on historical volatilities of a peer group. The Company uses historical data to estimate option exercise and post-vesting termination behavior.

The expected term of options granted represents the period of time that options granted are expected to be outstanding, which takes into account that the options are not transferable. The risk-free interest rate for the expected term of the option is based on the U.S. Treasury yield curve in effect at the time of the grant.

18

The fair value of options granted was determined using the following weighted-average assumptions as of grant date.

| | | | | | | | |

| | | September 30,

2015 | | | September 30,

2014 | |

Risk-free interest rate | | | 1.84 | % | | | 1.81 | % |

Expected term | | | 7.5 years | | | | 5.9 years | |

Expected stock price volatility | | | 25.00 | % | | | 10.85 | % |

Dividend yield | | | 0.22 | % | | | 0.23 | % |

The weighted average fair value of options granted for the nine months ended September 30, 2015 and 2014 were $6.41 and $4.12, respectively.

A summary of the activity in the stock option plans for the nine months ended September 30, 2015 follows:

| | | | | | | | | | | | | | | | |

| | | Shares | | | Weighted

Average

Exercise

Price | | | Weighted

Average

Remaining

Contractual

Term | | | Aggregate

Intrinsic

Value | |

Outstanding at beginning of year | | | 1,210,660 | | | $ | 11.32 | | | | 6.53 | | | $ | 7,244 | |

Granted | | | 226,782 | | | | 20.78 | | | | | | | | | |

Exercised | | | (93,754 | ) | | | 11.53 | | | | | | | | | |

Forfeited, expired, or cancelled | | | (4,417 | ) | | | 19.02 | | | | | | | | | |

| | | | | | | | | | | | | | | | |

Outstanding at period end | | | 1,339,271 | | | $ | 12.88 | | | | 6.39 | | | $ | 12,685 | |

| | | | | | | | | | | | | | | | |

Vested or expected to vest | | | 1,272,307 | | | $ | 12.88 | | | | 6.39 | | | $ | 12,051 | |

Exercisable at period end | | | 829,072 | | | $ | 10.76 | | | | 5.06 | | | $ | 9,606 | |

| | | | | | | | | | | | | | | | |

The Company received cash proceeds of $780 for the options exercised during the nine months ended September 30, 2015. The exercised options had an aggregate intrinsic value of $839 at the date of exercise.

As of September 30, 2015, there was $1,733 of total unrecognized compensation cost related to non-vested stock options granted under the Plan. The cost is expected to be recognized over a weighted-average period of 1.7 years.

Restricted Share Award Plan: Additionally, the Company’s 2007 Omnibus Equity Incentive Plan provides for the granting of restricted share awards and other performance related incentives. During 2014, the Company awarded 87,374 restricted common shares to employees of the Company. When the restricted shares are awarded, a participant receives voting and dividend rights with respect to the shares, but is not able to transfer the shares until the restrictions have lapsed. These awards have a vesting period of three to five years and vest in equal annual installments on the anniversary date of the grant.

A summary of activity for non-vested restricted share awards for the nine months ended September 30, 2015 is as follows:

| | | | | | | | |

Non-vested Shares | | Shares | | | Weighted-

Average

Grant-Date

Fair Value | |

Non-vested at beginning of year | | | 102,710 | | | $ | 13.93 | |

Granted | | | 31,938 | | | | 20.69 | |

Vested | | | (25,075 | ) | | | 14.08 | |

Forfeited | | | (3,709 | ) | | | 15.99 | |

| | | | | | | | |

Non-vested at period end | | | 105,864 | | | $ | 15.89 | |

| | | | | | | | |

Compensation expense associated with the restricted share awards is recognized on a straight-line basis over the time period that the restrictions associated with the awards lapse based on the total cost of the award at the grant date. As of September 30, 2015, there was $1,524 of total unrecognized compensation cost related to non-vested shares granted under the Plan. The cost is expected to be recognized over a weighted-average period of 3.5 years.

19

NOTE 7—REGULATORY CAPITAL MATTERS

In July 2013, the Federal Reserve Board and the FDIC approved final rules that substantially amended the regulatory risk-based capital rules applicable to the Company and Bank. The final rules implement the regulatory capital reforms of the Basel Committee on Banking Supervision reflected in “Basel III: A Global Framework for More Resilient Banks and Banking Systems” (“Basel III”) and changes required by the Dodd-Frank Wall Street Reform and Consumer Protection Act.

Under these rules, the leverage and risk-based capital ratios of financial holding companies may not be lower than the leverage and risk-based capital ratios for insured depository institutions. The final rules implementing the Basel III regulatory capital reforms became effective to the Company and Bank on January 1, 2015, and include new minimum risk-based capital and leverage ratios. Moreover, these rules refine the definition of what constitutes capital for purposes of calculating those ratios, including the definitions of Tier 1 capital and Tier 2 capital.

In addition to the new minimum capital level requirements, the rules also establish a “capital conservation buffer” of 2.5% (to be phased in over three years) above the new regulatory minimum risk-based capital ratios, and result in the following minimum ratios once the capital conservation buffer is fully phased in: (i) a common Tier 1 risk-based capital ratio of 7.0%, (ii) a Tier 1 risk-based capital ratio of 8.5%, and (iii) a total risk-based capital ratio of 10.5%. The capital conservation buffer is to be phased in beginning in January 2016 at 0.625% of risk-weighted assets and will increase each year until fully implemented in January 2019. An institution will be subject to limitations on paying dividends, engaging in share repurchases, and paying discretionary bonuses if capital levels fall below minimum levels plus the buffer amounts. These limitations establish a maximum percentage of eligible retained income that could be utilized for such actions.

The final rules allow banks and their holding companies with less than $250 billion in assets a one-time opportunity to opt-out of a requirement to include unrealized gains and losses in accumulated other comprehensive income in their capital calculation. The Company has opted out of this requirement.

Management believes, as of September 30, 2015, that the Company and Bank met all capital adequacy requirements to which they are subject and met the requirements to be considered well-capitalized. The Company’s and Bank’s actual capital amounts and ratios are presented in the following table (in thousands):

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Actual | | | Required

For Capital

Adequacy Purposes | | | To Be Well

Capitalized Under

Prompt Corrective

Action Regulations | |

| | | Amount | | | Ratio | | | Amount | | | Ratio | | | Amount | | | Ratio | |