Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22107

SEI Structured Credit Fund, LP

(Exact name of registrant as specified in charter)

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

James Ndiaye

c/o SEI Investments Management Corporation

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: (610) 676-2269

Date of fiscal year end: December 31, 2009

Date of reporting period: December 31, 2009

Table of Contents

| Item 1. | Reports to Stockholders. |

Table of Contents

SEI STRUCTURED CREDIT FUND, L.P.

Financial Statements

For the year ended December 31, 2009

With report of Independent Registered Public Accounting Firm

Table of Contents

SEI Structured Credit Fund, L.P.

Financial Statements

For the year ended December 31, 2009

Contents

| 1 | ||

Audited Financial Statements | ||

| 2 | ||

| 8 | ||

| 9 | ||

| 10 | ||

| 11 | ||

| 12 | ||

| 25 | ||

The Fund files its complete schedule of Fund holdings with the Securities and Exchange Commission for the first and third quarters of each fiscal year on Form N-Q within sixty days after the end of the period. The Fund’s Form N-Q is available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling (888) 786-9977; and (ii) on the Commission’s website at http://www.sec.gov.

Table of Contents

Report of Independent Registered Public Accounting Firm

To the Partners and Board of Directors of

SEI Structured Credit Fund, LP

We have audited the accompanying statement of assets and liabilities of SEI Structured Credit Fund, L.P. (the “Fund”), including the schedule of investments, as of December 31, 2009, and the related statements of operations, and cash flows for the year then ended and the statement of changes in partners’ capital for each of the two years indicated therein. These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2009, by correspondence with the custodian and management of the underlying investment funds. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of SEI Structured Credit Fund, L.P. at December 31, 2009, the results of its operations, and its cash flows for the year then ended and the changes in its partners’ capital for each of the two years indicated therein, in conformity with U.S. generally accepted accounting principles.

March 1, 2010

1

Table of Contents

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2009

Description | Par Value | Fair Value | ||||

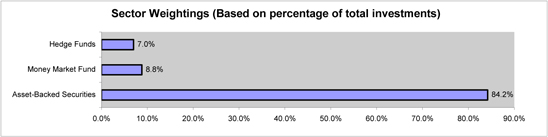

ASSET-BACKED SECURITIES — 89.3% | ||||||

CAYMAN ISLANDS — 89.3% | ||||||

Aberdeen Loan Funding, Ser 2008-1A, Cl B | ||||||

1.931%, 11/01/18 (A)(B)(C) | $ | 4,500,000 | $ | 3,592,800 | ||

ACAS Business Loan Trust , Ser 2005-1A | ||||||

0.532%, 07/25/19 (A)(B)(C) | 9,505,563 | 7,794,562 | ||||

ACAS Business Loan Trust, Ser 2004-1A, Cl A | ||||||

0.602%, 10/25/17 (A)(B)(C) | 677,363 | 646,882 | ||||

ACAS Business Loan Trust, Ser 2007-1A, Cl A | ||||||

0.414%, 08/16/19 (A)(B)(C) | 1,139,805 | 946,038 | ||||

ACAS Business Loan Trust, Ser 2007-2A, Cl A | ||||||

0.673%, 11/18/19 (A)(B)(C) | 915,966 | 751,092 | ||||

ACAS CLO, Ser 2007-1A, Cl A1J | ||||||

0.594%, 04/20/21 (A)(B)(C) | 6,800,000 | 4,964,000 | ||||

Apidos CDO, Ser 2005-2A, Cl B | ||||||

1.082%, 12/21/18 (A)(B)(C) | 2,000,000 | 1,393,600 | ||||

Ares IIIR/IVR CLO, Ser 2007-3RA, Cl E | ||||||

11.460%, 04/16/21 (B)(C) | 2,000,000 | 560,000 | ||||

3.784%, 04/16/21 (A)(B) (C) | 5,000,000 | 2,000,000 | ||||

Ares IX CLO, Ser 2007-11A, Cl SUB | ||||||

20.930%, 04/20/17 (A)(B)(C) | 3,050,000 | 549,000 | ||||

Ares XI CLO, Ser 2007-11A | ||||||

14.850%, 10/11/21 (B)(C) | 5,000,000 | 1,500,000 | ||||

Babson CLO, Ser 2004-2A | ||||||

20.027%, 11/15/16 (B)(C) | 1,000,000 | 280,000 | ||||

Babson CLO, Ser 2006-2A, Cl INC | ||||||

25.520%, 10/16/20 (B)(C) | 1,000,000 | 320,000 | ||||

Babson CLO, Ser 2007-1A, Cl INC | ||||||

N/A%, 01/18/21 (B)(C)(I) | 5,000,000 | 1,300,000 | ||||

Babson CLO, Ser 2007-2A, Cl D | ||||||

1.984%, 04/15/21 (A)(B)(C) | 900,000 | 405,000 | ||||

Battalion CLO, Ser 2007-1A, Cl SUB | ||||||

5.389%, 07/14/22 (B)(C) | 4,200,000 | 1,260,000 | ||||

Battalion CLO, Ser 2007-1A, Cl E | ||||||

4.534%, 07/14/22 (A)(B)(C) | 2,000,000 | 950,000 | ||||

Brentwood CLO, Ser 2006-1A, Cl C | ||||||

1.881%, 02/01/22 (A)(B)(C) | 917,114 | 229,279 | ||||

Brentwood CLO, Ser 2006-1A, Cl B | ||||||

1.101%, 02/01/22 (A)(B)(C) | 2,532,595 | 886,408 | ||||

Brentwood CLO, Ser 2006-1I, Cl D | ||||||

4.031%, 02/01/22 (A)(C) | 6,632,719 | 994,908 | ||||

Capitalsource Advisors, Ser 2006-1A, Cl B | ||||||

0.956%, 08/27/20 (A)(B)(C) | 5,000,000 | 3,100,000 | ||||

CapitalSource Commercial Loan Trust, Ser 2006-2A, Cl A1B | ||||||

0.563%, 09/20/22 (A)(B)(C) | 2,684,000 | 2,066,680 | ||||

CapitalSource Commercial Loan Trust, Ser 2006-2A, Cl C | ||||||

0.913%, 09/20/22 (A)(B)(C) | 5,000,000 | 2,650,000 | ||||

2

Table of Contents

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2009

Description | Par Value | Fair Value | ||||

CapitalSource Commercial Loan Trust, Ser 2006-2A, Cl A1A | ||||||

0.443%, 09/20/22 (A)(B)(C) | $ | 947,880 | $ | 872,050 | ||

CapitalSource Commercial Loan Trust, Ser 2007-1A, Cl A | ||||||

0.363%, 03/20/17 (A)(B)(C) | 5,744,895 | 5,256,579 | ||||

CIFC Funding, Ser 2006-1BA, Cl B2L | ||||||

4.251%, 12/22/20 (A)(C) | 6,000,000 | 2,257,200 | ||||

CIFC Funding, Ser 2006-1BA | ||||||

1.081%, 12/22/20 (A)(B)(C) | 2,500,000 | 1,517,750 | ||||

CIFC Funding, Ser 2006-2A | ||||||

4.256%, 03/01/21 (A)(B)(C) | 1,637,050 | 543,173 | ||||

CIFC Funding, Ser 2006-I, Cl I | ||||||

—%, 10/20/20 (A)(B)(C) | 2,000,000 | 300,000 | ||||

CIFC Funding, Ser 2007-1A, Cl A3L | ||||||

1.024%, 05/10/21 (A)(B)(C) | 2,800,000 | 1,687,000 | ||||

CIFC Funding, Ser 2007-1A, Cl INC | ||||||

23.380%, 05/10/21 (C) | 1,000,000 | 200,000 | ||||

CIFC Funding, Ser 2007-2A, Cl B | ||||||

1.034%, 04/15/21 (A)(B)(C) | 5,000,000 | 2,750,000 | ||||

CIFC Funding, Ser 2007-3A, Cl B | ||||||

1.532%, 07/26/21 (A)(B)(C) | 12,000,000 | 6,600,000 | ||||

CIFC Funding, Ser 2007-IV | ||||||

18.570%, 09/20/19 (C) | 2,000,000 | 500,000 | ||||

CIT CLO, Ser 2007-1A, Cl D | ||||||

2.253%, 06/20/21 (A)(B)(C) | 3,000,000 | 1,350,000 | ||||

CIT CLO, Ser 2007-1A, Cl E | ||||||

5.253%, 06/20/21 (A)(C) | 3,000,000 | 1,050,000 | ||||

COLTS Trust, Ser 2005-2A, Cl C | ||||||

1.103%, 12/20/18 (A)(B)(C) | 5,000,000 | 2,700,000 | ||||

COLTS Trust, Ser 2007-1A, Cl C | ||||||

1.053%, 03/20/21 (A)(B)(C) | 19,000,000 | 10,830,000 | ||||

Copper River CLO, Ser 2006-1A, Cl C | ||||||

1.084%, 01/20/21 (A)(B)(C) | 3,000,000 | 1,950,000 | ||||

Denali Capital CLO VI, Ser 2006-6A, Cl B2L | ||||||

4.533%, 04/21/20 (A)(C) | 1,000,000 | 362,800 | ||||

Duane Street CLO II, Ser 2006-2A, Cl SUB | ||||||

N/A%, 08/20/18 (B)(C)(I) | 4,000,000 | 400,000 | ||||

Duane Street CLO V, Ser 2007-5A, Cl SN | ||||||

N/A%, 10/14/21 (B)(C)(I) | 2,500,000 | 175,000 | ||||

Duane Street CLO, Ser 2005-1A, Cl SUB | ||||||

12.510%, 11/08/17 (B)(C) | 2,000,000 | 350,000 | ||||

Duane Street CLO, Ser 2005-1X | ||||||

12.510%, 11/18/17 (C) | 1,000,000 | 175,000 | ||||

Duane Street CLO, Ser 2006-3A, Cl C | ||||||

1.044%, 01/11/21 (A)(B)(C) | 5,000,000 | 3,075,000 | ||||

Emporia Preferred Funding, Ser 2007-3A, Cl C | ||||||

1.183%, 04/23/21 (A)(B)(C) | 21,238,000 | 11,680,900 | ||||

Emporia Preferred Funding, Ser 2007-3A, Cl D | ||||||

1.783%, 04/23/21 (A)(B)(C) | 15,450,000 | 6,180,000 | ||||

FM Leveraged Capital Fund, Ser 2006-2A, Cl D | ||||||

1.873%, 11/15/20 (A)(B)(C) | 7,605,000 | 3,346,200 | ||||

Franklin CLO IV | ||||||

5.200%, 09/20/15 (C) | 2,000,000 | 120,000 | ||||

Fraser Sullivan CLO, Ser 2006-2A, Cl B | ||||||

0.653%, 12/20/20 (A)(B)(C) | 3,000,000 | 2,160,000 | ||||

Fraser Sullivan CLO, Ser 2006-2A, Cl D | ||||||

1.792%, 12/20/20 (A)(B)(C) | 9,000,000 | 4,320,000 | ||||

Fraser Sullivan CLO, Ser 2006-2A, Cl C | ||||||

0.973%, 12/20/20 (A)(B)(C) | 5,000,000 | 3,550,000 | ||||

Freidbergmilstein Private Capital Fund I | ||||||

N/A%, 01/15/19 (A)(C)(I) | 1,000,000 | 15,000 | ||||

3

Table of Contents

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2009

Description | Par Value | Fair Value | ||||

Friedbergmilstein Private Capital Fund, Ser 2004-1A, Cl B1 | ||||||

1.184%, 01/15/19 (A)(B)(C) | $ | 1,400,000 | $ | 866,880 | ||

Gale Force CLO, Ser 2005-1A, Cl D1 | ||||||

2.122%, 11/15/17 (A)(B)(C) | 1,000,000 | 545,000 | ||||

Gale Force CLO, Ser 2007-3A, Cl D | ||||||

1.684%, 04/19/21 (A)(B)(C) | 5,500,000 | 2,475,000 | ||||

Gale Force CLO, Ser 2007-3A, Cl C | ||||||

0.984%, 04/19/21 (A)(B)(C) | 5,000,000 | 2,850,000 | ||||

Gale Force CLO, Ser 2007-3A, Cl E | ||||||

3.784%, 04/19/21 (A)(B)(C) | 1,000,000 | 395,000 | ||||

Gale Force CLO, Ser 2007-4A, Cl E | ||||||

6.669%, 08/20/21 (A)(C) | 1,500,000 | 720,000 | ||||

Gale Force CLO, Ser 2007-4A, Cl INC | ||||||

—%, 08/20/21 (A)(C) | 3,000,000 | 1,065,000 | ||||

Global Leveraged Capital Credit Opportunity Fund CLO, | ||||||

Ser 2006-1A, Cl B | ||||||

0.884%, 12/20/18 (A)(B)(C) | 15,500,000 | 10,068,800 | ||||

Global Leveraged Capital Credit Opportunity Fund CLO, | ||||||

Ser 2006-1B, Cl C | ||||||

1.284%, 12/20/18 (A)(B)(C) | 5,012,470 | 2,506,235 | ||||

Golub Capital Management CLO, Ser 2007-1A, Cl D | ||||||

2.681%, 07/31/21 (A)(B)(C) | 4,000,000 | 2,000,000 | ||||

Grayson CLO, Ser 2006-1A, Cl A1B | ||||||

0.641%, 11/01/21 (A)(B)(C) | 18,000,000 | 11,070,000 | ||||

Grayson CLO, Ser 2006-1A, Cl A2 | ||||||

0.691%, 11/01/21 (A)(B)(C) | 10,000,000 | 4,800,000 | ||||

Green Lane CLO, Ser 2004-1A, Cl B | ||||||

1.431%, 01/30/17 (A)(B)(C) | 10,000,000 | 6,400,000 | ||||

Greenbriar CLO, Ser 2007-1A, Cl D | ||||||

3.031%, 11/01/21 (A)(B)(C) | 4,111,490 | 1,315,677 | ||||

Harch CLO, Ser 2005-2A | ||||||

2.233%, 10/22/17 (A)(B)(C) | 9,802,000 | 4,704,960 | ||||

Harch CLO, Ser 2007-1A, Cl C | ||||||

1.031%, 04/17/20 (A)(B)(C) | 3,333,000 | 2,166,450 | ||||

Harch CLO, Ser 2007-1A, Cl D | ||||||

2.031%, 04/17/20 (A)(B)(C) | 4,000,000 | 1,800,000 | ||||

Hudson Straits CLO, Ser 2004-1A, Cl B | ||||||

1.034%, 10/15/16 (A)(B) (C) | 6,200,000 | 4,755,400 | ||||

ING Investment Management I CLO | ||||||

14.520%, 12/01/17 (A)(B)(C) | 1,500,000 | 300,000 | ||||

Jasper CLO, Ser 2005-1A, Cl B | ||||||

0.861%, 08/01/17 (A)(B)(C) | 5,000,000 | 3,534,500 | ||||

Kennecott Funding, Ser 2005-1A, Cl C | ||||||

1.084%, 01/13/18 (A)(B)(C) | 6,000,000 | 3,780,000 | ||||

Landmark CDO, Ser 2007-9A, Cl D | ||||||

1.734%, 04/15/21 (A)(B)(C) | 1,500,000 | 838,350 | ||||

Lightpoint CLO, Ser 2005-3A, Cl C | ||||||

2.154%, 09/15/17 (A)(B)(C) | 5,750,000 | 2,415,000 | ||||

Lightpoint CLO, Ser 2006-4A, Cl C | ||||||

2.084%, 04/15/18 (A)(B)(C) | 6,750,000 | 3,037,500 | ||||

MC Funding CLO, Ser 2006-1A, Cl C | ||||||

1.203%, 12/20/20 (A)(B)(C) | 15,000,000 | 9,000,000 | ||||

Momentum Capital Fund, Ser 2007-1A, Cl C | ||||||

1.684%, 09/18/21 (A)(B)(C) | 4,850,000 | 3,346,500 | ||||

Mountain Capital CLO, Ser 2007-6A, Cl B | ||||||

0.632%, 04/25/19 (A)(B)(C) | 2,000,000 | 1,480,000 | ||||

Mountain Capital CLO, Ser 2007-6A, Cl C | ||||||

0.932%, 04/25/19 (A)(B)(C) | 5,000,000 | 3,200,000 | ||||

NACM CLO, Ser 2006-1X, Cl D | ||||||

4.333%, 06/20/19 (A)(C) | 250,000 | 103,125 | ||||

Nautique Funding CLO, Ser 2006-1A, Cl INC | ||||||

22.460%, 04/15/20 (B)(C) | 1,500,000 | 300,000 | ||||

4

Table of Contents

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2009

Description | Par Value | Fair Value | ||||

Ocean Trails CLO, Ser 2007-2A, Cl A2 | ||||||

0.644%, 06/27/22 (A)(B) (C) | $ | 500,000 | $ | 377,500 | ||

Osprey CDO, Ser 2006-1A, Cl B2L | ||||||

4.523%, 04/08/22 (A) (C) | 2,262,029 | 113,101 | ||||

Osprey CDO, Ser 2006-1A, Cl B1L | ||||||

2.423%, 04/08/22 (A)(B) (C) | 2,811,900 | 281,190 | ||||

Red River CLO, Ser 1A, Cl B | ||||||

0.731%, 07/27/18 (A)(B)(C) | 5,000,000 | 3,025,000 | ||||

Rockwall CDO, Ser 2006-1A, Cl B1L | ||||||

2.531%, 08/01/21 (A)(B)(C) | 3,351,235 | 167,562 | ||||

Sands Point Funding, Ser 2006-1A, Cl C | ||||||

1.084%, 07/18/20 (A)(B)(C) | 5,100,000 | 2,856,000 | ||||

Sargas CLO, Ser 2006-1A, Cl C | ||||||

0.884%, 10/20/18 (A)(B)(C) | 19,284,807 | 13,692,213 | ||||

Sargas CLO, Ser 2006-1A, Cl B | ||||||

0.684%, 10/20/18 (A)(B)(C) | 1,885,626 | 1,395,363 | ||||

Sargas CLO, Ser 2006-1A | ||||||

N/A%, 10/20/18 (B)(C) | 1,062,901 | 403,902 | ||||

Saturn CLO, Ser 2007-1A, Cl D | ||||||

4.273%, 05/13/22 (A)(B)(C) | 1,070,000 | 470,800 | ||||

Stanfield Azure CLO | ||||||

N/A%, 05/27/20 (A)(C)(I) | 5,000,000 | 750,000 | ||||

Stanfield Bristol CLO, Ser 2005-1A, Cl B1 | ||||||

1.073%, 10/15/19 (A)(B)(C) | 6,000,000 | 3,960,000 | ||||

Stanfield Daytona CLO, Ser 2007-1A | ||||||

N/A%, 04/27/21 (C)(I) | 5,000,000 | 1,600,000 | ||||

Stanfield Veyron CLO, Ser 2006-1A, Cl D | ||||||

1.884%, 07/15/18 (A)(B)(C) | 100,000 | 48,500 | ||||

Stone Tower CDO, Ser 2004-1A, Cl B1L | ||||||

3.031%, 01/29/40 (A)(B)(C) | 3,632,313 | 272,423 | ||||

Telos CLO, Ser 2006-1A, Cl D | ||||||

1.984%, 10/11/21 (A)(B)(C) | 8,000,000 | 2,800,000 | ||||

Telos CLO, Ser 2006-1A, Cl A2 | ||||||

0.684%, 10/11/21 (A)(B)(C) | 2,911,000 | 2,008,590 | ||||

Telos CLO, Ser 2006-1A, Cl C | ||||||

1.134%, 10/11/21 (A)(B)(C) | 7,000,000 | 3,255,000 | ||||

Telos CLO, Ser 2007-2A, Cl D | ||||||

2.484%, 04/15/22 (A)(B)(C) | 12,000,000 | 4,800,000 | ||||

Tralee CDO, Ser 2007-1A, Cl C | ||||||

1.784%, 04/16/22 (A)(B)(C) | 6,000,000 | 2,880,000 | ||||

Tralee CDO, Ser 2007-1X, Cl COM3 | ||||||

1.274%, 04/16/22 (C) | 7,000,000 | 1,960,000 | ||||

Venture CDO, Ser 2006-7A, Cl C | ||||||

0.984%, 01/20/22 (A)(B)(C) | 4,000,000 | 2,400,000 | ||||

Venture CDO, Ser 2006-7A, Cl A1B | ||||||

0.614%, 01/20/22 (A)(B)(C) | 3,690,000 | 3,021,741 | ||||

Waterfront CLO, Ser 2007-1A, Cl A2 | ||||||

0.684%, 08/02/20 (A)(B)(C) | 8,750,000 | 6,650,000 | ||||

Waterfront CLO, Ser 2007-1A, Cl A3 | ||||||

0.834%, 08/02/20 (A)(B)(C) | 9,500,000 | 6,840,000 | ||||

Westwood CDO, Ser 2007-2A, Cl A2 | ||||||

0.632%, 04/25/22 (A)(B)(C) | 5,000,000 | 3,400,000 | ||||

Westwood CDO, Ser 2007-2A, Cl C | ||||||

0.982%, 04/25/22 (A)(B)(C) | 10,123,218 | 4,555,448 | ||||

White Horse II | ||||||

14.510%, 06/15/17 (A)(B)(C) | 6,000,000 | 1,500,000 | ||||

Wind River CLO, Ser 2004-1A, Cl B1 | ||||||

1.353%, 12/19/16 (A)(B)(C) | 3,245,000 | 2,206,600 | ||||

Total Asset-Backed Securities (Cost $231,764,384) | 284,944,211 | |||||

5

Table of Contents

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2009

Description | Shares/Cost | Fair Value | |||

MONEY MARKET FUND — 9.3% | |||||

UNITED STATES — 9.3% | |||||

SEI Daily Income Trust Prime Obligation Fund, Cl A, 0.110% (E)(F) (Cost $29,705,590) | 29,705,590 | $ | 29,705,590 | ||

HEDGE FUNDS — 7.4% | |||||

CAYMAN ISLANDS — 7.4% | |||||

Ares Enhanced Credit Opportunities Fund, L.P.(D)(H)(I) | 9,000,000 | 8,305,101 | |||

Goldentree Credit Opportunities Fund, L.P.(D)(H)(I) | 7,500,000 | 6,568,133 | |||

Highland Financial Partners, L.P.(D)(G)(I) | 7,500,000 | — | |||

Stone Tower Credit Fund, L.P. (D) | 10,000,000 | 8,786,430 | |||

| 23,659,664 | |||||

Total Hedge Funds (Cost $34,000,000) | 23,659,664 | ||||

Total Investments — 106.0% (Cost $295,469,974) | $ | 338,309,465 | |||

The following restricted securities were held by the Fund as of December 31, 2009:

| Acquisition Date | Cost | Fair Value | % of Partners’ Capital | First Available Redemption Date | Liquidity Frequency | ||||||||||

Ares Enhanced Credit Opportunities Fund, L.P. | 5/1/2008 | $ | 9,000,000 | $ | 8,305,101 | 2.6 | % | 6/30/2011 | Quarterly | ||||||

Goldentree Credit Opportunities Fund, L.P. | 12/4/2007 | 7,500,000 | 6,568,133 | 2.0 | % | 12/31/2010 | Semi-Annual | ||||||||

Highland Financial Partners, L.P. | 6/11/2008 | 7,500,000 | — | 0.0 | % | N/A - Fund in liquidation | N/A - Fund in liquidation | ||||||||

Stone Tower Credit Fund, L.P. | 8/1/2008 | 10,000,000 | 8,786,430 | 2.8 | % | 3/31/2010 | Quarterly | ||||||||

Percentages based on Partners’ Capital of $319,274,003.

CDO — Collateralized Debt Obligation

CIFC — Commercial Industrial Finance Corporation

Cl — Class

CLO — Collateralized Loan Obligation

L.P. — Limited Partnership

Ser — Series

6

Table of Contents

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2009

| (A) | Variable rate security. The rate reported is the effective rate as of December 31, 2009. |

| (B) | Securities sold within terms of a private placement memorandum, exempt from registration under Section 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in that program or other “accredited investors.” |

| (C) | Securities considered illiquid. The total value of such securities as of December 31, 2009 was $284,944,211 and represented 89.3% of Partners’ Capital. |

| (D) | Security considered restricted. |

| (E) | Rate shown is the 7-day effective yield as of December 31, 2009. |

| (F) | Investment in affiliated security. |

| (G) | Hedge Fund is in liquidation. Distributions from the Hedge Fund in liquidation may be received at anytime, subject to the discretion of the Hedge Fund. |

| (H) | The selected class of Hedge Fund is still in its initial lock – up period. Redemptions may be delayed until the Hedge Fund exits this period. |

| (I) | Non – Income Producing Security |

The following is a summary of the inputs used as of December 31, 2009 in valuing the Fund’s investments carried at value:

| Investments in Securities | Level 1 | Level 2 | Level 3 | Total | ||||||||

Asset-Backed Securities | $ | — | $ | — | $ | 284,944,211 | $ | 284,944,211 | ||||

Hedge Funds | — | 8,786,430 | 14,873,234 | 23,659,664 | ||||||||

Money Market Fund | 29,705,590 | — | — | 29,705,590 | ||||||||

Total Investments in Securities | $ | 29,705,590 | $ | 8,786,430 | $ | 299,817,445 | $ | 338,309,465 | ||||

The following is a reconciliation of the investments in which significant unobservable inputs (Level 3) were used in determining value:

| Asset-Backed Securities | Hedge Funds(1) | |||||

Beginning balance as of January 1, 2009 | $ | 38,380,689 | $ | 6,205,980 | ||

Accrued discounts/premiums | 6,413,131 | — | ||||

Realized gain/(loss) | 66,811,730 | — | ||||

Change in unrealized appreciation/(depreciation) | 119,191,415 | 7,167,254 | ||||

Net purchases/sales | 50,665,119 | 1,500,000 | ||||

Net transfer in and/or out of Level 3 | 3,482,127 | — | ||||

Ending balance as of December 31, 2009 | $ | 284,944,211 | $ | 14,873,234 | ||

Changes in unrealized gains/ (losses) included in earnings related to securities still held at reporting date | $ | 41,329,964 | $ | 7,167,254 | ||

| (1) | The beginning balance of the Level 3 fair value measurements have been restated due to additional guidance related to liquidity provided by hedge funds as provided within ASU No. 2009-12 “Investments in Certain Entities That Calculated Net Asset Value per Share (or its Equivalent).” |

For more information on valuation inputs, see Note 2 — Significant Accounting Policies in Notes to Financial Statements.

Amounts designated as “—”are zero or have been rounded to zero.

See accompanying notes to the financial statements.

7

Table of Contents

SEI Structured Credit Fund, L.P.

Statement of Assets and Liabilities

December 31, 2009

Assets | |||

Investments, at fair value (cost $265,764,384) | $ | 308,603,875 | |

Affiliated investment, at fair value (cost $29,705,590) | 29,705,590 | ||

Interest receivable from investments | 1,094,067 | ||

Total assets | $ | 339,403,532 | |

Liabilities | |||

Redemptions payable | $ | 20,000,000 | |

Administration fees payable | 28,275 | ||

Other liabilities | 101,254 | ||

Total liabilities | 20,129,529 | ||

Partners’ capital | |||

Limited partners’ capital | 319,274,003 | ||

Total liabilities and partners’ capital | $ | 339,403,532 | |

See accompanying notes.

8

Table of Contents

SEI Structured Credit Fund, L.P.

Statement of Operations

For the year ended December 31, 2009

Investment income | ||||

Interest income | $ | 15,581,536 | ||

Income from affiliate | 52,990 | |||

| 15,634,526 | ||||

Expenses | ||||

Administration fee | 196,374 | |||

Professional fees | 123,420 | |||

Directors’ fees | 22,500 | |||

Miscellaneous expenses | 233,562 | |||

Total expenses | 575,856 | |||

Less: Administration fee waiver | (10,153 | ) | ||

Net expenses | 565,703 | |||

Net investment income | 15,068,823 | |||

Net realized and unrealized gain on investments | ||||

Net realized gain on investments | 70,735,025 | |||

Net change in unrealized appreciation on investments | 135,850,833 | |||

Net realized and unrealized gain on investments | 206,585,858 | |||

Net increase in partners’ capital resulting from operations | $ | 221,654,681 | ||

See accompanying notes.

9

Table of Contents

SEI Structured Credit Fund, L.P.

Statement of Changes in Partners’ Capital

| For the year ended December 31, 2009 | For the year ended December 31, 2008 | |||||||

From operations | ||||||||

Net investment income | $ | 15,068,823 | $ | 10,834,719 | ||||

Net realized gain on investments | 70,735,025 | 364,266 | ||||||

Net change in unrealized appreciation (depreciation) on investments | 135,850,833 | (93,212,134 | ) | |||||

Net increase (decrease) in partners’capital resulting from operations | 221,654,681 | (82,013,149 | ) | |||||

Partners’ capital transactions | ||||||||

Capital contributions | 44,884,375 | 129,891,587 | ||||||

Capital redemptions | (20,157,850 | ) | (20,000 | ) | ||||

Net increase in partners’ capital derived from capital transactions | 24,726,525 | 129,871,587 | ||||||

Net increase in partners’ capital | 246,381,206 | 47,858,438 | ||||||

Partners’ capital beginning of year | 72,892,797 | 25,034,359 | ||||||

Partners’ capital end of year | $ | 319,274,003 | $ | 72,892,797 | ||||

See accompanying notes.

10

Table of Contents

SEI Structured Credit Fund, L.P.

Statement of Cash Flows

For the year ended December 31, 2009

Cash flows from operating activities | ||||

Net increase in partners’ capital resulting from operations | $ | 221,654,681 | ||

Adjustments to reconcile net increase in partners’ capital resulting from operations to net cash used in operating activities: | ||||

Purchases of long-term investments | (287,991,628 | ) | ||

Proceeds from sales of long-term investments | 247,074,102 | |||

Amortization | (6,419,386 | ) | ||

Net purchases of short-term investments | (19,830,045 | ) | ||

Net realized gain on investments | (70,735,025 | ) | ||

Net change in unrealized appreciation (depreciation) on investments | (135,850,833 | ) | ||

Decrease in interest receivable | 1,033,123 | |||

Decrease in payable for investment securities purchased | (705,000 | ) | ||

Increase in administration fees payable | 15,175 | |||

Increase in other accrued expenses | 20,418 | |||

Net cash used in operating activities | (51,734,418 | ) | ||

Cash flows from financing activities | ||||

Capital contributions | 39,884,375 | |||

Capital redemptions | (157,850 | ) | ||

Net cash provided by financing activities | 39,726,525 | |||

Net decrease in cash and cash equivalents | (12,007,893 | ) | ||

Cash and cash equivalents | ||||

Beginning of year | 12,007,893 | |||

End of year | $ | — | ||

Supplemental disclosure of non-cash financing activities: | ||||

Capital contributions received in advance from previous year | 5,000,000 | |||

Transfer of capital to redemption payable | (20,000,000 | ) | ||

See accompanying notes.

11

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements

December 31, 2009

1. Organization

SEI Structured Credit Fund, LP (the “Fund”) is a Delaware limited partnership established on June 26, 2007 and commenced operations on August 1, 2007. The Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”) as a closed-end, non-diversified, management investment company. The Fund offers limited partnership interests (“Interests”) of the Fund solely through private placement transactions to investors (“limited partners”) that have signed an investment management agreement with SEI Investments Management Corporation (“SIMC” or the “Adviser”), the investment adviser to the Fund. SEI Structured Credit Segregated Portfolio (the “Segregated Portfolio”), has invested substantially all of its assets into the Fund. As of December 31, 2009, the Segregated Portfolio owned 79.7% of the Fund; while the remaining limited partner owned 20.3% of the Fund.

The Fund’s objective is to seek to generate high total returns. There can be no assurance that the Fund will achieve its objective. The Fund pursues its investment objective by investing in a portfolio comprised of collateralized debt obligations (“CDOs”) and other structured credit investments. CDOs involve special purpose investment vehicles formed to acquire and manage a pool of loans, bonds and/or other fixed income assets of various types. CDOs fund their investments by issuing several classes of securities, the repayment of which is linked to the performance of the underlying assets, which serve as collateral for certain securities issued by the CDO. In addition to CDOs, the Fund’s investments may include fixed income securities, loan participations, credit-linked notes, medium term notes, registered and unregistered investment companies or pooled investment vehicles, and derivative instruments, such as credit default swaps and total return swaps (collectively with CDOs, “Structured Credit Investments”).

SEI Investment Strategies, LLC (the “General Partner”), a Delaware limited liability company, serves as the General Partner to the Fund and has no investment in the Fund as of December 31, 2009. The General Partner has delegated the management and control of the business and affairs of the Fund to the Board of Directors (the “Board”). A majority of the Board is and will be persons who are not “interested persons” (as defined in the 1940 Act) with respect to the Fund.

12

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

2. Significant Accounting Policies

Financial Accounting Standards Board (“FASB”) has issued FASB ASC 105 (formerly FASB Statement No. 168), The FASB Accounting Standards Codification and the Hierarchy of Generally Accepted Accounting Principles (“ASC 105”). ASC 105 established the FASB Accounting Standards Codification (“Codification” or “ASC”) as the single source of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by non-governmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal securities laws are also sources of authoritative GAAP for SEC registrants. The Codification supersedes all existing non-SEC accounting and reporting standards. All other non-grandfathered, non-SEC accounting literature not included in the Codification will become non-authoritative.

Following the Codification, the FASB will not issue new standards in the form of Statements, FASB Staff Positions or Emerging Issues Task Force Abstracts. Instead, it will issue Accounting Standards Updates, which will serve to update the Codification, provide background information about the guidance and provide the basis for conclusions on the changes to the Codification.

GAAP is not intended to be changed as a result of the FASB’s Codification project, but it will change the way the guidance is organized and presented. As a result, these changes will have a significant impact on how companies reference GAAP in their financial statements and in their accounting policies for financial statements issued for interim and annual periods ending after September 15, 2009. The Fund has implemented the Codification as of December 31, 2009.

The following is a summary of significant accounting policies followed by the Fund:

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Management believes that the estimates utilized in preparing the Fund’s financial statements are reasonable and prudent; however, actual results could differ from these estimates and is reasonably possible that differences could be material.

13

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

2. Significant Accounting Policies (continued)

Fair Value of Financial Instruments

The fair value of the Fund’s assets and liabilities, which qualify as financial instruments approximates the carrying amounts presented on the Statement of Assets and Liabilities. At any given time, fair value of financial investments could be materially different from market value of the investments.

Valuation of Investments

CDOs and other structured credit investments are priced based upon valuations provided by independent, third party pricing agents using their proprietary valuation methodology. The third-party pricing agents may value structured credit investments at an evaluated bid price by employing methodologies that utilize actual market transactions, broker-supplied valuations, or other methodologies designed to identify the market value for such securities. Such methodologies generally consider such factors as security prices, yields, maturities, call features, ratings and developments relating to specific securities in arriving at valuations.

If a price for a CDO or other structured credit investment cannot be obtained from an independent, third-party pricing agent, the Fund shall seek to obtain a bid price from at least one independent broker. In such cases, it is possible that the independent broker providing the price on the CDO or structured credit investment is also a market maker, and in many cases the only market maker, with respect to that security. As of December 31, 2009 all of asset-backed securities are valued by an independent broker who is also a market maker.

Debt obligations with remaining maturities of sixty days or less may be valued at their amortized cost, which approximates fair value.

14

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

2. Significant Accounting Policies (continued)

Valuation of Investments (continued)

Securities for which market prices are not “readily available” or may be unreliable are valued in accordance with Fair Value Procedures established by the Board. The Fund’s Fair Value Procedures are implemented through a Fair Value Committee (the “Committee”) designated by the Board. When a security is valued in accordance with the Fair Value Procedures, the Committee will determine the value after taking into consideration relevant information reasonably available to the Committee.

Examples of factors the Committee may consider are: the last trade price, the performance of the market or of the issuer’s industry, the liquidity of the security, the size of the holding in the Fund, or any other appropriate information. The determination of a security’s fair value price often involves the consideration of a number of subjective factors, and is therefore subject to the unavoidable risk that the value assigned to a security may be higher or lower than the security’s value would be if a reliable market quotation for the security was readily available. At December 31, 2009, there were no securities that were fair valued by the Committee.

Certain structured credit investments may be structured as private investment partnerships. Traditionally, a trading market for holdings of this type does not exist. The fair value of the Fund’s interest in such a private investment fund will represent the amount that the Fund could reasonable expect to receive from the private investment fund if the Fund’s interest were sold at the time of valuation, determined based on information reasonably available at the time the valuation is made and that the Fund believes to be reliable. Unless determined otherwise in accordance with the Fund’s fair value procedures, the fair value of the Fund’s interest in a private investment fund will usually be the value attributed to such interest, as of that time of valuation, as reported to the Fund by the private investment fund’s manager, administrator, or other designed agent. As a practical matter, the Adviser and the Board have little or no means of independently verifying the valuations provided by such private investment funds. In the unlikely event that a private investment fund does not report a value to the Fund on a timely basis and such fund is not priced by independent pricing agents of the Fund, the Fund would determine the fair value of the private investment fund based on the most recent value reported by the private investment fund, as well as any other relevant information available at the time the Fund values its portfolio. As of December 31, 2009, the Fund held the attributed fair value of approximately $23,700,000 in investment funds.

15

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

2. Significant Accounting Policies (continued)

The Board will periodically review the Fund’s valuation policies and will update them as necessary to reflect changes in the types of securities in which the Fund invests.

In accordance with the authoritative guidance on fair value measurements and disclosure under GAAP, ASC 820 (formerly FASB Statement No. 157), the Fund discloses the fair value of their investments in a hierarchy that prioritizes the inputs to valuation techniques used to measure the fair value. The objective of a fair value measurement is to determine the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (an exit price). Accordingly, the fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). The three levels of the fair value hierarchy under ASC 820 are described below:

Level 1 – Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the funds have has the ability to access at the measurement date;

Level 2 – Quoted prices which are not active, or inputs that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and

Level 3 – Prices, inputs or exotic modeling techniques which are both significant to the fair value measurement and unobservable (supported by little or no market activity).

Investments are classified within the level of the lowest significant input considered in determining fair value. Investments classified within Level 3 whose fair value measurement considers several inputs may include Level 1 or Level 2 inputs as components of the overall fair value measurement.

For the year ended December 31, 2009, there have been no significant changes to the Fund’s fair valuation methodologies.

In September 2009, the FASB issued Accounting Standards Update (“ASU”) No. 2009-12, “Investments in Certain Entities That Calculate Net Asset Value per Share (or Its Equivalent”). ASU No. 2009-12 provides guidance about using net asset value to measure the fair value of interests in certain investments and requires additional disclosures about interests in investments. The Fund adopted ASU No. 2009-12 during the year ended December 31, 2009. Since the Fund’s current fair value measurement policies are consistent with ASU No. 2009-12, adoption did not affect the Fund’s financial condition, results of operations or cash flows.

16

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

2. Significant Accounting Policies (continued)

Income Recognition and Security Transactions

Security transactions are recorded on the trade date. Costs used in determining net realized capital gains and losses on the sale of securities are on the basis of specific identification. Dividend income is recognized on the ex-dividend date, and interest income is recognized using the accrual basis of accounting. Amortization and accretion is calculated using the scientific interest method, which approximates the effective interest method over the holding period of the security. Amortization of premiums and discounts are included in interest income.

Collateralized Debt Obligations

The Fund invests in CDOs which include collateralized loan obligations (“CLOs”) and other similarly structured securities. CLOs are a type of asset-backed security. A CLO is a trust typically collateralized by a pool of loans, which may include, among others, domestic and foreign senior secured loans, senior unsecured loans, and subordinate corporate loans, including loans that may be rated below investment grade or equivalent unrated loans. CDOs may charge management fees and administrative expenses. For CDOs, the cashflows from the trust are split into two or more portions, called tranches, varying in risk and yield. The riskiest portion is the “equity” tranche which bears the bulk of defaults from the bonds or loans in the trust and serves to protect the other, more senior tranches from default in all but the most severe circumstances. Since it is partially protected from defaults, a senior tranche from a CDO trust typically has a higher rating and lower yield than their underlying securities, and can be rated investment grade. Despite the protection from the equity tranche, CDO tranches can experience substantial losses due to actual defaults, increased sensitivity to defaults due to collateral default and disappearance of protecting tranches, market anticipation of defaults, as well as aversion to CDO securities as a class.

The risks of an investment in a CDO depend largely on the type of the collateral securities and the class of the CDO in which the Fund invests. Normally, CLOs and other CDOs are privately offered and sold, and thus, are not registered under the securities laws. As a result, investments in CDOs may be characterized by the Fund as illiquid securities; however, an active dealer market may exist for CDOs, allowing a CDO to qualify for Rule 144A transactions.

17

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

2. Significant Accounting Policies (continued)

Collateralized Debt Obligations (continued)

In addition to the normal risks associated with fixed income securities (e.g., interest rate risk and default risk), CDOs carry additional risks including, but not limited to: (i) the possibility that distributions from collateral securities will not be adequate to make interest or other payments; (ii) the quality of the collateral may decline in value or default; (iii) the funds may invest in CDOs that are subordinate to other classes; and (iv) the complex structure of the security may not be fully understood at the time of investment and may produce disputes with the issuer or unexpected investment results.

Federal Taxes

The Fund intends to be treated as a partnership for federal, state, and local income tax purposes. The Partners are responsible for the tax liability or benefit relating to its distributive share of taxable income or loss. Accordingly, no provision for federal, state, or local income taxes is reflected in the accompanying financial statements.

For the year ended December 31, 2009, in accordance with the accounting guidance provided in the AICPA Audit and Accounting Guide, “Audits of Investment Companies,” the Fund reclassified $15,068,823 and $70,735,025 from accumulated net investment income and accumulated net realized gain, respectively, to net partners’ capital. The reclassification was to reflect, as an adjustment to net partners’ capital, the amount of taxable income that has been allocated to the Partners and has no effect on net assets.

The Fund evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether it is “more-likely-than-not” (i.e., greater than 50-percent) that each tax position will be sustained upon examination by a taxing authority based on the technical merits of the position. Tax positions not deemed to meet the more-likely-than-not threshold are recorded as a tax benefit or expense in the current year. The Fund did not record any tax provisions in the current period. However, management’s conclusions regarding tax positions taken may be subject to review and adjustment at a later date based on factors including, but not limited to, examination by tax authorities (i.e., the last 3 tax year ends, as applicable), on-going analysis of and changes to tax laws, regulations and interpretations thereof.

18

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

2. Significant Accounting Policies (concluded)

Indemnifications

The Fund enters into contracts that contain a variety of indemnifications. The Fund’s maximum exposure under these arrangements is unknown. However, since inception the Fund has not had claims or losses pursuant to these contracts and expects the risk of loss to be remote.

Restricted Securities

At December 31, 2009, the Fund owned private placement investments that were purchased through private offerings or acquired through initial public offerings and cannot be sold without prior registration under the Securities Act of 1933 or pursuant to an exemption therefrom. In addition, the Fund has generally agreed to further restrictions on the disposition of certain holdings as set forth in various agreements entered into in connection with the purchase of this investment. These investments are valued at fair value as determined in accordance with the procedures approved by the Board. For the acquisition dates, cost and fair value of these investments, along with their liquidity terms at December 31, 2009, see the Schedule of Investments.

3. Adviser, Administrator and Other Transactions

The Adviser does not charge a management fee to the Fund. Limited partners are responsible for paying the fees of the Adviser directly under their individual investment management agreement with the Adviser. Each agreement sets forth the fees to be paid to the Adviser, which are ordinarily expressed as a percentage of the limited partners assets managed by the Adviser. This fee, which is negotiated between the limited partner and the Adviser, may include a performance-based fee and/or a fixed-dollar fee for certain specified services.

The Adviser has voluntarily agreed that certain expenses of the Fund, including custody fees and administrative fees, calculated monthly, shall not in the aggregate exceed 0.50% per annum of the Fund’s net asset value, and the Adviser or its affiliates will waive Fund fees or reimburse Fund expenses to the extent necessary so that such 0.50% limit is not exceeded. The following expenses of the Fund are specifically excluded from the expense limit: organizational expenses; extraordinary, non-recurring and certain other unusual expenses; taxes and fees; and expenses incurred indirectly by the Fund through its investments in Structured Credit Investments. The Adviser may discontinue all or part of this waiver at any time.

19

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

3. Adviser, Administrator and Other Transactions (continued)

SEI Global Services, Inc. (the “Administrator”), serves as the Fund’s administrator. The Administrator is a wholly-owned subsidiary of SEI Investments Company. The Administrator provides certain administrative, accounting, and transfer agency services to the Fund. The services to be performed by the Administrator may be completed by one or more of its affiliated companies. The Fund pays the Administrator a fee equal to 0.10% (on an annualized basis) of the Fund’s Net Asset Value which is accrued monthly based on month-end net assets and is paid monthly, and reimburses the Administrator for certain out-of-pocket expenses.

SEI Investments Distribution Co. (the “Placement Agent”) serves as the Fund’s placement agent pursuant to an agreement with the Fund. The Placement Agent is a wholly owned subsidiary of SEI Investments Company. The Placement Agent was not compensated by the Fund for its services rendered under the agreement.

4. Allocation of Profits and Losses

The Fund maintains a separate capital account for each of its limited partners. As of the last day of each month, the Fund shall allocate net profits or losses for that month to the capital accounts of all limited partners, in proportion to their respective opening capital account balances for such month (after taking into account any capital contributions deemed to be made as of the first day of such month).

5. Partners’ Capital

The Fund, in the discretion of the Board, may sell interests to new limited partners and may allow existing limited partners to purchase additional Interests in the Fund on such days as are determined by the Board in its sole discretion. It is the Fund’s intention to allow limited purchases of Interests only during designated subscriptions periods as may be established by the Board or its designees (currently, the Adviser) and communicated to limited partners. The Board or its designee will determine the amount of Interests offered to limited partners during a subscription period at its discretion. During the established subscription periods, interests may be purchased on a business day, or at such other times as the Board may determine, at the offering price (which is net asset value). The Fund may discontinue its offering at any time.

20

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

5. Partners’ Capital (continued)

The Fund is a closed-end investment company, and therefore no limited partner will have the right to require the Fund to redeem its Interests. The Fund from time to time may offer to repurchase outstanding Interests pursuant to written tenders by limited partners. Repurchase offers will be made at such times and on such terms as may be determined by the Board in its sole discretion. In determining whether the Fund should repurchase Interests from limited partners pursuant to written tenders, the Board will consider the recommendations of the Adviser.

The Adviser expects that it will recommend to the Board that the Fund offer to repurchase interests four times each year, as of the last business day of March, June, September, and December. However, limited partners will not be permitted to tender for repurchase interests that were acquired less than two years prior to the effective date of the proposed repurchase.

Even after the initial two year period, it is possible that there will be extended periods during which illiquidity in the underlying investments held by the Fund or other factors will cause the Board to elect not to conduct repurchase offers. Such periods may coincide with periods of negative performance. In addition, even in the event of a repurchase offer, it is possible that there will be an oversubscription to the repurchase offer, in which case an Investor may not be able to redeem the full amount that the Investor wishes to redeem.

6. Investment Transactions

The cost of security purchases and proceeds from the sale and maturity of securities, other than temporary cash investments, during the year ended December 31, 2009 were $287,991,628 and $240,654,716 (net of amortization), respectively.

As of December 31, 2009, the aggregate cost of investments for tax purposes was expected to be similar to book cost of $295,469,974. Net unrealized appreciation on investments for tax purposes was $42,839,491 consisting of $80,569,117 of gross unrealized appreciation and $37,729,626 of gross unrealized depreciation.

21

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

7. Concentrations of Risk

In the normal course of business, the Fund trades various financial instruments and enters into various investment activities with off-balance sheet risk. The Fund’s satisfaction of the obligations may exceed the amount recognized in the statement of assets and liabilities.

(a) Market risk

Market risk encompasses the potential for both losses and gains and includes price risk and interest rate risk. The Fund’s market risk management strategy is driven by the Fund’s investment objective. The investment manager oversees each of the risks in accordance with policies and procedures.

(i) Price risk

Price risk is the risk the value of the instrument will fluctuate as a result of changes in market prices, whether caused by factors specific to an individual investment, its issuer or any factor affecting financial instruments traded in the market. As all of the Fund’s financial instruments are carried at fair value with fair value changes recognized in the Statement of Operations, all changes in market conditions directly affect net assets.

(ii) Interest rate risk

The fair value of the Fund’s investments will change in response to interest rate changes and other factors. During periods of falling interest rates, the values of fixed income securities generally rise. Conversely, during periods of rising interest rates, the values of such securities generally decline. Changes by recognized rating agencies in the ratings of any fixed income security and in the ability of an issuer to make payments of interest and principal may also affect the value of these investments.

(b) Counterparty credit risk

Counterparty credit risk is the risk a counterparty to a financial instrument could fail on a commitment that it has entered into with the Fund. The Fund minimizes counterparty credit risk by undertaking transactions with large well-capitalized counterparties or brokers and by monitoring the creditworthiness of these counterparties.

22

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

8. Financial Highlights

The following represents the ratios to average net assets and other supplemental information for the following periods:

| For the year ended December 31, 2009 | For the year ended December 31, 2008 | For the period August 1, 2007* through December 31, 2007 | ||||||||||

Total return(1) | 189.59 | % | (62.03 | )% | 5.82 | %(3) | ||||||

Partners’ capital, end of period (000’s) | $ | 319,274 | $ | 72,893 | $ | 25,034 | ||||||

Ratios to average partners’ capital † | ||||||||||||

Net investment income ratio | ||||||||||||

Net investment income, net of waivers | 8.11 | % | 18.28 | % | 9.13 | %(2) | ||||||

Expense ratio | ||||||||||||

Operating expenses, before waivers | 0.31 | % | 0.51 | % | 1.54 | %(2)(4) | ||||||

Operating expenses, net of waivers | 0.30 | % | 0.49 | % | 0.37 | %(2)(4) | ||||||

Portfolio turnover rate | 141.21 | % | 13.88 | % | 21.85 | %(3) | ||||||

| * | Commenced operations. |

| † | Ratios do not include the Fund’s allocated share of income/expense from hedge funds. |

| (1) | Total return is calculated for all the limited partners taken as a whole. A limited partner’s return may vary from these returns based on the timing of capital transactions. |

| (2) | Annualized. |

| (3) | Not annualized. |

| (4) | Expense ratios include offering costs and tax liability costs, which are not annualized. Had the offering costs and tax liability costs been annualized, the ratio for “Operating expenses, before waivers” and “Operating expenses, net of waivers” would have been 1.67% and 0.50%, respectively. |

23

Table of Contents

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2009

9. New Accounting Pronouncement

In January 2010, the Financial Accounting standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No, 201 0-06 “Improving Disclosures about Fair Value Measurements”. ASU 2010-06 amends FASB Accounting Standards Codification Topic 820, Fair Value Measurements and Disclosures, to require additional disclosures regarding fair value measurements. Certain disclosures required by ASU No. 2010-06 are effective for interim and annual reporting periods beginning after December 15, 2009, and other required disclosures are effective for fiscal years beginning after December 15, 2010, and for interim periods within those fiscal yeas, Management is currently evaluating the impact ASU No. 2010-06 will have on its financial statement disclosures.

10. Subsequent Event

The Fund has evaluated the need for additional disclosures and/or adjustments resulting from subsequent events through March 1, 2010, the date the financial statements were issued. On January 29, 2010, the Fund paid redemptions of $20,000,000. On February 1, 2010, the Fund paid a capital distribution of $95,000,000.

24

Table of Contents

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited)

December 31, 2009

Set forth below are the Names, Age, Addresses, Position with the Partnership, Length of Time Served, the Principal Occupations During the Past Five Years, Number of Portfolios in Fund Complex Overseen by the Director, and Other Directorships Outside the Fund Complex of each of the persons currently serving as Directors and Officers of the Partnership. The Partnership’s Statement of Additional Information (“SAI”) includes additional information about the Directors and Officers. The SAI may be obtained without charge by calling 1-800-342-5734.

Name, Age and Address of Independent Directors | Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of Portfolios in Fund Complex Overseen by Director** | Other Directorships Held by Director | ||||

Nina Lesavoy (52) 840 Park Avenue New York, NY 10021 | Since 2007 | Founder & Managing Director, Avec Capital since April 2008, Partner, Cue Capital since 2002. | 80 | Trustee of SEI Alpha Strategy Portfolios, L.P., SEI Opportunity Fund, L.P.,(until September 2009) SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Institutional Investments Trust, SEI Tax Exempt Trust, and SEI Institutional Managed Trust. |

25

Table of Contents

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (continued)

December 31, 2009

Name, Age and Address of Independent Directors | Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of in Fund Complex Overseen by Director** | Other Directorships Held by Director | ||||

George J. Sullivan (67) 7 Essex Green Drive, Suite 52B Peabody, MA 01960 | Since 2007 | Self Employed Consultant, Newfound Member of independent review | 80 | Trustee of State Street Navigator Securities Lending Trust, The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II (f/k/a The Arbor Fund), Bishop Street Funds, SEI Alpha Strategy Portfolios, L.P., SEI Opportunity Fund, L.P., (until September 2009) SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional Investments Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust, and SEI Institutional Managed Trust. |

26

Table of Contents

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (continued)

December 31, 2009

Name, Age and Address of Independent Directors | Length of Served | Principal Occupation(s) During Past 5 Years | Number of | Other Directorships Held by Director | ||||

James M. Williams (62) 1200 Getty Drive, Suite 400, Los Angeles, CA 90049-1681 | Since 2007 | Vice President and Chief Investment Officer, J. Paul Getty Trust, Non Profit Foundation for Visual Arts, since December 2002 | 80 | Trustee of Ariel Mutual Funds, SEI Alpha Strategy Portfolios, L.P., SEI SEI Tax Exempt Trust, and SEI Institutional Managed Trust. |

27

Table of Contents

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (continued)

December 31, 2009

Name, Age and Address of Independent Directors | Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of Portfolios in Fund Complex Overseen by Director** | Other Directorships Held by Director | ||||

Robert A. Nesher* (63) One Freedom Valley Drive Oaks, PA 19456 | Since 2007 | President of the Fund, Chairman of the Board, SEI Funds and The Advisor’s Inner Circle Fund. Currently performs various services on behalf of SEI Investments for which Mr. Nesher is compensated. | 80 | Trustee of The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II (f/k/a The Arbor Fund) and Bishop Street Funds; Director of SEI Global Master Fund, plc, SEI Global Assets Fund, plc, SEI Global Investments Fund, plc, SEI Islamic Investments Fund, plc, SEI Investments Global, Limited, SEI Investments – Global Fund Services Limited, SEI Investments (Europe) Limited, SEI Investments – Unit Trust Management (UK) Limited, SEI Global Nominee Ltd, SEI Alpha Strategy Portfolios, L.P., SEI Opportunity Fund, L.P., (until September 2009) SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional Investments Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust, and SEI Institutional Managed Trust. |

28

Table of Contents

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (continued)

December 31, 2009

Name and Age of Officers | Position(s) Held with the Master Fund and Length of Time Served | Principal Occupation(s) During Past 5 Years | ||

| Stephen F. Panner (39) | Treasurer, since June 2008 | Fund Accounting Director of the Administrator, 2005-present. Fund Administration Manager, Old Mutual Fund Services, 2000-2005. Chief Financial Officer, Controller and Treasurer, PBHG Funds and PBHG Insurance Series Fund, 2004-2005. Assistant Treasurer, PBHG Funds and PBHG Insurance Series Funds and PBHG Insurance Series Fund, 2000-2004. Assistant Treasurer, Old Mutual Fund Advisors Fund, 2004-2005. | ||

| Timothy D. Barto (42) | Vice President, since 2007 and Assistant Secretary, since 2008 | General Counsel Vice President and Secretary of the Adviser since 2004. Vice President and Assistant Secretary of the Administrator since November 1999. | ||

| James Ndiaye (41) | Vice President since 2007 Secretary, December 2009 | Vice President and Assistant Secretary of Adviser since 2005; Vice President, Deutsche Asset Management, 2003 to 2004. | ||

29

Table of Contents

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (concluded)

December 31, 2009

Name and Age of Officers | Position(s) Held with the Master Fund and Length of Time Served | Principal Occupation(s) During Past 5 Years | ||

| Aaron Buser (39) | Vice President and Assistant Secretary, since June 2008 | Vice President and Assistant Secretary of Adviser since 2007. Associate at Stark & Stark 2004–2007. | ||

| Russell Emery (47) | Chief Compliance Officer, since 2007 | Chief Compliance Officer of SEI Opportunity Bishop Street Funds, The Advisors’ Inner Circle | ||

| * | Mr. Nesher is a trustee who may be deemed to be an “interested” person of the Fund as that term is defined in the 1940 Act by virtue of his affiliation with the Fund’s Distributor. |

| ** | The “Fund Complex” consists of registered investment companies that are part of the following investment trusts and limited partnerships: SEI Institutional Investments Trust, SEI Institutional Management Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Daily Income Trust, SEI Tax Exempt Trust, SEI Asset Allocation Trust, SEI Alpha Strategy Portfolios, L.P. and SEI Opportunity Fund, L.P. (until September 2009) |

30

Table of Contents

| Item 2. | Code of Ethics. |

The Registrant has adopted a code of ethics that applies to the Registrant’s Chief Executive Officer and its Chief Financial Officer. The Registrant has not made any amendments to this code of ethics during the period covered by this report, nor were there any waivers granted from a provision of the code of ethics. A copy of its code of ethics is filed with this Form N-CSR under

Item 12(a)(1).

| Item 3. | Audit Committee Financial Expert. |

| (a)(1) | The registrant’s board of directors has determined that the registrant has at least one audit committee financial expert serving on the audit committee. |

| (a)(2) | The audit committee financial expert is George Sullivan. Mr. Sullivan is independent as defined in Form N-CSR Item 3(a)(2). |

| Item 4. | Principal Accountant Fees and Services. |

Fees billed by Ernst & Young, LLP Related to the registrant.

Ernst & Young, LLP billed the registrant aggregate fees for services rendered to the registrant for the last two fiscal years as follows:

| 2009 | 2008 | |||||||||||||||

| All fees and services to the Fund that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | All fees and services to the Fund that were pre-approved | All fees and services to service affiliates that were pre-approved | All other fees and services to service affiliates that did not require pre-approval | |||||||||||

(a) | Audit Fees | $ | 70,000 | N/A | N/A | $ | 60,000 | N/A | N/A | |||||||

(b) | Audit-Related Fees | $ | 0 | N/A | N/A | $ | 0 | N/A | N/A | |||||||

(c) | Tax Fees | $ | 0 | N/A | N/A | $ | 0 | N/A | N/A | |||||||

(d) | All Other Fees | $ | 0 | N/A | N/A | $ | 0 | N/A | N/A | |||||||

Notes:

| (1) | Audit fees include amounts related to the audit of the registrant’s annual financial statements and services normally provided by the accountant in connection with statutory and regulatory filings. |

| (2) | Other fees and services not requiring pre-approval include amounts billed in fiscal year 2009 and 2008 related to services provided in connection with internal control reports issued pursuant to SAS No. 70. |

Table of Contents

| (e)(1) | The Fund’s Audit Committee has adopted and the Board of Directors has ratified an Audit and Non-Audit Services Pre-Approval Policy (the “Policy”), which sets forth the procedures and the conditions pursuant to which services proposed to be performed by the independent auditor of the Fund may be pre-approved. |

The Policy provides that all requests or applications for proposed services to be provided by the independent auditor must be submitted to the Registrant’s Chief Financial Officer (“CFO”) and must include a detailed description of the services proposed to be rendered. The CFO will determine whether such services:

| (1) | require specific pre-approval; |

| (2) | are included within the list of services that have received the general pre-approval of the Audit Committee pursuant to the Policy; or |

| (3) | have been previously pre-approved in connection with the independent auditor’s annual engagement letter for the applicable year or otherwise. In any instance where services require pre-approval, the Audit Committee will consider whether such services are consistent with SEC’s rules and whether the provision of such services would impair the auditor’s independence. |

Requests or applications to provide services that require specific pre-approval by the Audit Committee will be submitted to the Audit Committee by the CFO. The Audit Committee will be informed by the CFO on a quarterly basis of all services rendered by the independent auditor. The Audit Committee has delegated specific pre-approval authority to either the Audit Committee Chair or financial expert, provided that the estimated fee for any such proposed pre-approved service does not exceed $100,000 and any pre-approval decisions are reported to the Audit Committee at its next regularly scheduled meeting.

Services that have received the general pre-approval of the Audit Committee are identified and described in the Policy. In addition, the Policy sets forth a maximum fee per engagement with respect to each identified service that has received general pre-approval.

All services to be provided by the independent auditor shall be provided pursuant to a signed written engagement letter with the Registrant, the investment advisor or applicable control affiliate (except that matters as to which an engagement letter would be impractical because of timing issues or because the matter is small may not be the subject of an engagement letter) that sets forth both the services to be provided by the independent auditor and the total fees to be paid to the independent auditor for those services.

In addition, the Audit Committee has determined to take additional measures on an annual basis to meet its responsibility to oversee the work of the independent auditor and to assure the auditor’s independence from the Registrant, such as reviewing a formal written statement from the independent auditor delineating all relationships between the independent auditor and the Registrant, and discussing with the independent auditor its methods and procedures for ensuring independence.

| (e)(2) | Percentage of fees billed applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows: |

| Fiscal 2009 | Fiscal 2008 | |||||

Audit-Related Fees | 0 | % | 0 | % | ||

Tax Fees | 0 | % | 0 | % | ||

All Other Fees | 0 | % | 0 | % |

Table of Contents

| (f) | Not Applicable. |

| (g) | The aggregate non-audit fees and services billed by Ernst & Young, LLP for the fiscal years 2009 and 2008 were $0 and $0, respectively. |

| (h) | During the past fiscal year, Registrant’s principal accountant provided certain non-audit services to the Registrant’s investment adviser or to entities controlling, controlled by, or under common control with Registrant’s investment adviser that provide ongoing services to Registrant that were not subject to pre-approval pursuant to paragraph (c)(7)(ii) of Rule 2-01 of Regulation S-X. The audit committee of Registrant’s board of directors reviewed and considered these non-audit services provided by Registrant’s principal accountant to Registrant’s affiliates, including whether the provision of these non-audit services is compatible with maintaining the principal accountant’s independence. |

| Item 5. | Audit Committee of Listed Registrants. |

Not applicable

| Item 6. | Schedule of Investments. |

Included in Item 1.

| Item 7. | Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies. |

SEI INVESTMENTS MANAGEMENT CORPORATION PROXY VOTING PROCEDURES

Proxy Voting (Rule 206(4)-6)

Policy Statement: A public company’s shareholders typically have the right to vote on various corporate issues. Clients typically delegate to SEI Investments Management Corporation (“SIMC”) the authority to vote proxies for shares they own. Under the Advisers Act, SIMC has a duty of care and loyalty with respect to all services undertaken for clients, including proxy voting.

Rule 206(4)-6 under the Advisers Act requires that SIMC must vote proxies in a manner consistent with clients’ best interest and must not place its interests above those of its clients when doing so. It requires SIMC to: (i) adopt and implement written policies and procedures that are reasonably designed to ensure that SIMC votes proxies in the best interest of its clients, and (ii) to disclose to the clients how they may obtain information on how SIMC voted proxies. In addition, Rule 204-2 requires SIMC to keep records of proxy voting and client requests for information.

As a registered investment adviser, SIMC has an obligation to vote proxies with respect to securities held in its client portfolios in the best economic interests of the clients for which it has proxy voting authority.

Procedures: SIMC has adopted the following procedures to implement the firm’s policy and to monitor compliance with the firm’s policy:

1. Third Party Proxy Voting Service - SIMC has elected to retain a third party proxy voting service (the “Service”) to vote proxies with respect to those clients. The Service shall vote proxies in accordance with guidelines approved by SIMC’s Proxy Voting Committee (the “Guidelines”). The Guidelines set forth the manner in which SIMC shall vote, or the manner in which SIMC shall determine how to vote, with respect to various matters that may come up for shareholder vote. So long as the Service votes proxies in accordance with the Guidelines, SIMC believes that there is an appropriate presumption that the manner in which SIMC voted was not influenced by, and did not result from, a conflict of interest. SIMC Compliance shall conduct periodic reviews of the Service to ensure compliance with SIMC’s proxy voting guidelines and the appropriateness of the Service.

Table of Contents

2. Establishment of Proxy Voting Committee - SIMC shall establish a Proxy Voting Committee (the “Committee”), comprised of representatives of SIMC’s Investment Management Unit and Legal and/or Compliance personnel. Currently, the members of the Committee are as follows:

Eric Hoerdemann

Larry Vasquez

Aimei Zhong

Noreen Martin

Stephanie Cavanagh

Tom Williams

The membership of the Committee may be changed at any time upon approval of the existing members of the Committee or by the President of SIMC. The Committee shall meet as necessary to perform any of the activities set forth below. Any action requiring approval of the Committee shall be deemed approved upon an affirmative vote by a majority of the Committee present or represented. The submission of votes electronically (i.e., via email) by the Committee members shall be considered acceptable. The Committee shall consult with counsel or other experts as it deems appropriate to carry out its responsibilities.

3. Approval of Proxy Voting Guidelines - The Committee shall approve Guidelines that set forth the manner in which SIMC shall vote, or the manner in which SIMC shall determine how to vote, with respect to various matters that may come up for shareholder vote with respect to securities held in client accounts and for which SIMC has proxy voting responsibility. In the event that any employee of SIMC recommends a change to SIMC’s Guidelines, the Committee shall meet to consider the proposed change and consider all relevant factors. If approved by the Committee, the change shall be accepted, and the Guidelines revised accordingly.

4. Certain Proxy Votes May Not Be Cast - In some cases, the Committee may determine that it is in the best interests of SIMC’s clients to abstain from voting certain proxies. SIMC will abstain from voting in the event any of the following conditions {listed below} are met with regard to a proxy proposal:

| • | Neither the Proxy Voting Guidelines nor specific client instructions cover an issue; |

| • | The Service does not make a recommendation on the issue; |

| • | The Committee cannot convene on the proxy proposal at issue to make a determination as to what would be in the client’s best interest. This could happen, for example, if the Committee found that there was a material conflict or if despite all best efforts the Committee is unable to meet the requirements necessary to make a determination. |

In addition, it is SIMC’s policy not to vote proxies for accounts that engage in securities lending, SIMC believes that the additional income derived by clients from such activities generally outweighs the potential economic benefit of recalling securities for the purpose of voting. Therefore, SIMC generally will not recall securities on loan for the sole purpose of voting proxies. Further, in accordance with local law or business practices, many foreign companies prevent the sales of shares that have been voted for a certain period beginning prior to the shareholder meeting and ending on the day following the meeting (“share blocking”). Depending on the country in which a company is domiciled, the blocking period may begin a stated number of days prior to the meeting (e.g., one, three or five days) or on a date established by the company. While practices vary, in many countries the block period can be continued for a longer period if the shareholder meeting is adjourned and postponed to a later date. Similarly, practices vary widely as to the ability of a shareholder to have the “block” restriction lifted early (e.g., in some countries shares generally can be “unblocked” up to two days prior to the meeting whereas in other countries the removal of the block appears to be discretionary with the issuer’s transfer agent). SIMC believes that the disadvantage of being unable to sell the stock regardless of changing conditions generally outweighs the advantages of voting at the shareholder meeting for routine items. Accordingly, SIMC generally will not vote those proxies subject to “share blocking.”

Table of Contents