UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22107

SEI Structured Credit Fund, LP

(Exact name of Registrant as specified in charter)

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

Timothy Barto

c/o SEI Investments Management Corporation

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: (610) 676-2533

Date of fiscal year end: December 31, 2015

Date of reporting period: December 31, 2015

EXPLANATORY NOTE

Registrant is filing this amendment to its Form N-CSR for the fiscal year ended December 31, 2015, originally filed with the Securities and Exchange Commission on March 10, 2016 (Accession Number 0001193125-16-499847). The sole purpose of this filing is to include the signed audit opinion in Item 1, which was inadvertently omitted in the original filing. There were no other changes to the report and no issues with respect to the audit opinion at the time of the original filing.

Item 1. Reports to Stockholders.

SEI STRUCTURED CREDIT FUND, L.P.

Financial Statements

For the year ended December 31, 2015

With Report of Independent Registered Public Accounting Firm

SEI Structured Credit Fund, L.P.

Financial Statements

For the year ended December 31, 2015

| 1 | ||||

Audited Financial Statements | ||||

| 2 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

Additional Information (Unaudited) | ||||

| 27 | ||||

| 30 | ||||

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“Commission”) for the first and third quarters of each fiscal year on Form N-Q within sixty days after the end of the period. The Fund’s Form N-Q is available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling (888) 786-9977; and (ii) on the Commission’s website at http://www.sec.gov, no later than August 31st of each year.

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Shareholders of the SEI Structured Credit Fund, L.P.:

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations, of changes in limited partners’ capital and of cash flows and the financial highlights present fairly, in all material respects, the financial position of SEI Structured Credit Fund, L.P. (the “Fund”) at December 31, 2015, the results of its operations and its cash flows for the year then ended and the changes in its limited partner’s capital for each of the two years in the period then ended and the financial highlights for each of the two years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audit, which included confirmation of securities at December 31, 2015 by correspondence with the custodian and brokers, provides a reasonable basis for our opinion. The financial highlights presented for each of the three years in the period ended December 31, 2013 were audited by another independent registered public accounting firm whose report dated March 3, 2014 expressed an unqualified opinion on those statements and financial highlights.

February 29, 2016

PricewaterhouseCoopers LLP, Two Commerce Square, Suite 1800, 2001 Market Street, Philadelphia, PA 19103-7042

T: (267) 330-3000, F: (267) 330-3300, www.pwc.com/us

1

SEI Structured Credit Fund, L.P.

December 31, 2015

Description | Par Value | Fair Value | ||||||

ASSET-BACKED SECURITIES (A) — 99.6% | ||||||||

CAYMAN ISLANDS — 6.2% | ||||||||

Battalion CLO, Ser 2014-5A, Cl SUB | $ | 33,031,000 | $ | 9,909,300 | ||||

Benefit Street Partners CLO IV | 21,676,000 | 14,739,680 | ||||||

Benefit Street Partners CLO VIII | 18,340,000 | 16,506,000 | ||||||

Fortress Credit Opportunities CLO, Ser 2015-6A, Cl D | 2,000,000 | 1,944,400 | ||||||

Fortress Credit Opportunities CLO, Ser 2015-6A, Cl F | 8,300,000 | 7,727,300 | ||||||

Freidbergmilstein Private Capital Fund | 1,000,000 | 4,000 | ||||||

Highbridge Loan Management, Ser 2015-7A, Cl F | 2,000,000 | 1,580,560 | ||||||

Hildene CLO, Ser 2014-2A, Cl E | 6,000,000 | 4,934,400 | ||||||

Peaks CLO, Ser 2014-1A, Cl D | 2,750,000 | 2,502,500 | ||||||

Venture CDO, Ser 2012-11A, Cl SUB | 12,500,000 | 5,250,000 | ||||||

Zais Investment Grade IX, Ser 9A, Cl B | 18,000,000 | 15,975,000 | ||||||

|

| |||||||

| 81,073,140 | ||||||||

|

| |||||||

IRELAND — 81.4% | ||||||||

ACIS CLO, Ser 2014-5A, Cl E1 | 10,500,000 | 7,980,000 | ||||||

Arrowpoint CLO, Ser 2014-2A, Cl F | 4,000,000 | 3,051,200 | ||||||

Arrowpoint CLO, Ser 2014-2A, Cl SUB | 11,000,000 | 5,390,000 | ||||||

B&M CLO, Ser 2014-1A, Cl C | 10,000,000 | 8,549,000 | ||||||

B&M CLO, Ser 2014-1A, Cl D | 8,750,000 | 5,823,125 | ||||||

B&M CLO, Ser 2014-1A, Cl E | 5,250,000 | 3,263,400 | ||||||

Battalion CLO, Ser 2012-3A, Cl SUB | 39,200,000 | 21,222,880 | ||||||

Battalion CLO, Ser 2013-4A, Cl SUB | 31,800,000 | 9,540,000 | ||||||

Battalion CLO, Ser 2014-7A, Cl D | 6,417,000 | 5,420,440 | ||||||

Battalion CLO IV, Ser 2013-4A, Cl E | 882,000 | 671,731 | ||||||

Battalion CLO VII, Ser 2014-7A, Cl SUB | 11,375,000 | 6,142,500 | ||||||

2

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2015

Description | Par Value | Fair Value | ||||||

Battalion CLO VIII, Ser 2015-8A, Cl D | $ | 7,750,000 | $ | 5,974,010 | ||||

Battalion CLO VIII, Ser 2015-8A, Cl SUB | 25,125,000 | 21,607,500 | ||||||

Battalion CLO X | 7,500,000 | 7,500,000 | ||||||

Benefit Street Partners CLO, Ser 2012-IA, Cl SUB | 8,650,000 | 5,190,000 | ||||||

Benefit Street Partners CLO, Ser 2015-IA, Cl DR | 9,444,000 | 8,462,768 | ||||||

Benefit Street Partners CLO, Ser 2015-VIA, Cl SUB | 36,203,000 | 24,618,040 | ||||||

Benefit Street Partners CLO, Ser 2015-VII, Cl SUB | 36,750,000 | 30,719,325 | ||||||

Benefit Street Partners CLO II, Ser 2013-IIA, Cl SUB | 23,450,000 | 15,711,500 | ||||||

Benefit Street Partners CLO III, Ser 2013-IIIA, Cl SUB | 21,873,500 | 12,686,630 | ||||||

Benefit Street Partners CLO V | 19,200,000 | 9,744,000 | ||||||

Benefit Street Partners CLO VIII, Ser 2015-8A, Cl D | 5,880,000 | 4,835,124 | ||||||

Brentwood CLO, Ser 2006-1A, Cl C | 8,500,000 | 7,279,400 | ||||||

Carlyle Global Market Strategies, Ser 2012-1A, Cl F | 7,975,000 | 7,008,749 | ||||||

Carlyle Global Market Strategies, Ser 2012-1A, Cl SUB | 1,400,000 | 567,000 | ||||||

Carlyle Global Market Strategies, Ser 2014-3A, Cl SUB | 19,600,000 | 12,348,000 | ||||||

Cathedral Lake CLO, Ser 2015-3A, Cl SUB | 10,500,000 | 8,898,750 | ||||||

Cathedral Lake CLO 2015-3, Ser 2015-3A, Cl D | 9,000,000 | 8,977,500 | ||||||

Cathedral Lake CLO 2015-3, Ser 2015-3A, Cl E | 8,250,000 | 8,002,500 | ||||||

Cerberus Onshore II CLO, Ser 2014-1A, Cl E | 22,500,000 | 20,916,450 | ||||||

CIFC Funding, Ser 2012-2A | 16,399,000 | 8,363,490 | ||||||

CIFC Funding, Ser 2013-2A | 2,000,000 | 1,056,000 | ||||||

CVP Cascade CLO, Ser 2014-2A, Cl D | 5,539,000 | 3,348,325 | ||||||

CVP Cascade CLO, Ser 2014-2A, Cl E | 8,000,000 | 4,831,200 | ||||||

Fifth Street Senior Loan Fund, Ser 2015-1A, Cl E | 9,000,000 | 8,111,520 | ||||||

Fifth Street Senior Loan Fund, Ser 2015-2A, Cl A1T | 2,000,000 | 1,984,200 | ||||||

Fifth Street Senior Loan Fund, Ser 2015-2A, Cl D | 19,050,000 | 16,927,830 | ||||||

Fifth Street Senior Loan Fund, Ser 2015-2A, Cl SUB | 34,362,000 | 30,582,180 | ||||||

Figueroa CLO, Ser 2013-1 | 17,500,000 | 10,214,750 | ||||||

Figueroa CLO, Ser 2013-2 | 13,070,000 | 8,329,511 | ||||||

Figueroa CLO, Ser 2013-2A, Cl D | 4,000,000 | 2,800,000 | ||||||

Fortress Credit Funding, Ser 2012-5A | 10,000,000 | 9,520,000 | ||||||

Fortress Credit Funding, Ser 2012-5I, Cl E | 19,800,000 | 18,871,380 | ||||||

3

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2015

Description | Par Value | Fair Value | ||||||

Fortress Credit Funding, Ser 2012-6A | $ | 8,415,000 | $ | 7,588,647 | ||||

Fortress Credit Opportunities CLO, Ser 2014-5A, Cl C | 2,000,000 | 1,933,200 | ||||||

Fortress Credit Opportunities CLO, Ser 2014-5A, Cl D 4.821%, 10/15/26 (B)(D) | 4,000,000 | 3,758,400 | ||||||

Fortress Credit Opportunities CLO, Ser 2014-5A, Cl F | 9,000,000 | 8,145,900 | ||||||

Golub Capital Partners CLO, Ser 2015-23A, Cl E | 3,300,000 | 2,665,674 | ||||||

Grayson CLO, Ser 2006-1A, Cl C | 10,250,000 | 8,712,500 | ||||||

Great Lakes CLO, Ser 2012-1A, Cl E | 12,897,000 | 11,091,420 | ||||||

Great Lakes CLO, Ser 2012-1A, Cl SUB | 21,336,000 | 14,508,480 | ||||||

Great Lakes CLO, Ser 2014-1A, Cl F | 7,750,000 | 5,541,250 | ||||||

Great Lakes CLO, Ser 2014-1A, Cl SUB | 24,200,000 | 16,456,000 | ||||||

Great Lakes CLO, Ser 2015-1, Cl SUB | 22,855,000 | 18,055,450 | ||||||

Great Lakes CLO, Ser 2015-1A, Cl E | 15,750,000 | 13,308,750 | ||||||

Great Lakes CLO, Ser 2015-1A, Cl F | 7,175,000 | 5,417,125 | ||||||

Halcyon Loan Advisors Funding 2015-2, Ser 2015-2A, Cl E | 7,500,000 | 5,291,250 | ||||||

Harbourview CLO VII, Ser 2014-7A, Cl E | 7,000,000 | 5,110,000 | ||||||

Hildene CLO, Ser 2014-2A, Cl D | 4,000,000 | 3,656,800 | ||||||

ICE EM CLO, Ser 2007-1A, Cl A3 | 5,000,000 | 4,500,000 | ||||||

ICE Global Credit CLO, Ser 2012-1A, Cl C | 1,000,000 | 964,300 | ||||||

ICE Global Credit CLO, Ser 2012-1A, Cl E | 13,500,000 | 11,070,000 | ||||||

ICE Global Credit CLO, Ser 2013-1A, Cl B1 | 34,500,000 | 32,861,250 | ||||||

ICE Global Credit CLO, Ser 2013-1A, Cl C1 | 24,500,000 | 21,560,000 | ||||||

ICE Global Credit CLO, Ser 2013-1A, Cl D | 15,000,000 | 11,250,000 | ||||||

ICE Global Credit CLO, Ser 2013-1A, Cl INC | 12,500,000 | 3,750,000 | ||||||

Ivy Hill Middle Market Credit Fund, Ser 7A, Cl SUB | 24,552,000 | 17,677,440 | ||||||

Jamestown CLO, Ser 2015-7A, Cl D | 6,000,000 | 4,722,600 | ||||||

Jamestown CLO, Ser 2015-7A, Cl E | 6,000,000 | 4,113,600 | ||||||

JFIN MM CLO, Ser 2014-1A, Cl C | 3,750,000 | 3,421,875 | ||||||

JFIN MM CLO, Ser 2014-1A, Cl D | 14,990,000 | 12,441,700 | ||||||

JFIN MM CLO, Ser 2014-1A, Cl E | 12,500,000 | 10,250,000 | ||||||

JFIN MM CLO, Ser 2015-2A, Cl E | 15,000,000 | 13,725,000 | ||||||

JFIN Revolver CLO, Ser 2013-1A, Cl B | 4,000,000 | 3,950,000 | ||||||

JFIN Revolver CLO 2014, Ser 2014-2A, Cl C | 4,500,000 | 4,297,500 | ||||||

4

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2015

Description | Par Value | Fair Value | ||||||

Kingsland, Ser 2013-6A, Cl E | $ | 2,000,000 | $ | 1,606,600 | ||||

KVK CLO, Ser 2012-2A, Cl SUB | 33,573,000 | 10,911,225 | ||||||

Lockwood Grove CLO, Ser 2014-1A, Cl E | 15,000,000 | 13,950,000 | ||||||

Lockwood Grove CLO, Ser 2014-1A, Cl SUB | 25,988,000 | 18,451,480 | ||||||

Midocean Credit CLO, Ser 2014-3A, Cl F | 7,250,000 | 4,827,775 | ||||||

Nelder Grove CLO, Ser 2014-1A, Cl D1 | 4,500,000 | 4,230,000 | ||||||

Nelder Grove CLO, Ser 2014-1A, Cl E | 9,000,000 | 7,470,000 | ||||||

Neuberger Berman CLO, Ser 2012-13A, Cl SUB | 4,274,000 | 1,410,420 | ||||||

Neuberger Berman CLO, Ser 2013-15A, Cl SUB | 18,151,850 | 7,260,740 | ||||||

Neuberger Berman CLO, Ser 2014-16A, Cl SFN | 1,995,000 | 1,256,850 | ||||||

Neuberger Berman CLO, Ser 2014-16A, Cl SUB | 29,925,000 | 9,875,250 | ||||||

Neuberger Berman CLO, Ser 2014-17A, Cl SFN | 341,579 | 215,195 | ||||||

Neuberger Berman CLO, Ser 2014-17A, Cl SUB | 5,900,000 | 2,773,000 | ||||||

Newstar Arlington Senior Loan Program, Ser 2014-1A, Cl E | 15,000,000 | 12,787,650 | ||||||

Newstar Clarendon Fund CLO, Ser 2014-1A, Cl E | 23,726,000 | 19,355,671 | ||||||

Newstar Commercial Loan Funding, Ser 2015-1A, Cl D | 3,625,000 | 3,529,699 | ||||||

Newstar Trust, Ser 2012-2A, Cl A | 5,000,000 | 5,006,250 | ||||||

OCP CLO, Ser 2012-2A, Cl SUB | 18,445,000 | 6,824,650 | ||||||

OFSI Fund VI, Ser 2014-6A, Cl C | 5,250,000 | 4,213,650 | ||||||

Rockwall CDO, Ser 2007-1A, Cl A1LA | 5,195,051 | 5,034,005 | ||||||

Saranac CLO, Ser 2014-2A, Cl E | 6,667,000 | 5,000,250 | ||||||

Shackleton CLO, Ser 2014-6A, Cl E | 9,000,000 | 7,353,900 | ||||||

Shackleton CLO, Ser 2014-6A, Cl SUB | 23,850,000 | 9,540,000 | ||||||

Shackleton I CLO, Ser 2012-1A, Cl INC | 23,500,000 | 9,752,500 | ||||||

TICP CLO, Ser 2014-3A, Cl SUB | 7,000,000 | 3,290,000 | ||||||

Tricadia CDO, Ser 2006-6X, Cl B2L | 4,005,978 | 5,408,069 | ||||||

Trinitas CLO, Ser 2014-1A, Cl C | 2,500,000 | 2,236,250 | ||||||

Trinitas CLO, Ser 2014-1A, Cl D | 4,000,000 | 3,360,000 | ||||||

Trinitas CLO, Ser 2014-1A, Cl SUB | 16,713,000 | 8,523,630 | ||||||

Trinitas CLO, Ser 2014-2A, Cl D | 15,054,000 | 12,118,470 | ||||||

Valhalla CLO, Ser 2004-1A, Cl EIN | 6,500,000 | 1,430,000 | ||||||

Venture CDO, Ser 2012-10A, Cl F | 5,000,000 | 4,550,000 | ||||||

5

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2015

Description | Par Value/Shares | Fair Value | ||||||

Venture CDO, Ser 2012-10A, Cl SUB | $ | 12,312,000 | $ | 6,525,360 | ||||

Venture CDO, Ser 2012-11AR, Cl FR | 11,000,000 | 9,342,080 | ||||||

Venture CDO, Ser 2012-12A, Cl SUB | 46,931,000 | 23,934,810 | ||||||

Venture XIII CLO, Ser 2013-13A, Cl E | 7,000,000 | 5,530,000 | ||||||

Venture XIV CLO, Ser 2013-14A, Cl SFN | 1,338,889 | 749,778 | ||||||

Venture XIV CLO, Ser 2013-14A, Cl SUB | 21,930,000 | 10,307,100 | ||||||

Venture XV CLO, Ser 2013-15A, Cl SUB | 20,003,000 | 10,501,575 | ||||||

Venture XXII CLO, Ser 2016-22A, Cl E | 15,675,000 | 14,264,250 | ||||||

Venture XXII CLO, Ser 2016-22A, Cl F | 5,700,000 | 4,845,000 | ||||||

Venture XXII CLO, Ser 2016-22A, Cl SUB | 13,706,000 | 10,073,910 | ||||||

Zohar CDO, Ser 2007-3A, Cl A2 | 90,000,000 | 18,225,000 | ||||||

Zohar CDO, Ser 2007-3A, Cl A3 | 56,000,000 | 14,560,000 | ||||||

|

| |||||||

| 1,057,250,061 | ||||||||

|

| |||||||

UNITED STATES — 11.9% | ||||||||

Fortress Credit Opportunities CLO, Ser 2014-3A, Cl E | 13,000,000 | 11,681,800 | ||||||

Ivy Hill IV | 85,000,000 | 57,800,000 | ||||||

NXT Capital CLO, Ser 2012-1A, Cl E | 10,286,000 | 10,010,130 | ||||||

TICC CLO, Ser 2012-1A | 75,000,000 | 74,962,500 | ||||||

|

| |||||||

| 154,454,430 | ||||||||

|

| |||||||

Total Asset-Backed Securities (Cost $1,634,390,295) | 1,292,777,631 | |||||||

|

| |||||||

REGISTERED INVESTMENT COMPANIES (E) — 1.9% | ||||||||

UNITED STATES — 1.9% | ||||||||

Ares Dynamic Credit Allocation Fund | 710,488 | 9,492,120 | ||||||

Blackstone/GSO Senior Floating Rate Term Fund | 67,044 | 995,603 | ||||||

Guggenheim Strategic Opportunities Fund | 199,752 | 3,361,826 | ||||||

Neuberger Berman High Yield Strategies Fund | 352,746 | 3,559,207 | ||||||

Stone Harbor Emerging Markets Income Fund | 377,557 | 4,549,562 | ||||||

Western Asset Emerging Markets Income Fund | 288,365 | 2,805,792 | ||||||

|

| |||||||

Total Registered Investment Companies (Cost $27,723,639) | 24,764,110 | |||||||

|

| |||||||

COMMON STOCK — 0.4% | ||||||||

UNITED STATES — 0.4% | ||||||||

Ares Capital | 347,000 | 4,944,750 | ||||||

|

| |||||||

Total Common Stock (Cost $4,928,058) | 4,944,750 | |||||||

|

| |||||||

6

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2015

Description | Shares | Fair Value | ||||||

CASH EQUIVALENT — 1.3% | ||||||||

UNITED STATES — 1.3% | ||||||||

SEI Daily Income Trust Prime Obligation Fund, Cl A, 0.230%(F)(G) | $ | 17,291,790 | $ | 17,291,790 | ||||

|

| |||||||

Total Cash Equivalent (Cost $17,291,790) | 17,291,790 | |||||||

|

| |||||||

Total Investments — 103.2% | $ | 1,339,778,281 | ||||||

|

| |||||||

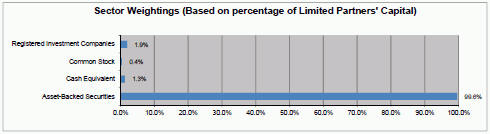

Percentages based on Limited Partners’ Capital of $1,298,480,321.

Transactions with affiliated funds during the year ended December 31, 2015 are as follows:

| Value of Shares Held as of 12/31/2015 | Purchases at Cost | Proceeds from Sales | Realized Gain(Loss) | Dividend Income | ||||||||||||||||

SEI Daily Income Trust Prime Obligation Fund, Cl A | $ | 17,291,790 | $ | 404,923,999 | $ | 443,657,282 | $ | — | $ | 16,370 | ||||||||||

CDO — Collateralized Debt Obligation

Cl — Class

CLO — Collateralized Loan Obligation

L.P. — Limited Partnership

Ser — Series

| (A) | Securities considered illiquid. The total value of such securities as of December 31, 2015 was $1,292,777,631 and represented 99.6% of Limited Partners’ Capital. |

| (B) | Securities sold within terms of a private placement memorandum, exempt from registration under Section 144A of the Securities Act of 1933, as amended. At December 31, 2015, the market value of the Rule 144A positions amounted to $1,107,210,170 or 85.3% of Limited Partners’ Capital. |

| (C) | Represents equity / residual tranche. |

| (D) | Variable rate security. The rate reported is the rate in effect as of December 31, 2015. |

| (E) | Closed-End Fund traded on exchange. |

| (F) | Rate shown is the 7-day effective yield as of December 31, 2015. |

| (G) | Investment in affiliated security. |

| (H) | Securities are fair valued using methods determined in good faith by the Fair Value Committee of the Fund. The total value of such securities as of December 31, 2015 was $50,462,440 and represented 3.9% of Limited Partners’ Capital. |

The following is a summary of the inputs used as of December 31, 2015 in valuing the Fund’s investments carried at value:

| Level 1 | Level 2 | Level 3(1) | Total | |||||||||||||

Investments in Securities | ||||||||||||||||

Asset-Backed Securities | $ | — | $ | — | $ | 1,292,777,631 | $ | 1,292,777,631 | ||||||||

Registered Investment Companies | 24,764,110 | — | — | 24,764,110 | ||||||||||||

Common Stock | 4,944,750 | — | — | 4,944,750 | ||||||||||||

Cash Equivalent | 17,291,790 | — | — | 17,291,790 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total Investments in Securities | $ | 47,000,650 | $ | — | $ | 1,292,777,631 | $ | 1,339,778,281 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| (1) | Of the $1,292,777,631 in Level 3 securities as if December 31, 2015, all were valued via dealer |

7

SEI Structured Credit Fund, L.P.

Schedule of Investments

December 31, 2015

The following is a reconciliation of the investments in which significant unobservable inputs (Level 3) were used in determining fair value:

| Asset-Backed Securities | ||||

Beginning balance as of January 1, 2015 | $ | 1,338,325,013 | ||

Accrued discounts/premiums | 87,310,127 | |||

Realized gain/(loss) | 18,155,773 | |||

Change in unrealized appreciation/(depreciation) | (240,654,628 | ) | ||

Proceeds from Sales | (478,653,061 | ) | ||

Purchases | 568,294,407 | |||

|

| |||

Ending balance as of December 31, 2015 | $ | 1,292,777,631 | ||

|

| |||

Changes in unrealized gains/(losses) included in earnings related to securities still held at reporting date | $ | (223,877,473 | ) | |

|

| |||

For the year ended December 31, 2015, there were no transfers between Level 1, Level 2 and Level 3 assets and liabilities.

For more information on valuation inputs, see Note 2 – Significant Accounting Policies in Notes to Financial Statements.

Amounts designated as “—” are $0 or have been rounded to $0.

See accompanying notes, which are an integral part of the financial statements.

8

SEI Structured Credit Fund, L.P.

Statement of Assets and Liabilities

December 31, 2015

Investments in securities, at value (cost $1,667,041,992) | $ | 1,322,486,491 | ||

Investment in affiliated security, at value (cost $17,291,790) | 17,291,790 | |||

Cash at broker | 34,058,279 | |||

Interest and dividends receivable | 7,626,930 | |||

Prepaid expenses | 430,427 | |||

|

| |||

Total assets | 1,381,893,917 | |||

|

| |||

Liabilities | ||||

Capital contributions received in advance | 32,756,880 | |||

Payable for investment securities purchased | 30,283,160 | |||

Capital withdrawals payable | 20,155,000 | |||

Administration fees payable | 109,955 | |||

Other accrued expenses | 108,601 | |||

|

| |||

Total liabilities | 83,413,596 | |||

|

| |||

Limited Partners’ capital | $ | 1,298,480,321 | ||

|

| |||

Limited Partners’ capital Represented by: | ||||

Paid-in-capital | $ | 1,643,035,822 | ||

Net unrealized depreciation on investments | (344,555,501 | ) | ||

|

| |||

Limited Partners’ capital | $ | 1,298,480,321 | ||

|

|

See accompanying notes, which are an integral part of the financial statements.

9

SEI Structured Credit Fund, L.P.

For the year ended December 31, 2015

Interest Income | $ | 127,837,661 | ||

Dividend income from affiliated security | 16,370 | |||

|

| |||

Total investment income | 127,854,031 | |||

Expenses | ||||

Administration fee | 1,404,934 | |||

Professional fees | 124,170 | |||

Directors’ fees | 30,000 | |||

Miscellaneous expenses | 113,639 | |||

|

| |||

Total expenses | 1,672,743 | |||

|

| |||

Net investment income | 126,181,288 | |||

|

| |||

Realized and unrealized gains (losses) on unaffiliated investments | ||||

Net realized gain on investments | 18,355,063 | |||

Net change in unrealized appreciation (depreciation) on investments | (243,022,382 | ) | ||

|

| |||

Net realized and unrealized loss on investments | (224,667,319 | ) | ||

|

| |||

Net decrease in Limited Partners’ capital resulting from operations | $ | (98,486,031 | ) | |

|

|

See accompanying notes, which are an integral part of the financial statements.

10

SEI Structured Credit Fund, L.P.

Statements of Changes in Limited Partners’ Capital

| For the year ended December 31, 2015 | For the year ended December 31, 2014 | |||||||

From investment activities | ||||||||

Net investment income | $ | 126,181,288 | $ | 103,323,683 | ||||

Net realized gain on investments | 18,355,063 | 31,079,688 | ||||||

Net change in unrealized appreciation (depreciation) on investments | (243,022,382 | ) | (67,247,898 | ) | ||||

|

|

|

| |||||

Net increase (decrease) in Limited Partners’ capital resulting from operations | (98,486,031 | ) | 67,155,473 | |||||

Partners’ capital transactions | ||||||||

Capital contributions | 67,547,458 | 162,499,593 | ||||||

Capital withdrawals | (57,778,313 | ) | (79,108,912 | ) | ||||

|

|

|

| |||||

Net increase in Limited Partners’ capital derived from capital transactions | 9,769,145 | 83,390,681 | ||||||

Net increase (decrease) in Limited Partners’ capital | (88,716,886 | ) | 150,546,154 | |||||

Limited Partners’ capital beginning of year | 1,387,197,207 | 1,236,651,053 | ||||||

|

|

|

| |||||

Limited Partners’ capital end of year | $ | 1,298,480,321 | $ | 1,387,197,207 | ||||

|

|

|

| |||||

See accompanying notes, which are an integral part of the financial statements.

11

SEI Structured Credit Fund, L.P.

For the year ended December 31, 2015

Cash flows from operating activities | ||||

Net decrease in Limited Partners’ capital resulting from operations | $ | (98,486,031 | ) | |

Adjustments to reconcile net decrease in Limited Partners’ capital resulting from operations to net cash used in operating activities: | ||||

Purchases of long-term investments | (596,079,853 | ) | ||

Proceeds from sales of long-term investments | 482,718,715 | |||

Accretion of discount (see Note 2) | (87,310,127 | ) | ||

Net purchases of short-term investments | 38,733,283 | |||

Net realized gain on investments | (18,355,063 | ) | ||

Net change in unrealized (appreciation) depreciation on investments | 243,022,382 | |||

Increase in interest/dividends receivable | (1,388,019 | ) | ||

Increase in prepaid expenses | (299,682 | ) | ||

Increase in payable for securities purchased | 8,797,843 | |||

Decrease in administration fees payable | (5,451 | ) | ||

Increase in other accrued expenses | 4,446 | |||

|

| |||

Net cash used in operating activities | (28,647,557 | ) | ||

|

| |||

Cash flows from financing activities | ||||

Capital contributions | 100,304,338 | |||

Capital withdrawals | (37,623,313 | ) | ||

|

| |||

Net cash provided by financing activities | 62,681,025 | |||

|

| |||

Net change in cash and cash equivalents | 34,033,468 | |||

|

| |||

Cash and cash equivalents | ||||

Beginning of year | 24,811 | |||

|

| |||

End of year | $ | 34,058,279 | ||

|

|

See accompanying notes, which are an integral part of the financial statements.

12

SEI Structured Credit Fund, L.P.

December 31, 2015

1. Organization

SEI Structured Credit Fund, L.P. (the “Fund”) is a Delaware limited partnership established on June 26, 2007 and commenced operations on August 1, 2007. The Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a closed-end, non-diversified, management investment company. The Fund offers limited partnership interests (“Interests”) solely through private placement transactions to investors (“Limited Partners”) that have signed an investment management agreement with SEI Investments Management Corporation (“SIMC” or the “Adviser”), the investment adviser to the Fund. As of December 31, 2015, the SEI Structured Credit Segregated Portfolio owned approximately 83.5% of the Fund, while the other Limited Partners owned approximately 16.5% of the Fund.

The Fund’s objective is to generate high total returns. There can be no assurance that the Fund will achieve its objective. The Fund pursues its investment objective by investing in a portfolio comprised of collateralized debt obligations (“CDOs”), which includes collateralized loan obligations (“CLOs”) and other structured credit investments. In the current year, the Fund also invested in registered investment companies. CDOs are special purpose investment vehicles formed to acquire and manage a pool of loans, bonds and/or other fixed income assets of various types. CDOs fund their investments by issuing several classes of debt and equity securities, the repayment of which is linked to the performance of the underlying assets, which serve as collateral for certain securities issued by the CDO. In addition to CDOs, the Fund’s investments may include fixed income securities, loan participations, credit-linked notes, medium-term notes, registered and unregistered investment companies or pooled investment vehicles, and derivative instruments, such as credit default swaps and total return swaps (collectively with CDOs, “Structured Credit Investments”).

SEI Investment Strategies, LLC (the “General Partner”), a Delaware limited liability company, serves as the General Partner to the Fund and has no investment in the Fund as of December 31, 2015. The General Partner has delegated the management and control of the business and affairs of the Fund to the Board of Directors (the “Board”). A majority of the Board is and will be persons who are not “interested persons” (as defined in the 1940 Act) with respect to the Fund.

13

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

2. Significant Accounting Policies

The following is a summary of significant accounting and reporting policies followed by the Fund in preparing the financial statements:

Use of Estimates

The Fund is an investment company and follows accounting and reporting guidance in the Financial Accounting Standards Board Accounting Standards Codification Topic 946 (ASC 946). The preparation of financial statements in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Management believes that the estimates utilized in preparing the Fund’s financial statements are reasonable; however, actual results could differ from these estimates and it is possible that differences could be material.

Valuation of Investments

Securities listed on a securities exchange, market or automated quotation system for which quotations are readily available (except for securities traded on NASDAQ) are valued at the last quoted sale price on the primary exchange or market (foreign or domestic) on which they are traded, or, if there is no such reported sale, at the most recent quoted bid price. For securities traded on NASDAQ, the NASDAQ Official Closing Price will be used. When available, Structured Credit Investments are priced based upon valuations provided by independent, third party pricing agents using their proprietary valuation methodology. The third-party pricing agents may value Structured Credit Investments at an evaluated bid price by employing methodologies that utilize actual market transactions, broker-supplied valuations, or other methodologies designed to identify the market value for such securities. Such methodologies generally consider such factors as security prices, yields, maturities, call features, ratings and developments relating to specific securities in arriving at valuations.

If a price for a Structured Credit Investment cannot be obtained from an independent, third-party pricing agent, the Fund shall seek to obtain a bid price from at least one dealer who is independent of the Fund. In such cases, the independent dealer providing the price on the Structured Credit Investment may also be a “market maker”, and in many cases the only market maker, with respect to that security. As of December 31, 2015, all asset-backed securities are valued by an independent dealer who is also a market maker.

14

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

2. Significant Accounting Policies (continued)

Valuation of Investments (continued)

A dealer’s valuation reflects its judgment of the price of an asset, assuming an arm’s length transaction at the valuation date between knowledgeable and willing market participants. It generally assumes a round lot institutional transaction, without consideration for whether the client is long or short the instrument, and without adjustment for the size of the client’s position. The valuation pertains to an assumed transaction and may not necessarily reflect actual quoted or other prices, and does not indicate that an active market exists for the financial instrument.

A dealer’s valuation may be formulated using inputs such as a combination of observable market transactions of the exact security or a similar security and internal models. Bids-Wanted-In Competition (“BWIC”) are widely distributed auctions of securities whose results are the primary input used by dealers to establish valuations for structured credit securities. Dealers supplement BWIC results with private transactions and model-driven valuations. Model-driven valuations require assumptions regarding default, recovery, and prepayment rates that are consistent with current market conditions.

In situations where market inputs are not available or do not provide a sufficient basis under current market conditions for pricing the instrument, the valuation may reflect the dealer’s view of the assumptions that market participants would use in pricing the instrument. Since market participants may have materially different views as to future supply, demand, credit quality and other factors relevant to pricing financial instruments, as well as bid and ask prices, valuations may differ materially among dealers. The actual level at which these instruments trade (if trades occur) could be materially different from the dealer’s valuation.

Securities for which market prices are not “readily available” or may be unreliable are valued in accordance with Fair Value Procedures established by the Board. The Fund’s Fair Value Procedures are implemented through a Fair Value Committee (the “Committee”) designated by the Board. The Committee is currently composed of two members of the Board, as well as representatives from SIMC and its affiliates. The Committee provides regular reports to the Board concerning investments for which market prices are not readily available or may be unreliable.

15

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

2. Significant Accounting Policies (continued)

Valuation of Investments (concluded)

When a security is valued in accordance with the Fair Value Procedures, the Committee will determine the value after taking into consideration relevant information reasonably available to the Committee. Examples of factors the Committee may consider are: (i) the facts giving rise to the need to fair value; (ii) the last trade price; (iii) the performance of the market or issuer’s industry; (iv) the liquidity of the security; (v) the size of the holding in the Fund; or (vi) any other appropriate information. The determination of a security’s fair value price often involves the consideration of a number of subjective factors, and is therefore subject to the unavoidable risk that the value assigned to a security may be higher or lower than the security’s value would be if a reliable market quotation for the security was readily available. At December 31, 2015, there were three securities that were fair valued by the Committee.

The Board will periodically review the Fund’s valuation policies and will update them as necessary to reflect changes in the types of securities in which the Fund invests.

Fair Value of Financial Instruments

In accordance with the authoritative guidance on fair value measurements and disclosure under U.S. GAAP, the Fund discloses the fair value of its investments in a hierarchy that prioritizes the inputs to valuation techniques used to measure the fair value. The objective of a fair value measurement is to determine the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (an exit price).

Accordingly, the fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3). Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions the market participants would use in pricing the asset or liability. The three levels of the fair value hierarchy are described below:

Level 1 – Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date;

16

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

2. Significant Accounting Policies (continued)

Fair Value of Financial Instruments (continued)

Level 2 – Observable market based inputs or unobservable inputs that are corroborated by market data, which includes financial instruments that are valued using models or other valuation methodologies. These models are primarily industry standard models that consider various assumptions, including time value, yield curve, volatility factors, prepayment speeds, default rates, loss severity, current market and contractual prices for the underlying financial instruments, as well as other relevant economic measures. Substantially all of these assumptions are observable in the marketplace, can be derived from observable data or are supported by observable levels at which transactions are executed in the marketplace; and

Level 3 – Unobservable inputs that are not corroborated by market data (supported by little or no market activity), which is comprised of financial instruments whose fair value is estimated based on internally developed models or methodologies utilizing significant inputs that are generally not observable.

Investments are classified within the level of the lowest significant input considered in determining fair value. Investments classified within Level 3 whose fair value measurement considers several inputs may include Level 1 or Level 2 inputs as components of the overall fair value measurement.

For the year ended December 31, 2015, there have been no significant changes to the Fund’s fair valuation methodologies.

The following table summarizes the quantitative inputs and assumptions used for items categorized as Level 3 investments as of December 31, 2015. The disclosure below also includes quantitative information on the sensitivity of the fair value measurements to changes in the significant unobservable inputs.

Assets | Fair Value as of December 31, 2015 | Valuation Technique(s) | Unobservable Input | Price Range | ||||||||||

CLO Debt* | $ | 714,081,752 | Market Quotes | Broker Quote | $20.50 - $135 | |||||||||

CLO Equity** | 578,695,879 | Market Quotes | Broker Quote | $22 - $100 | ||||||||||

|

| |||||||||||||

Total | $ | 1,292,777,631 | ||||||||||||

| * | Includes two securities that were fair valued by the Committee. |

| ** | Includes one security that was fair valued by the Committee. |

17

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

2. Significant Accounting Policies (continued)

Fair Value of Financial Instruments (concluded)

The unobservable input used to determine fair value of the Level 3 asset may have similar diverging impacts on valuation. Significant increases and decreases in this input could result in significantly higher or lower fair value measurement.

Income Recognition and Security Transactions

Security transactions are recorded on the trade date for financial reporting purposes. Costs used in determining net realized capital gains and losses on the sale of securities are on the basis of specific identification. Dividend income is recognized on the ex-dividend date, and interest income is recognized using the accrual basis of accounting. Amortization and accretion of debt instruments is calculated using the scientific interest method, which approximates the effective interest method over the estimated life of the security. Amortization of premiums and accretion of discounts are periodically adjusted and are included in interest income on the Statement of Operations.

Collateralized Debt Obligations

The Fund invests in CDOs which include CLOs, a type of asset-backed security, and other similarly structured securities. A CLO is a trust typically collateralized by a pool of loans, which may include, among others, domestic and foreign senior secured loans, senior unsecured loans, and subordinate corporate loans, including loans that may be rated below investment grade or equivalent unrated loans. CDOs may charge management fees and administrative expenses. For CDOs, the cash flows from the trust are split into two or more portions, called tranches, varying in risk and yield. The riskiest portion is the “equity” tranche which bears the bulk of defaults from the bonds or loans in the trust and serves to protect the other, more senior tranches from default in all but the most severe circumstances. Since it is partially protected from defaults, a senior tranche from a CDO trust typically has a higher rating and lower yield than their underlying securities, and can be rated investment grade. Despite the protection from the equity tranche, CDO tranches can experience substantial losses due to actual defaults, increased sensitivity to defaults due to collateral default and disappearance of protecting tranches, market anticipation of defaults, as well as aversion to CDO securities as a class.

Legislation enacted in 2010 imposes a withholding tax of 30% on payments of U.S. source interest and dividends paid after December 31, 2013, or gross proceeds from the disposition of an instrument that produces U.S. source interest or dividends paid after December 31, 2016, to certain non-U.S. entities, including certain non-U.S. financial

18

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

2. Significant Accounting Policies (concluded)

Collateralized Debt Obligations (concluded)

institutions and investment funds, unless such non-U.S. entity complies with certain reporting requirements regarding its United States account holders and its United States owners. Most CLO vehicles in which we invest will be treated as non-U.S. financial entities for this purpose, and therefore will be required to comply with these reporting requirements to avoid the 30% withholding. If a CLO vehicle in which we invest fails to properly comply with these reporting requirements, it could reduce the amounts available to distribute to equity and junior debt holders in such CLO vehicle, which could materially and adversely affect our operating results and cash flows.

Federal Taxes

The Fund intends to be treated as a partnership for federal, state, and local income tax purposes. Each Limited Partner is responsible for the tax liability or benefit relating to its distributive share of taxable income or loss. Accordingly, no provision for federal, state, or local income taxes is reflected in the accompanying financial statements.

For the year ended December 31, 2015, in accordance with U.S. GAAP, the Fund reclassified $126,181,288 and $18,355,063 from accumulated net investment income and accumulated net realized gain, respectively, to Limited Partners’ capital. The reclassification was to reflect, as an adjustment to Limited Partners’ capital, the amount of taxable income that has been allocated to the Limited Partners and has no effect on net assets.

The Fund evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether it is “more-likely-than-not” (i.e., greater than 50-percent) that each tax position will be sustained upon examination by a taxing authority based on the technical merits of the position. Tax positions not deemed to meet the more-likely-than-not threshold are recorded as a tax benefit or expense in the current year. The Fund did not record any tax provisions in the current period. However, management’s conclusions regarding tax positions taken may be subject to review and adjustment at a later date based on factors including, but not limited to, examination by tax authorities (i.e., the last 3 tax year ends, as applicable), on-going analysis of and changes to tax laws, regulations and interpretations thereof.

19

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

3. Adviser, Administrator and Other Transactions

The Adviser does not charge a management fee to the Fund. Limited Partners are responsible for paying the fees of the Adviser directly under their individual investment management agreement with the Adviser. Each agreement sets forth the fees to be paid to the Adviser, which are ordinarily expressed as a percentage of the Limited Partner’s assets managed by the Adviser. This fee, which is negotiated between the Limited Partner and the Adviser, may include a performance-based fee and/or a fixed-dollar fee for certain specified services that is unrelated to the return of the Fund.

The Adviser has voluntarily agreed that certain expenses of the Fund, including custody fees and administrative fees shall not in the aggregate exceed 0.50% per annum of the Fund’s monthly average net asset value, and the Adviser or its affiliates will waive Fund fees or reimburse Fund expenses to the extent necessary so that such 0.50% limit is not exceeded. The following expenses of the Fund are specifically excluded from the expense limit: organizational expenses; extraordinary, non-recurring and certain other unusual expenses; taxes and fees; and expenses incurred indirectly by the Fund through its investments in Structured Credit Investments. The Adviser may discontinue all or part of this waiver at any time. In the current year, the Adviser did not waive any expenses.

SEI Global Services, Inc. (the “Administrator”) serves as the Fund’s administrator. The Administrator is a wholly-owned subsidiary of SEI Investments Company, which is also a parent company of the Adviser. The Administrator provides certain administrative, accounting, and transfer agency services to the Fund. The services performed by the Administrator may be completed by one or more of its affiliated companies. The Fund pays the Administrator a fee equal to 0.10% (on an annualized basis) of the Fund’s net asset value which is accrued monthly based on month-end net assets and is paid monthly, and reimburses the Administrator for certain out-of-pocket expenses.

SEI Investments Distribution Co. (the “Placement Agent”) serves as the Fund’s placement agent pursuant to an agreement with the Fund. The Placement Agent is a wholly owned subsidiary of SEI Investments Company, which is also a parent company of the Adviser. The Placement Agent is not compensated by the Fund for its services rendered under the agreement.

4. Allocation of Profits and Losses

The Fund maintains a separate capital account for each of its Limited Partners. As of the last day of each month, the Fund shall allocate net profits or losses for that month to the capital accounts of all Limited Partners, in proportion to their respective opening capital account balances for such month (after taking into account any capital contributions deemed to be made as of the first day of such month).

20

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

5. Limited Partners’ Capital

The Fund, in the discretion of the Board, may sell interests to new Limited Partners and may allow existing Limited Partners to purchase additional Interests in the Fund on such days as are determined by the Board in its sole discretion. It is the Fund’s intention to allow limited purchases of Interests only during designated subscription periods as may be established by the Board or its designees (currently, the Adviser) and communicated to Limited Partners. The Board or its designee will determine the amount of Interests offered to Limited Partners during a subscription period at its discretion. During the established subscription periods, Interests may be purchased on a business day, or at such other times as the Board may determine, at the offering price (which is net asset value). The Fund may discontinue its offering at any time.

The Fund is a closed-end investment company, and therefore no Limited Partner will have the right to require the Fund to redeem its Interests. The Fund from time to time may offer to repurchase outstanding Interests pursuant to written tenders by Limited Partners. Repurchase offers will be made at such times and on such terms as may be determined by the Board in its sole discretion. In determining whether the Fund should repurchase Interests from Limited Partners pursuant to written tenders, the Board will consider the recommendations of the Adviser.

The Adviser expects that it will recommend to the Board that the Fund offer to repurchase Interests four times each year, as of the last business day of March, June, September, and December. However, Limited Partners will not be permitted to tender for repurchase Interests that were acquired less than two years prior to the effective date of the proposed repurchase.

Even after the initial two year period, it is possible that there will be extended periods during which illiquidity in the underlying investments held by the Fund or other factors will cause the Board to elect not to conduct repurchase offers. Such periods may coincide with periods of negative performance. In addition, even in the event of a repurchase offer, it is possible that there will be an oversubscription to the repurchase offer, in which case a Limited Partner may not be able to redeem the full amount that the Limited Partner wishes to redeem.

21

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

5. Limited Partners’ Capital (concluded)

During the year ended December 31, 2015, the Fund made offers to repurchase Interests resulting in capital withdrawals of $57,778,313 in aggregate.

6. Investment Transactions

The cost of security purchases and proceeds from the sale and maturity of securities, other than temporary cash investments, during the year ended December 31, 2015 were $596,079,853 and $482,718,715, respectively.

As of December 31, 2015, the cost of investments for tax purposes is $1,684,333,782. Net unrealized depreciation on investments for tax purposes was $344,555,501 consisting of $39,699,120 of gross unrealized appreciation and $384,254,621 of gross unrealized depreciation.

7. Concentrations of Risk

In the normal course of business, the Fund trades financial instruments involving market risk and counterparty credit risk.

(a) Market risk

Market risk encompasses the potential for both losses and gains and includes price risk, interest rate risk, prepayment risk and collateral performance risk. The Fund’s market risk management strategy is driven by the Fund’s investment objective. The Adviser oversees each of the risks in accordance with policies and procedures.

(i) Price risk

Price risk is the risk that the value of the instrument will fluctuate as a result of changes in market prices, whether caused by factors specific to an individual investment, its issuer or any factor affecting financial instruments traded in the market. As all of the Fund’s Structured Credit Investments are carried at fair value with fair value changes recognized in the Statement of Operations, all changes in market conditions directly affect net assets.

22

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

7. Concentrations of Risk (continued)

(a) Market risk (continued)

(ii) Interest rate risk

The fair value of the Fund’s investments will change in response to interest rate changes and other factors. During periods of falling interest rates, the values of fixed income securities generally rise. Conversely, during periods of rising interest rates, the values of such securities generally decline. Changes by recognized rating agencies in the ratings of any fixed income security and in the ability of an issuer to make payments of interest and principal may also affect the value of these investments.

(iii) Prepayment risk

Prepayment risk is the risk associated with the early unscheduled return of principal on a fixed-income security. Some fixed-income securities, such as CDOs, have embedded call options which may be exercised by the issuer, or in the case of a CDO, the borrower. The yield-to-maturity of such securities cannot be known for certain at the time of purchase since the cash flows are not known. When principal is returned early, future interest payments will not be paid on that part of the principal. If the security was purchased at a premium (a price greater than 100) the security’s yield will be less than what was estimated at the time of purchase.

(iv) Collateral performance risk

Collateral performance risk is the risk that defaults or underperformance of the CDO’s underlying collateral negatively impacts scheduled payments to a tranche based on relative seniority in the overall capital structure of each deal.

(v) Liquidity risk

The risks of an investment in a CDO depend largely on the type of the collateral securities and the class of the CDO in which the Fund invests. Normally, CLOs and other CDOs are privately offered and sold, and thus, are not registered under the securities laws. As a result, investments in CDOs may be characterized by the Fund as illiquid securities; however, an active dealer market may exist for CDOs, allowing a CDO to qualify for Rule 144A transactions.

23

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

7. Concentrations of Risk (continued)

(a) Market risk (concluded)

(v) Liquidity risk (concluded)

In addition to the normal risks associated with fixed income securities (e.g., interest rate risk, reinvestment risk, prepayment risk and default risk), CDOs carry additional risks including, but not limited to: (i) the possibility that distributions from collateral securities will not be adequate to make interest or other payments; (ii) the quality of the collateral may decline in value or default; (iii) the Fund may invest in CDOs that are subordinate to other classes; and (iv) the complex structure of the security may not be fully understood at the time of investment and may produce disputes with the issuer or unexpected investment results.

(vi) Leverage risk

CLO vehicles are typically very highly levered (10 – 14 times), and therefore the junior debt and equity tranches that the Fund invests in are subject to a higher degree of risk of total loss. In particular, investors in CLO vehicles indirectly bear risks of the underlying debt investments held by such CLO vehicles. The Fund generally has the right to receive payments only from the CLO vehicles, and generally does not have direct rights against the underlying borrowers or the entity that sponsored the CLO vehicle. While the CLO vehicles the Fund targets generally enable the investor to acquire interests in a pool of senior loans without the expenses associated with directly holding the same investments, the Fund generally pays a proportionate share of the CLO vehicles’ administrative and other expenses. Although it is difficult to predict whether the prices of indices and securities underlying CLO vehicles will rise or fall, these prices (and, therefore, the prices of the CLO vehicles) will be influenced by the same types of political and economic events that affect issuers of securities and capital markets generally. The failure by a CLO vehicle in which we invest to satisfy financial covenants, including with respect to adequate collateralization and/or interest coverage tests, could lead to a reduction in its payments to us. In the event that a CLO vehicle fails certain tests, holders of debt senior to us may be entitled to additional payments that would, in turn, reduce the payments we would otherwise be entitled to receive. Separately, we may incur expenses to the extent necessary to seek recovery upon default or to negotiate new terms with a defaulting CLO vehicle or any other investment we may make. If any of these occur, it could materially and adversely affect our operating results and cash flows.

24

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (continued)

December 31, 2015

7. Concentrations of Risk (concluded)

(b) Counterparty credit risk

Counterparty credit risk is the risk a counterparty to a financial instrument could fail on a commitment that it has entered into with the Fund. The Fund minimizes counterparty credit risk by undertaking transactions with large well-capitalized counterparties or brokers and by monitoring the creditworthiness of these counterparties.

(c) Credit risk

When the Fund invests in structured credit investments, the Fund does not have custody of the assets of the structured credit investment or control over the investment. In certain structured credit investments, the Fund may have limited access to or information regarding the assets of or collateral underlying the structured credit investment. Furthermore, the Fund may not be able to confirm independently the accuracy of the information provided by the managers of structured credit investments. As such, there may be uncertainty with respect to the information available to the Fund for purposes of analyzing the reasonableness of an independent price obtained for a structured credit investment or to fair value a structured credit investment. Ultimately, the uncertainty of the reliability of (or limited access to) information received in respect of a structured credit investment may impair the Fund’s ability to value its investment. As a result, the amount realized by the Fund upon disposition of the structured credit investment could be materially different from that which is reported as the carrying value of the investment at any point in time.

8. Indemnifications

The Fund enters into contracts that contain a variety of indemnifications. The Fund’s maximum exposure under these arrangements is unknown. However, since inception the Fund has not had claims or losses pursuant to these contracts and expects the risk of loss to be remote.

25

SEI Structured Credit Fund, L.P.

Notes to Financial Statements (concluded)

December 31, 2015

9. Financial Highlights

The following represents the ratios to average net assets and other supplemental information for the following periods:

| For the year | For the year | For the year | For the year | For the year | ||||||||||||||||

| ended | ended | ended | ended | ended | ||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

Total return (1) | -6.95 | % | 5.06 | % | 8.03 | % | 25.46 | % | 8.36 | % | ||||||||||

Limited Partners’ capital, end of year (000’s) | $ | 1,298,480 | $ | 1,387,197 | $ | 1,236,651 | $ | 894,989 | $ | 396,345 | ||||||||||

Ratio to average partners’ capital† | ||||||||||||||||||||

Net investment income ratio†† | ||||||||||||||||||||

Net investment income | 9.00 | % | 7.63 | % | 10.02 | % | 9.27 | % | 7.23 | % | ||||||||||

Expense ratio†† | ||||||||||||||||||||

Operating expenses | 0.12 | % | 0.12 | % | 0.13 | % | 0.16 | % | 0.18 | % | ||||||||||

Portfolio turnover rate | 35.45 | % | 53.74 | % | 62.90 | % | 86.43 | % | 76.57 | % | ||||||||||

| † | Ratios to average partners’ capital are calculated based on the outstanding Limited Partners’ capital during the period. |

| †† | Ratios do not include the Fund’s allocated share of income/expense from investments in other funds. |

| (1) | Total return, which reflects the month-to-month change in Limited Partners’ capital, is calculated using returns that have been geometrically linked based on capital contributions and withdrawals. |

10. Subsequent Events

The Fund has evaluated the need for additional disclosures and/or adjustments resulting from subsequent events through the date the financial statements were issued. Based on this evaluation, no disclosures and/or adjustments were required to the financial statements.

26

SEI Structured Credit Fund, L.P.

Approval of the Advisory Agreements with the Adviser (Unaudited)

SEI Structured Credit Fund, L.P. (the “Fund”) has entered into an investment advisory agreement with SEI Investments Management Corporation (“SIMC” or the “Adviser”) dated July 20, 2007 (the “Advisory Agreement”). Pursuant to the Advisory Agreement, SIMC is responsible for the day-to-day investment management of the Fund’s assets.

The Investment Company Act of 1940, as amended (the “1940 Act”), requires that the initial approval of, as well as the continuation of, the Fund’s Advisory Agreement must be specifically approved by: (i) the vote of the Board of Directors of the Fund (the “Board”) or by a vote of the shareholders of the Fund; and (ii) the vote of a majority of the directors who are not parties to the Advisory Agreement or “interested persons” (as defined under the 1940 Act) of any party to the Advisory Agreement (the “Independent Directors”), cast in person at a meeting called for the purpose of voting on such approval. In connection with their consideration of such approvals, the Board must request and evaluate, and SIMC is required to furnish, such information as may be reasonably necessary to evaluate the terms of the Advisory Agreement. In addition, the Securities and Exchange Commission (“SEC”) takes the position that, as part of their fiduciary duties with respect to a fund’s fees, fund boards are required to evaluate the material factors applicable to a decision to approve an advisory agreement.

The discussion immediately below summarizes the materials and information presented to the Board in connection with the Board’s Annual Review of the Advisory Agreement and the conclusions made by the Directors when determining to continue the Advisory Agreement for an additional one-year period.

Consistent with the responsibilities referenced above, the Board called and held a meeting on March 23, 2015 to consider whether to renew the Advisory Agreement. In preparation for the meeting, the Board provided SIMC with a written request for information and received and reviewed extensive written materials in response to that request, including information as to the performance of the Fund versus benchmarks, the levels of fees for various categories of services provided by SIMC and its affiliates and the overall expense ratio of the Fund, comparisons of such fees and expenses with such fees and expenses incurred by other funds, the costs to SIMC and its affiliates of providing such services, including a profitability analysis, SIMC’s compliance program, and various other matters. The information provided in connection with the Board meeting was in addition to the detailed information about the Fund that the Board reviews during the course of each year, including information that relates to the operations and performance of the Fund.

27

SEI Structured Credit Fund, L.P.

Approval of the Advisory Agreements with the Adviser (Unaudited)

(continued)

The Directors also received a memorandum from Fund counsel regarding the responsibilities of directors in connection with their consideration of an investment advisory agreement. In addition, prior to voting, the Independent Directors received advice from Fund counsel regarding the contents of the Adviser’s written materials.

As noted above, the Board requested and received written materials from SIMC. Specifically, this requested information and written response included: (a) the quality of SIMC’s investment management and other services; (b) SIMC’s investment management personnel; (c) SIMC’s operations and financial condition; (d) SIMC’s investment strategies; (e) the level of the advisory fees that SIMC charges the Fund compared with the advisory fees charged to comparable funds; (f) the overall fees and operating expenses of the Fund compared with similar funds; (g) the level of SIMC’s profitability from its Fund-related operations; (h) SIMC’s compliance systems; (i) SIMC’s policies on and compliance procedures for personal securities transactions; (j) SIMC’s reputation, expertise and resources in domestic and/or international financial markets; and (k) the Fund’s performance compared with benchmark indices.

The Independent Directors met in executive session, outside the presence of Fund management, and the full Board met in executive session to consider and evaluate a variety of factors relating to the approval of the continuation of the Advisory Agreement. The Independent Directors also participated in question and answer sessions with representatives of the Adviser. At the conclusion of the Board’s deliberations, the Board including the Independent Directors unanimously approved the continuation of the Advisory Agreement for an additional one-year period. The approval was based on the Board’s (including the Independent Directors’) consideration and evaluation of a variety of specific factors discussed at the March 23, 2015 Board meeting and other Board meetings held throughout the year, including:

| • | the nature, extent and quality of the services provided to the Fund under the Advisory Agreement, including the resources of SIMC and its affiliates dedicated to the Fund; |

| • | the Fund’s investment performance and how it compared to that of appropriate benchmarks; |

| • | the expenses of the Fund under the Advisory Agreement and how those expenses compared to those of other comparable funds; |

| • | the profitability of SIMC and its affiliates with respect to the Fund, including both direct and indirect benefits accruing to SIMC and its affiliates; and |

28

SEI Structured Credit Fund, L.P.

Approval of the Advisory Agreements with the Adviser (Unaudited)

(concluded)

| • | the extent to which economies of scale would be realized as the Fund grows and whether fee levels in the Advisory Agreement reflect those economies of scale for the benefit of Fund investors. |

Nature, Extent and Quality of Services. The Board concluded that, within the context of its full deliberations, the nature, extent and quality of services provided by SIMC to the Fund and the resources of SIMC and its affiliates dedicated to the Fund supported renewal of the Advisory Agreement.

Fund Performance. The Board concluded that, within the context of its full deliberations, the performance of the Fund supported renewal of the Advisory Agreement.

Fund Expenses. The Board concluded that, within the context of its full deliberations, the expenses of the Fund are reasonable and supported renewal of the Advisory Agreement.

Profitability. The Board concluded that, within the context of its full deliberations, the profitability of SIMC is reasonable and supported renewal of the Advisory Agreement.

Economies of Scale. The Board concluded that, within the context of its full deliberations, the Fund obtains reasonable benefit from economies of scale.

Based on its evaluation of the information and the conclusions with respect thereto at its meeting on March 23, 2015, the Board, including all of the Independent Directors, unanimously approved the Advisory Agreement and concluded that the compensation under the Advisory Agreement is fair and reasonable in light of such services and expenses and such other matters as the Independent Directors and the Board considered to be relevant in the exercise of their reasonable judgment. In the course of their deliberations, the Board, including the Independent Directors, did not identify any one particular factor or specific piece of information that determined whether to approve the Advisory Agreement.

29

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited)

December 31, 2015

Set forth below are the Names, Age, Addresses, Position with the Partnership, Length of Time Served, the Principal Occupations During the Past Five Years, Number of Portfolios in Fund Complex Overseen by the Director, and Other Directorships Outside the Fund Complex of each of the persons currently serving as Directors and Officers of the Partnership.

Name, Age and Address of Independent Directors | Length of | Principal Occupation(s) During Past 5 | Number of Portfolios in Fund Complex Overseen by Director** | Other Directorships Held by Director | ||||

Nina Lesavoy (58) 3 E. 63rd St. New York, NY 10065 | Since 2007 | Founder & Managing Director, Avec Capital since April 2008, Partner, Cue Capital 2002-2008. | 99 | Trustee of SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Institutional Investments Trust, SEI Tax Exempt Trust, SEI Institutional Managed Trust, Adviser Managed Trust, New Covenant Funds, SEI Insurance Products Trust and the SEI Catholic Values Trust. |

30

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (continued)

December 31, 2015

Name, Age and Address of Independent Directors | Length of | Principal Occupation(s) During Past 5 | Number of Portfolios in Fund Complex Overseen by Director** | Other Directorships Held by Director | ||||

George J. Sullivan (73) 7 Essex Green Drive, Suite 52B Peabody, MA 01960 | Since 2007 | Self Employed Consultant, Newfound Consultants Inc., since April 1997. Member of independent review committee for SEI’s Canadian-registered mutual funds since 2009. | 99 | Trustee of State Street Navigator Securities Lending Trust, The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II, Bishop Street Funds, SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional Investments Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust, SEI Institutional Managed Trust, Adviser Managed Trust, New Covenant Funds, SEI Insurance Products Trust and the SEI Catholic Values Trust. |

31

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (continued)

December 31, 2015

Name, Age and Address of Independent Directors | Length of | Principal Occupation(s) During Past 5 | Number of Portfolios in Fund Complex Overseen by Director** | Other Directorships Held by Director | ||||

James M. Williams (68) 1200 Getty Drive, Suite 400, Los Angeles, CA 90049-1681 | Since 2007 | Vice President and Chief Investment Officer, J. Paul Getty Trust, Non Profit Foundation for Visual Arts, since December 2002. | 99 | Trustee of Ariel Mutual Funds, SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional Investments Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust, SEI Institutional Managed Trust, Adviser Managed Trust, New Covenant Funds, SEI Insurance Products Trust and the SEI Catholic Values Trust. |

32

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (continued)

December 31, 2015

Name, Age and Address of Independent Directors | Length of | Principal Occupation(s) During Past 5 | Number of Portfolios in Fund Complex Overseen by Director** | Other Directorships Held by Director | ||||

Robert A. Nesher* (69) One Freedom Valley Drive Oaks, PA 19456 | Since 2007 | Currently performs various services on behalf of SEI Investments for which Mr. Nesher is compensated. | 99 | Trustee of The Advisors’ Inner Circle Fund, The Advisors’ Inner Circle Fund II and Bishop Street Funds; Director of SEI Global Master Fund, plc, SEI Global Assets Fund, plc, SEI Global Investments Fund, plc, SEI Investments Global, Limited, SEI Investments – Global Fund Services Limited, SEI Investments (Europe) Limited, SEI Global Nominee Ltd, SEI Asset Allocation Trust, SEI Daily Income Trust, SEI Institutional Investments Trust, SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Tax Exempt Trust, SEI Institutional Managed Trust, Adviser Managed Trust, New Covenant Funds, SEI Insurance Products Trust and the SEI Catholic Values Trust. |

33

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (continued)

December 31, 2015

Name and Age of Officers | Position(s) Held with the Master Fund and Length of Time Served | Principal Occupation(s) During Past 5 Years | ||

| Arthur Ramanjulu (51) | Treasurer, since 2015 | Director, Funds Accounting, SEI Investments Global Fund Services (March 2015); Senior Manager, Funds Accounting, SEI Global Funds Services (March 2007 to February 2015). | ||

| Timothy D. Barto (47) | Vice President, since 2007 and Assistant Secretary, since 2008 | General Counsel Vice President and Secretary of the Adviser since 2004. Vice President and Assistant Secretary of SEI since 2001, and of the Administrator since November 1999. | ||

| Aaron Buser (45) | Vice President and Assistant Secretary, since June 2008 | Vice President and Assistant Secretary of Adviser since 2007. Associate at Stark & Stark 2004-2007. | ||

34

SEI Structured Credit Fund, L.P.

Additional Information

Directors and Officers of the Partnership (Unaudited) (concluded)

December 31, 2015

Name and Age of Officers | Position(s) Held with the Master Fund and Length of Time Served | Principal Occupation(s) During Past 5 Years | ||

| Brian F. Vrabel (35) | Vice President and Secretary, since June 2012 | Vice President and Assistant Secretary of the Adviser since 2012. Associate at Klehr Harrison Harvey Branzburg LLP 2007 – April 2012. | ||

| Russell Emery (52) | Chief Compliance Officer, since 2007 | Chief Compliance Officer of SEI Fund Complex, Bishop Street Funds, The Advisors’ Inner Circle Fund and the Advisors’ Inner Circle Fund II, since March 2006; New Covenant Funds, since February 2012; Chief Compliance Officer of New Covenant Funds since February 2012. Chief Compliance Officer of SEI Insurance Products Trust since 2013. Chief Compliance Officer of SEI Catholic Values Trust since 2015. | ||

| * | Mr. Nesher is a trustee who may be deemed to be an “interested” person of the Fund as that term is defined in the 1940 Act by virtue of his affiliation with the Fund’s Distributor. |

| ** | The “Fund Complex” consists of registered investment companies that are part of the following investment trusts and limited partnerships: SEI Institutional Investments Trust, SEI Institutional Management Trust, Adviser Managed Trust SEI Institutional International Trust, SEI Liquid Asset Trust, SEI Daily Income Trust, SEI Tax Exempt Trust, SEI Asset Allocation Trust, SEI Structured Credit, L.P., New Covenant Funds, SEI Insurance Products Trust and SEI Catholic Values Trust. |

35

Item 2. Code of Ethics.

The Registrant has adopted a code of ethics that applies to the Registrant’s principal executive officer, principal financial officer, comptroller or principal accounting officer. A copy of its code of ethics is filed with this Form N-CSR under Item 12(a)(1).

Item 3. Audit Committee Financial Expert.

(a)(1) The Registrant’s board of directors has determined that the Registrant has at least one audit committee financial expert serving on the audit committee.

(a)(2) The audit committee financial expert is George Sullivan. Mr. Sullivan is independent as defined in Form N-CSR Item 3(a)(2).

Item 4. Principal Accountant Fees and Services.

Fees billed by PricewaterhouseCoopers LLP (“PwC”) related to the Registrant.

PwC billed the Registrant aggregate fees for services rendered to the Registrant for the last two fiscal years as follows:

| 2015 | 2014 | |||||||||||||||||||||||||

| All fees and services to the Fund that were pre- approved | All fees and services to service affiliates that were pre- approved | All other fees and services to service affiliates that did not require pre- approval | All fees and services to the Fund that were pre- approved | All fees and services to service affiliates that were pre- approved | All other fees and services to service affiliates that did not require pre- approval | |||||||||||||||||||||

(a) | Audit Fees (1) | $ | 86,700 | N/A | N/A | $ | 85,000 | N/A | N/A | |||||||||||||||||

(b) | Audit-Related Fees | $ | 0 | N/A | N/A | $ | 0 | N/A | N/A | |||||||||||||||||

(c) | Tax Fees | $ | 0 | N/A | N/A | $ | 0 | N/A | N/A | |||||||||||||||||

(d) | All Other Fees | $ | 0 | N/A | N/A | $ | 0 | N/A | N/A | |||||||||||||||||

Notes: