Investor Conference February 15, 2010 Exhibit 99.2 |

February 2011 1 |

Investor Conference February 15, 2010 |

February 2011 3 Please review the corresponding video link "Customer Service Video" on the American Water website |

Introduction Ed Vallejo Vice President - Investor Relations |

February 2011 5 Certain statements in this presentation are forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are predictions based on our current expectations and assumptions regarding future events and may relate to, among other things, our future financial performance, our growth and portfolio optimization strategies, our projected capital expenditures and related funding requirements, our ability to repay debt, our ability to finance current operations and growth initiatives, the impact of legal proceedings and potential fines and penalties, business process and technology improvement initiatives, trends in our industry, regulatory or legal developments or rate adjustments. Actual results could differ materially because of factors such as the completion of the independent audit of our financial statements; decisions of governmental and regulatory bodies, including decisions to raise or lower rates; the timeliness of regulatory commissions’ actions concerning rates; changes in laws, governmental regulations and policies, including environmental, health and water quality and public utility regulations and policies; weather conditions, patterns or events, including drought or abnormally high rainfall; changes in customer demand for, and patterns of use of, water, such as may result from conservation efforts; significant changes to our business processes and corresponding technology; our ability to appropriately maintain current infrastructure; our ability to obtain permits and other approvals for projects; changes in our capital requirements; our ability to control operating expenses and to achieve efficiencies in our operations; our ability to obtain adequate and cost-effective supplies of chemicals, electricity, fuel, water and other raw materials that are needed for our operations; our ability to successfully acquire and integrate water and wastewater systems that are complementary to our operations and the growth of our business or dispose of assets or lines of business that are not complementary to our operations and the growth of our business; cost overruns relating to improvements or the expansion of our operations; changes in general economic, business and financial market conditions; access to sufficient capital on satisfactory terms; fluctuations in interest rates; restrictive covenants in or changes to the credit ratings on our current or future debt that could increase our financing costs or affect our ability to borrow, make payments on debt or pay dividends; fluctuations in the value of benefit plan assets and liabilities that could increase our cost and funding requirements; our ability to utilize our U.S. and state net operating loss carryforwards; migration of customers into or out of our service territories; difficulty in obtaining insurance at acceptable rates and on acceptable terms and conditions; the incurrence of impairment charges ability to retain and attract qualified employees; and civil disturbance, or terrorist threats or acts or public apprehension about future disturbances or terrorist threats or acts. Any forward-looking statements we make, speak only as of the date of this presentation. Except as required by law, we do not have any obligation, and we specifically disclaim any undertaking or intention, to publicly update or revise any forward- looking statements, whether as a result of new information, future events, changed circumstances or otherwise. Cautionary Statement Concerning Forward-Looking Statements |

6 Jeff Sterba: Strategy Overview Walter Lynch: Regulated Overview Break Ellen Wolf: Financial Overview Closing and Q&As Today’s Agenda February 2011 |

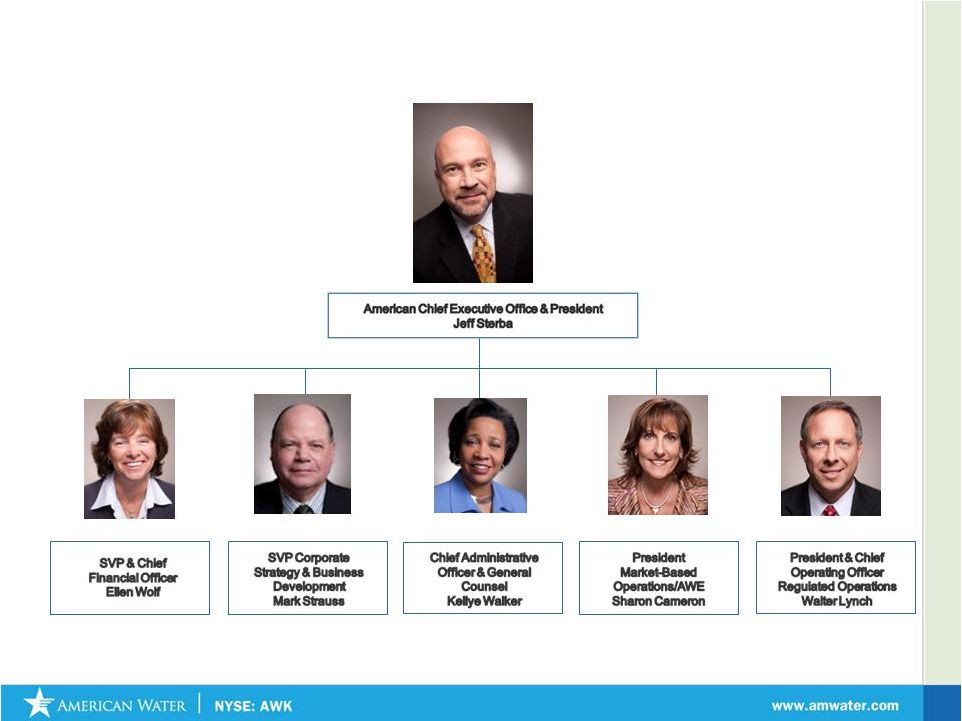

American Water Overview: Strategy & Goals Jeff Sterba President and Chief Executive Officer |

8 Executive Team February 2011 |

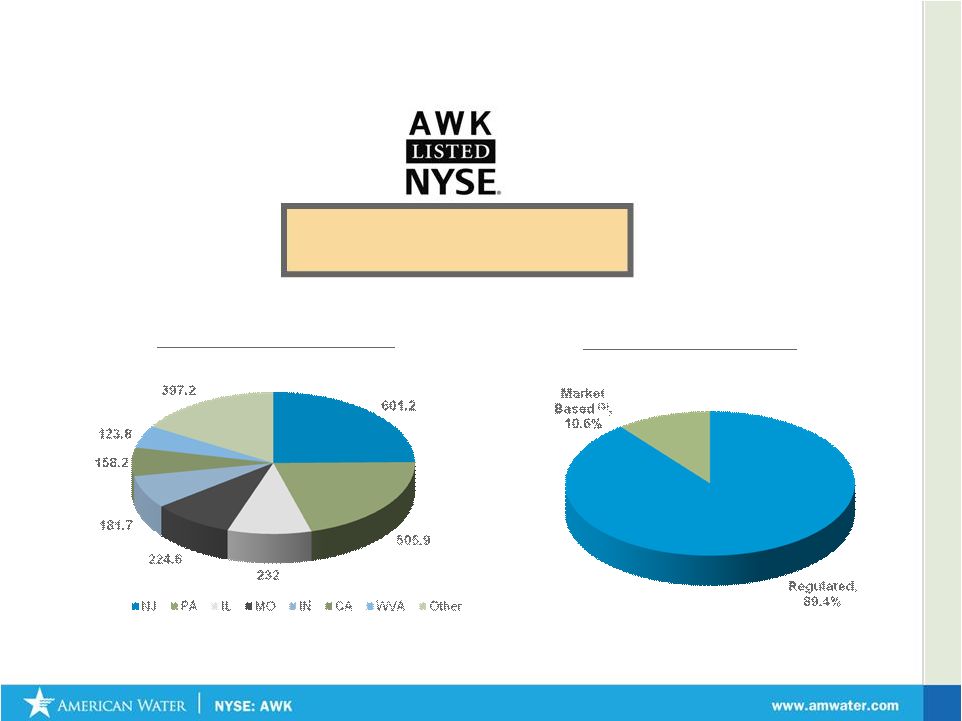

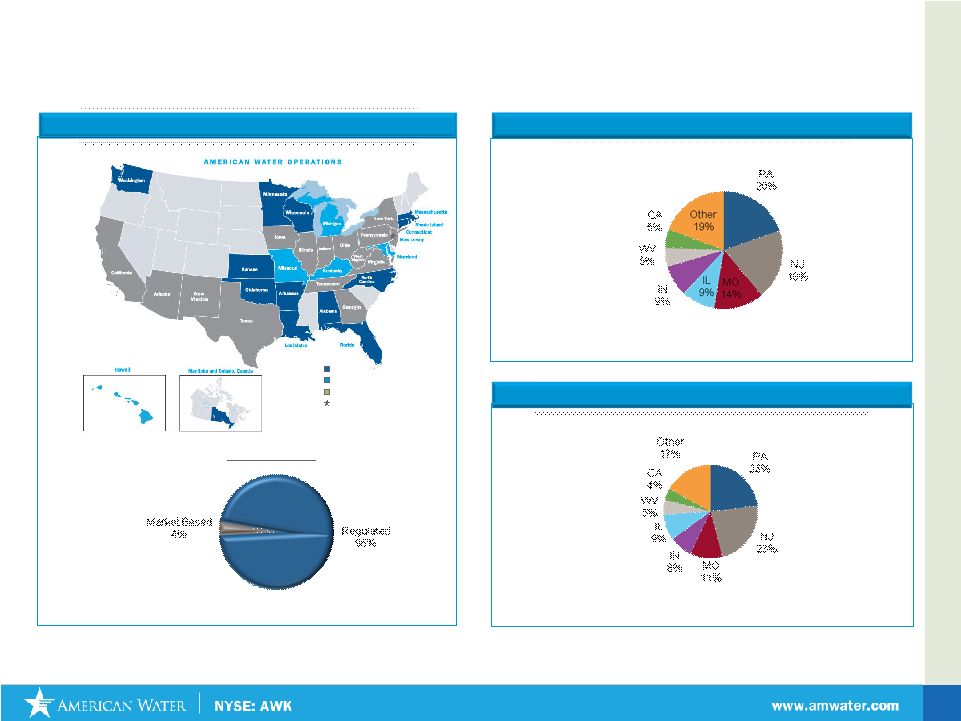

9 American Water: The Premier Water Services Provider in North America Geographic Diversity (1) Business Diversity (1) Market Cap: $4.7 Billion Enterprise Value: $10.2 Billion Average Volume Traded: 1.1 Million shares (1) 2010 Revenues (2) Market data as of 2/9/11 (3) Market Based includes Other February 2011 |

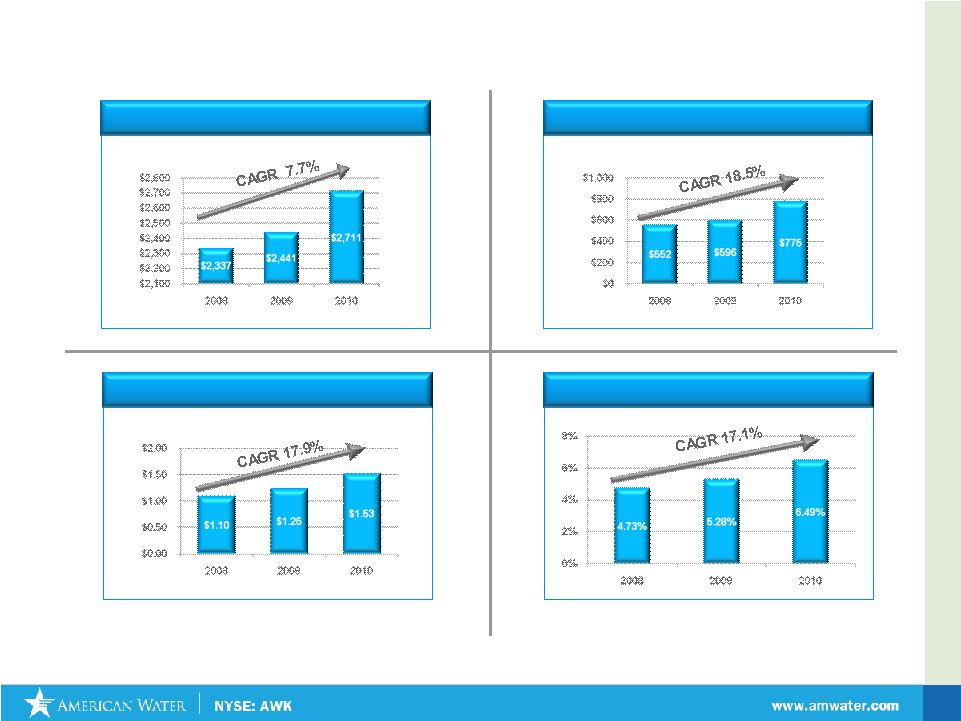

February 2011 10 American Water: A Snapshot • 2010 Preliminary Results • EPS and ROE exclude impairment charges Cash Flow From Operations (in millions) Earnings Per Share Operating Revenues (in millions) Return on Equity |

11 What You’ll Hear Today Sound Corporate Strategy and Key Initiatives Portfolio Optimization Regulatory Policy Regulated and Market-Based Opportunities Operational Excellence Continued Investment in Infrastructure Driving Excellent Results and Prospects 2010 Financial Results – Expected $1.53 Long Term Growth 2011 Guidance of $1.65-$1.75 Sustained 7-10% EPS Growth Improving Rates of Return Commitment to our Customers, Employees and Shareholders February 2011 |

The U.S. Water Industry February 2011 12 |

February 2011 13 Water Industry Has a Favorable Utility Profile Water Utility Characteristics Implications • Capital projects focused on maintaining public health & safety standards • Regulators supportive of prudent projects • Water bills low portion of household budget • Essential product – no substitutes • Demand is more price inelastic than electric or gas • Raw input costs (i.e. water and chemicals) less volatile than other utility commodity costs (i.e. coal and natural gas) • More stable rates for customers • Cost forecasting and regulatory lag is more manageable • M&A primarily small tuck-ins enabling targets to meet health & safety standards • Regulators generally support the strengthening of water systems via M&A • Water storage more feasible and cheaper than electricity or gas storage • Water utilities can be more cost efficient and responsive to demand fluctuations • Large water utilities diversified across multiple geographies • Mitigates impact of localized severe weather conditions / regulatory outcomes |

February 2011 Our Values • Honesty and Integrity • Communication •Teamwork • Excellence • Engagement Our Mission • Providing safe, reliable water services to our customers and communities • Driving Operational Excellence • Enabling employees to innovate • Ensuring long-term stewardship of all resources •Engaging customers, regulators and other constituencies in solving critical water issues •Earning a fair return for our shareholders Our Vision To be the trusted steward of your precious resource – water What We Stand For 14 |

15 American Water: Providing Value to Customers, Employees and Shareholders Operational Excellence Employer of Choice Sustainability Customer Focus Regulatory & Public Policy Targeted Growth American Water provides value-added products and services that address customers’ needs Investor Driven Customer Driven Value Price Cost February 2011 |

February 2011 • Earn appropriate return on investments • Promote constructive regulatory frameworks • Grow Regulated Businesses through focused acquisitions • Pursue “regulated-like” opportunities • Focus on Operations Efficiencies Goals Actions Regulated Operations & Support • Invest in states where we can add value to customers and generate an appropriate return • Move from “Rate Case Catchup” to “Regulatory Strategy” • Drive Operational Excellence Market Based Operations • Regulated-Like • Value-Added Services Future Pursuits • Disciplined pursuit of growth through acquisitions and applying technological expertise Strategy Specifics 16 |

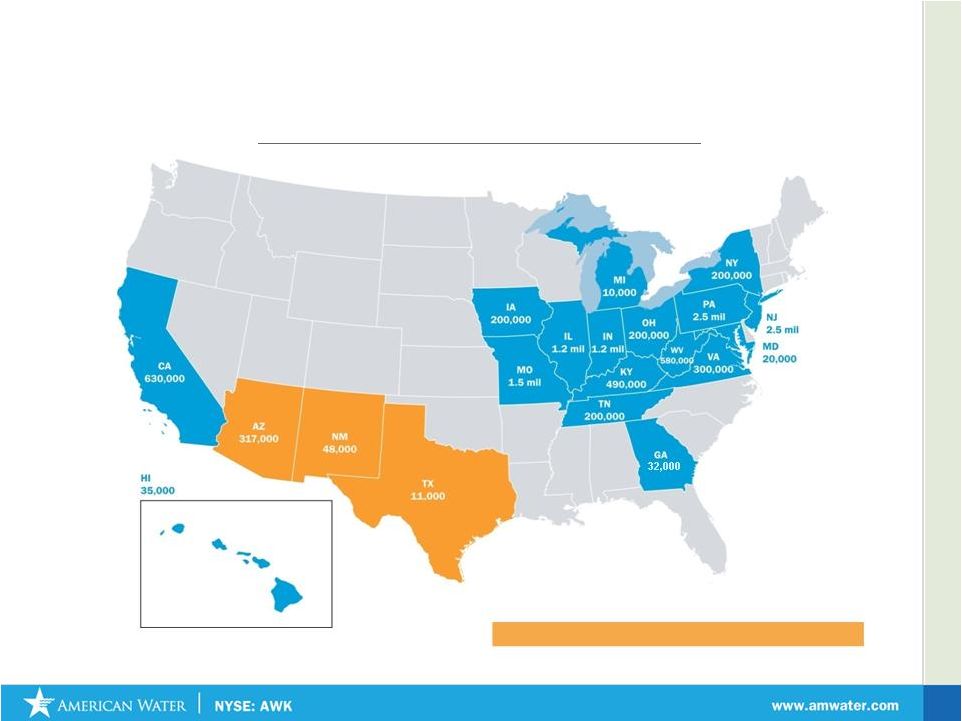

17 Strategy Specifics: Regulated Operations - Invest in states where we can add value American Water Regulated Operations: Population Served States we are in process of exiting thru Portfolio Optimization 32,000 * 2009 Data February 2011 |

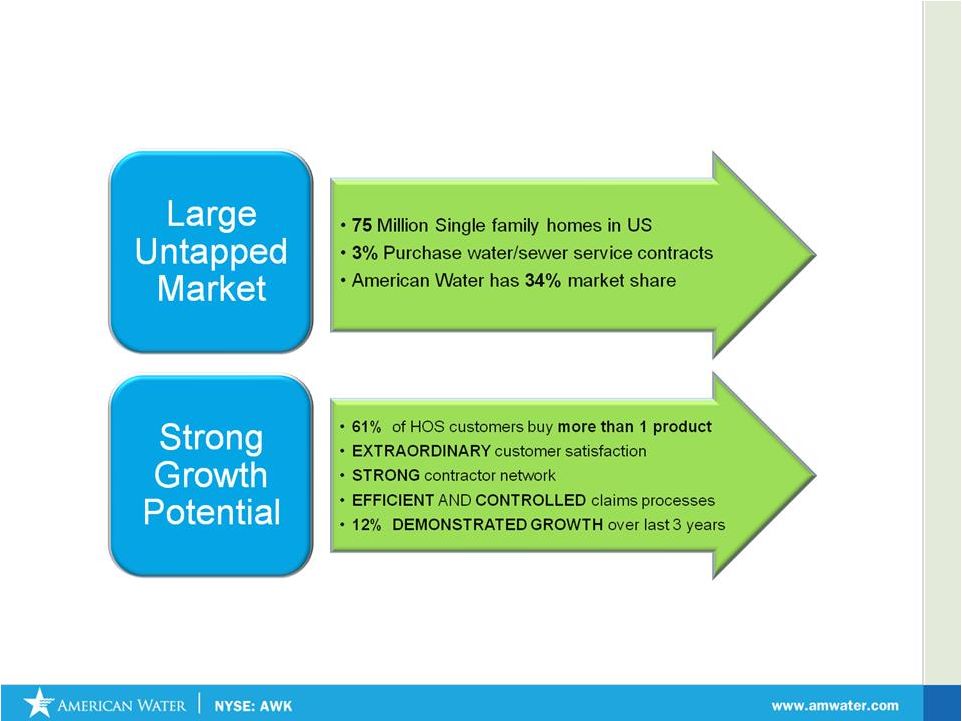

Strategy Specifics: Homeowner Services Growth 18 February 2011 |

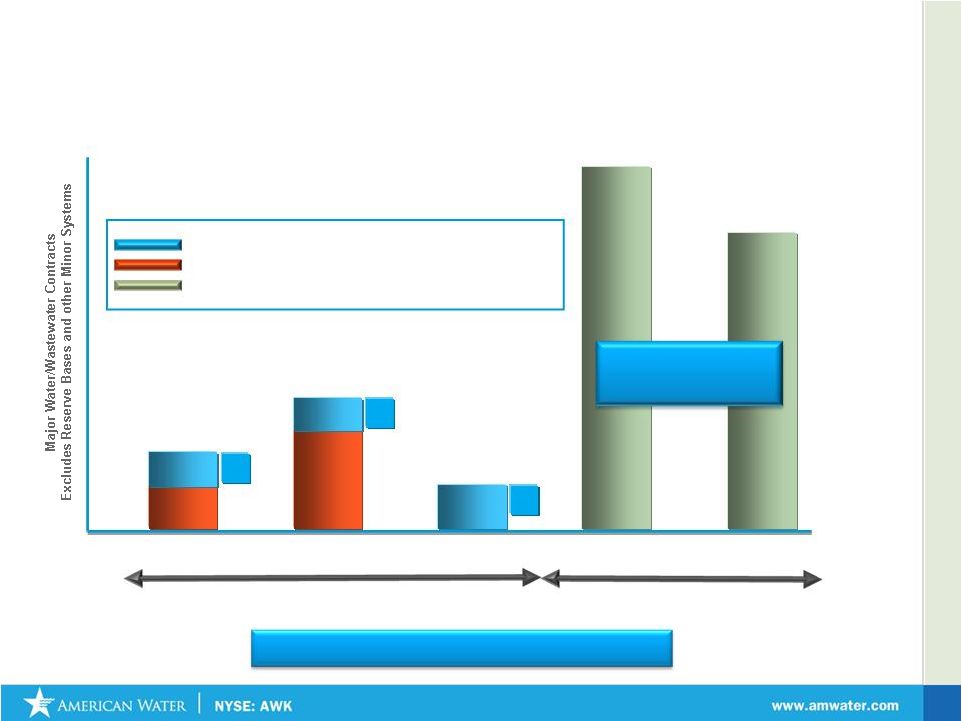

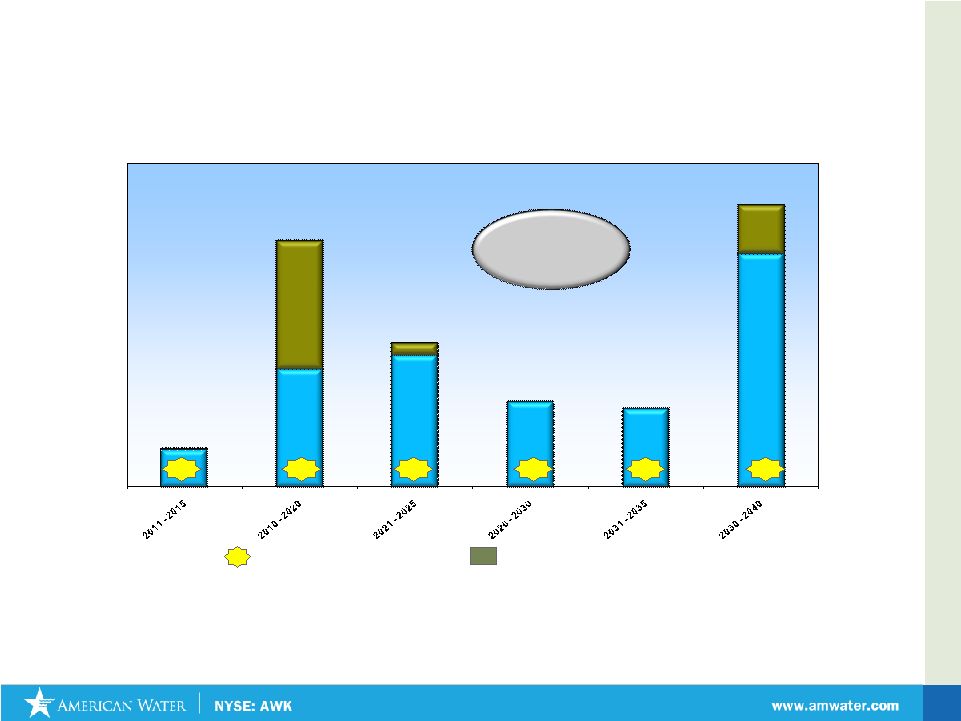

19 Strategy Specifics: Market Size of Military Utility Privatizations 2011-13 2014-16 Major Water/Wastewater Contracts to be Awarded Contracts Awarded to American Water Contracts Awarded to Competitors Contracts Programmed by Dept. of Defense for Award Over $2 Billion in Revenues Backlog 2002 2005-07 2008-10 Major Water/Wastewater Awards to Date Market Opportunity represents approximately $11Bn in Total Revenues 3 3 4 7 12 4 February 2011 |

February 2011 20 • Shorter Term Contracts • Heavy Competition • High Risk • Low Margin • Resource Intensive • Minimal Scalability Strategy Specifics – Municipal Contract Operations The Current Model Our Value Model • Longer Term Contracts • Form of Public Private Partnership • Shared Risk • Performance Metrics • Price Redetermination • Priority of Payment |

21 Profitable Growth Drivers Core Businesses • Infrastructure Investment • Tuck Ins • Homeowner Services • Military Utility Privatizations New Markets New Products Strategy Specifics: Growth Avenues • Acquisitions in new territories • Homeowner Services (new territories) • Military (beyond Army) • Homeowner Services (new services) • New Municipal Contract Model • Technology . February 2011 |

February 2011 22 Investment Thesis: Sustained 7-10% EPS Growth Future Growth Short Term Long Term New Services Regulated Investments Acquisitions Operational Excellence/ Efficiencies ROE improvement Long Term Growth Conceptual Representation |

Regulated Operations Initiatives Walter Lynch President & Chief Operating Officer Regulated Operations |

February 2011 24 Regulated Customers Net Utility Plant Total = 3,335,518 Regulated Market Based Both Corporate headquarters 2010 EBIT Total = $748 million American Water’s Geographic Presence Total = $11.1 billion American Water’s Regulated Portfolio |

American Water: Providing Value to customers and shareholders 25 Operational Excellence Employer of Choice Sustainability Customer Focus Regulatory & Public Policy Targeted Growth Value Price Cost February 2011 |

February 2011 Goal: To earn appropriate rate of return on investments Advancing consistent operational regulations Shaping constructive regulatory policies through participation in industry, regulatory and legislative settings Working with stakeholders to determine appropriate allowed ROE American Water’s Regulatory Initiatives 26 |

American Water’s Business Transformation Project Promote operating excellence, efficiency, and economies of scale Business Transformation Project Increase employee effectiveness and satisfaction Enhance the customer experience Upgrade legacy systems near the end of useful lives February 2011 27 |

28 American Water’s Business Transformation Project: Looking Ahead Implementation Oct. ’10 System Implementer selection Sep. ’11 Start EAM & CIS (Target “go live” Summer 2014) May ’11 Start ERP (Target “go live” summer 2012) Blueprint Project to be completed late 2014 Jan. ’11 Blueprint Phase begins (Completed in April 2011) May ’10 SAP software selection February 2011 |

American Water’s Portfolio Optimization Initiatives Continue to Lower Costs Focus on Value Drivers Optimizing Long-term Value Through Proactive Management Redeploy Value Into Core Growth Markets • Balanced Portfolio Analysis • Focus Achieving Authorized Rates of Return • Monetize Non-Producing Assets • Focused Capital Resources • Selective Acquisition Opportunities • Leverage Internal Growth Explore Opportunities for Long-Term Success Drive Profitability and Returns 29 February 2011 |

Portfolio Optimization Criteria STRATEGIC IMPORTANCE & RELEVANCE MATERIALITY OF INVESTMENT PROJECTED CAPITAL INTENSITY REGULATORY ENVIRONMENT POTENTIAL TO ACHIEVE CRITICAL MASS American Water’s Portfolio Optimization Criteria 30 February 2011 |

31 Portfolio Optimization Implementation *Transaction Details • Sale Price: $470 million • Sale Multiple: 1.14x Book Equity • AZ Rate Base (1) : $319 mm • NM Rate Base (1) : $34 mm Acquired by American Water Sold to AQUA MO TX NM AZ Agreement to sell by American Water * Missouri Transaction Details • Purchase Price: $3 million • Annual Revenue of $3.4 million • 59 wastewater systems • 10,000 people served (1) Rate base approved in rate cases by respective commissions *Transactions subject to closing risk and regulatory approval February 2011 |

February 2011 32 Please review the corresponding video link "KY Capex Video" on the American Water website |

Financial Overview Ellen Wolf Senior Vice President & Chief Financial Officer |

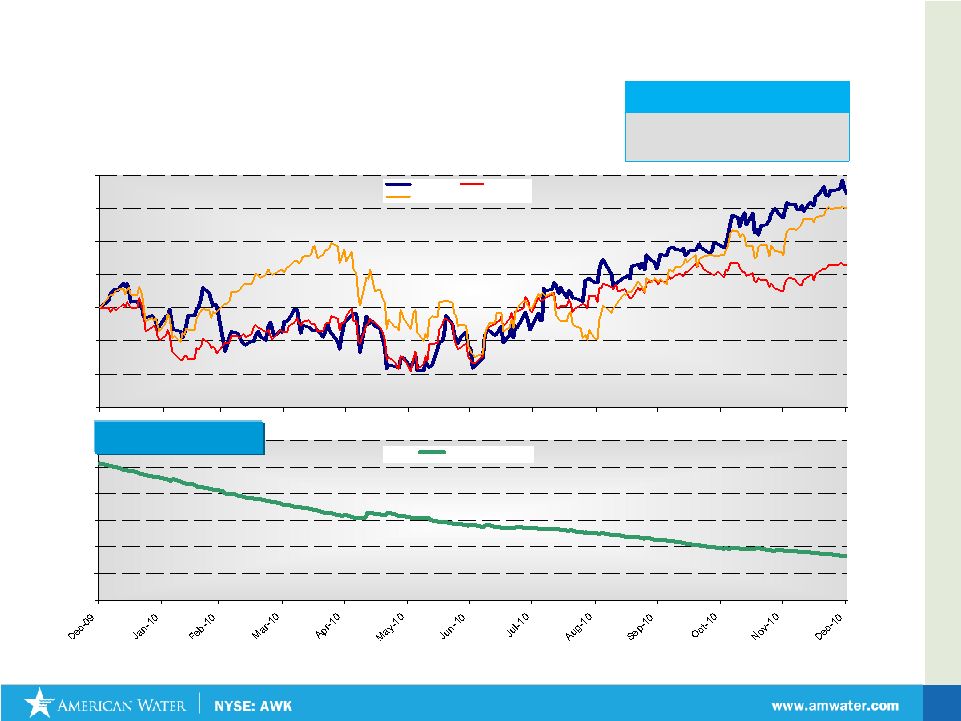

February 2011 85% 90% 95% 100% 105% 110% 115% 120% AWK DJ Util S&P 500 0.40 0.45 0.50 0.55 0.60 0.65 0.70 AWK Beta 34 Price as a percent of base (December 31, 2009 = 100%) Shareholder Return YTD American Water S&P 500 Dow Jones Utilities +17.3% +15.1% +6.5% S&P 500 Beta = 1 Total Shareholder Return : American Water vs. Indices (January 1, 2010 – December 31, 2010) |

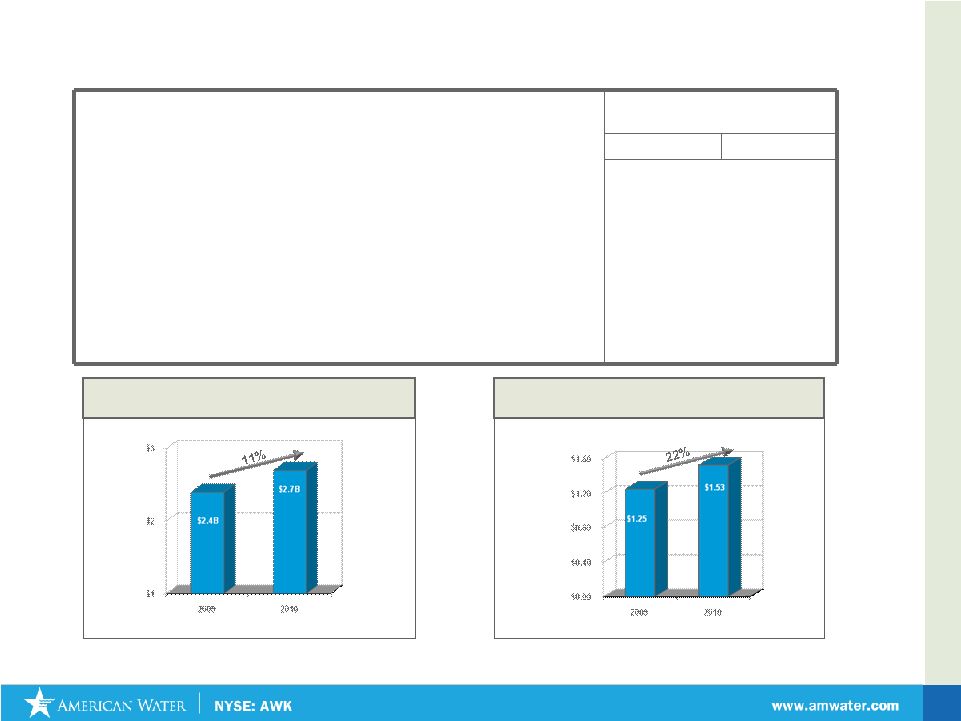

February 2011 35 For the Year Ended December 31, 2010 2009 (In thousands, except per share data) Revenue $2,710,677 $2,440,703 Gross Margin $748,091 $623,609 Gross Margin % 27.6% 25.6% Net income to common $267,827 $209,941 Common dividends paid $150,301 $137,331 Average common shares outstanding during the period 175,124 168,164 Net income per common share $1.53 $1.25 2010 Preliminary Financial Results Operating Revenues (in billions) Earnings per Share * Note: 2009 excludes impairment charge |

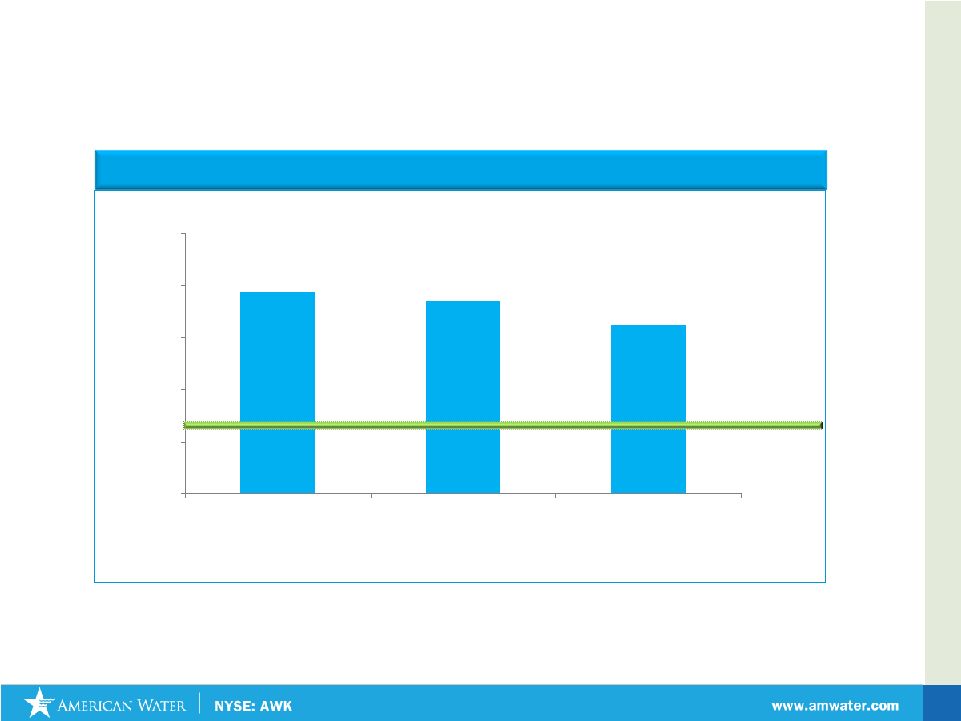

February 2011 36 Adjusted O & M Efficiency Ratio* 49.4% 48.5% 46.2% 30% 35% 40% 45% 50% 55% 2008 2009 2010 Regulated O&M Efficiency Ratio Continues to Improve *O&M Efficiency Ratio = operating and maintenance expenses / revenues, adjusted for purchased water Long Term Goal: Below 40% |

February 2011 37 Residential Commercial Industrial American Water Total American Water Customer – Gallons Consumption – Period over Period Analysis -5.8% -13.8% 11.9% -20.0% -15.0% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0% 2007-2008 2008-2009 2009-2010 -4.2% -4.9% 0.7% -6.0% -5.0% -4.0% -3.0% -2.0% -1.0% 0.0% 1.0% 2007-2008 2008-2009 2009-2010 -3.3% -4.9% 3.1% -6.0% -5.0% -4.0% -3.0% -2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 2007-2008 2008-2009 2009-2010 Fiscal Year Gallons by customer class 2008 2009 2010 Residential 213,423 203,701 204,575 Commercial 90,542 86,120 88,749 Industrial 42,032 36,212 40,539 Public and Other 58,838 55,911 56,604 Total Water Sales Volume (MM gal) 404,835 381,314 390,467 |

Rate Cases & Infrastructure Charges Granted in 2010 that will have impact on 2011 Core Strategy: Continuing Effort to Earn Appropriate Rate of Return on Prudent Investments Average Timing of Rate Cases: Approximately every 2 Years February 2011 38 |

February 2011 39 Rate Cases Awaiting Final Order as of December 31, 2010 Index of Rate Case Status 1 - Case Filed 2 - Discovery (Data Requests, Investigation) 3 - Negotiations / Evidentiary Hearings / Briefings 4 - Recommended order issued / settlement reached, without interim rates 5 - Interim rates in effect, awaiting final order Docket / Revenue Increase ROE Rate Base Filing Case Number Date Filed Filed Requested (Filed) Status Virginia Case No. PUE 2010-00001 3/8/2010 $6.9 11.50% $99.1 5 California Case No. A 10-07-007 7/1/2010 $37.3 10.20% $409.6 2 West Virginia Case No 10-920-W-42T 6/22/2010 $18.4 11.50% $437.6 3 Tennessee Case No 2010-00189 9/17/2010 $10.0 11.50% $125.5 2 Arizona W-01303A-10-0448 11/3/2010 $20.8 11.50% $148.9 1 Total $93.4 $1,220.7 * Final Order not yet issued. Interim rates are in effect. |

February 2011 40 Key Business Assumptions Continued decline in water usage per customer Low flow fixtures Declining family size Unemployment General conservation (promoted by US EPA) Downward trend has accelerated in most states since the late 1990’s Continued improvement in operating efficiency and cost structure Continued rate case recovery of prudent investments Gradual economic recovery by industrial and commercial customers Housing market slow to recover |

February 2011 Land, Bldgs, & Structures 4% Distribution 38% Pumping and Power 4% Treatment 9% Storage 4% Customer Meters 15% Source of Supply incl Mains 7% Info. and Comm. Systems * 4% Wastewater 3% Other 12% Capital Expenditure Plan, by Asset Type: 2011-2013 * includes Business Transformation capital spend • $800 - $1 Billion in Capex to be spent each year for the foreseeable future • 20% of Capital Expenditures will be recovered by Infrastructure Surcharge mechanisms 41 |

February 2011 42 Cash Flow from Operations Continues to Improve Relative to Capital Expenditures (CAPEX) No anticipated need for Equity Offering in 2011 Improving Cash Flow Metrics Increasingly Offset Need for Capital Raising CAPEX $800 Million - $1 Billion |

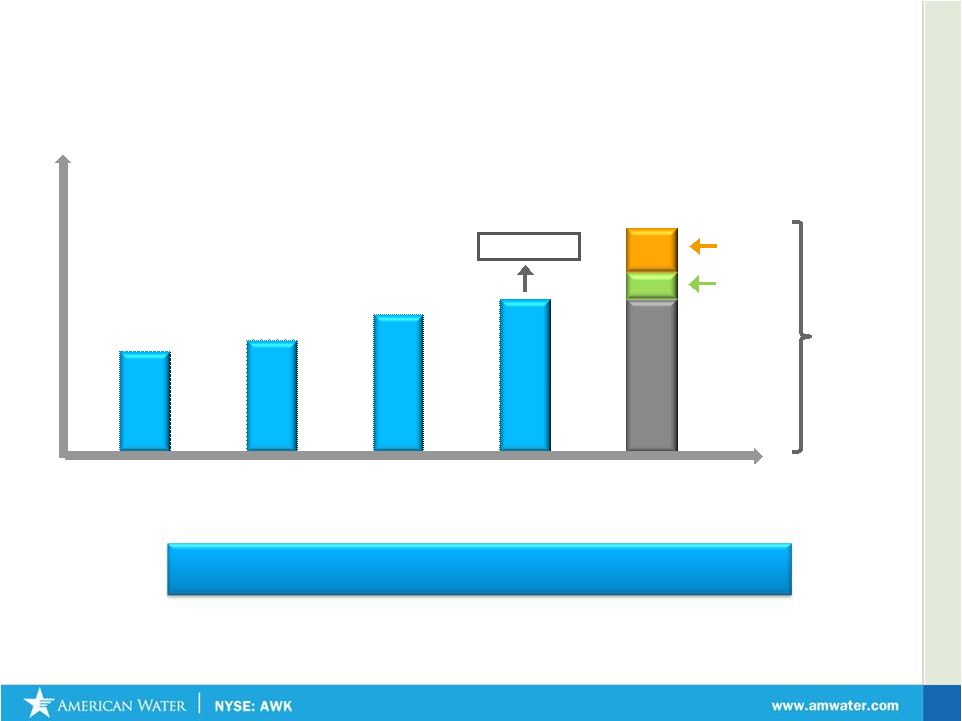

* Not to scale Key Factors Influencing Earnings * Not to scale 2011 Earnings Per Share Guidance: $1.65 - $1.75 Interest Rates (+/- 1%) 2011 EPS Guidance $1.65 - $1.75 Consumption (+/-1%) Fuel & Power (+/- 10%) Chemicals (+/- 10%) O&M Expense (+/- 1%) $1.77 $1.63 $1.65 $1.75 February 2011 43 |

4.73% 5.28% 6.49% 2008 2009 2010 2011 Allowed ROE Expected Return on Equity 10 % - 10.5 % ROE (2) 6.8% - 7.2% 1. ROE calculation excludes impairment charges 2. Range of allowed ROE 1.25% Parent Co. Debt Opportunity American Water continues to close ROE Gap February 2011 44 |

February 2011 45 $235 $728 $816 $524 $485 $1,439 $7 $790 $70 $303 Total Debt: $5,397M 5.5% 6.0% 6.0% 6.3% 6.0% Weighted Average Interest Rates Debt Maturities (in millions) Parent Company Debt 6.4% * * Amount excludes Preferred Stock with Mandatory Redemptions |

February 2011 125 years Investing in Water Infrastructure and paying Dividends to Shareholders 1886 1947 2003 2008 Dividend paid to private holders American Water Listed on NYSE – Dividend paid to common shareholders RWE takes AWK private. Dividend paid to shareholder AWK IPO Lists on NYSE. Pays dividends to common shareholders Watermain work in Pennsylvania. in the early 1900’s Infrastructure improvement in New Jersey in 2009 46 |

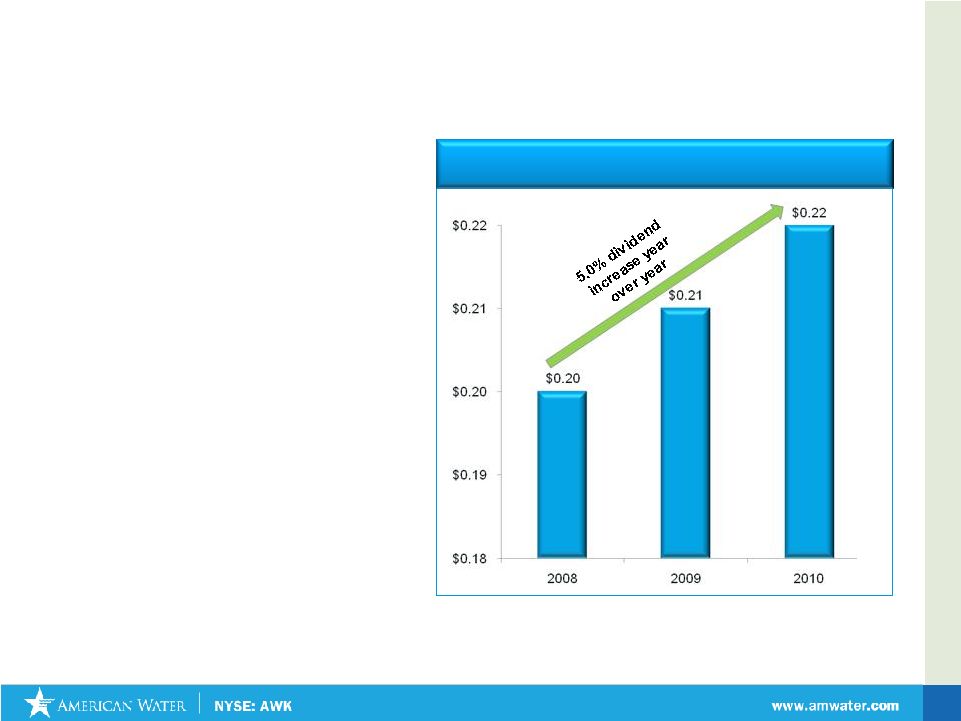

February 2011 Recent Dividend History Quarterly Dividend Rate as of Year-end • Key component of American Water’s total shareholder return proposition • Dividend Growth – Board of Directors increased dividend 5% to $0.22 or $0.88 annualized • Dividend Yield – 3.3% at 2/9/2011 • Growth in Dividend reflects growth in Net Income 47 |

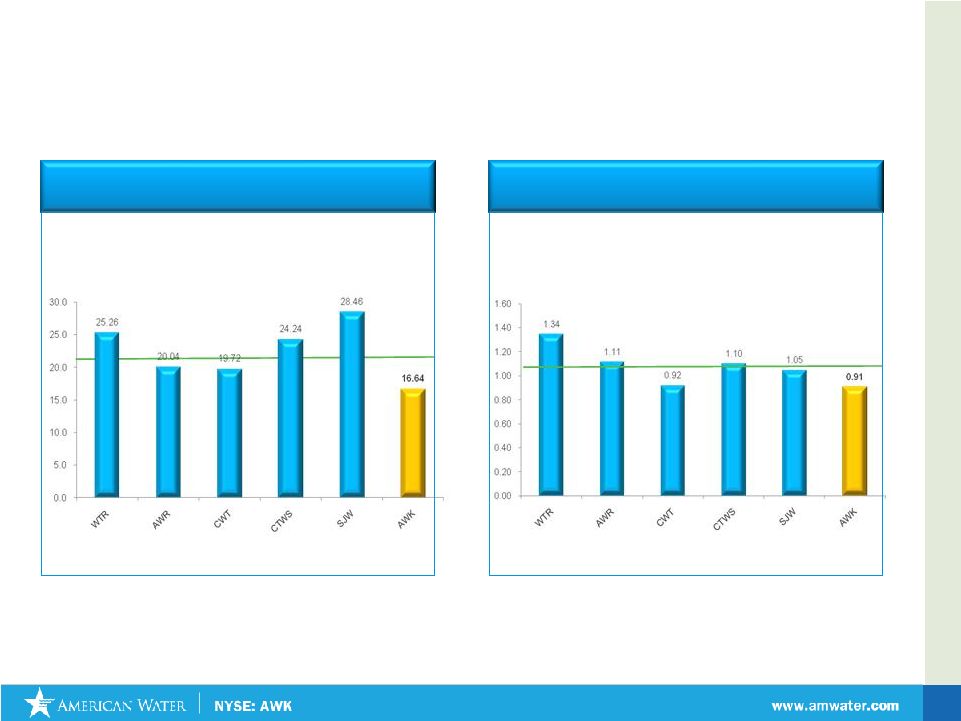

February 2011 P/E Ratio Enterprise Value* / Net PP&E* American Water – A Compelling Value 48 AW Stock Price at Average PE: $34.04 AW Stock Price at Highest PE: $43.26 AW Stock Price at Average EV/Net PP&E: $35.29 AW Stock Price at Highest EV/Net PP&E: $52.30 Average Average Close price 12/31/10 unless otherwise indicated; trailing twelve months diluted GAAP EPS as of 9/30/2010 *Data from Bloomberg Data Systems |

Closing |

February 2011 50 What to Expect from American Water in 2011 Start execution of Portfolio Optimization Initiative December 15, 2010: Announcement of acquisition of Missouri properties & sale of Texas American January 24, 2011: Announcement of sale of Arizona American and New Mexico American Resolve Rate Cases worth $93MM of filed Annualized Revenues by December 31, 2011 Initiate state specific efforts to address declining usage Continue reduction in Operating Efficiency Ratio Five-year goal below 40% Increase Earned Regulated Return Expand Market Based businesses with focus on Homeowner Services & Military Contract Operations Optimize Municipal Contract Operations Business Model |

February 2011 American Water – A Compelling Value Value Proposition Market Leader Strong Visible Growth Proven Management Trades at Discount to Peers Sound Regulatory Framework 51 |

February 2011 Investor Relations Contacts: • Ed Vallejo Vice President – Investor Relations Edward.vallejo@amwater.com •Muriel Lange Manager – Investor Relations Muriel.lange@amwater.com Tel: 856-566-4005 Fax: 856-782-2782 52 |

|