Institutional Investor Meetings July 2011 Exhibit 99.1 |

2 Certain statements in this presentation are forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are predictions based on our current expectations and assumptions regarding future events and may relate to, among other things, our future financial performance, including return on equity performance, our growth and portfolio optimization strategies, our projected capital expenditures and related funding requirements, our ability to repay debt, our ability to finance current operations and growth initiatives, the impact of legal proceedings and potential fines and penalties, business process and technology improvement initiatives, trends in our industry, regulatory or legal developments or rate adjustments. Actual results could differ materially because of factors decisions of governmental and regulatory bodies, including decisions to raise or lower rates; the timeliness of regulatory commissions’ actions concerning rates; changes in laws, governmental regulations and policies, including environmental, health and water quality and public utility regulations and policies; weather conditions, patterns or events, including drought or abnormally high rainfall; changes in customer demand for, and patterns of use of, water, such as may result from conservation efforts; significant changes to our business processes and corresponding technology; our ability to appropriately maintain current infrastructure; our ability to obtain permits and other approvals for projects; changes in our capital requirements; our ability to control operating expenses and to achieve efficiencies in our operations; our ability to obtain adequate and cost-effective supplies of chemicals, electricity, fuel, water and other raw materials that are needed for our operations; our ability to successfully acquire and integrate water and wastewater systems that are complementary to our operations and the growth of our business or dispose of assets or lines of business that are not complementary to our operations and the growth of our business; cost overruns relating to improvements or the expansion of our operations; changes in general economic, business and financial market conditions; access to sufficient capital on satisfactory terms; fluctuations in interest rates; restrictive covenants in or changes to the credit ratings on our current or future debt that could increase our financing costs or affect our ability to borrow, make payments on debt or pay dividends; fluctuations in the value of benefit plan assets and liabilities that could increase our cost and funding requirements; our ability to utilize our U.S. and state net operating loss carryforwards; migration of customers into or out of our service territories; difficulty in obtaining insurance at acceptable rates and on acceptable terms and conditions; the incurrence of impairment charges ability to retain and attract qualified employees; and civil disturbance, or terrorist threats or acts or public apprehension about future disturbances or terrorist threats or acts. Any forward-looking statements we make, speak only as of the date of this presentation. Except as required by law, we do not have any obligation, and we specifically disclaim any undertaking or intention, to publicly update or revise any forward- looking statements, whether as a result of new information, future events, changed circumstances or otherwise. Cautionary Statement Concerning Forward-Looking Statements July 2011 |

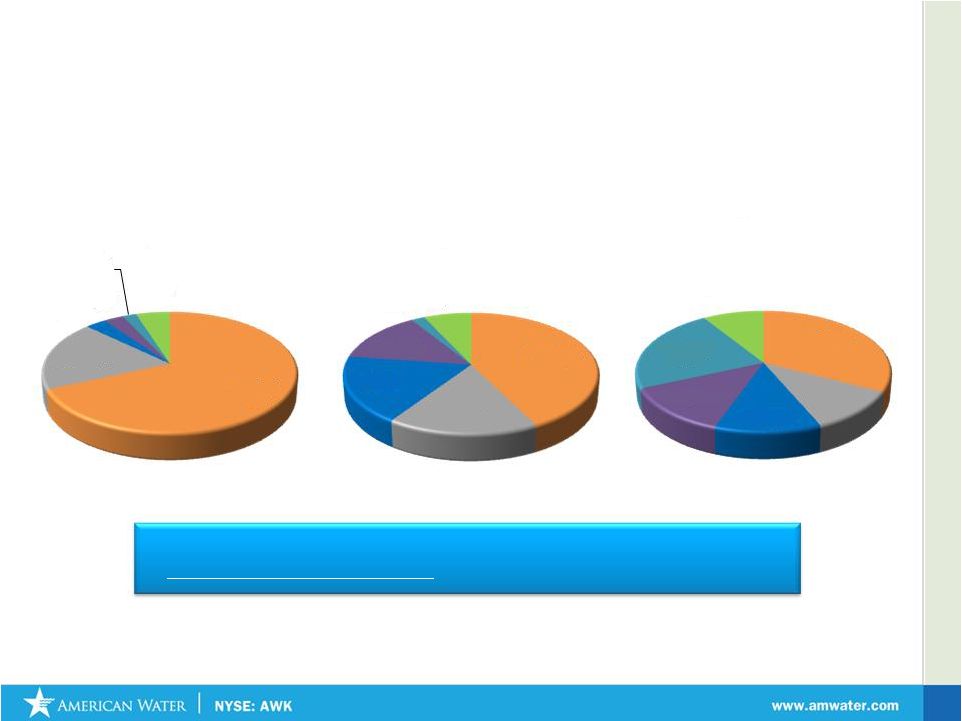

July 2011 American Water: The Premier Water Services Provider in North America Geographic Diversity (1) Business Diversity (1) Market Capitalization: $5.2 Billion Enterprise Value: $10.8 Billion Average Daily Volume Traded: 1.1 Million shares (1) Based on 2010 Revenues (2) Market data as of 6/29/11 (3) Market-Based includes Other 3 $601.2 $505.9 $232.0 $224.6 $181.7 $158.2 $123.4 NJ PA IL MO IN CA WVA Regulated, 89.4% Market Based , (3) 10.6% |

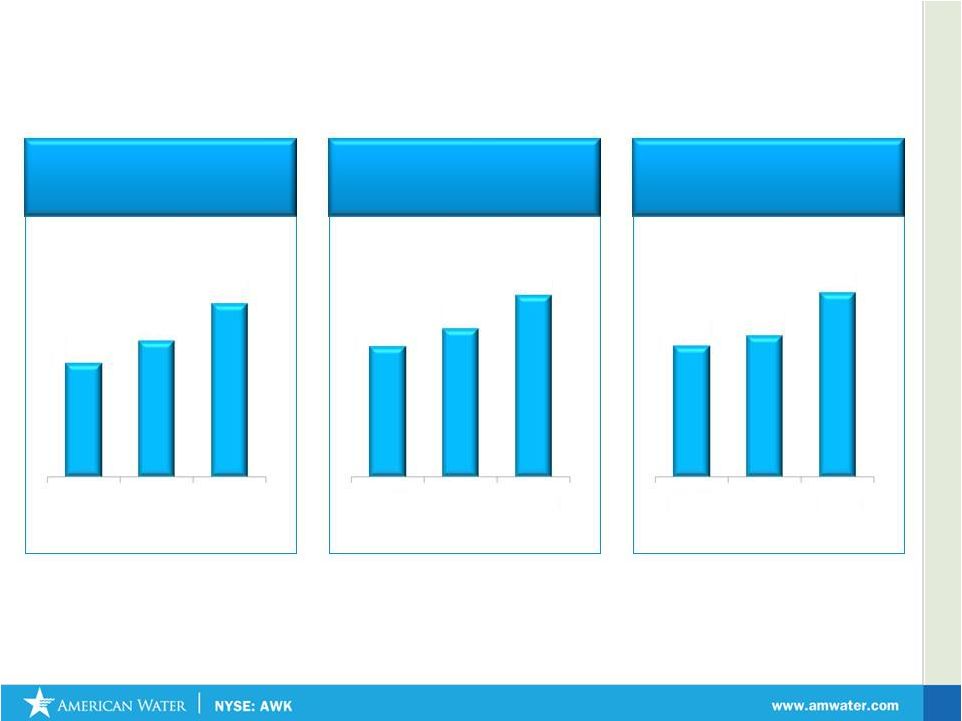

July 2011 4 American Water has achieved impressive Growth since its IPO * 2008 and 2009 exclude impairment charges. See slide 42 for reconciliation table Earnings Per Share* Cash Flow From Operations (millions) $268 $210 $176 2010 2009 2008 $1.10 $1.25 $1.53 $552 $596 $775 2008 2009 2009 2010 2010 2008 Net Income (millions) |

The US Water Industry |

July 2011 The U.S. Water Industry 6 Key Water Sector Themes Aging Infrastructure Fragmented Industry Increasing Environmental Requirements Capital Availability Technology |

7 Water Industry Has a Favorable Utility Profile Water Utility Characteristics Implications • Capital projects focused on maintaining public health & safety standards • Regulators supportive of prudent projects • Water bills low portion of household budget • Essential product – no substitutes • Demand is more price inelastic than electric or gas • Raw input costs (i.e. water and chemicals) less volatile than other utility commodity costs (i.e. coal and natural gas) • More stable rates for customers • Cost forecasting and regulatory lag is more manageable • M&A primarily small tuck-ins enabling targets to meet health & safety standards • Regulators generally support the strengthening of water systems via M&A • Water storage more feasible and cheaper than electricity or gas storage • Water utilities can be more cost efficient and responsive to demand fluctuations • Large water utilities diversified across multiple geographies • Mitigates impact of localized severe weather conditions / regulatory outcomes July 2011 |

July 2011 Aging US Infrastructure Investment Remains Critical *Source: U.S. Environmental Protection Agency’s 2007 Drinking Water Infrastructure Needs Survey and Assessment. In billions, adjusted to January 2007 dollars. Transmission & Distribution: $200.8 Treatment: $75.1 Storage: $36.9 Source: $19.8 Other: $2.3 Total: $334.8 Billion 8 **Source: 2002 U.S. Environmental Protection Agency Clean Water and Drinking Water Gap analysis US EPA Estimated 20 Year Total Needs of US Public Water Systems* American Society of Civil Engineers (ASCE) grades US infrastructure • 2009: $335 billion • 2005: $277 billion • 2002: $154 billion • 2009 Grade: D- • 2005 Grade: D- • 2001 Grade: D US EPA estimates upwards to $1 trillion needed for public water and wastewater systems** |

Without renewal or replacement of existing systems, pipe classified as poor, very poor or life elapsed will increase from 10% to 44% by 2020 Aging Pipe Infrastructure Network Propels Need for Capital Expenditures Percentage of Pipes by Classification Source: American Water Works Association, Dawn of the Replacement Era: Reinvesting in Drinking Water Infrastructure, May 2001 9 Excellent, 69% Good, 19% Fair, 3% Poor, 3% Very Poor, 2% Life Elapsed, 5% 1980 Excellent, 43% Good, 17% Fair, 18% Poor, 14% Very Poor, 2% Life Elapsed, 7% 2000 Excellent, 33% Good, 11% Fair, 12% Poor, 13% Very Poor, 23% Life Elapsed, 9% 2020 July 2011 |

10 Water and wastewater rates in U.S. vs. other countries (cents per gallon) (1) Source: 2008-2009 Bureau of Labor Statistics; Assumes four person household. (2) Canadian government data, using standard business conversions (3) Assumes purchasing parity pricing index Domestically: % of Annual Household Budget (1) Internationally: Cost comparison vs other countries (cents per gallon (2) ) July 2011 |

American Water |

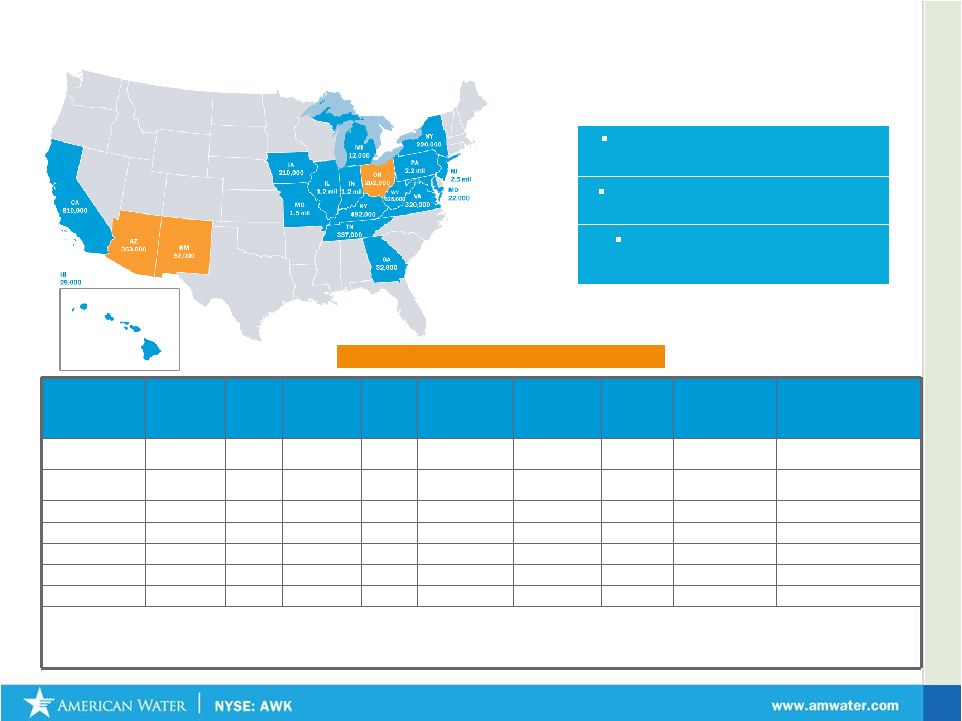

July 2011 Note: Numbers may not total due to rounding. 12 Top Seven States Customers Served (2010) % of Total 2010 Revenues ($ mm) % of Total Rate Base Approved per Last Rate Case Date of Last Rate Case DSIC Test Year (1) Tariff Structure (2) Pennsylvania 654,578 19.6% $505.9 20.9% $1,956,954,730 1/1/2011 Yes Historic Single New Jersey 645,939 19.4% $601.2 24.8% 1,771,009,863 1/1/2011 No Historic Single Missouri 452,102 13.6% $224.6 9.2% 791,837,186 7/1/2010 Yes Historic Multiple Illinois 308,399 9.2% $232.0 9.6% 607,356,502 4/23/2010 Yes Future Multiple Indiana 284,568 8.5% $181.7 7.5% 667,501,558 5/3/2010 Yes Historic Multiple California 173,075 5.2% $158.2 6.5% 337,529,472 7/1/2010 No Future Multiple West Virginia 172,340 5.2% $123.4 5.1% 427,325,204 4/18/2011 No Historic Single NOTES: (1) In most cases historic test year includes adjustments for known and measurable changes. (2) Single Tariff Structure represents a single rate structure within a state whereas a Multiple Tariff Structure includes many different tariffs by district or other subdivision within a state. American Water’s Regulated Presence Largely residential customer base promotes consistent operating results Geographic presence hedges both weather and regulatory risk Scale enables multiple growth opportunities across service areas States we are in process of exiting Regulated Operations |

July 2011 13 Prudent Investments in US Water Infrastructure drive Long Term Growth Net Utility Plant ($ mm) % Projected CAPEX by Purpose *Net utility plant as of 1Q 2011 of $10,555,698 excluding Discontinued Operations Quality of Service, 20% Other, 6% Asset Renewal, 44% Regulatory Compliance, 13% Capacity Expansion, 17% $10,496,524 $10,555,698 Q4 2010 Q1 2011 |

July 2011 American Water’s Portfolio Optimization Initiatives • Balanced Portfolio Analysis • Focus Achieving Authorized Rates of Return • Monetize Non-Producing Assets • Focused Capital Resources • Selective Acquisition Opportunities • Leverage Internal Growth 14 Continue to Lower Costs Focus on Value Drivers Redeploy Value Into Core Growth Markets Explore Opportunities for Long -Term Success Drive Profitability and Returns Optimizing Long-term Value Through Proactive Management |

July 2011 15 Our Market-Based Operations: A Portfolio of Water Resource Services For 2010, American Water reported $311.8 million of Market-Based Operations revenues Contract Operations Over 200 contracts** Serving 3.1m people Clarksville, IN Seattle, WA Warren Township, NJ 25 industrial contracts Design, Build and Operate 20 current projects* Lake Pleasant Plant, AZ Fillmore, CA Carnegie Abbey, RI Seattle, WA *Includes 16 AWM projects **Includes 137 AWM and 48 EMC projects Military Bases Privatization Fort Bragg, NC Fort Sill, OK Fort Rucker, AL Fort AP Hill, VA Scott AFB, IL Fort Polk, LA Fort Hood, TX Fort Belvoir, VA Fort Meade, MD Fort Leavenworth, KS Biosolids Management Canada Halton, ON Niagara, ON Hamilton, ON Emerging Water Technologies Desalination plant Tampa Bay Seawater, FL Water Reuse; 22 Projects; 7 States Gillette Stadium, MA Battery Park, NY Butterball Turkey, NC Homeowner Services Over 870,000 contracts 17 States |

July 2011 16 Strategy Specifics: Homeowner Services Growth Large Untapped Market Strong Growth Potential • 75 Million Single family homes in US • 3% Purchase water/sewer service contracts • American Water has 34% market share • 61% of HOS customers buy more than 1 product • EXTRAORDINARY customer satisfaction • STRONG contractor network • EFFICIENT AND CONTROLLED claims processes • 12% DEMONSTRATED GROWTH over last 3 years |

July 2011 17 Strategy Specifics: Market Size of Military Utility Privatizations 2011-13 2014-16 Major Water/Wastewater Contracts to be Awarded Contracts Awarded to American Water Contracts Awarded to Competitors Contracts Programmed by Dept. of Defense for Award 2002 2005-07 2008-10 Major Water/Wastewater Awards to Date 7 12 4 Market Opportunity represents approximately $11Bn in Total Revenues Over $2 Billion in Revenues Backlog 3 3 4 |

Financial Update |

July 2011 19 Total Shareholder Return : American Water vs. Indices (July 12, 2010 – July 12, 2011) Shareholder Return YTD American Water S&P 500 Dow Jones Utilities +45.8% +24.8% +18.6% |

American Water: A Solid First Quarter 20 Adjusted Net Income Adjustment for cessation of depreciation Adjusted Net Income Adjustment for cessation of depreciation July 2011 * Adjusted Net Income reflects the effect of the cessation of depreciation on assets subject to an agreement of sale – a Non-GAAP measure. Such depreciation would have been $4.7 million, after tax, or $0.3 per share. See reconciliation table on Slide 41 |

21 Regulated O&M Efficiency Ratio Continues to Improve * O&M Efficiency Ratio (A Non-GAAP, unaudited measure) = operating and maintenance expenses / revenues, adjusted to eliminate revenues and expenses related to purchased water. * Quarterly data reflects the effect of discontinued operations. (See table in Appendix). 55% 50% 45% 40% 35% 30% 49.4% 48.2% 3/31/2010 3/31/2011 July 2011 Adjusted O & M Efficiency Ratio |

22 Rate Cases Awarded That Will Have an Impact on 2011 Results (As of July 13, 2011) July 2011 ($ in millions) Effective Date for new rates ROE Granted Annualized Increase to Revenue General Rate Cases: Illinois 4/23/2010 10.38% 41.4 $ New Mexico (Edgewood) 5/10/2010 10.00% 0.5 Indiana 5/3/2010 10.00% 31.5 Virginia (Eastern) 5/8/2010 10.50% 0.6 Ohio 5/19/2010 9.34% 2.6 Missouri 7/1/2010 10.00% 28.0 California (Sac, LA, Lark) 7/1/2010 10.20% 14.6 Michigan 7/1/2010 10.50% 0.2 Kentucky 10/1/2010 9.70% 18.8 New Jersey 1/1/2011 10.30% 39.9 Pennsylvania Wastewater 1/1/2011 10.60% 8.4 Arizona (Anthem, etc.) 1/1/2011 9.50% 14.7 Tennessee 4/5/2011 10.00% 5.6 West Virginia 4/19/2011 9.75% 5.1 Subtotal - General Rate Cases 211.9 $ Infrastructure Charges: Pennsylvania 19.3 Indiana 5.4 Missouri 6.3 Illinois 1.7 Other 1.4 Subtotal - Infrastructure Charges 34.1 $ Total 246.0 $ |

Rate Cases Awaiting Final Order 23 Docket / Revenue Increase ROE Rate Base Filing Case Number Date Filed Filed Requested (Filed) Status Virginia* PUE 2010-00001 03/08/10 6.9 $ 11.50% 99.1 $ 5 California A 10-07-007 07/01/10 37.3 10.20% 409.6 3 Arizona W-01303A-10-0448 11/03/10 20.8 11.50% 148.9 2 Hawaii 2010-0313 02/22/11 1.8 11.85% 25.2 3 Pennsylvania R-2011-2232243 04/29/11 70.7 11.50% 2,096.2 2 New York 11-W-0200 04/29/11 9.6 11.50% 126.9 2 Iowa RPU-2011-0001 04/29/11 5.1 11.35% 88.9 2 Indiana 44022 05/02/11 20.4 11.50% 733.4 2 New Mexico 11-00196-UT 05/18/11 2.6 11.75% 33.6 2 Missouri WR-2011-0037 06/30/10 42.9 11.50% 845.6 2 Ohio 11-4161-WS-AIR 07/01/11 8.3 11.50% 92.3 1 Total 226.4 $ 4,699.7 $ * Final Order not yet issued. Interim rates are in effect Note: Above excludes rate case file in 2007 for Hawaii for which interim rates have been in effect since October 2008 Index of Rate Case Status 1 - Case Filed 2 - Discovery (Data Requests, Investigation) 3 - Negotiations / Evidentiary Hearings / Briefings 4 - Recommended order issued / settlement reached, without interim rates 5 - Interim rates in effect, awaiting final order July 2011 |

125 years Investing in Water Infrastructure and paying Dividends to Shareholders 24 July 2011 1886 1947 2003 2008 Dividend paid to private holders American Water Listed on NYSE – Dividend paid to common shareholders RWE takes AWK private. Dividend paid to shareholder AWK IPO Lists on NYSE. Pays dividends to common shareholders Watermain work in Pennsylvania. in the early 1900’s Infrastructure improvement in New Jersey in 2009 |

Quarterly Dividend Rate Increases Recent Dividend History • Key component of American Water’s total shareholder return proposition • Dividend Growth – Board of Directors increased dividend 5% to $0.23 or $0.92 annualized • Dividend Yield – 3.1% at 7/13/11 • Growth in Dividend reflects growth in Net Income 25 July 2011 |

July 2011 26 American Water’s past performance and future growth expectations compare very favorably vs Water, Electric and Gas Peers 2008 – 2010 EPS CAGR + Average Dividend Yield (4) Total Shareholder Return (Long Term Expected EPS Growth* and Dividend Yield**) 1) Water Companies Include: AWR, CTWS, CWT, MSEX, SJW, WTR, YORW. 2) Gas Companies include ATO, LG, GAS, NWN, PNY, SJI, SWX, WGL. 3) Regulated Electric Companies include HE, NU, TE, LNT, XEL, SO, CNP, PCG, SCG, POR, DUK, UIL, PGN, AEP. 4) Average monthly dividend yield for 2008 – 2010 period. 5) Non GAAP: American Water EPS adjusted to exclude impairment charges. Source: Thomson Reuters * For AWK represents 7-10% Long Term EPS CAGR market guidance . All other data from First Call Consensus Estimates ** as of 7/11/11 Note: Consensus Estimates are calculated by First Call based on the earnings projections made by the analysts who cover companies noted (other than AWK). Please note that any opinions, estimates or forecasts regarding performance made by these analysts (and therefore the Consensus estimate numbers) are theirs alone and do not represent opinions, forecasts or predictions of American Water or its management. |

July 2011 Source: Thomson Reuters * PE data as of July 2011 27 American Water’s higher growth expectations are not fully reflected in its PE multiple P/E Compared with Total Return CTWS LG MSEX SWX NWN ATO YORW WGL AWR PCG AEP WTR PNY DUK UIL XEL SJI SO CNP NU TE AWK CWT HE 11.0x 16.0x 21.0x 6% 7% 8% 9% 10% 11% 12% 13% 14% Forward P/E Expected Total Return SCG POR LNT PGN |

What to Expect from American Water - 2011 Accomplishments Start execution of Portfolio Optimization Initiative Missouri acquisition closed May, Texas sale closed June Filed for regulatory approvals for transactions in NM and AZ Agreement to purchase Aqua’s NY subsidiary and sell to Aqua our Ohio subsidiary Resolve Rate Cases worth $93 MM of filed Annualized Revenues by December 31, 2011 Finalized Tennessee and West Virginia Rate Cases Initiate state specific efforts to address declining usage Addressed in rate cases filed in Iowa, Long Island, Pennsylvania, and Indiana Continue reduction in Operating Efficiency Ratio Operating Efficiency Ratio improved 120 bps in the first quarter 2011 vs. first quarter 2010, an improvement of 2.5% Increase Earned return on equity ROE increased 39 bps or 6% over comparable last twelve months ending March 31, 2011 Expand Market Based businesses with focus on Homeowner Services & Military Contract Operations Homeowner Services entered into the Commercial Market Optimize Municipal Contract Operations Business Model July 2011 28 |

July 2011 American Water – A Compelling Value Value Proposition Market Leader Strong Visible Growth Proven Management Trades at Discount to Peers Sound Regulatory Framework 29 |

July 2011 Ed Vallejo Vice President – Investor Relations Muriel Lange Manager – Investor Relations Tel: 856-566-4005 Fax: 856-782-2782 30 Edward.vallejo@amwater.com Muriel.lange@amwater.com Investor Relations Contacts: |

Appendix |

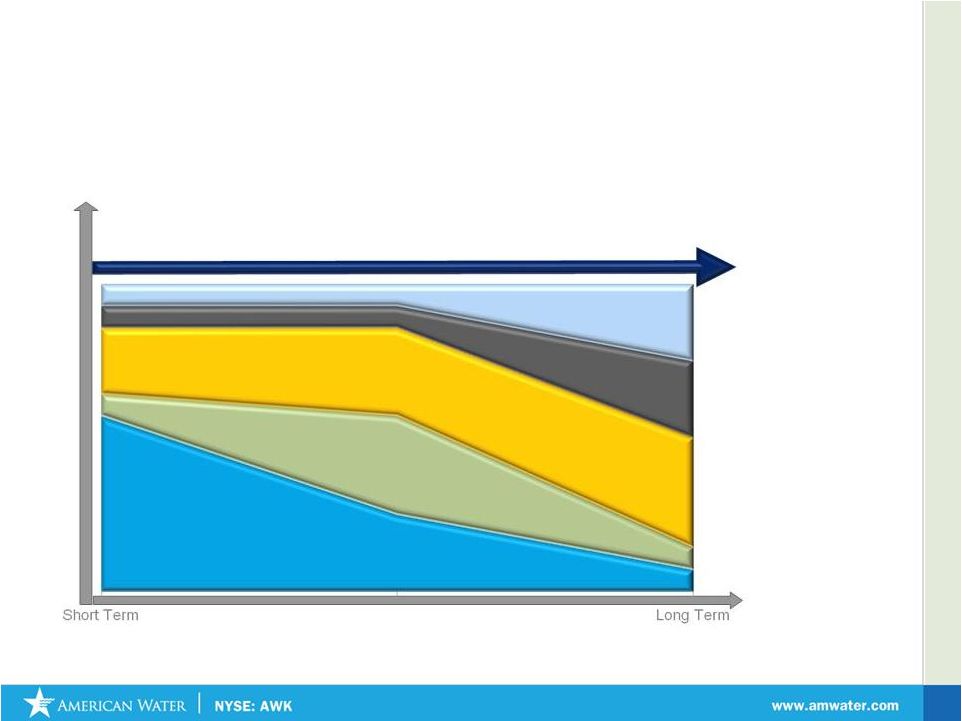

July 2011 32 Investment Thesis: Sustained 7-10% EPS Growth Future Growth New Services Regulated Investments Acquisitions Operational Excellence/ Efficiencies ROE improvement Long Term Growth Conceptual Representation |

Rate of Return Regulation in the United States Prudent Investment Drives Need for Rate Cases American Water has experience in securing appropriate rates of return and promoting constructive regulatory frameworks Operating Expenses Taxes, Depr & Amortization WACC Allowed Return Allowed Return Revenue Requirement Step 2 Step 1 + + x = = 33 Establish Rate Base July 2011 |

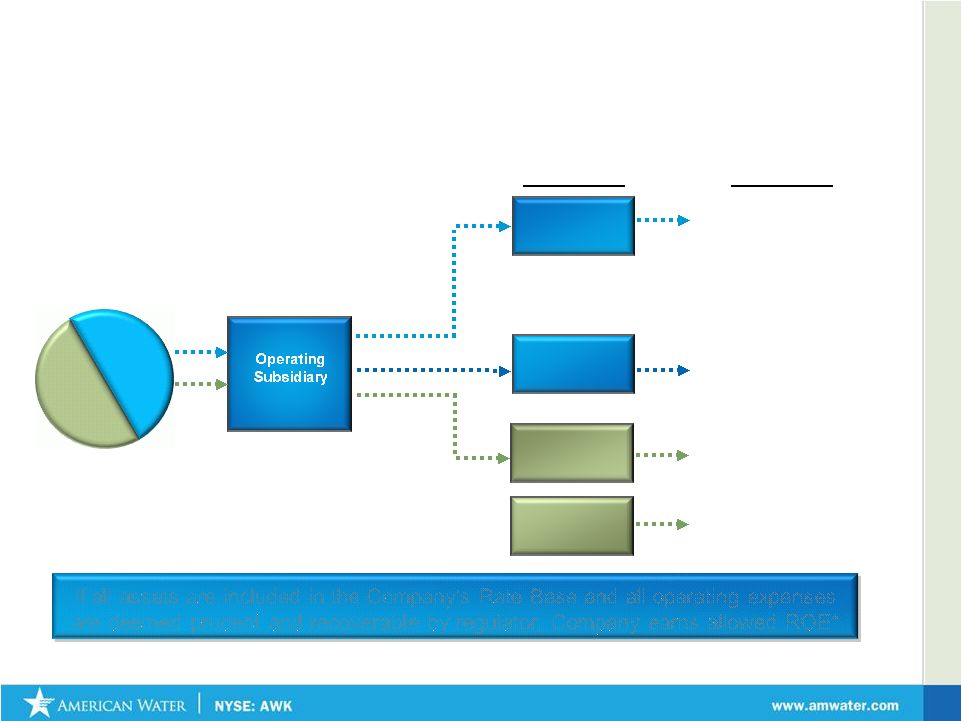

July 2011 34 AW Parent Company Debt Equity (Capex) Operating Expenses Debt Regulatory Treatment Net Income Impact • Neutral, if interest costs are deemed prudent and fair to the consumer by regulator How is Net Income generated in Rate of Return Regulation? Pass Through 1:1 Pass Through 1:1 Return of (Depreciation) Return on Equity (ROE) • Neutral, if all operating expenses are deemed prudent and fair to the consumer by regulator • Depreciation is neutral if all depreciable assets are in rate base • Rate Base x Earned ROE + Gross Up for Taxes is Added Revenue * Assuming no regulatory lag between rate cases Debt Equity Equity If all assets are included in the Company’s Rate Base and all operating expenses are deemed prudent and recoverable by regulator, Company earns allowed ROE* |

Water Utility Expenditures Water vs Other Utility Expenditures Water Use in the Home 35 July 2011 |

July 2011 Infrastructure Surcharges: A viable mechanism to address Regulatory Lag Infrastructure Surcharges allows companies to recover infrastructure replacement costs without necessity of filing full rate proceeding States that currently allow use of infrastructure surcharges Pennsylvania Indiana Illinois Ohio Surcharges are typically reset to zero when new base rates become effective and incorporate the costs of the previous surcharge investments Delaware New York Missouri (St Louis County) California - Trial basis 36 |

Case in point: Increased investment in Pennsylvania’s Infrastructure 37 July 2011 |

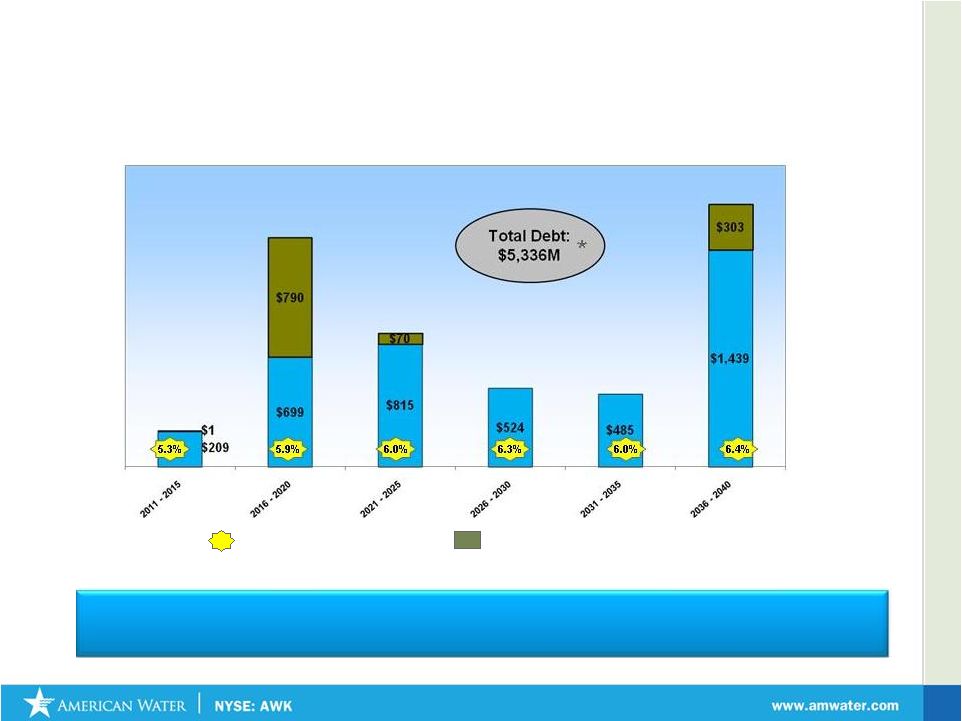

July 2011 Weighted Average Interest Rates Debt Maturities at March 31, 2011 (in millions) Parent Company Debt * Amount excludes Preferred Stock with Mandatory Redemptions 38 $100 million of Parent Company debt swapped from 6.085% to 6 month LIBOR + 3.422%, to mature with fixed-rate debt in 2017 |

July 2011 Income Statement 39 ($ in Thousands, except per share data) Three Months Ended March 31, 2011 2010 Operating revenues $ 610,936 $ 566,762 Operating expenses Operation and maintenance 320,571 305,642 Depreciation and amortization 88,019 82,056 General taxes 57,205 54,486 Loss (gain) on sale of assets 268 (71) Total operating expenses, net 466,063 442,113 Operating income 144,873 124,649 Other income (expenses) Interest, net (76,482) (78,696) Allowance for other funds used during construction 2,916 2,146 Allowance for borrowed funds used during construction 1,242 1,382 Amortization of debt expense (1,295) (1,201) Other, net (1,141) 69 Total other income (expenses) (74,760) (76,300) Income from continuing operations before income taxes 70,113 48,349 Provision for income taxes 28,649 18,669 Income from continuing operations 41,464 29,680 Income from discontinued operations, net of tax 5,868 1,128 Net income $ 47,332 $ 30,808 Basic and diluted earnings per common share: Income from continuing operations $ 0.24 $ 0.17 Income from discontinued operations, net of tax $ 0.03 $ 0.01 Net income $ 0.27 $ 0.18 Average common shares outstanding during the period: Basic 175,259 174,720 Diluted 176,048 174,796 Dividends per common share $ 0.22 $ 0.21 |

July 2011 First Quarter 2011 Reconciliation Tables In thousands 2011 2010 Total Regulated Operation and Maintenance Expenses 270,157 $ 256,312 $ Less: Regulated Purchased Water Expenses 21,100 20,633 Adjusted Regulated Operation and Maintenance Expenses (a) 249,057 $ 235,679 $ Total Regulated Operating Revenues 537,395 $ 498,197 $ Less: Regulated Purchased Water Revenues 21,100 20,633 Adjusted Regulated Operating Revenues (b) 516,295 $ 477,564 $ Regulated Operations and Maintenance Efficiency Ratio (a)/(b) 48.2% 49.4% In thousands except per share data Three Months Ended March 31, 2011 Net income 47,332 $ Less: Cessation of depreciation, net of tax 4,729 Adjusted net income, exclusive of the cessation of depreciation associated with assets of discontinued operations 42,603 $ Basic earnings per common share: Adjusted net income 0.24 $ Diluted earnings per common share: Adjusted net income 0.24 $ with assets of discontinued operations (a Non-GAAP, unaudited number) Three Months Ended March 31, Regulated Operations and Maintenance Efficiency Ratio (A Non-GAAP, unaudited measure) Adjusted net income and earnings per share, exclusive of the cessation of depreciation associated 40 |

July 2011 Financial Tables GAAP and Non-GAAP Measures Net Income (Loss) – Earnings per Share Excluding Impairment Charge (A Non-GAAP Unaudited Number) Historical ($ in thousands, except per share data) 2008 2009 2010 LTM 3/31/11 Net income (Loss) ($562,421) ($233,083) $267,827 $284,351 Add: Impairment 750,000 450,000 0 0 Net income excluding impairment charge before associated tax benefit 187,579 216,917 267,827 284,351 Less: Income tax benefit relating to impairment charge 11,525 6,976 0 0 Net income excluding impairment charge $176,054 $209,941 $267,827 $284,351 Income (loss) per common share: Basic ($3.52) ($1.39) $1.53 Diluted ($3.52) ($1.39) $1.53 Net income per common share excluding impairment charge: Basic $1.10 $1.25 $1.53 Diluted $1.10 $1.25 $1.53 41 Rate Base as of March 31, 2011 (1) ($ in Thousands) Net Utility Plant $10,421,125 Less Advances for Construction 408,701 CIAC – Contributions in Aid of Construction 932,355 Deferred income taxes 1,136,432 Deferred investment tax credits 30,588 Sub Total $2,508,076 Rate Base TOTAL $7,913,049 (1) An approximation of rate base, which includes Net Utility Plant not yet included in rate base pending rate case filings/outcomes |

|