Exhibit 99.2 2024 Third Quarter Earnings & 2025 Outlook Conference Call October 31, 2024

Aaron Musgrave Vice President, Investor Relations 2

FORWARD-LOOKING STATEMENTS Safe Harbor This presentation includes forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and the Federal securities laws. They are not guarantees or assurances of any outcomes, financial results, levels of activity, performance or achievements, and readers are cautioned not to place undue reliance upon them. The forward-looking statements are subject to a number of estimates and assumptions, and known and unknown risks, uncertainties and other factors. Actual results may differ materially from those discussed in the forward-looking statements included in this presentation. The factors that could cause actual results to differ are discussed in the Appendix to this presentation, and in our Quarterly Report on Form 10-Q for the quarter ended September 30, 2024, as filed with the SEC on October 30, 2024. Non-GAAP Financial Information This presentation includes non-GAAP financial measures. Further information regarding these non-GAAP financial measures, including a reconciliation of each of these measures to the most directly comparable GAAP measure, is included in the Appendix to this presentation. 3

John Griffith President 4

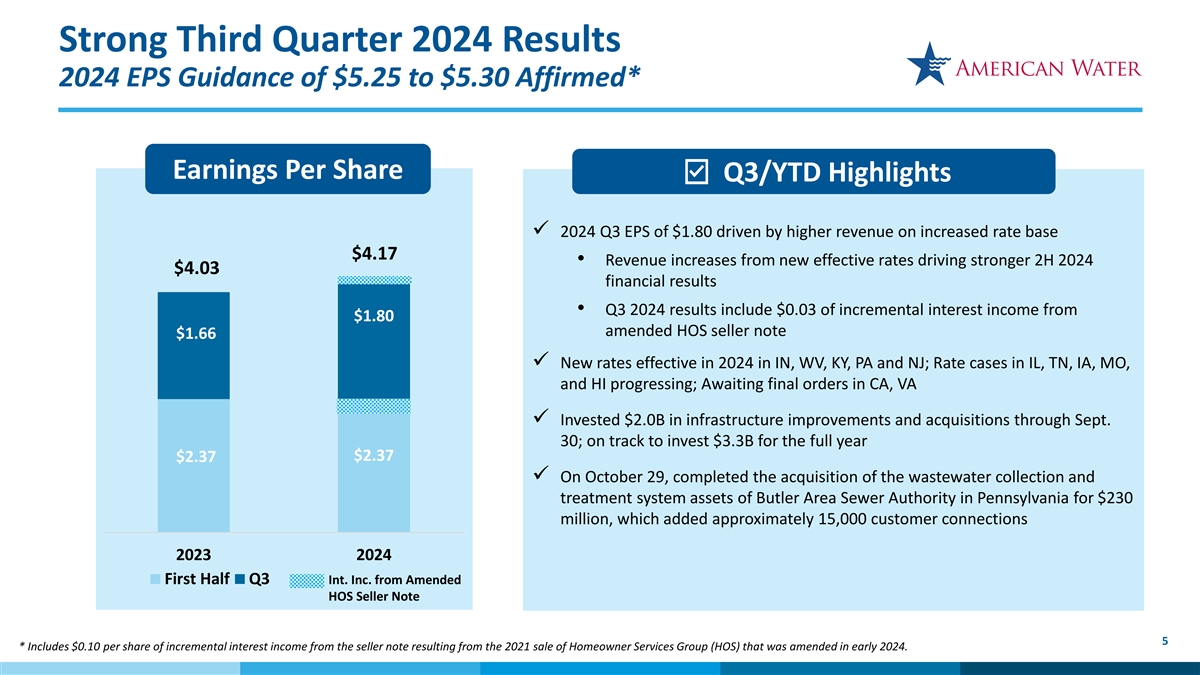

Strong Third Quarter 2024 Results 2024 EPS Guidance of $5.25 to $5.30 Affirmed* Earnings Per Share Q3/YTD Highlights ü 2024 Q3 EPS of $1.80 driven by higher revenue on increased rate base $4.17 • Revenue increases from new effective rates driving stronger 2H 2024 $4.03 financial results • Q3 2024 results include $0.03 of incremental interest income from $1.80 amended HOS seller note $1.66 ü New rates effective in 2024 in IN, WV, KY, PA and NJ; Rate cases in IL, TN, IA, MO, and HI progressing; Awaiting final orders in CA, VA ü Invested $2.0B in infrastructure improvements and acquisitions through Sept. 30; on track to invest $3.3B for the full year $2.37 $2.37 ü On October 29, completed the acquisition of the wastewater collection and treatment system assets of Butler Area Sewer Authority in Pennsylvania for $230 million, which added approximately 15,000 customer connections 2023 2024 Int. Inc. from Amended First Half Q3 HOS Seller Note 5 * Includes $0.10 per share of incremental interest income from the seller note resulting from the 2021 sale of Homeowner Services Group (HOS) that was amended in early 2024.

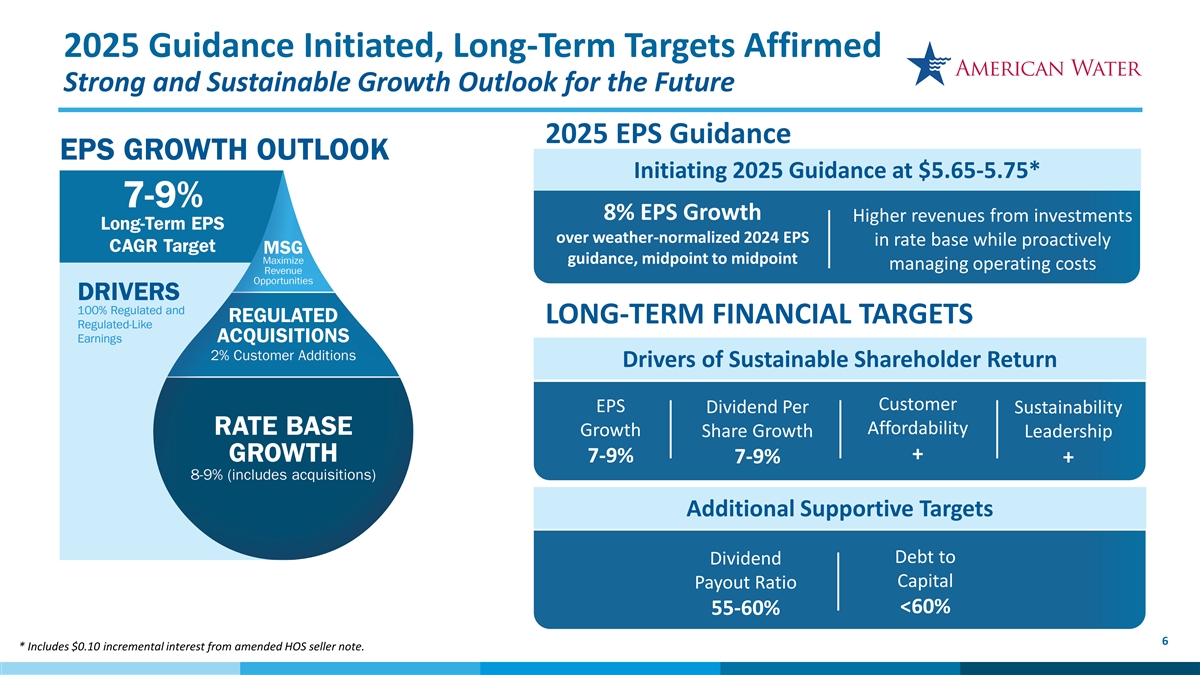

2025 Guidance Initiated, Long-Term Targets Affirmed Strong and Sustainable Growth Outlook for the Future 2025 EPS Guidance Initiating 2025 Guidance at $5.65-5.75* 8% EPS Growth Higher revenues from investments over weather-normalized 2024 EPS in rate base while proactively guidance, midpoint to midpoint managing operating costs LONG-TERM FINANCIAL TARGETS Drivers of Sustainable Shareholder Return Customer EPS Dividend Per Sustainability Affordability Growth Share Growth Leadership + 7-9% 7-9% + Additional Supportive Targets Debt to Dividend Capital Payout Ratio <60% 55-60% 6 * Includes $0.10 incremental interest from amended HOS seller note.

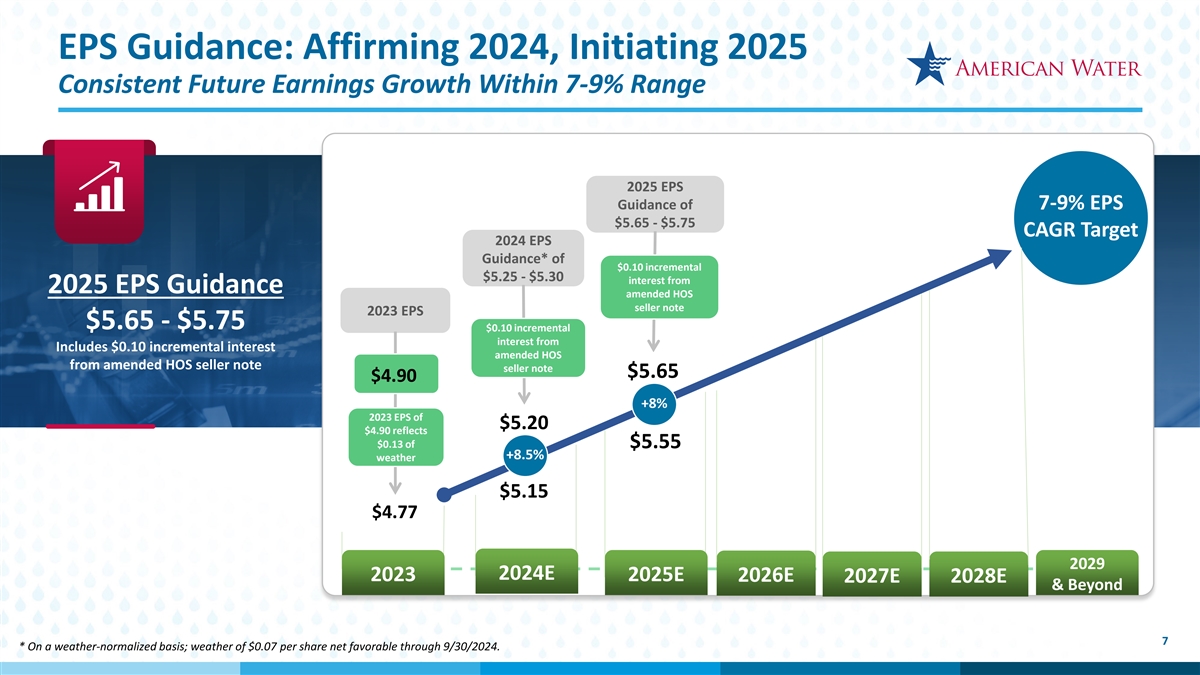

EPS Guidance: Affirming 2024, Initiating 2025 Consistent Future Earnings Growth Within 7-9% Range 2025 EPS Guidance of 7-9% EPS $5.65 - $5.75 CAGR Target 2024 EPS Guidance* of $0.10 incremental $5.25 - $5.30 interest from 2025 EPS Guidance amended HOS seller note 2023 EPS $5.65 - $5.75 $0.10 incremental interest from Includes $0.10 incremental interest amended HOS from amended HOS seller note seller note $5.65 $4.90 +8% 2023 EPS of $5.20 $4.90 reflects $0.13 of $5.55 +8.5% weather $5.15 $4.77 2029 2024E 2023 2025E 2026E 2027E 2028E & Beyond 7 * On a weather-normalized basis; weather of $0.07 per share net favorable through 9/30/2024.

David Bowler Executive Vice President & Chief Financial Officer 8

Details of Year-To-Date 2024 EPS 0.84 (0.19) (0.06) (0.21) 0.07 $4.17 0.01 $4.10 $4.03 (0.28) (0.04) Sept. YTD 2023 Weather* Revenue O&M General Tax - D eprec iati on Long-Term Other, net Sept. YTD 2024 Interest from Sept. YTD 2024 Property and Financing Subtotal Amended HOS Reported Gross Receipts Note * Includes weather of $0.07 per share net favorable in 2024 ($0.03 in Q2, $0.04 in Q3) and 0.11 per share net favorable in 2023 ($0.07 in Q2, $0.04 in Q3). 9

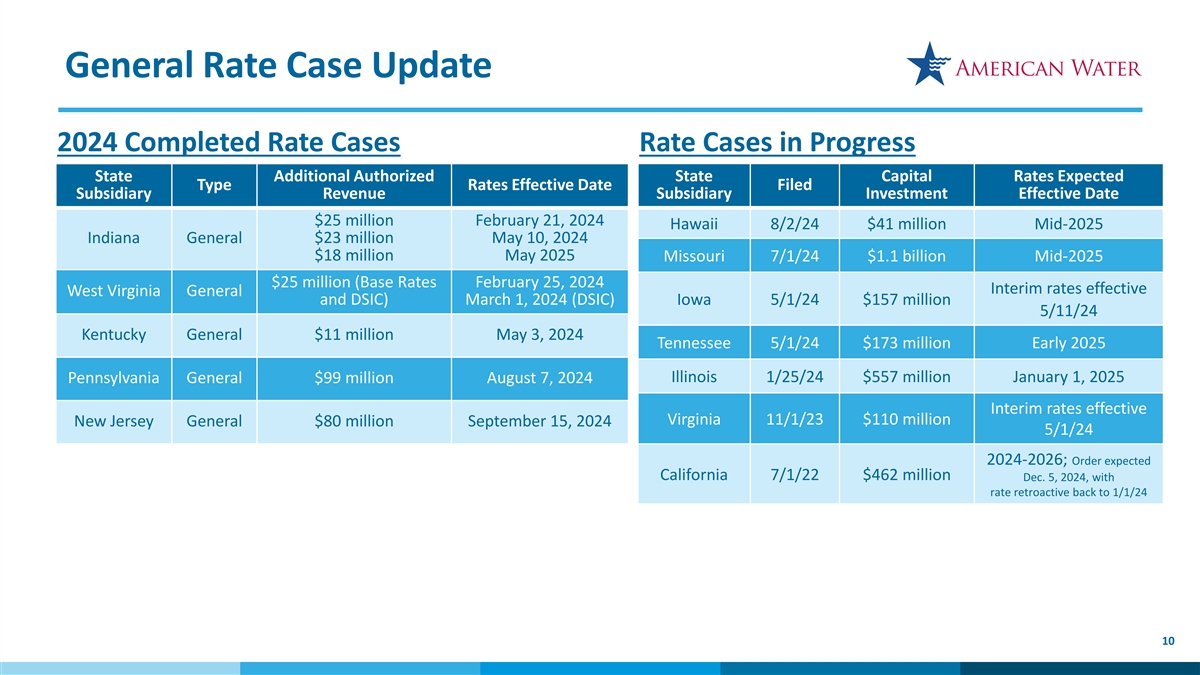

General Rate Case Update 2024 Completed Rate Cases Rate Cases in Progress State Additional Authorized State Capital Rates Expected Type Rates Effective Date Filed Subsidiary Revenue Subsidiary Investment Effective Date $25 million February 21, 2024 Hawaii 8/2/24 $41 million Mid-2025 Indiana General $23 million May 10, 2024 $18 million May 2025 Missouri 7/1/24 $1.1 billion Mid-2025 $25 million (Base Rates February 25, 2024 Interim rates effective West Virginia General and DSIC) March 1, 2024 (DSIC) Iowa 5/1/24 $157 million 5/11/24 Kentucky General $11 million May 3, 2024 Tennessee 5/1/24 $173 million Early 2025 Illinois 1/25/24 $557 million January 1, 2025 Pennsylvania General $99 million August 7, 2024 Interim rates effective Virginia 11/1/23 $110 million New Jersey General $80 million September 15, 2024 5/1/24 2024-2026; Order expected California 7/1/22 $462 million Dec. 5, 2024, with rate retroactive back to 1/1/24 10

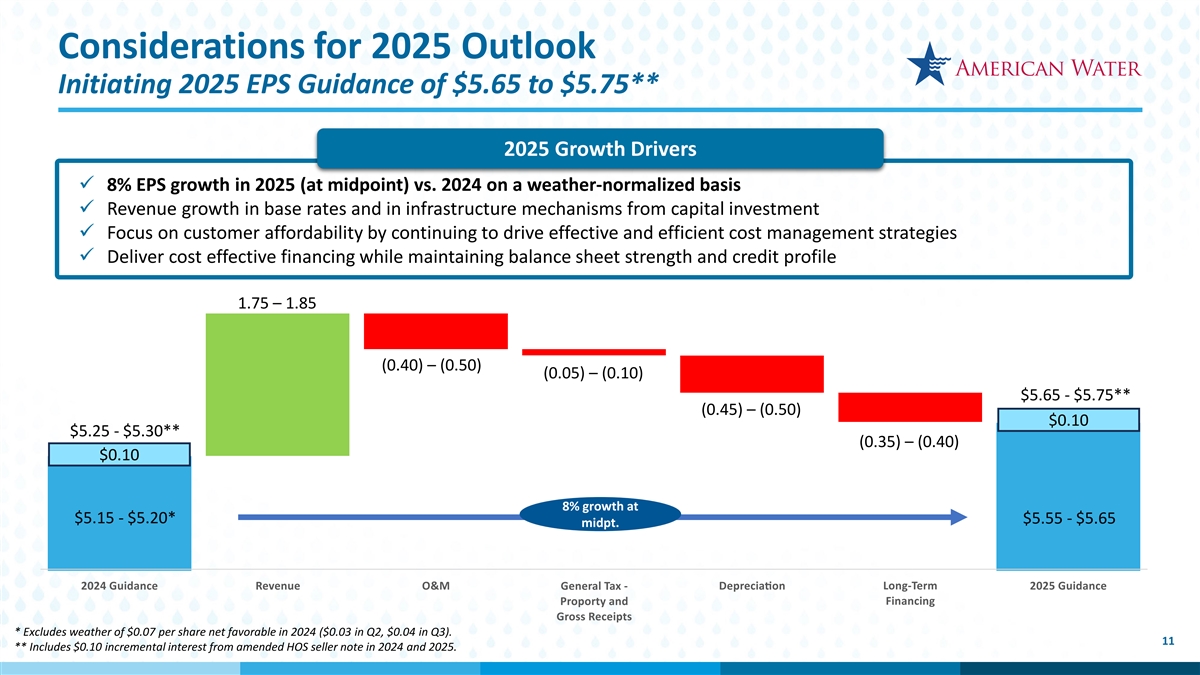

Considerations for 2025 Outlook Initiating 2025 EPS Guidance of $5.65 to $5.75** 2025 Growth Drivers ü 8% EPS growth in 2025 (at midpoint) vs. 2024 on a weather-normalized basis ü Revenue growth in base rates and in infrastructure mechanisms from capital investment ü Focus on customer affordability by continuing to drive effective and efficient cost management strategies ü Deliver cost effective financing while maintaining balance sheet strength and credit profile 1.75 – 1.85 (0.40) – (0.50) (0.05) – (0.10) $5.65 - $5.75** (0.45) – (0.50) $0.10 $5.25 - $5.30** (0.35) – (0.40) $0.10 8% growth at $5.15 - $5.20* $5.55 - $5.65 midpt. 2024 Guidance Revenue O&M General Tax - D eprec iati on Long-Term 2025 Guidance Proporty and Financing Gross Receipts * Excludes weather of $0.07 per share net favorable in 2024 ($0.03 in Q2, $0.04 in Q3). 11 ** Includes $0.10 incremental interest from amended HOS seller note in 2024 and 2025.

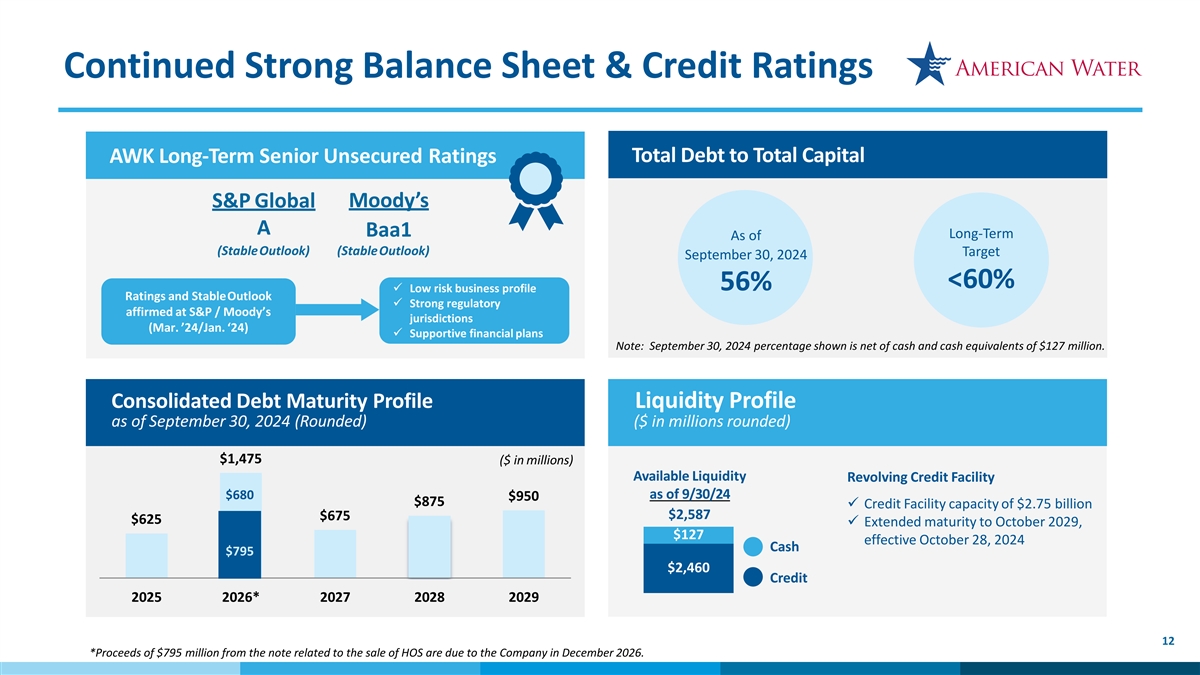

Continued Strong Balance Sheet & Credit Ratings AWK Long-Term Senior Unsecured Ratings Total Debt to Total Capital S&P Global Moody’s A Baa1 Long-Term As of (StableOutlook) (StableOutlook) Target September 30, 2024 <60% 56% ü Low risk business profile Ratings and Stable Outlook ü Strong regulatory affirmed at S&P / Moody’s jurisdictions (Mar. ’24/Jan. ‘24) ü Supportive financial plans Note: September 30, 2024 percentage shown is net of cash and cash equivalents of $127 million. Consolidated Debt Maturity Profile Liquidity Profile as of September 30, 2024 (Rounded) ($ in millions rounded) $1,475 ($ in millions) Available Liquidity Revolving Credit Facility as of 9/30/24 $680 $950 $875 ü Credit Facility capacity of $2.75 billion $2,587 $675 $625 ü Extended maturity to October 2029, $127 effective October 28, 2024 Cash $795 $2,460 Credit 2025 2026* 2027 2028 2029 12 *Proceeds of $795 million from the note related to the sale of HOS are due to the Company in December 2026.

Funding the 2025-2029 Capital Investment Plan ($ in millions) Financing Plan: 2025-2029 Operating Cash Flows $13,000 Debt Financing $10,500 Equity Issuances $2,500 Sale Proceeds (HOS) $795 Total Sources: ~$27 Billion Ø $2.5B equity issuance in 2025-2029 plan, driven by capital investment needs and consistently achieving <60% debt to cap target • Includes $1.0 billion equity financing from prior plan, plus an additional $1.5 billion near end of plan, to support growth in the business; issuances are subject to market conditions • Uses of funds: primarily ~$17-18 billion of capital investments, ~$4.5 billion of LTD maturities, and dividends • Current 2025 financing plan includes $1.5-2.0B of long-term debt financing; does not include any equity financing Ø Investors should expect equity financing to occur consistent with a traditional regulated utility financing strategy and to maintain our strong balance sheet and credit metrics, with timing and sizing in alignment with our investment program and rate case cycle 13

Cheryl Norton Executive Vice President & Chief Operating Officer 14

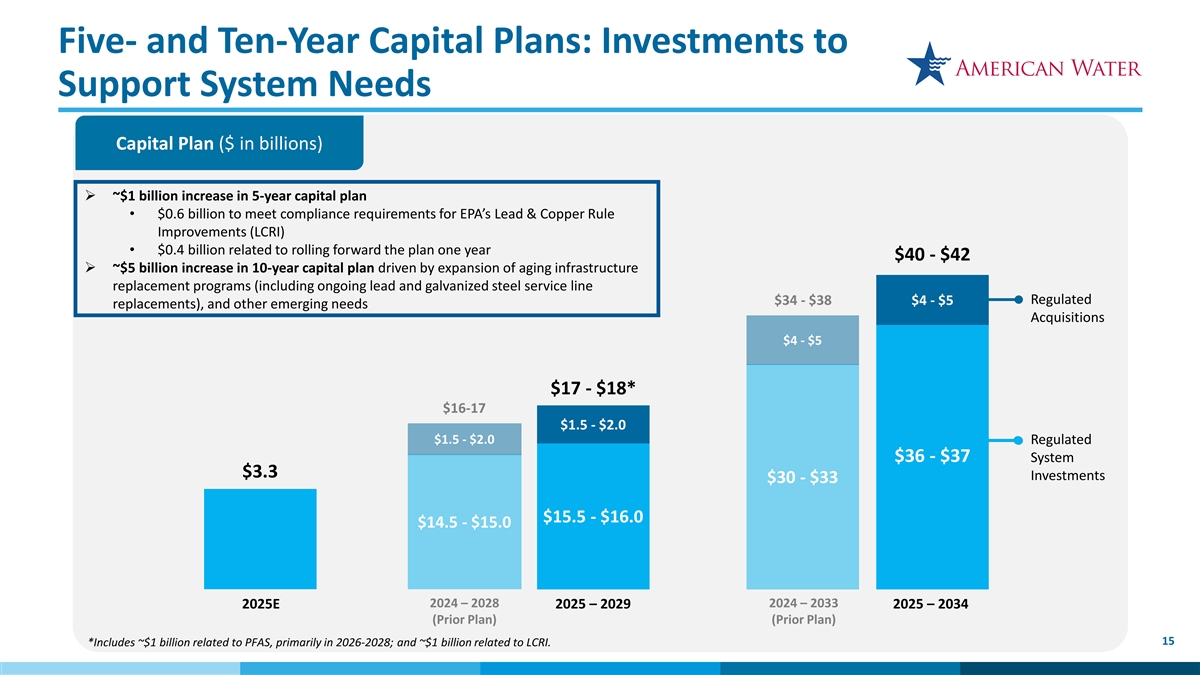

Five- and Ten-Year Capital Plans: Investments to Support System Needs Capital Plan ($ in billions) Ø ~$1 billion increase in 5-year capital plan • $0.6 billion to meet compliance requirements for EPA’s Lead & Copper Rule Improvements (LCRI) • $0.4 billion related to rolling forward the plan one year $40 - $42 Ø ~$5 billion increase in 10-year capital plan driven by expansion of aging infrastructure replacement programs (including ongoing lead and galvanized steel service line Regulated $34 - $38 $4 - $5 replacements), and other emerging needs Acquisitions $4 - $5 $17 - $18* $16-17 $1.5 - $2.0 $1.5 - $2.0 Regulated $36 - $37 System $3.3 Investments $30 - $33 $15.5 - $16.0 $14.5 - $15.0 2024 – 2028 2024 – 2033 2025E 2025 – 2029 2025 – 2034 (Prior Plan) (Prior Plan) 15 *Includes ~$1 billion related to PFAS, primarily in 2026-2028; and ~$1 billion related to LCRI.

Timely Recovery of Capital Investments Cap Ex Driven by Infrastructure Renewal, Resiliency, and Water Quality Capital Recovery Capital by Purpose Outlook (2025-2034) ~3% ~5% Infrastructure Infrastructure ~70% ~6% Surcharge Renewal Mechanisms Resiliency ~8% ~45% Water Quality, Including PFAS ~10% Operational Efficiency, Future Test Technology & Innovation ~30% Traditional ~68% Years Recovery System Expansion ~25% ~30% ~25% Other 16

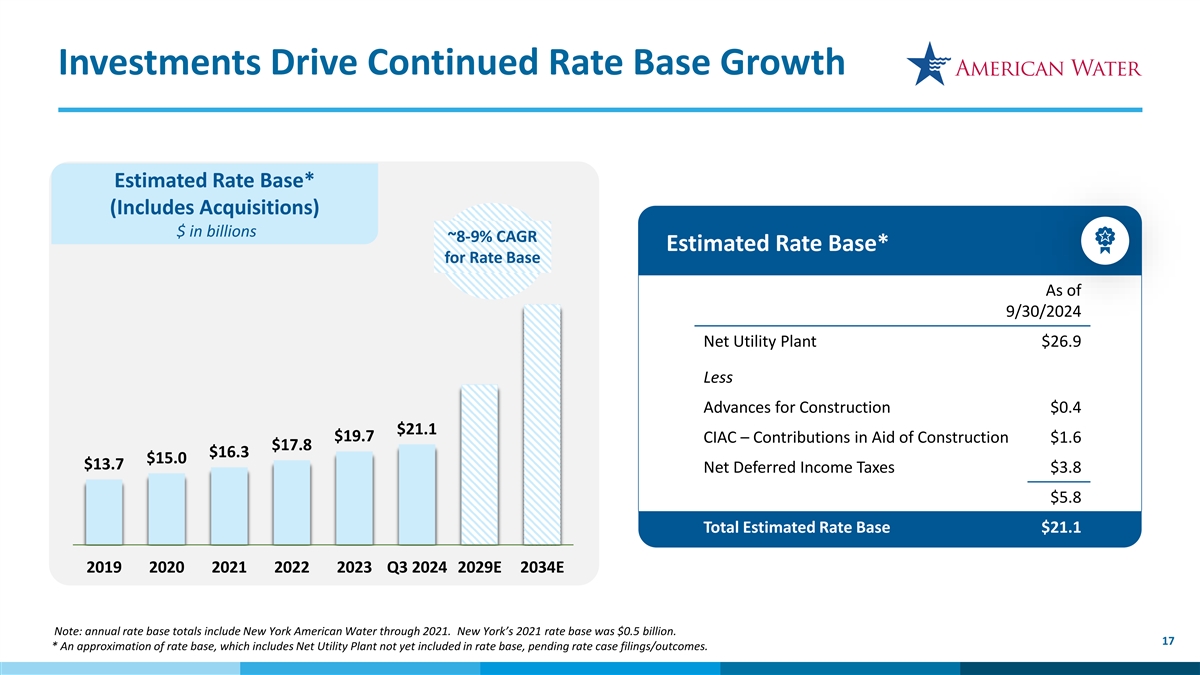

Investments Drive Continued Rate Base Growth Estimated Rate Base* (Includes Acquisitions) $ in billions ~8-9% CAGR Estimated Rate Base* for Rate Base As of 9/30/2024 Net Utility Plant $26.9 Less Advances for Construction $0.4 $21.1 $19.7 CIAC – Contributions in Aid of Construction $1.6 $17.8 $16.3 $15.0 $13.7 Net Deferred Income Taxes $3.8 $5.8 Total Estimated Rate Base $21.1 2019 2020 2021 2022 2023 Q3 2024 2029E 2034E Note: annual rate base totals include New York American Water through 2021. New York’s 2021 rate base was $0.5 billion. 17 * An approximation of rate base, which includes Net Utility Plant not yet included in rate base, pending rate case filings/outcomes.

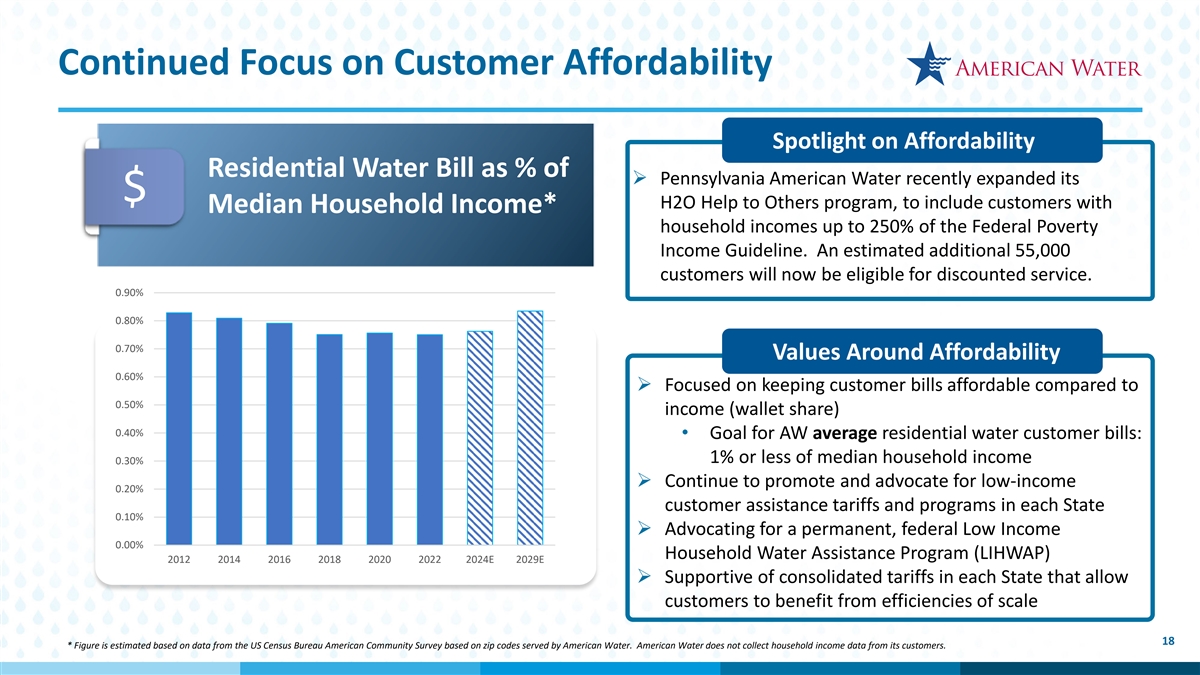

Continued Focus on Customer Affordability Spotlight on Affordability Residential Water Bill as % of Ø Pennsylvania American Water recently expanded its $ H2O Help to Others program, to include customers with Median Household Income* household incomes up to 250% of the Federal Poverty Income Guideline. An estimated additional 55,000 customers will now be eligible for discounted service. 0.90% 0.80% 0.70% Values Around Affordability 0.60% Ø Focused on keeping customer bills affordable compared to 0.50% income (wallet share) 0.40% • Goal for AW average residential water customer bills: 1% or less of median household income 0.30% Ø Continue to promote and advocate for low-income 0.20% customer assistance tariffs and programs in each State 0.10% Ø Advocating for a permanent, federal Low Income 0.00% Household Water Assistance Program (LIHWAP) 2012 2014 2016 2018 2020 2022 2024E 2029E Ø Supportive of consolidated tariffs in each State that allow customers to benefit from efficiencies of scale 18 * Figure is estimated based on data from the US Census Bureau American Community Survey based on zip codes served by American Water. American Water does not collect household income data from its customers.

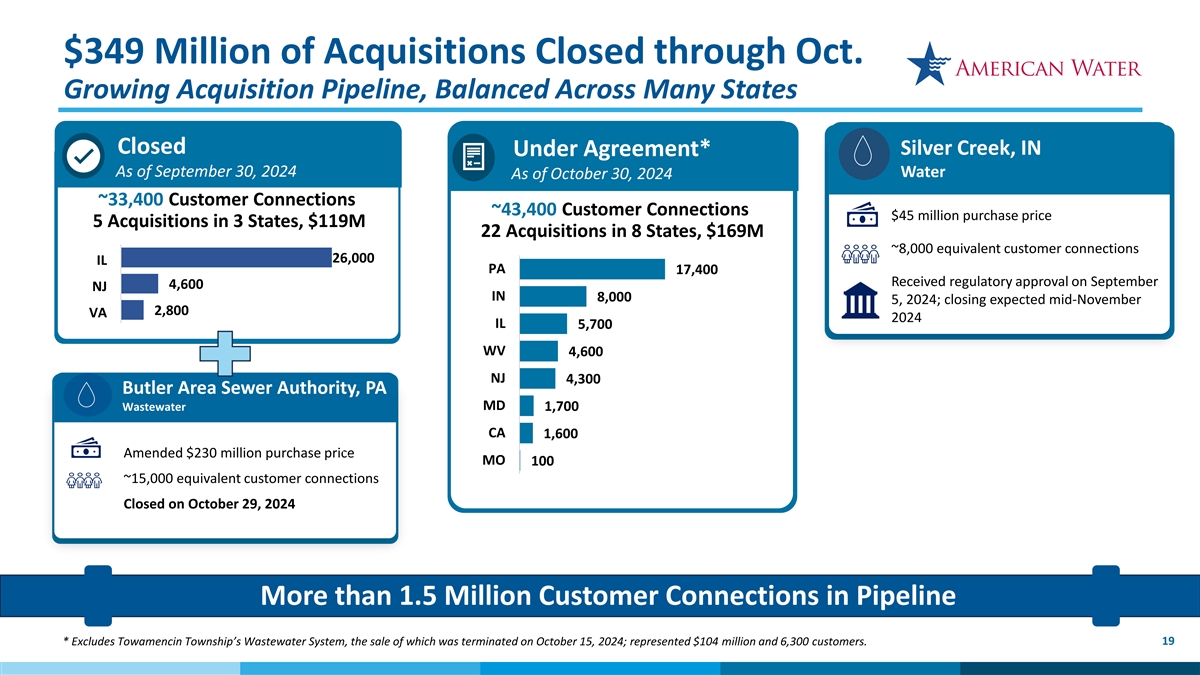

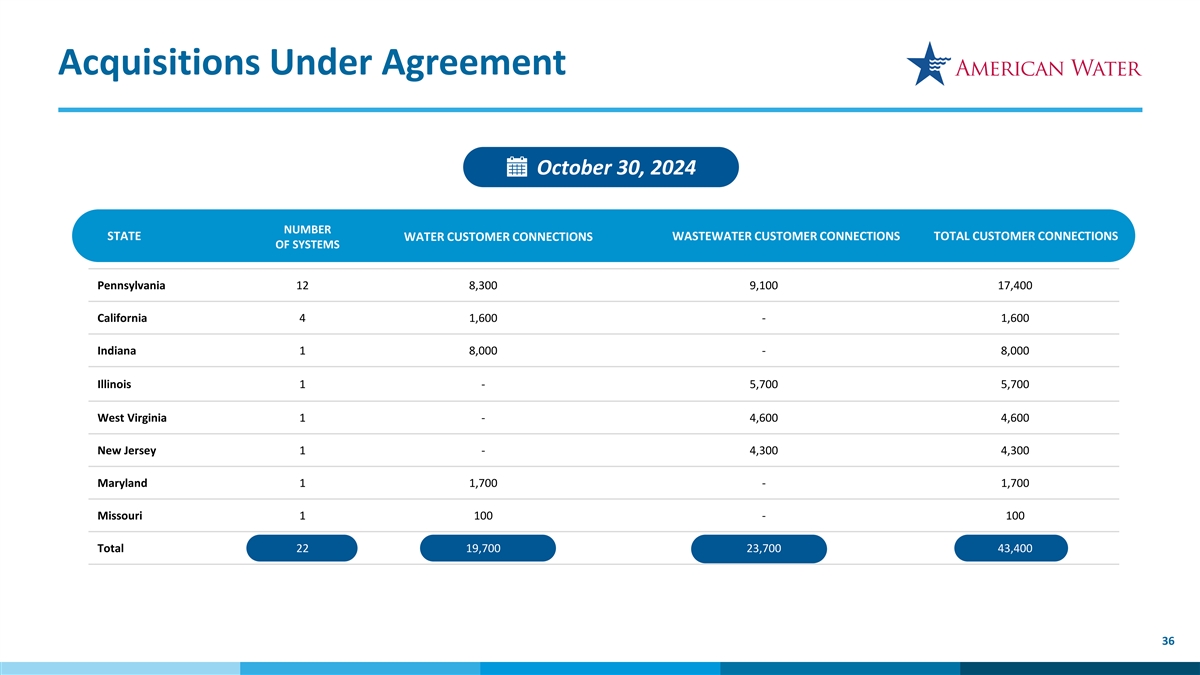

$349 Million of Acquisitions Closed through Oct. Growing Acquisition Pipeline, Balanced Across Many States Closed Silver Creek, IN Under Agreement* As of September 30, 2024 Water As of October 30, 2024 6 4 ~33,400 Customer Connections IL 3 ~43,400 Customer Connections $45 million purchase price 3 5 Acquisitions in 3 States, $119M 3 22 Acquisitions in 8 States, $169M CA 3 2 ~8,000 equivalent customer connections 2 26,000 IN IL 1 PA 17,400 Received regulatory approval on September 4,600 NJ IN 8,000 5, 2024; closing expected mid-November 2,800 VA 2024 IL 5,700 WV 4,600 NJ 4,300 Butler Area Sewer Authority, PA MD Wastewater 1,700 6 CA 1,600 4 IL 3 3 Amended $230 million purchase price 3 MO 100 CA 3 2 2 ~15,000 equivalent customer connections IN 1 Closed on October 29, 2024 More than 1.5 Million Customer Connections in Pipeline * Excludes Towamencin Township’s Wastewater System, the sale of which was terminated on October 15, 2024; represented $104 million and 6,300 customers. 19

M. Susan Hardwick Chief Executive Officer 20

Investing in AWK as a Premium, Pure-Play U.S. Regulated Water and Wastewater Utility Near and Long-Term Top Tier Earnings and Customer Affordability Why American Dividend Growth Advantage Water Deserves a Premium Multiple Geographic and Increase Wastewater Within and Adjacent to Regulatory Diversity Water Footprint Lower Risk Cap Ex Excellent Plan and Decades Sustainability Significant Pipeline Continuing of Investment Values and of Acquisition Theme of Need Credentials Opportunities due Water as an to Industry Investable, Fragmentation Scarce Asset 21

Q&A Session 22

INVESTOR RELATIONS CONTACTS Aaron Musgrave, CPA Jack Quinn, CPA Vice President, Investor Relations Senior Manager, Investor Relations aaron.musgrave@amwater.com jack.quinn@amwater.com Kelley Uyeda Janelle McNally Analyst, Investor Relations & ESG Director, Sustainability kelley.uyeda@amwater.com janelle.mcnally@amwater.com UPCOMING EVENTS EEI Financial Conference November 10-12, 2024 Q4 2024 & Year-End Earnings Call February 20, 2025 (projected) 23

Appendix 24

Forward Looking Statements Certain statements made, referred to or relied upon in this presentation including, without limitation, 2024 and 2025 earnings guidance, the Company’s long-term financial, growth and dividend targets, the ability to achieve the Company’s strategies and goals, customer affordability and acquired customer growth, the outcome of the Company’s pending acquisition activity, the amount and allocation of projected capital expenditures and its capital recovery outlook, and estimated revenues from rate cases and other government agency authorizations, are forward- looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and the Federal securities laws. In some cases, these forward-looking statements can be identified by words with prospective meanings such as “intend,” “plan,” “estimate,” “believe,” “anticipate,” “expect,” “predict,” “project,” “propose,” “assume,” “forecast,” “outlook,” “likely,” “uncertain,” “future,” “pending,” “goal,” “objective,” “potential,” “continue,” “seek to,” “may,” “can,” “will,” “should” and “could” and or the negative of such terms or other variations or similar expressions. These forward-looking statements are predictions based on American Water’s current expectations and assumptions regarding future events. They are not guarantees or assurances of any outcomes, financial results, levels of activity, performance or achievements, and readers are cautioned not to place undue reliance upon them. The forward-looking statements are subject to a number of estimates, assumptions, known and unknown risks, uncertainties and other factors. The Company’s actual results may vary materially from those discussed in the forward-looking statements included in this presentation as a result of the factors discussed in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023, and subsequent filings with the SEC, and because of factors such as: the decisions of governmental and regulatory bodies, including decisions to raise or lower customer rates; the timeliness and outcome of regulatory commissions’ and other authorities’ actions concerning rates, capital structure, authorized return on equity, capital investment, system acquisitions and dispositions, taxes, permitting, water supply and management, and other decisions; changes in customer demand for, and patterns of use of, water and energy, such as may result from conservation efforts, or otherwise; limitations on the availability of the Company’s water supplies or sources of water, or restrictions on its use thereof, resulting from allocation rights, governmental or regulatory requirements and restrictions, drought, overuse or other factors; a loss of one or more large industrial or commercial customers due to adverse economic conditions or other factors; present and future proposed changes in laws, governmental regulations and policies, including with respect to the environment (such as, for example, potential improvements to existing Federal regulations with respect to lead and copper service lines and galvanized steel pipe), health and safety, data and consumer privacy, security and protection, water quality and water quality accountability, contaminants of emerging concern (including without limitation per- and polyfluoroalkyl substances (“PFAS”)), public utility and tax regulations and policies, and impacts resulting from U.S., state and local elections and changes in federal, state and local executive administrations; the Company’s ability to collect, distribute, use, secure and store consumer data in compliance with current or future governmental laws, regulations and policies with respect to data and consumer privacy, security and protection; the company’s plans and efforts to protect and remediate its computer networks and systems following the company’s October 3, 2024 cybersecurity incident, and the impacts of such incident on the company and/or its financial condition and results of operations; weather conditions and events, climate variability patterns, and natural disasters, including drought or abnormally high rainfall, prolonged and abnormal ice or freezing conditions, strong winds, coastal and intercoastal flooding, pandemics (including COVID-19) and epidemics, earthquakes, landslides, hurricanes, tornadoes, wildfires, electrical storms, sinkholes and solar flares; the outcome of litigation and similar governmental and regulatory proceedings, investigations or actions; the risks associated with the Company’s aging infrastructure, and its ability to appropriately improve the resiliency of or maintain, update, redesign and/or replace, current or future infrastructure and systems, including its technology and other assets, and manage the expansion of its businesses; exposure or infiltration of the Company’s technology and critical infrastructure systems, including the disclosure of sensitive, personal or confidential information contained therein, through physical or cyber attacks or other means, and impacts from required or voluntary public and other disclosures related thereto, including with respect to the company’s reported October 3, 2024 cybersecurity incident; the Company’s ability to obtain permits and other approvals for projects and construction, update, redesign and/or replacement of various water and wastewater facilities; changes in the Company’s capital requirements; the Company’s ability to control operating expenses and to achieve operating efficiencies, and the Company’s ability to create, maintain and promote initiatives and programs that support the affordability of the Company’s regulated utility services; the intentional or unintentional actions of a third party, including contamination of the Company’s water supplies or the water provided to its customers; the Company’s ability to obtain and have delivered adequate and cost-effective supplies of pipe, equipment (including personal protective equipment), chemicals, power and other fuel, water and other raw materials, and to address or mitigate supply chain constraints that may result in delays or shortages in, as well as increased costs of, supplies, products and materials that are critical to or used in the Company’s business operations; the Company’s ability to successfully meet its operational growth projections, either individually or in the aggregate, and capitalize on growth opportunities, including, among other things, with respect to acquiring, closing and successfully integrating regulated operations, including without limitation the Company’s ability to (i) obtain required regulatory approvals for such acquisitions, (ii) prevail in litigation or other challenges related to such acquisitions, and (iii) recover in rates the fair value of assets of the acquired regulated operations, the Company’s Military Services Group entering into new military installation contracts, price redeterminations, and other agreements and contracts with the U.S. government, and realizing anticipated benefits and synergies from new acquisitions; risks and uncertainties following the completion of the sale of the Company’s Homeowner Services Group (“HOS”), including the Company’s ability to receive amounts due, payable and owing to the Company under the amended secured seller note when due, and the ability of the Company to redeploy successfully and timely the net proceeds of this transaction into the Company’s Regulated Businesses; risks and uncertainties associated with contracting with the U.S. government, including ongoing compliance with applicable government procurement and security regulations; cost overruns relating to improvements in or the expansion of the Company’s operations; the Company’s ability to successfully develop and implement new technologies and to protect related intellectual property; the Company’s ability to maintain safe work sites; the Company’s exposure to liabilities related to environmental laws and regulations, including those enacted or adopted and under consideration, and the substances related thereto, including without limitation lead and galvanized steel, PFAS and other contaminants of emerging concern, and similar matters resulting from, among other things, water and wastewater service provided to customers; the ability of energy providers, state governments and other third parties to achieve or fulfill their greenhouse gas emission reduction goals, including without limitation through stated renewable portfolio standards and carbon transition plans; changes in general economic, political, business and financial market conditions; access to sufficient debt and/or equity capital on satisfactory terms and as needed to support operations and capital expenditures; fluctuations in inflation or interest rates, and the Company’s ability to address or mitigate the impacts thereof; the ability to comply with affirmative or negative covenants in the current or future indebtedness of the Company or any of its subsidiaries, or the issuance of new or modified credit ratings or outlooks by credit rating agencies with respect to the Company or any of its subsidiaries (or any current or future indebtedness thereof), which could increase financing costs or funding requirements and affect the Company’s or its subsidiaries’ ability to issue, repay or redeem debt, pay dividends or make distributions; fluctuations in the value of, or assumptions and estimates related to, its benefit plan assets and liabilities, including with respect to its pension and other post-retirement benefit plans, that could increase expenses and plan funding requirements; changes in federal or state general, income and other tax laws, including (i) future significant tax legislation or regulations (including without limitation impacts related to the Corporate Alternative Minimum Tax); and (ii) the availability of, or the Company’s compliance with, the terms of applicable tax credits and tax abatement programs; migration of customers into or out of the Company’s service territories and changes in water and energy consumption resulting therefrom; the use by municipalities of the power of eminent domain or other authority to condemn the systems of one or more of the Company’s utility subsidiaries, including without limitation litigation and other proceedings with respect to the water system assets of the Company’s California subsidiary located in Monterey, California, or the assertion by private landowners of similar rights against such utility subsidiaries; any difficulty or inability to obtain insurance for the Company, its inability to obtain insurance at acceptable rates and on acceptable terms and conditions, or its inability to obtain reimbursement under existing or future insurance programs and coverages for any losses sustained; the incurrence of impairment charges, changes in fair value and other adjustments related to the Company’s goodwill or the value of its other assets; labor actions, including work stoppages and strikes; the Company’s ability to retain and attract highly qualified and skilled employees and/or diverse talent; civil disturbances or unrest, or terrorist threats or acts, or public apprehension about future disturbances, unrest, or terrorist threats or acts; and the impact of new, and changes to existing, accounting standards. These forward-looking statements are qualified by, and should be read together with, the risks and uncertainties set forth above and the risk factors included in American Water’s annual, quarterly and other SEC filings, and readers should refer to such risks, uncertainties and risk factors in evaluating such forward-looking statements. Any forward-looking statements American Water makes speak only as of the date of this presentation. American Water does not have any obligation, and it specifically disclaims any undertaking or intention, to publicly update or revise any forward-looking statements, whether as a result of new information, future events, changed circumstances or otherwise, except as otherwise required by the federal securities laws. New factors emerge from time to time, and it is not possible for the Company to predict all such factors. 25 Furthermore, it may not be possible to assess the impact of any such factor on the Company’s businesses, either viewed independently or together, or the extent to which any factor, or combination of factors, may cause results to differ materially from those contained in any forward- looking statement. The foregoing factors should not be construed as exhaustive.

2024 and 2025 Earnings Guidance (Non-GAAP) This presentation includes a description of American Water’s 2024 and 2025 earnings guidance ranges, and its expected 2024 dividend payout ratio, excluding the incremental $0.10 per share of interest to be recognized from the amended HOS seller note. This information would constitute “non-GAAP financial measures” under SEC rules. They are derived from American Water’s consolidated financial information but are not presented in financial statements prepared in accordance with generally accepted accounting principles (“GAAP”). This information supplements American Water’s GAAP disclosures and should be considered in addition to, and not in substitution of, measures of financial performance prepared in accordance with GAAP. Management believes this information is useful to American Water’s investors because it excludes an item not reflective of its ongoing operating results and the presentation will allow investors to understand better the operating performance of American Water’s regulated businesses. Although management will use this information internally to evaluate American Water’s results of operations and to facilitate a meaningful year-to-year comparison thereof, management does not intend this information to represent future results as defined by GAAP, and investors should not consider it as such. In addition, this information may not be comparable to similar presentations by other companies, and, accordingly, it may have significant limitations in its use. 26

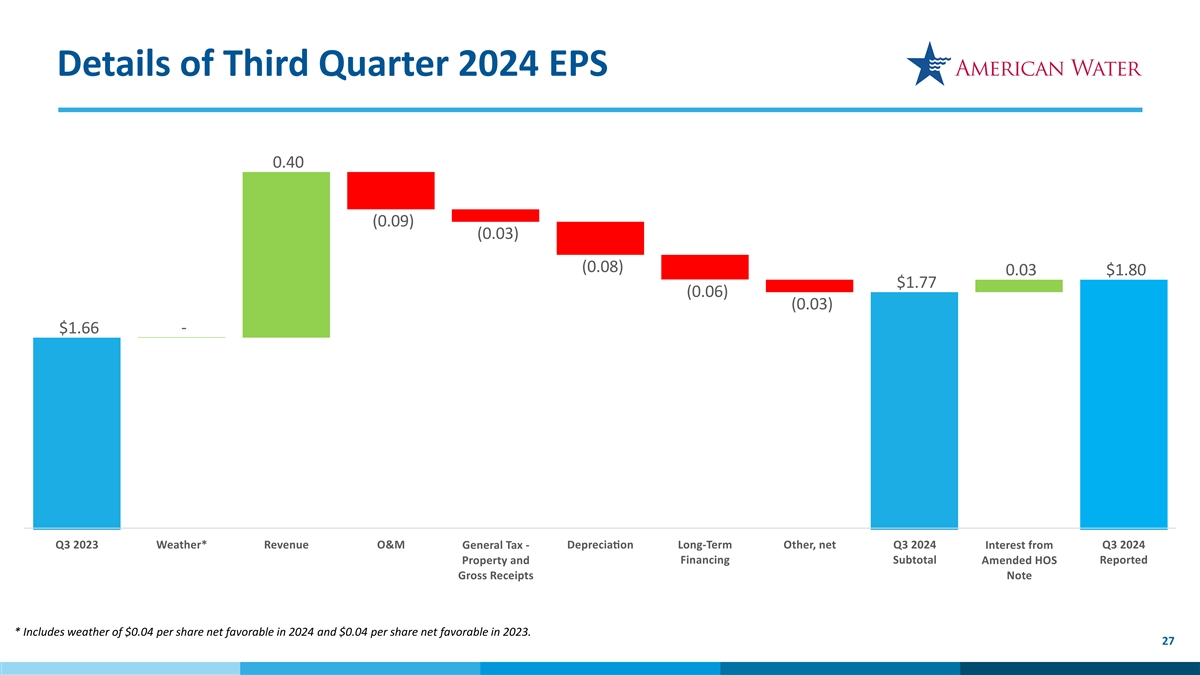

Details of Third Quarter 2024 EPS 0.40 (0.09) (0.03) (0.08) 0.03 $1.80 $1.77 (0.06) (0.03) $1.66 - Q3 2023 Weather* Revenue O&M General Tax - D eprec iati on Long-Term Other, net Q3 2024 Interest from Q3 2024 Property and Financing Subtotal Amended HOS Reported Gross Receipts Note * Includes weather of $0.04 per share net favorable in 2024 and $0.04 per share net favorable in 2023. 27

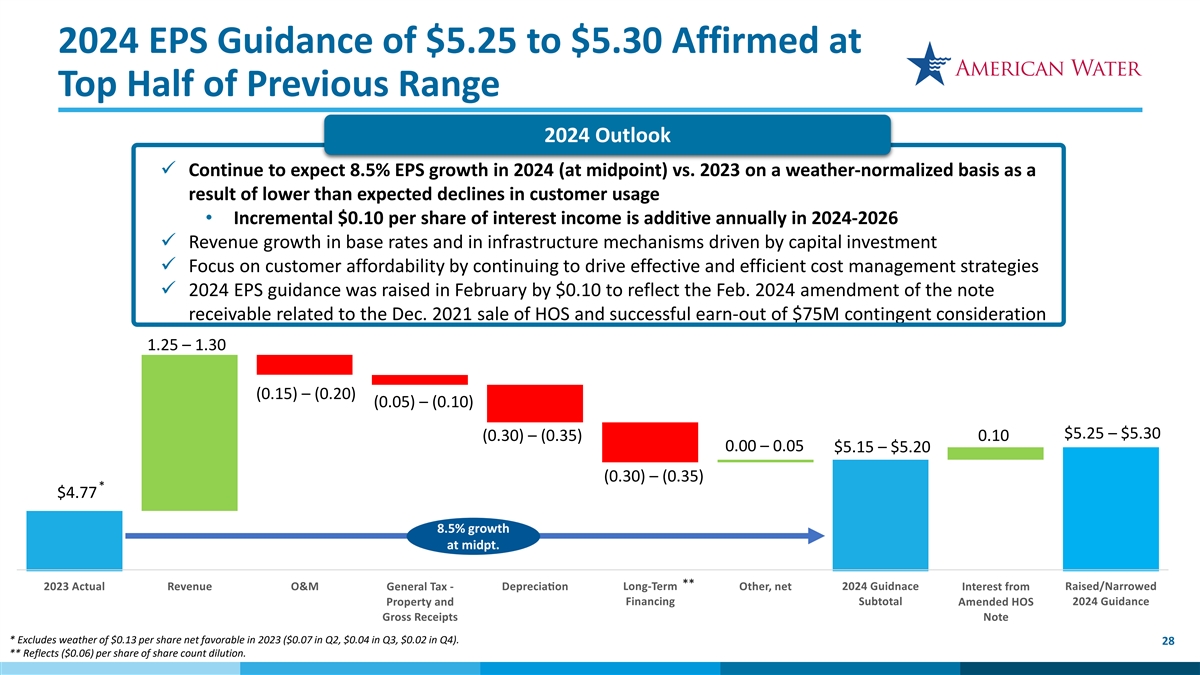

2024 EPS Guidance of $5.25 to $5.30 Affirmed at Top Half of Previous Range 2024 Outlook ü Continue to expect 8.5% EPS growth in 2024 (at midpoint) vs. 2023 on a weather-normalized basis as a result of lower than expected declines in customer usage • Incremental $0.10 per share of interest income is additive annually in 2024-2026 ü Revenue growth in base rates and in infrastructure mechanisms driven by capital investment ü Focus on customer affordability by continuing to drive effective and efficient cost management strategies ü 2024 EPS guidance was raised in February by $0.10 to reflect the Feb. 2024 amendment of the note receivable related to the Dec. 2021 sale of HOS and successful earn-out of $75M contingent consideration 1.25 – 1.30 (0.15) – (0.20) (0.05) – (0.10) $5.25 – $5.30 (0.30) – (0.35) 0.10 0.00 – 0.05 $5.15 – $5.20 (0.30) – (0.35) * $4.77 8.5% growth at midpt. ** 2023 Actual Revenue O&M General Tax - D eprec iati on Long-Term Other, net 2024 Guidnace Interest from Raised/Narrowed Financing Subtotal 2024 Guidance Property and Amended HOS Gross Receipts Note * Excludes weather of $0.13 per share net favorable in 2023 ($0.07 in Q2, $0.04 in Q3, $0.02 in Q4). 28 ** Reflects ($0.06) per share of share count dilution.

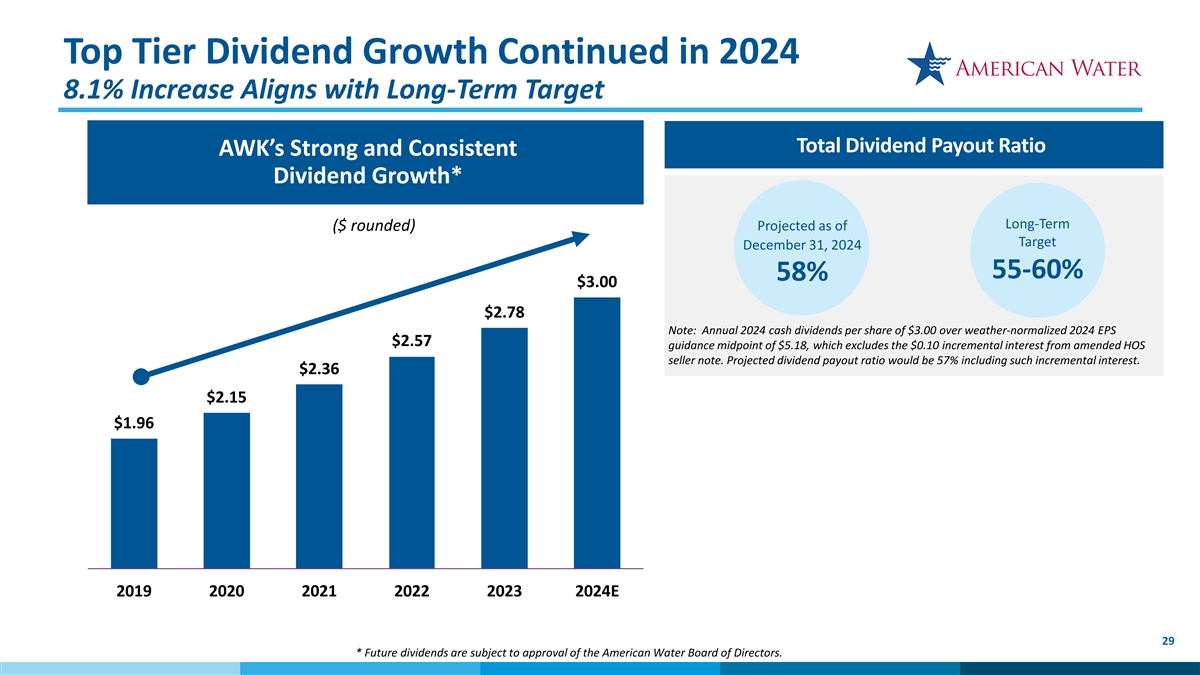

Top Tier Dividend Growth Continued in 2024 8.1% Increase Aligns with Long-Term Target Total Dividend Payout Ratio AWK’s Strong and Consistent Dividend Growth* Long-Term ($ rounded) Projected as of Target December 31, 2024 55-60% 58% $3.00 $2.78 Note: Annual 2024 cash dividends per share of $3.00 over weather-normalized 2024 EPS $2.57 guidance midpoint of $5.18, which excludes the $0.10 incremental interest from amended HOS seller note. Projected dividend payout ratio would be 57% including such incremental interest. $2.36 $2.15 $1.96 2019 2020 2021 2022 2023 2024E 29 * Future dividends are subject to approval of the American Water Board of Directors.

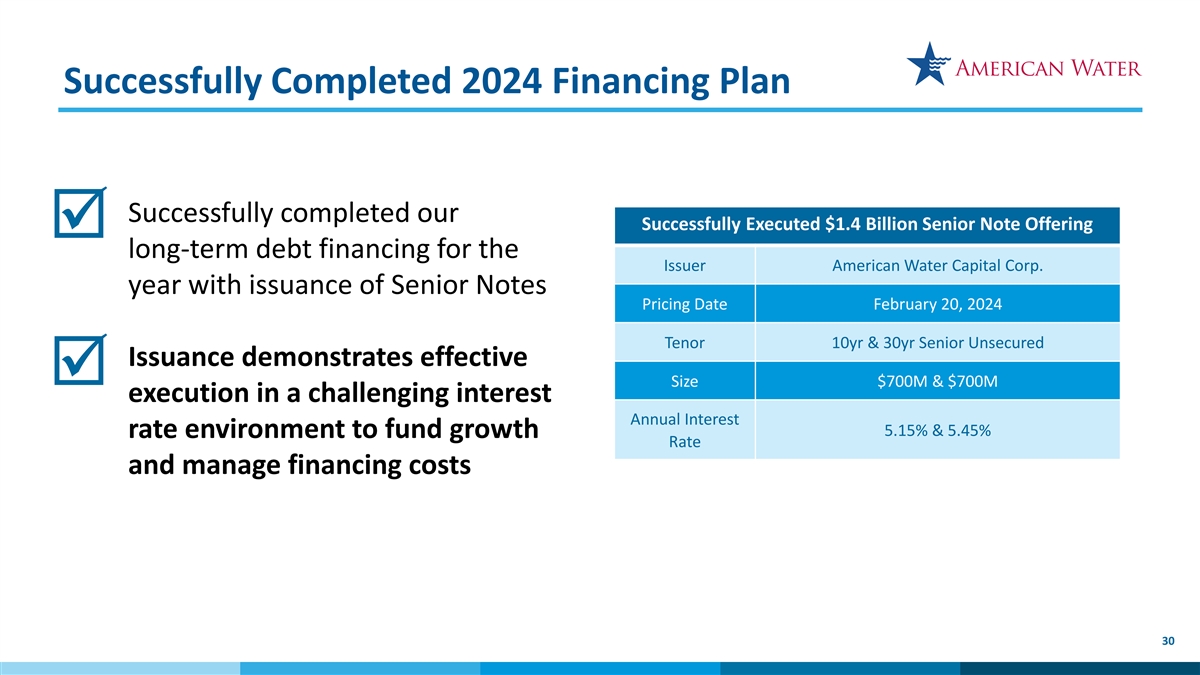

Successfully Completed 2024 Financing Plan Successfully completed our Successfully Executed $1.4 Billion Senior Note Offering þ long-term debt financing for the Issuer American Water Capital Corp. year with issuance of Senior Notes Pricing Date February 20, 2024 Tenor 10yr & 30yr Senior Unsecured Issuance demonstrates effective þ Size $700M & $700M execution in a challenging interest Annual Interest 5.15% & 5.45% rate environment to fund growth Rate and manage financing costs 30

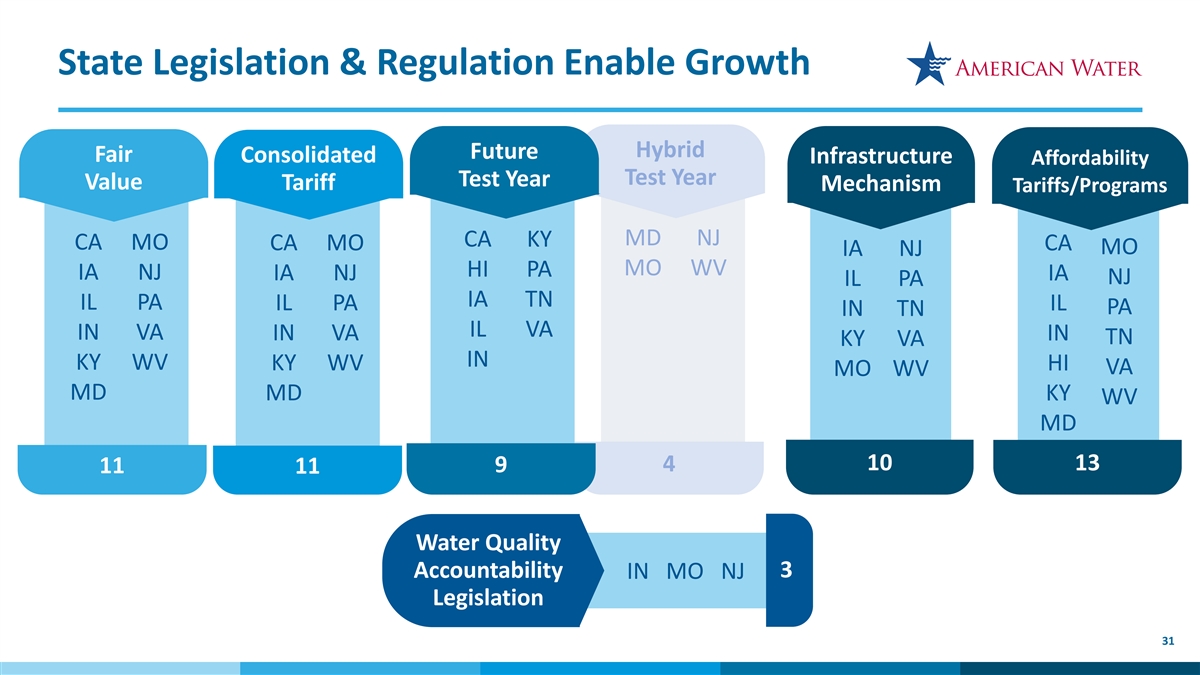

State Legislation & Regulation Enable Growth Hybrid Future Fair Consolidated Infrastructure Affordability Test Year Test Year Value Tariff Mechanism Tariffs/Programs MD NJ CA KY CA MO CA MO CA MO IA NJ MO WV HI PA IA NJ IA NJ IA NJ IL PA IA TN IL PA IL PA IL PA IN TN IL VA IN VA IN VA IN TN KY VA IN KY WV KY WV HI VA MO WV MD MD KY WV MD 10 13 4 9 11 11 Water Quality Accountability 3 IN MO NJ Legislation 31

U.S. EPA PFAS Rule Announced on April 10, 2024 Largely unchanged from proposed rule Final Federal PFAS Rule Recap Ø Drinking water limits of 4.0 parts per trillion (ppt) for PFOA and PFOS unchanged vs. proposed rule • Limits set for three additional PFAS Ø Five years to comply versus three years in the proposed rule (2029 versus 2027) Ø U.S. EPA designated PFOA and PFOS as hazardous substances under CERCLA through a separate rulemaking in April. The Company is actively advocating and supporting bipartisan legislation that would provide PFAS liability protections under CERCLA for water and wastewater systems, as passive receivers of PFAS. Ø American Water’s estimates ~$1B of capital and up to ~$50M annually for operating expenses * *Includes PFAS treatment PFAS Litigation Recap Ø American Water is a party to the Multi-District Litigation (MDL) lawsuit against several PFAS manufacturers. Ø In Dec. 2023, we decided to remain a party to two settlements, which we believe is the best path for our customers. • In Feb. and Mar. 2024, the MDL court approved settlements with DuPont and 3M, respectively; the amount of proceeds to be received from each settlement is pending. 32

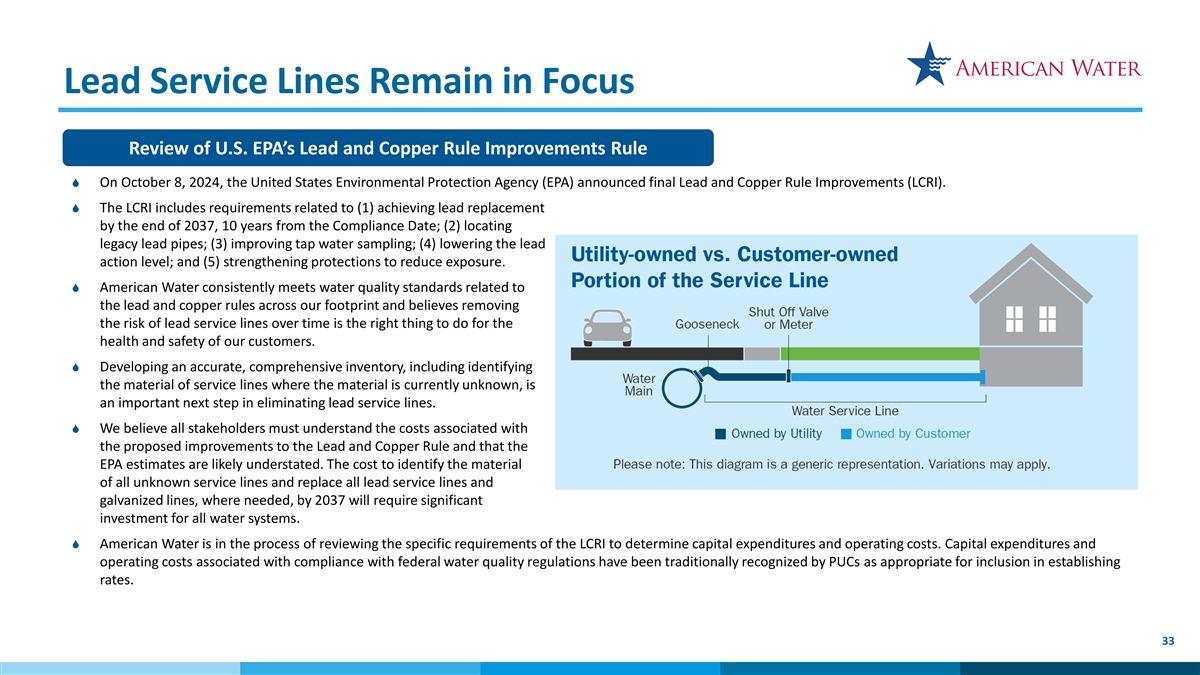

Lead Service Lines Remain in Focus Review of U.S. EPA’s Lead and Copper Rule Improvements Rule S On October 8, 2024, the United States Environmental Protection Agency (EPA) announced final Lead and Copper Rule Improvements (LCRI). S The LCRI includes requirements related to (1) achieving lead replacement by the end of 2037, 10 years from the Compliance Date; (2) locating legacy lead pipes; (3) improving tap water sampling; (4) lowering the lead action level; and (5) strengthening protections to reduce exposure. S American Water consistently meets water quality standards related to the lead and copper rules across our footprint and believes removing the risk of lead service lines over time is the right thing to do for the health and safety of our customers. S Developing an accurate, comprehensive inventory, including identifying the material of service lines where the material is currently unknown, is an important next step in eliminating lead service lines. S We believe all stakeholders must understand the costs associated with the proposed improvements to the Lead and Copper Rule and that the EPA estimates are likely understated. The cost to identify the material of all unknown service lines and replace all lead service lines and galvanized lines, where needed, by 2037 will require significant investment for all water systems. S American Water is in the process of reviewing the specific requirements of the LCRI to determine capital expenditures and operating costs. Capital expenditures and operating costs associated with compliance with federal water quality regulations have been traditionally recognized by PUCs as appropriate for inclusion in establishing rates. 33

Military Services Group Provides Strategic Value Currently Serving 70 Additional Installation 18 Military Installations Opportunities 12 Army 15 Army Military Services Group 5 Air Force 23 Air Force S Regulated-like earnings S Favorable ROI opportunity S Capital light / cash flow positive 1 Navy 19 Navy S Positive branding S Leverage core competencies S Dual wins for AWK & U.S. ESG values 0 Marine Corps 13 Marine Corps 34

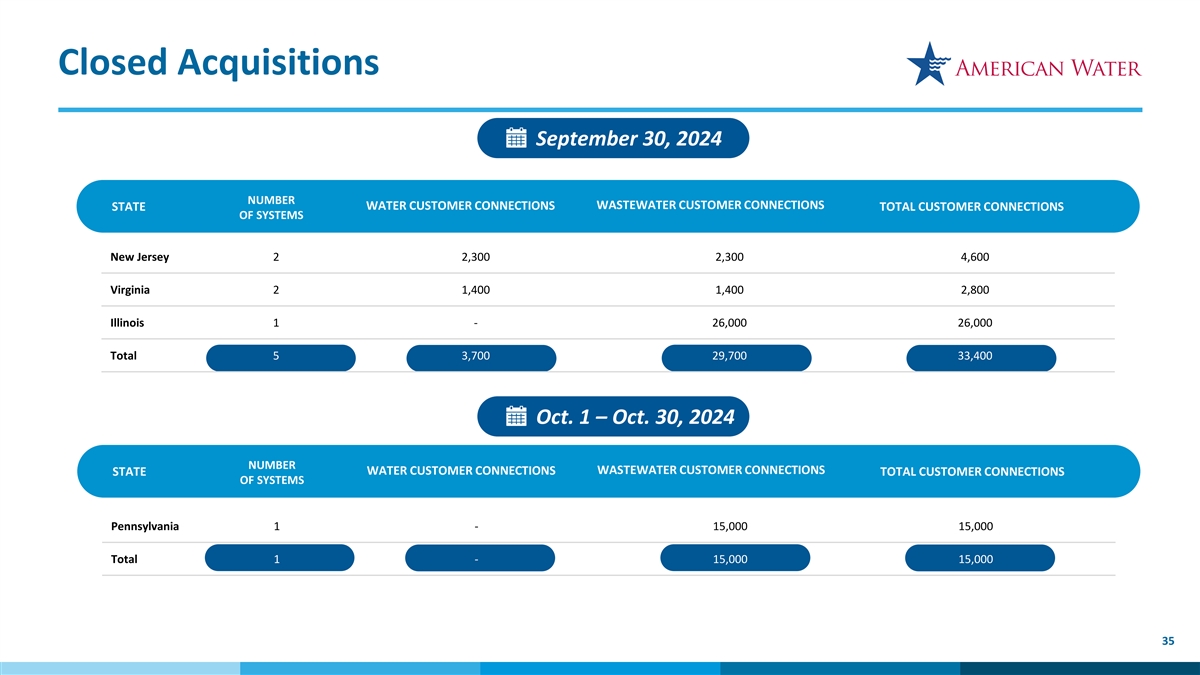

Closed Acquisitions September 30, 2024 NUMBER WASTEWATER CUSTOMER CONNECTIONS WATER CUSTOMER CONNECTIONS STATE TOTAL CUSTOMER CONNECTIONS OF SYSTEMS New Jersey 2 2,300 2,300 4,600 Virginia 2 1,400 1,400 2,800 Illinois 1 - 26,000 26,000 Total 5 3,700 29,700 33,400 Oct. 1 – Oct. 30, 2024 NUMBER WASTEWATER CUSTOMER CONNECTIONS WATER CUSTOMER CONNECTIONS STATE TOTAL CUSTOMER CONNECTIONS OF SYSTEMS Pennsylvania 1 - 15,000 15,000 Total 1 - 15,000 15,000 35

Acquisitions Under Agreement October 30, 2024 NUMBER STATE WASTEWATER CUSTOMER CONNECTIONS TOTAL CUSTOMER CONNECTIONS WATER CUSTOMER CONNECTIONS OF SYSTEMS Pennsylvania 12 8,300 9,100 17,400 California 4 1,600 - 1,600 Indiana 1 8,000 - 8,000 Illinois 1 - 5,700 5,700 West Virginia 1 - 4,600 4,600 New Jersey 1 - 4,300 4,300 Maryland 1 1,700 - 1,700 Missouri 1 100 - 100 Total 22 19,700 23,700 43,400 36

Annualized Revenue from Rate Proceedings ($ in millions) Rate Filings Completed* Requested Revenue in Pending Rate Proceedings Effective since January 1, 2024 $23 $375 $90 $346 $352 $256 Rate Cases Infrastructure Total Rate Cases** Total Infrastructure Charges (Includes Charges Step Increases) * Annualized revenue increase for rates effective since January 1, 2024 ** Excludes revenue already approved through infrastructure mechanisms 37

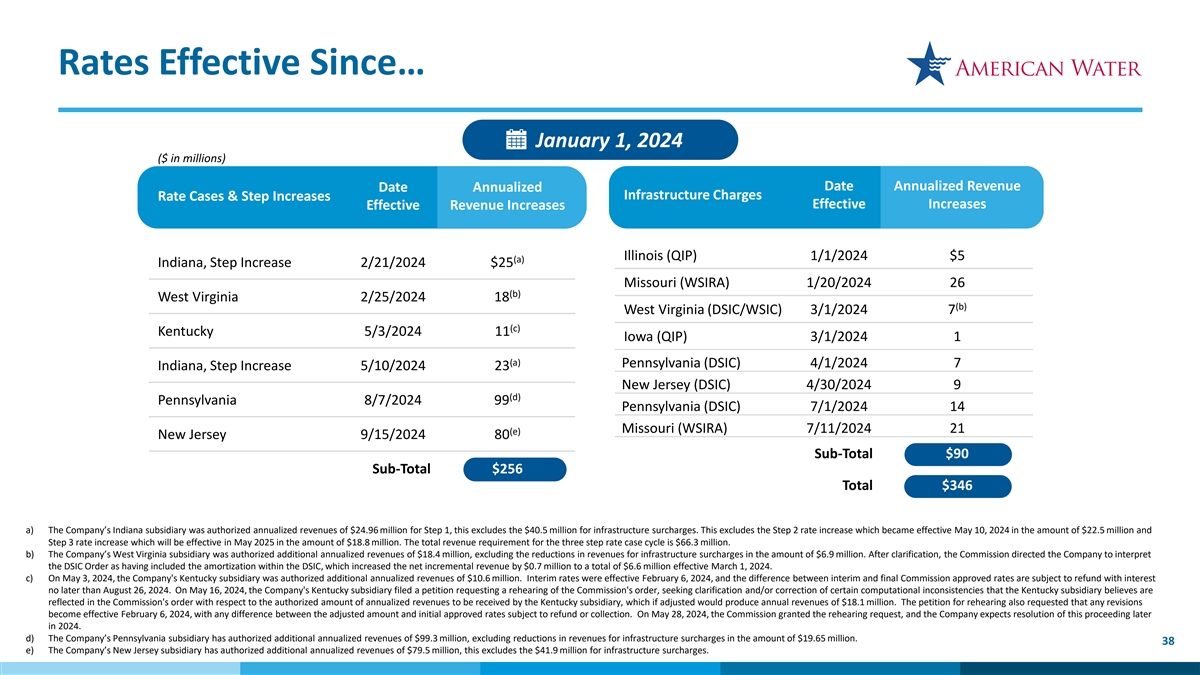

Rates Effective Since… January 1, 2024 ($ in millions) Date Annualized Revenue Date Annualized Infrastructure Charges Rate Cases & Step Increases Effective Increases Effective Revenue Increases Illinois (QIP) 1/1/2024 $5 (a) Indiana, Step Increase 2/21/2024 $25 Missouri (WSIRA) 1/20/2024 26 (b) West Virginia 2/25/2024 18 (b) West Virginia (DSIC/WSIC) 3/1/2024 7 (c) Kentucky 5/3/2024 11 Iowa (QIP) 3/1/2024 1 (a) Pennsylvania (DSIC) 4/1/2024 7 Indiana, Step Increase 5/10/2024 23 New Jersey (DSIC) 4/30/2024 9 (d) Pennsylvania 8/7/2024 99 Pennsylvania (DSIC) 7/1/2024 14 Missouri (WSIRA) 7/11/2024 21 (e) New Jersey 9/15/2024 80 Sub-Total $90 Sub-Total $256 Total $346 a) The Company’s Indiana subsidiary was authorized annualized revenues of $24.96 million for Step 1, this excludes the $40.5 million for infrastructure surcharges. This excludes the Step 2 rate increase which became effective May 10, 2024 in the amount of $22.5 million and Step 3 rate increase which will be effective in May 2025 in the amount of $18.8 million. The total revenue requirement for the three step rate case cycle is $66.3 million. b) The Company’s West Virginia subsidiary was authorized additional annualized revenues of $18.4 million, excluding the reductions in revenues for infrastructure surcharges in the amount of $6.9 million. After clarification, the Commission directed the Company to interpret the DSIC Order as having included the amortization within the DSIC, which increased the net incremental revenue by $0.7 million to a total of $6.6 million effective March 1, 2024. c) On May 3, 2024, the Company's Kentucky subsidiary was authorized additional annualized revenues of $10.6 million. Interim rates were effective February 6, 2024, and the difference between interim and final Commission approved rates are subject to refund with interest no later than August 26, 2024. On May 16, 2024, the Company's Kentucky subsidiary filed a petition requesting a rehearing of the Commission's order, seeking clarification and/or correction of certain computational inconsistencies that the Kentucky subsidiary believes are reflected in the Commission's order with respect to the authorized amount of annualized revenues to be received by the Kentucky subsidiary, which if adjusted would produce annual revenues of $18.1 million. The petition for rehearing also requested that any revisions become effective February 6, 2024, with any difference between the adjusted amount and initial approved rates subject to refund or collection. On May 28, 2024, the Commission granted the rehearing request, and the Company expects resolution of this proceeding later in 2024. d) The Company’s Pennsylvania subsidiary has authorized additional annualized revenues of $99.3 million, excluding reductions in revenues for infrastructure surcharges in the amount of $19.65 million. 38 e) The Company’s New Jersey subsidiary has authorized additional annualized revenues of $79.5 million, this excludes the $41.9 million for infrastructure surcharges.

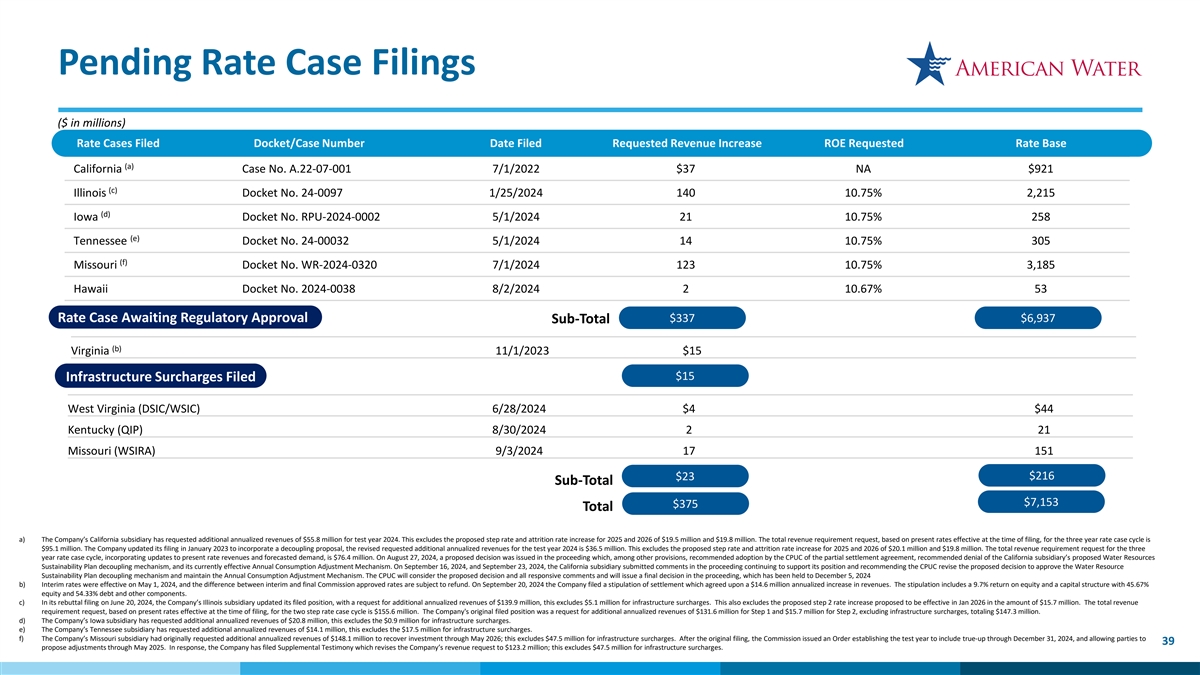

Pending Rate Case Filings ($ in millions) Rate Cases Filed Docket/Case Number Date Filed Requested Revenue Increase ROE Requested Rate Base (a) California Case No. A.22-07-001 7/1/2022 $37 NA $921 (c) Illinois Docket No. 24-0097 1/25/2024 140 10.75% 2,215 (d) Iowa Docket No. RPU-2024-0002 5/1/2024 21 10.75% 258 (e) Tennessee Docket No. 24-00032 5/1/2024 14 10.75% 305 (f) Missouri Docket No. WR-2024-0320 7/1/2024 123 10.75% 3,185 Hawaii Docket No. 2024-0038 8/2/2024 2 10.67% 53 Rate Case Awaiting Regulatory Approval $337 $6,937 Sub-Total (b) Virginia 11/1/2023 $15 $15 Infrastructure Surcharges Filed West Virginia (DSIC/WSIC) 6/28/2024 $4 $44 Kentucky (QIP) 8/30/2024 2 21 Missouri (WSIRA) 9/3/2024 17 151 $23 $216 Sub-Total $7,153 $375 Total a) The Company’s California subsidiary has requested additional annualized revenues of $55.8 million for test year 2024. This excludes the proposed step rate and attrition rate increase for 2025 and 2026 of $19.5 million and $19.8 million. The total revenue requirement request, based on present rates effective at the time of filing, for the three year rate case cycle is $95.1 million. The Company updated its filing in January 2023 to incorporate a decoupling proposal, the revised requested additional annualized revenues for the test year 2024 is $36.5 million. This excludes the proposed step rate and attrition rate increase for 2025 and 2026 of $20.1 million and $19.8 million. The total revenue requirement request for the three year rate case cycle, incorporating updates to present rate revenues and forecasted demand, is $76.4 million. On August 27, 2024, a proposed decision was issued in the proceeding which, among other provisions, recommended adoption by the CPUC of the partial settlement agreement, recommended denial of the California subsidiary’s proposed Water Resources Sustainability Plan decoupling mechanism, and its currently effective Annual Consumption Adjustment Mechanism. On September 16, 2024, and September 23, 2024, the California subsidiary submitted comments in the proceeding continuing to support its position and recommending the CPUC revise the proposed decision to approve the Water Resource Sustainability Plan decoupling mechanism and maintain the Annual Consumption Adjustment Mechanism. The CPUC will consider the proposed decision and all responsive comments and will issue a final decision in the proceeding, which has been held to December 5, 2024 b) Interim rates were effective on May 1, 2024, and the difference between interim and final Commission approved rates are subject to refund. On September 20, 2024 the Company filed a stipulation of settlement which agreed upon a $14.6 million annualized increase in revenues. The stipulation includes a 9.7% return on equity and a capital structure with 45.67% equity and 54.33% debt and other components. c) In its rebuttal filing on June 20, 2024, the Company’s Illinois subsidiary updated its filed position, with a request for additional annualized revenues of $139.9 million, this excludes $5.1 million for infrastructure surcharges. This also excludes the proposed step 2 rate increase proposed to be effective in Jan 2026 in the amount of $15.7 million. The total revenue requirement request, based on present rates effective at the time of filing, for the two step rate case cycle is $155.6 million. The Company's original filed position was a request for additional annualized revenues of $131.6 million for Step 1 and $15.7 million for Step 2, excluding infrastructure surcharges, totaling $147.3 million. d) The Company’s Iowa subsidiary has requested additional annualized revenues of $20.8 million, this excludes the $0.9 million for infrastructure surcharges. e) The Company’s Tennessee subsidiary has requested additional annualized revenues of $14.1 million, this excludes the $17.5 million for infrastructure surcharges. f) The Company’s Missouri subsidiary had originally requested additional annualized revenues of $148.1 million to recover investment through May 2026; this excludes $47.5 million for infrastructure surcharges. After the original filing, the Commission issued an Order establishing the test year to include true-up through December 31, 2024, and allowing parties to 39 propose adjustments through May 2025. In response, the Company has filed Supplemental Testimony which revises the Company’s revenue request to $123.2 million; this excludes $47.5 million for infrastructure surcharges.

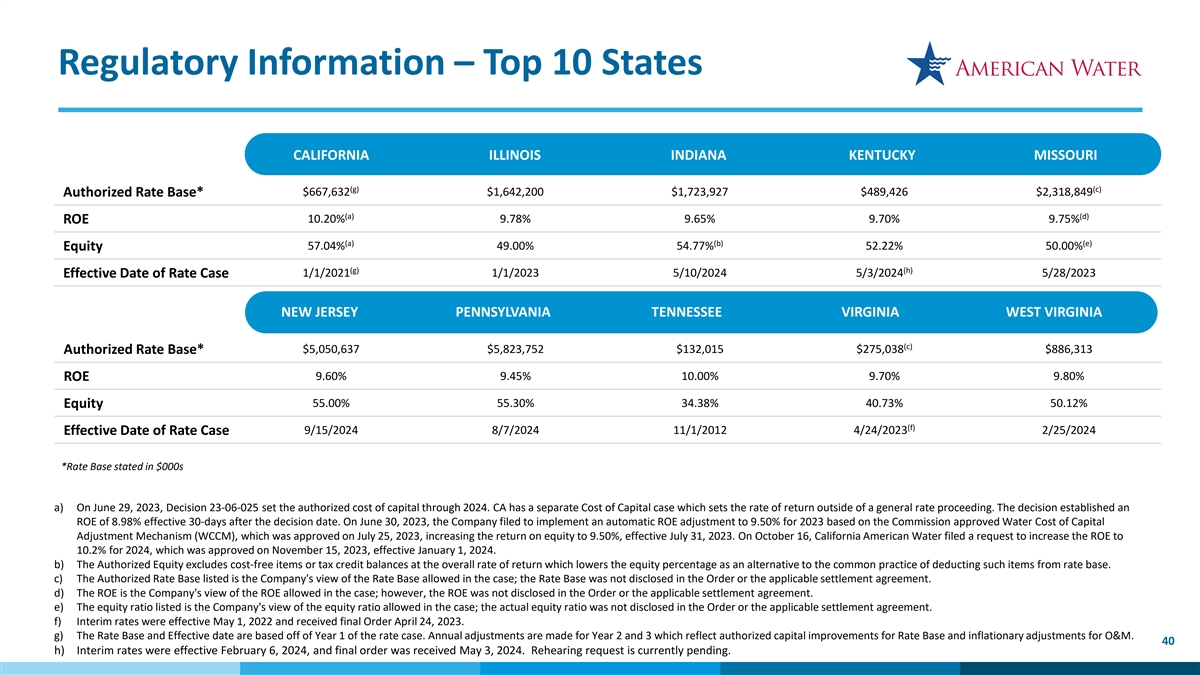

Regulatory Information – Top 10 States CALIFORNIA ILLINOIS INDIANA KENTUCKY MISSOURI (g) (c) Authorized Rate Base* $667,632 $1,642,200 $1,723,927 $489,426 $2,318,849 (a) (d) 10.20% 9.78% 9.65% 9.70% 9.75% ROE (a) (b) (e) 57.04% 49.00% 54.77% 52.22% 50.00% Equity (g) (h) Effective Date of Rate Case 1/1/2021 1/1/2023 5/10/2024 5/3/2024 5/28/2023 NEW JERSEY PENNSYLVANIA TENNESSEE VIRGINIA WEST VIRGINIA (c) Authorized Rate Base* $5,050,637 $5,823,752 $132,015 $275,038 $886,313 9.60% 9.45% 10.00% 9.70% 9.80% ROE Equity 55.00% 55.30% 34.38% 40.73% 50.12% (f) 9/15/2024 8/7/2024 11/1/2012 4/24/2023 2/25/2024 Effective Date of Rate Case *Rate Base stated in $000s a) On June 29, 2023, Decision 23-06-025 set the authorized cost of capital through 2024. CA has a separate Cost of Capital case which sets the rate of return outside of a general rate proceeding. The decision established an ROE of 8.98% effective 30-days after the decision date. On June 30, 2023, the Company filed to implement an automatic ROE adjustment to 9.50% for 2023 based on the Commission approved Water Cost of Capital Adjustment Mechanism (WCCM), which was approved on July 25, 2023, increasing the return on equity to 9.50%, effective July 31, 2023. On October 16, California American Water filed a request to increase the ROE to 10.2% for 2024, which was approved on November 15, 2023, effective January 1, 2024. b) The Authorized Equity excludes cost-free items or tax credit balances at the overall rate of return which lowers the equity percentage as an alternative to the common practice of deducting such items from rate base. c) The Authorized Rate Base listed is the Company's view of the Rate Base allowed in the case; the Rate Base was not disclosed in the Order or the applicable settlement agreement. d) The ROE is the Company's view of the ROE allowed in the case; however, the ROE was not disclosed in the Order or the applicable settlement agreement. e) The equity ratio listed is the Company's view of the equity ratio allowed in the case; the actual equity ratio was not disclosed in the Order or the applicable settlement agreement. f) Interim rates were effective May 1, 2022 and received final Order April 24, 2023. g) The Rate Base and Effective date are based off of Year 1 of the rate case. Annual adjustments are made for Year 2 and 3 which reflect authorized capital improvements for Rate Base and inflationary adjustments for O&M. 40 h) Interim rates were effective February 6, 2024, and final order was received May 3, 2024. Rehearing request is currently pending.