SCHNEIDER WEINBERGER & BEILLY LLP

2200 Corporate Boulevard, N.W.

Suite 210

Boca Raton, Florida 33431

telephone (561) 362-9595

telecopier (561) 362-9612

jim@swblaw.net

| January 20, 2011 |

'CORRESP'

United States Securities and Exchange Commission

100 F Street N.E.

Washington, D.C. 20549

| Attention: | Heather Clark, Sonia Bednarowski |

| Linda Cvrkel, Branch Chief |

| Re: | China Armco Metals, Inc. |

| Form 10-K for the year ended December 31, 2009 Filed March 31,2010 | |

| Form 10-Q for the quarter ended June 30, 2010 Filed August 16, 2010 | |

| Form 10-Q for the quarter ended September 30, 2010 Filed November 15, 2010 | |

| File No. 001-34631 |

Ladies and Gentlemen:

China Armco Metals, Inc. (the “Company”) is in receipt of the staff’s comment letter dated November 29, 2010. Following are the Company’s responses to the staff’s comments contained in such letter.

Annual Report on Form 10-K for the year ended December 31. 2009

Board Committees, page 7

| 1. | Please confirm that in future filings you will discuss whether, and if so how, your nominating and governance committee considers diversity in identifying nominees for director. Refer to Item 407(c)(2)(vi). |

RESPONSE: The Company hereby confirms that it will include in its future filings information on if and how its nominating and governance committee considers diversity in identifying nominees for its Board of Directors, in accordance with Item 407(c)(vi) of Regulation S-K.

Our performance, page 22

| 2. | We note from your disclosure in the second paragraph that your accounts receivable increased by $11.7 million mainly due to the extension of credit terms given to your customers. Please tell us if such extension was outside of the customary credit terms issued to your customers and if so, tell us what effect, if any, the change in credit terms had on revenue recognition such as the company's ability to meet the following revenue recognition criteria: (1) sales price is fixed and determinable and (2) collectability is probable. If no consideration was given, please explain why. |

RESPONSE: The credit terms for sales in the second half of fiscal 2009 did not depart materially from the Company’s standard credit terms. The Company’s use of the term “extension of credit terms” was intended to explain that credit terms were given to the Company’s customers consistent with the Company’s established practices, albeit on a significant increase in sales volume. This language was not intended to mean that the Company gave its customers a longer period of time to pay for their purchases. These credit terms had no impact on the Company’s revenue recognition as all of the revenue recognition criteria, including that the sales price be fixed and determinable and that collectability is reasonably assured, were met. The Company will revise the language in future periods as appropriate to make this clear.

- 1 -

Critical Accounting Policies, page 29

| 3. We note that your critical accounting policies disclosures refer to note 2 of the financial statements. In this regard, we believe this disclosure in MD&A should supplement, not duplicate, the description of accounting policies disclosed in the notes. In this regard, please ensure that your critical accounting estimates disclosure - (i) provide greater insight into the quality and variability of information in the consolidated financial statements; (ii) address specifically why the accounting estimates or assumptions bear the risk of change; (iii) analyze the factors on how the company arrived at material estimates including how the estimates or assumptions have changed in the past and is reasonably likely to change in the future; and (iv) analyze the specific sensitivity to change of your critical accounting estimates or assumptions based on other outcomes with quantitative and qualitative disclosure, as necessary. Refer to the guidance in Section V of FRR-72 (Release No. 33-8350) and please revise in future filings accordingly. |

RESPONSE: In an effort to improve the Company’s disclosure regarding its critical accounting policies, the Company will endeavor to address the areas listed above in its Annual Report on Form 10-K for the year ended December 31, 2010, which the Company expects to file no later than March 31, 2011.

Financial Statements, page F-I

Report of Independent Registered Public Accounting Firm, page F-2

| 4. | We note from the report of the independent registered public accounting firm that the independent registered public accounting firm conducts its operations from Skillman, New Jersey. We also note from the discussion contained throughout the filing that the company's operations are conducted in China. Given that the company's operations are conducted entirely in China, it is unclear if the independent registered public accounting firm performed the audit of the company's financial statements using its own employees or whether it relied on the work of another firm or by using the work of assistants engaged from outside of the firm. Please tell us whether the audit of the company's financial statements was completed by personnel from the firm Li & Company, PC or by using the work of other auditors or outside assistants. Furthermore, if the audit was completed using the work of other auditors or outside assistants, please explain how the independent registered accounting firm complied with the guidance outlined in Staff Audit Practice Alert No.6 issued by the Public Company Accounting Oversight Board on July 12, 2010. We may have further comment upon receipt of your response. |

RESPONSE: The Company’s independent registered public accounting firm, Li & Company, PC, performed the audit of the Company’s financial statements using its own employees and the audit of the Company's financial statements was completed by personnel from the firm Li & Company, PC. Li & Company’s personnel performed all of the audit fieldwork and audit procedures at the Company’s premises in China from February 21, 2010 through March 15, 2010. Li & Company did not utilize the services of any other auditors or outside assistants in performing the audits of the Company’s financial statements.

Consolidated Statements of Income and Comprehensive Income, page F-4

| 5. | Please tell us the nature of the line item "Gain from contracts termination." Your response should include the nature of the contract terminated and the calculation of the gain recognized of $1.2 million. |

RESPONSE: This item pertains to a contract for the sale of laterite-nickel ore that was entered into in June 2007 between Henan Armco, a subsidiary of the Company, and Sichuan Xinhe (“Xinhe”). A dispute arose between the two parties regarding the percentage of nickel content of the goods delivered relative to the percentage specified in the contract, with Xinhe refusing to take delivery of the goods. On November 6, 2007 Henan Armco filed a lawsuit against Xinhe. On February 15, 2008, under court mediation, both parties reached a settlement of RMB 8 million (equivalent to $1,151,453) of compensatory damages from Xinhe to Henan Armco, which was comprised of (i) forfeiture of the RMB 4 million deposit made by Xinhe per the original contract and (ii) RMB4 million to be paid by Xinhe. The Company recognized the entire balance of RMB8 million ($1,151,453) as a gain from contract termination upon receipt of the RMB 4 million in 2008.

- 2 -

Consolidated Statement of Stockholders' Equity, page F-5

| 6. | We note the column "Deferred Compensation" on your Consolidated Statement of Stockholders' Equity. Please note that under upon adoption of the updated accounting guidance in ASC Topic 718, deferred compensation accounts were to be eliminated against the appropriate equity accounts, generally paid-in-capital, and no longer used. Please revise your statement of stockholders' equity in future filings to eliminate deferred compensation from your statement of stockholders' equity and record such transactions in additional paid in capital. |

RESPONSE: The Company acknowledges the staff’s comment and will revise its future filings accordingly.

Notes to the Consolidated Financial Statements, page F-7

Note 1 - Organization and Operations, page F-7

Merger of Armco & Metawise (H.K) Ltd. and Subsidiaries ("Armco"), page F-7

| 7. | We note that the company has accounted for the June 27, 2008 transaction as a reverse acquisition. We further note that the company simultaneously acquired Armco & Metawise. In this regard, please clarify the following for us: |

| • | Tell us the amount of shares of the company that were issued to the former owner of Cox in exchange for the outstanding shares of Cox, including the amount of Cox shares; |

| • | Explain in further detail how the company accounted for the issuance of the option to Ms. Gao on June 27,2008, entitling Ms. Gao to exercise the option for 5,300,000 shares at an exercise price of $1.30 per share of the new company's stock and 2,000,000 shares at an exercise price of $5 per share; and |

| • | Further explain the cancellation of shares related to the fertilizer business on December 30, 2008, including to whom the fertilizer business was sold, any proceeds received from the sale, including any gain or loss recognized on the sale and any consideration paid for the cancellation of the shares, if applicable. |

RESPONSE: No shares of the Company’s common stock, or other securities, were issued to Stephen Cox, the former majority shareholder and founder of the Company. There were 10,000,000 shares of Cox common stock issued and outstanding prior to the reverse acquisition, 7,694,000 of which were cancelled, and 2,306,000 shares were retained by the former shareholders of Cox Distributing subsequent to the June 27, 2008 purchase of Armco. Of this amount, 6,200 shares were owned by Mr. Cox, as disclosed in the Company’s Form 8-K filed with the Commission on July 1, 2008.

The Company accounted for the issuance of both options to Ms. Gao as a reverse acquisition and recapitalization. The terms of the option for 5,300,000 shares allowed the Company, upon five days prior written notice, to demand that the holder of the option purchase all or part of the shares subject to the option in the event the option was not exercised. Prior to the acquisition of Armco, Cox had minimal cash and net assets and had no capability of satisfying the $6,890,000 promissory note issued to Ms. Gao in cash. On August 12, 2008, Ms. Gao exercised her option to purchase the 5,300,000 shares of common stock and cancelled the June 25, 2008 Promissory Note in the principal amount of $6,890,000 in payment of the purchase of the 5,300,000 shares. The 5,300,000 shares issued represented approximately 69.7% (5,300,000/(5,300,000+(10,000,000-7,694,000))) of the issued and outstanding common stock immediately after the consummation of the reverse acquisition and exercise of the option to purchase 5,300,000 shares of the Company’s common stock at $1.30 per share, resulting in a change in control of the Company.

On December 30, 2008, the Company sold all of the assets of its fertilizer business to Mr. Stephen E. Cox in exchange for 6,200 shares of the Company’s common stock owned by Mr. Cox and his agreement to assume all the liabilities associated with the business. Upon closing of the sale, the Company cancelled the 6,200 shares of its stock and recognized a gain of $61,514 from disposal of the fertilizer business.

Note 2 - Summary of Significant Accounting Policies, page F-8

Stock-based compensation for obtaining employee services, page F-12

| 8. | We note that a volatility of 0% was used in the valuation of stock options granted to employees. Please tell us why you believe using a volatility of 0% is appropriate given the lack of trading history of the company. Refer to SAB Topic 14D, question 6 and advise. |

RESPONSE: A volatility of 0% was inadvertently used in the valuation of stock options granted to Ms. Feng Gao in connection with the Company’s acquisition of Armco. Volatility should have been 89% using the historical volatility of 14 comparable companies in the metal/industrial metals industries. Because the Company did not record the fair value of the options granted Ms. Gao as the options were included as part of the reverse acquisition and recapitalization, the volatility attributable to the Company’s common stock did not have an effect on the Company’s consolidated financial statements for fiscal 2009 or fiscal 2010. The Company also notes that no stock options were granted to employees during fiscal 2009 and fiscal 2010.

- 3 -

Note 12 - Stockholders' Equity, page F-29 Stock Options, page F-30

| 9. | Your disclosure indicates that the fair value of the stock option granted to Ms. Gao during 2008 was zero and as such, although fully vested, no compensation cost was recognized. In this regard, please provide us with your calculation of the option's fair value at issuance, including all relevant facts and assumptions used in the calculation which support your conclusion that the stock options to purchase shares of your common stock should be assigned no value. We may have further comment upon receipt of your response. |

RESPONSE: The fair value of the June 27, 2008 option to purchase 2 million common shares exercisable at $5.00 per share vested upon issuance was approximately $435,000, using the Black-Scholes option-pricing model with the following assumptions:

Expected option life (year) | 2.00 | |||

Expected volatility | 89.00% | |||

Risk-free interest rate | 2.65% | |||

Dividend yield | 0.00% |

The Company concluded that no compensation expense should be recognized for the issuance of this option since it was granted as part of the terms of the reverse acquisition.

Form 8-K filed May 17, 2010

| 10. | Item 2.02 of Form 8-K and Item 10(e)(l)(i) of Regulation S-K requires that whenever one or more non-GAAP financial measures are included in a filing with the Commission the registrant must include a presentation, with equal or greater prominence, of the most directly comparable financial measure or measures calculated and presented in accordance with generally accepted accounting principles. Given that your non-GAAP net income and non-GAAP earnings per share are disclosed prior to the corresponding GAAP amounts in both the "Financial Highlights" and "First Quarter 2010 Financial Results" section, we believe the non-GAAP measures have been given greater prominence. Please revise future filings to present the equivalent GAAP measure with equal or greater prominence. |

RESPONSE: The Company acknowledges the staff’s comment and will ensure that the GAAP financial measurements are given equal or greater prominence than the corresponding or related non-GAAP financial measurements in future filings, in accordance with Regulation S-K.

Quarterly Report on Form 10-Q for the quarter ended June 30, 2010

Financial Statements, page 1

Consolidated Statements of Cash Flows, page 4

| 11. | We refer to the line item "Change in fair value of derivative liability" in the amount of $(610,127) for the six months ended June 30, 2010. Please reconcile this amount with the $(106,127) reported in the consolidated statements of income on page 3 for the "loss (gain) on change in fair value of derivative liability." Similarly reconcile the difference contained in the financial statements for the quarter ended March 31, 2010. |

RESPONSE: The line item "Change in fair value of derivative liability" contained in the consolidated statements of cash flows should have been ($106,127) for the six months ended June 30, 2010, the same amount reported in the consolidated statements of income for the "loss (gain) on change in fair value of derivative liability." The amount reflected in the consolidated statements of cash flows as filed incorrectly included an adjustment to financing activities of $500,000 related to the exercise of warrants to purchase the Company’s common stock and $4,000 related to stock based compensation. The effect of this error was to understate cash provided by operating activities and overstate cash provided by financing activities by $500,000 in the consolidated statements of cash flows for the six months ended June 30, 2010. The Company does not believe that it is necessary to amend its Quarterly Report for the period ended June 30, 2010 as management believes these misstatements are immaterial and have no impact to the Company’s liquidity, financial condition or results of operations.

- 4 -

With respect to the differences contained in the financial statements for the quarter ended March 31, 2010, the Company inadvertently filed a draft consolidated statement of cash flows for the three months ended March 31, 2010 during the EDGAR preparation process. Attached to this letter as Exhibit A is the correct consolidated statement of cash flows for the period that should have been filed. There is no difference between the amount reported in the consolidated statements of income for the loss (gain) on change in fair value of derivative liability and the corresponding amount contained in the final consolidated statements of cash flows attached as Exhibit A. The Company will amend its quarterly report on Form 10-Q for the three months ended March 31, 2010 to include the final consolidated statement of cash flows for the quarter then ended which is attached to this letter.

Consolidated Statements of Stockholders' Equity

| 12. | We note from your disclosures contained the notes to the consolidated financial statements numerous transactions and issuances of equity instruments during fiscal 2010 which impacted shareholder's equity, for example, the sale of your common stock and related issuance of warrants in April 2010; issuance of common stock for consulting services; proceeds received from exercises of warrants and stock options; issuance of common stock for loan guarantee in June 2010; and extinguishment of derivative warrant liability. In light of the significant activity, please provide us with your statements' of stockholders' equity in your next response to us. Furthermore, in order to better provide investors with a clear understanding of the transactions effecting shareholders' equity, we believe you should also include a statements of stockholders' equity in future quarterly filings. Please confirm your understanding of this matter as part of your next response to us. |

RESPONSE: Included as Exhibit B of this letter is the Company’s Statement of Stockholders’ Equity for the nine months ended September 30, 2010. The Company also confirms its understanding of the staff’s comment and will include a Statement of Stockholders’ Equity in its future quarterly filings.

Notes to the Consolidated Financial Statements, page 5

Note 2 - Summary of Significant Accounting Policies, page 6

Property, Plant and Equipment, page 8

| 13. | Previously you included a footnote which reflected the various categories of property plant and equipment at each balance sheet date; however, we note that such footnote has been omitted from notes to the financial statements included in the Form 10-Q for the quarter ended June 30, 2010. Given the significant additions that have been made during fiscal 2010 and the quarter ended June 30. 2010, we believe such information is important to investors especially in light of the fact that the scrap metal recycling facility became operational during the second quarter of fiscal 2010 for which the balance of your construction in progress was attributed. In this regard, please provide us with a breakdown of the various categories of property, plant, and equipment as of your most recent balance sheet date and revise future filings, accordingly. As part of your response and revised disclosure, please provide the estimated useful lives of property plant and equipment by category. Also, please tell us and revise MD&A to disclose where depreciation expense is being recorded within the statements of operations as it is unclear from your current disclosures. |

RESPONSE: The Company’s property, plant and equipment as of September 30, 2010 is comprised of the following:

| Estimated Useful Life (Years) | ||||||||

| Buildings and leasehold improvements | 20 | $ | 442,429 | |||||

| Construction in progress | 21,158,011 | |||||||

| Machinery and equipment | 7 | 10,760,649 | ||||||

| Vehicles | 5 | 301,013 | ||||||

| Office equipment | 5-8 | 433,744 | ||||||

| 33,095,846 | ||||||||

| Less: accumulated depreciation | (354,306 | ) | ||||||

| 32,741,540 | ||||||||

- 5 -

Depreciation expense is included in general and administrative expenses. The Company confirms that it will revise its future filings to include the breakdown of property, plant and equipment by category in the notes to the financial statements and will disclose in its MD&A where depreciation expense is recorded in its statement of operations.

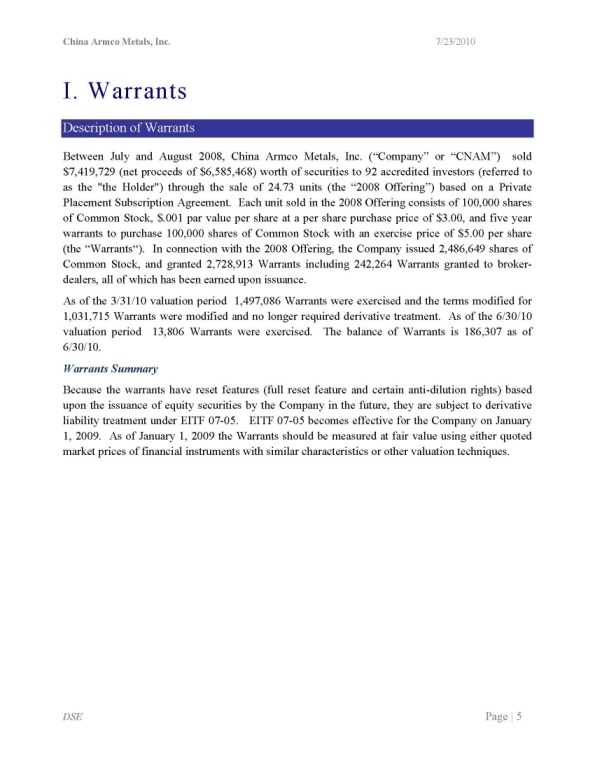

Note 6 - Instruments and Fair Value of Financial Instruments, page 19 (in Warrants issued in April 2010. page 20)

Derivative Analysis, page 21

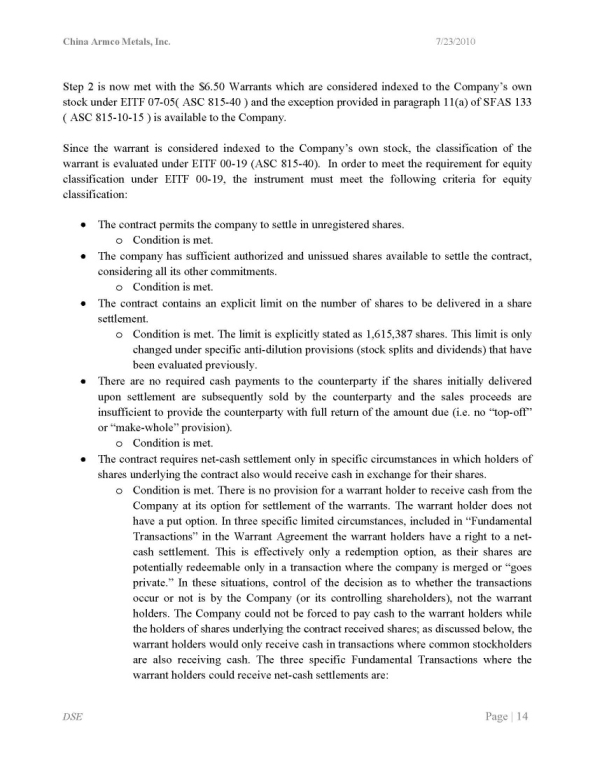

| 14. | We note your disclosure that the derivatives issued in April 2010 meet the requirements of ASC 815-40 for equity classification. Please provide us with your analysis. |

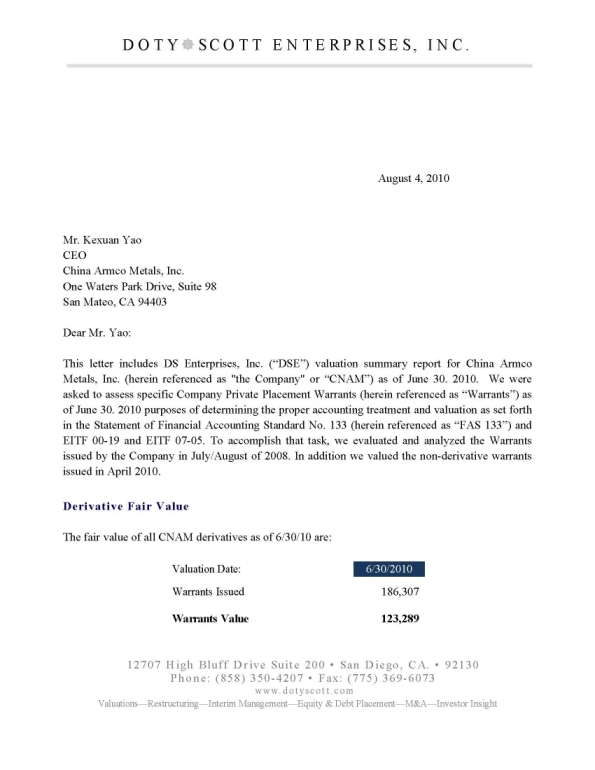

RESPONSE: Attached as Exhibit C is the report of the Company’s third party valuation specialist covering all of the Company’s warrants outstanding as of June 30, 2010. Exhibit A of the valuation report evaluates the warrants that were issued in April of 2010 to determine if they meet the requirements of ASC 815-40 for equity classification.

Note 7 - Stockholders' Equity, page 22

Sale of common stock, page 22

| 15. | Please reconcile for us the gross proceeds and expenses from the April 2010 stock issuance to the amount reflected on the cash flow statement of $9,112,973 for the issuance of common stock and warrants. |

RESPONSE: On April 20, 2010, the Company issued 1,538,464 shares of its common stock and warrants to purchase an additional 1,538,464 shares of its common stock for total gross proceeds of $10,000,016. In connection with this offering, the Company paid $499,987 to the placement agent, Rodman & Renshaw, LLC, and paid $300,000 to China Direct Investments, Inc. for professional services pertaining to this transaction. In addition, the Company incurred legal fees in the amount of $83,556 and escrow fees in the amount of $3,500. As a result, the net cash proceeds to the Company from this offering were $9,112,973.

Issuance of common stock for services, page 22

| 16. | We note that you issued 80,000 shares of common stock to China Direct Investments as consideration for management and accounting consulting services for the period beginning January 1. 2010 through December 31, 2010. We also note that you indicate there is no performance commitment at the date of the agreement and that you are using the date(s) at which performance is complete as the measurement dates(s). In this regard, please provide us with the pertinent terms of the arrangement, including whether the shares of common stock issued to China Direct Investments are fully vested and/or non-forfeitable. If such shares are fully vested and non-forfeitable, please tell us how your accounting treatment complies with the guidance prescribed in ASC 505-50-25-7. |

RESPONSE: Under the terms of the agreement with China Direct Investments, Inc., 25% of the shares issued were earned by China Direct Investments for the services provided during each of the three month periods ended March 31, 2010, June 30, 2010, September 30, 2010 and December 31, 2010. China Direct Investments had the right to terminate the agreement at any time by providing the Company with 30 days prior written notice, and the Company had the right to terminate the agreement in the event of a material breach of the agreement by China Direct Investments, subject to a 30 day cure period. In the event the agreement were terminated either by the Company or by China Direct Investments, China Direct Investments would have been required to return to the Company all unearned consulting fees as of the date of termination. As a result, the shares issued to China Direct Investments on February 5, 2010 were not fully vested and were forfeitable.

- 6 -

| 17. | Notwithstanding the above, please tell us how you determined the value of $5.48 per share used in calculating consulting expense associated with the shares earned for the quarter ended March 31, 2010. We note that you have also recorded deferred compensation of $563,400 representing the 60,000 shares of common stock at $9.39 per share that were unearned at March 31, 2010. Please tell us why you believe such treatment is appropriate and explain why it appears no amounts were recognized as consulting expense during the quarter ended June 30, 2010. As part of your response, please provide us with the accounting guidance you relied upon in determining your treatment. Please note that your presentation of deferred compensation within shareholders' equity does not appear to comply with the guidance prescribed in ASC 505-50-45-1. Please advise or revise your presentation accordingly. We may have further comment upon receipt of your response. |

RESPONSE: The value of $5.48 per share was determined using the average daily closing price of the Company's common stock for the period from January 1, 2010 through March 31, 2010. Although the Company failed to update the disclosure in Note 7, consulting expense in the amount of $104,200 was recorded for the quarter ended June 30, 2010 for the shares earned during the period. This amount was based on the average daily closing price of the Company’s common stock for the three months ended June 30, 2010 and applying the remeasurement provisions of ASC 505-50-55-31/32 where there is no performance commitment before the completion of performance and all terms are known up front.

The Company also acknowledges the staff’s comment regarding the presentation of deferred compensation within shareholders’ equity and will ensure that all future filings, both in the statement of stockholders’ equity and in notes to the financial statements, give effect to the current guidance as set forth in ASC 505 and ASC 718.

Quarterly Report on Form 10-0 for the Quarter ended September 30.2010

Notes to the Consolidated Financial Statements (Unaudited), page 4

Note 2 - Summary of Significant Accounting Policies, page 5

Investments, page 6

| 18. | Please tell us what accounting consideration was given to the stock options granted to you to purchase an additional five million shares of Apollo Mineral common stock as part of your purchase of the 19.9% equity interest in Apollo Minerals. Your response to us should include the value assigned to such options, if any, or if no value was assigned, please explain why. |

RESPONSE: The Company did not assign any value to the options to purchase an additional five million shares of Apollo Minerals common stock as these options may only be exercised in order for the Company to maintain its 19.9% stake in the investee should it issue additional common shares in the future. The Company also believes that any value that would be assigned to the options would not change the overall accounting for the purchase of Apollo Minerals equity securities as a cost method investment.

| 19. | Furthermore, reference is made to the third paragraph on page 7 with respect to the off-take rights the company will obtain from Apollo Minerals upon completion of all regulatory approvals. Please provide us with an update on the current status of regulatory approvals. Also, tell us your planned accounting treatment the off-take rights, including what value, if any, will be assigned to such rights, or if no value will be assigned, please explain why. Please include the authoritative accounting literature that supports your basis for your conclusions as part of your next response to us. |

RESPONSE: Apollo Minerals has obtained shareholder and regulatory approval of the off-take rights to allow the Company to purchase no less than 15% of the iron ore production from Apollo Minerals’ Mount Oscar Mining Project at market rates. Since the Company will purchase the iron ore production at market rates, the future iron ore transactions between Apollo Minerals and the Company would be considered arms’ length transactions. As a result, although the off-take rights meet the contractual-legal criterion for a separately identifiable intangible asset as described in ASC 805, these rights do not contain any terms that are favorable relative to market terms, therefore the Company believes that no value should be assigned to the off-take rights.

- 7 -

Exhibits 31.1 and 31.2

| 20. | Please confirm that in future filings you will remove the words "nine months" from your certification required by Rule 13a-14(a) of the Exchange Act. |

RESPONSE: The Company confirms that in future filings the certification required by Rule 13a-14(a) of the Exchange Act will not contain the words “nine months.”

The Company acknowledges that:

| • | the Company is responsible for the adequacy and accuracy of the disclosure in their filings; |

| • | staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| • | the Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

The Company trusts the foregoing sufficient responds to the staff’s comments.

| Sincerely, | |

| /s/ James M. Schneider | |

| James M. Schneider |

| cc: | Mr. Kexuan Yao, CEO |

Li & Company, PC

- 8 -

EXHIBIT A

CHINA ARMCO METALS, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

| For the Three Months Ended | For the Three Months Ended | |||||||

| March 31, 2010 | March 31, 2009 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

Net income (loss) | $ | 53,224 | $ | 297,462 | ||||

Adjustments to reconcile net income (loss) to net cash | ||||||||

provided by (used in) operating activities | ||||||||

Depreciation expense | 24,415 | 18,033 | ||||||

Amortization expense | 11,482 | 39,648 | ||||||

Change in fair value of derivative liability | 321,754 | (169,826) | ||||||

Stock based compensation | 169,494 | - | ||||||

Changes in operating assets and liabilities: | ||||||||

Accounts receivable | 14,986,098 | 1,907,901 | ||||||

Inventories | 458,375 | (1,623,282) | ||||||

Advance on purchases | 422,443 | 352,071 | ||||||

Prepayments and other current assets | (2,503,657) | 82,565 | ||||||

Accounts payable | 640,907 | 5,274,564 | ||||||

Customer deposits | 467,609 | (521,128) | ||||||

Taxes payable | (846,233) | (263,217) | ||||||

Accrued expenses and other current liabilities | 1,256,788 | (244,474) | ||||||

NET CASH PROVIDED BY OPERATING ACTIVITIES | 15,462,699 | 5,150,317 | ||||||

CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

Proceeds from release of pledged deposits | 564,495 | - | ||||||

Payment made towards pledged deposits | - | (2,943,372) | ||||||

Purchases of property and equipment | (5,536,245) | (1,065,260) | ||||||

NET CASH USED IN INVESTING ACTIVITIES | (4,971,750) | (4,008,632) | ||||||

CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

Repayment of loans payable | (17,022,321) | - | ||||||

Proceeds from long-term debt | 1,462,822 | (2,914,345) | ||||||

Amounts received from (paid to) related parties | 1,835,137 | (196,973) | ||||||

Exercise of warrants | 6,621,652 | 25,000 | ||||||

NET CASH USED IN FINANCING ACTIVITIES | (7,102,710) | (3,086,318) | ||||||

EFFECT OF EXCHANGE RATE CHANGES ON CASH | (6,958) | 5,693 | ||||||

NET CHANGE IN CASH | 3,381,281 | (1,938,940) | ||||||

Cash at beginning of period | 743,810 | 3,253,563 | ||||||

Cash at end of period | $ | 4,125,091 | $ | 1,314,623 | ||||

SUPPLEMENTAL DISCLOSURE OF CASH FLOWS INFORMATION: | ||||||||

Interest paid | $ | 338,133 | $ | 18,036 | ||||

Taxes paid | $ | 974,865 | $ | - | ||||

EXHIBIT B

China Armco Metals, Inc. and Subsidiaries

Consolidated Statement of Stockholders’ Equity (Unaudited)

For the Nine Months Ended September 30, 2010

| Common Stock, $0.001 Par Value | ||||||||||||||||||||||||

| Number of Shares | Amount | Additional Paid-in Capital | Retained Earnings | Accumulated Other | Total Stockholders' Equity | |||||||||||||||||||

| Balance, December 31, 2009 | 10,310,699 | $ | 10,310 | $ | 1,880,466 | $ | 14,936,915 | $ | 297,681 | $ | 17,125,372 | |||||||||||||

| Issuance of common stock upon exercise of warrants to purchase 1,324,346 common shares at $5.00 per share for the three-month period ending March 31, 2010 | 1,324,346 | 1,325 | 6,620,405 | 6,621,730 | ||||||||||||||||||||

| Issuance of 78,217 common shares upon cashless exercise of warrants to purchase 167,740 common shares at $5.00 per share for the three-month period ending March 31, 2010 | 78,217 | 78 | (78 | ) | - | |||||||||||||||||||

| Extinguishment of derivative liability associated with the exercise of warrants to purchase common stock for the three-month period ending March 31, 2010 | 1,875,107 | 1,875,107 | ||||||||||||||||||||||

| Reclassification of derivative liability to additional paid-in capital associated with the waiver of anti-dilution provision of warrants to purchase 1,074,048 common shares | 1,292,227 | 1,292,227 | ||||||||||||||||||||||

| Issuance of common stock upon exercise of warrants to purchase 13,806 common shares at $5.00 per share for the three-month period ending June 30, 2010 | 13,806 | 14 | 69,016 | 69,030 | ||||||||||||||||||||

| Reclassification of derivative liability to additional paid-in capital associated with the exercise of warrants to purchase 13,806 common shares | 21,229 | 21,229 | ||||||||||||||||||||||

| Sale of common stock and warrants at $6.50 per unit on April 20, 2010 | 1,538,464 | 1,538 | 9,111,435 | 9,112,973 | ||||||||||||||||||||

| Issuance of common stock upon exercise of options to purchase 1,400,000 common shares at $5.00 per share for the three-month period ending June 30, 2010 | 1,400,000 | 1,400 | 6,998,600 | 7,000,000 | ||||||||||||||||||||

| Issuance of common stock to China Direct Industries, Inc. for consulting services | 80,000 | 80 | 283,542 | 283,622 | ||||||||||||||||||||

| Issuance of common stock to Bespoke for consulting services | 22,500 | 23 | 78,502 | 78,525 | ||||||||||||||||||||

| Issuance of common stock to Chaoyang Steel for loan guarantee services | 500,000 | 500 | 124,832 | 125,332 | ||||||||||||||||||||

| Stock-based compensation expense | 179,370 | 179,370 | ||||||||||||||||||||||

| Issuance of restricted stock to Director pursuant to 2009 Stock Incentive Plan for future services valued at $3.28 per share granted on September 16, 2010 | 6,250 | 6 | (6 | ) | - | |||||||||||||||||||

| Net loss | (594,102 | ) | (594,102 | ) | ||||||||||||||||||||

| Foreign currency translation gain | 790,597 | 790,597 | ||||||||||||||||||||||

| Balance, September 30, 2010 | 15,274,282 | $ | 15,274 | $ | 28,534,647 | $ | 14,342,813 | $ | 1,088,278 | $ | 43,981,012 | |||||||||||||

EXHIBIT C