American Realty Capital Trust, Inc. 2nd Quarter 2012 Shareholder Letter & Subsequent Events

2nd Quarter 2012 Shareholder Letter & Subsequent Events Dear Shareholder: I could not be more pleased with the company's performance these last three months. Since listing our shares on the NASDAQ on March 1, 2012, American Realty Capital Trust (NASDAQ: ARCT) has outperformed the broader equities market, reaffirmed its earnings guidance, announced a dividend increase, confirmed its acquisition program by placing $64 million of property purchases under contract consistent with its investment strategy, and demonstrated continued improvements in its overall balance sheet metrics. We have solidified our financial position and have embarked on the next phase of our value creation strategy. Let's take a closer look at what this means to you. Market Performance Economic uncertainty and global distress contributed to the broader equity market's underperformance in the second quarter. During this time, many investors fled the traded markets in favor of yield-rich investments like real estate investment trusts (REITs). While the S&P 500 was down almost three percent for the quarter, REITs were up approximately four percent, outperforming the broader equity market by 700 basis points. Triple net REITs gained 100 basis points above the REIT index, likely due to the lower perceived risk associated with net lease real estate and predictable dividends. You will be pleased to know that we have posted even stronger results for the quarter, up over eight percent, outperforming an index of triple net REITs on a total return basis by almost four percentage points. (See Exhibit A.) Exhibit A ARCT - Total Return Q2 2012 Property Portfolio Highlights As of June 30, 2012, we owned a portfolio of 486 properties, or a total of 15.6 million square feet in 43 states plus Puerto Rico. Our property portfolio is comprised of high quality corporate credit tenants, and today boasts almost 75 percent investment grade tenancy as measured by annualized rents. This percentage Exhibit B* Tenant Diversification Top 25 Tenants (by Revenue) Tenant % of GAAP Rent Cumulative Tenant FedEx 16.8% 16.8% Walgreens 10.0% 26.8% CVS 6.6% 33.4% GSA 4.6% 38.0% Dollar General 3.5% 41.5% Bridgestone Firestone 3.1% 44.6% Express Scripts 2.7% 47.3% Payless Shoe Source 2.4% 49.7% PetSmart 2.1% 51.8% PNC Bank 2.1% 53.9% IHOP 2.0% 55.9% Whirlpool 1.9% 57.8% 3M 1.9% 59.7% Reliant Healthcare 1.9% 61.6% Tractor Supply Co 1.9% 63.5% First Niagara Bank 1.8% 65.3% Home Depot 1.6% 66.9% Royal Ahold 1.6% 68.5% Reckitt Benckiser 1.5% 70.0% Rockland Trust 1.5% 71.5% Texas Instruments 1.5% 73.0% Brown Shoe Co 1.4% 74.4% Kum & Go 1.4% 75.8% Bojangles 1.3% 77.1% Aaron's 1.3% 78.4% Exhibit C* Industry Diversity / 20 Distinct Industries Consumer Goods 1.1% Consumer Products 3.4% Discount Retail 5.8% Gas/Convenience 2.5% Financial Services 1.1% Government Services 4.6% Healthcare 7.9% Home Maintenance 2.6% Manufacturing 5.6% Auto Services 4.1% Technology 1.5% Supermarket 2.5% Specialty Retail 9.5% Retail Banking 6.5% Restaurant 4.3% Aerospace 0.6% Telecommunications 0.6% Auto Retail 1.6% Freight 16.9% Pharmacy 17.4% American Realty Capital Trust, Inc. American Realty Capital Trust, Inc. 405 Park Avenue 14th Floor New York, NY 10022 www.arctreit.com (10.0%) (5.0%) 0.0% 5.0% 10.0% 15.0% Percentage (%) Change ARCT - Total Return Q2 2012 ARCT Triple Net REITs MSCI US REIT (RMS) S&P 500 Source: Bloomberg (Past performance is not indicative of future results.) ARCT Triple Net REITs MSCI U.S. REIT (RMS) S&P 500 * Based on data as of June 30, 2012. Percentages by revenue. 8.10% 4.79% 3.75% -2.75% American Realty Capital Trust, Inc. 405 Park Avenue 14th Floor New York, NY 10022 www.arctreit.com

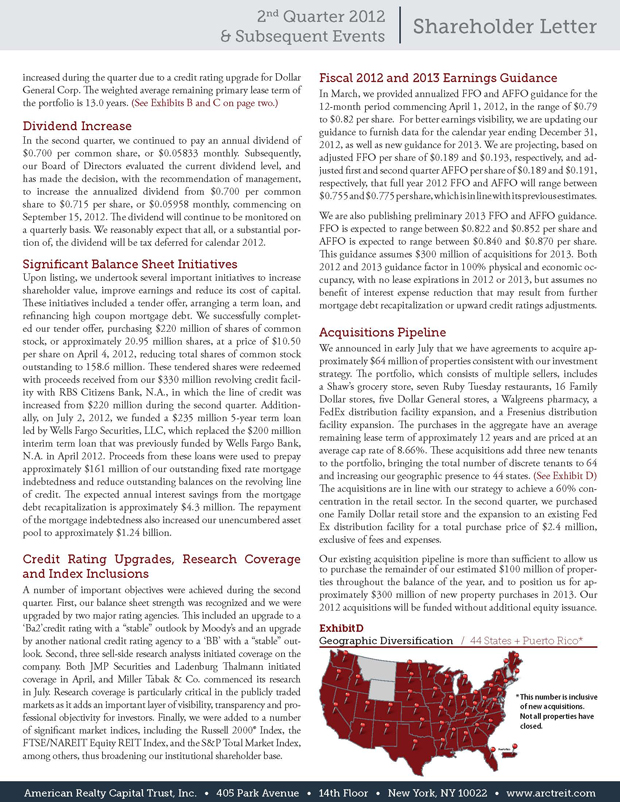

2nd Quarter 2012 Shareholder Letter & Subsequent Events increased during the quarter due to a credit rating upgrade for Dollar General Corp. The weighted average remaining primary lease term of the portfolio is 13.0 years. (See Exhibits B and C on page two.) Dividend Increase In the second quarter, we continued to pay an annual dividend of $0.700 per common share, or $0.05833 monthly. Subsequently, our Board of Directors evaluated the current dividend level, and has made the decision, with the recommendation of management, to increase the annualized dividend from $0.700 per common share to $0.715 per share, or $0.05958 monthly, commencing on September 15, 2012. The dividend will continue to be monitored on a quarterly basis. We reasonably expect that all, or a substantial portion of, the dividend will be tax deferred for calendar 2012. Significant Balance Sheet Initiatives Upon listing, we undertook several important initiatives to increase shareholder value, improve earnings and reduce its cost of capital. These initiatives included a tender offer, arranging a term loan, and refinancing high coupon mortgage debt. We successfully completed our tender offer, purchasing $220 million of shares of common stock, or approximately 20.95 million shares, at a price of $10.50 per share on April 4, 2012, reducing total shares of common stock outstanding to 158.6 million. These tendered shares were redeemed with proceeds received from our $330 million revolving credit facility with RBS Citizens Bank, N.A., in which the line of credit was increased from $220 million during the second quarter. Additionally, on July 2, 2012, we funded a $235 million 5-year term loan led by Wells Fargo Securities, LLC, which replaced the $200 million interim term loan that was previously funded by Wells Fargo Bank, N.A. in April 2012. Proceeds from these loans were used to prepay approximately $161 million of our outstanding fixed rate mortgage indebtedness and reduce outstanding balances on the revolving line of credit. The expected annual interest savings from the mortgage debt recapitalization is approximately $4.3 million. The repayment of the mortgage indebtedness also increased our unencumbered asset pool to approximately $1.24 billion. Credit Rating Upgrades, Research Coverage and Index Inclusions A number of important objectives were achieved during the second quarter. First, our balance sheet strength was recognized and we were upgraded by two major rating agencies. This included an upgrade to a 'Ba2'credit rating with a "stable" outlook by Moody's and an upgrade by another national credit rating agency to a 'BB' with a "stable" outlook. Second, three sell-side research analysts initiated coverage on the company. Both JMP Securities and Ladenburg Thalmann initiated coverage in April, and Miller Tabak & Co. commenced its research in July. Research coverage is particularly critical in the publicly traded markets as it adds an important layer of visibility, transparency and professional objectivity for investors. Finally, we were added to a number of significant market indices, including the Russell 2000 Index, the FTSE/NAREIT Equity REIT Index, and the S&P Total Market Index, among others, thus broadening our institutional shareholder base. Fiscal 2012 and 2013 Earnings Guidance In March, we provided annualized FFO and AFFO guidance for the 12-month period commencing April 1, 2012, in the range of $0.79 to $0.82 per share. For better earnings visibility, we are updating our guidance to furnish data for the calendar year ending December 31, 2012, as well as new guidance for 2013. We are projecting, based on adjusted FFO per share of $0.189 and $0.193, respectively, and adjusted first and second quarter AFFO per share of $0.189 and $0.191, respectively, that full year 2012 FFO and AFFO will range between $0.755 and $0.775 per share, which is in line with its previous estimates. We are also publishing preliminary 2013 FFO and AFFO guidance. FFO is expected to range between $0.822 and $0.852 per share and AFFO is expected to range between $0.840 and $0.870 per share. This guidance assumes $300 million of acquisitions for 2013. Both 2012 and 2013 guidance factor in 100% physical and economic occupancy, with no lease expirations in 2012 or 2013, but assumes no benefit of interest expense reduction that may result from further mortgage debt recapitalization or upward credit ratings adjustments. Acquisitions Pipeline We announced in early July that we have agreements to acquire approximately $64 million of properties consistent with our investment strategy. The portfolio, which consists of multiple sellers, includes a Shaw's grocery store, seven Ruby Tuesday restaurants, 16 Family Dollar stores, five Dollar General stores, a Walgreens pharmacy, a FedEx distribution facility expansion, and a Fresenius distribution facility expansion. The purchases in the aggregate have an average remaining lease term of approximately 12 years and are priced at an average cap rate of 8.66%. These acquisitions add three new tenants to the portfolio, bringing the total number of discrete tenants to 64 and increasing our geographic presence to 44 states. (See Exhibit D) The acquisitions are in line with our strategy to achieve a 60% concentration in the retail sector. In the second quarter, we purchased one Family Dollar retail store and the expansion to an existing Fed Ex distribution facility for a total purchase price of $2.4 million, exclusive of fees and expenses. Our existing acquisition pipeline is more than sufficient to allow us to purchase the remainder of our estimated $100 million of properties throughout the balance of the year, and to position us for approximately $300 million of new property purchases in 2013. Our 2012 acquisitions will be funded without additional equity issuance. ExhibitD Geographic Diversification / 44 States + Puerto Rico* Shareholder Letter American Realty Capital Trust, Inc. 405 Park Avenue 14th Floor New York, NY 10022 www.arctreit.com

Company Metrics: We believe that we have eff ectively created a defensive dividend stock that provides for infl ation protection and tax advantages. Portfolio Metrics (as of June 30, 2012) $2.6 Billion Est. Enterprise Value ($1.73 Billion Equity Market Cap) 486 Properties Owned 62 Tenants 5.3 Years Average Property Age 15.6 Million Square Feet 74.6% Rents from Investment Grade Credit Tenants No Material Lease Expirations Until 2018 13.0 Years Average Remaining Primary Lease Term $0.700 Per Share Annualized Distributions (Increased to $0.715 per share subsequent to the end of the quarter) Balance Sheet Metrics (as of June 30, 2012) 34.2% Net Debt to Enterprise Value 4.4 Years Average Remaining Debt Maturity 4.01% Weighted Average Interest Rate $330 Million Revolving Line of Credit (Libor Plus 2.05% to 2.85%) $235 Million Permenent Term Loan (Libor Plus 2.35%) Value Creation Going Forward We will continue to focus on maintaining portfolio quality, increasing earnings per share, reducing capital costs, achieving investment grade credit ratings and building our capacity to grow our dividend over time. Earnings growth will result from accretive acquisitions and contractual rent growth, which should allow us to increase distributable cash fl ow. By December 2012, we intend to purchase approximately $100 million of new properties net leased on a long-term basis to tenants with strong credit; of this amount, $64 million has already been placed under contract. Furthermore, we expect to enhance earnings by managing our balance sheet to reduce our cost of capital. In this regard, we continue to work closely with the ratings agencies to achieve an investment grade rating. Management's interests remain closely aligned with those of our shareholders, as a material portion of our compensation is tied directly to producing earnings growth, generating total shareholder return, and outperforming our peer group. In conclusion, we will diligently continue to carry out the game plan we have set for the company in our ongoing eff ort to maximize shareholder value. Management intends to build upon the company's previous successes and focus on asset and earnings growth consistent with our investment strategy and acquisition opportunities that are accretive to the dividend in an eff ort to www.arctreit.com This Is A Shareholder Communication. Not For Use As Sales Material improve shareholder returns. We continue to be very excited about our strong market position and compelling growth prospects, and we are grateful for your ongoing support. For more information on ARCT, please visit us at www.arctreit.com. To obtain our public fi lings, please refer to www.sec.gov. Do not hesitate to contact your fi nancial professional or our Investor Relations department at 646-937-6904 should you have additional questions. William M. Kahane Chief Executive cer