Exhibit 99

CAPE BANCORP

Market Focused Community Bank

Positioned for Growth

CAPE BANCORP

This presentation is for informational

purposes only and does not constitute an

offer to sell shares of common stock of

Cape Bancorp, Inc.

Please refer to the Prospectus dated

November 13, 2007 and the Prospectus

Supplement dated December 21, 2007

2

CAPE BANCORP

Forward-Looking Statements

Certain comments in this presentation are forward-looking statements, which can be identified by the use of such words as estimate, project, believe, intend, anticipate, plan, seek, expect and similar expressions. These forward-looking statements include, but are not limited to:

| • | | statements of our goals, intentions and expectations; |

| • | | statements regarding our business plans and prospects and growth and operating strategies; |

| • | | statements regarding the asset quality of our loan and investment portfolios; and |

| • | | estimates of our risks and future costs and benefits. |

These forward-looking statements are subject to significant risks, assumptions and uncertainties, including, among other things, the following important factors that could affect the actual outcome of future events:

| • | | significantly increased competition among depository and other financial institutions; |

| • | | inflation and changes in market interest rates that reduce our net interest margin or reduce the fair value of financial instruments; |

| • | | general economic conditions, either nationally or in our market area, that are worse than expected; |

| • | | adverse changes in the securities markets; |

| • | | legislative or regulatory changes that adversely affect our business; |

| • | | our ability to successfully integrate Boardwalk Bank; |

| • | | our ability to enter new markets successfully and take advantage of growth opportunities, and the possible short-term dilutive effect of potential acquisitions orde novobranches, if any; |

| • | | changes in management’s estimate of the adequacy of the allowance for loan and lease losses; |

| • | | effects of and changes in trade, monetary and fiscal policies and laws, including interest rate policies of the Federal Reserve Board; |

| • | | costs and effects of litigation and unexpected or adverse outcomes in such litigations; |

| • | | changes in consumer spending, borrowing and savings habits; |

| • | | changes in accounting policies and practices, as may be adopted by bank regulatory agencies and the Financial Accounting Standards Board; |

| • | | inability of third-party providers to perform their obligations to us; and |

| • | | changes in our organization, compensation and benefit plans. |

Because of these and other uncertainties, our actual future results may be materially different from the results indicated by these forward-looking statements.

Cape Bancorp, Inc. has filed a prospectus concerning the conversion with the Securities and Exchange Commission. Prospective purchasers of Cape Savings Bank are urged to read the prospectus because it contains important information. Prospective purchasers are able to obtain all documents filed with the SEC by Cape Bancorp, Inc. free of charge at the SEC’s website, www.sec.gov. In addition, documents filed with the SEC by Cape Bancorp, Inc. are available free of charge from the Corporate Secretary of Cape Bancorp, Inc. at 225 North Main Street, Cape May Court House, New Jersey 08210, telephone (800) 858-BANK. The directors, executive officers, and certain other members of management and the employees of Cape Bancorp, Inc. are participants in the solicitation of proxies in favor of the conversion from the mutual to stock form of ownership. Information about the directors and executive officers of Cape Bancorp, Inc. is included in the prospectus and the proxy statement/prospectus filed with the SEC.

The shares of common stock of Cape Bancorp, Inc. are not savings accounts or savings deposits, may lose value and are not insured by the Federal Deposit Insurance Corporation or any other government agency.

3

CAPE BANCORP

Offering Summary

| | |

| Issuer | | Cape Bancorp, Inc. |

| |

| Listing / Ticker | | Nasdaq Global Select Market / “CBNJ” |

| |

| Price Per Share | | $10.00 |

| |

| Gross Proceeds | | $78.2 Million - $92.0 Million(1) |

| |

| Shares Offered | | 7,820,000 - 9,200,000 shares(1) |

| |

| Shares Sold in Subscription & Community Offerings | | 2,750,000 shares |

| |

| Shares To Be Sold in Syndicated Offering | | 5,070,000 - 6,450,000 shares |

| |

| Shares Issued in the Merger | | 4,939,424 |

| |

| Pro Forma Shares Outstanding | | 13,306,824 - 14,783,424 shares(2) |

| |

| Pro Forma Market Value | | $133.1 Million - $147.8 Million(2) |

| |

Maximum Purchase Limits

(Individual / Group) | | $2.5 Million / $ 3.6 Million |

| |

| Selling Agent | | Stifel, Nicolaus & Company, Incorporated |

| |

| Expected Closing Date | | Late January 2008 |

| (1) | Range based on minimum through midpoint of the independent valuation appraisal. |

| (2) | Includes the shares to be issued to Boardwalk Bancorp shareholders and the contribution of 7% of the shares sold in the offering to our charitable foundation. |

4

CAPE BANCORP

Boardwalk Acquisition Overview

| | |

| Purchase Price per Share: | | $23.00 |

| |

| Aggregate Transaction Value: | | $101.0 million |

| |

| Form of Consideration: | | 50% common stock / 50% cash |

| |

| Exchange Ratio: | | Fixed at 2.3 shares of Cape Bancorp common stock |

| |

| Price / Book Value (1): | | 196.1% |

| |

| Price / Tangible Book Value (1): | | 196.1% |

| |

| Price / LTM EPS (1): | | 53.5x |

| |

| Board of Directors: | | Three directors from Boardwalk Bancorp (Michael D. Devlin, Agostino R. Fabietti and Thomas K. Ritter) will join both the Cape Bancorp and Cape Savings Bank Boards of Directors |

| |

| Structure: | | Boardwalk Bancorp will be merged with and into Cape Bancorp and Cape Savings Bank will acquire Boardwalk Bank by merging Boardwalk Bank with and into Cape Savings Bank |

| |

| Termination Fee: | | $5.0 million |

| (1) | At or for the 12 months ended June 30, 2007. |

5

CAPE BANCORP

Overview of the Simultaneous Structure

6

CAPE BANCORP

Rationale for the Conversion and Acquisition

| • | | Our primary reasons for this offering are to: |

| | • | | Raise capital to provide the stock and funds necessary to acquire Boardwalk Bancorp |

| | • | | Improve our overall competitive position |

| | • | | Provide us the flexibility to support our growth initiatives: |

| | • | | Organic growth initiatives through lending in communities we serve |

| | • | | Enhance our product and service offerings |

| | • | | Pursue limitedde novobranching opportunities and future acquisition opportunities |

| | • | | Additional size and scale provides opportunity for enhanced profitability and flexible capital management strategies |

| | • | | To retain and attract qualified personnel by establishing stock benefit plans for management and employees |

7

CAPE BANCORP

Corporate Overviews

Cape Savings Bank

| | • | | Organized in 1923 as a New Jersey-chartered mutual savings bank |

| | • | | Headquartered in Cape May Court House, New Jersey |

| | • | | Operate from 13-full service locations in Cape May and Atlantic Counties |

| | • | | Customers consist primarily of individuals and small businesses |

| | • | | Financial data as of September 30, 2007: |

| | | | |

• Assets | | – | | $620.1 million |

| | |

• Deposits | | – | | $489.6 million |

| | |

• Net Loans | | – | | $450.1 million |

| | |

• Equity | | – | | $72.7 million |

Boardwalk Bancorp

| | • | | Boardwalk Bancorp is the holding company for Boardwalk Bank, a New Jersey-chartered commercial bank chartered in 1999. |

| | • | | Headquartered in Linwood, New Jersey |

| | • | | Operate 7 full-service branch offices in Cape May and Atlantic Counties and an loan production office in Cumberland County |

| | • | | Customers consist primarily of small to medium-sized businesses and individuals |

| | • | | Financial data as of September 30, 2007: |

| | | | |

• Assets | | – | | $445.3 million |

| | |

• Deposits | | – | | $311.2 million |

| | |

• Net Loans | | – | | $298.1 million |

| | |

• Equity | | – | | $49.9 million |

8

CAPE BANCORP

Enhanced Franchise and Branch Footprint

| | |

| Combined Company* |

| Total Assets: | | $1.1 Billion |

| |

| Net Loans: | | $741.7 Million |

| |

| Total Deposits: | | $791.7 Million |

| |

| Total Equity: | | $181.9 Million |

| |

| Branches: | | 20 |

| * | At June 30, 2007 pro forma for the acquisition and offering assuming the minimum of the offering range. |

9

CAPE BANCORP

Pro Forma Market Share Analysis and Overview

| | | | | | | | |

| Atlantic County, NJ |

| Rank | | Institution (ST) | | Number

of

Branches | | Deposits in Market

($000) | | Market

Share

(%) |

| 1 | | Bank of America Corp. (NC) | | 14 | | 1,197,542 | | 25.29 |

| 2 | | Commerce Bancorp Inc. (NJ) | | 8 | | 1,047,505 | | 22.12 |

| | Pro Forma Company | | 10 | | 455,338 | | 9.62 |

| 3 | | Sun Bancorp Inc. (NJ) | | 10 | | 454,575 | | 9.60 |

| 4 | | Wachovia Corp. (NC) | | 9 | | 379,611 | | 8.02 |

| 5 | �� | Boardwalk Bancorp Inc. (NJ) | | 5 | | 289,331 | | 6.11 |

| 6 | | PNC Financial Services Group (PA) | | 8 | | 269,876 | | 5.70 |

| 7 | | Susquehanna Bancshares Inc. (PA) | | 6 | | 218,368 | | 4.61 |

| 8 | | Ocean Shore Holding Co. (MHC) (NJ) | | 6 | | 214,152 | | 4.52 |

| 9 | | Cape Savings Bank (NJ) | | 5 | | 166,007 | | 3.51 |

| 10 | | Absecon Bancorp (NJ) | | 4 | | 124,929 | | 2.64 |

| | Total For Institutions In Market | | 86 | | 4,735,370 | | |

|

| Cape May County, NJ |

| Rank | | Institution (ST) | | Number

of

Branches | | Deposits in Market

($000) | | Market

Share

(%) |

| 1 | | Sturdy Savings Bank (NJ) | | 7 | | 361,911 | | 14.40 |

| 2 | | Commerce Bancorp Inc. (NJ) | | 4 | | 348,746 | | 13.88 |

| | Pro Forma Company | | 10 | | 348,184 | | 13.85 |

| 3 | | PNC Financial Services Group (PA) | | 10 | | 312,634 | | 12.44 |

| 4 | | Cape Savings Bank (NJ) | | 8 | | 307,595 | | 12.24 |

| 5 | | Crest Savings Bancorp MHC (NJ) | | 8 | | 240,349 | | 9.56 |

| 6 | | Ocean Shore Holding Co. (MHC) (NJ) | | 2 | | 206,574 | | 8.22 |

| 7 | | Bank of America Corp. (NC) | | 8 | | 193,670 | | 7.71 |

| 8 | | Sun Bancorp Inc. (NJ) | | 7 | | 180,505 | | 7.18 |

| 9 | | Sea Isle Financial Corp. MHC (NJ) | | 3 | | 171,345 | | 6.82 |

| 10 | | Wachovia Corp. (NC) | | 1 | | 60,758 | | 2.42 |

| 11 | | Boardwalk Bancorp Inc. (NJ) | | 2 | | 40,589 | | 1.61 |

| | Total For Institutions In Market | | 65 | | 2,513,469 | | |

Demographically attractive market characteristics:

| | • | | 11% population growth in Atlantic County from 2000 to 2007 |

| | • | | 26% and 23% projected household income growth in Cape May and Atlantic Counties |

| | • | | Located within our primary market area is an important regional economic hub (Atlantic City) for individuals and businesses |

Economy characterized by:

| | • | | A variety of service businesses |

| | • | | Vacation-related businesses in the coastal areas |

| | • | | Commercial fishing and agriculture |

| | • | | Tourism centered around the gaming industry (Atlantic City) |

| * | Source: FDIC and ESRI. Deposit data as of June 30, 2007. |

10

CAPE BANCORP

Experienced Management Team

| | | | | | | | |

Executive Officer Team | | Age | | Position | | Years of Experience |

Herbert L. Hornsby, Jr. | | 58 | | President and Chief Executive Officer | | 34 |

Michael D. Devlin | | 57 | | Executive Vice President and Chief Operating Officer | | 32 |

Robert J. Boyer | | 55 | | Executive Vice President and Chief Financial Officer | | 34 |

Guy A. Deninger | | 59 | | Executive Vice President and Chief Lending Officer | | 40 |

| | | | |

Directors | | Age | | Position Held with Cape Savings Bank | | Director

Since | | Current Term

Expires |

Robert F. Garrett, III | | 69 | | Chairman | | 1974 | | 2009 |

Frank J. Glaser | | 59 | | Director | | 2006 | | 2010 |

Louis H. Griesbach, Jr. | | 70 | | Director | | 1977 | | 2008 |

Herbert L. Hornsby, Jr. | | 58 | | Director | | 1983 | | 2008 |

David C. Ingersoll, Jr. | | 60 | | Director | | 1977 | | 2010 |

Joanne D. Kay | | 62 | | Director | | 2002 | | 2008 |

Matthew J. Reynolds | | 36 | | Director | | 2004 | | 2009 |

| | |

Boardwalk Bancorp Directors to join Cape Bancorp/ Cape Savings Bank Board of Directors | | Term

Expires |

Thomas K. Ritter | | 2010 |

Michael D. Devlin | | 2009 |

Agostino R. Fabietti | | 2008 |

11

CAPE BANCORP

Post Conversion and Acquisition - Business Strategy

Our business strategy is to operate and grow a profitable community-oriented financial institution. We plan to achieve this by:

| • | | Pursuing new opportunities to increase commercial lending in our primary market area |

| • | | Maintain the high quality of our loan portfolio |

| • | | Continuing to originate residential mortgage loans in our primary market area |

| • | | Providing superior customer service with an emphasis on increasing transaction deposit accounts and deposit balances |

| • | | Increasing our non-interest income, through a broader range of products and services |

| • | | Expand our franchise through acquisitions, including our merger with Boardwalk Bancorp, and by opening additional branch offices in our primary market area |

12

CAPE BANCORP

Consistent Balance Sheet Growth

13

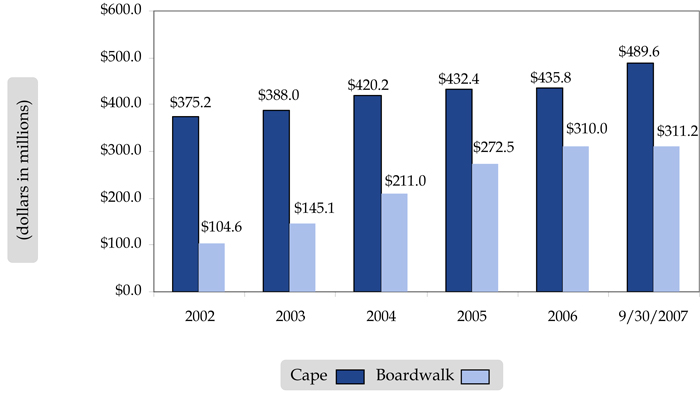

CAPE BANCORP

Strong Loan Growth

Since 2002, the loan portfolios have demonstrated strong growth primarily driven by commercial real estate and commercial loan growth. Boardwalk’s loan portfolio will be additive to our current strategy to increase our commercial lending initiative.

14

CAPE BANCORP

Increasing Emphasis on Commercial Lending

(Commercial & Commercial Real Estate)

Since 2002, the loan portfolio mix has continued to shift to more higher yielding commercial-based products.

15

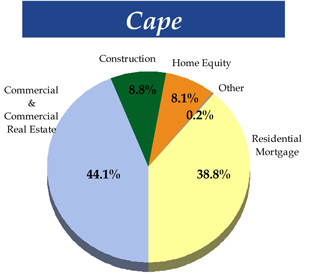

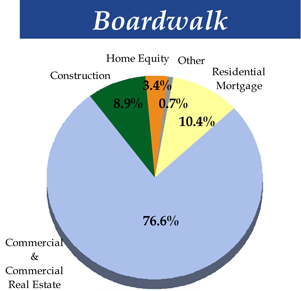

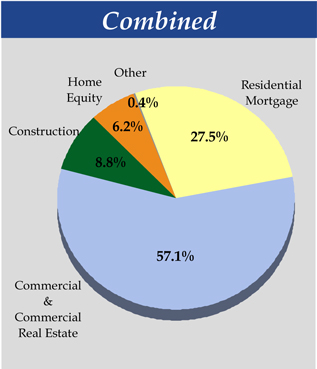

CAPE BANCORP

Loan Portfolio Composition

| • | | Majority of loan portfolio comprised of higher yielding commercial-based loans |

| • | | More diversified loan portfolio |

| • | | Additional commercial market expertise |

As of June 30, 2007.

16

CAPE BANCORP

Disciplined Credit Culture

Since 2002, both banks have maintained a conservative credit culture resulting in superior asset quality.

Cape

| | | | | | | | | | | | | | | | | | |

| | | 2002 | | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | 9/30/2007 | |

NPAs / Total Assets | | 0.31 | % | | 0.38 | % | | 0.23 | % | | 0.49 | % | | 0.62 | % | | 0.54 | % |

NPLs/ Total Loans | | 0.36 | % | | 0.55 | % | | 0.34 | % | | 0.68 | % | | 0.84 | % | | 0.74 | % |

Allowance/NPLs | | 190.20 | % | | 160.30 | % | | 289.86 | % | | 134.52 | % | | 105.20 | % | | 118.82 | % |

Allowance/Total Loans | | 0.69 | % | | 0.88 | % | | 0.98 | % | | 0.91 | % | | 0.89 | % | | 0.88 | % |

Boardwalk

| | | | | | | | | | | | | | | | | | |

| | | 2002 | | | 2003 | | | 2004 | | | 2005 | | | 2006 | | | 9/30/2007 | |

NPAs / Total Assets | | 0.51 | % | | 0.71 | % | | — | | | — | | | 0.11 | % | | 0.29 | % |

NPLs/ Total Loans | | 0.84 | % | | 1.32 | % | | — | | | — | | | 0.17 | % | | 0.43 | % |

Allowance/NPLs | | 184.32 | % | | 94.82 | % | | — | | | — | | | 681.88 | % | | 283.13 | % |

Allowance/Total Loans | | 1.55 | % | | 1.26 | % | | 1.21 | % | | 1.17 | % | | 1.18 | % | | 1.22 | % |

17

CAPE BANCORP

Solid Deposit Growth

18

CAPE BANCORP

Conversion Offering Information

CAPE BANCORP

Offering Overview

(Pricing ratios are on a pro forma basis, at or for the six months ended June 30, 2007)

| | | | | | | | |

| | | MINIMUM | | | MIDPOINT | |

| | | Offering Price Per Share: $10.00 | |

General | | | | | | | | |

Number of shares offered | | | 7,820,000 | | | | 9,200,000 | |

Charitable Foundation shares (7%) | | | 547,400 | | | | 644,000 | |

Shares Issues in the Merger | | | 4,939,424 | | | | 4,939,424 | |

| | | | | | | | |

Total shares outstanding (100.0%) | | | 13,306,824 | | | | 14,783,424 | |

Pro forma market capitalization | | $ | 133.1M | | | $ | 147.8M | |

Boardwalk's Ownership | | | 37.12 | % | | | 33.41 | % |

Pro forma net income(1) | | $ | 1,247 | | | $ | 1,317 | |

Pro forma net income per share | | $ | 0.10 | | | $ | 0.10 | |

Offering price to pro forma net income per share | | | 50.00x | | | | 50.00x | |

Pro forma stockholders' equity | | $ | 181,875 | | | $ | 194,080 | |

Pro forma tangible stockholders' equity | | $ | 125,706 | | | $ | 137,911 | |

Pro forma stockholders' equity per share | | $ | 13.67 | | | $ | 13.13 | |

Pro forma tangible stockholders' equity per share | | $ | 9.45 | | | $ | 9.33 | |

Offering price to pro forma stockholders' equity per share | | | 73.15 | % | | | 76.16 | % |

Offering price to pro forma tangible stockholders' equity per share | | | 105.82 | % | | | 107.18 | % |

| (1) | Does not include the effect of synergies or revenue enhancements. |

20

CAPE BANCORP

Attractive Valuation

Based on the independent appraisal, when compared to the average fully converted New Jersey thrift on a price to book basis, Cape Bancorp’s common stock is valued at a44% discount at the minimum of the offering range and a42% discount at the midpoint of the offering range.

On a price to tangible book basis, Cape Bancorp’s common stock is valued at a27% discount at the minimum of the offering range and a26% discount at the midpoint of the offering range.

| | | | | | | | | | | | |

| | | Cape Bancorp (Minimum) | | | Cape Bancorp (Midpoint) | | | Average Appraisal Peer Group(2) | | | Average Fully Converted New Jersey Thrifts(3) | |

Price / Book(1) | | 73.15 | % | | 76.16 | % | | 105.39 | % | | 130.50 | % |

Price / Tangible Book(1) | | 105.82 | % | | 107.18 | % | | 121.54 | % | | 145.40 | % |

(1) | Based on Cape Bancorp financial data as of June 30, 2007. |

(2) | Peer group as determined by RP Financial includes the following companies: ABNJ, BFBC, FKFS, FSBI, HARL, OCFC, PBCI, PFS, THRD and WFBC. |

(3) | Fully converted NJ group includes the following companies: ABNJ, HCBK, OCFC, PBCI, PFS and RBLG. |

| * | Pricing ratios as of January 7, 2008. |

21

CAPE BANCORP

Investment Highlights

| • | | Merger solidifies Cape’s position as the largest banking institution headquartered in Cape May and Atlantic Counties |

| • | | Merger combines two companies with strong cultural compatibility and complementary business models |

| • | | Growing presence in demographically attractive markets |

| • | | Seasoned combined management team with an intimate knowledge of the local markets and strong ties to the community |

| • | | Diversified loan portfolio with a continuing emphasis on commercial lending |

| | • | | Increase in loan-to-one borrower limit creates additional lending flexibility |

| • | | Conservative credit practices have maintained superior asset quality |

22